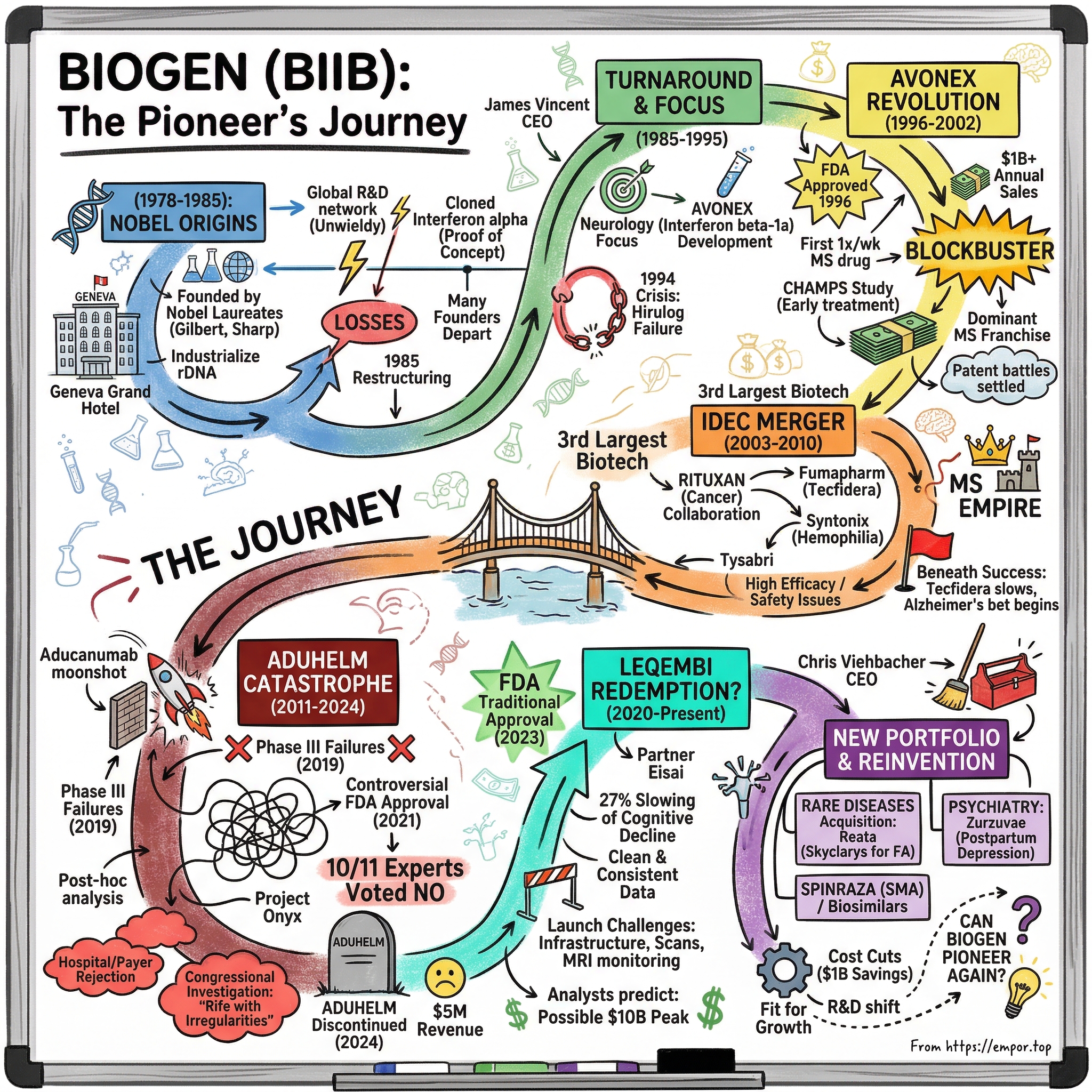

Biogen: The Pioneer that Lost Its Way (and Found It Again?)

I. Introduction & Cold Open

The conference room at Biogen's Cambridge headquarters fell silent on June 7, 2021. After months of controversy, the FDA had just approved Aduhelm—the company's $56,000-per-year Alzheimer's drug—despite overwhelming opposition from its own advisory committee. Ten of eleven experts had voted against approval, citing insufficient evidence. The eleventh abstained. None voted yes.

Yet here it was: approved under the FDA's accelerated pathway, making it the first new Alzheimer's treatment in eighteen years. Champagne corks should have been popping. Instead, the atmosphere was tense. Everyone in that room knew what the outside world was about to discover—this wasn't a triumph. It was the beginning of biotech's biggest controversy.

Within weeks, three FDA advisory committee members would resign in protest. Major hospital systems including Cleveland Clinic and Mount Sinai would refuse to administer the drug. Insurance companies would balk at coverage. A congressional investigation would find the FDA-Biogen collaboration "rife with irregularities." By January 2024, Biogen would discontinue Aduhelm entirely, writing off one of the most expensive drug development failures in pharmaceutical history.

How did we get here? How did a company founded by Nobel laureates, a pioneer that literally invented modern biotechnology, become a cautionary tale about hubris, regulatory capture, and scientific compromise?

The answer requires us to go back to 1978, to a hotel room in Geneva where a group of scientists sketched out an audacious plan to use recombinant DNA to manufacture human proteins. Among them were Walter Gilbert, who would win the Nobel Prize in Chemistry just two years later, and Phillip Sharp, who would claim his Nobel in 1993. They weren't just founding a company—they were creating an industry.

Today, Biogen trades at a market cap of $19.34 billion, generating annual revenues of $9.67 billion. Those numbers tell a story of survival, but not triumph. The company that once dominated multiple sclerosis treatment watches its franchise erode quarter by quarter. The Alzheimer's breakthrough it chased for decades became its greatest embarrassment.

Yet there's another story emerging. A potential redemption arc centered on Leqembi, the "other" Alzheimer's drug developed with partner Eisai. A pivot toward rare diseases through smart acquisitions. A new CEO with a turnaround mandate. The question isn't whether Biogen was a pioneer—that's historical fact. The question is whether it can pioneer again, or whether it's destined to become another fallen giant, a reminder that in biotech, scientific brilliance alone isn't enough.

This is the story of how Biogen created an industry, conquered a disease category, lost its way chasing the ultimate prize, and now fights for relevance in a world it helped create. It's a story about the tension between scientific integrity and commercial pressure, between patient need and shareholder returns, between breakthrough innovation and incremental improvement.

Most importantly, it's a story that's still being written. Because while Aduhelm may be dead, Biogen isn't—not yet. And understanding how we got here might just tell us where we're going.

II. The Nobel Prize Origins: Creating Biotech (1978–1985)

The Grand Hotel in Geneva had hosted its share of historic meetings—diplomatic summits, peace negotiations, secret wartime conferences. But in the winter of 1978, a different kind of history was being made in one of its conference rooms. Charles Weissmann, a molecular biologist from the University of Zurich, had assembled what might have been the most intellectually powerful group ever to start a company.

Around the table sat Walter Gilbert from Harvard, already considered a lock for the Nobel Prize for his DNA sequencing work. Phillip Sharp from MIT, whose discovery of RNA splicing would revolutionize our understanding of genetics. Kenneth Murray from Edinburgh, who had helped develop the hepatitis B vaccine. Heinz Schaller from Heidelberg, a pioneer in gene expression. Together, they represented not just scientific excellence but a radical bet: that the techniques of molecular biology could be industrialized to produce human proteins at scale. The company name itself—Biotechnology Geneva—captured their ambition. They weren't just starting another pharmaceutical company; they were creating an entirely new category. The "biotechnology" industry barely existed. Genentech had been founded just two years earlier in San Francisco. The entire field consisted of perhaps a dozen companies worldwide, most still operating out of university labs.

Weissmann would later recall the electricity in that room. These weren't venture capitalists looking for a quick flip or corporate executives managing quarterly earnings. They were scientists who believed they could change medicine. Gilbert would receive his Nobel Prize in 1980 for DNA sequencing work; Sharp would win his in 1993 for discovering RNA splicing. This level of scientific firepower in a startup was unprecedented. Their first breakthrough would come from Weissmann's lab in Zurich, where he successfully cloned and produced interferon alpha—the first cloning and expression of interferon, a protein the human body produces to fight viral infections. This wasn't just a scientific achievement; it was proof that their radical idea could work. Human proteins could be manufactured in bacteria. The biotechnology industry was no longer theoretical.

But transforming scientific brilliance into commercial success proved far more challenging than any of them anticipated. Gilbert, despite his Nobel credentials, approached the company like an extended academic research project. He established a global research and development network during the early 1980s that sported operations in Zurich, Geneva, Belgium, Germany, and the United States. It was impressive on paper—multiple labs pursuing cutting-edge research simultaneously. In practice, the organization eventually became unwieldy and lacked focus

The coordination challenges were immense. Scientists in Geneva couldn't easily collaborate with colleagues in Cambridge. Research priorities shifted depending on which lab director shouted loudest. By 1984, this ambitious global network had produced groundbreaking science—but also $100 million in accumulated losses.

The board faced a stark choice: shut down or radically restructure. They chose the latter, bringing in James Vincent as CEO in 1985. Vincent wasn't a scientist—he was a turnaround specialist who had previously worked at Abbott Laboratories. His mandate was clear: save Biogen from bankruptcy.

Vincent's first move was brutal but necessary. He consolidated operations, shutting down the European labs and centralizing research in Cambridge, Massachusetts. The company that had once sprawled across two continents would now operate from a single headquarters. Many of the founding scientists departed, unable to accept the new commercial focus. Gilbert himself stepped back from day-to-day operations, though he remained on the board.

The transformation was painful but effective. Vincent negotiated with creditors, restructured licensing agreements, and most importantly, began the long process of reclaiming Biogen's intellectual property. In the rush to raise capital during the early years, the company had licensed away rights to many of its discoveries. Getting them back would take years, but Vincent understood that without control of its own innovations, Biogen would never be more than a research boutique.

III. The Turnaround & Finding Focus (1985–1995)

By 1989, Vincent's strategy was bearing fruit. Through a combination of renegotiations, buybacks, and strategic partnerships, Biogen had regained control of 90% of its original patents. The company that had nearly died from lack of focus now had a clear direction: neurological diseases.

The pivot wasn't arbitrary. While other biotech companies chased cancer or cardiovascular diseases—larger markets with more competition—Biogen's scientists had noticed something interesting about interferon. Beyond its antiviral properties, the protein seemed to have effects on the immune system that might be relevant to autoimmune conditions affecting the nervous system. Multiple sclerosis, in particular, appeared to be a promising target. In 1992, alpha interferon began generating meaningful revenue, validating the commercial viability of their science. But the real breakthrough was taking shape in the laboratories. Biogen's scientists had begun modifying interferon beta for a specific purpose: treating multiple sclerosis.

The insight was elegant. MS was understood to be an autoimmune disease where the body's immune system attacks the myelin sheath protecting nerve fibers. Interferon beta appeared to modulate this immune response, potentially slowing the disease's progression. The pivotal clinical trial of Biogen's intramuscular interferon beta-1a (AVONEX) was being conducted when interferon beta-1b was approved in 1993 as the first DMT for relapsing-remitting MS.

But 1994 brought another crisis. The company posted $7.4 million in revenue against $18 million in losses. Their anti-clotting drug Hirulog, which had consumed significant resources, failed in clinical trials and had to be discontinued. Critics questioned whether Biogen could ever translate its scientific prowess into sustainable profits.

Vincent remained focused on the MS opportunity. He understood that success in this market wouldn't just mean revenue—it would establish Biogen as a serious pharmaceutical company. The entire organization pivoted toward getting their interferon beta-1a, branded as Avonex, across the regulatory finish line.

IV. The Avonex Revolution: Conquering Multiple Sclerosis (1996–2002)

The FDA advisory committee meeting on May 17, 1996, was standing room only. MS patients, many in wheelchairs, had traveled from across the country to witness what they hoped would be a historic moment. After three hours of deliberation, the committee voted unanimously to approve Avonex for relapsing forms of multiple sclerosis.

Avonex was launched in the U.S. in 1996 and in Europe in 1997 for the treatment of relapsing forms of MS to slow the progression of disability and reduce relapses. The approval made it only the second disease-modifying therapy for MS, but Biogen had a crucial advantage: their once-weekly intramuscular injection was far more convenient than the existing treatment's every-other-day regimen.

The clinical trial results were compelling. Biogen introduced four clinical trial innovations that became standard practice, including defining disability progression as a specified event using survival curves. AVONEX produced a 38% reduction in disability progression using this method. After two years of treatment, 22% of patients treated with Avonex had a worsening of disability compared to 35% of patients treated with placebo.

But success brought immediate challenges. Schering AG sued for patent infringement, claiming Avonex violated their interferon beta patents. The legal battle threatened to derail everything Biogen had built. After months of litigation, the companies reached a settlement that allowed both products to remain on the market, though the terms remained confidential.

The real breakthrough came in 2000 when Biogen demonstrated that Avonex could delay MS development in patients who had experienced their first demyelinating event—essentially catching the disease before it fully manifested. The CHAMPS study was the first trial in patients with a first acute demyelinating event to show efficacy in delaying time to clinically definite MS and introduced the concept of early treatment.

By 2002, Avonex had become a blockbuster, generating over $1 billion in annual sales. Avonex became the most prescribed treatment for relapsing forms of MS worldwide, with more than 130,000 patients on therapy. The drug's orphan status, which provided market exclusivity and tax benefits, was set to expire in 2003, but Biogen had already established such market dominance that generic competition seemed a distant threat.

The transformation was complete. The company that had nearly collapsed twice was now one of biotechnology's biggest success stories. But Vincent and his team knew that relying on a single product, no matter how successful, was dangerous. They needed to build a broader portfolio, and they found the perfect partner in IDEC Pharmaceuticals.

V. The IDEC Merger: Scale and Synergy (2003–2010)

The merger announcement on June 23, 2003, sent shockwaves through the biotechnology industry. Biogen and San Diego-based IDEC Pharmaceuticals would combine in a $6.8 billion deal, creating the world's third-largest biotechnology company. It was a merger of equals in the truest sense—both companies brought blockbuster drugs and complementary expertise.

IDEC's crown jewel was Rituxan, a revolutionary cancer drug that had emerged from a 1995 collaboration between the two companies. The partnership had already proven successful: Rituxan was generating over $1 billion annually treating non-Hodgkin's lymphoma. Now, as a combined entity, Biogen Idec could leverage both the neurology expertise from Avonex and the oncology success of Rituxan.

The strategic logic was compelling. Both companies faced similar challenges—concentrated revenue streams, looming patent expirations, and the need for pipeline diversification. Together, they would have the scale to compete with big pharma while maintaining biotech's innovative culture.

Jim Mullen, who became CEO of the combined company, embarked on an acquisition spree to further strengthen the portfolio. In 2006, Biogen Idec acquired Conforma Therapeutics for $250 million, gaining access to heat shock protein inhibitors for cancer. Fumapharm AG followed, bringing an oral MS drug candidate that would eventually become Tecfidera. Syntonix Pharmaceuticals added $120 million worth of long-acting clotting factors for hemophilia.

But the real prize was building an MS empire. By 2008, Biogen Idec wasn't just participating in the MS market—it was dominating it. Avonex remained the market leader, but the company was developing second and third-generation treatments. Tysabri, acquired through the merger, showed unprecedented efficacy despite safety concerns that required careful monitoring.

The golden years had arrived. Revenue exceeded $4 billion by 2009. The company's market capitalization topped $15 billion. Biogen Idec had become what its founders envisioned: a fully integrated biopharmaceutical company competing on equal terms with century-old pharmaceutical giants.

Yet beneath the success, troubling trends were emerging. Avonex's growth was slowing as newer oral MS drugs entered the market. The oncology franchise, despite Rituxan's success, wasn't producing next-generation winners. Most ominously, the company had begun pouring resources into Alzheimer's disease—a graveyard of pharmaceutical ambitions where hundreds of drugs had failed.

VI. The Aduhelm Catastrophe: Hubris and Controversy (2011–2024)

In 2007, Biogen licensed aducanumab from Neurimmune, a small Swiss biotech company. It was a monoclonal antibody designed to clear amyloid plaques from the brain—the protein deposits that many scientists believed caused Alzheimer's disease. After decades of failures in the field, Biogen executives saw this as their moonshot, the drug that could transform them from an MS company into something greater.

The early signs were promising. Phase I trials showed the drug could indeed clear amyloid plaques. Biogen launched two massive Phase III trials—EMERGE and ENGAGE—enrolling over 3,000 patients across hundreds of sites globally. The investment was staggering: over $1 billion in development costs, with plans to spend $3.3 billion on sales and marketing between 2020 and 2024.

Then came March 2019. A futility analysis showed the trials were failing. Neither EMERGE nor ENGAGE would meet their primary endpoints. Biogen's 2 clinical trials on the drug were halted in 2019 as data revealed it provided no benefit to patients' cognitive function. The company's stock crashed 29% in a single day, wiping out $18 billion in market value.

But Biogen didn't give up. In an unprecedented move, they conducted a post-hoc analysis with additional data from patients who had continued treatment. This new analysis, involving only 55% of the original participants, suggested that high doses in the EMERGE trial showed a 22% slowing of cognitive decline. The ENGAGE trial still showed no benefit.

What happened next would become one of the most controversial chapters in FDA history. The investigation found that the FDA and Biogen engaged in at least 115 meetings, calls and substantive email discussions from July 2019 to July 2020, including 40 meetings to guide Aduhelm's potential approval. Documents later revealed Biogen had launched an internal campaign dubbed "Project Onyx" to convince FDA officials to approve the drug.

The November 2020 FDA advisory committee meeting was a disaster for Biogen. At that meeting, none of the committee's members voted to say that the studies presented strong evidence that the drug was effective at treating Alzheimer's. Ten members voted against approval. One abstained. None voted yes.

Yet on June 7, 2021, the FDA approved Aduhelm anyway, using the accelerated approval pathway. The decision stunned the medical community. Three advisory committee members resigned in protest. Dr. Aaron Kesselheim told CNN in 2021 that the relationship between the FDA and the company was out of the ordinary.

The pricing decision added fuel to the fire. The report says Biogen set an "unjustifiably high price" for Aduhelm to "make history" for the company, and thought of the drug as an "unprecedented financial opportunity." Biogen priced Aduhelm at $56,000 per year, even though analysts estimated it should cost between $3,000 and $8,400 annually to be cost-effective.

The market rejection was swift and brutal. Cleveland Clinic, Mount Sinai, and other major hospital systems refused to administer the drug. Medicare severely restricted coverage, essentially blocking access for most patients. The European Medicines Agency rejected the drug entirely.

In December 2022, a congressional investigation delivered the final blow. A congressional investigation found that the US Food and Drug Administration's "atypical collaboration" to approve a high-priced Alzheimer's drug was "rife with irregularities." The report detailed how FDA officials had essentially coached Biogen through the approval process, even helping draft documents for the advisory committee.

By January 2024, it was over. Wednesday, Biogen said it's pulling all efforts from the first-of-its-kind anti-amyloid beta therapy to focus on Leqembi, its Eisai-partnered newer medicine, and its pipeline candidates. Biogen is taking a $60 million charge and is discontinuing all development and sales of Aduhelm, the company said. It's terminating the ENVISION clinical study, which sought to confirm the benefit of the medicine as required under its 2021 accelerated approval.

Aduhelm had generated less than $5 million in total revenue—a catastrophic failure for a drug that was supposed to generate billions. More importantly, it had shattered trust: in Biogen's scientific judgment, in the FDA's independence, and in the drug approval process itself.

VII. The MS Empire Crumbles: Generic Competition & Portfolio Decay (2015–Present)

While Biogen was chasing Alzheimer's glory, its MS foundation was quietly eroding. The warning signs had been there for years. In 2013, Tecfidera launched to great fanfare as an oral MS drug, quickly becoming a multi-billion dollar product. But by 2015, growth was slowing. New competitors were entering the market monthly, it seemed. The numbers told a brutal story. In the fourth quarter, sales for Biogen's multiple sclerosis (MS) franchise—which includes drugs like Tysabri and Tecfidera—declined 9% at constant currencies to a little more than $1 billion. For all of 2024, Biogen's multiple sclerosis sales came in at $4.4 billion, a 7% drop over the sum the business brought home in 2023.

The collapse of Tecfidera was particularly painful. In 2020, Mylan launched a generic version of Tecfidera in the US, and since then other companies have launched generic versions of the drug. The entry of the discounted generics led to a sharp decline in Tecfidera's revenue. It dropped from generating peak sales of $4.4bn in 2019 to $1.4bn in 2022, with the US sales of the drug being $417.7m in 2022.

Tysabri faced its own challenges. Much of that decline was driven by generic competition to Tecfidera around the world, as well as Tysabri's limited exposure to biosimilars in Europe. "Although a biosimilar has not yet launched in the U.S., we continue to see competition increasing in the high efficacy class," McDonnell said of Tysabri's performance at home.

The competitive landscape had fundamentally changed. Roche's Ocrevus, which Biogen had actually co-developed and received royalties on, was cannibalizing their own products. Novartis's Mayzent, Merck KGaA's Mavenclad, and a dozen other therapies flooded the market. The monopolistic pricing power Biogen had enjoyed for two decades evaporated overnight.

CEO Chris Viehbacher, brought in after the Aduhelm disaster, didn't sugarcoat the situation. "We've had several years of declining revenue and profit, which is not unusual when you're dealing with patent expirations," Biogen CEO Christopher Viehbacher told reporters on a media call Tuesday. He added that one of the key ways Biogen will return to growth is to "reposition the company away from our legacy franchise of multiple sclerosis towards new products."

Summarizing the current situation Biogen finds itself in, Viehbacher postulated that there's about $4.5 billion left to gain in MS revenue, and about $3 billion in remaining profit for the business. From a peak of over $9 billion annually, the MS franchise that had built Biogen was in terminal decline.

Looking at the year ahead, Biogen expects 2025 revenue to fall by a mid-single-digit percentage point versus 2024. That's a greater fall than consensus expectations of a 2.8% decline this year. The empire hadn't just crumbled—it was still crumbling.

VIII. The Leqembi Redemption Story (2020–Present)

Even as Aduhelm imploded, Biogen had another iron in the fire. In partnership with Japan's Eisai, they were developing lecanemab, branded as Leqembi—another anti-amyloid antibody but with crucial differences. The clinical data was cleaner. The trial design more robust. The relationship with regulators more traditional. The Alzheimer's Association celebrates today's U.S. Food and Drug Administration (FDA) action to grant traditional approval of Leqembi® (lecanemab, Eisai/Biogen) for the treatment of early Alzheimer's disease with confirmation of elevated amyloid beta. This is the first traditional approval of an Alzheimer's treatment that changes the underlying course of the disease.

In a Phase 3 clinical trial, Leqembi delayed cognitive decline by 5.3 months compared to placebo after 18 months of treatment, at a time when such delays are most valuable to the individual. The 27% slowing of cognitive decline was modest but real—and crucially, the data was clean and consistent.

Unlike Aduhelm's tortured path, Leqembi followed a traditional regulatory journey. It received accelerated approval in January 2023, then full approval in July 2023 after confirmatory trials validated the benefit. Broader Medicare coverage is now available for Biogen and Eisai's Leqembi (the brand name for lecanemab) following the Food and Drug Administration's (FDA) move to grant traditional approval to the drug that treats individuals with Alzheimer's disease.

But the launch faced its own challenges. For the last three months of 2024, Leqembi generated global sales of $87 million, growing about 30% quarter over quarter. While growth was steady, it was far slower than anticipated. Biogen CEO Viehbacher told reporters on the media call Tuesday that there are around 2,000 patients currently on Leqembi. There are some 8,000 U.S. patients currently waiting to get on treatment, executives from Eisai said on an earnings call last week.

The infrastructure challenges were immense. Patients needed amyloid PET scans or lumbar punctures to confirm eligibility. They required MRI monitoring for brain swelling. Infusion centers needed capacity for biweekly treatments. Many neurologists weren't equipped to manage the complex protocol.

Analysts at RBC Capital Markets have predicted Leqembi, which is currently priced at $26,500 per year, could at its peak reach $10 billion in annual sales. The breakthrough drug is predicted to be a blockbuster, generating total forecast sales of $12.9 billion between 2023 and 2028, according to GlobalData, a leading data and analytics company.

Whether Leqembi could achieve these projections remained uncertain. Competition was coming—Eli Lilly's donanemab showed similar efficacy with less frequent dosing. But for Biogen, Leqembi represented something more than revenue: redemption. Proof they could still develop important medicines. Evidence that the Alzheimer's pursuit, despite Aduhelm's catastrophe, wasn't entirely misguided.

IX. The New Portfolio: Rare Diseases & Reinvention (2023–Present)

Chris Viehbacher understood that Biogen couldn't wait for Leqembi to save them. The former Sanofi CEO, brought in to clean up the Aduhelm mess, embarked on a buying spree focused on rare diseases—smaller markets, but with less competition and premium pricing.

The crown jewel was Reata Pharmaceuticals, acquired for $7.3 billion in July 2023. In July, Biogen agreed to purchase Texas-based Reata Pharmaceuticals and its approved Friedreich's ataxia drug Skyclarys. The drugmaker is the "natural owner" of Skyclarys, Viehbacher said after striking the deal. Analysts believe the drug could hit $1.5 billion in sales by 2030.

Skyclarys was already showing promise. Skyclarys on Monday secured approval from the European Commission to treat the neurodegenerative disorder Friedreich's ataxia (FA). In March 2023, Skyclarys got U.S. approval becoming the first-ever FDA-approved therapy for FA. By Q2 2024, it was generating $100 million in quarterly sales.

The rare disease strategy extended beyond acquisitions. Spinraza, Biogen's treatment for spinal muscular atrophy, remained a billion-dollar product despite intense competition from Novartis's gene therapy Zolgensma. The drug demonstrated Biogen's ability to maintain market share through superior patient support and real-world evidence.

In psychiatry, Biogen partnered with Sage Therapeutics on Zurzuvae, the first oral treatment for postpartum depression. Biogen has also partnered with Sage Therapeutics on the first pill for postpartum depression, which won FDA approval in August. But the agency declined to clear the drug for major depressive disorder, which is a far larger commercial opportunity. While sales started slowly—$14.9 million in Q2 2024—the drug addressed a massive unmet need.

The biosimilars business provided steady, if unglamorous, revenue. Biogen's versions of blockbuster drugs like Humira and Rituxan generated nearly $200 million quarterly with minimal investment. It wasn't transformative, but it helped offset MS declines.

William Blair noted that executives have pegged the pipeline as having potential for $14 billion in peak revenue. Truist Securities noted that new products Qalsody for ALS, Skyclarys in Friedreich's ataxia (FA) and Zurzuvae in postpartum depression are all Biogen drugs with recent approvals in indications where there's little precedent. "Biogen is building a market in each case where there wasn't previously existing infrastructure," Truist wrote. That's a tough haul for any company, even one the size of Biogen.

X. Cost Cuts & Financial Engineering

Viehbacher's transformation went beyond portfolio reshaping. In 2023, he launched "Fit for Growth," a restructuring program targeting $1 billion in gross cost savings by 2025. The cuts were brutal but necessary—shuttering facilities, consolidating research programs, laying off hundreds of employees.

The financial engineering was sophisticated. R&D spending shifted from broad platform research to targeted programs with clearer commercial paths. Marketing budgets concentrated on launch products rather than defending dying franchises. Administrative layers disappeared.

Total revenues are expected to decline by a mid-single-digit percentage in constant currency terms in 2025 from the 2024 level. A further decline in MS revenues is expected to be partially offset by higher revenues from new products. Adjusted earnings per share are expected in the range of $15.25 to $16.25, which represents a decline from the 2024 levels.

The 2025 guidance disappointed investors—revenue declining mid-single digits, EPS falling to $15.25-$16.25 from 2024 levels. But Viehbacher argued this was the trough. The cost base would be right-sized. The portfolio would be rebalanced. Growth would return.

The balance sheet remained strong with over $5 billion in cash and minimal debt. This provided flexibility for additional acquisitions or partnerships. But time was running out. The MS franchise declined faster than new products grew. Investors' patience wore thin.

XI. Playbook: Lessons from Biogen's Journey

Biogen's trajectory offers a masterclass in both biotech success and failure. The lessons are stark:

The dangers of single-product dependence: Avonex made Biogen, but relying on the MS franchise for two decades left them vulnerable when competition arrived. Diversification isn't optional—it's survival.

Regulatory relationships require boundaries: The Aduhelm scandal showed how close collaboration can become inappropriate influence. A congressional investigation found that the US Food and Drug Administration's "atypical collaboration" to approve a high-priced Alzheimer's drug was "rife with irregularities." Companies need FDA's expertise, but independence must be maintained.

Scientific integrity versus commercial pressure: When clinical data is ambiguous, the temptation to push forward can be overwhelming. Aduhelm showed the cost of yielding to that temptation—not just financially, but reputationally.

Platform transitions are existential challenges: Moving from small molecules to biologics, from one therapeutic area to another, from proprietary drugs to biosimilars—each transition risks destroying value before creating it. Few companies navigate multiple transitions successfully.

Pricing strategy in specialty pharma: The report says Biogen set an "unjustifiably high price" for Aduhelm to "make history" for the company, and thought of the drug as an "unprecedented financial opportunity." Biogen priced Aduhelm at $56,000 per year, even though its actual effects on a broad patient population were unknown. Premium pricing requires clear value demonstration. Without it, payer pushback can kill a launch regardless of FDA approval.

XII. Bear vs. Bull Case

Bear Case: The pessimists see a company in terminal decline. The MS franchise faces continued erosion with no floor in sight. Leqembi's launch trajectory suggests peak sales far below initial projections, especially with Lilly's competitive entry. The rare disease portfolio, while promising, can't offset the MS losses quickly enough.

The pipeline lacks transformative assets. BIIB080 for Alzheimer's won't report data until 2026. The lupus and ALS programs face long development timelines and high failure risk. Meanwhile, competition intensifies across all therapeutic areas.

Financially, the company trades at 13x forward earnings—cheap for a reason. Revenue declines accelerate. Margins compress. The dividend yield of 3.5% might attract income investors, but growth investors have fled. At $130 per share, the stock could fall to $100 as reality sets in.

Bull Case: The optimists see a turnaround story at an inflection point. Leqembi's steady growth will accelerate as infrastructure improves and subcutaneous formulation launches. The drug could still reach $5-7 billion in peak sales. Skyclarys alone justifies much of the Reata acquisition price. Together, new products offset MS declines by 2026.

The company's deep neuroscience expertise remains valuable. BIIB080 could revolutionize Alzheimer's treatment by targeting tau. The ALS pipeline addresses massive unmet need. Success in even one program transforms the equity story.

Strategically, Biogen becomes an acquisition target. At current valuation, big pharma could pay a 50% premium and still create value. The neurology franchise, despite challenges, provides immediate scale. The pipeline offers optionality. At $130, risk-reward favors bulls.

XIII. The Verdict: Can Biogen Reinvent Itself?

Biogen stands at a crossroads that many former high-flyers have faced. Like Motorola after smartphones disrupted mobile phones, like Xerox after PCs democratized computing, Biogen must reinvent itself while its core business crumbles.

The parallels to other pharmaceutical transitions are instructive. Merck survived the Vioxx crisis through disciplined R&D and smart business development. Abbott split itself to unlock value. Allergan sold itself at peak valuation. Each chose a different path; not all succeeded.

CEO Chris Viehbacher brings credibility from his Sanofi transformation. His strategy is clear: stabilize the base business, invest in high-value niches, maintain financial flexibility for opportunities. It's textbook turnaround management. But textbooks don't account for the pace of MS erosion or the challenges of launching first-in-class drugs.

Success in five years would mean Leqembi generating $3-5 billion annually, Skyclarys and other rare disease drugs contributing $2-3 billion, and at least one pipeline asset becoming a blockbuster. The MS franchise would stabilize at $2-3 billion. Total revenues would approach $12 billion with expanding margins. The stock would trade above $200.

Failure looks like continued MS declines, Leqembi peaking below $2 billion, rare disease drugs underperforming, and pipeline failures. Revenue falls below $7 billion. The company becomes acquisition fodder at distressed valuations, perhaps $80-100 per share.

The most likely outcome falls between these extremes. Biogen survives but doesn't thrive. It becomes a solid, midsized biotech generating $9-10 billion in revenue, growing slowly, paying dividends, occasionally launching innovative drugs. Not the pioneering giant it once was, but not a cautionary tale either.

XIV. Recent News Update

Biogen to Highlight Scientific Progress Across Alzheimer's Disease at the Alzheimer's Association International Conference 2025. The company continues to advance its Alzheimer's portfolio beyond Leqembi.

The U.S. Food and Drug Administration (FDA) has granted Fast Track designation to BIIB080, an investigational antisense oligonucleotide (ASO) therapy targeting tau, for the treatment of Alzheimer's disease. Fast Track designation is intended to facilitate the development and expedite the review of investigational drugs that treat serious conditions and address unmet medical needs. The Phase 2 CELIA study is now fully enrolled, with a data readout expected in 2026.

In rare diseases, Biogen announced a collaboration for the development and commercialization of zorevunersen, a potential first-in-class disease modifying medicine in development for the treatment of Dravet syndrome, in all territories outside the United States, Canada, and Mexico. Upon closing of this transaction, Stoke will receive an upfront payment of $165 million. The parties will share external clinical development costs for zorevunersen (30 percent Biogen; 70 percent Stoke). Additionally, Stoke may receive up to $385 million in development and commercial milestone payments.

ZURZUVAE® (zuranolone) Receives Positive Opinion from CHMP for the Treatment of Women with Postpartum Depression, expanding the drug's potential market to Europe.

The company also announced strategic infrastructure changes. Biogen Inc. (Nasdaq: BIIB) announced plans for its new global headquarters at Kendall Common, located at 75 Broadway in Cambridge, as part of a multi-year real estate consolidation plan in Massachusetts. The move centralizes Biogen's presence in Kendall Square, integrating Biogen's research and development and technical operations teams alongside its global and North American commercial organizations into a co-located innovation hub. Scheduled to open when Biogen celebrates its 50th anniversary in 2028, the new state-of-the-art facility will commemorate five decades of excellence in scientific discovery, clinical development, and delivering innovative new treatments.

XV. Links & Resources

SEC Filings & Investor Materials: - Biogen Investor Relations: investors.biogen.com - Annual Reports (10-K): 2020-2024 - Quarterly Reports (10-Q): Most recent quarters - Proxy Statements: Executive compensation and governance

Clinical Trial Resources: - ClinicalTrials.gov: Biogen-sponsored trials - FDA Drug Approval Database: Aduhelm, Leqembi approvals - European Medicines Agency: Leqembi review documents - CHAMPIONS and CHAMPS study publications

Congressional & Regulatory Documents: - House Committee on Oversight and Reform: Aduhelm Investigation Report (2022) - FDA Advisory Committee Meeting Materials: Aduhelm (November 2020) - CMS National Coverage Determination: Alzheimer's drugs

Academic Publications: - Nature Reviews Neurology: "The Aduhelm Controversy" (2021) - New England Journal of Medicine: Leqembi Phase 3 results - Journal of Alzheimer's Disease: Anti-amyloid therapy reviews - Multiple Sclerosis Journal: Avonex long-term follow-up studies

Industry Analysis: - GlobalData: Alzheimer's market forecasts - Evaluate Pharma: MS market analysis - Jefferies Research: Biogen coverage reports - William Blair: Biotechnology sector analysis

Books & Long-form Journalism: - "The Drug Hunters" by Donald R. Kirsch and Ogi Ogas - "Science Business: The Promise, the Reality, and the Future of Biotech" by Gary Pisano - STAT News investigation: "Project Onyx" series - Wall Street Journal: Coverage of Aduhelm approval process

Key Executive Interviews: - Chris Viehbacher at J.P. Morgan Healthcare Conference (2023, 2024) - Michel Vounatsos exit interviews (2022) - Walter Gilbert oral history (MIT Archives)

Patient Advocacy Resources: - Alzheimer's Association: Treatment guidelines - National Multiple Sclerosis Society: Drug comparison tools - Friedreich's Ataxia Research Alliance: Skyclarys resources

Final Thoughts

Biogen's story isn't finished. From Nobel Prize origins to the Aduhelm catastrophe, from MS dominance to portfolio decay, the company embodies both the promise and peril of biotechnology. Whether it emerges stronger from this crucible or becomes another cautionary tale depends on decisions being made today in Cambridge boardrooms and research labs.

The stakes extend beyond shareholders. Millions of patients with neurological diseases need innovative treatments. The biotechnology industry needs examples of successful reinvention. The drug approval system needs restoration of trust.

Biogen at 47 years old faces the same existential question that confronts all aging innovators: Can past glory inspire future greatness, or does it become a burden that prevents necessary transformation? The next few years will provide the answer. For now, Biogen remains what it has always been—a company defined by both its spectacular successes and spectacular failures, forever chasing the next breakthrough while running from the last disaster.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube