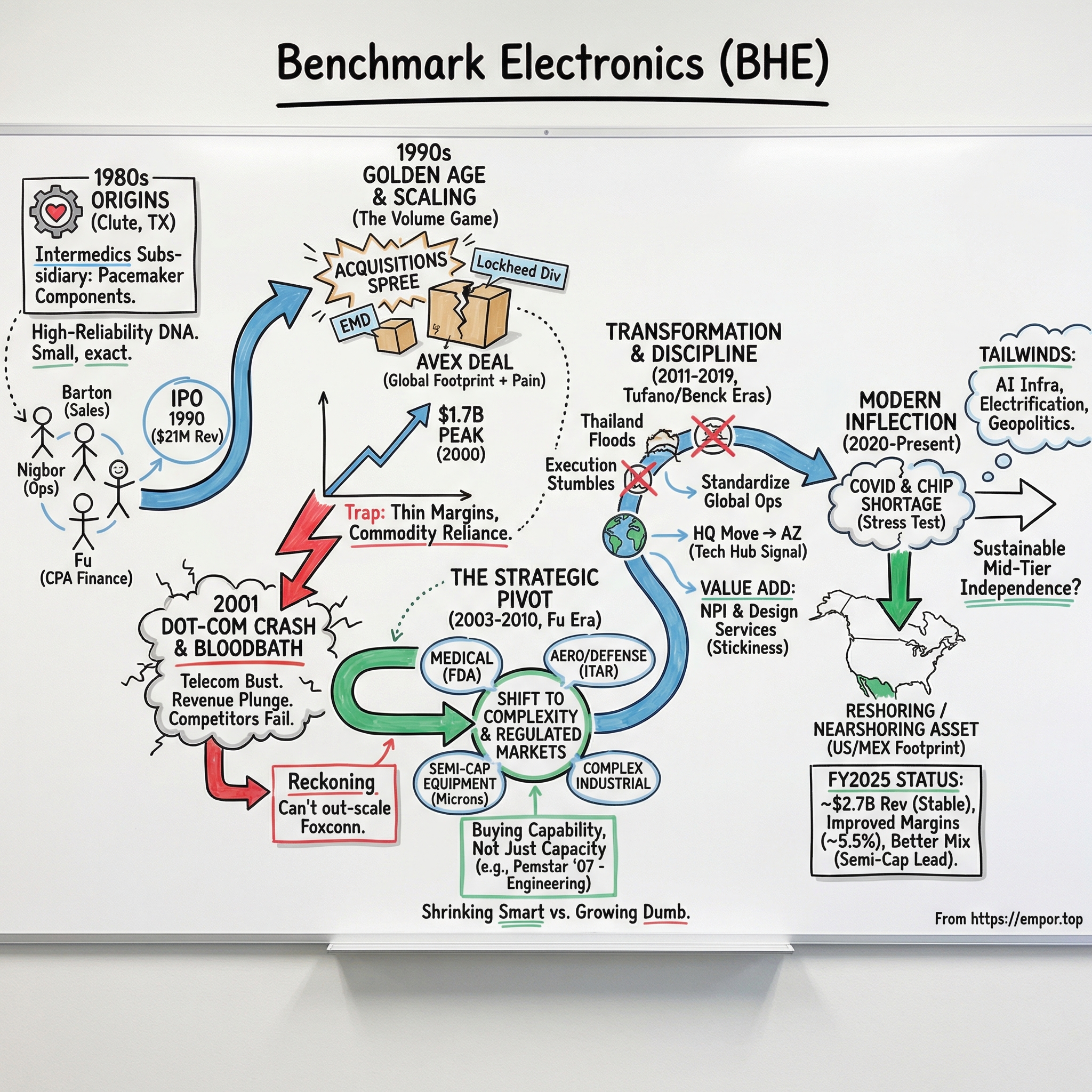

Benchmark Electronics Inc.: The Story of a Contract Manufacturing Survivor

I. Introduction & Episode Roadmap

Picture a factory floor somewhere in Angleton, Texas, in the mid-1980s. Fluorescent lights hum above rows of soldering stations. A handful of technicians are hand-placing components onto printed circuit boards destined for pacemakers—devices that will literally keep human hearts beating. The operation is small, maybe a few dozen people, housed in a facility most Americans would drive past without a second glance.

This is where Benchmark Electronics began. Not with venture capital or a Stanford dorm room pitch, but with the steady, exacting, unglamorous work of assembling electronics for someone else's product.

Fast forward nearly four decades, and Benchmark Electronics trades on the New York Stock Exchange under the ticker BHE, generating over $2.6 billion in annual revenue across 22 manufacturing sites in eight countries. The company employs roughly 12,000 people who build some of the most complex electronic assemblies on the planet—components for semiconductor fabrication equipment, medical devices, defense systems, and industrial machinery.

Yet most people in the technology world have never heard of them.

That anonymity is, in a strange way, the point. Benchmark operates in the electronics manufacturing services industry—EMS for short. Think of EMS companies as the general contractors of the tech world. When a medical device company designs a next-generation surgical robot, or when a defense contractor needs circuit boards for a missile guidance system, they often don't build those things themselves. They hand the designs to an EMS provider like Benchmark and say: "Make this, at scale, perfectly, on time, and for less than we could do it ourselves."

The central question of this story is deceptively simple: How did a small Texas PCB assembler survive more than thirty-five years in the brutal contract manufacturing game while peers went bankrupt, got swallowed by competitors, or faded into irrelevance? The answer involves at least five near-death experiences, a wrenching strategic pivot away from the very markets that built the company, multiple CEO transitions, and a relentless fight to move up the value chain in an industry that constantly tries to commoditize you.

This is a story about the unglamorous but critical middle of technology supply chains. It is a story about what happens when you cannot out-scale the biggest player in your industry—Foxconn, in this case, a company roughly seventy-five times Benchmark's size—and must find another way to survive. It is a story about the difference between growing dumb and shrinking smart. And it is, ultimately, a story about whether a mid-sized, independent contract manufacturer can carve out a durable position in one of the toughest competitive landscapes in global business.

The themes that run through this narrative—the EMS industry's relentless consolidation wave, the pivot from commodity assembly to value-added engineering partnership, and survival through strategic repositioning rather than brute-force scaling—are relevant far beyond contract manufacturing.

They speak to a universal business challenge: what do you do when you are too small to compete on scale and too large to be ignored? Benchmark's answer, refined through decades of trial and error, offers a case study in strategic survival that any operator or investor in a competitive, capital-intensive industry should study closely.

II. The Birth of EMS & Benchmark's Founding (1979–1990s)

To understand Benchmark's origin, you first have to understand why electronics manufacturing services existed at all. In the 1970s and early 1980s, most electronics companies designed and built their own products in-house. If you were IBM or Hewlett-Packard or Texas Instruments, you owned the factories, employed the assembly workers, and controlled every step from silicon wafer to finished product. This was the vertically integrated model, and for decades it was gospel.

But a quiet revolution was underway. As electronics grew more complex and product cycles shortened, OEMs—original equipment manufacturers, the companies whose brand names appear on the finished products—began asking a heretical question: "Do we really need to own all these factories?" The math was compelling.

Manufacturing requires enormous capital investment in equipment, facilities, and labor. It demands specialized expertise in procurement, quality control, and supply chain management. And it ties up capital that could be deployed in research, design, and marketing—the activities that actually create brand value and intellectual property.

The "make versus buy" decision was tilting hard toward buy. Companies realized they could focus on what they did best—designing products and selling them—while outsourcing the physical assembly to specialists. This was the soil from which the EMS industry grew.

Benchmark's particular origin story begins not in a garage or a dorm room, but inside a medical device company. In 1979, Intermedics, Inc., a Texas-based manufacturer of implantable cardiac pacemakers, created a wholly owned subsidiary called Electronics, Inc. in Clute, Texas, a small Gulf Coast town in Brazoria County.

The subsidiary existed for one purpose: to produce patient monitoring equipment and perform the low-volume, highly complex assembly of electronic components for Intermedics' life-saving devices. This was not commodity work. Assembling electronics for pacemakers demanded precision measured in microns and quality standards measured in lives.

When Intermedics hit financial difficulties in the mid-1980s, the subsidiary's fate hung in the balance. In 1986, the parent company sold ninety percent of Electronics, Inc. to a newly formed investment entity called Electronic Investors Corp., created by three former Intermedics executives who saw opportunity in the outsourcing wave. Donald Nigbor, who became president and CEO, brought operational leadership.

Steven Barton took charge of marketing and sales. And Cary Fu, a CPA with a master's in accounting from the University of Houston who had served as controller at Intermedics, became the financial architect. In 1988, the entities merged to form Benchmark Electronics, Inc.

The timing proved fortuitous. The late 1980s saw the personal computer revolution accelerating, the telecom industry expanding, and an increasing number of OEMs deciding that factory ownership was a distraction from their core business. Benchmark, born from the exacting world of medical device manufacturing, entered this growing market with a built-in advantage: a reputation for quality in the most demanding regulatory environment imaginable. When your first customers' products go inside human bodies, everything else feels a little more manageable.

What made the founding trio effective was the complementarity of their skills. Nigbor was the operational leader—the person who understood factory floors, production schedules, and the mechanics of scaling a manufacturing operation.

Barton was the rainmaker, building customer relationships and evangelizing the outsourcing value proposition to OEMs that were still skeptical about handing over their manufacturing. And Fu was the financial disciplinarian—the CPA who kept the books clean, managed cash flow, and ensured that growth did not outrun the company's balance sheet capacity. This division of labor—operations, sales, and finance—would prove critical in the capital-intensive EMS business where any one of those functions, if poorly managed, could sink the enterprise.

In July 1990, Benchmark made its initial public offering on the American Stock Exchange at $8.75 per share, raising approximately $9 million. At the time, the company reported revenue of just $21.3 million and net income of $2 million. The IPO was a bold move—the United States was sliding into recession—but the capital was essential. EMS is a capital-intensive business: you need factories, equipment, inventory, and working capital to win and fulfill contracts.

The IPO gave Benchmark the financial foundation to participate in what was about to become the greatest growth period in contract manufacturing history. In 1991, the company opened a new manufacturing facility in Beaverton, Oregon, employing approximately two hundred people—its first footprint outside of Texas. By 1994, the company had relocated its headquarters from Clute to nearby Angleton, Texas, and revenue had grown to $98.2 million with over six hundred employees. The trajectory was steep: from $21 million at IPO to nearly $100 million in four years, almost entirely through organic growth and the relentless cultivation of new customer relationships. The question was whether this tiny Texas assembler could scale fast enough to matter in the coming boom.

III. The Golden Age of EMS & Scaling Ambitions (1990s–Early 2000s)

The 1990s were, for the EMS industry, what the California Gold Rush was for the American West. Everyone was rushing in, staking claims, and building as fast as they could. The logic was irresistible: as more OEMs outsourced manufacturing, the EMS companies that could offer the broadest geographic footprint, the fastest turnaround times, and the most competitive prices would capture an ever-growing pie. Companies like Solectron, Flextronics, Jabil Circuit, Sanmina, and Celestica all raised capital and went on acquisition sprees, gobbling up factories and capabilities in a race to achieve scale.

Benchmark, starting from its modest $21 million revenue base in 1990, played this game with calculated aggression. The growth trajectory told the story: revenue hit $98 million by 1994, crossed $200 million in 1996, reached $325 million in 1997 after the company moved its listing to the New York Stock Exchange, and surged past $500 million in 1998. Don Nigbor publicly stated his goal of reaching $1 billion in sales before the new millennium—a nearly fifty-fold increase from where the company stood at IPO.

The engine of this growth was acquisitions. In March 1996, Benchmark acquired EMD Technologies in Winona, Minnesota, for $51 million in cash and stock. The deal nearly doubled the company's volume, adding $160 million in annual sales and nineteen new customers.

More importantly, it expanded Benchmark's design and engineering capabilities beyond pure assembly. In January 1998 came the $70 million cash acquisition of Lockheed Martin's Commercial Electronics division in Hudson, New Hampshire, which gave Benchmark a Northeast manufacturing presence and deepened its aerospace and defense credentials. Then in 1999, a deal that would define the decade: the $289 million acquisition of AVEX Electronics from J.M. Huber Corporation.

The AVEX deal was transformational and traumatic in roughly equal measure. It was, at the time, the largest acquisition in the contract electronics manufacturing sector. In a single stroke, Benchmark nearly tripled its workforce by adding 4,440 employees and gained nine international manufacturing plants spanning Alabama, Tennessee, Hungary, Mexico, Brazil, Ireland, Scotland, Singapore, and Sweden. Benchmark went from being a largely domestic operation to a truly global manufacturer overnight.

But the deal also exposed the risks of acquisition-driven growth. Integration proved rocky, and poor third-quarter 1999 results sent Benchmark's stock plummeting from $35 to $15 per share. Benchmark eventually sued AVEX's former parent, alleging fraud related to false financial statements and undisclosed customer contract losses. The episode was an early lesson in a theme that would recur throughout the company's history: in EMS, the gap between strategic ambition and operational execution can swallow enormous amounts of value.

What made the 1990s EMS boom so seductive—and ultimately so dangerous—was the underlying business economics. Contract manufacturing operated on structurally thin margins, typically three to five percent at the operating level.

This meant that growth was essential not just for ambition but for survival: you needed scale to spread fixed costs, negotiate better component pricing, and win the large contracts that kept your factories running at high utilization. But growth also required constant capital investment in equipment and facilities, and it brought customer concentration risk—losing a single major account could crater your financials overnight.

OEMs understood this dynamic perfectly and exploited it. They demanded lower prices year after year, faster turnaround times, and increasingly global capabilities. If your competitor opened a factory in China, you needed one too. If they offered design services alongside assembly, you had to match. The EMS industry was, in essence, a manufacturing Olympics where the contestants competed on speed, quality, and price simultaneously, with their customers serving as judges who could switch allegiance at any moment.

By 2000, Benchmark had achieved Nigbor's goal, surpassing $1 billion in revenue and reaching $1.7 billion—a staggering eighty-fold increase from the IPO a decade earlier. The company had factories on multiple continents, thousands of employees, and relationships with major OEMs across telecom, computing, and industrial markets. It looked like a triumph.

But beneath the surface, the entire industry was building on a foundation of sand. The dot-com bubble had inflated demand forecasts to fantasy levels. Telecom carriers were ordering equipment based on projections of exponential bandwidth growth that would take a decade to materialize.

Internet startups were buying servers and networking gear with venture capital money that would evaporate. And EMS companies—Benchmark included—had built factory capacity to match these inflated forecasts. The industry was, in effect, constructing a manufacturing base sized for a future that would not arrive on schedule. When the music stopped, the reckoning would be severe—and it would reshape the competitive landscape for a generation.

IV. The Dot-Com Crash & Consolidation Bloodbath (2000–2003)

The year 2001 arrived like a wrecking ball swung at the entire electronics supply chain. The telecom and dot-com bubbles burst almost simultaneously, and the carnage was staggering. Telecom carriers that had been laying fiber-optic cable as if bandwidth demand would grow forever suddenly stopped ordering equipment. Internet companies that had been buying servers by the truckload vanished. The broader semiconductor industry saw revenue plunge thirty-three percent in a single year—the worst decline in its history.

For EMS companies, the pain was acute and structural. They had spent the late 1990s furiously building factories and adding capacity to meet demand that evaporated almost overnight. Benchmark's revenue fell twenty-five percent in 2001, dropping from $1.7 billion to $1.27 billion.

Across the industry, the story was worse. Solectron, which had been the crown jewel of the EMS sector and won the Malcolm Baldrige National Quality Award twice, began a death spiral that would eventually end in its acquisition by Flextronics in 2007. Smaller EMS companies simply disappeared—ACT Manufacturing, IEC Electronics, and others either went bankrupt or were sold for pennies on the dollar.

The mechanics of an EMS downturn are particularly brutal because of the industry's operating leverage characteristics. When your factories are running at high utilization, fixed costs are spread across a large revenue base, and even thin margins produce decent returns. But when utilization drops—when the orders stop coming and the assembly lines slow down—those same fixed costs become an anchor. You are still paying for the building, the equipment, the lease, the insurance, and the skeleton crew needed to maintain operations. Revenue goes away; costs do not.

Benchmark navigated this period better than many peers, but it was far from unscathed. The company took restructuring charges, closed underperforming facilities, and wrote down inventory. The AVEX integration headaches that had plagued the company in 1999 compounded the challenges of the downturn.

Yet Benchmark avoided the fatal mistakes that destroyed others. It did not carry excessive debt—a testament to Cary Fu's financial conservatism and the discipline instilled by the founding team's CPA-led approach to capital management. It had diversified its customer base sufficiently that no single industry's collapse could take it down entirely—telecom was painful, but computing, industrial, and medical customers provided a floor. And its management team, led by the founding trio of Nigbor, Barton, and Fu, maintained financial discipline even when competitors were scrambling.

The contrast with Solectron is instructive. Solectron had been the EMS industry's darling—a company that won the Malcolm Baldrige National Quality Award not once but twice, that was profiled in business school case studies, and that grew to over $18 billion in revenue at its peak. But Solectron had fueled that growth with aggressive acquisitions funded by debt and had concentrated heavily in telecom and computing.

When both sectors collapsed simultaneously, the company's debt load became an anchor. Revenues plummeted, losses mounted, and Solectron spent the next several years in a slow-motion death spiral, eventually selling itself to Flextronics in 2007 for a fraction of its former market capitalization. Benchmark's survival through the same period, while less dramatic, was ultimately more valuable.

Revenue gradually recovered—reaching $1.63 billion in 2002 and $1.83 billion in 2003—but the experience left deep scars and prompted a fundamental rethinking of strategy. The dot-com crash had revealed an uncomfortable truth: competing on volume in commodity electronics manufacturing was a game that Benchmark could not win.

The mega-EMS players—particularly Foxconn's parent Hon Hai Precision Industry in Taiwan—were building manufacturing campuses in China that employed hundreds of thousands of workers at wage rates no American or European competitor could match. Trying to out-scale Foxconn was like trying to outswim a whale. You needed a different ocean.

The post-crash period was also a time of leadership transition. Don Nigbor, who had led Benchmark from a twenty-person operation to a multi-billion-dollar enterprise, stepped aside as CEO in September 2004, remaining as chairman of the board.

His co-founder Cary Fu, the meticulous CPA who had served as the company's financial backbone for nearly two decades, assumed the top role. Fu brought a different temperament to the job—more analytical, more conservative, more focused on margins than on top-line growth. It was precisely the leadership profile that the moment demanded, because the strategic choice Benchmark was about to make would define the company for the next two decades.

The question that Fu and the leadership team wrestled with was existential: What kind of EMS company should Benchmark be? They could continue chasing volume, racing to build factories in low-cost countries, competing for the massive but margin-destroying consumer electronics contracts that defined the industry. Or they could take a fundamentally different path—one that meant deliberately shrinking certain parts of the business to strengthen others. They chose the latter, and it changed everything.

V. The Strategic Pivot: From Commodity to Complexity (2003–2010)

In the history of Benchmark Electronics, no single decision matters more than what happened in the years following the dot-com crash. The company made the deliberate, painful choice to walk away from commodity consumer electronics manufacturing and reposition itself toward higher-value, higher-complexity markets. This was not a press release strategy or a consultant's PowerPoint. It was a fundamental rewiring of the business that meant turning down revenue, closing facilities, and telling customers—paying customers—that Benchmark no longer wanted their business.

To understand why this mattered, think about the difference between assembling a consumer-grade Wi-Fi router and assembling a circuit board for a Class III implantable medical device. The router is a high-volume, low-mix product: you make millions of identical units, the bill of materials is simple, and the customer's primary concern is cost. Any competent factory in Shenzhen can do it.

The medical device, by contrast, is low-volume, high-mix: you might make a few thousand units per year, each with hundreds of unique components, assembled in a cleanroom environment, subject to FDA validation requirements, and traceable down to the individual solder joint. Getting that certification takes years. Maintaining it requires continuous investment in quality systems, training, and documentation. It is a nightmare of complexity—and that complexity is the moat.

Benchmark's leadership recognized that the company's founding DNA—born from pacemaker manufacturing at Intermedics—had always pointed toward this kind of work. The dot-com crash simply forced the reckoning. Under Fu's leadership, the company identified its target verticals: medical technologies, aerospace and defense, semiconductor capital equipment, complex industrials, and selective opportunities in telecom and computing where the work was sufficiently complex to command reasonable margins.

Each of these markets had characteristics that made them attractive to an EMS provider willing to invest in the capabilities to serve them. Medical devices required FDA-compliant manufacturing processes, design history files, and quality management systems that took years to establish and validate.

Aerospace and defense demanded AS9100 quality certifications, ITAR compliance for handling controlled technologies, and security clearances that limited the pool of eligible manufacturers. Semiconductor capital equipment—the machines that make the chips that power everything—required precision machining and cleanroom assembly at tolerances measured in microns.

The pivot was reinforced by a major acquisition in January 2007: the stock-for-stock merger with Pemstar, Inc. Pemstar, founded in 1994, brought roughly $871 million in revenue, 3,500 employees, and eleven design and manufacturing locations worldwide, including a facility in Penang, Malaysia.

The deal approximately doubled Benchmark's workforce to around 10,000 employees and significantly expanded capabilities in medical, industrial, and data storage markets. Critically, Pemstar brought engineering and design talent—not just assembly capacity—which aligned with Benchmark's evolving strategy of becoming more than a "build to print" manufacturer.

The Pemstar acquisition also illustrated the type of deal-making that characterized this era of Benchmark's evolution. Rather than acquiring raw manufacturing capacity—more square footage, more assembly lines, more labor—the company was buying capabilities. Pemstar's strength in engineering services, product fulfillment, and supply chain management complemented Benchmark's assembly expertise. The deal structure—a tax-free stock-for-stock merger—also reflected financial discipline, avoiding the debt that had sunk other EMS acquirers during the dot-com bust.

Simultaneously, Benchmark began building its Precision Technologies capabilities—a business unit focused on precision machining, tooling, and cleanroom manufacturing for semiconductor capital equipment. In 2010, the company acquired facilities and assets in Malaysia and Singapore specifically to expand this capability.

Precision Technologies represented a fundamentally different kind of manufacturing than PCB assembly. Instead of soldering components onto circuit boards, this work involved machining metal parts to tolerances measured in microns—the kind of work required for the vacuum chambers, gas delivery systems, and wafer-handling equipment used in semiconductor fabrication. This capability would become one of Benchmark's most important differentiators in the years ahead, as the global demand for semiconductor manufacturing equipment exploded.

The financial profile of this transformation told an important story. Revenue, which had peaked at $2.91 billion in 2007, declined during the Great Recession to $2.08 billion in 2009 before recovering to $2.4 billion in 2010.

The top-line trajectory was volatile, but the mix was shifting. A growing percentage of revenue came from higher-margin, more defensible market segments. The company was trading some growth for resilience—accepting that it would never be the biggest EMS provider in exchange for being positioned in markets where customer relationships were stickier and pricing pressure was less extreme.

The China question loomed large during this period. Every EMS competitor was expanding aggressively in China to capture the cost advantages of lower labor rates and proximity to Asian component supply chains.

Benchmark opened a facility in Suzhou, China, in 2002, but it approached China as one element of a diversified geographic strategy rather than as the centerpiece. The company's thinking was that many of its target customers—particularly in aerospace, defense, and medical—either required or strongly preferred domestic U.S. manufacturing for regulatory, security, or intellectual property reasons. This bet on a balanced, "right-shored" footprint rather than an all-in China strategy would prove prescient years later when geopolitical tensions and supply chain disruptions made heavy China dependence a liability.

For investors studying Benchmark today, the 2003–2010 pivot is the single most important piece of historical context. Every strategic decision the company has made since—every facility opened, every acquisition completed, every customer pursued—flows from the choice made in those post-crash years to compete on complexity rather than cost. The question is whether that positioning provides sufficient differentiation to sustain an independent company in an industry that relentlessly pressures margins.

VI. The Near-Death Experience & CEO Transition (2010–2016)

Just when it seemed like Benchmark had found its strategic footing, the company walked into a buzzsaw. The period from 2011 to 2016 was arguably the most turbulent stretch in the company's history—a combination of natural disaster, customer concentration blowups, operational stumbles, and leadership upheaval that tested whether the strategic pivot of the prior decade would hold.

The trouble started with literal floodwaters. In late 2011, severe flooding in Thailand damaged Benchmark's manufacturing operations in the country, disrupting production and creating uncertainty about the company's ability to maintain adequate insurance coverage for those assets. The timing was terrible.

Cary Fu, who had led the company through the financial crisis and the strategic repositioning, announced his retirement effective December 31, 2011. He handed the reins to Gayla Delly, a Benchmark lifer who had joined in 1995 as corporate controller and risen through the ranks to become CFO and then president. Fu himself acknowledged that Delly was taking on leadership "in the midst of our recovery from the unprecedented flooding in Thailand."

Delly became the first woman to lead Benchmark, and she inherited a company under stress. Revenue was essentially flat—hovering between $2.25 billion and $2.5 billion from 2011 through 2013—during a period when parts of the EMS industry were growing.

The telecom sector, historically one of Benchmark's larger verticals, was undergoing wrenching transitions as Nokia's handset business collapsed and Motorola's mobile division changed hands. Customers in these segments were restructuring their own supply chains, and the resulting program losses rippled through Benchmark's revenue base. This was the customer concentration problem manifesting in real time: when a major telecom customer restructures, the EMS provider that built their equipment takes the hit directly.

Delly's background was deeply operational. She had spent nearly two decades inside Benchmark, starting as corporate controller in 1995, rising to chief financial officer in 2001, and then to president before her elevation to CEO.

She knew the company's finances intimately—every facility's contribution margin, every customer's profitability profile, every line item in the capital expenditure budget. This financial fluency was both her strength and, arguably, her limitation. The company needed operational turnaround and bold strategic repositioning, and the board ultimately concluded that fresh external perspective was required.

The company pursued acquisitions during this period—absorbing Suntron Corporation for $18.5 million in June 2013 and acquiring the EMS segment of CTS Corporation the same year—but these deals added complexity during a time when the core business was struggling to find its footing. Revenue peaked at $2.79 billion in 2014 but then declined to $2.54 billion in 2015 and $2.31 billion in 2016, a trajectory that reflected both market headwinds and internal execution challenges.

The board eventually made a decisive move. In September 2016, Paul Tufano was appointed president and CEO, replacing Delly effective immediately. Tufano was an outsider—the first non-Benchmark-lifer to lead the company. His background was in telecommunications: he had spent over thirty-five years in the industry, most recently serving as CFO and then COO of Alcatel-Lucent, the Franco-American telecom equipment giant. Tufano brought a global perspective, financial rigor, and a willingness to challenge assumptions that had calcified during years of incremental decision-making.

His first move was symbolic but significant. Tufano visited every Benchmark site globally, meeting with employees and customers to understand the company's capabilities and pain points firsthand.

What he found was a company that had the right strategic vision—the complexity-focused, higher-value-market positioning was sound—but lacked the execution discipline to fully deliver on it. The go-to-market approach was too passive, the operational systems were inconsistent across sites, and the company's headquarters in Angleton, Texas—a small Gulf Coast town far from any major technology ecosystem—made it difficult to recruit the executive talent needed for transformation.

Tufano announced in April 2017 that Benchmark would relocate its headquarters to Tempe, Arizona, placing it in the Phoenix metropolitan area's growing technology corridor. The move was both practical and symbolic: a signal that Benchmark was shedding its small-town origins and positioning itself as a modern technology solutions company, not just a contract assembler.

Delly, for her part, went on to serve on the boards of Broadcom, Flowserve, and National Instruments—evidence that her capabilities were recognized even if the Benchmark tenure had been turbulent. The lesson of this period was painfully clear: in EMS, even a sound strategy can be undone by operational inconsistency, customer concentration, and external shocks. The question for Tufano was whether he could take the strategic framework his predecessors had built and add the execution discipline it needed.

VII. The Tufano Era and the Benck Transition: Transformation & Repositioning (2016–2020)

Paul Tufano's tenure at Benchmark was relatively brief—roughly two and a half years—but it laid the groundwork for the transformation that continues to define the company today. He approached the job like a surgeon: diagnose the problems, develop a treatment plan, and begin cutting.

His diagnosis centered on three interconnected issues. First, Benchmark's operational execution was inconsistent. Quality systems, manufacturing processes, and customer engagement varied too widely from site to site. A medical device customer working with the Winona, Minnesota, facility might have a fundamentally different experience than one working with the Penang, Malaysia, operation.

In a business where reputation and reliability are everything, this inconsistency was corrosive. Second, the company's go-to-market approach was too transactional. Sales teams were quoting jobs and competing on price rather than building deep, consultative relationships where Benchmark's engineering expertise could command a premium. Third, the "higher value markets" strategy that had been articulated since the mid-2000s needed sharper definition and more aggressive investment.

Tufano's response organized around three pillars. Operational excellence meant implementing consistent lean manufacturing practices, Six Sigma quality methodologies, and standardized processes across all sites.

Market focus meant doubling down on the sectors where Benchmark had genuine competitive advantages—medical, aerospace and defense, semiconductor capital equipment, and advanced industrials—while continuing to de-emphasize commodity work. Engineering-led selling meant transforming the sales force from order-takers into consultants who could engage with customers early in the product development cycle, offering design for manufacturability advice, new product introduction services, and testing capabilities that justified higher margins.

The concept of "new product introduction"—NPI—deserves explanation because it is central to how companies like Benchmark create stickiness with customers. When an OEM designs a new product, there is a critical phase between the prototype and full-scale production where the design must be translated into a manufacturable product.

This involves optimizing the design for the realities of factory floor assembly, selecting components that are available and cost-effective at scale, building and testing pilot runs, and establishing the quality processes that will govern production. An EMS provider that participates in this NPI phase becomes deeply embedded in the customer's product—understanding the design intent, the critical quality parameters, and the supply chain requirements in ways that make switching to another manufacturer genuinely disruptive and risky. This is where the real switching costs in EMS are created—not in the assembly itself, which is ultimately a commodity, but in the engineering knowledge and process validation that surrounds it.

Tufano also made a move that reshaped the company's identity. By announcing the headquarters relocation to Tempe, Arizona, he signaled that Benchmark was no longer the small-town Texas assembler of its founding myth. The Phoenix metro area offered proximity to a growing semiconductor and technology ecosystem, better access to executive talent, and a geographic position that facilitated connections to the company's Mexican manufacturing operations.

Revenue during Tufano's tenure grew modestly—from $2.31 billion in 2016 to $2.56 billion in 2018—but the real progress was in the quality of the business rather than its size. Margin improvement, customer mix optimization, and operational standardization were slow-burn initiatives that would take years to fully materialize in the financial results.

Tufano announced his planned retirement in late 2018 and stepped down in March 2019. His successor, Jeff Benck, took the helm on March 18, 2019.

Benck brought a different but complementary background. He held an engineering degree from the Rochester Institute of Technology and a master's in management of technology from the University of Miami. His career had spanned eighteen years at IBM in various executive roles, followed by leadership positions at QLogic, Emulex (where he served as CEO until its acquisition by Avago Technologies), and Lantronix, where he more than doubled profitability and tripled market capitalization, earning recognition as "IoT CEO of the Year."

Where Tufano had been the diagnostician and architect, Benck became the builder.

He completed the headquarters move to Tempe, opened a new manufacturing facility in Phoenix in 2020, and would later oversee the construction of a state-of-the-art cleanroom facility in Mesa, Arizona, specifically designed for precision technologies work in the semiconductor capital equipment space. Benck continued and sharpened the strategic framework Tufano had established, pushing the company toward what he described as a transformation from a traditional EMS provider into a "technology and engineering solutions partner."

The rebranding was more than cosmetic. It reflected a genuine evolution in what Benchmark offered its customers. The company was no longer simply saying "give us your designs and we'll assemble them." It was saying "engage us early, let us help you design for manufacturability, let us manage your supply chain, let us handle the regulatory compliance, and let us be a partner through the entire product lifecycle." Whether the market would reward this positioning with sustainably higher margins was the multi-billion-dollar question—and the jury, as of 2019, was still very much out.

What Benck brought that his predecessors had not was a technology industry perspective rather than a pure manufacturing mindset. His years at IBM, QLogic, and Emulex had given him firsthand experience as the customer in an EMS relationship.

He understood what OEMs valued in their manufacturing partners—not just cost and quality, which were table stakes, but responsiveness, engineering insight, and the ability to solve problems proactively rather than waiting to be told what to build. This customer empathy informed his push to transform Benchmark's culture from reactive order fulfillment to proactive partnership.

The financial results during the pre-COVID Benck period showed the beginning of this transformation. Revenue in 2019 came in at $2.26 billion—lower than the prior year, partly reflecting the deliberate exit from lower-margin business—but the margin profile was improving.

The company was getting more profitable per dollar of revenue even as the top line compressed. For investors accustomed to evaluating manufacturing companies on revenue growth, this was a difficult narrative to embrace. But for those who understood the EMS industry's economics, margin improvement on a more defensible revenue base was arguably more valuable than top-line growth built on commodity business that could disappear at any time.

VIII. Recent Inflection Points & Modern Challenges (2020–Present)

When COVID-19 shut down factories and scrambled supply chains in early 2020, the pandemic did not treat all of Benchmark's end markets equally. Medical device demand surged as hospitals raced to acquire ventilators, patient monitors, and diagnostic equipment.

Aerospace, by contrast, collapsed as airlines grounded fleets and defense programs faced budget uncertainty. Semiconductor capital equipment orders initially softened before roaring back as the chip shortage exposed the world's desperate need for more fabrication capacity. The net effect on Benchmark's 2020 results was a revenue decline to $2.05 billion—a nine percent drop—but the underlying dynamics were far more complex than the headline number suggested.

What the pandemic really did was validate Benchmark's strategic positioning in two important ways. First, the company's diversified end-market exposure meant that strength in medical partially offset weakness in aerospace, preventing the kind of catastrophic revenue collapse that a more concentrated business would have suffered.

Second, the reshoring and nearshoring conversation that had been largely theoretical for years suddenly became urgent. Companies that had concentrated their supply chains in China discovered the fragility of that dependence when factories shut down, ports backed up, and geopolitical tensions escalated. Benchmark's substantial North American manufacturing footprint—with facilities across the United States and Mexico—became a genuine competitive advantage rather than a cost liability.

The semiconductor shortage of 2021-2022 presented its own challenges and opportunities. To understand why chip shortages hit EMS companies so hard, consider the mechanics. An EMS provider might need two hundred different components to assemble a single circuit board.

If one hundred and ninety-nine are available but the two hundredth—a specific microcontroller or power management chip—is backordered for six months, the entire board cannot be built. The finished board sits incomplete on the factory floor, the customer's product launch is delayed, and the EMS provider's revenue recognition is pushed out. Now multiply that scenario across hundreds of different products and thousands of different components, and you begin to appreciate the operational nightmare.

EMS companies that could manage their component supply chains effectively—securing allocations through strong supplier relationships, managing inventory buffers without over-committing capital, communicating transparently with customers about lead times and priorities—strengthened their customer relationships during this period. Those that couldn't lost business and credibility. Revenue recovered to $2.25 billion in 2021 and then surged to $2.88 billion in 2022, driven by strong demand across semiconductor capital equipment, aerospace recovery, and the broader industrial economy.

Jeff Benck continued to execute on the transformation playbook throughout this period, making strategic investments in manufacturing capacity. The company opened a new facility in Almelo, Netherlands, in 2023 to serve European customers.

A cleanroom facility in Mesa, Arizona, designed for precision technologies work—the kind of ultra-precise machining and assembly required for semiconductor fabrication equipment—also opened in 2023. Expansions followed in Penang, Malaysia, and Brasov, Romania, in 2024, and a major 321,000-square-foot advanced manufacturing facility opened in Guadalajara, Mexico, in 2025, strengthening the nearshoring position.

A notable leadership change occurred in early 2024 when CFO Roop Lakkaraju, who had served since January 2018, departed to pursue another opportunity. Arvind Kamal, the company's vice president of finance, stepped in as interim CFO. The departure of a sitting CFO always raises eyebrows, but the company reiterated its quarterly guidance and the transition appeared orderly.

By fiscal year 2025, the financial profile of Benchmark had evolved meaningfully. Revenue came in at $2.66 billion—essentially flat with the prior year—but the margin story was more encouraging. Non-GAAP operating margin reached 5.5 percent in the fourth quarter, up seventy basis points sequentially, and the full year generated $85 million in free cash flow. The company's fourth-quarter results beat analyst expectations on both revenue and earnings, with non-GAAP earnings per share of $0.71 representing a sixteen percent year-over-year increase.

The segment mix told the story of the strategic pivot's progress. Semiconductor capital equipment represented the largest segment at roughly thirty percent of revenue. Aerospace and defense led annual growth at nineteen percent year-over-year. Medical grew seven percent. Advanced computing and communications, while down twenty-seven percent for the full year, showed strong sequential recovery in the fourth quarter. The revenue composition looked fundamentally different from the telecom-and-computing-heavy mix of two decades earlier.

Then, in late 2025, came the announcement that Jeff Benck would retire as CEO effective March 31, 2026, concluding a seven-year tenure.

His successor, David Moezidis—a thirty-five-year industry veteran who had spent twenty-five years at Flex before joining Benchmark as chief commercial officer in 2023—was named president and will assume the CEO role upon Benck's departure. The transition represents continuity: Moezidis was deeply involved in developing the commercial strategy that Benck championed, and his background at Flex, one of Benchmark's larger competitors, gives him an intimate understanding of the competitive landscape.

For investors watching Benchmark today, the company sits at an interesting juncture. The margin expansion story is real—operating margins have improved from the low-four-percent range to the mid-five-percent range over several years. The end-market mix is higher quality.

The geographic footprint is well-positioned for the reshoring trend. But revenue remains stubbornly in the $2.5-to-$2.9-billion range where it has been, with minor exceptions, for nearly two decades. The question is whether the coming AI infrastructure buildout, the electrification wave, and the continued reshoring of critical manufacturing will provide the growth catalyst that has eluded the company—or whether Benchmark is destined to be a margin improvement story without the top-line growth to truly excite the market.

IX. The Industry Dynamics: Why EMS Is So Brutal

To fully appreciate Benchmark's position, you need to understand why the electronics manufacturing services industry is one of the most structurally challenging businesses in the global economy. It is a business where enormous companies generate billions in revenue and employ tens of thousands of people, yet consistently earn net profit margins that would make a lemonade stand operator wince.

The fundamental issue is the power dynamic between EMS providers and their customers. OEMs hold almost all the cards. They own the product designs, the brand names, the customer relationships, and the intellectual property. The EMS provider owns a factory, some equipment, and expertise in manufacturing processes—all of which are, to varying degrees, replicable. When an OEM hands a contract to an EMS company, it is essentially saying: "We trust you to build our product, but we could take this work to your competitor next quarter if you don't meet our price, quality, and delivery requirements."

This dynamic creates relentless pricing pressure. OEMs typically negotiate annual cost reductions into their contracts—demanding two to five percent price decreases each year. The EMS provider must find ways to reduce costs through process improvements, automation, component cost negotiations, and labor efficiency just to maintain margins, let alone improve them. It is a treadmill that never stops.

The result is an industry where operating margins typically hover between three and five percent, and net margins are often in the low single digits. Compare this to the software industry, where operating margins of thirty to forty percent are common, or even to the semiconductor industry, where leading companies like NVIDIA or TSMC earn operating margins above forty percent. EMS companies take on the capital intensity and operational complexity of manufacturing without capturing the value creation that comes from owning the design or the brand.

Here is a useful way to think about it: an EMS company is essentially a very expensive, very specialized service business. It provides a service—manufacturing—that its customers could theoretically do themselves but choose to outsource for economic reasons. Unlike a software company, which creates a product once and sells it millions of times at near-zero marginal cost, an EMS company must physically build each unit, investing labor, materials, and machine time every single time.

Unlike a brand-name consumer electronics company, which captures the premium that consumers pay for design, innovation, and marketing, the EMS provider's contribution is invisible to the end user. Nobody buys a medical device because Benchmark assembled it. They buy it because of the OEM's brand, the surgeon's recommendation, or the hospital's purchasing contract. The EMS provider captures none of that end-market value—only the thin manufacturing margin that the OEM is willing to share.

The competitive landscape reinforces these dynamics. At the top sits Foxconn, the Taiwanese giant controlled by Terry Gou, with over $200 billion in annual revenue and more than a million employees. Foxconn's scale is so massive that it operates in a different competitive universe—it assembles a significant portion of the world's iPhones and has purchasing power that no competitor can match.

Below Foxconn, Jabil and Flex each generate roughly $25-30 billion in revenue with hundreds of thousands of employees. Celestica and Sanmina operate in the $7-8 billion range. And then there is Benchmark, at $2.7 billion, along with its closest peer Plexus at roughly $4 billion, occupying what might be called the "specialty mid-tier."

Think of it as a marketplace with a few superstores, several department stores, and a handful of boutiques. Foxconn is the Walmart—impossible to beat on price and scale. Jabil and Flex are the Target and Costco equivalents—large, diversified, and capable.

Benchmark and Plexus are the specialty retailers—smaller, focused on specific categories where their expertise justifies a (slightly) higher price point. The danger for the boutiques is that the department stores can always decide to enter their niche, bringing superior resources to bear. The opportunity is that the superstores and department stores often find the low-volume, high-complexity work too fiddly and unprofitable to bother with.

The moats in EMS, to the extent they exist, are subtle and fragile. Customer switching costs are real but not prohibitive—they come primarily from the time and cost of qualifying a new manufacturer, particularly in regulated industries where FDA or defense agency approvals are required. Engineering relationships create stickiness, especially when an EMS provider is involved in the new product introduction process and accumulates design knowledge that would take months for a competitor to replicate. Regulatory qualifications in medical and aerospace create barriers that take years to build.

But none of these moats are permanent. Customers do switch. Competitors do invest in capabilities. Regulatory certifications can be obtained with sufficient time and money.

Technology trends are reshaping the landscape in ways that could either help or hurt mid-tier players like Benchmark. Automation and Industry 4.0 technologies—smart factories, AI-driven quality inspection, digital twins—can help smaller manufacturers close the productivity gap with larger competitors.

The growing complexity of electronics—driven by miniaturization, AI hardware, and advanced packaging—favors manufacturers with deep engineering capabilities over those that compete purely on assembly labor costs. But these same trends also require significant capital investment, creating a Darwinian dynamic where companies that cannot invest fast enough fall further behind.

X. Playbook: Business & Strategic Lessons

Benchmark's four-decade journey through one of the world's most unforgiving industries offers a set of strategic lessons that extend well beyond contract manufacturing. These are lessons about competitive positioning, capital allocation, and the art of surviving in a commodity business—themes that resonate with operators and investors across industries.

The first and most fundamental lesson is that in commodity businesses, strategic positioning is existential. You cannot out-scale the scale leader.

Foxconn's cost advantages come from a manufacturing workforce larger than the population of many countries, purchasing power that commands preferential pricing from every component supplier on earth, and factories operating at a scale that amortizes fixed costs to near zero on a per-unit basis. For Benchmark to have tried to compete on those terms would have been suicide. The decision to reposition toward complex, regulated, low-volume markets was not merely a strategic preference—it was the only viable path to survival.

The second lesson is that customer concentration is the silent killer in business-to-business companies. Benchmark has been burned by this repeatedly—from the telecom customer losses of the early 2010s to the ongoing reality that its top ten customers still represent a significant majority of revenue and its largest single customer accounts for roughly twenty percent.

In EMS, the loss of a single major customer can turn a profitable year into a loss. The company's ongoing effort to diversify its customer base and win new strategic accounts is not a growth initiative—it is a risk management imperative.

Third, operational excellence is table stakes, not a competitive advantage. Every EMS company claims to be operationally excellent. Every investor presentation features slides about lean manufacturing, quality metrics, and on-time delivery rates. The real differentiation comes from engineering relationships—from being so deeply embedded in a customer's product development process that switching manufacturers becomes genuinely risky and disruptive. This is why Benchmark's push into NPI services and design collaboration matters more than any factory efficiency metric.

Fourth, capital allocation in capital-intensive businesses requires iron discipline. The temptation to chase revenue by building factories and adding capacity is strong, particularly when customers are dangling large contracts. But in an industry where margins are three to five percent, every dollar of misallocated capital directly destroys returns. The shift toward return on invested capital as a primary financial metric—rather than revenue growth—represents a maturation in how Benchmark thinks about value creation.

Fifth, sometimes survival means shrinking smart rather than growing dumb. Benchmark's willingness to walk away from commodity business, close underperforming facilities, and accept lower revenue in exchange for better margins was counterintuitive in an industry obsessed with scale. But it worked. The company exists today as an independent entity precisely because it did not try to grow its way through every downturn.

Sixth, in manufacturing, culture and execution trump strategy every day of the week. The best strategic plan in the world is worthless if the factory floor cannot execute. Quality escapes, missed deliveries, and cost overruns do not care about your investor presentation. Benchmark's recurring operational challenges—from the AVEX integration difficulties to the Thailand floods to the execution stumbles of the early 2010s—demonstrate that sustained manufacturing excellence is harder than it looks and requires constant vigilance.

Finally, every company in a supply chain faces the same choice: move up the value chain or get commoditized. In manufacturing, the value migration runs from pure assembly toward engineering, design, testing, and supply chain management. Benchmark's evolution from "we assemble your PCBs" to "we partner with you from design through production and lifecycle management" follows this migration. The companies that fail to make this journey end up competing solely on price—a game that, in global manufacturing, only the lowest-cost producer can win.

There is a useful analogy from the legal industry. Law firms that handle commodity work—simple contracts, routine filings, basic compliance—face relentless price pressure from lower-cost competitors and increasingly from software automation.

Law firms that handle complex, high-stakes litigation or transformational M&A transactions command premium rates because the switching costs are high, the expertise is rare, and the consequences of choosing the wrong provider are severe. Benchmark's strategic journey from commodity electronics assembly to complex, regulated manufacturing mirrors exactly this dynamic. The company has spent two decades trying to become the white-shoe law firm of EMS—the provider you choose when the work is too complex, too regulated, or too mission-critical to risk with a less capable alternative.

XI. Analysis: Porter's Five Forces & Hamilton's Seven Powers

Stepping back from Benchmark's specific story, the frameworks of competitive strategy illuminate why this business is so structurally challenging—and where, if anywhere, durable competitive advantages might exist.

Starting with Michael Porter's Five Forces framework, the threat of new entrants into Benchmark's target markets is moderate to low. Building a contract electronics manufacturing operation capable of serving medical, aerospace, and semiconductor capital equipment customers requires tens of millions in capital investment, years of regulatory qualification, specialized engineering talent, and a track record that customers can trust with mission-critical products.

Nobody walks into this business on a whim. However, in the commodity segments that Benchmark has deliberately exited, new entrants from low-cost regions appear constantly, which is precisely why the company left those markets.

Supplier bargaining power is moderate and cyclical. In normal times, EMS companies aggregate component demand across multiple customers, giving them reasonable leverage with semiconductor manufacturers and other suppliers.

But during shortage periods—like the 2021-2022 chip crisis—the power dynamic inverts dramatically. Suppliers allocate scarce components, and EMS companies scramble to secure parts, sometimes paying premium prices or accepting extended lead times that disrupt their own production schedules. The ability to manage supplier relationships through both abundance and scarcity is a genuine differentiator.

Buyer bargaining power is the dominant force in this industry—and it is extremely high. OEMs can and do switch EMS providers. They benchmark pricing continuously. They use the threat of insourcing or competitor bids to extract cost reductions. And the concentration of Benchmark's revenue among a relatively small number of large customers amplifies this power. When a single customer represents twenty percent of your revenue, that customer knows it has leverage—and it uses it.

The threat of substitutes—primarily OEMs bringing manufacturing back in-house—is moderate. The long-term trend over the past three decades has been decisively toward outsourcing, as OEMs recognized that manufacturing is a scale business that benefits from specialization. But the trend is not irreversible. Apple's increasing investment in its own manufacturing capabilities, and the broader trend of companies seeking more control over their supply chains post-COVID, suggest that selective insourcing is possible, particularly for the highest-value or most strategically sensitive products.

Competitive rivalry is very high, arguably the most intense of any of the five forces. The EMS industry remains fragmented below the top tier, with dozens of competitors vying for contracts on the basis of price, quality, speed, and geographic presence. Differentiation is difficult and temporary—any process improvement or capability investment can eventually be replicated by competitors. The result is constant price competition in commodity segments and margin pressure even in specialty niches.

Turning to Hamilton Helmer's Seven Powers framework—which focuses specifically on the sources of durable competitive advantage—the picture for Benchmark is candid and sobering. Scale economies are weak for Benchmark specifically because competitors like Foxconn, Jabil, and Flex operate at multiples of its size, capturing purchasing leverage and fixed-cost absorption that Benchmark cannot match. Network effects are not applicable in a manufacturing business.

Counter-positioning—the idea that a company's strategy is one that competitors cannot copy without damaging their existing business—has some moderate applicability. Benchmark's focus on low-volume, high-complexity work is unattractive to mega-EMS providers because it requires different operational approaches, smaller run sizes, and deeper engineering investment per customer. But this protection is imperfect: if the economics of specialty manufacturing improve sufficiently, larger competitors can and will enter these segments.

Switching costs are moderate and represent perhaps Benchmark's most meaningful source of competitive advantage. In medical device manufacturing, for example, changing an EMS provider requires revalidating the manufacturing process with the FDA—a time-consuming and expensive undertaking that most OEMs prefer to avoid.

Engineering integration and NPI collaboration build institutional knowledge that creates friction against switching. But these costs are not insurmountable. Customers do move programs between manufacturers, and the switching costs are measured in months and hundreds of thousands of dollars, not in years and millions.

Branding power is weak in a business-to-business context where customers evaluate providers based on capabilities, price, and execution rather than brand perception. Process power—the advantage that comes from organizational processes that are difficult for competitors to replicate—is moderate.

Benchmark's quality systems, engineering workflows, and customer engagement processes create real operational advantages, but manufacturing process improvements can be studied and copied over time. Cornered resources are essentially nonexistent: Benchmark owns no significant proprietary technology or patents, and its manufacturing expertise, while valuable, is not unique.

The synthesis of these frameworks points to an uncomfortable but honest conclusion: Benchmark operates in a business with weak structural power. There are no strong, durable moats of the kind that make investors in companies like TSMC or Microsoft sleep soundly.

The company's strategy is best understood as survival through continuous execution and strategic positioning—carving out a defensible niche, serving it well, and hoping that the combination of regulatory barriers, engineering relationships, and operational excellence creates enough friction to maintain customer loyalty. This is a "show me" story that must be proven quarter by quarter, year by year.

The closest peer comparison is Plexus, a roughly $4 billion EMS company based in Wisconsin that pursues a remarkably similar strategy—high-mix, low-to-medium volume manufacturing focused on healthcare, aerospace and defense, and industrial markets. Plexus has achieved slightly higher margins than Benchmark historically, partly through stricter customer selectivity and a stronger engineering services culture.

Celestica, at roughly $8 billion in revenue, occupies a middle ground between the mega-EMS players and the specialty providers, with significant exposure to high-performance computing and AI infrastructure that has driven strong recent performance. The competitive positioning among these mid-tier players is fluid—each is trying to differentiate within a narrow band of strategic space while avoiding direct competition with the scale-driven mega-EMS providers above them.

What is ultimately clear is that there is no permanent competitive advantage in EMS. There are only temporary advantages that must be continuously earned and defended. Benchmark's bet is that the accumulation of small advantages—regulatory certifications, engineering relationships, precision manufacturing capabilities, geographic positioning—creates a composite moat that, while not individually impregnable, collectively provides sufficient customer stickiness to sustain the business. Whether that bet pays off depends entirely on execution.

XII. Bear vs. Bull Case

Every investment thesis is ultimately a bet on which narrative will prove correct. For Benchmark Electronics, the bear and bull cases are sharply defined and genuinely in tension.

The bear case begins with the structural economics of the business. EMS is a low-margin, capital-intensive industry where the best operators in the world struggle to consistently earn mid-single-digit operating margins.

Benchmark's non-GAAP operating margin of 5.5 percent in Q4 2025, while representing meaningful improvement, is still thin enough that a single bad quarter—a major customer loss, a supply chain disruption, an inventory writedown—can erase a year's worth of progress. The business generates returns on invested capital that, while improving, rarely exceed the cost of capital by a wide margin.

Customer concentration remains a structural vulnerability. Benchmark has acknowledged that its largest single customer represents approximately twenty percent of revenue, and the top ten customers account for a dominant share. The company has set a strategic goal to reduce the largest customer below fifteen percent, but this is a slow process that requires winning substantial new business to dilute the concentration. In the meantime, the loss of any top-five customer would be severely damaging.

The competitive moats, as the Seven Powers analysis demonstrated, are weak. Customers can and do switch EMS providers. Regulatory switching costs in medical and aerospace create friction but not impossibility. Engineering relationships are valuable but decay when key personnel change. The "value-add" narrative that Benchmark champions—the idea that it competes on engineering capability rather than price—is the same claim that virtually every EMS company makes in its investor presentations. Separating genuine differentiation from marketing is difficult from the outside.

The bull case, however, has strengthened considerably in recent years. The strategic transformation that began in the mid-2000s and accelerated under successive CEOs has genuinely changed the quality of Benchmark's business.

Operating margins have expanded from the low-four-percent range to the mid-five-percent range, and the trajectory is positive. The company's end-market mix—weighted toward semiconductor capital equipment, aerospace and defense, medical, and complex industrials—provides exposure to secular growth themes including AI infrastructure, defense modernization, aging demographics, and industrial automation.

The reshoring and nearshoring wave is perhaps Benchmark's single strongest near-term tailwind. The company maintains one of the largest U.S.-based electronics manufacturing footprints in the EMS industry, which is critical for ITAR-controlled defense programs and increasingly attractive to OEMs seeking to reduce dependence on Asian supply chains. The 2025 opening of the Guadalajara facility strengthens the nearshoring position further. In a world where "made in America" and "made near America" carry increasing strategic and political value, Benchmark's geographic footprint is an asset.

The engineering capabilities that the company has built—particularly in precision technologies for semiconductor capital equipment, cleanroom manufacturing, and new product introduction—create switching costs that, while not impregnable, are real and meaningful. A medical device customer that has spent eighteen months qualifying Benchmark as a manufacturing partner is not going to switch to a competitor to save two percent on unit costs.

On a valuation basis, Benchmark trades at relatively modest multiples despite the margin improvement story. The company generated $85 million in free cash flow in fiscal 2025 against a market capitalization of roughly $2 billion, implying a free cash flow yield that is attractive if the margin trajectory continues.

The KPIs that matter most for tracking Benchmark's ongoing performance distill to two essential metrics. The first is non-GAAP operating margin, which is the clearest measure of whether the strategic transformation is translating into better economics.

Sustained performance above five percent would validate the higher-value-market positioning; a regression toward four percent would signal that the structural forces of the industry are overwhelming the strategic efforts. Think of this metric as the vital sign of the entire strategic thesis—if the pivot to complexity is working, it should show up here, consistently, through economic cycles.

The second is revenue mix by sector—specifically, the percentage of revenue coming from semiconductor capital equipment, aerospace and defense, and medical.

Progress in these target verticals, measured as a growing share of total revenue, indicates that the company is winning in its chosen markets and reducing dependence on more cyclical or commodity segments. If the company achieves its stated goal of reducing its largest single customer to below fifteen percent of revenue while growing the target verticals, that would represent the most tangible evidence yet that the two-decade strategic repositioning has created a genuinely different and more resilient business.

A related but secondary metric worth monitoring is free cash flow conversion—the company's ability to translate operating earnings into actual cash. In a capital-intensive business like EMS, where working capital requirements can swing dramatically with customer demand and component availability, cash generation discipline separates the survivors from the casualties.

XIII. Epilogue: What's Next for Benchmark?

As David Moezidis prepares to assume the CEO role on March 31, 2026, Benchmark Electronics faces a strategic landscape shaped by forces that could make or break a mid-sized contract manufacturer.

The artificial intelligence infrastructure buildout represents the most significant near-term opportunity. The global race to build AI data centers, manufacture AI training and inference hardware, and produce the semiconductor capital equipment needed to fabricate advanced AI chips is driving enormous demand for complex electronics manufacturing.

Benchmark's precision technologies capabilities—cleanroom assembly, precision machining at micron-level tolerances, and experience with semiconductor equipment OEMs—position it to capture a share of this wave. The question is whether the company can grow its semi-cap business fast enough to offset the inherent cyclicality of the semiconductor equipment market, which has historically swung between feast and famine with bruising regularity.

Electrification and the energy transition are creating entirely new product categories that require sophisticated electronics manufacturing—from power conversion equipment for electric vehicle charging networks to control systems for renewable energy installations to battery management systems for grid-scale storage. These are precisely the kind of complex, regulated, moderate-volume products that fit Benchmark's sweet spot.

Medical device innovation, driven by aging demographics in developed markets and the proliferation of connected health devices, continues to offer growth potential for manufacturers with FDA-compliant operations. The trend toward personalized medicine and point-of-care diagnostics is creating demand for smaller, more complex medical devices that require the kind of high-mix, low-volume manufacturing capabilities that Benchmark has cultivated.

Geopolitical supply chain reconfiguration may be the most consequential macro trend for Benchmark over the next decade. The decoupling of U.S. and Chinese technology supply chains, the passage of legislation like the CHIPS Act incentivizing domestic semiconductor manufacturing, and the broader diversification of manufacturing away from China all favor companies with established North American and European manufacturing footprints. Benchmark's facilities in the United States, Mexico, the Netherlands, and Romania position it well for customers seeking "friend-shoring" alternatives.

The M&A question looms. Benchmark could be an acquirer—buying engineering capabilities or entering adjacent markets to deepen its competitive position. It could also be an acquisition target: private equity firms have historically found EMS companies attractive for their stable cash flows and margin improvement potential, and a strategic acquirer seeking to bolster its North American manufacturing capabilities might find Benchmark's footprint and customer relationships compelling. Whether Benchmark remains independent over the next five to ten years is a genuine open question.

Underlying all of these opportunities is the existential question that has followed the company since its founding: Is being a mid-sized, independent EMS provider sustainable over the long term? The history of the industry argues for skepticism—the graveyard of independent EMS companies is crowded with names that were once prominent.

Solectron, Viasystems, ACT Manufacturing, IEC Electronics—all were absorbed, restructured, or eliminated. The survivors in the mid-tier—Benchmark and Plexus—have endured through a combination of strategic discipline, operational execution, and a willingness to repeatedly reinvent themselves.

The M&A question looms over Benchmark from both directions. As an acquirer, the company could use targeted deals to add engineering capabilities, enter adjacent precision manufacturing niches, or strengthen its position in specific geographies. The company's track record with acquisitions is mixed—the AVEX deal was a near-disaster, while the Pemstar merger was strategically sound—which argues for disciplined, capability-focused deals rather than scale-driven empire building.

As a potential acquisition target, Benchmark presents an interesting profile. Private equity firms have historically found EMS companies attractive for their stable cash flows, margin improvement potential, and operational turnaround opportunities. A larger EMS competitor seeking to strengthen its position in medical, aerospace, or semiconductor capital equipment might also see Benchmark's customer relationships and capabilities as valuable assets. The company's relatively modest market capitalization—roughly $2 billion—makes it a feasible target for a range of potential acquirers.

Whether Benchmark remains independent over the next five to ten years depends on whether the company can continue its margin expansion trajectory, diversify its customer base, and prove that mid-tier independence is strategically viable. The history of the EMS industry argues for skepticism—the graveyard is crowded with formerly independent companies that were absorbed or eliminated.

Solectron, Viasystems, ACT Manufacturing—all were once prominent independent players. But Benchmark and Plexus have demonstrated that a specialty positioning, executed with discipline, can sustain independence through multiple industry cycles.

Benchmark's story is not one of brilliant innovation or market disruption. It is a story of strategic survival—of a company that was born assembling pacemaker components in a small Texas factory and, through four decades of booms, busts, technological upheaval, and competitive bloodshed, found a way to keep the lights on and the assembly lines running.

In an industry that punishes mediocrity with extinction and rewards excellence with merely adequate margins, that persistence is its own kind of achievement. Whether it is enough to sustain an independent company for another thirty-five years is the bet that every Benchmark investor is implicitly making.

XIV. Further Learning

For those wanting to go deeper on the Benchmark Electronics story and the EMS industry more broadly, the following resources provide valuable context and analysis.

Benchmark Electronics' annual reports from 2010 through 2024 offer the most direct window into management's evolving strategic narrative—the CEO letters, in particular, trace the transformation from commodity EMS to specialty manufacturer in real time. The company's investor presentations, available on its investor relations website, articulate the "higher value markets" framework and provide useful data on end-market composition.

For industry context, analyses from Technology Business Research and IPC, the Association Connecting Electronics Industries, provide market-level data on EMS trends, outsourcing penetration rates, and competitive dynamics. The earnings call transcripts from 2016 through 2025—spanning the Tufano and Benck eras—offer candid management commentary on strategy, challenges, and competitive positioning that is often more revealing than formal filings.

For broader strategic frameworks applicable to Benchmark's situation, "Staying Power: Six Enduring Principles for Managing Strategy" by Michael Cusumano provides relevant insight into how companies sustain competitive positions in dynamic industries. "Operations Rules" by David Simchi-Levi offers a rigorous treatment of operational excellence in manufacturing. And "Factory Man" by Beth Macy, while focused on the furniture industry rather than electronics, explores parallel themes of American manufacturing's challenges in the face of global competition.

The SEC 10-K filings, particularly the Risk Factors sections, provide an unvarnished view of the challenges Benchmark faces—from customer concentration and pricing pressure to regulatory compliance and geopolitical risk. For investors, these filings are essential reading because they describe the business as it actually is, stripped of the optimistic framing that characterizes investor presentations.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube