BioCryst Pharmaceuticals: From Academic Spinout to Rare Disease Powerhouse

I. Introduction & Episode Roadmap

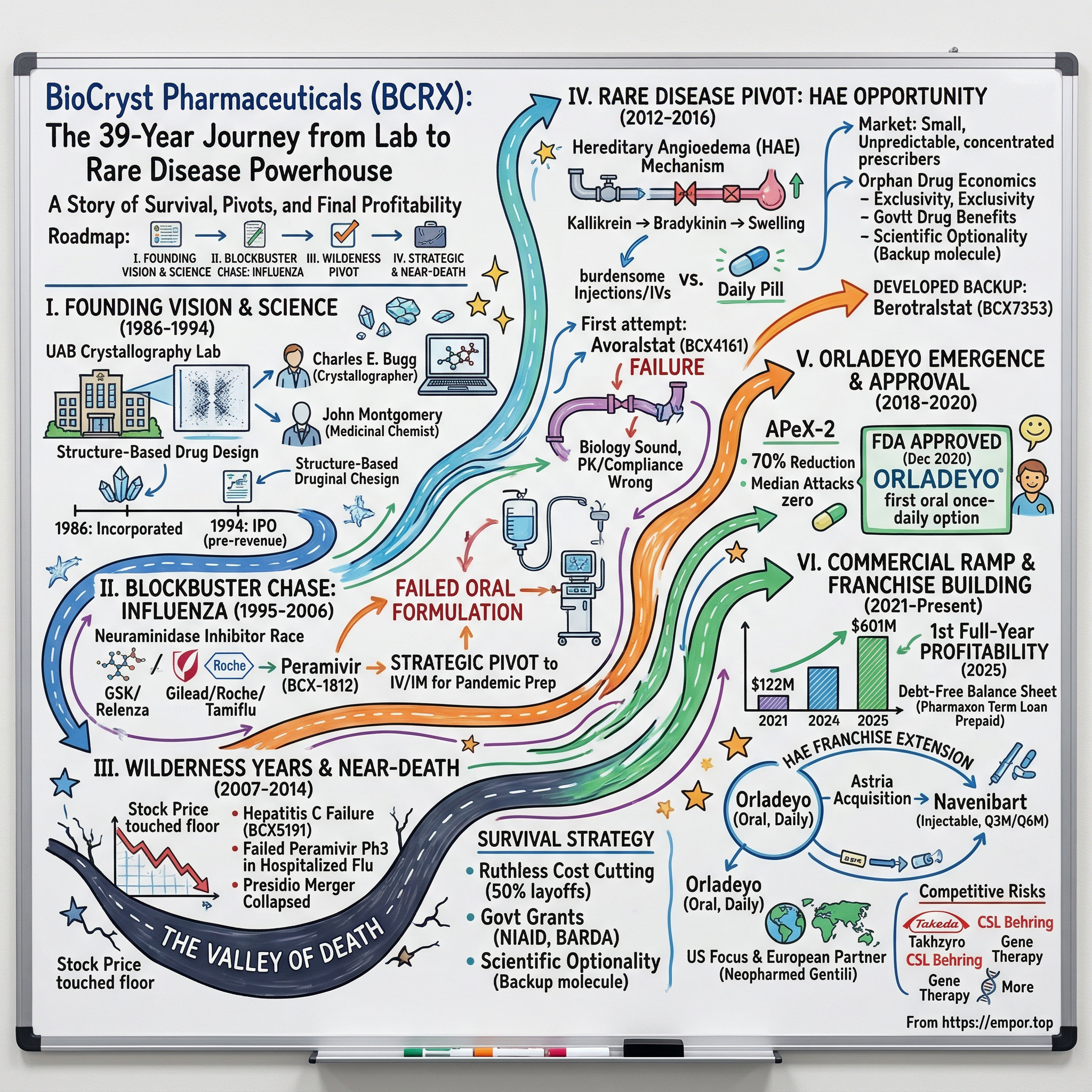

In the vast graveyard of biotech companies that burned through capital and never delivered a commercial product, BioCryst Pharmaceuticals stands as a stubborn exception. For thirty years, this Birmingham, Alabama-born company survived everything the industry could throw at it: failed clinical trials, delisting threats, a stock price that touched the floor, three major strategic pivots, and the constant question every board meeting: should we just shut this thing down?

The answer, remarkably, was always no.

Today, BioCryst generates over $600 million in annual revenue from Orladeyo, the first and only oral daily pill to prevent attacks of hereditary angioedema, a rare genetic disease that causes unpredictable, painful, and sometimes life-threatening episodes of swelling. The company achieved its first full-year profitability in 2025, nearly four decades after its founding. That sentence alone tells you everything about the brutal economics of biotech.

The central question of this story is deceptively simple: how did a company born in a university crystallography lab survive three decades of near-death experiences to finally crack the code on oral rare disease treatment? The answer involves a NASA astronaut, a $234 million government contract that went nowhere, a merger that collapsed within six weeks, a clinical trial failure that vaporized two-thirds of the company's market value overnight, and a backup drug that turned out to be the real breakthrough all along.

This is also a story about the economics of drug development, the wisdom of pivoting from blockbuster dreams to rare disease focus, and what separates the biotech companies that survive from the 90% that die. BioCryst's journey touches on structure-based drug design, pandemic preparedness, the orphan drug revolution, and the surprisingly powerful competitive advantage of turning an injectable therapy into a daily pill.

The themes that emerge are universal: when to abandon sunk costs, how to survive the valley of death, why differentiation matters more than superiority, and what thirty years of patience actually looks like in practice.

BioCryst's market capitalization today hovers around $1.9 billion, a fraction of the value its story might suggest. With $601 million in Orladeyo revenue in 2025 and first-year profitability, the company has crossed the Rubicon from "will they survive?" to "how big can they become?" But the stock still carries the scars of three decades of setbacks, and the market prices in real competitive risks from an increasingly crowded HAE landscape. Whether BioCryst's transformation is fully reflected in its share price, or whether significant value remains to be recognized, is the question that makes this story relevant to investors right now.

II. The Science Foundation & Founding Vision (1986-1994)

Every great biotech company begins with a scientist who believes something the rest of the world thinks is impossible.

In 1969, the University of Alabama at Birmingham hired a young crystallographer named Charles E. Bugg to start a lab. Bugg had come from Caltech, where he had studied under Bob Corey, and before that earned his PhD in Physical Chemistry at Rice and his bachelor's at Duke. He was a quiet, methodical scientist in a field that most pharmaceutical companies considered too slow and too expensive to matter. His specialty was X-ray crystallography: firing X-rays at protein crystals and using the diffraction patterns to map the three-dimensional structure of biological molecules, atom by atom.

Across campus at the Southern Research Institute, a medicinal chemist named John Montgomery had spent decades synthesizing anticancer compounds. Montgomery was a legend in his own right, eventually co-inventing five FDA-approved cancer drugs, including fludarabine and clofarabine. His genius was practical: given a molecular target, he could build a compound to hit it.

The partnership between Bugg and Montgomery was natural and powerful. Bugg could see the lock; Montgomery could build the key. Together, they pioneered what became known as structure-based drug design, an approach that sounds obvious in hindsight but was genuinely radical in the 1980s.

To understand why, consider how drugs were discovered at the time. Most pharmaceutical companies used what amounted to educated guessing: they would screen thousands of chemical compounds against a biological target and see which ones stuck. It was expensive, slow, and hit-or-miss. The idea that you could use a computer and a crystal structure to rationally design a molecule that would fit precisely into an enzyme's active site, like a hand sliding into a custom-fitted glove, was considered by most Big Pharma executives to be academic fantasy.

Bugg and Montgomery believed otherwise. And they found an unlikely ally in William M. Spencer III, a prominent Birmingham businessman who had co-founded Motion Industries and served on the boards of half the major companies in Alabama. Spencer had no background in biochemistry, but he understood something the scientists did not: how to raise money. In 1986, the three men incorporated BioCryst Limited, with Spencer connecting them to early investors through a vehicle called Molecular Engineering Associates.

Research began immediately, with drug synthesis commencing in 1987. That same year, Bugg's lab started determining the molecular structure of the influenza neuraminidase enzyme, a protein critical to how flu viruses spread from cell to cell. This work would define the company's first two decades.

The first full-time employee was Yarlagadda S. Babu, a crystallographer with a doctorate from the Indian Institute of Science who had spent five years on UAB's biochemistry faculty. Babu joined in 1988 and has remained with BioCryst ever since, rising to Chief Discovery Officer. He represents the living scientific continuity of the entire enterprise, from academic project to commercial rare disease company.

BioCryst's work even reached orbit. Larry DeLucas, who succeeded Bugg as director of the Center for Macromolecular Crystallography at UAB, flew aboard Space Shuttle mission STS-50 in June 1992 as a payload specialist. Influenza protein crystals were later flown on STS-77 in 1996 to grow higher-quality crystals in microgravity. "With the aid of NASA support," DeLucas said, "we successfully mapped the molecular structure of the influenza virus, exposing its weaknesses."

By 1991, BioCryst had published the first structure-based design of novel purine nucleoside phosphorylase inhibitors, a landmark in the field. The company's first drug candidate, BCX-34, entered clinical trials for psoriasis and T-cell lymphoma. On March 3, 1994, BioCryst completed its initial public offering on NASDAQ under the ticker BCRX, riding the early 1990s biotech wave. It was a pre-revenue company with no approved drugs, funded entirely on the promise that seeing molecular structures would lead to better medicines.

The early biotech wave of the early 1990s was marked by a unique kind of optimism. Amgen had launched Epogen in 1989. Genentech's human growth hormone was transforming endocrinology. The Human Genome Project was just getting started. The idea that computers and molecular biology could revolutionize medicine felt not just plausible but inevitable. BioCryst rode that wave to its IPO, but the wave would soon recede. The biotech bubble of the early 1990s gave way to a harsh correction, and companies that had gone public on promise alone would need to deliver results, or face extinction.

That promise would take nearly three decades to fully deliver.

III. The Blockbuster Chase: Influenza and the First Peak (1995-2006)

Picture a pharmaceutical war room in the late 1990s: whiteboards covered in molecular diagrams, scientists debating over crystallographic data, and executives watching the competition with equal parts admiration and dread. The race to develop neuraminidase inhibitors was one of the defining pharmaceutical competitions of the decade, and for BioCryst, it represented both the highest hopes and the cruelest lessons of its first chapter.

Three companies were chasing the same target: block the neuraminidase enzyme that influenza viruses need to escape from infected cells and spread through the body. Neuraminidase is essentially the flu virus's escape key. When the virus replicates inside a human cell and new viral particles assemble, they need neuraminidase to cut themselves free from the cell surface and move on to infect the next cell. Block neuraminidase, and the virus is trapped, unable to spread.

GlaxoSmithKline, working with Australia's Biota Holdings, developed zanamivir (Relenza), an inhaled powder. Gilead Sciences designed oseltamivir, which Roche licensed and developed as Tamiflu, an oral capsule. BioCryst, using its structure-based design expertise, created peramivir (BCX-1812), a cyclopentane-based inhibitor that was structurally distinct from both competitors.

The competitive dynamics were intense. Each company was using a slightly different chemical scaffold to achieve the same biological effect. Relenza was a transition-state analog that closely mimicked the natural substrate. Tamiflu was redesigned for oral bioavailability, sacrificing some structural fidelity for practical convenience. Peramivir, BioCryst's entry, used a cyclopentane backbone that gave it unique binding characteristics and, in laboratory assays, some of the tightest binding affinities of the three.

In September 1998, BioCryst signed a worldwide license agreement with Johnson & Johnson's R.W. Johnson Pharmaceutical Research Institute. J&J received exclusive global rights to peramivir, designated RWJ-270201, and Phase III trials of the oral formulation commenced in early 2000. For a small Birmingham biotech, partnering with J&J felt like validation.

Then came the blow. Around 2001, Johnson & Johnson terminated the collaboration and halted development, citing poor oral bioavailability. The drug simply was not being absorbed well enough when swallowed as a pill. Tamiflu and Relenza were already on the market. BioCryst had come in third in a winner-take-all race.

But the company made a critical strategic decision that would prove prescient: rather than abandoning peramivir entirely, BioCryst pivoted to an injectable formulation, intravenous and intramuscular. This gave peramivir a unique clinical niche. Tamiflu required swallowing a pill. Relenza required inhaling a powder. Neither worked for the sickest influenza patients, those on ventilators in intensive care units who could not swallow or inhale anything. An IV neuraminidase inhibitor was the missing piece of the pandemic preparedness arsenal.

The H5N1 avian influenza scare of the mid-2000s transformed peramivir from a struggling also-ran into a strategic national security asset. H5N1 was spreading globally with a human case fatality rate exceeding 60%, and public health authorities recognized that the existing antiviral toolkit was dangerously thin. In January 2007, the U.S. Department of Health and Human Services awarded BioCryst a landmark $102.6 million, four-year contract to develop injectable peramivir for "seasonal and life-threatening influenza, including avian flu." For a company that had been struggling to keep the lights on, it was a lifeline.

Then came the pandemic that nobody expected. In April 2009, H1N1 swine flu emerged and spread rapidly. On October 23, 2009, FDA Commissioner Margaret Hamburg issued an Emergency Use Authorization for intravenous peramivir, the first EUA ever granted for an unapproved drug product in U.S. history. The authorization was for critically ill hospitalized patients who could not take oral Tamiflu or inhaled Relenza. BioCryst's decision to pivot to an IV formulation after J&J walked away had created exactly the product the world suddenly needed.

But the H1N1 pandemic subsided faster than feared. The EUA expired in June 2010. And the deeper problem remained: BioCryst had a product filling a narrow niche in an already-served market. Peramivir's story was far from over, but its era as a potential blockbuster was.

Peramivir did eventually receive full FDA approval as RAPIVAB on December 19, 2014, based on a new NDA filed in December 2013 with continued BARDA funding support and data from over 2,700 subjects across 27 clinical trials. In 2017, the approval was expanded to pediatric patients aged two years and older. It became a modest revenue contributor and a permanent fixture in the U.S. Strategic National Stockpile, with the government awarding a $34.7 million contract in 2018 for 50,000 doses and another $69 million contract in September 2024 for up to 95,625 doses. RAPIVAB occupies a unique clinical niche that remains relevant decades after its initial development: it is still the only IV neuraminidase inhibitor available for critically ill hospitalized influenza patients who cannot take oral or inhaled medications.

But peramivir was never going to be a blockbuster. By the time it received full approval in 2014, Tamiflu had captured the vast majority of the influenza antiviral market. BioCryst's annual revenue from RAPIVAB remained in the tens of millions, not the hundreds. The drug was clinically important but commercially insufficient to sustain a company.

For investors, the influenza years taught a harsh lesson about biotech's winner-take-all dynamics. Being the best-designed molecule means nothing if you arrive late and in the wrong form factor. Tamiflu's oral convenience crushed everything in its path. BioCryst had entered the race with a potentially superior molecule, backed by compelling structural biology, but the market did not care about binding affinity data or crystallographic elegance. It cared about whether a patient could swallow a pill at home. That lesson about convenience and form factor would prove deeply relevant a decade later.

IV. The Wilderness Years: Hepatitis C Hopes & Near-Death (2007-2014)

Jon Stonehouse arrived as BioCryst's new CEO on January 8, 2007, succeeding founder Charles Bugg, who transitioned to non-executive Chairman. Stonehouse was a different breed from the crystallographers who had built the company. He had started as a Merck sales representative, risen through AstraZeneca's commercial ranks selling Prilosec, then moved to Merck KGaA where he led the acquisition of Serono, at the time Europe's largest biotech. The board hired him specifically for his "demonstrated skills in late-stage product development, as well as pharmaceutical sales and marketing." The scientists had built the science; now BioCryst needed someone who could build a business.

Stonehouse inherited a company still riding the peramivir government contract but facing an uncertain future. The $102.6 million HHS contract eventually grew into a $234.8 million BARDA commitment. That sounds impressive until you realize the money was earmarked for clinical development of a drug serving a narrow niche, not for building a sustainable commercial enterprise.

Meanwhile, BioCryst was also chasing the Hepatitis C gold rush. In the early 2010s, Hep C was the pharmaceutical industry's most frenzied land grab. The virus infected an estimated 170 million people worldwide, and the existing treatments, interferon injections that made patients feel like they had the flu for months, were brutal and only partially effective. Every major drugmaker was racing to develop all-oral, interferon-free cures.

The scale of the competition was staggering. Gilead Sciences paid $11 billion to acquire Pharmasset in November 2011, gaining the nucleotide drug that became Sovaldi. When Sovaldi launched in December 2013, it generated over $10 billion in its first full year, one of the most successful drug launches in history. Vertex, AbbVie, Bristol-Myers Squibb, and Merck all had programs. BioCryst's entry was BCX5191, a nucleoside analog inhibitor of HCV polymerase.

It never had a chance. The FDA raised concerns about preclinical toxicity at exposure levels that would be needed to reduce viral load in patients. BioCryst withdrew the IND application. Against the Gileads and AbbVies of the world, a small biotech with a single undifferentiated compound was bringing a knife to a thermonuclear war.

The Hep C failure carried a broader lesson about market selection that would inform BioCryst's subsequent strategy. In mass-market diseases with enormous commercial potential, the competitive dynamics are merciless. The same huge prize that attracts small biotechs also attracts the largest pharmaceutical companies in the world, armed with billions in capital and massive clinical development infrastructures. BioCryst was not unique in losing the Hep C race; dozens of companies pursued Hep C programs that never reached the market. The lesson was not that BioCryst's science was bad, but that the competitive arena was wrong for a company of its size.

In October 2012, BioCryst announced a merger with Presidio Pharmaceuticals, a private company, in an all-stock transaction valuing Presidio at approximately $101 million. The strategic rationale was to combine three oral Hep C antivirals into a competitive combination therapy. Six weeks later, on November 30, 2012, the merger was mutually terminated. Both parties had likely looked at the Gilead data emerging from clinical trials and realized that small-player Hep C combinations were dead on arrival.

The timing could not have been worse. Within a span of weeks in late 2012, three catastrophes converged: BCX5191's IND was withdrawn, the Presidio merger collapsed, and on November 7, 2012, an independent Data Monitoring Committee recommended terminating peramivir's Phase 3 trial in hospitalized influenza patients for futility. After enrolling 405 patients, the difference between peramivir and control groups was negligible. The $234.8 million government program had failed to demonstrate efficacy in its most important indication.

On December 7, 2012, BioCryst announced a restructuring that cut 50% of its workforce, eliminating 38 positions. Projected cash usage was slashed from $40 million in 2012 to $22-25 million in 2013. The company retained three programs: BCX4161, an early-stage oral kallikrein inhibitor for hereditary angioedema; BCX4430, a broad-spectrum antiviral; and the remnants of the Hep C program for a minimal chimpanzee study. Everything else was deprioritized or shelved.

What kept BioCryst alive during these years, when the stock price languished in the low single digits and the company had no commercial revenue? Two things: government grants and a scientific thesis that refused to die.

The antiviral program BCX4430, later renamed galidesivir, attracted significant non-dilutive government funding. NIAID awarded a contract valued up to $22 million in September 2013. When the 2014 Ebola epidemic erupted in West Africa, BARDA awarded an additional contract with a potential value of $35 million for BCX4430 development. These government contracts, totaling over $57 million in potential funding, were not glamorous. They did not generate headlines or stock price momentum. But they paid the bills and kept the labs running while BioCryst quietly redirected its drug design expertise toward a disease that almost nobody outside the rare disease community had heard of.

The company's survival through this period was not inevitable. Dozens of biotechs in similar positions simply shut down or sold their assets for pennies. Consider the odds: in late 2012, BioCryst had no commercial revenue, no approved drugs of commercial significance, three major program failures in rapid succession, a stock price in the low single digits, and a workforce that had just been cut in half. The Hep C market was being conquered by companies with fifty times BioCryst's resources. The influenza antiviral market was already served. The company's entire future rested on a single early-stage compound, BCX4161, targeting a rare disease that affected perhaps 10,000 diagnosed patients in the United States.

BioCryst survived because Stonehouse was willing to cut ruthlessly (half the workforce in a single day), because government grants provided a non-dilutive funding bridge, and because the company's core competence, designing enzyme inhibitors through structural analysis, turned out to be directly applicable to a new target. There was also an element of organizational resilience that deserves acknowledgment: J. Claude Bennett, the former UAB president and Harvard Medical School graduate who served as BioCryst's President and COO from 1997 to 2008, had helped establish a culture of scientific rigor that sustained the company's credibility with partners and regulators even through its darkest financial periods. When you have co-invented five FDA-approved cancer drugs on your founding team and a NASA astronaut helping grow your crystals in space, the scientific foundation is difficult to dismiss, even when the stock chart suggests the market has given up.

V. The Rare Disease Pivot: Finding the Real Opportunity (2012-2016)

To understand why BioCryst's pivot to hereditary angioedema was both audacious and brilliant, you first need to understand the disease itself.

Hereditary angioedema, or HAE, was first described in 1888 by Sir William Osler. It is a rare genetic disorder affecting roughly 1 in 50,000 people worldwide, an estimated 80,000 to 160,000 patients globally, with perhaps 6,600 to 13,000 diagnosed in the United States. Patients experience recurrent, unpredictable episodes of severe swelling in the extremities, face, abdomen, and most dangerously, the throat. Laryngeal attacks can obstruct the airway and historically carried a mortality rate of approximately 30% when untreated. Abdominal attacks cause severe cramping and vomiting so intense that patients are frequently misdiagnosed with appendicitis and subjected to unnecessary surgery.

The average untreated patient suffers an attack every one to two weeks, with each episode lasting three to four days. About 28% of patients experience at least one attack per week. The disease is so unpredictable that even between attacks, the constant anxiety of not knowing when the next episode will strike causes significant psychological burden. Studies show that 42.5% of HAE patients exhibit scores indicative of depressive symptomatology. Workers lose an average of 3.3 working days per attack; 70% say the disease has been a barrier to certain careers.

The molecular mechanism is elegant in its cruelty. In healthy people, a protein called C1 esterase inhibitor acts as a brake on the contact activation system, a cascade of enzymes in the blood. In HAE patients, this brake is either deficient (Type I, 85% of cases) or dysfunctional (Type II, 15%). Without it, Factor XII activates uncontrollably, converting prekallikrein into plasma kallikrein. Kallikrein then cleaves a protein called high-molecular-weight kininogen to release bradykinin, the molecule that causes blood vessels to become leaky. Fluid pours out of the vasculature into surrounding tissue, producing the characteristic swelling.

Think of it like a plumbing system: the C1 inhibitor is a shutoff valve, kallikrein is the water pressure, and bradykinin is the flood. In HAE patients, the valve is broken, so the pressure builds unchecked and the flood comes.

The critical insight for BioCryst was that blocking plasma kallikrein, the enzyme upstream of bradykinin, should prevent attacks. And BioCryst's entire scientific platform was built around designing small-molecule enzyme inhibitors using X-ray crystallography. The same approach that had produced neuraminidase inhibitors for flu could produce kallikrein inhibitors for HAE.

Before BioCryst entered the market, treatment options were limited and burdensome. Shire dominated the HAE landscape through its acquisition of ViroPharma in November 2013 for $4.2 billion, gaining Cinryze, an intravenous C1 inhibitor replacement that cost upwards of $400,000 per year and required twice-weekly IV infusions. Other options included Firazyr (an injectable bradykinin receptor blocker), Kalbitor (an injectable kallikrein inhibitor that required a healthcare setting due to anaphylaxis risk), and the old-school attenuated androgens like danazol, which caused virilization, liver damage, and were unsuitable for women and children.

Every prophylactic treatment required needles. There was no oral option. For a disease that already imposed enormous psychological and physical burden, requiring patients to also endure regular IV infusions or injections felt like adding insult to injury.

BioCryst's bet was straightforward: use structure-based drug design to create a small molecule that could inhibit plasma kallikrein, make it orally bioavailable so patients could take a pill instead of getting injections, and target the rare disease market where smaller clinical trials, orphan drug protections, and concentrated prescriber bases favored small companies.

BCX4161, later named avoralstat, was the first attempt. Phase 1 in healthy volunteers confirmed safety and on-target kallikrein inhibition. Then came the OPuS-1 Phase 2a trial, a crossover study in HAE patients, and the results announced on May 27, 2014 were genuinely exciting: a statistically significant 35% reduction in attack rates versus placebo. It was proof of concept that an oral kallikrein inhibitor could prevent HAE attacks.

Hope returned to BioCryst. The stock responded. The company began planning OPuS-2, a larger Phase 2b/3 trial. But crucially, BioCryst's scientists were already working on a backup compound, BCX7353, designed from the ground up to address every pharmacokinetic weakness they suspected in avoralstat. That decision to run parallel drug development programs, rather than betting everything on a single molecule, would prove to be one of the most important in the company's history.

The rare disease economics made the math work. Under the Orphan Drug Act of 1983, companies developing drugs for diseases affecting fewer than 200,000 Americans receive seven years of market exclusivity, tax credits for clinical trial expenses, FDA fee waivers, and expedited regulatory pathways. Clinical trials in HAE could enroll 50-150 patients instead of thousands. The prescriber base was concentrated among a few hundred allergists and immunologists, enabling a focused salesforce of 50-100 representatives rather than armies of thousands. And payers accepted premium pricing, often $200,000-500,000 per patient per year, because the alternative was expensive emergency room visits and intensive care admissions.

For a small biotech that had been trying to compete with Gilead and Roche in mass-market diseases, the rare disease model was a revelation. The Orphan Drug Act of 1983 had created an entire ecosystem designed to make rare disease development viable for small companies. The economics were almost perfectly inverted from mass-market pharmaceuticals: where a Hep C drug needed to treat millions at moderate prices, an HAE drug needed to treat thousands at premium prices. Where a flu antiviral required a salesforce of thousands calling on every primary care doctor in America, an HAE drug required perhaps fifty to one hundred reps covering a concentrated base of allergists and immunologists. Where mass-market Phase 3 trials enrolled thousands of patients at enormous cost, HAE trials could achieve statistical significance with fifty to one hundred fifty patients.

The math was elegant. If the United States had approximately 10,000 diagnosed HAE patients and BioCryst could capture even a fraction of them at an annual price point of $400,000-500,000, the revenue potential was substantial. And unlike mass-market drugs, where generic erosion could destroy revenues overnight, orphan drug protections provided seven years of market exclusivity plus patent protection, creating long-duration revenue visibility. Average orphan drug pricing runs roughly 4.5 times higher than non-orphan drugs, and approximately 14% of orphan drugs achieve blockbuster status of over $1 billion in annual sales.

VI. The Avoralstat Failure & Berotralstat Emergence (2015-2018)

February 8, 2016, was the worst day in BioCryst's history. The OPuS-2 results were unambiguous. Avoralstat 500 mg showed a mean attack rate of 0.63 per week. The placebo arm: 0.61 per week. A difference of 0.02. The drug was no better than sugar pills. Both dose arms failed to achieve statistical significance.

BioCryst shares crashed approximately 67% in a single day, falling to around $2.05. Within hours, multiple securities law firms announced investigations, a familiar pattern in biotech where trial failures are followed almost reflexively by litigation threats. For employees who had survived the 2012 restructuring, who had watched the Hep C program and the peramivir Phase 3 both collapse, this felt like the final blow. The company's entire rare disease thesis, the idea that had given BioCryst a reason to exist after the influenza disappointments, appeared to have been invalidated by a simple comparison: drug versus sugar pill, no difference.

But Stonehouse and the scientific team did not panic. They did what scientists are supposed to do: they analyzed the data.

But the published post-mortem, later detailed in the journal Allergy, revealed something important: the failure was not one of biology but of pharmacokinetics. Plasma concentrations were widely distributed, with many time points showing drug levels below the therapeutic range. Avoralstat had low oral bioavailability and was cleared from the body too rapidly, creating periods of no protection between doses. The three-times-daily dosing regimen on an empty stomach proved unworkable in practice. Despite 99% reported compliance, patients spaced their doses unevenly, with the largest gap averaging eleven hours. The biology was sound. The molecule was wrong.

This distinction mattered enormously because BCX7353, berotralstat, had been designed specifically to solve these problems. Where avoralstat had poor absorption, berotralstat had dramatically improved oral bioavailability. Where avoralstat required three doses daily on an empty stomach, berotralstat could be taken once daily with or without food. Its potency was exceptional: an inhibition constant of 0.44 nanomolar against human plasma kallikrein, with high selectivity over related enzymes. The half-life supported true once-daily dosing.

Phase 1 results, reported in 2015-2016, confirmed that oral berotralstat was safe and well-tolerated at doses up to 500 mg once daily for seven days. No dose-limiting toxicity was identified. The APeX-1 Phase 2 dose-ranging trial, initiated in August 2016, tested four doses against placebo, and the results were published in the New England Journal of Medicine. Oral administration at 125 mg or more resulted in significantly lower attack rates compared to placebo. The dose-response relationship was clear.

Meanwhile, the competitive landscape was shifting. In November 2015, Shire had paid approximately $5.9 billion to acquire Dyax Corporation, gaining lanadelumab (DX-2930), a fully human monoclonal antibody targeting the same enzyme, plasma kallikrein. Analysts projected lanadelumab could generate up to $2 billion in annual sales. In 2018, Takeda acquired Shire in a roughly $62 billion mega-merger, gaining the entire HAE franchise.

On August 23, 2018, the FDA approved Takhzyro (lanadelumab) for HAE prophylaxis. The Phase 3 HELP study showed that Takhzyro 300 mg every two weeks reduced monthly HAE attacks by an average of 87% versus placebo. It was a subcutaneous injection, administered every two to four weeks. This was a dramatically better product than the old IV infusions, and it set the efficacy bar that BioCryst would have to contend with.

Takhzyro's approval was, paradoxically, both a competitive threat and a validation for BioCryst. It proved that the HAE prophylaxis market was real, that payers would reimburse premium-priced prophylactic therapies at approximately $500,000 per patient per year, and that patients would embrace convenient prevention over reactive on-demand treatment. Every dollar Takeda spent educating physicians and patients about HAE prophylaxis helped build the market that Orladeyo would later enter.

But BioCryst's positioning was never about beating Takhzyro on efficacy numbers. It was about the route of administration. Takhzyro was an injection. BioCryst was building a pill. For patients already burdened by a disease that caused unpredictable swelling requiring on-demand injections, adding another set of prophylactic injections doubled the needle burden. An oral, once-daily pill was fundamentally different in kind, not just in degree.

The Takhzyro approval also intensified BioCryst's urgency. Lanadelumab was now the de facto standard of care for HAE prophylaxis, and every month that BioCryst delayed its own approval was a month in which Takhzyro deepened its hold on physicians and patients. The race was on, and BioCryst needed to execute its APeX-2 Phase 3 trial flawlessly.

Financing through this period required creativity. In December 2020, coinciding with the FDA approval of Orladeyo, BioCryst secured $325 million in funding through a combination of a $125 million upfront payment from Royalty Pharma (in exchange for tiered royalties on Orladeyo sales) and a $200 million credit facility from Athyrium Capital Management. In November 2021, an additional $350 million in financing followed from Royalty Pharma and OMERS Capital Markets. These deals gave BioCryst the commercial runway it needed without requiring a massively dilutive equity raise.

The Royalty Pharma deal was cleverly structured. The royalty rate was 8.75% on the first $350 million in annual Orladeyo sales, dropping to 2.75% between $350 million and $550 million, and zero above $550 million. This meant that as the drug scaled, BioCryst would keep an increasingly large share of incremental revenue, a structure that incentivized aggressive commercial execution.

VII. Orladeyo Approval: The Transformation (2018-2020)

The APeX-2 Phase 3 trial was the moment of truth. A double-blind, parallel-group, placebo-controlled study conducted across 40 sites in 11 countries, it randomized patients to berotralstat 110 mg, berotralstat 150 mg, or placebo, taken once daily by mouth.

The primary endpoint was the rate of investigator-confirmed HAE attacks during a 24-week treatment period. The 150 mg dose reduced the attack rate to 1.31 per month compared to 2.35 for placebo, a statistically significant reduction with a p-value below 0.001. Fifty percent of patients on the 150 mg dose experienced a 70% or greater reduction in attacks from baseline. Long-term data through 96 weeks showed an 80% average reduction in monthly attacks, with median attack rates falling to zero in 16 of 17 treatment months.

The safety profile was favorable: the most common adverse events were gastrointestinal (abdominal pain, vomiting, diarrhea) and back pain, with no drug-related serious adverse events reported. These were manageable side effects for patients whose alternative was either enduring regular HAE attacks or receiving injectable therapies with their own burden of injection-site reactions and inconvenience. BioCryst submitted its NDA in December 2019 and received FDA acceptance in February 2020.

On December 3, 2020, the FDA approved Orladeyo (berotralstat) as the first oral, once-daily therapy to prevent HAE attacks in adults and pediatric patients 12 years and older. After 34 years, BioCryst had its first commercially significant drug approval. The moment was especially poignant given the journey: a company that had been founded to use rational drug design against infectious disease had finally achieved commercial success in a rare genetic disorder that almost no one had heard of when the company was born. The approval came with orphan drug exclusivity, providing seven years of market protection for the specific HAE indication.

The commercialization challenge was immense. BioCryst had never sold a drug at scale. It needed to build a rare disease sales force from scratch, navigate the labyrinthine world of specialty pharmacy reimbursement, and convince physicians and patients to try a new therapy in a market where Takhzyro had a two-year head start and demonstrably higher attack reduction numbers in clinical trials.

The COVID-19 pandemic, which was raging when Orladeyo launched, proved to be a double-edged sword. On one hand, it disrupted physician access and made in-person sales calls difficult. On the other hand, HAE-treating allergists and immunologists were not as disrupted as some other specialties, and BioCryst had hired its entire sales team by April 2020, eight months before approval, conducting all training and territory mapping virtually. When launch day arrived, reps already knew their key targets and had been making virtual visits for months.

The competitive dynamics with Takhzyro were nuanced. Takhzyro's clinical trial showed an 87% reduction in attacks; Orladeyo's showed 44%. On paper, this looked like a clear Takhzyro advantage. But real-world comparisons are more complex. Trial designs differed. Patient populations differed. And Orladeyo's longer-term data showed progressively better outcomes. More fundamentally, the comparison missed the point for many patients. The question was not "which drug reduces attacks more in a trial?" but "would I rather take an injection every two weeks or a pill every morning?"

The answer, for a growing number of patients, was the pill. Pricing also favored Orladeyo: a wholesale acquisition cost of approximately $485,000 per year compared to Takhzyro's roughly $591,000. The oral route eliminated injection-site reactions, self-injection anxiety, cold-chain storage requirements, and the need for nurse training on injection technique.

International expansion followed rapidly. Japan's Ministry of Health approved Orladeyo in January 2021, with Torii Pharmaceutical serving as the commercial partner. The European Commission approved it in April 2021, covering all EU member states plus Iceland, Norway, and Liechtenstein. Germany served as the first European launch market, followed by Ireland and other countries. Chile also approved the drug. Each geography brought its own regulatory and reimbursement challenges, but the core value proposition translated universally: HAE patients everywhere preferred the option of a daily pill over regular injections.

The significance of the Orladeyo approval extended beyond the drug itself. For BioCryst, it validated the structure-based drug design approach that had been the company's founding thesis since 1986. Berotralstat was literally designed by examining the three-dimensional crystal structure of plasma kallikrein's active site and engineering a molecule to fit precisely into that pocket with subnanomolar potency. The same intellectual framework that Charles Bugg and John Montgomery had championed in a university lab thirty-four years earlier had produced a commercially successful drug that was changing patients' lives. Yarlagadda Babu, who had walked through the door as BioCryst's first employee in 1988, oversaw the discovery process that delivered berotralstat. The arc from academic theory to patient impact had taken an entire career to complete.

VIII. Orladeyo Ramp & Pipeline Expansion (2021-2023)

Orladeyo's commercial ramp was one of the rare disease industry's more impressive launches, and it offers a case study in how to build a commercial business in rare disease from scratch.

BioCryst had essentially no commercial infrastructure when it received FDA approval. The company had spent its entire history as a research-stage organization, funded by government grants and investor capital, with no experience manufacturing, distributing, or selling a drug at scale. Building the commercial operation required hiring a specialized sales force of approximately eighty representatives, establishing relationships with specialty pharmacies, creating a comprehensive patient services program (which BioCryst branded as "BioCryst CARES"), navigating complex insurance reimbursement processes, and developing physician education materials for a disease that many allergists encountered only a handful of times in their careers.

First-quarter 2021 revenue, the first full quarter after the December 2020 approval, was $10.9 million. By the fourth quarter, quarterly revenue had reached $45.6 million. Full-year 2021 revenue came in at $122 million.

The trajectory accelerated. Full-year 2022 revenue hit $252 million, more than doubling the prior year. In 2023, revenue reached $326 million, a 29% increase. Each quarter set new records as patient additions remained strong and retention proved durable. Approximately 70% of patients starting Orladeyo, including those switching from injectable prophylaxis, remained on therapy through the first year. That retention number is significant because it addresses a common bear case question: are patients sticking with a less-efficacious oral drug, or are they switching back to injectables after trying Orladeyo? The data suggested they were staying.

The growth was driven by multiple sources: newly diagnosed HAE patients who had never been on prophylaxis, patients switching from on-demand-only treatment to prophylactic therapy, and patients switching from injectable prophylaxis to the convenience of a daily pill. More than half of new Orladeyo patients since launch had previously been on a prophylactic medicine, with most of the remainder moving up from acute-only treatment.

BioCryst also pursued pipeline expansion beyond HAE, with mixed results. BCX9930, an oral Factor D inhibitor targeting complement-mediated diseases like paroxysmal nocturnal hemoglobinuria (PNH) and C3 glomerulopathy, entered Phase 2 and showed clinical benefit in treatment-naive PNH patients. But competitive data presented at the 2022 American Society of Hematology meeting, particularly from Alexion's next-generation complement inhibitors, suggested BCX9930 could not meet the rapidly evolving standard of care. In December 2022, BioCryst made the difficult decision to discontinue BCX9930, demonstrating the same willingness to cut losses that had served the company through its wilderness years.

Rather than abandoning the complement space entirely, BioCryst advanced BCX10013, a next-generation oral Factor D inhibitor designed to achieve potency and pharmacokinetic characteristics that BCX9930 could not. Phase 1 data in January 2023 showed that the highest dose studied achieved 97.8% suppression of alternative pathway complement activity at 24 hours post-dose. The first patient was enrolled in a proof-of-concept trial for PNH in October 2023.

The galidesivir antiviral program, which had sustained BioCryst through the wilderness years via government grants, continued under NIAID contracts with over $70 million in cumulative government R&D funding. However, galidesivir would eventually be divested to Island Pharmaceuticals in 2025, with Island pursuing development for Marburg virus disease.

The BCX9930 discontinuation deserves closer examination because it illustrates how BioCryst's leadership had internalized the lessons of its wilderness years. In complement-mediated diseases like PNH, the standard of care was evolving rapidly. Alexion's Soliris and Ultomiris had established the complement inhibitor category, and next-generation oral Factor D inhibitors from competitors were showing superior profiles. Rather than spend hundreds of millions chasing a target where the odds of achieving competitive differentiation were low, BioCryst killed the program and redirected resources. This is the same muscle Stonehouse exercised in 2012 when he cut the workforce in half to focus on HAE. Companies that survive in biotech are not the ones that never fail; they are the ones that recognize failure early and reallocate capital to higher-probability programs.

The balance sheet transformation was dramatic. From a company that had slashed its workforce by half in 2012 and burned through $40 million a year with no commercial revenue, BioCryst was now generating hundreds of millions in product sales with a clear path to profitability. The Royalty Pharma and Athyrium financing deals had provided the bridge without catastrophic dilution, and as revenue scaled past $350 million and then $550 million, BioCryst retained increasingly larger shares of each incremental dollar.

The stock price reflected this transformation, but imperfectly. From its post-avoralstat nadir around $2 in early 2016, shares climbed to the mid-teens by late 2020 as the FDA approved Orladeyo. The share count had grown substantially through years of dilutive financing, a common cost of survival in biotech. But the fundamental business underneath had been completely rebuilt: from a pre-revenue clinical-stage company dependent on government grants to a commercial-stage rare disease franchise generating strong and growing product revenue.

IX. The Present & Future: Becoming a Sustainable Rare Disease Company (2024-Present)

If the rare disease pivot was BioCryst's strategic inflection point and the Orladeyo approval its clinical vindication, then 2024-2025 represented the financial transformation that validated the entire thirty-year journey.

Full-year 2024 Orladeyo revenue reached $437 million, a 34% increase over 2023. But 2025 was the transformational year. Orladeyo generated $601 million in net revenue, beating the company's own guidance range and growing 37% year-over-year. For the first time in BioCryst's nearly four-decade history, the company achieved full-year profitability: GAAP operating profit of $341 million and non-GAAP operating profit of $214 million.

Total revenue of $874.8 million in 2025 included a significant gain from a strategic move that reshaped the company: on October 1, 2025, BioCryst completed the sale of its European Orladeyo business to Neopharmed Gentili for up to $264 million ($250 million upfront plus $14 million in milestones). The deal eliminated approximately $70 million in future interest payments and generated over $50 million in annual operating expense savings by exiting the cost of maintaining a European commercial infrastructure.

BioCryst used the European sale proceeds to prepay its entire remaining Pharmakon term loan of $198.7 million, achieving a debt-free balance sheet on the term loan side. The strategic logic was clear: concentrate commercial resources on the U.S. market, where Orladeyo's growth was strongest, and let a European partner with local expertise handle that geography.

But the most significant move came in October 2025, when BioCryst announced the acquisition of Astria Therapeutics for approximately $700 million, completed in January 2026. Astria's crown jewel was navenibart, a long-acting injectable monoclonal antibody that inhibits plasma kallikrein with the potential for every-three-month and every-six-month dosing. Interim clinical data from the ALPHA-SOLAR study showed mean attack rate reductions of 92% with quarterly dosing and 90% with twice-yearly dosing, with 97% median reductions in both arms.

The strategic rationale for the Astria acquisition was compelling: BioCryst could offer physicians and patients a comprehensive HAE franchise covering the full spectrum of treatment preferences. For patients who want a daily pill, there is Orladeyo. For patients who prefer the "set it and forget it" convenience of a long-acting injection a few times a year, there would be navenibart, pending Phase 3 results expected in early 2027 and a regulatory filing targeted by year-end 2027.

The acquisition brought personnel as well. Jill C. Milne, Astria's co-founder and CEO, joined BioCryst's board, and John Ruesch, Astria's SVP, joined as Chief Technical Operations Officer. The transaction was financed through cash on hand, approximately $396.6 million drawn from a Blackstone credit facility, and roughly 37.3 million new BioCryst shares.

The leadership transition that had been underway reached completion. Jon Stonehouse, who had guided BioCryst from the wilderness years through the HAE pivot, avoralstat failure, berotralstat triumph, and Orladeyo commercialization, stepped down as President on August 1, 2025 and retired as CEO on December 31, 2025. Charlie Gayer, who had joined BioCryst in 2015 as VP of Global Strategic Marketing and rose to Chief Commercial Officer in January 2020, became CEO on January 1, 2026. Gayer had been the architect of Orladeyo's commercial launch and growth strategy. Vincent Milano, a veteran rare disease executive who had previously chaired ViroPharma (which developed Cinryze for HAE before the Shire acquisition), was elected Board Chair in January 2026.

In December 2025, the FDA approved Orladeyo oral pellets for pediatric patients aged 2 to 11 years, making it the first and only oral prophylactic treatment for this younger age group, with commercial availability expected in April 2026. The 2026 guidance calls for Orladeyo net revenue of $625-645 million, with total revenue including RAPIVAB of $635-660 million. Non-GAAP operating expenses are projected at $450-470 million, including Astria integration costs, with continued profitability expected.

The competitive landscape, however, has intensified dramatically. In 2025 alone, three new HAE treatments received FDA approval: garadacimab (Andembry) from CSL Behring in June, a first-in-class Factor XIIa inhibitor administered via once-monthly subcutaneous autoinjector; sebetralstat (Ekterly) from KalVista in July, the first oral on-demand treatment for acute HAE attacks; and donidalorsen (Dawnzera) from Ionis/Otsuka in August, the first RNA-targeted prophylactic therapy, dosed subcutaneously every four to eight weeks. There are now twelve FDA-approved HAE products in total.

What makes the 2025 approval wave particularly interesting is how each new product validates a different therapeutic approach. Garadacimab attacks the contact activation cascade at Factor XIIa, upstream of kallikrein. Donidalorsen uses antisense RNA to reduce prekallikrein production at the genetic level. Sebetralstat provides on-demand oral rescue for breakthrough attacks. This proliferation of mechanisms means that HAE patients now have unprecedented choice, but it also means the market is fragmenting across multiple modalities. For BioCryst, the question is whether this proliferation expands the overall treated patient population (by giving physicians more options for patients who were previously untreated or undertreated) or whether it primarily redistributes existing patients across more products. Early evidence suggests the former: the shift from on-demand to prophylactic treatment continues to accelerate, and awareness of HAE among physicians is improving, shortening the diagnostic delay that has historically kept many patients undiagnosed for eight to ten years.

The most existential competitive threat, however, comes from gene therapy. Intellia Therapeutics has advanced NTLA-2002 (lonvo-z), a one-time CRISPR/Cas9 gene editing treatment delivered via lipid nanoparticle to the liver. It knocks out the KLKB1 gene encoding prekallikrein, theoretically eliminating HAE attacks permanently with a single infusion. Phase 1/2 data showed 97% of patients receiving the 50 mg dose remained attack-free with up to three years of follow-up. Phase 3 enrollment completed in September 2025. However, a patient death in Intellia's separate ATTR amyloidosis program in October 2025 raised broader safety questions about the Cas9 platform, creating uncertainty around the gene therapy path.

X. The Biotech Business Model & Strategic Frameworks

To evaluate BioCryst's competitive position systematically, it is worth applying two of the most widely used strategic frameworks: Michael Porter's Five Forces, which analyzes industry structure, and Hamilton Helmer's Seven Powers, which identifies the sources of durable competitive advantage.

Porter's Five Forces

Threat of New Entrants: Moderate and Rising. The barriers to entering the HAE market are substantial: clinical trials still cost tens of millions, regulatory expertise in rare disease takes years to build, and established players like BioCryst and Takeda have deep physician relationships built over years of education and patient support. The seven-year orphan drug exclusivity blocks identical molecules. However, the 2025 approval wave, three new drugs in three months, demonstrates that the FDA is receptive and that novel mechanisms can gain entry. Venture capital continues to fund HAE challengers. Gene therapy represents the ultimate disruptive entrant.

Bargaining Power of Buyers: Low but Evolving. In rare disease, patients have minimal bargaining power because alternatives are limited and the consequences of untreated disease are severe. Payers face regulatory mandates to cover orphan drugs, and the 2025 expansion of the "One Big Beautiful Bill Act" now exempts orphan drugs from Medicare drug price negotiations entirely, as long as they have not been approved for non-orphan uses. However, as the market fills with six-plus prophylactic options, payers may gain leverage through formulary positioning and step therapy requirements.

Bargaining Power of Suppliers: Low. For synthetic small molecules like berotralstat, manufacturing inputs are relatively commoditized and contract manufacturing organizations compete for business. The exception is plasma-derived C1 inhibitor products (Cinryze, Haegarda, Berinert), where plasma supply is a genuine constraint and CSL Behring's vertical integration in plasma collection provides a competitive advantage. BioCryst does not face this issue with Orladeyo.

Threat of Substitutes: High and Growing. This is the most dynamic force. Patients can switch between six prophylactic options based on convenience, efficacy, and personal preference. The 70% patient preference for oral prophylaxis, up from 50% in 2023, favors Orladeyo but is not unassailable. Gene therapy, if proven safe and effective, would represent the ultimate substitute: a single infusion that eliminates attacks for life, disrupting the entire chronic prophylaxis revenue model. The arrival of oral on-demand treatment (Ekterly) may also lead some patients to forgo daily prophylaxis entirely, relying on pills only when attacks occur.

Competitive Rivalry: High and Intensifying. Six approved prophylactic treatments now compete in HAE, up from two or three just a few years ago. Takeda's Takhzyro leads on revenue at approximately $1.47 billion annually. Orladeyo leads on growth trajectory. CSL Behring controls the legacy C1 inhibitor segment. The competitive battlegrounds are convenience (oral vs. monthly injection vs. quarterly injection vs. one-time gene therapy), efficacy (attack-free rates), patient population expansion (pediatric, geographic), and payer access. However, the market continues to expand through increased diagnosis and the shift from on-demand to prophylactic treatment, which cushions competitive pressure.

Hamilton's 7 Powers

Scale Economies: Limited. Rare disease markets are inherently small, roughly 80,000-160,000 HAE patients globally. BioCryst cannot achieve the kind of manufacturing or distribution scale economies that matter in mass-market pharmaceuticals. However, the fixed costs of regulatory infrastructure, patient support programs, and commercial operations do create modest scale advantages for companies already serving the market versus new entrants.

Network Effects: Minimal in the Traditional Sense. There is no direct network effect where more Orladeyo users make the product more valuable to each additional user. However, patient communities and physician referral networks create a form of social proof. BioCryst's investment in patient advocacy relationships, the HAE Association partnerships, educational programs, and patient services creates a soft network of trust that is difficult for newcomers to replicate quickly.

Counter-Positioning: Strong. This is arguably BioCryst's most powerful strategic asset. Orladeyo's oral daily format is a direct counter-position against incumbent injectable therapies. Takeda cannot easily make Takhzyro oral without developing an entirely new molecule. The incumbents' business models are built around injectable biologics with high-touch patient support, cold-chain logistics, and nursing networks. Offering a pill that eliminates all of that complexity forces them to compete on a dimension where they have a structural disadvantage. The Astria acquisition extends this counter-positioning logic: navenibart with quarterly or semi-annual dosing counter-positions against monthly and biweekly injectables.

Switching Costs: High. Once an HAE patient finds a prophylactic therapy that controls their attacks, switching carries real risk. Patients are reluctant to change a working regimen for an unknown, especially when attacks can be life-threatening. Physicians are similarly conservative. This stickiness protects incumbents, including Takhzyro, but it also protects Orladeyo patients from migrating to newer entrants. The 70% one-year retention rate on Orladeyo reflects this dynamic.

Branding: Important. In rare disease, brand trust is built through physician education, patient advocacy, and the quality of patient support services (insurance navigation, copay assistance, side effect management). BioCryst has invested heavily in these areas, and the company's long presence in HAE since the avoralstat days gives it credibility with key opinion leaders. Trust takes years to build and is not easily replicated.

Cornered Resource: Moderate. BioCryst's intellectual property on berotralstat and its specific chemical structure provides protection, but the kallikrein inhibitor target class is not exclusive. Multiple competitors have found different ways to inhibit kallikrein or related cascade targets. The cornered resource is less about the molecule and more about the institutional knowledge, the three decades of structure-based drug design expertise, the commercial infrastructure, and the patient services platform.

Process Power: Emerging. BioCryst's commercial execution, patient services, reimbursement expertise, and physician relationship management have become genuine competitive advantages that are difficult for new entrants to replicate without years of investment. The company's ability to launch Orladeyo during a pandemic and grow revenue from $10.9 million in its first quarter to $601 million in four years reflects organizational capabilities that go beyond the molecule itself.

Where BioCryst's Durable Advantage Lies

The combination of counter-positioning (oral versus injectable), switching costs (patients staying on working therapies), and emerging process power (commercial execution in rare disease) creates a defensible position. The first-mover advantage in oral HAE prophylaxis is real: Orladeyo was the first, it has four years of commercial momentum, and it has captured a growing share of patients who prefer pills over needles. The Astria acquisition, adding a potential every-three-to-six-month injectable, extends the franchise across the full spectrum of patient preferences.

The vulnerability is gene therapy. If Intellia's lonvo-z proves safe and effective, a one-time cure fundamentally disrupts the chronic prophylaxis model. However, the patient death in Intellia's separate program, the inherent uncertainties of CRISPR technology, the massive pricing challenges of gene therapy (Zevaskyn, approved in April 2025, carries a $3.1 million list price), and the long path to broad adoption all suggest that chronic prophylaxis has years of commercial relevance ahead.

XI. The Playbook: Lessons for Biotech Founders & Investors

BioCryst's story offers a remarkably rich set of lessons for biotech founders, investors, and anyone interested in how companies survive extended periods of uncertainty. Here are the most important takeaways, drawn not from textbooks but from three decades of lived experience.

The Pivot Masterclass. BioCryst executed three major strategic pivots over thirty years: from antiviral/anticancer drug design to influenza neuraminidase inhibitors, from influenza to hepatitis C (and quickly away from it), and finally from mass-market diseases to rare disease. Each pivot required abandoning years of sunk costs and emotional investment. The December 2012 restructuring, cutting half the workforce and narrowing to a single unproven HAE program, was the most consequential business decision in the company's history. The lesson is not that pivoting is always right, but that the willingness to pivot, to honestly assess when a strategy is failing and redirect resources, is the difference between survival and death.

Rare Disease Economics. BioCryst's journey illustrates why orphan drugs changed the biotech equation. In mass-market diseases like influenza and hepatitis C, small biotechs face Gilead-sized competitors with billions in development budgets. In rare disease, smaller trials, premium pricing, concentrated prescriber bases, and orphan drug protections create a playing field where a focused small company can build a sustainable business. Orladeyo's success demonstrates that you do not need to treat millions of patients to build a profitable pharmaceutical company. You need to treat thousands of patients exceptionally well.

The Valley of Death. BioCryst's survival through the 2012-2014 period, when it had no commercial revenue, three failed programs, and a stock price in the low single digits, offers a textbook case in crossing the valley of death. The playbook was: cut costs ruthlessly (50% workforce reduction), pursue non-dilutive government grants (over $57 million from NIAID and BARDA for galidesivir), maintain just enough R&D capability to advance the one program that mattered (BCX4161/avoralstat, and its backup BCX7353), and structure financing creatively when equity markets are hostile. Most biotechs die in the valley not because they lack good science but because they run out of time and money. BioCryst survived by buying time through government contracts while maintaining scientific optionality.

The Importance of Differentiation. Orladeyo is not the most efficacious HAE prophylaxis in clinical trials. Takhzyro's 87% attack reduction in the HELP study beats Orladeyo's 44% in APeX-2 on headline numbers. But Orladeyo has grown to $601 million in annual sales because it is a pill, not an injection. The seemingly small difference in route of administration creates an entirely different patient experience. This principle extends broadly: in pharmaceutical markets, differentiation on convenience, route of administration, dosing frequency, or patient experience can be more commercially powerful than marginal efficacy improvements. The best drug is the one patients will actually take.

The Long Game. From founding in 1986 to first full-year profitability in 2025, BioCryst took 39 years. From IPO in 1994 to profitability, 31 years. Very few investment theses accommodate that kind of timeline. This is not necessarily a model to replicate, but it is a reminder that transformative biotech outcomes sometimes require extraordinary patience. Jon Stonehouse's 18-year tenure as CEO, from 2007 to 2025, through multiple clinical failures, near-bankruptcy, and finally commercial triumph, is a rare example of the long-term commitment that building a pharmaceutical company sometimes demands.

Running Parallel Programs. Perhaps the most underappreciated lesson is the decision to develop berotralstat (BCX7353) alongside avoralstat (BCX4161). When avoralstat failed in February 2016, the company had a backup compound already in Phase 1 with dramatically improved pharmacokinetics. This was not an accident or luck. It was deliberate portfolio management within a focused therapeutic area. The cost of running a second early-stage program was trivial compared to the strategic insurance it provided. The Astria acquisition in 2025-2026 reflects the same logic at a larger scale: by acquiring navenibart alongside Orladeyo, BioCryst is again running parallel programs in the same therapeutic area, hedging against the risk that any single product falls short while creating a comprehensive franchise if both succeed.

Capital Allocation Discipline. BioCryst's capital allocation decisions tell a consistent story of learning from failure. The company spent over $234 million of government money on peramivir's failed Phase 3 trial in hospitalized influenza. It spent years and unknown sums chasing Hep C. It invested in avoralstat through Phase 2b/3 only to see it fail. Each failure sharpened the company's ability to distinguish between programs worth pursuing and programs worth killing. By the time BCX9930 showed competitive weakness in complement diseases, BioCryst discontinued it without hesitation. The 2025 sale of the European Orladeyo business reflected similar clarity: rather than maintaining an expensive European commercial infrastructure with limited near-term growth, the company monetized the asset, eliminated debt, and concentrated resources on the U.S. market where returns were highest. These are not the decisions of a company that learned capital discipline from a textbook. They are the decisions of a company that learned it from decades of near-death experiences.

XII. Bull vs. Bear Case & Investment Thesis

Myth vs. Reality

Before examining the bull and bear cases, it is worth addressing several consensus narratives that deserve scrutiny.

Myth: Orladeyo is an inferior drug because its clinical trial efficacy numbers are lower than Takhzyro's. Reality: Cross-trial comparisons in HAE are misleading. Different trial designs, patient populations, baseline attack rates, and endpoint definitions make headline number comparisons unreliable. More importantly, commercial performance has demonstrated that patients and physicians value oral convenience alongside efficacy. Orladeyo's revenue growth trajectory, from zero to $601 million in four years with 37% year-over-year growth, suggests the market values the product more than the clinical trial comparison alone would predict.

Myth: Gene therapy will make all chronic HAE therapies obsolete within a few years. Reality: While CRISPR-based approaches like Intellia's lonvo-z show remarkable early data, the path from Phase 3 readout to broad commercial adoption is measured in many years, not months. Manufacturing challenges, safety monitoring requirements (the patient death in Intellia's ATTR program underscores this), pricing at potentially $2-3 million per treatment, payer adoption hurdles, and patient willingness to undergo an irreversible genetic modification all create friction. Chronic therapies are likely to remain the standard of care for the majority of HAE patients for the foreseeable future, even if gene therapy eventually proves safe and durable.

Myth: BioCryst is still a fragile biotech that could relapse into crisis. Reality: The company crossed a meaningful threshold in 2025 with first-year profitability, debt retirement, and a proven commercial infrastructure serving thousands of patients. While pipeline and competitive risks remain real, the existential risk that defined BioCryst's first three decades has materially diminished. The company is no longer dependent on government grants or emergency financing to survive. It generates cash from operations and has the infrastructure to sustain itself as a going concern independent of any single pipeline readout.

The Bull Case

Orladeyo's commercial momentum remains strong, with 37% revenue growth in 2025 and guidance for $625-645 million in 2026. The trend toward oral prophylaxis continues to strengthen, with 70% of U.S. HAE patients now expressing a preference for oral therapy, up from 50% in 2023. The pediatric pellet formulation approved in December 2025 opens an entirely new patient segment. If navenibart succeeds in Phase 3 and is approved, BioCryst would control the most comprehensive HAE franchise in the industry, offering oral daily prophylaxis, a potential best-in-class long-acting injectable with quarterly or semi-annual dosing, and potentially partnered geographic access globally.

The Orladeyo royalty structure with Royalty Pharma is designed to improve as revenue scales. Above $550 million in annual sales, where the drug already operates, there is no royalty to Royalty Pharma on incremental U.S. revenue. This means every dollar of revenue growth above that threshold flows entirely to BioCryst.

The HAE market itself continues to expand through improved diagnosis rates, reducing the 8-10 year average diagnostic delay, and the ongoing shift from on-demand to prophylactic treatment. Even with increased competition, market growth may accommodate multiple winners.

The company is now consistently profitable, with a clean balance sheet after retiring its Pharmakon term debt. The 2025 non-GAAP operating profit of $214 million demonstrates that the business model works at scale. Analyst consensus is Strong Buy with an average price target of approximately $20, implying roughly 150% upside from the current trading price near $7.60-7.90 and suggesting the market may be undervaluing the franchise.

The Bear Case

Competition has intensified dramatically. Three new HAE products were approved in 2025 alone: garadacimab, sebetralstat, and donidalorsen. Each offers a differentiated value proposition that could pressure Orladeyo's market share growth. CSL Behring's garadacimab provides once-monthly autoinjector convenience with very high efficacy. Donidalorsen offers dosing every four to eight weeks. Ekterly gives patients an oral on-demand option that could discourage some from adopting daily prophylaxis.

BioCryst remains essentially a one-product company. Orladeyo generates the vast majority of revenue. If growth plateaus due to competitive pressure or market saturation, there is no second product to offset the deceleration. The pipeline beyond HAE rests primarily on BCX10013, still in proof-of-concept with years of development ahead and no guarantee of success, in a complement space where BioCryst already failed once with BCX9930.

The Astria acquisition adds $396.6 million in Blackstone facility debt and diluted shareholders by approximately 37.3 million shares. Navenibart remains in Phase 3 with no guarantee of success. If it fails, BioCryst will have paid $700 million for a failed asset and taken on significant leverage.

Gene therapy poses an existential long-term risk. If Intellia's lonvo-z or a successor CRISPR-based treatment demonstrates safety and durability, a one-time cure priced at even $2-3 million per patient could be economically superior to decades of chronic therapy at $500,000+ per year. Payers would have strong incentives to prefer the one-time option. While gene therapy commercialization is likely years away and faces significant hurdles, it represents a genuine tail risk to all chronic HAE therapy revenue.

The stock trades at a significant discount to analyst targets, which could reflect either mispricing or the market pricing in competitive and pipeline risks that analyst models underweight. BioCryst's historical pattern of promising programs followed by disappointments (peramivir, Hep C, avoralstat, BCX9930) creates a narrative overhang that weighs on investor sentiment, even as the company's current commercial execution has been strong.

There is also a structural challenge embedded in BioCryst's story: the company's market capitalization of approximately $1.9 billion represents a relatively low multiple on a drug generating over $600 million in revenue. In part, this reflects the royalty obligations to Royalty Pharma and the Blackstone credit facility that reduce the economics flowing to equity holders. In part, it reflects the market's skepticism about whether a company that took 39 years to reach profitability can sustain it. And in part, it reflects the genuine uncertainty around navenibart, gene therapy, and competitive dynamics. The disconnect between analyst targets and market price is itself informative: it suggests that the fundamental story is sound but the market demands proof of durability before assigning a higher multiple.

Key Metrics to Track

For investors monitoring BioCryst's ongoing performance, three metrics matter most:

1. Quarterly Orladeyo Net Revenue Growth Rate. This is the single most important indicator of franchise health. Sustained growth above 20% year-over-year signals that oral convenience continues to win market share and that competitive entries are expanding the market rather than taking share. A deceleration below 15% would warrant closer examination of competitive dynamics.

2. New Patient Starts per Quarter (U.S.). BioCryst has disclosed that 2025 marked the highest level of new patient prescriptions in U.S. history. This leading indicator reveals whether the competitive inflow of new products is expanding the diagnosed and treated patient pool or cannibalizing Orladeyo's new patient funnel. Strong new patient starts, even as competition increases, would validate the market expansion thesis.

3. Navenibart Phase 3 Readout and Regulatory Milestones. Top-line Phase 3 data expected in early 2027 and a potential regulatory filing by year-end 2027 represent the highest-impact binary event for the company. Success validates the $700 million Astria acquisition and creates a comprehensive franchise. Failure eliminates the second growth pillar and leaves BioCryst as a single-product company with significant acquisition-related debt.

These three metrics capture the core of BioCryst's investment thesis: can the company sustain Orladeyo growth in a competitive market (KPI #1), continue to expand the treated patient population (KPI #2), and successfully execute on the Astria acquisition to build a multi-product franchise (KPI #3)? Everything else, pipeline programs, international expansion, cost management, flows from these three drivers.

XIII. Epilogue & Reflections

In February 2026, BioCryst reported its full-year 2025 results from its headquarters, which had long since relocated from Birmingham to Durham, North Carolina, though the company retained its Alabama roots and research presence. The numbers told a story that would have seemed fantastical to anyone who had watched the stock languish below $2 after the avoralstat failure a decade earlier: $601 million in Orladeyo revenue, $214 million in non-GAAP operating profit, and a debt-free term loan balance sheet.

Charlie Gayer, the new CEO who stepped into the role just weeks before this report, had built the commercial organization that achieved those numbers. Gayer represents a generational shift in BioCryst's leadership: where Bugg was the scientist-founder and Stonehouse the turnaround operator, Gayer is the commercial executor. His entire BioCryst career, from VP of Global Strategic Marketing in 2015 through Chief Commercial Officer from 2020 to 2025, was defined by one question: how do you sell a rare disease drug to a small, dispersed patient population? His answer, a high-touch patient services model combined with concentrated physician education and a value proposition built on oral convenience, proved effective beyond most analysts' expectations.

Gayer outlined a 2026 plan centered on sustaining Orladeyo growth, integrating the Astria acquisition, launching the pediatric pellet formulation, and advancing BCX10013 through proof-of-concept. The company was also presenting new data on both Orladeyo and navenibart at the 2026 American Academy of Allergy, Asthma & Immunology meeting, reinforcing its commitment to deepening physician education across its expanding HAE portfolio.

The bigger picture of BioCryst's story is what it reveals about the biotech model itself. The company's 39-year path from founding to profitability is an outlier, and not one that most investors or founders could tolerate. But it demonstrates that in biotech, the line between failure and success is often a single molecule's pharmacokinetic profile. Avoralstat and berotralstat target the same enzyme, treat the same disease, and were designed by the same team using the same approach. One failed spectacularly; the other generated $601 million in its fourth full year of sales. The difference was oral bioavailability and half-life, technical parameters that can only be optimized through the kind of deep structural understanding that BioCryst's founders bet on four decades ago.

The M&A question is also worth addressing. At a market capitalization of approximately $1.9 billion, BioCryst is a plausible acquisition target for larger pharmaceutical companies seeking to build or expand rare disease franchises. The company controls the leading oral HAE prophylaxis, has a potentially best-in-class long-acting injectable in Phase 3, and operates commercial infrastructure already serving thousands of rare disease patients. Companies like Takeda (which owns Takhzyro), CSL Behring, or mid-cap specialty pharma companies could find strategic value in acquiring BioCryst's franchise. Conversely, BioCryst could be the acquirer of additional rare disease assets, using its commercial platform to launch new products in adjacent orphan drug markets. The Astria acquisition demonstrated the company's willingness and ability to execute transformative deals.

Could this story have happened outside the U.S. biotech ecosystem? It is difficult to see how. BioCryst relied on NASDAQ public markets for early capital, NIH and BARDA government grants for survival funding during the wilderness years, FDA regulatory pathways (orphan drug designation, fast track, breakthrough therapy) for accelerated development, and Royalty Pharma-style financing structures for commercial launch. The American biotech infrastructure, for all its inefficiencies and waste, remains uniquely suited to supporting the kind of long-duration, high-risk drug development that BioCryst represents.