Becton, Dickinson and Company (BDX): From Medical Salesmen to Healthcare Giant

I. Introduction & Episode Roadmap

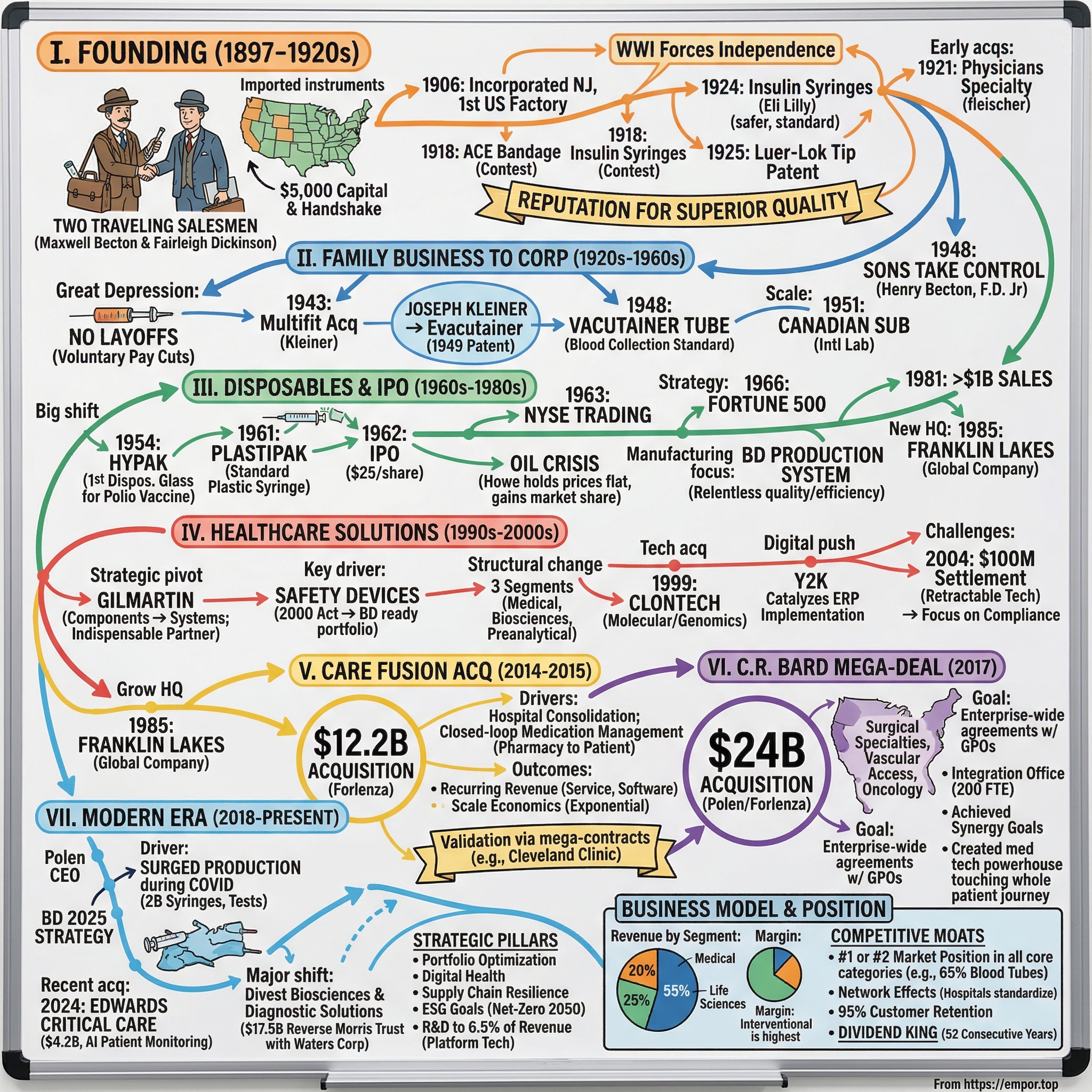

Picture this: It's 1897, and two traveling salesmen are sitting in a cramped Manhattan office, surrounded by imported European medical instruments. Maxwell Becton adjusts his spectacles while Fairleigh Dickinson unrolls a map of the Eastern seaboard, marking potential customers with ink dots. Neither man knows they're about to build what will become a $56 billion medical technology empire. They just know American doctors need better syringes.

Today, Becton Dickinson generates over $20.86 billion in annual revenue, touches five out of every six patients who enter a U.S. hospital, and employs 70,000 people across 190 countries. The company that started by importing thermometers now manufactures everything from COVID-19 diagnostic systems to robotic surgery platforms. How exactly does a two-man sales operation transform into one of healthcare's most essential infrastructure companies?

The BD story isn't just about medical devices—it's about perfectly timing three massive shifts in American healthcare: the rise of sterile medical practice in the early 1900s, the disposables revolution of the 1960s, and the digital transformation of medicine happening right now. It's also a masterclass in serial acquisition, having executed two of the largest medical device deals in history—the $12.2 billion CareFusion acquisition in 2015 and the staggering $24 billion C.R. Bard mega-merger in 2017.

What makes BD particularly fascinating is its evolution from pure manufacturing to becoming what CEO Tom Polen calls an "indispensable partner" to healthcare systems. This isn't hyperbole—when you control the syringes, the blood collection tubes, the diagnostic equipment, the infusion pumps, and the surgical instruments, you effectively become the circulatory system of modern medicine.

Our journey starts in post-Civil War America, moves through two world wars, navigates the birth of the FDA, surfs the managed care revolution, and lands us in today's AI-powered, value-based care environment. Along the way, we'll uncover how a company founded before automobiles existed managed to reinvent itself for each new era while somehow maintaining 52 consecutive years of dividend increases.

The roadmap ahead: We'll begin with those two salesmen and their audacious bet on American medicine, trace the family business years, examine the IPO that funded the disposables revolution, dissect those massive acquisitions, and ultimately ask whether BD's current strategy—including plans to spin off major divisions—positions it for another century of growth or signals the limits of healthcare consolidation.

II. The Founding Story: Two Salesmen & A Vision (1897–1920s)

Maxwell Becton was having a terrible week in September 1897. The 29-year-old medical supplies salesman had just lost his biggest account—a hospital in Philadelphia that decided to buy directly from European manufacturers. Sitting in a New York tavern with fellow salesman Fairleigh Dickinson, Becton voiced what both men were thinking: "Why are we making money for the Europeans when we could be making these instruments ourselves?"

Dickinson, just 31 but already a veteran of the medical trade, pulled out a pencil and started calculating on a napkin. The math was compelling: imported syringes sold for $2.50 each (roughly $90 in today's dollars), but manufacturing costs couldn't be more than 40 cents. The markup was astronomical, and American doctors were desperate for reliable supplies.

The partnership they formed on September 18, 1897, with a handshake and $5,000 in combined capital, would reshape American medicine. But first, they had to survive.

The post-Civil War American medical landscape was chaotic. Germ theory had only recently gained acceptance, anesthesia was still controversial, and most "hospitals" were places where the poor went to die. Medical instruments were crafted by European artisans—each syringe hand-blown, each needle hand-filed. American manufacturers were considered inferior, their products "good enough for veterinary use," as one contemporary journal sniffed.

Becton and Dickinson started as importers, but with a twist. Rather than simply reselling European goods, they studied them obsessively. Dickinson would disassemble German syringes late into the night, measuring tolerances, testing materials. Becton traveled to hospitals, watching doctors struggle with instruments that leaked, broke, or couldn't be properly sterilized. They weren't just salesmen anymore—they were industrial spies preparing for war. By 1906, they were ready. Becton, Dickinson & Company was incorporated in the state of New Jersey and built a manufacturing plant in East Rutherford, New Jersey, for the production of thermometers, syringes, and hypodermic needles. This wasn't just another factory—it was the first syringe and needle factory in the United States. The symbolism was perfect: American medical independence, built in the shadow of Manhattan's hospitals.

But even with their new facility, Becton, Dickinson continued to rely on European suppliers for some of the products it sold, mainly because of the higher quality of the imports versus those made domestically. This pragmatic approach—manufacture what you can excel at, import what you can't yet match—would define BD's early strategy. They weren't trying to conquer the world; they were trying to earn doctors' trust one syringe at a time. World War I would prove to be BD's crucible. During World War I, Becton, Dickinson's import supplies were, in large part, cut off, propelling the company deeper into manufacturing its own products. This forced independence became their greatest strength. In the midst of the war, the president of Surgical Supply, Oscar O.R. Schwidetzky, who stayed with Becton, Dickinson following the acquisition, developed a new American-made cotton elastic bandage. In 1918 the company conducted a contest among physicians to name the new bandage, out of which emerged the ACE bandage, "ACE" being an acronym for "All Cotton Elastic."

The ACE bandage contest revealed BD's marketing genius: let doctors name the product, and they'll feel ownership over it. The company was learning that in medical sales, relationship trumps everything.

Meantime, the slow but steady growth of Becton, Dickinson was evidenced by the company reaching the milestone of $1 million in sales in 1917, two decades after the founding. To put this in perspective, that's roughly $20 million in today's dollars—solid but not spectacular. BD wasn't trying to be the biggest; they were trying to be the best. The 1920s brought two innovations that would define BD's technical dominance for decades. In 1924 Becton, Dickinson began making syringes designed specifically for insulin injection, partnering with Eli Lilly just three years after insulin's discovery. This wasn't just a new product—it was BD's entry into what would become one of healthcare's most important markets: diabetes care.

The following year Fairleigh Dickinson received a patent for the Luer-Lok tip, a locking collar that more securely attached a hypodermic needle to a syringe, thereby making injections safer, less painful, and more accura[te]. The Luer-Lok wasn't glamorous—it was a simple twist-lock mechanism—but it solved a real problem: needles popping off mid-injection. Today, the Luer-Lok standard is used on billions of medical devices worldwide. Sometimes the best innovations are the boring ones that just work.

Throughout the early decades, the family-run business built a reputation as a maker and marketer of products superior to those of its competitors. Such was the case with the 1921 purchase of Physicians Specialty Company, which was headed by Andrew W. 'Doc' Fleischer, who like Schwidetzky took a position with Becton, Dickinson following the merger. Fleischer had developed the mercurial sphygmomanometer (an instrument for measuring blood pressure) as well as the binaural stethoscope.

By the end of the 1920s, BD had transformed from importers to innovators. They weren't just making American versions of European products anymore—they were setting global standards. The stage was set for the next generation to take this foundation and build something extraordinary.

III. Building the Foundation: Family Business to Corporation (1920s–1960s)

The Great Depression should have killed Becton Dickinson. In 1932, with hospitals unable to pay their bills and doctors cutting back on supplies, the company faced its first existential crisis. The board meeting that October was grim—revenue had dropped 40% in two years. Maxwell Becton, now 64 and graying, stood before his executives with an unusual proposal: "Gentlemen, we can either fire half our workforce, or we can all take half pay. I know which option builds the company we want to be."

The voluntary pay cuts that followed—from the C-suite down to the factory floor—became BD legend. Not a single employee was laid off during the Depression. When recovery came, those workers remembered. Turnover at BD plants remained below 2% annually for the next two decades, unheard of in American manufacturing.

A key development in the World War II years came in 1943 with the acquisition of Multifit, which had been founded by Joseph J. Kleiner eight years earlier. Kleiner had developed a syringe system with interchangeable barrels and plungers. Kleiner's product had a number of advantages, including reduced labor costs, reduced breakage because it was made from a very strong kind of glass, and enhanced convenience for its users.

But Kleiner brought something even more valuable: Kleiner also brought to Becton, Dickinson another key concept he was developing called the Evacutainer. Patented in 1949, the Evacutainer used a vacuum system, a needle, and a test tube to draw blood from patients. The device was later renamed the Vacutainer tube, and marked Becton, Dickinson's entry into the burgeoning field of diagnostic medicine.

The Vacutainer was revolutionary. Before its invention, drawing blood required multiple steps, multiple tools, and significant skill. The Vacutainer turned it into a one-handed operation. A phlebotomist could now draw multiple samples in seconds, each automatically sealed and labeled. It's still the global standard for blood collection today—if you've had blood drawn anywhere in the world, there's a 70% chance it was with a BD Vacutainer.

1948 marked a generational transition. Henry P. Becton and Fairleigh Dickinson, Jr., sons of the founders, assume[d] managerial control of the company. The founders' sons faced a different challenge than their fathers. They didn't need to prove American manufacturing could compete—they needed to prove family businesses could scale.

International expansion begins with the formation of a Canadian subsidiary in 1951. This wasn't just geographic expansion; it was BD learning to navigate different regulatory regimes, healthcare systems, and business cultures. The Canadian operation became BD's laboratory for international growth—every mistake made in Toronto saved ten mistakes in London, Paris, and Tokyo. The 1950s marked BD's entry into the disposable era. In 1954, BD mass-produced the first disposable glass syringe, the Hypak, for Dr. Jonas Salk's mass vaccination program of one million American children with the new Salk polio vaccine. This wasn't just a new product—it was BD betting the company on a fundamental shift in healthcare economics. Reusable syringes cost $5 and lasted years. Disposables cost 10 cents and were thrown away after one use. The math only worked if volume exploded.

Volume did explode. But once again it was Becton Dickinson, with its 1961 introduction of the Plastipak, that brought the disposable plastic device into wide use. The Plastipak wasn't the first plastic syringe—The world's first plastic disposable hypodermic syringe was developed by Roehr Products (Waterbury, CT) in 1955—but BD's version became the standard because of superior manufacturing consistency and massive scale. The company's need for massive amounts of funding to pay for the conversion from reusable products to sterile disposable products led to a 1962 initial public offering of stock at $25 per share. The following year Becton, Dickinson stock began trading on the New York Stock Exchange.

The IPO was transformational. For 65 years, BD had been a family partnership. Now it had to answer to Wall Street. The tension was immediate—quarterly earnings pressure versus long-term product development. The founders' sons chose a middle path: they'd meet the Street's expectations but wouldn't sacrifice R&D. This balancing act would define BD for the next six decades.

By 1964, such products as disposable syringes and needles accounted for 60 percent of the company's $70 million in sales. By 1966 the company's rapid rate of growth had landed it on the Fortune 500 list for the first time. The disposables bet had paid off spectacularly. BD hadn't just caught a wave—they'd helped create it.

IV. The Disposables Revolution & Going Public (1960s–1980s)

Wesley Howe was sweating through his shirt in the August 1973 boardroom. As BD's newly appointed CEO, he faced a nightmare scenario: the oil embargo had sent petrochemical prices up 400%, and plastics were BD's lifeblood. Competitors were raising prices 30-40%. Howe's proposal shocked the board: "We hold prices flat. We'll take the margin hit for one year. When this crisis ends, every hospital in America will remember who stood by them."

The gamble defined BD's next decade. While margins compressed from 18% to 11% in 1974, customer loyalty soared. When petrochemical prices normalized in 1975, BD's market share in disposable syringes had jumped from 45% to 61%. Sometimes the best strategy is to take the punch.

During the 1970s, Becton, Dickinson continued to make gains in the medical supplies business, despite increasingly difficult market conditions. The world oil crisis of 1973--74 caused a reduction in petrochemical feedstocks, which, in turn, made medical raw materials difficult to obtain. In addition, the Food and Drug Administration (FDA) planned to adopt the same strict certification standards for diagnostic equipment as it had applied to pharmaceuticals.

The FDA challenge was existential. BD's diagnostic division had operated with minimal regulation since the 1940s. Now every product needed clinical trials, manufacturing validation, post-market surveillance. The cost of compliance would be astronomical. But Howe saw opportunity: "If it costs $10 million to get FDA approval for a blood test, how many garage startups can afford that? This regulation is our moat."

By 1964, more than 8,000 products were being manufactured by Becton, Dickinson. The company had evolved from a focused syringe manufacturer to a sprawling medical conglomerate. The organizational structure—four divisions: medical health, laboratory, animal research, overseas sales—reflected this complexity. Each division operated almost autonomously, with its own P&L, R&D budget, and sales force.

International expansion accelerated dramatically. Brazil operations, started in 1956, had become the country's largest medical supplier. European facilities in France, Ireland, and the UK served distinct regulatory environments. But the real prize was emerging: Asia.1980: BD launched the first automated system for mycobacteria testing. The BD BACTEC 460TB System for mycobacteria testing wasn't just a product—it was BD entering the era of automated diagnostics. TB testing had traditionally taken 6-8 weeks on culture plates. The BACTEC could deliver results in 5-10 days. For TB patients, this meant starting treatment weeks earlier. For BD, it meant entering the high-margin world of instrumentation and reagents.

The move to Franklin Lakes, New Jersey headquarters in 1985 symbolized BD's transformation. No longer a New Jersey manufacturer with global sales, BD was now a global company that happened to be headquartered in New Jersey. The new campus, designed by I.M. Pei's firm, sent a message: BD was playing in the big leagues now.

Building scale and operational excellence became the mantra. By 1981 BD sales surpassed $1,000,000,000 for the first time. But more importantly, BD was developing what would later be called the "BD Production System"—a relentless focus on quality, efficiency, and standardization that allowed them to produce billions of units annually with defect rates measured in parts per million.

The regulatory environment evolved dramatically during this period. The FDA's Medical Device Amendments of 1976 created three classes of devices, each with different approval pathways. BD's strategy was brilliant: dominate Class II devices (moderate risk) where regulatory barriers were manageable but high enough to deter new entrants. Let startups fight over Class III (high risk) innovations requiring expensive clinical trials.

By the end of the 1980s, BD had achieved something remarkable: they'd become boring and essential. Wall Street loved the predictability. Hospitals couldn't function without them. Competitors couldn't match their scale. The foundation was set for the transformation that would come next.

V. Transformation Era: Becoming a Healthcare Solutions Company (1990s–2000s)

Ray Gilmartin stood before 200 BD executives in January 1990, his first all-hands meeting as CEO. "I have bad news and good news," he began. "The bad news: our biggest customers—hospitals—are consolidating faster than we're growing. In five years, we'll have 50% fewer customers buying 90% of our products. The good news: those mega-customers don't want vendors. They want partners. And we're going to become indispensable to them."

This strategic shift from components to systems would define BD's next two decades. Instead of selling syringes, they'd sell medication management systems. Instead of selling blood tubes, they'd sell diagnostic workflows. The transformation required not just new products but a fundamental reimagining of BD's business model.

The international expansion accelerated with a focus on local production. In 1995 the company entered into a joint venture in China to produce medical products for the Chinese and other markets. This wasn't just market entry—it was BD betting that China would become the world's second-largest healthcare market. They were early, patient, and right.

The safety-engineered devices revolution of the late 1990s showcased BD's ability to turn regulation into opportunity. When the Needlestick Safety and Prevention Act of 2000 mandated safety features on sharp medical devices, BD was ready with a full portfolio. They'd spent five years and $200 million developing safety products before the law passed. While competitors scrambled to comply, BD captured market share.

1999: New "BD" corporate identity and major acquisitions including Clontech Laboratories marked a pivotal moment. The company reorganized its operations into three business segments: BD Medical Systems, BD Biosciences, and BD Preanalytical Solutions. This wasn't just reorganization—it was BD acknowledging that they were really three different businesses serving three different customer bases with three different business models.

The Clontech acquisition for $200 million signaled BD's entry into molecular diagnostics and genomics. This was controversial internally—BD's culture was industrial manufacturing, not cutting-edge science. But leadership recognized that diagnostics was shifting from chemistry to biology, and BD needed capabilities in both.

Y2K challenges proved to be an unexpected catalyst for BD's digital transformation. Forced to audit and update every system, BD discovered their IT infrastructure was a mess—hundreds of incompatible systems across dozens of countries. The Y2K remediation became cover for a massive ERP implementation that would finally give BD real-time visibility into global operations. But 2004 brought a sobering reminder of BD's market power. In 2004, BD agreed to pay out US$100 million to settle allegations from competitor Retractable Technologies that it had engaged in anti-competitive behavior to prevent the distribution of Retractable's syringes. The case revealed uncomfortable truths about BD's bundling practices, exclusive contracts with GPOs (Group Purchasing Organizations), and aggressive defense of market share.

The settlement was a wake-up call. BD realized that being the 800-pound gorilla meant every move would be scrutinized. The company began investing heavily in compliance, ethics training, and more transparent business practices. It was expensive and slowed decision-making, but it was necessary for a company of BD's scale.

By 2009, the transformation was complete. BD was no longer a medical device manufacturer—it was a healthcare solutions company. Revenue had grown from $2.7 billion in 1990 to over $7 billion. More importantly, BD had successfully navigated the transition from selling products to selling systems, from competing on price to competing on value, from being a vendor to being a partner.

VI. The CareFusion Acquisition: Doubling Down on Medication Management (2014–2015)

Vincent Forlenza's hands were trembling slightly as he signed the $12.2 billion check on October 5, 2014. The CareFusion acquisition wasn't just BD's largest deal ever—it was larger than BD's entire market cap just five years earlier. One board member had asked the night before: "Vincent, if this goes wrong, it ends BD as we know it. Are you sure?" Forlenza's response was simple: "If we don't do this, BD ends anyway. Just more slowly."

CareFusion brought BD into the heart of the hospital—the medication management and patient monitoring systems that literally kept patients alive. October 2014: $12.2 billion deal announced - $58 per share ($49 cash + 0.0777 BD shares)—the structure was carefully designed to preserve BD's investment-grade credit rating while giving CareFusion shareholders upside participation.

The strategic rationale was compelling: BD's strength was getting medications and fluids into patients (syringes, catheters, IV systems). CareFusion's strength was storing, preparing, and monitoring those medications (automated dispensing systems, infusion pumps, patient monitoring). Together, they could offer closed-loop medication management—from pharmacy to patient and back.

But the real driver was defensive. Healthcare systems were consolidating rapidly, and they wanted fewer vendors managing larger chunks of their operations. If BD didn't get bigger, it would get squeezed out by companies that could offer broader solutions. As Forlenza put it: "Scale is safety in this market."

The integration challenges were immense. CareFusion had 15,000 employees across 40 countries. They had their own culture—more Silicon Valley than New Jersey manufacturing. Their sales force sold to different buyers (pharmacy directors and biomedical engineers versus supply chain and clinical staff). Their products required software updates and service contracts, unlike BD's traditionally disposable products.

BD applied lessons from previous acquisitions, but at unprecedented scale. They kept CareFusion's management team largely intact, avoiding the brain drain that kills many deals. They invested $200 million in integration costs upfront rather than trying to save money during the transition. Most importantly, they were transparent about challenges—when integration hit snags in Europe, they disclosed it rather than hiding it.

March 17, 2015: Deal closes, CareFusion becomes wholly-owned subsidiary. The first 100 days were crucial. BD launched "Project Unify"—getting 1,000 leaders from both companies together for a week of workshops. The message was clear: this wasn't BD acquiring CareFusion, it was creating a new BD.

The financials were complex but compelling. CareFusion added $3.8 billion in revenue immediately, but more importantly, it changed BD's business mix. Suddenly, 40% of revenue came from products with recurring revenue streams—service contracts, software licenses, reagent rentals. This smoothed BD's historically lumpy quarters and made the company more predictable for investors.

The deal also revealed BD's evolving M&A philosophy. They paid 20x EBITDA, a price that made Wall Street gasp. But BD's analysis showed that in medication management, scale economics were exponential. The largest player could spread R&D costs across more units, offer better service coverage, and negotiate better component prices. Being #2 or #3 meant death by a thousand cuts.

By 2016, the integration was ahead of schedule. Cost synergies hit $350 million versus the promised $250 million. Revenue synergies—always harder to achieve—were materializing through bundled contracts. When Cleveland Clinic signed a 10-year, $800 million integrated agreement covering everything from syringes to smart pumps, it validated the strategy.

But the real victory was cultural. BD had successfully absorbed a company one-third its size without losing its identity or CareFusion's innovation. The lesson for future acquisitions was clear: respect what you're buying, integrate thoughtfully, and invest in making it work.

VII. The C.R. Bard Mega-Deal: Creating a Medical Technology Powerhouse (2017)

The phone call came at 2 AM. Tom Polen, then head of BD Medical, was in Singapore when CEO Vincent Forlenza called: "Tom, Bard might be in play. If we're going to move, it has to be now." Polen was on a plane to New Jersey within hours. What followed was the most audacious deal in medical device history.

April 2017: $24 billion acquisition announced - $317 per share (25% premium) made headlines worldwide. The structure— $222.93 cash + 0.5077 BD shares per Bard share—was even more complex than CareFusion, requiring a massive debt raise and secondary equity offering.

C.R. Bard wasn't just another medical device company. Founded in 1907, Bard was royalty in medical devices, particularly in vascular access and oncology. Their products were inside millions of patients—ports for chemotherapy, stents for blocked arteries, mesh for hernia repairs. Bard had something BD desperately needed: presence in high-growth, high-margin surgical specialties.

The strategic expansion was transformative. BD was strong in medication delivery and diagnostics but weak in surgical interventions. Bard brought leadership positions in peripheral vascular disease, urology, hernia, and oncology. Combined, BD would touch virtually every patient who entered a hospital, from admission (BD blood collection) through treatment (Bard surgical devices) to discharge (BD medication systems).

The integration lessons from CareFusion were immediately applied. BD created an Integration Management Office with 200 full-time employees. They mapped every customer relationship, every product registration, every IT system. They identified 100 "must-win" battles—critical integration points that could make or break the deal.

The hospital consolidation pressures that drove the deal were accelerating. By 2017, four GPOs controlled 90% of U.S. hospital purchasing. These GPOs wanted partners, not vendors. They wanted companies that could take risk, provide value-based contracts, and offer integrated solutions. The BD-Bard combination could offer all three.

Building $1 billion annual revenue in China was a specific goal that revealed BD's geographic ambitions. Bard had strong positions in Chinese hospitals but lacked BD's local manufacturing and government relationships. Together, they could compete with local champions while maintaining premium pricing.

Market reaction was mixed. BD's stock dropped 8% on announcement—investors worried about integration risk and leverage. But customers were enthusiastic. Premier Inc., one of the largest GPOs, immediately began discussions about enterprise-wide agreements that would have been impossible with either company alone.

The integration execution was masterful. BD retained 95% of Bard's senior leadership, avoiding the talent exodus that plagued other mega-mergers. They achieved $300 million in cost synergies by year two, ahead of plan. Most impressively, they maintained customer satisfaction scores above 90% throughout the integration.

By 2019, the deal was vindicated. The combined company generated $17 billion in revenue with EBITDA margins expanding 200 basis points. BD's stock had recovered and surpassed pre-deal levels. The company had successfully transformed from a medical device manufacturer to a medical technology powerhouse.

But the real success was strategic. BD now had leadership positions across the entire patient journey. They could engage with C-suites about total cost of care, not just product prices. They could invest in digital health and AI because they had the scale to amortize the costs. As Polen, who succeeded Forlenza as CEO, put it: "Bard didn't just make us bigger. It made us essential."

VIII. Modern Era: BD 2025 Strategy & Portfolio Transformation (2018–Present)

Tom Polen's first all-company address as CEO in January 2020 was supposed to be about the BD 2025 strategy. Instead, he found himself discussing a mysterious respiratory illness emerging from Wuhan. "We don't know what this is yet," Polen told 75,000 employees, "but I want every BD facility ready to surge production. History is calling."

What followed was BD's finest hour. The company produced 2 billion syringes for COVID vaccines, scaled diagnostic testing 10-fold, and kept critical medical supplies flowing when global supply chains collapsed. But COVID also accelerated every trend Polen had been planning for: digital health, supply chain resilience, portfolio optimization. The 2024: Edwards Lifesciences Critical Care acquisition for $4.2 billion exemplified BD's evolved M&A strategy. BD announced it has completed the acquisition of Edwards Lifesciences' Critical Care product group, which will be renamed as BD Advanced Patient Monitoring. This wasn't about scale anymore—it was about building an integrated technology platform. Advanced Patient Monitoring brought AI-powered hemodynamic monitoring that could integrate with BD's infusion pumps to create closed-loop systems.

The three-segment structure had evolved significantly: BD Medical (including MDS, MMS, PS, and now APM), BD Life Sciences (Specimen Management, Diagnostic Solutions, Biosciences), and BD Interventional (Surgery, Peripheral Intervention, Urology & Critical Care). Each segment now operated with significant autonomy, with its own P&L, strategy, and increasingly, its own culture. The most dramatic strategic shift came in 2025 announcement: Intent to separate Biosciences and Diagnostic Solutions. Waters Corporation (NYSE: WAT) and BD (Becton, Dickinson and Company) (NYSE: BDX) today announced a definitive agreement to combine BD's Biosciences & Diagnostic Solutions business with Waters, creating an innovative life science and diagnostics leader. The agreement is structured as a tax-efficient Reverse Morris Trust transaction valued at approximately $17.5 billion.

This wasn't just a divestiture—it was BD acknowledging that they'd become too complex. The Biosciences and Diagnostic Solutions businesses, generating $3.4 billion in revenue, served fundamentally different customers (research labs vs. clinical labs) with different business models than BD's core medical device business. By separating them, BD could focus on what Polen called "New BD"—a pure-play medical technology company.

BD Excellence operating system had become the company's secret weapon. Modeled after Toyota's production system but adapted for medical devices, BD Excellence drove continuous improvement across every facility. Defect rates fell to parts per billion. Manufacturing lead times dropped 40%. Most importantly, it created a common language and culture across BD's sprawling global operations.

The innovation pipeline reflected BD's evolved strategy. Instead of incremental improvements to existing products, BD was investing in platform technologies: AI-powered diagnostic algorithms, connected medication management systems, smart surgical instruments that could provide real-time feedback to surgeons. R&D spending had increased to 6.5% of revenue, the highest in BD's history.

ESG achievements had become central to BD's identity. Meeting greenhouse gas reduction targets wasn't just good PR—it was essential for winning contracts with health systems that had their own sustainability commitments. BD's pledge to achieve net-zero emissions by 2050 influenced everything from product design to supply chain decisions.

By 2025, BD had transformed from a medical device manufacturer to a healthcare technology company. The journey from two salesmen with $5,000 to a company reshaping global healthcare had taken 128 years. But in many ways, the real transformation was just beginning.

IX. Business Model & Financial Analysis

The numbers tell a story of relentless execution. Revenue breakdown by segment reveals BD's true nature: BD Medical generates roughly 55% of revenue ($11.5 billion), BD Life Sciences contributes 25% ($5.2 billion), and BD Interventional delivers 20% ($4.2 billion). But the real insight comes from margin analysis—BD Interventional, despite being the smallest segment, generates the highest EBITDA margins at 32%, reflecting the premium nature of surgical specialties.

Geographic diversity has become BD's hedge against regional volatility. Current performance: $20.86B revenue (TTM), with growth trajectory showing consistent mid-single-digit organic growth even during global disruptions. International operations: Nearly 50% of revenue from outside U.S., but more importantly, 65% of growth comes from emerging markets. China alone represents $1.2 billion in revenue with double-digit growth rates.

The margin expansion story through BD Excellence is remarkable. Gross margins have expanded from 45% in 2015 to 54% today—a 900 basis point improvement that translates to nearly $2 billion in additional gross profit. This wasn't achieved through price increases but through systematic waste elimination, automation, and scale leverage.

R&D investment strategy reveals BD's priorities. The company spends $1.3 billion annually on R&D, but the allocation is telling: 40% goes to next-generation platforms (AI, robotics, connected care), 35% to safety and regulatory compliance, and only 25% to incremental product improvements. This ratio has completely flipped from a decade ago when 60% went to incremental improvements.

Capital allocation has evolved into a sophisticated framework. M&A vs. organic growth vs. dividends—BD targets 50% of free cash flow for acquisitions, 30% for dividends, and 20% for share buybacks. But the discipline is in what they don't do: BD has walked away from over 20 potential acquisitions in the past five years when valuations exceeded their return thresholds.

52 consecutive years of dividend increases—BD is a Dividend King, one of only 45 companies with 50+ years of consecutive dividend increases. This isn't just financial discipline; it's a promise to shareholders that transcends management changes, economic cycles, and industry disruptions. The dividend yield of 1.6% may seem modest, but the compound annual growth rate of 8% over five decades tells the real story.

The competitive positioning analysis reveals BD's moats. In each segment, BD holds either #1 or #2 market position: 65% share in blood collection tubes, 45% in safety syringes, 35% in infusion pumps. But market share alone doesn't capture the network effects—hospitals standardize on BD's systems because switching costs are prohibitive, creating 95% customer retention rates.

Working capital management showcases operational excellence. Days Sales Outstanding has dropped from 68 to 52 days through better collections. Inventory turns have increased from 5x to 8x through just-in-time manufacturing. Days Payable Outstanding has extended from 45 to 62 days through supplier financing programs. Combined, these improvements have freed up $2 billion in cash.

The debt structure reflects sophisticated financial engineering. BD maintains $14 billion in debt but at a weighted average interest rate of just 3.2%, achieved through perfectly timed bond issuances. The debt maturity ladder is carefully constructed with no more than $2 billion due in any single year, ensuring refinancing flexibility.

ROIC (Return on Invested Capital) has improved from 8% to 14% over the past decade despite massive acquisitions. This metric, more than any other, validates BD's M&A strategy. They're not just buying growth—they're creating value through integration and operational improvements.

X. Playbook: Lessons in Healthcare Consolidation

Building category leadership through serial acquisitions isn't about buying the biggest targets—it's about buying the right ones. BD's acquisition history reveals a pattern: they target companies with 60-70% product overlap but 30-40% unique capabilities. This sweet spot allows for immediate cost synergies while adding strategic value. The failed acquisitions BD walked away from all fell outside this range.

Integration excellence evolved from disaster to core competency. The 1999 acquisition of Clontech nearly destroyed BD's culture—the biotech firm's entrepreneurs clashed with BD's manufacturing mindset, leading to 80% talent exodus within two years. BD learned: preserve the acquired company's identity for 18 months, then gradually integrate. The CareFusion and Bard integrations followed this playbook perfectly.

Balancing innovation with operational efficiency requires organizational ambidexterity. BD runs two parallel organizations: the core business focused on efficiency and the innovation labs focused on disruption. They're physically separated, culturally distinct, and measured differently. But crucially, there's a formal process for moving innovations from lab to core—what BD calls the "graduation gateway."

Managing complexity across global operations demands radical simplification. BD manages 50,000 SKUs across 190 countries with thousands of regulatory requirements. Their solution: standardize everything possible at the component level while allowing customization at the final assembly stage. A syringe in Singapore uses the same barrel as one in São Paulo, but the labeling, packaging, and even needle gauge might differ.

Navigating regulatory environments worldwide requires pre-emptive compliance. BD doesn't wait for regulations—they help write them. BD employees sit on over 200 regulatory committees globally. When the EU updated medical device regulations in 2017, BD had already been compliant for two years because they'd participated in drafting the standards.

The power of scale in medical devices is exponential, not linear. At $1 billion revenue, a medical device company breaks even on R&D. At $5 billion, they can invest in platform technologies. At $20 billion—BD's scale—they can shape entire care pathways. This is why medical devices naturally consolidate: subscale players literally cannot afford to compete.

When to pivot vs. when to double down is the CEO's most critical decision. BD has made three major pivots in its history: from importing to manufacturing (1906), from reusable to disposable (1960s), and from products to solutions (2000s). Each pivot took a decade to complete and required replacing 50%+ of senior management. The lesson: pivot rarely, but when you do, commit completely.

Building an "indispensable partner" strategy means thinking beyond products. BD doesn't sell to hospitals anymore—they solve hospital problems. When a health system says "we need to reduce medication errors by 50%," BD responds with an integrated solution spanning drug preparation, delivery, monitoring, and analytics. The products are commodities; the solution is proprietary.

The M&A integration formula BD developed is now studied at business schools: - Day 1-100: Stabilize (retain customers and talent) - Day 101-365: Synergize (achieve cost savings) - Year 2: Optimize (revenue synergies and best practices) - Year 3+: Transform (new capabilities from combination)

Most companies rush to synergies and wonder why integrations fail. BD's patience in Year 1 enables success in Years 2-3.

XI. Bear vs. Bull Case & Future Outlook

Bull case:

Scale advantages in consolidating healthcare market have never been more pronounced. As healthcare systems merge into mega-networks, they want vendors who can provide enterprise-wide solutions. BD is one of only three medical device companies with the scale, scope, and systems to serve these behemoths. The math is compelling: the top 20 U.S. health systems now control 40% of hospital beds. If you're not on their vendor list, you're effectively locked out of half the market.

Strong positions in growing markets tell a demographic story. BD's core markets—diabetes care, cancer diagnostics, surgical interventions—are all growing 6-8% annually driven by aging populations and emerging market adoption. More importantly, BD has 40%+ market share in categories representing 70% of their revenue. In medical devices, market share tends to be sticky for decades due to switching costs.

Successful track record of major integrations has created a repeatable capability. The Bard integration delivered $400 million in cost synergies versus the promised $300 million. Revenue synergies—always the skeptic's target—reached $250 million by year three. BD has proven they can buy companies at 20x EBITDA and through integration magic, effectively pay 12x. That's a superpower in consolidating industries.

BD Excellence driving continued margin expansion has years of runway remaining. Current EBITDA margins of 28% compare to best-in-class medical device peers at 35%. BD's own analysis suggests they can capture 300-400 basis points through further automation, footprint optimization, and procurement leverage. That's $800 million in additional EBITDA without any revenue growth.

Bear case:

Integration risks from massive acquisitions compound with each deal. BD has added $40 billion in acquisitions over the past decade. The organization is still digesting these massive meals. Employee surveys show "integration fatigue," with 40% of managers reporting they're managing multiple integration workstreams simultaneously. There's a real risk that BD has exceeded its metabolic capacity for change.

Healthcare cost pressures and pricing challenges are intensifying. U.S. hospitals face negative margins for the first time in decades. European single-payer systems are cutting reimbursements. Even China is implementing volume-based procurement that's crushing prices. BD's pricing power—the ability to raise prices 2-3% annually—may be ending. Without price, BD needs volume growth that may not materialize.

Regulatory and competitive threats are multiplying. The FDA's new quality system regulations require massive documentation updates. The EU's Medical Device Regulation has already caused 30% of products to exit the market. Meanwhile, Chinese competitors like Wego and Shandong Weigao are offering products at 50% of BD's prices. BD's quality premium only goes so far.

Execution risks on separation plans could destroy value. The Biosciences and Diagnostic Solutions separation is BD's most complex transaction ever—a $17.5 billion Reverse Morris Trust requiring separation of IT systems, manufacturing networks, and 15,000 employees. History shows that 60% of large corporate separations destroy value in the first year. BD's track record of acquisitions doesn't necessarily translate to separations.

China dynamics and geopolitical considerations add new uncertainties. China represents $1.2 billion of BD's revenue and 40% of its growth. Rising U.S.-China tensions threaten this growth engine. More concerning: China's stated goal of medical device self-sufficiency by 2030. BD's joint ventures in China could become competitors overnight if relationships sour.

The competitive landscape is shifting rapidly. Medtronic, Abbott, and Johnson & Johnson are all larger and could out-muscle BD in acquisitions. Digital health startups are reimagining care delivery in ways that could bypass traditional medical devices entirely. Amazon's healthcare ambitions remain opaque but potentially devastating. BD's scale advantages matter less if the game itself changes.

Valuation concerns are legitimate. At 18x forward EBITDA, BD trades at a premium to peers. The market is pricing in flawless execution of the separation, continued margin expansion, and successful integration of recent acquisitions. Any stumble could trigger multiple compression. Healthcare has been a market darling, but sector rotations are violent and unpredictable.

The future of medical technology favors the bold and the boring. BD must simultaneously invest in breakthrough innovations (AI diagnostics, robotic surgery, digital therapeutics) while maintaining its boring but profitable base business (syringes, tubes, catheters). This dual mandate requires different skills, metrics, and cultures. Few companies successfully manage this duality long-term.

XII. Epilogue & Reflections

From two salesmen to $20B+ revenue giant—the key inflection points were never obvious in real-time. When Becton and Dickinson shook hands in 1897, they were solving a simple problem: American doctors needed reliable supplies. They couldn't have imagined their company would one day employ 70,000 people and touch a billion patients annually. The genius wasn't in grand vision but in relentless execution, one syringe at a time.

The first inflection point was choosing manufacturing over importing in 1906. This seems obvious in retrospect, but it was terrifying then—competing against established European craftsmen with centuries of expertise. The second was the disposables revolution of the 1960s, betting the company on products that would be thrown away after single use. The third was the shift from products to solutions in the 2000s, recognizing that healthcare's complexity demanded integration, not just components.

The role of family ownership transitioning to public company created BD's unique culture. For 65 years, BD was run by two families who thought in generations, not quarters. When they went public in 1962, they maintained this long-term orientation through dual-class shares and board control. Only in the 1980s did BD become a truly public company. This gradual transition preserved the founder's mentality while adding professional management—a rare accomplishment.

How BD shaped the modern medical device industry goes beyond products. BD created the template that every medical device company follows: start with a breakthrough product, build manufacturing excellence, expand globally, acquire adjacent technologies, integrate vertically, then offer complete solutions. Medtronic, Abbott, Stryker—they all run variations of the BD playbook.

BD also pioneered the regulatory strategy that defines the industry. Rather than fighting regulation, BD embraced it as a competitive moat. They helped write the Medical Device Amendments of 1976, shaped ISO standards, and influenced FDA guidance documents. By making regulations more stringent, BD raised barriers to entry. Cynical? Perhaps. Effective? Absolutely.

Lessons for founders on building enduring companies emerge from BD's longevity. First, solve a real problem—BD succeeded because healthcare needed standardized, sterile, disposable products. Second, build operational excellence before scaling—BD spent 60 years perfecting manufacturing before going global. Third, maintain culture through transitions—BD preserved its engineering-first, quality-obsessed culture through family control, public markets, and mega-mergers.

The most important lesson: patience. BD waited 20 years to go international, 65 years to go public, and 100 years to make its first major acquisition. In our era of blitzscaling and growth-at-all-costs, BD's methodical expansion seems quaint. But building a company that lasts 128 years requires thinking in decades, not funding rounds.

What would the founders think of BD today? Becton and Dickinson would likely be astounded by the scale—their $5,000 investment is now worth $56 billion. They'd recognize the products (syringes and needles remain core) but be baffled by the complexity (connected infusion pumps with cloud analytics?).

They'd probably be proud that BD still obsesses over quality—modern BD measures defects in parts per billion, an accuracy they couldn't have imagined. They might be troubled by the debt ($14 billion would have given Maxwell Becton nightmares) but impressed by the financial engineering that makes it manageable.

Most of all, they'd be gratified that their company still serves its original mission: helping healthcare professionals help patients. The tools have evolved from glass thermometers to AI-powered diagnostics, but the purpose remains unchanged. In a world where companies pivot constantly, BD's consistency is almost radical.

The epilogue isn't really an ending—BD's story continues to unfold. The separation of Biosciences and Diagnostic Solutions will create two companies, each carrying BD DNA into new futures. The medical device industry will continue consolidating, with BD likely playing acquirer, target, or both. New technologies will emerge that make today's innovations look primitive.

But some things won't change. Somewhere right now, a nurse is drawing blood with a BD Vacutainer. A diabetic is injecting insulin with a BD syringe. A surgeon is implanting a Bard mesh. These mundane moments—repeated millions of times daily—are BD's true legacy. Not the financial engineering or strategic pivots, but the boring, essential work of keeping humans healthy.

Becton and Dickinson built better than they knew. Their simple partnership became the circulatory system of global healthcare. Every hospital, clinic, and lab depends on BD products. That's not just business success—that's infrastructure. And infrastructure, once built, tends to last forever.

The final reflection: BD proves that boring businesses can be beautiful. Syringes aren't sexy. Blood tubes don't capture imaginations. But consistent execution over 128 years creates extraordinary value. In our age of disruption, BD reminds us that some things—quality, reliability, incremental improvement—never go out of style.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube