Blackstone Digital Infrastructure Trust (BXDC): The Landlord of the AI Revolution

I. Introduction: The Physical Layer of the Internet

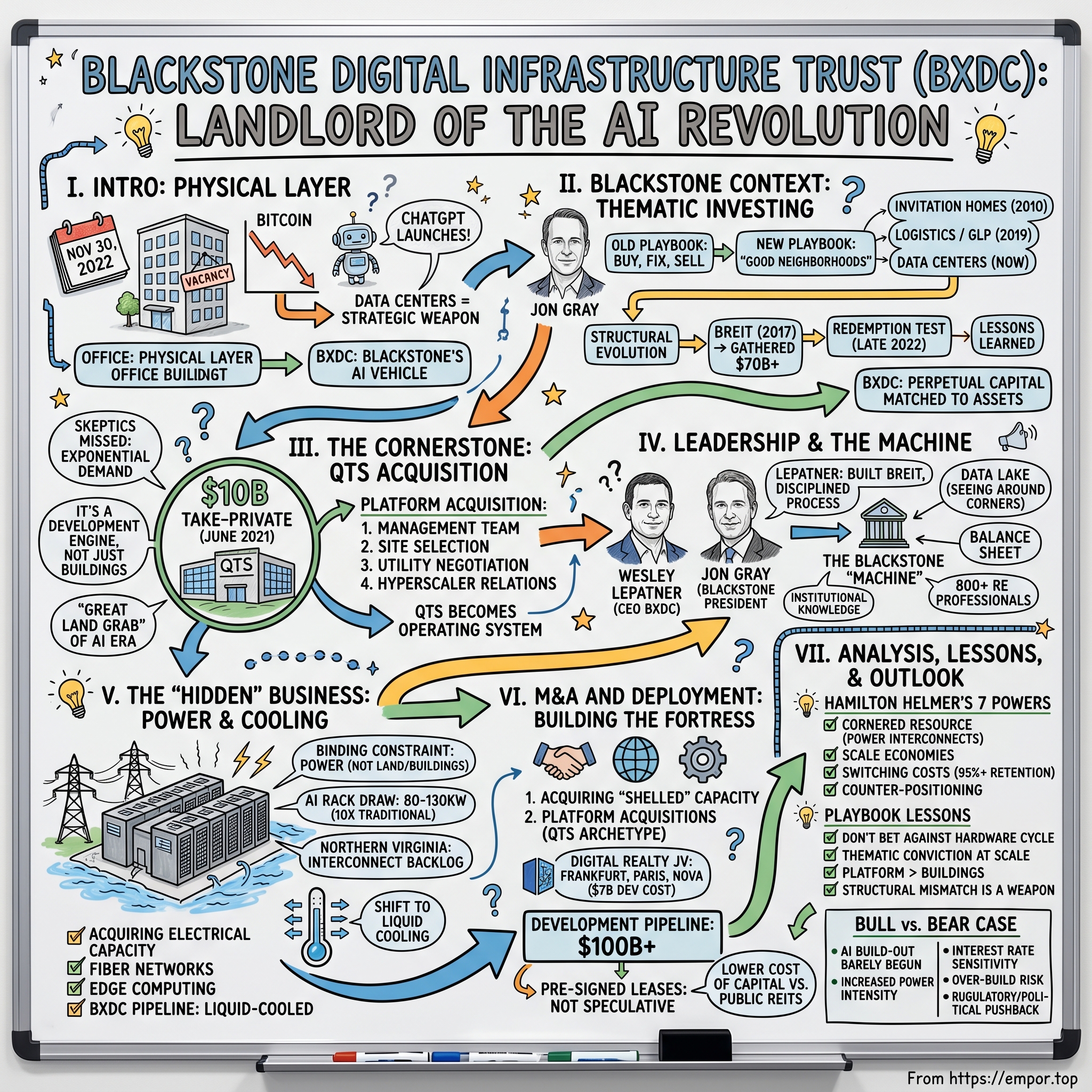

It is November 30, 2022, in the boardrooms of Manhattan's 345 Park Avenue. The world has not yet learned the phrase "large language model." Bitcoin is collapsing through $17,000. Office vacancies in San Francisco are spiking toward 30%, and the entire commercial real estate industry is whispering one word in panic — "remote." The smart money is selling buildings. Cheap money is dead. Anyone wagering capital on physical infrastructure is, at best, a contrarian and, at worst, a relic.

Then OpenAI quietly publishes a "research preview" of something called ChatGPT.1

Within five days, that research preview crosses one million users. Within sixty, it crosses one hundred million. And inside a particular subset of skyscrapers — buildings without windows, ringed by fences, located in places like Ashburn, Virginia and Hillsboro, Oregon — every square foot of space, every megawatt of power, and every dripping cold-aisle of liquid cooling has just become the most valuable commercial real estate on Earth.

This is the moment the data center stopped being plumbing and started being a strategic weapon. And no firm on the planet saw it coming earlier, sized for it bigger, or built a vehicle to harvest it more efficiently than Blackstone Inc. The vehicle is called Blackstone Digital Infrastructure Trust — BXDC. It is the firm's newest, perpetually offered, non-traded real estate trust, and it sits atop a portfolio that Blackstone itself describes as "the largest data center business in the world."2

BXDC is, in many ways, a culmination. It is the convergence of three decades of Blackstone's real estate craftsmanship, fifteen years of perpetual-capital innovation born inside BREIT and BCRED, and a single, audacious 2021 take-private of QTS Realty Trust that — depending on whether you ask a critic in 2021 or a portfolio manager in 2026 — was either the most aggressive deal of the post-COVID cycle or the great "land grab" of the AI era.[^3]

Here is the wider canvas. Blackstone president Jon Gray has openly called digital infrastructure "the most exciting investment theme" he has seen in his career, with a development pipeline he pegged at more than $100 billion stretched across four continents.[^4] In a world where hyperscalers like Microsoft, Alphabet, Amazon, and Meta have collectively committed to spending hundreds of billions of dollars on AI capex annually, the choke point is no longer GPUs. It is power, land, water, and skilled construction labor — all of which are the natural hunting ground of a private market real estate giant.

This article is not about a stock chart. It is about a structural bet. How did the largest alternative asset manager in history come to the conclusion that the highest-conviction trade of the 2020s was not a software business, not a chip designer, not a model lab, but a fleet of windowless concrete boxes humming with the heat of a billion inferences per second? And what does it mean for the individual investor that, for the first time, that bet is being offered through the wrapper of a non-traded REIT designed for the private wealth channel?

The roadmap is this. We will begin with the evolution of Blackstone Real Estate itself, the school in which BXDC's playbook was written. We will then dissect the QTS acquisition — the cornerstone — and the management platform it bought. We will profile Wesley LePatner, the executive Blackstone tapped to run the trust. We will go deep into the unglamorous but decisive war over megawatts. We will analyze BXDC against Helmer's 7 Powers and Porter's 5 Forces. And we will end at the question every long-term allocator is asking right now — bull or bear, has the AI build-out run too far, or has it not yet begun?

The thesis at the center of all of it is simple. In every gold rush, the durable fortune accrues to the seller of picks, shovels, and — most of all — to the landlord of the gold-fields. BXDC, more than any vehicle in market history, is engineered to be that landlord.

II. The Blackstone Context: From "Buy, Fix, Sell" to "Thematic Investing"

To understand BXDC, you have to understand Jon Gray. And to understand Jon Gray, you have to rewind to a kid from suburban Highland Park, Illinois, who joined Blackstone's then-small real estate group in 1992 directly out of the University of Pennsylvania, a few years before founders Stephen Schwarzman and Pete Peterson were even sure the real estate business was going to survive as a line of work inside the firm.3 Blackstone Real Estate, in those years, was a four-person team with a name on a door. By the time Gray turned forty, it would be the largest commercial property owner in the world.

The original Blackstone Real Estate playbook was classic post-savings-and-loan, opportunistic value-add. Buy assets the market hates, fix the operations, sell into a recovering cycle. The watershed moments were the Equity Office Properties take-private in 2007 — a $39 billion deal that Gray famously chopped and flipped at speed, banking enormous gains just before the financial crisis cratered office values — and then the Hilton acquisition the same year, where Blackstone wrote a $26 billion check at what looked, in 2008 and 2009, like the worst possible moment in the modern history of hospitality. Hilton ultimately became the most profitable private equity deal ever recorded.

What changed in the 2010s was that Gray stopped buying assets and started buying themes. Around 2010, Blackstone built Invitation Homes, a portfolio of single-family rentals, on the conviction that millennials would rent suburbia rather than buy it. Around 2014, the firm tilted hard into logistics — the warehouses behind e-commerce — culminating in 2019 with the $18.7 billion purchase of GLP's U.S. industrial portfolio, the largest private real estate deal in history at the time.4

The pivot was not subtle. Inside Blackstone, the phrase that traveled was that the firm wanted to be in "good neighborhoods." Bad neighborhoods were shopping malls, suburban office, and B-quality hotels. Good neighborhoods were warehouses, rental housing, life-sciences labs, student dorms in undersupplied markets, and — increasingly, after 2018 — data centers. This was thematic investing, and what made it Blackstone-specific was the institutional discipline to act on a thesis at multibillion-dollar scale, even when the asset class was crowded or the multiples looked rich on a backward-looking basis.

The second great evolution was structural rather than thematic. In 2017, Blackstone launched a vehicle called Blackstone Real Estate Income Trust — BREIT — a non-traded REIT engineered for the private wealth channel. The math was elegant. Institutional capital is finite, slow-moving, and demands periodic exits. Retail capital, by contrast, can be perpetually raised, allows for permanent ownership of compounding assets, and pays a steady management fee for the privilege. BREIT scaled with terrifying speed, ultimately gathering more than $70 billion of equity before the rate shock of late 2022 triggered a wave of redemption requests that became, briefly, a Wall Street obsession.[^7]

That redemption episode is essential context for BXDC, because Blackstone learned from it. The lesson was not that perpetual capital was broken — the firm has consistently argued the gating provisions worked exactly as designed — but that the products had to be matched even more precisely to the underlying assets. A trust raising open-ended capital in a single-asset-class, supply-constrained, hyper-cyclical theme would behave very differently from a diversified core-plus real estate fund. BCRED, the private credit cousin launched in 2021, vindicated the model on the debt side. BXDC was conceived as the third leg of that perpetual-capital stool, this time channeled into a single, thunderous secular trend.

That secular trend was clear by 2022. Hyperscalers were quietly signing fifteen-year leases at rents 30% to 50% above prior peaks. Power interconnect queues in Northern Virginia were stretching past five years. And inside Blackstone's real estate team, the rolling thesis update — the one Gray walked through with limited partners every quarter — kept tilting more and more of the firm's marginal dollar toward the same asset.

What followed was not so much a fund launch as a coronation. By the time BXDC was registered with the SEC, the underlying business it would acquire and grow into already existed inside Blackstone's existing funds. The trust was simply the wrapper — engineered, like BREIT before it, to let individual investors own a slice of the firm's highest-conviction theme. The cornerstone of that wrapper, the asset every diligence call eventually returned to, was a take-private that had closed three years earlier and that had quietly become Blackstone's most important real estate transaction of the decade.

III. The Cornerstone: The QTS Realty Trust Acquisition

It is June 7, 2021. Vaccines are rolling out. The S&P 500 has just crossed 4,200 for the first time. And in a press release that few outside the data center industry pay close attention to, Blackstone announces it is acquiring QTS Realty Trust — a publicly listed REIT trading on the New York Stock Exchange — for $78 per share in an all-cash deal, taking the company private at an enterprise value of approximately $10 billion.[^3]

To understand the courage in that headline, you have to understand QTS in 2021. QTS was the seventh- or eighth-largest data center REIT in the United States. It owned roughly 6 million square feet of facilities across more than two dozen sites, mostly in Atlanta, Dallas, Chicago, Manassas, Phoenix, and the Netherlands. It was a respected operator, but it was not Equinix, and it was not Digital Realty — the two giants who together controlled most of the market's mindshare and most of the institutional flows.

Blackstone offered a 21% premium to the prior-day close.[^3] On a multiple of EBITDA, the deal cleared the high twenties — a number that, to a generalist REIT analyst in 2021, looked indefensible. There were public notes from sell-side desks suggesting Blackstone had paid "tomorrow's price for today's portfolio." A few argued the firm had simply outrun its own discipline.

The skeptics missed three things.

First, they missed that hyperscaler demand was not a steady-state phenomenon. It was an exponentially curving phenomenon, and even before generative AI re-priced the entire market, QTS had been quietly signing leases for individual buildings at terms that fully amortized the construction cost within the first lease period. Second, they missed that QTS was not a portfolio of buildings; it was a development engine, with a land bank and an entitlement pipeline that allowed it to add hundreds of megawatts per year inside existing campuses. The capacity inside the land bank, not the buildings already standing, was the prize. Third, and most importantly, they missed that the data center industry's binding constraint was about to change — from capital, where Blackstone enjoyed a structural advantage, to power, where Blackstone would soon learn to build an even bigger one.

Sixteen months after the take-private closed in August 2021, ChatGPT launched.1 Within twenty-four months of the close, QTS's contracted backlog had multiplied multiple-fold, and every megawatt the platform could deliver was pre-leased years ahead of construction completion. Lease rates that had penciled at $120 to $140 per kilowatt-month on the underwriting model were re-trading at $180 to $220, and in select markets, well above that. The 2021 deal that had looked aggressive was, by 2024, widely characterized inside the industry as one of the great real estate land grabs of the modern era.5

But the cleverer part of the QTS acquisition was not the buildings. It was the platform. When Blackstone took QTS private, it inherited a senior management team with decades of operating expertise — site selection, utility negotiation, mechanical engineering, network density planning, customer relationships with every major hyperscaler. That team became, in effect, the operating system on which Blackstone would build the rest of its global data center business. It was the difference between owning a fleet of trucks and owning a logistics company. QTS gave Blackstone the people, not just the property.

This is the most underappreciated point about BXDC. The trust is not a passive collection of long-leased buildings. It is a sponsor-aligned vehicle that sits on top of an integrated operating platform — one whose institutional knowledge cannot be replicated by writing a check. Hyperscalers do not sign hundred-megawatt leases with newcomers. They sign with the operators they trust to deliver on time, at the agreed power-usage-effectiveness, with the proper redundancy, in the right power market. QTS, post-acquisition, became one of perhaps four operators in the world that could credibly bid for those mandates at multi-gigawatt scale.

There is a second layer here worth dwelling on. The 2021 take-private also gave Blackstone the legal flexibility to do something a publicly listed REIT could not easily do — re-shape the portfolio at speed without quarterly earnings volatility. Within months of the close, the firm shifted the development pipeline aggressively toward hyperscale-only campuses, exited non-strategic colocation footprints, and quietly began accumulating land in markets — Indiana, central Ohio, Arizona, Aragón in Spain — that were not yet on the radar of public-market analysts but where utility capacity was available. By the time the rest of the market understood the scarcity of grid interconnection, Blackstone already owned a multi-year head start.

That head start became the asset base on which BXDC would be built. And the operator inside BXDC — the institutional knowledge that turns concrete and copper into compounding cash flow — would be the next thing to understand.

IV. Current Leadership and the Blackstone "Machine"

To meet Wesley LePatner is to meet, in many ways, the archetypal Blackstone executive of the 2020s. She is not a flashy public-markets persona. She does not give long interviews. She does not write op-eds. What she does do, according to those who have worked with her, is run the kind of relentlessly disciplined investment process that Blackstone has spent four decades institutionalizing — the calibrated underwriting, the deep diligence cadence, the alignment of every incentive with long-duration outcome.

LePatner was tapped to serve as Chief Executive Officer of BXDC, after a career inside Blackstone that included senior roles in the firm's Real Estate Americas and Core+ business, where she helped build BREIT into the largest non-traded REIT in history.6 That résumé is the giveaway. Blackstone's choice of leader for BXDC was not a digital infrastructure specialist parachuted in from outside; it was an executive who had already led the firm's most successful retail-channel real estate vehicle through both its great accumulation phase and its great redemption test. The institutional message was unmistakable. BXDC was going to be operated less like a niche tech-adjacent fund and more like a permanent-capital franchise designed to outlive any one cycle.

Above her sits the apex of the Blackstone machine. Jon Gray, as president and chief operating officer, remains the firm's chief narrator on data centers. His public commentary — particularly his statement on CNBC in May 2024 that data centers represent "the most exciting investment theme" the firm has seen in his career, against a development pipeline of more than $100 billion — sets the tone that limited partners and individual investors alike use to calibrate the importance of BXDC inside the broader Blackstone portfolio.[^4] When Gray uses words like "thematic conviction," he means them in a specific, technical sense — that Blackstone is willing to allocate marginal capital at scale years before consensus catches up. That phrase has been used inside the firm to describe the warehouse trade, the rental housing trade, and now, most aggressively, the data center trade.

The economics of BXDC's management arrangement matter. Non-traded REITs in the Blackstone style typically charge an annual management fee around 1.25% of net asset value, plus a performance-linked participation above a defined hurdle.7 The specifics for BXDC mirror the architecture pioneered in BREIT, with refinements informed by the redemption-cycle experience. The deeper alignment, though, is the balance-sheet commitment. Blackstone has historically signaled conviction in its perpetual-capital vehicles by warehousing seed assets, co-investing alongside outside shareholders, and providing fee waivers during ramp periods. The point is not the precise basis points; the point is that, for an individual investor evaluating BXDC, the management is co-invested in the same vehicle, on the same terms, at meaningful scale.

But the truly hard-to-replicate advantage isn't the people or the fees. It's the data lake. Blackstone owns operating businesses across more than 250 portfolio companies and more than 12,000 real estate assets globally. Every one of those businesses generates a real-time signal — what tenants are paying for warehouse rent in Phoenix, how much electricity a logistics campus is consuming in Madrid, what wage inflation is doing inside a private hotel chain in Texas. In data centers specifically, the firm sees power consumption patterns, AI training cluster utilization, hyperscaler leasing velocity, and chip-supply cycles months before public-market analysts can stitch the same picture together from earnings calls and trade press.

The cultural framing of this data advantage inside the firm is striking. Gray and his team often describe it as "seeing around corners," which is a polite way of saying that having a real-time view across hundreds of billions of dollars of operating assets is, in itself, a non-trivial information edge. For BXDC specifically, that edge translates into two operational decisions. It informs where to buy land — meaning which utility service territories will be able to deliver new power and which won't. And it informs how to structure leases — meaning whether to lock in long-duration contracts with fixed escalators or accept shorter terms in exchange for mark-to-market upside.

Stepping back, the picture is that of an operating engine, not a fund. BXDC has a CEO with deep retail-channel REIT experience. It has a chief investment narrator in Gray who has been articulating the data center thesis to limited partners for half a decade. It has the QTS management team underneath it. And it has, behind all of them, the broader Blackstone organization — eight hundred real estate professionals, hundreds of analysts in adjacent verticals, and a balance sheet that allows the firm to underwrite the longest-duration capital projects in the industry.

That is the corporate context. The next question is the operational one. What exactly is being built, and why is the binding constraint no longer concrete or fiber, but electrons?

V. The "Hidden" Business: The Power and Cooling Bottleneck

There is a phrase circulating among data center developers in 2026 that captures the inversion of the industry. "We used to be in the real estate business. Now we're in the power business that happens to occupy buildings."[^11]

That sentence, more than any chart, explains why BXDC matters and why Blackstone moved with the speed it did. A data center, from the perspective of a hyperscale tenant, is the integration of three things — land in the right jurisdiction, power delivered at scale, and a building that can house the cooling and the racks. Land is cheap relative to the other two. Buildings are commoditized. Power is the binding constraint.

The reason is physics. A single rack inside a modern AI cluster, populated with the most recent generation of NVIDIA GPUs, can draw 80 to 130 kilowatts of power — roughly ten times what a traditional cloud computing rack drew a decade ago. Multiply that by tens of thousands of racks inside a single training cluster, and you arrive at a campus that consumes 200 to 500 megawatts continuously. To put that in context, 500 megawatts of continuous draw is roughly the power consumption of a city of half a million people. And the U.S. utility grid, which was not built for that kind of point-load growth, simply cannot deliver it on demand. Interconnection queues in major markets stretch past five years. In Northern Virginia — the largest data center market on Earth — Dominion Energy publicly acknowledged a multi-year backlog before any new mega-campus could be energized.[^11]

This is what Gray has been quietly building Blackstone around since 2018. The firm is not just buying buildings; it is buying the only thing that limits the buildings — long-term, contracted access to electrical capacity. In some cases, that means partnering with regulated utilities. In others, it means investing directly into power generation. In a 2023 transaction that drew comparatively little public attention at the time, Blackstone backed a series of energy investments designed to deliver dedicated generation capacity to its digital infrastructure portfolio.[^11] The strategic logic was identical to the 1990s playbook of vertically integrating supply chains — except the supply chain in question is electrons, and the customer is a $3 trillion hyperscaler.

The portfolio composition of BXDC reflects this. The trust's primary asset base is the hyperscale data center campus — large, single-tenant or anchor-tenant facilities purpose-built for cloud and AI workloads. But around that core sits a thoughtful constellation of adjacent businesses. Fiber network assets — the long-haul and metro fiber that connects campuses to cloud regions and to internet exchanges — function as the circulatory system for the entire data infrastructure economy. Edge computing — smaller-format facilities closer to end users that handle latency-sensitive workloads — sit on the periphery, growing in importance as autonomous systems and immersive applications scale. Together, these segments form what BXDC describes in its filings as digital infrastructure broadly defined, not narrowly as data center real estate.

The most technically demanding shift is in cooling. For two decades, data centers cooled their servers with air. Cold air was pumped under raised floors, drawn up through racks, and exhausted out the top of buildings. That topology works for racks drawing 5 to 20 kilowatts. It does not work for racks drawing 80 to 130 kilowatts. The thermal density of modern AI clusters has forced the industry into liquid cooling — circulating fluid directly through cold plates attached to the chips, or in newer designs, immersing the servers themselves in non-conductive fluid baths. NVIDIA's most recent server architecture, the Blackwell generation, was designed assuming liquid cooling as the default rather than the exception.8

This matters for BXDC because it changes the economics of new construction versus retrofit. A data center built before 2022 can be retrofitted for liquid cooling, but only partially, and at significant capital cost. A data center designed from the ground up for liquid cooling — with the appropriate piping, pumping, heat-rejection equipment, and structural reinforcement — commands a premium lease rate and a longer effective useful life. BXDC's development pipeline, sitting on the QTS engineering platform, has been designed under the assumption that liquid-cooled, AI-ready capacity is the baseline standard for new construction, not an upgrade option.

The economic implication of all of this is that the cost curve in the industry is bifurcating. Existing capacity — air-cooled, in well-located markets, with adequate power — is rising in value because it is impossible to replace at the same cost basis. New capacity — purpose-built, liquid-cooled, with secured power — is being signed at lease rates that justify the construction cost and then some. BXDC sits in both pockets simultaneously. It owns existing assets whose replacement cost is far above carrying value, and it is building new assets whose contracted economics print attractive long-duration cash flows.

A reader steeped in commercial real estate will recognize the pattern. It is the same pattern that has historically rewarded the best operators in the warehouse and apartment sectors — own the irreplaceable, build the in-demand, and let the rest of the market chase yesterday's vintage. The difference is the scale of the demand curve. Apartments and warehouses are normal-growth markets. Hyperscale AI compute is, at least at the moment, growing at rates that look more like the early years of mobile telecommunications than like a normal real estate cycle.

The next question is the corollary. If demand is this strong and supply is this constrained, how is Blackstone deploying capital — and what is its discipline?

VI. M&A and Capital Deployment: Building the Fortress

In December 2023, Blackstone and Digital Realty Trust — itself a S&P 500-listed REIT and one of the two largest publicly traded data center operators in the world — announced a joint venture to develop hyperscale data center campuses in Frankfurt, Paris, and northern Virginia, an arrangement reported to involve as much as $7 billion of total development cost.9

The deal was important for two reasons that have nothing to do with the headline number. First, it signaled that even the largest dedicated public REIT in the industry had concluded that the most efficient way to build at the scale the market now demands is to partner with private capital. The economics of a 300-megawatt campus, with construction taking three to five years and lease commencement another year beyond that, simply do not fit cleanly inside the quarterly-earnings rhythm of a public company. Blackstone's perpetual-capital balance sheet does. Second, the deal extended BXDC's geographic footprint into the most supply-constrained markets in Europe, where regulatory permitting, grid interconnection, and political acceptance of large industrial loads are slower and harder than in the U.S. Sun Belt.

The Digital Realty venture is illustrative of a broader BXDC acquisition pattern. Rather than pursuing fully leased, stabilized assets at fully-priced cap rates, the trust has consistently preferred two more attractive entry points. The first is acquiring "shelled" capacity — concrete buildings whose construction is finished but which have not yet been fully leased or fitted out for tenants. Shelled capacity carries leasing risk, but it dramatically compresses the time to first cash flow versus ground-up development, and it commands a price-to-replacement-cost discount that compensates for the leasing exposure. The second is the platform acquisition — buying an entire operator, with its team and land bank and customer book, rather than just its standing assets. QTS in 2021 was the archetype.

Why does Blackstone outbid traditional REIT buyers on these mandates? The answer is cost of capital, but in a more subtle sense than the phrase implies. A public REIT's cost of equity is whatever the public market is willing to pay for its dividend yield in a given quarter, and that number is volatile. A public REIT's cost of debt is whatever spread the corporate bond market is willing to give it, and that, too, is volatile. A perpetually offered private REIT, by contrast, raises capital at a relatively steady annualized rate from the private wealth channel, deploys it into long-duration assets, and matches that with private debt issued through Blackstone's own credit platforms. The result is a stable, integrated, long-duration capital stack that can underwrite ten-to-fifteen-year construction-plus-lease economics on terms that no quarterly-reporting public competitor can match.

The capital deployment isn't just about price; it is about speed. By 2025, BXDC and the wider Blackstone data center business had reportedly committed or deployed tens of billions of dollars across U.S., European, and Asia-Pacific markets, with a development pipeline that Gray described publicly as more than $100 billion in total.[^4] To put that in scale, $100 billion of data center construction is roughly the equivalent of building the entire 1990s-era U.S. internet backbone — power, cooling, fiber, structure — every year, for several years running.

There is a sober question hidden inside that headline. Is $100 billion of pipeline a number to celebrate, or a number to fear? Traditional real estate cycles have ended in tears precisely when developers raced to build inventory ahead of demonstrated demand. The 2007 condominium boom in Miami and the late-1980s office build-out in Houston are textbooks on that pattern. The reason BXDC's pipeline looks different — and this is the crux of the bull case — is that the great majority of the pipeline is being built against pre-signed leases from investment-grade hyperscalers, with rents fixed for ten years or more before the first kilowatt is even delivered. The pipeline is not speculative inventory. It is contracted infrastructure.

The competitive landscape is illustrative. The publicly listed peer set — Digital Realty, Equinix — has been growing, but at a pace constrained by public-market discipline. Private peers like Vantage Data Centers, Aligned Data Centers, and CyrusOne (taken private by KKR and Global Infrastructure Partners in 2021 in a transaction valued around $15 billion) have been growing aggressively but lack the integrated balance sheet and global platform Blackstone has assembled. At the largest end of the market — the mandates for full multi-gigawatt campuses — the realistic bidder set narrows to perhaps four or five names globally. BXDC, on the strength of QTS plus the broader Blackstone real estate machine, is consistently in that bidder set.

The deeper strategic insight is this. In real estate, you make money in three ways — you can buy below replacement cost, you can develop into demonstrable shortages, or you can extract operating leverage from an established platform. BXDC, structurally, is set up to do all three simultaneously, which is unusual. Most real estate strategies have to pick. The QTS platform gives operating leverage. The pipeline gives development upside. And the firm's ability to acquire shelled capacity from distressed or capital-constrained competitors gives it the below-replacement-cost entry point. Each of those three engines runs at a different pace, and together they produce the integrated franchise that makes BXDC plausibly Blackstone's most important real estate vehicle of the decade.

But strategy and pipeline alone do not protect a business in the long run. What protects a business is the durability of its competitive advantages. To assess BXDC properly, you have to put it inside the analytical frameworks that long-term fundamental investors actually use.

VII. Analysis: Hamilton's 7 Powers and Porter's 5 Forces

Hamilton Helmer's framework asks a simple question. What is the durable, structural advantage that allows a business to earn excess returns over the long term? There are seven possible answers, and any honest analyst will admit most companies do not actually have one. BXDC has at least three, and possibly four.

The first is what Helmer calls Cornered Resource. In BXDC's case, the cornered resource is not patented intellectual property or a rare commodity — it is the power interconnection itself. Once a data center campus has secured a 500-megawatt feed from the local utility, with substations built, switchgear installed, and capacity contractually committed, that interconnect is, in a literal physical and regulatory sense, impossible to replicate at the same site for a competitor. Utility queues do not allow it. Substation costs do not allow it. Permitting timelines do not allow it. A campus's power interconnect is, in effect, a deed to a portion of the electrical grid, and the value of that deed has gone up multiple-fold as AI demand has emerged.

The second is Scale Economies. The economics of negotiating multi-gigawatt power contracts, of buying GPU cooling systems at fleet scale, of building campuses concurrently with shared mechanical and electrical infrastructure, are dramatically tilted in favor of the largest operators. A single 200-megawatt project requires a procurement effort. Ten 200-megawatt projects in parallel can share that procurement, share the engineering design, and negotiate transformer and generator orders years in advance — vital in an environment where switchgear lead times have stretched to two and a half years. Blackstone's combined data center footprint, far larger than any other single owner globally, generates a scale advantage in procurement, in engineering, and in customer relationships that smaller operators simply cannot match.

The third is Switching Costs, and this one is profound. Once a hyperscaler racks its servers, runs its fiber, configures its load balancing, deploys its automation software, and trains its operations team on a particular data center campus, the cost of moving — in dollars, in downtime, in operational risk — becomes prohibitive. The industry data on hyperscaler tenant retention is striking. Renewal rates inside large data center portfolios are routinely above 95%, with many leases ending in expansions rather than relocations.10 In effect, once a customer chooses your campus, you have effectively rented them a piece of geography that they will not voluntarily abandon for the life of the build.

The fourth, more arguable, power is Counter-Positioning. Public REIT competitors structurally cannot offer the same length-of-lease commitments or absorb the same near-term margin compression during ramp because doing so would damage their public-market multiple. Private capital does not have that constraint. The result is that BXDC can win contracts on terms that public competitors cannot match without harming their own equity story. That is the textbook definition of counter-positioning.

Turning to Michael Porter's Five Forces, the picture is, in most dimensions, structurally favorable to BXDC.

Threat of New Entrants is low. The capital required to build a single hyperscale campus runs to several billion dollars. The expertise required to deliver one on time, at the requisite power-usage-effectiveness, with the requisite redundancy and security, lives inside perhaps a dozen organizations globally. Most importantly, the binding constraint — utility power — cannot be acquired with capital alone, because utility queues are gated by regulators, not by checkbooks.

Bargaining Power of Suppliers is mixed, and the most interesting variable in the analysis. The primary suppliers are utilities (or independent power producers) and chipmakers (most consequentially, NVIDIA). Utilities are regulated and have limited ability to extract supernormal profits — but they do have the ability to delay or refuse new interconnections, which is functionally a form of supplier power. Chipmakers, especially NVIDIA, hold pricing power at the chip level, but this is a power exerted on the hyperscaler tenants, not on BXDC. The trust's economics depend on hyperscaler demand for capacity, not on the chip margin embedded inside that capacity. In a perverse way, NVIDIA's pricing power is helpful to BXDC because it accelerates hyperscaler urgency to lock in scarce real estate before their compute fleets are ready to deploy.

Bargaining Power of Buyers is the most interesting force to dwell on. Hyperscalers are large, sophisticated, and concentrated — fewer than ten companies globally account for the dominant share of new data center leasing. In a normal real estate market, that concentration would represent crushing buyer power. The reason it does not crush BXDC's economics is supply scarcity. As long as the industry is short on power-and-cooling capacity, hyperscalers are bidding for sites, not the other way around. If — and this is the bear case to take seriously — the demand growth slows or the build-out catches up, that balance of power can invert. For now, in 2026, hyperscaler leasing decisions look more like queue-management problems than vendor-selection negotiations.

Threat of Substitutes is low at the level of the asset class. There is, today, no substitute for physical compute infrastructure to host AI workloads. There are subtle, second-order substitution risks — distributed compute, edge deployments displacing centralized capacity, quantum or neuromorphic architectures with very different physical footprints — but these are speculative and many years out. The nearer-term substitution risk is geographic, not technological. If new markets like the Gulf states, Malaysia, or sub-Saharan Africa become viable hyperscale destinations, capacity may shift to those markets rather than expanding in existing ones.

Industry Rivalry, finally, is intense in bidding, but cooperative in delivery. The major operators routinely partner with one another on individual campuses, share build-out best practices through industry trade groups, and recruit from a small common talent pool. Rivalry has not, to date, materially compressed lease economics, because the binding constraint has remained capacity rather than competition.

Pulling it together, the picture for BXDC is of a business operating in a structurally attractive industry, with at least three durable Helmer powers, against a backdrop of demand growth far in excess of supply growth. That is a rare configuration, and it explains why Blackstone is willing to make data centers the largest single thematic bet of its history.

VIII. Playbook: Business and Investing Lessons

There is a common thread running through every great real estate fortune in history — Astor in 1830s Manhattan, Reichmann in 1980s London, Sam Zell in 1990s offices, Blackstone in 2010s logistics. The thread is conviction in the trend before consensus arrives, paired with the operational ability to execute at scale once the conviction is in place. Every part of the BXDC story is an attempt to compress that pattern into a single vehicle.

The first lesson is simple to state and difficult to live by. Don't bet against the hardware cycle. The history of technology investing is littered with platform-level capital allocators who concluded — in the early 1990s, in the late 1990s, in the late 2010s — that the physical layer was a commoditized loser and that the value would all accrue to software, services, or content. They were each right for a window and wrong on a decade-long view. The picks-and-shovels layer is structurally where capital intensity creates moats. Owning the landlord to the picks-and-shovels providers — which is what BXDC is — is, on a multi-decade view, often the safest way to participate in a technology super-cycle. It is the same insight that drove Levi Strauss to make jeans rather than mine gold.

The second lesson is about the courage of thematic conviction. Blackstone did not gently dip its toe into data centers. Once Gray and his team concluded that the asset class was a structural beneficiary of multiple, reinforcing secular trends — cloud migration, then AI training, then AI inference, then edge computing — the firm moved capital into the theme at scale that dwarfed every prior real estate trade in its history. The lesson for the individual investor is not to imitate Blackstone's exact moves, but to internalize the discipline. When the evidence is overwhelming, the right answer is rarely a small position. The right answer is to size for conviction. The risk is that conviction without humility metastasizes into hubris, and the great risk to BXDC's long-run performance is precisely whether the firm maintains the humility to under-build into demand slowdowns when they come.

The third lesson is operational. Owning the management platform matters more than owning the buildings. The QTS acquisition gave Blackstone a capability that could not be replicated by writing a larger check for a fully leased portfolio. Operating expertise, in capital-intensive industries, compounds in ways that pure capital does not. Every campus QTS builds becomes the curriculum for the campus after it. Every hyperscaler relationship becomes the foundation for the next contract. The lesson for analysts evaluating BXDC is to weight the platform — meaning the people, the systems, the customer book — at least as heavily as the standing portfolio in any valuation framework.

The fourth lesson, painfully learned, is about liquidity. The BREIT redemption episode of 2022 and 2023 was a defining stress test for the entire non-traded REIT category, and Blackstone walked away from it with a sharpened understanding of how perpetual-capital structures behave under stress. The key insights — long-duration assets cannot fund short-duration liquidity demands, gating provisions are features rather than bugs, and individual investors must enter these vehicles with a multi-year horizon — are now embedded in the design of BXDC. The lesson for the individual investor is that the wrapper matters. A non-traded REIT is not a mutual fund. It is, by design, less liquid and more matched to the underlying assets. That trade-off is appropriate for some portfolios and inappropriate for others, and any allocation discussion should start with that.

A final, more contrarian lesson — perhaps the most Acquired-style takeaway in the whole story — is the lesson of using a structural form mismatch as a competitive weapon. Blackstone's perpetual-capital advantage over public REIT competitors exists because public companies are structurally penalized by markets for the same long-duration decisions that Blackstone is rewarded for. That asymmetry will not last forever — markets adapt — but for a window of probably a decade, it represents one of the cleanest examples in modern finance of a vehicle structure being a competitive advantage in its own right. The history of investing has many examples of this. Berkshire Hathaway's structural ability to hold permanent capital was, for forty years, one of its largest unappreciated edges. BXDC is the data-center-era equivalent.

What about the KPIs an investor would actually watch? In a business with this much complexity, the temptation is to track dozens of metrics. The discipline is to track few. For BXDC, three numbers matter more than all the rest. The first is contracted leased capacity as a percentage of installed and under-construction capacity — meaning, what share of the megawatts the trust controls are committed under long-term leases to investment-grade tenants. The second is weighted-average remaining lease term, expressed in years — a measure of how long the cash flow is locked in. The third is the development yield, meaning the unlevered yield on cost the trust earns on newly delivered capacity relative to its construction expenditure. If those three numbers stay healthy, the story stays intact. If any of them deteriorates materially over consecutive quarters, the story is in question.

With the lessons articulated, the harder analytical question is what could go wrong. Every great real estate story has been a great real estate story until, suddenly, it was not. To analyze BXDC seriously is to take both sides equally.

IX. The Bear vs. Bull Case

The bear case for BXDC is not what most people assume. It is not that AI is a fad. The bear case is more sophisticated, and more important to engage with honestly.

Start with interest rate sensitivity. BXDC is, structurally, a long-duration real estate asset. Its cash flows extend for decades. Its valuation, like that of any long-duration cash flow stream, is highly sensitive to the discount rate. In an environment where the U.S. ten-year Treasury yield rose materially — say to a sustained level above 6% — the implied cap rate on hyperscale data centers would rise, and the net asset value of the trust would compress. The 2022 to 2023 rate cycle showed how sharp that effect can be on real estate trusts more broadly. Investors who buy BXDC expecting equity-like returns must accept that the vehicle carries meaningful duration risk.

Next is the over-build risk. Every great real estate cycle ends in a glut, and the question is not whether but when. The current AI capital expenditure cycle is being funded by perhaps eight to ten hyperscalers, almost all of whom carry investment-grade balance sheets and are guiding to multi-year capital plans. If any of those hyperscalers materially reduces its capex pace — whether because AI inference economics disappoint, or because a model architecture innovation reduces compute intensity, or because a regulatory shock constrains demand — the leasing pipeline that BXDC relies on could decelerate sharply. The pipeline does not need to disappear; it merely needs to slow, while supply that has already been committed continues to come online. That mismatch is the textbook recipe for a vacancy and lease-rate correction.

A more technical bear case is the obsolescence risk from on-site power generation and modular nuclear technology. If, over the next decade, modular nuclear reactors become commercially deployable at scale, hyperscalers may begin to source their own power generation on-site, bypassing the utility entirely. That would be net positive for the data center industry as a whole — it would unlock capacity that grid constraints currently prevent — but it could also reduce the strategic value of existing campuses that depend on grid interconnection. BXDC's response, visible in the firm's energy investments, is to position to participate in that transition rather than be disrupted by it. But the risk is real and worth tracking.

A bear case worth highlighting separately is the regulatory and political risk. Data centers consume enormous amounts of power and water. Communities that initially welcomed them are increasingly pushing back — moratoria in parts of Virginia, height and noise restrictions in Ireland, water-use restrictions in Arizona. As individual hyperscale campuses get larger, the political attention they attract grows nonlinearly. The risk is not that any single jurisdiction shuts the industry down, but that incremental restrictions on land use, water draw, and power allocation slow the rate at which new capacity can be added relative to the lease demand the industry is creating.

The bull case, equally seriously articulated, is that the AI build-out has barely begun. Total AI compute capacity globally remains a small fraction of what would be needed to serve every enterprise workload that could plausibly be re-architected to use generative or agentic AI. Public estimates of the inference compute required to migrate a meaningful share of enterprise applications to AI-native architectures run into multiples of the entire current global hyperscale fleet. Gray and the Blackstone team's published thesis — that this is "the most exciting investment theme in a generation" — is rooted in that arithmetic.[^4] If the bull case is right, the current pipeline that critics worry is an over-build is, in fact, an under-build, and the binding constraint will continue to be power and land for the rest of the decade.

The bull case also has a corollary worth stating. As enterprises migrate from on-premise infrastructure to cloud, and from cloud-native applications to AI-native applications, the unit economics of compute shift. AI workloads are an order of magnitude more power-intensive than traditional cloud workloads. They are also less elastic in deployment — once a training cluster is configured, it tends to run continuously at high utilization, unlike traditional cloud workloads that scale up and down with daily and weekly patterns. The implication for the landlord is favorable. AI tenants pay for more megawatts, on longer leases, with smoother power utilization. That is, in every respect, a better customer for a real estate trust.

The myth versus reality discussion is interesting here. The consensus narrative — repeated in financial press and on countless quarterly calls — is that "AI demand is insatiable and BXDC is the cleanest way to play it." The reality is more nuanced. AI demand is large and growing, but it is also concentrated in a small number of buyers, sensitive to chip availability, and dependent on the economics of AI applications generating real revenue for those buyers. The cleanest mental model is to treat BXDC less as a pure AI play and more as a play on the broader trajectory of digital infrastructure scarcity — of which AI is the most acute current demand source but not the only one. Cloud migration alone, even absent AI, would have justified significant data center build-out for the rest of the decade.11

A holistic frame brings the Helmer and Porter analyses back into the bull-bear conversation. The structural advantages BXDC enjoys — the cornered resource of power interconnects, the scale economies in procurement and operations, the switching costs of hyperscaler tenants — are durable. They will outlast any individual demand cycle. The risks — interest rate sensitivity, over-build, regulatory pushback, on-site power disruption — are cyclical or technological, and they will require active management by the trust's leadership. The question for any long-term investor is whether the structural advantages compound faster than the cyclical risks erode them. That is the question Wesley LePatner and Jon Gray are, in effect, paid to answer with every capital decision they make.

The honest summary is that BXDC is a high-quality vehicle inside a structurally favorable industry with real but identifiable risks. It is not riskless. No real estate trust ever has been. But the combination of asset quality, platform expertise, and capital structure is unusual, and it deserves to be evaluated on its own terms rather than against the rhythms of a typical real estate cycle.

X. Epilogue and Final Reflections

There is a recurring pattern in the history of capital markets. A new asset class emerges. It is initially the domain of specialists — a handful of institutional investors who recognize the structural opportunity before consensus forms. Then, over time, the asset class is packaged into vehicles accessible to broader pools of capital, first to institutions, then to individual investors. The packaging often outlasts the initial opportunity. Railroad bonds, oil partnerships, suburban shopping centers, mortgage-backed securities, real estate investment trusts themselves — each was, in its time, a structural innovation that converted a specialist asset into an investable wrapper.

BXDC sits squarely inside that lineage. The asset — hyperscale digital infrastructure — has been a specialist allocation for institutional capital since the early 2010s, accessible through private funds, joint ventures, and the equity of a small number of public REITs. The innovation is the wrapper. By packaging this asset class into a perpetually offered, non-traded real estate trust designed for the private wealth channel, Blackstone has effectively democratized institutional-grade infrastructure for individual investors. Whether that is a benefit or a risk depends on whether the wrapper is well-matched to the assets and whether the investors entering it understand what they are buying.

The trust's eventual scale is the great open question. Blackstone's BREIT, at peak, exceeded $70 billion of equity raised. If BXDC reaches that scale — and the addressable market for digital infrastructure exposure inside the private wealth channel is plausibly large enough to support it — it would become one of the largest pools of dedicated data center capital on Earth. It would also, by virtue of its size, become a price-setter rather than a price-taker in the market for hyperscale campus acquisitions and developments. That dynamic is uncomfortable in some ways and advantageous in others. Price-setters earn returns on scale economies but absorb the responsibility of being the marginal bidder in market downturns. The exit from that role, if and when it comes, will be a defining stress test for the trust.

The broader legacy question is more interesting than the size question. Will BXDC be remembered as a tactical product launched at the right moment to capture a generational theme — or as a structural step forward in how individual investors can access infrastructure exposure on terms previously reserved for sovereign wealth funds and pension plans? The case for the latter rests on a quietly important observation. Until the launch of trusts like BXDC, the only way for an individual investor to own a sliver of the digital infrastructure layer was to buy public REITs like Equinix or Digital Realty, whose price action and lease economics are heavily influenced by quarterly earnings dynamics and equity market sentiment. BXDC offers an alternative — direct, private market exposure to the underlying assets, with the trade-off of reduced liquidity and a longer holding horizon.

The democratization comes with risks worth naming. Non-traded REITs require investors to plan for liquidity that is, by design, partial. They require trust in the sponsor's net asset value calculations, which are model-driven rather than market-driven. They carry fee loads that, while competitive within the category, are higher than passive public market exposure. The reason long-term-oriented investors might still find the trade attractive is that the underlying assets — hyperscale data centers — are themselves long-duration and structurally illiquid, so the wrapper matches the asset more honestly than a daily-traded vehicle would.

Stepping back from the structural debate, what is most striking about BXDC at this moment in 2026 is how cleanly it captures the spirit of its parent firm. Blackstone has spent four decades building the institutional capacity to act on themes at scale, to underwrite long-duration assets with patient capital, and to compound advantages by owning platforms rather than collecting deals. BXDC is the purest distillation of that capability deployed against what may turn out to be the most important physical infrastructure theme of this generation. The bet is sized for conviction, the platform is built for scale, and the structure is engineered for permanence.

Whether that bet plays out as the bulls expect or the bears warn, history will judge in fifteen-year increments, not in quarterly headlines. What is already clear, in this spring of 2026, is that the firm that built the largest commercial real estate portfolio in the world by buying neighborhoods has decided, with characteristic concentration, that the neighborhood of the next decade is the place where electrons meet silicon meet steel. Every hyperscaler at this moment is competing to lease space inside someone's campus. Increasingly, that campus is owned by Blackstone, operated by the QTS team, and capitalized through BXDC.

The picks and shovels of the AI revolution turned out, after all, not to be made of metal. They are made of concrete, switchgear, copper, fiber, and cold water — assembled in windowless boxes on the cheap land between airports and high-voltage substations. The landlord business, as ever, was the one to watch.

References

-

Blackstone Digital Infrastructure Trust (BXDC) Official Fund Page — Blackstone ↩

-

Jon Gray on Thematic Investing and Data Centers — WSJ, 2024-01-10 ↩

-

The Great Data Center Land Grab — Financial Times, 2024-03-15 ↩

-

QTS Realty Trust: The Engine of Blackstone's AI Strategy — Reuters, 2023-11-20 ↩

-

Wesley LePatner Named CEO of BXDC — Blackstone Leadership Bio ↩

-

Blackstone Quarterly Earnings Call Transcript (Q1 2024) — Blackstone Investor Relations ↩

-

Blackstone and Digital Realty Form $7 Billion Data Center JV — Bloomberg, 2023-12-07 ↩

-

QTS Realty Trust: The Engine of Blackstone's AI Strategy — Reuters, 2023-11-20 ↩

-

The Great Data Center Land Grab — Financial Times, 2024-03-15 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube