BlackBerry: The Invisible Nervous System of the Modern World

I. Introduction & Episode Roadmap

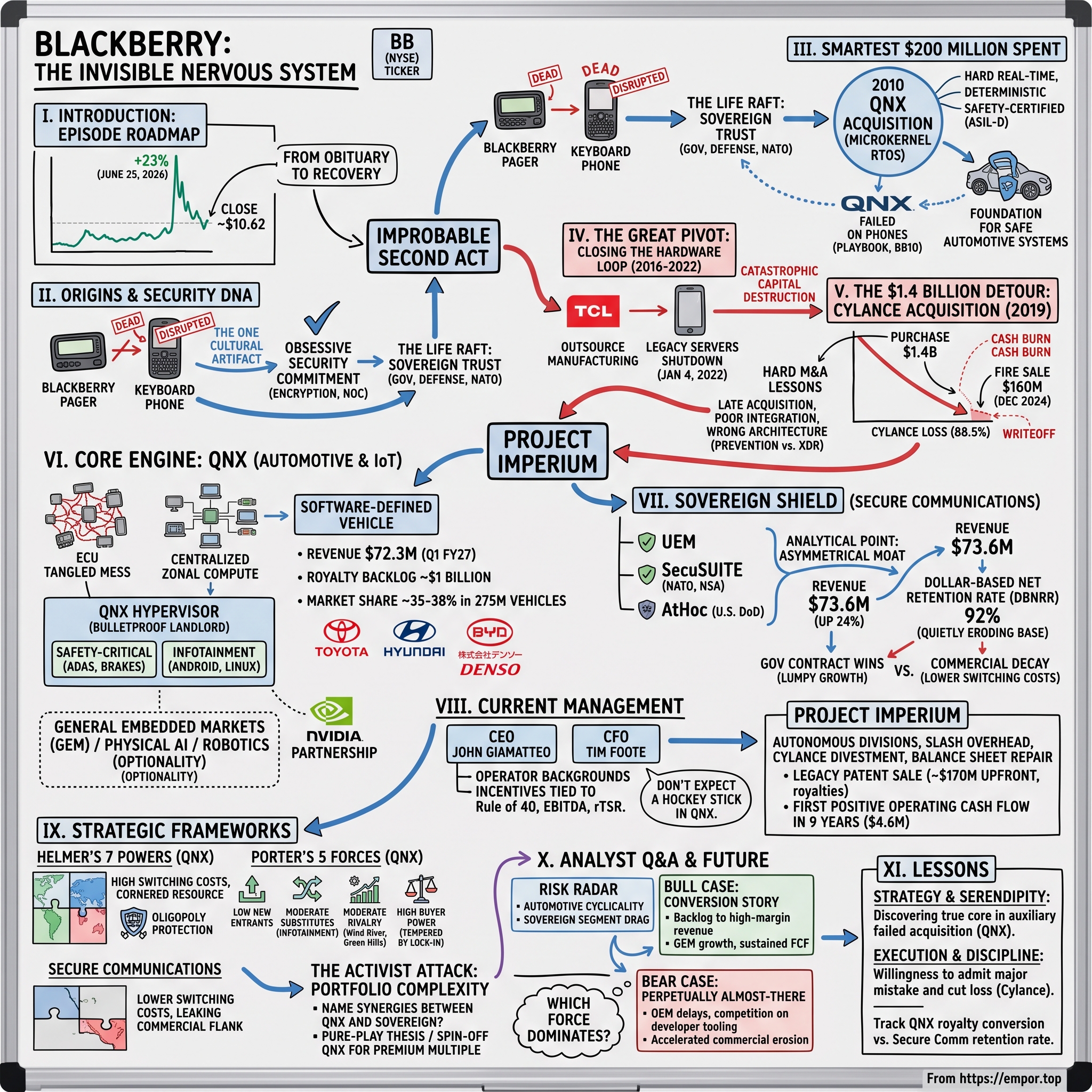

On Thursday, June 25, 2026, something happened to a stock that most of the investing world had long ago filed under "obituary." Shares of BlackBerry Limited, trading on the New York Stock Exchange under the ticker BB, jumped roughly 23% in a single session, closing near $10.62 and capping a run that had nearly tripled the company's value since the start of the year.[^1] For a name that a decade earlier had become shorthand for getting disrupted into oblivion, it was a strange and slightly surreal spectacle. Old-timers on the trading desks rubbed their eyes. BlackBerry? The keyboard phone company? Up 23%?

Here is the thing the average consumer never understood, and still doesn't. To most people, BlackBerry is a museum piece—a memory of clattering physical keys, of "BBM pins" exchanged like secret handshakes, of executives thumbing out emails in the back of town cars circa 2008. It is the company that Steve Jobs and Android steamrolled. That story is true, and it is also completely beside the point of what BlackBerry is in 2026.

Because to the automotive industry, to the defense establishment, to the engineers who build industrial robots and infusion pumps and the brains of cars, BlackBerry is something else entirely. It is the silent, safety-certified operating system humming underneath hundreds of millions of vehicles. It is the encrypted voice line that NATO governments use to discuss things they would prefer adversaries never hear. It is, to borrow a phrase, a kind of invisible nervous system threaded through the physical machinery of the modern world—almost never seen, almost never credited, and increasingly difficult to rip out.

This is the story of one of the most improbable second acts in modern technology. How does a company get utterly annihilated in its core consumer market—not wounded, annihilated—and emerge years later as critical infrastructure for the software-defined vehicle? How does the same company nearly destroy itself a second time with a single catastrophic acquisition, then claw back to its first positive operating cash flow in nine years?

Today we trace that arc. We will examine the legacy security pedigree that kept the lights on when the hardware business collapsed. We will look at what we think is the smartest $200 million the company ever spent—the 2010 acquisition of an obscure operating system called QNX. We will dissect the opposite: the $1.4 billion Cylance acquisition that the company would later dump for pennies on the dollar, an 88% write-off and a master class in how to destroy capital. We will go deep on the economics of QNX, the "hypervisor battle" for control of the car's dashboard, and the expansion into what the company calls General Embedded Markets. We will pressure-test the "sovereign" secure communications business and its defense-grade moat. And we will scrutinize the current leadership—CEO John Giamatteo and CFO Tim Foote—their pay, their incentives, and the turnaround they call internally "Project Imperium."

Throughout, we will keep our analytical posture independent. BlackBerry's management tells a clean story. Our job is to ask what evidence supports it, and what could prove it wrong. Let's get into it.

II. Origins & The Legacy Security Pedigree

Picture Waterloo, Ontario in 1984—a mid-sized Canadian town better known for insurance companies and a strong engineering university than for technology. Two friends, Mike Lazaridis and Douglas Fregin, founded a small electronics consultancy and gave it the slightly grand name Research In Motion, or RIM.1 Lazaridis was the visionary engineer, a man who would later fund a theoretical physics institute and who approached product design with an almost monastic intensity. For years RIM did contract electronics work—a barcode reader here, a film-editing system there—before stumbling onto the idea that would define it: the wireless email pager that became the BlackBerry.

We are going to do something unusual for an origin story and move quickly past the smartphone wars. You know how that movie ends. The iPhone arrived in 2007, Android followed, and within a handful of years BlackBerry's commanding share of the smartphone market evaporated into a rounding error. The keyboards, the BBM messaging, the once-unassailable enterprise grip—gone.

But to understand the company that exists today, you have to isolate the one cultural artifact that survived the collapse. Strip away the hardware, the consumer brand, the marketing. What was left, encoded into the company's DNA from those early enterprise years, was a fanatical, almost obsessive commitment to security—to end-to-end encryption, to hardware-software isolation, to the idea that a communication should be unreadable to anyone but its intended recipient.

This was not a marketing slogan. It was architecture. In its heyday, RIM operated something called the BlackBerry NOC, a Network Operations Center that functioned as a proprietary global relay for secure traffic. Every BlackBerry message, in the classic enterprise configuration, routed through this private infrastructure. That design is precisely why, for years, certain governments demanded access to BlackBerry's systems and why others refused to let their officials use anything else. When the security and intelligence apparatus of a G7 nation trusts your network to carry sensitive traffic, you have built something that is very hard to replicate and even harder to fake.

This is the crucial inheritance. When the consumer hardware business died, that institutional trust—painstakingly accumulated inside central banks, defense ministries, and intelligence agencies over two decades—did not die with it. It became the life raft. Regulated, security-obsessed customers do not switch vendors casually, and they certainly do not switch away from a vendor whose entire identity is built around never being the weak link. The brand that consumers abandoned was, to a general or a finance minister, still synonymous with "the phone the bad guys can't crack."

That distinction—worthless in the consumer market, priceless in the sovereign one—is the thread that kept the company alive long enough to discover what it would become. And the single most important thing it discovered was sitting inside an acquisition almost nobody noticed at the time.

III. The Smartest $200 Million Ever Spent: The QNX Acquisition

Rewind to April 2010. RIM is still, at this moment, a titan—but a nervous one. The iPhone is three years old and accelerating. Internally, the engineers know an uncomfortable truth: BlackBerry's operating system, a creaking edifice of C++ and Java assembled over years of incremental patching, is buckling. It cannot scale to the rich, fluid, app-driven experience that Apple has just normalized. RIM needs a modern, robust, scalable operating system—something to power its planned tablet, the PlayBook, and eventually a next-generation smartphone platform it would call BB10.

So RIM goes shopping. And it buys, from Harman International, a small Canadian software company called QNX Software Systems for approximately $200 million.2 Harman, the audio and infotainment giant, had itself acquired QNX in 2004 for about $138 million.2 At the time, the financial press treated the deal as a footnote—RIM picking up some automotive infotainment software. Almost nobody understood what had just changed hands.

So what exactly is QNX? Here is where we need to slow down, because the technology is the entire investment case. QNX is a real-time operating system, an RTOS, built around an architecture called a microkernel. It was originally developed in 1980 by two University of Waterloo students, Dan Dodge and Gordon Bell, who built a tiny, ferociously reliable operating system and then spent decades refining it.

Let's unpack what "microkernel" actually means, because it's the whole ballgame, and you don't need to be an engineer to get it. Think of an operating system as the management of a building. In a conventional, "monolithic" operating system—Windows, Linux, Android—the kernel is like a single enormous open-plan office where the building's electrician, plumber, security guard, and accountant all share one giant room with no walls. It's efficient when everything works. But if the electrician knocks over a candle, the whole room catches fire, and the entire building goes down with it. A single faulty driver can crash the whole system. We have all watched a phone or a laptop freeze; that is, loosely, a monolithic failure cascading.

QNX's microkernel does the opposite. It puts almost everything—every driver, every file system, every application—into its own sealed room, isolated outside the kernel itself. The kernel is kept deliberately tiny, doing only the most essential coordination. If the plumber's room floods, the fire in the electrician's room is irrelevant; the walls hold. One component can fail and be restarted while everything else keeps running, undisturbed. And critically, the system is deterministic and "hard real-time"—meaning it can guarantee that a given task will complete within a precise, predictable slice of time, every single time, with no exceptions.

For a phone, that reliability is nice to have. For a braking system, it is the difference between life and death.

Now, the irony. RIM tried to use QNX exactly where it intended to: in consumer products. The PlayBook tablet, launched in 2011, ran a QNX-based OS and flopped badly against the iPad. The BB10 smartphone platform, which finally arrived in 2013, was genuinely well-engineered and arrived years too late to matter against an entrenched iOS and Android. Both commercial bets failed. By that measure, the QNX acquisition was a footnote to a tragedy.

Except QNX was never really meant for phones. Its microkernel architecture, its determinism, its bulletproof isolation—these were the precise qualities required by safety-critical automotive systems: anti-lock brakes, electronic steering, advanced driver-assistance. Those systems must be certified to brutal standards, the most stringent of which is ASIL-D—Automotive Safety Integrity Level D—the highest rating under the ISO 26262 functional safety standard. To get there, software must essentially prove it will not fail in ways that kill people. QNX could meet that bar. Almost nothing else could.

So the crown jewel that RIM bought to save its phones could not save its phones at all. Instead, it turned out to be the foundation for an entirely different company—one that wouldn't fully reveal itself for another decade. But before that future could arrive, the company had to do something painful: it had to kill what was left of the past.

IV. The Great Pivot: Closing the Hardware Loop

There is a particular kind of corporate courage required to admit that the thing your company is famous for is dead, and to stop spending money pretending otherwise. Between roughly 2016 and 2022, BlackBerry—it had by then renamed itself from Research In Motion to BlackBerry Limited, taking the name of its most famous product—finally found that courage.

The strategic shift was from being a device manufacturer to being a pure-play software and security licensing firm. The decision was as much arithmetic as philosophy. Designing, building, and selling phones is a capital-intensive, low-margin grind dominated by Apple and a sea of Android makers with vastly greater scale. Licensing software and a brand, by contrast, is capital-light: you let someone else absorb the cost and risk of manufacturing, and you collect high-margin royalties on the way through.

So BlackBerry outsourced. It signed deals letting third parties like the Chinese electronics manufacturer TCL design, build, and sell BlackBerry-branded phones, while BlackBerry collected licensing royalties and, crucially, stopped bleeding cash on inventory and factories it didn't own. The strategy wasn't to revive the hardware business—it was to extract a thin, steady stream of brand rent from its corpse while the real business pivoted elsewhere.

The final act of closure came on January 4, 2022. On that date, BlackBerry officially terminated the provisioning infrastructure for its legacy BlackBerry OS and BlackBerry 10 devices—shutting down the servers that allowed those old phones to reliably make calls, send texts, or connect to data through BlackBerry's systems.3 It was a quiet, almost ceremonial guillotine. The phones that had defined an era became, functionally, paperweights. There was no grand funeral, just a press notice and a date.

What remained, once the hardware was buried, was clarifying. BlackBerry was now a high-margin, pure-play software company organized around two clear pillars. The first was IoT—the Internet of Things—built entirely on the QNX engine and aimed primarily at the automotive industry. The second was cybersecurity, increasingly centered on what the company would come to call Secure Communications: the sovereign, government-grade security business descended directly from that old NOC-era pedigree.

Two clean pillars. A capital-light model. A genuine technological crown jewel. On paper, this was the setup for a disciplined, focused turnaround. Instead, management chose this exact moment to make the single largest capital allocation error in the company's modern history.

V. The $1.4 Billion Detour: The Cylance Acquisition & Hard M&A Lessons

In February 2019, flush with cash from its patent-rich balance sheet and hungry to prove it could be a growth company again, BlackBerry made the biggest bet of its post-phone life. It acquired Cylance, an artificial-intelligence-driven cybersecurity company based in Irvine, California, for $1.4 billion in cash.4

On paper, the logic had a certain seductive cleanliness. Cylance was a darling of the cybersecurity world's first AI wave. Its pitch was elegant: rather than relying on traditional antivirus signatures—essentially a list of known threats, useless against anything new—Cylance used machine-learning models to predict whether a file was malicious before it ever executed. "Prevention, not detection." It promised to stop attacks at the door using mathematics rather than a constantly-updated blacklist. For BlackBerry, the strategic intent was to vault from being a legacy mobile-management vendor into a high-growth, next-generation enterprise endpoint security player. Marry Cylance's AI to BlackBerry's security brand and government relationships, the thinking went, and you'd have a contender.

To understand how badly this went, you have to benchmark what BlackBerry paid against what the rest of the market was doing at that exact moment. The 2018–2019 window was, in hindsight, the most expensive possible time to buy a first-generation AI security asset—and the worst possible architecture to be buying.

Consider the comparables. Around the same period, the private-equity firm Thoma Bravo acquired Sophos, a profitable, broad-based endpoint security vendor, for $3.9 billion.5 Carbon Black, an endpoint-detection player, was acquired by VMware for about $2.1 billion before later being folded toward Symantec.6 And most tellingly, CrowdStrike—the company that would come to define modern cybersecurity—went public in June 2019 at roughly a $6.7 billion valuation and grew, over the following years, into a giant worth north of $60 billion.7

That CrowdStrike comparison is the dagger. Because the entire industry was, at that very moment, pivoting away from the philosophy BlackBerry had just spent $1.4 billion buying. Cylance's "predict and prevent at the door" model was a static approach. The future—the one CrowdStrike and later SentinelOne rode to enormous valuations—was cloud-native, continuous monitoring: EDR (Endpoint Detection and Response) and its broader cousin XDR. The new paradigm assumed attackers would get in, and focused on watching everything continuously, detecting anomalous behavior in real time, and responding fast. BlackBerry paid roughly 10 times revenue for a preventative mathematical model just as the world decided that prevention alone was not enough.4

Overpaying for the wrong architecture is a venial sin if you integrate well and adapt. BlackBerry committed the mortal sin: it integrated badly. Management attempted to force-fit Cylance's technology into its broader "Spark" security platform, a move that alienated Cylance's existing customers, slowed independent product development, and left the cloud-native rivals to feast. While BlackBerry was busy reorganizing boxes on an internal architecture chart, CrowdStrike and SentinelOne were aggressively capturing the market that Cylance had once helped pioneer. The asset withered from neglect and strategic confusion as much as from competitive pressure.

The reckoning came in December 2024. BlackBerry sold Cylance to Arctic Wolf, a security operations firm, for approximately $160 million in cash and stock.[^9] Let that land. A $1.4 billion asset, sold five years later for $160 million—a loss of roughly 88.5%, something on the order of $1.24 billion of shareholder capital incinerated.[^9]

What is the analytical lesson here, beyond "they overpaid"? It is a textbook case of the dangers of late-cycle technology acquisitions. BlackBerry bought a buzzy asset at a peak multiple, on the wrong side of an architectural transition, and then compounded the error by failing to fund and support that asset's migration to the cloud-native SaaS model the market demanded. The eventual fire sale was not the mistake; it was the painful, correct admission of a mistake already made years earlier. As we will see, the decision to finally cut the cord was itself a signal of a different kind of management—one willing to take the loss to stop the bleeding. But to appreciate why that mattered, we first have to understand the asset that made BlackBerry worth saving in the first place.

VI. The Core Engine: QNX and the Battle for the Software-Defined Vehicle

Walk onto the floor of an automotive engineering center—Toyota City, Ulsan, Stuttgart, Shenzhen—and you will find engineers wrestling with a problem that sounds abstract but is reshaping the entire industry. For a century, a car was a mechanical object with some electronics bolted on. Today, a premium vehicle is a computer on wheels, and the question of which software runs that computer has become one of the most consequential battles in technology. This is the arena where BlackBerry's accidental crown jewel finally pays off.

Start with the numbers, because they frame everything. In the first quarter of fiscal year 2027, reported June 25, 2026, BlackBerry's IoT division—overwhelmingly QNX—generated revenue of $72.3 million, up 26% year over year, representing about 47.3% of total company revenue.[^1] But the headline figure that matters more for the long-term thesis is the royalty backlog: roughly $1 billion of contracted future revenue, design wins already secured that will convert to royalties as vehicles ship in the years ahead.[^1] That backlog is the closest thing the company has to a crystal ball, and it is the primary reason the investment case exists at all.

To understand why QNX is positioned the way it is, you have to understand the architectural earthquake reshaping the automobile. For decades, cars added features by adding little computers—Electronic Control Units, or ECUs. One for the engine, one for the brakes, one for the windows, one for the radio. A modern luxury car might contain over 100 of these scattered ECUs, a tangled, heavy, expensive birds-nest of wiring and redundant chips. The industry is now collapsing this mess into a handful of powerful centralized or "zonal" computers, each built on an enormous System-on-Chip, or SoC. Instead of 100 weak brains, the car gets a few very powerful ones. This is the "software-defined vehicle."

Here is where BlackBerry made a genuinely shrewd strategic choice, and it's worth dwelling on because it's counterintuitive. QNX does not try to win the dashboard. It does not fight Google's Android Automotive OS or open-source Linux for control of the touchscreen, the maps, the music, the apps. That is a fight against the deep pockets and developer ecosystems of Big Tech, and it is a fight QNX would lose.

Instead, QNX changes the board. Its weapon is the hypervisor—and this concept deserves a plain-English explanation, because it's the key to the whole strategy. A hypervisor is a thin, ultra-reliable layer of software that sits directly on the silicon and lets a single chip run multiple, completely isolated operating systems at once, as if they were separate computers. Think of it as a bulletproof landlord that rents out sealed apartments on the same building. QNX's safety-certified hypervisor hosts the safety-critical functions—the digital instrument cluster behind the steering wheel, the ADAS logic—running on rock-solid QNX, in one sealed apartment. And in another sealed apartment on the very same chip, it lets Android or Linux run the infotainment system, the flashy consumer-facing stuff. If the Android infotainment crashes mid-drive—and consumer software crashes—the speedometer and the collision-avoidance system, sealed off in the QNX apartment, never even notice.

This is brilliant positioning. QNX doesn't have to beat Google. It can host Google, sitting underneath as the safety-certified foundation that makes the whole arrangement legal and safe to ship. It turns a potential competitor into a tenant.

Let's war-game the competitive landscape, because this is an oligopoly with real players, not a monopoly. In the safety-critical automotive operating system layer, QNX is the clear leader, with estimates putting its share in the range of 35% to 38%, deployed in over 275 million vehicles worldwide.[^10] Its design wins span global OEMs including トヨタ自動車 Toyota Motor Corporation, 현대자동차 Hyundai Motor Company, and 比亚迪 BYD, along with Tier-1 suppliers like 株式会社デンソー DENSO Corporation.[^10]

Its most direct competitor is Wind River, maker of the VxWorks RTOS, now owned by the auto-parts giant Aptiv. Wind River is formidable—by some measures it holds the largest overall commercial RTOS share, around 31.9%, with deep roots in aerospace, defense, and industrial automation.8 VxWorks is a serious competitor in automotive ADAS, though its footprint in the digital cockpit is smaller than QNX's. Then there is Green Hills Software and its INTEGRITY operating system—the high-assurance, aerospace-grade specialist, estimated at 10% to 15% of the automotive OS layer, focused on the most extreme safety-critical applications.[^10] In the infotainment layer above, Google's Android Automotive is rapidly grabbing the consumer UI, perhaps around 11.5% share, but it pointedly lacks safety certification for chassis and powertrain functions.[^10] And open-source Linux, particularly the Automotive Grade Linux project, holds a meaningful slice of the non-safety infotainment layer but cannot run a real-time braking loop.[^10]

The pattern is clear: the higher you go on the safety ladder, the fewer the players and the more dominant QNX becomes. Anyone can write infotainment software. Almost nobody can get a microkernel certified to keep a steering system alive.

Which brings us to the speculative frontier, and we want to size it honestly rather than hype it. BlackBerry talks increasingly about General Embedded Markets, or GEM—extending QNX's safety-certified RTOS beyond cars into industrial robotics, medical devices, and factory automation. The logic is sound: a robot arm working next to a human, or a surgical device, needs exactly the same real-time determinism and fail-safe isolation as a car's brakes. As industrial machinery becomes more AI-driven and autonomous—what some call "Physical AI"—the addressable market for a safety-certified RTOS expands well beyond the driveway. A partnership with NVIDIA, integrating QNX with NVIDIA's robotics and edge-AI platforms, gives the company real optionality to become an operating system for intelligent physical machines.[^12]

But let's be disciplined. GEM today is a promising sub-plot, not the main story. The overwhelming majority of QNX's revenue and backlog is automotive. The Physical AI thesis is optionality—worth watching, potentially material in five to ten years, but not something an investor should underwrite as if it were already happening. The honest framing: the core thesis is the car, and GEM is a free call option attached to it.

So what does all this mean for an investor? QNX possesses something rare in technology—a position protected less by a fast-moving feature war and more by the glacial, high-stakes nature of automotive safety certification. That moat, however, only pays off if the backlog actually converts to royalties, and royalties only flow when cars actually ship. We'll return to that vulnerability. First, the other pillar.

VII. The "Sovereign" Shield: Secure Communications Segment

If QNX is BlackBerry's future, Secure Communications is its inheritance—the direct lineal descendant of that obsessive security DNA we traced back to the NOC era. And in the first quarter of fiscal 2027, it was, just barely, the larger of the two pillars. Secure Communications revenue came in at $73.6 million, up 24% year over year, representing roughly 48.1% of total revenue.[^1] For one quarter at least, the old security business and the new automotive business stood almost exactly shoulder to shoulder.

The segment rests on three pillars, each aimed squarely at customers for whom a security breach is not an inconvenience but a catastrophe. The first is BlackBerry UEM—Unified Endpoint Management—which secures and manages fleets of devices for heavily regulated enterprises and governments. The second is SecuSUITE, a high-security encrypted voice and text platform that has earned validations from NATO, the U.S. government's NIAP program, and the NSA for classified communications.[^13] When the rules say a conversation must be protected at a level appropriate for state secrets, SecuSUITE is on the very short list of products allowed in the room. The third is AtHoc, a critical-event-management platform used by the U.S. Department of Defense and federal agencies for mass-crisis notification and personnel accountability—the system that pings every person on a base during an emergency and confirms they are safe.

Now let's apply the skeptical lens this segment deserves, because the marketing language—"sovereign, military-grade, unassailable"—invites exactly the kind of scrutiny we are paid to provide.

What is the actual evidence for an edge? It is real and it is concrete: substantial government contract wins across defense and federal agencies, riding a genuine geopolitical tailwind. As nations grow anxious about "digital sovereignty"—the desire to keep sensitive data and communications out of foreign and Big Tech hands—and as European data-residency laws tighten, a vendor with deep government certifications and no conflicting commercial-data agenda has a credible pitch. In the sovereign niche, BlackBerry's pedigree, certifications, and trust are difficult to replicate. New entrants cannot simply self-certify their way past the NSA.

But here is where the edge gets thin, and management's broader claims deserve pushback. Step outside the government and defense bunker into the ordinary commercial enterprise market, and BlackBerry's advantage largely evaporates. In standard corporate IT—managing the laptops and phones of a typical company—BlackBerry has comprehensively lost. The winner there is Microsoft, whose Intune device-management tool comes bundled into enterprise software agreements that companies already pay for, alongside a swarm of cloud-native SaaS competitors. Against a free-with-your-existing-subscription incumbent, a standalone security vendor has a brutal time.

And the numbers expose it. The single most revealing KPI in this segment is the Dollar-Based Net Retention Rate, which BlackBerry has disclosed for Secure Communications at 92%.[^1] Let's translate what that means, because it's quietly devastating. A net retention rate measures how much revenue your existing customers, in aggregate, generate this year versus last year, including upgrades, downgrades, and churn. A number above 100% means your installed base is organically growing; the best software companies post 120% or more. A number at 92% means the existing base is shrinking by about 8% a year on a same-customer basis. In other words: even as the segment posts a healthy 24% revenue increase on the back of large new government contracts, the underlying book of business is quietly eroding underneath the headline.[^1]

This is the crucial analytical point, and it cuts against the triumphant narrative. The 24% growth is being driven by lumpy, episodic government wins layered on top of a commercial base that is in slow structural decline. That tells you the "sovereign shield" is genuine but narrow—a strong position in a defensible niche, attached to a commercial business that is losing ground every year. For an investor, the question becomes whether the government tailwind can durably outrun the commercial decay, or whether the 92% is a flashing indicator of a business with a structural ceiling. We don't have to resolve that today; we just have to refuse to let the headline growth number hide the retention number.

Two pillars, then—one with a genuine moat and a conversion question, one with a genuine niche and an erosion problem. The company that has to manage both, and prove it has finally learned discipline, is run by a leadership team that arrived only recently. They deserve their own examination.

VIII. Current Management & "Project Imperium"

For most of the past fifteen years, BlackBerry's story was inseparable from the long, complex, and frequently controversial tenure of John Chen, the executive who arrived in 2013 and spent a decade keeping the company alive through a dizzying series of pivots, promises, and strategic reinventions. That era ended with a deliberate turn toward something leaner and more operationally focused. The new regime is defined by two men: CEO John Giamatteo, appointed in December 2023, and CFO Tim Foote, appointed in July 2024.[^14][^15]

Giamatteo is, by background, an operator rather than a visionary—and that appears to be the point. Before taking the top job, he ran BlackBerry's cybersecurity division. Before BlackBerry, his résumé read like a tour through the trenches of enterprise security and software: President and Chief Revenue Officer at McAfee, Chief Operating Officer at the antivirus firm AVG.[^14] These are not jobs for dreamers; they are jobs for people who carry a number, manage a P&L, and are measured on execution. The board's choice signaled a clear intent: the era of grand reinvention was over; the era of grinding out profitability had begun.

His compensation structure reinforces that read. Giamatteo's base salary was set at $700,000, with a target annual bonus of 100% of salary.9 But the real story, as always, is in the equity. His incentives are heavily weighted toward performance-based stock units tied to Relative Total Shareholder Return—rTSR—measured over a three-year period, alongside specific corporate revenue and EBITDA targets framed around the "Rule of 40," the software-industry benchmark that says growth rate plus profit margin should exceed 40%.9 The rTSR mechanism is worth flagging as a governance positive: it pays out based on how BlackBerry's stock performs relative to a peer group, meaning Giamatteo gets rewarded for beating comparable companies, not merely for riding a rising market. As of April 2026, he held 899,146 common shares directly, giving him a personal stake that rises and falls with ordinary shareholders.9 That's meaningful alignment, though we'd note it's modest relative to the fortunes founders typically hold.

Foote, the CFO, represents continuity of a different kind—an internal promotion. He had previously served as VP of Investor Relations and as CFO of the cybersecurity unit, meaning he knows where the bodies are buried.[^15] His base salary was set at $400,000 with a 75% target bonus, and his performance equity is tied directly to the operational levers that matter: QNX revenue growth, Secure Communications margin expansion, and corporate cash-flow targets.9 The incentive design is telling—the CFO is paid to grow the crown jewel, fatten the margins on the sovereign business, and generate cash. That is a coherent, disciplined set of marching orders.

The strategic program these two have executed is known internally as "Project Imperium." Its substance is unglamorous and, frankly, exactly what the situation demanded: separate the IoT and Cybersecurity units into autonomous operating divisions with their own accountability, slash corporate overhead, and excise the loss-making Cylance business. We've already seen the result of that last item—the painful but correct December 2024 fire sale.

What stands out about the capital allocation record under this regime is its restraint. Rather than chasing another splashy, expensive acquisition to manufacture a growth narrative—the very impulse that produced the Cylance disaster—Giamatteo and Foote have focused on organic execution and repairing the balance sheet. The clearest example came before they fully took the reins but defines the philosophy: in 2023, BlackBerry monetized its legacy mobile patent portfolio, selling it to a vehicle called Malikie Innovations for up to $900 million—structured as roughly $170 million upfront, a further $30 million payable by 2026, plus a stream of future royalties.[^17][^18] It was a way to extract value from a dormant, non-core asset and generate non-dilutive liquidity without issuing new shares or taking on debt. Squeezing cash out of old patents rather than betting it on new acquisitions is precisely the temperament that had been missing.

The clearest evidence of the cultural shift, though, came on the Q1 FY2027 earnings call. Management had genuine good news to deliver: the first positive operating cash flow in nine years, at $4.6 million.[^1] That is a real milestone for a company that had bled cash for the better part of a decade. And yet, rather than spiking the football, CFO Tim Foote actively tempered expectations about the QNX royalty ramp, telling analysts in effect not to expect a sudden vertical surge: "Don't expect a hockey stick in QNX. You see it start to turn up in the backlog and then over time that really starts to cascade and escalate."[^1]

That sentence is worth more than it appears. For years, BlackBerry's management—across different eras—was associated with promotional narratives that consistently outran results, the overpromise-underdeliver cycle that trains investors to distrust everything. A CFO who, on a good-news day, deliberately walks down expectations and describes a slow cascade rather than a moonshot is doing something subtle and important: he is rebuilding credibility by setting targets he can actually beat. Whether the team sustains that discipline over multiple years is the open question, but the early behavior—taking the Cylance loss, monetizing patents instead of acquiring, tempering the hockey-stick narrative—is consistent across filings and calls. For a company with BlackBerry's history of strategic whiplash, consistency is itself a form of progress.

A turnaround built on discipline rather than dazzle invites a particular kind of question: is the structure that remains actually the right one? That is the terrain of strategy, and of the skeptics.

IX. Playbook & Strategic Frameworks

Let's put BlackBerry's surviving businesses on the analytical workbench and run them through the frameworks that strategy nerds—us included—reach for when we want to know whether an advantage is real or merely asserted. The honest finding is that the two pillars score very differently, and the divergence is the whole point.

Start with Hamilton Helmer's 7 Powers, applied to QNX. The dominant power here is High Switching Costs, and in QNX's case they are almost comically large. Designing a safety-critical operating system into a vehicle's primary compute architecture is not a software-download decision; it is a 5-to-7-year development lifecycle. An OEM that selects QNX for its ASIL-D braking and ADAS microkernel embeds that choice into thousands of engineering decisions, supplier contracts, and safety cases. To switch to Wind River's VxWorks or Green Hills' INTEGRITY mid-stream would mean hundreds of millions of dollars in software rewrites, a re-mobilization of scarce safety engineers, and—the real killer—a complete regulatory re-certification of life-critical systems. No rational automaker incurs that cost to save a few dollars per unit on a license. Once you're in, you're in for a vehicle generation, often two. That is switching-cost lock-in of the highest order.

The second power QNX enjoys is a Cornered Resource: the certifications themselves and the human expertise behind them. ISO 26262 compliance and ASIL-D status are not features you bolt on; they are the product of decades of validation, formal mathematical proofs, and accumulated safety-engineering judgment. You cannot write a safety-certified microkernel over a weekend, or even over a couple of well-funded years. The scarcity of organizations that have actually done it—essentially three—is a resource competitors cannot quickly conjure. Capital can't buy it; only time and rare expertise can.

Now run Porter's Five Forces over the same automotive business, and the picture is strikingly favorable on most axes. The Threat of New Entrants is very low—the safety standards, regulatory validation, and decade-deep Tier-1 relationships form an almost impassable barrier, the same point from a different angle. The Threat of Substitutes is moderate but bounded: Linux and Android genuinely substitute for QNX in the infotainment layer, but they cannot touch the safety-critical chassis, ADAS, and autonomy domains where QNX lives. Competitive Rivalry is moderate—a tight, three-way oligopoly of QNX, Wind River, and Green Hills, where competition is real but the pie is protected and the players are few.

The one force with genuine tension is the Bargaining Power of Buyers, which we'd rate moderate-to-high. Toyota, Hyundai, and BYD are colossal, sophisticated buyers who negotiate ferociously and would love nothing more than to commoditize their software suppliers. That power is real. But it runs headlong into the switching costs and the cornered resource: an OEM can squeeze QNX on price at the margin, but it cannot credibly threaten to walk, because there is nowhere safety-certified to walk to on short notice. The buyer's whip has a short handle.

Here is the analytical sting, though, and it's why this section matters beyond the automotive cheerleading. Almost everything we just said applies to QNX and only QNX. Run the same frameworks over Secure Communications and the powers thin out fast. Switching costs in government UEM and encrypted comms are real but lower than in automotive. The cornered resource—government certifications—is genuine but narrower. And in the commercial market, the buyer power is overwhelming and the substitutes (Microsoft Intune) are devastating, which is exactly why that 92% retention rate looks the way it does. The frameworks don't just flatter BlackBerry; they diagnose it. One pillar has a deep, durable moat. The other has a defensible foxhole and a leaking commercial flank. That asymmetry is precisely what sets up the activist's central argument.

X. The Analyst Q&A, Activist Stress Test, and Bear vs. Bull Cases

Imagine a sharp activist investor building a slide deck on BlackBerry. Where does she aim? Not at the technology—QNX is genuinely good. She aims at the structure. And her opening question is devastatingly simple: why on earth are these two businesses still inside the same company?

This is the Portfolio Complexity attack, and post-Cylance it has real teeth. With the cybersecurity distraction divested, what remains is an automotive embedded-software business and a sovereign government-communications business. The activist's challenge: name one technical or commercial synergy between selling a safety-certified RTOS to Toyota and selling encrypted voice to a defense ministry. There essentially isn't one. They share a logo and a balance sheet and almost nothing else—no common customers, no shared technology stack, no cross-sell. They are two unrelated companies wearing a single corporate costume.

The pure-play thesis follows naturally. A focused automotive embedded-software business with a $1 billion backlog and structural switching-cost moats could plausibly command a premium revenue multiple—the kind of 8-to-10-times-revenue valuation the market awards to high-quality, mission-critical software franchises—if it traded on its own merits. Bundled inside BlackBerry, that jewel trades at the company's depressed, blended multiple, weighed down by the slower-growth, eroding-commercial-base secure-communications segment sitting next to it. The activist's pitch writes itself: spin off or sell QNX, let it re-rate to its standalone worth, and stop letting the sovereign business's baggage discount the crown jewel. We are not endorsing the trade—spinoffs carry costs, dis-synergies, and execution risk of their own—but as an analytical challenge to the status quo, it is the sharpest arrow in the quiver.

Now the risk radar, focused only on what is material. The first genuine threat is automotive cyclicality. QNX's economics depend heavily on per-unit royalties earned when vehicles actually ship. The $1 billion backlog is a promise, not a deposit; it converts to cash only as cars roll off lines. A global downturn in auto production—from a recession, a supply shock, or a demand slump—would directly throttle royalty conversion regardless of how many design wins sit in the pipeline. The backlog gives visibility; it does not give immunity from the business cycle. The second material risk is the sovereign-segment drag we've already diagnosed: if the commercial DBNRR stays stuck near 92%, the slow organic decay of that base will keep acting as a quiet anchor on consolidated margins and on the company's valuation multiple, partially offsetting QNX's progress.

So let's lay out the two cases honestly.

The bull case is a conversion story. QNX steadily turns its $1 billion backlog into high-margin royalty revenue as software-defined vehicles ramp; the GEM expansion captures real share of the Physical AI and robotics boom, turning the free option into actual revenue; and Project Imperium's discipline compounds into durable structural profitability and sustained positive free cash flow. In that world, the market eventually stops valuing BlackBerry as a washed-up phone company and re-rates it as the mission-critical software franchise it has quietly become. The first positive operating cash flow in nine years is, on this view, the first data point of a long climb.

The bear case attacks every link in that chain. Auto OEMs, notorious for moving slowly, delay the rollout of the centralized architectures that QNX's growth assumes, pushing royalty conversion years to the right. Wind River, armed with modern cloud-native developer tooling, chips away at QNX's digital-cockpit share by making its platform easier and cheaper for developers to build on—competition on developer experience rather than safety pedigree, where QNX is less obviously dominant. And the secure-communications business keeps shedding commercial customers to Microsoft, so that even as government wins roll in, blended corporate margins erode. In that world, BlackBerry remains a perpetually-almost-turning-the-corner story, cheap for good reason.

The truth, as usual, lives in the execution between these poles. The frameworks tell us the QNX moat is real; the retention rate tells us the sovereign flank is leaking; the cash-flow milestone tells us the discipline is, so far, genuine. Which force dominates over the next several years is exactly what an investor is being asked to underwrite.

XI. Outro & Lessons

There are two lessons in the BlackBerry story, and they sit in tension with each other in a way that makes the whole saga worth telling.

The first is a lesson about strategy and serendipity. Sometimes the path to survival is not defending your primary kingdom, but discovering that an obscure, auxiliary asset you acquired almost by accident is in fact the core of the future world. RIM bought QNX for $200 million to save its smartphones. The smartphones died anyway. But buried inside that "failed" acquisition was a safety-certified microkernel that turned out to be one of the most strategically defensible positions in the entire automotive software stack—a position the company could not have engineered on purpose if it had tried. The crown jewel was hiding in plain sight, mislabeled, for a decade. That is a humbling reminder that companies rarely understand their own most valuable assets in real time.

The second is a lesson about execution and the discipline to admit you were wrong. The same company that got lucky with QNX got catastrophically unlucky—or rather, made catastrophically poor decisions—with Cylance, lighting $1.24 billion on fire on the wrong side of a technology transition. What ultimately mattered was not avoiding the mistake, which had already been made, but the willingness to take the 88% loss, cut the cord, separate the divisions, and stop pretending. Pragmatic capital allocation requires the institutional humility to crystallize a painful loss in service of a cleaner future. It is far easier to keep a failing acquisition on life support and hope; it is far harder, and far more valuable, to bury it.

Together, those two lessons describe a company that survived less through grand vision than through a combination of accidental good fortune and, belatedly, hard-nosed discipline. BlackBerry in 2026 is a leaner, stranger, and considerably more interesting business than the keyboard-phone ghost the consumer world remembers. Whether the invisible nervous system threaded through the world's cars and government networks becomes a great investment depends on questions we cannot answer here: whether the backlog converts, whether the moat holds, whether the discipline lasts. But the watch items are now clear—QNX royalty conversion against that $1 billion backlog, and the Secure Communications retention rate as the tell on whether the sovereign edge can outrun the commercial decay. Track those two numbers, and you will know which story is winning.

References

-

SEC Edgar Search — BlackBerry Limited CIK 0001070235 Filings ↩↩

-

BlackBerry Q1 FY2027 Earnings SEC Form 10-Q — BlackBerry Limited, 2026-06-25 ↩

-

SEC Form DEF 14A Definitive Proxy Circular — BlackBerry Limited, 2025-05-16 ↩↩

-

BlackBerry CIK 0001070235 Corporate SEC Filings Archive — SEC.gov ↩

-

SEC Edgar Search — BlackBerry Limited Filings Archive, CIK 0001070235 ↩

-

Wind River Market Share and Industry Leadership Report — VDC Research, 2024-05-15 ↩

-

SEC Form DEF 14A Definitive Proxy Circular — BlackBerry Limited, 2025-05-16 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube