Brixmor Property Group: The Rise, Fall, and Reinvention of America's Shopping Center Empire

I. Introduction & Episode Roadmap

Picture this: you are standing in a parking lot somewhere in suburban America. Maybe it is a Tuesday morning in Orlando, or a Saturday afternoon outside Houston. The asphalt stretches out before you. To your left, a Publix or a Kroger hums with steady foot traffic. To your right, a TJ Maxx, a nail salon, a Chipotle, and a UPS Store sit side by side in an L-shaped strip, their storefronts facing the lot. There is nothing glamorous about it. No soaring glass atrium, no designer water features, no valet parking. Just a grocery-anchored strip center doing what strip centers have done since Eisenhower built the highways: serving the daily, unglamorous needs of the American suburb.

Now multiply that scene by 348. That is Brixmor Property Group — the largest pure-play open-air shopping center REIT in the United States, owner and operator of roughly 63 million square feet of retail space spread across more than thirty states. It is a company most Americans have never heard of, yet one whose properties they almost certainly visit every week.

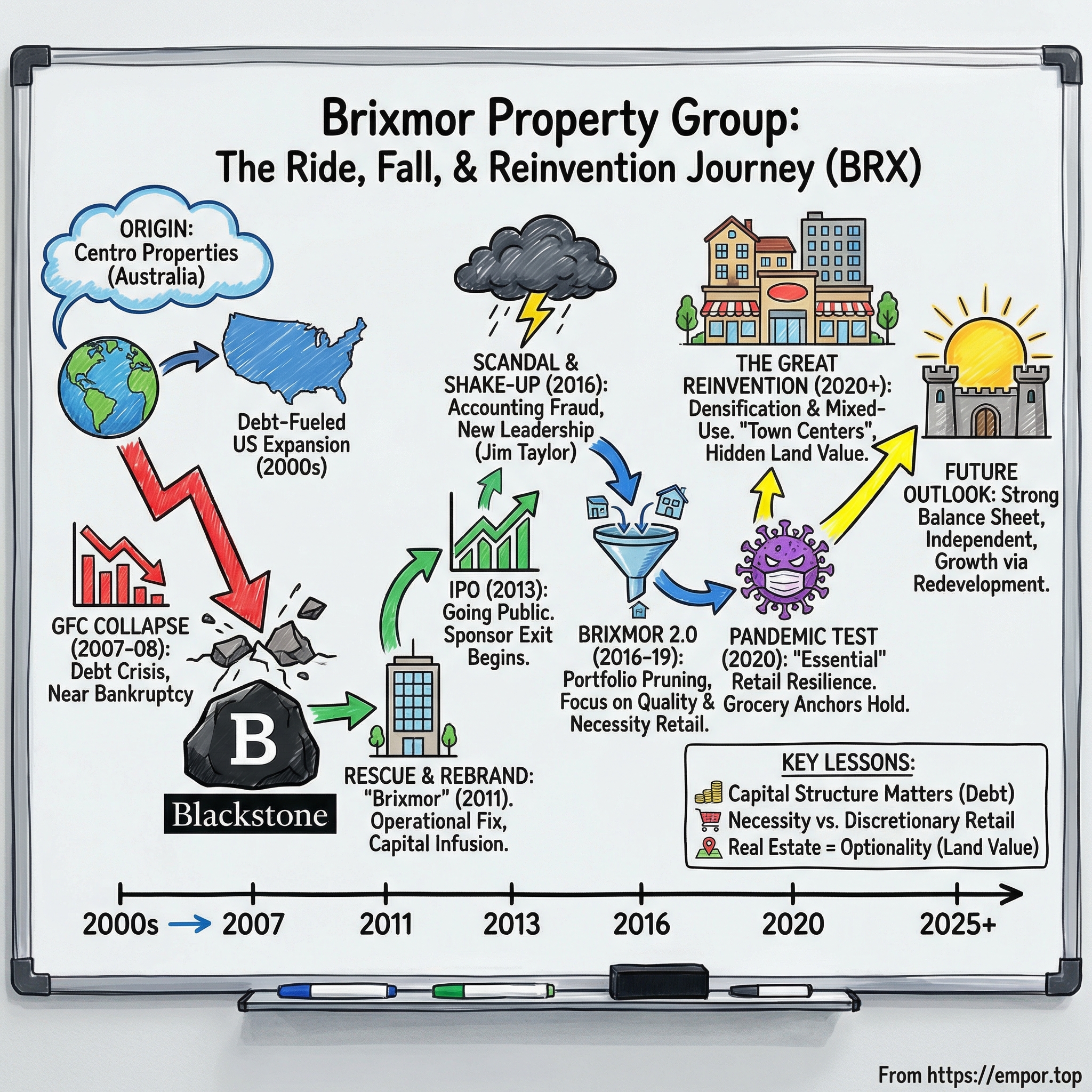

The Brixmor story is not a simple one. It is the story of an Australian company called Centro Properties that built a shopping center empire on short-term debt and watched it collapse spectacularly during the Global Financial Crisis. It is the story of Blackstone, the world's largest alternative asset manager, swooping in to buy those distressed assets for pennies on the dollar and transforming them into a publicly traded company. It is the story of an accounting scandal that toppled the entire management team. It is the story of a retail apocalypse that investors feared would render these properties worthless, followed by a global pandemic that stress-tested that fear in real time. And it is, ultimately, the story of how a collection of asphalt parking lots and single-story retail boxes turned out to be sitting on some of the most valuable land in suburban America.

The central question is deceptively simple: How did a Blackstone rollup of distressed shopping centers survive the most hostile operating environment in the history of American retail and emerge not just intact, but arguably stronger?

The answer involves private equity engineering, the difference between narrative and reality, the surprising durability of grocery stores, a management scandal and its aftermath, and a quiet transformation that is turning shopping centers into something that looks a lot more like town centers. Along the way, we will encounter an Australian company that collapsed under the weight of its own leverage, a private equity giant that saw opportunity where others saw only ruins, a whistleblower who exposed accounting fraud, and a pandemic that turned out to be the ultimate validation of a thesis that everyone had dismissed.

This is a company that died, was reborn, and had to reinvent itself twice. Let us start from the beginning — not with the company itself, but with the humble, underappreciated asset class at its core.

II. The Strip Center: Understanding the Asset Class

Before diving into corporate history, it is worth pausing to understand what a shopping center actually is, because the terminology matters enormously and the distinction between different types of retail real estate has been worth billions of dollars in market capitalization.

When most people hear "shopping center," they picture an enclosed mall — a climate-controlled cathedral of consumption with department store anchors, food courts, and teenagers loitering near the fountain. That is not what Brixmor owns. Brixmor owns open-air shopping centers, commonly known as strip centers or neighborhood centers. These are the unglamorous, single-story, L-shaped or U-shaped retail properties anchored by a grocery store or a discount retailer, surrounded by smaller inline shops — your dry cleaner, your dentist, your pizza place, your phone repair shop. They are typically between 100,000 and 250,000 square feet, serve a trade area of three to five miles, and are designed around one simple idea: convenience.

The anatomy of a grocery-anchored center is elegant in its simplicity. The anchor tenant — usually a grocery store occupying 40,000 to 60,000 square feet — generates the traffic. Americans visit the grocery store an average of 1.6 times per week, and that habitual, non-discretionary trip creates a reliable stream of foot traffic that smaller tenants can tap into. The nail salon does not need to advertise; it just needs to be next to the Kroger. The Subway does not need a destination draw; it catches the shopper who picks up a sandwich on the way out. This co-tenancy dynamic — where the anchor generates traffic and the inline shops harvest it — is the fundamental economic engine of the strip center.

The economics work through a structure called a triple-net lease, or NNN. In a triple-net lease, the tenant pays not just base rent but also their proportional share of property taxes, insurance, and common area maintenance charges (known as CAM charges — the cost of keeping the parking lot paved, the lights on, and the landscaping maintained). This means the landlord's revenue is relatively predictable and the operating costs are largely passed through to tenants. Think of it like a toll road: Brixmor builds and maintains the road, and every tenant pays a toll to be on it.

This asset class emerged from the great American suburbanization wave following World War II. As millions of families moved to newly built suburbs in the 1950s and 1960s, they needed places to shop that were closer to home than downtown. Developers realized they could build simple, cost-effective retail strips along major roads and arterials, anchor them with a grocery store, and fill the remaining spaces with services.

The timing was not coincidental. The Federal Aid Highway Act of 1956 — which created the Interstate Highway System — made suburban living practical on a mass scale. Families could live ten or twenty miles from the city center and still commute by car. But those families also needed places to shop within a five-minute drive of home. Strip centers filled that need. The formula was so effective that by the early 2000s, there were an estimated 100,000 strip centers across America — far more than enclosed malls, which peaked at roughly 1,500. For every glamorous shopping mall built by a developer like Victor Gruen, dozens of humble strip centers sprouted along suburban arterials, quietly generating the rental income that built fortunes for their owners.

The critical distinction for investors is between "necessity retail" and "discretionary retail." Necessity retail includes categories that people need regardless of economic conditions or online alternatives: groceries, haircuts, dental visits, auto repair, medical clinics, banking, dry cleaning, pet care. Discretionary retail includes things people want but can defer or buy online: clothing, electronics, books, sporting goods. Think of it this way: when the economy contracts, you still need to eat, you still need a haircut, your dog still needs to go to the vet, and your car still needs an oil change. You might skip the new jacket from Nordstrom, but you are not skipping the weekly trip to Publix. The retail apocalypse of the 2010s devastated discretionary retail. Necessity retail barely flinched. Understanding this distinction is the key to understanding why Brixmor survived while enclosed malls struggled, and it is the foundation upon which the entire investment thesis rests.

There is another layer to the economics that is worth understanding: how the different tenant types within a strip center interact financially. Anchor tenants — the grocery stores and big-box retailers that occupy 40,000 square feet or more — typically pay the lowest rents per square foot, sometimes as little as $8 to $12. They get this discount because they generate the traffic that makes the entire center viable. Inline tenants — the smaller shops of 1,200 to 5,000 square feet — pay significantly higher rents per square foot, often $20 to $35 or more, because they are essentially paying for access to the anchor's traffic. This rent gradient means that a well-leased strip center generates disproportionate revenue from its smaller tenants. When small shop occupancy rises from 88 percent to 92 percent, the impact on revenue is outsized relative to the square footage involved. This is why Brixmor's record small shop occupancy of 92.2 percent at year-end 2025 was such a meaningful achievement — it represented the monetization of the highest-value space in the portfolio.

For more than fifty years, the strip center model worked beautifully. But vulnerability always lurked beneath the surface. The business depended on two things remaining true: that Americans would continue to live in car-dependent suburbs, and that certain categories of commerce would remain stubbornly physical. As we will see, both assumptions were tested severely — and both, remarkably, held up better than almost anyone predicted. Before Brixmor could prove that thesis, though, someone else had to build the portfolio. And that someone was an Australian company with a spectacular appetite for leverage.

III. The Pre-History: Centro Properties and the Australian Bubble

In the early 2000s, a company called Centro Properties Group was one of Australia's most admired REITs. Founded in 1985 as Jennings Properties Limited — a spin-off from the Jennings Group, an Australian property developer — Centro had built a respectable portfolio of Australian shopping centers through patient acquisitions and solid management. The company was renamed Centro Properties in 1991 and spent the rest of the decade growing methodically, securing management rights over other Australian property trusts and building expertise in retail asset management.

But patient acquisitions were not what made Centro famous. What made Centro famous was an audacious, debt-fueled expansion into the United States that turned a mid-sized Australian REIT into the fifth-largest shopping center owner in America — and then, in the span of two days, nearly destroyed it.

Centro's US expansion began modestly in 2003 with a single shopping center in Los Angeles. But the strategy quickly escalated. By 2006, Centro was making billion-dollar acquisitions, purchasing Heritage Property Investment Trust for approximately $2.1 billion. Then in April 2007, Centro completed its most ambitious deal yet: the acquisition of New Plan Excel Realty Trust for approximately $6.2 billion, including the assumption of debt. In the space of just four years, Centro had gone from a single US property to controlling more than 680 shopping centers with assets worth $26.6 billion across Australia and the United States.

The rollup playbook was straightforward: buy portfolios of neighborhood and community shopping centers, many in secondary and tertiary markets, and finance the purchases with short-term bridging loans that Centro planned to refinance once the deals closed. The assumption underlying the entire strategy was that credit markets would remain liquid and accommodating — that Centro could always roll its short-term paper into longer-term debt at favorable rates. It was the financial equivalent of running a marathon while breathing through a straw: technically possible under perfect conditions, catastrophic if anything went wrong.

The red flags were visible to anyone who looked. The Heritage and New Plan Excel acquisitions came with additional debt components of $1.5 billion and $1.4 billion respectively. Centro's balance sheet was a tower of leverage, with maturity dates clustered in the near term. The strategy depended entirely on the availability of cheap refinancing — what financial professionals call "rollover risk." To use an everyday analogy: imagine buying a house with a mortgage that has to be fully repaid and re-originated every six months. As long as banks are happy to lend, you are fine. The moment they are not, you lose the house — regardless of what it is worth. That was Centro's position, multiplied by billions of dollars across hundreds of properties.

The company's financial reports, as would later be revealed in court, failed to properly classify billions of dollars in short-term liabilities, making the balance sheet appear healthier than it was. Approximately $2 billion worth of liabilities were incorrectly categorized as non-current — meaning investors and analysts looking at the balance sheet thought this was long-term debt when it was actually due within twelve months. Another $1.75 billion in short-term guarantee obligations was not disclosed at all. Eight directors would eventually be found to have breached Australia's Corporations Act for signing off on those misleading reports.

But in the frothy credit markets of 2006 and 2007, none of this seemed to matter. Debt was cheap, asset prices were rising, and the global financial system was humming with the kind of confidence that, in retrospect, always precedes a crash. Centro's share price peaked above A$10 in May 2007. The company's acquisition binge had been cheered by analysts and investors who saw a growth story without questioning the fragility of the foundation. It is a pattern that repeats across industries and eras: when leverage is cheap, growth is easy, and the risks are invisible until suddenly they are the only thing anyone can see. Centro had become a case study in how financial engineering could transform a modest Australian property company into a global retail empire. What it had actually become was a case study in what happens when leverage meets illiquidity. That lesson was about to arrive with devastating speed.

IV. The Global Financial Crisis and Centro's Collapse

On December 17, 2007, Centro Properties announced that it had been unable to refinance $1.3 billion in short-term debt. The admission was the corporate equivalent of a heart attack. In two trading days, Centro's share price collapsed from A$10.06 to A$0.42 — a decline of more than ninety percent. Market capitalization evaporated from nearly $10 billion to just $1.35 billion. It became one of the largest corporate collapses in Australian history, and the largest Australian casualty of the American credit squeeze.

The mechanics of the collapse were brutally simple. Centro had funded long-term assets — shopping centers with decades of useful life — with short-term debt that needed to be rolled every few months. When global credit markets seized up in the second half of 2007, triggered by the US subprime mortgage crisis, Centro's lenders simply refused to extend new loans. The company had the assets. It had the cash flow. What it did not have was the ability to meet its near-term obligations, and in financial markets, liquidity trumps solvency every time. A company can be theoretically solvent — its assets worth more than its debts — and still die if it cannot pay the bills that come due this week.

What followed was years of corporate agony. Centro posted a $1.8 billion loss in 2008. Emergency capital raises diluted existing shareholders into near-oblivion. Debt restructuring negotiations dragged on with dozens of lenders across multiple jurisdictions. The company's US portfolio — those 680-plus shopping centers that were supposed to be the growth engine — sat in a kind of financial purgatory, their valuations frozen, their management distracted by survival rather than operations.

The human toll was significant. Eight executives and directors faced legal proceedings from the Australian Securities and Investments Commission. The Federal Court of Australia found in June 2011 that they had breached the Corporations Act by failing to disclose approximately $2 billion in liabilities that were incorrectly classified as non-current, along with $1.75 billion in short-term guarantee obligations that went undisclosed entirely. Former CEO Andrew Scott received a fine of just $30,000 and was not disqualified from serving as a director — a penalty so light that it sparked a national debate about whether Australia's corporate governance enforcement had any teeth.

A $200 million class action settlement was eventually reached in 2012, funded by Centro entities, auditor PricewaterhouseCoopers (which contributed $67 million and acknowledged deficiencies in its audit work), and insurance proceeds. Approximately 5,000 retail investors were represented, though institutional investors received the bulk of the payout.

The timeline of Centro's unwinding stretched across several painful years. After the initial shock in December 2007, the company spent 2008 through 2010 in a state of managed decline — selling assets where it could find buyers, negotiating with lenders to extend maturities, and watching its stock price hover near penny-stock levels. The Australian operations were eventually restructured and merged into what became Vicinity Centres, one of Australia's largest retail REITs today. But the US portfolio — the engine of Centro's growth ambitions — needed to be divested entirely. The Australian parent simply could not manage a portfolio of nearly 600 American shopping centers while fighting for its own survival on the other side of the Pacific.

The lesson of Centro is timeless and applies far beyond real estate: maturity mismatches kill companies. It does not matter how good the underlying assets are if the financing structure cannot survive a credit contraction. Centro's shopping centers were still generating rent, still attracting shoppers, still anchored by grocery stores. The business was fine. The balance sheet was fatal. This distinction — between the health of the operating business and the viability of the capital structure — would echo throughout Brixmor's subsequent history. It was a distinction that Centro's management failed to understand and that Brixmor's later management would obsess over. And it was precisely this gap between operating value and market price that caught the attention of a firm that had built its entire reputation on buying distressed assets from overleveraged sellers.

V. Enter Blackstone: The 2011 Mega-Deal

In the aftermath of the financial crisis, while most investors were still running from anything associated with real estate, Blackstone Group was doing what Blackstone does best: buying fear. The firm's real estate division, led by veterans who had spent the crisis cataloging distressed opportunities, identified Centro's US portfolio as one of the most compelling risk-reward propositions in the market. Here were hundreds of shopping centers — many grocery-anchored, many in solid demographic locations — available at a massive discount to replacement cost, from a seller with absolutely no negotiating leverage.

The thesis was characteristically Blackstonian in its simplicity: necessity retail was not going away. Americans were still going to buy groceries, get haircuts, visit the dentist, and drop off dry cleaning. The properties generating that revenue were trading at distressed prices not because the underlying business was broken, but because the previous owner's capital structure had been broken.

This is the essence of distressed investing — and Blackstone had mastered it. The firm understood that asset value and entity value can diverge dramatically in financial distress. Centro's shopping centers were still collecting rent from grocery stores, still drawing foot traffic, still generating cash flow. But Centro's equity was worthless because the debt was unpayable. If Blackstone could acquire the assets, clean up the balance sheet, professionalize the management, and invest in the properties, the value creation could be enormous. The key insight was that the distress was in the capital structure, not in the real estate.

In 2011, Blackstone Real Estate Partners VI completed the acquisition of Centro's entire US portfolio for approximately $9.4 billion, including the assumption of debt. The deal closed on June 29, 2011, and delivered to Blackstone 588 shopping centers encompassing roughly 92 million square feet — making the new entity the second-largest owner of community and neighborhood shopping centers in the United States. It was one of the largest real estate transactions since the financial crisis and a defining moment in Blackstone's emergence as the world's dominant real estate private equity firm.

On September 28, 2011, the entity was rebranded as Brixmor Property Group. The name was entirely new — a deliberate break from the Centro association. "Brix" evoked bricks, building, foundations. "Mor" suggested more — more value, more growth, more potential. It was the kind of corporate naming exercise that consultants charge millions for and that nobody outside of investor presentations ever thinks about again.

What mattered far more than the name was what Blackstone did with the properties. The operational playbook was aggressive and methodical. Blackstone installed professional management teams with deep REIT experience. They launched a capital investment program targeting more than 276 properties that had been starved of maintenance capital during Centro's years of financial distress — upgrading facades, improving landscaping, repaving parking lots, modernizing signage. They began the process of remerchandising the tenant base, replacing weaker tenants with stronger national and regional chains. They restructured the debt, converting Centro's chaotic web of obligations into a cleaner, more manageable capital structure.

Perhaps most importantly, Blackstone began sorting the portfolio into keepers and disposables. Not all 588 shopping centers were created equal. Some were well-located, grocery-anchored properties in growing suburban markets with strong demographics. Others were tired strip malls in declining small towns with limited growth potential. Blackstone understood that the path to maximum value creation ran through concentration: keep the best, improve them, and sell the rest. This portfolio triage would become even more aggressive under subsequent management, but the strategic logic was established from the beginning.

The early wins were tangible. Occupancy rates stabilized and began to climb. Rent collections improved as stronger tenants replaced weaker ones. Property-level net operating income grew as capital investments attracted better tenants willing to pay higher rents. The physical transformation was visible: faded facades got fresh paint, cracked parking lots were repaved, dated signage was modernized, and outdated landscaping was replaced. These were not glamorous improvements, but they signaled to tenants that the ownership was serious, that capital was being deployed, and that the properties had a future. In shopping center real estate, perception matters — a tenant deciding between two comparable locations will choose the one where the landlord is clearly investing in the property, because investment signals stability, which signals foot traffic, which signals revenue.

Blackstone also consolidated the management structure. Centro's US operations had been run from Australia, with all the inefficiencies and communication challenges that implied. Blackstone established a US-based management team with regional expertise, giving local operators the authority and resources to make decisions quickly. This operational decentralization, combined with centralized capital allocation and strategic direction, created a management model that balanced local knowledge with institutional discipline.

Within two years, Blackstone had transformed a distressed collection of neglected shopping centers into a credible REIT platform — and they were ready to take it public.

VI. The 2013 IPO: Taking Brixmor Public

On October 29, 2013, Brixmor Property Group priced its initial public offering at $20 per share, raising $948.8 million in gross proceeds including the full exercise of the underwriters' overallotment option. Joint bookrunners included Bank of America Merrill Lynch, Citigroup, JP Morgan, and Wells Fargo Securities. The stock climbed two percent on its first day of trading — a modest but reassuring debut.

The IPO pitch was compelling in its clarity. Brixmor was positioned as the largest wholly owned portfolio of grocery-anchored community and neighborhood shopping centers in the United States. At IPO, the portfolio comprised 558 centers. The investment thesis centered on defensive, necessity-based retail: these are not the places where Americans buy luxury handbags — these are the places where Americans buy milk. The demographic profiles of Brixmor's trade areas were solid, with average household incomes and population densities that supported stable demand. And as a REIT, the company would distribute the vast majority of its taxable income as dividends, giving investors a steady income stream backed by physical real estate.

For readers unfamiliar with the REIT structure, it is worth a brief explanation because it fundamentally shapes how companies like Brixmor operate and how investors should think about them. A Real Estate Investment Trust is a company that owns, operates, or finances income-producing real estate. In exchange for distributing at least 90 percent of taxable income to shareholders as dividends, REITs pay no corporate income tax. This pass-through structure makes REITs essentially a way for individual investors to own a piece of large-scale commercial real estate — something that would otherwise be inaccessible — and receive the rental income generated by those properties.

The trade-off is significant: because REITs must distribute the vast majority of their income, they cannot retain earnings to fund growth the way a typical corporation can. Instead, they fund acquisitions and development through a combination of debt and periodic equity issuances. This makes REITs particularly sensitive to capital markets conditions — access to cheap debt and the ability to raise equity at attractive prices are critical enablers of growth. It also means that REIT dividends are not optional — they are structural, which provides income certainty for investors but limits management's flexibility.

The REIT sector was hot in late 2013. The Federal Reserve's zero-interest-rate policy had pushed yield-hungry investors into dividend-paying equities, and REITs were among the primary beneficiaries. But cracks were already appearing in the retail landscape. Amazon's revenue had more than doubled over the prior four years. E-commerce was beginning to chip away at physical retail's dominance. The smart money was starting to distinguish between different types of retail exposure, and the question of which retail real estate would survive the digital transition was becoming more urgent with each passing quarter.

Blackstone retained a majority stake after the IPO, with affiliated directors maintaining board seats. Net proceeds of roughly $891 million went primarily to pay down Brixmor's unsecured credit facility — a responsible use of capital that reduced leverage and improved the balance sheet. The management team installed by Blackstone was led by CEO Michael Carroll and CFO Michael Pappagallo, both experienced real estate executives tasked with running the newly public company.

For investors, the unspoken tension was clear: Blackstone was a financial sponsor, not a permanent owner. The IPO was not the end of the Blackstone story — it was the beginning of the exit. Every secondary offering would create selling pressure on the stock. Every board decision would carry the question of whether it served long-term shareholders or Blackstone's exit timeline.

This sponsor overhang is a familiar dynamic in private-equity-to-public-company transitions, and it creates a specific set of challenges for public market investors. When a PE firm holds a majority stake, the stock trades with a structural discount because the market anticipates future selling. The PE firm is not buying more stock — it is selling. That knowledge depresses the stock price in a way that has nothing to do with the underlying business. For Brixmor, this overhang would persist for nearly three years until Blackstone's full departure.

There was an additional, subtler tension embedded in the governance structure. Blackstone's representatives sat on the board, giving the sponsor effective control over major strategic decisions. Was the company being managed for long-term shareholder value, or was it being managed to maximize Blackstone's exit price? In practice, these objectives often overlap, but not always. Decisions about capital investment, dividend policy, and strategic direction can look very different depending on whether the decision-maker's horizon is three years (a PE fund's remaining life) or thirty years (a long-term shareholder's perspective). This tension would persist until Blackstone's departure — and in the meantime, far more consequential storms were gathering, both for the retail industry at large and, more immediately, within Brixmor's own executive suite.

VII. Storm Clouds: The Retail Apocalypse and the Accounting Scandal

The years between 2014 and 2018 brought a convergence of crises that would have destroyed a lesser company. From the outside, the threat was existential: the so-called retail apocalypse, a wave of store closings, tenant bankruptcies, and investor panic that cratered the market capitalization of nearly every publicly traded retail landlord. From the inside, the threat was self-inflicted: an accounting scandal that exposed management fraud and triggered a complete leadership overhaul.

The external pressure came first. Amazon's Prime membership surged past 100 million subscribers. E-commerce penetration of total retail sales climbed relentlessly. The bankruptcy wave accelerated: Sports Authority in 2016, Toys R Us in 2017, Bon-Ton in 2018. At the peak in 2017, more than 12,000 physical stores closed across the United States. The financial press declared the death of brick-and-mortar retail with the certainty usually reserved for obituaries. Headlines screamed about the "retail apocalypse," and investors fled anything with the word "retail" in its description — malls, strip centers, department stores, outlet centers. The sell-off was indiscriminate.

For Brixmor, the pain was real but nuanced. Anchor tenant bankruptcies created dark spaces — empty boxes that generated no rent, required costly re-leasing, and depressed foot traffic to adjacent inline tenants. Re-leasing costs spiked as Brixmor had to offer concessions to attract replacement tenants. Rent growth stalled. The stock price, which had traded as high as the mid-$20s, began a painful decline.

But here is where the distinction between malls and strip centers became critical — and ultimately worth billions. Enclosed malls depended on department store anchors like Sears, JCPenney, and Macy's, all of which were in structural decline. When those anchors closed, malls lost their traffic generators, and the co-tenancy clauses in other tenants' leases allowed them to reduce rent or exit entirely. It was a death spiral. Strip centers, by contrast, depended on grocery stores — and grocery stores were not going bankrupt. Americans were not buying their produce on Amazon (not yet, at least, and still not in meaningful volumes). The traffic engine of the strip center remained intact even as the traffic engine of the mall was failing.

Then came the internal crisis. In February 2016, a whistleblower complaint triggered an audit committee investigation that uncovered a troubling pattern of accounting manipulation. From the third quarter of 2013 through the third quarter of 2015 — essentially from the moment of the IPO onward — senior executives had been smoothing Brixmor's same-property net operating income growth rate, a key metric that investors and analysts relied on to assess the company's organic performance. The technique was known internally as "cookie jar" accounting: executives would store reportable income in a reserve account during strong quarters and release it during weaker ones, creating an artificially smooth growth trajectory that consistently hit the company's publicly stated targets.

Four executives resigned simultaneously: CEO Michael Carroll, CFO Michael Pappagallo, Chief Accounting Officer Steven Splain, and Senior Vice President of Accounting Michael Mortimer. The SEC would later formally charge all four with fraud. Brixmor as an entity settled without admitting or denying the allegations, paying a $7 million fine. Criminal charges were filed by the US Attorney's Office for the Southern District of New York in August 2019. In a rare outcome, however, all charges were eventually dismissed — the SEC voluntarily dropped charges against Carroll in July 2021, and prosecutors dropped the remaining cases in 2024, stating they could not prove wrongdoing.

The stock cratered on the disclosure. Investors were now dealing with a company in a hated sector, run by a management team that had just been fired for cooking the books, with a private equity sponsor still looking to exit. It was, by almost any measure, the nadir.

The board moved quickly. In May 2016, Brixmor named James M. Taylor Jr. as CEO and President. Taylor's background was the opposite of a typical REIT operator — he was a capital markets veteran. After starting his career as a senior accountant at Price Waterhouse and practicing corporate securities law at Hunton & Williams, Taylor spent fourteen years at Eastdil Secured, the premier real estate investment bank, where he rose to head the firm's real estate investment banking practice and completed over $100 billion in transactions. He then served as CFO of Federal Realty Investment Trust, one of the most respected retail REITs in the industry. Taylor brought credibility, capital markets sophistication, and an outsider's willingness to make hard decisions. His mandate was clear: rebuild trust, rationalize the portfolio, and prove that Brixmor had a viable future.

Taylor launched what became known internally as "Brixmor 2.0." The strategy was aggressive portfolio optimization: sell the bottom quartile of properties based on anchor sales productivity, rents, and demographics, and reinvest in the remaining higher-quality centers. In 2018 alone, Brixmor sold more than 60 non-core assets for approximately $1 billion, exceeding the planned disposition volume by thirty to forty percent. The company sold nearly fifteen percent of its entire portfolio over an eighteen-month period. The goal was to shrink from roughly 425 properties in 150 markets to about 400 properties in 100 markets — fewer, better assets in stronger locations.

The combination of the accounting scandal and the retail apocalypse created a toxic cocktail for the stock. Brixmor was, for a period, virtually un-investable for many institutional investors. Governance-focused funds would not touch a company that had just fired its management for cooking the books. Retail-skeptic funds would not touch any company with the word "shopping" in its description. And momentum-driven funds saw nothing but a falling stock price with no catalyst for reversal. The trading volume thinned, the analyst coverage became more skeptical, and the stock languished.

But the narrative and the reality were diverging in ways that would ultimately prove consequential. While investors priced the stock as if all physical retail was dying, the actual operating performance of well-located, grocery-anchored strip centers told a different story. Occupancy held up better than expected. Rent collection remained stable. The grocery anchors kept generating foot traffic, and the inline tenants that survived were, in many cases, stronger and more creditworthy than the ones they replaced. The necessity retail thesis was holding. The question was whether the market would ever recognize it — and whether new management could execute a turnaround before investor patience ran out entirely.

VIII. The Blackstone Exit and True Independence

Amid the portfolio transformation, a quieter but strategically important transition was also completing: Blackstone's exit from the company. The private equity giant had been systematically reducing its stake since the IPO. In March and April 2015, Blackstone sold roughly 26 million shares through secondary offerings, reducing its ownership to approximately forty-nine percent. Then in August 2016 — just months after the accounting scandal and the management shake-up — Blackstone commenced a secondary offering of 42.4 million shares and distributed its remaining 455,585 shares to its partners, fully exiting its position in Brixmor.

The timing was notable and, from Blackstone's perspective, likely frustrating. The firm completed its exit at what was close to the stock's low point, with the shares weighed down by both the accounting scandal and the broader retail apocalypse narrative. The returns on the Brixmor investment were likely lower than the firm had modeled when it purchased the Centro portfolio in 2011.

But the exit was strategically necessary. Blackstone operates on fund timelines — its limited partners (pension funds, sovereign wealth funds, university endowments) expect capital returned within defined periods, typically eight to twelve years. Fund VI needed to close out its positions. The Centro acquisition had been made five years earlier, the IPO had occurred nearly three years prior, and the fund was approaching the end of its natural life cycle. In private equity, you cannot hold forever, even when selling at the bottom feels painful. The fund structure demands exits, regardless of market conditions.

For Brixmor, Blackstone's departure was liberating. The sponsor overhang — the perpetual expectation of another secondary offering creating selling pressure — was gone. The board was free to refresh itself with truly independent directors. Management was now fully accountable to public shareholders rather than serving two masters. And the company's strategic decisions could be made on their own merits rather than filtered through the lens of a sponsor's exit timeline.

Blackstone later acknowledged that it had served as "an invaluable sponsor since 2011, investing in the platform and laying the strong foundation for the business." That was generous but accurate. Blackstone had rescued the portfolio from distress, professionalized management, invested capital in properties, and created the institutional framework for a public company. The accounting scandal was a serious blemish, but it was a failure of the individuals Blackstone installed, not of the underlying business strategy.

The Blackstone chapter of the Brixmor story is worth reflecting on from a private equity perspective. The playbook — buy distressed assets cheaply, improve operations, clean up the balance sheet, take public, exit through secondary offerings — is the canonical PE value creation model. In Brixmor's case, it worked as designed, even if the absolute returns were likely below initial projections given the accounting scandal and sector-wide headwinds. For Blackstone, the deal reinforced the firm's reputation as the premier buyer of distressed real estate. For Brixmor, the departure of its sponsor meant that the company's destiny was now entirely in its own hands. The new investor base would be composed of public market institutions — pension funds, mutual funds, ETFs — with different return expectations and governance demands than a private equity sponsor. The company's stock would live or die on quarterly earnings calls, analyst ratings, and the daily judgment of the public markets. With Blackstone gone and Taylor at the helm, Brixmor was truly independent for the first time — and it was about to face its greatest test.

IX. COVID-19: The Ultimate Stress Test

In March 2020, when state and local governments across the United States began issuing shutdown orders in response to the COVID-19 pandemic, the prevailing assumption among investors was that retail real estate was finished. Shopping center REITs cratered. Brixmor's stock plummeted to approximately $8 per share — a decline of more than sixty percent from pre-pandemic levels. The question was existential: if tenants cannot open their stores, they cannot pay rent. If they cannot pay rent, landlords cannot service their debt. If landlords cannot service their debt, the entire capital structure unwinds.

Rent collection became the single most important metric in real estate, tracked with an obsessiveness usually reserved for election returns. REIT management teams that had previously reported financial results quarterly were suddenly providing monthly — sometimes weekly — updates on rent collection percentages. Analysts built spreadsheet models that tracked the delta between each company's collection rates, and basis points of collection improvement drove stock price moves.

In the second quarter of 2020, Brixmor collected just 76.6 percent of billed base rent — a terrifying number for a business built on predictable cash flows. To put that in perspective, Brixmor's pre-pandemic collection rate was consistently above 98 percent. A drop to 76.6 percent meant that nearly a quarter of billed rent was simply not coming in. But the data had a critical nuance that told the real story: among essential tenants — groceries, pharmacies, medical services, hardware stores, pet supplies — collection rates were 98.1 percent. Among hybrid tenants that could partially operate, collection was 78 percent. The shortfall was concentrated among non-essential retailers who had been forced to close entirely by government mandate.

This is where Brixmor's portfolio composition proved decisive. With approximately seventy to eighty percent of its centers anchored by grocery stores, Brixmor's properties were classified as essential and remained open throughout the shutdowns. Grocery stores experienced a surge in demand as Americans stockpiled pantry staples and shifted from restaurant dining to home cooking. The parking lots that had seemed like a symbol of suburban monotony became drive-through COVID testing sites — Brixmor partnered with Collection Sites to launch testing operations at 340 locations across the country.

Management's response combined pragmatism with strategic opportunism. The "BrixAssist" program provided support to small shop tenants, many of whom had been forced to close temporarily. These were the local pizza shop owners, the independent nail salon operators, the family-run dry cleaners — businesses with thin cash reserves and limited access to capital markets. Losing them to permanent closure would have been devastating not just for the tenants themselves, but for Brixmor's portfolio, because these small shop tenants paid the highest rents per square foot and were the hardest to replace.

Brixmor worked with tenants on rent deferrals, lease modifications, and creative solutions like licensing agreements that allowed restaurants and retailers to extend their operations into common areas at no additional cost. The outdoor dining setups that became ubiquitous during the pandemic found a natural home in strip center parking lots, where the open-air configuration made the transition effortless compared to enclosed malls or urban storefronts.

On the balance sheet, the company drew on its revolving credit facility and maintained over $550 million in cash with more than $600 million in additional borrowing capacity — a liquidity cushion that ensured Brixmor could weather an extended downturn without tripping covenants or facing a Centro-style liquidity crisis. The contrast with Centro was not lost on management or investors. Centro died because it could not refinance short-term debt during a market disruption. Brixmor entered the pandemic with exactly the kind of balance sheet that Centro never had — one designed to absorb shocks rather than amplify them.

By the fourth quarter of 2020, rent collection had recovered to 92.7 percent — a remarkable trajectory from the depths of Q2. The speed of the recovery surprised even optimistic observers and demonstrated a fundamental truth about necessity retail: when governments said "you can open again," the customers were already waiting. The demand had not disappeared — it had merely been suppressed by government mandate.

The pandemic had accomplished something that years of retail apocalypse hand-wringing had not: it definitively sorted the winners from the losers in physical retail. Weak tenants — those already teetering on the edge of viability — were pushed into bankruptcy or lease termination. Stronger tenants survived and, in many cases, emerged with better economics as they renegotiated leases in adjacent spaces or expanded into locations vacated by weaker competitors. For Brixmor, this accelerated Darwinism was a silver lining: the pandemic cleared out marginal tenants and created opportunities to remerchandise with stronger, more creditworthy replacements paying higher rents.

The contrast with enclosed malls was stark. Mall-dependent REITs faced significantly worse rent collection rates and a slower recovery, because their tenant bases were concentrated in discretionary categories — apparel, department stores, entertainment — that were either shut down entirely or saw demand permanently impaired. Brixmor's grocery anchors, by contrast, were not just open — they were busier than ever. The pandemic had drawn a bright red line between necessity retail and everything else, and Brixmor was on the right side of that line.

The stock recovery that followed validated the necessity retail thesis in real time. As investors realized that grocery-anchored strip centers were not just surviving the pandemic but actively benefiting from changed consumer behavior — more cooking at home, more local shopping, more demand for essential services — Brixmor shares began a steady climb from their pandemic lows. The path from roughly $8 to recovery was not linear, but it was directional. The company that many had left for dead had proven its resilience in the most hostile operating environment imaginable. And it had done so while maintaining its dividend (though at reduced levels during the worst of the crisis) and avoiding the covenant violations and emergency capital raises that had destroyed Centro a decade earlier. The lesson of the pandemic for Brixmor shareholders was not just that the thesis worked — it was that the balance sheet discipline implemented after Centro's collapse had created a company that could absorb shocks without existential risk.

X. The Great Reinvention: Densification and Mixed-Use

If the pandemic validated what Brixmor was, the post-pandemic era revealed what it could become. Starting around 2020 and accelerating through 2023 and beyond, Brixmor embraced a strategic transformation that went beyond simply being a better shopping center company. The vision was to become something fundamentally different: a platform for suburban mixed-use development, leveraging the company's most underappreciated asset — not the buildings, but the land beneath them.

The insight was hiding in plain sight. Brixmor's shopping centers sat on large parcels of land in established suburban neighborhoods, surrounded by residential density, with excellent road access and visibility. The centers themselves typically used only a fraction of their total land area for buildings — the rest was parking lots designed for peak holiday shopping volumes that sat mostly empty the other 350 days of the year. In many of Brixmor's markets, those parking lots occupied land that was now worth far more as residential or mixed-use development sites than as surface parking.

Several macro trends converged to make this transformation viable. America's housing shortage had reached crisis proportions, and municipalities were increasingly willing to rezone commercial land for residential use. Urban planning philosophy had shifted toward mixed-use, walkable development — the very model that Brixmor's well-located suburban sites could support. And the economics were compelling: by ground-leasing portions of parking lots to multifamily or life sciences developers, Brixmor could generate high-margin income streams without the capital intensity of building the projects themselves, while simultaneously increasing the residential density around their retail centers and creating a virtuous cycle of more residents driving more retail traffic.

The reinvestment pipeline told the story of this transformation in concrete terms. As of early 2025, Brixmor had 37 reinvestment projects in process with an aggregate estimated cost of roughly $391 million and expected incremental NOI yields of approximately ten percent. These ranged from anchor space repositionings — subdividing large vacant boxes into multiple smaller tenant spaces — to outparcel developments yielding an extraordinary twenty-three percent return on invested capital, to major redevelopments that would fundamentally reimagine entire centers.

The most ambitious example was University Mall in Davis, California, where Brixmor proposed converting an 8.25-acre parcel with roughly 104,000 square feet of single-story retail into approximately 808,000 square feet of mixed-use development, including 560,000 square feet of residential and retail space. The fiscal analysis showed that the redevelopment only made financial sense when the new buildings were at least four stories tall — a dramatic illustration of how significantly the highest-and-best use of these sites had shifted from single-story retail to multi-story mixed-use.

In full-year 2025, Brixmor stabilized $183.3 million of reinvestment projects at roughly ten percent incremental NOI yields. This reinvestment activity was not just generating returns — it was transforming the character of the portfolio itself, turning generic strip centers into mixed-use nodes that combined retail, dining, services, and increasingly, housing. The company had begun describing its vision as transforming "shopping centers into town centers" — a phrase that captured both the physical evolution and the strategic ambition.

Another important element of the reinvestment program involved outparcel development — building new small structures on the edges of existing parking lots, typically for drive-through restaurants, coffee shops, or bank branches. These projects were relatively small in absolute dollar terms but generated extraordinary returns, with expected yields of roughly twenty-three percent on invested capital. The reason is simple: Brixmor already owns the land, already has the infrastructure (roads, utilities, drainage), and already has the traffic. Building a new pad for a Chick-fil-A or a Chase Bank branch is essentially monetizing idle land with minimal incremental cost. It is the real estate equivalent of finding twenty-dollar bills under the couch cushions.

Technology played an increasingly important role in this evolution. Brixmor deployed proprietary data analytics to optimize tenant mix decisions, using granular consumer behavior data to identify which tenants would generate the most traffic and the highest rents in each specific location. This data-driven approach to leasing represented a meaningful operational advantage: rather than relying on instinct and relationships alone, Brixmor could match tenants to locations with a precision that smaller landlords could not replicate. The analytics also informed acquisition decisions — helping the company identify properties where the gap between current rents and market rents was widest, signaling the greatest opportunity for remerchandising gains.

For investors, the densification strategy represented hidden optionality. The market valued Brixmor based on its current NOI — the rent it collected from existing tenants. But the land beneath those tenants, in many cases, was worth substantially more than the capitalized value of the current cash flows. Every parking lot was a potential development site. Every single-story building was a potential four-story mixed-use project. This embedded optionality did not show up in traditional REIT valuation metrics, and the market was only beginning to price it in.

XI. The New Competitive Landscape and Tenant Evolution

Walk through a Brixmor shopping center in 2026 and the tenant mix looks strikingly different from what you would have found a decade ago. The changes tell the story of how physical retail adapted, evolved, and in many cases, found renewed purpose.

The dominant tenants are off-price retailers — TJX Companies (TJ Maxx, Marshalls, HomeGoods), Ross Stores, Burlington — whose treasure-hunt shopping experience is inherently physical and nearly impossible to replicate online. You will find dollar stores, whose low price points make e-commerce delivery economics unworkable. You will find fitness centers, urgent care clinics, dental offices, veterinary hospitals, and a proliferating array of service-based businesses that require physical presence by definition. You will find restaurants — fast casual, full service, and quick service — that have become the new traffic anchors, driving evening and weekend visits that grocery stores alone cannot generate.

The most counterintuitive development has been the "clicks-to-bricks" reversal. After years of physical retailers losing share to e-commerce, the flow began running in both directions. Digitally native brands — companies born online — discovered that physical stores were essential for customer acquisition, returns processing, and brand experience. The math was surprisingly simple: digital customer acquisition costs had risen dramatically as Facebook and Google ad auctions became more competitive. A physical store in a high-traffic shopping center could acquire customers at a lower effective cost than online advertising, while simultaneously providing a returns hub, a brand showroom, and a fulfillment point.

Opening a physical location in a well-trafficked shopping center proved to be a more cost-effective customer acquisition channel than digital advertising for many direct-to-consumer brands. The physical store, once declared dead, turned out to be the cure for rising customer acquisition costs in the digital economy. This reversal expanded Brixmor's addressable tenant universe at precisely the moment when traditional tenants were contracting — a fortunate timing that helped offset the losses from retail apocalypse-era bankruptcies.

Brixmor's tenant mix evolution reflected these dynamics. The company systematically reduced its exposure to categories vulnerable to e-commerce disruption — traditional apparel, electronics, books — and increased its exposure to categories that require physical presence. Today, the top tenants include TJX Companies, Kroger, Publix Super Markets, Ross Stores, and Sprouts Farmers Market. More than 5,000 tenants occupy Brixmor's centers, and the company describes its tenant credit quality as the strongest in its history.

The grocery wars have been particularly beneficial. Kroger, Albertsons, Publix, Sprouts, and other grocery chains continued to expand their store counts and invest in existing locations, driven by competitive pressure from each other and from new entrants like Amazon Fresh and specialty grocers. Every new grocery store opening or renovation in a Brixmor center reinforced the traffic engine that powered the entire property. Dining has become equally important — restaurants now function as evening and weekend anchors, complementing the grocery store's daytime and after-work traffic patterns. A well-merchandised center might draw a shopper to Kroger at 5 PM, who grabs a coffee at Starbucks, picks up dry cleaning, and stops at Chipotle for dinner on the way out.

Perhaps the most significant shift, however, has been the blurring of the line between anchor and inline tenant. Traditionally, the grocery store was the traffic anchor and everything else was secondary. Today, a well-merchandised Brixmor center might have three or four traffic generators: the grocery store for weekday shoppers, a fitness center drawing members six days a week, a popular restaurant driving evening traffic, and an urgent care clinic providing a steady stream of patients — and their accompanying retail spending — throughout the day. This multi-anchor model makes the center more resilient because the failure of any single tenant does not collapse the entire traffic ecosystem.

Looking forward, there is growing speculation about whether shopping centers could serve as logistics nodes for last-mile delivery. The same attributes that make strip centers good for retail — proximity to residential density, easy road access, ample parking — also make them attractive for fulfillment operations. Some retailers already use store locations as micro-fulfillment centers for online orders. The potential for Brixmor's centers to host delivery hubs, curbside pickup operations, or even dark stores represents another layer of optionality that the market has yet to fully value. Rather than e-commerce being the enemy of the strip center, the two may be converging — physical retail locations becoming the distribution infrastructure that e-commerce needs to achieve same-day delivery economics.

XII. Business Model Deep Dive and Modern Operations

Brixmor's current portfolio, as of year-end 2025, comprises 348 shopping centers containing approximately 63 million square feet of gross leasable area. The average center is roughly 180,000 square feet — about the size of four football fields. The geographic footprint concentrates in the top 50 metropolitan statistical areas, with the largest state exposures in Florida at fourteen percent of annualized base rent, Texas at nearly twelve percent, and California at close to twelve percent. This Sun Belt concentration reflects both the company's deliberate strategy and the demographic realities of where population and income growth have been strongest.

The leasing machine is the operational heartbeat of the business. Brixmor signs more than 1,500 leases annually — a pace that requires institutional-grade systems, deep tenant relationships, and the ability to process enormous volumes of real estate transactions simultaneously. Leasing spreads — the difference between the rent on a new or renewed lease and the rent on the expiring lease it replaces — are a critical health indicator. Positive leasing spreads mean the company is consistently extracting higher rents from its portfolio, evidence of demand for its locations and pricing power relative to tenants.

The occupancy picture tells a story of steady improvement through disciplined execution. Total leased occupancy stood at 95.1 percent at year-end 2025. Anchor occupancy was even higher at 96.6 percent, while small shop occupancy reached a record 92.2 percent. These numbers are worth pausing on. A leased occupancy of 95 percent means that of Brixmor's 63 million square feet, only about three million square feet are vacant. In a portfolio of 348 centers, that is a remarkably thin layer of available space, and it gives the company pricing power when negotiating new leases.

Average base rent was $18.77 per square foot — a number that reflects the strip center's inherently lower rent profile compared to enclosed malls (which can command $40 to $80 per square foot in premium locations) or lifestyle centers, but also one that has been steadily increasing as Brixmor remerchandises with stronger tenants. The lower absolute rent level is actually a competitive advantage: it makes occupancy more sustainable for tenants during economic downturns and reduces the incentive for tenants to seek cheaper alternatives. A retailer paying $18 per square foot at a well-trafficked Brixmor center is unlikely to relocate to save two dollars per square foot at a less-trafficked competitor — the math simply does not work.

Capital allocation follows a clear hierarchy that reveals management's priorities. First priority is reinvestment in existing properties — the redevelopment and densification pipeline discussed earlier, which generates the highest risk-adjusted returns because Brixmor is investing in assets it already knows intimately. When a company can earn ten percent incremental NOI yields by repositioning an anchor space it has operated for twenty years, that is a far lower-risk proposition than buying a new property in an unfamiliar market.

Second is acquisitions, but only of properties that meet strict criteria for location quality, demographics, and remerchandising potential. The acquisition strategy has shifted meaningfully under the Taylor and Finnegan regimes. Rather than the Centro-era approach of buying in bulk at low prices, Brixmor now focuses on surgical acquisitions — individual centers in target markets where the company sees specific value-creation opportunities through remerchandising, densification, or operational improvement. In 2025, Brixmor completed $416.8 million in acquisitions and $296.5 million in dispositions — a net investment posture that reflected management's confidence in the portfolio's trajectory while maintaining discipline about which assets belong in the portfolio and which do not.

Third is maintaining balance sheet strength, which provides both defensive resilience and the capacity to act opportunistically during market dislocations. The experience of Centro's collapse — and the fact that Brixmor literally exists because of another company's over-leveraging — makes balance sheet management a cultural priority, not just a financial one.

The balance sheet itself reflects the lessons learned from Centro's collapse. One hundred percent of Brixmor's debt is fixed-rate — eliminating the interest rate risk that has plagued other REITs in the rising-rate environment. The weighted average debt maturity is 4.8 years, with an average interest rate of 4.2 percent. Net debt to adjusted EBITDA stands at approximately 5.5 to 5.7 times — comfortably within the investment-grade range. Available liquidity totals $1.63 billion between cash on hand and credit facility capacity. In 2025, the company issued $800 million of senior notes, demonstrating continued strong access to capital markets. This is a balance sheet designed to survive crises, not one designed to maximize leverage for short-term returns. The ghost of Centro haunts every capital structure decision, and that is entirely intentional.

The CEO transition at the start of 2026 brought Brian T. Finnegan to the top job, succeeding the retiring James Taylor. Finnegan grew up in Roxborough, Pennsylvania, and has spent his entire career in shopping center real estate, joining Brixmor more than two decades ago. He rose through the ranks in a way that tells you exactly what kind of leader he is: Executive Vice President of Leasing, then Chief Revenue Officer, then Chief Operating Officer, then President — each role adding another layer of operational mastery over the portfolio. He also served as interim CEO during two periods when Taylor was on medical leave, proving he could handle the full scope of the job under pressure. Finnegan serves as Vice Chair of the ICSC Foundation Board of Directors, reflecting his standing in the broader shopping center industry.

Where Taylor was a capital markets architect brought in from outside to rebuild credibility — a man who had completed over $100 billion in transactions at Eastdil Secured and served as CFO of Federal Realty — Finnegan is a lifer who knows every market, many of the tenants by first name, and the operational nuances of individual properties. The transition in leadership style is itself a signal about where Brixmor stands: the rebuilding phase is complete, the balance sheet is repaired, the portfolio is pruned, and the company is entering an execution phase where deep operational knowledge matters more than external credibility. Taylor built the plane. Finnegan flies it.

The CFO role has also transitioned. Angela Aman, who served as President, CFO, and Treasurer, departed in January 2024 to become CEO of Kilroy Realty Corporation — a move that underscored the quality of Brixmor's management bench. Steven T. Gallagher, who had served as Chief Accounting Officer since 2017, stepped into the CFO role. The fact that Brixmor's former CFO was recruited to run another major REIT speaks to the caliber of talent that the post-scandal rebuild attracted.

XIII. Playbook: Business and Investing Lessons

Every great business story contains lessons that extend beyond the specific company and industry. Brixmor's journey from distressed Centro asset to thriving mixed-use platform distills into a set of principles that apply to investing, management, and competitive strategy across sectors.

The first and most fundamental: capital structure kills, not business quality. Centro's shopping centers did not stop generating rent during the financial crisis. Tenants were still shopping, leases were still in force, cash flow was still arriving. What killed Centro was a maturity mismatch — funding long-duration assets with short-duration liabilities. Brixmor learned this lesson so thoroughly that it now maintains 100 percent fixed-rate debt, a liquidity buffer exceeding $1.6 billion, and a weighted average debt maturity approaching five years. The lesson extends to every levered business: the margin of safety lives in the liability structure, not in the income statement.

The second lesson: narratives and reality can diverge for years. Between 2015 and 2020, the consensus narrative was that physical retail was dying and all retail real estate was worthless. This narrative was partially correct — enclosed malls with department store anchors were indeed in structural decline. But it was also wildly overapplied. Grocery-anchored strip centers serving necessity retail needs were not dying. They were adapting, evolving, and in many cases, gaining market share as weaker competitors exited. The market priced Brixmor as if it were a dying mall company. It was not. For patient investors, the divergence between narrative and reality was an opportunity. For those who sold at the bottom, it was a permanent loss.

Third: asset quality is destiny. The most consequential decision in Brixmor's post-Blackstone history was the aggressive portfolio culling executed under Jim Taylor. By selling more than 200 lower-quality properties and concentrating the portfolio in the top metropolitan areas with the strongest demographics, Taylor ensured that Brixmor's remaining centers would be the survivors — the A and B locations in markets where demand for physical retail space remained robust. The C and D locations in declining secondary markets were someone else's problem. In real estate, as in most businesses, the Pareto principle applies with punishing clarity: eighty percent of value comes from twenty percent of assets.

Fourth: real estate is optionality. The most underappreciated aspect of Brixmor's value proposition is not the current income stream — it is the land. Every shopping center sits on a parcel of land that was purchased decades ago at prices reflecting suburban commercial land values. Today, many of those parcels are in established neighborhoods where residential demand far exceeds supply, zoning is evolving to permit higher density, and the highest-and-best use of the land may be multi-story mixed-use development rather than single-story retail. The income stream is the dividend. The land is the call option.

Fifth: the myth versus reality test. The consensus narrative about retail real estate from 2015 to 2020 was that physical retail was dying and shopping center REITs were value traps. The reality was far more nuanced. Enclosed malls with department store anchors were indeed in structural decline. But open-air, grocery-anchored strip centers were adapting, not dying. The market failed to distinguish between these fundamentally different asset classes for years, creating a valuation gap that patient investors could exploit. The lesson is broader: whenever a narrative becomes universally accepted, it is worth asking whether the narrative applies uniformly or whether there are pockets of the condemned sector that are actually thriving. In Brixmor's case, the "all retail is dead" narrative was approximately half right — which made it precisely wrong about the half that mattered.

Finally: patience. This story took fifteen years to play out, from the Centro collapse in 2007 to the validation of the necessity retail thesis through a pandemic and the emergence of the densification strategy. An investor who bought Brixmor at the IPO in 2013 endured an accounting scandal, a retail apocalypse, a pandemic, and a bear market in REITs before arriving at a point where the thesis was largely proven. Real estate is a long-duration asset class, and the investment thesis for real estate companies operates on a correspondingly long timeline. This is not a venture capital story of rapid hypergrowth. It is a story of slow, grinding, occasionally agonizing value creation through operational excellence, capital discipline, and the simple passage of time.

XIV. Strategic Frameworks Analysis

Porter's Five Forces

The competitive dynamics of the open-air shopping center business can be understood through the lens of industry structure, and the analysis reveals a business that is far more defensible than the "retail is dead" narrative would suggest.

The threat of new entrants is low in the traditional sense — virtually no new shopping centers of any scale have been built in the United States since the financial crisis. The barriers are formidable: land in established suburban locations is scarce and expensive, the entitlement process (securing zoning approvals, environmental permits, community support) takes years and costs millions, and construction costs have risen sharply. However, e-commerce represents the ultimate "new entrant" — a substitute channel that does not need land, permits, or parking lots. The physical barriers to entry protect Brixmor's existing centers while the digital channel continues to chip away at physical retail's total addressable market, making the competitive picture more nuanced than a simple "high barriers" conclusion would suggest.

The bargaining power of suppliers is low. Brixmor owns the real estate and outsources construction, maintenance, and property management services from a competitive market of commoditized providers. No single contractor or service provider has meaningful leverage over the company.

The bargaining power of tenants — the buyers in this framework — is moderate to high and has shifted dramatically over the past decade. During the retail apocalypse, tenants gained significant leverage as vacancy rates rose and landlords competed aggressively for occupancy. Quality tenants could demand lower rents, more generous tenant improvement allowances, and favorable lease terms. However, as the market has tightened and Brixmor's occupancy has climbed to record levels, the balance has shifted back toward the landlord in the strongest locations. Centers in high-demographic, supply-constrained markets with strong grocery anchors maintain meaningful pricing power. Centers in weaker markets do not — which is precisely why Brixmor sold them.

The threat of substitutes is the most important force in this analysis, and it is high. E-commerce is an existential substitute for physical retail, and its penetration of total retail sales continues to climb. But the threat is highly category-dependent. Groceries, haircuts, dental visits, fitness, dining, and other necessity and service categories face minimal substitution risk. Apparel, electronics, and general merchandise face severe risk. Brixmor's strategy of concentrating in necessity-retail-heavy categories is a direct response to this force.

Competitive rivalry among open-air shopping center REITs is moderate. The industry is fragmented, with major players including Regency Centers (which focuses on affluent suburban markets and high-quality grocery anchors), Kimco Realty (a close peer in terms of portfolio size and composition), Federal Realty Investment Trust (which pioneered the mixed-use model in premium suburban locations), and several smaller operators like SITE Centers and Retail Opportunity Investments Corp. These companies compete for the same tenants and the same investment capital. When TJX or Ross Stores wants to open a new location in a given market, they will evaluate sites from multiple shopping center REITs, and the competition for that lease comes down to location, co-tenancy, economics, and the landlord's willingness to invest in the space.

Differentiation is possible through location quality, operational excellence, tenant relationships, and strategic vision. Brixmor's advantages include its scale (the largest pure-play portfolio provides efficiency and tenant relationship leverage), its geographic diversity (reducing concentration risk), and its densification strategy, which represents an attempt to differentiate beyond traditional leasing by offering tenants embedded residential density and mixed-use environments that drive traffic in ways competitors may struggle to replicate. The key competitive question is whether Brixmor can maintain and expand its quality advantage — operating the best-located, best-merchandised centers in each of its markets — or whether competitors with more capital or more focused strategies can cherry-pick the most attractive opportunities.

Hamilton Helmer's 7 Powers

The more revealing framework for assessing Brixmor's durable competitive advantage is Hamilton Helmer's 7 Powers, which focuses not on competitive dynamics (the lens Porter provides) but on sustainable sources of differential value creation — what gives a company the ability to earn superior returns over long periods.

Brixmor's strongest power is cornered resource — and specifically, irreplaceable locations. The company's centers occupy land in established suburban neighborhoods where new development is either impossible (no available land), prohibitively expensive, or politically blocked by local opposition. You cannot build a new shopping center next to a Brixmor center in a mature, built-out suburb. The land simply does not exist. This scarcity is increasing as municipalities tighten zoning regulations and communities resist new commercial development. Every year that passes without new supply being added makes Brixmor's existing locations more valuable.

Scale economies provide moderate advantage. A portfolio of 348 centers creates better corporate overhead leverage than a portfolio of fifty — the CEO, CFO, legal team, and technology infrastructure are spread across more properties. Scale also provides negotiating leverage with national tenants who prefer working with a single landlord across multiple markets rather than dealing with dozens of individual property owners. But individual shopping centers compete locally, and the competitive advantage of scale diminishes at the property level.

Network economies are emerging through the densification strategy. As Brixmor adds residential density to its centers, it creates a self-reinforcing system: more residents drive more retail traffic, more retail amenities make the residences more attractive, and the combined mixed-use environment generates higher land values than either use alone. There is also a portfolio-level network effect: national tenants like TJX, Ross Stores, or Sprouts prefer to work with landlords who can offer locations across multiple markets. A retailer planning a ten-store expansion finds it far easier to negotiate a single deal with Brixmor for ten locations than to negotiate individually with ten different landlords. This preference gives large-portfolio REITs an edge in attracting the most desirable tenants — a subtle but meaningful competitive advantage.

Switching costs are moderate to high for tenants. A retailer that has built a customer base at a specific location faces real costs — both financial and in lost customers — from relocating. Lease termination penalties, the cost of building out a new space, and the risk of losing habitual shoppers all create stickiness. For Brixmor, the switching costs are even higher: its locations cannot be replicated.

Branding power is low in the traditional sense — consumers do not choose a shopping center because of the Brixmor name. Nobody has ever said, "Let's go to the Brixmor center" the way they might say, "Let's go to the Apple Store." The brand matters to tenants, though, as a signal of management quality, investment commitment, and operational reliability. National tenants evaluating potential landlords will consider a company's track record and reputation, and Brixmor's brand has improved meaningfully since the Taylor-era reforms.

Process power is medium. Brixmor has developed genuine expertise in leasing velocity, tenant mix optimization, and data-driven asset management. Signing over 1,500 leases annually requires institutional processes and systems that smaller competitors lack. But these capabilities, while valuable, are ultimately replicable by well-run peers with sufficient scale and investment.

The primary moat, then, is the combination of cornered resource and emerging network effects, supported by scale economies and switching costs. These are not overwhelming advantages — a well-capitalized competitor with strong locations could replicate much of what Brixmor does. But the combination, applied consistently across a portfolio of 348 centers in demographically attractive markets, creates a defensible competitive position that is difficult to erode. The moat is not a fortress — it is more like a well-maintained wall that requires ongoing investment and operational excellence to keep it intact.

XV. Bull vs. Bear Case

The Bull Case

The optimistic view on Brixmor begins with the most fundamental force in real estate economics: supply and demand. Virtually no new open-air shopping centers have been built in the United States in over a decade, while population and household formation have continued to grow. The result is a supply-constrained market where well-located centers have genuine pricing power. Brixmor's occupancy at 95.1 percent and record small-shop occupancy at 92.2 percent are evidence that demand for its space exceeds supply.

The necessity retail thesis has been validated by the most severe test imaginable — a global pandemic that shuttered discretionary retail while grocery-anchored centers remained open and essential. The clicks-to-bricks trend provides incremental tenant demand from a source that did not exist a decade ago. Digitally native brands are actively seeking physical retail space, expanding the addressable tenant universe.