Bajaj Mobility AG: The Ultimate Rescue of Europe's Premium Motorcycle Empire

I. Introduction & Episode Roadmap

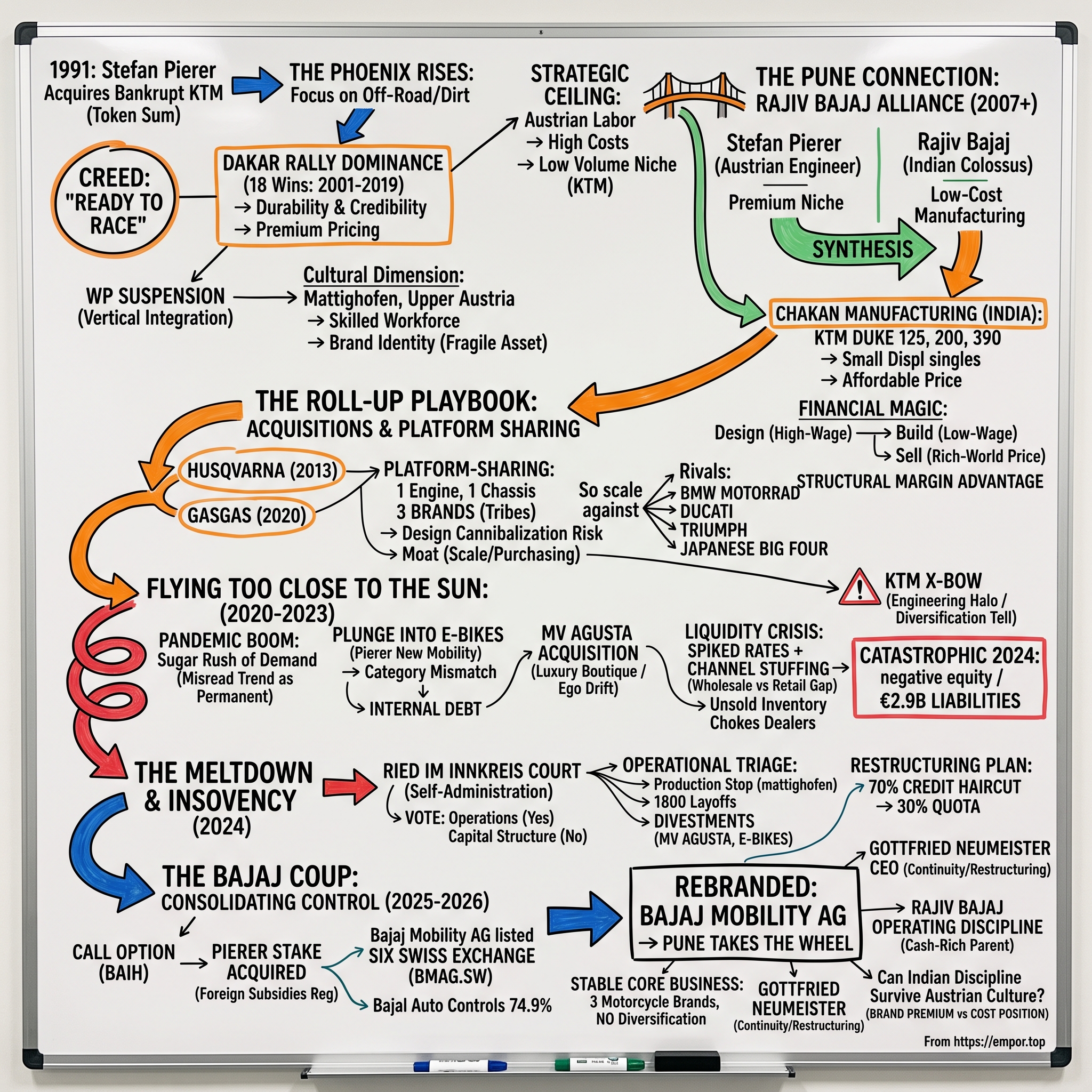

Picture the scene inside the Ried im Innkreis regional court in Upper Austria on a grey morning in late November 2024. In a room more accustomed to routine commercial disputes, lawyers filed paperwork that would make history for all the wrong reasons: KTM AG, the orange-clad crown jewel of European motorcycling, the maker of the machines that had won the Dakar Rally eighteen years running, was seeking court protection from its creditors. The reported liabilities read like a misprint — roughly €2.9 billion.1 It was the largest industrial insolvency Austria had ever seen. And the company that would eventually walk away owning it was not a German rival, not a private-equity fund from London or New York, but a family-controlled motorcycle manufacturer headquartered eight thousand kilometres away in Pune, India.

This is the story of how that happened — and of the company that emerged from the wreckage. As of January 13, 2026, the entity once known as PIERER Mobility AG trades on the SIX Swiss Exchange under a new name and ticker: Bajaj Mobility AG, BMAG.SW.2 Behind it sits a reconstituted ownership chain in which Bajaj Auto Limited of Pune, through its Dutch subsidiary Bajaj Auto International Holdings B.V., controls 100% of the intermediate holding company and, through it, a 74.9% controlling interest in the listed parent of KTM, Husqvarna, and GASGAS.3

The central paradox is almost operatic. Here was a brand built on the philosophy of "Ready to Race" — a company whose engineers obsessed over shaving grams off a rally bike's subframe, whose orange became a tribal identity for off-road riders worldwide. And yet it did not crash on a mountain stage in the Atacama. It crashed on the far more treacherous terrain of its own balance sheet: a decade of debt-fuelled roll-ups, a pandemic-era sugar rush of demand that management mistook for permanent, tens of thousands of unsold motorcycles stuffed into a bloated dealer network, and a vanity foray into electric bicycles that quietly bled cash until it couldn't be hidden any longer.

Our roadmap runs the full arc. We begin with Stefan Pierer buying a bankrupt motorcycle company for a token sum in 1991 and rebuilding it into a racing legend. We trace the 2007 alliance with Rajiv Bajaj — one of the most productive East-West industrial partnerships of the century, hidden in plain sight inside every KTM Duke sold in an emerging market. We walk through the aggressive acquisition years, when Pierer bolted Husqvarna, GASGAS, WP Suspension, and eventually a slice of MV Agusta onto the group. We examine how a boom became a bubble, how the bubble became an insolvency, and how a brutal Austrian court process handed creditors a 70% haircut. And we end with the November 2025 corporate coup and the disciplined Indian operating culture now attempting to run the crown jewels of Austrian engineering.

Throughout, we will keep an independent posture. Management now speaks of a "successful turnaround," and the early numbers do show a genuine operational recovery.4 But a turnaround is a claim about the future dressed up as a fact about the present, and our job is to separate the two — to ask what the evidence actually supports, and what could still break the case.

There is a deeper reason this story matters beyond the fate of one motorcycle maker. For most of the industrial era, the flow of corporate control ran in one direction: European and American capital acquiring, restructuring, and operating the productive assets of the developing world. What happened to KTM inverts that arrow. A family-controlled manufacturer from an Indian city that most European riders could not place on a map ended up owning the company whose bikes hung on their bedroom walls as teenagers. If you want to understand where global industrial power is drifting in the 2020s, the ledger of the Ried im Innkreis court is a surprisingly good place to start. Keep three questions in mind as we go. Why did a company with genuine engineering superiority and a fanatically loyal customer base still manage to nearly destroy itself? What, precisely, does Bajaj now own — a brand, a factory network, a cost advantage, or all three? And can the discipline that made Bajaj rich in India survive contact with the expensive, proud, unionised engineering culture of Upper Austria?

II. The Phoenix of Mattighofen: Stefan Pierer's Ready-to-Race Rise (1991–2006)

In 1991, the town of Mattighofen was watching its most important employer die. Kronreif & Trunkenpolz Mattighofen — KTM, the initials of its founders and its home town — had been building motorcycles since the 1950s, but by the early 1990s it was insolvent, hollowed out by a bloated product range and a collapsing market. Into this walked Stefan Pierer, a young Austrian mechanical engineer who had made his early money not in motorcycles at all but in industrial heating systems through his firm Pierer Industrie. He was, by temperament, a turnaround operator: unsentimental, numbers-driven, and allergic to complexity. He bought the motorcycle division out of the ashes for what amounted to a symbolic price and set about doing the one thing the old KTM had failed to do — pick a lane.

The lane he picked was dirt. Rather than chase the Japanese giants across the vast, low-margin street-bike market, Pierer bet the company on off-road: motocross, enduro, and the punishing world of rally raid. Out of this focus came a phrase that would become less a slogan than a creed — "Ready to Race." The idea was radical in its simplicity. Every machine that left Mattighofen should feel like a competition bike you could buy in a showroom. The brand's signature orange stopped being a paint choice and became a tribe. For a certain kind of rider, an orange bike signalled that you were serious.

Understanding Pierer's temperament is essential to understanding both the rise and the eventual fall. He was not a rider first and a businessman second, in the mould of many motorcycle-industry founders. He was the reverse: a numbers man who happened to have bought a motorcycle company, and who ran it with the cold logic of a portfolio operator. His holding structure — Pierer Industrie AG at the top, with cascading stakes down into the operating businesses — reflected a financier's instinct for control through layered ownership rather than a factory boss's instinct for the shop floor. That instinct built an empire. It also, years later, built the leverage that would nearly bury it. But in the 1990s and early 2000s, the discipline was exactly what a bloated, dying KTM needed. He cut the range, focused the engineering, and pointed the entire company at winning races.

Nothing cemented that reputation like the Dakar Rally, the most brutal test in motorsport — thousands of kilometres across desert and dune where finishing is an achievement and machinery is destroyed daily. Beginning in 2001, KTM won the motorcycle category. And then it kept winning — eighteen consecutive years, through 2019, a streak recognised by Guinness World Records as the most dominant in the event's history.5 Each January, the orange bikes came home first, and each victory was worth more than any advertising campaign could buy. Durability and engineering credibility are precisely the attributes a premium motorcycle buyer is paying for, and KTM was demonstrating them in the harshest imaginable laboratory. There is a specific commercial mechanism at work here that is easy to miss. In off-road motorcycling, the buyer often is the racer — the weekend enduro rider, the club-level motocrosser — and that buyer treats a factory's competition record as a direct proxy for how the bike will hold up under his own abuse. Racing wasn't marketing spend for KTM; it was product validation performed in public, and it justified a price premium that pure specification sheets never could.

To control the ride quality that underpinned all of this, Pierer pulled a key supplier in-house: WP Suspension, the Dutch-Austrian maker of high-performance forks and shocks. Owning the suspension meant owning a decisive part of how the bikes felt on the ground — vertical integration in the service of a very specific competitive edge.

There was a cultural dimension to all of this that would matter enormously later. Mattighofen became a company town in the truest sense — a place where thousands of skilled Austrian engineers, machinists, and designers built their careers and their identities around the orange brand. The "Ready to Race" ethos was not a poster in the lobby; it was a hiring filter and a retention tool. People who worked there believed they were building the best off-road motorcycles in the world, and for two decades they largely were. That intangible — a workforce that identifies with the product at an almost religious level — is a genuine asset. It is also fragile, and it does not appear on any balance sheet. When ownership eventually passed to a parent eight thousand kilometres away that talked in the language of cost per unit and stock turns, this was precisely the asset most at risk.

But there was a ceiling built into the model, and Pierer knew it. World-class engineering executed with high-cost Austrian labour produces wonderful motorcycles at painful unit economics. Premium pricing kept volumes low; low volumes kept fixed costs spread thin. A factory that builds forty thousand premium bikes a year can never enjoy the purchasing power, the tooling amortisation, or the supplier leverage of one that builds four million. By the mid-2000s KTM was the undisputed king of a valuable niche and a bit player in the market that actually moved millions of units a year — the entry-level and mid-displacement street bikes of Asia and Latin America, where a new middle class was buying its first powered two-wheeler by the tens of millions. KTM had the brand and the engineering to sell into that market; what it lacked was any way to build a motorcycle cheap enough that an aspiring rider in India or Indonesia or Brazil could actually afford it. To break the ceiling, Pierer needed something he could not build in Mattighofen: scale, and a partner with a radically different cost structure. That partner was about to arrive from India.

III. The Pune Connection: Rajiv Bajaj and the 2007 Alliance

The meeting of Stefan Pierer and Rajiv Bajaj is one of those industrial pairings that looks obvious only in hindsight. On one side, an Austrian engineer running a premium niche brand that could design brilliant engines but couldn't manufacture them cheaply. On the other, the managing director of Bajaj Auto — a Pune-based two-wheeler colossus that manufactured motorcycles by the millions at a cost base European rivals could scarcely comprehend, but whose own products lacked the high-performance engineering cachet that commanded premium prices. Each held exactly what the other lacked.

To understand why the alliance worked, you have to understand Rajiv Bajaj, who is one of the more idiosyncratic industrialists in Asia. He inherited a company synonymous with a single product — the humble scooter that had carried Indian families for generations, immortalised in the "Hamara Bajaj" ("Our Bajaj") advertising that made the brand a national institution. Rajiv's insight, pursued with almost obsessive conviction, was that Bajaj should abandon scooters entirely and become a specialist in motorcycles. He is famous for management ideas borrowed from unlikely places — he has spoken publicly of applying the principles of homeopathy and of strategic "specialisation" to business, of doing fewer things with more focus rather than spreading across every segment. That philosophy produced the Pulsar, the motorcycle that made performance biking aspirational for a generation of young Indians and transformed Bajaj from a scooter also-ran into a motorcycle powerhouse.

In 2007, Bajaj Auto took an initial minority stake in KTM — a bridgehead rather than a takeover, but the beginning of a deepening relationship that would run for nearly two decades.6 Rajiv Bajaj understood immediately what KTM's platform could do for his ambitions, and Pierer understood what Bajaj's factories could do for his margins. What is striking, and rare in cross-border industrial partnerships, is how disciplined the escalation was. Bajaj did not lunge for control. It took a stake, proved the manufacturing model, deepened the engineering collaboration, and only over many years lifted its economic interest — a patience that reflected Rajiv Bajaj's temperament and that, crucially, left him perfectly positioned when the crisis finally came. The eventual takeover was not a bolt from the blue; it was the last step of a courtship two decades long.

The synergy was almost too neat. What KTM needed was a way to build small-displacement bikes — 125cc to 400cc singles — at a price that emerging-market buyers could afford, without gutting the brand. What Bajaj needed was access to liquid-cooled, high-revving engine and chassis engineering to move its domestic Pulsar and Dominar ranges upmarket. The answer was a joint manufacturing arrangement at Bajaj's plant in Chakan, near Pune, where the KTM Duke 125, 200, and 390 would be assembled.

Here is where the financial magic happened, and it is worth slowing down to explain because it is the single most important mechanism in this entire story. KTM would design its performance engines in Austria, where the engineering talent lived. Bajaj would manufacture them in India, where the cost structure lived. And the finished bikes would sell across Europe, North America, and Asia at premium European prices. Design cost sits in a high-wage country; assembly cost sits in a low-wage country; revenue is collected at rich-world price points. Do that at scale and you have manufactured a structural margin advantage that a purely European competitor — building in Germany or Italy — simply cannot replicate.

The benefits flowed both ways, and this is the part often lost in the European telling of the story. Bajaj did not merely become KTM's low-cost factory; it absorbed KTM's engineering DNA into its own products. The Pulsar and Dominar lines climbed steadily upmarket, borrowing chassis philosophy, liquid-cooling expertise, and performance credibility from the Austrian collaboration. For Bajaj, the KTM relationship was a two-decade masterclass in high-performance motorcycle engineering that would have taken far longer and cost far more to develop from scratch. For KTM, Bajaj was the manufacturing arm that finally made the entry-level dream real. The KTM Duke 200 and 390, built in Chakan and sold across dozens of markets, did something no Mattighofen-built bike ever could: they put a genuine KTM within reach of a first-time buyer in a developing economy, seeding brand loyalty at the bottom of the pyramid that could migrate upward as riders grew richer and wanted bigger bikes.

The results validated the thesis. KTM's global unit sales climbed through the 2010s, and a growing majority of the group's volume came to be manufactured by Bajaj in India rather than in Mattighofen. Bajaj steadily lifted its economic interest toward roughly half of the holding structure, becoming not a passive investor but a co-owner and the group's manufacturing backbone. The Chakan line became the beating heart of KTM's mass-market volume, and by the late 2010s the two companies were so intertwined — shared platforms, shared roadmaps, shared factories — that it was no longer meaningful to describe them as separate businesses so much as two halves of one global operation with very different balance sheets.

The lesson an investor should draw is subtle. The alliance was a genuine and durable competitive advantage — a real edge, not a slogan. But it also created a dependency. KTM's premium brand equity was Austrian; its economics were increasingly Indian. For years that division of labour worked beautifully because the two partners' interests were aligned. The eventual insolvency would test what happened when one partner held the brand and the other held the factories — and the money.

IV. The Roll-Up Playbook: Resurrecting Brands & Platform Sharing

By 2013, Stefan Pierer had discovered something intoxicating: he was good at acquisitions. Not the megadeal kind, but the opportunistic capture of storied brands that larger, clumsier owners no longer wanted. And in early 2013, one of the most storied of all came onto the market. BMW, which had bought Husqvarna Motorcycles in 2007 and never quite figured out what to do with the Swedish-Italian heritage brand, agreed to sell it to Pierer Industrie AG. Both sides declined to disclose the price — a silence that itself told you the asset had changed hands cheaply.7

Husqvarna carried a heritage almost too rich for its own good. Founded as a Swedish arms manufacturer in the seventeenth century, it had built motorcycles since the early twentieth and dominated motocross in the 1960s and 70s before passing through a bewildering series of owners — the Italian Cagiva group, then MV Agusta's orbit, then BMW. Each owner had struggled to make the economics work, because Husqvarna suffered exactly KTM's original disease: a premium off-road brand without the volume to justify its own engineering. BMW, which had bought it in 2007 hoping to pivot it toward urban electric mobility, gave up within six years. That is the context for the undisclosed-but-clearly-cheap price: BMW was not selling an asset it valued, it was disposing of a problem.

What Pierer did with Husqvarna became the template for everything that followed. He did not spend years and fortunes developing a distinct Husqvarna engine and chassis. Instead he applied the platform-sharing playbook: take the proven KTM engine, gearbox, and frame, wrap them in Husqvarna's own bodywork and design language, position the result as the more sophisticated, design-led sibling to KTM's raw aggression, and sell it through a parallel dealer network. Two brands, two personalities, one set of expensive underlying components. The engineering was amortised across far more units than KTM alone could ever justify. This is a genuine strategic chess move, and it is worth naming the mechanism precisely: it is the automotive industry's badge-engineering logic — the same trick Volkswagen runs across VW, Audi, Škoda, and SEAT — imported into motorcycling. The risk of badge engineering is always brand cannibalisation and dilution, but in off-road, where riders segment sharply by discipline and self-image, KTM found it could sell the same hardware three times to three tribes that would never cross-shop.

The same logic drove the acquisition of GASGAS, the Spanish trials and enduro specialist, which Pierer's group brought into the fold around 2019 and 2020. Now there were three orange-adjacent brands — KTM the racer, Husqvarna the connoisseur, GASGAS the accessible entry point — riding on shared architecture. Each addressed a slightly different rider and price point; each fed volume back into the same components, the same WP suspension, the same purchasing contracts. The industrial moat here was real and mechanical: shared platforms meant enormous purchasing power in a specialised European high-performance supply chain, and the ability to launch a new model across three brands off a single engine program.

It is worth pausing on who this scale was aimed at, because the competitive set defines the whole strategy. At the premium end sat BMW Motorrad, the benchmark for big adventure-touring machines, and Ducati, the Italian performance icon backed by the deep pockets of Audi and the wider Volkswagen group. Triumph Motorcycles carried the British heritage banner. And looming over the entire industry were the Japanese "Big Four" — 本田技研工業株式会社 Honda Motor Co., Ltd., ヤマハ発動機株式会社 Yamaha Motor Co., Ltd., スズキ株式会社 Suzuki Motor Corporation, and 川崎重工業株式会社 Kawasaki Heavy Industries, Ltd. — whose combined manufacturing scale and reliability had defined mainstream motorcycling for half a century.

There was also a tell, a small one, that Pierer's ambitions were beginning to wander beyond the two-wheeler core: the KTM X-Bow, a radical, track-focused carbon-fibre sports car launched in 2008. It was a technical showpiece and a marketing halo, but it was also a sports car built by a motorcycle company — a hint of the founder's appetite for projects that flattered the brand's engineering ego more than they served its economics. In isolation it was a rounding error. As a pattern, it foreshadowed the far more expensive diversifications to come.

Against that field, Pierer's three-brand orange bloc plus the Bajaj manufacturing alliance had, for a moment, assembled something formidable: European engineering prestige married to Asian cost. The strategy was working. Group volumes were rising, the brands were distinct, and the platform-sharing genuinely lowered unit costs. For the long-term investor, the lesson of this era is that a real, mechanical competitive advantage had been assembled — not a narrative advantage but a cost-and-scale one that showed up in the unit economics. The danger — invisible in the good years — was structural to Pierer's own temperament. The same acquisitive, financially-minded instinct that captured Husqvarna cheaply and bolted on GASGAS and dabbled in sports cars could, in a euphoric market awash with cheap money, be turned toward assets that were neither cheap nor core. A founder who thinks like a portfolio manager will keep adding to the portfolio. That is exactly what happened next.

V. Flying Too Close to the Sun: E-Bikes, MV Agusta, and the Pandemic Hangover (2020–2023)

When the world locked down in 2020, something unexpected happened to the motorcycle business: it boomed. With gyms shut, travel banned, and disposable income piling up, consumers rediscovered the outdoors. Off-road riding — solitary, socially distant, exhilarating — was perfectly suited to the moment. KTM's order books swelled. Dealers couldn't get enough bikes. For a company built on the premise that off-road was a passionate niche, the pandemic looked like proof that the niche had gone mainstream. Management responded the way managements usually do at the top of a boom: by assuming it would last.

It is worth being fair to management about how convincing the boom looked from inside. This was not obvious folly at the time. Order books were genuinely full, waiting lists were genuinely long, and every competitor in the powersports industry was reading the same demand signals and reaching similar conclusions. The error was not optimism; it was the failure to ask the single question that separates a durable trend from a pull-forward: are these new riders, or are these existing riders buying earlier than they otherwise would have? A customer who buys his next bike in 2021 instead of 2024 does not represent growth. He represents a hole in 2024. Pandemic demand across the leisure-goods complex — boats, bicycles, RVs, motorcycles — was overwhelmingly the second kind, and the hole arrived precisely on schedule.

The clearest expression of that overconfidence was the plunge into electric bicycles. Pierer established Pierer New Mobility and expanded aggressively into high-end e-bikes, acquiring the American brand Felt Bicycles and launching electric bicycles under the Husqvarna and GASGAS names. The logic, on a slide, was seductive: e-bikes were the fastest-growing category in personal mobility, the brands could plausibly stretch into them, regulators across Europe were subsidising the category, and the future was electric. Any strategy consultant would have drawn the adjacency. The execution ran into a wall of category mismatch that no slide captured. The motorcycle business ran on distributor credit and dealership models — shipping product to dealers on generous terms and letting the channel carry inventory. Bicycles are a different animal entirely: lower price points, thinner margins, radically different retail channels, brutal seasonality, and — critically — a supply chain that during the pandemic ordered years of components in advance to escape shortages, then drowned in them when demand reversed. Applied to that industry, KTM's channel-financing model loaded risk into a network that had no capacity to absorb it. The group had exported its worst habit into its weakest business.

Then came the MV Agusta episode, which analysts would later single out as the emblematic misstep. Beginning in late 2022, the group bought into the ultra-luxury Italian marque, taking an initial 25.1% stake and lifting it to a controlling 50.1% by early 2024. The ambition was to add a jewelled top tier above KTM. The problem was that MV Agusta was a historically unprofitable boutique — a brand that had spent much of its modern life in financial distress — being acquired at precisely the moment KTM should have been hoarding cash. It had the hallmarks of an ego-driven acquisition: capital and management attention diverted into a prestige asset while the core generated warning signs.

Because by 2023, the core was flashing red. Interest rates had spiked across the developed world as central banks fought inflation, and the pandemic demand pull-forward reversed hard. A premium motorcycle is one of the most discretionary purchases in a household budget and is very often bought on credit; when financing costs double, the marginal buyer simply disappears. Consumers stopped buying big-ticket leisure machines. But KTM kept building and kept shipping.

To understand what happened next, it helps to understand how motorcycle companies actually book revenue — because this is the mechanism at the heart of the collapse, and it is genuinely counterintuitive. A manufacturer does not recognise a sale when a rider takes a bike home. It recognises the sale when the bike leaves the factory for the dealer. That shipment is called a wholesale. The rider's actual purchase is a retail sale, visible in registration data. In a healthy business, the two track each other. But a manufacturer under pressure can, for a while, manufacture its own revenue: keep shipping bikes to dealers, extend the credit terms so dealers don't have to pay for them yet, and book the wholesale as revenue. The reported numbers look fine. The bikes are simply sitting in a dealer's warehouse instead of the factory's. This is channel stuffing, and it is one of the oldest ways in industry to borrow from tomorrow's earnings to flatter today's.

KTM did exactly this, and at scale. It continued pushing motorcycles into its dealer network on extended credit lines, becoming — in effect — an unbacked bank to its own dealers, financing inventory that wasn't selling through to real riders. Wholesale numbers looked acceptable; retail registrations told the truth. The gap between the two was filling warehouses across Europe and North America with orange bikes nobody had yet bought. And channel stuffing has a vicious property: it is self-accelerating. Every quarter you do it, you need to stuff harder to hit the next quarter's number, because last quarter's stuffed inventory is now competing with your new bikes at the same dealer — often discounted, cannibalising the new model's price. The channel becomes both your customer and your competitor. There is no graceful exit; there is only the moment when the dealers stop accepting deliveries or the cash runs out, whichever comes first.

Meanwhile the e-bike venture had become a sinkhole. Pierer New Mobility piled up losses and, critically, owed a mountain of internal debt directly to KTM AG — a receivable that would ultimately be measured in the hundreds of millions of euros.8 The bicycle division was, quite literally, borrowing its survival from the motorcycle division that was itself running short of cash. When the group later confirmed it would exit the bicycle businesses entirely, the scale of the retreat was stark: bicycle and e-bike unit sales had already collapsed from about 155,859 in 2023 to 106,311 in 2024, roughly a third gone in a single year.8

A skeptical investor reading the disclosures in 2023 had the evidence available, if they knew where to look. The tell was never in the revenue line — it was in the divergence between wholesale shipments and registration data, and in the working-capital line, where inventory and receivables were ballooning relative to sales. Cash flow, not profit, is the lie detector in a channel-stuffing situation, because you cannot fake cash you have not collected. A company shipping bikes on credit to dealers who cannot sell them reports revenue and generates no cash. That divergence was visible well before the filing.

Stack these together — a demand cliff, a channel stuffed with unsold inventory, a cash-draining e-bike adventure, and a capital-consuming luxury acquisition — and you have the anatomy of a liquidity crisis in the making. The 2024 figures, when they came, were catastrophic: revenue down roughly 29% to about €1.9 billion from €2.7 billion in 2023, and shareholders' equity driven into negative territory at minus €199 million.8 Negative equity is not a soft signal. It means that if you sold everything the company owned at book value and paid off everything it owed, you would still be short — the shareholders' stake had been mathematically erased. Under EU financial rules, it triggered a legal obligation to convene an extraordinary general meeting.8

The pattern here is one long-term investors should learn to recognise, because it recurs across industries and generations. A company stops treating its core product as the engine of value and starts financialising itself — growth through debt-funded acquisition, earnings through channel manipulation, strategy through adjacency slides. Each individual decision has a defensible rationale. Collectively they describe a business that has lost the plot. Gravity always eventually wins. Gravity was about to arrive.

VI. The Meltdown: The 2024 Insolvency & Austrian Court Restructuring

By the autumn of 2024, the arithmetic no longer worked. Net debt had swollen to roughly €1.6 billion, equity had turned negative by December 31, and the group faced a liquidity cliff it could not climb.8 Under EU financial law, negative equity triggered emergency obligations. But the decisive moment came on November 26, 2024, when KTM AG and key component subsidiaries filed for court-supervised restructuring with self-administration at the regional court in Ried im Innkreis.1 With reported liabilities of roughly €2.9 billion, it was the largest industrial failure in Austrian corporate history — a national embarrassment centred on one of the country's proudest brands.

Self-administration is a specific and revealing choice, and it is worth explaining in plain terms because the mechanism shaped everything that followed. Think of it as the Austrian cousin of America's Chapter 11. Unlike a straight liquidation — where an administrator seizes the company, fires management, and sells the parts for whatever they'll fetch — self-administration lets existing management stay at the controls under court and administrator supervision while they attempt to negotiate a restructuring plan with creditors. The court is essentially making a judgment: this business is viable but its balance sheet is not, and the people who know how to build motorcycles should keep building motorcycles while the lawyers sort out the debt. It is a vote of confidence in the operations and a vote of no confidence in the capital structure — precisely the right diagnosis in KTM's case.

The clock, however, was merciless. Austrian restructuring rules gave the company a tight window, roughly 90 days from the formal start of proceedings in late November, to win creditor approval of a plan.9 Ninety days to persuade thousands of banks, bondholders, and suppliers — many of them small Austrian and German engineering firms for whom KTM's unpaid invoices were an existential matter — to accept a deal. The pressure this creates is deliberate. It forces a resolution before the enterprise value bleeds out, but it also hands enormous leverage to whoever can credibly promise the cash.

Spare a thought for the human dimension, because it is not incidental to the investment story. Mattighofen is a town of roughly six thousand people whose economic life had been organised around the orange factory for seventy years. The insolvency was not an abstraction there; it was neighbours, families, and a regional supply chain of small machining shops staring at ruin. Austrian political pressure to save KTM was intense, and that pressure was itself a factor in the negotiation — a reminder that in continental Europe, industrial restructuring is never a purely financial exercise.

That plan, when creditors approved it in late February 2025, was brutal in its arithmetic and blunt in its message.10 Creditors accepted a cash quota of 30% of their claims — which is another way of saying they agreed to write off 70% of what they were owed, one of the steepest haircuts a company of this size has ever imposed on its lenders and suppliers. To fund even that 30%, KTM AG had to deposit a very large sum — around €548 million — with the restructuring administrator by a hard deadline of May 23, 2025.9 Miss the deadline, and the whole plan collapsed back into full insolvency.

Consider what a 70% haircut actually means from the other side of the table. A supplier owed €10 million for parts already delivered received €3 million and wrote off the rest. Some of those suppliers were themselves pushed to the brink. That creditors nonetheless voted yes tells you something important about their alternative: in a liquidation, the recovery would have been worse. A motorcycle brand's value lives in its intellectual property, its racing heritage, and its dealer network — assets that evaporate the moment the company stops being a going concern. Nobody wants to own the Mattighofen tooling at auction. The creditors were not being generous; they were choosing 30% of something over a far smaller fraction of nothing. That is the brutal arithmetic that makes restructurings possible.

The operational triage running alongside the financial surgery was equally severe. The company cut its workforce hard — on the order of 1,800 jobs across the group — and pushed Mattighofen staff onto reduced hours.11 Most striking of all, it stopped building motorcycles. From December 2024 through March 2025, the Mattighofen assembly lines fell silent, deliberately idled so that the enormous glut of unsold bikes already sitting in the dealer network could clear. A motorcycle company that halts production for a quarter is doing something profoundly counterintuitive: it is admitting that its biggest problem is the inventory it already made. Every bike built during those months would have made the situation worse — more cash consumed, more units competing with the unsold stock already choking the channel. Stopping the line was the only rational move, and it was also a public confession of exactly how bad the channel stuffing had become. Production restarted in mid-March 2025.9

The divestments came fast. MV Agusta was sold back to the Sardarov family — the transaction completing on July 9, 2025, for a "mid double-digit million" euro figure, a quiet admission that the luxury adventure had destroyed rather than created value.12 The bicycle division was wound down and its assets, including Felt, shed. Everything non-core was jettisoned to concentrate cash and management on the one thing that still worked: building and selling motorcycles.

And yet all of this — the haircut, the layoffs, the production stop, the fire sale — still left one gaping hole. The 30% quota and the restart both required fresh liquidity the company did not have, a scramble for roughly €600 million by mid-2025.8 KTM had a viable plan on paper and no money to execute it. It needed a deep-pocketed rescuer willing to write a very large cheque. There was really only one candidate who already understood the business from the inside.

VII. The Bajaj Coup: Consolidating Control & The Rebranding of 2025–2026

For nearly two decades, Bajaj Auto had been the patient partner — the manufacturer, the co-owner, the presence that built the bikes but let the Austrians run the show. The insolvency changed the balance of power completely. When KTM needed capital that only a financially fortress-like parent could supply, the family from Pune finally moved to take the wheel.

The mechanism was a call option. On May 22, 2025, Bajaj Auto International Holdings B.V. — the group's Dutch vehicle, "BAIH" — signed a call option agreement with Stefan Pierer's Pierer Industrie AG, giving Bajaj the right to acquire all of Pierer Industrie's shares in Pierer Bajaj AG, the jointly-owned holding company sitting above the listed group.3 Pierer Industrie, itself weakened by the crisis, was in no position to refuse. After the European Commission cleared the transaction on November 10, 2025 — declining to prohibit it under the EU's foreign-subsidies regulation — Bajaj exercised the options in full.3

The regulatory dimension deserves a note, because it is a sign of the times. The European Commission reviewed the deal not only on ordinary competition grounds but under Regulation (EU) 2022/2560 — the foreign subsidies regulation, a relatively new instrument designed to scrutinise whether non-EU acquirers are being propped up by state support when they buy European assets.3 That Brussels examined an Indian family firm's purchase of an Austrian icon through this lens, and then declined to block it, is itself a small landmark: the EU looked hard at emerging-market capital acquiring European industrial heritage and concluded there was no basis to intervene.

On November 18, 2025, the deal completed. BAIH bought out the remaining 50.1% of the holding company it did not already own, lifting Bajaj's stake in that entity from 49.9% to 100%.3 The holding company, formerly Pierer Bajaj AG, was renamed Bajaj Auto International Holdings AG. Because that holding vehicle owned 74.9% of the listed parent, Bajaj now controlled 74.9% of KTM's ultimate parent outright, with roughly a quarter of the shares remaining in public free float on the SIX Swiss Exchange.3 The Pierer era of control was over.

The price tag tells its own story about what distress does to valuations. The equity purchases themselves were remarkably modest — the two-step acquisition of control was reported at roughly $58 million in total — while the real money went into the rescue: Bajaj committed on the order of €800 million in cash to settle creditors and restart production.22 Read that ratio carefully. Bajaj paid almost nothing for the shares and almost everything for the survival. That is what a controlling stake costs when the alternative is liquidation: the equity is nearly worthless, and the buyer's real consideration is the cheque that makes the enterprise viable again. For Bajaj, having spent eighteen years as the manufacturing partner, it was the cheapest possible route to owning outright a brand it had already helped build — provided the rescue worked.

The rebranding followed with almost ceremonial finality. On January 13, 2026, PIERER Mobility AG legally became Bajaj Mobility AG, and the ticker changed from PKTM to BMAG.2 The headquarters would remain in Mattighofen — the orange heart still beats in Austria — but the name over the door now belonged to Pune.2

The boardroom sweep had already begun. Stefan Pierer had stepped down as CEO on January 23, 2025, at the very depths of the crisis, replaced by Gottfried Neumeister, who had joined as co-CEO the previous September.13 By June 2025, with the restructuring proceedings concluded, Pierer left the executive board entirely.14 The supervisory board was reconstituted around Bajaj's nominees, including Pradeep Shrivastava, an executive director of Bajaj Auto, replacing the directors Pierer had installed.14 Pune's capital-allocation discipline now sat at the top of the governance chain.

The new leadership team is worth knowing. Gottfried Neumeister, the CEO steering the turnaround, is not a lifelong motorcycle man — and that may be the point. An International Business Administration graduate of the University of Vienna, he co-founded the low-cost airline flyniki with Formula 1 legend Niki Lauda in 2003, then spent years at catering giant DO & CO Aktiengesellschaft, rising to co-CEO.13 He is an operator and a cost surgeon, precisely the profile a distressed turnaround demands, and in January 2026 his contract was extended through the end of 2028 — a signal that Bajaj wants continuity, not a caretaker.15 Petra Preining, the CFO, was retained to enforce exactly the balance-sheet hygiene whose absence had nearly killed the company.4

Why is Bajaj the credible savior? Because its own operating record is the antithesis of what sank KTM. Bajaj Auto runs a cash-rich, effectively debt-free balance sheet in India and has for years posted EBITDA margins around 20% — in FY2026, a consolidated EBITDA margin of roughly 19% on record revenue of about ₹58,732 crore, with standalone profit after tax of ₹9,825 crore and consolidated PAT up 47% to ₹10,744 crore.16 It sold more than five million vehicles in the year, of which some 2.25 million were exports.16 These are not the numbers of a company that needs to borrow to grow. A firm that disciplined taking control of a firm that undisciplined is the entire investment thesis compressed into one sentence.

But the thesis has a hard edge worth naming now rather than later. Bajaj's margins were earned in a specific context: high-volume, low-displacement motorcycles built in India for Indian and emerging-market buyers, with a cost structure and a labour market that bear no resemblance to Upper Austria. It does not automatically follow that the same playbook produces 20% margins on premium European machines built by Austrian engineers under Austrian labour law. Capital discipline travels well — you can always refuse to fund a bad project from Pune. Operating culture travels far less well. The question is whether Bajaj's philosophy can be imposed on Mattighofen without destroying the thing that made the bikes worth a premium in the first place. That tension runs through the rest of this story, and it is not yet resolved.

VIII. Strategic & Financial Deep Dive: Porter's 5 Forces & Hamilton Helmer's 7 Powers

Strip away the drama and look at what Bajaj Mobility actually is today, financially, and a cleaner picture emerges. The 2025 annual report — the first under the Bajaj name, published March 26, 2026 — recorded revenue of €1.009 billion on 209,704 motorcycles, and a headline net profit of €590 million.4 But that profit is a mirage of accounting: it was driven by a one-off restructuring gain of €1.193 billion, the bookkeeping mirror image of the 70% debt that creditors forgave.4 Underneath the accounting windfall, revenue had fallen roughly 46% year on year and units dropped about 28% — the scars of the production halt and inventory purge, not the signs of a healthy business.4 What matters is what happened to the balance sheet and the trajectory: net debt was nearly halved to €798 million, equity was restored to €385 million (a 24.3% equity ratio), and inventory was slashed by 101,153 units, from 248,580 to 147,427.4 The company survived. Whether it thrives is a 2026 question.

The early 2026 data points toward genuine operational recovery rather than mere accounting cleanup. In Q1 2026, revenue jumped roughly 70% to €331.3 million, motorcycle units rose 125% to 40,332, and EBITDA turned positive at €5.5 million — a swing from an EBITDA margin of about −29% a year earlier to roughly +2%.17 The company was still loss-making at the bottom line — an EBIT loss of €26.1 million and a net loss of €35.1 million in the quarter — a reminder that "positive EBITDA" and "profitable" are not the same thing, and that depreciation, interest, and restructuring costs still outweighed the operating recovery.18 The Q2 2026 preliminary figures, released July 16, 2026, extended the trend: revenue of about €370 million (up from €231 million), units outside India up 71%, and an EBITDA margin near 8.7% versus a deeply negative figure a year before.18 The direction of travel is unmistakable — demand across KTM, Husqvarna, and GASGAS has come back, and dealers are ordering again.

The product strategy underpinning the recovery is deliberately un-flashy, and that restraint is itself a signal. Rather than chasing new segments, the 2026 plan leans on refreshing the core: new models like the KTM 990 RC R and the KTM 1390 Super Adventure S Evo, launched off the existing platform architecture, plus an extension of warranty coverage to four years on street-legal models — a low-cost, high-trust gesture aimed squarely at reassuring a dealer network and a customer base rattled by two years of turmoil.4 A four-year warranty is cheap to promise and powerful in perception: it tells a wavering buyer that the company expects to be around, and that it stands behind bikes built during and after the crisis. It is exactly the kind of confidence-rebuilding move a disciplined operator makes when the priority is stabilising demand rather than expanding it.

A word of caution on those growth rates, because they are the kind of numbers that can mislead an unwary reader. Revenue up 70% and units up 125% sound spectacular, but they are measured against a base quarter in which the factory was literally not running. Comparing 2026 to 2025 is comparing a functioning motorcycle company to one in the depths of a court-supervised production halt. The correct read is not "this business is growing at triple digits" — it is "this business has resumed operating." The more meaningful signal is the sequential trend and the margin trajectory: EBITDA moving from deeply negative to roughly break-even in Q1 and to nearly 9% by Q2 is genuine evidence that the cost base has been reset and that the bikes are selling through at acceptable prices rather than being dumped at a discount.1718 That said, an 8.7% EBITDA margin in a seasonally strong riding quarter is progress, not victory; the historical benchmark for this business is considerably better.

Segment reality. The core motorcycle division is now the sole engine of value, exactly as the crisis forced it to become. The non-core drags have been surgically removed: the e-bike business is fully written off and discontinued, eliminating a very large annual operating loss, and CFMOTO and other third-party Chinese-brand distribution was halted to concentrate on "the core business, the motorcycle business," as management put it on the Q1 2026 call.19 The margin recovery is being driven by inventory normalising — dealer stock returning from the absurd levels of 2023–24 toward healthy turns, which management now targets at more than 2x annually.17

A disclosure quirk worth flagging. On the Q1 2026 call, Neumeister made a revealing aside: the reported wholesale figures exclude units sold from India. "We sold 40,000 without India," he said, adding that Indian volumes had likely exceeded that.19 This matters analytically. It means the headline unit numbers reported by the listed entity understate the true global footprint of the KTM brand, because a large share of KTM-branded production and sale in India runs through Bajaj Auto rather than through Bajaj Mobility AG. An investor in BMAG.SW is therefore buying a claim on the European-and-export motorcycle business, not on the entirety of the KTM franchise worldwide. Where exactly the profit lands between the Pune parent and the Swiss-listed subsidiary — on transfer pricing for engines, components, and licensed brand use — is an intercompany judgment now made by a controlling shareholder that sits on both sides of the transaction. That is not an allegation of wrongdoing; it is a structural feature that minority shareholders should understand clearly.

Porter's Five Forces. Rivalry is high — Bajaj Mobility fights BMW Motorrad, Ducati, Triumph, and the Japanese Big Four in a mature market where demand is cyclical and interest-rate-sensitive. Supplier power is moderate-to-high — the bikes depend on specialised components from powerful suppliers like Bosch electronics and Brembo brakes, whose pricing the group does not control. Buyer power is moderate — enthusiast loyalty supports premium pricing, but the dealer network, freshly traumatised by channel stuffing and a production halt, is fragile, and dealers are the real buyers who can defect to rival franchises. Threat of substitutes and new entrants runs through cheaper Chinese manufacturers climbing the displacement ladder — the very partners KTM once relied on.

The force that deserves the most attention is the one Porter would classify under new entrants and substitutes, because it is the one actively changing. For years, the Chinese motorcycle industry was a source of cheap components and contract manufacturing — useful, unthreatening. That era is ending. CFMOTO, once KTM's manufacturing partner in Hangzhou, has been climbing the displacement and quality ladder with its own engineering, and it is not alone. The strategic problem for any premium Western brand is that the Chinese challengers are attacking from precisely the direction that KTM's own cost advantage came from: cheaper manufacturing, competent engineering, aggressive pricing in the mid-displacement segment. Bajaj Mobility's Indian cost base is a defence against this, but it is a defence, not an immunity.

Hamilton Helmer's 7 Powers sharpen the edge. The clearest is Scale Economies: the Pune manufacturing alliance gives Bajaj Mobility a structural unit-cost advantage in mid-displacement bikes that pure European peers cannot match — the design-in-Austria, build-in-India, sell-at-premium mechanism described earlier. Note the important caveat that the historic Hangzhou joint venture with 浙江春风动力股份有限公司 Zhejiang CFMOTO Power Co., Ltd. (春风动力 CFMOTO) wound down around 2025 as the Chinese partner developed its own engineering, so the China leg of the cost structure is diminishing, not growing.20 Branding is the second power: "Ready to Race," validated by eighteen Dakar wins and a record 29 motorsport titles in 2025, remains a durable, hard-to-replicate enthusiast identity.4 Process Power is the third: the proprietary platform-sharing R&D system that launches KTM, Husqvarna, and GASGAS models off shared architecture at a speed and cost rivals struggle to match. These are real powers — but two of the three (scale and process) depend on the Bajaj relationship that now also owns the company, which is both the source of the moat and a governance concentration.

It is equally instructive to note which of Helmer's powers Bajaj Mobility conspicuously lacks. There are no Switching Costs worth the name: a rider who owns a KTM today faces essentially no friction buying a Ducati next time. Nothing locks him in — no ecosystem, no data, no subscription, no installed base of accessories that couldn't be replaced. There is no Network Economy: a KTM does not become more valuable because other people bought KTMs, except in the soft, real, but easily-eroded sense of community and resale liquidity. There is no Cornered Resource — no patent thicket or exclusive input that rivals cannot access. And there is no Counter-Positioning, the power that protects a disruptor because incumbents cannot copy it without destroying their own business; every rival can and does pursue exactly the same platform-sharing and low-cost-manufacturing strategies. What this inventory reveals is important for anyone assessing the durability of the franchise: Bajaj Mobility's moat rests on brand affection and cost position. Those are genuine, but they are also the two moats most vulnerable to precisely the risks this company faces — brand affection can be spent, and cost position can be matched by manufacturers with even cheaper bases. The company must keep earning its position every single model cycle. There is no structural lock-in doing the work for it.

Management credibility, tested over time. For a business whose previous leadership presided over the largest industrial insolvency in Austrian history, the question of whether to believe management is not academic. The honest assessment is mixed but improving. On the positive side of the ledger, the current team has done what it said it would: it promised inventory reduction and delivered a cut of over 101,000 units; it promised refinancing and delivered a €550 million unsecured facility from a four-bank consortium on better terms than the Bajaj bridge it replaced; it promised divestment of non-core assets and actually sold MV Agusta, exited bicycles, dropped the X-Bow, and terminated third-party distribution.421 Promises kept are the currency of credibility, and this team has been paying. On the cautious side, guidance discipline remains untested — management declined to give explicit forward guidance on the Q1 call, which is defensible for a company mid-turnaround but means there is not yet a track record of setting targets and hitting them.19 Neumeister's language also runs warm; describing dealers as being "in a good mood" and claiming the group is "outperforming in terms of registration most of our competitors" are assertions without published evidence attached.19 The right posture is neither cynicism nor faith: watch whether the concrete promises keep getting kept.

IX. The Investment Case: Bull vs. Bear Case & Risk Radar

Here is the stress test a skeptical investor should run: can a premium Austrian heritage brand keep its soul — and its cult-like community of engineers and riders — under the direct control of a mass-market Indian corporate parent optimising for capital returns? The bull and bear cases both hinge on the answer.

The material risk radar. Three risks dominate, and each has a concrete business mechanism. First, dealer channel friction: the 2023–24 channel stuffing and the subsequent production halt did real damage to dealer trust, leaving some franchisees sitting on unsold, aging inventory and unpaid for months. Dealers who feel used can quietly shift showroom space and financing toward BMW or Ducati, and that erosion is slow, hard to reverse, and largely invisible until registrations soften. Management's claim on the Q1 2026 call that "the dealers are really in a good mood" and that the group is "gaining back market share" is encouraging but is a management assertion; the proof will be sustained retail registrations, not wholesale shipments.19 Second, execution and cultural risk: the exit of Stefan Pierer and a further 500-person efficiency-program headcount cut announced for 2026, concentrated in salaried and middle-management roles, raises the risk that key Austrian R&D engineers — the actual source of the process power — walk out the door.21 Third, macro demand: premium leisure motorcycles are among the most postponable purchases in a consumer's budget, and persistently high interest rates in North America and Europe continue to suppress exactly the discretionary, credit-financed demand KTM depends on.

Two further items belong on the radar because they are the kind of second-layer detail that rarely makes headlines until it matters. First, accounting judgment. The 2025 accounts contain an enormous one-off restructuring gain and substantial write-offs of the bicycle division — the sort of year in which the reported profit figure tells you almost nothing about earning power, and in which the auditors' treatment of provisions, impairments, and the valuation of what remains deserves careful reading. An investor who anchors on "€590 million net profit" has misread the company entirely. Second, the intercompany dependency. The company was rescued in part by a loan from its own controlling shareholder, subsequently refinanced with third-party banks — a healthy development that reduces reliance on Pune's balance sheet and subjects the company to the discipline of external lenders. But the residual pattern, in which the controlling shareholder is simultaneously the manufacturer, the former financier, and the counterparty on platform and component arrangements, is the sort of related-party complexity that governance-minded investors are right to watch.

The bull case. Bajaj's capital discipline and balance-sheet strength do the heavy lifting. The 70% debt haircut has already slashed the interest burden, the €550 million unsecured bank facility from J.P. Morgan, HSBC, DBS, and MUFG has replaced the more expensive €450 million Bajaj bridge loan at better terms, and the non-core losses are gone.4 With the core brands focused purely on higher-margin models and supercharged by low-cost Indian manufacturing, EBIT margins can climb back toward historical levels as volumes recover and fixed costs are spread across a leaner organisation. On the Q1 2026 call, management framed the sequencing clearly: become "profitable" first, then scale growth again — a discipline conspicuously absent in the boom years.19

There is a quieter bull argument that deserves airing: the crisis may have accomplished what no functioning board could have. In good times, no management team voluntarily fires 1,800 people, halts production for a quarter, sells its luxury brand at a loss, and shutters an entire division. Institutional inertia and founder ego make it impossible. Insolvency made all of it not merely possible but mandatory. The company that emerged is radically simpler than the one that went in — three motorcycle brands, one platform strategy, no bicycles, no sports cars, no Italian boutique, no third-party distribution. Simplicity is underrated as an operating asset. The 2026 efficiency program's removal of an entire management layer points in the same direction.21 If you believe the core motorcycle business was always sound and merely buried under accumulated diworsification, then what Bajaj bought is a good business finally stripped back to itself.

The bear case. Brand dilution under Indian ownership erodes the enthusiast premium that justifies KTM's pricing; the very cult that pays up for "Ready to Race" is the kind of community that can turn on a brand it perceives as cost-engineered and financialised. Motorcycle enthusiasts are, famously, not a forgiving constituency — the forums have long memories, and the perception that "KTM isn't really Austrian anymore" is the sort of narrative that spreads without any factual change in the product. Dealers, once burned, drift to rivals, and dealer defection is a slow bleed that shows up in registrations long after the relationship has actually broken.

The structural problem never fully goes away either. Austrian labour and R&D remain expensive, and here the bear case finds its sharpest edge: the obvious fix — shift more production to Pune — is also the thing most likely to hollow out the engineering culture that is the whole point of owning KTM rather than simply building Bajaj-branded bikes. It is a genuine strategic vice. Cut Austrian cost too little and the margins never recover; cut it too much and you are left with an orange badge on a commodity motorcycle, which is worth a great deal less. There is no obvious escape, and management's ability to navigate that trade-off is the real test of the next three years.

An activist would press hardest on governance. A controlling shareholder holding 74.9% that is also the manufacturing partner, the former lender, and the counterparty on intercompany arrangements creates related-party complexity and leaves the 25% minority float structurally dependent on Pune's goodwill. Minority holders in a company like this have essentially no ability to influence outcomes: they cannot force a board change, cannot block a transaction, and cannot compel disclosure on transfer pricing. They are along for whatever ride the controlling family chooses. That may well be a good ride — Bajaj's record with minorities in its own listed entity is respectable, and it has every incentive to make the Swiss-listed vehicle work. But the structure means the investment case rests substantially on trusting a controlling shareholder rather than on enforceable rights, and that is a materially different proposition from owning a widely-held company.

The 3 KPIs that matter most. An investor tracking this story should watch, first, the EBIT margin of the motorcycle segment — the single cleanest measure of whether the turnaround is real, with historical levels around 8–10% as the recovery benchmark. Second, dealer inventory / weeks of supply — the metric whose collapse caused the crisis; a stable band in the low-double-digit weeks (management targets stock turns above 2x annually) signals the channel is healthy, while any renewed build-up is the earliest warning of a relapse.19 Third, the Pune-versus-Mattighofen production split — the lever behind margin expansion, since moving more mid-capacity volume to India's cost base is how the structural advantage actually shows up in the numbers. These three, tracked over time, will tell you whether Bajaj is genuinely fixing the business or merely renaming it.

X. Epilogue & Key Takeaways

The most durable lesson of the KTM saga is about the danger of financialising an enthusiast brand. Stefan Pierer built one of the great modern comeback stories — a bankrupt Austrian motorcycle maker turned into a Dakar-conquering, three-brand European champion. But somewhere in the pandemic boom, the company stopped treating the motorcycle as the main driver of value and started treating the balance sheet as a growth engine: debt-funded acquisitions, a diversification into e-bikes that made strategic sense only on a slide, and channel stuffing to paper over a demand cliff. When a company begins borrowing from its healthy core to feed its non-core ambitions, the reckoning is not a question of if but when. The eighteen Dakar victories could not save a business that had quietly become a bank to its own dealers.

There is a subtler founder lesson layered underneath. Stefan Pierer's greatest strength and his fatal flaw were the same trait: he thought like a financier, not a motorcyclist. That mindset let him buy a bankrupt company for a token sum, focus it ruthlessly, capture Husqvarna cheaply, and structure a brilliant manufacturing alliance with Bajaj. The very same mindset — control through layered holdings, growth through acquisition, earnings smoothed through the channel — is what eventually produced a €2.9 billion insolvency. A financier's instincts are enormously valuable at the bottom of a cycle, when assets are cheap and discipline is scarce. They become dangerous at the top, when cheap money makes every acquisition look accretive and every stuffed quarter looks like growth. The skill that builds an empire is often the very skill that loses it, and the difference is usually nothing more than where you are in the cycle.

The second takeaway is bigger than one company. Bajaj Auto's full takeover of KTM is a marker of a genuine shift in the direction of global industrial capital. For a century, the flow ran one way — Western capital and Western management acquiring and operating assets across the developing world. Here, a highly profitable, cash-generative, family-controlled manufacturer from Pune has acquired, rescued, and now operates one of the crown jewels of European motorcycling heritage. It is a template that will recur: emerging-market champions with disciplined balance sheets and structural cost advantages stepping in to rescue distressed icons of Western industry, and keeping the brand while relocating the economics.

For the long-term investor, Bajaj Mobility AG is neither a finished triumph nor a lost cause — it is a turnaround in mid-motion. The accounting profit of 2025 was a one-off gift from creditors; the real test is the operating margin of 2026 and 2027, and the early quarters point genuinely upward.1718 The moat — brand, platform-sharing process, and Indian-anchored scale — is real, but two of its three legs now depend on the same controlling shareholder that also holds the governance keys. Whether Pune's discipline can preserve Mattighofen's soul is the question the numbers will answer over the next several years. The rescue is complete. The proof is still being written.

References

-

KTM AG Files for Court-Supervised Restructuring — Austrian Press Agency / EQS News, 2024-11-26 ↩↩

-

PIERER Mobility AG: Change of company name to Bajaj Mobility AG completed — EQS News, 2026-01-13 ↩↩↩

-

PIERER Mobility AG: Bajaj acquires sole control / Transition to New Ownership — webdisclosure.com / EQS, 2025-11-18 ↩↩↩↩↩↩

-

Bajaj Mobility AG Annual Financial Report 2025: Successful Turnaround — EQS News, 2026-03-26 ↩↩↩↩↩↩↩↩↩↩

-

Most Dakar Rally motorcycle category wins by a manufacturer (18, KTM, 2001–2019) — Guinness World Records ↩

-

How Bajaj Auto Secured Control of Europe's Largest Motorcycle Holding — Autocar India, 2025-11-20 ↩

-

BMW sells Husqvarna to KTM CEO Pierer — Powersports Business, 2013-02-18 ↩

-

Pierer Mobility to exit e-bike business amid restructuring struggle — Powersports Business, 2025-05-07 ↩↩↩↩↩↩

-

What we know about KTM's restructuring deal — Powersports Business, 2025-02-27 ↩↩↩

-

Motorbike Maker KTM's Lenders Take 70% Hit in Restructuring — Bloomberg Law, 2025-02-28 ↩

-

KTM Parent Company Faces €1.6 Billion Debt, Confirms Massive Layoffs and Exit from E-Bikes — Visordown, 2025-05 ↩

-

KTM complete sale of MV Agusta shares back to Sardarov family — MCNews, 2025-07-09 ↩

-

Stefan Pierer Steps Down As CEO of Pierer Mobility And KTM — MotoMatters, 2025-01-23 ↩↩

-

PIERER Mobility AG: Changes in the Executive Board / Supervisory Board — Bajaj Mobility AG Newsroom, 2025-06 ↩↩

-

KTM CEO Gottfried Neumeister to remain in charge through 2028 — Visordown, 2026-01 ↩

-

Bajaj Auto Hits Record ₹58,732 Cr FY26 Revenue, Profit Surges 21% With KTM Boost — Whalesbook, 2026 ↩↩

-

Bajaj Mobility AG Reports Strong Q1 2026 Performance with 70.2% Revenue Growth — ScanX, 2026-05-13 ↩↩↩↩

-

Is KTM finally through the worst of its financial crisis? Bajaj Mobility Q2 2026 preliminary results — MCNews, 2026-07-16 ↩↩↩↩

-

Earnings call transcript: Bajaj Mobility Q1 2026 revenue surges 70% — Investing.com, 2026-05-18 ↩↩↩↩↩↩↩

-

KTM and CFMOTO Joint Venture Developments / KTMR2R Hangzhou — Cycle World & Bajaj Mobility AG news, 2024–2025 ↩

-

Bajaj Mobility AG: Next Steps in the Restructuring as Part of the Efficiency Program (≈500 job cuts) — Yahoo Finance / EQS, 2026-01-13 ↩↩↩

-

Bajaj Completes Acquisition of KTM — Motorcycle.com, 2025-11 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube