Bristol-Myers Squibb: The Pharmaceutical Giant's Quest for Reinvention

I. Cold Open & Episode Setup

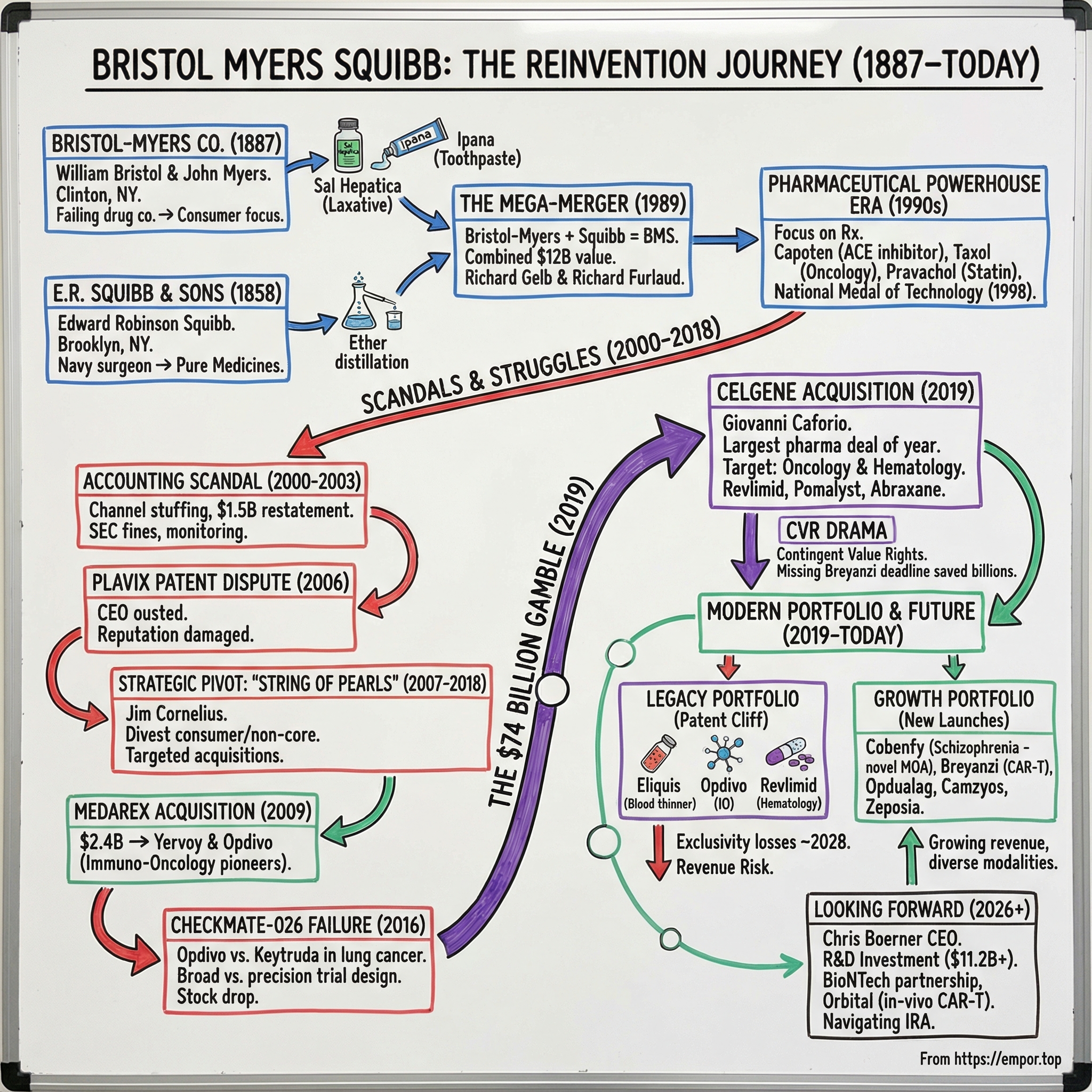

Picture the boardroom at Bristol-Myers Squibb's Princeton, New Jersey headquarters on a frigid January morning in 2019. CEO Giovanni Caforio, a soft-spoken Italian-born physician who had risen through the company's commercial ranks, was about to place the largest bet in the company's 130-year history.

The target: Celgene Corporation, a biotech powerhouse built almost entirely on a single blockbuster drug called Revlimid.

The price tag: seventy-four billion dollars.

The reaction from Wall Street was swift and merciless. BMS shares cratered more than fifteen percent on the announcement. Activist investor Starboard Value launched a public campaign calling the deal "poorly conceived and ill-advised." Even Wellington Management, BMS's largest institutional shareholder with an eight percent stake, publicly declared it was "not supportive."

Why would a company with a hundred-and-sixty-year legacy, a company that had already navigated accounting scandals, patent cliffs, and a devastating clinical trial failure that erased billions in market value, voluntarily walk into what many considered the pharmaceutical equivalent of a burning building?

The answer lies in understanding what Bristol-Myers Squibb actually is: not just a pharmaceutical company, but a case study in perpetual reinvention. Founded in 1887 by two college friends who bought a failing drug manufacturer with horse-and-buggy distribution, BMS has survived and thrived by repeatedly betting its future on transformative deals.

It merged two century-old companies in 1989 to create a global powerhouse. It pioneered the immuno-oncology revolution with Opdivo, only to watch Merck's Keytruda seize the throne in lung cancer. And then it doubled down with the Celgene acquisition, a deal that looked reckless at the time but now forms the backbone of a portfolio generating over forty-eight billion dollars in annual revenue.

Today, Bristol-Myers Squibb ranks among the world's largest pharmaceutical companies, consistently appearing on the Fortune 500 with a market capitalization exceeding one hundred and twenty billion dollars. It employs tens of thousands of people worldwide and operates across oncology, immunology, cardiovascular disease, and neuroscience. In September 2024, BMS received FDA approval for Cobenfy, the first drug with a novel mechanism of action for schizophrenia in over seventy years, a breakthrough that illustrates the company's ongoing capacity for reinvention.

But the central question of this story remains unresolved. BMS faces perhaps the steepest patent cliff in pharmaceutical history. Eliquis, its thirteen-billion-dollar blood thinner, and Opdivo, its nine-billion-dollar cancer immunotherapy, will both lose exclusivity around 2028. Together, they account for roughly half of the company's revenue.

Can a portfolio of newer drugs, many born from the Celgene acquisition, fill that gap? This is the story of how BMS arrived at this crossroads, and what it tells us about the nature of innovation, risk, and survival in the pharmaceutical industry.

II. The Origins: Two Friends, Two Companies (1887-1989)

In the spring of 1887, two young men walked across the commencement stage at Hamilton College in Clinton, New York. William McLaren Bristol, born July 28, 1860, and John Ripley Myers, four years his junior, had bonded over their years as fraternity brothers in the small liberal arts college nestled in upstate New York.

What they did next would have seemed absurd to anyone with business sense. Each scraped together five thousand dollars, pooled their resources, and bought the Clinton Pharmaceutical Company, a failing drug manufacturer located in their college town. Neither man had any training in chemistry or pharmaceutical manufacturing. Their business model, such as it was, consisted of loading medical preparations onto a horse-drawn buggy and selling them door-to-door to local doctors and dentists.

The early years were brutal. The company lacked capital, its founders lacked expertise, and its products lacked differentiation. In 1889, Bristol and Myers relocated the operation to Syracuse, hoping better rail connections would expand their reach. A decade later, they moved again to Brooklyn, chasing proximity to the lucrative markets of the Eastern seaboard.

But Myers would never see the company succeed. On December 22, 1899, at just thirty-five years old, John Ripley Myers died of pneumonia in New York City. The company had still not achieved real profitability. His heirs inherited his shares, and his name remained permanently attached to the business that William Bristol renamed Bristol-Myers Company in 1900.

The breakthrough came with two products that sound quaint today but were revolutionary for their era. Sal Hepatica was a laxative mineral salt that, when dissolved in water, replicated the therapeutic properties of the famed Bohemian mineral springs. By 1903, it had become a genuine bestseller.

Ipana toothpaste, introduced in 1901, became the first toothpaste to contain a disinfectant, helping prevent bleeding gums. Together, these two products transformed Bristol-Myers from a regional curiosity into an international brand. By 1924, gross profits exceeded one million dollars and products shipped to twenty-six countries.

Bristol-Myers became a pioneer in radio advertising during the 1920s, sponsoring "The Ipana Troubadours," a dance band show built around the unforgettable slogan: "Ipana for the Smile of Beauty; Sal Hepatica for the Smile of Health." William Bristol led the company until his death in 1935, when his eldest son Henry took the reins.

The company William Bristol built was, by today's standards, a consumer products company that happened to sell medicines. Its identity was shaped by advertising savvy and brand building rather than scientific discovery. Sal Hepatica and Ipana were household names, but they were not innovative pharmaceuticals. Bristol-Myers made money, but it was not advancing medicine. That distinction belonged to a very different company taking shape in Brooklyn, founded by a man whose moral convictions would literally set him on fire.

Edward Robinson Squibb was born on July 4, 1819, in Wilmington, Delaware, into a Quaker family that would suffer devastating losses. All three of his sisters died within a single year. His mother followed in 1831. His father suffered a debilitating stroke. Young Edward and his brother were raised by their grandmothers in Darby, Pennsylvania. Despite this bleak childhood, Squibb developed a fierce determination to practice medicine. He apprenticed under a Philadelphia pharmacist, worked his way through Jefferson Medical College, and graduated in 1844.

In a decision that cost him his Quaker fellowship, Squibb enlisted in the U.S. Navy in 1847 as an assistant surgeon. Over four years aboard the USS Perry, Erie, and Cumberland, he witnessed something that appalled him: the medicines used to treat sailors were dangerously impure. Drug merchants routinely adulterated their products with stones, bullets, and cheaper substitutes.

In a famous act of principled defiance, Squibb threw overboard entire supplies of medicines he deemed unfit for human consumption while overhauling the Cumberland's dispensary.

At the Brooklyn Naval Hospital, he collaborated with Dr. Benjamin Franklin Bache to develop a steam-powered method for distilling ether, replacing the terrifyingly dangerous open-flame technique then in use. True to his Quaker idealism, Squibb refused to patent the invention, publishing the diagrams freely in the American Journal of Pharmacy because he believed scientific knowledge belonged to everyone.

On September 6, 1858, Squibb established his own pharmaceutical laboratory on Furman Street in Brooklyn. Just three and a half months later, on December 29, a helper's accident with ether caused a catastrophic explosion and fire. Squibb rushed into the flames to rescue his scientific notes and books, suffering severe burns to his face and hands that left him scarred for life. The Brooklyn community rallied, raising over two thousand dollars. The principled Squibb insisted on repaying every cent with interest.

The Civil War proved transformative. Squibb's Brooklyn laboratory manufactured medicines supplying approximately one-twelfth of the entire Union Army's medical stores. By 1883, his company produced over three hundred drugs and distributed worldwide. In 1892, he brought his sons Edward and Charles into the business, renaming it E.R. Squibb and Sons. His crusade for pharmaceutical purity culminated in a proposed national pure food and drug bill in 1881 that, though it failed in his lifetime, directly inspired the landmark Food and Drug Act of 1906. Squibb died on October 25, 1900, having established the gold standard for pharmaceutical quality in America.

The contrast between Bristol-Myers and Squibb could not have been more stark. Bristol-Myers was a marketing machine that sold consumer products to the masses. Squibb was a scientist's company, founded on the principle that pharmaceutical purity was a moral imperative. Bristol-Myers made money through advertising. Squibb made money through trust. These two distinct corporate DNAs would eventually merge, but the tension between commercial orientation and scientific idealism would persist for decades.

Both companies expanded dramatically during World War II through penicillin production. Bristol-Myers acquired Cheplin Biological Laboratories, a producer of acidophilus milk, in 1943 and converted the plant to mass-produce penicillin for Allied forces. The key insight was brilliant in its simplicity: the fermentation expertise required for acidophilus milk transferred directly to antibiotic manufacturing.

By the late 1940s, Bristol Laboratories in Syracuse was considered the world's largest producer of penicillin. Squibb, meanwhile, was one of three American companies (alongside Merck and Eli Lilly) that received the original Oxford penicillin culture from England in 1940, and in 1944 opened what it called the world's largest penicillin plant in New Brunswick, New Jersey.

The penicillin era was transformative for the entire pharmaceutical industry, but it was particularly significant for Bristol-Myers. Before the war, the company was fundamentally a consumer products business. After the war, with Bristol Laboratories humming in Syracuse, it had genuine pharmaceutical manufacturing capability and the credibility to compete in prescription drugs. The antibiotic boom of the 1940s and 1950s created the modern pharmaceutical industry as we know it, companies that invested in research and development to discover new drugs, ran clinical trials to prove they worked, and sold them to physicians rather than directly to consumers.

Through the 1950s and 1960s, Bristol-Myers diversified aggressively into consumer products. In 1959, the company acquired Clairol, the leading American hair-coloring company famous for its legendary advertising campaign, "Does she or doesn't she?" That acquisition brought an unintended consequence that would reshape the entire company's destiny. Lawrence Gelb, Clairol's founder, had a son named Richard. The younger Gelb reluctantly joined Bristol-Myers to run the Clairol division after the acquisition. He performed so brilliantly that he rose through the ranks, becoming president, then CEO in 1972, and finally chairman in 1976. He would become the architect of the mega-merger that created Bristol-Myers Squibb.

Additional acquisitions followed: Drackett household products in 1965 and Mead Johnson, the infant formula giant behind Enfamil, in 1967.

Bristol-Myers also waded into the competitive pain reliever market, launching Datril as a challenger to Johnson & Johnson's Tylenol in the mid-1970s. J&J responded by slashing Tylenol's price, and the challenge fizzled. More successfully, when concerns about fluorocarbons threatened spray deodorant products in the mid-1970s, Bristol-Myers pivoted its Ban deodorant advertising to the roll-on format. The move vaulted Ban into the top-selling spot and increased sales of all roll-on products industry-wide by seventy-five percent in a single year, demonstrating the marketing agility that remained the company's core competence.

By the late 1980s, Bristol-Myers was a sprawling consumer-healthcare conglomerate with products spanning hair dye, baby formula, household cleaners, toothpaste, and an increasingly serious pharmaceutical research operation. Richard Gelb, who had spent four hundred million dollars on brand advertising and invested heavily in oncology and antiretroviral research, understood that the real money and the real future lay in prescription pharmaceuticals.

Consumer products were mature, low-margin businesses. Prescription drugs, protected by patents and sold to an aging population with growing healthcare spending, offered far superior economics. Gelb needed a partner with the scientific credibility and prescription drug expertise that Bristol-Myers still lacked. He had one in mind, a man he had known for a quarter century.

III. The Mega-Merger: Creating a Pharmaceutical Powerhouse (1989-2000)

Richard Gelb and Richard Furlaud had been friends for twenty-five years. Gelb, the Yale and Harvard Business School graduate who had transformed Bristol-Myers from a consumer products company into a serious pharmaceutical player, and Furlaud, the Princeton and Harvard Law graduate who had built Squibb into a cardiovascular powerhouse, had discussed the idea of combining their companies "occasionally over the previous three years." By the summer of 1989, the conversation turned serious.

Squibb brought something Bristol-Myers desperately needed: a world-class prescription drug franchise anchored by Capoten, the first ACE inhibitor ever developed. Captopril, Capoten's active ingredient, had been synthesized in 1975 by researchers Miguel Ondetti, Bernard Rubin, and David Cushman at the Squibb Institute for Medical Research, through a remarkable study of snake venom's natural ability to inhibit the angiotensin-converting enzyme.

To understand why Capoten mattered, consider the problem it solved. High blood pressure, or hypertension, is called the "silent killer" because it often has no symptoms but dramatically increases the risk of heart attacks and strokes. The angiotensin-converting enzyme, or ACE, is a protein in the body that narrows blood vessels and raises blood pressure. By blocking this enzyme, Capoten relaxed blood vessels and lowered pressure. When the FDA approved Capoten in April 1981, it opened an entirely new field of cardiovascular medicine. It became Squibb's first billion-dollar drug, and the class of drugs it spawned, ACE inhibitors, remains one of the most widely prescribed categories in medicine to this day.

On July 27, 1989, the two companies announced their merger, valued at approximately twelve billion dollars through a stock swap in which Squibb shareholders received 2.4 Bristol-Myers shares for each Squibb share. The combined entity boasted 1988 revenues of eight and a half billion dollars and profits of one point three billion, instantly creating the world's second-largest pharmaceutical enterprise behind only Merck.

Gelb became chairman and CEO of Bristol-Myers Squibb. Furlaud became president, heading the pharmaceutical business. The board split sixty-forty in favor of Bristol-Myers directors.

The strategic logic was compelling on paper. Bristol-Myers brought consumer brand strength, over-the-counter medicine expertise, and a growing oncology research capability. Squibb contributed deep expertise in ethical prescription drugs, particularly cardiovascular therapeutics, and a strong European market presence. Together, they would have the scale to compete globally in both consumer health and prescription pharmaceuticals.

The deal was, at the time, one of the largest mergers in any industry. It created a company with operations spanning prescription drugs, consumer health products, medical devices, and nutritional products. The two companies were described as having similar corporate cultures, which was supposed to ease integration. Similar cultures, however, is a phrase that appears in every merger press release and almost never survives contact with reality.

Integration is where pharmaceutical mergers go to die, and Bristol-Myers Squibb was no exception. Within a year, two thousand employees, four percent of the combined workforce, had been laid off. The company announced plans to close sixty pharmaceutical plants worldwide and six of its eighteen consumer products facilities by 1993.

The two predecessor companies maintained separate R&D centers on different sides of the organizational divide: Squibb's researchers in Lawrence, New Jersey, near Princeton, and Bristol-Myers' scientists in Wallingford, Connecticut. Cultural integration proceeded unevenly. The Squibb side prided itself on scientific rigor and ethical drug development. The Bristol-Myers side brought marketing firepower and consumer product instincts. Getting these two cultures to work as one proved far harder than the merger architects had anticipated.

Furlaud retired from the company in 1991, just two years after the merger, departing for board positions at American Express and the Rockefeller University. Gelb stepped down as CEO in 1993 and as chairman in 1995. Their successors inherited a company that was still digesting the merger while navigating the post-patent world of cardiovascular blockbusters.

Despite the integration challenges, the merged company delivered results. By 1993, worldwide revenues had grown to eleven point four billion dollars. The pharmaceutical pipeline expanded into oncology, where the company invested heavily in Taxol (paclitaxel) for cancer treatment, and into antivirals for HIV and next-generation cardiovascular drugs including Pravachol (pravastatin), which competed against Merck's Mevacor and later Pfizer's Lipitor in the statin class.

Bristol-Myers Squibb sold Drackett to S.C. Johnson for one point one five billion dollars in 1992, an early signal that the consumer diversification era was ending. The company continued divesting non-pharmaceutical assets over the following decade: Clairol went to Procter & Gamble, the Zimmer orthopedic implants business was spun off, and gradually the sprawling conglomerate narrowed its focus toward what would become its defining identity as a biopharmaceutical company.

The 1990s were the golden era for the pharmaceutical industry broadly. The global population was aging, healthcare spending was accelerating, and the regulatory environment, while rigorous, was navigable for well-funded companies with strong clinical development capabilities. BMS benefited from this rising tide, and its portfolio of cardiovascular, oncology, and anti-infective drugs performed well. The company also settled breast implant liabilities and prescription drug pricing claims totaling approximately four hundred to five hundred million dollars in the late 1990s, an early encounter with the legal and regulatory risks that would intensify in the years ahead.

In 1998, President Bill Clinton awarded Bristol-Myers Squibb the National Medal of Technology and Innovation, America's highest honor for technological achievement. CEO Charles Heimbold Jr. accepted the medal on behalf of the company. The citation honored BMS "for extending and enhancing human life through innovative pharmaceutical research and development, and for redefining the science of clinical study through groundbreaking and hugely complex clinical trials that are recognized models in the industry." The award marked the high point of the post-merger era. It would not last.

Richard Gelb himself provides an interesting study in pharmaceutical leadership. The son of a hair dye entrepreneur, educated at elite northeastern institutions, diagnosed with stomach cancer in 1986 yet continuing to lead the company through the merger, Gelb embodied a particular type of corporate leader. He was not a scientist. He was not a pharmacist. He was, fundamentally, a marketer who understood that Bristol-Myers needed to transform itself from a marketing company into a science company. The Squibb merger was his vehicle for that transformation. It is worth noting that many of the most important strategic decisions in pharmaceutical history have been made not by scientists but by commercially minded leaders who recognized where the industry's center of gravity was shifting.

For investors, the 1989 merger established a template that would define BMS's strategy for decades: use transformative deals to pivot the portfolio toward higher-growth, higher-margin pharmaceutical assets. The Clairol-to-Capoten arc illustrates the company's capacity for reinvention. But the merger also revealed a persistent challenge, namely that combining two large organizations with distinct cultures, geographies, and therapeutic focus areas produces friction that can take years to resolve. This tension between bold dealmaking and difficult integration would echo throughout BMS's subsequent history.

IV. The Transformation Years: Scandals, Struggles & Strategic Pivots (2000-2018)

The first years of the new millennium nearly destroyed Bristol-Myers Squibb.

Between the first quarter of 2000 and the fourth quarter of 2001, the company engaged in a systematic scheme to overstate its sales and earnings. The method was channel stuffing: BMS used financial incentives to pressure pharmaceutical wholesalers into buying and holding far greater quantities of drugs than actual patient demand warranted. Think of it like a retail store stuffing its distribution partners' warehouses with excess inventory and then booking the shipments as "sales," even though real consumer demand had not materialized.

The scheme improperly recognized approximately one and a half billion dollars in revenue from what were essentially phantom sales. When channel stuffing was not enough, CFO Frederick Schiff dipped into "cookie jar" reserves, stashed accounting reserves from prior periods, to further inflate earnings numbers.

To put the magnitude of the fraud in perspective: one and a half billion dollars in improperly recognized revenue is not a rounding error. It is the equivalent of an entire blockbuster drug's annual sales being fabricated through accounting gimmicks. The scheme inflated BMS's reported performance at exactly the moment investors were trusting the post-merger company to deliver on its pharmaceutical transformation promise.

The house of cards collapsed in March 2003, when BMS was forced to restate its prior financial statements. The SEC charged two former officers, Schiff and Richard Lane, with conspiracy and securities fraud. BMS paid one hundred and fifty million dollars to settle fraud charges with the SEC in 2004 and three hundred million in restitution under a 2005 Deferred Prosecution Agreement with the U.S. Attorney's Office. Former federal judge Frederick Lacey was appointed as an independent monitor, essentially putting the company under federal supervision.

But the scandals were not over. In July 2006, the FBI raided BMS corporate offices over allegations that the company had entered into a secret arrangement with Canadian generic manufacturer Apotex to keep a generic version of the blockbuster blood thinner Plavix off the market. On September 12, 2006, monitor Lacey urged the board to remove CEO Peter Dolan for his conduct in the Plavix dispute. Dolan was ousted that same day. Board member James Cornelius, a turnaround specialist, was named interim CEO with a mandate to clean house. Every executive involved in the scandals eventually left the company.

The scandals left BMS's reputation in tatters. A company that had been awarded the National Medal of Technology less than a decade earlier was now operating under federal supervision with a court-appointed monitor reviewing its every move. The brand damage extended beyond the courtroom: physicians, investors, and potential research partners questioned whether BMS could be trusted. Rebuilding that trust would take years and require leadership willing to fundamentally reimagine what kind of company BMS would become.

Cornelius launched what he called the "Biopharma Transformation Strategy" in 2007, the most ambitious strategic pivot in BMS history. The vision was to transform the company from a large, diversified pharmaceutical conglomerate into a focused specialty biopharmaceutical company.

This meant shedding non-core businesses, closing half of the company's manufacturing facilities, freezing the pension plan, and cutting thousands of jobs. In November 2009, BMS announced it was spinning off Mead Johnson Nutrition, the infant formula business it had acquired four decades earlier. By 2000, Clairol had been divested to Procter & Gamble, and the Zimmer orthopedic implants business had been separated. The consumer products era was definitively over.

Rather than pursuing a single mega-merger as many peers were doing, Cornelius adopted what he called the "String of Pearls" strategy: a series of targeted, smaller acquisitions designed to build the pipeline organically.

The most consequential pearl came in August 2009, when BMS acquired Medarex for approximately two point four billion dollars. Medarex was a small biotech company that had developed two experimental antibody drugs through a research collaboration with Japan's Ono Pharmaceutical. Those two drugs, ipilimumab and nivolumab, would become Yervoy and Opdivo, among the first immuno-oncology drugs approved by the FDA and the foundation of an entirely new approach to treating cancer.

The science behind these drugs was elegant and revolutionary. To explain it simply: the immune system's T cells are the body's soldiers against disease, including cancer. But T cells have built-in brakes, checkpoint proteins, that prevent them from attacking normal cells.

Cancer cells exploit this system by displaying a protein called PD-L1 on their surface, which binds to the PD-1 receptor on T cells and sends a "stand down" signal. The cancer cell essentially fools the immune system into thinking it is a normal cell.

Opdivo is a monoclonal antibody that blocks the PD-1 receptor, preventing cancer cells from pressing the brake pedal. With the brake released, T cells can recognize and attack the tumor. This approach, called checkpoint inhibition, represented a paradigm shift from traditional chemotherapy, which kills cancer cells directly but devastates healthy tissue in the process.

Cornelius handed the CEO role to Lamberto Andreotti in May 2010, who continued the String of Pearls strategy and expanded R&D spending to three point six billion dollars annually. When Giovanni Caforio succeeded Andreotti as CEO in May 2015, Opdivo was already generating nearly one billion dollars in annual sales and analysts projected it could reach nine billion by 2019, with much of that growth expected from first-line lung cancer treatment.

Then came the catastrophe that would haunt BMS for years. And it was not a drug failure in the traditional sense. It was a strategic miscalculation about how to prove a drug works.

Yervoy had received FDA approval in 2011 for melanoma and generated billions in revenue, establishing BMS as a pioneer in the new field of cancer immunotherapy. Opdivo followed with approvals in melanoma (December 2014) and then squamous non-small cell lung cancer (March 2015), based on the CheckMate-017 trial which was stopped early because Opdivo showed a forty-one percent reduction in the risk of death compared to chemotherapy. In October 2015, Opdivo expanded into non-squamous lung cancer based on CheckMate-057, also stopped early. By 2016, Opdivo was generating three point eight billion dollars in annual revenue, far outpacing Merck's rival drug Keytruda at one point four billion. BMS appeared to be running away with the immunotherapy market.

But the battleground that mattered most was still ahead. The competition between Opdivo and Keytruda (pembrolizumab) was first-line lung cancer, the single largest commercial opportunity in oncology.

Merck made a critical strategic decision: it designed its KEYNOTE-024 trial to enroll only patients whose tumors expressed PD-L1 on at least fifty percent of their cells, a biomarker-enriched population most likely to respond to immunotherapy alone. BMS made the opposite bet. Its CheckMate-026 trial enrolled patients with PD-L1 expression on as little as five percent of tumor cells, believing Opdivo would work broadly without biomarker selection.

To put this in simpler terms: Merck cherry-picked the patients most likely to respond, while BMS tried to prove its drug worked for everyone. Merck's approach was more conservative but more likely to succeed. BMS's approach was bolder but riskier.

The results were devastating. Merck's narrow, precision-focused KEYNOTE-024 trial succeeded spectacularly, showing a fifty percent reduction in the risk of death compared to chemotherapy. BMS's broad CheckMate-026 trial failed its primary endpoint entirely. In the broader population BMS had chosen to study, Opdivo actually performed worse than chemotherapy on progression-free survival.

The August 2016 announcement wiped out billions in BMS market value. Keytruda began its inexorable rise to become the world's best-selling drug, reaching nearly thirty billion dollars in 2024 sales, while Opdivo was locked out of the largest lung cancer treatment setting.

The strategic error was clear in retrospect. BMS had bet against precision medicine at exactly the moment precision medicine was winning. Patients whose tumors expressed PD-L1 at high levels likely responded just as well to Opdivo as to Keytruda, but their results were diluted by the larger group of patients who did not benefit from immunotherapy as monotherapy. It was a trial design decision, not a drug quality difference, that handed Merck the oncology crown.

The Opdivo-Keytruda episode carries a profound lesson that extends beyond pharmaceuticals. In many industries, the first mover with a technically superior or equivalent product can still lose if a competitor makes a better strategic bet on how to demonstrate that product's value. BMS had the earlier data, the bigger sales force, and the initial market share lead. Merck had a better clinical strategy. Strategy won.

Meanwhile, BMS was hemorrhaging revenue from patent expirations. Plavix, which had been co-marketed with Sanofi and was the company's top seller, lost patent protection in May 2012, and sales plummeted sixty-five percent almost immediately. Abilify, the antipsychotic partnered with Otsuka that generated two point eight billion dollars in 2012, lost exclusivity in 2015. Other major products including Sustiva, Reyataz, and Baraclude also faced generic competition. BMS needed to replace over ten billion dollars in annual revenue just to tread water.

Not all the pearls shone, however. BMS acquired Inhibitex for two point five billion dollars in 2012 for its hepatitis C drug pipeline, only to see the lead compound fail in clinical studies, resulting in a one-point-eight-billion-dollar write-down. The company also partnered with AstraZeneca to acquire Amylin Pharmaceuticals for five point three billion in the diabetes space.

The Inhibitex failure was a stark reminder that even the most disciplined acquisition strategy carries binary clinical risk: drug development is, at its core, a bet on whether a molecule will work in the human body, and no amount of due diligence can eliminate that uncertainty.

The String of Pearls strategy was producing growth assets but not fast enough to replace the patent cliff revenue. Something more dramatic was needed.

V. The Celgene Acquisition: The $74 Billion Gamble (2019)

On January 3, 2019, Giovanni Caforio announced that Bristol-Myers Squibb would acquire Celgene Corporation for approximately seventy-four billion dollars in cash and stock. It was the largest pharmaceutical deal of the year and one of the largest in the industry's history, rivaled only by AbbVie's sixty-three-billion-dollar acquisition of Allergan announced later that same year.

The deal terms were aggressive. Each Celgene shareholder would receive one share of BMS common stock plus fifty dollars in cash, valuing each Celgene share at one hundred and two dollars and forty-three cents, a fifty-three-point-seven percent premium to the prior closing price.

In addition, Celgene shareholders received one tradeable Contingent Value Right, or CVR, entitling them to an additional nine dollars per share if three specific pipeline drugs received FDA approval by specified deadlines. This CVR structure would later become one of the most controversial elements of the deal. BMS would add approximately thirty-two billion dollars in new debt while also assuming twenty billion in existing Celgene obligations.

Brad Loncar, CEO of Loncar Investments, captured the deal dynamic perfectly: "Both companies were kind of limping into 2019."

BMS was struggling with Opdivo's constrained growth following the Keytruda defeat. Celgene was in even worse shape. Its stock had fallen more than thirty-seven percent in 2018 alone. The company was overwhelmingly dependent on Revlimid, which accounted for sixty-four percent of total revenue, and Revlimid's patents were expected to expire with generic entry looming. Adding insult to injury, the FDA had issued an embarrassing refuse-to-file notice on ozanimod, Celgene's key pipeline asset for multiple sclerosis, raising doubts about the pipeline that was supposed to replace Revlimid revenue.

Wall Street's initial verdict was damning. BMS shares sank more than fifteen percent on the announcement while Celgene shares surged thirty-three percent, a clear signal that investors believed BMS was overpaying. Jeffrey Smith of Starboard Value went public with a scathing open letter to BMS shareholders on February 28, 2019, calling the deal "poorly conceived and ill-advised" and arguing that BMS was "deeply undervalued" as a standalone company. Wellington Management, BMS's largest institutional shareholder, added its own public opposition.

Caforio was undeterred. The strategic rationale centered on creating a dominant oncology and hematology platform. BMS would combine its immuno-oncology franchise, Opdivo and Yervoy, with Celgene's hematology powerhouse, Revlimid, Pomalyst, and Abraxane, along with a deep pipeline of near-term launches including two CAR-T cell therapies.

CAR-T, or chimeric antigen receptor T-cell therapy, represents a radical approach to cancer treatment. Think of it as custom-building a weapon designed specifically for one patient's cancer. A patient's own T cells are extracted via a blood draw, shipped to a specialized laboratory, genetically reprogrammed to recognize and attack cancer cells, multiplied into the millions, and then infused back into the patient. It is, in essence, a living drug manufactured individually for each patient, and it represents one of the most complex manufacturing challenges in the history of medicine.

The proxy fight climaxed when both Institutional Shareholder Services and Glass Lewis, the two most influential proxy advisory firms, recommended shareholders vote in favor of the deal. Starboard withdrew its campaign on March 29, 2019. Shareholders approved the merger on April 12.

But regulators had a condition. The Federal Trade Commission required divestiture of Otezla, Celgene's oral psoriasis treatment, to avoid anticompetitive overlap. On August 26, 2019, BMS announced that Celgene had agreed to sell Otezla to Amgen for thirteen point four billion dollars in cash, the largest divestiture the FTC had ever required in a merger enforcement action. BMS would use the proceeds to reduce the mountain of debt from the acquisition.

The merger closed on November 20, 2019. Mark Alles, who had served as Celgene's CEO and had publicly stated his ambition to "make Revlimid obsolete" by building out the pipeline, departed the combined company. Caforio now led a pharma giant with approximately thirty-four thousand employees, operations in dozens of countries, and a portfolio spanning immuno-oncology, hematology, cell therapy, cardiovascular disease, and immunology. He also led a company carrying more than fifty billion dollars in combined debt. The integration of Celgene's Thousand Oaks, California-based operations with BMS's Princeton, New Jersey headquarters began immediately, along with the inevitable layoffs and organizational restructuring that accompany every mega-merger.

Then the CVR drama began.

The Contingent Value Rights required FDA approval of three Celgene pipeline drugs by specific deadlines: Zeposia (ozanimod) for multiple sclerosis by December 31, 2020; Breyanzi (lisocabtagene maraleucel), a CAR-T therapy for non-Hodgkin lymphoma, by the same date; and Abecma (idecabtagene vicleucel), a CAR-T for multiple myeloma, by March 31, 2021.

Zeposia made its deadline, winning approval in March 2020. Abecma was approved in March 2021, barely squeezing under its wire. But Breyanzi was approved on February 5, 2021, just five weeks after its December 31 deadline.

Because the CVR agreement required all three drugs to hit their milestones, the entire nine-dollar payment, worth up to six point four billion dollars to former Celgene shareholders, was never triggered.

Former Celgene shareholders cried foul. They alleged that BMS had deliberately delayed Breyanzi's approval process. The FDA's manufacturing inspection had identified issues, and plaintiffs claimed BMS had failed to make books and records available for inspection upon request on December 29, 2020.

UMB Bank, acting as trustee, filed a six-point-four-billion-dollar lawsuit against BMS. In October 2024, U.S. District Judge Jesse Furman dismissed the suit, ruling UMB Bank lacked standing. Earlier lawsuits filed directly by CVR holders in both New York and New Jersey had also been tossed. The CVR controversy left a bitter taste, but it also saved BMS billions that went instead toward debt reduction and pipeline investment.

The CVR episode illustrates one of the darker dynamics of large-scale pharmaceutical M&A. The structure was designed to bridge a valuation gap: BMS could offer Celgene shareholders a lower upfront price by adding contingent payments tied to pipeline milestones. But contingent value rights create misaligned incentives. Once BMS owned Celgene, it controlled the pace and priority of the pipeline programs that determined whether CVR payments would be triggered. Whether BMS deliberately slow-walked Breyanzi or simply encountered the kind of manufacturing delays that routinely plague CAR-T production, the end result was the same: former Celgene shareholders lost out on six point four billion dollars in potential payments, and BMS avoided that cash outflow. The structure functioned as designed, but the design itself embedded a conflict of interest that was arguably foreseeable from the start.

The Celgene deal reshaped BMS's financial profile overnight. The combined company was now the sixth-largest pharmaceutical company globally by revenue, with a portfolio spanning immuno-oncology, hematology, cardiovascular disease, immunology, and cell therapy. But the real test was whether the pipeline assets Caforio had bet seventy-four billion dollars on would actually deliver.

VI. The Modern Portfolio: Building for the Future (2019-Today)

The myth of the Celgene acquisition is that BMS overpaid for a declining asset. The reality, five years in, is more nuanced. Critics focused on Revlimid's patent cliff, but the deal also brought an entire portfolio of near-term launches, two CAR-T programs, and a deep pipeline that has since generated multiple approvals. BMS did not buy Celgene for Revlimid's remaining revenue. It bought Celgene for the portfolio that would replace Revlimid. That distinction matters enormously in evaluating the deal's success.

Five years after the Celgene acquisition closed, the results tell a nuanced story. BMS reported total 2024 revenues of forty-eight point three billion dollars, up seven percent year-over-year. The three largest products, Eliquis at thirteen point three billion, Opdivo at nine point three billion, and Revlimid at five point eight billion, still dominated the top line. But the growth story lies elsewhere.

BMS has organized its portfolio into two categories that reveal the company's central strategic tension. The "Legacy Portfolio" includes the established blockbusters: Eliquis, Opdivo, Revlimid, Pomalyst, Sprycel, and Abraxane. These products generated twenty-five point seven billion dollars in 2024 but are collectively approaching patent cliffs.

The "Growth Portfolio" contains nine newer products launched since the Celgene merger, and this is where the future lives. In 2024, the growth portfolio generated twenty-two point six billion dollars, up seventeen percent from the prior year.

The portfolio includes Reblozyl for anemia at one point eight billion, Opdualag, the first dual checkpoint inhibitor combining Opdivo with a LAG-3 blocker called relatlimab, at nine hundred and twenty-eight million, Breyanzi at seven hundred and forty-seven million with a stunning one-hundred-and-five percent growth rate, Camzyos for hypertrophic cardiomyopathy at six hundred and two million, Zeposia for multiple sclerosis and ulcerative colitis at five hundred and sixty-six million, and several earlier-stage launches still building revenue.

The growth portfolio's diversity is itself a strategic asset. Unlike Celgene, which was dangerously dependent on a single product (Revlimid at sixty-four percent of revenue), BMS's growth portfolio spans multiple therapeutic areas and modalities. No single growth product exceeds eight percent of total company revenue. This diversification reduces binary risk and provides multiple shots on goal for revenue growth.

The jewel in the growth portfolio may be Cobenfy, which represents a genuine scientific breakthrough. In September 2024, the FDA approved Cobenfy, known chemically as xanomeline and trospium chloride, as the first drug with a novel mechanism of action for schizophrenia in over seventy years. Every previous antipsychotic worked by blocking D2 dopamine receptors, an approach that controlled psychotic symptoms but caused debilitating side effects including severe weight gain, metabolic syndrome, tardive dyskinesia, and heavy sedation. These side effects are the primary reason patients stop taking their medication, and non-adherence is the central challenge in schizophrenia treatment.

Cobenfy works differently. It is a fixed-dose combination of two drugs. Xanomeline is a muscarinic agonist that selectively targets M1 and M4 receptors in the brain. Think of it as taking a completely different highway to the same destination: instead of blocking dopamine (the traditional route), it modulates the muscarinic acetylcholine system, a parallel brain circuit that also influences psychotic symptoms.

The catch is that xanomeline, when given alone, causes intolerable gastrointestinal and cardiovascular side effects through muscarinic receptors elsewhere in the body. The second component, trospium chloride, is an anticholinergic that blocks those peripheral muscarinic side effects without crossing the blood-brain barrier, leaving the brain effects intact. It is an elegant pharmacological one-two punch.

BMS acquired this asset by purchasing Karuna Therapeutics for fourteen billion dollars in March 2024. The compound's journey was remarkable: xanomeline had originally been tested in the late 1990s for Alzheimer's cognitive decline and unexpectedly showed benefits for psychotic symptoms, but its peripheral side effects prevented standalone use for decades until the pairing with trospium.

Cobenfy launched in late October 2024 at a list price of eighteen hundred and fifty dollars per month. It generated ten million in its first partial quarter, then ramped to one hundred and fifty-six million in full-year 2025 across all four quarters. Weekly prescriptions reached over sixteen hundred by mid-2025, tracking ahead of all branded schizophrenia comparators.

BMS has fourteen studies ongoing or planned across schizophrenia, Alzheimer's psychosis (the ADEPT-2 trial, with data expected by end of 2026), and bipolar disorder. However, the Phase 3 ARISE trial testing Cobenfy as an add-on to existing antipsychotics failed, denting the blockbuster narrative.

BMS has acknowledged that "deeply ingrained" prescribing habits in schizophrenia are slowing initial uptake. The schizophrenia market has been resistant to novel therapies for decades precisely because clinicians are comfortable with the drugs they know, even with their significant side effects. Changing physician behavior is often harder than developing the drug itself.

The patent cliff looms large over this growth story. Revlimid's generic erosion is already well underway, with revenue falling from a peak of twelve point eight billion dollars in 2021 to five point eight billion in 2024. Eliquis faces generic entry beginning around April 2028 based on litigation settlements, though Medicare price negotiations under the Inflation Reduction Act already reduced its price by fifty-six percent for Medicare beneficiaries starting in January 2026. BMS management has somewhat counterintuitively forecast Eliquis revenue growing ten to fifteen percent in 2026, arguing that lower prices will expand patient access and increase volume among Medicare beneficiaries.

Opdivo has a slightly longer runway, with U.S. biosimilar exclusivity estimated through 2028, European protection through 2030, and Japanese exclusivity through 2031. BMS moved aggressively to defend the franchise, winning FDA approval for Opdivo Qvantig, a subcutaneous formulation, in December 2024. This formulation delivers in three to five minutes versus a thirty-minute intravenous infusion, offering a meaningful convenience advantage that could retain patients even as biosimilars enter the intravenous market.

The cost structure is being restructured to match the revenue challenge. BMS initially targeted one point five billion dollars in savings by 2025, then expanded the program to an additional two billion by 2027, for a combined three point five billion in cost reductions.

These efforts include organizational redesign, operational efficiency improvements, over two thousand layoffs, and exploration of sale-leaseback transactions for major facilities including a one-point-two-million-square-foot life sciences campus in Summit, New Jersey.

R&D investment remained elevated at eleven point two billion dollars in 2024, a twenty percent increase from the prior year, reflecting BMS's commitment to outrunning the patent cliff through pipeline innovation. The company is essentially cutting everywhere except the lab.

For investors, the critical math is straightforward: can the growth portfolio, which generated twenty-two point six billion in 2024 and is growing at seventeen percent annually, scale fast enough to replace the combined twenty-four billion or so at risk from Eliquis and Opdivo exclusivity losses around 2028? BMS management projects confidence, pointing to six pivotal trial readouts expected in 2026 and a growth portfolio that already exceeds fifty percent of legacy portfolio revenue. But the replacement math requires these newer products to collectively add twenty billion or more in revenue over the next three to five years, a formidable challenge by any measure.

VII. Competitive Landscape & Industry Dynamics

The immunotherapy war between Opdivo and Keytruda remains one of the most instructive competitive battles in pharmaceutical history. In 2024, Merck's Keytruda generated twenty-nine point five billion dollars in revenue versus Opdivo's nine point three billion, a ratio of roughly three to one. Keytruda holds approvals across more than forty indications spanning seventeen tumor types. The gap traces back to that fateful 2016 clinical trial design divergence, but the competitive picture is more nuanced than the headline numbers suggest.

Opdivo carved out durable positions where Keytruda is weaker or absent. In kidney cancer, the Opdivo-Yervoy combination demonstrated the longest median overall survival in previously untreated advanced disease, with nearly half of patients alive at five years. In melanoma, liver cancer, esophageal cancer, and mesothelioma, Opdivo combinations with Yervoy remain standard-of-care options.

BMS's dual-checkpoint strategy, combining PD-1 blockade (Opdivo) with CTLA-4 blockade (Yervoy), is a competitive differentiator that Merck cannot easily replicate because it lacks a comparable CTLA-4 inhibitor. And Opdualag, which pairs Opdivo with the LAG-3 inhibitor relatlimab, represents a next-generation approach to checkpoint combination therapy.

The irony is that Keytruda now faces its own patent cliff around 2028, creating one of the most dramatic revenue replacement challenges in pharmaceutical history. Merck's dependence on Keytruda is far more concentrated than BMS's exposure to any single product. Keytruda accounts for over forty-five percent of Merck's total revenue. BMS's diversified portfolio, built through acquisitions and the Celgene merger, may prove a strategic advantage as both companies navigate the biosimilar era simultaneously.

In June 2025, BMS signed an eleven-point-one-billion-dollar deal with BioNTech to co-develop BNT327, a next-generation bispecific antibody targeting both PD-L1 and VEGF-A, positioning for the post-Keytruda competitive landscape. This deal signals BMS's intent to maintain its immuno-oncology franchise beyond Opdivo's patent life.

The CAR-T cell therapy market tells a competitive story of its own. The total market reached four point six five billion dollars in 2024 and is projected to grow to nearly sixteen billion by 2030. Gilead's Yescarta leads with one point six billion in revenue and thirty-seven percent market share.

BMS's Breyanzi has the broadest approved label, spanning large B-cell lymphoma, chronic lymphocytic leukemia, mantle cell lymphoma, and follicular lymphoma, and is growing fastest at one hundred and five percent year-over-year.

But Abecma is struggling. In the multiple myeloma CAR-T market, Johnson & Johnson and Legend Biotech's Carvykti has seized roughly eighty percent of late-line market share at treatment centers offering both products. Carvykti's advantage is structural: it won second-line approval, while Abecma is limited to third-line and later use. BMS took a one-hundred-and-twenty-two-million-dollar impairment charge on Abecma in the fourth quarter of 2024 and acquired its partner 2seventy bio for two hundred and eighty-six million to gain full manufacturing control.

BMS's competitive response has been to look beyond the current CAR-T paradigm entirely. In October 2025, the company acquired Orbital Therapeutics for one point five billion dollars, gaining access to an in-vivo CAR-T reprogramming platform using circular RNA technology.

Instead of extracting a patient's T cells, reprogramming them in a factory, and infusing them back (a process that takes weeks, costs over four hundred thousand dollars per treatment, and requires specialized manufacturing), in-vivo CAR-T aims to inject RNA-containing nanoparticles directly into the patient's bloodstream, reprogramming T cells inside the body.

If it works, it could democratize cell therapy by eliminating the manufacturing bottleneck and dramatically reducing costs. Think of it as moving from custom-built artisanal weapons to mass-produced ammunition. The lead asset, OTX-201, targets autoimmune diseases rather than cancer, extending cell therapy into an entirely new therapeutic area.

The Novartis Kymriah experience offers a cautionary tale in the CAR-T space. Once heralded as the first-ever FDA-approved CAR-T therapy in 2017, Kymriah's revenue has declined from five hundred and thirty-six million in 2022 to four hundred and forty-three million in 2024, hampered by manufacturing problems and a failed clinical trial in second-line lymphoma. Kymriah's struggles demonstrate that being first to market in cell therapy does not guarantee long-term success. The technology is complex enough that manufacturing reliability and clinical expansion matter far more than first-mover advantage.

The broader oncology landscape features intense competition from AstraZeneca, whose oncology franchise grew to twenty-two billion in 2024 driven by Enhertu (up forty-eight percent) and Imfinzi (up fifty-two percent), and Pfizer, which is rebuilding through the forty-three-billion-dollar Seagen acquisition that added antibody-drug conjugates like Padcev. Roche is managing a painful transition as biosimilars erode its legacy blockbusters Avastin, Herceptin, and Rituxan. BMS sits in a strong second position in global oncology revenue behind only Merck but faces the most acute near-term patent cliff risk of any major player.

Only AbbVie's acquisition of Allergan for sixty-three billion dollars rivaled the size of BMS's Celgene deal, and comparing the two mega-mergers is instructive. AbbVie was explicitly buying current revenue, specifically Botox and the aesthetics franchise, to diversify away from Humira dependency. BMS was making a pipeline bet, acquiring Celgene primarily for its near-term launches and R&D potential.

Five years in, both deals have delivered mixed results. BMS's growth portfolio is generating twenty-two-plus billion and growing at seventeen percent, vindicating the pipeline thesis. AbbVie's aesthetics franchise has underperformed, with the company revising its target downward from nine billion to "north of seven billion" by 2029.

The lesson: in pharma mega-mergers, buying innovation often outperforms buying mature revenue, but both strategies carry significant execution risk.

VIII. Playbook: Lessons in Pharmaceutical Strategy

BMS's hundred-and-sixty-year history distills into a set of strategic lessons that apply broadly to pharmaceutical companies navigating the perpetual challenge of patent cliffs and portfolio renewal.

The first lesson is about timing in mega-mergers. BMS acquired Celgene when both companies were at or near their lowest ebb, a contrarian moment that maximized the potential upside while exposing BMS to maximum criticism. The stock dropped fifteen percent on announcement day. Wellington and Starboard publicly opposed the deal. But by buying when sentiment was terrible, BMS secured Celgene's pipeline at a valuation that reflected the market's fear rather than the portfolio's potential. Caforio's willingness to absorb short-term pain for long-term strategic positioning stands in contrast to deals made at the top of the cycle, which tend to leave acquirers paying peak multiples for assets whose growth is already priced in.

The second lesson concerns the build-versus-buy innovation model. BMS's String of Pearls strategy, pioneered under Jim Cornelius and continued by his successors, demonstrates the advantages of targeted acquisitions over internal R&D alone.

The two-point-four-billion-dollar Medarex acquisition in 2009 yielded Yervoy and Opdivo, drugs that have generated tens of billions in cumulative revenue. The fourteen-billion-dollar Karuna acquisition delivered Cobenfy, potentially the first new schizophrenia mechanism in seventy years. The four-billion-dollar RayzeBio deal positioned BMS in radiopharmaceuticals, a modality that barely existed commercially five years ago.

The pattern is consistent: BMS identifies promising science at the biotech stage, acquires it, then applies its large-company capabilities in clinical development, regulatory navigation, manufacturing, and global commercialization to drive scale. The catastrophic exception was Inhibitex, whose lead hepatitis C drug failed in clinical studies after a two-point-five-billion-dollar acquisition. Even the best acquisition strategies carry binary clinical risk.

The third lesson is about portfolio management in the face of patent cliffs. BMS has now navigated three major patent cliffs: Plavix and Abilify in the early-to-mid 2010s, Revlimid starting in 2022, and the upcoming Eliquis and Opdivo expirations around 2028. Each time, the company has used a combination of new launches, lifecycle management (like subcutaneous Opdivo Qvantig), cost restructuring, and strategic acquisitions to bridge the revenue gap. The playbook is consistent: cut costs aggressively, invest heavily in R&D to fill the pipeline, and use the balance sheet for acquisitions that bring near-term revenue potential rather than speculative early-stage science.

The fourth lesson addresses regulatory and pricing navigation. The Inflation Reduction Act's Medicare drug price negotiation provisions, which reduced Eliquis's Medicare price by fifty-six percent starting in 2026, represent a new structural challenge for the industry. BMS's response has been pragmatic: rather than fighting the lower price, management has reframed it as a volume catalyst, arguing that lower out-of-pocket costs will bring more Medicare patients onto Eliquis. Whether this proves correct will be closely watched as a precedent for the entire pharmaceutical industry as more drugs enter Medicare negotiation in subsequent years.

The fifth lesson concerns cost structure optimization during periods of revenue pressure. BMS's approach to cost-cutting during the patent cliff is notable for its ambition: three point five billion dollars in targeted savings represents roughly seven percent of total revenue. The company is making difficult choices, including exploring the sale-leaseback of its Summit, New Jersey campus and reducing its workforce by thousands. But it has deliberately protected R&D spending, which increased twenty percent in 2024 to eleven point two billion dollars. The message to investors and employees is clear: we will cut everything except the one thing that generates our future revenue. Whether this balance is sustainable remains to be seen, but the strategic logic is sound. In a patent-driven business, cutting R&D to meet near-term earnings targets is slow corporate suicide.

The sixth lesson is perhaps the most painful: the CheckMate-026 failure illustrates how a single clinical trial design decision can reshape competitive dynamics for a decade. BMS's choice to study Opdivo in a broad, biomarker-unselected population while Merck chose a biomarker-enriched design was not a mistake of execution but of strategy. BMS believed in the broad-population thesis; Merck bet on precision. The lesson is not that BMS's drug was inferior, there is no evidence it was, but that clinical trial strategy is a competitive weapon every bit as powerful as the molecule itself. For investors evaluating pharmaceutical companies, understanding how a company designs its trials is as important as understanding the science behind its drugs.

IX. Financial Analysis & Investment Thesis

BMS's financial profile reflects a company in mid-transition between two eras. Full-year 2024 revenues of forty-eight point three billion grew seven percent, and full-year 2025 revenues came in at forty-eight point two billion, essentially flat. Guidance for 2026 calls for forty-six to forty-seven and a half billion, a modest decline that reflects Revlimid's continued generic erosion partially offset by growth portfolio momentum and Eliquis volume gains from Medicare price negotiations.

The company invested eleven point two billion dollars in R&D in 2024, representing roughly twenty-three percent of revenue, a high ratio that signals the intensity of BMS's effort to outrun its patent cliffs. Cash flow generation remains robust: BMS has used its cash flows to reduce the massive debt load from the Celgene acquisition while simultaneously funding three major acquisitions in 2024 alone (Karuna for fourteen billion, RayzeBio for four billion, and Mirati for four point eight billion). The three-point-five-billion-dollar combined cost reduction program provides additional financial flexibility.

Understanding BMS's competitive position requires looking beyond traditional financial metrics to analyze the structural forces shaping its industry.

A framework analysis reveals both BMS's competitive strengths and vulnerabilities. In terms of market structure, pharmaceutical companies benefit from extraordinarily high barriers to entry: drug development costs one to three billion per approved product, regulatory timelines span ten to fifteen years, and patent protection creates legal monopolies.

Buyer power, however, is high and increasing. PBMs, government payers, hospital group purchasing organizations, and now the IRA's direct Medicare negotiation all compress pricing. Competitive rivalry in oncology is the most intense in any therapeutic area, with Merck, AstraZeneca, Roche, Pfizer, and Johnson & Johnson all fighting for the same patient populations with overlapping modalities. The threat of biosimilar and generic substitution is the most material near-term risk for BMS.

Applying Hamilton Helmer's Seven Powers framework sharpens the competitive picture further.

BMS has moderate scale economies, sufficient to run large global clinical trials and manufacture complex biologics, but it is not the largest pharma company, and competitors like Merck, Roche, and Pfizer operate at comparable or greater scale. Network effects are essentially absent in pharmaceuticals; more patients using Opdivo does not inherently make it more valuable to the next patient, unlike a social network or marketplace.

Counter-positioning, the ability to adopt a strategy that incumbents find difficult to replicate, was evident in BMS's early entry into immuno-oncology and CAR-T cell therapy, but competitors have now largely caught up. Switching costs are real but eroding: once Opdivo or Eliquis is established in treatment guidelines, physicians are reluctant to change, but generic and biosimilar competition eventually overcomes that inertia.

Branding matters in the sense that oncologists trust BMS's clinical data and support programs, but pharmaceutical prescribing is fundamentally evidence-based, and clinical trial results ultimately trump brand loyalty.

BMS's most defensible competitive asset is what might be called cornered resources: its patent portfolios, proprietary clinical trial databases spanning decades of CheckMate trials across dozens of tumor types, specialized CAR-T and radiopharmaceutical manufacturing capabilities, and deep relationships with oncology key opinion leaders worldwide.

These are difficult for competitors to replicate, but they are also time-decaying. Patents expire, competitors build manufacturing capacity, and clinical data can be superseded by newer trials. BMS's process power in managing complex drug development, regulatory submissions, and M&A execution provides a secondary competitive advantage, but one that other large pharma companies can match.

The overall picture is a company with meaningful but time-decaying competitive advantages. BMS's moat is real but narrow: it consists primarily of patent protection, proprietary data, and specialized manufacturing know-how, all of which erode over time unless continuously replenished through R&D and acquisitions. This is the fundamental tension of the pharmaceutical business model: your most valuable assets are literally designed to expire.

The bear case centers on arithmetic. Eliquis and Opdivo together generated approximately twenty-four billion in 2025 revenue. Both face U.S. exclusivity losses around 2028. Historical patterns suggest generic and biosimilar competition can erode eighty to ninety percent of branded revenue over several years. The growth portfolio, while impressive at twenty-two-plus billion, would need to essentially double to fully offset these losses, a feat requiring sustained high-teens growth rates for several years.

Additional bear case risks include integration fatigue from multiple large acquisitions in rapid succession (Karuna, RayzeBio, and Mirati all in 2024 alone), the Cobenfy launch trajectory underperforming expectations if prescribing habits prove stickier than anticipated, and the ADEPT-2 trial in Alzheimer's psychosis failing, which would narrow Cobenfy's addressable market. Regulatory risk is also material: the IRA's Medicare negotiation framework will expand to more drugs in future years, potentially affecting Opdivo and growth portfolio products. And the competitive environment is intensifying: AstraZeneca, Pfizer, and emerging Chinese biopharma companies are all investing heavily in oncology.

The bull case rests on pipeline potential and proven execution. BMS has six pivotal trial readouts expected in 2026. Cobenfy addresses a thirty-billion-dollar-plus schizophrenia market with the first new mechanism in seventy years. Breyanzi is growing at over one hundred percent annually and expanding into new indications.

The Opdivo Qvantig subcutaneous formulation and lifecycle management strategies could slow biosimilar erosion. The BioNTech partnership positions BMS for next-generation immuno-oncology. And the radiopharmaceutical platform acquired through RayzeBio represents an emerging modality with limited competition.

BMS has proven it can execute large acquisitions and successfully launch new products, with nine post-merger launches already generating meaningful revenue.

The two KPIs that matter most for tracking BMS's ongoing performance are:

First, Growth Portfolio revenue growth rate, which measures whether the newer products are scaling fast enough to offset legacy declines.

Second, the ratio of Growth Portfolio to Legacy Portfolio revenue, which indicates how close BMS is to completing its portfolio transition. In 2024, the Growth Portfolio represented eighty-eight percent of the Legacy Portfolio's revenue. When that ratio approaches or exceeds one-to-one, BMS will have largely navigated its transition.

Full-year 2025 non-GAAP EPS came in at six dollars and fifteen cents, and 2026 guidance of six-oh-five to six-thirty-five suggests management expects to hold earnings relatively stable through the initial phase of the patent cliff, supported by cost cuts and growth product acceleration.

X. Looking Forward: The Next Chapter

Chris Boerner took over as CEO in November 2023, becoming the first BMS chief executive whose career was built entirely in commercial roles rather than R&D or general management.

An Arkansas native with a PhD from UC Berkeley's Haas School of Business, where he researched how organizational factors influence biotech drug development, Boerner spent eight years at Genentech in marketing leadership and then moved to Seattle Genetics before joining BMS in 2015. His appointment was a deliberate board decision: the company needs a commercially oriented leader to navigate a launch-heavy, transition-intensive period.

Boerner has emphasized company culture as the "missing piece" of the patent cliff management plan, arguing that execution and employee engagement matter as much as the pipeline itself.

The pipeline assessment heading into 2026 includes several potential catalysts.

The ADEPT-2 trial testing Cobenfy in Alzheimer's disease psychosis, delayed due to site irregularities but expected to deliver data by end of 2026, could meaningfully expand Cobenfy's addressable market if successful. The Alzheimer's psychosis market is substantially larger than schizophrenia, and success here would transform Cobenfy's revenue trajectory.

The ALOFT-IPF Phase 3 trial of admilparant in idiopathic pulmonary fibrosis addresses an unmet need in a disease with limited effective treatments. Iberdomide, a next-generation CELMoD protein degrader for multiple myeloma, showed significant improvement in measurable residual disease negativity in the Phase 3 EXCALIBER-RRMM trial. Six pivotal readouts in total are expected in 2026.

Computational drug discovery and artificial intelligence are becoming increasingly important to BMS's R&D strategy. The company has partnered with Evinova to incorporate AI tools in clinical trial design and has pledged to invest forty billion dollars in U.S. R&D and manufacturing over time. BMS's acquisition of Orbital Therapeutics' circular RNA platform represents a bet on programmable biology, the idea that diseases can be treated by delivering genetic instructions to reprogram the body's own cells. If the in-vivo CAR-T approach works, it could fundamentally alter the economics of cell therapy and potentially position BMS ahead of competitors still relying on expensive, individualized ex-vivo manufacturing.

One underappreciated aspect of BMS's strategy is its multi-modality approach to drug development. The company is simultaneously pursuing checkpoint immunotherapy (Opdivo, the BioNTech partnership), cell therapy (Breyanzi, Abecma, Orbital's in-vivo platform), radiopharmaceuticals (RayzeBio), targeted small molecules (Krazati, Augtyro), protein degraders (iberdomide), and muscarinic agonists (Cobenfy). This breadth is unusual among pharmaceutical companies, which tend to concentrate in one or two modalities. The strategic rationale is hedging: by maintaining competence across multiple drug development platforms, BMS reduces the risk that any single modality proves less effective than expected. The tradeoff is complexity. Running this many different types of programs simultaneously requires diverse scientific talent, varied manufacturing capabilities, and management bandwidth that can be stretched thin.

The international dimension of BMS's strategy is evolving. Cobenfy's UK launch is planned for 2026. The company derived fourteen point two billion dollars in international revenue in 2024, with eight percent ex-currency growth suggesting ongoing demand outside the U.S. The international market matters increasingly as domestic pricing pressure intensifies under Medicare negotiation.

What does success look like in 2030? Management would point to a fully transitioned portfolio in which the growth products collectively exceed thirty-plus billion in annual revenue, Cobenfy has established itself across multiple psychiatric indications, Opdivo's franchise persists through subcutaneous formulations and next-generation combinations, and one or more pipeline assets (radiopharmaceuticals, bispecifics, in-vivo CAR-T) have achieved blockbuster status.

The bear scenario involves growth product scaling falling short of the replacement math, Cobenfy failing to overcome prescribing inertia, and biosimilar and generic competition eroding legacy revenues faster than new products can fill the gap.

Bristol-Myers Squibb has been reinventing itself since two fraternity brothers bought a failing drug company with horse-and-buggy distribution in 1887. From toothpaste and laxatives to penicillin and hair dye, from ACE inhibitors and checkpoint immunotherapy to muscarinic agonists and in-vivo cell reprogramming, the company has survived by placing bold bets at moments of maximum uncertainty.

Whether the current bet, the biggest yet, pays off will depend on whether the growth portfolio can clear the highest patent cliff in pharmaceutical history. The math is daunting. But then again, buying a failing drug company with no pharmaceutical expertise and five thousand dollars apiece was daunting too.

XI. Recent News

Q4 2025 / Full-Year 2025 Results (reported February 5, 2026): BMS reported full-year 2025 revenue of forty-eight point two billion dollars, essentially flat with 2024, and non-GAAP EPS of six dollars and fifteen cents. The Growth Portfolio grew seventeen percent for the full year, while the Legacy Portfolio declined.

Fourth-quarter revenue of twelve point five billion included Opdivo at two point six nine billion (up nine percent), Eliquis at three point four five billion (up eight percent), and Breyanzi at three hundred and ninety-two million (up forty-nine percent). BMS issued 2026 guidance of forty-six to forty-seven point five billion in revenue and non-GAAP EPS of six-oh-five to six-thirty-five, meaningfully above analyst consensus.

Cobenfy Launch Update: Full-year 2025 Cobenfy revenue totaled approximately one hundred and fifty-six million dollars across all four quarters, with steady quarterly growth from twenty-seven million in Q1 to fifty-one million in Q4. Weekly prescriptions surpassed sixteen hundred by mid-2025, though management acknowledged slower-than-hoped uptake driven by entrenched prescribing habits in schizophrenia.

The ARISE adjunctive therapy trial failed, but fourteen other studies remain ongoing or planned, including the pivotal ADEPT-2 trial in Alzheimer's psychosis with data expected by end of 2026.

Opdivo Qvantig Approval: FDA approved the subcutaneous formulation of Opdivo in December 2024, offering three-to-five-minute administration versus the thirty-minute IV infusion. EU approval followed in 2025. This lifecycle management strategy is designed to retain patients as IV biosimilars enter the market.

BioNTech Partnership (June 2025): BMS entered an eleven-point-one-billion-dollar collaboration with BioNTech to co-develop BNT327, a next-generation PD-L1/VEGF-A bispecific antibody for solid tumors, positioning for the post-Opdivo competitive era.

Orbital Therapeutics Acquisition (October 2025): BMS acquired Orbital for one point five billion dollars, gaining in-vivo CAR-T reprogramming technology using circular RNA, with lead asset OTX-201 targeting autoimmune diseases expected to enter clinical trials in 2026.

Cost Reduction Expansion (February 2025): BMS expanded its cost-cutting program by an additional two billion dollars, bringing total targeted savings to three point five billion by end of 2027.

Stock Performance: BMS shares traded around sixty-one dollars as of mid-February 2026, with a market capitalization of approximately one hundred and twenty-four billion dollars and a fifty-two-week range of forty-two fifty-two to sixty-three thirty-three.

XII. Links & Resources

- BMS Annual Reports and Investor Presentations: bms.com/investors

- BMS Q4 2025 Earnings Press Release (February 5, 2026): news.bms.com

- SEC Filings: sec.gov/cgi-bin/browse-edgar?company=bristol+myers&CIK=&type=10-K

- Cobenfy FDA Approval Letter (September 26, 2024): accessdata.fda.gov

- Opdivo Qvantig FDA Approval (December 27, 2024): accessdata.fda.gov

- Celgene Acquisition Proxy Statement (2019): sec.gov

- FTC Otezla Divestiture Order: ftc.gov/news-events (November 2019)

- KEYNOTE-024 Trial Publication: New England Journal of Medicine (2016)

- CheckMate-026 Trial Publication: New England Journal of Medicine (2017)

- "How Biomarkers Cost Bristol-Myers the Lung Cancer Market" - BioPharma Dive

- "A Decade of Cancer Immunotherapy" - BioPharma Dive

- "Bristol-Myers Squibb's Acquisition of Celgene: A 5-Year Retrospective" - Inovia Bio

- Medicare Negotiated Drug Prices for 2026: aspe.hhs.gov

- "From Snake Venom to ACE Inhibitor: The Discovery and Rise of Captopril" - The Pharmaceutical Journal

- History of Bristol-Myers Squibb Company - FundingUniverse

- Edward Robinson Squibb Biography - Encyclopedia.com

- National Medal of Technology Citation (1998): nationalmedals.org

- CAR-T Cell Therapy Market Report - Grand View Research

- BMS Pipeline Overview: bms.com/researchers-and-partners/in-the-pipeline

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube