BJ's Wholesale Club: The East Coast Underdog of Warehouse Retail

I. Introduction: The Third Brother

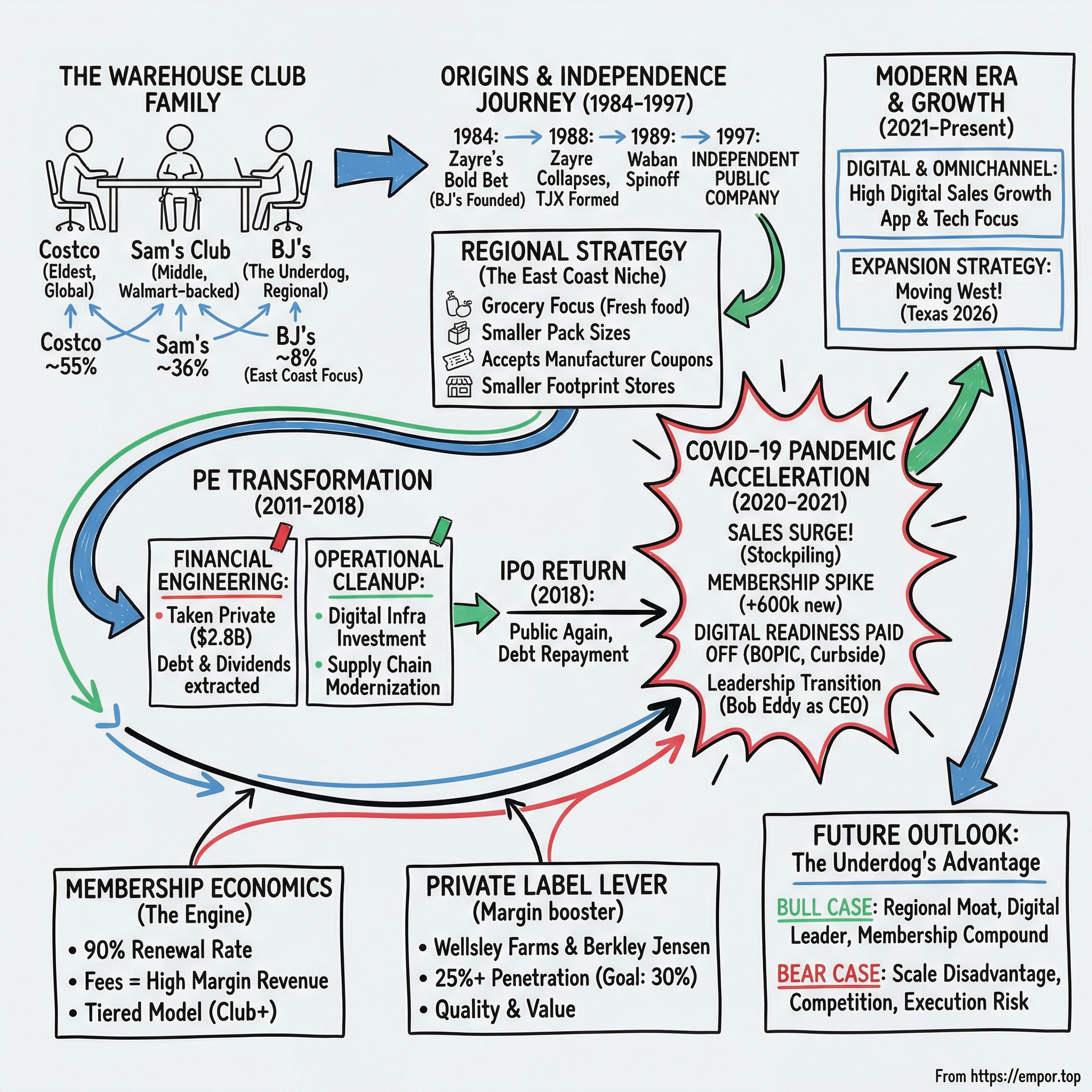

Picture the warehouse club industry as a family reunion. At the head of the table sits Costco, the wildly successful eldest sibling with a $350 billion market cap and stores spanning four continents. To its right sits Sam's Club, the middle child backed by the world's largest retailer. And at the far end, often overlooked, sits BJ's Wholesale Club—the regional player that wasn't supposed to survive.

As of August 2022, Costco held 55.5% of the wholesale club market, Sam's followed with 36.2%, and BJ's came in far behind at 8.3%. By any conventional measure, BJ's should have been crushed decades ago. It lacks Costco's international reach. It doesn't have Walmart's logistics backbone. Yet here it stands—not just surviving, but thriving.

The numbers tell a remarkable story. BJ's Wholesale Club's annual revenue for fiscal 2025 reached $20.5 billion, a 2.67% increase from 2024. More impressively, the company's membership base just hit a record 8 million members in the second quarter of fiscal year 2025, with Q2 2025 total revenue of $5.38 billion. The stock has delivered spectacular returns: from the day the COVID-19 pandemic began in March 2020, BJ's shares surged more than 300%.

How did a regional player survive—and thrive—against two of retail's most fearsome competitors? The answer lies in a combination of strategic discipline, private equity transformation, digital acceleration, and an unwavering commitment to the grocery-focused East Coast consumer. This is the story of how BJ's Wholesale Club turned geographic limitation into strategic advantage, and why the third brother at the reunion table might just have the last laugh.

II. Origins: The Warehouse Club Revolution and Zayre's Bold Bet (1984-1989)

The Invention of a Category

Every industry has its founding myth, and for warehouse clubs, that myth begins in a converted airplane hangar in San Diego. Price Club, founded by Sol and Robert Price on July 12, 1976, in San Diego, California, pioneered the warehouse club concept in the United States. Initially serving only business shoppers, the store provided members access to a limited selection of discounted general merchandise and food items, promoting bulk purchasing at reduced prices.

Sol Price was considered the "father" of the warehouse store retail model. His innovation was deceptively simple: strip away the frills—no fancy displays, no sales staff, no advertising—and pass the savings directly to customers. Membership fees allowed customers to save money compared to traditional retail prices, with the model appealing particularly to small business owners who struggled with high supply costs. Over time, membership expanded to include the general public, with the warehouse club format becoming a significant retail strategy.

Sam Walton of Walmart wrote in his book "Made in America" that he "borrowed as many ideas from Sol Price as from anybody else in the business." He added that he especially liked the idea of calling his discount chain "Wal-Mart" because he "really liked Sol's FedMart name." In 1983, Walton dined with Price and later that year the first Sam's Club opened in Oklahoma City.

Zayre's Strategic Gamble

While Sol Price was revolutionizing retail on the West Coast, a different story was unfolding in Massachusetts. The company was started by discount department store chain Zayre in 1984, on the Medford/Malden border in Massachusetts. This put BJ's squarely in the first wave of the warehouse club movement—founded right around the same time as both Sam's Club and Costco, which both opened just a year earlier, in 1983.

The name itself carries a personal touch that speaks to the company's origin. The company's name was derived from the initials of Beverly Jean Weich, the daughter of Mervyn Weich, the president of the new company. It was a family affair from the start—a regional discount chain betting on a new retail format, naming it after the founder's daughter.

The initial concept was to offer a more focused and convenient shopping experience. The business model centered on an annual membership fee for access to wholesale prices. The first offerings included a wide range of general merchandise and groceries.

Early Leadership and Growing Pains

The new venture faced immediate challenges. Weich announced his resignation as president in June 1987, and left on August 1. He was replaced by John Levy. The departure came as Zayre's broader retail empire was beginning to unravel—a development that would have profound implications for BJ's future.

Initial growth was rapid, with the company expanding primarily in the Northeast, capitalizing on limited regional competition and rising demand for value-oriented retail during the mid-1980s economic environment. Unlike Costco and Sam's Club, which had national ambitions from the start, BJ's focused on dense population centers where parking lots were small but customer density was high.

The strategic choice to remain regional—whether by design or necessity—would prove both a limitation and an advantage. BJ's couldn't compete with Costco's West Coast dominance or Sam's Club's Southern expansion. But in the crowded Northeast corridor, with its tight communities and value-conscious shoppers, BJ's found fertile ground.

The Parent Company Collapses

When Zayre Corporation sold the Zayre nameplate to rival discount chain Ames in October 1988, TJX was formed. The Zayre collapse could have spelled doom for its warehouse club subsidiary. Instead, it triggered a series of corporate maneuvers that would ultimately give BJ's its independence.

For investors, the origins reveal something essential about BJ's DNA: this was never meant to be a national behemoth. From its first day, BJ's was designed to serve the dense, demanding markets of the Eastern seaboard—a focus that continues to define its strategy four decades later.

III. Corporate Musical Chairs: TJX, Waban & the Road to Independence (1988-1997)

The Waban Experiment

The late 1980s were turbulent years for BJ's. Having survived its parent company's demise, the young warehouse club found itself shuttled between corporate owners. In 1989, TJX spun off their warehouse division, consisting of BJ's and now-defunct HomeClub (later known as HomeBase, then House2Home), to form Waban, Inc.

The Waban era represented an awkward pairing. HomeClub was a home improvement concept competing in a very different retail segment. Managing two distinct retail formats under one roof created complexity without obvious synergies. BJ's was a warehouse club focused on groceries and general merchandise; HomeClub was trying to challenge Home Depot in the home improvement space.

During this period, BJ's continued its methodical expansion through New England and the Mid-Atlantic states. The company developed its distinctive focus on grocery items—a differentiation that would later become central to its competitive strategy. While Costco emphasized general merchandise and Sam's Club leaned into its Walmart supply chain advantages, BJ's doubled down on fresh foods and perishables.

Independence at Last

In August 1997, Waban spun off BJ's to become an independent company, BJ's Wholesale Club, Inc., headquartered in Natick, Massachusetts, while Waban renamed itself to HomeBase, Inc.

The 1997 spin-off marked BJ's first opportunity to chart its own course as a publicly traded company. No longer a subsidiary, no longer sharing resources with an unrelated retail concept, BJ's could finally focus entirely on its warehouse club business.

The timing, however, was challenging. In the early 2000s, the company expanded its stores beyond the East Coast of the United States and into Ohio, Michigan, Indiana, and Pennsylvania, with a total of 195 stores by 2005. By 2011, BJ's was the third-largest warehouse club chain in the United States.

But being third in a three-player market presented existential questions. Costco was building an international empire. Sam's Club had Walmart's infrastructure. What exactly was BJ's competitive advantage?

The answer wasn't yet clear, and the stock reflected that uncertainty. BJ's traded as a public company from 1997 to 2011, growing steadily but never achieving the valuation multiples of its larger peers. The company appeared stuck—too small to compete nationally, too large to pivot easily, and facing increasingly fierce competition in its core markets.

IV. The Regional Strategy: Why BJ's Stayed East Coast

Geography as Destiny

Walk into a BJ's Wholesale Club in suburban New Jersey or Connecticut, and you'll notice something different from a typical Costco or Sam's Club. The parking lot is smaller. The store footprint is more compact. And the grocery section—particularly fresh foods—takes up a larger share of the floor.

This isn't accident; it's strategy. BJ's Wholesale is currently concentrated on the East Coast, with roughly 20% of BJ's annual sales coming from the New York metro area. The company built its business around the specific needs of Northeastern consumers: densely populated areas, smaller homes with less storage space, and a strong appetite for fresh food.

BJ's takes a grocery focus that includes a full-service deli, a wider assortment of center-store and perishable items, and smaller pack sizes in perishables. Meanwhile, Costco boasts one of retail's strongest private brands in Kirkland, and the retailer balances its consumables offering with strong general merchandise and services.

The Differentiation Formula

Several key choices distinguish BJ's from its national competitors. First, product assortment: In BJ's fiscal 2021 year report, the company said its clubs range in size from 63,000 square feet to 163,000 square feet. These smaller formats carry fewer SKUs but focus them more intensely on grocery categories.

Second, and critically, BJ's accepts manufacturer coupons—the only major warehouse club to do so. For coupon-clipping Northeastern shoppers, this represents genuine additional savings that neither Costco nor Sam's Club offers.

Third, smaller pack sizes. While bulk purchasing remains central to the warehouse club model, BJ's recognized that Northeastern households—often smaller, with less pantry space—need different pack configurations than Midwestern families with basement storage.

The Third-Place Paradox

Financial intelligence firm CFRA Research estimates that Costco had 62% of the warehouse club market in the United States in 2022, versus Sam's Club with 31% and BJ's with 7%.

These numbers would suggest BJ's is an afterthought. Yet within its core markets, the picture looks very different. In the New York metro area, BJ's has competitive density that rivals its larger peers. In New England, where the company was born, it enjoys brand loyalty built over four decades.

Strong sales and customer gains, new locations and business model advantages—notably paid memberships and one-stop shopping—have positioned the "big three" club chains as more formidable grocery retail competitors, with a better growth outlook than conventional grocers. Within this rising tide, BJ's has carved out a defensible position.

For investors, the regional strategy represents both limitation and opportunity. BJ's will never match Costco's scale. But in its core markets, it has achieved something perhaps more valuable: genuine customer loyalty backed by differentiated service.

V. The 2011 Private Equity Acquisition: A Pivotal Inflection Point

Why Go Private?

By early 2011, BJ's faced a strategic crossroads. The company had grown steadily but struggled to break through its regional constraints. In January 2011, management acknowledged the challenges by announcing difficult decisions: store closures and headquarters layoffs signaled a business under pressure.

In 2011, BJ's was involved in a bidding war between several private equity firms before being sold to Leonard Green & Partners and CVC Capital Partners. The auction process attracted significant interest—a sign that sophisticated investors saw latent value in the struggling warehouse club.

The Deal

BJ's Wholesale Club entered into a definitive agreement to be acquired by affiliates of Leonard Green & Partners and funds advised by CVC Capital Partners in an all-cash transaction valued at approximately $2.8 billion. Under the terms of the agreement, BJ's shareholders received $51.25 per share in cash, representing an approximately 38% premium to the closing price of BJ's shares on June 30, 2010.

The transaction was approved by the Company's stockholders at a special meeting held on September 9, 2011. BJ's common stock was delisted from the New York Stock Exchange prior to the opening of business on Monday, October 3, 2011.

The private equity thesis was straightforward: BJ's had a solid business model constrained by public market short-termism. With patient capital and operational focus, the sponsors believed they could transform the company into a more efficient, growth-oriented enterprise.

The PE Playbook: Dividends, Debt & Transformation

What followed was a masterclass in private equity financial engineering—for better and worse.

The private equity owners invested about $630 million in equity to take the company private in 2011. By the time of the 2018 IPO, they had paid themselves dividends totaling at least $1.8 billion, a massive return on their initial equity slice. What this estimate hides, of course, is the debt load used to finance those dividends.

Leonard Green and CVC Capital Partners took a series of payouts from the warehouse retailer's debt coffers, bringing the total to some $1.8 billion in their five years of ownership and bumping the debt-to-earnings ratio to unhealthy levels.

Critics of private equity often point to such dividend recapitalizations as examples of financial extraction that weakens underlying businesses. And indeed, BJ's emerged from private ownership carrying significant leverage.

The Other Side: Operational Improvements

But the private equity owners didn't just extract capital—they also invested in transforming the business. The 2011 privatization was a masterclass in financial engineering and operational cleanup.

During the private ownership period, BJ's opened new stores, invested heavily in technology infrastructure, and refined its merchandise strategy. The company modernized its supply chain, upgraded its digital capabilities, and prepared for the omnichannel future that would prove so critical during the pandemic.

The digital infrastructure investments proved particularly prescient. While the immediate returns were modest, these capabilities would become the foundation for BJ's pandemic-era surge—a transformation that would have been difficult to achieve under public market pressure for quarterly results.

For investors, the PE era illustrates both the risks and rewards of private ownership in retail. The debt load created genuine vulnerability. But the operational improvements positioned BJ's for growth that public shareholders might never have funded.

VI. The 2018 IPO: Return to Public Markets

IPO Mechanics

Seven years after going private, BJ's returned to the public markets with timing that raised eyebrows. On June 27, 2018, BJ's Wholesale Club announced the pricing of its initial public offering of 37,500,000 shares of its common stock at a public offering price of $17.00 per share.

The wholesale retailer sold 37.5 million shares in its IPO, raising net proceeds of $637.5 million which it intended to use primarily to repay debt. The company's shares opened at $21.25, well above its pricing of $17 a share.

BJ's Wholesale Club closed up 29% after raising $637.5 million in its initial public offering, leading the busiest week in three years for U.S. listings. Shares in the grocery and consumer goods membership club opened at $21.25 per share in New York after selling 37.5 million shares at $17 apiece, at the top of its marketed range. The shares rose as much as 32% in their trading debut before closing at $22, valuing BJ's at $2.78 billion.

PE Returns and Exit

The company was taken private by equity firms Leonard Green & Partners LP and CVC Capital in 2011 for $2.8 billion. Currently, CVC and Green Equity each own 34.5% stake in the company.

The math was remarkable. The PE sponsors had invested roughly $630 million in equity. Through dividends and their remaining stakes at IPO, they stood to quintuple their money—a return that, by any measure, ranked among the most successful retail PE transactions of the decade.

Market Context and Skepticism

BJ's return to public markets came amid a retail apocalypse narrative. Amazon was supposedly destroying physical retail. Mall anchors were filing for bankruptcy. Yet warehouse clubs—with their membership-based model and treasure-hunt shopping experience—seemed immune to the digital onslaught.

Walmart also gave the company a boost early in 2018 when it closed 63 Sam's Club stores. That factored into the Moody's Investors Service assessment that the planned IPO could mitigate the company's debt.

The Sam's Club closures created a windfall for BJ's, particularly in overlapping markets. Suddenly, the smallest warehouse club had room to grow without aggressive head-to-head competition from a well-funded rival.

Yet skeptics wondered whether BJ's could sustain growth. The company remained heavily levered from its PE years. Competition from Costco was intensifying in the Northeast. And Amazon's Whole Foods acquisition suggested tech-enabled grocery competition was only beginning.

What no one anticipated was that within two years, a global pandemic would turn warehouse clubs into essential infrastructure—and BJ's, with its grocery focus and newly enhanced digital capabilities, would be perfectly positioned to capture the surge.

VII. COVID-19: The Pandemic Acceleration (2020-2021)

The COVID Surge

March 2020 transformed American retail almost overnight. Consumers who had never stepped inside a warehouse club suddenly found themselves stocking up on bulk paper towels, frozen foods, and cleaning supplies. The membership model that some had questioned proved perfectly suited to crisis-era shopping behavior.

For BJ's, the timing was extraordinary. BJ's Wholesale Club "gained considerable share" after net and comparable sales jumped more than 20% and net income more than doubled in the fiscal 2020 first quarter. For the quarter ended May 2, net sales totaled $3.72 billion, up 21.1% from $3.07 billion a year earlier. Membership fee income also rose 8.4% to $79.6 million, powered by a 40% year-over-year gain in members.

Comparable-club sales climbed 19.9% from a year ago and, excluding fuel, were up 27%.

The second quarter proved even more dramatic. BJ's Wholesale Club posted record fiscal second-quarter sales and earnings that blew past analysts' forecasts as consumers flocked to the retailer's stores to stock up on essential goods. The company earned $107.5 million, or 77 cents an adjusted share, almost double the $55 million, or 39 cents, in the prior year. Sales rang in at $3.9 billion, up from $3.3 billion. Same-store sales rose by 24.2%, including e-commerce growth of more than 300%.

Membership Surge

BJ's added around 600,000 new members since COVID-19 began, bringing its membership base to more than 6 million. "The pandemic has led to younger families moving out of cities to the suburbs," said CEO Eddy. "Many of our members join when they start a family."

Warehouse clubs have "gained quite a bit of share during Covid and continue to," said KK Davey, president of strategic analytics at market research firm IRI. "Lots of members have signed up. Once you're in the club, you continue to buy." Club stores gained 0.5% of market share in 2020 and 0.5% in 2021, adding up to around $16 billion.

Digital Readiness Pays Off

The pandemic revealed a crucial advantage: BJ's was digitally prepared when many competitors were not.

GroupBy had already built technology to support buy online pickup in club and same day delivery for BJ's well before COVID-19 existed. When the pandemic hit, BJ's was therefore able to shift quickly to an expanded version of omnichannel, adding curbside pickup for their members.

During the third quarter of fiscal 2020, digitally-enabled sales surged 200%, adding 4 percentage points to comparable club sales. This followed an increase of 300% and 350% in the second and first quarters, respectively.

The digital investments made during private ownership—investments that had seemed expensive and slow to pay off—suddenly proved their worth. While some retailers scrambled to implement curbside pickup, BJ's already had the infrastructure in place.

Leadership Transition

The pandemic coincided with a planned leadership transition that took a tragic turn. On December 19, 2019, BJ's had named Lee Delaney as its next CEO, effective February 2, 2020. Delaney, a former Bain Capital partner, took over as BJ's CEO in early 2020, guiding it through the COVID-19 crisis and supply challenges driven by consumers stockpiling everything from cleaning supplies and toilet paper to fresh meat.

BJ's Wholesale Club announced that Lee Delaney, the Company's President and Chief Executive Officer, passed away unexpectedly on April 8, 2021 due to presumed natural causes. He was just 49 years old.

BJ's Wholesale Club named Bob Eddy as president and CEO on April 20, 2021. Eddy had been filling the top slot since the untimely death of Lee Delaney earlier that month. Laura Felice, who joined BJ's in 2016 and most recently served as senior vice president and controller, filled Eddy's former role as chief financial officer.

Eddy, who had been CFO since 2011, brought deep institutional knowledge. His promotion signaled continuity rather than disruption—appropriate for a company navigating both a pandemic and the loss of its leader.

For investors, the pandemic period demonstrated BJ's resilience. Membership surged, digital capabilities proved their worth, and the company emerged from COVID-19 with a fundamentally stronger business.

VIII. Digital Transformation & Modern Era (2021-Present)

Omnichannel Investment

The pandemic accelerated trends already underway. BJ's Wholesale Club has been directing resources toward expanding digital capabilities to better engage with members and provide them with a convenient way to shop, including same-day delivery, curbside pick-up, and buy online, pick up in-club.

BJ's has built a strong digital portfolio with BJs.com, BerkleyJensen.com, Wellsleyfarms.com and BJ's mobile app. These enable members to buy, review products and digitally add coupons to their membership cards. Members can track their annual savings as well. BJ's Wholesale Club has also teamed up with DoorDash, Instacart and Roadie to provide on-demand delivery from its stores. The company has also rolled out Same-Day Select, through which members, on payment of an upfront fee, can avail of either unlimited or 12 same-day grocery deliveries.

Digital Sales Performance

The numbers tell the story. BJ's digital growth has been nothing short of impressive. The company has posted double-digit growth in digitally enabled sales every quarter for the past two years. Its success is driven in part by the expansion of digital conveniences such as buy online, pick up in club, curbside pickup, and same-day delivery.

Members who shop digitally tend to spend 90% more than in-store-only shoppers. This statistic illuminates why BJ's continues to invest in digital capabilities even when the immediate margin impact is negative.

In Q4 2024, digitally enabled comparable sales surged 26.0% year-over-year, with a two-year stacked comp growth of 53.0%. This outperformance reflects a strategic shift toward omnichannel retailing, including expanded online ordering, curbside pickup, and delivery partnerships.

Technology Modernization

Beyond customer-facing features, BJ's has invested significantly in backend infrastructure. BJ's has also invested heavily in modernizing its order management and fulfillment systems. In 2023, the company transitioned its omnichannel inventory operations to a microservices-based order management system through a partnership with Nextuple. The new system enables BJ's to optimize fulfillment across various channels—whether in-store, curbside, or through same-day delivery—allowing for more flexibility and faster service. The new OMS provides real-time visibility into inventory levels.

The warehouse club is using autonomous inventory robots and AI to generate efficient order batch and pick routes, which reduced the time associates spend collecting items by more than 45%.

The BJ's mobile app, which is now used by 60% of members, has become an integral part of the company's digital strategy. Members can use the app to clip coupons, navigate stores and utilize features like Express Pay Checkout. Additionally, the app's personalization features, including product recommendations and AI-powered shopping lists, keep members engaged between visits.

Expansion Strategy

For decades, BJ's expansion was modest—sometimes opening only a handful of stores per year. That's changed dramatically. BJ's Wholesale Club announced plans to open 25-30 clubs over the next two fiscal years, including several clubs set for the Dallas-Fort Worth area starting in early 2026.

"Economic expansion and a growing population make Texas a great fit for us," BJ's Chairman and CEO Bob Eddy said. The first stores in the Dallas area are expected to open in early 2026.

The Texas expansion represents a significant strategic pivot. For decades, BJ's stayed within its Eastern comfort zone. Now, emboldened by strong financials and operational improvements, the company is venturing into Sam's Club heartland.

BJ's is preparing four regional sites in Texas, including Forney, Fort Worth, Grand Prairie and Waxahachie. It also announced adding a second retail spot in Alabama. "Our momentum remains strong," said Bill Werner, executive vice president of strategy and development. "We're on track to open our first clubs in the Dallas-Fort Worth area in 2026."

Current Scale and Operations

BJ's Wholesale Club operates 257 clubs across 21 states in the eastern half of the United States, serving more than 8 million members through a model that emphasizes bulk purchases and discounted pricing.

For investors, the digital transformation and geographic expansion represent the next phase of BJ's growth story. The question isn't whether BJ's can compete—it's proven that repeatedly. The question is how much market opportunity remains in new territories while defending its Northeastern stronghold.

IX. Membership Economics Deep Dive

The Beating Heart of the Business

If there's a single metric that defines warehouse club economics, it's membership renewal rates. Unlike traditional retailers who must win every transaction, membership clubs earn recurring revenue that provides stability regardless of quarterly fluctuations.

In fiscal 2024, BJ's reported an 8.5% year-over-year increase in membership fee income to $456.5 million, driven by a 90% tenured member renewal rate. This loyalty is no accident.

The 90% renewal rate represents remarkable stickiness. Consider what it means: nine out of every ten members who've been with BJ's for more than a year choose to renew. That's brand loyalty translated into predictable cash flow.

Current Membership Base

BJ's membership base hit a record 8 million members in the second quarter of fiscal year 2025. The growth trajectory is striking—up 55% since the 2018 IPO.

The company's focus on delivering value and taking care of families drove Membership Fee Income up by 9.0% to $123.3 million in Q2 of fiscal year 2025.

Tiered Membership Strategy

Like its competitors, BJ's operates a two-tier membership system, but with some distinctive features. Share of higher tier membership topped 40% for the first time, according to President and CEO Bob Eddy.

The higher-tier Club+ membership costs $120 annually and includes 2% cash back on most purchases plus a 5-cent-per-gallon gas discount. These premium members generate significantly more lifetime value than standard members.

2025 Price Increase

BJ's Wholesale Club raised its annual membership fees by $5 to $60 per year, and its Club+ fee rose $10 to $120 per year, effective January 1, 2025. The increases were the first in seven years.

The move follows the same step by BJ's larger competitor Costco, which in September 2024 raised its basic membership fee to $65 from $60, its first increase since 2017. Sam's Club raised its fees in 2022.

The fee increase came with enhanced benefits. Effective January 1, 2025, Club+ members receive two free same-day deliveries on eligible orders of $50 or more during each annual membership period.

Membership Fee Revenue Durability

Membership fees operate differently than merchandise sales. They're collected upfront, recognized over the membership period, and generate nearly 100% gross margin. This high-margin revenue provides a cushion against merchandise margin pressure and competitive pricing.

Healthy membership growth is crucial for BJ's economics: fees are high-margin, recurring revenue that help offset thin merchandising margins typical in the warehouse-club model.

For investors, membership metrics deserve close attention. Renewal rates, tier mix, and absolute member counts all signal the health of BJ's core business model more reliably than quarterly comp sales.

X. Private Label: The Margin Lever

The Strategic Imperative

Every major retailer invests in private label, but for warehouse clubs, store brands represent an especially powerful strategic lever. BJ's Wholesale Club regularly markets numerous products under its own private labels. Unlike its competitors—such as Costco's Kirkland Signature line and Sam's Club's Member's Mark brand—BJ's uses multiple private label brands depending on merchandise segment. Grocery products are primarily branded as Wellsley Farms, while general merchandise items are sold under the Berkley-Jensen name.

This multi-brand approach differs from the single-brand strategies of competitors. Costco's Kirkland Signature has become almost synonymous with the warehouse club experience, appearing on everything from vodka to vitamins. BJ's chose segmentation instead—allowing distinct brand identities for different categories.

Growth and Penetration

Private label sales at BJ's Wholesale Club currently make up more than 25% of its total business, and continued own brand momentum has officials confident they will soon hit their 30% penetration rate goal.

Private labels have been a key growth driver for BJ's, with its in-house brands Wellsley Farms and Berkley Jensen now accounting for over 25% of the company's business.

The exclusive brands are limited to BJ's members, with more than 90% of them purchasing Wellsley Farms and Berkley Jensen products.

Quality Ratings

More than 95% of Wellsley Farms and Berkley Jensen private label products earn shopper ratings of four out of five stars or more, according to Bob Eddy. This demonstrates the "rigor in which our teams ensure that we have the best combination of assortment, quality, and price."

Industry Context

The three clubs collectively have about 20% of the market in private brands and have seen growth of about 50% in 2024, according to Jim Griffin, president of Daymon North America.

Private label growth is also in the cards at BJ's Wholesale as executives reported they were on track to reach the 30% penetration rate goal set for its assortment of private brands. While value certainly plays a vital role in this continued growth, product quality is also of major importance. In fact, 95% of BJ's own-brand products earn ratings of four out of five stars.

For investors, private label penetration offers a window into margin trajectory. Each percentage point shift from national brands to private label typically adds 10-15 basis points to gross margin. BJ's path from 25% to 30% penetration represents meaningful earnings potential.

XI. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

The warehouse club industry presents formidable barriers to entry. Capital requirements are substantial—each new club represents a $9-15 million construction investment plus land acquisition. Building the supplier relationships necessary for competitive pricing takes years. And the membership model creates switching costs that benefit incumbents.

No significant new entrant has emerged in the U.S. warehouse club market in decades. The last serious attempt was Costco itself, which succeeded only through merger with Price Club. For practical purposes, the industry is a stable oligopoly.

2. Bargaining Power of Suppliers: MODERATE

Warehouse clubs occupy an interesting position with suppliers. Their curated assortment—roughly 7,000 SKUs at BJ's versus 30,000+ at a typical supermarket—means each vendor relationship carries significant volume. This gives clubs meaningful leverage.

However, the clubs' limited selection also means they can't easily drop major brands without losing customer traffic. Coca-Cola, Procter & Gamble, and other category leaders maintain bargaining power because their products drive club visits.

BJ's takes a grocery focus that includes a full-service deli, a wider assortment of center-store and perishable items, and smaller pack sizes in perishables. This grocery concentration creates additional supplier complexity compared to more diversified competitors.

3. Bargaining Power of Buyers: MODERATE-HIGH

Individual members face low switching costs. Costco, Sam's Club, and BJ's memberships are all reasonably priced, and many households hold multiple warehouse club memberships. Price transparency is high, and the clubs compete aggressively on value perception.

However, the membership model leads customers to spend more than they would without one. A sunk-cost fallacy often drives people to keep buying to try to get the most bang for their subscription fees. This psychological dynamic somewhat reduces buyer power once membership is established.

4. Threat of Substitutes: MODERATE

Traditional supermarkets, mass merchants, e-commerce, and specialty grocers all compete for the same consumer wallet. Warehouse club retailers are in an expansion phase and, in the process, siphoning grocery market share from traditional supermarkets.

The warehouse club model's combination of price and convenience has proven resilient against most substitutes. Amazon's entry into grocery through Whole Foods hasn't significantly dented club traffic. Traditional grocers continue losing share.

5. Competitive Rivalry: HIGH

Within the warehouse club segment, competition is intense. Costco maintains clear market leadership and continues expanding aggressively. Sam's Club, after years of stagnation, has resumed store openings. And BJ's itself is accelerating expansion into new markets.

"Sam's Club, Costco and BJ's Wholesale are all ramping up the pace of new club openings over the next several years. Sam's Club and Costco are the only two warehouse club operators with a nationwide presence. BJ's Wholesale is currently concentrated on the East Coast but slowly expanding towards the Midwest."

XII. Hamilton's Seven Powers Analysis

1. Scale Economies: MODERATE (Relative Disadvantage)

BJ's operates approximately 250 clubs versus Costco's 900+ and Sam's Club's 600+. This scale disadvantage affects purchasing power, distribution efficiency, and marketing leverage.

However, regional density partially compensates. In the Northeast corridor, BJ's achieves club density comparable to its larger rivals, enabling efficient distribution and marketing within its core markets.

2. Network Effects: LOW-MODERATE

Warehouse clubs don't exhibit strong network effects in the traditional sense. More members don't directly make the service more valuable to other members. However, membership scale does enable better vendor negotiations and more frequent store visits (since the cost is already sunk), creating indirect benefits.

3. Counter-Positioning: MODERATE

BJ's differentiation—grocery focus, smaller pack sizes, manufacturer coupons, smaller footprint stores—represents genuine counter-positioning against Costco and Sam's Club. These choices appeal to Northeastern consumers in ways that would be difficult for national competitors to replicate without cannibalizing their existing formats.

4. Switching Costs: LOW-MODERATE

Membership fees create modest switching costs, but most are under $100 annually. The real switching costs are behavioral: once shoppers learn a store's layout and develop purchasing routines, they're unlikely to change without compelling reason.

5. Branding: MODERATE

BJ's brand resonates strongly in its core markets but lacks national recognition. The company's purpose statement—"We take care of the families who depend on us"—reflects its community-oriented positioning.

6. Cornered Resource: LOW

BJ's doesn't possess any truly proprietary resources. Its locations are valuable but not irreplaceable. Its supplier relationships are important but not exclusive.

7. Process Power: MODERATE-HIGH

The company's operational expertise in grocery—particularly fresh food management, perishables logistics, and club operations—represents genuine process power developed over four decades. This is difficult for competitors to replicate quickly, even with superior resources.

XIII. Key Performance Indicators for Investors

For long-term fundamental investors monitoring BJ's, three KPIs deserve particular attention:

1. Membership Fee Income Growth

This metric captures both member count growth and tier mix improvement. Because membership fees generate nearly 100% gross margin, this line item has outsized impact on profitability. Recent performance: 8-10% annual growth, driven by new member acquisition, strong retention, and increasing Club+ penetration. Fiscal 2024 membership fee income reached $456.5 million.

2. Comparable Club Sales (Excluding Gas)

Gas prices introduce volatility that obscures underlying merchandise trends. Comp sales excluding gas reveal whether BJ's is gaining or losing share in its core categories. The company targets low-to-mid single-digit annual growth in this metric. Recent performance has been solid, with traffic growth driving positive comps.

3. Digitally Enabled Sales Growth

This measures the success of BJ's omnichannel investments. The 30%+ growth rates of recent quarters reflect both pandemic-era acceleration and sustained adoption of convenience features. Watch for this metric to normalize as the base grows larger—but continued double-digit growth signals successful digital transformation.

XIV. Bull Case and Bear Case

Bull Case

Regional Moat with National Optionality: BJ's has proven it can defend its Northeast stronghold against well-funded competitors. The Texas expansion represents upside optionality without betting the company. If successful, it opens a large new market; if not, core operations remain robust.

Membership Economics Compound: With 90% renewal rates and growing Club+ penetration, BJ's membership base generates increasingly valuable recurring revenue. Each fee increase drops almost entirely to the bottom line. The January 2025 increase alone adds significant annual profit.

Digital Leadership: Among warehouse clubs, BJ's has invested most aggressively in omnichannel capabilities. The digital pivot is more than a trend—it's a structural advantage. As consumers increasingly demand convenience, BJ's is capturing market share from competitors slower to adapt.

Inflation Beneficiary: As discretionary spending tightens, bulk retailers like BJ's thrive. Membership growth and higher-tier penetration signal customers are doubling down on cost savings.

Private Label Runway: The path from 25% to 30%+ private label penetration represents meaningful margin expansion opportunity.

Bear Case

Scale Disadvantage: BJ's will never match Costco's purchasing power or Sam's Club's logistics infrastructure. This limits pricing flexibility and creates permanent cost disadvantage.

Geographic Concentration Risk: Roughly 20% of sales from the New York metro area creates meaningful concentration risk. Economic weakness in the Northeast would disproportionately impact BJ's.

Expansion Execution Risk: Texas represents a step into Sam's Club's heartland with no existing brand recognition. Opening costs are high, and new store economics typically take 3-5 years to mature.

Balance Sheet Overhang: While improved from PE-era leverage, BJ's still carries meaningful debt that constrains financial flexibility during downturns.

Competitive Response: As BJ's expands into new markets, competitors may defend aggressively. Price wars could pressure margins throughout the industry.

XV. Myth vs. Reality

Myth: BJ's is just a smaller version of Costco. Reality: BJ's has a distinctly different merchandise strategy, focusing heavily on grocery with smaller pack sizes and accepting manufacturer coupons. The customer experience differs meaningfully from both Costco and Sam's Club.

Myth: Private equity destroyed BJ's balance sheet. Reality: While the PE owners extracted substantial dividends, they also invested in digital infrastructure and operational improvements that positioned BJ's for its pandemic success. The company emerged from PE ownership with more debt but also more capability.

Myth: Regional focus limits growth. Reality: BJ's geographic concentration created defensible market position in high-value markets. The company is now selectively expanding while maintaining regional density advantages.

Myth: Warehouse clubs are Amazon-proof. Reality: While warehouse clubs have shown resilience, Amazon continues investing in grocery delivery and Whole Foods. The competitive threat hasn't disappeared—it's evolving.

XVI. Risks and Regulatory Considerations

Accounting Considerations: BJ's revenue recognition for membership fees requires judgment about member acquisition costs and the timing of revenue recognition. The company defers membership fees and recognizes revenue ratably over the membership period—a conservative approach that smooths revenue but delays cash recognition.

Regulatory Environment: The warehouse club model faces periodic regulatory scrutiny around alcohol sales licenses, pharmacy operations, and gasoline pricing. BJ's operates in 21 states with varying regulatory requirements.

Labor Relations: BJ's approximately 25,000 employees represent meaningful labor cost exposure. Minimum wage increases in Northeastern states—where BJ's concentrates its operations—have direct impact on operating margins.

Real Estate Commitments: Long-term lease obligations represent significant fixed costs. In an economic downturn, these commitments could constrain flexibility to close underperforming locations.

XVII. Conclusion: The Underdog's Advantage

Four decades after opening its first store on the Medford/Malden border in Massachusetts, BJ's Wholesale Club has defied expectations at nearly every turn. It survived the collapse of its parent company. It endured private equity ownership. It emerged from a pandemic stronger than before. And now it's expanding into territory once considered off-limits.

The numbers tell a story of steady transformation: BJ's Wholesale Club had revenue of $5.38B in the quarter ending August 2, 2025, with 3.36% growth. In the fiscal year ending February 1, 2025, BJ's had annual revenue of $20.50B with 2.67% growth.

But numbers alone miss what makes BJ's remarkable. In an industry dominated by two giants, the third player carved out a defensible niche through strategic discipline, customer focus, and digital investment. BJ's never tried to be Costco. It tried to be the best warehouse club for Northeastern families—and largely succeeded.

"Our terrific fourth quarter performance contributed to a record year at BJ's, powered by all-time high membership results. Our improved assortment, investments in value and significant growth in digital sales drove our 12th consecutive quarter of traffic growth. We are also growing our footprint at pace to serve even more members," said Bob Eddy.

The Texas expansion represents the next test. Can BJ's replicate its Northeastern success in new markets against entrenched competition? The early signs are encouraging—the company is entering methodically, with multiple sites announced and realistic timelines.

For investors, BJ's presents an unusual proposition: a proven business model with meaningful growth optionality trading at a discount to its larger peer. The risks are real—scale disadvantage, geographic concentration, execution uncertainty. But so are the strengths—membership economics, digital capabilities, and a management team that has repeatedly exceeded expectations.

The story of BJ's Wholesale Club isn't one of overnight success or venture-backed disruption. It's the story of methodical execution, strategic patience, and the enduring power of delivering value to customers who notice the difference. In an era obsessed with scale and speed, BJ's offers a reminder that sometimes the underdog strategy is simply to be really, really good at serving your customers.

The third brother at the reunion table may not be the loudest or the richest. But he's still here, still growing, and still taking care of the families who depend on him.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube