Biofrontera: The Razor, The Blade, and the War for the Skin

I. The "Big Bang" of 2025

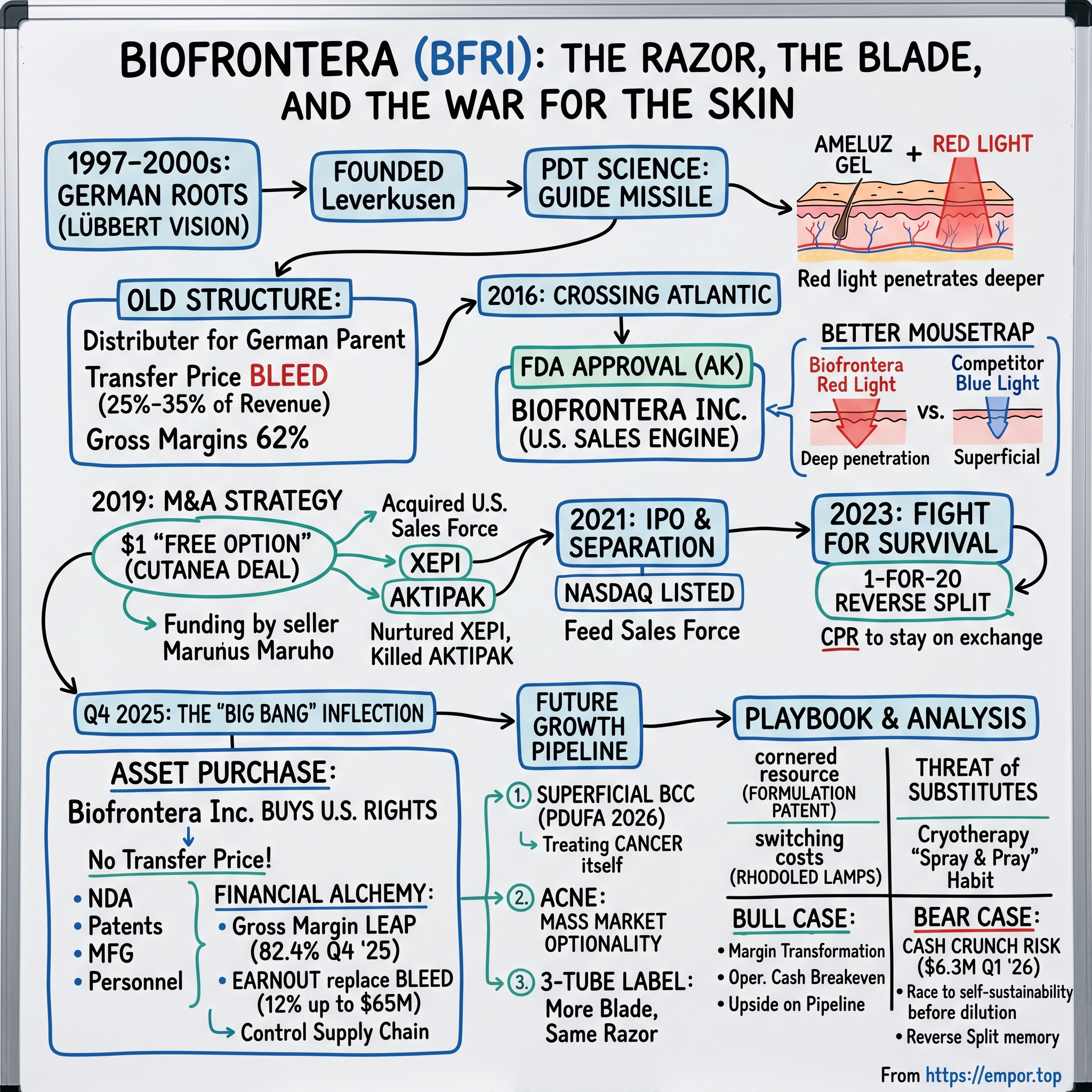

Picture the kind of corporate event that almost never makes the news, because on the surface nothing seems to have happened. No new drug. No blockbuster trial readout. No celebrity CEO ringing a bell. And yet, in the fourth quarter of 2025, a micro-cap dermatology company called Biofrontera Inc. did something that should make any student of business stop and stare.

It changed its own chemistry.

For years, Biofrontera Inc. had been a peculiar creature on the NASDAQ: an American sales-and-marketing engine selling a German-made skin-cancer therapy, paying its German parent a punishing slice of every dollar it collected — somewhere between 25% and 35% of revenue — simply for the right to sell the product. Imagine running a restaurant where, before you pay your rent, your staff, or your electric bill, a third of every check is wired overseas to the company that owns the recipe. That was Biofrontera Inc. Its gross margins sat in the low 60s, and no amount of sales hustle could move them, because the cost of goods was structurally rigged against it.

Then, in October 2025, the company bought the recipe. In a single transaction, Biofrontera Inc. acquired all of the U.S. rights, the New Drug Application, the patents, the manufacturing contracts, and even the personnel behind its flagship products from its former parent, Biofrontera AG.1 The old transfer-price arrangement — that 25%-to-35% bleed — was torn up and replaced with a simple earnout: 12% of U.S. net sales of the drug up to $65 million a year, and 15% above that.2 By the fourth quarter of 2025, gross margin had leapt to roughly 82%.3 By the first quarter of 2026, with a price increase layered on top, it held at approximately 80%, against the 62% the company posted a year earlier.4

A company does not normally improve its gross margin by twenty percentage points in a single quarter. You can grind out two or three points by negotiating with suppliers or automating a warehouse. Twenty points is not operations; it is a change of identity. Overnight, Biofrontera Inc. stopped being a tenant and became the landlord.

That is the thesis of this episode, and it is a deceptively simple one. Biofrontera Inc. is no longer merely a distributor of someone else's medicine. It is now an asset owner — and it owns a business with one of the most underappreciated structures in all of medicine: a razor-and-blade model in a doctor's office, where the razor is a $20,000-plus red-light lamp bolted to the wall, and the blade is a tube of gel that gets squeezed out, visit after visit, year after year. The question that animates everything that follows is whether that razor-and-blade machine can finally dethrone the reigning king of the dermatology clinic — not a rival drug, but a habit. A can of liquid nitrogen. The "spray and pray" of cryotherapy that has frozen warts and pre-cancers off American skin for generations.

To understand how a sub-$50-million market-cap company ended up holding this hand, we have to go back — to a German laboratory in the late 1990s, to a professor who believed light could cure cancer, to a $1.00 acquisition, to a reverse stock split that nearly ended the story, and finally to that quiet 2025 transaction that rewrote the company's DNA. And we have to keep our eyes on a single date now circled on every investor's calendar: September 28, 2026, when the U.S. Food and Drug Administration is scheduled to decide whether Biofrontera's red light gets to attack not just pre-cancers, but cancer itself.4

Let's start in Leverkusen.

II. German Roots: The Lübbert Vision

The town of Leverkusen, on the right bank of the Rhine in western Germany, is a company town in the oldest European sense. It exists because of Bayer; the football club is named for the aspirin-maker; the skyline is dominated by the Bayer cross. It is fitting, then, that the story of Biofrontera begins there in 1997, in the long shadow of one of the great pharmaceutical houses of the world, founded by a man who wanted to build something of his own.5

That man was Professor Doctor Hermann Lübbert. He was not a salesman or a financier; he was a scientist's scientist — a molecular biologist and pharmacologist by training, the kind of academic who had spent years inside the machinery of big pharma before deciding the truly interesting work was happening at the edges. When Lübbert founded Biofrontera AG in 1997, he set himself a goal that, in hindsight, borders on the audacious: to take a drug from a German laboratory bench all the way through both the European and the American regulatory gauntlets, and to do it as an independent, founder-led company.5 To appreciate how rare that ambition was, consider this: Biofrontera would go on to become the first German founder-led pharmaceutical company ever to win both a centralized European approval and a U.S. approval for a drug it had developed entirely in-house.5 Most German biotech founders sell out to a Bayer or a Boehringer long before their molecule ever reaches an American patient. Lübbert refused to.

The science he bet the company on was photodynamic therapy — PDT — and it is worth slowing down to understand it, because the entire investment case rests on what makes it different. Most people, when they hear "skin cancer treatment," picture either a scalpel or a cream. PDT is neither. It is a two-part chemical-and-light reaction, and the easiest way to grasp it is to think of invisible ink under a black light.

Here is how it works. A doctor applies a gel — Biofrontera's product is called Ameluz — onto a patch of sun-damaged skin. The gel contains a compound that the body's own cells absorb and convert into a light-sensitive molecule. Crucially, the rapidly dividing, damaged, pre-cancerous cells gobble up far more of this molecule than healthy cells do. So after an incubation period, those bad cells are now glowing with a chemical that healthy cells largely ignore. Then comes the second step: the doctor shines a very specific, narrow band of red light onto the skin using a lamp — Biofrontera's is the BF-RhodoLED. The light activates the molecule, which reacts with oxygen inside the cell and effectively detonates it from within. The damaged cells die. The healthy ones, which never took up much of the compound, are largely spared.

It is, in a sense, a guided missile rather than a carpet bomb — and that distinction is the whole ballgame. Because PDT is not "a cream." It is a combination product: a drug that is useless without a specific medical device, and a device that is useless without the drug. You cannot copy half of it. A generic manufacturer can, in theory, reverse-engineer a gel; it is far harder to also build, certify, and sell the precisely-tuned lamp that the gel's label legally requires. This is the seed of the razor-and-blade moat we will return to again and again.

But in the early 2000s, none of that was a moat yet. It was a hypothesis, and an expensive one. Lübbert and his small team spent the better part of a decade in the grind that defines drug development: proving, in trial after trial, that Ameluz plus the RhodoLED lamp could clear actinic keratoses — the rough, scaly patches of sun damage that are the most common precursor to certain skin cancers. They navigated the European Medicines Agency first, the natural home market, and won a centralized European approval. But Lübbert always had his eyes on the bigger prize across the Atlantic, where dermatology is a far larger and more lucrative market, and where the FDA's bar is famously higher. The decision to chase that American approval — to subject a small German company to the full cost and rigor of the FDA — would define the next chapter of Biofrontera's life, and force it to become, in effect, two companies on two continents.

III. Crossing the Atlantic: The 2016 FDA Inflection

In May 2016, a tube of German gel went on sale in the United States.6 For a company of Biofrontera's size, the FDA's approval of Ameluz, in combination with the BF-RhodoLED lamp, for the treatment of actinic keratoses on the face and scalp was the milestone Lübbert had spent nearly two decades building toward.6 It was the moment the hypothesis became a product with a price tag in the world's most important drug market.

But an approval is a door, not a destination. Walking through it raised an immediately practical question that turned out to be one of the most consequential strategic choices in the company's history: how do you actually sell a German drug in America?

The answer Biofrontera arrived at was to build a wholly separate American entity — Biofrontera Inc. — rather than running U.S. sales out of the German parent. On paper this looks like mere corporate plumbing. In practice it reflected a hard truth about capital markets. German and American investors think differently, value companies differently, and fund growth differently. A U.S. commercial dermatology business — which lives and dies by an expensive, feet-on-the-street sales force pounding the pavement of American dermatology practices — needed American capital, American investors, and eventually an American stock listing to fund its expansion. Trying to finance a U.S. sales war from a Frankfurt-listed parent was like trying to run an American political campaign on euros. The structure that emerged — a German R&D and manufacturing parent, and a U.S. commercial subsidiary — set up the central tension of this entire story. Because the parent owned the asset, the subsidiary had to pay rent for it. That rent was the transfer price. And that transfer price is precisely what would strangle the U.S. company's margins for the better part of a decade, right up until the 2025 transaction that we opened with.

Now, walking through the American door, Biofrontera found the room already occupied. The incumbent in photodynamic therapy was Levulan Kerastick, a product of DUSA Pharmaceuticals, which had been absorbed into the empire of सन फार्मा Sun Pharmaceutical Industries, the giant Indian generics-and-specialty house. Levulan was the established player, the default PDT that American dermatologists already knew. And here the technical story becomes a competitive story, because the two products do not use the same light.

Levulan's protocol relied on blue light. Biofrontera's relied on red. To a patient, the difference is invisible. To a dermatologist treating a real lesion, it is everything — and the reason comes down to a principle of physics that is almost poetically simple: longer wavelengths of light penetrate deeper into tissue. Blue light, sitting at the short end of the visible spectrum, scatters quickly and treats only the most superficial layers of the skin. Red light, at the long end, reaches deeper. Think of it as the difference between a flashlight pressed against the back of your hand — under blue light you see only a faint surface glow; under red light, your whole hand lights up because the photons are traveling all the way through.

For thin, surface-level sun damage, that distinction may not matter much. But for thicker lesions, and — looking ahead — for actual tumors that have rooted themselves below the surface, depth of penetration is the difference between killing the whole problem and merely singeing its top. Red light was, in the language of business strategy, the "better mousetrap": a genuine technical advantage rooted in physics, not marketing. It gave Biofrontera a real answer to the most dangerous question any challenger faces — "why should I switch?" The answer was: because the deeper your light reaches, the more completely you treat the disease.

A better mousetrap, however, does not sell itself, and it certainly does not generate the cash to fund a national sales force. Biofrontera had the science. What it lacked, in those years after 2016, was scale, a broader product bag for its reps to carry, and the capital to fight a ground war against an entrenched competitor. To get all three, it would make one of the strangest acquisitions you will ever encounter — for the price of a single dollar.

IV. M&A Strategy: The $1 "Free Option"

There is a particular kind of deal that, when you first hear the headline number, sounds like a typo. In March 2019, Biofrontera AG acquired Cutanea Life Sciences, an American dermatology company, from its Japanese owner, the Osaka-based pharmaceutical house マルホ Maruho, for a purchase price of exactly one U.S. dollar.[^7]

One dollar. Less than the cost of the gum at the pharmacy checkout.

Now, anyone who has spent time around mergers knows that a $1 price tag is never the real price. It is a signal — a flare shot into the sky that says the assets being sold come bundled with liabilities, obligations, and ongoing cash needs that the seller is desperate to hand off. The art of the $1 acquisition is in reading what is hidden behind that dollar, and on that score, the Cutanea deal is a small masterclass in capital deployment.

What did the dollar buy? It bought Cutanea's commercial infrastructure and its product portfolio, the most notable of which was Xepi, a topical antibiotic for impetigo — the crusty, contagious bacterial skin infection familiar to every parent of a school-age child. It also brought a second product, Aktipak, an acne treatment. And, just as importantly, it brought an experienced U.S. dermatology sales organization — exactly the kind of feet-on-the-street commercial muscle that Biofrontera had been struggling to fund on its own.

But the genius of the structure was not in what Biofrontera bought; it was in who paid for the downside. As part of the arrangement, Maruho — the seller, eager to exit the U.S. market — agreed to fund a substantial portion of Cutanea's ongoing operating and start-up costs going forward.[^7] Read that again, because it is the whole trick. Biofrontera acquired a U.S. commercial platform while the previous owner kept writing the checks to keep it alive during the transition. That converts the acquisition from a gamble into something much more elegant: a free option on the American dermatology market. If the products worked and the sales force could cross-sell Ameluz alongside Xepi, the upside flowed to Biofrontera. If they didn't, the downside had been pre-funded by someone else. Heads, Biofrontera wins; tails, Maruho loses.

Was it a steal? Yes and no — and the honest answer reveals more about the company's discipline than a simple "yes" would. The Cutanea portfolio was not all gold. Aktipak, the acne product, ultimately failed to find a viable path and was wound down. Xepi survived and gave the sales force a second product to put in the bag. The lesson here is one that separates durable small-cap operators from the ones that flame out: the ability to kill a product without killing the company. A weaker management team falls in love with everything it owns, pours good money after bad into a failing asset, and bleeds out. Biofrontera's handling of the Cutanea assets — nurturing Xepi, euthanizing Aktipak — showed a willingness to cut losses, to treat each product as a position to be sized rather than a child to be saved. In a business where cash is the only thing standing between you and the void, that discipline is not a nicety; it is survival.

The Cutanea deal gave Biofrontera Inc. the commercial bones of a real American business. What it did not give the company was independence — or, frankly, enough cash. The acquisition was made by the German parent, layering yet another set of obligations onto the corporate structure. To truly stand on its own two feet, the U.S. business would have to do the one thing every American growth company eventually attempts: go public, and ask the market for money.

V. The Pivot: IPO and the Separation

On November 2, 2021, Biofrontera Inc. listed its shares on the NASDAQ.7 The timing, in retrospect, was brutal. The company placed up to 3,450,000 shares with U.S. investors in a price range of $5.00 to $7.00 per share — a modest raise, on the order of $18 million in gross proceeds, into a market that was just beginning to turn cold on exactly the kind of small, cash-burning, pre-profitability healthcare names that investors had been happy to fund a year earlier.7 The window that had been wide open in early 2021 was closing fast, and Biofrontera squeezed through it just before it slammed.

The purpose of the IPO was singular and unglamorous: feed the sales force. Commercializing a combination drug-device product in American dermatology is enormously expensive. Every dermatology practice is its own fortress that must be visited, educated, and converted, one office at a time. The IPO capital was the ammunition for that ground war — money to hire reps, to support the lamps placed in offices, to fund the unglamorous, grinding work of building U.S. demand for red-light PDT.

But raising $18 million into a falling market is like filling a bathtub with the drain open. The years that followed the IPO were, to put it plainly, a fight for survival. The stock drifted. The cash burned. And by the summer of 2023, Biofrontera faced the small-cap company's most humbling rite of passage: its share price had fallen so low that it risked being delisted from the NASDAQ for failing to meet the minimum bid price requirement. On July 3, 2023, the company executed a 1-for-20 reverse stock split, collapsing twenty shares into one to mechanically lift the price back into compliance.8 A reverse split is financial CPR — it keeps the patient on the exchange, but no one mistakes it for a sign of health. It is the kind of maneuver a company undertakes when the alternative is the morgue.

Through all of this, the constant was Lübbert. The founder who had started the German company in 1997 was now Chairman and Chief Executive of the American one — the rare founder who followed his molecule not just across two decades but across an ocean, taking personal command of the U.S. entity that carried his life's work.5 Alongside him on the financial side was Chief Financial Officer Fred Leffler, charged with the unenviable job of managing a chronically thin balance sheet through a hostile market. The defining trait of this leadership team is not charisma; it is persistence. They are operators who kept a structurally disadvantaged company alive long enough to fix the structure.

And here is where the human-incentive layer becomes interesting for investors. Management's alignment runs through the company's equity incentive plan, originally adopted around the 2021 listing and meaningfully expanded in 2026 with a large addition to the share reserve.4 On the surface, share-reserve increases at a cash-strapped micro-cap can read as a warning — more potential dilution for existing holders. But there is a more constructive reading, and the timing supports it. You expand an incentive pool, and lock in your management with multi-year equity, when you believe the prize is in sight and you want the team's hands chained to the oars for the final push toward profitability. The question of which interpretation is correct — dilution-as-rot versus alignment-for-the-finish — is one every shareholder has to weigh, and we will return to it in the bull-and-bear analysis.

Crucially, Biofrontera was not navigating this alone. The names that recur through its restructuring are two specialist healthcare investors: Rosalind Advisors and AIGH Capital. These were the adults in the room — sophisticated, deep-pocketed funds who understood the asset and were willing to keep funding it through the lean years, not as passive index money but as engaged backers with skin in the game.2 Their continued willingness to write checks was, in a very real sense, the company's life-support system. And it was these same two investors who would underwrite the single most important transaction in Biofrontera's history — the deal that finally severed the cord to Germany and let the American company own its own future.

VI. The 2025 "Strategic Transaction": The Real Inflection

For nearly a decade, the central fact of Biofrontera Inc.'s existence was that it did not own the thing it sold. The drug was the parent's. The lamp was the parent's. The New Drug Application — the legal document that is, in effect, the deed to the entire U.S. franchise — sat in Germany. Biofrontera Inc. was a sales agent renting its own flagship from its family. Every strategic conversation, every margin analysis, every financing decision happened in the shadow of that dependency.

On October 23, 2025, that shadow lifted.

In a transaction the company plainly called transformative, Biofrontera Inc. closed the purchase of all U.S. assets and rights related to Ameluz and the RhodoLED lamps from Biofrontera AG.1 This was not a license or a royalty tweak. It was a wholesale transfer of ownership: the U.S. New Drug Application, the Investigational New Drug applications behind the pipeline, the manufacturing rights and contracts, the entire body of related intellectual property, and even the relevant personnel all moved from the German parent to the American company.1 In one stroke, Biofrontera Inc. stopped being a customer of Germany and became the master of its own house.

The financial alchemy at the heart of the deal is what investors will remember. Recall the old structure: a transfer price of roughly 25% to 35% of revenue paid to the parent — a crushing, uncapped levy that kept gross margins stuck in the low 60s no matter how well the sales force performed. The new structure replaced that with an earnout: Biofrontera Inc. pays 12% of U.S. net sales of Ameluz in years where those sales run at or below $65 million, stepping up to 15% on sales above that threshold — and, critically, those payments end when the relevant patents expire, rather than running forever.2 Cutting your single largest cost from a third of revenue to roughly an eighth is not a rounding adjustment; it is the difference between a business model that can never reach profitability and one that can. It is exactly this swap that detonated the margin "big bang" we opened with — the jump to 82.4% gross margin in the fourth quarter of 2025, holding near 80% into the first quarter of 2026.34

But the margin story, dramatic as it is, may not even be the most important part of the deal. The quieter, deeper win is control of the supply chain. By acquiring the manufacturing rights, contracts, and the NDA itself, Biofrontera Inc. took command of its own destiny in a way that pure financial engineering never could. A company that does not control its own manufacturing or its own regulatory filing is permanently hostage — to a supplier's pricing, to a parent's strategic whims, to the risk that the entity upstream of you stumbles into its own financial trouble and drags you down with it. After October 2025, Biofrontera Inc. owned the product, the filing, and the right to make it. It could plan its own capacity, pursue its own label expansions, and pledge its own assets to raise its own money. Independence, in pharma, is not an abstraction; it is the precondition for everything else.

How was such a transformative deal financed by a company that had been fighting for its life? Through the same backers who had stood behind it all along. The transaction was funded by an $11 million investment — $8.5 million committed earlier and $2.5 million released at closing — led by Rosalind Advisors and AIGH Capital, with Biofrontera AG taking back a roughly 10% post-money equity stake in the U.S. company in exchange for the assets.2 That last detail is elegant: the German parent did not simply walk away with cash it did not have to give; it became a shareholder in the very company it sold to, aligning the two entities' interests for the first time in their history.

Step back and benchmark this against the broader pharmaceutical world, and the favorability of the terms comes into focus. Royalty rates on approved, marketed, high-margin specialty pharma assets routinely run into the high teens and beyond; double-digit-to-twenties royalties are common, and they typically run for the life of the product. Securing the full U.S. ownership of an already-approved, growing dermatology franchise for an effective cash royalty of 12% — capped at a known sales threshold and set to expire with the patents — is, by the standards of the industry, a genuinely advantageous outcome for the buyer. Biofrontera Inc. did not just renegotiate a contract. It bought back its own freedom, and it bought it cheaply.

With the structure finally fixed and the balance sheet finally aligned, the question shifts from survival to growth. Because owning the asset only matters if the asset has room to run. And Biofrontera's pipeline — the hidden businesses tucked behind the actinic-keratosis franchise everyone already knew about — is where the next several years of the story will be written.

VII. Hidden Businesses: The Growth Pipeline

Every good razor-and-blade business eventually asks the same question: now that we have the razor installed in the customer's hand, how many more blades can we sell them? For Biofrontera, with thousands of RhodoLED lamps already placed in American dermatology offices, the answer comes in three distinct flavors — and each one is a lever on revenue that requires no new lamp, no new customer, and very little new marketing spend.

Start with the biggest swing: superficial basal cell carcinoma, or sBCC. Until now, Biofrontera's red light has been approved to treat actinic keratoses — pre-cancers. The body, scientifically speaking, of someone who has not yet developed cancer. But the company has filed a supplemental New Drug Application to extend Ameluz PDT into the treatment of superficial basal cell carcinoma — actual non-melanoma skin cancer, the most common cancer in human beings — and the FDA has accepted the filing and set a PDUFA target action date of September 28, 2026.4 This is the catalyst around which the entire 2026 investment thesis revolves, and it is worth being clear about why it matters so much. This is not "more actinic keratosis." It is a category leap — from treating the kindling to treating the fire. And remember the physics from earlier: red light's deeper penetration is precisely the attribute that makes PDT a credible weapon against tumors that have rooted below the skin's surface, where blue light cannot reach. If approved, sBCC opens a genuinely new market for the franchise, one where the technical advantage is not a marginal nicety but the whole reason the therapy can work at all.

The second flavor is the mass market: acne. Actinic keratosis and skin cancer are, in the grand scheme, niche dermatology. Acne is universal — tens of millions of patients, a vast and perennially underserved market. In Phase 2b testing, PDT with Ameluz produced a 58% reduction in inflammatory acne lesions using a three-hour incubation protocol, compared with a 37% reduction for the vehicle (placebo) light treatment.4 That spread between drug and placebo is the signal that the therapy is doing real biological work. Acne is a longer, more speculative shot — it would require further trials and carries real risk — but the prize is enormous precisely because the addressable population dwarfs everything else in the portfolio. It is the optionality that could one day make Biofrontera something far larger than a skin-cancer company.

The third flavor is the most immediate, the least glamorous, and quite possibly the most underrated by the market: the three-tube label. Here is the mechanics. Historically, a single PDT session used one tube of Ameluz to treat a defined spot. But sun damage does not respect tidy boundaries — a patient with a field of actinic keratoses across an entire balding scalp or both forearms has far more surface to treat than one tube comfortably covers. Biofrontera has been advancing the science and the label toward field treatment using up to three tubes of Ameluz in a single session.9 Think through what that does to the economics. The same patient, the same office visit, the same lamp, the same marketing dollar — but three tubes of high-margin gel consumed instead of one. You have, in effect, tripled the blade consumption per razor-pull without spending a cent more to acquire the customer. In a razor-and-blade model, that is the purest form of leverage there is: more blade, same razor, same channel. It is the kind of quiet, structural revenue expansion that does not generate headlines but compounds powerfully on the bottom line.

Supporting all three is a steady drumbeat of clinical progress — including positive Phase 3 results for treating mild-to-moderate actinic keratoses on the extremities, neck, and trunk, broadening the approved body real estate beyond the face and scalp.4 Each expansion is another reason for a dermatologist who already owns the lamp to reach for Ameluz more often.

So the growth pipeline is really three bets stacked on one installed base: a near-term catalyst (sBCC), a mass-market moonshot (acne), and a quiet revenue multiplier (three tubes). But pipelines are promises, and promises in pharma are cheap. The harder question — the one that determines whether any of this is durable — is whether Biofrontera's business is actually defensible. To answer that, we need to run it through the frameworks.

VIII. Playbook: Porter's Five Forces and Hamilton's 7 Powers

Let's war-game this business properly. A growing micro-cap with a fixed balance sheet is interesting; a growing micro-cap with a structural moat is investable. So where, exactly, does Biofrontera's defensibility come from — and where is it dangerously exposed?

Begin with Hamilton Helmer's concept of a cornered resource — a preferential access to something coveted that competitors simply cannot get. In pharma, the canonical cornered resource is a patent, and Biofrontera's most important one protects the specific propylene-glycol-free formulation of Ameluz, with patent protection that the company has positioned as extending into the early 2040s.1 This matters more than a casual reader might think. A formulation patent that runs that long means that for the better part of two decades, a competitor cannot simply copy the gel and undercut Biofrontera on price. The cornered resource is the reason the 12%-to-15% earnout can have a defined end date tied to patent expiry — the company is paying for an asset whose exclusivity is legally fenced for years to come. In pharma, a long-dated formulation patent on an approved product is about as close to a fortress wall as the industry offers.

Next, switching costs — and this is where the razor-and-blade structure does its real work. When a dermatologist installs a RhodoLED lamp, they are making a capital commitment of roughly $20,000 and dedicating clinic space and staff training to a specific PDT system.1 That lamp is calibrated for, and the label legally ties it to, Ameluz. Once that hardware is bolted to the wall, the economic and clinical gravity pulling the doctor toward Biofrontera's gel — rather than a competitor's — is enormous. Why would a practice that has sunk five figures into a red-light system go through the friction of switching drugs, retraining staff, and altering protocols to save a little on the blade? They overwhelmingly don't. The installed base of lamps is, in effect, a fleet of locked-in vending machines that only dispense one brand of snack. Every lamp placed is an annuity.

Now flip to the threats, via Porter's Five Forces, because a moat is only as good as the dangers it holds back.

The most important force here is not rivalry — it is the threat of substitutes, and the substitute is not even another drug. It is a habit. The overwhelming default treatment for actinic keratoses and many superficial skin lesions in America is cryotherapy: freezing the lesion off with a spray of liquid nitrogen. It is fast, it is cheap, it is reimbursed, and the dermatologist can do it in ninety seconds with a can they already own. Cryotherapy commands the dominant share of the lesion-treatment market — by most industry estimates, the large majority of these procedures.10 This is the real war, and it is crucial to understand who Biofrontera is actually fighting. It is not primarily battling Sun Pharma's Levulan for the small PDT pie. It is battling the muscle memory of an entire profession — the reflexive reach for the nitrogen can. PDT's pitch against cryotherapy is field treatment versus spot treatment: freezing kills the one lesion you can see, while red-light PDT treats the entire damaged field, including the sub-clinical lesions you cannot yet see. That is a genuinely better clinical outcome. But "better" has to overcome "fast, cheap, and what I've always done," and that is the single hardest force this company faces.

On rivalry, the direct competitor remains Sun Pharma's DUSA franchise and its blue-light Levulan system. The rivalry has at times been litigious — the kind of patent and competitive friction common when a challenger with a differentiated technology pushes into an incumbent's space. Part of what the 2025 restructuring accomplished, alongside its financial benefits, was a general clearing of the decks — consolidating ownership, obligations, and liabilities under one roof so the U.S. company could fight its battles with a clean balance sheet and clear title to its own assets.1 A challenger cannot wage a competitive war while its corporate structure is a tangle of cross-border obligations and unresolved liabilities. Simplifying the structure was a precondition for competing.

The remaining forces are more benign. Bargaining power of buyers — the dermatologists — is real but blunted by those switching costs once the lamp is installed. Bargaining power of suppliers was, ironically, the company's single greatest vulnerability for years, because its most important "supplier" was its own parent extracting a 25%-to-35% transfer price. The 2025 transaction did not just lower a cost; it eliminated the most dangerous supplier-power dynamic in the entire business by bringing manufacturing and the NDA in-house. And the threat of new entrants is held off by the formidable combination of FDA approval, the long-dated formulation patent, and the sheer expense and difficulty of building both a drug and a certified medical device and a national dermatology sales force simultaneously.

Put it all together and you get a business with two genuine powers — a cornered formulation patent and razor-and-blade switching costs — pitted against one formidable substitute, the liquid-nitrogen habit. Whether the moat is wide enough, and whether the company can survive long enough to exploit it, is exactly the debate that defines the bull and bear cases.

IX. Analysis: The Bull vs. The Bear Case

Here is the tension that makes Biofrontera such a fascinating little puzzle: the business has, in the span of about a year, fixed the single biggest flaw in its model — and yet it remains one cash crunch away from the abyss. Both of those things are true at once, and an honest investor has to hold them simultaneously.

The bull case starts with the margin transformation and never really has to leave it. A company selling a patented, switching-cost-protected product at roughly 80% gross margin, growing revenue 17% year over year to $10.1 million in the first quarter of 2026, is a fundamentally different animal than the 62%-margin tenant it was a year earlier.4 The operating leverage in that swing is the whole story: in the first quarter of 2026, the company burned essentially no cash from operations — about $70 thousand, against $4.1 million consumed in the prior-year quarter.4 That is a near-total elimination of operating cash burn, achieved not through brutal cost-cutting but through the structural margin lift dropping straight to the cash line. If the company is genuinely approaching cash-flow breakeven on its current AK franchise alone, then everything in the pipeline — the September 2026 sBCC decision, the three-tube field-treatment expansion, the acne optionality — is upside layered on top of a business that no longer needs the capital markets to survive. And against that, the equity market has at times valued the whole enterprise at a level that looks almost incidental relative to the revenue it is now capable of producing. If Biofrontera can convert its installed lamp base and its pipeline into a $50-million-plus revenue business at these margins, the gap between today's valuation and that outcome is the bull's entire thesis. The cornered patent and the razor-and-blade lock-in are the reasons to believe the margins are durable rather than fleeting.

The bear case is shorter, colder, and impossible to dismiss: cash. The company ended the first quarter of 2026 with $6.3 million in cash.4 For a business that, even in its dramatically improved state, still posted a $4.8 million net loss in the quarter and carries the heavy fixed costs of clinical programs and a commercial organization, that is a thin cushion — a cash runway that, on the wrong set of assumptions, can be measured in quarters, not years.4 Micro-cap biopharma is littered with companies that had a great asset and a fixed business model and still died, because they ran out of money one financing short of the finish line. Going-concern risk — the auditor's formal warning that a company may not have the resources to operate for the next twelve months — has been a recurring feature of Biofrontera's life, and the bear's central worry is straightforward: even a structurally healthier company can be forced into a dilutive emergency raise if a catalyst slips, a launch underwhelms, or the capital markets simply close. The very share-reserve expansion that the bull reads as alignment, the bear reads as preparation for more dilution. A reverse split sits in the recent past as a reminder of how close to the edge this company has lived.8 The race is explicit: can rising, high-margin revenue reach self-sustaining cash flow before the balance sheet forces another raise on bad terms?

Synthesizing the two through the frameworks: the powers are real but young. The cornered resource (the formulation patent) and the switching costs (the installed lamps) are exactly the kind of structural advantages that produce durable economics — but they only pay off if the company has the cash to keep selling, keep placing lamps, and keep funding the pipeline long enough for the substitute-fighting, habit-breaking work against cryotherapy to compound. The 2025 transaction dramatically improved the odds by killing the supplier-power problem and fixing the margin. It did not, by itself, refill the bank account. The bull and the bear are not really arguing about the quality of the asset — they largely agree it is good. They are arguing about the clock.

Which brings us to the single most important thing for an investor to actually watch.

X. Epilogue and Final Reflections

If you track only a few numbers on Biofrontera from here, track these. First and above all, the path to cash-flow breakeven — operating cash burn per quarter — because that single line determines whether the company controls its own destiny or whether the capital markets do; the move from $4.1 million of quarterly burn to roughly nothing is the most important thing that has happened to this business, and whether it holds is everything.4 Second, U.S. Ameluz net sales and units, the blade-consumption metric that tells you whether the razor-and-blade flywheel is actually spinning — and against which the 12%/15% earnout, and the $65 million threshold where the rate steps up, are measured.24 And third, the binary event now circled in red: the September 28, 2026 FDA decision on superficial basal cell carcinoma, which will either open a genuine new cancer market for the franchise or remove a pillar from the growth story.4 Everything else — acne, geographic label expansions, valuation — is downstream of those three.

Step back, and the deepest lesson of Biofrontera's story is a counterintuitive one about the nature of acquisitions themselves. We tend to think of M&A as buying growth, buying technology, buying customers. But the most important acquisition in this company's entire history was the one where it bought nothing new at all. In October 2025, Biofrontera Inc. acquired the rights to a product it had already been selling for nearly a decade. It bought back its own freedom from its own parent.1 Sometimes the highest-return capital deployment available to a company is not expansion into something new, but the repatriation of something it already had — paying to own outright the asset it had only been renting. The twenty-point margin leap was not the discovery of a new business; it was the reclaiming of value that had been leaking overseas all along.

And what of the bigger war — red light versus the nitrogen can? Picture the dermatology office of 2030. In one version, nothing changes: the can of liquid nitrogen still rules, the ninety-second freeze still pays the bills, and PDT remains a premium niche. In the other version, the field-treatment logic wins — the recognition that freezing one visible spot while ignoring the damaged field around it is treating the symptom and missing the disease. In that office, a patient sits under a calm red glow while a precisely-targeted molecule does its quiet, guided work below the surface, sparing the healthy skin the nitrogen would have blistered. That is the elegance Biofrontera is selling: not brute force, but precision. Not freezing the visible, but illuminating the invisible.

Whether the office of 2030 looks like the first version or the second is, in the end, a question of habit versus physics — of whether the easiest thing keeps winning, or whether the better mousetrap finally gets its decade. Biofrontera spent twenty-nine years, two continents, a $1 acquisition, a reverse split, and a transformative buyback earning the right to find out. Now it has a fixed business model, a defensible asset, a thin balance sheet, and a date in September. The razor is on the wall. The only question left is how many blades the world is ready to buy.

References

-

Biofrontera Inc. Closes Purchase of All Ameluz and RhodoLED US Assets from Biofrontera AG — GlobeNewswire, 2025-10-23 ↩↩↩↩↩↩↩

-

Biofrontera (NASDAQ: BFRI) acquires U.S. Ameluz and RhodoLED rights, $11M funding — StockTitan, 2025-10-23 ↩↩↩↩↩

-

Biofrontera Inc. Form 8-K (Q4 2025 results) — SEC EDGAR, 2025 ↩↩

-

Biofrontera Inc. Reports First Quarter 2026 Financial Results and Provides a Business Update — BioSpace, 2026-05-14 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Biofrontera Inc. Names Founder and Executive — SEC EDGAR (Form 8-K exhibit), 2023 ↩↩↩↩

-

FDA Drugs@FDA: Ameluz (aminolevulinic acid HCl) approval overview, ApplNo 208081 — FDA.gov ↩↩

-

Biofrontera AG Form 6-K (U.S. IPO of Biofrontera Inc., November 2021) — SEC EDGAR, 2021 ↩↩

-

Biofrontera Inc. Announces 1-for-20 Reverse Stock Split — AccessNewswire, 2023-07-03 ↩↩

-

Biofrontera enrolls first patient to Phase I safety study evaluating photodynamic therapy with three tubes of Ameluz — Biofrontera AG corporate news ↩

-

Earnings call transcript: Biofrontera Q1 2026 sees gross margin leap — Investing.com, 2026-05-14 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube