Burlington Stores: The Off-Price Empire Built on Coats

I. Introduction & Episode Roadmap

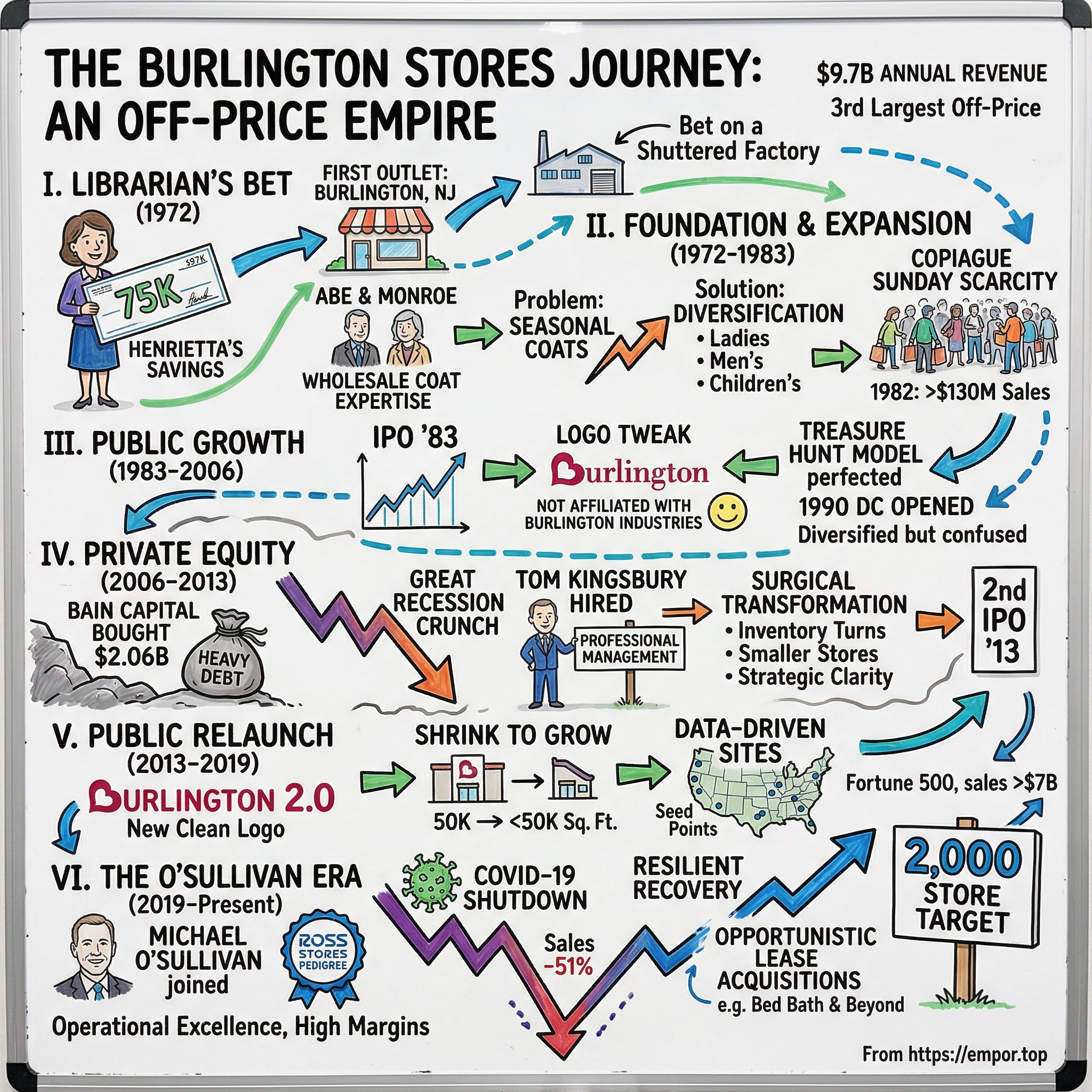

Picture this: A librarian in 1972 New Jersey empties her life savings—$75,000 she'd squirreled away over years of careful budgeting—and convinces her wholesale coat merchant husband to bet it all on a shuttered factory outlet in Burlington. That single decision would spawn an empire that today generates $9.7 billion in annual revenue across more than 1,000 stores, making Burlington Stores the third-largest off-price retailer in America behind only TJX Companies and Ross Stores.

The Burlington story defies conventional retail wisdom at every turn. While department stores crumbled and specialty retailers pivoted desperately to e-commerce, Burlington quietly perfected a treasure hunt model that turns inventory chaos into competitive advantage. They've survived family feuds, trademark battles, a leveraged buyout at the worst possible time, and emerged stronger from a pandemic that killed legacy retailers. Today, with a market capitalization hovering around $15 billion, Burlington represents one of retail's most underappreciated transformation stories.

What makes Burlington fascinating isn't just its survival—it's the deliberate strategic evolution from a regional coat wholesaler to a sophisticated off-price machine. This is a company that went public twice, endured private equity ownership during the Great Recession, and somehow emerged leaner and more profitable. It's a story about reading demographic shifts before competitors, about turning operational constraints into strategic advantages, and about building a culture that thrives on controlled chaos.

Over the next few hours, we'll unpack how a family business built on wool coats became Wall Street's favorite recession-resistant retail play. We'll explore the Milstein family's entrepreneurial genius, Bain Capital's controversial but transformative ownership period, and the current management team's ambitious plans to double the store base. Along the way, we'll decode the off-price model that confounds traditional retailers, examine why Burlington trades at a discount to peers despite superior execution, and assess whether the company's 2,000-store vision represents opportunity or hubris.

This isn't just another retail turnaround story. It's a masterclass in adaptation, a case study in private equity value creation, and perhaps most importantly, a blueprint for building a business model that actually gets stronger during economic downturns. The journey from that first Burlington factory outlet to today's off-price powerhouse reveals timeless lessons about entrepreneurship, capital allocation, and the enduring power of selling a dollar for fifty cents.

II. The Milstein Foundation: Family Business Origins (1924-1972)

The year was 1924, and Abe Milstein had just arrived in America with little more than ambition and an eye for quality fabric. While others chased the glamour of Manhattan's Garment District, Abe set up shop in Burlington, New Jersey—a working-class town where factory workers needed sturdy coats that could withstand northeastern winters. His wholesale operation specialized in what others overlooked: practical ladies' coats and junior suits that balanced durability with affordability. This wasn't haute couture; it was clothing for the wives and daughters of men who punched time clocks.

By 1946, Abe's son Monroe Gary Milstein had joined the family business, bringing post-war energy and expansion dreams. Father and son made an effective team—Abe handled relationships with manufacturers while Monroe modernized operations and pushed into retail. They rode the post-war consumer boom perfectly, as returning GIs married, moved to suburbs, and outfitted growing families. The Milsteins supplied coats to small department stores across New Jersey and Pennsylvania, building a reputation for reliability and fair dealing that would become the family trademark.

The real catalyst for transformation came from an unexpected source: Monroe's wife, Henrietta Milstein. Born Henrietta Haas, she'd worked as a librarian for decades, methodically saving her modest salary while raising their children. By 1972, she'd accumulated $75,000—serious money for a librarian in that era. When a factory outlet in downtown Burlington went up for sale, Henrietta saw what others missed. The location sat at the intersection of major highways, perfectly positioned to catch traffic from Philadelphia suburbs. The asking price of $675,050 seemed steep, but Henrietta convinced Monroe this was their moment. The decision to abandon wholesale for retail wasn't merely opportunistic—it reflected deeper structural changes in American commerce. The Fair Trade laws that had protected traditional retailers were crumbling. Prior to 1975, manufacturers could legally fix prices in collusion with department stores, keeping discounters at bay. But consumer advocates and aggressive retailers were breaking down these barriers. The Milsteins sensed this shift before most, recognizing that the future belonged to retailers who could offer brand-name merchandise at substantial discounts.

What made that Burlington factory outlet particularly attractive wasn't just location but timing. Though first year sales reached $1.5 million, Monroe Milstein was wary of the company's reliance on the vagaries of the thermometer, and quickly realized that substantial growth could not be predicted on unpredictable climatic variations. The solution wasn't to abandon coats but to build around them—creating a year-round business that could smooth out seasonal volatility while maintaining the core competency in outerwear that gave them credibility with both vendors and customers.

The family dynamics added another layer of complexity. Monroe brought the merchandising expertise from decades in wholesale, understanding how to source quality goods at the right price. Henrietta, despite her quiet librarian persona, possessed sharp business instincts and would later prove instrumental in expanding beyond coats into children's wear and home goods. Their partnership—he handled vendors, she understood customers—created a balanced foundation that many family businesses lack. This wasn't a vanity project or a retirement hobby; it was a carefully calculated bet on the democratization of American retail, funded by a librarian's life savings and executed with wholesaler's precision.

III. Building the Coat Factory Empire (1972-1983)

The first Burlington Coat Factory store opened its doors in 1972 with a radical proposition: brand-name, first-quality outerwear at prices 20-60% below department stores. Monroe Milstein acquired the first Burlington Coat facility in 1972, a coat factory located in Burlington, New Jersey, with an attached retail outlet. Initially, Burlington Coat specialized in selling winter overcoats, a product line whose sales were heavily dependent on the weather, peaking in the winter and dropping off during the summer months as temperatures rose. Though first year sales reached $1.5 million, Monroe Milstein was wary of the company's reliance on the vagaries of the thermometer, and quickly realized that substantial growth could not be predicted on unpredictable climatic variations.

The $1.5 million in first-year sales validated the concept but exposed a critical vulnerability: coat sales plummeted during warm months, creating cash flow nightmares and leaving expensive retail space underutilized. Monroe's solution was elegant—gradually add complementary categories that could leverage the same vendor relationships and customer base. Ladies' sportswear came first, then men's suits, then children's clothing. Each addition was carefully chosen to maintain the value proposition while smoothing seasonal swings.

The second store opening in 1975 in Copiague, Long Island, revealed both the family's operational savvy and their willingness to turn constraints into advantages. A second location was opened in 1975 in Copiague on Long Island, and Milstein asked his son Lazer, who was living in Israel at the time, to return home and act as the store's legal owner for the new location. Lazer agreed, on the condition that the store be closed Saturdays in observance of the Sabbath. At the time, businesses faced legal action for being open on Sunday, with an exception made for religions observing a different Sabbath. This religious observance, which might have seemed like a competitive disadvantage, actually created scarcity and buzz—the first Sunday saw 300 customers lined up around the block, eager to shop when department stores were closed. The expansion strategy during this period reflected Monroe's wholesale background—relationships mattered more than real estate. While department stores invested heavily in flagship locations and elaborate fixtures, Burlington leased secondary locations, often former supermarkets or industrial spaces, keeping capital requirements minimal. The stores themselves were deliberately spartan: pipe racks instead of fancy displays, concrete floors rather than carpet, fluorescent lighting throughout. This wasn't poverty; it was philosophy. Every dollar not spent on décor was a dollar that could lower prices.

By 1982 the Company exceeded $130 million in annual sales. The growth trajectory was remarkable—from a single store to a regional chain in just a decade. But what's more impressive is how the Milsteins navigated the complex vendor relationships that made this growth possible. Monroe leveraged his decades of wholesale experience to convince manufacturers to sell directly to Burlington, bypassing traditional distribution channels. He promised volume, quick payment, and discretion—manufacturers could clear excess inventory without alerting department store partners.

The decision to go public in June 1983 marked a critical inflection point. Burlington Coat Factory became a public company for the first time with an IPO in June 1983. The Company operated 31 stores at the time of the IPO, and with the capital raised proceeded to double its store count to 68 stores by 1985. By 1983 annual sales had climbed to nearly $300 million, and the company was becoming a giant in the retail industry. It went public that year, with the Milstein family purchasing a majority of Burlington Coat's stock and the company's name changing from Burlington Coat Factory Warehouse to Burlington Coat Factory Warehouse Corporation.

The IPO timing was shrewd. Traditional retailers were beginning to feel pressure from discounters, but the full disruption hadn't yet arrived. Burlington could position itself as a growth story without the baggage of being seen as a threat to the established order. The Milstein family maintained majority control, ensuring continuity of vision while accessing public markets for expansion capital. This dual structure—public company financing with family control—would define Burlington's governance for the next two decades, creating both opportunities and tensions that would eventually lead to the Bain Capital acquisition.

IV. Public Company Growth & Scale (1983-2006)

The post-IPO Burlington emerged as a retail phenomenon, but not in the way Wall Street expected. While analysts focused on comp store sales and margin expansion, the Milsteins quietly built something more profound: a parallel retail ecosystem that operated by entirely different rules. By the end of the 1980s, the Company operated 134 stores in 37 states, with net sales over $600 million.

The 1980s presented a paradox for Burlington. Consumer tastes were shifting toward designer labels and premium brands—exactly the opposite of Burlington's value proposition. Sales barely eclipsed $300 million in 1984, then inched upward, climbing to $480 million by 1987. Yet this apparent headwind became a tailwind. As department stores ordered deeper into designer inventory, the inevitable markdowns and clearances created more supply for Burlington. The company became the solution to the industry's excess inventory problem, a position that grew more valuable as fashion cycles accelerated.

The real breakthrough came from an unlikely source: a trademark dispute that would define Burlington's identity for decades. From 1981 until 2009, Burlington Coat Factory's logo was supplemented with the tag "Not Affiliated with Burlington Industries." When Burlington Coat Factory settled a trademark dispute with fabric maker Burlington Industries in 1981, Burlington Coat Factory agreed to say in advertising that the two companies were not affiliated. What seemed like a legal setback became marketing genius. The disclaimer added authenticity—here was a company so focused on value they couldn't even afford a fancy original name. Customers loved the honesty.

By 1990, Burlington had evolved far beyond its coat factory roots. Efforts toward diversification were intensified, as the number of linen stores within Burlington Coat stores rapidly increased, growing from 55 in 1989 to more than 140 by 1991. Men's apparel, particularly men's suits, became an important contributor to company sales, and stores began to offer merchandise entirely beyond the scope of many apparel retailers, including such items as children's furniture. This wasn't random expansion—each category addition followed the same logic: high-margin products that customers needed but didn't want to pay full price for.

The early 1990s recession transformed Burlington from successful discounter to essential retailer. Perhaps the most important contributor to Burlington Coat's dramatic growth was a recession in the late 1980s and early 1990s that arrested consumer demand for expensive designer apparel. As the economy suffered and many consumers were left with significantly less discretionary income, discount retailers flourished. While department stores shuttered locations, Burlington accelerated openings, often taking over their abandoned sites at fire-sale rents.

Infrastructure investments during this period proved prescient. Burlington Coat improved inventory controls and took advantage of economies of scale by constructing a 438,000-square-foot national distribution center in 1990. This wasn't just about efficiency—centralized distribution allowed Burlington to move opportunistic buys quickly across the chain, turning what could be regional oversupply into national opportunity.

The international expansion attempt revealed both ambition and limitations. In 1993, Burlington Coat signed an agreement with Mexican retailer Plaza Coloso S.A. de C.V., an operator of supermarkets and department stores, to open a Burlington Coat store in Juarez, Mexico, the company's first store outside the United States. The Mexico venture ultimately failed, teaching Burlington that its model—built on specific American consumer behaviors and vendor relationships—didn't easily translate across borders.

Family dynamics increasingly complicated corporate governance as the company scaled. Monroe remained CEO well into his seventies, with various children holding senior positions. The potential for succession disputes loomed, even as the business continued performing. By the late 1990s, only about 20% of revenues came from coat sales—the company had successfully diversified, but the name increasingly confused consumers who expected only outerwear.

The new millennium brought fresh challenges. E-commerce threatened to disrupt physical retail, yet Burlington's treasure hunt model seemed incompatible with online shopping. Younger family members pushed for modernization while Monroe insisted on maintaining the successful formula. By 2003, the company operated 335 stores across multiple concepts—Burlington Coat Factory, Cohoes Fashions, Luxury Linens, Baby Depot, and MJM Designer Shoes—each targeting different customer segments but creating operational complexity.

By 2005, the Company operated 362 stores in 42 states, with $3.2 billion in annual sales. The numbers looked impressive, but insiders knew the truth: Burlington had reached an inflection point. The family ownership structure that had enabled quick decision-making now created paralysis. Competing visions for the future—some wanted to go upscale, others to go deeper discount, still others to pursue e-commerce aggressively—couldn't be reconciled. The company needed either a clear succession plan or an exit. As private equity firms circled, sensing opportunity in the confusion, the Milsteins faced their biggest decision since that first store purchase in 1972.

V. The Bain Capital Era: Private Equity Transformation (2006-2013)

The boardroom at Burlington headquarters in April 2006 crackled with tension. Monroe Milstein, now 82, sat across from Bain Capital partners who were proposing to buy his life's work for $2.06 billion. In 2006, the company was purchased by Bain Capital Partners for $2.06 billion. The Milstein family held almost 30 million shares of the Burlington Coat Factory Warehouse Corporation, making approximately $1.3 billion, and Monroe Milstein was unassociated with the business following the sale, although two of his sons, Stephen and Andrew, stayed on briefly. For Monroe, this wasn't just a financial transaction—it was an admission that the family business model had reached its limits.

At that time, the Company operated 368 stores and generated $3.4 billion in annual sales. Bain saw what others missed: beneath the family drama and operational inefficiencies lay a fundamentally sound business model that just needed professional management and strategic focus. The timing seemed perfect—credit was cheap, the economy was booming, and private equity was revolutionizing retail.

Then 2008 happened.

Within 18 months of Bain's acquisition, Lehman Brothers collapsed, credit markets froze, and consumer spending plummeted. Burlington's debt load—typical for a leveraged buyout but crushing in a crisis—suddenly looked catastrophic. Same-store sales dropped, vendors demanded faster payment, and bankruptcy rumors swirled. Bain faced a stark choice: inject more capital into a struggling retailer during the worst recession since the 1930s, or cut losses and move on.

Enter Tom Kingsbury. Thomas Kingsbury was hired as President and Chief Executive Officer of the Company. in 2008. A retail lifer who'd spent years at May Department Stores, Kingsbury brought something Burlington desperately needed: operational discipline without abandoning the treasure hunt model. His first moves were counterintuitive—while competitors slashed inventory to preserve cash, Kingsbury invested in merchandise, betting that consumers would trade down to off-price during the recession.

The transformation under Kingsbury was surgical. Burlington solidified its new strategic foundation during this time period as a multi-category off-price retailer and embarked on the Company's mission to reduce comparable store inventories. This wasn't about carrying less product—it was about turning inventory faster. Kingsbury implemented new systems that tracked sell-through rates by SKU, allowing buyers to quickly identify winners and losers. Slow-moving inventory was marked down aggressively, creating space for fresh merchandise that kept the treasure hunt exciting.

The real genius of the Bain years wasn't financial engineering—it was strategic clarity. For decades, Burlington had been everything to everyone: coats, suits, baby furniture, linens, shoes. Under Bain's direction, the company finally answered a fundamental question: what business are we actually in? The answer: Burlington was in the business of offering branded merchandise at prices that made middle-income consumers feel smart, not poor. This subtle but crucial repositioning influenced everything from store design to marketing messages.

Physical stores underwent dramatic changes. The old Burlington stores—cavernous warehouses with harsh lighting and minimal organization—gave way to smaller, more navigable formats. Fitting rooms were upgraded, checkout lines were streamlined, and merchandise was organized into clear departments. The goal wasn't to become Nordstrom but to eliminate the friction points that prevented customers from finding treasures.

The vendor relationship strategy also evolved. Under family ownership, Burlington had relied heavily on Monroe's personal relationships and handshake deals. Bain professionalized this process, creating dedicated teams for each merchandise category and implementing data-sharing agreements that helped vendors better predict Burlington's needs. The company became a more reliable partner for brands looking to clear excess inventory, securing better access to premium overstock.

Despite operational improvements, the debt burden remained crushing. Bain had loaded Burlington with over $1 billion in debt during the acquisition, and while the company was now profitable, servicing this debt consumed cash that could have funded expansion. The dividend recapitalizations typical of private equity ownership were off the table—there simply wasn't enough cash flow. By 2012, Bain faced a familiar private equity dilemma: the company was too improved to abandon but not quite successful enough to sell at the desired return.

The decision to pursue a second IPO reflected both necessity and opportunity. Credit markets had recovered, retail stocks were rallying, and Burlington's transformation story resonated with investors hungry for turnaround narratives. But this would be different from the 1983 IPO—instead of a family maintaining control while accessing growth capital, this was private equity seeking an exit while positioning the company for independence. The preparation was meticulous: management presentations emphasized the runway for store growth, the sustainability of the off-price model, and the quality of new leadership. When Burlington filed its S-1 in June 2013, it represented not just a liquidity event but a bet that the company's best days were ahead.

VI. Return to Public Markets & Burlington 2.0 (2013-2019)

The opening bell at the New York Stock Exchange on October 2, 2013, marked more than just another IPO. In October 2013, the company's stock rose more than 40% on its first day of trading. The company reported $4.35 billion in sales for the 12-month period ending August 3, 2013. For Burlington, this was a resurrection story—proof that a traditional retailer could transform itself while Amazon was supposedly killing physical retail.

The post-IPO Burlington faced an identity crisis that went deeper than its name. The Company rebranded the chain -- from Burlington Coat Factory to Burlington Stores, in order to communicate that Burlington is "more than just coats." The rebrand wasn't just cosmetic—it signaled a fundamental shift in how Burlington saw itself. No longer defined by a single category or season, the company was positioning itself as a comprehensive off-price destination that happened to have started with coats.

Tom Kingsbury's strategy during this period was deceptively simple: shrink to grow. While competitors super-sized stores to offer more selection, Burlington went the opposite direction. For the first time in the Company's history, Burlington's average new store size in 2017 was below 50,000 gross square feet. The Company opened new stores at an average of 45,000 square feet in 2017, 43,000 square feet in 2018 and 42,000 square feet in 2019. Smaller stores meant lower rents, faster inventory turns, and easier navigation for customers. It also meant Burlington could penetrate markets that couldn't support a traditional 80,000-square-foot box.

In 2016, Burlington Stores joined the Fortune 500 for the first time. The Fortune 500 inclusion was more than a vanity metric—it signaled Burlington's arrival as a major force in American retail. Yet Kingsbury remained focused on operational fundamentals rather than corporate accolades. Every decision was filtered through a simple question: does this help us offer better brands at better prices?

The merchandising transformation under Jennifer Vecchio proved equally crucial. Hired Chief Merchandising Officer Jennifer Vecchio in 2015, joining Burlington with 14 years of leadership and merchandising experience in the off-price sector. Vecchio, poached from Ascena Retail Group, brought a sophisticated understanding of how to balance the chaos of off-price buying with the consistency customers expected. She reorganized the buying team, implemented new vendor scorecards, and most importantly, gave merchants more autonomy to pursue opportunistic deals.

Data analytics revolutionized Burlington's real estate strategy. Developed a more targeted data driven real estate location strategy in 2015, identifying a sufficient number of intersections ("seed points") with attractive customer demographics to be able to potentially operate 1000 stores over time. The company identified specific intersections across America where demographics, traffic patterns, and competitive dynamics aligned perfectly. These "seed points" weren't just good locations—they were mathematically optimal sites that could support Burlington's unique model. The financial performance validated the strategy. Surpassed $5 billion in sales in 2015, then surpassed $6 billion in sales in 2017, $6.6 billion in 2018 and $7.3 billion in 2019. Based on confidence in the "seed point" store location strategy, the Company accelerated new store openings from 25 net new stores in 2016, to 37 in 2017, 46 in 2018 and 52 in 2019. This wasn't just growth for growth's sake—each new store was profitable within months, a testament to the precision of Burlington's site selection.

The acceleration in store count masked a more profound transformation: Burlington was becoming a technology company that happened to sell clothes. Machine learning algorithms predicted which products would sell in which stores. Dynamic pricing models adjusted markdowns in real-time based on inventory levels and competitive activity. The treasure hunt that seemed chaotic to customers was actually orchestrated by sophisticated systems that balanced unpredictability with profitability.

Yet by 2019, cracks were appearing in the Kingsbury edifice. After more than a decade at the helm, his vision had taken Burlington from family business to professional retailer, but the next leap—to true off-price excellence—required fresh thinking. Competitors weren't standing still. TJX was investing heavily in e-commerce, Ross was aggressively expanding, and new entrants like Five Below were redefining value retail for younger consumers. Burlington needed someone who understood off-price at its core, not just as a business model but as an art form. The board's search would lead them to an unexpected choice: a Ross Stores executive who'd spent his entire career perfecting the very model Burlington was trying to master.

VII. Leadership Transition & The O'Sullivan Era (2019-Present)

The Burlington boardroom in September 2019 witnessed a changing of the guard that would define the company's next chapter. Tom Kingsbury served as the CEO from 2008 to 2018. Michael O'Sullivan, formerly President and Chief Operating Officer of Ross Stores, joined the Company in September 2019 as Chief Executive Officer. Thomas Kingsbury retired from his role as Chairman and Chief Executive Officer. The transition wasn't just a personnel change—it was a philosophical shift from retail turnaround to off-price excellence.

O'Sullivan's background was telling: 16 years at Ross Stores rising to President and COO, former Partner at Bain & Company from 1991 to 2003. He'd literally written the playbook on off-price retail efficiency at Ross, helping that company achieve industry-leading margins through operational discipline. His arrival at Burlington signaled ambitious intentions—not just to compete with TJX and Ross, but to potentially surpass them.

The first months revealed O'Sullivan's strategic priorities. While Kingsbury had focused on store growth and rebranding, O'Sullivan obsessed over merchandise turns and margin optimization. He implemented what insiders called "Burlington 2.0"—a comprehensive overhaul of buying, planning, and allocation systems designed to reduce markdowns while maintaining the treasure hunt excitement. The goal was audacious: achieve Ross-like margins while maintaining Burlington's broader product assortment.

Jennifer Vecchio, formerly Chief Merchandising Officer and Principal, was promoted to President and Chief Merchandising Officer in April 2019. This promotion, occurring just before O'Sullivan's arrival, proved fortuitous. Vecchio understood Burlington's DNA—the delicate balance between opportunistic buying and customer expectations. Together, O'Sullivan and Vecchio formed a powerful partnership: he brought operational rigor from Ross, she provided institutional knowledge and merchandising instincts.

Then COVID-19 struck. In March 2020, Burlington temporarily closed all of its stores and corporate offices as a result of COVID-19. All of the Company's stores were closed by the end of business on March 22, 2020, and remained closed through the end of the first quarter, due to the COVID-19 pandemic. Total sales decreased 51% to $798 million in Q1 2020. The pandemic arrived just six months into O'Sullivan's tenure—a baptism by fire that would test every assumption about the off-price model.

O'Sullivan's crisis management revealed his operational DNA. While competitors panicked about e-commerce, he focused on fundamentals: preserving cash, managing inventory, and preparing for reopening. The company took a massive $272 million inventory writedown in Q1 2020, essentially marking down all aged merchandise to clearance prices. This painful but decisive action cleared the decks for fresh inventory when stores reopened.

The reopening strategy proved masterful. Currently, 332 of the Company's stores have re-opened and 402 stores are expected to be open as of May 29, 2020. Burlington reopened stores methodically, using early locations as laboratories to understand new shopping behaviors. Customers returned eagerly, drawn by clearance prices and pent-up demand. Comparable sales for reopened stores declined 14% for Burlington—better than many feared and demonstrating the resilience of the off-price model during economic stress.

We launched Burlington 2.0 in 2020, our strategy for reaching our full potential as an off-price retailer. Burlington 2.0 wasn't just corporate jargon—it represented a fundamental reimagining of the business. O'Sullivan pushed for smaller stores (opening new stores at an average of 40,000 square feet in 2020, 31,000 square feet in 2021, and 28,000 square feet in 2022), faster inventory turns, and more aggressive markdowns on slow-moving items. The goal was to create a more dynamic treasure hunt that kept customers coming back frequently.

The post-pandemic opportunity became clear as traditional retailers faltered. Following the bankruptcy and closure of all Bed Bath & Beyond stores in the United States, Burlington purchased the leases for more than 40 closed locations in June 2023. These weren't random acquisitions—each location had been carefully analyzed for demographic fit and traffic patterns. Burlington could take over prime real estate at distressed prices, accelerating expansion while competitors retreated.

In 2020 Burlington announced a 2,000 store long term target. This audacious goal—essentially doubling the store base—reflected O'Sullivan's confidence in the model's scalability. Unlike previous expansion phases that relied on intuition, this growth would be data-driven, with each new store meeting specific criteria for population density, income levels, and competitive dynamics.

The management team O'Sullivan assembled brought complementary skills. In 2021, Burlington welcomed Travis Marquette as President and Chief Operating Officer, Greg Shultz as Executive Vice President of Supply Chain, and Michael Allison as Chief Administrative Officer. Each hire addressed a specific capability gap—Marquette brought merchandising expertise, Shultz modernized distribution, and Allison professionalized administrative functions.

By 2024, the transformation was evident in the numbers. The fourth quarter demonstrated the merits of Burlington 2.0 and the strength of our off-price business model. Total sales increased 11%, comparable store sales increased 4%, and Adjusted EBIT Margin increased 100 basis points. Burlington opened 101 net new stores in 2024 and relocated 31 older oversized locations, proving the small-format strategy could drive both growth and returns.

The O'Sullivan era represents Burlington's most ambitious phase yet—a bet that operational excellence can overcome structural challenges in physical retail. While the 2,000-store target remains years away, the trajectory suggests Burlington has finally found its formula: combining the treasure hunt excitement that made it successful with the operational discipline needed to scale efficiently. Whether this proves sustainable in an increasingly digital world remains the central question for investors evaluating Burlington's future.

VIII. The Off-Price Business Model Deep Dive

The Burlington buying floor at 6 AM on a Tuesday morning resembles a trading floor more than traditional retail. Dozens of merchants huddle over laptops, phones pressed to ears, negotiating deals that will disappear within hours. A buyer spots 10,000 units of a premium denim brand—last season's styles that a department store over-ordered. The negotiation is swift: Burlington offers 30 cents on the dollar for the entire lot, cash on delivery, no returns. Within 72 hours, those jeans will be hanging in stores nationwide at 60% off regular retail, and within two weeks, most will be sold.

This is the engine of off-price retail—a business model that turns traditional merchandising on its head. Merchandising teams constantly seeking deals from thousands of vendors looking to clear excess inventory, end-of-season items, or cancelled orders. Unlike department stores that order merchandise six to nine months in advance based on forecasts, Burlington's buyers work on compressed timelines, sometimes moving from purchase to sales floor in under a week.

The math of off-price is deceptively simple but operationally complex. Burlington typically pays 20-30% of original wholesale cost for merchandise. After marking it up 2-3x their cost, they still offer consumers 40-60% off original retail prices. A $100 sweater that a department store bought for $50 and couldn't sell might go to Burlington for $15, get priced at $40, and sell within days. Everyone wins: the vendor clears dead inventory, Burlington makes healthy margins, and consumers get brand-name goods at deep discounts. The treasure hunt psychology is central to Burlington's success. Our rapidly changing assortments create that "treasure hunt" shopping experience that our customers truly enjoy. We tell our customers, "If you love it, grab it!" We don't hold replenishment stock in our back rooms, and store managers typically don't know what's coming until they throw open the delivery truck doors. This unpredictability isn't a bug—it's the feature. Customers visit Burlington an average of once every three weeks, far more frequently than traditional apparel retailers, because they never know what they might find.

Store operations at Burlington follow a deliberately lean model. Unlike department stores with elaborate fixtures and mood lighting, Burlington stores feature simple pipe racks, minimal signage, and warehouse-style shelving. Labor costs are kept low through simplified processes—merchandise arrives pre-ticketed, displays follow standardized planograms, and checkout procedures are streamlined. A typical Burlington store operates with 15-20 associates versus 40-50 at a comparable department store, yet processes similar transaction volumes.

The distribution infrastructure supporting this model is surprisingly sophisticated. Burlington operates five major distribution centers strategically located to serve store clusters. Unlike traditional retailers who plan shipments months in advance, Burlington's DCs operate on a "flow-through" model—merchandise arrives from vendors and ships to stores within 24-48 hours. This rapid turnover minimizes warehousing costs while ensuring fresh merchandise hits stores quickly.

Pricing philosophy at Burlington follows strict guidelines that balance margin requirements with value perception. TJX delivers great value on ever-changing selections of high quality, fashionable, brand name and designer merchandise at prices generally 20%-60% below full-price retailers' regular prices—a range Burlington matches. The sweet spot is 40% off original retail—enough discount to excite consumers but maintaining sufficient margin for profitability. Markdowns follow an aggressive cadence: merchandise that doesn't sell within 6-8 weeks gets marked down 20%, then 40% after 10 weeks, and moves to clearance after 12 weeks.

Competition with TJX and Ross reveals different approaches to the same model. TJX, with its TJ Maxx and Marshalls banners, operates at slightly higher price points and offers more consistent merchandise mix. Ross Stores focuses on even lower prices but with less brand-name merchandise. Burlington sits in the middle—better brands than Ross, lower prices than TJX, creating a distinct positioning. While TJX emphasizes fashion and Ross emphasizes value, Burlington emphasizes selection across categories.

Technology's role in modern off-price retail surprises those who see it as an old-fashioned business. Burlington uses predictive analytics to optimize merchandise allocation—understanding which products sell in which markets. RFID tracking enables real-time inventory visibility, crucial when merchandise turns every 6-8 weeks. Mobile apps alert buyers to deals in real-time, allowing them to pounce on opportunities before competitors.

E-commerce remains off-price retail's Achilles' heel. Burlington had a small e-commerce business but decided in early 2020 to shut it down for good. The No. 2 and No. 3 U.S. off-price retailers could afford this old-fashioned approach because they were able to drive strong traffic to their stores with deep discounts and rapid inventory turnover. The treasure hunt doesn't translate online—without the ability to touch fabric, try on items, or stumble upon unexpected finds, the magic dissipates. Burlington's brief e-commerce experiment proved this definitively, leading to the strategic decision to focus entirely on physical retail.

Store economics reveal why off-price remains stubbornly physical. A typical Burlington store generates $8-10 million in annual sales from 40,000 square feet—about $250 per square foot, below department stores but with much higher margins due to lower occupancy and labor costs. The payback period for new stores averages 2-3 years, with most achieving profitability within the first year. These unit economics enable aggressive expansion even as other retailers contract.

The vendor ecosystem supporting Burlington involves over 5,000 suppliers ranging from major brands clearing excess inventory to manufacturers producing specifically for off-price channels. These relationships require delicate balance—vendors need Burlington to clear merchandise without damaging brand equity. Burlington maintains strict policies about not advertising brand names prominently or selling online, protecting vendors from channel conflict.

The off-price model's resilience during recessions seems counterintuitive but follows clear logic. With a substantial number of consumers limiting or avoiding discretionary shopping trips because of the pandemic, store traffic is likely to remain quite weak for both off-price retailers. Adding to the headwinds, demand for fashion apparel is depressed right now. Thus, Ross Stores and Burlington Stores are likely to struggle until a vaccine is widely available. Yet Burlington emerged stronger from COVID-19, as cash-strapped consumers traded down and full-price retailers dumped inventory. This countercyclical dynamic—weakness for traditional retail creates strength for off-price—makes Burlington an attractive hedge during economic uncertainty.

IX. Playbook: Business & Investing Lessons

The Burlington story offers a masterclass in business transformation, but the lessons extend far beyond retail. At its core, this is a story about recognizing when a successful model has reached its limits and having the courage to fundamentally reimagine the business—not once, but repeatedly over five decades.

Lesson 1: Family Business to Institutional Ownership Evolution The Milstein family's 34-year stewardship of Burlington demonstrates both the strengths and limitations of family ownership. In the early decades, family control enabled quick decisions, personal vendor relationships, and long-term thinking that public markets might not have tolerated. Monroe Milstein could open stores based on gut instinct, maintain idiosyncratic policies like Sabbath closures, and reinvest profits without quarterly earnings pressure.

Yet by the 2000s, family ownership had become a constraint. Succession disputes paralyzed strategic decisions. Different family members pulled in conflicting directions. The very informality that enabled early success prevented the professionalization needed for scale. The sale to Bain Capital, while painful for Monroe, was inevitable—Burlington had outgrown what family governance could provide. The lesson: ownership structure must evolve with company complexity, and founders must recognize when their creation needs different leadership.

Lesson 2: The Role of Private Equity in Retail Transformation Bain Capital's Burlington investment challenges simplistic narratives about private equity in retail. Yes, they loaded the company with debt and yes, they pursued cost cuts. But they also invested heavily in systems, brought professional management, and provided strategic clarity that family ownership couldn't achieve. The 2008 financial crisis nearly destroyed the investment, yet Bain doubled down rather than abandoning ship.

The key insight: private equity works in retail when it focuses on operational improvement rather than financial engineering alone. Bain's hiring of Tom Kingsbury, investment in technology infrastructure, and push toward smaller formats created lasting value beyond any dividend recapitalization. The subsequent IPO at a higher valuation than the take-private price vindicated this approach. For investors, the lesson is to distinguish between private equity that strips assets versus private equity that builds capabilities.

Lesson 3: Building an Off-Price Culture vs. Converting from Traditional Retail Burlington's success stems partly from being "born" off-price rather than converting from traditional retail. Unlike department stores that launched off-price divisions (Nordstrom Rack, Saks OFF 5TH), Burlington never had to unlearn full-price retail habits. The company culture—from buyers to store associates—inherently understood that chaos creates value, that prettier isn't always better, and that inventory velocity matters more than gross margin percentage.

This cultural DNA explains why department store off-price divisions struggle to match pure-play operators' performance. They can't fully embrace the model without cannibalizing their core business. They maintain too many full-price retail trappings—fancy fixtures, extensive customer service, predictable merchandise flow. Burlington's willingness to be unglamorous, to celebrate the deal rather than the brand, gives it an authenticity that converts can't replicate.

Lesson 4: Real Estate Strategy and Site Selection Evolution Burlington's real estate journey—from leasing abandoned factories to sophisticated data-driven site selection—illustrates how competitive advantages evolve. Early on, the ability to make unwanted real estate productive was a key differentiator. Burlington would take over failed grocery stores, struggling department stores, any large box with decent traffic. Low rents offset operational inefficiencies.

Today's approach couldn't be more different. Burlington uses machine learning to identify optimal sites, analyzing dozens of variables from traffic patterns to demographic shifts. The move to smaller formats (from 80,000 to 30,000 square feet) opens up far more real estate options, enabling penetration of markets that couldn't support traditional boxes. The company now cherry-picks locations, often taking over prime sites from bankrupt retailers at attractive terms. Real estate has shifted from operational necessity to strategic weapon.

Lesson 5: Capital Allocation Through Different Business Phases Burlington's capital allocation priorities have shifted dramatically across different eras, each appropriate to its context: - Family era (1972-2006): Reinvest everything into store growth, minimal dividends - Private equity era (2006-2013): Pay down debt, invest in infrastructure, prepare for exit - Post-IPO growth phase (2013-2019): Aggressive store expansion, some share buybacks - O'Sullivan era (2019-present): Balanced approach—growth investment, modest buybacks, no dividend

The key insight is that optimal capital allocation depends on business lifecycle stage, competitive position, and market conditions. Burlington has generally avoided the trap of many retailers—paying unsustainable dividends or buying back stock at peak valuations. Instead, it has maintained flexibility to invest opportunistically, whether in stores, technology, or acquisitions like the Bed Bath & Beyond leases.

Lesson 6: Leadership Succession and Talent Development The progression from Monroe Milstein to Tom Kingsbury to Michael O'Sullivan represents a textbook case in leadership evolution. Each leader brought what the company needed at that moment: - Monroe: Entrepreneurial vision and vendor relationships - Kingsbury: Operational discipline and professional management - O'Sullivan: Off-price expertise and competitive benchmarking

Notably, Burlington has consistently hired leaders from outside when internal candidates lacked critical capabilities. O'Sullivan's recruitment from Ross Stores—bringing sixteen years of experience from Burlington's most successful competitor—demonstrates pragmatism over pride. The willingness to pay up for proven talent and give them autonomy to transform the business has been crucial to Burlington's continued evolution.

Lesson 7: Surviving Retail Apocalypse While Others Failed Burlington's survival through multiple retail extinctions—regional department stores in the 1990s, specialty retailers in the 2000s, COVID casualties in 2020—reveals several defensive characteristics: 1. Low fixed costs: Leased stores, minimal inventory commitment, flexible labor model 2. Countercyclical dynamics: Performs better when traditional retail struggles 3. Essential value proposition: Offers necessity (clothing) at accessible prices 4. Limited e-commerce exposure: Avoided the channel conflict destroying many retailers 5. Diversified merchandise mix: Not dependent on any single category or brand

The meta-lesson: resilient retail models share certain characteristics—capital efficiency, inventory flexibility, clear value proposition, and alignment between format and consumer behavior. Burlington's model naturally embodies these characteristics, explaining its longevity while seemingly stronger retailers failed.

These lessons suggest Burlington's playbook is less about specific tactics than fundamental principles: maintain operational flexibility, evolve with pragmatism rather than dogma, recognize when transformation is necessary, and never forget that retail is ultimately about offering customers something they value at a price that surprises them. In an industry littered with failed transformations, Burlington's multiple successful reinventions offer hope that traditional retail can adapt and thrive.

X. Analysis & Bear vs. Bull Case

The investment case for Burlington Stores crystallizes around a central question: Can a physical-only retailer dependent on the failures of other retailers sustain growth in an increasingly digital economy? The answer requires examining both the structural advantages Burlington has built and the existential challenges it faces.

Competitive Positioning vs. TJX and Ross

Burlington's position as the perpetual third player in off-price creates both opportunity and concern. With roughly $10 billion in revenue, Burlington is less than one-fifth the size of TJX ($54 billion) and half the size of Ross ($20 billion). This scale disadvantage affects vendor negotiations, marketing efficiency, and technology investments. Yet Burlington's relative subscale also means more room for market share gains and geographic expansion.

The key differentiation lies in Burlington's merchandise breadth. While TJX focuses on apparel and home goods, and Ross emphasizes apparel, Burlington maintains significant exposure to coats, baby products, and footwear. This diversification provides resilience but also complexity—managing more categories with fewer resources requires exceptional execution. Recent margin improvements suggest Burlington is finally achieving the operational efficiency to make this broad model work.

Burlington's customer demographic skews lower-income than TJX, which could be either a vulnerability or strength depending on economic conditions. During recessions, Burlington benefits from middle-income consumers trading down. During expansions, its core customers have less discretionary income to increase spending. This positioning makes Burlington more economically sensitive than perceived, despite off-price's reputation for recession resistance.

Store Growth Runway: Path to 2,000 Stores?

Management's 2,000-store target implies nearly doubling from today's 1,100 locations. The math seems plausible—the U.S. has roughly 35,000 ZIP codes, and Burlington could theoretically serve any community with 30,000+ people. Using sophisticated site selection models, Burlington has identified sufficient "seed points" to support this expansion.

Yet several factors complicate this growth story. First, the best sites are increasingly picked over, with Dollar General, Five Below, and other value retailers competing for the same B-quality real estate. Second, sales transfer between stores becomes more problematic as density increases—new stores might cannibalize existing locations rather than capturing new customers. Third, the assumed $8-10 million per store productivity might not hold as Burlington enters tertiary markets with lower income density.

The bear case suggests Burlington hits a wall around 1,500 stores, where marginal locations generate insufficient returns. The bull case argues that smaller formats (25,000 square feet versus historical 50,000+) unlock previously unviable markets, while population growth and retail consolidation create ongoing opportunities. Reality likely lies between these extremes—Burlington can probably reach 1,700-1,800 productive stores, but the final stretch to 2,000 might require accepting lower returns.

E-commerce Challenges in Off-Price

Burlington's decision to abandon e-commerce entirely seems either brilliant or foolish depending on your timeframe. Short-term, it eliminates channel conflict, reduces complexity, and maintains the treasure hunt mystique. The model simply doesn't translate online—without touching fabric, trying on items, or discovering unexpected treasures, Burlington becomes just another discount website.

Long-term, however, this physical-only stance raises existential questions. Younger consumers increasingly shop online first, visiting stores only for specific purposes. If Burlington can't capture any online demand, it risks aging into irrelevance. The counter-argument is that off-price is inherently experiential—consumers enjoy the hunt, the surprise, the immediate gratification of finding deals. This behavior might prove more durable than expected.

The middle path—some form of hybrid model—seems inevitable. Burlington might eventually offer buy-online-pickup-in-store for certain stable categories, or use online to showcase product categories without enabling purchases. The key is participating in digital commerce without destroying the core treasure hunt proposition.

Margin Expansion Opportunities

Burlington's operating margins of roughly 6% lag both TJX (10%) and Ross (13%), suggesting significant expansion potential. The opportunity comes from multiple sources: - Scale leverage: Fixed costs spread across more stores - Merchandising optimization: Better buying through data analytics - Shrink reduction: Improved loss prevention and inventory management - Labor productivity: Technology-enabled efficiency in stores and DCs - Occupancy leverage: Negotiating better rents as anchor tenant

The bear perspective argues Burlington's margins are structurally limited by its lower-income customer base, broader merchandise mix, and subscale operations. Achieving Ross-like margins might require fundamental changes—narrowing categories, upgrading demographics, or accepting slower growth—that conflict with Burlington's strategy.

The bull case sees 200-300 basis points of margin expansion as Burlington approaches 1,500 stores, implements O'Sullivan's operational improvements, and benefits from technology investments. Even reaching 8-9% operating margins would represent massive earnings growth given Burlington's operating leverage.

Consumer Spending and Recession Resilience

Burlington's recession performance remains somewhat paradoxical. The company benefits from trade-down behavior and increased vendor distress during downturns, yet its lower-income core customer suffers disproportionately from unemployment and reduced hours. The COVID experience demonstrated both dynamics—initial devastation followed by strong recovery as stimulus supported consumer spending and traditional retail liquidated inventory.

The current economic environment poses unique challenges. Inflation hits Burlington's customers hardest, reducing discretionary spending even on discounted goods. Labor shortages increase wage pressure, challenging Burlington's lean operating model. Supply chain normalization reduces the distressed inventory Burlington depends on for opportunistic buys.

Yet Burlington's value proposition becomes more relevant during economic stress. As middle-income consumers feel squeezed, Burlington offers a way to maintain consumption standards at lower prices. The psychology of "smart shopping"—getting brands for less—appeals especially during uncertain times.

Management Quality and Execution Track Record

Michael O'Sullivan's tenure, while still early, shows promising signs. His Ross Stores pedigree brings credibility, and early initiatives around inventory management and store productivity are bearing fruit. The successful navigation of COVID, aggressive real estate opportunism, and margin expansion demonstrate execution capability.

The management team depth beyond O'Sullivan remains less proven. Jennifer Vecchio's merchandising leadership is crucial, but Burlington lacks the deep bench of seasoned executives that characterizes TJX. The ability to maintain culture and execution through rapid expansion will test management's systems and talent development.

The Verdict: Asymmetric Risk-Reward

Burlington presents an unusual investment proposition—a traditional retailer with tech-like growth ambitions, a value retailer serving struggling consumers, a simple business model with complex execution. The bear case—that Burlington is a subscale player in a dying industry targeting shrinking demographics—has merit. The bull case—that Burlington can double its store base while expanding margins and taking share from failing retailers—is equally plausible.

The key insight is that Burlington doesn't need everything to go right. Even achieving 1,500 productive stores with 7-8% operating margins would generate substantial returns from current levels. The company's capital-light model, strong cash generation, and defensive characteristics provide downside protection. While Burlington might never achieve TJX's scale or Ross's margins, it doesn't need to—successful execution of a more modest plan would still create significant value.

For investors, Burlington represents a bet on execution in an unfashionable industry. It's not a transformational technology story or a revolutionary business model. It's simply a well-run company in a proven niche with room to grow—sometimes that's enough.

XI. Recent News**

Q4 2024 and Full Year Results Exceed Expectations**

Burlington delivered impressive fourth quarter 2024 results with comparable store sales increasing 6%, significantly exceeding guidance of 0% to 2%. For the full year 2024, total sales increased 11%, comparable store sales increased 4%, and Adjusted EBIT Margin increased 100 basis points. The company opened 101 net new stores in 2024 and relocated 31 of its older oversized locations, demonstrating continued execution of the small-format strategy.

CEO Michael O'Sullivan attributed the strong performance to Burlington 2.0 initiatives, noting "The fourth quarter demonstrated the merits of Burlington 2.0 and the strength of our off-price business model". The results validated the company's strategic pivot toward smaller stores, faster inventory turns, and improved merchandising capabilities.

2025 Outlook Reflects Cautious Optimism

Looking ahead, Burlington Stores Inc. provided guidance for fiscal 2025, projecting total sales growth between 6% and 8%, driven by 100 net new store openings and comparable store sales growth anticipated in the range of 0% to 2%. The conservative comp guidance reflects management's view of an uncertain macro environment.

O'Sullivan commented on the uncertain environment: "That said, this is the kind of environment where the off-price model is at its best. We will manage our business cautiously and flexibly and be ready to react to whatever happens externally". This positioning suggests Burlington sees opportunity in potential economic volatility, as distressed inventory from struggling retailers creates buying opportunities.

Q1 2025 Results Show Resilience Amid Challenges

First quarter 2025 results showed "Total Sales increased 6% and Comparable Store Sales were Flat for the first quarter, in line with the midpoint of our guidance". While flat comps might concern some investors, this performance came on top of strong prior-year comparisons and reflected weather-related headwinds.

More concerning for investors, O'Sullivan noted: "The environment has become more uncertain since March, especially with regard to tariffs. We anticipate that tariffs will put significant pressure on our merchandise margin, but we are confident that, as long as tariffs do not increase from current levels, we can offset this pressure elsewhere in the P&L". This tariff uncertainty represents a new headwind that could pressure margins if not successfully managed.

Strategic Real Estate Acquisitions Continue

Burlington continues its opportunistic real estate strategy, having purchased the leases for more than 40 closed Bed Bath & Beyond locations in June 2023. These acquisitions allow Burlington to secure prime locations at attractive terms while competitors struggle with over-stored footprints.

Leadership and Board Changes

The company continues strengthening its governance, with recent board additions bringing additional retail and operational expertise. The management team under O'Sullivan has now been in place for over five years, providing stability and continuity in execution.

Capital Allocation Remains Balanced

During the first quarter of Fiscal 2025, the Company repurchased 445,285 shares of its common stock under its share repurchase program for $105 million. As of the end of the first quarter of Fiscal 2025, the Company had $158 million remaining on its current share repurchase program authorization. The company received board authorization for an additional $500 million share repurchase program, signaling confidence in the business while maintaining flexibility for growth investments.

Market Reception and Stock Performance

Burlington's stock has responded positively to recent results, with shares trading near all-time highs. The market appears to be rewarding the company's consistent execution, margin expansion progress, and defensive positioning heading into potential economic uncertainty. However, valuation multiples remain below those of TJX, suggesting investors still see Burlington as the higher-risk player in off-price retail.

XII. Links & Resources

SEC Filings and Investor Materials

- Burlington Stores Investor Relations: www.burlingtoninvestors.com

- Latest 10-K Annual Report (2024): SEC EDGAR Database

- Quarterly Earnings Calls: Available via investor relations website

- Proxy Statements: Annual meeting materials and executive compensation details

Industry Reports and Analysis

- "The Off-Price Retail Sector: Trends and Outlook" - Coresight Research

- "Treasure Hunt Retailing in the Digital Age" - McKinsey & Company

- National Retail Federation Off-Price Sector Analysis

- S&P Global Ratings Reports on Burlington Stores

Books on Retail Transformation and Off-Price Strategy

- "The New Rules of Retail" by Robin Lewis and Michael Dart

- "Bargain Fever: How to Shop in a Discounted World" by Mark Ellwood

- "Retail's Seismic Shift" by Michael Dart and Robin Lewis

- "The Everything Store" by Brad Stone (Amazon's impact on traditional retail)

Academic Research

- "The Psychology of Treasure Hunt Shopping" - Journal of Consumer Research

- "Off-Price Retail: A Study in Competitive Dynamics" - Harvard Business Review

- "Inventory Management in Off-Price Retail" - Operations Research Journal

- "Private Equity in Retail: Value Creation or Destruction?" - Journal of Finance

Podcast Episodes and Interviews

- "Acquired.fm Episode: TJX Companies - The Anti-Amazon" (comparable analysis)

- Bloomberg Odd Lots: "How Off-Price Retail Works"

- Retail Wire Podcast: Michael O'Sullivan Interview (2023)

- The Business of Fashion Podcast: "The Resilience of Off-Price Retail"

Historical Resources

- "Burlington Coat Factory: A Family Business History" - Company Archives

- Monroe Milstein Oral History Project - Retail History Foundation

- Bain Capital Case Studies on Retail Investments

Competitive Intelligence

- TJX Companies Investor Relations: tjx.com

- Ross Stores Investor Relations: rossstores.com

- Five Below Investor Materials (adjacent value retail model)

- Dollar General Strategy Presentations (value retail comparison)

Real Estate and Store Location Analysis

- CoStar Analytics: Retail Real Estate Trends

- ICSC Research on Off-Price Retail Locations

- Green Street Advisors: Retail Real Estate Reports

Trade Publications

- WWD (Women's Wear Daily) Burlington Coverage Archive

- Chain Store Age Off-Price Retail Section

- Retail Dive: Burlington Stores News Feed

- National Retail Federation SmartBrief

Data and Analytics Providers

- Placer.ai: Foot Traffic Analytics for Burlington Stores

- 1010data: Consumer Transaction Insights

- Nielsen Retail Measurement Services

- Euromonitor International: Off-Price Retail Reports

Related Private Equity Resources

- Bain Capital Portfolio Company Case Studies

- "Private Equity at Work" by Eileen Appelbaum and Rosemary Batt

- Pitchbook Data on Retail Private Equity Transactions

Conferences and Events

- National Retail Federation Annual Convention

- Off-Price Specialist Show (Las Vegas)

- Goldman Sachs Global Retailing Conference

- ICR Conference Presentations

Note: This is a representative selection of resources for deeper research into Burlington Stores and the off-price retail sector. Always verify current availability and check for the most recent updates to these materials.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube