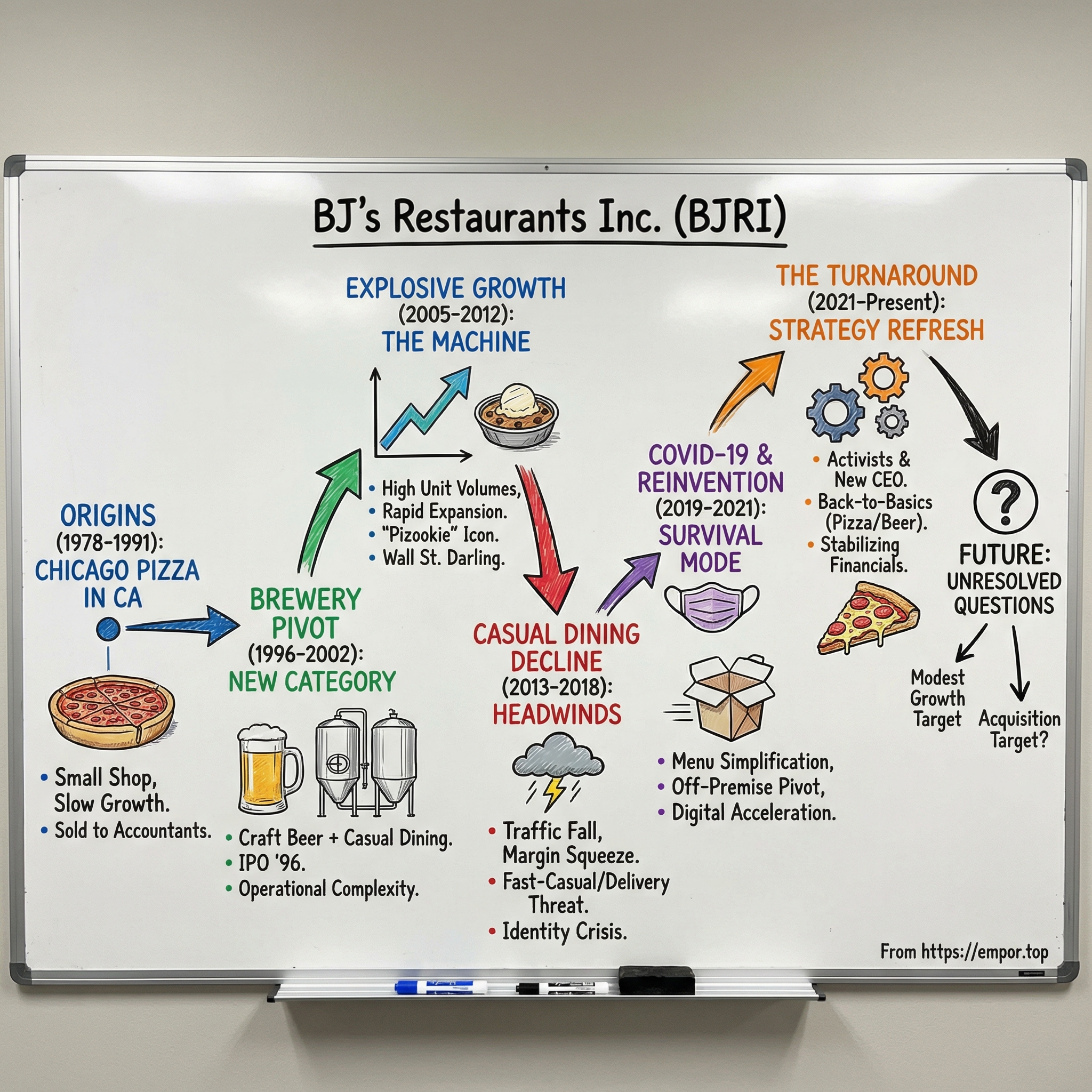

BJ's Restaurants Inc.: The Story of Southern California's Brewery-Restaurant Pioneer

I. Introduction and Episode Roadmap

Picture this: a 10,000-square-foot restaurant in a suburban strip mall somewhere between Dallas and Denver. Families stream in on a Friday night. Kids are reaching for the dessert menu before they even sit down, parents are scanning a beer list that would make a Portland taproom jealous, and a server is carrying a deep-dish pizza that could have been pulled from a South Side Chicago kitchen. This is BJ's Restaurant and Brewhouse, and it is one of the more peculiar success stories in American dining.

Today, BJ's Restaurants operates more than 200 locations across 31 states, generating roughly $1.4 billion in annual revenue. It is a publicly traded company on the NASDAQ under the ticker BJRI, with a market capitalization that has oscillated wildly over the past decade, reflecting both the promise and the peril of its position in the American restaurant landscape.

The concept is a hybrid that, on paper, probably should not work: authentic Chicago-style deep-dish pizza (recently reimagined in a Detroit-style format), a menu with more than 100 items spanning burgers and tacos and salads and slow-roasted entrees, and a brewing operation that produces award-winning craft beer across multiple states. It is casual dining meets craft brewery meets something that defies easy categorization.

The question that makes this story worth telling is not just how a pizza joint in Orange County became a billion-dollar enterprise. It is how two accountants who bought a small chain from its original founders managed to create an entirely new category in American restaurants, rode the resulting wave to extraordinary growth, nearly drowned when the casual dining industry entered secular decline, survived a global pandemic that should have killed the concept, and are now attempting yet another reinvention under new leadership and activist investor pressure.

This is a story about category creation, about the treacherous economics of scaling restaurants, and about what happens when the industry you helped build starts dying underneath you. It is about whether operational excellence alone can sustain a business in a structurally challenged market.

It touches on themes that matter far beyond the restaurant industry: the difference between a genuine competitive advantage and a nice concept, the tension between growth and sustainability, and the brutal reality that even well-run companies can be trapped by the economics of their industry.

The cast of characters is rich: founders who sold their chain to their own accountants, a CFO who became CEO and then was fired, activist investors who demanded change and got it, the legendary founder of Panera Bread investing $70 million and lending his playbook, and a new CEO from Buffalo Wild Wings betting that the answer lies in rediscovering BJ's original DNA.

Over the next several sections, we will trace BJ's from its origins in late-1970s Southern California, through the pivotal decision to add brewing operations, the explosive growth that followed, the near-death experience of COVID-19, and the turnaround attempt currently underway. Along the way, we will dig into unit economics, competitive positioning, and the strategic frameworks that explain why this company occupies such an unusual spot in the market. Buckle up.

II. Founding Story and The Original Concept (1978-1991)

In 1978, two men named Jim Kozen and Leonard Allenstein opened a restaurant in Santa Ana, California, with an idea that was both simple and slightly contrarian: bring authentic Chicago-style deep-dish pizza to Southern California. The restaurant they opened was originally called BJ Grunts, a name that lasted about as long as it took for lawyers representing RJ Grunts, a well-known Chicago hamburger joint, to send a cease-and-desist letter. The name changed to BJ's Chicago Pizzeria, and the concept took root.

To understand why this mattered, you need to understand Orange County in the late 1970s. Southern California was in the middle of a suburban explosion. New housing tracts were spreading across former farmland. Malls were being built at a feverish pace. The family dining market was wide open, dominated by chains like Sizzler, Denny's, and early iterations of what would become the casual dining boom. But nobody was doing Chicago deep-dish pizza. In a region obsessed with thin-crust, wood-fired, or even the emerging California-cuisine style of pizza, deep-dish was an exotic import. It was comfort food with a regional identity, and it gave BJ's an immediate hook.

Shortly after the first restaurant opened, two men named Mike Phillips and Bill Cunningham bought a 50 percent stake in the company for the princely sum of $14,000. That number tells you everything about the scale of the operation in those early years. This was not a venture-backed startup with grand ambitions. It was a small pizza restaurant that happened to make good deep-dish pies. Fourteen thousand dollars for half of what would become a billion-dollar company. The most important decisions in business often happen at scales so small they are almost invisible.

Kozen and Allenstein eventually departed after the seventh store opened, leaving Phillips and Cunningham to run the show. Growth through the 1980s was slow, steady, and entirely bootstrapped. No private equity. No franchise model. Just one restaurant at a time, reinvesting profits into the next location. This was the era of Reagan-era suburban expansion, of shopping malls as community centers, of families who went out for dinner on Friday night as a weekly ritual. BJ's found its niche in that ritual, a place where you could bring the family for a deep-dish pizza that felt a little more special than the Domino's down the street but did not require a babysitter or a sport coat.

The menu began to expand beyond pizza through the late 1980s, adding salads, pastas, and sandwiches, a gradual evolution from "Chicago pizza specialty shop" toward something that looked more like casual dining. This was not accidental. Phillips and Cunningham could see that the pure pizza concept, while beloved, had a ceiling. The average check was limited. The occasions were limited. Families might come for pizza night, but they were not coming for a birthday dinner or an anniversary. Broadening the menu broadened the appeal and, critically, broadened the revenue potential per visit.

Then, in 1991, something happened that would ultimately reshape the company's trajectory: Phillips and Cunningham sold the business to their accountants. Paul Motenko and Jerry Hennessy had been handling the books for the chain and saw an opportunity that the original operators perhaps did not fully appreciate. They took over a company with roughly ten locations, profitable but unremarkable, a small regional chain in a market full of small regional chains.

What Motenko and Hennessy brought was not restaurant operating experience but financial acumen and strategic ambition. They had spent years watching the numbers, understanding the unit economics, seeing the margins and the customer patterns. They understood that BJ's had something valuable: a differentiated product, Chicago-style deep-dish pizza, with genuine customer loyalty in a growing market. What it lacked was a growth engine, something that would transform it from a nice local chain into a scalable concept. They looked at BJ's not just as a collection of pizza restaurants but as a platform, a brand with a clear identity and loyal customers that could be built into something much larger. The question was how. For the next five years, they would search for the answer, experimenting with menu expansion and operational improvements while laying the groundwork for a decision that would change everything.

That decision involved beer.

III. The Brewery Pivot: Creating a New Category (1996-2002)

In 1996, something remarkable happened in Brea, California, a suburban city in northern Orange County known mostly for its shopping mall and proximity to Disneyland. BJ's Chicago Pizzeria opened a microbrewery inside one of its restaurants, and in doing so, stumbled into an entirely new category of American dining.

To appreciate why this was radical, you need to understand the state of craft beer in America in the mid-1990s. The craft beer revolution was in its infancy. The Brewers Association would later track the explosive growth of small, independent breweries across the country, but in 1996, craft beer was still a niche pursuit. Brewpubs existed, certainly, but they were almost universally small, independent, beer-geek destinations. The idea of a full-service casual dining restaurant with a menu of more than fifty items also operating a professional brewing facility was essentially unheard of. Chains did not brew. Brewers did not operate chains. The two worlds were separate.

Motenko and Hennessy saw the gap. Their insight was that the craft beer consumer and the casual dining consumer were, in many cases, the same person. A family dad who cared about what beer he was drinking also wanted to take his kids somewhere with a broad menu and a welcoming atmosphere. A couple on a date night might choose a restaurant specifically because it had interesting, house-brewed beer they could not get anywhere else. The brewery was not just a gimmick; it was a genuine differentiator in a market where casual dining chains were increasingly commoditized.

The same year, the company went public. Under a newly formed holding company called Chicago Pizza and Brewery Inc., they sold 1.8 million shares at five dollars apiece, raising approximately $9.4 million. The stock traded on NASDAQ under the symbol CHGO. The capital raised was earmarked for renovation, debt reduction, and expansion, including the brewery infrastructure that would define the company's future.

Also in 1996, the company made an aggressive acquisition play, purchasing 26 Pietro's Pizza restaurants for $2.8 million in cash and assumed debt. They sold off seven locations and converted the remaining units to the BJ's format. This was the first sign of the growth ambitions that Motenko and Hennessy harbored, and the first real test of whether the concept could be replicated beyond its original Orange County base.

The early beer program produced beers that would become signatures of the brand: Piranha Pale Ale, with its bright hop bite, Tatonka Stout, a roasty, chocolatey dark beer, and a rotating lineup that established BJ's as a genuine player in the craft beer world, not just a restaurant that happened to sell house beer. The Brea brewery was large enough to supply surrounding restaurants, creating a hub-and-spoke model that solved one of the fundamental challenges of the brewery-restaurant concept: you cannot put a brewery in every location, but you can centralize production and distribute to nearby units.

The operational complexity was staggering, and it is worth dwelling on because it explains both BJ's differentiation and its vulnerability. Running a restaurant is hard enough: managing perishable inventory, coordinating a kitchen during peak hours, training servers, maintaining health and safety standards, all while keeping costs below the thin margins that the industry demands. Running a brewery requires an entirely different set of skills: understanding fermentation science, managing temperature-sensitive processes that take weeks rather than minutes, maintaining specialized stainless steel equipment, sourcing hops and malts from agricultural suppliers with different cycles than food commodities, and navigating a regulatory landscape that involves federal, state, and local alcohol licensing.

Running both simultaneously, while maintaining consistency across a growing number of locations, was something that had essentially never been done at scale. Think of it as trying to run a manufacturing facility and a service business under the same roof, with the same management team, using different supply chains, different quality control processes, and different skill sets. The company was, in effect, building two businesses inside one set of walls. Every competitor who looked at BJ's model and considered replicating it would have to grapple with this same complexity, and most decided it was not worth the effort. That reluctance, more than any patent or trade secret, was BJ's real competitive advantage during the early years.

By the early 2000s, the concept had crystallized into what BJ's would become: a large-format restaurant, typically 7,000 to 10,000 square feet, with a full menu that offered something for everyone, anchored by deep-dish pizza and craft beer. The name evolved from BJ's Chicago Pizzeria to BJ's Restaurant and Brewery, and eventually to BJ's Restaurant and Brewhouse, each iteration reflecting the broadening of the concept beyond its pizza roots.

By 2002, the company operated roughly 30 locations, had clear differentiation from every major competitor in the casual dining space, and was building momentum. In August 2004, the company formally changed its name from Chicago Pizza and Brewery Inc. to BJ's Restaurants Inc., and the stock ticker migrated from CHGO to BJRI. The stage was set for what would become one of the great growth stories in American casual dining.

There is a myth in the restaurant industry that concepts need to be simple to scale. The McDonald's playbook: limited menu, standardized processes, minimum skill required at the unit level. BJ's was betting on the opposite approach: more complexity, more specialization, more capital intensity, but with a differentiated customer experience that justified the investment. It was a high-risk bet, and the early returns suggested it was working. The restaurants with brewing operations consistently outperformed those without, drawing a different customer demographic, one that was slightly more affluent, slightly more food-savvy, and significantly more likely to linger over a second or third beer.

The real question, of course, was whether a concept built on the marriage of craft beer and casual dining could scale far beyond its Southern California home turf. The next decade would provide a definitive answer.

IV. The Growth Machine: Going Public and Explosive Expansion (2005-2012)

There is a particular kind of story that Wall Street loves: a restaurant concept with high unit-level economics, a clear growth runway, and a differentiated position in a large market. In the mid-2000s, BJ's Restaurants was exactly that story. And like all great growth stories, it began with a single number that changed everything.

By the start of fiscal 2005, BJ's was generating approximately $178 million in annual revenue from around 40 locations. Think about what that implies: roughly $4.5 million per restaurant, significantly above the casual dining industry average at the time. The stock, now trading under the BJRI ticker, was attracting attention from growth-oriented investors who saw what the company saw: a concept that worked in California and had barely begun to penetrate the rest of the country. The unit economics were compelling. Individual restaurants were averaging strong sales volumes, well above the casual dining industry average, driven by the combination of a broad menu, the craft beer differentiator, and larger-format locations that could accommodate high traffic.

The expansion strategy was methodical. Rather than scattering restaurants across the country in a land-grab approach, BJ's clustered new locations in target markets, building density before moving on. This is a lesson that the best restaurant operators learn early: clustering creates marketing efficiency, supply chain efficiency, and management efficiency. Three restaurants in Houston are more profitable than one each in Houston, Atlanta, and Boston.

California was the base, and the company built outward from there: Texas, which became the second-largest market, then the Pacific Northwest, Arizona, Colorado, and eventually pushing east into Florida and the Mid-Atlantic. Each new market was carefully chosen based on demographics, real estate availability, and the presence of the suburban, middle-to-upper-middle-class consumers who made up BJ's core audience.

The real estate playbook was precise. BJ's targeted spaces of 7,000 to 10,000 square feet in highly visible locations, typically near major retail centers or in suburban corridors with heavy traffic. These were not strip-mall afterthoughts; they were prominent, purpose-built locations designed to draw attention and accommodate high volumes. The build-out costs were significant, running several million dollars per unit, particularly for locations with brewing equipment. But the revenue potential justified the investment.

During this era, a particular menu item ascended from afterthought to icon: the Pizookie. Short for "pizza cookie," the Pizookie is BJ's trademarked dessert, a deep-dish cookie baked in a small pizza pan and served warm with ice cream on top. It sounds simple because it is simple. It is also, arguably, the single most important menu item in the company's history.

How did it happen? The Pizookie was not the product of a consulting firm or a focus group. It emerged organically from the kitchen, a riff on the idea that if you bake a cookie in the same kind of pan you use for deep-dish pizza, you get something warm, gooey, and enormous, and when you put a scoop of vanilla ice cream on top, you get something that makes people involuntarily reach for their phone to take a photo. It sounds trivial, but the Pizookie became the thing people talked about, the thing they posted on social media, the thing that turned a meal at BJ's from a dining occasion into an experience with its own moment.

Outside California, the Pizookie became the bestselling item on the entire menu. Inside California, it was second only to the pizza itself. Every restaurant chain in America searches for a signature item, the thing that defines the brand in the consumer's mind: Olive Garden has its breadsticks, Outback has its Bloomin' Onion, Chili's has its baby back ribs. For BJ's, the Pizookie filled that role, and it did so with a simplicity and emotional resonance that no amount of marketing spend could have manufactured. For a company working to differentiate in a crowded market, the Pizookie was an accidental masterstroke of brand building.

The revenue trajectory during this period was extraordinary. From $178 million in fiscal 2005, the company grew to $239 million in 2006, then $316 million, $374 million, $427 million, $514 million. By fiscal 2012, revenues had surpassed $700 million. The company was growing at better than 20 percent annually, a rate that made it one of the fastest-growing restaurant chains in America. The National Retail Federation recognized it as one of the ten fastest-growing restaurants in the country based on year-over-year sales between 2010 and 2011.

Greg Levin joined the company in September 2005 as Chief Financial Officer, having come from SB Restaurant Co., the parent company of the Elephant Bar polished-casual chain. Levin would become one of the most important executives in BJ's history, bringing financial discipline and operational rigor to a company that was growing fast enough to lose both.

The challenge of scaling a restaurant chain at this pace is underappreciated by people outside the industry. Each new restaurant requires hiring and training approximately 100 to 150 employees. Each kitchen needs to execute a menu with more than 100 items at consistent quality. Each bar needs trained staff who can speak knowledgeably about a craft beer lineup. Each manager needs to understand not just restaurant operations but the unique requirements of the brewhouse concept. Doing this once is challenging. Doing it 15 to 20 times per year, across multiple states, with different labor markets, different real estate dynamics, and different consumer preferences, is a feat of organizational capability.

Under the professional management team that coalesced during this period, the company standardized its operations, built sophisticated training programs, and developed the systems needed to maintain consistency across a rapidly expanding footprint. Greg Trojan, who had joined the board in 2005 and became CEO in 2013, was instrumental in professionalizing the organization. The management bench that BJ's built during the growth years, from district managers to corporate operations leaders, became one of the company's most valuable assets.

The stock reflected the optimism. Investors who bought in during the mid-2000s saw multi-bagger returns as the company executed quarter after quarter. The narrative was irresistible: a differentiated concept in a massive market with a long growth runway. Unit count grew from roughly 55 at the end of fiscal 2006 to 82 by 2008, and the pace only accelerated from there. By 2012, the chain operated more than 135 locations, and the company had proven that the concept worked well beyond Southern California. Texas, which would become the second-largest market, was particularly successful: the combination of suburban growth, family-oriented dining culture, and a customer base that embraced both craft beer and hearty food made it a natural fit.

The financial profile during this era was a Wall Street dream. Revenue compounded at better than 20 percent annually for seven consecutive years. Same-store sales, the metric that separates genuine demand growth from mere unit proliferation, were consistently positive. Restaurant-level margins held up even as the company expanded into new markets, suggesting that the concept's economics were robust, not just a California phenomenon. The company was not just opening restaurants; it was opening profitable restaurants in new geographies, which is the holy grail of restaurant chain expansion.

But here is the thing about growth stories in the restaurant industry: the growth eventually has to slow.

The easy markets get filled first. Every new market after that is incrementally harder: less favorable demographics, less brand recognition, higher customer acquisition costs. The real estate gets more expensive as the company competes for premium locations with larger, better-capitalized chains. New management layers are required to oversee a national footprint, adding corporate overhead that did not exist when the chain was concentrated in Southern California. District managers, regional vice presidents, training centers, supply chain logistics across multiple time zones: the bureaucratic infrastructure of scale is expensive and sometimes stifling.

And the competitive landscape does not stand still. While BJ's was busy replicating its concept across the Sunbelt and beyond, the very definition of dining out in America was beginning to change. As BJ's crossed 140 locations and pushed toward 200, the industry beneath it was beginning to shift in ways that would challenge the very foundation of the casual dining model. The seeds of the next chapter, the painful one, were already being planted during the glory years.

V. The Perfect Storm: Casual Dining's Decline (2013-2018)

If you wanted to pick the worst possible industry to be in during the mid-2010s, American casual dining would be a strong contender. The segment that had dominated American restaurant culture for three decades, the Applebee's and Chili's and TGI Friday's and Olive Gardens that lined every suburban corridor in the country, was entering a period of secular decline that would close thousands of locations and destroy billions in shareholder value. It was the kind of slow-motion industry collapse that is painful to watch and even more painful to live through.

The forces were multiple and compounding. Start with demographics. Millennials, who were aging into their peak dining years, showed remarkably little interest in the casual dining format. Surveys consistently found that younger consumers preferred fast-casual concepts like Chipotle and Panera, which offered higher-quality food at lower price points with faster service. They did not want to wait 15 minutes for a table, then 20 minutes for food, then flag down a server for the check. They wanted to order at a counter, get their food in five minutes, and eat on their own schedule. The entire service model that casual dining was built on, the sit-down, be-waited-upon, tip-your-server model, was losing relevance with the generation that was supposed to be its future customer base.

Then add technology. Delivery platforms like DoorDash, Uber Eats, and Grubhub did not just create a new distribution channel for restaurants; they fundamentally changed the competitive landscape. Suddenly, every restaurant in a five-mile radius was competing for the same customer, not based on location or atmosphere but on food quality, price, and the photograph in the app. A BJ's that used to benefit from being the best option in a particular strip mall was now competing against 200 restaurants in the delivery radius. The geographic moat that location had always provided in the restaurant business was dissolving.

The traffic crisis that resulted was brutal. Applebee's would close hundreds of locations over the next several years. TGI Friday's went from a dominant chain to an afterthought. Ruby Tuesday filed for bankruptcy. Red Robin, Bob Evans, Perkins, and a host of regional chains either contracted, restructured, or disappeared entirely. The entire casual dining segment saw year after year of declining guest counts, a structural shift that no amount of menu innovation or promotional activity seemed able to reverse.

BJ's was not immune. Despite its brewery differentiation and broader appeal, the company was caught in the same undertow. Revenue continued to grow as new restaurants opened, reaching $845 million in fiscal 2014 and $920 million in 2015, crossing the billion-dollar threshold in fiscal 2017. But same-store sales, the metric that truly matters in restaurants because it strips out the effect of new unit openings and reveals whether the existing business is growing or shrinking, turned troublesome.

In 2016, comparable-unit sales dropped 1.3 percent. Management blamed the rancorous presidential election campaign for contributing to consumer negativity, a refrain heard across the restaurant industry that year, but the problems were deeper than politics. In 2017, the same-store sales figure took another hit, declining 0.7 percent. Unit growth, which had been the engine of the company's Wall Street appeal, slowed dramatically as management pulled back on new openings to focus on fixing the existing base.

The stock, which had been as high as the low $60s during the peak growth years, cratered. Investors who had bought the growth story now faced a company with decelerating traffic, rising costs, and an unclear path to reigniting momentum. Food commodity prices spiked. Labor costs surged as minimum wages rose across BJ's key markets, particularly California. The margin compression was painful: restaurants that had been generating strong operating margins saw those margins squeezed from multiple directions simultaneously.

The cost squeeze was relentless. California, BJ's largest market, led the nation in minimum wage increases, pushing labor costs higher each year. Food commodity prices, particularly proteins and dairy, were volatile. And the company's large-format restaurants, which had been an advantage during the growth era because they could accommodate high volumes, now represented a fixed-cost burden when those volumes declined. A 10,000-square-foot restaurant costs roughly the same to heat, light, and maintain whether it serves 300 guests a night or 250.

Meanwhile, the competitive landscape was evolving in ways that directly threatened BJ's positioning. Fast-casual pizza concepts like Blaze Pizza and MOD Pizza offered customized, high-quality pizzas at a fraction of BJ's price point with no wait time. Craft breweries, which had exploded in number across the country, now offered food menus that competed directly with BJ's beer-and-food proposition. The very category BJ's had helped create was being unbundled: you could get great craft beer at the local taproom, great pizza at the fast-casual pizza spot, and great burgers at Five Guys, and all of it would cost less time and money than a sit-down meal at BJ's. The delivery platforms made it possible for consumers to order from virtually any restaurant, eliminating the geographic advantage that a well-positioned BJ's location once enjoyed.

Then came a sharp reversal that briefly rekindled the optimism of the growth years. In 2018, BJ's posted a remarkable recovery. For the first nine months of the fiscal year, comparable-store sales rose 5.5 percent over the prior year. In the third quarter alone, comps surged 6.9 percent, the strongest growth in 29 quarters, nearly seven and a half years. The stock rallied to an all-time closing high of $74.38 in August 2018, briefly making the company worth more than it had ever been. Management pointed to menu innovation, operational improvements, and technology investments as the drivers.

Was this a genuine turnaround or a dead-cat bounce? The optimists argued that BJ's had differentiated itself from the worst of the casual dining decline through its brewery concept and menu quality, and that the 2016-2017 downturn was a temporary correction, not a structural shift. The pessimists noted that one strong year in a declining industry does not make a trend, and that the fundamental forces pushing consumers away from casual dining had not changed.

The recovery masked a deeper strategic question that the company had not resolved. Was BJ's a growth concept or a mature cash cow? The unit count had reached approximately 200, and the rate of new openings had slowed to a handful per year. The easy expansion markets had been filled. The remaining whitespace required either entering less-proven geographies or accepting that the footprint was largely built out. For a company whose stock price had been built on the growth story, this was an existential question.

Activist investors began circling during this period. Shareholders who believed the company was not maximizing value pushed for strategic alternatives, from operational improvements to an outright sale. The tension between the board and certain shareholders reflected a deeper strategic disagreement: was BJ's a growth company that needed to invest its way back to momentum, or was it a mature business that should be managed for cash flow and shareholder returns? The answer was not obvious, and the disagreement would persist for years, ultimately culminating in the dramatic boardroom changes that would reshape the company's leadership in 2024.

Cost-cutting initiatives were launched, targeting labor optimization through scheduling technology, supply chain efficiencies through renegotiated vendor contracts, and menu engineering to shift the sales mix toward higher-margin items. These efforts were necessary and produced real results, but they were also, in a sense, rearranging deck chairs. The fundamental challenge was not that BJ's was poorly managed. It was that the industry in which BJ's operated was entering a period of structural decline, and no amount of operational optimization could change that macro reality.

By late 2018, the company stood at a crossroads. Roughly 200 locations. Revenue above a billion dollars. A stock that had recovered to the $40s but remained well below its peak. And a management team that was running hard just to stay in place. Then something arrived that nobody anticipated, something that would push BJ's and every restaurant in America to the brink.

VI. COVID-19: Near-Death and Forced Reinvention (2019-2021)

In early 2020, BJ's Restaurants was a company already wrestling with pre-existing conditions. Traffic trends in casual dining remained weak. The competitive environment was intensifying. Management was working through the strategic questions that had defined the previous several years. And then, in March 2020, the world stopped.

The speed of the collapse was breathtaking. On March 15, 2020, California Governor Gavin Newsom ordered all bars and nightclubs to close and asked restaurants to operate at half capacity. Within days, most states followed with even stricter orders: dining rooms shut entirely, no indoor seating, no exceptions. BJ's went from a business built almost entirely on in-restaurant dining, a business where the experience of sitting down with friends and family over craft beer and Pizookies was the entire value proposition, to a business with essentially no revenue model.

The operational response was immediate and brutal. The company furloughed approximately 16,000 employees, the vast majority of its workforce. It slashed 45 percent of its menu overnight, keeping only the items that could be prepared efficiently with skeleton crews and that traveled well in to-go containers. It drew down credit facilities to ensure liquidity. And it began the grim work of calling landlords, 200-plus of them, to negotiate rent relief on leases that required millions in monthly payments whether or not a single customer walked through the door.

For a brief period, the question was not about growth or strategy or competitive positioning. The question was simpler and more primal: would BJ's Restaurants survive to see 2021?

The stock tells the story in its own stark language. BJ's shares, which had been trading in the $30s and $40s before the pandemic, plummeted. By late March 2020, the stock had fallen roughly 65 percent from its 52-week highs. The market was pricing in a very real possibility that a significant portion of the casual dining industry might not survive. And unlike fast-casual or quick-service restaurants, which could relatively easily pivot to takeout and drive-through, casual dining chains like BJ's were structurally disadvantaged: large dining rooms designed for the sit-down experience, complex menus that required large kitchen staffs, and a value proposition that depended heavily on the ambiance and service that only dine-in could provide.

But something interesting happened during the scramble to survive. BJ's discovered that its food actually traveled well. The deep-dish pizza, the burgers, the slow-roasted proteins, and most importantly, the Pizookies, all held up remarkably well in to-go containers and delivery bags. Pre-pandemic, off-premise sales had been a minor part of the business, roughly $10,000 per week per restaurant. During the initial phase of the shutdown, from mid-March to mid-May 2020, off-premise sales tripled to approximately $30,000 per week. The company rapidly built out online ordering capabilities, curbside pickup systems, and delivery partnerships with third-party platforms.

The menu rationalization that was forced by the crisis turned out to be a blessing, and it illustrates a paradox that applies far beyond the restaurant industry: organizations rarely make their best decisions in comfortable times.

Cutting 45 percent of the menu items eliminated enormous operational complexity. Prep times shortened because cooks were preparing fewer items and could focus on doing them well. Food waste decreased because fewer unique ingredients meant tighter inventory management and fewer items expiring on shelves. Kitchen throughput improved because simplified ticket lines moved faster. The reduced menu allowed kitchens to operate with fewer staff without a proportional decline in output or quality. It was the kind of efficiency gain that consultants had probably recommended for years but that no management team would have implemented voluntarily, because every menu item has a constituency, every removed dish generates customer complaints, and every simplification feels like an admission of failure rather than an act of discipline.

The brewery infrastructure, which had been a point of pride and differentiation, initially looked like a stranded asset. Millions of dollars in stainless steel tanks, fermentation equipment, and distribution systems were sitting idle or underutilized in closed or capacity-restricted restaurants. But necessity bred creativity. The company pivoted to packaged beer sales, offering six-packs and growlers for take-out and delivery. The beer club concept, where members paid $30 for access to limited-edition beers and assorted freebies, was expanded and proved to be a meaningful revenue supplement. These were not transformative revenue streams, but they demonstrated the versatility of the brewing asset and kept the brand's beer identity alive during a period when many restaurants were reduced to commodity food delivery.

Even as dining rooms reopened through the latter half of 2020 and into 2021, the off-premise business held. BJ's maintained roughly 80 percent of its pandemic-era off-premise growth even with open dining rooms, meaning the off-premise channel more than doubled compared to pre-COVID levels. More than 80 percent of off-premise orders came through digital channels, mobile and web, giving the company a customer data pipeline it had never possessed before. This was a revelation. For decades, BJ's had no way to reach customers between visits, no email addresses, no purchase histories, no personalization capabilities. The pandemic's forced digital adoption changed that virtually overnight.

Revenue for fiscal 2020 collapsed to $778.5 million, down from $1.16 billion in 2019, a 33 percent decline that was consistent with the casual dining sector but devastating in absolute terms. The company survived through a combination of government assistance programs, particularly the Paycheck Protection Program and the Employee Retention Tax Credit, aggressive landlord negotiations that yielded rent concessions, credit facility draws that provided essential liquidity, and the surprisingly robust off-premise business. The capital markets, which had briefly written off the casual dining sector, began to price in recovery as vaccination programs rolled out.

The experience forced a set of realizations that would shape the company's post-pandemic strategy. First, off-premise was not a temporary accommodation but a permanent and significant revenue channel. The pre-pandemic off-premise mix of roughly $10,000 per week per restaurant had more than doubled, and even with dining rooms fully reopened, the elevated off-premise demand persisted. Consumers had learned that BJ's food traveled well, that Pizookies were just as satisfying at home, and that the convenience of digital ordering was worth the trade-off of not dining in.

Second, the menu had been bloated and the crisis-driven rationalization had actually improved operations. Cutting 45 percent of the menu had reduced food waste, simplified prep, shortened ticket times, and allowed kitchens to operate with fewer staff. The question post-pandemic was not whether to restore the old menu but how much of the reduction to preserve.

Third, the digital infrastructure that the company had built under duress was an asset that could drive efficiency and customer engagement going forward. For the first time, BJ's had direct digital relationships with a significant portion of its customer base, data that could inform marketing, menu development, and operational decisions.

Fourth, and perhaps most importantly, BJ's had learned that it could operate effectively with a leaner cost structure. The pre-pandemic model, with its high labor levels and operational complexity, had been carrying weight that the crisis stripped away. Labor allocation shifted permanently: tasks that had been manual were automated, staffing levels were optimized through better scheduling technology, and roles were restructured to reflect the elevated off-premise business.

The balance sheet bore the scars. Debt levels increased as the company borrowed to survive. But by the time vaccination rates climbed and consumers flooded back to restaurants in 2021, BJ's was not just surviving but positioning itself for recovery. The question was whether the company could translate the hard-won lessons of the pandemic into a sustainable competitive advantage, or whether they would simply revert to the pre-COVID normal that had been slowly eroding the business for years.

VII. The Turnaround Attempt: Strategy Refresh (2021-Present)

The post-pandemic era at BJ's has been defined by a word that management teams love and investors greet with skepticism: transformation. But unlike many corporate transformations that amount to PowerPoint slides and press releases, the changes at BJ's have involved real shifts in leadership, strategy, and operations, accompanied by a degree of boardroom drama that makes this chapter of the story particularly compelling.

Greg Trojan, who had served as CEO since 2013 and guided the company through the pandemic crisis, retired on September 1, 2021. The title passed to Greg Levin, who had spent 16 years at BJ's in various executive roles, most recently as President and CFO. Levin had been present for the entire growth era and the subsequent challenges. He knew the operation intimately. The transition was framed as continuity with evolution: same company DNA, but a mandate to modernize.

Under Levin, the company embraced a hybrid operating model that reflected the pandemic lessons. Dining rooms remained the core of the business, but off-premise was built into the operating rhythm permanently. Purpose-built pickup areas were added to restaurants. Delivery partnerships were refined. The loyalty program, BJ's Premier Rewards, was expanded and positioned as a customer data and retention tool. Technology integration accelerated, with investments in point-of-sale systems, kitchen display technology, and digital ordering infrastructure.

The menu strategy evolved significantly. The pandemic-era simplification was not fully reversed. Instead, management took a more disciplined approach, focusing on limited-time offers and seasonal items that could drive traffic without permanently expanding the menu's complexity. The company also experimented with new revenue streams, including the Slo Roast virtual brand, a delivery-only concept built on DoorDash that leveraged BJ's existing kitchen capacity and slow-roasted protein expertise without requiring any new physical infrastructure.

Same-store sales recovered strongly as consumers returned to restaurants. Revenue climbed back to $1.09 billion in fiscal 2021, then $1.28 billion in 2022, and $1.33 billion in 2023. But the recovery was not without challenges. Inflation hit restaurant operators hard, driving up food costs and making it more expensive to staff kitchens and dining rooms. Labor shortages, a persistent post-pandemic issue, forced changes to operating models and pushed wages higher. And consumer spending began to soften as the economic stimulus faded and interest rates climbed.

Then came the activist investors, and this is where the BJ's story takes its most dramatic turn since the brewery pivot nearly three decades earlier.

In February 2024, BJ's entered into a cooperation agreement with Fund 1 Investments, which had accumulated an 11 percent stake in the company. Eleven percent is a massive position in a company of BJ's size, enough to influence board elections and force strategic conversations that management might prefer to avoid. The agreement resulted in the appointment of C. Bradford Richmond to the board. Richmond was not a passive board member; he was a former Darden Restaurants CFO with decades of experience at Olive Garden and Red Lobster, two of the most successful casual dining brands in America. His appointment brought genuine operational expertise to a board that the activists believed had become too comfortable with the status quo. A Shareholder Value Initiatives Committee was formed to review operations and strategy, a polite corporate governance term for what amounted to a comprehensive audit of everything management was doing and whether they should be doing it differently.

A month later, in March 2024, a second cooperation agreement was struck with PW Partners, which held more than five percent of the company's shares. PW Partners took a particularly aggressive approach, securing access to restaurants, records, and documents to conduct their own independent assessment of BJ's cost structure. They wanted to see everything: how the kitchens were staffed, how food was sourced, how marketing dollars were spent, where the inefficiencies lurked. This level of transparency is unusual in a cooperation agreement and reflected the depth of investor frustration with the company's pace of improvement.

The message from shareholders was unmistakable: the current trajectory was not acceptable.

On August 28, 2024, Greg Levin was terminated without cause. The 8-K filing revealed that the departure was a termination per Levin's employment agreement and was "not related to any disagreement between Levin and BJ's." But the subtext was clear: after 19 years with the company, including nearly three years as CEO, Levin had not delivered the consistent sales and profit momentum that the board, now significantly influenced by activist shareholders, demanded. During his tenure, BJ's had grown from about 45 restaurants to more than 200 and from roughly $140 million to $1.4 billion in annual revenue, but the most recent chapters of that story had been written in invisible ink: growth that barely exceeded inflation, traffic trends that remained stubbornly flat, and a stock price that had gone essentially nowhere.

Richmond, the former Darden executive who had joined the board just six months earlier, was named interim CEO. It was a dramatic shift that signaled the board's willingness to break with the past and the activist investors' growing influence over the company's direction.

Around the same time, Lyle Tick joined as President and Chief Concept Officer. Tick's background was significant and worth examining in detail, because it reveals what the board was looking for in its next leader.

Tick had served as Brand President of Buffalo Wild Wings from 2018 to 2023, working within the Inspire Brands family of restaurants. At Buffalo Wild Wings, he had led a comprehensive brand revitalization that shared striking parallels with BJ's challenges: a once-differentiated casual dining concept that had lost its way, a menu that had expanded beyond its core identity, and a customer base that needed to be reminded why the brand mattered. Tick's playbook at Buffalo Wild Wings was straightforward: re-embrace the sports bar heritage, revamp the menu (which was recognized with the 2020 MenuMasters award for Best Menu Revamp), evolve the restaurant design, and simplify operations. His appointment at BJ's signaled that the board wanted a similar back-to-basics approach.

Adding another layer of intrigue, Ron Shaich, the legendary founder and former CEO of Panera Bread, entered the picture. Shaich's investment firm, Act III Holdings, along with T. Rowe Price, invested $70 million in BJ's. More importantly, the cooperation agreement with Act III committed Shaich's team to collaborate with management on culinary, supply chain, marketing, design, technology, and recruiting initiatives. Having the architect of Panera's transformation, one of the most successful brand-building stories in restaurant history, actively engaged in BJ's turnaround added credibility and expertise.

Tick was promoted to CEO and President effective June 5, 2025. His strategic vision centered on what he described as rediscovering BJ's DNA: the company had been founded on pizza and beer and bringing people together, but over the years, it had become more known for variety than for anything specific. The menu strategy shifted to emphasize the core pillars: pizza, Pizookies, and craft beer, along with an expanded focus on shareable items.

The pizza itself, the product that started it all nearly five decades ago, was reformulated from the ground up. The new version features a Detroit-style crust, a meaningful departure from the original Chicago deep-dish that founded the brand but a nod to the Detroit-style pizza trend that had been sweeping American food culture. The sauce was reformulated using fresh tomatoes instead of paste. The cheese was upgraded to 100 percent whole-milk mozzarella. Toppings were reimagined: sausage is now slow-roasted in-house rather than purchased premade, and multiple pepperoni options were consolidated into a single cupped variety that crisps when cooked, creating those satisfying little cups of rendered fat that have become an Instagram staple.

The Pizookie Meal Deal, offering an entree, side, and Pizookie for $13 Monday through Friday, became a key traffic driver, particularly among budget-conscious consumers who found the value compelling. The deal effectively converted the Pizookie from a splurge dessert into an everyday value proposition, bringing people through the door during traditionally slower weekday periods. It was a clever use of BJ's most iconic product as a traffic magnet rather than just a menu item.

Financially, the trajectory has been positive. Fiscal 2024 delivered $1.36 billion in revenue with restaurant-level operating profit margins of 14.4 percent. Fiscal 2025 pushed revenue to $1.40 billion, with margins expanding to 15.5 percent and diluted EPS climbing to $2.16 from $0.70 the prior year. For fiscal 2026, management has guided for comparable restaurant sales growth of one to three percent, restaurant-level operating profit of $221 to $233 million, and adjusted EBITDA of $140 to $150 million.

The balance sheet has strengthened meaningfully. Net funded debt ended fiscal 2025 at $61.2 million, composed of $85 million in debt offset by $23.8 million in cash. The debt-to-equity ratio has declined from 41 percent to 25.1 percent over five years. The company has authorized up to $50 million in share repurchases for fiscal 2026, signaling confidence in the financial position.

But the strategic positioning question remains unresolved, and it is the central tension of the BJ's story today.

BJ's is not fast-casual: the dining rooms are too large, the service model too traditional, and the check average too high. It is not fine dining: the atmosphere is casual, the menu accessible, the locations suburban. It is not a traditional casual dining chain either, because the brewery operation and craft beer identity set it apart from the Applebee's and Chili's of the world.

In a market that is bifurcating between convenience-driven, quick-service concepts on one end and premium, experience-driven destinations on the other, BJ's sits in a middle ground that could be either a sweet spot or a no-man's land. If consumers continue to value the combination of quality food, craft beer, and a family-friendly atmosphere, BJ's occupies a niche that few competitors can match. If consumers increasingly choose between fast-and-cheap and slow-and-premium, the middle ground becomes a killing field. The next several years will determine which.

VIII. The Business Model Deep Dive

To understand BJ's Restaurants as a business, you need to understand the economics of a single restaurant, because in the restaurant industry, the unit is everything. The chain is just a collection of units, and if the individual unit does not work, nothing else matters.

A typical BJ's restaurant generates roughly five to six million dollars in annual sales. That is significantly above the casual dining average, driven by the combination of a high-traffic, large-format location and a menu that encourages higher check averages through craft beer and premium items. The target for restaurant-level operating margins is 15 to 20 percent, which translates to roughly $750,000 to $1.2 million in restaurant-level profit per unit. In fiscal 2025, the company achieved 15.5 percent restaurant-level margins across the system, which represents meaningful improvement from the 14.4 percent achieved the prior year but still sits below the pre-decline peak.

The cost structure breaks down into familiar restaurant buckets: cost of goods sold (food and beverage costs), labor, occupancy (rent and related costs), and other operating expenses.

Food costs typically run in the mid-to-high 20s as a percentage of revenue. This means for every dollar a customer spends, roughly 26 to 28 cents goes to the ingredients on the plate and the beer in the glass. This is generally in line with casual dining peers, though the craft beer component offers slightly better margins than food.

Labor is BJ's single largest expense, running in the low-to-mid 30s as a percentage of revenue, and has been the most persistent source of pressure. In California, where BJ's operates its highest concentration of restaurants, minimum wage increases have been particularly aggressive, pushing base wages for restaurant workers well above the national average. This is not a temporary cost spike; it is a structural cost escalation that affects every operator in the state but disproportionately affects chains like BJ's with heavy California exposure.

Occupancy costs, including rent, property taxes, and common area maintenance, are relatively fixed and thus benefit from higher sales volumes. A restaurant that does $6 million in annual sales pays roughly the same rent as one that does $4.5 million, so the profit impact of traffic growth or decline is amplified by the fixed nature of these costs.

The brewery economics add an interesting wrinkle. Building and maintaining brewing operations requires significantly higher upfront capital expenditure than a standard casual dining restaurant. Brewing equipment, storage, distribution infrastructure, and the specialized personnel to run it all represent a meaningful incremental investment. However, the economics of selling house-brewed beer are inherently attractive: the markup on a pint of beer is substantial, and proprietary beers eliminate the wholesale cost that restaurants pay to third-party brewers or distributors. When the Piranha Pale Ale or Tatonka Stout is brewed in-house, the margin is considerably higher than what BJ's earns on a Budweiser or a Modelo.

The company has historically operated brewing in a hub-and-spoke model, with larger brewing operations in select locations producing beer that is distributed to surrounding restaurants. This approach avoids the capital cost of putting a brewery in every location while maintaining the craft authenticity that differentiates the brand. BJ's currently operates brewing operations in five states and supplements production through partnerships with independent third-party craft brewers.

One of the most consequential strategic decisions in BJ's history is the choice to remain entirely company-owned rather than pursuing a franchise model. This is unusual in casual dining, where franchising is the dominant growth mechanism. The argument for corporate ownership at BJ's is straightforward: the brewery operations require a level of quality control and operational complexity that would be difficult to maintain through franchisees. Brewing is not just another kitchen function; it requires trained brewers, specialized equipment maintenance, and consistency standards that are easier to enforce through direct corporate management.

The cost of this decision is equally straightforward: capital intensity. Every new BJ's restaurant requires the company to fund the entire build-out, typically running into several million dollars per unit. A franchise model would push that cost to franchisees, allowing the company to grow faster with less capital. BJ's has chosen quality control over capital efficiency, a trade-off that makes sense strategically but constrains the pace of growth.

The technology stack has evolved significantly in recent years. BJ's has invested in modern point-of-sale systems, kitchen display technology that optimizes order flow, and a digital ordering infrastructure that handles both delivery and takeout. The Premier Rewards loyalty program captures customer data that informs marketing decisions and drives repeat visits. More than 80 percent of off-premise orders are placed through digital channels, giving the company a direct relationship with customers that delivery-platform intermediaries had threatened to commoditize.

The marketing approach has historically been conservative, which is a polite way of saying BJ's has never been a marketing-first company. Unlike Applebee's, which has historically spent heavily on national television, or Chili's, which has invested in brand campaigns and celebrity partnerships, BJ's has relied on local market efforts, digital channels, and the organic word-of-mouth generated by its menu. The Pizookie, in particular, has been a social media phenomenon without the company having to spend much to promote it: Instagram and TikTok posts of the warm cookie-and-ice-cream dessert generate their own viral momentum. This is partly strategic, reflecting the company's regional brand strength, and partly pragmatic, reflecting the reality that with slightly more than 200 locations, the cost of national television advertising would be prohibitive relative to the number of markets where BJ's actually operates. In recent quarters, the viral success of BJ's secret menu items on social media platforms demonstrated the power of organic, digital-first marketing for a brand with a visually compelling product.

The competitive moat question is the one that keeps investors up at night. What, exactly, prevents someone from replicating BJ's concept? The honest answer is: not much, at least in theory. The combination of casual dining and craft brewing is not patented. The Pizookie, while trademarked, is conceptually just a warm cookie with ice cream. The menu, while broad, draws on widely available culinary techniques and ingredients. The true barriers to entry are operational: the years of accumulated expertise in running brewery-restaurants at scale, the relationships with real estate developers, the brand equity in core markets, and the institutional knowledge embedded in more than 200 management teams across 31 states. These are real advantages, but they are not impregnable walls. They are sand castles, well-built and impressive, but vulnerable to the tide.

IX. Competitive Analysis: Porter's Five Forces and Hamilton's Seven Powers

Understanding BJ's competitive position requires stepping back from the company and examining the structural forces that shape its industry. Two frameworks illuminate the challenge with particular clarity: Michael Porter's Five Forces, which analyzes the attractiveness of the industry itself, and Hamilton Helmer's Seven Powers, which identifies the sources of durable competitive advantage that individual companies may or may not possess. Together, they paint a comprehensive picture of why BJ's occupies the strategic position it does, and why that position is both harder to attack and harder to defend than it might appear.

Starting with Porter's Five Forces.

The threat of new entrants into the restaurant industry is a paradox. At the small scale, barriers to entry are almost nonexistent. Anyone with a commercial kitchen, a health permit, and a dream can open a restaurant. The initial capital required can be as little as $100,000 for a small independent concept. This creates relentless competition at the local level, with new restaurants opening and closing constantly in every market where BJ's operates.

However, building a brewery-restaurant hybrid at scale presents a genuinely different challenge. Centralized brewing operations, standardized processes across 200-plus locations, specialized brewing personnel, regulatory compliance across multiple states, and the capital to fund multi-million-dollar build-outs collectively represent a barrier that limits direct imitation. The barrier is not legal or regulatory; it is operational, financial, and experiential. This gives BJ's some protection from direct replication of its specific model, though it does not protect against the far more dangerous threat of substitutes.

Supplier bargaining power is moderate, but the nuances matter. On the food side, BJ's purchases commodity ingredients from multiple suppliers, which limits any single supplier's leverage. But the company is subject to the same food cost volatility that affects all restaurants: when the price of chicken, cheese, or avocado spikes, there is no hedge, no pass-through mechanism, and limited ability to raise menu prices without risking traffic declines. On the brewing side, supplies (hops, malt, yeast) are specialized but sourced from a competitive market.

The more consequential supplier relationship is actually with landlords. BJ's large-format locations in premium retail corridors mean that landlords, particularly those controlling desirable suburban properties, hold meaningful negotiating power. Long-term leases, typically ten to fifteen years with renewal options, lock in occupancy costs and provide stability. But they also create inflexibility when markets shift, consumer patterns change, or a location underperforms. Exiting a lease early is expensive and often impossible without substantial penalties.

Buyer power is high and arguably the most important force shaping the industry. Consumers have essentially unlimited choice in dining. Switching costs are literally zero. A customer who ate at BJ's last Friday might choose Chipotle, a local taqueria, DoorDash delivery from a restaurant across town, or a meal kit from HelloFresh next Friday without a second thought. The BJ's Premier Rewards loyalty program creates some retention benefit, but it is modest compared to the fundamental reality that restaurant consumers are extraordinarily fickle. Price sensitivity has increased post-pandemic, with consumers trading down from casual dining to fast-casual or fast food when household budgets tighten.

The threat of substitutes is the existential force, and it deserves particular attention because it is the single most important structural dynamic shaping BJ's future.

This is what has driven the secular decline of casual dining. The substitutes are not just other restaurants in the traditional sense. They are fast-casual concepts like Chipotle, Panera, and Sweetgreen, offering comparable food quality at lower price points with faster service. They are fast-food chains like McDonald's and Taco Bell that have dramatically improved food quality while maintaining convenience and value. They are delivery platforms that make every restaurant in a city accessible from a couch, eliminating the location advantage that casual dining chains spent decades and billions of dollars building. And they are grocery store prepared foods, meal kits, and the growing quality of convenience-store food options that bring restaurant-adjacent meals into the home at a fraction of the cost.

Each of these substitutes chips away at the casual dining value proposition: "a nice sit-down meal at a reasonable price." When you can get a comparable meal faster, cheaper, or more conveniently, the appeal of spending 60 to 90 minutes in a mid-market restaurant diminishes. The consumer is not making a choice between BJ's and Chili's; the consumer is making a choice between dining out at all and the dozen other ways to feed a family on a Tuesday night.

Competitive rivalry is intense and unforgiving. The casual dining segment is saturated with too many seats chasing too few diners. Major chains like Applebee's and Chili's have struggled through years of declining traffic and periodic reinventions. Regional competitors exist in every market where BJ's operates. Craft breweries, which have proliferated enormously since BJ's first opened its Brea brewery in 1996, now number more than 9,000 nationally, and a growing percentage of them offer food service that directly competes for the craft-beer-and-a-meal occasion. The competitive dynamic is essentially zero-sum: one chain's traffic gain is another's traffic loss.

The overall Porter's assessment is sobering. BJ's operates in a structurally challenging industry where the most powerful forces, buyer power and the threat of substitutes, work against incumbents. Success requires clear differentiation and relentless operational execution, but even those may not be sufficient to overcome the structural headwinds.

Turning to Hamilton Helmer's Seven Powers framework, which asks a more pointed question: what durable competitive advantages, if any, does BJ's possess?

Scale economies are weak. With just over 200 units, BJ's achieves some purchasing power and spreads corporate overhead across a meaningful base, but the advantage is incremental, not transformative. A chain with 100 locations can negotiate nearly as effectively with food suppliers as one with 200. The brewery infrastructure actually adds cost relative to competitors who simply purchase beer from third-party distributors and avoid the capital expenditure and operational complexity of in-house brewing entirely. Scale helps, but it is not the kind of cost advantage that drives structural outperformance.

Network effects are nonexistent. A restaurant does not become more valuable because more people eat there. In fact, the opposite is often true: a crowded restaurant with long wait times can actively deter customers. There is no platform dynamic, no marketplace effect, no increasing returns from user growth. This is a fundamental limitation of the restaurant business model, and it is why restaurants as a category rarely produce the kind of winner-take-all economics that technology companies enjoy.

Counter-positioning was historically BJ's strongest power, and understanding its rise and decline illuminates the company's strategic arc. In the late 1990s and 2000s, the brewery-casual dining hybrid was genuinely counter-positioned against traditional casual dining chains. An Applebee's could not easily add a brewery without completely restructuring its operations, retraining its staff, redesigning its restaurants, and reallocating capital away from its existing model. The incumbent's rational response was to not copy BJ's, because the cost of doing so would damage the existing business. BJ's was doing something that incumbents could not easily replicate without self-harm.

But this power has eroded significantly over the past decade. The concept has been observed, studied, and partially replicated. Some casual dining competitors have added craft beer programs, if not full breweries. More importantly, the market has shifted in ways that made BJ's original counter-position less relevant: fast-casual concepts created their own form of counter-positioning against all of casual dining, and craft breweries added food service, attacking BJ's from the beer side. BJ's original counter-position is no longer unique or particularly powerful.

Switching costs are very weak. The loyalty program creates minimal lock-in compared to, say, a subscription service or a technology platform where migrating data or rebuilding workflows creates genuine friction. The most meaningful switching cost exists for the small segment of beer enthusiasts who have developed a genuine attachment to specific BJ's beers, like the Piranha Pale Ale or the seasonal releases, and cannot find comparable alternatives elsewhere. But this is a niche within a niche, and for the vast majority of customers, switching to any other dining option is effortless.

Branding is moderate and regional. In California and core markets, BJ's has genuine brand equity built over nearly five decades of consistent presence. The Pizookie has achieved a degree of cultural recognition that few menu items at any chain can claim: it is one of those rare products where the trademarked name has become synonymous with a category. But national brand awareness is limited compared to chains with much larger footprints and marketing budgets. BJ's does not command the kind of pricing power that truly strong consumer brands enjoy. Nobody drives past three other restaurants to get to a BJ's the way a Chick-fil-A customer might. Consumers go to BJ's because it is a good option, not because it is the only option they would consider.

Cornered resources are weak. The proprietary beer recipes have some value, particularly award-winning beers that have built followings among craft beer enthusiasts. Premium real estate locations in certain markets represent locational advantages that would be expensive and time-consuming for a competitor to replicate. But nothing in BJ's resource portfolio is truly irreplaceable or defensible over the long term. Recipes can be approximated by talented brewers. Locations can be outbid by well-capitalized competitors. There is no patent, no exclusive license, no natural resource, no single asset that creates a durable barrier.

Process power is BJ's strongest source of competitive advantage, and it is the one that matters most. Operating brewery-restaurants at scale, maintaining consistency across more than 200 locations, managing the dual complexity of restaurant and brewing operations, and doing all of it with the quality standards that generate repeat visits, requires deep institutional expertise that has been refined over three decades. This process power is real and meaningful. It is why BJ's has survived and why no competitor has precisely replicated the model at comparable scale. But process power is also the least durable of Helmer's powers. It can be learned, copied, and eroded over time by determined competitors.

The overall Seven Powers assessment reveals a company whose primary defense is operational excellence in a specific niche, supported by moderate branding in core markets, but lacking the strong, durable competitive advantages that create sustained economic outperformance. Compare this to a company like Chipotle, which possesses genuine process power (its unique food preparation model), meaningful branding (cultural cachet with younger consumers), and arguably some counter-positioning (its commitment to "Food With Integrity" creates a positioning that traditional fast-food competitors struggle to match without cannibalizing their own business model). Or compare it to Chick-fil-A, which has extraordinary branding power and process power, combined with a franchise model that creates alignment between corporate and operators. BJ's simply does not possess advantages of comparable strength.

This explains BJ's modest valuation multiples relative to restaurant companies with clearer competitive moats. In a low-power business, success requires constant execution, continuous adaptation, and the willingness to evolve faster than the market evolves around you. BJ's must earn its position every quarter, because there is no moat to defend. The strategic challenge for any CEO running BJ's is clear: in the absence of strong powers, the company must compete on execution, innovation, and cultural relevance, every single day. The moment it stops earning its place, the market will take it away.

X. Bull vs. Bear Case and What to Watch

The case for BJ's Restaurants starts with scarcity.

There are very few concepts in American dining that combine a full-service casual dining menu with an in-house craft brewery operation at scale. It sounds like a simple idea, but the operational complexity of executing it across 200-plus locations, with centralized brewing operations in five states and quality standards enforced across 31, has proven to be a genuine barrier to imitation. Nobody else has done it at this scale. That scarcity has value, even if it is hard to quantify on a balance sheet.

The brand strength in core markets, particularly California and Texas, is real and measurable. Customer loyalty to BJ's in these markets is above industry average, driven by the combination of the craft beer program, the Pizookie, and the overall dining experience. The off-premise business, which barely existed pre-pandemic, now represents a significant and growing revenue stream that diversifies the company away from its historical dependence on dine-in traffic. The menu breadth, while sometimes criticized as too wide, gives BJ's broad appeal across demographic groups, making it a reliable choice for family dinners, date nights, and group outings.

The operational improvements implemented during and after the pandemic are genuine. Restaurant-level margins have expanded meaningfully, from 14.4 percent in fiscal 2024 to 15.5 percent in fiscal 2025, suggesting that the leaner operating model is producing results. The balance sheet has strengthened, with net funded debt declining to $61.2 million and the debt-to-equity ratio nearly halved over five years. Management has guided for continued improvement, targeting restaurant-level profit of $221 to $233 million and EBITDA of $140 to $150 million in fiscal 2026.

The involvement of Ron Shaich through Act III Holdings adds a dimension that pure financial analysis does not capture. Shaich built Panera Bread from a regional bakery-cafe into a national powerhouse before selling it to JAB Holding for $7.5 billion. His operational playbook, focused on menu quality, customer experience, and technology integration, is directly relevant to BJ's challenges. The cooperation agreement commits Act III's resources to collaborate on culinary, supply chain, marketing, and technology initiatives. Having a proven restaurant operator actively engaged in the turnaround is qualitatively different from having passive investors demanding generic "value creation."

The craft beer market, despite its maturation, continues to represent a meaningful consumer segment. According to the Brewers Association, craft beer accounted for more than a quarter of total beer market revenue in the United States, and craft drinkers tend to be the kind of higher-income, experience-seeking consumers that BJ's targets. The brewery differentiation, while no longer novel, still resonates with this consumer base in a way that a Bud Light tap handle at Applebee's simply cannot match.

There is also a scarcity premium in the market for restaurant acquisition targets. BJ's, with its 200-plus company-owned locations, established brand, and brewery infrastructure, would be an attractive target for a private equity firm or a strategic acquirer looking to consolidate in casual dining. The company's fully corporate-owned model means an acquirer would gain direct control of every location, with no franchise agreements to navigate or renegotiate. This does not mean a sale is imminent or even likely, but it provides a floor on the downside that pure fundamental analysis might understate.

The bear case begins with an uncomfortable structural observation: casual dining as a category may be in permanent decline.

This is not hyperbole. Guest traffic across the segment has been falling for more than a decade, and there is limited evidence that the trend will reverse. The industry data tells a stark story: total casual dining visits in the United States have declined in most years since 2012, even as population has grown and nominal GDP has increased. Consumer preferences have shifted toward convenience, speed, and value, all of which favor fast-casual and delivery-forward concepts over traditional sit-down restaurants.

BJ's can outperform the category, and in recent quarters it has done exactly that. But if the category is shrinking, outperformance may simply mean declining more slowly. It is the difference between swimming faster than the current and actually reaching shore. A company can post positive same-store sales growth through price increases while still losing traffic, and that is precisely the pattern that has characterized much of the casual dining industry in recent years.

The competitive moat, as the Seven Powers analysis reveals, is thin. The brewery-restaurant concept, while operationally complex, is not protected by any structural barrier that would prevent a well-capitalized competitor from replicating it. The operational complexity that serves as BJ's primary defense also creates cost disadvantages: maintaining brewing operations adds capital and operating expense that competitors who simply purchase beer from distributors do not bear. If the pricing premium that craft beer commands narrows, or if consumers increasingly view house-brewed beer as interchangeable with the excellent independent craft beer available at retail, the economic justification for the brewery investment weakens.

The real estate portfolio is a double-edged sword. Long-term leases on 200-plus large-format locations provide stability but also create inflexibility. Locations that were selected during the growth era, when the suburban casual dining market was booming, may not be optimally positioned for the current market. Closing or relocating an underperforming restaurant is expensive and slow, particularly when lease terms extend for a decade or more.

The leadership transition introduces execution risk. BJ's has had three CEOs in the past four years: Greg Trojan through September 2021, Greg Levin through August 2024, and now Lyle Tick as of June 2025, with Brad Richmond serving as interim between Levin and Tick. Leadership instability at this pace raises legitimate questions about strategic continuity and organizational morale. Tick's background at Buffalo Wild Wings is relevant, but BJ's is a different concept with different challenges, and the turnaround he is attempting is the kind of multi-year project that requires sustained commitment and consistent execution.

Consumer trends pose a long-term threat that goes beyond simple preference changes. Younger generations have grown up with delivery apps, fast-casual options, and a food culture that values authenticity, sustainability, and novelty over the reliable-but-predictable casual dining experience. The average Gen Z consumer has more dining options available to them via their smartphone than any previous generation had in an entire city. BJ's menu innovations and value propositions may attract budget-conscious diners today, but the deeper question is whether the concept resonates with the next generation of consumers who will determine its long-term relevance. The Pizookie may be iconic on TikTok today, but cultural relevance is fleeting, and the competitive set for a Gen Z diner's attention includes not just other restaurants but also cooking at home, meal kits, and the rapidly improving quality of convenience-store and grocery-store prepared foods.

For investors watching this story unfold, two metrics matter above all others.