Borr Drilling: The Phoenix of the High Seas

I. Introduction: The Contrarian Bet

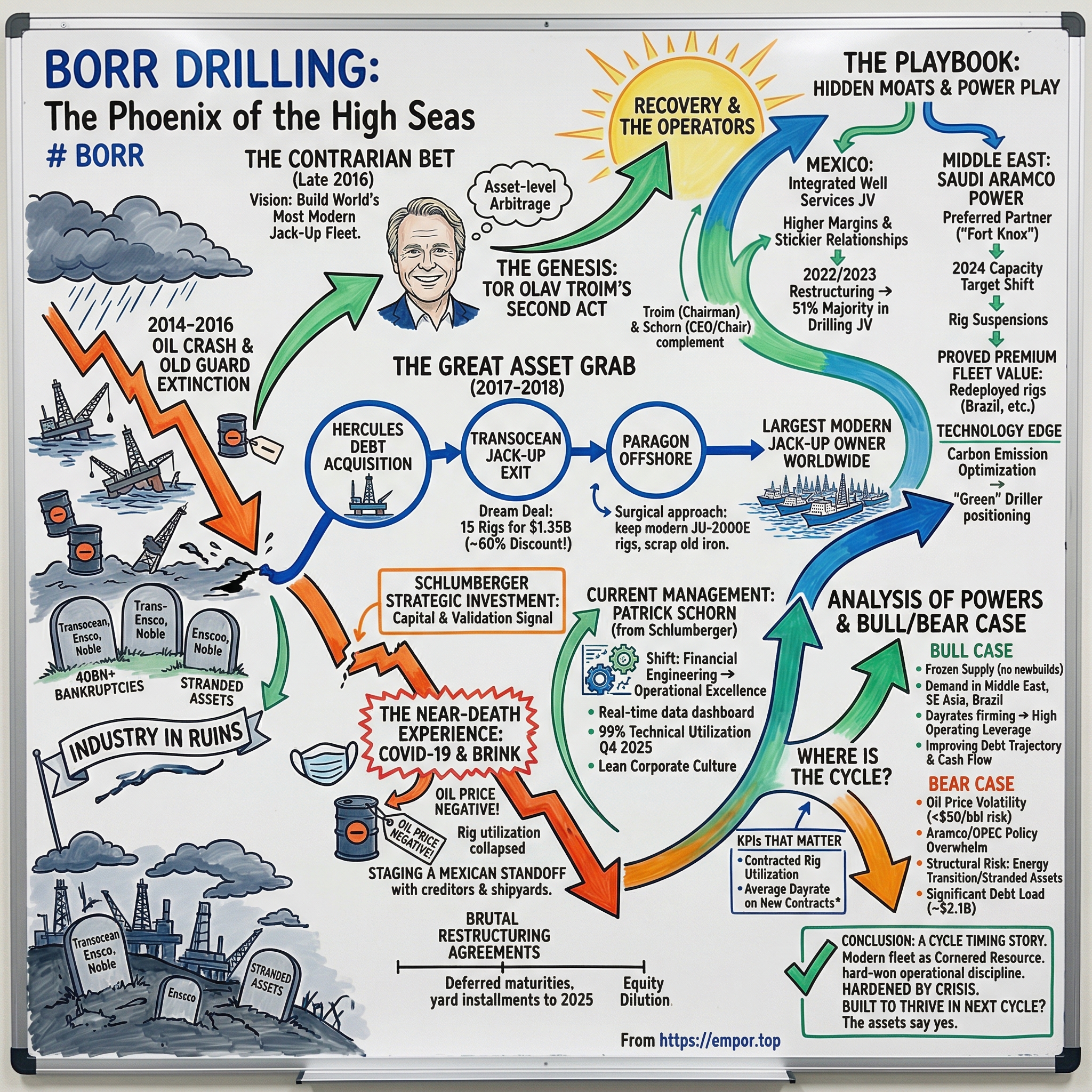

Picture the scene. It is late 2016. The offshore drilling industry lies in ruins. Oil prices, which had soared above a hundred dollars a barrel just two years earlier, have cratered to thirty. The great drillers of the world, companies with names like Diamond Offshore, Hercules, and Paragon, are filing for bankruptcy or teetering on the edge. Shipyards in Singapore and South Korea are littered with brand-new, state-of-the-art drilling rigs that nobody wants. Billions of dollars of steel sit idle, rusting in tropical humidity, waiting for owners who will never come. The offshore drilling industry, which had been the beating heart of the global energy boom for a decade, looks like it may never recover.

And into this carnage walks a Norwegian financier named Tor Olav Troim, who announces he is going to start a brand-new drilling company. Not to ride out the storm. Not to pick up scraps. To build, from zero, the most modern jack-up drilling fleet the world has ever seen.

The financial press treated it as somewhere between quixotic and insane. Who starts an offshore drilling company when the entire sector is being carried out on stretchers? Who raises capital for oil rigs when institutional investors are running screaming from anything that smells like hydrocarbons? The answer, it turns out, is someone who has been through cycles before. Someone who understands that the best time to buy world-class assets is when everyone else is desperate to sell them. And someone who has the relationships, the credibility, and the nerve to convince other people to write very large checks at the worst possible moment.

This is the story of Borr Drilling. It is a story about asset-level arbitrage executed at industrial scale, about buying premium drilling rigs for a fraction of their replacement cost during a generational downturn, and about positioning those assets for what many in the industry now call the offshore "supercycle." It is, in many ways, the ultimate Acquired story, because the entire company is built on a single, audacious thesis: that the world will always need oil from beneath the ocean floor, that the rigs capable of extracting it are scarce and getting scarcer, and that the market had temporarily lost its mind about what those rigs were worth.

But it is also a story about near-death. About a pandemic that nearly destroyed everything. About a Mexican standoff with creditors that lasted months. And about the question that hangs over every cyclical business: Is the cycle your friend, or is it a trap waiting to spring?

To understand Borr, you first have to understand the industry it was born into, the wreckage it was built from, and the man who saw opportunity where everyone else saw a graveyard.

II. The Context: The 2014 Oil Crash and the Old Guard

To appreciate what Troim pulled off, you need to rewind to the decade before Borr existed and understand just how badly the offshore drilling industry destroyed itself.

The 2000s were a golden age for offshore drilling. China's insatiable appetite for energy, combined with declining production from legacy onshore fields, drove oil prices from twenty dollars a barrel in 2002 to nearly a hundred and fifty by mid-2008. Every major oil company in the world was racing to develop offshore reserves, and they all needed rigs. Dayrates, the daily rental price for a drilling rig, skyrocketed. A premium jack-up that might have commanded sixty thousand dollars a day in 2004 was fetching a hundred and sixty thousand by 2013. At those prices, the economics of building new rigs were irresistible.

So the industry did what industries always do in a boom: it over-ordered. Hundreds of new jack-up rigs were commissioned from shipyards across Asia. Legacy drillers like Transocean, Ensco (now Valaris), and Rowan loaded up on new builds financed with cheap debt. The assumption was simple: demand would keep growing, dayrates would stay elevated, and the new rigs would pay for themselves many times over. It was the kind of logic that feels bulletproof right up until the moment it is not.

The bullet arrived in 2014, and it came from an unexpected direction. The American shale revolution, which had been building quietly for years, suddenly hit critical mass. Hydraulic fracturing and horizontal drilling unlocked vast quantities of oil and gas from formations in Texas, North Dakota, and Pennsylvania. U.S. oil production surged from five million barrels per day in 2008 to nearly ten million by 2015. The world was drowning in oil, and prices collapsed.

Brent crude fell from a hundred and fifteen dollars in June 2014 to below thirty dollars by early 2016. For offshore drillers, the math inverted overnight. Projects that had been economically compelling at a hundred dollars a barrel became money-losers at fifty. Exploration and production companies slashed their capital budgets. Drilling contracts were canceled or allowed to expire. Dayrates plummeted. And those hundreds of new rigs that had been ordered at the peak of the cycle? Many of them were still being built in shipyards, with no customers waiting on the other end.

This created what industry insiders called the "stranded assets" crisis. Shipyards in Singapore, particularly Keppel FELS and Sembcorp Marine, had dozens of completed or nearly completed rigs sitting on their docks. The original buyers had either gone bankrupt or simply refused to take delivery. The yards were stuck holding billions of dollars in steel that nobody wanted. Some rigs had been completed to full specification, brand-new and never used, and there was literally no one willing to buy them at any price.

The legacy drillers were in even worse shape. Companies like Transocean, the world's largest offshore driller, found themselves with massive fleets of aging rigs that were increasingly expensive to maintain and impossible to keep contracted. Their balance sheets, loaded with debt from the boom-era ordering spree, became crushing liabilities. Between 2015 and 2020, the offshore drilling industry saw more than forty billion dollars in bankruptcy filings. Noble Corporation, Diamond Offshore, Valaris, and Seadrill all went through Chapter 11. It was a mass extinction event.

But buried in all this destruction was something that a handful of people recognized: a once-in-a-generation opportunity. The rigs sitting idle in shipyards were not junk. They were modern, premium-specification assets that had cost two hundred and fifty million dollars or more to build. And they could be acquired for a fraction of that cost. The question was whether anyone had the capital, the conviction, and the operational capability to buy them, put them to work, and ride the next upcycle.

One person did. And he had spent two decades preparing for exactly this moment.

III. The Genesis: Tor Olav Troim's Second Act

The story of Borr Drilling is inseparable from the story of Tor Olav Troim, and understanding Troim requires understanding his remarkable, tumultuous career in Norwegian shipping and energy.

Born in 1963, Troim studied naval architecture and marine engineering at the Norwegian Institute of Technology in Trondheim, graduating in 1985. He spent the late 1980s as a portfolio manager at Storebrand, one of Norway's largest financial institutions, before becoming CEO of DNO, a Norwegian oil and gas company, in 1992. But the defining chapter of his career began in 1995, when he joined Seatankers Management in Cyprus and entered the orbit of John Fredriksen.

Fredriksen, a Norwegian-born, Cypriot-domiciled billionaire, is one of the most formidable figures in global shipping. Over the decades, he built a sprawling empire spanning tankers, dry bulk carriers, liquefied natural gas, fish farming, and offshore drilling. And for nearly twenty years, Troim was his chief architect. The two men operated as a tandem, with Fredriksen providing the capital and the strategic vision and Troim executing with ruthless precision. Troim held CEO positions at Frontline, one of the world's largest tanker companies, and Golar LNG, a pioneer in floating LNG technology. He sat on the boards of Marine Harvest, Golden Ocean, Ship Finance International, and, crucially, Seadrill.

Seadrill is the most relevant piece of the puzzle. Founded by Fredriksen in 2005, Seadrill became one of the world's premier offshore drilling companies by pursuing an aggressive strategy of fleet modernization, acquiring and ordering new rigs at a breathtaking pace. At its peak, Seadrill had one of the youngest, most technologically advanced fleets in the industry. Troim was a director from 2005 to 2014 and played a central role in shaping the company's strategy. He understood, at a molecular level, what made a good drilling rig, what operators valued, and how the economics of the business worked.

Then, in 2014, the partnership spectacularly collapsed. The reported trigger was a disagreement over the strategic direction of Golar LNG. Troim wanted to push aggressively into floating LNG production and regasification, a bet that Fredriksen considered "too speculative." In late July, the two announced that Troim would scale back his roles to focus on Golar and Seadrill. But within weeks, the arrangement fell apart completely. Fredriksen sold his controlling stake in Golar LNG, and Troim resigned from the boards of Seadrill, Archer, and Marine Harvest. Norwegian media dubbed it the end of the "Dynamic Duo." As part of the separation, Troim received three million Golar shares and two million Seadrill shares. The two men reportedly have not spoken since.

Troim wasted no time. He founded Magni Partners in London in 2014, named after the Norse god of strength, and began looking for his next major play. The offshore drilling downturn gave him exactly the canvas he needed.

In August 2016, Troim incorporated a new company in Hamilton, Bermuda, initially called Magni Drilling. He raised approximately a hundred and fifty-five million dollars through a private placement, an impressive feat given that the words "offshore drilling" were essentially radioactive in capital markets at the time. By December, the company had been renamed Borr Drilling, after the Norse father of Odin, and completed its first acquisition: two premium jack-up rigs, the Hercules Resilience and Hercules Triumph, bought out of the Hercules Offshore bankruptcy for a hundred and thirty million dollars. They were renamed Frigg and Ran, continuing the Norse mythology theme that would define the fleet.

The strategy was crystalline in its clarity. Borr would acquire only modern, high-specification jack-up rigs built after 2010. No "old iron." No semi-submersibles. No deepwater rigs. Jack-ups only, the workhorses of shallow-water drilling, which operate in water depths up to four hundred feet and are used for the vast majority of offshore wells worldwide. The thesis was that a fleet of exclusively modern rigs would command premium dayrates, achieve higher utilization, require less maintenance, and appeal to the most demanding customers, particularly national oil companies in the Middle East that were increasingly requiring newer equipment.

In March 2017, Troim landed a strategic investment that supercharged the entire operation. Schlumberger, the world's largest oilfield services company and arguably the most sophisticated operator in the industry, took a roughly twenty percent stake in Borr for approximately two hundred and twenty million dollars. This was not just capital. It was a validation signal. Schlumberger's interest was in creating an integrated drilling platform combining Borr's modern rigs with Schlumberger's technology and services. For Troim, it was both funding and a stamp of credibility that made everything that followed possible.

Within months, Borr was listed on the Oslo Bors. The company that had existed for barely a year was about to embark on one of the most aggressive acquisition sprees the industry had ever seen.

IV. The Great Asset Grab: M&A and Benchmarking

The period from late 2016 through early 2018 was Borr Drilling's "shock and awe" phase, a concentrated burst of dealmaking that transformed a startup with two rigs into the world's largest owner of premium jack-up drilling units. Each deal was different in structure, but they all shared a common logic: acquire modern rigs at distressed prices from sellers who had no choice but to accept.

The Transocean deal in 2017 was the one that changed everything. Transocean, the world's largest offshore driller, had decided to exit the jack-up business entirely and focus on ultra-deepwater operations. For Borr, this was a dream scenario: a motivated seller with premium assets looking for a single-transaction exit. The deal was structured at one point three five billion dollars for fifteen rigs, ten existing units from Transocean's fleet and five newbuilds under construction at Keppel FELS in Singapore. At roughly ninety million dollars per rig, Borr was acquiring assets that had cost two hundred and fifty million dollars or more to build, at a discount of roughly sixty percent to replacement cost.

The Paragon Offshore acquisition in February 2018 was a different kind of deal, more surgical in nature. Paragon had recently emerged from Chapter 11 bankruptcy with a fleet of thirty-two drilling units, mostly older jack-ups plus one semi-submersible. Borr acquired all outstanding shares for approximately two hundred and thirty-two million dollars. But the real strategy was not to operate the entire Paragon fleet. It was to cherry-pick the modern units, particularly the two premium JU-2000E jack-ups built in 2013 and 2014, and dispose of the rest. Within two months, Borr sold fourteen of the older rigs in a single block sale, effectively scrapping them. The company kept the modern assets and discarded the "junk," exactly as the strategy demanded.

By mid-2018, Borr had assembled a fleet of fifty-seven jack-up rigs, making it the largest jack-up owner in the world. The total acquisition spend was enormous, well over two billion dollars, but the math was compelling when viewed through the lens of replacement cost. Borr was acquiring newbuild-quality rigs for roughly a hundred to a hundred and fifty million dollars each. Building a comparable rig from scratch, even in 2018, would have cost two hundred and fifty million dollars and taken two and a half to three years. By 2024, that replacement cost had risen to three hundred million dollars or more, with shipyard capacity severely constrained.

This is what the company and its investors referred to as "steel value," the idea that the intrinsic worth of the physical assets provided a floor for the investment, even if utilization and dayrates stayed depressed for a while. A modern jack-up rig is roughly forty-five thousand tons of high-grade steel, heavy machinery, drilling equipment, and sophisticated control systems. Even in a terrible market, the scrap value of the steel alone provides meaningful downside protection. And in a recovering market, the gap between acquisition cost and replacement cost becomes a source of enormous competitive advantage, because no new competitor can replicate the fleet at anything close to the same price.

Did they overpay? The question deserves scrutiny. At the time of the acquisitions, many analysts argued that Borr was taking on too much debt to buy assets in a market with no clear recovery timeline. The Transocean deal, in particular, added significant leverage. And the newbuild rigs from Keppel FELS came with ongoing construction payments that would weigh on the balance sheet for years. But viewed from the vantage point of 2026, with newbuild costs exceeding three hundred million dollars per rig and essentially zero new jack-up orders being placed anywhere in the world, the acquisitions look like a masterclass in countercyclical asset procurement. Borr built its fleet at the bottom. The industry cannot replicate it at the top.

The acquisitions also had a strategic coherence that went beyond price. By focusing exclusively on modern rigs, Borr avoided the trap that had ensnared legacy drillers: maintaining a mixed fleet of old and new assets, where the old rigs drag down margins, require expensive maintenance, and struggle to win contracts in a market that increasingly demands newer equipment. Borr's fleet was born clean. Every rig was built to the latest specifications, with the latest safety systems, the latest drilling technology, and the latest environmental controls. This "clean sheet" approach would prove to be one of the company's most important strategic decisions.

But first, the company would have to survive the worst crisis in the history of the oil industry.

V. The Near-Death Experience: COVID-19 and the Brink

On April 20, 2020, something happened that no one in the oil industry had ever seen before: the price of West Texas Intermediate crude oil went negative. Producers were literally paying people to take their oil. For an industry that had already been battered by six years of downturn, the COVID-19 pandemic and the Saudi-Russia price war were the final hammer blows.

For Borr Drilling, the timing could not have been worse. The company had spent the previous three years on an aggressive acquisition spree, accumulating the world's largest fleet of premium jack-ups. That fleet had been financed with substantial debt and ongoing shipyard obligations. Now, with oil demand cratering and exploration budgets being slashed worldwide, Borr was staring into the abyss.

The numbers were terrifying. Rig utilization collapsed as operators suspended or canceled contracts. Revenue dried up. Meanwhile, Borr still owed hundreds of millions to Keppel FELS for five newbuild rigs under construction. The company's total exposure to Keppel alone was approximately eight hundred and ninety-two million dollars across loans and newbuild commitments. Debt maturities were looming. Cash was burning. And the capital markets were completely shut for anything related to offshore drilling.

To put the severity in context, every major competitor was going down. Noble Corporation filed for Chapter 11 in July 2020. Diamond Offshore filed in April. Valaris, the largest offshore driller in the world by rig count, filed in August. Seadrill, the company that Troim himself had helped build, was already in bankruptcy proceedings. The question was not whether the industry would consolidate; it was whether anyone would be left standing.

Borr's survival came down to a grueling, multi-party negotiation that management later described in terms that evoked hostage situations. The company was caught in what amounted to a Mexican standoff between its secured lenders, the shipyards holding its newbuild rigs, and its bondholders, each of whom had conflicting interests but all of whom stood to lose if the company went under.

In June 2020, Borr reached a comprehensive restructuring agreement that provided more than three hundred and fifteen million dollars in liquidity relief. The key elements were brutal but effective. Shipyard deliveries for the five Keppel newbuilds were pushed out to mid-2022, saving roughly a hundred and ninety million in near-term payments. Interest payments totaling about sixty million dollars were deferred. And sixty-five million in scheduled debt amortization was pushed to loan maturity. The company bought itself breathing room, but just barely.

The real stroke of survival came in December 2021, when Borr reached agreements to defer a staggering one point four billion dollars in debt maturities and yard installments from 2023 to 2025. This was the deal that saved the company. It pushed the wall of maturities far enough into the future that Borr could ride the market recovery that was just beginning to take shape.

Payment delays from Pemex in Mexico added another layer of stress. Borr had five rigs working in Mexico through joint ventures, and the state oil company's chronic cash flow problems meant payments were routinely delayed. During the worst of COVID, this created a cash flow squeeze that pushed the company to the edge.

There was also equity dilution. Management conducted equity offerings to shore up the balance sheet, targeting up to two hundred and fifty million dollars in raises. Existing shareholders were diluted, but the alternative was Chapter 11. It was survival-mode decision-making: ugly, painful, necessary.

Looking back, what separated Borr from the companies that went bankrupt was a combination of factors. The fleet was young enough and high-quality enough that customers still wanted it, even in a terrible market. The company's relationships with shipyards, while strained, were ultimately cooperative because Keppel had even more to lose from a Borr bankruptcy than Borr did. And management demonstrated a willingness to do whatever was necessary, including diluting equity and deferring everything deferrable, to keep the company alive long enough for the cycle to turn.

The cycle did turn. And when it did, Borr was the company best positioned to benefit, because it had the youngest fleet, the lowest operating costs, and a balance sheet that, while still leveraged, was no longer imminently lethal.

VI. Current Management: The Operators

In September 2020, with the company fighting for its life, Borr Drilling made a leadership change that signaled a fundamental shift in how it intended to operate. Patrick Schorn, a thirty-year veteran of Schlumberger, was appointed CEO.

Schorn's background was pure operational excellence. He had joined Schlumberger in 1991 as a stimulation engineer in Europe and spent the next three decades climbing through progressively senior roles across virtually every geography and business line the company operated. He ran operations in France, Russia, the Gulf of Mexico, and Latin America. He served as President of Well Services, President of Completions, President of the Production Group, and ultimately as President of Operations for the entire company. His final role before joining Borr was Executive Vice President of Wells, one of the most senior positions in the world's largest oilfield services company.

What made Schorn unusual in the context of Borr was the contrast with Troim. Troim is a financier, a dealmaker, a capital allocator who thinks in terms of asset values, replacement costs, and market cycles. Schorn is an operator who thinks in terms of non-productive time, equipment reliability, and customer relationships. The shift from Troim's financial engineering phase to Schorn's operational execution phase was deliberate and necessary. The company had assembled an extraordinary fleet. Now it needed to run that fleet at world-class levels.

Schorn's Schlumberger DNA showed up in several ways. He brought a data-driven approach to rig operations, pushing for real-time monitoring of equipment performance, fuel consumption, and drilling efficiency. He restructured the organization to reduce overhead, creating what management described as a "lean" corporate culture that runs with a fraction of the general and administrative expenses of legacy competitors. And he leveraged his decades of relationships in the industry to win contracts with demanding customers who valued operational reliability over price.

In September 2025, Schorn was elevated to Executive Chairman of the Board, a role that reflected both his strategic importance to the company and the ongoing evolution of the management structure. Troim, through Magni Partners, remained the company's most significant individual shareholder and continued to shape capital allocation strategy. The two complemented each other: Troim set the financial architecture and identified acquisition opportunities, while Schorn ensured the fleet ran at peak performance.

The incentive structure told an important story about management priorities. Compensation was heavily weighted toward EBITDA growth and debt reduction rather than fleet expansion or revenue growth for its own sake. This was a deliberate choice that aligned management with the interests of shareholders and creditors alike. After the near-death experience of 2020, the last thing the company needed was incentives that encouraged more empire-building. The focus was on sweating the assets that had already been acquired, maximizing utilization, and paying down the debt that had nearly killed the company.

Insider ownership provided additional alignment. Troim's personal stake through Magni Partners represented a significant personal bet on the company's success. He had made multiple open-market purchases, including at least one buy of twenty million dollars, reinforcing the message that management was eating its own cooking. Collectively, insiders held approximately six to seven percent of outstanding shares, meaningful enough to ensure that management felt the pain and the gain alongside public shareholders.

The operational results under Schorn's leadership were striking. By Q4 2025, Borr was reporting technical utilization of nearly ninety-nine percent and economic utilization of nearly ninety-eight percent for its working rigs. In an industry where equipment breakdowns, weather delays, and maintenance issues routinely eat into productive time, those numbers reflected exceptional operational discipline. This was the Schlumberger playbook in action: measure everything, eliminate waste, and treat every hour of downtime as a failure to be analyzed and prevented.

VII. Hidden Moats and Segments: The Mexico and Middle East Power Play

When investors look at Borr Drilling, they tend to see a simple business: own rigs, rent them to oil companies, collect dayrates. But the reality is more nuanced, and some of the most interesting parts of the business model are the ones that do not show up cleanly in the headline numbers.

Mexico has been one of Borr's most complex and, at times, most frustrating markets, but it has also been a source of strategic differentiation. The company operates five rigs in Mexico through a joint venture structure with a local partner, and the business model there goes well beyond simple rig rental. Instead of just providing a rig and crew, Borr's Mexican operations deliver integrated well services to Pemex, Mexico's state oil company. This means the company is responsible not just for the drilling equipment but for the full suite of services needed to drill and complete a well.

The integrated model captures significantly higher margins than pure contract drilling because it bundles multiple revenue streams into a single package. It also creates stickier customer relationships, because replacing an integrated service provider is far more complex and disruptive than swapping out a rig contractor. The combined contract value for the five Mexican rigs was approximately seven hundred and fifteen million dollars.

In 2022 and 2023, Borr restructured its Mexican joint ventures in an important way. The company sold its forty-nine percent stake in the integrated well services JVs to its Mexican partner, freeing up twenty-eight million dollars in historic profits and settlements. Simultaneously, Borr acquired an incremental two percent stake in the drilling JVs, bringing its ownership to a fifty-one percent majority. This was a shrewd move that simplified the corporate structure, reduced exposure to the more volatile services business, and gave Borr majority control over the drilling operations that were the core of its value proposition.

The Middle East represents a different kind of strategic prize. Saudi Aramco, the world's largest oil company, is arguably the most coveted customer in offshore drilling. Aramco contracts are long-term, well-paid, and backed by the financial resources of the Saudi state. Borr secured multiple contracts with Aramco, including rigs designated Arabia I, II, and III, establishing itself as a preferred partner in what the industry considers the "Fort Knox" of drilling markets.

However, the Middle East story also illustrates the risks of depending on sovereign customers. In 2024, Saudi Arabia reduced its maximum sustained production capacity target from thirteen million to twelve million barrels per day. The immediate consequence was that Aramco suspended operations on multiple jack-up rigs across the industry, including Borr's Arabia I and Arabia II. Across the sector, roughly eighteen rigs received suspension notices, a significant headwind for the entire jack-up market.

Borr's response demonstrated the value of having a young, premium fleet. Arabia I, freed from its Aramco commitment, secured a four-year firm contract with Petrobras in Brazil, one of the world's most demanding offshore operators. Arabia II picked up a binding letter of award from another Middle East customer for five hundred days firm plus a two-hundred-day option. The modern, high-specification nature of the rigs meant they were in demand globally, even when one particular market softened.

Beyond Mexico and the Middle East, Borr operates across West Africa, Southeast Asia, and other regions, maintaining geographic diversification that reduces dependence on any single market. The company's Arabia III rig remained contracted with Saudi Aramco through September 2028, maintaining the relationship even as other rigs were redeployed.

There is also a technology angle that often gets overlooked. Borr has invested in what it calls its operational dashboard, a real-time data platform that monitors fuel consumption, equipment performance, and environmental metrics across the fleet. In an industry where fuel is one of the largest variable costs and where carbon emissions are under increasing scrutiny, the ability to optimize fuel use and demonstrate environmental performance has become a genuine differentiator. Several customers, particularly national oil companies with public sustainability commitments, have cited Borr's fleet age and environmental profile as factors in contract awards. Being the "green" driller is an unusual positioning for a company in one of the world's most carbon-intensive industries, but the relative advantage is real. A rig built in 2015 with modern engine technology and emissions controls has a fundamentally different environmental profile than a rig built in 1995.

VIII. The Playbook: Analysis of Powers

Every great business story requires a framework for understanding what the business actually has, and what it lacks, in terms of durable competitive advantage. For Borr Drilling, the analysis is both interesting and uncomfortable, because the company operates in an industry where sustainable moats are notoriously difficult to build.

Start with Hamilton Helmer's Seven Powers framework. The most compelling power that Borr possesses is what Helmer would call a Cornered Resource. The fleet itself is the resource, and it is genuinely cornered. Borr owns twenty-nine premium jack-up rigs with an average age of roughly seven years, in an industry where the average fleet age is fifteen to twenty years. Crucially, you cannot replicate this fleet today. Building a new premium jack-up rig costs three hundred million dollars or more and takes two and a half to three years. No shipyard in the world has significant jack-up construction capacity available. And the financial returns required to justify a newbuild, roughly two hundred thousand dollars a day in dayrates at ninety-plus percent utilization sustained over twenty-five years, are higher than the current market supports. This means the supply of premium jack-ups is essentially frozen. Every rig that Borr owns was acquired at a fraction of current replacement cost, and no competitor can build a comparable fleet from scratch without spending multiples of what Borr paid.

Counter-Positioning is the second power at work. Legacy drillers like Valaris, Noble (now Diamond Offshore after their merger), and Shelf Drilling are stuck with mixed fleets that include older rigs built in the 1990s and early 2000s. These older rigs require more maintenance, achieve lower utilization, command lower dayrates, and are increasingly uncompetitive with newer equipment. But legacy players cannot simply retire them, because doing so would reduce their fleet size and revenue base, triggering negative reactions from investors and lenders. They are caught in a classic innovator's dilemma: the old assets are dragging them down, but abandoning them is too painful. Borr started with a clean sheet. It never had to make that trade-off.

Switching to Porter's Five Forces, the picture is equally instructive. The threat of new entrants is extremely low, and this is arguably the most important force at work. The capital required to enter the jack-up drilling market is now astronomical. A fleet of ten modern rigs would cost three billion dollars to build from scratch, plus years of construction time. There is no venture capital or private equity firm in the world that would fund a de novo jack-up drilling company today. The barriers to entry are, as one industry analyst put it, "made of very expensive steel."

Buyer power has shifted meaningfully in favor of the drillers. When utilization rates were low and rigs were abundant, oil companies could play drillers against each other and negotiate aggressively on dayrates. As global marketed jack-up utilization has climbed toward ninety percent, that dynamic has reversed. Operators increasingly find themselves competing for rig availability rather than the other way around. Borr's premium fleet, with its near-perfect technical reliability, is particularly well-positioned in this environment, because the most demanding customers, the national oil companies and major operators, will pay a premium for rigs that show up on time, drill efficiently, and do not break down.

Supplier power is moderate. The key suppliers are shipyards (for construction and major maintenance), equipment manufacturers (for drilling systems, engines, and control technology), and labor markets (for skilled drilling crews). Shipyard capacity is constrained, which works in Borr's favor for the moat argument but works against it when major maintenance or upgrades are needed. Labor markets for experienced offshore drilling crews are tight globally, a consequence of the industry's extended downturn driving talent into other sectors.

Rivalry among existing competitors remains intense but is evolving. The post-bankruptcy consolidation of the industry has reduced the number of players, and the remaining companies are generally more disciplined about pricing than their predecessors. The days of aggressive underbidding to fill rigs at any cost are largely over, replaced by a more rational approach to capacity management.

The substitute threat is the most philosophically interesting force. Onshore drilling, particularly shale, is the primary substitute for offshore production. But offshore and onshore resources serve different geographies and reservoir types, and the world's easiest onshore fields are increasingly depleted. The longer-term substitute threat comes from the energy transition itself: solar, wind, batteries, and electrification reducing demand for the oil that offshore rigs exist to produce. This is real, but its timeline matters enormously, and most credible forecasts see global oil demand remaining robust through at least 2035.

IX. The Bull vs. Bear Case

The investment debate around Borr Drilling comes down to a single, unavoidable question: Where are we in the offshore drilling cycle? The answer to that question determines whether Borr's stock is dramatically undervalued or a leveraged bet on a cycle that may already be peaking.

The Bull Case

The bull case begins with supply. There are essentially no new jack-up rigs being ordered anywhere in the world. The last significant newbuild cycle ended in the mid-2010s, and since then, hundreds of older rigs have been scrapped or permanently retired. The global marketed jack-up fleet is roughly four hundred rigs, with utilization around eighty-nine to ninety percent. As older rigs continue to be retired due to age, maintenance costs, and regulatory requirements, the effective supply will shrink further. Meanwhile, demand for shallow-water drilling is being driven by long-cycle development programs in the Middle East, Southeast Asia, West Africa, and Brazil, programs that have multi-year timelines and are relatively insensitive to short-term oil price swings.

In this environment, dayrates should continue to firm. Borr's 2025 average dayrate was approximately a hundred and forty-four thousand dollars per day. If dayrates climb toward the hundred and sixty to hundred and eighty thousand dollar range that the tightest market conditions would support, the impact on Borr's bottom line would be dramatic, because the company's operating costs are largely fixed. Each incremental dollar of dayrate flows almost entirely to the bottom line. At a hundred and sixty thousand dollars a day with twenty-five working rigs, the incremental EBITDA generation compared to current levels would be substantial.

The January 2026 acquisition of five premium rigs from Noble Corporation for three hundred and sixty million dollars, roughly seventy-two million per rig, reinforced the thesis. Borr acquired these assets at less than twenty-five percent of newbuild replacement cost, with two rigs generating immediate revenue under existing Noble contracts. The fleet expanded to twenty-nine rigs, strengthening Borr's position as the industry's dominant premium jack-up operator.

The debt trajectory is also improving. With adjusted EBITDA of four hundred and seventy million dollars in 2025 and annual debt amortization of roughly a hundred and forty-four million, the company is generating meaningful free cash flow for deleveraging. If the cycle cooperates, net debt to EBITDA could drop from current levels near three and a half to four times toward two times by the end of 2026. That delevering would open the door to meaningful capital returns through dividends or buybacks. The current dividend of two cents per share per quarter is token, but the potential for significant increases exists if the balance sheet continues to improve.

The Bear Case

The bear case starts with the most obvious risk: oil prices. Borr is a leveraged bet on offshore drilling activity, which is itself a leveraged bet on oil prices. If crude falls below fifty dollars a barrel and stays there, exploration budgets will be cut, contracts will be canceled, and dayrates will collapse. The company's debt load, while manageable at current activity levels, becomes dangerous if revenue declines materially. This is not a theoretical risk. It happened in 2015 and again in 2020.

The Saudi Aramco suspensions in 2024 were a warning shot. Eighteen rigs were suspended across the industry when Saudi Arabia reduced its production target. While Borr managed to redeploy its affected rigs, the episode demonstrated that even the most stable customers can change course quickly, and that OPEC production policy can overwhelm the micro-level supply-demand dynamics that underpin the bull case.

The energy transition represents a structural risk that grows over time. If global oil demand peaks earlier than expected, whether due to electric vehicle adoption, renewable energy deployment, or policy action on climate change, the long-term value of offshore drilling assets declines. Jack-up rigs have operational lives of thirty to forty years. If demand for their services peaks in the 2030s, rigs built in the 2010s may not generate returns over their full economic life. The "stranded asset" risk that Borr exploited during the downturn could ultimately apply to Borr's own fleet.

Geopolitical risk in the Middle East, one of Borr's most important markets, is an ever-present concern. Conflict or instability in the region could disrupt operations, delay contract awards, or make it impossible to deploy rigs in key markets.

Finally, there is the balance sheet itself. At approximately two point one billion dollars in total debt, Borr remains significantly leveraged. The company's senior secured notes carry a ten point three seven five percent coupon, reflecting the market's assessment of credit risk. If the cycle turns down before the company has sufficiently deleveraged, the combination of high fixed costs, high interest expense, and declining revenue could recreate the same near-death dynamics that nearly destroyed the company in 2020.

The KPIs That Matter

For investors tracking Borr's ongoing performance, three metrics tell the essential story. First, contracted rig utilization, meaning the percentage of the marketed fleet that is under active contract at any given time. This is the single most important indicator of demand for Borr's assets and the company's ability to maintain pricing power. Second, average dayrate on new contracts. The direction of dayrates on newly signed or renewed contracts reveals whether the market is tightening or loosening, independent of backlog composition. Watching the dayrate on new fixtures, not the blended average of the existing book, provides the clearest signal of market direction.

X. Conclusion and Reflections

The story of Borr Drilling is, at its core, a story about cycle timing executed at industrial scale. Tor Olav Troim saw something in 2016 that most of the market missed: that the offline drilling downturn had created a once-in-a-generation disconnect between the intrinsic value of premium jack-up rigs and the prices at which those rigs could be acquired. He had the conviction to act on that insight, the relationships to raise capital when no one wanted to fund offshore drilling, and the strategic clarity to build a fleet that was pure and modern rather than the mixed-quality grab bags that plagued legacy competitors.

The execution was far from perfect. The aggressive pace of acquisitions loaded the balance sheet with debt that nearly proved fatal during COVID. The Keppel newbuild obligations became an anchor during the worst possible moment. And the Mexican operations, while strategically interesting, created cash flow complications that added stress during the liquidity crisis. Troim and his team very nearly lost everything.

But they survived. And the company that emerged from the 2020 crisis was, in many ways, stronger than the one that entered it. The fleet was intact and younger than ever. The competitive landscape had been thinned by a wave of bankruptcies. And the appointment of Patrick Schorn brought operational rigor that transformed Borr from a financial engineering vehicle into a genuine operating company with world-class utilization rates and customer relationships.

The question that remains is whether Borr represents a new kind of drilling company, one built for the modern era of capital discipline and supply scarcity, or whether it is simply the latest iteration of a familiar pattern in cyclical industries: buy at the bottom, ride the wave up, and hope to get out before the cycle turns. The answer probably contains elements of both. The fleet is genuinely exceptional. The supply dynamics are genuinely favorable. But the industry remains fundamentally cyclical, tied to oil prices and OPEC decisions and geopolitical forces that no management team can control.

What Borr has demonstrated, beyond any argument, is that the assets matter. A fleet of twenty-nine premium jack-up rigs, averaging seven years of age, acquired at a fraction of replacement cost, in an industry with no new supply coming, is a powerful thing to own. Whether the world's need for offshore drilling is a five-year story or a fifty-year story, those rigs will be in demand for as long as the world produces oil from beneath the ocean floor.

And as long as the world continues to grow, to industrialize, to power itself with energy drawn from every available source, the shallow waters of the continental shelves will remain one of humanity's most important frontiers. The companies that own the machines capable of unlocking those resources, the modern, efficient, reliable machines that Borr spent a decade assembling, will be the ones that determine how that chapter of the energy story unfolds.

The question is not whether the world still needs offshore drilling. It does. The question is whether Borr Drilling, born in the wreckage of one cycle, hardened by the near-death of another, is built to thrive in the next one. The fleet says yes. The balance sheet says probably. And the cycle, as always, will have the final word.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube