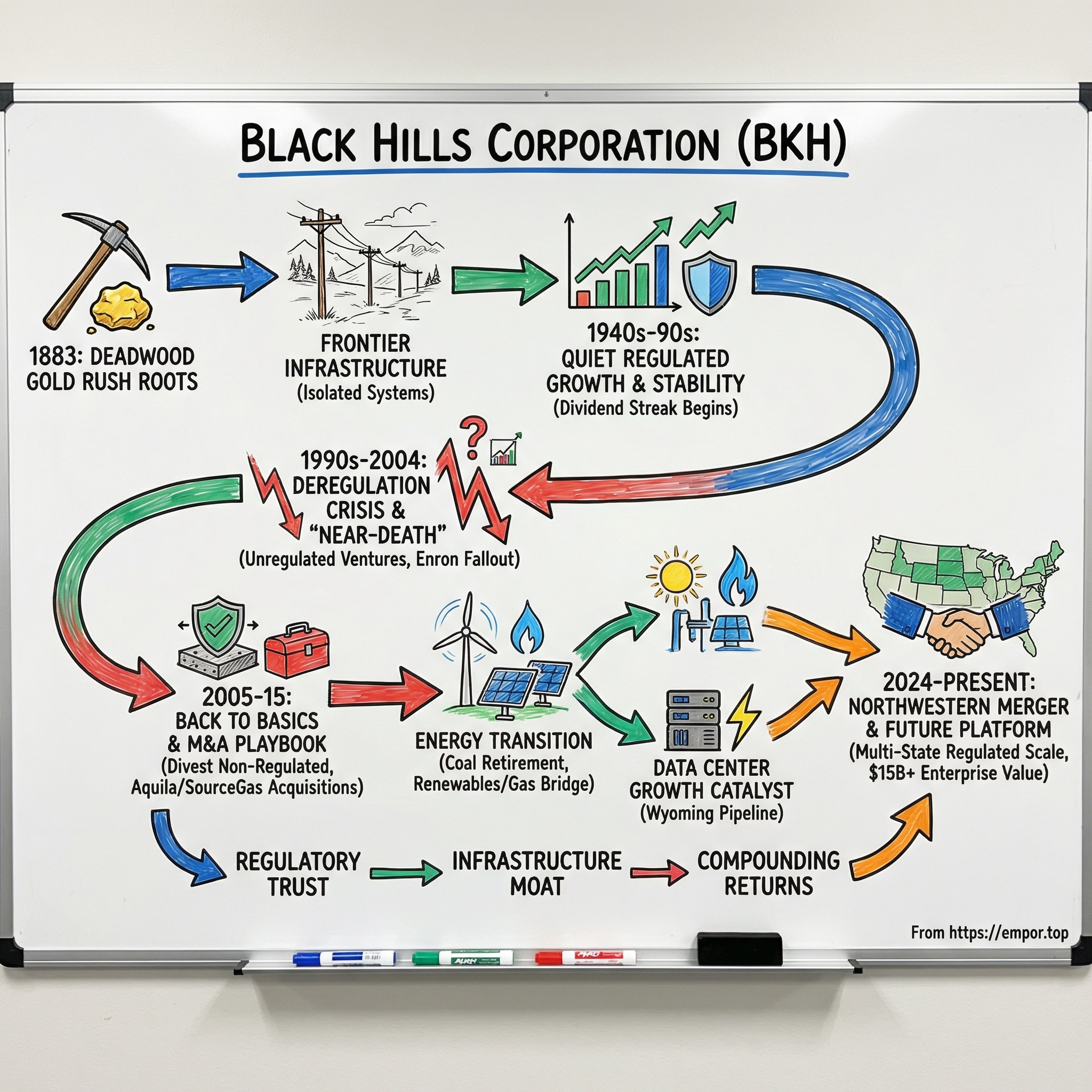

Black Hills Corporation: From Gold Rush Roots to Modern Energy Infrastructure

I. Introduction & Episode Roadmap

There is a company headquartered in Rapid City, South Dakota, that has been paying dividends without interruption since 1944 and has increased those dividends for 56 consecutive years, the second-longest streak in the entire American electric and natural gas utility industry. It operates across eight states, serves nearly 1.4 million customers, and commands an enterprise value north of ten billion dollars. And yet, if you asked most investors on Wall Street to name it, you would get a blank stare.

The company is Black Hills Corporation, ticker BKH on the New York Stock Exchange. And its story is one of the most fascinating case studies in American infrastructure capitalism.

The central question of this deep dive is deceptively simple: How did a frontier-era company incorporated during the Deadwood gold rush of 1883 become a diversified energy infrastructure operator spanning from Arkansas to Montana? The answer involves a near-death experience, a radical strategic pivot, a masterclass in regulatory capitalism, and a long-running M&A playbook that turned a sleepy South Dakota utility into a regional powerhouse now merging with NorthWestern Energy to create a combined enterprise worth over fifteen billion dollars.

This story matters because it illuminates the hidden world of regulated utilities, a sector that most investors dismiss as boring but that contains some of the most durable business models in capitalism. Regulated utilities are, in a sense, the ultimate infrastructure moat: geographic monopolies backed by legal franchise, earning guaranteed returns on physical assets that last for decades. They are the antithesis of the venture-backed technology startups that dominate financial media, and yet they are the literal foundation upon which modern society operates. Every time someone flips a light switch, turns on a furnace, or charges an electric vehicle, they are interacting with companies like Black Hills.

The themes that run through this story are universal: regulatory capitalism and how to make money inside highly regulated industries; M&A as strategy rather than distraction; survival through reinvention after near-catastrophic failure; and the energy transition, which is simultaneously the greatest challenge and the greatest opportunity facing the utility sector. By the end, the framework for evaluating any regulated utility will be clear, along with an understanding of why a 143-year-old company from the Black Hills of South Dakota might be more relevant today than at any point in its history.

II. Origins: The Wild West & Early Infrastructure (1880s-1940s)

Picture Deadwood, South Dakota, in the early 1880s. The gold rush that drew Wild Bill Hickok and Calamity Jane to this lawless gulch a few years earlier had matured from a tent-city bonanza into something more permanent. Miners were staking claims, saloons were being replaced by general stores, and the emerging town faced a fundamental problem: darkness. Underground mining shafts needed illumination. Streets needed light. And the same streams and geological forces that deposited gold in the Black Hills also offered something else, moving water and combustible fuel to generate electricity.

In 1883, Black Hills Corporation was incorporated as a South Dakota company, its origins inextricably tied to the gold mining industry and the electricity generation needed to power it. This was frontier infrastructure in the most literal sense: building energy systems in remote, harsh terrain where winter temperatures plummeted well below zero and the nearest major city was hundreds of miles away. The early operators were not financiers or professional utility managers. They were pragmatists, mining engineers and entrepreneurs who understood that whoever controlled the energy supply controlled the economic lifeblood of the region.

Over the next several decades, the company evolved from its mining roots into a dedicated power provider, consolidating smaller operations across the Black Hills region. The geography itself became the moat. Building competing power infrastructure in this terrain, across vast distances of sparsely populated high plains and rugged hills, was economically irrational. One set of power lines, one set of generating stations, one distribution network. This was a natural monopoly before anyone used that term, and the customers who depended on it had no alternative.

By 1941, the company had formally reorganized as Black Hills Power & Light Company, a name that signaled its full transformation from mining adjunct to standalone utility. The philosophy that took root during those frontier decades still defines the company: provide essential services to communities that have no other option, invest in durable infrastructure that lasts for generations, and earn the trust of the people you serve because they cannot go anywhere else. That last part, the captive customer base, is what makes the regulated utility model so distinctive. It is also what makes the regulatory relationship so critical, because a monopoly provider without oversight would be a recipe for exploitation.

What those early pioneers built in the Black Hills was more than copper wire and wooden poles. They built the template for a business that would compound quietly for over a century. The infrastructure investments made in those early decades, the transmission lines, the generation capacity, the distribution networks, created assets that would earn returns for their owners long after the gold mines played out. And the geographic monopoly they established, reinforced by state franchise agreements and regulatory compact, proved to be one of the most durable competitive advantages in American business.

Those frontier roots also instilled a cultural identity that would prove decisive when the company later faced existential crisis: the belief that they were infrastructure operators, not financial engineers. Builders of things that mattered, not traders chasing speculative profits. That distinction would nearly be forgotten in the 1990s, almost killing the company, before being rediscovered just in time.

III. The Regulated Utility Model: Understanding the Game

Before going further into Black Hills' story, it is worth pausing to understand the peculiar business model that governs nearly everything about how this company, and its peers, make money. The regulated utility model is one of the oldest and most misunderstood structures in American capitalism, and understanding its mechanics is essential to understanding why utilities behave the way they do.

The foundation is something called the "regulatory compact," a bargain first articulated in the Supreme Court's 1865 Binghamton Bridge case. The deal is straightforward: the government grants a utility an exclusive franchise to serve a defined geographic territory, a legal monopoly. In exchange, the utility accepts two obligations. First, it must serve every customer in its territory, regardless of how remote or unprofitable that customer might be. Second, it must submit to price regulation by a state Public Utilities Commission (PUC), which determines how much the utility can charge.

This creates a business model unlike almost anything else in the economy. Think of it this way: imagine a business where the government guarantees you will have no competition, guarantees that every household and business in your territory must buy your product, and then tells you exactly how much profit you are allowed to make. That is, in essence, what a regulated utility is.

The profit mechanism works through something called "rate base." Rate base is the total value of the utility's physical assets, power plants, transmission lines, gas pipelines, distribution networks, minus accumulated depreciation. The utility is allowed to earn a regulated rate of return on this asset base. The formula is straightforward: Revenue Requirement equals Rate Base multiplied by the authorized Weighted Average Cost of Capital, plus operating expenses. The most contested variable in this formula is the authorized Return on Equity, which in recent years has averaged around 9.6-9.8 percent for electric utilities and similar for gas utilities.

Here is a simplified analogy to make this concrete. Imagine a landlord who owns a building worth one million dollars and is allowed by law to charge rent that generates a ten percent return on the building's value, or one hundred thousand dollars per year. If the landlord builds an addition worth five hundred thousand dollars and the regulator approves it as a legitimate investment, the landlord can now charge rent on a $1.5 million building, generating $150,000 per year. The building is the rate base, the rent is the revenue requirement, and the ten percent is the authorized ROE. The incentive to keep building is obvious.

The implications of this formula are profound. Because the utility earns a fixed percentage return on its asset base, every dollar of new capital investment that a regulator approves translates directly into more profit. This is the Averch-Johnson effect, named after the economists who identified it: regulated utilities have a built-in incentive to invest as much capital as possible, because a larger rate base means larger absolute profits. A utility that spends a billion dollars on a new transmission line, with an approved ten percent return on equity, earns a hundred million dollars annually on that investment. The more you build, the more you earn.

This incentive structure explains why utilities love capital expenditure announcements, why they enthusiastically embrace grid modernization and renewable energy mandates, and why they are among the most aggressive acquirers of infrastructure assets. It also explains why regulators exist: without oversight, utilities would gold-plate every pole, wire, and pipeline. The regulatory relationship is a constant negotiation, with the utility seeking to maximize its rate base and the regulator seeking to protect ratepayers from excessive costs.

At the federal level, the Federal Energy Regulatory Commission (FERC) oversees interstate transmission and wholesale electricity markets. But the real action happens at the state level, where Public Utilities Commissions conduct "rate cases," essentially trials in which the utility presents its costs and investment needs, consumer advocates argue for lower rates, and commissioners make the final determination. A constructive regulatory environment, one where commissioners understand the need for infrastructure investment and approve reasonable returns, can make or break a utility's financial performance.

This is why the regulated utility model is sometimes called "boring but beautiful." The cash flows are remarkably predictable. The dividend streams are among the most reliable in any industry. The risk profile is low, with beta values typically well below one. But the trade-offs are real: growth is constrained to the rate at which regulators approve new investment, political exposure is constant, and a single bad rate case decision can impair returns for years. The game is not about disrupting markets or launching new products. It is about deploying capital efficiently, earning regulatory trust, and compounding returns slowly over decades.

Black Hills Corporation has played this game for over a century. But as the story will reveal, it once tried to play a different game entirely, and nearly destroyed itself in the process.

IV. Steady State: The Quiet Decades (1940s-1990s)

The half-century following Black Hills Power & Light's 1941 reorganization was the golden age of the American utility model. Across the country, utilities were electrifying rural America, extending natural gas pipelines to communities that had relied on coal stoves and kerosene lamps, and building the physical infrastructure that would underpin the postwar economic boom. Black Hills was a small but steady participant in this transformation.

The company's territory encompassed some of the most sparsely populated landscape in the continental United States: the western Dakotas, parts of Wyoming and Montana. This was cattle country, ranch country, mining country, places where the nearest neighbor might be ten miles away and where winter storms could isolate entire communities for days. Serving these customers was not glamorous. It required linemen willing to repair downed power lines in forty-below windchills, engineers who understood the stress that extreme temperature swings imposed on equipment, and a management team content with slow, steady growth rather than headline-grabbing expansion.

And slow, steady growth is exactly what they delivered. Year after year, Black Hills paid its dividends, maintained its infrastructure, and served its customers. The company's dividend streak, which would eventually stretch to 56 consecutive years of increases, began its unbroken run in the late 1960s. Management was conservative, customer-focused, and community-oriented, reflecting the values of the small cities and towns it served. Rapid City, the company's headquarters and South Dakota's second-largest city, was and remains a place where the utility CEO knows the mayor personally, where employees are neighbors to the customers they serve, and where corporate decisions are felt directly by the community.

This intimacy cut both ways. It created deep loyalty and trust, assets that would prove invaluable in regulatory proceedings. But it also fostered a certain insularity, a sense that the world beyond the Black Hills would always remain at arm's length. During these decades, the broader utility industry was beginning to change. Deregulation debates were gaining momentum in academic circles and state legislatures. Larger utilities were consolidating, forming holding companies, and preparing for what many believed would be a fundamental restructuring of the electricity business.

Black Hills stayed independent. Partly by choice, partly by circumstance. The company was too small and too remote to attract serious acquisition interest, and its management saw no reason to fix what was not broken. During the great consolidation waves of the 1980s and 1990s, when holding companies like American Electric Power, Duke Energy, and Southern Company were assembling sprawling multi-state empires, Black Hills barely registered on the radar of investment bankers looking for acquisition targets. Its market capitalization was a rounding error compared to the industry giants. Its service territory, while vast in geography, was thin in customer density. And its management, deeply rooted in the communities they served, had no appetite for the financial engineering that characterized the era's mega-mergers.

But this independence, which might have looked like irrelevance at the time, was actually preservation. The company retained its identity, its culture, and its focus on the fundamentals of utility operations. The foundations being laid during these quiet decades, the transmission networks, the customer relationships, the regulatory trust, the operational expertise in harsh-climate utility operations, were invisible to the outside world but would prove to be the bedrock upon which the company's future was built.

Financially, the quiet decades established the pattern that investors would come to depend upon. The dividend payout, unbroken since 1944, grew slowly but steadily. Earnings per share expanded modestly, driven by population growth in the service territory and periodic rate case approvals that allowed the company to recover its infrastructure investments. There was nothing spectacular about the numbers, no year that would have caught anyone's attention on a Bloomberg terminal. But the trajectory was unmistakably upward, and the reliability was extraordinary. The brewing tension of deregulation, however, was about to test everything the company had built.

V. The Deregulation Shock & Strategic Pivot (1990s-2000s)

In 1992, Congress passed the Energy Policy Act, a piece of legislation that sent shockwaves through the utility industry. The Act created a new category of power generators, called "exempt wholesale generators," that could operate outside traditional utility regulation. It also directed FERC to develop rules opening utility transmission networks to competition. The conceptual separation of generation from transmission and distribution had begun, and the implications were revolutionary. For the first time since the utility model was established, the question was on the table: could electricity be bought and sold in competitive markets, like wheat or oil?

By 1996, FERC had issued Orders 888 and 889, mandating non-discriminatory access to utility transmission systems and creating the framework for Independent System Operators and Regional Transmission Organizations. States began experimenting with retail deregulation: California led the way with AB 1890 in 1996, freezing retail rates while deregulating wholesale markets. Pennsylvania, Texas, and others followed.

The industry fractured along philosophical lines. Some utilities embraced the new world with evangelical fervor, spinning off generation assets, building merchant power plants, and creating energy trading desks that would have been unrecognizable to the engineers who had built the grid. Enron became the poster child for this vision, a company that reimagined itself as an energy trading platform rather than a traditional gas pipeline operator, eventually expanding into bandwidth trading, weather derivatives, and increasingly exotic financial instruments. At its peak, Enron was the seventh-largest company in America by revenue, and its executives preached that the old regulated model was dead.

Black Hills faced a choice that every utility in America confronted during this period: stay the course with the traditional regulated model, or diversify into the exciting, fast-growing, higher-margin world of unregulated energy. Management chose to diversify. The company expanded into independent power production, building and acquiring merchant generating plants that sold electricity on the wholesale market. It launched energy marketing operations. It entered the oil and gas exploration business. The rationale was understandable: if the regulatory compact was going to unravel, better to have a foot in both worlds.

The early results looked promising. Non-regulated revenues grew. Earnings diversified. The company appeared to be successfully adapting to the new energy landscape. But beneath the surface, something dangerous was building. The non-regulated businesses introduced volatility into what had been one of the most stable earnings streams in corporate America. The skills required to run a regulated utility, patience, regulatory relationship management, long-term infrastructure planning, were fundamentally different from the skills required to trade energy commodities or manage merchant power plant economics. The company was stretching itself across businesses that demanded different cultures, different risk tolerances, and different management competencies. Warning signs were visible to anyone who looked closely, but in the late 1990s, with Enron's stock soaring and the merchant power model appearing to print money, few were looking.

The broader industry context is important here. Between 1992 and 2001, approximately fifteen states and the District of Columbia implemented some form of retail deregulation. The theory was intellectually elegant: separate the naturally monopolistic elements of the electricity business (transmission and distribution wires) from the potentially competitive elements (generation and retail supply), and let market forces drive down prices. In practice, the implementation was riddled with design flaws, particularly in California, where retail rate freezes were paired with wholesale deregulation, creating an asymmetry that would prove catastrophic. But at the time, deregulation felt inevitable, like the tide of history. Utilities that clung to the old regulated model were dismissed as dinosaurs. Black Hills did not want to be a dinosaur.

VI. Crisis & Near-Death Experience (2000-2004)

The unraveling began in California. The state's deregulated wholesale market, combined with frozen retail rates, created a perfect storm. Wholesale electricity prices exploded, rising 277 percent in a single year, from $7.4 billion in 1999 to $27.1 billion in 2000. Enron's traders actively manipulated the market using strategies with darkly colorful names like "Fat Boy," "Death Star," and "Ricochet," including encouraging suppliers to shut down plants for unnecessary maintenance during peak demand. California experienced six days of rolling blackouts, the first statewide power curtailments since World War II. The total damage was estimated at forty to forty-five billion dollars. PG&E, the state's largest utility, filed for Chapter 11 bankruptcy in April 2001.

Then Enron itself imploded. In October 2001, the company disclosed massive accounting fraud involving off-balance-sheet entities designed to hide debt and inflate earnings. By December, Enron had filed for bankruptcy, then the largest in American history. Its auditor, Arthur Andersen, was dissolved. The Sarbanes-Oxley Act of 2002 followed, imposing sweeping new governance requirements on public companies.

For Black Hills, the consequences were immediate and severe. The merchant power plants that had seemed like smart diversification bets were suddenly hemorrhaging cash. Wholesale electricity prices, which had spiked during the California crisis, collapsed in the aftermath, leaving merchant generators with expensive assets producing power nobody wanted to buy at profitable prices. Energy trading operations, which depended on liquid markets and willing counterparties, seized up as credit dried up across the entire energy sector. Banks and rating agencies that had cheerfully financed the deregulation boom now demanded blood.

Black Hills' stock price collapsed, declining over seventy percent from its highs. Credit ratings were downgraded, tightening the company's access to the capital markets that utilities depend upon for continuous infrastructure investment. The liquidity crunch was existential. For a company that had paid dividends without interruption since 1944, the possibility of cutting or eliminating the dividend, the ultimate sign of distress for a utility, was no longer theoretical.

The boardroom response was dramatic. Management was shaken up. A comprehensive strategic review was launched. The hard questions that should have been asked before the diversification push were now asked under duress: What business are we actually in? What are we good at? What nearly killed us? The answers were painful but clarifying. Black Hills was an infrastructure operator, not an energy trader. The company's competence was in building and maintaining physical assets, earning regulatory trust, and delivering essential services to captive customers. Every dollar invested in non-regulated businesses had been a dollar diverted from the core competency that had sustained the company for over a century.

The asset sales began. Non-regulated generation was divested. Energy marketing operations were wound down. Oil and gas interests were sold. Cost cuts rippled through the organization. The company retrenched to what it knew: regulated utility operations in the Northern Great Plains.

The philosophical reset was profound. In corporate strategy, there is a concept called "strategic clarity," the moment when an organization stops trying to be everything and commits fully to what it actually is. For Black Hills, the crisis of 2000-2004 delivered that clarity through pain. The company's board and incoming management articulated a principle that sounds simple but required enormous discipline to maintain: "We are infrastructure operators, not traders." This was not just a slogan. It was a binding commitment that would govern capital allocation, acquisitions, and organizational design for the next two decades. Every proposed initiative would be tested against a simple question: does this expand our regulated infrastructure platform, or does it take us back toward the unregulated risk that nearly destroyed us?

The comparison with PG&E is instructive. PG&E's first bankruptcy in 2001 was a product of the same deregulation disaster that threatened Black Hills. But PG&E would go on to face a second, even more devastating bankruptcy in 2019 over wildfire liabilities, a product of California's unique inverse condemnation doctrine that holds utilities strictly liable for fire damage caused by their equipment regardless of negligence. Black Hills, operating in states without such punitive liability frameworks, was insulated from that particular risk. But the near-death experience of 2000-2004 left scars that would shape every strategic decision for the next two decades. The lesson was seared into the corporate DNA: stay in your lane, and your lane is regulated infrastructure.

VII. Back to Basics & The M&A Playbook (2005-2010)

The man who would chart the company's course out of crisis was David Emery, who took the helm as CEO in 2004. Emery inherited a company that was bruised, humbled, and strategically confused, but not broken. The regulated utility operations had continued to function throughout the turmoil, generating stable cash flows and maintaining the dividend streak that was the company's most prized financial credential. What Emery brought was clarity of purpose and a contrarian conviction.

His strategic pivot was simple to articulate but difficult to execute: sell every non-regulated asset, double down on regulated utilities, and grow through disciplined acquisitions. This was contrarian because, even after the Enron disaster, many utility executives still believed in the deregulated model. The merchant power market was down but not out, and some companies continued to chase unregulated upside. Emery went the other direction entirely.

The company systematically exited independent power production, shed its oil and gas operations, and unwound its energy marketing business. Every dollar of proceeds was recycled into the regulated utility platform. And then Emery unveiled the real strategy: geographic diversification through acquisition.

The thesis was elegant. Black Hills would identify subscale regulated utilities in growing regions, particularly in the western Great Plains and Rocky Mountain states, acquire them at reasonable prices, improve their operations, and earn regulatory trust in new jurisdictions. The playbook had several advantages. First, it expanded the company's earnings base without increasing its exposure to unregulated risk. Second, it diversified regulatory exposure across multiple states, reducing dependence on any single PUC's decisions. Third, it created operational scale that improved efficiency and justified the overhead of a public company.

The transformative deal came in 2008, when Black Hills acquired the regulated natural gas utility operations in Colorado, Kansas, Nebraska, and Iowa from Aquila, Inc. for approximately $940 million. The impact was staggering. The customer base surged from roughly 137,000 to 753,000, nearly a six-fold increase. The employee count more than doubled from 916 to approximately 2,000. Overnight, Black Hills went from a single-state electric utility to a multi-state, multi-commodity energy company operating gas and electric systems across five states.

The Aquila acquisition was not just about scale. It was about portfolio construction. By adding natural gas distribution to its predominantly electric platform, Black Hills gained a second revenue stream with different seasonal patterns, different capital investment cycles, and different regulatory dynamics. Gas utilities peak in winter when heating demand is highest; electric utilities in many Northern Plains territories peak in summer with air conditioning load. The combination smoothed earnings and created year-round capital deployment opportunities.

Financing this ambition while maintaining investment-grade credit ratings required discipline. Black Hills used a mix of debt and equity, careful to maintain the balance sheet ratios that rating agencies demanded. The company could not afford another credit downgrade, not after the near-death experience of the early 2000s. Every acquisition had to be immediately accretive or have a clear path to accretion within one to two years. And every acquired operation had to be integrated quickly and efficiently, with cost savings extracted and regulatory relationships preserved.

The cultural integration challenge was real. Aquila's operations had been run as part of a much larger, more complex organization that had its own strategic problems. Aquila itself was in the process of unwinding after its own disastrous foray into unregulated energy markets, a fate that paralleled Black Hills' experience but on a larger and more terminal scale. Black Hills' approach was to bring these utilities under the Black Hills Energy brand, impose its operational standards, and invest in the infrastructure that the prior owner had sometimes deferred. Customer-facing operations were unified, back-office functions were consolidated, and capital was deployed into the pipeline replacements and grid upgrades that had been deferred under prior ownership.

This "buy, improve, integrate" playbook would become the company's signature, repeated with increasing confidence over the following decade. The key insight was that regulated utility acquisitions, unlike many corporate M&A transactions, have a built-in integration advantage: the customer base is captive, the revenue stream is regulated and predictable, and the operational challenge is about execution quality rather than market competition. You do not have to worry about customers leaving after an acquisition because they cannot leave. What you do have to worry about is maintaining regulatory trust, preserving service quality, and demonstrating to the PUC that the new owner is a better steward of the franchise than the old one.

VIII. The Regulatory Arbitrage Strategy (2010-2015)

One of the least appreciated aspects of Black Hills' strategy is its implicit understanding that not all regulatory jurisdictions are created equal. This insight, obvious in hindsight but rarely articulated by utility management teams, became the foundation for how the company selected acquisition targets and allocated capital.

The states where Black Hills operates, South Dakota, Wyoming, Colorado, Kansas, Nebraska, Iowa, Montana, and Arkansas, share several important characteristics. All of them maintain traditional cost-of-service regulation with no retail deregulation. All of them have Public Utilities Commissions that, while rigorous, generally operate within a framework that recognizes the need for infrastructure investment and the importance of utilities earning adequate returns. And all of them are growing, some modestly and some significantly, particularly in energy-intensive sectors like data centers and manufacturing.

The company's approach to these regulators was not adversarial but collaborative. The "trusted operator" model meant investing proactively in infrastructure, maintaining high reliability, keeping costs disciplined, and being transparent in rate case proceedings. When Black Hills filed for rate increases, it came to the table with evidence of investments made, service improved, and costs managed. This approach earned the company consistently constructive outcomes across its jurisdictions.

The capital deployment machine that Black Hills built during this period was relentless. Every year, the company identified and executed hundreds of millions of dollars in infrastructure investments: pipeline replacements for safety and integrity, grid modernization to improve reliability, transmission upgrades to support growth, and early-stage renewable energy integration. Each of these investments expanded the rate base, and each expansion of the rate base translated into regulated earnings growth, which in turn supported dividend increases.

The dividend growth algorithm was the glue that held the strategy together for investors. Regulated earnings growth, driven by rate base expansion, funded predictable dividend increases. The market rewarded this predictability with a stable valuation and access to capital markets on favorable terms, which in turn enabled more investment. It was a virtuous cycle, the kind of compounding machine that value investors love but that rarely makes headlines.

How did Black Hills compare to its peers? The multi-state model was distinctive. Many utilities of similar size were concentrated in a single state, making them dependent on one regulatory relationship. A bad rate case in that one state could impair returns for years. Black Hills' eight-state footprint meant that an unfavorable outcome in one jurisdiction could be offset by constructive outcomes in others. Xcel Energy, the largest peer in the region, operated a similar multi-state model but at much greater scale. MDU Resources, Avista, NorthWestern Energy, and Otter Tail each had their own geographic and business-mix characteristics, but none replicated Black Hills' particular combination of eight-state diversification with a near-pure-play regulated utility focus.

How did Black Hills compare to its peers on the financial dimension? The company's authorized ROEs across its jurisdictions varied meaningfully: 9.3-9.5 percent in Colorado electric, 9.85 percent in Nebraska gas, with requests pending for 10.5 percent in Kansas and Arkansas gas operations. The spread between these authorized returns and the actual earned returns, a metric the industry calls "regulatory lag," was a constant management challenge. Utilities that consistently earn close to their authorized returns demonstrate operational efficiency and effective rate case execution. Those that chronically under-earn, a problem more common than investors realize, signal either operational inefficiency or an adversarial regulatory environment.

The risks of this strategy were real but manageable. Regulatory capture, the perception that a utility has too-cozy a relationship with its regulators, could invite political backlash. Stranded asset fears, particularly around coal generation, loomed as climate concerns intensified. And operating across eight regulatory jurisdictions meant fielding eight different rate cases, each with its own timeline, its own intervenors, and its own political dynamics. But for Black Hills, this complexity was a feature, not a bug. A bad outcome in Kansas could be offset by a constructive outcome in Colorado. A challenging political environment in one state would rarely coincide with difficulty in all eight.

IX. Modern Challenges: The Energy Transition (2015-2020)

By the middle of the decade, a new force was reshaping the utility industry: the energy transition. The rapid decline in renewable energy costs, the rise of ESG investing, and growing political pressure for decarbonization created both existential challenges and enormous opportunities for companies like Black Hills.

The company's coal problem was immediate and visible. Black Hills operated coal-fired generation at its Neil Simpson and Wygen complex near Gillette, Wyoming, adjacent to the Wyodak Mine, the oldest operating surface coal mine in the United States with permitted reserves of 286 million tons. In an era when institutional investors were divesting from coal and state legislatures were passing clean energy mandates, owning and operating coal generation made Black Hills a target for ESG-focused activists.

But the reality was more nuanced than the headlines suggested. The coal plants provided reliable, dispatchable power to communities that experienced some of the most extreme weather in the country. Shutting them down without adequate replacement capacity would threaten grid reliability and spike customer bills. The regulatory tightrope was delicate: retire coal assets on a timeline that satisfied environmental concerns while ensuring that replacement generation was in place and that customers were not burdened with excessive costs.

Black Hills navigated this tightrope more skillfully than most observers expected. The company became the first electric utility in Colorado to retire all of its coal plants, achieving that milestone in 2013. For the Wyoming and South Dakota operations, where coal dependence was deeper, the approach was more gradual. Neil Simpson I, a 21.7-megawatt unit, was retired in 2014. Larger units at the Wygen complex remained operational, but the company developed integrated resource plans that laid out pathways to reduce coal dependence over time.

The renewable pivot was real and substantive. The company's Colorado Clean Energy Plan, branded "2030 Ready," committed to adding 350 megawatts of new renewable resources by 2027, including two utility-scale solar projects totaling 300 megawatts and a 50-megawatt battery storage facility. By 2030, 75 percent of Colorado customers' energy needs would be powered by renewable resources, exceeding the state's mandate of 80 percent emissions reduction. An additional 400 megawatts of renewable resources were recommended beyond this initial plan.

Natural gas became the bridge fuel strategy. The Lange II project, a 99-megawatt natural gas generation facility in Rapid City featuring six reciprocating internal combustion engines with dual-fuel capability, was approved to replace the retiring Ben French coal units. At $280 million, it represented a significant rate base investment while providing the dispatchable generation needed to back up intermittent renewables. This approach, replacing coal with gas while simultaneously adding renewables, reflected the pragmatic middle path that most utilities in non-coastal states were pursuing.

The ESG investor pressure created a paradox that Black Hills and its peers exploited brilliantly. Environmental mandates required massive infrastructure investment, and massive infrastructure investment was exactly how regulated utilities grew their earnings. Every wind turbine, every solar panel, every battery storage facility, every mile of transmission line to connect renewable generation to the grid, all of it entered the rate base and earned the authorized return. The energy transition, far from being a threat to the utility business model, was potentially the greatest growth catalyst the industry had seen in decades.

Wildfire risk and infrastructure resilience entered the conversation as well. The catastrophic California wildfires of 2017-2018, and PG&E's resulting bankruptcy, terrified the entire utility industry. PG&E faced over thirty billion dollars in potential wildfire liabilities under California's inverse condemnation doctrine, which holds utilities strictly liable regardless of negligence. Warren Buffett, whose Berkshire Hathaway Energy subsidiary operated PacifiCorp, called the utility sector outlook "ominous" and said Berkshire would avoid investing in states with unfavorable wildfire liability laws. Black Hills' Northern Great Plains territory carried wildfire risk, particularly in Colorado and Montana, but nothing comparable to the tinderbox conditions of the Pacific coast. The regulatory frameworks in its states did not impose the same strict liability standards that made California utility ownership so perilous.

The business model advantage became increasingly clear: regulated utilities could actually benefit from the energy transition in ways few other industries could. For regulated utilities, every mandate to build clean energy, every requirement to modernize the grid, every directive to prepare for extreme weather translated into capital investment that entered the rate base and earned the authorized return. The energy transition was not happening to utilities. It was happening through them, and smart operators recognized that the regulatory framework transformed what looked like a threat into a generational growth opportunity.

Emissions reduction progress was measurable. By the time the company published its 2024 sustainability report, electric utility emissions had declined 38 percent from 2005 baseline levels. The company set targets of 40 percent reduction by 2030 and 70 percent by 2040, with plans already in place to achieve these goals without reliance on future technologies. On the natural gas side, the company committed to achieving net-zero emissions for its gas distribution system by 2035, reporting a 27 percent reduction in gas utility emissions since 2022 through pipeline replacement programs that reduced methane leaks. The company also began partnering on coal-to-hydrogen technology and completed initial testing of carbon sequestration capabilities at its Gillette, Wyoming energy complex, hedging against multiple potential futures for its coal-adjacent assets.

X. The Pandemic, Supply Chain, and Inflation Era (2020-2023)

When COVID-19 shut down the American economy in March 2020, utilities faced a paradox. They were among the most essential of essential services, operating under a federal classification that kept their workers in the field while most of the country sheltered at home. Power plants could not be idled. Gas pipelines could not be shut down. But the pandemic's economic fallout created real financial stress.

Black Hills moved proactively, suspending nonpayment disconnections and late-payment charges on March 16, 2020, ahead of statewide mandates. The company committed that no residential customer would lose service and extended this suspension well beyond most state requirements. Budget billing was made available to customers with past-due balances, reversing the prior requirement that only current accounts could access the program. The company allocated $375,000 for food insecurity and emergency pandemic needs through United Way organizations, plus $225,000 for its Black Hills Cares energy assistance program, helping approximately 2,500 families.

The financial impact was real but contained. Bad debt expense increased as customers struggled to pay bills. Commercial and industrial demand softened as businesses closed or reduced operations. Regulatory filings were complicated by the uncertain economic backdrop, as the normal cadence of rate cases and capital recovery proceedings was disrupted by the pandemic's logistical and political dynamics. Regulators in several states implemented emergency rate riders and recovery mechanisms to help utilities manage the financial stress.

But the regulated utility model provided meaningful insulation. Unlike retailers, airlines, or restaurants, which saw demand evaporate overnight, utilities experienced demand shifts rather than demand destruction. Residential usage increased as people worked from home. Commercial and industrial usage declined, but the net impact on total system demand was modest. Customers still needed heat in winter and electricity year-round. Revenue per customer remained relatively stable even as overall economic activity contracted. The company continued to execute its capital investment program, maintaining the rate base growth trajectory that drove earnings.

Then came Winter Storm Uri in February 2021, one of the most devastating weather events in American energy history. The Arctic blast that froze Texas and much of the central United States drove record demand for natural gas heating while simultaneously disrupting supply chains, causing natural gas commodity prices to spike to extraordinary levels. Black Hills incurred approximately $546 million in incremental costs across its gas utility operations to procure natural gas and maintain service during the storm. The company took out an $800 million unsecured term loan to provide the liquidity needed to absorb the spike.

The response tested every regulatory relationship the company had built. Black Hills filed for cost recovery in every affected state, and the outcomes demonstrated the value of decades of regulatory trust. Kansas approved recovery of $87.9 million over five years. Colorado settled at $72.7 million. Each state commission, working through its own process, approved recovery plans that spread costs over multiple years to minimize bill impact. The company provided $450,000 in additional customer assistance funding to mitigate the impact. Critically, Black Hills' pipeline system performed with excellent reliability during the storm. The cost was primarily from commodity procurement, not infrastructure failure, a distinction that mattered enormously in regulatory proceedings.

Supply chain chaos defined 2021-2023 across the utility sector. Lead times for large power transformers extended to two or three years. Equipment costs inflated significantly. Labor shortages complicated construction timelines. For Black Hills, these challenges meant delays and cost increases on capital projects, but the regulated cost recovery framework provided a mechanism to pass through reasonable costs to customers.

The inflation era's most painful impact on utilities was not operational but financial. The Federal Reserve's aggressive interest rate increases, which took the federal funds rate from near zero to over five percent, hammered utility stock valuations. Utilities are considered "bond proxies" because of their high dividend yields and stable cash flows. When Treasury yields exceed utility dividend yields, the relative attractiveness of utility stocks diminishes, and valuations compress. The utility sector's roughly 3.4 percent average dividend yield in 2025 trailed the approximately 4.7 percent ten-year Treasury yield, creating a headwind that depressed share prices across the sector.

Through all of this, Black Hills continued its acquisition playbook. The SourceGas acquisition, which had closed in February 2016 for $1.89 billion, had already added approximately 429,000 natural gas customers in Arkansas, Colorado, Nebraska, and Wyoming, increasing the total customer count by 55 percent and giving the company its first-ever presence in Arkansas. The deal also brought a 512-mile regulated intrastate natural gas transmission pipeline in Colorado, a significant infrastructure asset. By the early 2020s, these operations were fully integrated under the Black Hills Energy brand, rebranded beginning in March 2016, contributing stable regulated earnings and providing the geographic diversification that continued to reduce single-state regulatory risk.

The leadership transition during this period was notable. Linn Evans, who had joined Black Hills in 2001 as an attorney, succeeded David Emery as CEO on January 1, 2019. Evans brought an unusual background to the role: a mining engineer by training, with a BS from Missouri Science & Technology and experience in underground gold, iron ore, lead, and zinc mines across North and South America. He later earned a law degree from Lewis & Clark College specializing in environmental and natural resources law. His career at Black Hills had included stints as Associate General Counsel, head of the company's former telecommunications business (Black Hills FiberCom), and President and COO of utility operations. This combination of engineering pragmatism and legal acumen made Evans well-suited to navigate the regulatory complexities of an eight-state utility platform during a period of unprecedented operational challenge.

XI. Today & The Road Ahead (2024-Present)

If the deregulation crisis was the darkest chapter in Black Hills' history, the current moment may be its most consequential. The most significant corporate development in the company's 143-year history was announced on August 19, 2025: an all-stock merger with NorthWestern Energy. The deal, valued at approximately $3.6 billion, brings together two adjacent-territory operators in a combination that reflects the broader consolidation wave sweeping the utility sector. Under the terms, NorthWestern shareholders will receive 0.98 shares of Black Hills common stock for each NorthWestern share. Upon completion, Black Hills shareholders will own approximately 56 percent and NorthWestern shareholders approximately 44 percent of the combined entity.

The combined company will serve approximately 2.1 million customers, with roughly 700,000 electric and 1.5 million gas customers across eight contiguous states. The pro forma market capitalization is approximately $7.8 billion, with a combined enterprise value of roughly $15.4 billion. The combined rate base of approximately $11.4 billion provides the foundation for a capital plan exceeding seven billion dollars over the next five years. Brian Bird, NorthWestern Energy's current CEO, will lead the combined company, while Black Hills CEO Linn Evans will retire following the merger's close. Headquarters will remain in Rapid City.

The merger requires approval from FERC and public utilities commissions in Montana, Nebraska, and South Dakota. Both companies have scheduled virtual special shareholder meetings for April 2, 2026, to vote on the merger agreement. Closing is expected in the second half of 2026. The combined entity's long-term EPS growth target is 5-7 percent, an upgrade from each company's standalone target of 4-6 percent.

But the catalyst that has generated the most excitement among investors and analysts is something no one at Black Hills could have predicted when the company was exiting its non-regulated businesses two decades ago: data centers. Wyoming's low electricity costs, favorable tax climate, and access to transmission capacity have made it an increasingly attractive destination for hyperscale data center operators. Black Hills' data center pipeline now exceeds three gigawatts, having tripled in recent periods. To put that number in context, it is nearly eight times the current all-time peak load of 379 megawatts for the Wyoming Electric system.

Microsoft has been a long-standing customer in Cheyenne, Wyoming, and Black Hills has developed an innovative tariff structure that requires minimal capital investment from the utility to serve data center demand. In July 2024, the company announced a partnership with Meta to provide power for its newest AI data center in Cheyenne, with Meta expected to transition from construction power to permanent service in early 2026. Approximately 500 megawatts of data center demand is expected to be served by end of 2029, with the potential to more than double the EPS contribution to greater than ten percent of consolidated earnings.

The completion of the $350 million Ready Wyoming transmission project in December 2025, a 260-mile line interconnecting the Wyoming and South Dakota electric grids, is directly supportive of this data center growth thesis. Wyoming recorded 19 consecutive years of increasing electric demand, with a new all-time peak on June 20, 2025, representing a 21 percent increase over the prior year's record.

The financial picture as of early 2026 reflects steady execution. Black Hills reported 2025 adjusted EPS of $4.10, up nearly five percent from the prior year, excluding $0.12 per share of merger-related costs. Revenue for the full year reached $2.31 billion, rebounding from $2.13 billion in 2024, though revenue fluctuations at utilities are often driven by commodity pass-through costs rather than underlying business performance. The earnings trajectory and rate base growth are the more meaningful indicators of fundamental progress.

The company's 2026 guidance of $4.25 to $4.45 implies approximately six percent growth at the midpoint, positioned at the top end of the standalone 4-6 percent long-term target range. The 56th consecutive dividend increase was announced in early 2026, bringing the quarterly payout to $0.703 per share, representing approximately four percent growth and a yield of roughly 3.8 percent. These are not the growth rates that attract momentum investors, but they are exactly the kind of predictable, compounding returns that long-term holders of regulated utilities expect. The stock trades at approximately 13 to 14 times forward earnings with a dividend yield of roughly 3.8 percent, a valuation that reflects the quality of the business and the predictability of the cash flows, though elevated interest rates have compressed the multiple below historical averages.

The $4.7 billion five-year capital plan provides the foundation for continued rate base growth, focused on customer growth, system reliability, the Colorado Clean Energy Plan, data center infrastructure, and ongoing gas system safety investments across all eight states. Among the most notable near-term projects: the $280 million Lange II natural gas plant expected in service during the second half of 2026, the 350 megawatts of Colorado renewable resources by 2027, and 600 megawatts of data center-related infrastructure within the plan horizon. This capital intensity is the engine that drives regulated earnings growth, and the combined entity with NorthWestern will push the five-year capital plan above seven billion dollars.

XII. Porter's 5 Forces Analysis

Threat of New Entrants: Very Low

No one is going to build a competing electric distribution network in Rapid City. Think about what it would take: obtaining a Certificate of Public Convenience and Necessity from the state PUC, which would require proving that the existing utility is so deficient that a new entrant is necessary. Then investing billions of dollars in generation, transmission, and distribution infrastructure, much of it requiring rights-of-way, easements, and environmental permits that take years to obtain. Then convincing customers to switch to an unproven provider of a service that literally keeps their homes warm in forty-below winters. None of this happens in practice. The utility distribution network is the very definition of a natural monopoly: the cost of duplicating the physical infrastructure dwarfs any potential benefit from competition.

The only meaningful "entry" threat comes from distributed generation, primarily rooftop solar with battery storage, which allows customers to partially bypass the utility grid. But in Black Hills' Northern Plains territory, where solar irradiance is lower than in sunbelt states, where state incentives are more limited, and where the extreme winter climate makes grid independence impractical, this threat remains modest compared to what utilities in Arizona or California face.

Bargaining Power of Suppliers: Low to Moderate

Fuel costs, primarily natural gas and coal, are set by commodity markets but are largely passed through to customers via fuel adjustment clauses. The utility does not bear commodity price risk; customers do. Equipment suppliers have gained some leverage since 2022, with lead times for large power transformers extending to two or three years and costs inflating significantly. But these costs are ultimately recovered through the regulatory process. Black Hills' ownership of the Wyodak coal mine provides some vertical integration benefit, though coal's long-term role in the generation portfolio is diminishing.

Bargaining Power of Buyers: Very Low

This is the defining characteristic of the regulated utility model. Customers cannot switch providers. There is no competitor offering a lower price or better service. Electricity and natural gas are essential services with highly inelastic demand: people do not stop heating their homes because gas prices increase by five percent, and businesses do not relocate because electricity rates rise modestly. Rates are set by regulators, not negotiated individually.

The only meaningful check on utility pricing power is the regulatory process itself, where consumer advocates and industrial intervenors argue for lower rates during rate case proceedings. Large industrial customers with significant energy costs can participate aggressively in these proceedings, and their testimony can influence outcomes. Customer complaints do flow to regulators, and persistent dissatisfaction can influence commissioners' disposition toward the utility, but the fundamental dynamic is one of captive demand. No customer has ever "churned" away from Black Hills Energy to a competitor because no competitor exists.

Threat of Substitutes: Low but Growing

Rooftop solar paired with battery storage represents the most credible substitute, allowing customers to reduce or eliminate grid purchases. The "utility death spiral" thesis, which gained currency in the early 2010s, posits that as customers adopt solar and reduce grid purchases, the remaining customers bear a larger share of fixed infrastructure costs, driving rates higher and accelerating further defection. The thesis is intellectually coherent but has proven overstated in practice. Most research suggests that utility distribution infrastructure remains essential even for solar-equipped customers, and rate design reforms (fixed charges, time-of-use rates) can address the cross-subsidy problem.

Full grid defection remains impractical for most customers. The grid provides reliability that distributed systems cannot match, particularly in regions with harsh winters and limited solar resources like the Northern Great Plains. Energy efficiency reduces consumption but does not eliminate grid dependence. And the electrification megatrend, from vehicles to heating systems, actually increases total electricity demand, creating a tailwind for electric utilities even as it potentially threatens gas distribution volumes over the very long term. For Black Hills, whose gas customer base of 1.13 million dwarfs its 227,000 electric customers, the long-term trajectory of gas distribution volumes in an electrifying world is a question that deserves investor attention.

Competitive Rivalry: Very Low

Geographic monopolies eliminate direct competition within service territories by design. No two utilities compete for the same customer. This is the fundamental structural advantage that makes the utility business so different from virtually every other industry: there is no price competition, no product differentiation battle, no customer acquisition cost. The relevant "competition" occurs in three arenas: acquisition markets, where utilities bid against each other and private equity for regulated assets; regulatory benchmarking, where commissions compare performance metrics across utilities to determine whether their regulated utility is operating efficiently; and capital markets, where utilities compete for investor dollars based on growth profiles, dividend yields, and management credibility. Black Hills' relevant peer set includes Xcel Energy, NorthWestern Energy (soon to be merged), MDU Resources, Avista, and Otter Tail. But these companies do not compete for customers, making this one of the least competitive industry structures in the economy. The primary competitive variable, paradoxically, is not the market but the regulatory relationship.

XIII. Hamilton's 7 Powers Analysis

Scale Economies: Strong

Utility infrastructure is defined by high fixed costs spread over a customer base. Every mile of transmission line, every substation, every mile of gas pipeline represents a fixed cost that becomes cheaper per customer as density increases. Black Hills' eight-state platform, while not nationally scaled, is efficient within its footprint. The pending NorthWestern merger will create meaningful scale benefits, combining capital plans, shared services, and operational expertise across a contiguous geographic footprint. The combined $11.4 billion rate base provides a platform that neither company could have built independently in a reasonable timeframe.

Network Effects: Moderate

The physical grid exhibits network properties, more generation sources connected to the network improve reliability, and more transmission interconnections enable more efficient power flows, but customers do not directly benefit from other customers being on the same network the way social media users do. The emerging smart grid, with advanced metering infrastructure and real-time data analytics, creates nascent data network effects, but these are still early-stage. Network effects are not a primary source of competitive advantage for regulated utilities.

Counter-Positioning: Not Applicable

It is difficult to counter-position against a regulated monopoly. New entrants cannot offer a fundamentally different value proposition because the regulatory framework defines the product, the price, and the service obligation. Rooftop solar represents a partial counter-position, but utilities have adapted by owning community solar projects, integrating distributed resources, and advocating for rate design reforms that preserve their economics. Black Hills has not been meaningfully counter-positioned by any competitor or substitute.

Switching Costs: Absolute (for customers)

Customers literally cannot switch electric or gas utility providers in Black Hills' territories. This is not a switching cost in the traditional sense (where a customer could theoretically switch but faces friction), it is a legal impossibility. For investors, switching costs are moderate: one can sell BKH stock and buy another utility stock, but the dividend stream and compounding trajectory create meaningful stickiness for income-oriented investors. The regulatory franchise itself carries immense switching costs: once granted, a franchise is extraordinarily difficult to revoke.

Branding: Moderate

Black Hills is not a consumer brand in the traditional sense. Customers do not choose it; they are assigned to it by geography. But brand matters enormously in two contexts. First, regulatory proceedings: a utility with a reputation for reliability, responsiveness, and community investment is far more likely to receive constructive rate case outcomes than one known for poor service and antagonistic relationships. Second, acquisition approvals: when Black Hills seeks to acquire a utility in a new jurisdiction, its reputation as a "trusted operator" facilitates regulatory approval. The Black Hills Energy brand has been deliberately cultivated across all eight states, and its importance should not be underestimated even though it operates differently from a consumer-facing brand.

Cornered Resource: Strong

This is Black Hills' single most powerful source of competitive advantage. The franchise monopoly itself is a legally cornered resource, a government-granted exclusive right to serve a defined territory. The physical infrastructure, miles of pipe underground and wire overhead, cannot be replicated without billions of dollars and decades of effort. The regulatory relationships built over 140 years represent intangible assets that no competitor can quickly duplicate. Land rights, easements, rights-of-way, and interconnection points are physical cornered resources that enable the network to function. The eight-state platform that Black Hills has assembled through two decades of disciplined acquisitions is a unique resource in the mid-cap utility space.

Process Power: Moderate to Strong

Black Hills has developed genuine process power in several dimensions. Its rate case execution across eight jurisdictions reflects institutional expertise that competitors cannot easily replicate. The capital allocation discipline, identifying, acquiring, and integrating subscale utilities, has been refined through the Aquila and SourceGas deals and is now being applied at an even larger scale with the NorthWestern merger. Operational knowledge specific to harsh-climate utility operations, maintaining infrastructure at forty below zero, managing wildfire risk in the Mountain West, optimizing coal-to-gas-to-renewable generation transitions, represents embedded organizational capability built over 143 years.

Overall Power Assessment

Black Hills' moat is anchored in Cornered Resources (franchise monopolies, physical infrastructure, regulatory relationships), reinforced by Scale Economies and Absolute Switching Costs. This creates a business with very high durability, as infrastructure assets have useful lives of forty or more years, but with returns capped by regulation at approximately 9.5 to 10 percent ROE. The result is not a high-growth disruptor but a compounding machine: predictable earnings growth, predictable dividend growth, predictable capital deployment, year after year, decade after decade.

The comparison to peer utilities is worth drawing out. Xcel Energy, the largest comparable in the region with a market capitalization exceeding forty billion dollars, operates a similar multi-state regulated model but at dramatically greater scale, with a six-gigawatt data center pipeline and aggressive clean energy targets. Otter Tail Corporation offers a fascinating contrast, with its diversified plastics business creating earnings upside (record 2024 EPS of $7.17) but also introducing industrial cyclicality that pure-play utilities avoid. NorthWestern Energy, soon to be merged with Black Hills, has historically traded at a discount to peers due to its concentrated Montana exposure and contentious regulatory environment. MDU Resources has been simplifying through divestitures, moving toward a purer utility model. Avista operates in the Pacific Northwest with hydro-dependent generation and different regulatory dynamics. Each of these peers has strengths, but none replicates Black Hills' particular combination of eight-state regulatory diversification, near-pure-play regulated focus, and a data center growth catalyst that could meaningfully alter the growth trajectory.

XIV. Bull vs. Bear Case

The Bull Case

The case for Black Hills begins with the quality of its cash flows. This is a recession-resistant business providing essential services with captive customers. The 56-year dividend growth streak is not a statistical curiosity; it reflects the underlying stability of a revenue model that functions in economic booms and busts alike. At a roughly 3.8 percent yield with 4-6 percent dividend growth, the total return proposition is attractive for income-oriented investors, particularly if interest rates stabilize or decline.

The energy transition is the single biggest structural tailwind. Every coal plant retirement and renewable replacement, every mile of new transmission to connect wind and solar generation, every grid modernization project adds to the rate base and earns the authorized return. Black Hills' Colorado Clean Energy Plan alone represents hundreds of megawatts of new rate base investment. The $4.7 billion five-year capital plan is the company's largest ever, and the NorthWestern merger will push the combined capital plan above seven billion dollars.

The data center opportunity is potentially transformational. A three-plus gigawatt pipeline serving hyperscalers like Microsoft and Meta in Wyoming could reverse decades of flat electricity demand growth and provide a new earnings growth engine that is largely capital-light under the company's innovative tariff structure. The electricity demand inflection driven by AI, electric vehicles, and reshored manufacturing has the potential to change the growth profile of the entire utility sector.

Management execution has been consistent. Black Hills has delivered on its earnings guidance with remarkable reliability, and the acquisition track record, from Aquila to SourceGas to the NorthWestern merger, demonstrates a core competency in utility M&A that few peers can match. The multi-state regulatory footprint provides diversification that reduces single-jurisdiction risk. At approximately 13 to 14 times forward earnings, the valuation is reasonable for a quality utility with above-average growth prospects, particularly if rate expectations shift.

The Bear Case

Interest rate sensitivity remains the dominant near-term risk. With the ten-year Treasury yielding roughly 4.7 percent, utility dividend yields of 3.4-3.8 percent look less attractive on a relative basis. A "higher for longer" interest rate environment would continue to compress utility multiples and increase the cost of the debt that utilities rely on to fund capital investments. This is not a Black Hills-specific risk but an industry-wide headwind.

Regulatory risk is ever-present. Black Hills has built constructive relationships across eight jurisdictions, but any single adverse rate case outcome, a lower-than-expected ROE, a disallowance of capital investment, a punitive treatment of storm costs, can impair returns for years. The South Dakota electric rate case filed in February 2026, the first in twelve years, is particularly notable: the company is seeking $50.6 million in new annual revenue to recover $523 million in investments. The outcome will be closely watched.

The stranded asset question looms over the Wygen coal complex and Wyodak Mine. While the regulatory framework provides mechanisms for recovering undepreciated coal asset costs through securitization or amortization, accelerated retirement timelines driven by state or federal policy could create write-down risk. The company's gas distribution operations, which serve over 1.1 million customers, face a longer-term existential question: as building electrification accelerates, will gas distribution volumes decline materially?

Merger execution risk is real. Combining two multi-state utilities with different cultures, systems, and regulatory relationships is complex. Integration costs, employee retention challenges, and the distraction of merger proceedings can impair operational performance during the transition period. CEO succession, with Brian Bird taking the helm of the combined company, introduces leadership transition risk during a period of significant change.

Capital intensity creates a perpetual need to access debt and equity markets. Every capital investment, while earning regulated returns, must be financed. Equity issuances dilute existing shareholders. Debt issuances increase leverage and interest expense. In a higher-rate environment, the cost of this capital is meaningfully greater than it was during the zero-rate era that preceded it.

Myth vs. Reality

Myth: Utilities are safe havens that never lose money. Reality: Black Hills' own seventy-percent-plus stock price decline in the early 2000s demonstrates that utilities can suffer catastrophic losses, particularly when they stray from their core regulated model or when macro factors (interest rates, regulatory surprises) turn hostile. The "safety" of utilities is conditional on disciplined management and constructive regulation.

Myth: The energy transition is an existential threat to utilities. Reality: For regulated utilities, the energy transition is primarily an opportunity. Every dollar of mandated clean energy investment enters the rate base and earns the authorized return. The companies most threatened are unregulated merchant generators with stranded fossil fuel assets, not regulated utilities with captive customers and cost recovery mechanisms.

Myth: Data center demand will transform utility growth profiles overnight. Reality: While the three-plus gigawatt pipeline is real and exciting, converting pipeline to connected load takes years, and the innovative tariff structure that makes this growth capital-light for the utility also means the earnings contribution per megawatt may be lower than for traditional rate base investments. The data center opportunity is significant but should be evaluated with realistic timelines and revenue expectations.

Key KPIs to Track

For investors monitoring Black Hills' ongoing performance, three metrics matter most. First, rate base growth: this is the fundamental driver of regulated earnings. The rate at which the combined company's rate base grows, targeted at 5-7 percent annually, directly determines the trajectory of earnings and dividends. Any deceleration in rate base growth signals a potential problem. Second, authorized ROE trends across jurisdictions: the returns that regulators allow drive profitability. If authorized ROEs decline, earnings growth slows even with rate base expansion. The spread between authorized and earned ROE is equally important, as consistent under-earning relative to authorized levels suggests operational inefficiency. Third, data center load materialization: the three-plus gigawatt pipeline is the company's single most differentiated growth catalyst, and converting pipeline commitments into actual connected load and revenue is the critical execution challenge.

XV. Lessons & Takeaways: The Playbook

Black Hills Corporation's 143-year history distills into a set of principles that apply far beyond the utility sector.

Know thyself. The near-death experience of 2000-2004 was the defining crucible of modern Black Hills. The company tried to be something it was not, an energy trader and merchant power operator, and nearly died in the attempt. The recovery was rooted in a painful but honest self-assessment: we are infrastructure operators, and that is enough. This principle has analogs across industries. The companies that struggle most are often those that lose sight of their core identity in pursuit of fashionable strategies. Every great company must answer the question of what it fundamentally is, and the answer must be honest even when it is humbling.

The power of boring. In a financial world obsessed with disruption, hypergrowth, and moonshot bets, Black Hills offers a counter-narrative. Consistent four-to-six-percent earnings growth, compounded over decades, with a growing dividend that has not been cut in over eighty years, creates extraordinary long-term value. An investor who held BKH through its dividend reinvestment program over the past three decades would have compounded wealth at a rate that would surprise most growth-stock advocates. The excitement is in the compounding, not in any single year's performance. As the old Wall Street saying goes, the stock market is a device for transferring money from the impatient to the patient.

Regulatory capitalism is a learnable skill. Making money in highly regulated industries requires a different playbook than competing in free markets. The regulatory relationship is not an obstacle to profitability; it is the mechanism through which profitability is achieved. Earning regulatory trust, filing well-prepared rate cases, maintaining excellent service quality, and investing in the communities you serve are not compliance exercises. They are the strategy.

Geographic diversification reduces fragility. By expanding from a single state to eight, Black Hills insulated itself from the political and regulatory risks inherent in any one jurisdiction. This is the utility equivalent of portfolio diversification, and it has proven its value repeatedly when individual state outcomes have been below expectations.

M&A is a core competency, not a distraction. For Black Hills, acquisitions are not side projects or opportunistic additions. They are the primary engine of growth. The Aquila deal, the SourceGas deal, and now the NorthWestern merger represent a quarter-century of disciplined, compounding acquisition strategy. Each deal built on the capabilities and lessons of the prior one.

Infrastructure investments compound over decades. The transmission lines, gas pipelines, and distribution networks that Black Hills built and acquired generate returns for their useful lives of forty years or more. The Ready Wyoming project completed in December 2025 will be earning returns well into the 2060s. This is patient capital in its purest form.

Stakeholder balance is the real game. Regulated utilities must satisfy four constituencies simultaneously: customers who want low bills and reliable service, regulators who want prudent investment and fair pricing, communities who want economic development and environmental stewardship, and shareholders who want earnings growth and dividends. Getting this balance wrong in any dimension creates problems that cascade through the others. Black Hills' track record of constructive outcomes reflects skill in managing all four stakeholder groups simultaneously.

Crisis creates clarity. The near-death experience of the early 2000s was traumatic, but it forged a company that knew exactly what it was and what it was not. The strategic discipline that emerged from that crisis, the absolute commitment to regulated operations and the refusal to chase non-regulated risk, has been the foundation of two decades of steady performance. Sometimes the best thing that can happen to a company is a brush with mortality.

Moats in the physical world are different from digital moats. In the technology sector, moats are built from network effects, switching costs, and data advantages, all of which can erode quickly when a superior product arrives. In the infrastructure world, moats are literally made of copper, steel, and concrete buried underground and strung overhead. These physical moats degrade slowly, earn returns for decades, and cannot be disrupted by a startup in a garage. Black Hills' competitive position rests on assets that took 143 years to build and that no rational competitor would attempt to replicate.

XVI. Epilogue: The Next Chapter

As of February 2026, Black Hills Corporation stands at the threshold of its most ambitious transformation. The regulatory calendar is dense: the company filed its first South Dakota electric rate review in twelve years on February 19, 2026, seeking $50.6 million in new annual revenue to recover approximately $523 million in grid investments since 2014. An Arkansas gas rate review filed in December 2025 seeks $29.4 million in additional annual revenue. Nebraska approved $23.9 million in new gas rates effective January 2026. Each of these proceedings will test the regulatory relationships that have been cultivated over decades and will signal whether the constructive environment that Black Hills has enjoyed remains intact.

The NorthWestern Energy merger, if approved, will create the largest regulated utility in the Northern Great Plains, a combined entity with the scale, balance sheet, and geographic reach to capitalize on what may be the most significant demand growth opportunity the utility industry has seen in decades.