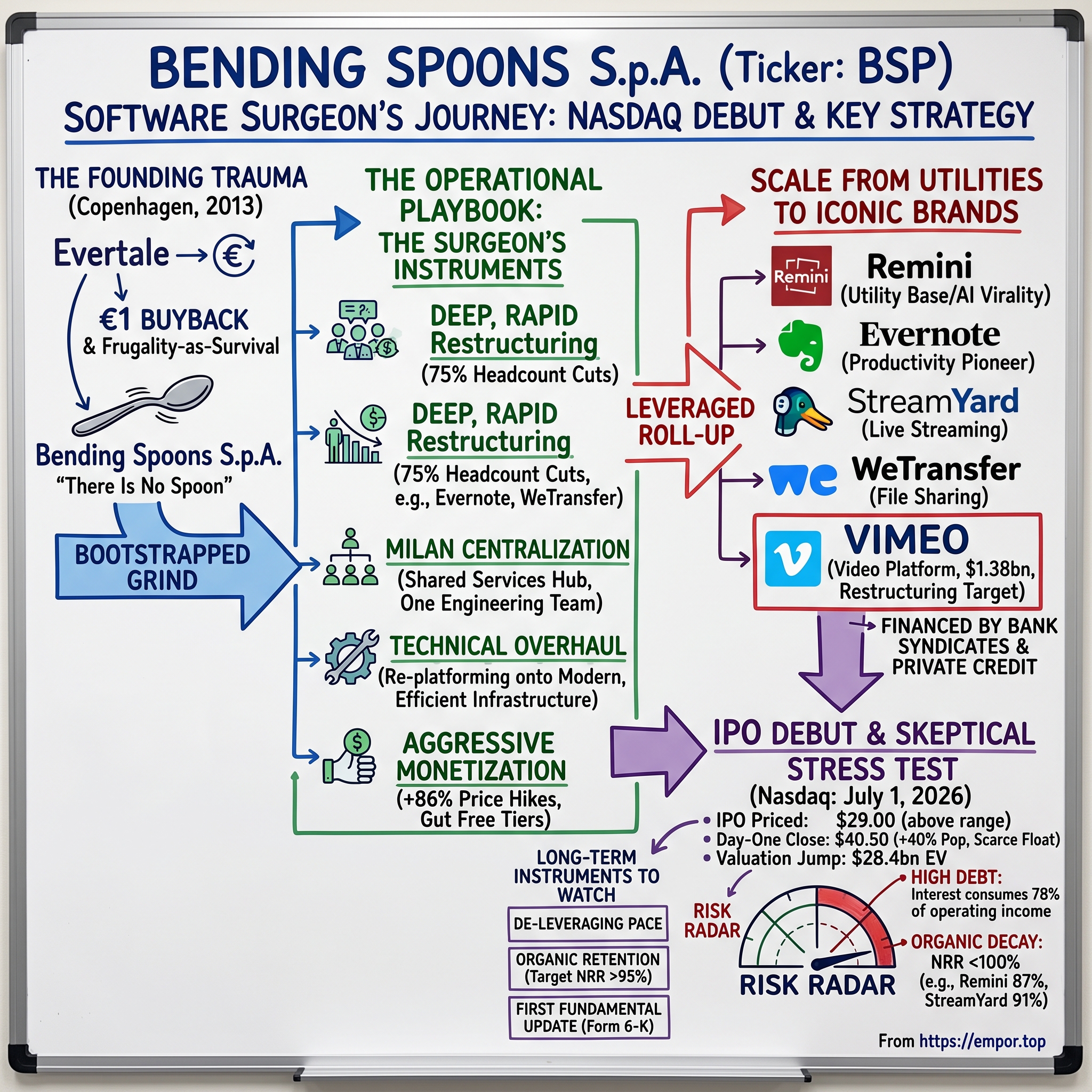

Bending Spoons S.p.A.: The Software Surgeon's Nasdaq Debut

On the last day of June 2026, a Milan software company most Americans had never knowingly used priced the largest technology IPO of the European year on a New York exchange. By the time the closing bell rang the next afternoon, Bending Spoons had done something that looked, on the surface, like a coronation — and something that, on closer inspection, resolved almost nothing about whether the business underneath the ticker deserves the price the market just stamped on it. This is the story of how four friends who once bought their own failing startup back for one euro built one of the most disciplined, most aggressive, and most heavily leveraged software machines in Europe — and of the questions a sophisticated investor should be asking now that the machine trades in public.

Introduction & The Day-One Pop

Picture the Nasdaq MarketSite on Wednesday, July 1, 2026. The confetti-and-podium theater of a first-day listing is designed to manufacture a single feeling: inevitability. Bending Spoons S.p.A. — ticker BSP — had priced its initial public offering the evening before at $29.00 per share, above the $26–28 range its bankers had marketed to institutions, a signal that demand had run hot.5 When the stock opened and climbed, the narrative wrote itself. It closed its first full session at $40.50, up 39.66% on the IPO price, on volume of roughly 17.1 million shares and an intraday range that swung from $30.70 to $43.98.12 The deal itself raised about $1.68 billion.5

A 40% first-day pop is the kind of number that ends arguments. It shouldn't. The most useful thing an independent analyst can do on a day like this is separate what the market actually revealed from what it merely dramatized. The pop is real, it is sourced, and it is decision-relevant — but it is a fact about the demand for a scarce new float, not a verdict on the durability of the underlying business.

Consider what the close did to the valuation. Bending Spoons has roughly 635.2 million total shares outstanding across two classes.3 At the $29.00 offer price, the whole company was worth about $18.4 billion in equity value; layering on roughly $2.68 billion of net debt produced an enterprise value near $21.1 billion.34 At $40.50, that equity value jumped to about $25.7 billion and enterprise value to roughly $28.4 billion — an intraday re-rating of more than seven billion dollars driven entirely by price, not by any new fact about the company.

Now put that against the yardstick. Bending Spoons is, at heart, a software consolidator — a firm that buys other people's software and runs it better. The public gold standard for that model is Canada's Constellation Software, a serial acquirer of vertical-market software that trades around 3.6x enterprise-value-to-sales.3 Against pro forma fiscal 2025 revenue of about $2.608 billion, Bending Spoons at its offer price already carried roughly 8x EV/sales; at the first-day close it reached nearly 10.9x.34 In other words, the market opened Bending Spoons at more than double Constellation's premium multiple and closed it at roughly three times Constellation's high end. Measured against a more directly comparable consumer-media roll-up, the gap looks even wider.

Why should an investor discount the pop rather than celebrate it? Because the structure of this specific listing was engineered — legally and legitimately, but engineered — to produce exactly this outcome. The IPO sold 57,971,015 shares, which is only 9.13% of total shares outstanding and about 17.84% of the ordinary, one-vote share class.35 The remaining 310.24 million Class A founder shares carry five votes each and do not trade publicly.3 A tiny float meeting heavy demand mechanically produces outsized price moves; that is textbook IPO market structure, not a signal about Bending Spoons in particular. And the book was tight: reporting on the deal indicated the top 10 investors were allocated 85% of the shares and the top 25 took 95%.6 When a handful of institutions who already agreed to pay $29 hold nearly the entire tradeable supply, the "market clearing price" on day one is closer to a scarcity auction than to broad price discovery.

So the honest framing is this: the debut confirmed that a concentrated set of large investors wanted in badly enough to bid the stock up 40% against a thin float. It did not confirm that Bending Spoons will grow organically, that its debt is safe, or that the beloved-but-decaying brands it has bought can hold their customers through aggressive price increases. Those are the questions that matter, and the trading session touched none of them. To understand why they are the right questions, you have to go back to the beginning — to a near-dead game studio in Copenhagen and a buyback priced at the cost of a cup of coffee.

Evertale's Ashes and the €1 Buyback

Before Bending Spoons was a software surgeon, it was a patient that nearly died on the table. The company's origin story does not begin in Milan; it begins in Copenhagen, with four young Italians trying and failing to build a hit.

The founders — Luca Ferrari, Francesco Patarnello, Matteo Danieli, and Luca Querella — had a venture-backed startup called Evertale, and by the early 2010s it was running out of money.712 What makes the story more than a standard failure is what Ferrari did about the cash crunch. Rather than let the team disband, he took a high-paying job at McKinsey & Company, using a consultant's salary to keep his co-founders fed while he wrote Evertale's code on nights and weekends.7 It is a small biographical detail that turns out to explain a great deal about the company he would build. Ferrari's instinct in a crisis was not to raise more money or chase a bigger vision; it was to cut personal costs to the bone, subsidize the mission from an outside income stream, and grind. Frugality-as-survival is not a slogan at Bending Spoons. It is the founding trauma.

By 2013 Evertale was effectively finished, and here the founders made the move that becomes the company's genesis myth. Rather than walk away, they bought their own shares back from the outside investors for a symbolic one euro, retaining roughly $40,000 of treasury cash still sitting in the corporate shell.712 Think about what that transaction represents. Professional investors had written the equity down to nothing; the founders' willingness to pay a single euro was, in effect, both sides agreeing the company was worthless. But the founders saw something the investors didn't: not the product, which had failed, but the team and the small pile of cash — a clean, debt-free vehicle they now owned outright. That instinct — to see residual value in an asset everyone else has left for dead, and to acquire it for almost nothing — is the exact instinct the company would later industrialize.

They relocated to Milan and renamed the venture Bending Spoons, after the scene in The Matrix in which a child tells Neo that the way to bend a spoon is to realize there is no spoon — that the constraint is in the mind.812 It is an unusually revealing name for a company that would go on to specialize in bending the apparent economic constraints of software businesses everyone else considered fully optimized. The philosophy embedded in the name — that supposedly fixed limits are often just unexamined assumptions — became the operating thesis.

What followed was a bootstrapped grind through the app economy. The team reinvested tiny early revenues, at one point buying a simple keyboard-customization app for around €10,000 and using it as a laboratory for what became their real competency: a data-driven, heavily automated mobile-marketing and monetization engine.12 They learned, app by app, how to acquire users profitably, how to convert them to paying subscribers, and how to squeeze more lifetime value out of each one than the previous owner had. Out of this era came the first genuine cash cows — the photo-editing tool Splice and, most importantly, the AI photo-enhancement app Remini, which would later become a viral phenomenon.12

The lesson of the Evertale years is not that the founders got lucky; it is that they emerged with a very specific, unglamorous skill — turning mediocre software into cash — and a temperament forged by near-death: extreme frugality, a stomach for hard decisions, and a conviction that the market routinely misprices tired assets. What they lacked, in 2013, was scale. The story of the next decade is the story of a small team methodically building the instruments that would let them perform this surgery not on €10,000 keyboard apps, but on some of the most recognizable names on the internet.

The Surgeon's Instruments: The Operational Playbook

Every roll-up needs a playbook, and the reason Bending Spoons earned the nickname "software surgeon" is that its playbook reads less like a growth strategy than like an operating manual for a very fast, very unsentimental restructuring.11 The consistency is the point. Where most acquirers improvise, Bending Spoons runs the same procedure on almost everything it buys, which is both the source of its remarkable margins and the source of its biggest reputational risk.

The first instrument is immediate operational surgery — deep, rapid headcount reduction. This is not gentle synergy-hunting over eighteen months. When Bending Spoons acquires a company, it typically removes a majority of the workforce within the first year, often 50% to 75% or more. After buying the Amsterdam file-sharing icon WeTransfer, it moved to cut roughly 75% of staff.10 The pattern was established even more starkly with Evernote, where the company laid off a large share of the existing team and effectively hollowed out its U.S. operation.11 To a casual observer this looks brutal, and it is; the analytical question is whether it is effective, and the evidence so far is that it dramatically lowers the cost base of businesses that had grown flabby under prior ownership.

The second instrument is centralization to Milan. Bending Spoons does not run its acquisitions as standalone units with their own offices, HR, finance, and engineering cultures. It shuts the satellite offices and pulls the surviving functions — engineering, product, design, customer support — into a shared services hub in Milan.1112 The logic is a scale economy: one recruiting engine, one infrastructure team, one design system, one monetization playbook serving a whole portfolio of apps. A single elite engineering organization maintaining ten products is structurally cheaper than ten separate teams, and it lets the company redeploy its best people across whichever asset most needs them.

The third instrument is a radical technical overhaul. Acquired products are re-platformed onto Bending Spoons' own unified, modern infrastructure, stripping out the expensive legacy code and third-party hosting arrangements that bloat the cost of running an aging app. For a non-technical listener, the analogy is buying an old house with good bones on an expensive plot, then gutting the wiring and plumbing and connecting it to a shared, efficient utility grid you already operate — the house looks the same to the resident, but it costs a fraction to run.

The fourth and most controversial instrument is aggressive monetization and price-elasticity testing. This is where the surgery gets personal for users. Bending Spoons raises subscription prices hard — reportedly on the order of an 86% increase on Evernote's Personal plan — and it caps or guts free tiers, at one point restricting Evernote's free plan to just 50 notes, a limit that renders the free product nearly unusable for its original purpose.11 The strategy deliberately pushes casual, low-value users out and refocuses the product on high-lifetime-value prosumers and enterprises willing to pay. Management's implicit bet is that a beloved tool has more pricing power than its previous owners ever dared to test.

That bet is exactly what an independent analyst should interrogate rather than accept. Raising prices 86% and slashing a free tier will always increase near-term revenue per user; the question is whether it increases durable revenue or simply harvests the loyal base while accelerating the exit of everyone else. The honest answer is that price hikes and churn are two sides of the same lever, and you cannot judge the strategy from the revenue line in the quarter of the increase. You judge it from retention over multiple years — which is precisely the metric Bending Spoons has been most guarded about, and which we will return to.

The final instrument is not operational but structural: control. The four co-founders retained the 310.24 million Class A founder shares that carry five votes each, ensuring that no matter how thin the public float or how loud the public criticism of the layoffs and price hikes, strategic control stays with the people who bought the company back for a euro.3 They pointedly do not pay dividends; they reinvest the cash their portfolio throws off into ever-larger acquisitions, behaving far more like the general partners of a private-equity fund than like the management of a conventional software company. Whether you find that reassuring or concerning depends on how much you trust the surgeons — and the way to build or withhold that trust is to watch what they bought, and how they paid for it. That is the next chapter.

The Great Roll-Up: Scaling from Utilities to Stagnant Icons

For its first decade, Bending Spoons practiced on small game. Then, beginning in 2023, it started operating on some of the most recognizable brands on the consumer internet — and financing those operations with an amount of debt that turned a bootstrapped app studio into a leveraged consolidator almost overnight.

The step-function began with Evernote. When Bending Spoons agreed to acquire the productivity pioneer — the digital notebook that a generation of knowledge workers had loved and then slowly abandoned — it was buying a wounded icon: beloved, bloated, feature-sprawled, and unprofitable.[^9] Evernote was the ultimate test of the playbook precisely because the brand carried so much emotional equity. If the surgeons could fire most of the team, hike prices, gut the free tier, re-platform the app, and turn a money-losing legend into an efficient cash generator without the brand collapsing, the model would prove it could scale to real size. The layoffs and price increases that followed made Bending Spoons a case study — literally, in S&P Global's coverage of the "software surgeon" restructuring model — and they generated a wave of public anger from long-time users.11 The strategy monetized the loyal core, but it also demonstrated the model's central tension in full public view: the same actions that fix the P&L can erode the brand that made the asset worth buying.

Momentum built quickly from there. In 2024 the company expanded beyond productivity into two adjacent consumer categories: it acquired the live-streaming studio StreamYard in April, adding a tool used by creators and businesses to broadcast to social platforms, and in July it completed its acquisition of WeTransfer, the Dutch file-transfer service whose clean, ad-supported interface was a daily habit for millions of designers and creative professionals.9 The WeTransfer deal, followed by the ~75% headcount reduction, showed the playbook running at a larger scale and against a business with a very different revenue model — advertising and light subscriptions rather than Evernote's pure SaaS.10

Then came the blockbuster. In 2025 Bending Spoons acquired Vimeo, the video platform, in a deal valued at roughly $1.38 billion, completing the transaction in May.[^13] Vimeo is worth dwelling on because it is where the bull and bear cases collide most directly. On paper, Bending Spoons bought a well-known video brand at what looked like a distressed revenue multiple — Vimeo had spent years struggling to define itself against YouTube on one side and enterprise video tools on the other. The skeptical question is whether "cheap on revenue" actually meant cheap, or whether it meant Bending Spoons bought a structurally challenged asset that required exactly the same violent restructuring — heavy layoffs in early 2026 and a pivot toward higher-margin enterprise video — just to make the economics work against the debt used to buy it.[^13] Benchmarked against video-software peers, the acquisition only pencils out if the enterprise pivot holds and the cost cuts stick; at a merely "distressed" multiple with the old cost structure, it would not.

None of this was financed out of app profits. The transition from bootstrapper to leveraged consolidator was underwritten by a power grid of banks and private-credit funds. Bending Spoons assembled multi-billion-dollar facilities arranged by syndicates including major Wall Street institutions and specialist private-credit lenders — the kind of capital structure, led by names such as JPMorgan and Goldman Sachs alongside private-credit players, that turns a software company into something closer to a private-equity portfolio with a term loan attached.12[^15] By the time of the F-1/A filing, gross debt stood at roughly $5.1 billion before accounting for the later Tractive acquisition, and net debt was about $2.68 billion once the final prospectus's capitalization table was reconciled at the actual $29 offer price.34

Here is the strategic read. Bending Spoons has demonstrated, repeatedly and at increasing scale, that it can take a tired consumer-software brand, cut its costs by more than half, raise its prices, and convert it into a cash machine. That is a genuine, evidenced capability, not a management boast. But every acquisition in the sequence has been a consumer or prosumer brand — apps that individuals choose and can un-choose — bought with a growing pile of debt. The model's engine and its vulnerability are the same thing: it runs on cheap, distressed assets and leverage, and it must keep finding both. To understand whether that engine can keep running, you have to look inside the portfolio it has assembled and ask which parts actually generate the cash — and which are quietly decaying.

The Portfolio Engine: Segment Economics & AI Optionality

If you want to understand a roll-up, ignore the logos on the website and follow the money. Bending Spoons' portfolio spans photo editing, note-taking, file transfer, live streaming, and video hosting, but these businesses are wildly unequal in economic weight, and the marketing narrative — a constellation of beloved apps — obscures where the pro forma $2.608 billion of fiscal 2025 revenue actually comes from.3

At the top sit the heavyweights. WeTransfer and Vimeo, the two largest and most recent major acquisitions, drive the majority of consolidated revenue, profit, and enterprise value today.3 These are the assets whose restructuring economics most determine whether the leveraged model works, which is why the aggressive early-2026 cuts at Vimeo and the deep reduction at WeTransfer matter so much more to the investment case than a headline about any single app. When a listener hears "Bending Spoons," they may think of a cute photo app; the balance sheet thinks of file transfer and video.

Below them is the prosumer core: Evernote and StreamYard, businesses built on recurring subscriptions from professionals and creators. These provide the stable, high-margin cash flows that the model is designed to maximize — customers who have integrated the tool into their daily workflow and who, in theory, will absorb price increases rather than rebuild their habits elsewhere. "In theory" is doing real work in that sentence, and the retention data, discussed shortly, is where theory meets evidence.

At the base is the utility legacy — Remini and the older mobile apps that built the company. They remain profitable, but they represent a shrinking share of the long-term case as the portfolio's center of gravity shifts toward the acquired icons. It would be a mistake, though, to dismiss Remini, because it is the clearest window into both the upside and the fragility of consumer-AI revenue.

Remini is where generative AI stopped being a buzzword for Bending Spoons and became a cash event. The app rode a viral wave of AI avatar and photo-enhancement filters — the kind of feature that briefly saturates social media as everyone generates stylized portraits of themselves — and converted that attention into a surge of short-term subscription revenue.12 The genius of Bending Spoons' marketing machine is that it is engineered to capture exactly these spikes: to acquire users cheaply the moment a feature goes viral and monetize them before the novelty fades. The danger is right there in the same sentence — "before the novelty fades." Viral AI revenue is, almost by definition, spiky and hard to underwrite as durable. A quarter that benefits from an avatar craze is not a run-rate.

The broader AI question for the portfolio is whether embedding proprietary generative-AI tools across WeTransfer, Vimeo, and Evernote represents real growth optionality or a speculative novelty. The disciplined answer is to size it honestly: these features are strategically useful for retention — giving a subscriber who just absorbed a price hike a reason to stay — but they do not yet drive material standalone segment revenue, and there is no disclosure suggesting otherwise. Treating AI as a plausible enhancer of pricing power and stickiness is defensible; treating it as a new revenue engine that justifies the multiple would be getting ahead of the evidence.

Put the segments together and a clear-eyed picture emerges. Bending Spoons is not, economically, a portfolio of viral consumer apps; it is increasingly a leveraged owner of a few mid-sized prosumer and enterprise-media franchises, topped up by opportunistic consumer-AI cash flows. The heavyweights carry the debt, the prosumer core provides the ballast, and the utility legacy provides optionality and occasional windfalls. Whether that structure compounds value or slowly bleeds it comes down to two forces pulling in opposite directions — the cost of the debt on one side, and the organic decay of consumer subscriptions on the other. That collision is the heart of the bear case, and it deserves its own stress test.

The Skeptical Investor Stress Test: Debt & Multi-Year Decay

Now put on the hat of a short-seller, or an activist, or simply a careful credit analyst, and ask the uncomfortable questions. Two of them, joined at the hip, define the entire risk profile of Bending Spoons: how heavy is the debt, and how fast does the underlying revenue decay on its own?

Start with leverage. Carrying roughly $5.1 billion of gross debt pre-Tractive against a business generating about $2.6 billion of revenue is aggressive by any software standard.3 But gross debt is an abstraction; the number that should stop a listener cold is the coverage ratio. In the first quarter of 2026, interest expense consumed about 78% of the company's total operating income.3 Translate that out of finance-speak: for roughly every dollar the operating business earned before interest, seventy-eight cents went straight to lenders. That leaves a very thin sliver — barely more than a fifth of operating profit — as the entire margin for error covering taxes, reinvestment, integration hiccups, and the inevitable acquisition that underperforms. A business that keeps 22 cents of operating profit after interest is a business with almost no cushion. If revenue softens, if an integration slips, or if the cost of the debt resets higher on refinancing, that sliver can vanish. This is the single most important structural fact about Bending Spoons, and no first-day pop changes it.

The bull's answer is that the debt is a feature, not a bug — that Bending Spoons deliberately uses cheap leverage to buy assets it can rapidly make more profitable, and that as it de-levers, equity holders capture the spread. That is a coherent private-equity logic. But it depends entirely on the cash flows being stable and growing. Which brings us to the second question, and the one that most distinguishes Bending Spoons from the consolidator it is most often compared to.

Constellation Software, the benchmark, buys business-to-business vertical-market software — the mission-critical systems that run a dental practice or a marina or a bus fleet. Those products have enormous switching costs and organic net revenue retention that typically exceeds 100%, meaning that even without acquisitions, the existing customer base spends more every year.3 That is the holy grail of software: a portfolio that grows organically while you sleep.

Bending Spoons buys the opposite kind of asset. Its products are consumer and prosumer apps — photo enhancers, note-takers, file-transfer tools — which people adopt casually and abandon easily, and which face structurally higher churn. The disclosed evidence bears this out: Remini's multi-year average net revenue retention was about 87%, and StreamYard's about 91%.3 A number below 100% means the existing customer base shrinks in value every year absent new customers or price increases. At 87%, roughly an eighth of the revenue base erodes annually on its own.

Sit with what that implies mechanically. If your portfolio organically decays, growth is not a bonus — it is a treadmill you must run just to stay in place. Bending Spoons has only two ways to offset organic decay: acquire ever-larger businesses to keep total revenue climbing, or impose continuous, compounding price increases on a shrinking user base. Both are exactly what the company does. And both have limits. The acquisition treadmill requires perpetual access to cheap debt and cheap targets — a condition that a higher-rate or more competitive environment can withdraw. The price-hike treadmill requires that switching costs be high enough to hold customers through repeated increases — and the Evernote experience, where a vocal cohort of users decamped for free or cheaper alternatives like Notion and Obsidian, is direct evidence that for at least some products, that pricing power has a ceiling.

Run the two frameworks investors reach for here. In Hamilton Helmer's 7 Powers, Bending Spoons has a legitimate claim to Scale Economies — the Milan shared-services hub genuinely lets it run many products more cheaply than standalone owners could, and that advantage strengthens with each acquisition. Its claim to Switching Costs is real but weaker and product-specific: strong for a deeply embedded prosumer who has years of notes or an enterprise video workflow locked in, and demonstrably fragile for the casual consumer the price hikes are designed to shed. It has little in the way of Network Economies or Branding power that it hasn't actively spent down through cost cuts. Through Porter's Five Forces, the buyer power of individual consumers is high (they can leave for free substitutes), the threat of substitutes is severe (Notion, Obsidian, YouTube, and a dozen free tools), and rivalry includes not just other private-equity roll-ups and IAC-style operators but Asian scale players like 美图公司 Meitu and 字节跳动 ByteDance — the owner of CapCut — that operate photo and video tools at enormous scale and lower cost structures. Bending Spoons' edge is operational and financial discipline, not an unassailable moat around any single product.

Finally, the disclosure radar. A skeptical investor should note that the final Form 424B4 prospectus explicitly excluded the Tractive acquisition — the pet-tracking business — from its capitalization table and pro forma statements entirely.4 There may be a perfectly ordinary reason (timing, deal mechanics), but the practical effect is that the leverage and revenue picture presented to IPO buyers is incomplete: the real, all-in debt load is higher than the $2.68 billion net figure the prospectus reconciles, and a material acquisition sits outside the numbers investors used to price the deal.4 As a foreign private issuer, Bending Spoons is not required to file the quarterly U.S.-style disclosures that would quickly close that gap; it reports on a lighter schedule, furnishing interim updates via Form 6-K at its discretion.4 For a highly leveraged company whose entire thesis turns on integration timelines and organic retention, thinner disclosure is itself a risk factor — it means investors will see the treadmill's speed less often and later than they would for a domestic filer. That combination of high leverage, organic decay, real-but-partial moats, and discretionary disclosure is the full shape of the bear case. Weigh it against the bull case, and the investment question comes into focus.

Bull vs. Bear Cases & The Long-Term Playbook

Every leveraged consolidator is, ultimately, a bet on whether a management team's edge compounds faster than its risks accumulate. Bending Spoons offers an unusually clean version of that bet, because both sides are so vivid.

The bull case is that the software-surgeon playbook is a repeatable, scalable machine that the public market has just handed a powerful new tool. In this view, the operational skill is proven: Bending Spoons really can cut a bloated acquisition's costs by more than half, re-platform it onto a shared low-cost stack, and drive portfolio operating margins to levels most software companies never see. High-value prosumer and enterprise customers, the argument goes, will keep absorbing price increases because the tools are genuinely embedded in their work. And now, with a Nasdaq-listed equity currency and a public profile, the company can both accelerate debt paydown and use its stock to keep acquiring distressed platforms — the next Evernote, the next Vimeo — at cheap multiples. If organic decay can be held to a manageable rate while the acquisition engine keeps compounding total revenue and the debt comes down, the equity math on a de-levering, high-margin compounder is powerful. The bulls point to the founders' decade-long consistency — frugal, disciplined, willing to make brutal decisions — as evidence that this is a management team that does what it says.

The bear case is that the same engine stalls the moment its two fuel sources — cheap debt and cheap targets — get expensive, and that the thin 22-cent coverage cushion leaves no room for the stall. In this view, the aggressive price increases don't demonstrate pricing power; they spend it, permanently eroding the brand equity of Evernote and WeTransfer and accelerating exactly the churn the sub-100% retention figures already reveal. Organic decay outruns the team's ability to find and finance the next big acquisition, the treadmill slows, and a company priced at nearly 11 times sales — three times its closest public analog — re-rates hard toward the peer multiples it currently trades far above.3 The activist's version adds governance to the indictment: five-vote founder shares that insulate management from accountability, a thin public float that concentrates power, an acquisition (Tractive) kept off the pro forma page, and a foreign-private-issuer status that limits how often outsiders can check the numbers. To the bear, this is not a compounder; it is a leveraged harvest of decaying assets, dressed as a growth story and sold into a scarcity-driven pop.

The independent read sits between these, and it is deliberately not a verdict. What is proven is the operational capability — the cost surgery is real and evidenced across multiple deals. What is unproven is the durability of the revenue those cost cuts sit on top of, and that is the crux. The bull case requires organic retention to stabilize near the levels of a true compounder; the disclosed retention figures show it currently well below that. The bull case requires the debt to be a temporary tool; the coverage ratio shows it is currently a binding constraint. The valuation the market assigned on day one prices in a resolution of these questions in the bulls' favor — which is precisely why the pop is a weaker signal than it looks, and why the burden of proof now sits with the fundamentals, not the ticker.

For a long-term investor, the noise of the debut and the daily quote matters far less than three specific instruments on the dashboard. Watch these, and you are watching the actual thesis:

One — the de-leveraging pace. The entire bull case depends on the roughly $2.68 billion of net debt falling, and the 78% interest-to-operating-income burden easing with it.34 The rate at which management pays down debt is the clearest test of whether the cash flows are as strong and as controllable as advertised. Stalled de-leveraging would be the first sign the machine is straining.

Two — organic net revenue retention across the heavyweights. Remini at 87% and StreamYard at 91% set the current baseline.3 The question that decides everything is whether NRR at WeTransfer, Vimeo, and Evernote can be stabilized above roughly 95% after the restructurings and price hikes. If it can, the "beloved brands hold their customers" thesis survives; if retention keeps sliding as prices rise, the treadmill is losing to gravity.

Three — the first genuine post-IPO business update. As a foreign private issuer, Bending Spoons will not file a U.S.-style quarterly report; its first clean look at post-listing organic growth and at the integration of excluded assets like Tractive will come whenever it furnishes an interim update, likely via Form 6-K, with market watchers pointing to a window around the third quarter of 2026.4 That first fundamental print — not the first-day close — is the event that will actually begin to resolve the entry-point-versus-exit question the debut left wide open.

Bending Spoons arrived on Nasdaq as one of the most disciplined operators in European software and one of the most leveraged, wrapped in a first-day pop engineered to feel like vindication. The founders who once bought their own company back for a euro have built something genuinely formidable and genuinely fragile at the same time. Which of those two words wins will not be decided by the price on the screen. It will be decided, quarter by unglamorous quarter, by whether the customers stay when the bill goes up — and whether the debt comes down before the cheap targets run out.

References

-

Bending Spoons Shares Jump After $1.68 Billion IPO Debut — Bloomberg, 2026-07-01 ↩

-

Bending Spoons S.p.A. Form F-1/A (Amendment No. 1) — SEC EDGAR, 2026-06-22 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Bending Spoons S.p.A. Form 424B4 (final prospectus) — SEC EDGAR, 2026-07-01 ↩↩↩↩↩↩↩↩

-

Bending Spoons prices IPO above range to raise $1.68bn ahead of Nasdaq debut — The Next Web, 2026-06-30 ↩↩↩

-

Bending Spoons IPO sees top 10 investors take 85% of shares — Bloomberg via Investing.com, 2026-07-01 ↩

-

Luca Ferrari, Co-founder & CEO of Bending Spoons — The Twenty Minute VC Podcast, 2023-11-20 ↩↩↩

-

Bending Spoons Official Corporate Homepage — Bending Spoons ↩

-

Bending Spoons Completes Acquisition of WeTransfer — Bending Spoons, 2024-07-31 ↩

-

WeTransfer Owner Bending Spoons to Cut 75% of Staff After Takeover — Bloomberg, 2024-09-03 ↩↩

-

Software Surgeons: Bending Spoons Evernote Layoffs Signal Rise of Restructuring — S&P Global, 2023-07-12 ↩↩↩↩↩

-

How Milan's Bending Spoons Became Europe's Quiet Tech Giant — Financial Times, 2024-02-18 ↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube