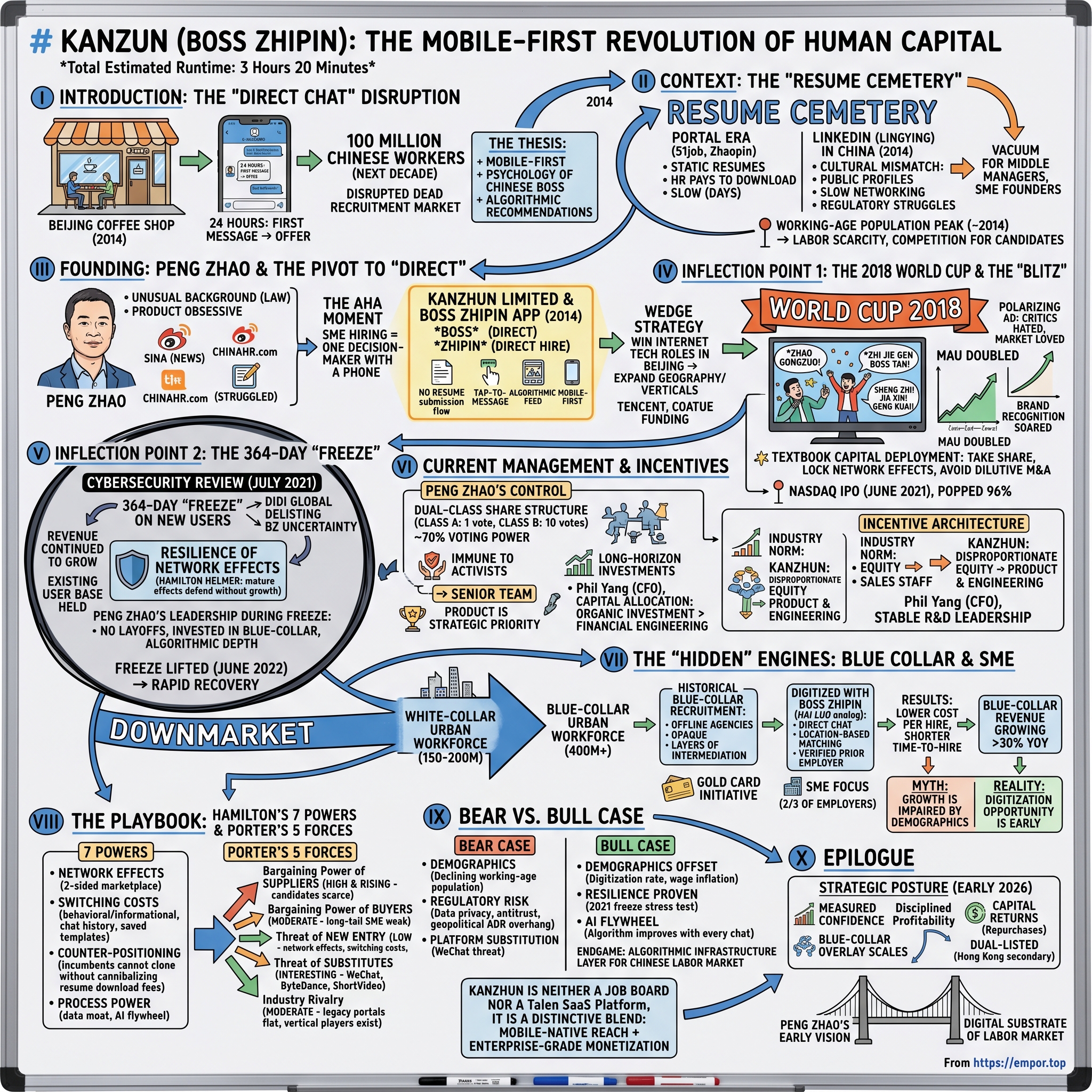

Kanzhun (BOSS Zhipin): The Mobile-First Revolution of Human Capital

I. Introduction: The "Direct Chat" Disruption

Picture a Beijing coffee shop in late 2014. A 28-year-old product manager at a fintech startup named Liu has just received an offer letter on his phone. Not via email. Not through a recruiter's call. Through a chat window that looked, to all the world, like WeChat. On the other side of that chat sat the company's co-founder—not an HR coordinator, not a third-party headhunter, but the actual decision-maker. Liu negotiated his salary in real time, between sips of his latte, in the same casual cadence he used to order takeaway. Twenty-four hours from first message to signed offer.

That experience, multiplied across a hundred million Chinese workers over the next decade, is the story of Kanzhun Limited.

The Chinese recruitment market in 2014 was, to put it bluntly, dead. The two listed incumbents—51job and Zhaopin—operated what amounted to digital newspaper classifieds. Job seekers uploaded a static resume into a "cemetery" of millions of others. Employers paid for the privilege of downloading those resumes, then dialed phone numbers, played voicemail tag, and waited. Average response times were measured in days. The notion that a hiring manager and a candidate might simply chat—directly, on a mobile screen, without the kabuki theater of cover letters and recruiter intermediation—was, frankly, considered absurd by the establishment.

Then a former product executive named Peng Zhao bet his career on the absurd. He named his company Kanzhun—literally "look at the boss"—and built an app whose entire interface was a chat thread. No resume cemetery. No keyword search. Just a recommendation feed and a tap-to-message button. The boss talks directly to the seeker. The seeker talks directly to the boss. Zhipin. Direct hire.

By 2018, that app had become unavoidable in Chinese popular culture, thanks to one of the most polarizing television commercials ever to air during a World Cup broadcast. By 2021, it had IPO'd on NASDAQ for over $5 billion, only to walk straight into a Cybersecurity Review Office investigation that froze new user registrations for 364 days. By 2026, having survived demographic headwinds, geopolitical chill, and the most aggressive regulatory environment any Chinese internet company has faced this decade, Kanzhun stands as the dominant online recruitment platform in the world's largest labor market—with a market capitalization of roughly ten billion dollars and an operating cadence that increasingly resembles enterprise SaaS more than it does a job board.

The thesis of this episode is straightforward but layered. Peng Zhao did not invent recruitment software. What he did invent was the marriage of two forces nobody else paired: the mobile-first expectations of the Chinese consumer, who by 2014 had already abandoned desktop computing for the smartphone, and the psychology of the Chinese boss—the SME founder, the team lead, the entrepreneur who hired with his gut and his thumb rather than through an HR committee. He gave these decision-makers a tool that felt like an extension of their existing chat habits, while simultaneously feeding them an algorithmic recommendation engine that did the searching for them.

Over the next three hours we will trace the full arc: the moribund "portal" era that BOSS Zhipin disrupted, the founding pivot from a struggling Q&A site into a recruitment juggernaut, the audacious 2018 World Cup advertising blitz that critics hated and the market loved, the 2021 cybersecurity freeze that became the ultimate stress test of the network effect, the dual-class governance structure that keeps Peng Zhao firmly in command, the quietly enormous blue-collar pivot that may dwarf the white-collar core, and finally the bull and bear cases through the lens of Hamilton Helmer's 7 Powers and Porter's 5 Forces.

By the end you should understand whether Kanzhun is, as bulls argue, the emerging "infrastructure" layer for the Chinese labor market—or, as bears warn, simply the best operator in a structurally shrinking pond.

II. Context: The "Resume Cemetery"

To understand why BOSS Zhipin felt revolutionary, you need to understand just how stagnant Chinese online recruitment had become by the early 2010s. The dominant narrative for fifteen years had been written by 51job, founded in 1998 by Rick Yan, and Zhaopin, founded in 1997 and eventually acquired by SEEK of Australia. Both companies came of age during the original portal era of the Chinese internet—the same era that produced Sina, Sohu, and NetEase. Their business model was a near-perfect mirror of the American job-board template that Monster.com had pioneered in the late 1990s. Resumes were the inventory. Employers were the customers. And the unit economics ran on resume downloads.

Imagine the workflow. A jobseeker named Wang opens his desktop browser, navigates to 51job, fills out a multi-page form documenting every employer he has worked for since university, and uploads the resulting profile into a database alongside thirty million others. On the other side, an HR administrator at a state-owned enterprise pays an annual package—often six figures in renminbi—for the right to download a quota of those resumes per month. The administrator runs keyword searches: "Java engineer, three years experience, Shanghai, Mandarin native." Wang's resume surfaces. The administrator downloads it. Wang's phone rings the next afternoon, or the day after, or never.

This system worked passably well in an era of labor surplus. China in 2003 had a flood of fresh graduates and an even larger flood of rural-to-urban migrants pouring into the coastal cities. Employers held all the leverage. They could afford to be slow. They could afford to ghost candidates. They could afford to staff up an entire HR department whose job was to wade through the resume cemetery, because labor was cheap and abundant.

But by the early 2010s the underlying demographics had begun to shift, and the existing tools could not adapt. China's working-age population peaked around 2014 at approximately one billion people—after which it began an irreversible decline that continues today. Salaries in the coastal megacities started climbing at double-digit annual rates. The fresh graduate cohort, born after 1990, was the first generation raised entirely under the one-child policy, and they had options their parents had never dreamed of. Suddenly the asymmetry of the labor market began to flip. Candidates were the scarce resource. Employers had to compete for them. And competing required speed.

The portals could not deliver speed. Their entire revenue model depended on selling resume access to employers, which meant the candidate experience was deliberately frictional. If you let a hiring manager DM a candidate directly, you cannibalize the resume download fee. If you push instant notifications to candidates' phones, you reduce the value of the keyword search subscription. The incumbents were structurally trapped, in textbook Christensen fashion, by their own profit pools.

And then there was LinkedIn. The American giant entered China formally in 2014 with Sequoia Capital and China Broadband Capital as local partners, and a Chinese name—Lingying—chosen for its phonetic resemblance to the brand. On paper, LinkedIn should have crushed the local portals. It had a superior product, a global network, and the cultural cachet of being the platform Silicon Valley used. In practice, it failed slowly and then quickly. The reasons are illuminating.

LinkedIn was built around the cultural assumption that a professional network is something you cultivate over decades, with carefully curated public profiles and high-stakes posts. That assumption mapped onto a North American or European white-collar worker who would change jobs perhaps every three to five years. It mapped poorly onto the Chinese knowledge worker, who in the rocketship startup environment of Beijing or Hangzhou might change jobs every twelve to eighteen months and who treated career moves as tactical, not narrative. The Chinese professional did not want to broadcast a public profile to his current boss. He wanted to message a hiring manager privately, get a sense of the role in twenty minutes, and decide. LinkedIn's slow-burn networking model was, quite literally, the opposite product.

There was also the regulatory dimension. LinkedIn's content moderation requirements under Chinese law forced the company into compromises that alienated both its users and its U.S. parent. By 2021 LinkedIn would announce the shutdown of its core social networking service in China, retreating to a bare-bones "InCareer" job board that itself was wound down in 2023.

The vacuum was enormous. And sitting in the middle of it was an underserved persona that nobody had built for: the middle manager. The team lead at a Series B startup who needed to hire two engineers by next month. The founder of a cross-border e-commerce SME who needed a Russian-speaking customer service rep yesterday. The branch manager at a regional logistics company who needed twenty warehouse staff before the Singles Day rush. None of these people had time for the portal workflow. None of them had the budget for a recruiter. All of them had a smartphone and the muscle memory of WeChat.

That muscle memory was the crucial insight. By 2014, the smartphone in China was not merely a device. It was the operating system of daily life. WeChat had crossed 500 million monthly active users. Mobile payments were leapfrogging credit cards entirely. The desktop-first portals looked, suddenly, like artifacts from a museum.

Into that demographic and technological inflection point walked Peng Zhao, with a mobile app and a thesis about who really makes the hire.

III. Founding: Peng Zhao & The Pivot to "Direct"

Peng Zhao is, by the standards of the Chinese tech founder pantheon, a relatively quiet figure. He does not give Davos keynotes. He rarely sits for English-language interviews. He has none of the charisma-cult around him that surrounds Jack Ma or the philosophical edge that defines Pony Ma. What he has, by all accounts of those who have worked with him, is something more durable: a near-religious devotion to product instinct and a willingness to bet his career on uncomfortable contrarian theses.

Born in 1973 in Hubei province, Peng Zhao came of age in the very first wave of Chinese internet professionals. He studied at the China University of Political Science and Law, an unusual academic background for a tech founder—most of his peers came out of Tsinghua or Peking University engineering programs. Friends from the era describe him as obsessive about product details and indifferent to most of the social signals that drive Chinese corporate culture.

His professional formation came at Sina, the early Chinese portal giant, where he worked on news products in the early 2000s. From there he moved through several recruitment and career-related ventures, including a stint at ChinaHR.com—then one of the established legacy players—where he absorbed everything that was wrong with the portal model from the inside. He saw the sales-led culture. He saw the contempt for product engineering. He saw the way the entire revenue stack was structured to extract rent from employers rather than serve candidates.

The decisive episode came at a venture called Quip—the Chinese career site, not the toothbrush. Peng ran product there and watched as the company struggled to find traction in the shadow of the portal incumbents. The lesson he took was not that recruitment was a bad business. The lesson was that everyone was attacking it wrong. They were trying to build a better resume cemetery. The opportunity, Peng concluded, was to abolish the cemetery entirely.

In 2014 he founded Kanzhun Limited and launched the BOSS Zhipin app. The name itself was a manifesto. BOSS in capital Latin letters—a deliberate signal that this was not your father's recruitment site. Zhipin—直聘—meaning "direct hire." The whole pitch in three syllables.

The aha moment, as Peng has described it in Chinese-language interviews, came from a simple observation about how SME hiring actually worked in China's startup-saturated ecosystem. In a Fortune 500 company, the hiring decision passes through a labyrinth: recruiter, screener, hiring manager, panel interview, hiring committee, comp committee. In a Chinese SME—which by 2014 employed over 80% of the urban workforce—the hiring decision was made by one person, often the founder himself. He had no HR department. He had a phone. He needed someone to start Monday.

If you accepted that premise, the entire architecture of recruitment software needed to be rebuilt. You did not need a polished resume; you needed a brief profile the boss could scan in fifteen seconds. You did not need a keyword search; you needed an algorithmic recommendation feed that surfaced the right candidates the moment they appeared. You did not need cover letters and application portals; you needed a chat window. And critically, you needed all of it on mobile, because the boss was not sitting at a desktop—he was on the subway, in a meeting, at lunch.

The product Peng shipped reflected that thesis with monastic discipline. Open BOSS Zhipin in 2015 and the home screen was a feed of recommended jobs (for seekers) or recommended candidates (for bosses), generated by a matching algorithm that improved with every interaction. Tap on any card and you went directly into a chat thread. There was no "apply" button. There was no resume submission flow. The entire transaction was a conversation.

This was not just a UX decision. It was a deep architectural bet on the recommendation model over the search model—a bet that, in retrospect, mirrored what TikTok parent ByteDance was doing with Toutiao news in the same era, and what Pinduoduo would later do with social commerce. Chinese mobile users were not, it turned out, looking to actively search through inventories. They wanted the inventory pushed to them. They wanted the algorithm to do the work.

The early years were hard. Recruitment is a chicken-and-egg problem of legendary brutality. You cannot attract bosses without seekers, and you cannot attract seekers without bosses. Peng's solution was the geographic and vertical wedge: focus initially on internet and tech roles in Beijing's Zhongguancun district, where startup founders were already doing direct hiring informally and where the cultural barriers to messaging strangers were lowest. Win that wedge first. Use the high-density, high-frequency tech hiring market as the seed crystal. Then expand outward by geography and by vertical.

It worked. By 2017, BOSS Zhipin had become the dominant recruitment app among Chinese internet workers. The whisper network in Beijing tech circles had completed its job—if you were a young engineer looking to switch teams, you opened BOSS Zhipin. Period. Capital began to follow. Tencent led major rounds. Coatue came in. The valuation multiplied.

But the real test of the thesis was about to come. Because in 2018, Peng Zhao made a marketing decision so polarizing that it would either define his company or destroy it.

IV. Inflection Point 1: The 2018 World Cup & The "Blitz"

If you happened to be watching the FIFA World Cup in the summer of 2018 from anywhere in mainland China, you probably remember the commercial. Even if you tried to forget it, your brain, against your will, retained the jingle.

Picture a stark white room. A crowd of well-dressed actors, bouncing in unison. A chant that builds in volume and intensity until it becomes almost a roar: "Zhao gongzuo! Zhi jie gen Boss tan! Sheng zhi! Jia xin! Geng kuai! Sheng zhi! Jia xin! Geng kuai!" Roughly translated: "Looking for a job! Talk directly to the Boss! Promotions! Raises! Faster! Promotions! Raises! Faster!" The chant repeats. And repeats. And repeats. For fifteen seconds of pure, unadulterated, brain-melting repetition.

Critics in the Chinese media establishment hated it. Marketing professors wrote op-eds calling it crude, manipulative, an insult to advertising. The State Administration of Radio and Television fielded complaints. Some viewers flat-out muted their televisions every time it came on.

It was also, by any quantitative measure, one of the most successful advertising campaigns in Chinese internet history.

To understand why Peng Zhao green-lit something so aesthetically offensive, you have to understand the strategic context. By the spring of 2018, BOSS Zhipin had achieved leadership in the white-collar tech vertical but remained a niche app in the broader population's awareness. The total addressable market—the entire urban Chinese workforce—was an order of magnitude larger than its current penetration. Meanwhile, two sources of capital had become available simultaneously. Tencent had led BOSS Zhipin's Series D in 2018, validating the company's positioning and providing a war chest. And Coatue, the New York-based crossover fund, had also taken a significant stake. The board greenlit a massive marketing spend.

The question was where to deploy it. The answer was the World Cup, an event that in Chinese cultural terms is a unique mass-attention vehicle. China itself does not qualify for the World Cup—a national wound that has, paradoxically, made the tournament an even bigger spectator phenomenon. Hundreds of millions of Chinese viewers, glued to CCTV broadcasts, often in mid-to-late evening prime slots. The commercial inventory was scarce and expensive. Three Chinese internet companies bought up huge slabs of it: Pinduoduo, Mobike rival Yongche, and BOSS Zhipin.

Peng's marketing team, working with the Shanghai-based agency Honor Brand, made a choice that violated every Western advertising convention. Instead of a clever, brand-building, story-driven spot, they produced what was essentially a chant set to no music. The reasoning was unsentimental: in a fifteen-second slot, repeated dozens of times across hundreds of broadcast hours, the only metric that mattered was whether viewers could recall the brand name and the core proposition. Subtlety was the enemy of recall. Sophistication would be drowned out. What you needed was raw, pneumatic, almost violent memorability.

The campaign worked precisely as designed. BOSS Zhipin's monthly active users roughly doubled in the months following the World Cup. Brand recognition surveys placed it alongside the legacy portals for the first time. Critically, the cost per acquired user, even at the eye-watering rate cards CCTV was charging, came in well below what the company would have spent on equivalent digital performance marketing. The math was not pretty. But the math was the math.

There is a deeper strategic point embedded in this episode that often gets lost in the noise about the commercial's aesthetics. Peng Zhao was making a textbook capital deployment decision. He had access to venture capital at extremely favorable terms. He had a product that converted users efficiently once they downloaded it. He had a competitive window during which the legacy portals were structurally unable to respond—because they could not pivot their business model fast enough, and because their own marketing budgets were optimized for B2B sales conferences, not consumer broadcast. The arbitrage was real, and it was time-limited. You burn the capital now, you take the share now, you lock in the network effects, and you let the lifetime value compound for the next decade.

This is also where it becomes useful to talk about what BOSS Zhipin did not do. It did not buy its competitors. In 2017 and 2018, both 51job and Zhaopin were potentially available—51job had been a public company on NASDAQ and was eventually taken private by a consortium led by Recruit Holdings of Japan; Zhaopin had been delisted from NYSE and was held by a consortium that included Hillhouse Capital. Both were generating real revenue and real cash flow, and at the right price, either could have been folded into Kanzhun for a significant share consolidation play.

Peng explicitly chose not to. The reasoning, as it has emerged in subsequent strategic communications, was that the legacy traffic was the wrong kind of traffic. Buying 51job would mean inheriting tens of millions of low-engagement users who came to the site to download a resume PDF, not to chat with a candidate in real time. Integrating that user base would require either degrading BOSS Zhipin's product to accommodate the legacy workflow, or alienating the legacy customers entirely. Neither was attractive. Better to spend the capital on acquiring fresh, mobile-native users through marketing, and on R&D for the proprietary recommendation algorithms that constituted the company's true moat.

That decision—to invest in product and brand rather than in M&A—is one of the cleanest expressions of the company's underlying strategic philosophy. Kanzhun is not, in its self-conception, a recruitment company. It is a mobile consumer technology company that happens to operate in the recruitment vertical. The capital allocation reflects that.

By the end of 2020, BOSS Zhipin had crossed 100 million verified job seekers and was approaching IPO readiness. The company filed an F-1 with the U.S. Securities and Exchange Commission in May 2021, planning to list on NASDAQ at a valuation that would imply something like $7 to $10 billion in equity value. The bookbuild was strong. The institutional reception was enthusiastic. The IPO priced on June 11, 2021. The stock opened at $19, popped 96% on the first trading day, and closed around $42, valuing Kanzhun at roughly $16 billion.

It would be, briefly, the high water mark. Twenty-one days later, the regulators came.

V. Inflection Point 2: The 364-Day "Freeze"

July 5, 2021. A Monday. Just over three weeks after Kanzhun's NASDAQ debut, the Cyberspace Administration of China announced via terse public notice that it was opening a cybersecurity review of BOSS Zhipin. Pending the outcome of that review, the app would be prohibited from registering any new users.

For context, the same week saw similar reviews opened against Full Truck Alliance and the Yunmanman platform, and most consequentially against Didi Global, which had IPO'd on NYSE only days earlier. The pattern was unmistakable. Beijing was sending a message about offshore listings of Chinese internet companies that held large pools of domestic user data, and about the regulatory consequences of executing those listings without first obtaining cybersecurity sign-off. Didi would ultimately be forced to delist from the U.S. Kanzhun's fate was, for many months, deeply uncertain.

The freeze lasted, almost literally, a year. From July 2021 until June 2022—eleven months and roughly twenty-five days, or 364 days by some counts—Kanzhun was prohibited from onboarding new users to its core BOSS Zhipin app in mainland China. Existing users could continue to log in, message, and transact. But the growth funnel at the top of the funnel was, by regulatory order, switched off.

For any normal consumer internet company, a year-long freeze on new user acquisition is an extinction-level event. The entire operating playbook of consumer mobile in China is built on continuous user growth. Marketing budgets are calibrated to growth targets. Investor models are calibrated to growth targets. Engineering organizations are calibrated to growth targets. And in a two-sided marketplace—where every job seeker who churns reduces the platform's value to bosses, and vice versa—the steady-state assumption of zero new users implies inevitable decay.

What happened, instead, was almost shocking in its boringness. Kanzhun's revenue continued to grow. The existing user base did not collapse. The marketplace did not unravel. The company reported revenue growth in the high double digits for fiscal 2021 even with the freeze in effect for the second half of the year, and it returned to triple-digit user growth almost immediately upon reinstatement in mid-2022.

The reason this happened is the most important conceptual point in the entire Kanzhun story, and it constitutes the single best real-world demonstration of network-effect resilience in modern Chinese internet history.

Hamilton Helmer, in 7 Powers, defines network effects as the property by which a product's value to each user increases with the number of other users on the same network. The classical examples are telephones, social networks, and credit card networks. What Helmer also notes, less famously, is that mature network effects produce extraordinary defensive power even in the absence of growth—because the existing network is itself the product. The 364-day freeze stress-tested exactly this property. Could Kanzhun's marketplace continue to deliver value to existing participants even with no top-of-funnel growth?

The answer was yes, decisively, and here is the operational reason. A typical white-collar Chinese knowledge worker in 2021 was not on BOSS Zhipin because she planned to find a job tomorrow. She was on it because she might find a job in eighteen months, and because the cost of maintaining the app on her phone was effectively zero. A typical SME boss was not on the platform because he had an open requisition this week. He was on it because hiring is continuous—someone is always quitting, growing, retiring—and because he had a year's worth of chat history and saved candidate profiles inside the app. Each side had accumulated switching costs that were behavioral and informational rather than monetary.

When the freeze hit, those existing relationships continued to transact. Bosses continued to post jobs. Seekers continued to apply. Subscriptions continued to renew. The flywheel kept spinning. And critically, because the freeze was a regulatory action against Kanzhun specifically and not against the entire industry, competitors had a one-year window to attack a wounded leader. They tried. Liepin, the white-collar focused incumbent, ran aggressive marketing. Several smaller mobile-first challengers raised capital. None of it materially dented BOSS Zhipin's position, because the network already in place was too valuable to leave.

For Peng Zhao personally, the year was a leadership crucible. According to multiple subsequent profiles in Chinese business press, he refused to lay off any employees during the freeze, instead redirecting engineering and product resources toward building out the blue-collar product line and investing heavily in algorithmic improvements to the matching engine. He took the position—correct, in retrospect—that the freeze would end, and that the company that emerged on the other side would be stronger if it had used the time to compound on product depth rather than retrenching to defend the financial model.

The freeze was lifted in June 2022, after Kanzhun completed the cybersecurity remediation requirements imposed by the regulators. New user registration resumed. By the end of 2022, the company had restored its growth trajectory. By 2023, it was reporting record revenue and crossing into sustained GAAP profitability. The stock, which had cratered from its post-IPO peak of around $45 down into the single digits at the worst of the regulatory panic, began a long slow recovery as investors re-underwrote both the political risk and the durability of the business.

The episode left two permanent imprints on the Kanzhun story. The first was reputational. Inside Chinese internet circles, BOSS Zhipin became known as the company that survived. Founders and investors who had previously underweighted regulatory risk now took it seriously, and Kanzhun's demonstrated resilience earned it a kind of grudging respect that translated into stickier institutional investor relationships.

The second imprint was strategic. The freeze accelerated, by perhaps two years, the company's pivot into the blue-collar segment. With white-collar growth artificially constrained, leadership had every incentive to look elsewhere for expansion. The blue-collar opportunity, which had been on the strategic roadmap, became the focus. We will return to this in detail.

But before we do, it is worth pausing on the people who steer this company, and on the governance architecture that lets them do so.

VI. Current Management & Incentives

Peng Zhao controls Kanzhun in a manner that would be unremarkable for a U.S. founder-led tech company and is increasingly common, though still notable, among U.S.-listed Chinese internet companies. The mechanism is the dual-class share structure. Class A shares, which are what trades publicly under the BZ ticker on NASDAQ, carry one vote per share. Class B shares, held substantially by Peng Zhao and a small number of co-founders, carry ten votes per share. The combined effect is that even though Peng's economic ownership of the company is in the rough vicinity of fifteen to twenty percent, his voting power is approximately seventy percent or higher. He controls every shareholder vote, full stop.

This matters for two practical reasons. First, it makes Kanzhun effectively immune to activist shareholder pressure or hostile takeover. There is no scenario in which a dissident hedge fund forces a strategic review or a sale of the company over Peng's objection. Second, and more subtly, it gives Peng the political cover to make long-horizon investment decisions without quarterly justification. When he decided to redirect engineering resources into the blue-collar product line during the 2021 freeze, he did not need to defend that decision to a board of independent directors who might have preferred share buybacks. He simply made the call.

For long-term fundamental investors, the standard objection to dual-class structures is that they entrench underperforming management and disenfranchise outside capital. The defense is that they enable founders to pursue strategies that public-market quarterly pressure would otherwise punish. Both arguments are true in the abstract, and the question for any specific company is whether the controlling founder has the judgment and integrity to use the structure productively. The track record at Kanzhun, on the evidence to date—surviving the freeze, executing the blue-collar pivot, refusing dilutive M&A—suggests that Peng has used it well. That assessment could change. It is worth monitoring.

The other distinctive feature of Kanzhun's incentive architecture is the share-based compensation philosophy embedded in the 2020 and 2021 Share Incentive Plans, which were disclosed in detail in the F-1 filing and subsequent annual reports. The standout feature, when compared to the Chinese recruitment industry norm, is the heavy weighting of equity grants toward product and engineering personnel rather than toward sales staff.

This is genuinely countercultural for the recruitment vertical. Legacy players like 51job and Zhaopin built their organizations around large sales forces that sold annual subscription packages to corporate HR departments. The compensation model was sales-led: large variable comp, aggressive quotas, modest equity. The cultural identity of those companies, even today, is closer to a B2B enterprise software vendor than to a consumer technology firm.

Kanzhun reversed the polarity. Engineering and product employees—the people building the matching algorithms, the mobile clients, the data infrastructure—receive disproportionate equity compensation relative to industry norms, while sales personnel are compensated more cash-heavily and in some segments of the business have been deliberately de-emphasized in favor of self-service customer onboarding. The signal this sends inside the company, and outside it to potential hires, is unmistakable. Product engineering is the strategic priority. Sales is a function, not a culture.

A second-layer note worth flagging here on management quality and operational signaling: during the 2021 freeze, Peng Zhao did not exit any meaningful portion of his equity position, did not take an extended sabbatical, and continued to communicate consistently with the management team in operating reviews. This is in marked contrast to several other founders of Chinese internet companies who, facing similar regulatory pressure in the same period, materially reduced their public profiles or stepped back from operational involvement. Peng's behavior during the freeze is one of the strongest qualitative signals available about his commitment and risk tolerance.

The senior management team beyond Peng is relatively low-profile in international media but well-regarded inside Chinese internet circles. Phil Yang, the chief financial officer, came from a finance background at major Chinese internet companies and has earned credibility on quarterly earnings calls for the directness of his disclosures and the consistency of his guidance philosophy. The product and engineering leadership has been notably stable, with several key executives having been with Kanzhun since the early founding years.

What this management configuration produces, observationally, is a company that behaves in capital markets more like a disciplined operator than a hyper-growth narrative stock. Disclosures are clean. Guidance is conservative. Capital allocation favors organic investment over financial engineering. The company began share repurchases in modest size as cash generation scaled, which is not a particularly common posture for a Chinese internet company at this stage of maturity. Whether all of this continues to hold under the demographic and regulatory pressures we will discuss is the open question. So far, the evidence is consistent.

With governance and incentives understood, we can now turn to the strategic surface area that may matter most over the next decade: the shift downmarket and out of white-collar offices, into the factory floors and warehouse loading docks of the much larger Chinese blue-collar economy.

VII. The "Hidden" Engines: Blue Collar & SME

A morning in late 2024 in an industrial park outside Suzhou. A factory line manager named Chen needs to staff up forty-five additional assembly workers before a production ramp begins in three weeks. Historically, his options were three: dispatch his HR coordinator to a labor intermediary—an offline agency that would assemble workers from migrant pools at an aggressive markup; post flyers at the gates of nearby labor markets and hope; or pay a recruitment broker a per-head finder's fee that would compound over time. None of these options were fast. None of them were transparent. All of them involved layers of intermediation that took a meaningful slice of the worker's first month of wages.

Chen opens his phone. He taps an app called "Hai Luo" or its in-app analog inside BOSS Zhipin. He posts the requisition, including the wage, the shift schedule, the required experience level, and the location. Within the hour, candidates begin chatting with him directly. Most have profiles that include verified prior employer information, transit accessibility data from their current location, and willingness-to-relocate signals derived from previous behavior on the platform. Within forty-eight hours, Chen has filled twelve of the forty-five slots. Within two weeks, he has filled all forty-five. The cost per hire has dropped by something like 60 to 70 percent versus the labor-agency model, and the time-to-hire has compressed from weeks to days.

This is the Kanzhun story almost nobody outside China appreciates. The company is no longer primarily a white-collar tech recruitment platform. It is, increasingly, the dominant digitization of an enormous, opaque, and historically inefficient blue-collar labor market.

Some sense of scale. The Chinese white-collar urban workforce—the population of office workers in coastal megacities who would historically have used 51job or Zhaopin or LinkedIn—is on the order of 150 to 200 million people. The Chinese blue-collar urban workforce, broadly defined to include factory workers, couriers, warehouse staff, restaurant servers, ride-share drivers, delivery riders, and the entire panoply of urban service labor, is estimated at over 400 million people. That is roughly an order of magnitude larger than the white-collar market in headcount, and while wages are lower and recruitment frequencies different, the aggregate addressable spend on labor matching is enormous.

Historically, this market has been served by offline labor agencies—the kind of operations that existed at scale long before the internet did, and that took commissions of often 20 to 40 percent of a worker's first paycheck for placement services that consisted of little more than a phone call. The industry was opaque, fragmented, occasionally exploitative, and almost completely undigitized as recently as the late 2010s.

BOSS Zhipin's incursion into this market accelerated meaningfully after the 2021 freeze. The product layer was adapted for the specifics of blue-collar hiring: location-based matching took on much greater weight in the algorithm, since a warehouse worker's commute matters more than a software engineer's; chat templates were standardized around shift scheduling and wage negotiation; verification flows were streamlined for workers who might not have a college degree but did have years of relevant experience.

The "Gold Card" initiative—launched in stages from 2022 onward—gave employers in the blue-collar segment higher-touch packaging and priority candidate access for a subscription fee. The Hai Luo platform, which functions as a focused blue-collar labor matching environment with deeper integrations to dispatch logistics, became a meaningful contributor to top-line growth.

The numbers, as they have emerged in successive quarterly disclosures over 2023 and 2024, told a story of segment divergence. White-collar revenue, which remained the larger segment in absolute terms, grew at a steady mid-teens annual rate—respectable, but not the headline. Blue-collar revenue, off a smaller base, grew at rates often in excess of 30 percent year-over-year and in some quarters considerably higher. The strategic implication is straightforward: even with the white-collar core normalizing toward GDP-plus growth, the blue-collar overlay has the potential to drive double-digit aggregate growth for years.

There is also a structural margin point worth understanding. White-collar SaaS-style recruitment subscriptions to large enterprises have well-understood unit economics. Blue-collar matching, because it operates at much higher transactional frequency per employer relationship, generates a different kind of revenue rhythm—shorter-duration packages, more recurring billings, higher cumulative spend per active employer over a multi-year horizon. As blue-collar mix grows, the company's revenue model edges closer to a hybrid of consumer subscription and B2B SaaS, with all the predictability premium that implies.

The SME thread runs across both segments. Approximately two-thirds of Kanzhun's paying employer customers are small and medium enterprises—the long tail of Chinese commerce. This is the precise opposite of LinkedIn's positioning, where the revenue concentration sits with Fortune 500 enterprise clients. The strategic implication of the long-tail orientation is twofold. First, no single customer concentration risk—the loss of any one employer customer is immaterial. Second, structural alignment with the secular growth of the Chinese SME sector, which over the long run represents a larger employment pool than the state-owned enterprise and large-cap private sector combined.

A myth-versus-reality aside is appropriate here. The consensus narrative on Chinese internet companies in the post-2021 era has been that growth is structurally impaired by the regulatory environment and the demographic ceiling. For Kanzhun, this narrative is partially right and importantly wrong. Right, in that the white-collar core market is approaching maturity and labor force shrinkage is a real long-term headwind. Wrong, in that the blue-collar digitization opportunity remains in early innings, and the company's penetration of the total Chinese employer base is still well below saturation in most categories.

Watching the segment mix shift quarter-by-quarter is therefore one of the most useful things an investor can do with this name. We will return to which KPIs deserve attention in the closing section.

For now, we turn to the strategic frameworks—Helmer's 7 Powers and Porter's 5 Forces—that explain why this business is structurally durable, and what would have to be true for that durability to break.

VIII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces

Hamilton Helmer's 7 Powers gives investors a vocabulary for what makes a business defensible. Most companies have one or two genuine powers. Kanzhun, on examination, demonstrates three with clear evidence and a fourth in incipient form.

The first and most obvious is Network Effects, in their classical two-sided marketplace formulation. The value of BOSS Zhipin to a job seeker is a function of the number and quality of bosses on the platform. The value to a boss is a function of the number and quality of seekers. Each side reinforces the other in a virtuous cycle that, as we saw during the 2021 freeze, can sustain even the absence of new user acquisition for extended periods. This network effect is the deepest source of Kanzhun's defensibility.

The second is Switching Costs, which are often overlooked in marketplace contexts but are powerful here. A boss who has been using BOSS Zhipin for two years has accumulated chat histories with hundreds of candidates, saved templates for common roles, hiring records that inform the recommendation algorithm's understanding of his preferences, and operational habits built around the app's specific affordances. To switch to a competing platform, he would need to recreate all of that context. Even a free, technically-superior competitor would face a significant adoption barrier among existing power users. The switching costs scale with usage intensity, which is precisely what compounds defensibility for the most valuable customers.

The third is Counter-Positioning, which is the Helmer term for the situation in which an incumbent cannot adopt the disruptor's business model without cannibalizing its own profit pool. The legacy Chinese recruitment portals—51job, Zhaopin, ChinaHR—were structurally unable to pivot to direct-chat-with-recommendation-feed product architecture, because doing so would have collapsed the pricing power of their resume download subscriptions. Counter-positioning is one of the rarer 7 Powers, and it tends to be most consequential in industries undergoing technology-driven business model transitions. Kanzhun's exploitation of it during the mid-2010s window was textbook.

The fourth, in incipient form, is Process Power. Helmer defines this as the operational know-how that competitors cannot easily replicate even if they understand the business model. Kanzhun's matching algorithms—the recommendation engines that pair seekers with bosses based on years of accumulated interaction data—are improving with every chat that occurs on the platform. Each session is, in a sense, training data for the next session. As the dataset compounds, the algorithm's match quality compounds. A new entrant attempting to clone the product would face a years-long catch-up problem on data alone. Whether this constitutes a fully-formed Process Power yet is debatable; that it is moving in that direction is not.

Switching to Porter's 5 Forces, which gives us a complementary lens on industry structure, the picture is mostly favorable but with one important caveat.

Bargaining Power of Suppliers—which in this context means the job seekers, who supply their attention and their candidacies—is high and rising. As the Chinese demographic transition continues and labor scarcity intensifies, candidates have more options. This is not bad for Kanzhun specifically; in fact, it is a tailwind, because employers must compete harder for candidates, which increases willingness to pay for premium recruitment access. But it does mean that the platform must continue to invest in candidate-side experience to retain the supply side of the marketplace.

Bargaining Power of Buyers—employers paying for recruitment services—is moderate. Large enterprise customers can negotiate hard on pricing, but the long-tail SME customer base has weak individual bargaining power. The customer mix matters. Kanzhun's heavy SME orientation means buyer power is structurally lower than it would be at a portal serving primarily large enterprises.

Threat of New Entry is low for the reasons explored above: network effects, switching costs, and the data moat. The capital requirement to mount a credible competitive offering today is enormous, and the network effect math is unforgiving—any new entrant must somehow assemble two-sided liquidity in a category where the dominant incumbent has a head start of a decade and tens of millions of active users.

Threat of Substitutes is the most interesting force, and the one investors should monitor most carefully. The plausible substitutes are several. WeChat itself, with its dominant position in Chinese social messaging, could in theory layer recruitment functionality on top of its existing chat infrastructure. Various ByteDance properties—Douyin, Toutiao—have experimented with recruitment content and could be more aggressive. ShortVideo platforms have begun to host job postings as content. None of these have to date materially eroded BOSS Zhipin's share, but the watching brief is real.

Industry Rivalry, the fifth force, is moderate. The legacy portals continue to operate but are not gaining share. Specialized vertical players exist—Liepin in executive search, Lagou in tech, JoB.com in some white-collar segments—but none have meaningful scale relative to BOSS Zhipin. The rivalry is most intense at the blue-collar end, where Kuaishou's labor matching products and various smaller mobile-first competitors are vying for share of a market that is still being defined. Kanzhun's first-mover advantage in mobile-native recruitment, combined with its capital base and brand recognition, position it well to capture the consolidation phase.

The composite picture is of a company that has assembled most of the structural ingredients of long-term defensibility. The remaining strategic question is whether the demographic and regulatory environment provides enough demand-side oxygen for that defensibility to translate into compounding returns, or whether the moat ends up protecting a slowly shrinking pond.

That tension is precisely the bull-bear debate.

IX. Bear vs. Bull Case

The bear case on Kanzhun begins with demographics, because the demographics are simply bad. China's working-age population has been declining since approximately 2014 and is projected by most major demographic models to continue declining for the remainder of this century. The cohort of young workers entering the labor market each year is structurally smaller than the cohort exiting via retirement or attrition. The total addressable market for any labor-matching platform in China is, in nominal headcount terms, contracting.

This is a real and quantifiable headwind. It is also less catastrophic than the headline numbers suggest, for two reasons. First, the digitization rate of recruitment within the existing labor force is still well below saturation, particularly in the blue-collar segment, which means there is meaningful runway for share-of-wallet growth even with a flat-or-declining headcount denominator. Second, the wage base of the Chinese labor market is growing at multiples of the headcount decline rate as the economy continues to shift toward higher-value-added employment. Recruitment spend tends to scale with wages, not with headcount. So the dollar TAM for recruitment software is growing even as the worker headcount is shrinking.

The bear case continues with regulatory risk. Kanzhun has already lived through one near-fatal regulatory episode, and the broader environment for Chinese internet companies remains less predictable than for U.S. or European peers. Future risks include data privacy regulations that could constrain the matching algorithms, antitrust scrutiny if the company's market share continues to consolidate, and the unresolved overhang of U.S.-listed Chinese ADRs and the ongoing Holding Foreign Companies Accountable Act compliance dynamics. None of these are dispositive. All of them are real.

The bear case finishes with the WeChat threat—or more broadly, the platform-substitution threat. Tencent, which holds a substantial equity stake in Kanzhun, is also the operator of WeChat, which sits at the center of essentially all Chinese digital social and commercial behavior. If Tencent ever chose to compete more directly with Kanzhun by layering recruitment functionality natively into WeChat, the competitive dynamic would change overnight. To date, this has not happened, and the structural alignment of Tencent as both shareholder and platform partner makes it less likely than the headline framing suggests. But it remains the largest single tail risk to the franchise.

The bull case is essentially the inversion of the bear case, with one additional layer.

The inversion: yes, demographics are a headwind, but digitization and wage inflation more than offset the headcount decline; yes, regulation is a risk, but the 2021 freeze stress-tested the franchise and demonstrated that the network effects survive even extreme political shocks; yes, WeChat could in theory compete, but in practice has not, and has structural reasons not to.

The additional layer is what could be called the AI flywheel thesis. Every conversation that happens on BOSS Zhipin is, at the data layer, a labeled training example for the matching algorithm. Boss messages seeker, seeker responds, conversation either converts to a hire or does not, and the platform learns from each outcome. As foundational AI capabilities have advanced—and the company has invested meaningfully in incorporating them into its product stack—the matching engine is becoming progressively more effective. The match quality improvement compounds. Bosses get better candidates faster; seekers get more relevant job recommendations; the time-to-hire continues to compress; the willingness to pay for premium subscriptions grows.

The endgame in the bull case is a company that is no longer best understood as a job board, but as the algorithmic infrastructure layer for the Chinese labor market. Every employer of consequence in China has a presence on it; every job seeker of consequence has a profile on it; the platform's pricing power scales with the value of the matches it produces; and the underlying business model converges toward something closer to enterprise SaaS than to consumer mobile.

Whether one ultimately favors the bear or the bull case depends in large part on time horizon and on confidence in the durability of network effects in a structurally changing demographic environment. For the long-term fundamental investor, the most useful analytical posture is to identify the small number of operating metrics that will, over time, distinguish between the two scenarios.

There are three KPIs worth tracking with discipline.

The first is paid enterprise customer count, broken out by segment where disclosed. This is the cleanest revealed-preference signal of whether the platform's value proposition is gaining or losing share among employers. A growing paid customer base, particularly in the blue-collar segment, indicates the franchise is expanding. A flat or declining paid customer base would be the first warning sign of competitive erosion.

The second is the blue-collar revenue mix shift. The pace at which blue-collar revenue grows as a share of total revenue is the single best indicator of whether the secular digitization opportunity is being captured at the rate the bull case implies. Acceleration would validate the thesis. Deceleration would suggest that the white-collar core has more dependency than the consensus narrative assumes.

The third is GAAP operating margin trajectory. Kanzhun's transition from a growth-investing posture to one of disciplined profitability has been one of the more impressive aspects of the post-2022 recovery, and continued operating margin expansion would suggest that the underlying unit economics are more SaaS-like than consumer-mobile-like. Margin compression, conversely, would indicate that competitive intensity is forcing reinvestment at rates that compromise the long-term profit pool.

Watching these three metrics, in the context of the network-effect and switching-cost moats described above, gives the investor a defensible framework for distinguishing between durable franchise compounding and gradual structural erosion.

X. Epilogue

The most recent quarterly cycles have continued to reinforce the SaaS-like character of the business. The shift toward higher-margin recruiter subscriptions—annual or multi-year packages priced for hiring intensity rather than for incremental resume access—has continued to build, and the cash conversion characteristics of the model have remained strong. Capital returns to shareholders, in the form of share repurchases, have been initiated and gradually scaled, signaling that management views the cash generation as durable rather than temporary.

The strategic posture as of early 2026 is one of measured confidence. The blue-collar overlay continues to scale. The white-collar core continues to defend share. The regulatory environment, while never fully predictable in China, has been stable. The U.S. listing, despite the persistent overhang of geopolitical tensions, has held, and the company's dual-listed structure—with a secondary Hong Kong listing completed in earlier years—provides optionality if circumstances change.

The deeper question that remains is the framing one. Is Kanzhun a job board, or is it a SaaS platform for talent? The answer, increasingly, appears to be neither in pure form. It is something in between, and that in-between position—mobile-native consumer reach combined with enterprise-grade platform monetization—is what makes it distinctive among publicly traded recruitment companies globally. Comparable U.S. peers like Indeed (private, owned by Recruit Holdings) and ZipRecruiter operate in a structurally different competitive environment. Comparable Chinese peers operate at meaningfully smaller scale.

For long-term investors thinking about the Chinese internet sector through the lens of structural winners, Kanzhun represents one of the cleaner stories available: a founder-controlled, product-led, profitable, network-effect-protected business operating in a vertical that, despite demographic headwinds, retains substantial digitization runway. The risks are real and have been enumerated. The franchise has been stress-tested in ways few companies have endured. The next several years will reveal whether the model continues to compound, or whether the structural ceiling arrives sooner than the bull case allows.

Either way, the story of how a former product manager from Hubei built a chat app that toppled a fifteen-year-old industry, survived a year-long regulatory freeze, and may yet become the digital substrate of an entire economy's labor market is one of the more instructive case studies in modern Chinese internet history. It belongs alongside the Pinduoduo and ByteDance stories in the canon of mobile-era disruption. And it is far from finished.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube