Berkshire Hills Bancorp: A New England Community Banking Story

I. Introduction and Episode Roadmap

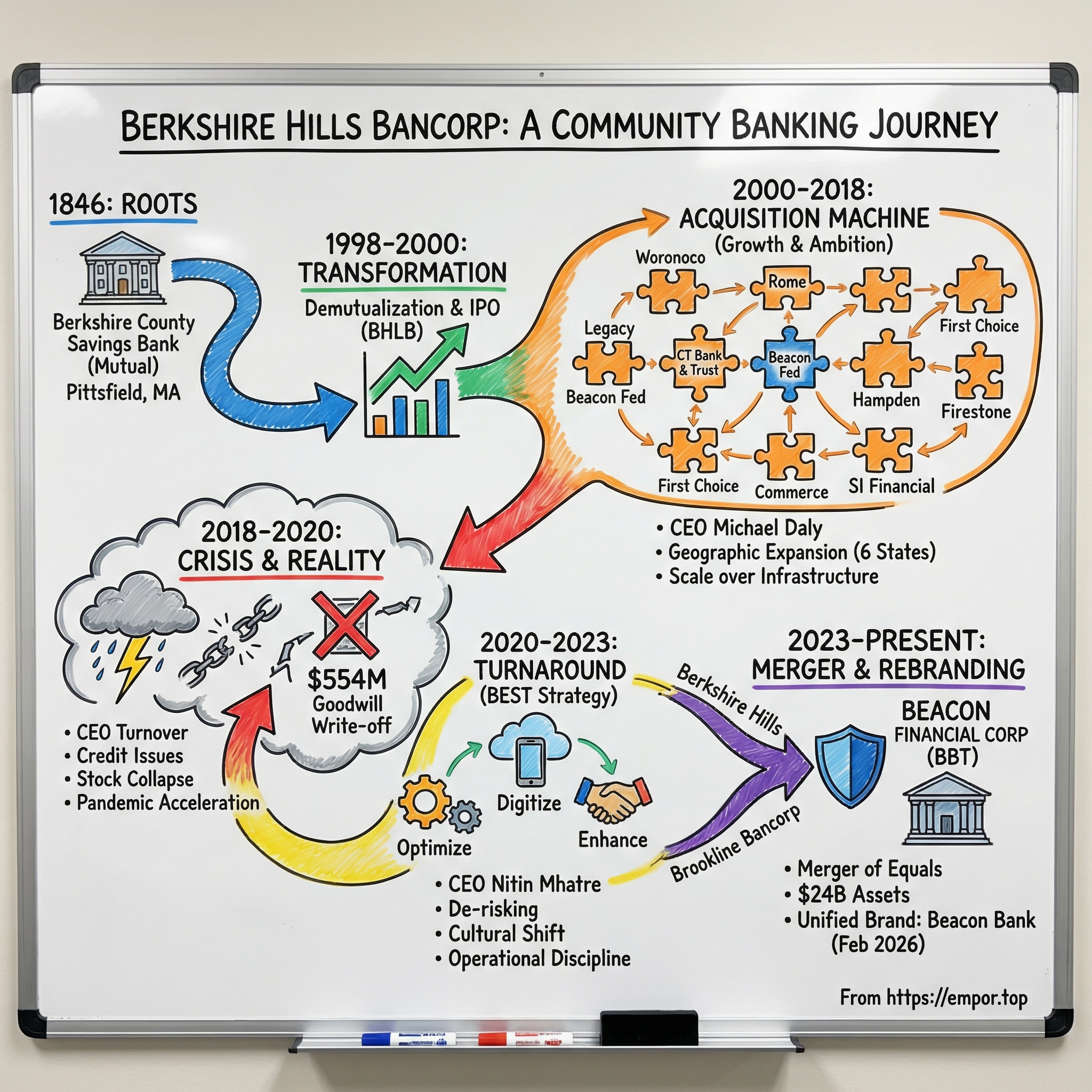

On a crisp autumn morning in Pittsfield, Massachusetts, a small savings bank opened its doors to local mill workers and shopkeepers in 1846. Nearly 180 years later, in February 2026, that same institution had just completed one of the largest multi-bank rebrandings in the northeastern United States, emerging as part of a $24 billion banking franchise called Beacon Bank. The journey between those two moments is one of the most compelling stories in American community banking — a saga of patient compounding, aggressive ambition, spectacular failure, disciplined reinvention, and ultimately, strategic transformation.

Berkshire Hills Bancorp — or as most locals knew it, simply "Berkshire Bank" — operated for most of its existence as a quiet mutual savings bank in the rolling hills of western Massachusetts. For over a century, it did what community banks do: it took deposits from neighbors, made mortgage loans to families, and funded small businesses on Main Street. Then, in the space of about two decades, it demutualized, went public, acquired more than a dozen banks across six states, watched its stock price collapse by two-thirds, fired two CEOs in rapid succession, wrote off more than half a billion dollars in goodwill, hired an outsider to rebuild from the ashes, and ultimately merged with Brookline Bancorp to form Beacon Financial Corporation.

The central question is irresistible: How did a sleepy savings bank from the Berkshire Hills become a $13 billion regional player, nearly destroy itself through ambition, and then find its way to a merger of equals that created one of the hundred largest banks in America?

This story matters because Berkshire Hills is not unique — it is archetypal. Thousands of community banks across America have faced the same existential questions: Stay small and risk irrelevance? Grow through acquisitions and risk losing your identity? Embrace technology and compete with trillion-dollar megabanks? Or find a partner and hope the combination is greater than the sum of its parts? Berkshire tried all of these strategies, in sequence, and the results were alternately inspiring and cautionary.

The themes here cut across every corner of banking and finance: the economics of scale in a regulated industry, the perils of growth-at-all-costs management, the social value of local institutions, and the relentless march of consolidation that has reduced the number of FDIC-insured banks in America from over 14,000 in the 1980s to fewer than 4,500 today. Along the way, we will meet the leaders who shaped this bank's destiny, examine the deals that built and nearly broke it, and assess what the future holds for regional banking in an era of fintech disruption, artificial intelligence, and regulatory uncertainty.

What makes this story particularly timely is the endgame. As of late February 2026, the Berkshire Hills name has ceased to exist. The four legacy banking brands — Berkshire Bank, Brookline Bank, Bank Rhode Island, and PCSB Bank — have been unified under the Beacon Bank banner, completing one of the most complex rebranding projects in recent northeastern banking history. The 180-year institutional journey from Berkshire County Savings Bank to Beacon Bank is, in a very real sense, complete. But the questions it raised — about scale, identity, ambition, and community — are more urgent than ever.

This is the story of Berkshire Hills Bancorp — and the soul of community banking in America.

II. The Berkshire Roots: Origins in Small-Town America (1846–1990s)

Picture Pittsfield, Massachusetts in the winter of 1846. The town sits in a broad valley surrounded by the gentle peaks of the Berkshire Hills, a landscape of dairy farms, paper mills, and the early stirrings of textile manufacturing. The population is modest — perhaps eight thousand souls — and the nearest major city, Albany, lies fifty miles to the west across the New York border. Boston is a grueling day's journey to the east. In this quiet corner of New England, a group of civic-minded citizens decided their community needed its own savings institution.

On February 6, 1846, Berkshire County Savings Bank received its charter from the Commonwealth of Massachusetts. It opened on North Street in Pittsfield — a location that would serve continuously as a bank address for the next 176 years — and began doing what mutual savings banks were designed to do: provide a safe place for working people to save money and earn modest interest, while channeling those deposits into mortgage loans for local homebuyers.

The mutual savings bank model deserves a moment of explanation because it shaped everything Berkshire would become — and everything it would eventually have to shed. Unlike a commercial bank, which is owned by shareholders seeking profit, a mutual savings bank has no shareholders at all. It is owned by its depositors, who are technically "members" of the institution. Profits are retained to strengthen the bank's capital base or returned to depositors through higher interest rates. There are no quarterly earnings calls, no activist investors demanding share buybacks, and no pressure to grow for growth's sake. The model is inherently conservative, community-focused, and stable.

This structure gave mutuals enormous advantages in small-town America. Without the pressure to maximize shareholder returns, they could make relationship-based lending decisions that larger banks would not. They could keep branches open in communities that were not economically "optimal." They could pay their presidents modest salaries and reinvest in the towns they served. For well over a century, this model worked beautifully for Berkshire County Savings Bank and thousands of institutions like it.

But the model also had profound limitations. Without access to equity capital markets, a mutual savings bank could only grow as fast as its retained earnings allowed. It could not issue stock to fund acquisitions. It could not use equity as currency to attract and retain talented executives. And in an era when banking was becoming increasingly competitive and technology-intensive, the mutual structure began to feel like a straitjacket.

Through the decades, Pittsfield itself underwent a transformation that mirrored the broader deindustrialization of New England. General Electric, which had been the city's dominant employer since the early twentieth century, began a long, painful contraction. The paper mills closed. The textile factories shuttered. By the 1980s, Pittsfield was losing population and economic vitality. But something unexpected happened: the Berkshires reinvented themselves as a cultural destination. Tanglewood, the summer home of the Boston Symphony Orchestra, drew hundreds of thousands of visitors. The Norman Rockwell Museum opened in nearby Stockbridge. Jacob's Pillow Dance Festival, MASS MoCA, and a constellation of smaller galleries and theaters transformed the region into a magnet for affluent second-home buyers from New York and Boston.

This cultural renaissance had banking implications. The depositor base was changing — from blue-collar mill workers to a mix of year-round residents and wealthy seasonal visitors. The real estate market was becoming more dynamic. And the competitive landscape was shifting, as larger banks from Springfield, Hartford, and Albany began encroaching on Berkshire County's territory.

By the early 1990s, the leadership of Berkshire County Savings Bank faced a fundamental choice. They could remain a mutual, stay small, and gradually lose relevance as larger competitors arrived with fancier products and bigger marketing budgets. Or they could take the radical step of converting to a stock company — demutualization — and use the capital markets to fund a growth strategy. It was a decision that would change everything.

III. The Demutualization Wave and Going Public (1998–2000)

The 1990s were the golden age of mutual-to-stock conversions in American banking. Across the country, hundreds of mutual savings banks and savings associations were shedding their century-old ownership structures and becoming publicly traded companies. The trend was driven by a confluence of factors: deregulation had expanded the competitive playing field, technology was raising the cost of doing business, and the booming stock market made IPOs irresistibly attractive.

The mechanics of a mutual-to-stock conversion are fascinating, and they created what many investors recognized as one of the most reliable money-making opportunities in finance. When a mutual converts, it sells shares to the public — but the existing depositors get first priority to buy stock at the offering price. Since the bank's assets already exist and the IPO capital is essentially additive, the newly public company is almost always worth more than the IPO price immediately after the offering. It was, in a sense, a legally sanctioned gift to depositors who participated.

Berkshire County Savings Bank began preparing for its conversion in the late 1990s. In 1997, it took a preparatory step by acquiring Great Barrington Savings Bank, another small mutual in the southern Berkshires, and changed its name to simply "Berkshire Bank." The acquisition gave the bank a broader geographic base and slightly larger scale — both important for an eventual IPO.

The conversion came in June 2000. Berkshire Bank filed its S-1 registration statement with the SEC on March 10, 2000, and offered shares to the public at $10.00 per share with a minimum subscription of 25 shares. Sandler O'Neill and Partners — the legendary community bank advisory firm that was itself tragically devastated by the September 11 attacks the following year, losing 83 employees including its three senior partners — served as the underwriter.

The offering raised approximately $71 million, and the newly formed holding company — Berkshire Hills Bancorp, Inc. — began trading on the American Stock Exchange. Shares would later migrate to the New York Stock Exchange under the ticker BHLB.

The strategic rationale was straightforward. The IPO capital gave Berkshire a war chest for acquisitions. Publicly traded stock could serve as currency for deals. Stock options and equity grants could be used to recruit and incentivize management talent. And the discipline of public markets — quarterly reporting, analyst coverage, institutional investors — would push the bank to become more professionally managed and growth-oriented.

But going public also brought immediate challenges. As a tiny publicly traded bank with about $1.5 billion in assets, Berkshire was suddenly operating in a world of larger competitors, demanding shareholders, and relentless consolidation pressure. The number of banks in America had been declining for decades, and the pace was accelerating. The message from Wall Street was clear: grow or be acquired. Berkshire chose growth.

The timing of the IPO was notable — and, in some ways, fortunate. June 2000 was near the peak of the dot-com bubble, and while the NASDAQ was already starting to crack, community bank stocks were relatively insulated from the technology sector's troubles. The $71 million in IPO proceeds was meaningful capital for an institution of Berkshire's size — enough to fund several acquisitions without needing to return to the capital markets. And the depositor-priority structure of the offering had created a base of loyal local shareholders who were unlikely to trade the stock aggressively.

The conversion also changed the governance dynamic in subtle but important ways. As a mutual, the bank had been governed by a self-perpetuating board of directors who answered to no one in a meaningful economic sense. As a public company, the board now had fiduciary duties to shareholders, executive compensation was subject to proxy disclosure, and activist investors could theoretically mount challenges if the bank underperformed. This accountability framework would, over the next two decades, prove to be both a discipline and a pressure cooker.

The early years of public life were not easy. James A. Cunningham Jr., who had been named president and CEO in 1998 to lead the conversion, resigned in 2002. The circumstances of his departure were not publicly detailed, but the bank needed new leadership — someone who could take the IPO capital and the public company platform and build something bigger. They found that leader in an insider who had been quietly working his way up through the ranks.

IV. The Acquisition Machine: Building a Regional Franchise (2000–2012)

In October 2002, the Berkshire Hills Bancorp board elevated Michael P. Daly to the presidency and CEO role. Daly was a lifer — he had joined Berkshire County Savings Bank back in 1986 as a commercial lender, risen through the ranks to executive vice president and chief lending officer, and knew every branch, every market, and every major customer by name. He held a bachelor's degree from Westfield State College and an MBA from Columbia Business School, a combination that reflected both his western Massachusetts roots and his professional ambition.

Daly's vision was audacious for a bank of Berkshire's size: he would use the public company platform to execute a systematic roll-up of community banks across New England and New York, building scale through disciplined acquisitions while preserving the relationship-banking culture that made community banks valuable in the first place. It was a strategy that dozens of regional bank CEOs had attempted. Few had executed it well. Daly, for a time, would prove to be one of the better practitioners.

What set Daly apart from many community bank CEOs was his clarity of purpose. He understood intuitively that the economics of community banking were shifting, that standalone institutions below a certain size would struggle to compete on technology, compliance, and talent. His solution was disciplined, geographically logical acquisition — not empire-building for its own sake, but strategic growth designed to reach a scale at which the bank could invest properly in the infrastructure that modern banking demanded.

The first major deal under Daly came in 2005 with the acquisition of Woronoco Savings Bank, a western Massachusetts institution. The deal, completed on June 1, 2005, was transformative in the most literal sense: it doubled Berkshire's size, creating a $2 billion institution with meaningful density across the region. In the banking world, density matters enormously — it reduces the cost of servicing customers, increases brand visibility, and makes the branch network more efficient. Woronoco gave Berkshire exactly that.

Two years later, in 2007, Berkshire acquired Factory Point National Bank through its holding company Factory Point Bancorp, pushing the franchise across the state line into Vermont. Vermont was a strategic fit — its affluent communities and seasonal tourism economy mirrored the Berkshires' own demographic profile. And critically, Vermont had relatively few large competitors, making it fertile ground for a well-run community bank with a relationship-oriented approach.

But it was the 2011-2012 period that truly defined the Daly era. In April 2011, Berkshire completed the acquisition of Rome Bancorp, the holding company for Rome Savings Bank in upstate New York. The deal, valued at approximately $74 million, marked Berkshire's entry into the Empire State and brought something the bank had lacked: meaningful commercial banking expertise and C&I (commercial and industrial) lending capabilities. Rome was not just a deposit-gathering franchise; it was a bank that knew how to lend to businesses, manage commercial real estate portfolios, and serve the middle-market companies that are the backbone of upstate New York's economy.

Just three months later, in July 2011, Berkshire closed the acquisition of Legacy Bancorp, a deal worth approximately $180 million that made Berkshire the largest bank headquartered in Berkshire County. The transaction required the divestiture of four Legacy branches to NBT Bank to satisfy regulatory requirements — an early sign that Berkshire was reaching a size where antitrust considerations mattered.

The following year brought two more deals. In April 2012, Berkshire acquired The Connecticut Bank and Trust Company for approximately $30 million, adding eight branches in Greater Hartford and marking its entry into Connecticut. The transaction pushed total assets to $4.3 billion with 68 branches. Then, in a deal announced on May 31, 2012, Berkshire agreed to acquire Beacon Federal Bancorp in the Syracuse, New York area for approximately $132 million. Beacon Federal brought seven offices and $677 million in deposits, substantially deepening Berkshire's New York presence.

The logic behind this acquisition spree was rooted in fundamental banking economics. Community banks face enormous fixed costs — compliance infrastructure, technology platforms, risk management systems, executive talent — that scale roughly with the complexity of the operation, not its size. A $1 billion bank needs essentially the same regulatory compliance apparatus as a $5 billion bank. By growing through acquisitions, Berkshire could spread these fixed costs across a much larger asset base, improving its efficiency ratio — the percentage of revenue consumed by operating expenses — and generating higher returns on equity.

There was also a revenue story. Each acquisition brought new customer relationships, new lending opportunities, and the ability to cross-sell products across a broader geographic footprint. A small business owner in Syracuse might need not only a commercial loan but also personal banking, wealth management, and insurance. Berkshire could offer all of these under one roof, while the smaller acquired banks could not.

But acquisition-driven growth is treacherous terrain. Every deal brings integration risk — the challenge of merging different technology systems, aligning different cultures, retaining key employees who may be loyal to the acquired institution, and managing customer disruption. The community banking world is littered with cautionary tales of acquirers who grew fast, integrated poorly, and watched their returns deteriorate even as their asset base expanded.

Under Daly, Berkshire managed this process reasonably well through 2012. The deals were disciplined in size, geographically logical, and executed with a consistent integration playbook. The bank was building something real: a multi-state franchise with genuine density in attractive New England and upstate New York markets.

The financial crisis of 2008-2009 passed through this period as well, and it is worth noting that Berkshire navigated it relatively unscathed. The bank's conservative residential lending practices — a legacy of its mutual savings bank heritage — had kept it largely out of the subprime mortgage business that destroyed so many larger institutions. While the crisis slowed deal activity temporarily, it actually created opportunities for well-capitalized acquirers like Berkshire, as weakened competitors became available at attractive prices. The Rome Bancorp and Legacy Bancorp deals, both completed in 2011, were in part products of the post-crisis landscape.

But success bred confidence, and confidence has a way of becoming overconfidence. The next phase would test whether Berkshire could manage the leap from small regional acquirer to ambitious growth company.

V. The Acceleration: Ambition Meets Complexity (2013–2018)

The Rome Bancorp acquisition had given Berkshire a taste of something intoxicating: commercial banking. Unlike residential mortgage lending, which is essentially a commodity business driven by interest rates and government programs, commercial lending offers higher margins, deeper client relationships, and the opportunity to build a genuinely differentiated franchise. A bank that does commercial lending well becomes indispensable to its business clients — handling payroll, treasury management, lines of credit, equipment financing, and a dozen other services that create switching costs and recurring revenue.

The strategic shift was clear: Berkshire would evolve from a residential-and-consumer-focused savings bank into a full-service commercial banking platform. It was an ambitious transformation, and Daly pursued it with increasing intensity through the middle of the decade.

To understand why this shift mattered so much, consider the economics. A typical residential mortgage might earn a bank 3 to 4 percent in interest, but the loan is largely commoditized — borrowers shop primarily on rate, and the bank's relationship advantage is minimal. A commercial banking relationship, by contrast, is multifaceted. The business owner needs a checking account, a line of credit, a commercial mortgage, treasury management services, perhaps an SBA loan, and eventually succession planning and wealth management advice. Each additional service deepens the relationship, increases revenue per client, and makes the customer less likely to switch to a competitor. In banking parlance, it is the difference between being a vendor and being a partner.

In April 2015, Berkshire completed the all-stock acquisition of Hampden Bancorp, the holding company for Hampden Bank, in a deal valued at approximately $109 million that added 25 branches. The same year, in August, Berkshire made an unusual move by acquiring Firestone Financial Corporation of Needham, Massachusetts, for approximately $53 million. Firestone was not a bank — it was a nationwide specialty finance company serving the amusement, fitness, vending, and laundry industries. The deal signaled Daly's ambition to build fee income streams beyond traditional banking, but it also introduced a business that was far afield from community banking's core competency.

Then came the real step-change. In December 2016, Berkshire acquired First Choice Bank in an all-stock deal valued at approximately $112 million, adding eight branches in Princeton, New Jersey and Greater Philadelphia — the bank's first foray outside its traditional New England and New York footprint. This was a significant geographic leap: New Jersey and Pennsylvania had no connection to Berkshire's existing markets, no brand recognition, and no operational synergies with the New England franchise. The rationale was partly strategic and partly opportunistic — First Choice brought with it First Choice Loan Services, a national mortgage origination platform that gave Berkshire a presence in the lucrative mortgage banking business far beyond its branch geography. The deal added roughly $1 billion in assets and pushed Berkshire into six states.

In retrospect, the First Choice acquisition marked the moment when Berkshire's growth strategy crossed from disciplined expansion to ambitious overreach. Every prior deal had built on geographic adjacency and market knowledge. New Jersey was neither adjacent nor familiar. It was, in the assessment of some analysts, a deal driven more by the availability of a willing seller than by a compelling strategic logic.

The following year, in October 2017, Daly orchestrated his largest deal yet: the acquisition of Commerce Bancshares Corp., the holding company for Commerce Bank and Trust Company in Worcester, Massachusetts. The transaction was valued at approximately $230 million and added roughly $1.8 billion in assets, catapulting combined assets to approximately $5.5 billion with nearly 2,000 employees.

It was a transformative deal — Worcester is the second-largest city in New England, a growing economic hub with major universities, healthcare systems, and a revitalizing downtown. Commerce Bank had served Worcester's business community for decades and had the kind of deep commercial relationships that Berkshire coveted. The deal also brought a new set of bankers with commercial lending expertise, further accelerating the strategic shift toward business banking. Worcester's proximity to Boston — just 40 miles to the west — also positioned Berkshire to tap into the spillover growth radiating from the state capital's booming economy.

In a move that symbolized the bank's evolving identity, Daly signed a lease in November 2017 to relocate Berkshire's corporate headquarters from Pittsfield to 60 State Street in Boston's Government Center district. The optics were striking: a bank that had been founded to serve Berkshire County mill workers was now running its operations from a glass tower in the financial heart of New England. For supporters, it was a sign of growth and ambition. For critics, it was evidence that the bank was losing touch with its roots.

The headquarters move also revealed the internal tension between Berkshire's community banking heritage and its growth-company aspirations. The employees in Pittsfield — many of whom had spent their entire careers at the bank — watched as decision-making migrated eastward. The new hires in Boston brought different skills, different expectations, and different cultural assumptions. This kind of cultural friction is inevitable in any acquisition-driven growth story, but in banking — where trust, relationships, and institutional memory are competitive assets — the costs of cultural disruption are particularly high.

By late 2018, Berkshire Hills Bancorp had grown from one of the smallest banks headquartered in Massachusetts to the largest, operating 75 branches across Massachusetts, New York, Connecticut, Vermont, New Jersey, and Pennsylvania. The stock price hit an all-time high of $35.31 on June 7, 2018. Michael Daly had built, by any objective measure, a remarkable franchise.

But warning signs were accumulating beneath the surface. The bank had grown fast — perhaps too fast. Integration of so many acquisitions in such a short period had stretched management bandwidth. The expansion into new markets like New Jersey and specialty businesses like Firestone Financial had diluted the local knowledge and relationship depth that were supposed to be Berkshire's competitive advantage. Commercial real estate exposure was growing. And the aggressive growth targets that Wall Street rewarded in good times would prove brutally punishing when the cycle turned.

In December 2018, Berkshire announced what appeared to be its most ambitious acquisition yet: SI Financial Group, the holding company for Savings Institute Bank and Trust Company in Connecticut, in an all-stock deal valued at approximately $180 million. The deal would add 18 branches in eastern Connecticut and five in Rhode Island, along with $1.7 billion in assets and $1.3 billion in low-cost deposits. It was a classic Berkshire playbook deal — geographic expansion, deposit gathering, the promise of cost synergies.

But just days before that deal was announced, on November 26, 2018, something extraordinary happened. Michael P. Daly — the man who had spent sixteen years building Berkshire into a regional powerhouse — abruptly resigned as CEO, effective immediately. The bank offered no public explanation. Daly received a separation package valued at $7.5 million.

S&P Global Market Intelligence described the departure as a "surprise" that left "analysts asking 'why?'" Bloomberg News later reported that an anonymous letter about a "toxic" workplace culture may have been a factor. Compass Point analyst Laurie Havener Hunsicker noted there were "no financial issues" related to the removal, suggesting the problem was cultural or managerial rather than financial. Whatever the truth, the architect of Berkshire's transformation was gone — and the foundation he had built was about to be tested in ways no one anticipated.

VI. The Crisis Years: When Ambition Met Reality (2018–2020)

Richard M. Marotta, a board member, stepped into the CEO role following Daly's departure. He inherited a bank in motion — the SI Financial acquisition was pending, the branch network spanned six states, and the organizational complexity of integrating more than a dozen acquisitions over sixteen years was straining management capabilities. Marotta was an experienced financial services executive, but he was inheriting a franchise that had been built by and for one man, and the transition was never going to be seamless.

The SI Financial deal closed on May 17, 2019, pushing assets to approximately $13 billion and adding 23 branches across eastern Connecticut and Rhode Island. On paper, it was a strong deal: $1.3 billion in low-cost deposits, attractive markets, and manageable integration complexity. But the timing could not have been worse. The bank was simultaneously digesting the Commerce Bank acquisition, managing the cultural upheaval of a CEO departure, and confronting the first signs of credit deterioration in its commercial portfolio. Adding another large integration to this already-strained organization was like putting a fourth plate on a spinning-plates act that was already wobbling.

Through 2019, asset quality began to deteriorate. The commercial loan portfolio — the crown jewel of the bank's strategic transformation — was showing stress. Non-performing assets ticked upward. Charge-offs increased. The aggressive loan growth that had powered the bank's expansion was revealing a darker side: underwriting standards that may have been relaxed in the pursuit of volume, concentrations in commercial real estate that exceeded prudent limits, and a risk management infrastructure that had not kept pace with the bank's rapid growth.

The financial results told a story that investors did not want to hear. While the exact quarterly progression of credit deterioration is complex, the trajectory was unmistakable: the bank was heading into trouble. Marotta and his team attempted to stabilize the situation, but they were fighting against a tide of accumulated risk that had been building for years.

Then came the pandemic.

COVID-19 arrived in March 2020 like a wrecking ball swung at the exact weakest point of the building. For Berkshire Hills, the pandemic did not create the problems — it accelerated and exposed them. The commercial real estate portfolio, already under stress, faced the sudden reality of shuttered businesses, deferred rents, and plummeting property values. The hospitality and retail sectors, which were significant components of Berkshire's lending book across its tourist-dependent markets, were devastated overnight. The branch network, spread across six states, became an operational liability as employees and customers alike retreated into lockdown.

The stock price, which had already declined from its mid-2018 peak, went into freefall. From around $27 at the start of 2020, shares plunged to approximately $11-12 as the pandemic's first wave swept through. By the time the dust settled, Berkshire Hills had lost approximately 68 percent of its value over the preceding two years — while the S&P 500 was essentially flat. The stock was trading at barely 55 percent of book value, a level that screamed distress to institutional investors and invited the attention of activist shareholders.

Then came the moment of maximum pain. In the second quarter of 2020, Berkshire Hills took a massive goodwill impairment charge of $554 million. Goodwill, for the uninitiated, is an accounting concept that represents the premium a company pays for acquisitions above the fair value of the acquired assets. When Berkshire had bought Rome Bancorp, Legacy Bancorp, Beacon Federal, Commerce Bank, and all the others, it had paid more than book value for each — reflecting the expected value of customer relationships, brand equity, and future earnings. That premium accumulated on the balance sheet as goodwill.

A goodwill impairment is, in essence, an admission that those premiums were overpaid — that the acquired banks are not worth what was paid for them. The $554 million charge represented virtually all of the goodwill Berkshire had accumulated through years of acquisitions. Combined with $30 million in additional credit losses attributed to the pandemic, the total noncash charges approached $584 million. The result: a net loss of approximately $549 million for the quarter — an $11.02 per share hit that vaporized years of retained earnings in a single stroke.

It was, in the language of banking, a kitchen-sink quarter — a moment when new or transitional management decides to write off everything questionable and reset the baseline. But the magnitude was staggering. To put it in perspective, $554 million in goodwill impairment at a bank with $13 billion in assets is like a homeowner discovering that the house they bought for $500,000 is actually worth $250,000. The house still stands, the mortgage still must be paid, but the equity has evaporated.

The boardroom drama intensified. Richard Marotta, who had been CEO for less than two years, resigned in August 2020 — once again with little public explanation. The bank had now burned through two CEOs in under two years during its most turbulent period. Sean Gray, the board chairman, stepped in as acting CEO, providing interim stability while the board searched for permanent leadership.

The diagnosis was painfully clear: Berkshire Hills had grown too fast, integrated too loosely, and allowed its risk management culture to atrophy under the pressure of ambitious growth targets. The community bank that had spent 150 years building a reputation for conservative, relationship-based banking had tried to transform itself into an aggressive commercial banking platform — and the attempt had nearly destroyed it.

In hindsight, the pattern is recognizable across dozens of community bank failures and near-failures. A charismatic CEO with a compelling growth vision drives a series of acquisitions that build scale and complexity faster than the institution's infrastructure can support. Underwriting standards relax because growth requires volume, and volume requires saying yes to deals that would have been declined five years earlier. Risk management takes a backseat because risk management is a cost center, and cost centers are the enemy of efficiency ratios that analysts scrutinize every quarter. The board, dazzled by rising assets and a climbing stock price, does not ask hard enough questions until the damage is already done.

What makes the Berkshire case especially instructive is the speed of the collapse. The stock went from its all-time high to crisis levels in barely two years. The goodwill — which represented the accumulated premium of every acquisition over two decades — was wiped out in a single quarter. And the leadership vacuum — three CEOs or acting CEOs in under two years — left the institution rudderless at precisely the moment it most needed steady hands.

The stock decline wiped out billions of dollars in shareholder value and made Berkshire one of the worst-performing regional bank stocks of the period. Institutional investors who had bought into the growth story — and at its peak, roughly 87 percent of the float was held by institutions including Vanguard Group at nearly 21 percent and Dimensional Fund Advisors at over 10 percent — were left nursing painful losses. The credibility of the management team was shattered, the strategic vision was discredited, and the very viability of the institution as an independent company was in question.

For investors, the lesson was expensive. For the banking industry, it was instructive. And for the people of Pittsfield, Springfield, Worcester, and all the other communities that Berkshire served, it raised an urgent question: Could this bank be saved?

VII. The Turnaround: New Leadership, New Strategy (2020–2023)

While Sean Gray served as acting CEO through the fall and winter of 2020, the board moved quickly to address the most immediate problems. In December 2020, Gray announced a dramatic restructuring of the branch network: the sale of six Mid-Atlantic branches in New Jersey and two in Pennsylvania to Investors Bank, plus the consolidation of sixteen full-service branches — a roughly 18 percent reduction in the branch footprint. The message was clear: Berkshire was retreating to its core, shedding the geographic overreach that had characterized the Daly era and focusing on the New England and New York markets where it had genuine competitive strength.

On January 25, 2021, the board announced the appointment of Nitin J. Mhatre as the new CEO, effective January 29. It was a watershed moment: Mhatre was the first CEO hired from outside the bank since the 2000 public conversion. Every previous leader had been an insider, steeped in the bank's culture and history. The board's decision to look externally was an implicit acknowledgment that the internal culture had been part of the problem.

Mhatre brought a résumé that blended community banking expertise with institutional sophistication. He had spent more than a decade at Webster Bank, a $31 billion Connecticut-based institution, where he served as executive vice president leading consumer and business banking for more than 1,500 employees. Before that, he had spent thirteen years at Citigroup in various leadership roles across consumer businesses globally. He held an MBA from the Jamnalal Bajaj Institute of Management Studies in Mumbai and had completed the General Management Program at Harvard Business School. He had also served as chairman of the Consumer Bankers Association board, giving him a panoramic view of industry trends and best practices.

His profile was precisely what the board needed: someone who understood community banking's relationship model but had the institutional experience to professionalize risk management, modernize operations, and restore investor confidence. His guiding philosophy, articulated early and often, was deceptively simple: "We want to get better before we get bigger."

His guiding philosophy, articulated early and often, was deceptively simple: "We want to get better before we get bigger." After years of a growth-first mentality that had nearly destroyed the bank, these seven words carried revolutionary implications for how the institution would operate.

On May 18, 2021, Mhatre unveiled his strategic vision: BEST — Berkshire's Exciting Strategic Transformation. The plan was built on three pillars.

The first pillar was "Optimize" — streamlining the geographic footprint through branch sales and closures, optimizing processes, products, and pricing, and eliminating the complexity that years of acquisitions had layered onto the organization. This was the unglamorous but essential work of cleaning house.

The second pillar was "Digitize" — investing in digital platforms and customer experience, partnering with fintech companies, and expanding the bank's proprietary "DigiTouch" strategy that combined digital convenience with personal human service. The concept behind DigiTouch was that technology should augment human relationships, not replace them. A customer might use the mobile app to check balances and transfer money at midnight, but when they needed advice on a mortgage or a business loan, they would speak with a human being who knew their name, understood their situation, and could make decisions locally.

The bank expanded its partnership with fintech firm Narmi to power consumer and small business mobile apps and online banking, offering personalized dashboards, savings tools, and seamless money transfer capabilities. Cloud migration, data warehousing, and modern CRM solutions rounded out the technology investment.

The third pillar was "Enhance" — improving the balance sheet through more profitable lending in business banking, SBA lending, and asset-based lending, while growing the wealth management business. This was about quality over quantity — pursuing loans and relationships that would generate sustainable returns rather than simply inflating the asset base.

The three-year financial targets were concrete: return on tangible common equity of 10-12 percent, return on assets of approximately 1 percent, and a meaningfully improved efficiency ratio. These were not heroic numbers by banking standards — they were the metrics of a healthy, well-run community bank. But for Berkshire, achieving them would represent a genuine transformation.

The turnaround unfolded in stages. In August 2021, Berkshire sold its insurance subsidiary, Berkshire Insurance Group, to Brown and Brown of Massachusetts for $41.5 million, generating a net gain of approximately $0.55 per share. The sale simplified the operating model and freed management attention for core banking operations. In September 2021, Mhatre announced the "BEST Community Comeback" — a $5 billion multi-year ESG commitment to fuel resilience in local communities, encompassing small business lending, community financing, financial access programs, and environmental sustainability initiatives. The program would eventually exceed its $5 billion goal, lending over $3.5 billion to invest in low-to-moderate-income neighborhoods and impacting over 800,000 individuals through financial wellness programming.

The loan portfolio underwent a deliberate contraction as the bank shed lower-quality assets — declining by approximately 27 percent from June 2020 to September 2021. In a growth-obsessed industry where larger loan books translate directly into higher revenue, intentionally shrinking the portfolio required genuine conviction. It was the banking equivalent of a retailer closing underperforming stores — painful in the short term, essential for long-term health.

This was the painful but necessary process of de-risking: sacrificing near-term revenue growth to rebuild asset quality and restore credibility with regulators and investors. Loan loss allowances declined from 1.71 percent of total loans in December 2020 to 1.56 percent by December 2021, reflecting improving credit conditions.

Mhatre also overhauled the leadership team, bringing in new executives for risk management, credit, and other critical functions. The bank brought in Kevin Conn — a veteran institutional investor with over 30 years of experience in financial stocks, including stints at Hudson Executive Capital, MFS Investment Management, Sanford Bernstein, and JP Morgan — as Senior Managing Director of Investor Relations and Corporate Development. Conn's deep buy-side perspective brought a much-needed investor lens to internal strategic discussions and helped rebuild credibility with the institutional shareholder base.

The cultural transformation was perhaps the most important and most difficult element: shifting from a growth-at-all-costs mentality to one that prioritized sustainable returns, disciplined underwriting, and genuine accountability. Mhatre spent considerable time in branches and with front-line employees, emphasizing that the bank's purpose was to serve customers and communities, not to chase metrics. The "DigiTouch" philosophy — combining digital capability with human service — was not just a technology strategy; it was a cultural statement about the kind of bank Berkshire aspired to be. In a notable coup for governance credibility, the bank appointed Eric Rosengren — the former president and CEO of the Federal Reserve Bank of Boston — as an independent director in 2023. Having a former Fed president on the board sent an unmistakable signal to regulators, investors, and the market about the seriousness of Berkshire's governance reforms.

A $140 million share repurchase program signaled confidence in the turnaround and returned capital to patient shareholders who had held through the crisis. In the context of a bank trading well below book value, share buybacks were among the highest-returning uses of capital available — every dollar spent repurchasing shares at a discount to tangible book value was immediately accretive to remaining shareholders.

The financial results gradually improved: operating earnings stabilized, the efficiency ratio came down, and asset quality metrics steadily strengthened. By 2023, the bank reported full-year GAAP income of $70 million and operating income of $93 million, or $2.14 per share. The bank took a strategic securities sale at year-end 2023 to reduce wholesale borrowings and improve its funding profile — a move that modestly impacted GAAP earnings but strengthened the balance sheet for 2024. Full-year 2024 operating income rose to $95 million, or $2.22 per share.

Technology investments contributed to an increase in returns on equity from 3 percent to 10 percent — a remarkable improvement that validated the BEST framework. Berkshire's SBA lending platform, 44 Business Capital, had originated over $500 million in SBA 7(a) loans since 2011, providing a fee income stream that diversified the bank's revenue base beyond traditional spread lending.

The turnaround was not dramatic or sudden. There was no single quarter where everything snapped into place. It was a patient, methodical, multi-year rebuilding effort — the banking equivalent of a house renovation where you have to fix the foundation and the plumbing before you can worry about the paint color. For investors who had watched the stock price collapse from $35 to $11, the recovery was welcome but incomplete. The stock had recovered significantly from its lows, but it was still far from its pre-crisis highs. The question was no longer whether Berkshire could survive — it was what it should become.

VIII. Modern Era: Finding Identity in a Changing World (2023–Present)

The spring of 2023 brought a terrifying reminder that the problems of regional banking were not unique to Berkshire Hills. In the span of a few weeks in March, three much larger institutions — Silicon Valley Bank, Signature Bank, and First Republic Bank — collapsed in rapid succession, triggering the most serious banking crisis since 2008. The panic was driven by a toxic combination of concentrated, uninsured deposit bases, unrealized losses on long-duration bond portfolios, and the viral speed of social media-driven bank runs.

For Berkshire Hills, the crisis was a stress test — both financially and psychologically. As a regional bank with approximately $12 billion in assets, it was squarely in the category of institutions that investors were fleeing. The stock sold off alongside the entire regional bank sector. But the underlying franchise proved more resilient than the market feared. Berkshire's deposit base was diversified, its concentration of uninsured deposits was manageable, and the turnaround under Mhatre had strengthened the bank's fundamental risk posture. Time deposits actually grew from $2.4 billion in June 2023 to $2.7 billion by December — suggesting that some depositors were actively seeking the safety of FDIC-insured community banks.

The bank also benefited, somewhat counterintuitively, from the competitive dislocation. As larger institutions retrenched and tightened lending standards, Berkshire was able to recruit experienced bankers from disrupted competitors and selectively add new customer relationships. The full-year 2023 operating earnings of $2.14 per share were essentially flat with the prior year — a modest result by normal standards, but a sign of stability at a moment when stability was the highest compliment.

In March 2024, Berkshire continued its strategic streamlining by announcing the sale of ten upstate and eastern New York branches to three buyers — Hudson Valley Credit Union, Glens Falls National Bank, and Pathfinder Bank — comprising approximately $485 million in deposits and $60 million in loans. The transaction generated a pre-tax gain of $16 million and reduced the branch count to 83. It was another chapter in the ongoing simplification of the franchise: retreating from peripheral markets and concentrating resources where the bank had genuine competitive advantage.

But the most consequential strategic decision was yet to come.

On December 16, 2024, Berkshire Hills Bancorp and Brookline Bancorp announced a merger of equals to create Beacon Financial Corporation. The all-stock transaction, valued at approximately $1.1 billion, would combine Berkshire's New England and New York franchise with Brookline's network of four banking subsidiaries — Brookline Bank, Bank Rhode Island, PCSB Bank, and Eastern Funding — to create a $24 billion regional banking franchise headquartered in Boston with more than 145 branches across New England and New York.

The deal structure reflected the "merger of equals" framing: Brookline shareholders would receive 0.42 Berkshire shares for each Brookline share, Berkshire's dividend was adjusted to neutralize the impact on Brookline shareholders, and the leadership was split — Paul A. Perrault, the former Brookline Bancorp chairman and CEO, would lead the combined company, while David M. Brunelle, Berkshire's board chairperson, would serve as chairman. Former Berkshire shareholders would control approximately 55 percent of voting interests.

Brookline Bancorp itself was an interesting merger partner. Founded in 1871, it had built a strong presence in the greater Boston market through its Brookline Bank subsidiary, with additional franchises in Bank Rhode Island and PCSB Bank serving communities across the region. Where Berkshire was strong in western Massachusetts, upstate New York, and Connecticut, Brookline was dominant in the Boston metro area, Rhode Island, and the lower Hudson Valley. The geographic complementarity was almost textbook — together, the two institutions could offer continuous coverage from the Berkshire Hills to the Rhode Island coast without significant branch overlap.

The strategic rationale was compelling on multiple dimensions. In an industry where scale drives efficiency and regulatory compliance costs are largely fixed, a $24 billion bank has meaningfully lower unit economics than a $12 billion bank. The geographic overlap between the two franchises was minimal, meaning the combination would expand market reach without requiring painful branch closures. And the combined entity would be large enough to invest in technology, talent, and risk management at a level that neither institution could sustain independently.

There was also a defensive rationale that neither side publicly emphasized but that was implicit in the deal logic. At $12 billion in assets, both Berkshire and Brookline were vulnerable to the same forces that had driven thousands of community banks to sell over the past three decades. At $24 billion, Beacon Financial sits more comfortably in the "super-community" tier — large enough to compete effectively, well-capitalized enough to weather economic cycles, and diversified enough geographically to reduce concentration risk. The merger was as much about survival as it was about growth.

The regulatory approval process moved relatively smoothly. The Federal Reserve, Massachusetts Division of Banks, New York Department of Financial Services, and Rhode Island Department of Business Regulation all signed off. The merger closed on September 1, 2025, and the combined entity began trading on the NYSE under the ticker BBT.

The integration moved swiftly. Banking systems integration was planned for the first quarter of 2026, and the rebranding followed close behind. On February 23, 2026 — just five days before this writing — Beacon Financial Corporation announced the successful unification of all four legacy banking institutions under the Beacon Bank brand. It was described as one of the largest multi-bank rebranding projects in the northeastern United States in the last fifteen years.

Beacon Bank is now one of the hundred largest banks in America.

For Nitin Mhatre, who had been brought in to save Berkshire Hills from crisis, the merger represented the completion of a remarkable arc. He had stabilized the bank, restored its financial health, rebuilt its culture, and ultimately positioned it for a strategic combination that created something larger and more durable than Berkshire could have achieved on its own. Paul Perrault now leads the combined enterprise, but Mhatre's fingerprints are on the foundation.

For the communities of the Berkshires, the transformation carries a particular poignancy. The bank that bore their name for 180 years — the institution founded on North Street in Pittsfield in 1846 — is now part of something bigger and arguably better. But the name is gone. The branches still serve customers, the loans are still made, the deposits are still insured. Yet something intangible has been lost: the identity of a hometown bank that grew up alongside its community.

In a poignant footnote, Michael Daly — the man who had built Berkshire into a regional powerhouse before his abrupt departure — came out of retirement in early 2025 to become CEO of Pittsfield Cooperative Bank, a small community institution right back in the town where his career began decades earlier. The arc of his career — from Berkshire County Savings Bank lender to public company CEO to retirement and then back to small-town banking — captures something essential about the gravitational pull of community banking. No matter how far these institutions reach, the human connections that define them ultimately trace back to a single community, a single Main Street, a single set of relationships built over decades.

IX. The Community Banking Business Model and Industry Dynamics

To understand Berkshire Hills — and the thousands of institutions like it — requires understanding how community banks actually make money, why the business is so structurally challenging, and why, despite everything, these institutions remain vital to the American economy.

The core business of banking is deceptively simple: borrow short, lend long. A bank takes in deposits — essentially short-term loans from customers — and uses those funds to make longer-term loans: mortgages, commercial real estate loans, business lines of credit. Think of it as a spread business, much like a wholesaler who buys goods at one price and sells at another. The "goods" here are dollars, and the margin comes from the difference in price between borrowing those dollars (deposits) and lending them out (loans).

The difference between the interest rate the bank charges on loans and the interest rate it pays on deposits is the net interest margin, or NIM. For most community banks, NIM is the single most important driver of profitability. It typically runs between 2.5 and 4 percent, depending on the interest rate environment, competitive dynamics, and the bank's mix of assets and liabilities. To put that in practical terms: if a bank pays 2 percent on a savings account and charges 5.5 percent on a mortgage, the 3.5 percent difference is NIM. That margin must cover all operating expenses — salaries, rent, technology, compliance — and still leave enough for profit and capital building. Berkshire Hills reported a NIM of 3.27 percent in 2024, which is a healthy figure suggesting the turnaround had improved the quality of its earning assets.

But NIM is not the whole story. Banks also generate fee income — from wealth management, mortgage origination, payment processing, insurance sales, and a variety of other services. For community banks, fee income is typically a smaller percentage of total revenue than it is for larger institutions, which have the scale to build sophisticated fee-generating businesses. Berkshire's 44 Business Capital division, which originated over $500 million in SBA 7(a) loans since 2011, was one example of a fee-generating business that leveraged specialized expertise.

The efficiency ratio — operating expenses divided by revenue — is the other critical metric. It measures how much of every dollar of revenue gets consumed by the cost of running the bank. A lower efficiency ratio is better. Large national banks like JPMorgan Chase can run efficiency ratios in the low 50s, thanks to massive scale advantages. Community banks typically operate in the 60-70 percent range, reflecting higher per-unit costs for compliance, technology, and branch operations. Berkshire's journey from crisis to recovery can be traced partly through this metric: as the bank shed unprofitable branches, rationalized operations, and invested in technology, its efficiency ratio improved meaningfully.

The structural challenges facing community banks are formidable. Rate sensitivity and yield curve dependence mean that profitability can swing dramatically based on Federal Reserve policy decisions that are entirely outside management's control. When the yield curve inverts — when short-term rates exceed long-term rates, as happened in 2022-2023 — the fundamental business model of borrowing short and lending long gets squeezed. Imagine a business where your input costs (deposit rates) are rising while your selling prices (loan rates) are flat or declining — that is what an inverted yield curve feels like for a community bank. And there is essentially nothing management can do about it except wait for the curve to normalize. Regulatory burden falls disproportionately on smaller banks, which must comply with many of the same rules as trillion-dollar institutions but lack the scale to absorb the costs. The technology investment required to meet customer expectations — mobile banking, real-time payments, cybersecurity — is staggering for a $12 billion bank that is competing with institutions fifty times its size.

And yet, community banks endure for reasons that are not captured in financial statements. Local relationship knowledge — understanding that the restaurant owner applying for a loan has been a pillar of the community for twenty years, or that the developer seeking construction financing has a track record of finishing projects on time — is a genuine competitive advantage that algorithms have not yet replicated. Decision-making speed and flexibility allow community banks to respond to customer needs in days rather than weeks. Personalized service, in an era when most financial interactions are mediated by chatbots and automated phone trees, creates genuine loyalty.

The consolidation trend continues — the number of banks in America has declined by roughly 70 percent since 1985 — but the drivers are shifting. Where earlier waves of consolidation were driven by geographic expansion and revenue synergies, today's mergers are increasingly motivated by technology investment requirements, regulatory compliance costs, and the simple reality that many community bank CEOs are reaching retirement age with no succession plan. The Berkshire-Brookline merger is a textbook example of this new dynamic: two healthy institutions choosing to combine not because either was failing, but because the combined entity could invest, compete, and serve customers more effectively than either could alone.

The social dimension should not be overlooked. Community banks are not just economic entities — they are civic institutions. Their officers serve on local boards, their branches sponsor little league teams, their loan officers attend chamber of commerce meetings. When a community bank disappears through merger or failure, something is lost that cannot be measured in basis points or efficiency ratios. The Berkshire Bank Foundation invested $1.7 million in 2024 alone to aid nearly 400 nonprofits addressing housing and food insecurity, and 100 percent of staff participated in annual community service programs. This kind of engagement is not just corporate social responsibility — it is the cultural DNA of community banking, and it represents a genuine competitive differentiation that national banks rarely replicate at the local level.

The question for the industry is whether this social capital can survive the relentless pressure toward consolidation and digitization. The optimistic view is that technology can actually enhance community banking by freeing bankers from administrative tasks and allowing them to spend more time on relationship building. The pessimistic view is that as banks get larger and more centralized, the local connections that make community banking special will inevitably atrophy. The truth, as usual, probably lies somewhere in between.

X. Strategic Frameworks: Competitive Positioning Analysis

Understanding where Berkshire Hills — now Beacon Financial — sits in the competitive landscape requires a structured analysis of industry forces and the sources of durable competitive advantage. The picture is not flattering for regional banks in general, but it reveals specific opportunities for institutions that execute well.

The competitive intensity in banking is extreme. In any given market, a community bank competes simultaneously against national giants like JPMorgan Chase, Bank of America, and Wells Fargo, which can offer the broadest product suites, the most sophisticated technology platforms, and the lowest prices on many products. It competes against other regional banks that may have greater scale and efficiency. It competes against credit unions, which enjoy a tax exemption that allows them to offer slightly better rates on deposits and loans. It competes against fintech startups — neobanks like Chime and SoFi, payment platforms like Venmo and Zelle, and lending marketplaces like LendingClub — that can unbundle specific banking services and deliver them at lower cost through digital channels. And increasingly, it competes against private credit funds that are moving aggressively into commercial lending, often with fewer regulatory constraints and lower capital requirements.

The threat of new entrants has evolved dramatically. Traditional barriers to entry in banking — the charter application process, capital requirements, regulatory approval — remain formidable and keep genuine de novo bank formation at historically low levels. But fintech companies have effectively circumvented these barriers by partnering with existing bank charters or operating in lightly regulated segments of financial services. A consumer today can open a "bank account" with a fintech company that is technically powered by a small community bank's charter but has no branch, no local relationship, and no community commitment. This disaggregation of the banking bundle is perhaps the most significant structural threat to community banks.

Customers have more choice than ever, and the switching costs that once kept depositors loyal to their local bank are eroding. Opening a new account takes minutes on a smartphone. Direct deposit can be redirected in a few clicks. Bill pay, which used to create significant friction for customers considering a switch, is now seamlessly portable. The relationship advantage that community banks rely upon must be continuously earned — it is not structurally embedded in the product the way network effects are embedded in, say, a social media platform.

The substitute products available to banking customers are proliferating at remarkable speed. Digital wallets, peer-to-peer payment apps, buy-now-pay-later services, cryptocurrency exchanges, and robo-advisors all compete for pieces of the traditional banking relationship. Private credit funds now account for an increasing share of commercial lending that once sat squarely in community bank loan portfolios. Shadow banking — the universe of non-bank financial institutions that provide bank-like services without bank-like regulation — continues to grow.

When assessing durable competitive advantages through Hamilton Helmer's Seven Powers framework, regional banks face a sobering reality. Scale economies, the most common source of competitive advantage in most industries, are weak for banks in the $10-25 billion range. They are too large to benefit from the simplicity and low overhead of a true community bank, but too small to achieve the per-unit cost advantages of a JPMorgan. This "no man's land" of banking — large enough to bear full regulatory burden but too small to spread it efficiently — is precisely where Berkshire Hills operated for most of its public life.

Network effects, which power platforms like Visa or Mastercard in the payments space, are largely absent from traditional banking. A deposit account is not more valuable because other people also have deposit accounts at the same bank. Counter-positioning — the ability to adopt a business model that incumbents cannot replicate because it would cannibalize their existing business — is limited for community banks because they cannot out-fintech the fintechs or out-scale the giants.

The supplier side of the equation — where "suppliers" in banking primarily means the cost of deposits and wholesale funding — presents a mixed picture. Deposit pricing is heavily influenced by Federal Reserve rate policy, which affects all banks equally. But in practice, community banks often enjoy a "deposit franchise" advantage: their loyal, relationship-driven depositor base tends to be less rate-sensitive than the hot money that flows to the highest-yielding online savings account. This was demonstrated during the 2023 banking crisis, when Berkshire actually saw time deposits grow as jittery depositors sought the perceived safety of a local, FDIC-insured institution. The deposit franchise is one of the few genuine structural advantages a community bank can possess.

Where regional banks can find additional advantage is in three specific areas. Switching costs, while declining, remain meaningful in relationship banking — particularly in commercial banking, where a business client's entire financial life may be integrated with a single banking relationship. Moving a commercial banking relationship involves changing treasury management systems, renegotiating loan covenants, establishing new credit relationships, and trusting new bankers with sensitive financial information. This creates real stickiness that is difficult to replicate digitally.

Local brand value, while fragile and market-specific, is genuine. In communities like Pittsfield, Worcester, and Hartford, Berkshire Bank built a brand that resonated with customers who valued the idea of a local institution making local lending decisions. This brand equity is not infinitely durable — it can be destroyed by poor service or scandal — but it creates a meaningful advantage over national competitors that are perceived as faceless and impersonal.

And finally, process power — the ability to develop superior internal processes for underwriting, risk management, customer service, and operational efficiency — is perhaps the most important and most achievable competitive advantage for regional banks. A bank that consistently makes better lending decisions, manages risk more effectively, and serves customers more responsively than its competitors can generate superior returns regardless of its size. This is the path that Mhatre's BEST plan attempted to chart for Berkshire Hills.

So what does this analysis tell us? The verdict for the institution now operating as Beacon Financial is sobering but not hopeless: it operates in a structurally challenging industry with limited sources of durable competitive advantage. Success requires relentless execution, disciplined capital allocation, and the ability to find and defend niches where local knowledge, relationship depth, and service quality create real value for customers. Scale alone is not a strategy — but at $24 billion in combined assets, Beacon has achieved a size that makes the economics of technology investment, regulatory compliance, and talent acquisition meaningfully more favorable than they were for a standalone Berkshire Hills.

XI. Playbook: Lessons for Founders, Operators, and Investors

Every crisis produces lessons, but the most valuable are those that can be applied across industries and situations. The Berkshire Hills story is rich with such lessons — some are universal truths of business strategy, others are specific to the dynamics of regulated, capital-intensive industries.

Together, they form a playbook that any operator, investor, or entrepreneur should internalize.

The Berkshire Hills story is rich with lessons that extend far beyond banking. Some are universal truths of business strategy; others are specific to the dynamics of regulated, capital-intensive industries. Together, they form a playbook that any operator, investor, or entrepreneur should internalize.

The first and most important lesson is that growth and discipline are not opposites — they are complements, and when you sacrifice one for the other, the consequences are severe. Berkshire's acquisition spree under Michael Daly was not inherently wrong. The strategic logic of consolidation in fragmented community banking was sound. The individual deals were generally priced reasonably and geographically sensible. What went wrong was the pace and the infrastructure: the bank grew faster than its risk management capabilities, integration processes, and management bandwidth could support. The $554 million goodwill impairment was not the result of one bad deal — it was the cumulative consequence of a dozen deals that, individually, looked reasonable but collectively overwhelmed the organization. The lesson is not "don't grow." It is "match your ambition to your operational capability, and invest in infrastructure before you need it."

The second lesson is that culture eats strategy for breakfast, lunch, and dinner — a maxim attributed to Peter Drucker that is particularly apt in banking, where the daily lending decisions of dozens of loan officers, relationship managers, and branch managers are fundamentally cultural acts. A culture that prioritizes growth above all else will produce loose underwriting, aggressive concentrations, and overlooked risks. A culture that prizes discipline and accountability will catch problems early, say no to marginal deals, and escalate concerns without fear of retribution. Berkshire's cultural breakdown — symbolized by the anonymous letter about toxic workplace culture that reportedly contributed to Daly's departure — was arguably more damaging than any specific financial decision.

The third lesson is about institutional identity. Community banks that try to become something they are not — that chase commercial banking sophistication without the infrastructure, or geographic expansion without the local knowledge, or fee income diversification without the expertise — usually fail. Berkshire's foray into New Jersey and Pennsylvania through First Choice Bank, and its acquisition of Firestone Financial's specialty lending business, were attempts to transcend the community banking model. Both were eventually unwound. The bank found its footing only when it returned to its core: relationship banking in communities where it had genuine presence and credibility.

The fourth lesson is about crisis response. When things go wrong — and in cyclical businesses like banking, they always eventually do — the speed, transparency, and decisiveness of leadership's response determines whether the crisis becomes a chapter in a longer story or the final chapter. Berkshire's crisis response was messy: two CEOs departed in rapid succession, the goodwill write-off was delayed until circumstances forced it, and the turnaround took years to take hold. Compare this to institutions that recognized problems early, took decisive action, communicated transparently with investors and regulators, and emerged stronger. The lesson is that early honesty about problems, even when it is painful, creates the conditions for faster recovery.

The fifth lesson is a reminder that banking is a privileged, regulated franchise. A bank charter is not just a business license — it is a social contract. Banks enjoy access to the Federal Reserve's discount window, FDIC deposit insurance, and the enormous implicit subsidy of government backing. In return, they accept regulatory oversight, capital requirements, and a responsibility to serve their communities. Institutions that forget this social contract — that treat the charter as merely a platform for profit maximization — eventually find that regulators, legislators, and the public will remind them. The Community Reinvestment Act, enhanced supervisory oversight, and consent orders are all tools that regulators use to enforce this social compact, and Berkshire experienced the pointy end of several of them during its crisis years.

The sixth lesson is about capital allocation in cyclical businesses. The time to build capital buffers, strengthen reserves, and invest in risk management is during good times — when growth is easy, credit is clean, and stock prices are high. Warren Buffett's maxim — "Only when the tide goes out do you discover who's been swimming naked" — is nowhere more applicable than in banking. Berkshire, like many community banks, was so focused on growth during the favorable years that it entered the downturn without adequate cushions. The banks that survive crises are invariably the ones that exercised discipline during prosperity.

The seventh lesson is about knowing when to be an acquirer and when to be a seller — or in Berkshire's case, a merger partner. For years, Berkshire operated as a serial acquirer, absorbing smaller banks into its growing franchise. The turnaround required a fundamental shift in mindset: from "how can we get bigger?" to "how can we get better?" And ultimately, the decision to merge with Brookline Bancorp reflected the maturity to recognize that the best path forward was not more acquisitions but a strategic partnership that created something neither institution could build alone. Knowing when to shift from offense to defense — and then to partnership — is one of the hardest strategic judgment calls any management team can make.

Finally, the turnaround playbook itself offers a template: stabilize, simplify, strengthen, then grow. Mhatre followed this sequence almost exactly. First, stabilize — stop the bleeding, retain key employees, reassure regulators and investors. Second, simplify — exit peripheral businesses and markets, shed branches, reduce complexity. Third, strengthen — invest in risk management, technology, talent, and culture. And only then, fourth, grow — cautiously, selectively, and on a foundation that can support the weight. The BEST plan even encoded this sequence in its three pillars — Optimize, Digitize, Enhance — which roughly correspond to simplify, strengthen, and grow.

XII. Bull vs. Bear Case and Investment Considerations

With the merger complete and Beacon Financial Corporation now operating as a unified entity under the Beacon Bank brand as of late February 2026, investors face a classic regional bank evaluation: a business with tangible strengths, genuine risks, and a future that depends heavily on execution, macroeconomic conditions, and industry dynamics that are largely outside management's control.

The bull case begins with the turnaround narrative. The most dangerous period in Berkshire Hills' history is firmly in the rearview mirror. Asset quality has been restored, the goodwill was written off entirely in 2020 (removing the overhang of potential future impairments), and the management team demonstrated the ability to navigate crisis and execute a multi-year strategic plan. The BEST plan's financial targets — including return on tangible common equity approaching 10 percent — were substantially achieved, with Q1 2025 showing operating ROTCE of 9.7 percent, up from 8.7 percent a year earlier, and operating EPS up 22 percent year-over-year. The trajectory entering the merger was clearly positive.

The merger with Brookline creates genuine strategic value. At $24 billion in combined assets with more than 145 branches, Beacon has crossed an important threshold of scale that improves the economics of technology investment, regulatory compliance, and talent acquisition. The geographic complementarity between the two franchises minimizes branch redundancy and maximizes market expansion. The combined deposit franchise serves some of the wealthiest communities in the northeastern United States — a structural advantage in deposit quality and customer lifetime value.

Management optionality is attractive. Beacon Financial could continue to grow organically, pursue selective acquisitions now that integration bandwidth has been freed up by the completion of the rebranding, or potentially become an acquisition target itself for a larger institution seeking Northeast market presence. The stock's valuation relative to tangible book value, while not as distressed as during the crisis years, may still reflect a discount for the uncertainty of post-merger integration.

The deposit franchise deserves particular emphasis in the bull case. Beacon serves communities across some of the wealthiest zip codes in the northeastern United States — from Boston's suburbs to the Berkshires' affluent second-home market to Rhode Island's coastal communities. Wealthy depositors tend to be stickier, less rate-sensitive, and more likely to maintain large balances that provide low-cost funding. This structural advantage in funding costs, if preserved through the integration, could translate into durable margin superiority relative to banks serving less affluent markets.

The bear case is equally compelling, and investors who have lived through the Berkshire Hills crisis understand viscerally that regional banking can destroy capital as efficiently as it creates it.

Regional banking remains structurally challenged: net interest margin compression is a persistent risk in uncertain rate environments, technology investment requirements continue to escalate, and competition from megabanks, credit unions, fintechs, and private credit funds shows no sign of abating. The "no man's land" problem — too large to benefit from community bank simplicity, too small to achieve national bank scale advantages — persists at $24 billion, even though it is less acute than it was at $12 billion.

Regulatory burden and compliance costs remain elevated for banks in this size category. The 2023 regional banking crisis prompted proposals for stricter capital and liquidity requirements for mid-sized banks — rules that, if implemented, would disproportionately impact institutions like Beacon. Technology investment requirements strain returns: a bank that must compete with JPMorgan's $15 billion annual technology budget using a tiny fraction of those resources is engaged in an arms race it cannot win. The best it can hope for is to be "good enough" — which may suffice for relationship-oriented customers but will not retain digital-native consumers.