Cardinal Health: The Drug Distribution Empire from Ohio

I. Introduction & Episode Roadmap

Picture this: A company that touches nearly every hospital bed, pharmacy counter, and medical procedure in America, yet most people have never heard of it. Cardinal Health moves $226.8 billion worth of drugs and medical supplies annually—more revenue than Microsoft, more than Meta, more than Boeing and Lockheed Martin combined. It sits at number 14 on the Fortune 500, quietly orchestrating the flow of pharmaceuticals that keep America healthy, or at least medicated.

The company serves over 100,000 locations daily, from corner pharmacies to major hospital systems. Its trucks roll through every state, its warehouses hum 24/7, and its logistics network rivals Amazon's in complexity. Yet Cardinal Health operates in the shadows of healthcare, a critical but unglamorous middleman in an industry obsessed with innovation and disruption.

Here's the question that should intrigue any student of business: How did a 26-year-old Harvard MBA transform a struggling Ohio food wholesaler into one of the three companies that essentially control drug distribution in America? The answer involves perfect timing, relentless acquisitions, political maneuvering, and a willingness to embrace the unsexy but essential plumbing of healthcare.

This is the story of Robert Walter's four-decade empire-building project, the creation of an acquisition machine that swallowed over 50 companies, and the modern colossus that emerged—complete with its share of controversies, from the opioid crisis to questions about whether middlemen deserve their cut in modern healthcare. It's a tale of strategic pivots, from distributing canned goods to controlling the flow of chemotherapy drugs, from regional player to national powerhouse.

We'll trace Cardinal's evolution through distinct eras: the scrappy startup years when Walter nearly lost everything to a salmonella outbreak, the pivot from food to pharmaceuticals that changed everything, the acquisition binge that built a conglomerate, and the modern challenges of operating in healthcare's most scrutinized sector. Along the way, we'll decode the playbook that turned distribution—arguably the most commoditized business model—into a durable competitive advantage worth tens of billions.

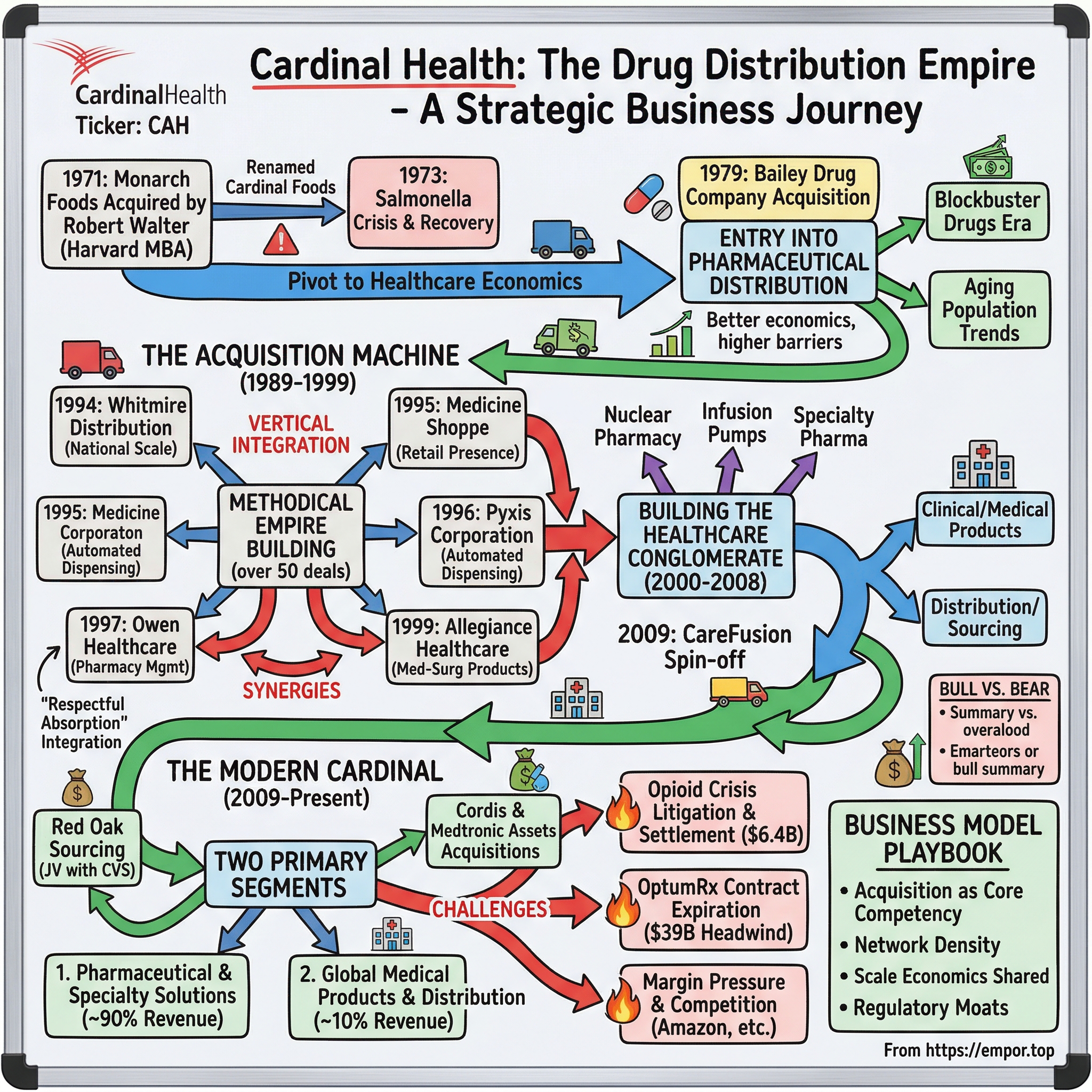

II. The Robert Walter Origin Story

Robert Walter didn't set out to build a healthcare empire. In 1971, fresh from Harvard Business School and armed with family money and boundless ambition, the 26-year-old acquired Monarch Foods, a small food wholesaler based in Dublin, Ohio. He renamed it Cardinal Foods after Ohio's state bird—a touch of local pride that would later seem quaint given the company's national ambitions.

The early years nearly killed the company before it could truly begin. In 1973, a salmonella contamination in Cardinal's distributed food products triggered a crisis that would have ended most entrepreneurial dreams. Lawsuits piled up, customers fled, and Walter found himself managing damage control rather than growth. He later recalled spending sleepless nights wondering if his Harvard professors had covered "what to do when your products poison people" in their case studies.

But Walter possessed a quality that separated him from typical MBAs: he could see around corners. While fighting through the salmonella crisis, he noticed something peculiar about the distribution business. Food wholesaling was becoming a commodity game—brutal margins, powerful buyers like emerging supermarket chains, and little differentiation beyond price. Meanwhile, he observed that pharmaceutical distribution, though operating on similar logistics principles, enjoyed better economics. Drug wholesalers had more fragmented customers, higher switching costs, and regulatory barriers that created natural moats.

Walter's management philosophy emerged during these trials. He believed in decentralized operations—let the acquired companies run themselves—while maintaining iron-fisted control over capital allocation and strategic direction. "I'm not smart enough to run every business we buy," he once told investors, "but I'm smart enough to buy businesses run by people smarter than me." This humility, rare among empire builders, would become Cardinal's secret weapon.

The entrepreneur also displayed an unusual comfort with leverage and risk. While his Ohio contemporaries built steadily and conservatively, Walter thought in exponential terms. He studied Henry Singleton's Teledyne, admired Harold Geneen's ITT conglomerate, and believed that in distribution, scale wasn't just an advantage—it was the only sustainable advantage. Every acquisition would make the next one easier, every new market would strengthen the core.

By the late 1970s, Walter had stabilized Cardinal Foods but recognized its limitations. The grocery consolidation wave he'd anticipated hadn't materialized as expected. Major chains were building their own distribution networks rather than relying on wholesalers. The writing was on the wall: food distribution would become a race to the bottom. Walter needed a new game, and he found it in an unlikely place—a small pharmaceutical distributor in Zanesville, Ohio, about 50 miles east of Columbus.

The Bailey Drug Company acquisition in 1979 seemed minor at the time, barely warranting a mention in Cardinal's annual report. But Walter saw what others missed: pharmaceutical distribution was about to explode. The 1980s would bring blockbuster drugs, an aging population, and healthcare spending growth that would outpace GDP for decades. While everyone else was chasing the next hot biotech or medical device company, Walter would quietly build the roads on which all those innovations would travel.

His leadership style crystallized during this period: patient but opportunistic, analytical but intuitive, collaborative but decisive. Employees described him as professorial—he'd walk the warehouse floors asking questions, genuinely curious about operations. But when acquisition opportunities arose, the professor transformed into a deal machine, working 20-hour days to get transactions done.

III. The Pivot: From Food to Drugs (1979–1988)

The year 1979 marked Cardinal's true founding moment, though few recognized it at the time. When Walter acquired Bailey Drug Company, he wasn't just buying a business—he was buying an education in pharmaceutical distribution. The Zanesville operation was tiny, serving local pharmacies in rural Ohio, but it revealed the elegant economics of drug wholesaling: high-value products in small packages, consistent demand regardless of economic cycles, and customers who needed reliable daily delivery more than rock-bottom prices.

The pharmaceutical industry in 1980 looked nothing like today's giant. Prescription drug spending totaled just $12 billion annually—less than Americans spent on alcohol. But the seeds of explosive growth were everywhere. Tagamet had just become the first billion-dollar drug. The FDA was approving new chemical entities at record pace. Medicare Part B was expanding coverage. And crucially for Walter, the industry remained incredibly fragmented—thousands of independent pharmacies, hundreds of small hospitals, and only a handful of national distributors.

Walter's entry into pharmaceutical distribution coincided with a technology revolution that most missed. While Silicon Valley obsessed over personal computers, Cardinal was quietly implementing sophisticated inventory management systems that could track millions of SKUs, predict demand patterns, and optimize delivery routes. The company's early IBM System/38 computers, housed in climate-controlled rooms in Ohio, became competitive weapons. A pharmacist could call Cardinal at 11 PM and have their order delivered by 7 AM—magic in an era of weekly deliveries and paper invoices.

Going public on NASDAQ in 1983 gave Walter the currency he needed for expansion. The IPO raised just $15 million—laughable by today's standards—but it transformed Cardinal from a private Ohio company into a potential acquirer of anything that moved pills from manufacturer to patient. The timing was exquisite: interest rates were finally falling from their Volcker-era peaks, making leveraged acquisitions feasible again.

The Ohio network came together piece by piece through the mid-1980s. Walter acquired Ellison Drug Company in Cincinnati, followed by Mr. Phillip Pharmacy in Cleveland. Each deal was small—$5 million here, $10 million there—but together they created density. In distribution, density is destiny. The same truck that delivered to one pharmacy could hit three others on the same route. Fixed costs spread across more deliveries. Manufacturers noticed Cardinal's growing reach and offered better terms.

But the masterstroke came in 1988 when Walter sold Cardinal's original food operations to Roundy's. The food business that had birthed the company, that had survived salmonella and struggled through grocery consolidation, was jettisoned for $80 million. Wall Street was puzzled—why sell a profitable division? Walter's answer was clarity: "We're a healthcare company now. Period." The proceeds would fund pharmaceutical acquisitions. More importantly, the sale sent a signal to the market, to employees, and to acquisition targets: Cardinal was all-in on drugs.

The technology embrace went beyond back-office systems. Cardinal pioneered electronic ordering systems, giving pharmacies dedicated terminals that connected directly to Cardinal's mainframes. While competitors still processed orders by phone and fax, Cardinal's customers could transmit orders electronically, check inventory availability, and receive confirmation in minutes. It seems primitive now, but in 1988, it was revolutionary—Amazon-like convenience before Amazon existed.

By decade's end, Cardinal had grown from essentially zero pharmaceutical revenue to over $500 million. The company served 5,000 pharmacy locations across Ohio and neighboring states. But Walter knew this was just the appetizer. The real feast was coming. The 1990s would bring managed care, pharmacy benefit managers, and consolidation waves that would reshape American healthcare. Cardinal needed to get big fast, or risk being someone else's acquisition.

IV. The Acquisition Machine Takes Off (1989–1999)

The 1990s began with Walter articulating what he called "The Cardinal Doctrine" to his board: acquire aggressively, integrate loosely, and let scale compound. Between 1991 and 1996, Cardinal's revenue exploded from $1.2 billion to $8.9 billion—a 49% compound annual growth rate that would make any Silicon Valley unicorn jealous. But this wasn't venture-funded hypergrowth; this was methodical empire building, one strategic acquisition at a time.

The Whitmire Distribution merger in 1994 marked Cardinal's transformation from regional player to national force. Whitmire brought California, Nevada, and Colorado—markets where Cardinal had zero presence. The $300 million deal was Cardinal's largest to date, and Walter personally spent three months in California overseeing integration. But "integration" in Cardinal's dictionary meant something different than most corporate mergers. Walter kept Whitmire's management, maintained their local warehouse operations, even retained their delivery trucks with Whitmire logos. Only the back-office functions—purchasing, financing, technology—were centralized.

That same year, Cardinal officially changed its name from Cardinal Distribution to Cardinal Health, signaling ambitions beyond mere logistics. Walter saw distribution as the foundation, but not the ceiling. The company immediately validated this vision by acquiring Medicine Shoppe International for $348 million in 1995—Cardinal's first non-distribution deal. Medicine Shoppe operated 1,000 franchised pharmacies, giving Cardinal direct retail presence and customer insights that pure wholesalers lacked.

The Pyxis Corporation acquisition in 1996 for $867 million shocked the industry. Pyxis made automated drug dispensing systems—essentially high-tech vending machines for hospitals that tracked every pill from pharmacy to patient bedside. Wall Street questioned why a distributor needed manufacturing capability. Walter's response revealed his strategic depth: "We don't just want to deliver products to hospitals. We want to help them manage those products through the entire facility." The Pyxis machines generated recurring revenue through service contracts and created switching costs that locked in hospital customers for years.

Owen Healthcare followed in 1997, adding pharmacy management services for 150 hospitals. The pattern was becoming clear: Cardinal wasn't just aggregating distribution points; it was vertically integrating across the pharmaceutical value chain. Each acquisition brought new capabilities that made Cardinal stickier with customers and more valuable to suppliers.

The decade's crescendo came with the 1999 Allegiance Healthcare acquisition—a $3.8 billion megadeal that catapulted Cardinal into medical-surgical products. Allegiance distributed everything from surgical gloves to hospital beds, serving 95% of U.S. hospitals. The merger faced intense regulatory scrutiny, with competitors crying monopoly. But Walter had learned from watching previous distribution consolidations: regulators cared more about consumer prices than middleman market share. Cardinal agreed to minor divestitures and the deal closed.

Walter's acquisition criteria, refined over hundreds of deals, became Cardinal's playbook: First, the target must be in healthcare—no diversification into adjacent industries regardless of how attractive. Second, it must either expand geographic reach, add new customer segments, or provide new capabilities. Third, existing management should want to stay. Fourth, the acquisition should be accretive within 12 months. And fifth, perhaps most importantly, it should make future acquisitions easier, not harder.

The integration philosophy was equally distinctive. Cardinal practiced what Walter called "respectful absorption"—maintaining the acquired company's culture and operational autonomy while extracting synergies through purchasing power and technology platforms. A California warehouse manager told me Cardinal felt less like a conquering army and more like a rich uncle who paid for upgrades but let you run your own household.

By 1999's end, Cardinal had completed over 30 acquisitions, operated distribution centers in 48 states, and generated $25 billion in revenue. The Ohio food wholesaler had become America's third-largest pharmaceutical distributor. But more importantly, it had proven that in healthcare's fragmented landscape, a disciplined acquirer could build something that was greater than the sum of its parts. The acquisition machine wasn't just running—it was accelerating.

V. Building the Healthcare Conglomerate (2000–2008)

The new millennium opened with Cardinal at an inflection point. Y2K had passed without the predicted pharmaceutical supply chain apocalypse, but Walter saw a different kind of disruption coming. He believed pure distribution would commoditize and that Cardinal needed to become what he called "a healthcare solutions company"—corporate speak that actually meant something in this case.

The Bindley Western Industries acquisition in 2001 for $2.1 billion represented Cardinal's final major distribution play. Bindley brought specialty pharmaceutical capabilities—handling complex biologics, oncology drugs, and other high-touch medications that required special handling, patient support, and reimbursement expertise. These weren't pills counted in bottles but therapies measured in patient outcomes. Margins were triple those of traditional distribution, and barriers to entry were substantial.

Cardinal's diversification strategy accelerated under Walter's direct leadership. The company acquired Syncor International for $850 million, entering nuclear pharmacy—preparing radioactive drugs for diagnostic imaging. It bought Alaris Medical Systems for $2.0 billion, adding infusion pumps and IV medication safety systems. Each deal pushed Cardinal further from its wholesale roots and deeper into specialized, higher-margin healthcare services.

The transformation was remarkable: By 2005, Cardinal operated the nation's largest network of nuclear pharmacies, managed pharmacies inside 160 hospitals, manufactured medical devices, provided consulting services, and still distributed one of every four prescription drugs dispensed in America. Revenue surpassed $65 billion. The company employed 55,000 people across multiple business units that increasingly had little in common except the Cardinal name and Walter's capital allocation.

But success bred complexity. The conglomerate structure that enabled rapid growth also created management challenges. Different businesses required different skills—running a nuclear pharmacy bore no resemblance to managing a distribution warehouse. Cardinal's decentralized approach, which had worked brilliantly for acquisitions, struggled with operational integration. Customers complained about dealing with multiple Cardinal divisions that didn't communicate.

In 2006, recognizing these challenges and perhaps his own limitations, Walter recruited R. Kerry Clark from Procter & Gamble as CEO while remaining Executive Chairman. Clark brought CPG discipline to Cardinal's sprawling operations—standardized processes, Six Sigma initiatives, and customer segmentation strategies. The cultural clash was immediate: Cardinal's entrepreneurial managers bristled at P&G-style bureaucracy, while Clark struggled to understand healthcare's regulatory complexity.

The transition accelerated when George Barrett, a longtime Cardinal executive who'd run the pharmaceutical distribution business, became CEO in 2008 as Walter fully retired. Barrett faced an immediate strategic choice: continue managing the conglomerate or break it apart. The answer came in 2009 with the CareFusion spin-off—a $6 billion separation of Cardinal's clinical and medical products businesses into an independent public company.

The CareFusion spin was Walter's final strategic act, orchestrated from his chairman emeritus role. He recognized that Cardinal's medical device businesses—the Pyxis dispensers, Alaris pumps, respiratory equipment—needed different investment levels, innovation cycles, and management focus than distribution. The separation was surgical: Cardinal kept pharmaceutical and medical supply distribution plus generic drug sourcing, while CareFusion took the manufactured products and clinical technologies.

Walter's three-decade run had transformed a $12 million food wholesaler into a $90 billion healthcare colossus. He'd completed over 50 acquisitions, built national scale in pharmaceutical distribution, and diversified into dozens of healthcare sectors. The strategy wasn't always elegant—Cardinal often looked more like a holding company than an integrated corporation—but it worked. Between 1983 and 2008, Cardinal's stock delivered a 23% compound annual return, crushing the S&P 500's 11% return over the same period.

The legacy of the Walter era extended beyond financial returns. He'd proven that in healthcare, unlike technology or consumer goods, slow and steady could win the race. While dot-coms flamed out and biotech startups gambled on blockbuster drugs, Cardinal methodically built infrastructure that became essential to American healthcare. It wasn't sexy, but it was durable. As Walter said in his final shareholder letter: "We never tried to be the most innovative company in healthcare. We tried to be the most important."

VI. The Modern Cardinal: Scale, Challenges & Controversies (2009–2020)

The post-Walter era began with Cardinal confronting a paradox: it had achieved massive scale—$98 billion in revenue by 2009—but faced existential questions about its role in American healthcare. George Barrett's tenure as CEO from 2009 to 2017 would be defined not by aggressive expansion but by navigating regulatory minefields, technological disruption, and the darkest chapter in the company's history—the opioid crisis.

Healthcare Solutions Holding joined Cardinal's portfolio in 2010 for $517 million, bringing home healthcare capabilities as America shifted from hospital to home-based care. The acquisition seemed prescient—aging baby boomers would need infusion therapy, medical supplies, and nursing support delivered to their doorsteps. Cardinal positioned itself as the infrastructure provider for this demographic wave, operating nationwide networks that could handle everything from chemotherapy administration to wound care.

The Red Oak Sourcing joint venture with CVS in 2013 represented a different kind of strategic thinking. Rather than acquire generic drug manufacturing capabilities, Cardinal partnered with one of its largest customers to create buying power that could rival even Walmart's. Red Oak negotiated directly with generic manufacturers, cutting out traditional middlemen and capturing margin that would normally leak away. The 50-50 partnership was unusual—customers and suppliers rarely share equity—but it locked CVS into Cardinal's ecosystem while giving both companies leverage against generic drug inflation.

Cardinal's medical device acquisitions continued with the $1.94 billion purchase of Cordis from Johnson & Johnson in 2015. Cordis made cardiac and vascular devices—stents, catheters, guidewires—products that required specialized sales forces and clinical expertise. The following year, Cardinal doubled down by acquiring Medtronic's patient care, deep vein thrombosis, and nutritional insufficiency business for $6.1 billion. These weren't distribution plays; they were manufacturing businesses that transformed Cardinal from middleman to maker.

But as Cardinal expanded its medical products portfolio, storm clouds gathered around its core pharmaceutical distribution business. In 2021, nationwide settlements were reached to resolve all opioids litigation brought by states and local political subdivisions against the three largest pharmaceutical distributors, McKesson, Cardinal Health, and AmerisourceBergen ("Distributors"). The crisis had been building for years, with prosecutors alleging that distributors failed to detect and report suspicious orders of opioid medications despite legal obligations to do so.

The numbers were staggering. McKesson, Cardinal Health and AmerisourceBergen distributed 44 percent of the nation's oxycodone and hydrocodone pills—the two most abused prescription opioid drugs. While Cardinal maintained it followed all regulations and worked to prevent diversion, the public narrative had shifted. Distributors were no longer invisible infrastructure; they were defendants in America's most devastating public health crisis.

Between 2014 and 2016, Cardinal spent $13 million lobbying for the "Ensuring Patient Access Act," legislation that critics argued weakened the DEA's ability to freeze suspicious drug shipments. The law required the agency to show "immediate" danger before halting distributions, a higher bar than previous standards. Cardinal defended the lobbying as ensuring legitimate patients maintained access to needed medications, but the optics were devastating—a company profiting from opioid distribution lobbying to reduce oversight.

In all, the Distributors will pay up to $21 billion over 18 years as part of the nationwide settlement framework announced in 2021. Cardinal's specific share represented approximately $6.4 billion, paid out over nearly two decades. The company admitted no wrongdoing but agreed to enhanced monitoring systems, data sharing with competitors to identify suspicious ordering patterns, and funding for addiction treatment programs.

The financial engineering around the settlement drew additional criticism. The Dublin, Ohio-based Cardinal Health said earlier this month it planned to collect a $974 million cash refund because it claimed its opioid-related legal costs as a "net operating loss carryback"—a tax provision Congress included in last year's coronavirus bailout package. Using pandemic relief provisions to offset opioid settlement costs seemed tone-deaf at best, cynical at worst.

Mike Kaufmann, who became CEO in 2018, inherited both the opioid overhang and questions about Cardinal's strategic direction. The company had become a complex conglomerate—drug distribution, medical products manufacturing, specialty pharmaceuticals, nuclear pharmacy, home healthcare. Some investors pushed for breakups, arguing the sum of parts exceeded the whole. Others worried that dismantling Cardinal would destroy synergies that took decades to build.

The pandemic provided unexpected validation of Cardinal's model. As COVID-19 overwhelmed hospitals, Cardinal's supply chain expertise became mission-critical. The company moved billions of units of PPE, distributed vaccines, and kept medications flowing despite global disruptions. Revenue surged past $160 billion in fiscal 2021. The crisis demonstrated that boring, reliable infrastructure companies might be exactly what healthcare needed.

VII. Current Operations & Business Model

Cardinal Health today operates through two primary segments that reflect decades of strategic evolution: Pharmaceutical and Specialty Solutions, generating roughly 90% of revenue, and Global Medical Products and Distribution, contributing the remaining 10%. This structure, simplified from the conglomerate complexity of the Walter era, focuses the company on what it does best—moving healthcare products efficiently and reliably.

The Pharmaceutical segment remains the earnings engine, distributing branded and generic drugs to retail pharmacies, hospitals, and mail-order facilities. Cardinal serves approximately 31,000 pharmacy locations daily, with delivery networks so precise that most customers receive orders within hours of placement. The business operates on razor-thin margins—typically 1-2% operating margin—but generates enormous cash flow through negative working capital dynamics. Cardinal gets paid by pharmacies before paying manufacturers, effectively using supplier credit to finance operations.

Specialty Solutions, embedded within the pharmaceutical segment, handles complex therapies requiring special handling, patient support, and reimbursement management. Think oncology drugs that cost $10,000 per dose, biologics requiring cold-chain logistics, and rare disease treatments serving hundreds of patients nationally. These products generate margins of 4-6%, triple the traditional distribution business, and create stickier customer relationships through value-added services.

The Red Oak Sourcing venture with CVS, now a decade old, has evolved into a powerful generic drug procurement engine. Red Oak negotiates on behalf of both companies' combined volume—over 25% of U.S. generic drug demand—extracting better pricing from manufacturers desperate for shelf space. The venture doesn't just negotiate prices; it manages product transitions when drugs go generic, ensures supply continuity during shortages, and even influences which generic manufacturers enter the U.S. market.

Global Medical Products serves over 75% of U.S. hospitals with everything from surgical gloves to OR equipment. The segment includes Cardinal's own manufactured products—surgical drapes, fluid management systems, wound care products—alongside third-party distribution. Following the Cordis acquisition, Cardinal became a significant player in cardiovascular devices, competing with Boston Scientific and Abbott in certain categories. The medical products business generates 4-5% operating margins, benefiting from both manufacturing economics and distribution density.

The at-Home Solutions division, accelerated by COVID-19 and demographic trends, provides direct-to-patient services including infusion therapy, medical supplies, and clinical support. Cardinal manages the entire continuum—from insurance verification to nurse visits to supply replenishment. With 160 locations nationwide, at-Home can reach 90% of Americans within 24 hours, critical for time-sensitive therapies like IV antibiotics or parenteral nutrition.

Technology underpins everything. Cardinal's data analytics platforms process millions of transactions daily, using AI to predict demand patterns, identify potential drug shortages, and optimize inventory placement. The company's Order Express system handles over 95% of customer orders electronically, with straight-through processing that requires no human intervention. Warehouse automation has reached the point where robots pick and pack orders, with humans primarily handling exceptions.

International operations remain limited compared to competitors. Cardinal generates less than 5% of revenue outside the United States, primarily in Canada and China. The company has deliberately avoided aggressive international expansion, believing the complexity and regulatory differences outweigh potential returns. This U.S. focus contrasts with McKesson's significant European presence but aligns with Cardinal's philosophy of depth over breadth.

Nuclear pharmacy, operated through 160 radiopharmacies nationwide, represents a unique niche. Cardinal prepares and delivers radioactive drugs used in diagnostic imaging, with half-lives measured in hours. A dose prepared at 3 AM must be injected by 8 AM or it becomes worthless. This time-critical logistics creates enormous barriers to entry—you can't build a nuclear pharmacy network without massive scale and expertise.

The OptiFreight® Logistics division leverages Cardinal's transportation network for third parties, moving products for manufacturers who need healthcare-compliant shipping but lack their own infrastructure. With over 30 distribution centers and a fleet of 3,000 vehicles, Cardinal has excess capacity that generates incremental margin when sold to others. It's a classic example of turning a cost center into a profit center.

Recent strategic reviews have questioned whether this portfolio makes sense. Activist investors argue Cardinal should divest medical products, focus purely on pharmaceutical distribution, and return capital to shareholders. Management counters that diversification provides stability, cross-selling opportunities, and negotiating leverage with suppliers who often span multiple segments. The debate reflects a fundamental tension: is Cardinal a focused distributor or a diversified healthcare services company?

VIII. Financial Performance & Market Position

Cardinal Health's fiscal 2024 financial results demonstrated the resilience of its business model despite significant headwinds. Fiscal year 2024 revenues were $226.8 billion, an 11% increase from fiscal year 2023. GAAP operating earnings were $1.2 billion and GAAP diluted EPS was $3.45. More impressively, Non-GAAP diluted EPS increased 29% to $7.53 for the year, reflecting the increase in non-GAAP operating earnings across the business, lower interest and other expense, a lower non-GAAP effective tax rate and a lower share count following in-year share repurchases.

The numbers tell a story of operational excellence masking strategic challenges. Cardinal generated operating cash flow of $3.8 billion and adjusted free cash flow of $3.9 billion—all-time highs that validate the cash-generative nature of distribution. Yet the company trades at just 0.05x revenue and 10x forward earnings, suggesting investors see a melting ice cube rather than a cash machine.

Comparing Cardinal to its Big Three peers reveals nuanced positioning. McKesson, the largest with over $300 billion in revenue, trades at higher multiples reflecting superior execution and international diversification. Cencora (formerly AmerisourceBergen), the smallest at roughly $260 billion in revenue, commands premium valuations due to specialty pharmaceutical focus and animal health exposure. Cardinal sits uncomfortably in the middle—bigger than Cencora but less profitable, smaller than McKesson but more complex.

The margin structure tells the real story. Pharmaceutical distribution generates 1-2% operating margins—essentially a toll on drug flow through the supply chain. Every basis point matters at this scale; a 10 basis point margin improvement on $200 billion of pharmaceutical revenue equals $200 million in operating profit. Cardinal has expanded margins through mix shift toward specialty drugs, operational efficiency, and generic sourcing benefits from Red Oak.

The GMPD segment operates at 4-5% margins but faces different dynamics. Medical products distribution competes with Owens & Minor, Medline, and increasingly Amazon Business. Manufacturing competes with multinational device companies with deeper R&D budgets. The segment generated just $175 million in profit on $12 billion in revenue in fiscal 2024—a 1.5% margin that raises questions about capital allocation.

Cash flow remains the bright spot, driven by negative working capital dynamics. Cardinal collects from customers in 20-30 days but pays suppliers in 40-50 days, creating a permanent float that funds operations. This float grows with revenue, generating "free" financing that explains how Cardinal can operate with minimal equity capital. The model works brilliantly until revenue declines—then the float unwinds, consuming cash.

The OptumRx contract expiration creates exactly this dynamic, with a $39 billion revenue headwind due to OptumRx contract expiration The loss of UnitedHealth's pharmacy benefit management business removes roughly 17% of pharmaceutical revenue overnight. While Cardinal will reduce corresponding costs, the working capital unwind will consume over $1 billion in cash—money that would otherwise fund share buybacks or acquisitions.

Capital allocation under CEO Jason Hollar reflects a balanced approach: maintain the dividend (yielding approximately 2.5%), buy back shares opportunistically ($500 million authorized for fiscal 2025), and preserve flexibility for tuck-in acquisitions. The company avoids transformational M&A, having learned from the conglomerate complexity of the Walter era. Small deals in specialty pharmacy or medical products make sense; another multi-billion distribution acquisition doesn't.

The company raised its fiscal year 2025 outlook for non-GAAP diluted EPS to $7.55 to $7.70 from the preliminary outlook of at least $7.50 previously communicated during the company's third quarter fiscal year 2024 earnings release. The company updated its Pharmaceutical and Specialty Solutions segment profit growth outlook to 1% to 3% growth, from at least 1% growth. This guidance implies continued operational improvement despite the OptumRx headwind, though skeptics question the quality of earnings given ongoing opioid settlement payments and restructuring charges.

Stock performance reflects this uncertainty. Cardinal trades at $115 per share, up from pandemic lows of $40 but below 2015 peaks of $90 (pre-split adjusted). The stock has delivered 15% annualized returns over the past five years, respectable but lagging the S&P 500's 18% return. More concerning: Cardinal trades at its lowest relative multiple to the market in decades, suggesting investors see structural challenges rather than temporary headwinds.

IX. Playbook: The Cardinal Health Model

The Cardinal Health playbook, refined over five decades, offers lessons that extend far beyond drug distribution. At its core lies a paradox: how to build competitive advantages in a business with no proprietary technology, no branded products, and no direct consumer relationships. The answer involves scale, scope, and systematic execution—boring virtues that compound over time.

Acquisition as Core Competency: Cardinal completed over 50 acquisitions not through financial engineering but operational integration. The company developed a repeatable process: identify targets that expand geographic reach or capabilities, pay fair prices (typically 8-12x EBITDA), retain management, integrate back-office functions while maintaining front-office autonomy, and realize synergies through purchasing power and overhead reduction. This decentralized integration model preserved entrepreneurial energy while capturing scale benefits.

Strategic Fit Discipline: Walter's cardinal rule—acquisitions must be in healthcare—seems obvious but proved genius. While competitors diversified into technology services or consumer products, Cardinal stayed focused. This discipline meant passing on apparently attractive deals but created deep domain expertise. Cardinal's executives understand healthcare regulation, reimbursement complexity, and provider economics in ways that generalist acquirers never could.

Scale Economics Shared: Cardinal practices what Amazon calls "scale economics shared"—passing efficiency gains to customers rather than capturing all margin improvement. When Cardinal negotiates better generic drug prices through Red Oak, it shares savings with pharmacy customers. When automation reduces warehouse costs, Cardinal lowers delivery fees. This approach seems to sacrifice profitability but creates switching costs and volume growth that more than compensate.

Regulatory Moat Building: Cardinal turned regulatory burden into competitive advantage. The company maintains licenses in all 50 states, DEA registrations for controlled substances, and compliance with thousands of federal and state regulations. New entrants face years of licensing procedures and millions in compliance costs. Cardinal's existing infrastructure—legal teams, compliance officers, government relations—spreads these costs across massive revenue base.

Network Density Optimization: Distribution economics depend on route density—deliveries per mile driven. Cardinal methodically built density through acquisition and organic growth, creating local monopolies in many markets. Once Cardinal serves 80% of pharmacies in a region, competitors can't achieve profitable scale. This dynamic creates winner-take-most markets where the leader enjoys permanently superior economics.

Customer Intimacy at Scale: Despite its size, Cardinal maintains close customer relationships through localized service. Each distribution center operates semi-autonomously, with managers who know their customers personally. Pharmacists call local Cardinal representatives, not distant call centers. This high-touch service in a high-scale business creates loyalty that pure digital disruptors struggle to replicate.

Vertical Integration Judgment: Cardinal selectively integrated upstream (generic sourcing, medical device manufacturing) and downstream (pharmacy management, home healthcare) but avoided full integration. The company doesn't own pharmacies or hospitals, maintaining arms-length relationships that preserve trust. This selective integration captures margin while avoiding channel conflict—a delicate balance many companies bungle.

Technology as Enabler, Not Disruptor: Cardinal embraced technology to enhance operations rather than transform business models. The company's investments in warehouse automation, predictive analytics, and electronic ordering improved efficiency without changing fundamental value propositions. Cardinal proves that incumbent advantages—relationships, regulatory expertise, physical infrastructure—can survive technological change if properly adapted.

Long-term Value Creation: The Cardinal model prioritizes long-term value over quarterly earnings. Major acquisitions take years to fully integrate. New distribution centers require decade-long paybacks. Generic sourcing contracts span multiple years. This long-term orientation, enabled by stable ownership and patient investors, allows Cardinal to make investments that short-term focused competitors avoid.

Managing Commodity Trap: In commodity businesses, the playbook usually involves differentiation or cost leadership. Cardinal chose a third path: becoming essential infrastructure. By handling complexity that customers prefer to avoid—regulatory compliance, inventory management, multi-supplier consolidation—Cardinal makes itself indispensable even with commodity economics. The margin may be thin, but the relationship is thick.

X. Analysis: Bull vs. Bear Case

The Bull Case: Essential Infrastructure in Growing Market

Bulls see Cardinal Health as the toll road of American healthcare—unglamorous but essential infrastructure that captures value from $4.5 trillion in annual health spending. Start with demographics: 10,000 Americans turn 65 daily, entering peak pharmaceutical consumption years. The average 65-year-old takes 4.5 prescription drugs daily; by 85, it's 7.5 drugs. This demographic tsunami will drive pharmaceutical volumes regardless of economic cycles or political changes.

The scale advantages are nearly insurmountable. Cardinal's distribution network took 50 years and tens of billions to build. Replicating it would require not just capital but regulatory approvals, customer relationships, and supplier agreements that take decades to develop. Even Amazon, with unlimited capital and technological sophistication, has struggled to crack pharmaceutical distribution beyond simple pharmacy operations. The complexity of handling controlled substances, managing cold chain logistics, and navigating 50-state regulation creates barriers that money alone can't overcome.

Diversification beyond pure distribution provides multiple earnings streams and strategic options. The GMPD segment, while currently underperforming, serves 75% of U.S. hospitals with essential products. at-Home Solutions rides the tailwind of site-of-care shifting from expensive hospitals to home settings. Specialty pharmaceuticals, growing at 10% annually, offer higher margins and stickier relationships. Nuclear pharmacy provides a regulatory moat few can penetrate.

Cash flow generation remains robust despite margin pressure. Cardinal converts nearly 100% of earnings to free cash flow, with working capital dynamics providing additional financing. Even modest margin expansion—say 10 basis points on pharmaceutical distribution—drops hundreds of millions to the bottom line. The company generated $3.9 billion in adjusted free cash flow in fiscal 2024, enough to fund dividends, buybacks, and growth investments while maintaining conservative leverage.

The opioid settlement, while painful, removes a major overhang. Cardinal's $6.4 billion obligation is defined, scheduled over 18 years, and tax-deductible. The payments average $350 million annually—significant but manageable given Cardinal's cash generation. More importantly, the settlement includes no admission of wrongdoing and releases Cardinal from future state and local government claims. The crisis forced Cardinal to strengthen compliance systems that now serve as competitive advantages.

Healthcare spending shows no signs of slowing. U.S. healthcare expenditures are projected to reach $6.8 trillion by 2030, growing faster than GDP. Pharmaceutical spending specifically will grow 5-7% annually driven by specialty drugs, biosimilars, and novel therapies like GLP-1 agonists for obesity. Cardinal captures value from all these trends regardless of which drugs succeed or which companies manufacture them.

The Bear Case: Structural Pressures and Disruption Risks

Bears see Cardinal as a melting ice cube, gradually losing relevance in modernizing healthcare. The OptumRx loss isn't just a revenue hit—it's a warning that large customers increasingly view distributors as replaceable vendors rather than strategic partners. If UnitedHealth can internalize distribution, why not CVS, Walgreens, or large hospital systems? The industry could face a doom loop of customer defections reducing scale advantages.

Margin pressure appears structural, not cyclical. Pharmacy chains consolidate, increasing buying power. Manufacturers explore direct-to-pharmacy models, cutting out middlemen. Pharmacy benefit managers squeeze distributors on generic pricing. Government regulators scrutinize drug pricing, potentially limiting distribution fees. Cardinal operates in the middle of a value chain where everyone else has pricing power—manufacturers set list prices, insurers determine reimbursement, pharmacies control consumer relationships.

Amazon and technology disruption loom larger than bulls acknowledge. Amazon's pharmacy business grew 50% year-over-year, now delivering medications to 45 states. While still small, Amazon has patient capital, technological advantages, and consumer trust that traditional distributors lack. More threatening: vertical integration by tech-enabled players like Mark Cuban's Cost Plus Drugs, which sources directly from manufacturers and ships to consumers, bypassing traditional distribution entirely.

The opioid overhang extends beyond financial settlements. Reputational damage lingers, making Cardinal a political target for drug pricing reform. ESG-focused investors avoid the stock, limiting institutional demand. Talented employees increasingly choose other industries, creating human capital challenges. The company spent $13 million lobbying for legislation that weakened DEA oversight—a fact that will haunt Cardinal in every future regulatory debate.

GMPD segment struggles suggest strategic confusion. Despite years of investment and multiple acquisitions, medical products generate minimal profits. The segment faces competition from pure-play distributors like Owens & Minor, GPO-aligned players like Medline, and increasingly sophisticated hospital self-distribution. Cardinal lacks the scale in medical products that it enjoys in pharmaceuticals, yet management seems reluctant to exit or meaningfully restructure.

Biosimilars and specialty pharmacy disruption could hurt more than help. While Cardinal touts specialty capabilities, these complex drugs increasingly flow through limited distribution networks controlled by manufacturers. Biosimilars promise to reduce drug costs by 30-50%, directly hitting Cardinal's revenue base. The company's percentage-of-sales pricing model means lower drug prices equal lower absolute dollar profits, even if volumes increase.

Financial engineering options are exhausted. Cardinal already operates with optimal leverage, minimal working capital, and efficient operations. Unlike the Walter era when acquisitions drove growth, today's antitrust environment prevents transformational deals. Organic growth barely exceeds inflation. Share buybacks provide temporary EPS boost but don't address fundamental challenges. The company is running harder to stay in place.

International expansion opportunities barely exist. Unlike McKesson with European operations or Cencora with global specialty networks, Cardinal remains U.S.-focused. International markets either have entrenched local distributors or government-controlled systems that exclude foreign players. Cardinal missed the window for global expansion and now lacks the resources or risk appetite for international adventures.

XI. Epilogue: The Future of Drug Distribution

The question haunting Cardinal Health—and all drug distributors—is existential: Does pharmaceutical distribution need to exist as an independent industry, or will it be absorbed into vertically integrated healthcare conglomerates? The answer will determine whether Cardinal remains a Fortune 20 company or becomes a cautionary tale about middlemen in the digital age.

The OptumRx contract loss signals more than a customer defection; it represents UnitedHealth's belief that distribution is better controlled than outsourced. UnitedHealth now operates its own pharmaceutical distribution, pharmacy benefit management, physician practices, and insurance plans—a fully integrated healthcare ecosystem that captures margin at every step. If this model succeeds, expect CVS Health, Elevance Health, and other integrated players to follow suit, gradually starving independent distributors of volume.

Yet Cardinal's leadership sees opportunity in portfolio optimization rather than panic. The ongoing strategic review of GMPD suggests management finally acknowledges that not all revenue is good revenue. Divesting low-margin medical products could focus Cardinal on higher-return pharmaceutical distribution and specialty services. The proceeds could fund share buybacks at depressed valuations or acquisitions in growing segments like biosimilars and home infusion.

Technology investments focus on evolutionary improvement rather than revolutionary disruption. Cardinal's new distribution center automation reduces labor costs by 30% while improving accuracy to 99.99%. Predictive analytics help anticipate drug shortages before they occur. Blockchain pilots promise to improve supply chain transparency and reduce counterfeit risk. These aren't headline-grabbing innovations, but they steadily improve economics in a business where basis points matter.

The biosimilar wave presents both threat and opportunity. As blockbuster biologics lose patent protection, biosimilars offer 30-50% cost savings. Cardinal's revenue will initially suffer as expensive branded drugs are replaced by cheaper biosimilars. But volume growth could compensate—if biosimilar adoption follows the generic drug playbook, unit volumes could triple even as prices fall. Cardinal's role in educating providers, managing inventory, and ensuring supply continuity becomes more valuable as product complexity increases.

Specialty pharmaceutical distribution remains the brightest growth area. These high-cost drugs for complex conditions require special handling, patient support services, and reimbursement expertise that commodity distributors can't provide. Cardinal's specialty revenue grows double-digits annually with margins triple those of traditional distribution. As drug development shifts toward targeted therapies and personalized medicine, specialty capabilities become increasingly strategic.

The political and regulatory environment presents wildcards. Drug pricing reform proposals range from minor tweaks to revolutionary restructuring. International reference pricing could slash U.S. drug costs by 50%, devastating distributor economics. Conversely, political gridlock could preserve the status quo for decades. Cardinal's lobbying expenditure—$2.8 million in 2023—seems like cheap insurance against existential regulatory threats.

For long-term investors, Cardinal Health presents a fascinating dilemma. The bear case is compelling: margins pressured, customers defecting, technology disrupting, politicians targeting. Yet the company generated nearly $4 billion in free cash flow last year, trades at decade-low valuations, and serves an industry growing faster than GDP. The question isn't whether Cardinal will exist in 10 years—it will—but whether it will thrive or merely survive.

The lessons for entrepreneurs and investors extend beyond healthcare. Cardinal Health proves that unglamorous businesses can generate enormous value through disciplined execution, strategic focus, and long-term thinking. It also warns that competitive advantages, no matter how durable they appear, require constant reinvention. Robert Walter built an empire by recognizing that in healthcare's complexity lay opportunity. Today's leaders must recognize that in healthcare's transformation lies both existential threat and generational opportunity.

The enduring question—can middlemen survive in modern healthcare?—misses the point. The real question is whether Cardinal can evolve from middleman to essential partner, from distributor to solution provider, from cost center to value creator. The answer will determine not just Cardinal's fate but the future of American healthcare infrastructure. In an industry that touches every American life, that's a story worth watching.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube