Bentley Systems: The Infrastructure Software Empire

I. Introduction & Opening Story

Picture this: September 23, 2020. The world is six months into a pandemic that has shuttered offices, halted construction projects, and frozen capital markets. Yet on this autumn morning, five brothers from Pennsylvania are watching their life's work debut on the Nasdaq at $22 per share. By day's end, their infrastructure software company—one that most investors have never heard of—will close at $33.49, a 52% first-day pop that values Bentley Systems at nearly $10 billion.

The ticker symbol they chose? BSY, pronounced "busy"—a winking acknowledgment of their relentless work ethic and perhaps a subtle dig at the investment bankers who suggested something more conventional. This is Bentley Systems in a nutshell: technically brilliant, fiercely independent, and just quirky enough to keep things interesting.

Founded in 1984 and headquartered in Exton, Pennsylvania, Bentley Systems has quietly become the backbone of global infrastructure design and operations. Their software touches nearly every major infrastructure project on the planet—from the Channel Tunnel to China's high-speed rail network, from Singapore's digital twin to America's power grid modernization. If you've driven on a highway, drunk tap water, or flipped a light switch today, chances are Bentley's software played a role in making it possible.

The company now commands a $17.93 billion market capitalization, generates over $1.35 billion in annual revenue, and serves more than 42,000 accounts across 189 countries. Yet for decades, it operated in the shadows, content to let competitors like Autodesk grab headlines while the Bentley brothers methodically built their empire one specialized acquisition at a time.

This is the story of how five brothers transformed a side project at DuPont into critical infrastructure for... infrastructure itself. It's a tale of patient capital triumphing over venture-backed competitors, of family control as competitive advantage, and of betting correctly on one of the most important megatrends of our time: the digital transformation of the physical world.

Our journey spans four decades, from CAD terminals in the 1980s to AI-powered digital twins today. We'll explore how Bentley pioneered the engineering software revolution, became a serial acquisition machine, forged a game-changing partnership with Siemens, and ultimately went public at the perfect moment—when COVID-19 made their cloud collaboration tools indispensable.

Along the way, we'll unpack the strategic playbook that enabled a family-run business to compete with—and often outmaneuver—public tech giants. We'll examine their unique business model, dissect their competitive moat, and debate whether their dual-class structure is a feature or a bug for public market investors.

Most importantly, we'll answer the question that matters most for investors: In a world spending trillions on infrastructure modernization and digital transformation, is Bentley Systems the picks-and-shovels play of the century, or a legacy software company facing disruption from cloud-native competitors?

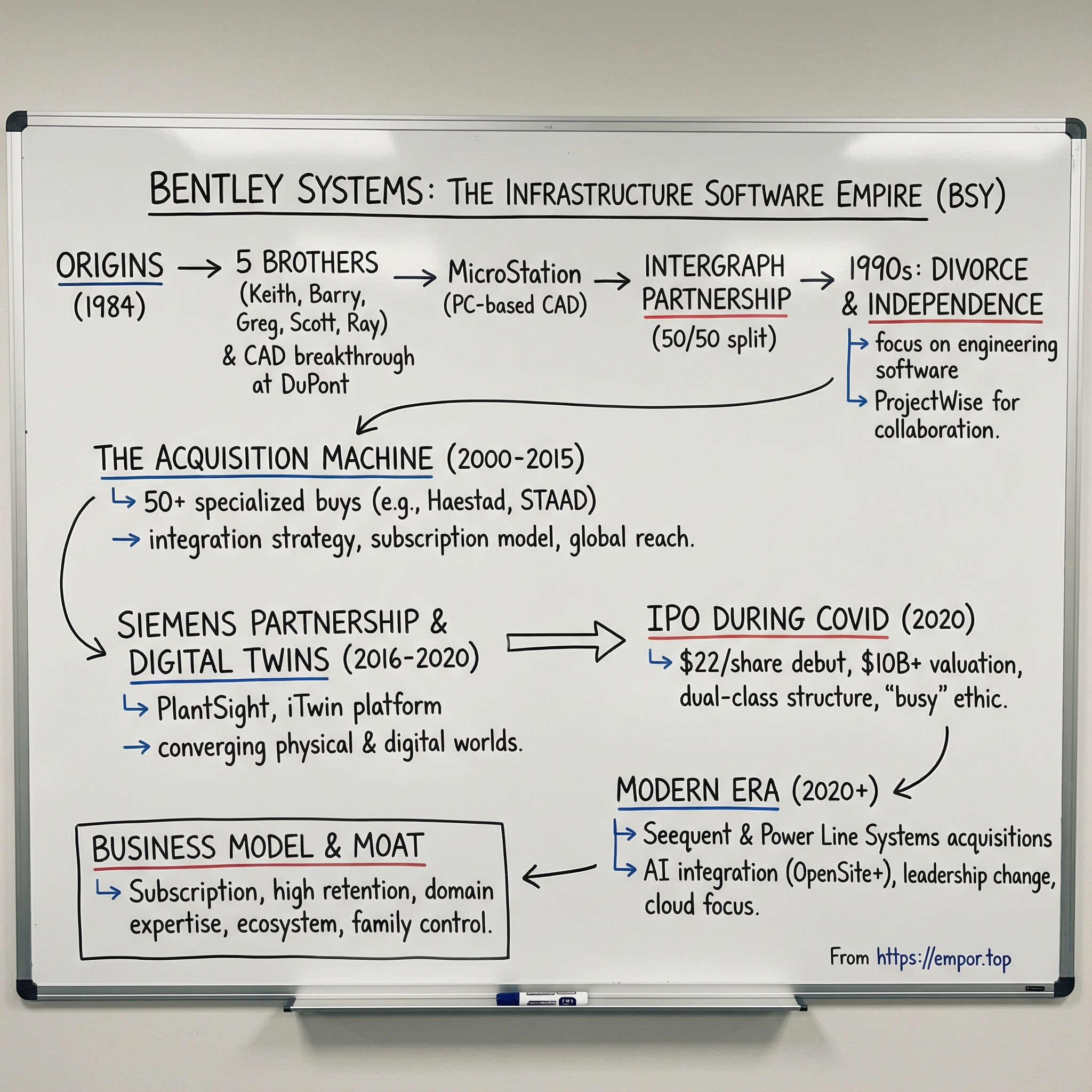

II. The Five Brothers & Origins (1984–1990)

The Bentley story begins not in Silicon Valley or Wall Street, but in the industrial heartland of Delaware, where chemical plants dot the landscape and DuPont reigned as the local tech giant before tech giants existed. It was here in the early 1980s that Keith Bentley, a programmer at DuPont, noticed something that would change his life: engineers were spending fortunes on specialized CAD workstations—sometimes $100,000 per seat—just to view and edit technical drawings.

Keith saw an opportunity that others missed. Personal computers were entering the mainstream, prices falling monthly thanks to Moore's Law. What if you could democratize CAD by making it run on affordable hardware? While his DuPont colleagues dismissed PCs as toys, Keith spent nights and weekends writing software that could display complex engineering drawings on simple terminals. The kicker? He negotiated to retain the intellectual property rights—a detail that would prove worth billions.

The technical breakthrough was elegant: instead of requiring expensive graphics workstations, Keith's software used clever algorithms to render CAD drawings on standard terminals that cost a fraction of the price. Engineers could suddenly access critical design information from anywhere in a facility, not just from dedicated workstations. It was cloud computing before the cloud existed.

But Keith wasn't alone in his entrepreneurial ambitions. His brother Barry was already running a software startup in Southern California, developing programs for chemistry laboratory data analysis. When Keith showed up with his CAD software prototype, the brothers faced a classic pivot moment. Barry's chemistry software was technically sound but served a niche market. Keith's CAD innovation, on the other hand, addressed a massive pain point in a rapidly growing industry.

The decision to pivot wasn't immediate. The brothers spent months analyzing the market, talking to potential customers, running the numbers. Their research methodology was refreshingly straightforward: they showed the prototype to engineers and simply asked, "What would you pay for this?" They averaged the responses and arrived at $7,943—an oddly specific price that would become company lore, demonstrating their data-driven approach even in those bootstrap days.

On September 5, 1984, Bentley Systems was officially incorporated. The timing was fortuitous. The CAD market was exploding—growing from $1.5 billion in 1983 to a projected $7.5 billion by 1988. Major players like Intergraph, Computervision, and AutoCAD were battling for market share, but they were focused on high-end workstations or basic 2D drafting. Bentley targeted the middle: sophisticated engineering firms that needed powerful capabilities but couldn't afford six-figure workstations for every engineer.

The early product development was a family affair in the truest sense. Greg Bentley, the eldest brother with a background in finance and law, joined to handle business operations. Scott came aboard to lead sales, bringing a natural charisma that could sell software to skeptical engineering departments. Ray, the youngest, would later join to run IT and operations. Each brother brought complementary skills—Keith the technical visionary, Barry the systematic thinker, Greg the strategist, Scott the dealmaker, Ray the operator.

Their first major breakthrough came in 1986 with the DOS version of MicroStation. While competitors required expensive UNIX workstations, MicroStation ran on standard PCs. The performance was remarkable: complex drawings that took minutes to render on competing systems appeared in seconds on MicroStation. Engineers were stunned. Here was professional-grade CAD software running on hardware that cost 90% less than the competition. The partnership that would change everything came through an unexpected channel. Toward the end of 1986, Intergraph invited Bentley Systems to Huntsville to demonstrate MicroStation. The CAD giant had heard enough about the software from its own customers to perhaps wonder whether it had backed the wrong horse in C-CADD. Intergraph, the Alabama-based CAD powerhouse, was facing a classic innovator's dilemma. Their high-margin workstation business was under threat from PC-based solutions, yet they couldn't ignore the market shift.

In January 1987, Intergraph purchased a 50 percent interest in Bentley Systems for $3 million. The deal gave Intergraph exclusive distribution rights to MicroStation, which it pledged to market on both PCs and its own Unix workstation platform. "The division of labor was that we would do all the development," Barry explained, "and they would do all the marketing, sales, and customer support."

The deal structure revealed the brothers' strategic genius. They retained 50% ownership and complete control over product development. Intergraph got exclusive distribution rights but also bore all the costs of sales, marketing, and support. For a bootstrap startup with five employees, it was the perfect arrangement—they could focus entirely on building great software while leveraging Intergraph's global sales force and customer relationships.

But the partnership also contained seeds of future conflict. One problem with this arrangement was that each party owned exactly 50 percent of the business and had half the board seats. Many joint ventures split something like 49/51 so that there is a clear controlling interest. This would prove to be a problem for Bentley a few years later. The 50-50 structure meant every major decision required consensus—a recipe for deadlock when strategic visions diverged.

The late 1980s saw explosive growth. MicroStation's user base expanded from hundreds to thousands, then tens of thousands. The software evolved rapidly, adding features that previously required million-dollar systems: 3D modeling, photorealistic rendering, animation capabilities. Each release pushed the boundaries of what PC hardware could do, turning $10,000 computers into engineering powerhouses.

The brothers also began assembling a world-class development team. They recruited from competitors, universities, and their own customer base. The culture they created was unique: part startup, part engineering firm, part family business. Developers had enormous autonomy but were expected to deliver. The only management philosophy was "hire smart people and get out of their way."

By 1990, the Bentley Systems story had all the elements of a classic American success story: brilliant outsiders disrupting an entrenched industry, a David-and-Goliath partnership with a giant, and a product that was genuinely transforming how infrastructure was designed. But the real growth—and the real challenges—were just beginning. The partnership with Intergraph that had catalyzed their rise would soon become a constraint on their ambitions.

III. MicroStation & The Engineering Software Revolution (1990s)

The 1990s opened with Bentley Systems at a crossroads. The Intergraph partnership had given them distribution muscle, but cracks were showing. Intergraph wanted MicroStation to drive hardware sales; the Bentleys saw it as a platform to democratize engineering software. This fundamental tension would define the decade's first half.

The market context was shifting dramatically. Intergraph became a publicly owned company in 1981. In the beginning it was a consulting firm that supported government agencies in using digital technology. Among these technologies were application-oriented user interfaces that communicated with users in the language of their applications, rather than in programming terminology. But by 1992, workstation margins were collapsing as PCs grew more powerful. Sun Microsystems and Silicon Graphics were eating into Intergraph's high-end market while Bentley's MicroStation cannibalized from below.

The divorce, when it came, was surprisingly civil. In 1994, after months of negotiations, Bentley Systems bought back Intergraph's 50% stake. The price wasn't disclosed, but industry insiders estimated it at $50-60 million—a 20x return on Intergraph's original $3 million investment. The settlement included a crucial provision: As part of the divorce settlement, an arbitrator had granted Bentley Systems the right to offer employment to a limited number of Intergraph personnel. After Bentley named 20 candidates, Intergraph could place 10 of them off-limits, three of whom Bentley would be permitted to claw back into a pool of potential new hires.

Free from Intergraph's constraints, the Bentleys unleashed an ambitious growth strategy. Revenue exploded from $95 million in 1995 to more than $182 million in 1999. By 2000, Bentley Systems was the second largest privately held software company in the United States, with revenue topping $200 million and offices spanning 38 countries supporting more than 315,000 MicroStation users.

The growth wasn't just organic. The Bentleys had discovered their superpower: acquiring and integrating niche engineering software companies. Their approach was unique in the software industry. Rather than strip assets and cut costs, they preserved the acquired company's domain expertise while integrating their technology into the MicroStation platform. Engineers who had spent decades perfecting hydraulic modeling or structural analysis software suddenly had access to Bentley's global distribution and development resources.

One acquisition stands out as transformative. In 1998, Bentley acquired Finland-based Opti Inter-Consult, whose TeamMate software would become the foundation for ProjectWise. The Bentleys recognized something others missed: engineering projects were becoming too complex for individual tools. What the industry needed was collaboration software purpose-built for infrastructure projects—something that could manage terabytes of CAD files, coordinate hundreds of engineers, and maintain version control across global teams.

ProjectWise launched officially in 1999, and the impact was immediate. Within five years, 46 of 50 U.S. State Departments of Transportation had adopted it. The software solved a problem every infrastructure project faced: how to coordinate massive teams working on interconnected systems. A highway project might involve traffic engineers, structural engineers, environmental consultants, and construction contractors—all needing access to the same models but with different permissions and workflows.

The competitive landscape of the 1990s was fascinating. Autodesk dominated architectural design with AutoCAD but struggled in specialized engineering. Dassault and PTC ruled mechanical CAD but couldn't crack infrastructure. Intergraph, post-divorce, pivoted to government and mapping software. Bentley found white space in the middle: complex infrastructure projects that required both broad capabilities and deep specialization.

The company's approach to product development was distinctly different from Silicon Valley norms. While competitors chased the latest trends—object-oriented programming, internet browsers, thin clients—Bentley focused on solving actual engineering problems. Their developers spent weeks on construction sites and in engineering offices, watching how professionals actually worked. This ethnographic approach to software development would become a defining characteristic.

Greg Bentley joined full-time as CEO in 1995, bringing a lawyer's precision to the family's engineering brilliance. His first major initiative was SELECT, a subscription program that bundled all Bentley software for a single annual fee. In an era when enterprise software was sold as perpetual licenses with 18% annual maintenance fees, SELECT was revolutionary. Customers got predictable costs and access to everything; Bentley got recurring revenue and deeper customer relationships.

The financial performance during this period was remarkable. While most software companies struggled with 60-70% gross margins, Bentley consistently achieved 80%+. Their secret? They didn't just sell software; they sold expertise. Every license came with training, support, and ongoing updates based on user feedback. Customers weren't buying a product; they were joining an ecosystem.

By decade's end, Bentley had also cracked the international market. European engineering firms, with their emphasis on precision and standards, embraced MicroStation enthusiastically. Asian markets, undergoing massive infrastructure buildouts, became growth engines. The company established development centers in Lithuania and India, tapping into deep pools of engineering talent at fraction of Silicon Valley costs.

The 1990s transformation was complete. Bentley Systems had evolved from a single-product company dependent on a distribution partner to a comprehensive platform with its own global sales force. Revenue had grown 10x. The employee count exceeded 1,000. Most importantly, they had established the playbook they would follow for the next two decades: acquire specialized companies, integrate them into a unified platform, and sell the complete solution through recurring subscriptions.

IV. The Acquisition Machine: Building Through M&A (2000–2015)

The new millennium brought a new challenge. The dot-com bubble had burst, taking with it many of Bentley's high-flying competitors. But while Silicon Valley licked its wounds, the Bentley brothers saw opportunity. Distressed engineering software companies were available at fraction of their previous valuations. With no venture capital masters demanding quick exits and no public market scrutiny, Bentley could play the long game.

Their acquisition strategy was surgical. They didn't want companies with the most users or highest revenues. They wanted companies with the best algorithms, the deepest domain expertise, and the most loyal customers. A typical target might have 50 customers but those customers couldn't imagine working without the software. Bentley would acquire the company, invest in modernizing the code, and then distribute it to their 40,000+ accounts globally.

The numbers tell the story. Between 2000 and 2015, Bentley acquired over 50 companies. Not mega-deals that made headlines, but strategic additions that filled specific gaps. On October 17, 2001, Bentley Systems bought Geopak design software for road and rail infrastructure. Bentley Systems acquired Rebis in 2003, Infrasoft Corporation in 2003, Haestad Methods, Inc. in 2004, and then agreed to acquire netGuru's Research Engineers International (REI) business which included its STAAD structural analysis and design product line on August 31, 2005.

Take Haestad Methods, acquired in 2004. This Connecticut company had spent 25 years perfecting water and wastewater modeling software. Their WaterCAD and SewerCAD products were the gold standard for hydraulic analysis. Under Bentley's ownership, these tools were integrated with MicroStation, enhanced with modern interfaces, and sold globally. Revenue from these products grew 10x within five years of acquisition.

The STAAD acquisition in 2005 was particularly strategic. After opening a development center in Lithuania in 2005, Bentley acquired STAAD and RAM International to help establish its leadership position in structural engineering software. Structural analysis software is the mathematical heart of engineering—it determines whether a bridge will stand or fall, whether a building can withstand earthquakes. STAAD's algorithms had been refined over decades. Combined with RAM International's building design tools, Bentley suddenly owned the structural engineering workflow end-to-end.

What made Bentley's M&A strategy work was their integration philosophy. Unlike typical software rollups that slash costs and milk maintenance revenues, Bentley invested heavily in acquired products. They would modernize codebases, add cloud capabilities, integrate with other Bentley products, and expand development teams. The original founders often stayed on, continuing to evolve their life's work with resources they never had as independents.

The company also made geographic acquisitions to establish local presence. The Lithuanian development center, established in 2005, became a 200-person R&D hub. Similar centers in India, China, and Romania provided 24-hour development cycles and deep local expertise. This distributed model meant Bentley could support infrastructure projects anywhere in the world with local language, local standards, and local support.

By 2010, Bentley's product portfolio resembled a Swiss Army knife for infrastructure. Need to design a highway? They had InRoads. Analyzing a steel structure? STAAD Pro. Modeling water distribution? WaterGEMS. Planning rail networks? GEOPAK. Each product was best-in-class for its specific domain, but they all worked together through common data formats and shared libraries.

The financial model during this period was increasingly attractive. The company re-invests 20% of their revenues in research and development. This massive R&D investment—double the software industry average—created a virtuous cycle. Better products attracted more users, generating more revenue to fund more R&D and acquisitions. The subscription model meant predictable cash flows to fund acquisitions without external capital.

Competition during this era came from unexpected angles. Autodesk went public and used its currency to acquire broadly. Oracle and SAP pushed into engineering software from enterprise systems. French companies like Dassault Systèmes leveraged government support to expand globally. Yet Bentley's focused strategy—infrastructure only, engineering depth, perpetual innovation—kept them ahead in their core markets.

The private ownership structure was crucial to this strategy's success. Public companies face quarterly earnings pressure, making it hard to invest in long-term integration. Venture-backed companies need exits within 5-7 years, forcing premature monetization. The Bentley family could take a 10-year view on every acquisition, investing patiently until products reached their potential.

Internal culture during this period remained remarkably consistent despite rapid growth. The company maintained its engineering-first mentality. Developers had direct contact with users. Feature requests from a highway department in Mongolia got the same attention as those from massive multinationals. This customer intimacy, scaled across thousands of accounts, created unmatched market intelligence.

By 2015, Bentley Systems had assembled something unique: a comprehensive infrastructure software platform built through strategic acquisition and patient integration. Revenue exceeded $500 million. The company employed over 3,000 people across 45 countries. Most impressively, customer retention rates exceeded 95%—once an engineering firm adopted Bentley software, they rarely left.

The acquisition machine had transformed Bentley from a CAD software vendor into the operating system for infrastructure. But the world was changing. Cloud computing, artificial intelligence, and IoT were transforming every industry. Infrastructure itself was becoming digital. The next chapter would require a different kind of partnership—one that could bridge the physical and digital worlds.

V. The Siemens Partnership & Digital Twin Revolution (2016–2020)

November 3, 2016, marked a watershed moment for Bentley Systems. In November 2016, German-based Siemens announced it would pay about $76 million for a minority stake in Bentley, but this was more than just a financial investment. It was a strategic alliance between two companies that saw the future of infrastructure converging physical and digital worlds.

The partnership made perfect sense strategically. Siemens brought industrial IoT expertise, operational technology, and global reach in manufacturing and energy. Bentley brought infrastructure design software, engineering workflows, and deep relationships with owner-operators. Together, they could offer something neither could alone: complete digital twins of industrial and infrastructure assets.

The two companies have decided to extend their existing agreement, to further develop their joint business cooperation and commercial initiatives. Therefore, the joint innovation investment program will be increased from the initial €50 million funding to €100 million. This wasn't venture capital looking for quick returns—it was patient industrial capital investing in decade-long technology development.

The crown jewel of the partnership was PlantSight, announced in October 2018. Greg Bentley, CEO for Bentley Systems, said, "From the start of Bentley Systems' strategic alliance with Siemens, we have together seen our development of PlantSight as having perhaps the most significance for our marketplace. Siemens' announced combination of its digital offerings for discrete and process plants enables our bringing together, through a cloud service, the complementary elements of Comos, OpenPlant, MindSphere, and Teamcenter.

PlantSight represented a fundamental reimagining of industrial software. PlantSight enables as-operated and up-to-date digital twins which synchronize with both physical reality and engineering data, creating a holistic digital context for consistently understood digital components across disparate data sources, for any operating plant. For the first time, operators could see their actual plant—not the design, not the plan, but the real, current, operating asset—in digital form.

The technical achievement was remarkable. PlantSight mirrors the physical plant through "continuous" surveys and reality modeling cloud services. Overlapping photographs and (as needed) supplemental laser scans, from UAVs and ground-level imagery, are processed to generate spatially-classified and engineering-ready reality meshes—the plant's digital context, within which can be geospatially located each tagged component. This wasn't just 3D modeling; it was continuous reality capture synchronized with engineering data.

The business model innovation was equally important. PlantSight operated as a cloud service, generating recurring revenue rather than one-time licenses. It created network effects—the more data fed into the digital twin, the more valuable it became. And it locked in customers for decades, as switching costs for a complete digital twin were astronomical.

During this period, Bentley also developed its broader infrastructure cloud strategy. The iTwin platform, launched in 2018, extended digital twin concepts beyond industrial plants to all infrastructure. Bridges could report their own structural health. Water networks could optimize themselves. Roads could communicate with autonomous vehicles. This wasn't science fiction—it was engineering reality being deployed at scale.

The financial impact was significant. Bentley Systems employs more than 3,500 colleagues, generates annual revenues of $700 million in 170 countries, and has invested more than $1 billion in research, development, and acquisitions since 2012. The Siemens partnership provided both capital and credibility to accelerate this investment.

In addition, as a result of the continuous investment of Siemens into secondary shares of Bentley's common stock the Siemens stake in Bentley Systems now exceeds 9%. This stake, while minority, was strategic. It gave Siemens insight into Bentley's roadmap and preferential partnership terms, while giving Bentley a deep-pocketed ally without sacrificing control.

The partnership also sparked acquisition rumors. A recent article from Bloomberg reads, "Siemens AG is weighing an acquisition of Bentley Systems Inc., according to people familiar with the matter". The industrial logic was compelling—Siemens could instantly become a leader in infrastructure software, while Bentley would gain unlimited resources for growth.

But the Bentley brothers had other plans. They had spent 35 years building their company, survived multiple technology transitions, and created a unique culture. They weren't ready to become a division of a German conglomerate. Instead, they began preparing for something that would have seemed impossible just years earlier: taking their family-controlled business public in the middle of a global pandemic.

The Siemens partnership had transformed Bentley from an engineering software company into a digital twin pioneer. It validated their vision, accelerated their technology development, and provided a financial cushion for ambitious investments. Most importantly, it positioned them perfectly for the infrastructure spending boom that was about to unfold.

VI. The IPO Story & Going Public During COVID (2020)

March 2020. The world shut down. Construction sites abandoned. Engineering offices emptied. Infrastructure projects frozen. For a company that had spent 36 years building software for physical infrastructure, the timing for an IPO couldn't have been worse. Or could it?

When the COVID-19 pandemic hit, collaboration via the cloud became the norm and pushed the infrastructure industry to go digital. Suddenly, engineering firms that had resisted cloud adoption for decades had no choice. ProjectWise, Bentley's collaboration platform, saw usage spike 300% in weeks. Digital twins went from nice-to-have to mission-critical as operators needed to manage infrastructure remotely. The pandemic didn't kill Bentley's IPO plans—it accelerated them.

The preparation had actually begun years earlier. Greg Bentley and his team had spent 2018 and 2019 quietly preparing the company for public markets: standardizing financial reporting, implementing SOX controls, building an independent board. They hired bankers from Goldman Sachs and Bank of America in late 2019, planning for a summer 2020 debut. Then COVID hit, and they had a choice: wait for normalcy or strike while their solutions were indispensable.

They chose to strike. In September 2020, Bentley Systems sets terms of its IPO valuing the company at about $4.96 billion. The company would offer 10.75 million shares priced between $17 and $19 per share. But demand was stronger than anyone anticipated. The price range was revised upward to $19-21, then priced at $22—above even the revised range.

Bentley Systems, Incorporated ("Bentley") today announced the pricing of the initial public offering of 10,750,000 shares of its Class B common stock at a price to the public of $22.00 per share. The shares of Class B common stock to be sold in the offering are being sold by existing stockholders of Bentley. This detail was crucial—the company itself wasn't raising capital. The Bentley family was providing liquidity for employees and early investors while maintaining control.

The dual-class structure was controversial but strategic. Following the completion of this offering, the shares of Class A common stock and Class B common stock held by members of the Bentley family (including their permitted transferees) will represent approximately 67% of our outstanding common stock and approximately 83% of the voting power. Class A shares carried 29 votes each; Class B shares just one. The brothers weren't giving up control—they were accessing public capital while keeping their hands firmly on the wheel.

The shares are expected to begin trading on the Nasdaq Global Select Market on September 23, 2020 under the symbol "BSY". The ticker choice was quintessentially Bentley—pronounced "busy," it captured both their work ethic and their irreverent humor. As CEO Greg Bentley explained: "We chose the ticker symbol BSY to connote 'staying busy,' doing what we're doing."

The first day of trading exceeded all expectations. Opening at $28 and closing at $33.49, the stock delivered a 52% first-day pop. The market valued Bentley at nearly $10 billion—double the initial target. For a company that had never taken venture capital, never needed external funding, and had been profitable for decades, it was vindication of their patient, methodical approach.

The investor base was telling. New investor Capital Research Global Investors intends to buy $40 million worth of shares in the offering. This wasn't speculative capital chasing the next unicorn. These were long-term fundamental investors who understood infrastructure cycles and appreciated Bentley's dominant market position.

The roadshow, conducted entirely virtually due to COVID, became a masterclass in strategic positioning. Greg Bentley didn't pitch revolutionary disruption or exponential growth. Instead, he sold inevitability: trillions in infrastructure spending, accelerating digital transformation, and Bentley's picks-and-shovels position in the middle of it all. The message resonated—infrastructure was having its moment, and Bentley was the pure play.

Financial metrics at IPO were impressive. Bentley Systems was founded in 1984 and booked $768 million in revenue for the 12 months ended June 30, 2020. As of June 30, 2020, Bentley had $125.5 million in cash and $679.4 million in total liabilities. Free cash flow during the twelve months ended June 30, 2020, was $206.1 million. These weren't venture-scale losses in pursuit of growth—this was a profitable, cash-generative business with 90%+ recurring revenue.

The competitive positioning was equally strong. The firm sells primarily through direct sales channels, generating approximately 92% of its 2019 revenues. Unlike software companies dependent on channel partners, Bentley controlled its customer relationships directly. This meant higher margins, better customer intelligence, and stronger retention.

The timing, initially seeming disastrous, proved perfect. Infrastructure stocks were surging as governments worldwide announced stimulus packages. Digital transformation budgets exploded as COVID made remote operations mandatory. And software multiples expanded as investors sought recurring revenue models. Bentley hit the trifecta.

But perhaps the most remarkable aspect of the IPO was what didn't change. The five Bentley brothers own about two-thirds of the economic interest and vote about 85% of the shares (co-founders Keith and Barry, plus Raymond and Greg, are directors; a fifth, brother, Richard, retains a 5.3% stake after selling 848,996 shares of Class B stock in the IPO). The family remained in control. The culture stayed intact. The long-term focus persisted.

The IPO wasn't an exit—it was an entry. Entry to public capital markets that would fund future acquisitions. Entry to a currency (public stock) for larger deals. Entry to a new level of visibility and credibility with enterprise customers. Most importantly, it was validation that a family-controlled business could access public markets without sacrificing its soul.

VII. The Modern Era: AI, Acquisitions & Growth (2020–Present)

The post-IPO era transformed Bentley from acquisition hunter to apex predator. Armed with public currency and proven integration playbook, they went shopping for transformational assets. Bentley stayed busy over the next four years, acquiring technologies in subsurface infrastructure like Seequent, a global leader in 3D modeling software for geosciences. The company pushed into electric transmission and distribution by acquiring Power Line Systems (PLS) and SPIDA, and announced Bentley Infrastructure Cloud, its end-to-end lifecycle combination of enterprise systems.

The Seequent acquisition in 2021 for $1.05 billion was the largest in company history. Bentley's world-leading expertise in above ground infrastructure perfectly complements Seequent's world-leading solutions for below ground infrastructure. This wasn't just adding another tool—it was completing the infrastructure stack. Engineers could now model everything from bedrock to sky, integrating geological, structural, and environmental data in a single platform.

Power Line Systems, acquired for $700 million in 2022, addressed the energy transition head-on. Power Line Systems was founded by University of Wisconsin professor Dr. Alain Peyrot in 1984, and is headquartered in Madison, WI. Its concentrated focus from the outset has been ever-improving engineering tools for overhead power line structures, earning the supportive confidence of transmission engineers as the industry standard of best practice throughout the U.S., increasingly across Europe, and opportunistically in Asia. With grid modernization requiring trillions in investment, PLS's software became mission-critical for utilities worldwide.

As an established subscription business with no full-time go-to-market staffing, Power Line Systems generates extraordinary profitability and cashflow, and accordingly, the acquisition is expected to be accretive to BSY's corresponding financial metrics. This detail revealed Bentley's acquisition genius—they weren't buying growth at any cost but acquiring profitable, established businesses with loyal customers.

Bentley also significantly expanded its iTwin Platform to better help engineering firms create and leverage digital twins. The platform evolved from concept to comprehensive ecosystem, enabling not just visualization but true operational intelligence. Infrastructure assets could self-report health, predict maintenance needs, and optimize performance autonomously.

The financial performance validated the strategy. For the first time, annual recurring revenue exceeded $1 billion in 2022. In 2024, Bentley Systems's revenue was $1.35 billion, an increase of 10.15% compared to the previous year's $1.23 billion. This wasn't hypergrowth by software standards, but for a company serving conservative infrastructure markets, double-digit growth at this scale was remarkable. The AI revolution at Bentley wasn't about chasing Silicon Valley trends—it was about solving real engineering problems. "AI is a new paradigm shift, transforming every industry, and infrastructure is no exception," said Nicholas Cumins, CEO of Bentley Systems, in his keynote address at Year in Infrastructure, which took place in October 2024 in Vancouver.

The company's AI strategy centered on the "Plus" products—enhanced versions of existing software powered by machine learning. Bentley's OpenSite+ is the first engineering application leveraging generative AI for civil site design. It helps engineers swiftly design residential, commercial, and industrial sites with AI tools, significantly boosting productivity and accuracy. The breakthrough wasn't just automation—it was intelligence. Bentley Systems announces a generative AI game-changer for civil site design, delivering optimized, accurate site designs up to 10x faster than traditional methods.

With post-COVID investments in infrastructure and net-zero pathways, the demand for engineering services has never been higher. There is more work than engineering services firms can handle and backlogs are getting longer. However, workforces are aging and firms can't hire fast enough. There are simply not enough engineers graduating from college. Engineering services firms are looking for ways to close their capacity and skills gaps and are turning to AI-driven solutions for automation and reuse that relieve engineers of the many mundane tasks that undermine their productivity.

In 2023, Bentley acquired Salt Lake City, Utah-based Blyncsy, a provider of breakthrough artificial intelligence services for departments of transportation to support operations and maintenance activities. This wasn't about building AI capabilities from scratch—it was about acquiring proven technology and integrating it across the platform.

In September 2024, Bentley announced the acquisition of Cesium GS, Inc., a provider of 3D geospatial software applications and platforms. The company recently acquired Cesium, a 3D geospatial platform company whose 3D Tiles standard has been adopted as the Open Geospatial Consortium community standard. The combination of iTwin and Cesium technologies enable an infrastructure asset owner to, for example, collect drone photos, build a reality model from them in iTwin, run the model through AI analytics to detect cracks, process the analytic data through a 3D tiling pipeline into 3D Tiles format, and disseminate the files into any of Cesium's runtimes.

The leadership transition from Greg Bentley to Nicholas Cumins in 2024 marked a generational shift. Greg remained as Executive Chairman, but Cumins—a former Microsoft executive who had led Bentley's cloud transformation—took the CEO reins. The message was clear: the future was cloud, AI, and digital twins, but the family values and long-term thinking would persist.

"By leveraging their past data to optimize future work, generative AI will revolutionize infrastructure design, improving engineers' productivity and accuracy without sacrificing on quality," said Mike Campbell, chief product officer at Bentley Systems. "OpenSite+ is just the first example of how Bentley is applying generative AI to benefit infrastructure design and project delivery."

The modern era also saw Bentley embracing ecosystem thinking. The iTwin Ventures Fund invested in startups building on their platform. Waveo's artificial intelligence (AI) algorithm improves the analysis of point clouds generated from multiple types of data sources. The iTwin platform allowed Waveo to integrate their AI algorithm into Bentley's OpenTower IQ enhancing its decision making and visualization capabilities. This wasn't defensive venture capital—it was offensive, building a moat through network effects.

By 2024, Bentley had transformed from a CAD software company into something much more ambitious: the operating system for global infrastructure. With AI augmenting engineers, digital twins monitoring assets, and cloud services connecting everything, they were positioned at the intersection of every major infrastructure trend. The question wasn't whether they would grow, but how fast—and whether public markets would properly value their unique position.

VIII. Business Model & Competitive Moat

The genius of Bentley's business model lies not in any single innovation but in how multiple reinforcing elements create an almost impregnable competitive position. The business model is cash-efficient, with approximately 70% of revenues billed in advance thanks to a subscription-driven revenue model. This isn't just good for cash flow—it fundamentally changes the company's relationship with customers from vendor to partner.

The subscription transformation began decades before SaaS became fashionable. Bentley's SELECT program, launched in the 1990s, bundled all software for a single annual fee. While competitors sold perpetual licenses with 18% maintenance fees, Bentley created true recurring relationships. Today, over 90% of revenue is recurring, providing predictability that enables long-term planning and patient capital allocation.

The unit economics are extraordinary. Gross margins consistently exceed 80%, among the highest in enterprise software. Operating margins of 24.17% and profit margins of 18.46% reflect a business that has achieved scale while maintaining pricing power. The company re-invests 20% of their revenues in research and development—double the software industry average—creating a virtuous cycle of innovation.

But the real moat isn't financial—it's structural. Bentley is the only infrastructure engineering software vendor that leads in market share in categories related to both the project and the asset lifecycle phases. Bentley Systems' accounts include 90% of the top 250 of the "ENR 2019 Top 500 Design Firms" and 64% of the "2019 Bentley Infrastructure 500 Top Owners". This isn't market share—it's market ownership in the segments that matter most.

The switching costs are astronomical, but not for the reasons you might expect. It's not just about data migration or retraining—it's about trust. When you're designing a bridge that must stand for a century, or a water system serving millions, you don't switch software lightly. Engineering firms have decades of institutional knowledge embedded in Bentley workflows. Projects worth billions depend on this software. The risk of switching far exceeds any potential savings.

Network effects compound over time. ProjectWise becomes more valuable as more stakeholders join projects. Digital twins improve as more sensor data flows in. AI models get smarter with more training data. Every user, every project, every data point makes the platform stronger for everyone else. It's a flywheel that's been spinning for 40 years.

The ecosystem play multiplies these advantages. With more than 42,000 accounts across 189 countries, we are the partner of choice for engineering firms and owner-operators worldwide. But it's not just breadth—it's depth. Bentley doesn't just sell to IT departments; they're embedded with actual engineers. Product managers spend time on construction sites. Developers understand hydraulic equations. This domain expertise can't be replicated by horizontal software companies.

The platform strategy—ProjectWise for collaboration, AssetWise for operations, iTwin for digital twins—creates multiple lock-in points. A customer might start with MicroStation for design, add ProjectWise for collaboration, integrate AssetWise for operations, and eventually run everything through iTwin. Each addition increases switching costs exponentially. It's not vendor lock-in through contracts—it's lock-in through value creation.

Geographic diversification provides resilience. Unlike companies dependent on Silicon Valley or Wall Street, Bentley serves infrastructure markets globally. When U.S. spending slows, Asian mega-projects accelerate. When China pauses, European green infrastructure investment surges. Infrastructure is the ultimate non-cyclical market—societies must maintain and upgrade regardless of economic conditions.

The competitive dynamics are fascinating. Autodesk has 10x the revenue but struggles in specialized engineering. Dassault dominates manufacturing but can't crack infrastructure. Oracle and SAP own enterprise systems but lack engineering depth. New entrants face a chicken-and-egg problem: you need the specialized tools to get customers, but you need customers to justify building specialized tools. Bentley spent 40 years solving this paradox.

The capital efficiency is remarkable. Unlike consumer software requiring massive marketing spend, or enterprise software demanding huge sales forces, Bentley grows through product excellence and word-of-mouth. The firm sells primarily through direct sales channels, generating approximately 92% of its 2019 revenues directly. Customer acquisition costs are low because customers come to them—when you need to design a highway, your options are limited.

Pricing power continues to expand. Annual price increases of 3-5% meet no resistance because the software value far exceeds its cost. A infrastructure project worth $100 million might spend $100,000 on software—0.1% of project value. If that software prevents one error, shortens the timeline by one day, or improves efficiency by 1%, it pays for itself many times over.

The family control, often seen as a governance negative, is actually a competitive advantage. Public companies optimize for quarterly earnings; Bentley optimizes for decades. Competitors must explain every acquisition to Wall Street; Bentley buys strategically without scrutiny. While others cut R&D in downturns, Bentley invests countercyclically.

This isn't a business model that can be disrupted by a startup with venture funding or replicated by a tech giant with unlimited resources. It's a 40-year accumulation of trust, expertise, relationships, and specialized technology. The moat isn't just wide—it's getting wider as infrastructure digitalization accelerates and switching costs compound. For investors seeking defensive growth in an uncertain world, it's hard to imagine a stronger competitive position.

IX. Playbook: Key Lessons & Strategy

After four decades of building a $17.93 billion infrastructure software empire, the Bentley playbook offers profound lessons for building enduring technology businesses. These aren't Silicon Valley growth hacks or blitzscaling tactics—they're time-tested strategies for creating multigenerational value.

Family Control as Competitive Advantage

The Bentley brothers proved that family ownership, often dismissed as provincial or unprofessional, can be a superpower in technology markets. Patient capital enables long-term thinking. When you're planning for grandchildren rather than quarterly earnings, you make fundamentally different decisions. You invest in R&D during recessions. You maintain products for decades even if they're not growing. You prioritize customer success over short-term revenue optimization.

The family structure also created unique cultural advantages. Decisions could be made quickly—no board politics, no activist investors, no quarterly guidance to hit. The brothers could disagree privately then present unified publicly. They could take massive bets, like spending $1 billion on acquisitions, without extensive committee approvals. In a world where public companies are increasingly short-term oriented, private family ownership became a differentiator.

The Power of Industry-Specific Vertical Software

Bentley chose depth over breadth—a contrarian strategy in an era of horizontal platforms. While competitors built general-purpose tools, Bentley built software for specific engineering workflows. A structural engineer doesn't need generic CAD—they need software that understands building codes, load calculations, and seismic requirements. A water engineer doesn't need basic modeling—they need hydraulic simulation with real-world pipe specifications.

This vertical focus created compounding advantages. Deep domain expertise led to better products. Better products attracted specialized users. Specialized users provided expert feedback. Expert feedback drove further specialization. It's a virtuous cycle that horizontal competitors can't replicate without abandoning their generalist approach.

M&A as Core Competency

Between 2000 and 2015, Bentley acquired over 50 companies. But unlike typical roll-ups that slash costs and milk maintenance revenue, Bentley perfected a different model: acquire for capability, invest for growth, integrate for synergy. They didn't buy companies to eliminate them as competitors—they bought them to add specialized capabilities to the platform.

The integration philosophy was crucial. Original founders often stayed on, continuing their life's work with more resources. Products retained their identity while gaining Bentley's distribution and development capabilities. Customer relationships were preserved and strengthened. This patient integration approach meant acquisitions added lasting value rather than one-time cost synergies.

Platform Strategy: From Point Solutions to Comprehensive Ecosystem

Bentley evolved from selling products to orchestrating ecosystems. MicroStation was just the entry point. Once customers adopted it, they needed ProjectWise for collaboration. Then AssetWise for operations. Then iTwin for digital twins. Each product worked standalone but delivered exponentially more value when integrated. It's the Microsoft Office strategy applied to infrastructure—except the lock-in is even stronger because switching costs are higher.

The platform approach also enabled partner leverage. Instead of building everything themselves, Bentley created APIs and SDKs for others to build on. Thousands of specialized applications integrate with Bentley products, creating network effects that benefit everyone. The platform becomes more valuable as more participants join—a moat that strengthens automatically.

Partnership Dynamics: Working with Giants While Maintaining Independence

The Siemens partnership demonstrated sophisticated strategic thinking. Bentley needed capital and credibility; Siemens needed software expertise and market access. Rather than selling out completely, Bentley structured a partnership that provided both while maintaining independence. Siemens got minority ownership and preferred partnership terms. Bentley got patient capital and industrial credibility. Both benefited without either sacrificing their core strategy.

This approach—strategic partnership without surrender—enabled Bentley to punch above their weight. They could compete with public companies while remaining private. They could access growth capital without venture dilution. They could leverage partner capabilities without losing control. It's a masterclass in having your cake and eating it too.

The Infrastructure Megatrend and Timing the Market

Bentley's greatest strategic insight was recognizing that infrastructure spending isn't cyclical—it's structural. Developed nations must replace aging infrastructure. Developing nations must build new infrastructure. Climate change demands resilient infrastructure. Urbanization requires smart infrastructure. These are decade-long trends with trillions in spending behind them.

But timing still mattered. Bentley went public in 2020 just as COVID accelerated digital transformation. They acquired Power Line Systems just before the grid modernization boom. They developed digital twins just as IoT sensors became affordable. This wasn't luck—it was patient positioning for inevitable trends. They were ready when the market turned their way.

The Recurring Revenue Transformation

Long before SaaS became standard, Bentley pioneered subscription software for enterprise engineering. The SELECT program in the 1990s was revolutionary—all software for one annual fee. This wasn't just a pricing model change—it was a relationship transformation. Customers became partners. Revenue became predictable. Growth became compoundable.

The subscription model also enabled continuous innovation. Instead of major releases every few years that customers might skip, Bentley delivered continuous updates that customers automatically received. This kept the software current, reduced support costs, and eliminated the upgrade cycle that plagued traditional software companies.

Cultural Coherence at Scale

Growing from 5 to 4,000+ employees while maintaining cultural coherence required intentional design. Bentley preserved its engineering-first culture by hiring engineers, promoting engineers, and thinking like engineers. Sales people needed to understand the products technically. Marketers needed to speak the language of infrastructure. Even finance needed to grasp project economics.

This cultural coherence created competitive advantage. While competitors struggled with sales-engineering alignment or product-market fit, Bentley operated with unusual unity. Everyone understood the mission: advance the world's infrastructure. Everyone spoke the same language: engineering excellence. Everyone shared the same values: long-term thinking, customer success, technical integrity.

The Bentley playbook proves that in enterprise software, patience beats pace, depth beats breadth, and ownership beats optionality. It's a blueprint for building businesses that last not just years but generations—businesses that create value not just for shareholders but for civilization itself.

X. Bear vs. Bull Case & Valuation

Bull Case: The Infrastructure Super-Cycle

The bull case for Bentley Systems rests on three powerful megatrends converging at once. First, the infrastructure modernization wave is not a cycle but a generational transformation. The American Society of Civil Engineers estimates $2.6 trillion needed in the U.S. alone by 2029. Globally, McKinsey projects $69 trillion in infrastructure investment through 2035. This isn't stimulus spending that comes and goes—it's decades of catch-up investment in critical systems that cannot be deferred.

Ongoing global infrastructure investment and digital transformation trends are boosting demand for Bentley's advanced AI and cloud solutions, supporting strong revenue and margin growth. Broadening the customer base and rapid adoption of subscription models improve revenue stability, reduce exposure to market cycles, and enhance long-term earnings prospects. The subscription model transformation is nearly complete, with 90%+ recurring revenue providing visibility and stability that commands premium multiples.

The digital twin opportunity alone could double Bentley's addressable market. Every piece of infrastructure—from bridges to water mains—will eventually have a digital twin for monitoring, maintenance, and optimization. Bentley's iTwin platform is years ahead of competitors. As IoT sensors proliferate and 5G enables real-time data transmission, digital twins transition from nice-to-have to mission-critical. Bentley owns this market.

AI represents another step-function growth opportunity. Engineering firms face a talent crisis—not enough engineers for the work ahead. Bentley's AI tools can make one engineer as productive as three. This isn't replacing engineers but augmenting them. The OpenSite+ product shows the potential: 10x productivity improvement in site design. Applied across the portfolio, AI could drive a step-change in customer value and pricing power.

Climate adaptation and sustainability create new demand vectors. Every infrastructure asset must be evaluated for climate resilience. Energy grids need complete redesign for renewable integration. Water systems require optimization for scarcity. These aren't optional upgrades—they're existential imperatives that require sophisticated modeling and simulation. Bentley's software is essential for this transition.

From a valuation perspective, Bentley trades at a significant discount to software peers. At current levels, the stock trades around 30x forward earnings versus 40-50x for high-quality SaaS companies. Gross margin is 81.21%, with operating and profit margins of 24.17% and 18.46%. These metrics are elite—yet the multiple doesn't reflect it. As the market recognizes Bentley's quality and growth durability, multiple expansion could drive 50%+ appreciation independent of fundamental growth.

Bear Case: Structural Headwinds

The bear case starts with competition from larger, better-capitalized rivals. Autodesk has 10x Bentley's revenue and is aggressively moving into infrastructure. The potential ANSYS acquisition would create a engineering software behemoth with complementary capabilities. Oracle, Microsoft, and SAP are all investing heavily in industry clouds. While Bentley has defended its niche for decades, the competitive intensity is unprecedented.

Enterprise sales cycles in infrastructure are notoriously long—often 12-24 months for major platform decisions. This creates inherent growth limitations. Unlike consumer software that can scale virally, or even enterprise SaaS that can land-and-expand quickly, infrastructure software requires extensive pilots, integration, and change management. Growth is fundamentally constrained by sales velocity.

The dual-class structure is a governance red flag. Following the completion of this offering, the shares of Class A common stock and Class B common stock held by members of the Bentley family will represent approximately 67% of our outstanding common stock and approximately 83% of the voting power. Public shareholders have no real say in strategic decisions. The family could make value-destructive acquisitions, resist necessary changes, or sell the company below fair value—and minority shareholders would be powerless.

Technology disruption is a constant threat. Cloud-native competitors could emerge with modern architectures that leapfrog Bentley's legacy code base. Open-source alternatives could commoditize basic functionality. AI could evolve to automate engineering tasks entirely rather than just augment them. Bentley's 40-year-old architecture, while proven, may become a liability in rapidly evolving technology markets.

Customer concentration risk is material. The firm is the only infrastructure engineering software vendor that leads in market share in categories related to both the project and the asset lifecycle phases. Bentley Systems' accounts include 90% of the top 250 of the "ENR 2019 Top 500 Design Firms". This dominance is impressive but also concerning—losing even a few major accounts could materially impact results.

Economic sensitivity may be underappreciated. While infrastructure spending is often countercyclical (governments invest during downturns), private sector spending is highly cyclical. Commercial construction, industrial projects, and private utilities—all major customer segments—cut capital spending aggressively during recessions. The subscription model provides some buffer but doesn't eliminate economic exposure.

Valuation Considerations

Current trading metrics suggest the market is pricing Bentley somewhere between the bull and bear cases. The P/E ratio around 40x is rich by traditional standards but reasonable for a high-quality software company. EV/Revenue of approximately 13x is premium but justified by 80%+ gross margins and 90%+ recurring revenue. The key question is whether growth can accelerate from low-double-digits to mid-teens—if yes, the stock is cheap; if no, it's fairly valued.

Peer comparison is challenging because Bentley is unique. Autodesk is the closest comparable but has lower margins and less recurring revenue. Ansys has similar margins but different end markets. Vertical SaaS companies like Veeva or Guidewire have similar models but different growth profiles. Perhaps the best comparison is to other family-controlled, vertical software leaders like Constellation Software—which has generated exceptional returns despite modest growth rates.

The dual-class discount is real but potentially overstated. Studies suggest dual-class structures reduce valuations by 10-20% on average. However, in Bentley's case, family control has historically been a positive—enabling long-term thinking, patient capital allocation, and strategic flexibility. The discount may narrow if the family continues to execute well and treat minority shareholders fairly.

The infrastructure spending thesis faces timing risk. While the long-term need is undeniable, the near-term pace depends on political will, funding availability, and execution capacity. The U.S. infrastructure bill is spread over many years. European green infrastructure plans face budget constraints. Chinese spending is slowing. The super-cycle is coming but may take longer than bulls expect.

On balance, Bentley appears attractively valued for patient investors who believe in the infrastructure megatrend and can tolerate family control. The combination of recurring revenue, high margins, competitive moats, and secular tailwinds creates an attractive risk-reward. However, investors seeking rapid growth or governance purity will likely be disappointed. This is a compound story, not a momentum trade—a marathon, not a sprint.

XI. Epilogue & Future Outlook

Standing at the 40-year mark, Bentley Systems faces an intriguing paradox: they've never been stronger, yet the challenges ahead have never been greater. The infrastructure software consolidation endgame is approaching. Autodesk's potential ANSYS acquisition would create a $50+ billion engineering software giant. Oracle and Microsoft are investing billions in industry clouds. Private equity firms circle the industry, seeking rollup opportunities. In this environment, can a family-controlled, sub-$20 billion market cap company remain independent?

The answer may lie in Bentley's unique position at the intersection of physical and digital infrastructure. The metaverse opportunity—though overhyped in consumer markets—is very real in infrastructure. Every bridge, building, and power plant will eventually exist as much in digital space as physical space. These aren't gaming environments but operational twins that control real-world systems. Bentley's iTwin platform is effectively the operating system for this new reality.

Climate change paradoxically strengthens Bentley's position. Every extreme weather event validates the need for resilient infrastructure. Every wildfire demands grid hardening. Every flood requires water system redesign. Every heat wave stresses power networks. These aren't problems that can be solved with simple software—they require sophisticated modeling, simulation, and optimization that Bentley has spent decades perfecting.

The sustainability transition creates entirely new categories of infrastructure that need design and management software. Offshore wind farms, solar installations, battery storage facilities, hydrogen pipelines, carbon capture systems—all require specialized engineering software. Bentley's acquisition strategy positions them to own these emerging verticals before they become mainstream.

What would happen if Siemens or another strategic made a bid? The speculation has persisted since 2016, when Siemens AG is weighing an acquisition of Bentley Systems Inc., according to people familiar with the matter, in what would mark a fresh push into industrial-software dealmaking by Europe's largest engineering firm. Siemens could certainly afford it—and the strategic logic is compelling. Combined with Siemens' industrial IoT platform, Bentley's infrastructure software would create an end-to-end digital backbone for the built environment.

Yet the Bentley family has consistently signaled their intention to remain independent. The dual-class structure ensures they control their destiny. The public listing provided liquidity for employees and early investors without sacrificing control. Unless the family dynamics change—always possible with five brothers and multiple generations involved—a sale seems unlikely in the near term.

The more probable path is continued evolution as an independent consolidator. With public currency and proven integration capabilities, Bentley can acquire specialized companies that larger competitors overlook. Each acquisition strengthens the moat, expands the addressable market, and increases customer value. It's a strategy that could work for another decade or more.

The generational leadership transition bears watching. Nicholas Cumins represents a new breed of leadership—technically sophisticated but also fluent in cloud economics and platform strategies. The founders remain involved but are gradually stepping back. This transition, handled smoothly so far, will determine whether Bentley remains a family business or evolves into a professionally managed corporation with family influence.

The AI revolution could be Bentley's greatest opportunity or existential threat. If AI augments engineers, Bentley's tools become more valuable. If AI replaces engineers, the entire market shrinks. The likely reality is somewhere between—AI will automate routine tasks while elevating human expertise for complex decisions. Bentley's early AI investments and domain expertise position them well for this transition.

Looking ahead, several scenarios seem plausible:

Scenario 1: Independent Domination - Bentley continues executing their playbook, growing steadily through acquisition and innovation, eventually becoming the clear infrastructure software leader with a $50+ billion market cap.

Scenario 2: Strategic Acquisition - Siemens, Schneider Electric, or another industrial giant acquires Bentley for $30-40 billion, integrating their software with hardware and services for complete infrastructure solutions.

Scenario 3: Private Equity Rollup - A large PE firm takes Bentley private, combines it with other infrastructure software assets, and creates a massive platform comparable to Constellation Software in vertical markets.

Scenario 4: Generational Pivot - The next generation of leadership transforms Bentley into an AI-first company, potentially disrupting their own legacy business while capturing new markets.

The infrastructure megatrend provides tailwind regardless of path. Governments worldwide are committing trillions to infrastructure investment. Private capital is flooding into infrastructure as an inflation-protected asset class. Technology advancement makes previously impossible projects feasible. Demographics demand age-friendly infrastructure redesign. Climate change necessitates systematic rebuilding. These forces will drive demand for decades.

For investors, Bentley represents a rare combination: a profitable, growing, defensible business riding secular tailwinds with capable management and reasonable valuation. It's not without risks—family control, competitive threats, technology disruption—but the risk-reward appears favorable for those with patience and conviction.

The ultimate question isn't whether Bentley will succeed—they've already succeeded by any reasonable measure. The question is how big they can become and whether public market investors will participate in that value creation. In a world desperately needing infrastructure modernization, betting against the company that builds the tools seems unwise.

Forty years ago, five brothers saw opportunity where others saw terminals and code. Today, their creation stands as critical infrastructure for infrastructure itself—a remarkable achievement that's still being written. The next chapter promises to be just as interesting as the last.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube