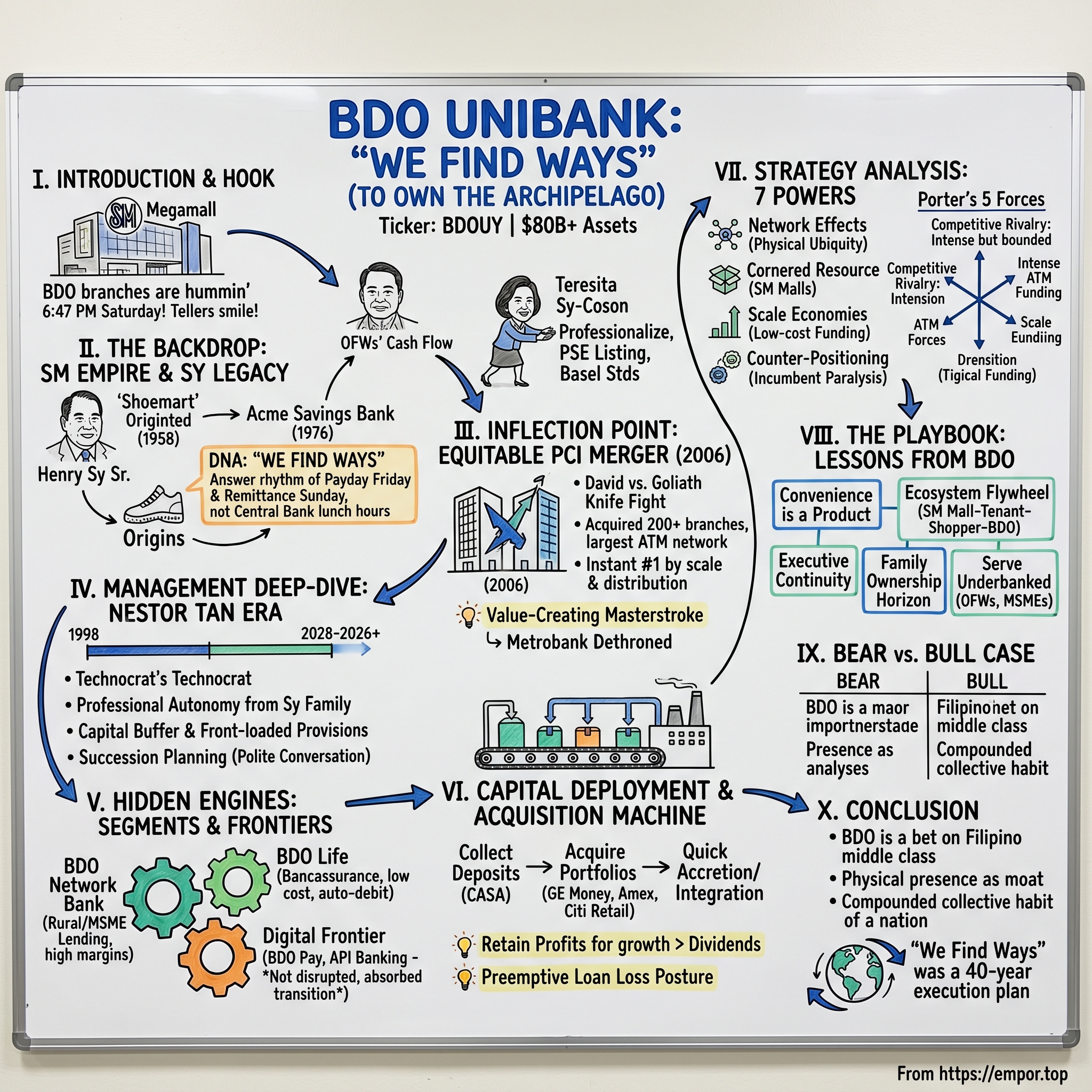

BDO Unibank: We Find Ways (To Own the Archipelago)

I. Introduction & The "Big" Hook

Picture a Saturday afternoon in Manila. The heat outside the SM Megamall is pushing 34 degrees, the jeepneys are snarled along EDSA, and a line of shoppers is moving briskly through a bank branch tucked between a Jollibee and a mobile phone kiosk. The lights are on. The tellers are smiling. It is 6:47 PM. On most of the planet, this would be an impossibility. Banks close. Bankers go home. Money waits until Monday. But here, inside a mall owned by the Sy family, a BDO branch is still humming, and there are still people three-deep at the counter, queuing to deposit envelopes of cash stuffed with peso bills sent home by a son welding ships in a Saudi dockyard or a daughter teaching English in Hong Kong.

This is the atmosphere of a company that has quietly become one of the most powerful consumer franchises in Southeast Asia. BDO Unibank holds roughly $80 billion in assets. It commands more than 20 percent market share in deposits, loans, trust, remittances, and credit cards in a country of 115 million people. It is bigger than the next three Philippine banks combined in some categories. Its branches number more than 1,700. Its ATMs exceed 5,000. Its customer base crossed 65 million accounts. And yet, for decades, most global investors either ignored it or confused it with a regional player half its size.

This is not merely a banking story. It is a platform story. It is the story of how a shoe salesman from Xiamen, China — a man who rode third-class ferries and slept in the back room of his first Manila store — built a financial fortress that now operates as the de facto payment and credit rail of the Filipino consumer. It is the story of how the bank became the financial operating system of the SM Group ecosystem, and by extension, the financial operating system of the Philippine middle class.

The central insight is almost embarrassingly simple. Most banks in the developing world copied the posture of their Western parent institutions: wood-paneled branches, 9-to-3 hours, a quiet preference for the wealthy and the well-connected. BDO did the opposite. BDO treated banking like shoe retail. It chased footfall. It opened where people already were. It made deposits easy and withdrawals faster. It answered to the rhythm of payday Fridays and remittance Sundays rather than to the rhythm of central banking lunch hours.

Over the next few sections, we will walk through the Acme origins, the cultural DNA that turned a family-owned savings bank into an institutional juggernaut, the audacious 2006 hostile takeover of Equitable PCI that catapulted BDO to number one and never let it back down, the quietly extraordinary 27-year stewardship of CEO Nestor Tan, the hidden engines that keep compounding, and the question every investor must eventually ask: when the country's malls become less central to Filipino life, does the moat hold?

Let us begin where every great platform story begins — with a restless founder who refused to believe the world had to stay the way he found it.

II. The Backdrop: The SM Empire & The Sy Legacy

In 1936, a twelve-year-old boy named Henry Sy arrived in Manila on a steamer from Jinjiang, Fujian. His father ran a sari-sari store in Quiapo — the kind of cramped neighborhood shop that sold rice by the cup and soap by the sachet. The boy slept on a folding cot near the cash drawer. He learned English by reading labels. He learned arithmetic by counting change. And, most consequentially, he learned that in a poor country, the merchant who can extend a little trust — the merchant who will let a customer pay next week — is the merchant who earns a lifetime of loyalty.

When World War II ravaged Manila, the Sy family store burned. Henry rebuilt. In 1958, with a partner, he opened a small storefront in downtown Manila selling imported American shoes. He called it Shoemart, shortened eventually to SM. The shoes were not elegant. They were sturdy. They were a size for every foot. And because Henry priced them just below the local competition, he could turn inventory twice as fast. By the late 1960s, Shoemart had expanded into a department store. By the early 1980s, it had become the dominant mall developer in the Philippines. By the 2000s, the SM Group was the largest retail conglomerate in the country, with malls, supermarkets, residential real estate, hotels, mining, and — crucially for this story — a bank.

The bank had entered the Sy orbit almost as an afterthought. In 1976, the family acquired a small thrift institution called Acme Savings Bank. In 1994, it was renamed Banco de Oro Savings and Mortgage Bank. It had a handful of branches. It financed car loans and small mortgages. Most observers considered it a treasury function — a place where SM's cash from its mall tenants could sit overnight and earn a modest return. The broader banking establishment in Manila at the time was dominated by old-money families like the Ayalas (BPI), the Yuchengcos (RCBC), and the Ty family (Metrobank). These institutions were polished, political, and polite. They were also sleepy.

Henry Sy looked at the sleepy banks and saw what he had seen decades earlier in the sleepy shoe stores: a door left ajar for someone willing to work weekends.

The cultural DNA of BDO crystallized around a single internal slogan that would eventually become external marketing: "We Find Ways." In a country where bureaucracy is a national pastime, where every transaction carries three forms and two signatures, BDO built a reputation for solving the customer's problem rather than citing the rulebook. Need to open an account on a Sunday? We find ways. Need to wire money to a province with no major bank branch? We find ways. Need a mortgage at a hour when other banks are closed? We find ways. It is the kind of slogan that sounds vaguely corny in English and absolutely native in Tagalog.

The critical human pivot arrived when Teresita "Tessie" Sy-Coson, Henry's eldest daughter, took the lead on banking. Tessie had grown up behind the Shoemart register. She had watched her father build a retail empire on the gospel of hustle. But she also understood, perhaps more clearly than her father, that to play in the global financial system you needed Western-grade risk management, disclosure, and governance. She was the one who pushed the bank to professionalize, to list on the Philippine Stock Exchange, to adopt Basel capital standards ahead of the local regulatory curve, and to attract foreign institutional shareholders who demanded transparency.

Under Tessie's stewardship, BDO transitioned from a family treasury to a public company with ambition. What happened next was the transaction that turned an upstart into a titan.

III. The Inflection Point: The Equitable PCI "David vs. Goliath" Merger

Picture a Manila hotel ballroom in the autumn of 2005. The room is thick with lawyers, bankers, and Social Security System board members. The subject on the table is what to do with the government's 28 percent stake in Equitable PCI Bank, the country's third-largest bank and the crown jewel of the Go family empire. For months, the bidding has been a slow-motion war of attrition. BDO, the upstart savings-bank-turned-universal-bank, has been circling. The Go family has been fighting. And the board of Social Security has been caught between regulators, politicians, and the cold logic of the highest bid.

To understand why this mattered, you have to understand what Equitable PCI was in 2005. It was the result of a 1999 merger between Equitable Banking Corporation and Philippine Commercial International Bank, two of the oldest and most establishment-rooted banks in the country. It held more than 200 billion pesos in deposits. It had 470 branches. It had the largest ATM network outside the top two. It had a corporate lending book full of prestige clients. And crucially, it had an international remittance franchise that blanketed the Gulf states, Hong Kong, and North America — the vital artery through which overseas Filipino workers sent money home.

BDO was smaller. It had fewer branches. It had less brand heritage. What it had was the SM Group's captive footfall, a growing but still mid-tier corporate lending book, and a thesis that Filipino retail banking was going to be won on the back of consumer convenience, not corporate relationships.

The merger path was anything but clean. It was, as Ben and David might say, a genuine knife fight. BDO spent the years from 2004 to 2007 methodically accumulating every share it could get its hands on. It courted the Social Security System, which owned 28 percent. It courted the Government Service Insurance System, which owned another significant block. It tendered for shares in the open market. The Go family, which had controlled Equitable for decades, mounted legal challenges, filed injunctions, and questioned the valuation. Editorial writers accused BDO of being too aggressive. Regulators occasionally wavered. For a stretch of 2006, the deal looked dead.

It was not dead. It was being ground forward by a combination of patient capital from the Sy family and steely execution from the BDO management team under CEO Nestor Tan. By the end of 2006, BDO had acquired enough shares and enough board influence to force the issue. In May 2007, the merger completed. The combined entity became BDO Unibank, instantly the largest bank in the Philippines by assets, deposits, and branches. Metrobank, which had held the number one spot for most of the prior decade, was dethroned.

Now, the Acquired question: did BDO overpay? The price-to-book multiple they paid for Equitable PCI was higher than what regional peers like DBS in Singapore or CIMB in Malaysia had been paying for acquisitions around that time. Critics argued that BDO was buying a franchise burdened with legacy costs, a unionized workforce, and cultural baggage from the messy Equitable-PCI integration of 1999. Some analysts believed BDO would struggle to digest the deal.

The verdict from almost two decades of hindsight is that it was a value-creating masterstroke. BDO did not just buy a bank. It bought a distribution network that would have taken fifteen years to build organically. It bought a corporate lending relationship book that gave it instant credibility with the country's largest business groups. It bought a remittance franchise that plugged directly into the single most important structural cash flow in the Philippine economy. And most importantly, it bought scale — the scale to spread fixed costs like technology, compliance, and branch infrastructure across a dramatically larger revenue base.

Within five years of the merger, BDO's return on equity had climbed into the mid-teens, its cost-to-income ratio had started to compress, and its deposit base had ballooned as the combined branch network absorbed customers from weaker competitors. The dethroning of Metrobank was not a temporary event. It was a permanent rearrangement of the Philippine banking hierarchy. And it set the stage for everything that followed — the GE Money acquisition, the Citibank consumer portfolio purchase, the One Network Bank absorption, and the transformation from a Manila-centric universal bank into a nationwide financial utility.

With the merger complete and the throne secured, the next question was who would keep the seat warm for the next two decades.

IV. Management Deep-Dive: The Nestor Tan Era

In a region where chief executives turn over like seasonal collections, Nestor Tan has held the same job for twenty-seven years. He became President and CEO of BDO in 1998, when the bank was still a second-tier thrift institution with modest ambitions. He remains in that role today, in 2026, presiding over a franchise more than fifty times its size at the moment of his appointment.

Tan is not a flamboyant executive. He does not do magazine covers. He does not write books. He rarely speaks at global conferences. His profile inside the Philippines is that of a technocrat's technocrat — meticulous about numbers, obsessed with risk, uninterested in the kind of banker-celebrity lifestyle that characterized the freewheeling era of Asian finance in the 1990s. Before BDO, he spent years at Bankers Trust and at the Bancom Group, one of the most influential financial institutions in Philippine history. He cut his teeth on corporate banking, trade finance, and the complex cross-border deals that defined 1980s Manila.

The Sy family's decision to back Tan for the long haul was itself a strategic choice. Plenty of Asian family conglomerates run their banks as princely fiefdoms — staffed by relatives, run as extensions of the parent holding company, and inclined to take outsized risks to please the patriarch. The Sys did the opposite. They installed a professional CEO. They granted him meaningful autonomy. They resisted the temptation to lard the bank's loan book with insider credits to SM tenants or related parties. They professionalized the board. They built a reputation with regulators for playing by the rules and often ahead of the rules.

This choice paid off during every crisis. During the 2008 Global Financial Crisis, BDO had almost zero exposure to the subprime and structured credit products that wrecked Western banks. During the 2013 taper tantrum, BDO's funding base was almost entirely domestic deposits, insulating it from the emerging market capital flight. During the COVID pandemic in 2020 and 2021, BDO's loan loss provisions were raised preemptively, its capital ratios held firm, and its branch network stayed open through lockdowns because the bank had classified itself as essential infrastructure. At no point in the last two decades has BDO been the bank that needed a bailout, the bank that embarrassed the regulator, or the bank that shocked the market with a hidden loss.

The alignment of incentives is worth unpacking. Tan is not a hired gun with a short-term options package. He holds equity in the bank. His tenure has given him time horizons that few public company CEOs ever achieve. And the Sy family, which controls roughly 40 percent of BDO through SM Investments Corporation, thinks in generations rather than quarters. This is what gives BDO its unusual willingness to invest through cycles — to keep expanding branches during recessions, to acquire distressed portfolios when others are selling, to absorb one-time integration costs without flinching at the short-term EPS impact.

Teresita Sy-Coson, as Chairperson, provides the family voice at the board. She is not a ceremonial chair. She asks hard questions. She has a particular focus on consumer-facing strategy, digital transformation, and the cultural integrity of the branch network. Nestor Tan runs operations. Tessie sets tone and guards legacy. The division of labor is the kind of thing business school cases are written about — and in fact, several have been.

There is also the question of succession, which is the polite conversation in every Manila banking circle. Tan is now in his late sixties. He has been grooming a bench of senior executives for years, and the bank has been explicit about the existence of a succession plan, even if the details remain confidential. The bench includes heads of investment banking, consumer banking, treasury, and the digital platform. When the transition eventually occurs, it will be the most-watched CEO handover in Philippine corporate history. For now, Tan continues.

The consequence of this governance stability shows up in a metric that is easy to miss but impossible to fake: corporate governance scores from international bodies like the ASEAN Corporate Governance Scorecard consistently place BDO near the top of Philippine listed companies. Foreign institutional investors, who have been historically skittish about Philippine banks due to concentrated family ownership, hold nearly a quarter of the free float. BDO is one of the very few Philippine listed companies that trades with any real institutional foreign interest.

With the leadership structure understood, we can now turn to the engines that make the machine run.

V. The Hidden Engines: Segments & New Frontiers

Peel open any universal bank annual report and you find the same boilerplate: corporate banking, consumer banking, treasury, trust. The labels are identical. The economics are not. BDO's segment disclosure tells a story that most casual readers miss entirely — a story about where the money really comes from, where it is growing fastest, and where the bank is quietly planting flags for the next decade.

The rough split of contribution looks like this: corporate banking accounts for roughly 40 percent of revenues, consumer banking accounts for another 40 percent, and the "others" bucket — which includes treasury, trust, remittances, insurance, and investment banking — accounts for the remaining 20 percent. This 40-40-20 distribution is itself a strategic statement. It means BDO is not overly dependent on any single lending book. It means that even if corporate credit slows in a cyclical downturn, consumer fee income and remittance flows keep the engine running.

The first hidden gem is BDO Network Bank. Formerly known as One Network Bank, this was a rural banking franchise that BDO acquired and rebranded. Rural banks in the Philippines operate under a different regulatory regime than universal banks. They can lend to small farmers, sari-sari store owners, tricycle drivers, and micro-entrepreneurs with loan sizes ranging from as little as five thousand pesos to a few hundred thousand. These are the Filipinos that universal banks historically ignored — not because they lacked creditworthiness, but because the cost-to-serve on a traditional branch model was prohibitive. BDO Network Bank changed that. It uses simplified onboarding, community-level credit committees, and digital tools to extend credit to micro, small, and medium enterprises, known locally as MSMEs, across the provinces. Loan growth here has consistently outpaced the parent bank, and the net interest margins are structurally higher because rural credit commands a premium over metropolitan prime lending.

Why does this matter? Because the MSME segment in the Philippines represents more than 99 percent of registered businesses and employs the majority of the workforce. It is the largest underbanked opportunity in the country. If BDO can extend its digital-first rural model across the archipelago, it can onboard millions of new customers at marginal cost — customers who will eventually graduate into consumer banking, credit cards, and mortgage lending.

The second hidden gem is BDO Life. This is the bancassurance play — the selling of life insurance, savings products, and protection policies through bank branches. Bancassurance is a classic financial services pattern. The bank already has the customer relationship. The bank already has the trust. The bank already has the distribution. All the bank needs is the product. BDO partnered with international insurers before eventually taking full ownership of the insurance subsidiary. The result is a growing life insurance franchise that distributes through the bank's 1,700 branches and cross-sells to the bank's 65 million customer accounts.

The economics of bancassurance are quietly beautiful. The cost of acquiring an insurance customer through a bank branch is a fraction of the cost of acquiring that same customer through an independent agent. The persistency of the policy — the probability that the customer keeps paying premiums year after year — is higher because the premium is debited automatically from the customer's BDO savings account. And the float generated by the insurance business gives BDO another pool of long-duration capital to deploy. BDO Life has been growing at double-digit rates for years, and it is one of the pieces of the franchise that remains undervalued by external analysts who tend to focus on the core banking numbers.

The third frontier is digital. Here, the narrative gets more complex. Over the past five years, the Philippine digital payments market has been upended by GCash, a mobile wallet owned by Globe Telecom in partnership with Ant Group, and Maya (formerly PayMaya), backed by PLDT and a consortium of international investors. These fintech challengers have built user bases in the tens of millions by offering free peer-to-peer transfers, QR code payments at sari-sari stores, and micro-investment products. For a period in 2020 and 2021, it looked like the digital wallets might disintermediate traditional banks entirely.

BDO's response was measured. It built BDO Pay, its own digital wallet, integrated into the core banking app. It joined InstaPay, the national real-time payments rail, so that transfers between banks and wallets became near-instantaneous. It invested in API banking so that businesses could plug directly into BDO's rails for payroll, supplier payments, and collections. It did not try to out-flashy the fintech challengers. It did not burn billions on customer acquisition subsidies. It simply made sure that when a Filipino customer wanted to move money, they could do so using BDO's infrastructure at zero or near-zero cost.

The question investors must wrestle with is whether BDO is a dinosaur slowly being disrupted or a cloaked technology company whose physical branch network is actually the moat. The answer so far has been neither. BDO has absorbed the digital transition without losing market share. Deposits have grown. Transactions have migrated to digital channels, reducing cost-to-serve. And the branch network continues to serve as the trust anchor for a population that, despite rising smartphone penetration, still prefers to deposit cash in a teller's hand on payday.

With the engines running on multiple cylinders, we turn now to how BDO allocates its capital — the acquisition machine that has quietly reshaped Philippine finance.

VI. Capital Deployment & The "Acquisition Machine"

Great bank management is, at its core, a capital allocation exercise. You collect deposits at one price, you lend at another, you provision for losses, you pay your taxes, you reinvest in technology and branches, and whatever is left flows to shareholders. Most banks are mediocre at this. A handful are genuinely excellent. BDO, over the past two decades, has earned a place in the small club of banks that treat capital allocation as a continuous, disciplined, and unsentimental exercise.

Consider the acquisition track record beyond the Equitable PCI transformation. In 2009, BDO acquired GE Money Bank Philippines, the consumer finance arm of General Electric that had been unwinding its global financial services operations in the wake of the GFC. The acquisition added a specialist auto loan and personal loan book, along with a network of specialized consumer finance branches. It was a tack-on deal — small in absolute size, high in strategic fit, and executed at a price that reflected GE's motivated-seller position.

In 2010, BDO acquired American Express's Philippine banking business, picking up the card issuing franchise and the associated merchant relationships. Then came the acquisition of Real Bank, another thrift institution, absorbed to expand the branch footprint. In 2016, BDO acquired the Philippine retail banking operations of Deutsche Bank. And the roll-up continued through the 2010s and into the 2020s with a series of portfolio purchases — the Citibank consumer banking business, the Standard Chartered retail portfolio, and smaller bolt-ons that rarely made international headlines but steadily compounded BDO's share of the Philippine consumer.

The BDO playbook is instructive. They do not buy banks to diversify geographically. They do not buy banks to chase fashionable product categories. They buy portfolios where the integration risk is low because the underlying business is similar to what BDO already does, and the return on equity is high because the acquired portfolio can be funded with BDO's lower-cost deposit base. This is the classic "buy and integrate" pattern that has driven compound returns at institutions like JPMorgan Chase in the United States and DBS in Singapore, adapted for the Philippine context.

The deals are also structured to be accretive quickly. BDO uses a combination of cash from retained earnings, equity raises, and in select cases, hybrid instruments like Tier 2 capital notes. The bank has been a regular issuer in the domestic peso bond market, and it has tapped international markets for dollar-denominated capital when rate conditions favored offshore funding. The rights offerings — the mechanism by which banks raise fresh equity from existing shareholders — have been executed at valuations that, in hindsight, represented strong returns for participating investors.

The discipline on the capital-return side is equally notable. BDO has maintained a dividend payout ratio that balances shareholder returns with the need to retain capital for growth. Unlike some Western banks that return 60 percent or more of earnings to shareholders, BDO has historically retained the majority of its profits. The logic is straightforward: in a country where nominal loan growth runs in double digits, and where every percentage point of market share gain creates durable competitive advantage, retaining capital to fund growth is almost always a better use of money than dividends.

The result is a Common Equity Tier 1 ratio — the headline measure of a bank's capital strength — that consistently sits well above regulatory minimums and, by global standards, looks remarkably strong for an emerging markets bank. Western banks often operate with capital ratios that barely clear regulatory floors, forcing them to either cut dividends or issue dilutive equity during downturns. BDO has the buffer to absorb shocks, fund acquisitions, and keep lending through cycles. This is the hidden moat of the balance sheet.

A useful second-layer observation: the loan loss provisioning discipline during the pandemic was a character-revealing moment. BDO front-loaded provisions in 2020, accepted a depressed earnings year, and emerged in 2021 and 2022 with a clean book. Compare that to some regional peers who staggered provisions, were later forced to top up, and faced awkward questions from auditors. The preemptive posture is not glamorous, but it is the kind of behavior that compounds trust with regulators, creditors, and institutional investors over decades.

With the capital structure understood, we can now move into the strategic frameworks — the why-does-this-business-persist analysis that is the soul of every Acquired episode.

VII. The Strategy Analysis: 7 Powers & 5 Forces

To understand why BDO wins — and why competitors have struggled to displace it — we need to look at the business through the twin lenses of Hamilton Helmer's Seven Powers and Michael Porter's Five Forces. These are not theoretical exercises. They are the scaffolding on which fundamental investors build their conviction.

Let us start with Network Effects. Traditional banks rarely enjoy true network effects in the way that Visa or Mastercard do. Banks are not marketplaces. A depositor does not benefit from the presence of other depositors. But BDO enjoys a version of network economics that comes from physical ubiquity. When you know that a BDO ATM will be at every mall, every major intersection, every airport, every bus terminal, and every ferry port — your willingness to open a BDO account rises. And as more customers open BDO accounts, more merchants accept BDO, more employers use BDO for payroll, and more government agencies route payments through BDO. The physical density compounds into a self-reinforcing loop where BDO becomes the default.

The second power is Cornered Resource. This is the SM Mall relationship — and it is genuinely unique. SM Prime Holdings operates more than 80 malls in the Philippines, and they are not just retail properties. They are the social infrastructure of the middle class. In a country where the public plaza has been displaced by the air-conditioned mall, where families spend Saturdays shopping, watching movies, and eating meals inside malls, the bank that is physically inside every mall has access to a stream of potential customers that no competitor can easily replicate. Other banks can rent retail space, but they cannot replicate the preferential placement, the co-marketing with anchor tenants, and the decades of accumulated customer routine that come from sharing a founder family with the country's largest mall operator.

The third power is Scale Economies. BDO's deposit base — more than 3 trillion pesos — is the cheapest funding cost structure in the Philippine banking industry. The majority of that deposit base is low-cost current and savings accounts, commonly called CASA in banking parlance. CASA means that customers are effectively giving BDO money for free or near-free, in exchange for the convenience of being able to access it whenever they need it. When your funding cost is a fraction of your competitors', every loan you write is structurally more profitable. Every basis point of spread you extend is durably wider. This is not a temporary advantage. It is a structural feature that gets more pronounced as the balance sheet grows.

The fourth power, Counter-Positioning, is where it gets interesting. BDO's model is not a model that incumbents can easily imitate without damaging their existing franchises. If BPI or Metrobank tried to match BDO's weekend hours, mall-based branches, and remittance-focused operations, they would have to rewire their cost structures, retrain their workforce, and potentially dilute their existing premium brand positioning. This creates a kind of incumbent paralysis that BDO has exploited for two decades.

The fifth, sixth, and seventh powers — Switching Costs, Branding, and Process Power — are all present in varying degrees. Switching bank accounts in the Philippines is non-trivial because of payroll arrangements, auto-debit mandates, and the sheer inertia of habit. The BDO brand, despite being less elegant than BPI's premium positioning, carries deep trust with the mass market. And BDO's internal processes, particularly around risk management, credit underwriting, and branch operations, have been refined over decades.

Now, Porter's Five Forces. The Threat of New Entrants is moderate. Digital banks have arrived. GoTyme, Tonik, Maya Bank, and others have launched with aggressive customer acquisition strategies. But the Bangko Sentral ng Pilipinas — the central bank — has been measured in issuing new licenses, and the economics of pure digital banking in a country with uneven smartphone adoption remain challenging. BDO's physicality is a genuine moat against a pure-digital challenger. On the Bargaining Power of Suppliers, the answer is low — BDO's suppliers are its depositors, and retail depositors have limited leverage. On the Bargaining Power of Buyers, retail customers are fragmented and have limited alternatives, while corporate customers have more negotiating power but are also stickier. The Threat of Substitutes includes fintech wallets and informal lending, but neither has fully displaced the need for a chartered bank in commerce. And Industry Rivalry, while intense, is structurally constrained by regulation — no Philippine bank is allowed to undermine financial stability through predatory pricing.

The synthesis is straightforward. BDO operates at the intersection of three genuine structural advantages: distribution density, low-cost funding, and a symbiotic relationship with the country's largest retail ecosystem. These advantages compound. They are not going away quickly. And they are the reason why, despite the arrival of dozens of digital challengers over the past decade, BDO's market share has been remarkably stable.

The strategy analysis leads naturally to the playbook — the transferable lessons that make BDO's story valuable beyond the specific context of Philippine banking.

VIII. The Playbook: Lessons from BDO

The first lesson is that convenience itself can be a product. Most banks in the developing world compete on interest rates, branch aesthetics, or brand prestige. BDO competed on something more elemental: being open when the customer was free. A Filipino factory worker who finishes her shift at 5 PM on a Friday does not want to take time off work on Monday morning to deposit her paycheck. She wants to handle her finances on Saturday afternoon while doing her grocery shopping. If you are the bank inside the mall where she shops, and you are open until 7 PM, you have essentially zero marketing cost per customer acquired. The customer comes to you because you are where she already is.

This insight generalizes far beyond banking. It is why McDonald's drive-throughs revolutionized fast food, why Amazon Prime reshaped retail expectations, why the original Starbucks third-place strategy rewrote café economics. The principle is that in industries where the product is roughly commoditized, the friction of access becomes the differentiator. Banking in the early 2000s was roughly commoditized — interest rates were regulated, products were similar, and brand equity was elusive. Convenience became the wedge.

The second lesson is the ecosystem flywheel. SM builds a mall. The mall attracts tenants. The tenants need working capital and payroll services, which BDO provides. The mall attracts shoppers. The shoppers need ATMs, credit cards, and remittance services, which BDO provides. The tenants pay rent to SM. The shoppers pay tenants. The money flows through BDO accounts at every step. The bank is not just a service provider to the ecosystem; it is a beneficiary of every transaction within the ecosystem.

This flywheel is harder to build than it looks. It requires a parent company that actually has control over the retail real estate. It requires a bank that is willing to be integrated into the mall operator's plans — not as an independent tenant, but as a strategic partner. And it requires patience. The SM-BDO flywheel took decades to mature. It is unlikely to be quickly replicated by a competitor without an equivalent retail anchor.

The third lesson is about executive continuity. Twenty-seven years of Nestor Tan at the top is extraordinary by any measure. In banking, where credit cycles run ten to fifteen years and where the memory of the last crisis is the foundation of risk discipline, long tenure compounds value in ways that are hard to measure but easy to see in the aggregate. Tan has personally been through the Asian Financial Crisis of 1997, the dot-com bust of 2001, the Global Financial Crisis of 2008, the taper tantrum of 2013, the COVID shock of 2020, and the inflation-rate-shock cycle of 2022 to 2024. Each of those experiences has shaped how BDO underwrites loans, how it manages liquidity, how it stress-tests its balance sheet. A new CEO arriving today would have to reconstruct that institutional memory from scratch.

The fourth lesson, perhaps the most uncomfortable for Western-trained investors, is that family ownership is not necessarily a governance weakness. Conventional wisdom holds that family-controlled companies suffer from nepotism, short-term thinking, and conflicts of interest. BDO's experience suggests the opposite can be true. The Sy family's long-term ownership horizon has allowed the bank to invest through cycles, to retain capital for acquisitions, and to resist the short-termism that plagues many publicly-held Western banks. The discipline required is professional management with meaningful autonomy — which the Sys, to their credit, provided.

The fifth lesson is about the power of serving a population that other banks ignore. BDO built much of its franchise by serving overseas Filipino workers, a demographic that global banks historically treated as an afterthought. OFW remittances represent close to 10 percent of Philippine GDP. The money comes in every month, every year, from Saudi Arabia, Hong Kong, Dubai, Tokyo, New York, and dozens of other cities. BDO built the rails to receive that money efficiently and reliably. Once the money was in a BDO account, the bank had the opportunity to sell savings products, investment products, loans, and insurance. The remittance service was the loss-leader. The relationship was the profit.

These lessons feed directly into the investment thesis, which is the subject of the next section.

IX. Bear vs. Bull Case

Let us start with the bear case, because that is where serious investors spend their time.

The first bear concern is digital disruption. The Philippines is one of the most mobile-first economies on the planet. Smartphone penetration has crossed 70 percent. GCash alone has surpassed 90 million registered users. A generation of Filipinos is growing up with their primary financial relationship being a mobile wallet, not a bank branch. If this generation never graduates to traditional banking — if they stay on wallets for deposits, on buy-now-pay-later for credit, on fintech platforms for investments — then BDO's physical moat becomes a physical liability. The 1,700 branches become stranded assets. The armored car fleet becomes a cost center with no corresponding revenue.

The counter-argument is that mobile wallets, while convenient for small-value transactions, have not proven themselves capable of being primary financial relationships for large deposits, mortgages, or business banking. GCash cannot extend a 20-year home loan. Maya cannot underwrite working capital for a mid-sized manufacturer. The regulatory barriers to becoming a full-service bank are real, and BDO holds the license, the capital, and the trust infrastructure that cannot be replicated overnight.

The second bear concern is geographic concentration. BDO is a pure-play Philippines bet. There is no Singapore subsidiary, no Indonesia expansion, no Vietnam acquisition. If the Philippines enters a prolonged economic downturn, BDO has nowhere to hide. The country's GDP growth has been strong — averaging 5 to 6 percent annually for much of the past decade — but it is also exposed to global remittance flows, commodity cycles, US dollar strength, and periodic political volatility. The Ferdinand Marcos Jr. administration, which took office in 2022, has generally been pro-business, but the political risk premium on Philippine assets has historically been higher than on comparable ASEAN peers.

The third bear concern is the end of the mall era. If Filipino consumer habits shift decisively toward e-commerce, away from physical retail, the SM-BDO flywheel loses its centrifugal force. Malls remain highly relevant today, but the Lazada-Shopee duopoly and the expansion of TikTok Shop and other direct-to-consumer platforms could erode mall footfall over time. If fewer people visit malls, fewer people pass BDO branches, fewer people deposit cash, and the physical moat becomes less effective.

The fourth bear concern, more technical, is interest rate sensitivity. Banks earn net interest income on the spread between what they charge borrowers and what they pay depositors. In a rising rate environment, that spread can widen — but only temporarily. Eventually, rising deposit rates compress margins, and if loan growth slows simultaneously, earnings can decline. BDO has navigated the 2022-2024 rate cycle well, but the rate environment going forward is uncertain, and any sustained compression of net interest margins would hit earnings directly.

Now, the bull case.

The first bull pillar is what could be called the "LVMH of the Philippines" thesis. BDO is not selling products; it is selling the luxury of convenience to a rising middle class. The Philippine middle class is projected to continue expanding through the 2030s, driven by remittances, BPO sector employment, and the natural dividends of a young demographic profile. A larger middle class means more credit cards, more mortgages, more auto loans, more wealth management, more insurance. BDO is positioned to capture a disproportionate share of that growth.

The second bull pillar is the remittance franchise. OFW remittances to the Philippines have continued to grow year after year, even through the pandemic, even through global economic slowdowns. The Philippines is one of the top remittance-receiving countries in the world. And BDO is one of the primary conduits for that money. This is a recurring, structurally-sticky, fee-generating business that does not require capital and does not incur credit risk. It is pure royalty on a macroeconomic flow.

The third bull pillar is MSME lending headroom. The Philippines has one of the lowest banking penetration rates in Southeast Asia relative to its GDP. Household credit as a percentage of GDP is well below that of Thailand, Malaysia, or Singapore. MSME credit is even more underdeveloped. If BDO can extend credit to even a modest fraction of the country's small businesses over the next decade, it adds incremental revenue at attractive spreads without meaningfully changing the risk profile of the balance sheet.

The fourth bull pillar is the digital transformation already in progress. BDO is not standing still on technology. It has invested in mobile banking, in API integration, in data analytics, in cybersecurity. The branch network, far from being a liability, provides a customer acquisition and trust-anchor advantage that pure-digital banks have struggled to match.

The Hamilton Helmer lens reinforces the bull case. Scale economies, cornered resources, and counter-positioning — the three structural powers most evident at BDO — are the powers that Helmer identifies as most durable. Network effects and switching costs provide additional reinforcement. The five-forces lens suggests that rivalry, while real, is structurally bounded by regulation and by the capital requirements of universal banking.

The key performance indicators for investors to track are refreshingly few. First, CASA ratio — the proportion of deposits in current and savings accounts versus time deposits. This is the single best proxy for BDO's funding cost advantage. Second, cost-to-income ratio — the measure of operating efficiency that captures whether the branch network and digital investments are generating operating leverage. Third, loan growth by segment, particularly in consumer and MSME — the proxy for whether BDO is capturing the structural growth in Philippine household and small business credit. These three metrics, followed over multi-year horizons, tell you almost everything important about whether the thesis is intact.

Which brings us to the conclusion.

X. Conclusion

Step back from the numbers for a moment and consider the shape of what BDO has built. This is a company whose founder started life as an immigrant shoe salesman, whose early banking business was a rounding error on a retail conglomerate's balance sheet, and whose trajectory was shaped by the audacity to attempt a takeover of an institution several times its size. Along the way, it stitched together more than a dozen acquisitions, survived multiple financial crises without a wobble, and became the largest bank in a country of 115 million people.

The deeper observation is that BDO is not just a bank. It is a bet on the Filipino middle class and, more specifically, on the enduring relevance of physical presence in a financial system serving an aspirational but still cash-heavy economy. Every Saturday afternoon, millions of Filipinos walk through SM malls with their families. Many of them stop at a BDO branch. Some deposit the week's earnings. Some pay a utility bill. Some pick up a Western Union transfer from a brother in Riyadh. Some open a savings account for a child. The volume of these micro-interactions, compounded over decades, is the true asset on BDO's balance sheet. It is an asset that does not show up in any regulatory filing. It is the collective habit of a nation.

Is there any other bank in the world that has so successfully tied its physical presence to the retail habits of an entire population? Bank of America has scale in the United States, but no single conglomerate partner with the footfall of SM. DBS has digital dominance in Singapore, but a population one-twentieth the size of the Philippines. Kotak Mahindra in India has a similar family-ownership story, but operates in a more fragmented banking landscape. ICBC in China has unparalleled scale but is a state-owned giant with different strategic imperatives. In truth, BDO occupies a category of one — a family-controlled, professionally-managed, mall-anchored universal bank operating in a high-growth emerging market with deep remittance flows. The closest global analog may be Banco de Chile, which also combines family ownership with scale, or perhaps Turkiye's Garanti BBVA in an earlier era. But none of these truly replicate the BDO configuration.

The final reflection is that "We Find Ways" was never just a slogan. It was a 40-year execution plan. It was a cultural orientation that began with a shoe salesman who understood that the customer's problem — not the bank's policy — was the starting point of any good business. It was extended through decades of acquisitions, branch openings, regulatory battles, and technology investments. It was codified in the management philosophy of Nestor Tan, who has quietly overseen the transformation of a family treasury into an institutional fortress. And it is now being tested, as every great franchise eventually is, by the arrival of digital challengers, demographic shifts, and the relentless forces of competitive evolution.

For investors thinking in decades rather than quarters, BDO offers a window into what a patient, disciplined, family-anchored financial franchise can achieve in a market where most participants are either too impatient or too constrained to compound at its pace. The questions going forward are whether the next CEO will preserve the culture, whether the digital transition will be navigated without losing the physical advantage, and whether the Philippine macroeconomy will continue to provide the tailwind that has carried the last twenty years.

None of those questions have easy answers. All of them are worth watching. And all of them point back to a truth that has been evident from the Shoemart days: in the end, the customer goes where the customer is welcomed. BDO has spent half a century making sure that, in the Philippines, the welcome is always open, always lit, and always inside the mall.

XI. Top Long-Form Links for Further Reading

- SM Investments Corporation Annual Reports — the "bible" of Philippine conglomerate disclosure, providing consolidated context for the SM Group's retail, property, and financial services flywheel.

- Nestor Tan's interviews and speeches on the professionalization of the family firm, particularly remarks delivered at Asian Banking & Finance forums and Philippine business school case discussions.

- University of the Philippines School of Economics case studies on the Equitable PCI merger, which remain the most detailed academic analyses of the transaction's valuation, legal strategy, and post-merger integration.

- Bangko Sentral ng Pilipinas banking statistics and quarterly reports, which document the evolution of market share, capital ratios, and industry structure across Philippine banking.

- Teresita Sy-Coson's profiles in Forbes, Fortune, and the Philippine business press, which illuminate the transition from Henry Sy's entrepreneurial vision to the institutional architecture of the modern BDO Unibank.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube