BlackRock: The Rise of the Investment Management Colossus

I. Introduction & Episode Roadmap

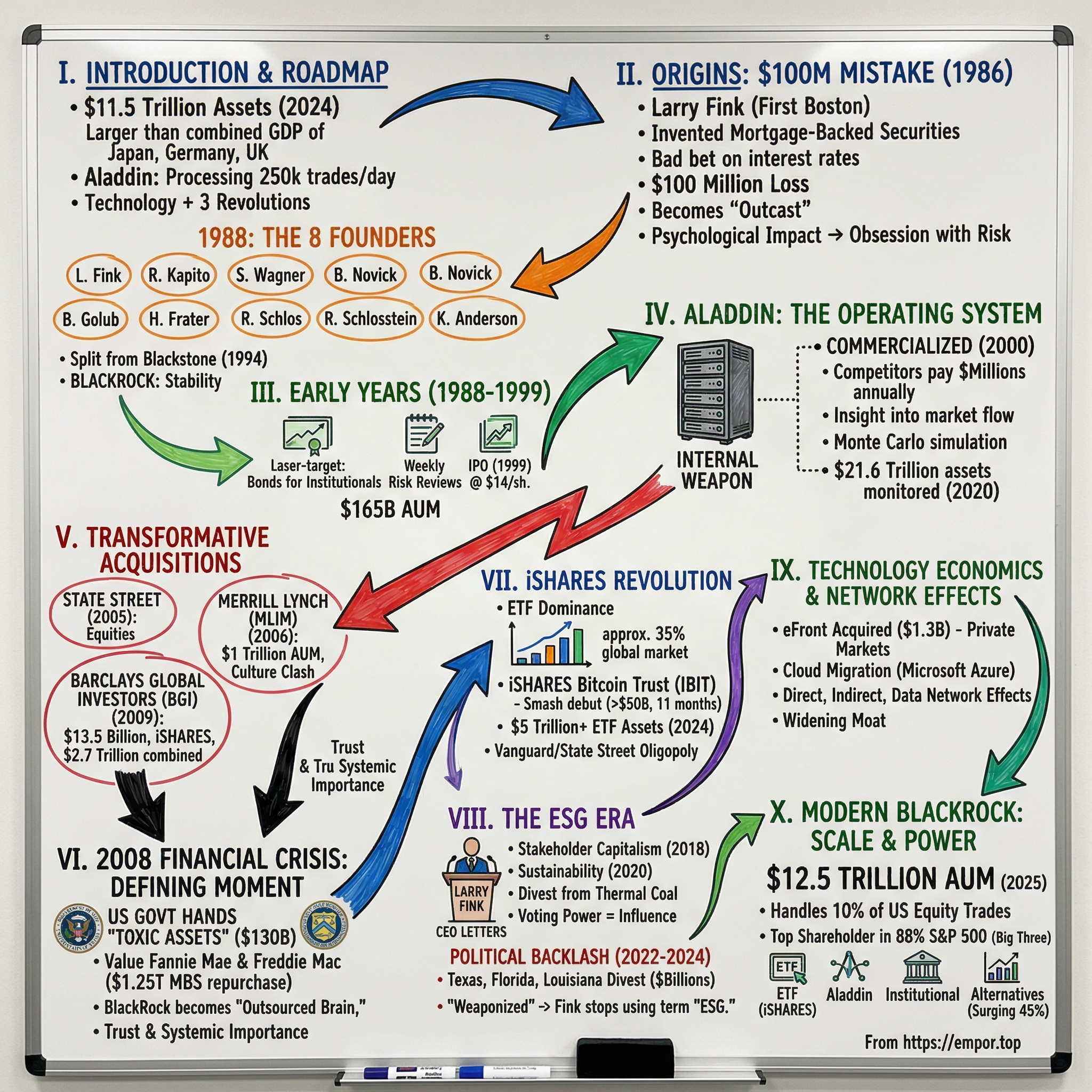

Picture this: A single company managing $11.5 trillion in assets—more money than the combined GDP of Japan, Germany, and the United Kingdom. A firm so deeply embedded in global finance that when markets sneeze, governments call them first. A technology platform processing 250,000 trades daily and analyzing 30 million positions across 2,000 portfolios in real-time. This is BlackRock in 2024, and if you don't understand how they got here, you don't understand modern capitalism.

The story begins not with triumph but with catastrophe. In 1986, a 33-year-old bond trader named Larry Fink lost $100 million in a single quarter—a career-ending disaster that would paradoxically birth the world's most powerful investment firm. What emerged from that failure was an obsession: What if you could see risk coming? What if you could model every scenario, stress-test every position, understand every correlation before disaster struck?

That obsession would manifest as Aladdin—a technology platform that started on a workstation wedged between a refrigerator and coffee machine. Today, it monitors $21.6 trillion in assets, roughly 10% of global financial wealth. Central banks use it. Pension funds depend on it. Even BlackRock's competitors pay millions to access it, creating perhaps the most elegant competitive moat in business history: your rivals funding your R&D.

But BlackRock isn't just a technology story. It's three revolutions wrapped into one company. First, they democratized risk management, transforming it from art to science. Second, they rode the passive investing tsunami through iShares, now commanding 35% of the global ETF market. Third, they've positioned themselves as capitalism's conscience—or its puppet master, depending on whom you ask—with Larry Fink's annual letters moving markets and shaping corporate behavior worldwide. The stories of how financial giants emerge from crisis are often sanitized in retrospect. But with BlackRock, you need to understand the raw emotional moment that birthed a $11.5 trillion empire. In 2024, BlackRock's assets under management reached a record $11.5 trillion, making it the single most powerful financial institution on Earth. Yet this colossus exists only because Larry Fink's department lost $100 million in 1986 due to his incorrect prediction about interest rates.

Here's the critical theme: BlackRock isn't a story of traditional ambition. It's a story of paranoia transformed into technology, of failure weaponized into competitive advantage, of risk management becoming so sophisticated it reshaped capitalism itself. Today, they oversee more wealth than existed in the entire global economy just decades ago, their Aladdin platform monitors 10% of world financial assets, and their CEO's annual letters move markets and corporate boards worldwide.

This is how eight outcasts from Wall Street built the operating system of modern finance—and what their dominance means for everyone who invests, saves, or simply exists in the modern economy.

II. Origins: The $100 Million Mistake That Created BlackRock

The trading floor at First Boston in 1986 was electric with the confidence of the Reagan-era bull market. Larry Fink, then 33, wasn't just another trader—he was royalty. He had started at First Boston in 1976 and become one of the first mortgage-backed security traders, eventually managing the firm's bond department. By some accounts, Fink's innovations in the MBS market had added as much as $1 billion to First Boston's bottom line over his tenure. He added as much as $1 billion to First Boston's bottom line.

Born November 2, 1952, Fink grew up as one of three children in a Jewish family in Van Nuys, California. His mother Lila was an English professor and his father Frederick owned a shoe store. He earned a BA in political science from UCLA in 1974, followed by an MBA in real estate at the UCLA Anderson School of Management in 1976.

Fink had essentially invented an entire market. Mortgage-backed securities were his creation, his domain. He understood their mathematics, their rhythms, their risks—or so he thought. Then came the miscalculation that would define not just his career, but the future of global finance.

The details vary depending on who tells the story, but the outcome was devastating: a bad bet on interest rates cost Fink's department at First Boston $100 million in 1986. In Fink's own words from a 2016 UCLA commencement address: "We lost the company a lot of money. And all of a sudden, we went from 'partners' to outcasts".

That word—"outcasts"—captures something essential. This wasn't just a financial loss; it was a shattering of identity. Fink had been the golden boy, the innovator, the profit machine. Now he was radioactive. The psychological impact was profound. The experience influenced his decision to start a company that would invest clients' money while also incorporating comprehensive risk management

What Fink understood in that moment of professional exile was something most Wall Street titans never grasp: the difference between taking risks and understanding them. "I realized I didn't know my business as well as I thought I did," he would later reflect. The firm had no proper risk management systems. They were flying blind, making billion-dollar bets based on intuition and spreadsheets that couldn't model interconnected risks.

The path from outcast to entrepreneur began with an unlikely patron. Stephen Schwarzman and Pete Peterson at Blackstone Group saw opportunity where others saw damaged goods. In 1988, they offered Fink and seven colleagues a $5 million credit line for a 50% stake in what would initially be called Blackstone Financial Management. The eight founding partners—Larry Fink, Robert S. Kapito, Susan Wagner, Barbara Novick, Ben Golub, Hugh Frater, Ralph Schlosstein, and Keith Anderson—weren't just starting an investment firm. They were building a machine to prevent what happened to Fink from ever happening again.

The founding team was deliberately constructed. Kapito brought institutional sales expertise from First Boston. Wagner understood the mechanics of mortgage securities. Novick had the operational knowledge to build systems from scratch. Golub possessed the quantitative skills to model complex risks. Each founder carried scars from Wall Street's boom-bust cycles, united by a shared belief: risk wasn't something you avoided—it was something you measured, modeled, and managed.

The name itself was telling. When they split from Blackstone in 1994, they chose "BlackRock"—evoking something solid, permanent, foundational. Not a person's name like Goldman or Morgan, but something that suggested bedrock stability in volatile markets. This wasn't ego; it was positioning. They were selling certainty in an uncertain world.

Peterson's initial investment terms were generous by private equity standards but reflected the risk: a new firm led by someone whose last major act had lost $100 million. Yet within five years, BlackRock would be managing $23 billion. The secret wasn't better trades or smarter picks—it was the systematic application of technology to risk management, a philosophy that would eventually reshape how the entire world invests.

III. The Early Years: Building a Risk Management Culture (1988-1999)

The first BlackRock office at 40 East 52nd Street in Manhattan was deliberately unglamorous. While competitors occupied marble-clad towers, Fink's team worked in functional space that prioritized computer terminals over corner offices. This wasn't accidental—it was philosophical. Every dollar saved on aesthetics was a dollar invested in technology and talent.

The initial focus was laser-targeted: fixed-income securities for institutional clients. This wasn't the sexy side of Wall Street—no hostile takeovers, no IPO roadshows, no trading floor dramatics. Instead, BlackRock pursued the unglamorous work of helping pension funds, insurance companies, and corporations manage their bond portfolios. The pitch was simple but revolutionary: "We'll manage your money as if we lost $100 million of our own."

What distinguished BlackRock from day one was their approach to information. While competitors relied on intuition and relationships, BlackRock built models. Every mortgage-backed security was decomposed into its constituent cash flows. Every interest rate scenario was simulated. Every correlation was tracked. The firm's early clients—including Chrysler, which gave them their first major mandate—weren't buying performance; they were buying peace of mind. The technological heart of this operation began with Charles Hallac, who joined as BlackRock's first employee in 1988 and purchased a Sun Microsystems workstation that stood between a refrigerator and coffee machine. Hallac, regarded as the initial architect of Aladdin, worked with Bennett W. Golub to develop the first mathematical models for what would become the industry's most powerful risk management platform.

The culture wasn't just about technology—it was about transparency to the point of discomfort. Every investment decision was documented. Every assumption was challenged. Every risk was quantified. Susan Wagner, one of the founding partners, instituted weekly risk reviews where portfolio managers had to defend their positions not with confidence but with data. "We were building a culture where being wrong was acceptable," she would later explain, "but being surprised was not."

Aladdin's first major deployment came in 1994 when General Electric hired BlackRock to analyze the problematic mortgage portfolio of Kidder, Peabody & Co, which was considered one of the most complex in the world. BlackRock completed the analysis successfully, and Kidder was sold to Paine Webber that same year.

The split from Blackstone in 1994 was both liberation and vulnerability. BlackRock was now independent, but without the safety net of a larger parent. The founders chose to reinvest virtually everything back into the business, particularly into technology. While competitors paid out 50-60% of revenues as compensation, BlackRock kept it closer to 35%, pouring the difference into systems and infrastructure.

By 1999, when BlackRock went public at $14 per share, they managed $165 billion in assets. The IPO wasn't about cashing out—most founders retained their stakes. It was about permanence. A public company with quarterly earnings calls and regulatory oversight signaled to institutional clients that BlackRock was built to last. The first day of trading saw the stock close at $20.25, valuing the company at $1.35 billion. Within the year, assets under management would cross $200 billion.

IV. Aladdin: Building the Operating System of Finance

The name itself was an acronym that only an engineer could love: Asset, Liability and Debt and Derivative Investment Network. But Aladdin represented something far more profound than its clunky title suggested. It began in 1988 on a single workstation from Sun Microsystems, but its ambitions were boundless: to create a single source of truth for every position, every risk, every scenario across an entire portfolio.

The origin story of Aladdin's commercialization reveals BlackRock's accidental genius. For the first decade, Aladdin was purely internal—BlackRock's secret weapon. Then in 1999, a competitor approached them with an unusual request: Could they buy the technology? The initial reaction was defensive—why would you arm your rivals? But Fink saw the bigger picture. If other firms used Aladdin, BlackRock would see how they traded, understand their risks, learn from their strategies. Your competitors would literally pay you to reveal their playbooks. By 2000, BlackRock created a new business division to officially offer Aladdin to external clients. The business model was brilliant in its simplicity: charge competitors millions in annual fees to use your risk management system while simultaneously gaining insight into how the entire market operated. A new business division was created and in 2000 the use of Aladdin was officially offered to clients.

The technical architecture was revolutionary for its time. Aladdin is based on a pool of historical data that uses Monte Carlo simulation to select large, randomly generated samples from the very large number of possible future scenarios. This generates a statistical picture of different scenarios for equities and bonds under different future conditions. The system could stress-test portfolios against any scenario—a pandemic, a sovereign default, a market crash—providing what Fink called "X-ray vision into risk."

What made Aladdin truly powerful wasn't just its analytics but its comprehensiveness. While competitors had separate systems for trading, risk management, and accounting, Aladdin unified everything. One platform, one source of truth, updated in real-time. By 2013, the platform was handling $11 trillion in assets—roughly 7% of the world's financial assets—and tracking 30,000 investment portfolios.

The genius of the user-provider model became apparent over time. Because BlackRock used Aladdin for its own investments, the platform had to be genuinely superior—not just marketing material but battle-tested technology. Every improvement BlackRock made for itself benefited external clients, and every client request made the platform stronger for BlackRock's own use. It was a perpetual innovation machine funded by competitors.

BlackRock's technology platform, Aladdin, contributed $1.6bn in revenues in 2024, but its true value transcended direct revenue. Aladdin became BlackRock's eyes and ears across global markets. It is currently used by more than 200 institutions covering pension funds, asset managers, banks and corporates and managed more than $21.6 trillion in assets as of 2020. When CalPERS made a trade, BlackRock knew. When Deutsche Bank shifted allocations, BlackRock saw it. Not the specific positions—client data was segregated—but the patterns, the flows, the sentiment. It was like having a radar system for global finance.

V. The Transformative Acquisitions Era (2005-2009)

BlackRock's transformation from a successful bond manager to a global colossus required more than organic growth—it demanded strategic acquisitions executed with surgical precision. The acquisition playbook that would define BlackRock's rise began in 2005 with State Street Research & Management, a $375 billion asset manager that brought crucial equity capabilities. The deal, valued at $375 million, wasn't just about scale—it was about completing BlackRock's evolution from fixed-income specialist to full-service asset manager.

But the real transformation came through two deals that would reshape not just BlackRock but the entire asset management industry. In 2006, Merrill Lynch approached BlackRock with a proposal: merge with Merrill Lynch Investment Managers (MLIM) in exchange for giving Merrill a 49.8% stake in the combined entity. The deal, valued at $9.8 billion, would double BlackRock's AUM to over $1 trillion overnight.

The MLIM merger was fraught with integration challenges. MLIM's culture was that of a wirehouse—relationship-driven, bonus-focused, hierarchical. BlackRock was engineering-driven, egalitarian, obsessed with risk management. Fink's solution was ruthless: integrate the assets, keep the best people, but impose BlackRock's culture without compromise. Within 18 months, the integration was complete, with minimal client defections and most key talent retained. The crown jewel acquisition came in June 2009, when BlackRock announced it would acquire Barclays Global Investors (BGI) for $13.5 billion. On June 11, 2009, BlackRock, Inc., the world's fourth-largest asset manager announced it was acquiring Barclays Global Investors (BGI) for $13.5 billion in stock and cash. The deal would more than double BlackRock's assets under management (AUM), making it the world's largest asset manager.

The BGI acquisition was transformative on multiple levels. BlackRock and BGI would combine to create an asset management firm operating under the name BlackRock Global Investors, with combined assets under management of more than $2.7 trillion. BGI brought with it iShares, the world's largest ETF platform with over $300 billion in assets across 350+ funds. It also brought systematic investing capabilities, global reach, and critically, a culture of innovation that meshed well with BlackRock's engineering mindset.

The deal structure was complex: BlackRock issued 37.8 million shares plus $6.6 billion in cash, with Barclays retaining a 19.9% economic interest in the combined entity. This stake would prove temporary—Basel III regulations made it uncomfortable for banks to hold such positions, and Barclays then sold its 19.9% stake for $6.1 billion in 2012. Barclays' shares were sold by way of an offering and a related buyback by BlackRock of up to $1 billion of the shares.

The integration of BGI was BlackRock's masterpiece of M&A execution. Unlike the cultural clashes that plagued many mega-mergers, BlackRock and BGI shared a quantitative, technology-driven approach to investing. Within 18 months, the platforms were integrated, teams were merged, and client retention exceeded 95%. The acquisition catapulted BlackRock from a large asset manager to the undisputed global leader, with assets that would grow from $3.2 trillion in 2009 to over $11 trillion by 2024.

VI. The 2008 Financial Crisis: BlackRock's Defining Moment

If the BGI acquisition made BlackRock the world's largest asset manager, the 2008 financial crisis made it indispensable. When Bear Stearns collapsed in March 2008, the Federal Reserve faced a problem: $30 billion in toxic mortgage securities that nobody could properly value. They turned to BlackRock.

The US government also placed its trust in Aladdin's risk management during the 2008 financial crisis and handed over "toxic assets" worth US$130 billion to the financial services provider for management. These "junk securities" came from the government and the US Federal Reserve, from the liquidation of Bear Stearns and American International Group.

What followed was unprecedented. BlackRock wasn't just hired as an advisor—they became the government's outsourced brain for understanding the crisis. The Fed allowed BlackRock to superintend the $130 billion debt settlement of Bear Stearns. When AIG needed unwinding, BlackRock was there. When Freddie Mac and Fannie Mae required analysis, BlackRock provided it.

The scope was staggering. During the 2008 financial crisis, BlackRock was allowed to value the balance sheet items of the now nationalized mortgage banks Fannie Mae and Freddie Mac and manage the repurchase of mortgage-backed securities for the US Federal Reserve in the amount of US$1.25 trillion.

This wasn't charity work. BlackRock earned hundreds of millions in fees, but more importantly, they gained something priceless: trust. When central banks and governments needed someone to understand complex securities, manage toxic assets, or provide liquidity analysis, they called BlackRock. The firm had become systemically important not through size alone but through competence.

Due to the 2008 financial crisis, risk management became a focal point for financial investments. Very few asset managers had the appropriate personnel and expertise for this. BlackRock's offer to use Aladdin's analysis tools and databases for risk assessment met market demand and brought BlackRock a very broad customer base. The 2008 financial crisis and Aladdin played a significant role in BlackRock's dominant market position today.

The crisis also accelerated Aladdin adoption exponentially. Financial institutions that had resisted outsourcing risk management suddenly realized they couldn't afford not to. Aladdin went from a competitive advantage to a necessity. The platform that had been monitoring $11 trillion in 2013 would reach $21.6 trillion by 2020.

But the crisis did more than establish BlackRock's technical competence—it embedded them in the architecture of global finance. They weren't just a service provider; they were the doctor called in when the patient was dying. This positioned them perfectly for what came next: the era of extraordinary monetary policy, where central banks would need partners to execute unprecedented asset purchase programs.

VII. The iShares Revolution & ETF Dominance

The iShares platform that came with the BGI acquisition wasn't just another product line—it was a revolution hiding in plain sight. When BlackRock acquired BGI in 2009, iShares had roughly $300 billion in assets. By 2017, iShares accounted for $1.41 trillion (26% of total AUM, 37% of base fee income). Today, BlackRock commands approximately 35% of the global ETF market, a dominance that generates not just fees but unprecedented market influence.

The genius of ETFs was their simplicity: trade a basket of securities like a single stock. But BlackRock understood something deeper—ETFs weren't just products, they were infrastructure. Every trade, every rebalancing, every creation and redemption unit generated data that fed back into Aladdin. BlackRock could see flows before they materialized in prices, understand sentiment before it moved markets.

The democratization narrative was real but incomplete. Yes, ETFs allowed retail investors to access sophisticated strategies for basis points instead of percentage points. But they also concentrated power. When millions of investors buy the same S&P 500 ETF, BlackRock votes those shares. When passive flows dominate active management, the "passive" manager becomes the most active corporate governance force in capitalism.

BlackRock's ETF strategy was methodical expansion. Start with broad market indices, then slice thinner: sectors, factors, themes, countries. By 2020, iShares offered over 350 funds covering virtually every investable asset class. The network effects were powerful—more assets meant tighter spreads, which attracted more assets, which enabled more niche products, which brought in more diverse investors.

The competition with Vanguard and State Street created an oligopoly that benefited all three. Together, these "Big Three" control over 80% of ETF assets, creating barriers to entry that even deep-pocketed competitors struggle to overcome. The game isn't just about low fees—it's about scale, liquidity, securities lending revenue, and the data exhaust that comes from managing trillions. The recent innovation in cryptocurrency ETFs demonstrates BlackRock's continued dominance. On January 11, 2024, the U.S. SEC approved 11 spot Bitcoin ETF filings, including BlackRock's IBIT. The iShares Bitcoin Trust (ticker IBIT) smashed industry records in its launch year of 2024. In just 11 months, it grew to a behemoth with more than $50 billion in assets. Simply put, no ETF has ever had a better debut.

Nate Geraci, president of advisory firm The ETF Store, called it "the greatest launch in ETF history." The success wasn't just about size—it was about legitimization. With BlackRock's more than $11 trillion in assets under management, the embrace by the world's largest investment firm helped drive Bitcoin's price past $100,000 for the first time, bringing both institutional investors and formerly skeptical individuals into the fold.

VIII. The ESG Era and Stakeholder Capitalism

Larry Fink's annual CEO letters transformed from investment updates into manifestos that moved markets and shaped corporate behavior. Starting in 2018, these letters became increasingly focused on environmental, social, and governance (ESG) issues, positioning BlackRock not just as an asset manager but as capitalism's conscience—or, critics argued, its unelected ruler.

The 2018 letter was a shot across the bow: corporations needed a social purpose beyond profit. By 2019, Fink was calling for corporations to play an active role in addressing environmental challenges, diversity issues, and social inequities. The 2020 letter went further, declaring environmental sustainability as a core goal and announcing BlackRock would divest from companies generating more than 25% of revenues from thermal coal production, affecting approximately $500 million in assets.

The power behind these letters wasn't moral authority—it was voting power. Through its index funds, BlackRock votes on behalf of millions of passive investors who never actively chose to support ESG initiatives. When BlackRock says jump, boards ask how high, not because they necessarily agree with the philosophy but because BlackRock controls significant voting blocks in virtually every major public company.

The backlash was swift and fierce. Conservative states began divesting pension funds from BlackRock, arguing the firm was using other people's money to advance a political agenda. The term "woke capitalism" became a rallying cry, with BlackRock as exhibit A. By 2022, Fink himself acknowledged the weaponization of ESG, saying he had stopped using the term entirely because it had become too politicized. The backlash intensified through 2023-2024. The U.S. states of West Virginia, Florida, and Louisiana have divested money away from or refuse to do business with the firm because of its ESG policies. The State of Texas is terminating a $8.5 billion investment with BlackRock in response to the firm's ESG policies which the state said signal a boycott of energy companies. Texas State Board of Education Chairman Aaron Kinsey said the so-called Texas Permanent School Fund (PSF) had delivered a notice to BlackRock on Tuesday, informing the New York City-based firm of the action.

BlackRock lost around $4 billion in assets under management as a result of a political backlash against environmental, social and governance (ESG) investing in the United States. However, Larry Fink, speaking at a Bloomberg News event in Davos, Switzerland on Tuesday, said the asset management group took in $230 billion over the course of 2022 from U.S. clients.

The irony of the ESG debate is that BlackRock finds itself attacked from both sides. Progressive activists argue the firm doesn't go far enough, continuing to invest in fossil fuels and defense contractors. Conservative critics see it as using other people's money to advance a political agenda. Fink's response has been to emphasize fiduciary duty—BlackRock invests in ESG not for political reasons but because it believes climate risk is investment risk.

In a talk at the Aspen Ideas Festival in June 2023, BlackRock CEO Larry Fink said he has stopped using the term "ESG" because the term has been "weaponized". According to an Axios reporter, Fink said, "I'm ashamed of being part of this conversation." The retreat from ESG terminology, however, hasn't meant a retreat from the underlying principles. BlackRock continues to vote shares based on long-term value creation, which often aligns with ESG principles even if they're no longer labeled as such.

IX. Technology Platform Economics & Network Effects

The economics of Aladdin represent one of the most elegant business models in enterprise software. BlackRock's technology platform, Aladdin, contributed $1.6bn in revenues in 2024, but this understates its true value. Aladdin isn't just a revenue stream—it's the gravitational center that holds BlackRock's entire ecosystem together.

The platform now oversees more than $20 trillion for 200+ clients, generating what industry analysts estimate at $1.5 billion in direct revenue. But the indirect benefits dwarf the direct revenue. Every client on Aladdin becomes harder to compete against because BlackRock understands their risk profiles, trading patterns, and portfolio construction. Every new module added to Aladdin makes it harder for clients to leave. Every year of historical data makes the models more accurate.

The network effects are multi-layered. Direct network effects emerge as more users make the platform more valuable for all users through shared learnings and benchmarking. Indirect network effects arise as third-party developers build on Aladdin, creating an ecosystem of complementary services. Data network effects compound as each transaction, each portfolio rebalancing, each risk calculation adds to the collective intelligence of the system.

The 2019 acquisition of eFront for $1.3 billion expanded Aladdin's capabilities into alternative investments—private equity, real estate, infrastructure. This wasn't just adding features; it was extending the network into previously opaque corners of finance. Suddenly, Aladdin could provide a unified view across public and private markets, liquid and illiquid assets, traditional and alternative investments.

The cloud migration partnership with Microsoft Azure, announced in 2019, represents the next evolution. Moving Aladdin to the cloud isn't just about cost savings or scalability—it's about embedding BlackRock's technology even deeper into the financial system's infrastructure. When your risk management platform runs on the same cloud infrastructure as your clients' other systems, integration becomes seamless, switching costs become prohibitive.

Competition exists but struggles to gain traction. Bloomberg's PORT system, State Street's Charles River, SimCorp Dimension—all offer pieces of what Aladdin does. But none match its comprehensiveness, its integration with BlackRock's investment expertise, or its network effects. The moat isn't just technological; it's ecological. Aladdin is less a product than a platform, less a platform than an ecosystem, less an ecosystem than the operating system of modern finance.

X. Modern BlackRock: Scale, Power & Influence

BlackRock is the world's largest asset manager, with US$12.5 trillion in assets under management as of 2025. To comprehend this scale, consider that BlackRock manages more money than the entire GDP of China. Every trading day, approximately 10% of all equity trades in the United States involve a BlackRock fund. The firm employs approximately 21,000 people across 70 offices in 30 countries, but its influence extends far beyond its headcount.

The business is organized into distinct but synergistic segments. The ETF business through iShares generates the highest margins, with operating margins often exceeding 70%. The institutional business provides stable, long-term fee streams from pension funds and sovereign wealth funds. BlackRock Solutions, powered by Aladdin, creates the technological moat. The alternatives platform, turbocharged by recent acquisitions, represents the growth frontier.

The "Big Three" dynamic with Vanguard and State Street has created an unprecedented concentration of corporate ownership. Together, these three firms are the largest shareholders in 88% of S&P 500 companies. This isn't conspiracy; it's math. When passive investing dominates and three firms control most passive assets, concentration is inevitable. The question isn't whether this concentration exists but what it means for capitalism.

BlackRock's proxy voting power is staggering. In 2023, the firm voted on over 155,000 proposals at nearly 18,000 shareholder meetings globally. These aren't just votes on executive compensation or board appointments—they're decisions about climate disclosures, diversity policies, corporate strategies. BlackRock doesn't just own shares; it shapes corporate behavior at scale.

The government relationships are perhaps most remarkable. When COVID-19 struck in 2020, the Federal Reserve again turned to BlackRock to manage its corporate bond purchase programs. The conflicts of interest were obvious—BlackRock would be buying bonds of companies in which it was already a major shareholder—but the expertise was irreplaceable. No other firm had the technology, scale, and operational capability to execute at the speed and scale required.

Geopolitically, BlackRock operates in a complex web of relationships. The firm manages money for China's sovereign wealth funds while also advising the U.S. government. It invests in Saudi Aramco while promoting renewable energy. These contradictions aren't bugs but features of being the world's financial utility. When you manage money for everyone, you must navigate everyone's politics.

XI. Playbook: Business & Investing Lessons

The BlackRock story offers a masterclass in building enduring business value, starting with the counterintuitive lesson that catastrophic failure can be the foundation for extraordinary success. Fink's $100 million loss wasn't hidden or minimized—it became the origin story, the cautionary tale that justified everything that followed. The lesson: authenticity about failure can be more powerful than any success story.

The infrastructure versus product lesson is critical. BlackRock didn't build better mutual funds; they built the platform on which everyone else's funds operated. This is the difference between competing in a market and creating the market itself. When you build infrastructure, competition becomes collaboration—your rivals pay you to make their products possible.

The technology investment philosophy challenges conventional wisdom about financial services. While competitors saw technology as a cost center, BlackRock saw it as the business itself. They didn't just invest in technology; they became a technology company that happened to manage money. The compound returns on these technology investments—not just financial but in terms of competitive advantage—demonstrate that in modern business, there's no such thing as "too much" investment in technology if it creates genuine moat expansion.

Acquisition integration emerges as perhaps BlackRock's most underappreciated competency. The firm has completed over 15 major acquisitions, from State Street Research to BGI to recent additions like GIP. The pattern is consistent: buy for capabilities not just assets, integrate rapidly but thoughtfully, impose BlackRock culture while respecting acquired expertise. The BGI integration, where two massive firms merged with minimal client defection, should be taught in business schools as the gold standard of M&A execution.

Managing conflicts of interest at scale offers lessons for any platform business. BlackRock simultaneously serves competitors, advises governments that regulate it, and votes shares in companies it analyzes for clients. The key insight: transparency and systematic processes matter more than avoiding conflicts entirely. When conflicts are inevitable, the solution isn't elimination but management through clear policies consistently applied.

The network effects in B2B financial services demonstrate that consumer internet companies don't have a monopoly on platform dynamics. Aladdin's network effects are actually stronger than many consumer platforms because switching costs are higher, integration is deeper, and the consequences of failure are catastrophic. The lesson: B2B network effects may be harder to build but they're also harder to break.

XII. Analysis & Bear vs. Bull Case

Bull Case:

The bull case for BlackRock rests on five pillars of competitive advantage that appear to be widening rather than narrowing. First, the Aladdin platform has achieved escape velocity as financial infrastructure. With $21.6 trillion under surveillance and switching costs measured in years and millions of dollars, Aladdin has become as embedded in finance as Windows in enterprise computing. The recent Preqin acquisition for $3.2 billion extends this infrastructure into private markets, opening an $8 billion total addressable market growing at 12% annually.

Second, the secular shift to passive investing continues unabated. Despite periodic predictions of "peak passive," ETF assets continue growing faster than active management. BlackRock's 35% market share in ETFs, combined with the oligopolistic structure of the industry, suggests this growth will continue flowing disproportionately to the incumbent leaders. The iShares Bitcoin ETF success—becoming the fastest-growing ETF in history—demonstrates BlackRock's ability to dominate new categories as they emerge.

Third, the alternatives expansion represents a massive growth opportunity. When the HPS deal closes, BlackRock's private markets and alternatives platform is expected to reach $600bn in client assets, making the firm a top-five provider. The current private markets and alternatives platform contributed over $3bn in revenues in 2024, or about 15% to the group. With private markets expected to grow from $13 trillion today to $40 trillion by 2032, BlackRock is positioned to capture an outsized share of this expansion.

Fourth, technology platform monetization remains in early innings. While Aladdin generates $1.6 billion in revenue, this represents a tiny fraction of the value it creates for clients. As BlackRock adds capabilities—risk analytics, trading algorithms, portfolio construction tools—pricing power should increase. The integration with Microsoft Azure and the development of AI capabilities could unlock entirely new revenue streams.

Fifth, the moat is widening through data advantages. Every day, BlackRock gains more information about markets, risks, and investor behavior than any competitor. This data advantage compounds: better data leads to better products, which attract more assets, which generate more data. It's a virtuous cycle that becomes harder to break with each passing year.

Bear Case:

The bear case begins with regulatory risk that grows with every dollar of assets. At $12.5 trillion AUM, BlackRock isn't just too big to fail—it's too big to comprehend. Regulators globally are increasingly uncomfortable with this concentration. The common ownership debate, where BlackRock owns significant stakes in competing companies, could lead to forced divestitures or voting restrictions. BlackRock's 2023 SEC annual report identified common ownership as a potential business risk, noting that "in 2023, the FTC and DOJ released new merger guidelines recognizing that common ownership may reduce competitive incentives." The company disclosed that common ownership "may be given greater consideration in regulatory investigations, studies, rule proposals, policy decisions and/or the scrutiny of mergers and acquisitions."

Fee compression in passive products represents an existential threat to BlackRock's highest-margin business. ETF fees have fallen 40% over the past decade and continue declining. While BlackRock has maintained share through scale advantages, a price war with Vanguard—which operates with a mutual ownership structure and doesn't need profits—could devastate margins. If ETF fees compress to near zero, as trading commissions did, BlackRock would need to find alternative revenue sources.

The ESG backlash has revealed political vulnerability. The withdrawal of $8.5 billion by Texas, while small relative to BlackRock's AUM, signals a broader risk. If ESG becomes thoroughly politicized, BlackRock could lose access to large pools of capital in conservative states. Worse, it could face a situation where serving some clients means being unable to serve others, fracturing the universal platform that is core to its value proposition.

Technological disruption from big tech or crypto natives poses a longer-term threat. While Aladdin dominates today, a sufficiently motivated competitor with deep pockets—think Google, Amazon, or a crypto-native firm—could build competitive infrastructure. The rise of DeFi and tokenization could bypass traditional asset management entirely. If assets become programmable and self-custodied, what role does a traditional asset manager play?

Competitive threats from sovereign wealth funds and large asset owners insourcing capabilities represent another pressure point. As technology becomes commoditized and talent becomes mobile, large institutions are increasingly bringing asset management in-house. The Canadian pension funds, Norwegian sovereign wealth fund, and others have built sophisticated internal capabilities. If this trend accelerates, BlackRock's addressable market shrinks.

XIII. Epilogue & Future Outlook

The next decade for BlackRock will be defined by three fundamental tensions that will determine whether the firm maintains its trajectory toward $20 trillion AUM or faces its first serious existential challenge.

The succession question looms largest. Larry Fink, at 71, has built BlackRock in his image—relationship-driven at the top, technology-driven at the core, philosophically ambitious about capitalism's future. The next CEO faces an impossible task: maintaining Fink's government relationships while navigating increasing political polarization, continuing innovation while managing regulatory scrutiny, expanding globally while nationalism rises. The internal candidates—Rob Kapito, Mark Wiedman, Rachel Lord—each bring different strengths, but none combine Fink's unique mixture of vision, relationships, and credibility.

Private markets integration represents the biggest opportunity and challenge. BlackRock's acquisitions of GIP, HPS, and Preqin signal a massive bet that the future of asset management lies in private markets. But private markets are fundamentally different from public markets—relationship-driven rather than technology-driven, opaque rather than transparent, illiquid rather than liquid. Can BlackRock's engineering culture successfully integrate with private equity's relationship culture? Can Aladdin bring transparency to private markets without destroying what makes them attractive?

The tokenization and digital assets future poses an existential question. BlackRock's successful Bitcoin ETF launch demonstrates adaptability, but tokenization could fundamentally restructure asset management. If real estate, private equity, and even public securities become tokenized and traded on blockchain rails, the entire infrastructure BlackRock has built could become obsolete. The firm must balance being early enough to shape the future while not so early that it alienates traditional clients.

Geopolitical fragmentation threatens the global platform model. As U.S.-China tensions escalate, BlackRock's position managing money for both sides becomes increasingly untenable. The firm may be forced to choose sides or split into regional entities, destroying the global network effects that underpin its competitive advantage. The Russia-Ukraine conflict already forced difficult decisions; Taiwan could force impossible ones.

What BlackRock means for the future of capitalism is perhaps the most profound question. The firm has become a laboratory for stakeholder capitalism, using its voting power to push companies toward long-term thinking, environmental responsibility, and social consciousness. Critics see this as unelected power shaping society without democratic input. Supporters see it as capitalism evolving to address its own externalities. The resolution of this debate will determine not just BlackRock's future but the future of market-based economies.

The lessons for founders and investors are clear but challenging to implement. Build infrastructure, not just products. Invest in technology as if your business depends on it—because it does. Turn catastrophic failure into competitive advantage. Manage conflicts through transparency rather than avoidance. Recognize that in modern business, network effects exist everywhere if you know how to create them.

BlackRock's story isn't finished. The firm that emerged from a $100 million loss to manage $12.5 trillion faces challenges proportional to its success. Whether it becomes the permanent infrastructure of global finance or the peak example of too-big-to-fail remains to be written. What's certain is that understanding BlackRock means understanding modern capitalism itself—its promises, its contradictions, and its possible futures.

XIV. Recent News**

Q2 2025 Earnings:** BlackRock (NYSE:BLK), the world's largest asset manager, revealed in its Q2 2025 earnings presentation that assets under management reached $12.5 trillion as of June 30, 2025. The presentation, released on July 15, 2025, showcased strong financial performance amid favorable market conditions, with the S&P 500 rising 14% year-over-year and 11% quarter-over-quarter. The figure increased 13% year over year. The rise was driven by an increase in all revenue components except investment advisory performance fees. Total expenses amounted to $3.69 billion, up 23% year over year.

Major Client Redemption: Long-term net inflows were impacted by a single institutional client redeeming $52 billion from a low-fee index fund. BlackRock did not name the client, but the outflow was large enough to be explicitly cited in the release. Without that one redemption, long-term net inflows would have come in around $120 billion — double the reported figure. While BlackRock emphasized that the mandate was low-fee and that organic base fee growth remained strong at 6%, it's relatively rare for the firm to isolate a single client decision in a quarterly update

HPS Acquisition Closed: Closed acquisition of HPS Investment Partners on July 1st, adding $165 billion of client AUM and $118 billion of fee-paying AUM

Alternatives Surge: The alternatives business represents a key growth area for BlackRock, with client assets increasing from $326 billion in Q2 2024 to $474 billion in Q2 2025, a remarkable 45% year-over-year growth. This segment now accounts for 15% of base fees despite representing only 3% of AUM, highlighting its higher fee structure and strategic importance.

Digital Assets Growth: Another notable development is the emergence of digital assets as a distinct asset class in BlackRock's portfolio, now representing 1% of both AUM and base fees. This follows the company's successful launch of Bitcoin ETFs and expansion into cryptocurrency-related investment products, as mentioned in previous earnings calls.

Stock Performance: Despite the positive results, BlackRock's stock traded down 0.99% in premarket trading to $1,100.50, following a closing price of $1,111.46 on July 14. This slight pullback comes after significant stock appreciation since the company's Q1 2025 earnings, when shares traded around $870.

XV. Links & Resources

Annual CEO Letters: - BlackRock Annual Reports and Letters to Shareholders (ir.blackrock.com) - Larry Fink's Annual Letters Archive (2012-2024)

Books on BlackRock History: - "The Index Revolution" by Charles D. Ellis - "Trillions" by Robin Wigglesworth - "Engine of Inequality" by Adrienne Buller

Aladdin Technology Documentation: - BlackRock Aladdin Platform Overview (blackrock.com/aladdin) - Aladdin Client Resources Portal

Academic Papers: - "Common Ownership, Competition, and Top Management Incentives" - Antón, Ederer, Giné, and Schmalz (2023) - "The Rise of Passive Investing and Index Funds" - Anadu et al., Federal Reserve Bank of Boston (2023) - "Hidden Power of the Big Three?" - Bebchuk & Hirst, Harvard Law Review (2019)

Industry Reports: - McKinsey Global Asset Management Survey (Annual) - PwC Asset & Wealth Management Revolution Reports - BCG Global Asset Management Report Series

Regulatory Filings: - SEC EDGAR Database - BlackRock Inc. (BLK) Filings - BlackRock Investment Stewardship Reports - Federal Reserve Statistical Releases

Key Executive Interviews: - Larry Fink at Davos World Economic Forum (Annual) - BlackRock Investor Day Presentations - Bloomberg Masters in Business Podcast Episodes

Historical Acquisition Documents: - BGI Acquisition Proxy Statement (2009) - GIP Transaction Documentation (2024) - HPS Investment Partners Merger Agreement (2024)

ETF Industry Resources: - ETF.com Analytics and Data - ETFGI Global ETF and ETP Industry Reports - iShares Product Documentation

Financial Crisis Retrospectives: - Financial Crisis Inquiry Commission Report (2011) - "Too Big to Fail" - Andrew Ross Sorkin - Federal Reserve Crisis Response Archives

This analysis represents independent research and should not be considered investment advice. All data sourced from public filings, company reports, and verified news sources as of August 2025.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube