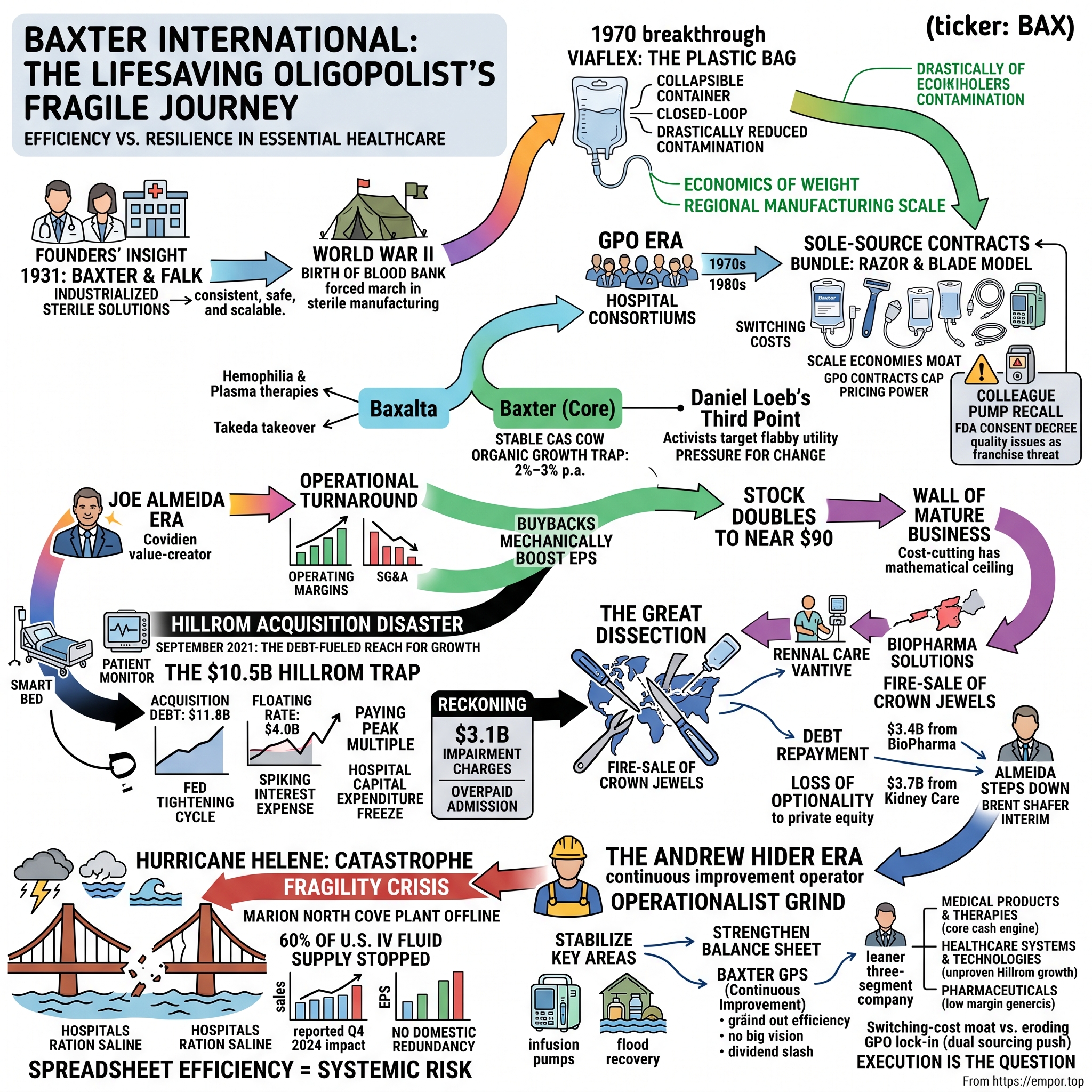

Baxter International: The Fragility of a Lifesaving Oligopolist

I. Introduction & Episode Roadmap

In the last days of September 2024, the rain over Western North Carolina simply would not stop. Hurricane Helene, a storm that had come ashore in Florida's Big Bend and refused to die, stalled over the southern Appalachians and dumped more than two feet of water onto mountains that funnel every drop downhill. In the small town of Marion, the Catawba River rose over its banks, a levee gave way, and floodwater poured into a sprawling 1.4-million-square-foot complex on the edge of town. Bridges providing access to the site were torn out. Within hours, the single largest source of intravenous fluid in the United States was underwater and offline.1

The consequences did not stay in Marion. Over the following days, hospital pharmacists from Boston to Los Angeles opened their supply portals and discovered they could not order saline. Health systems activated emergency conservation protocols. Surgeons postponed elective operations. Nurses were instructed to push medications by mouth where they could, to switch patients off drip bags and onto oral hydration, to treat the humble bag of salt water — the most basic, unglamorous product in all of medicine — as a rationed commodity. A Premier survey found that 86% of U.S. providers were affected by shortages.1 The U.S. Food and Drug Administration would not declare the sodium chloride shortage fully resolved until August 8, 2025 — nearly a year later.2

Here is the question that ought to stop any investor cold. Why did a single flooded plant in a town of 8,000 people hold the key to roughly 60% of the entire U.S. supply of IV solutions?1 How did the world's most essential medical liquid come to depend on one bend in one river in one Appalachian valley?

The answer is the story of Baxter International, and it is a more uncomfortable story than the company's ninety-year heritage of lifesaving innovation would suggest. Baxter did not stumble into that concentration by accident. It engineered it, deliberately, over decades, because for a product as heavy and cheap as salt water, scale is the whole game — and scale, pursued to its logical extreme, means putting an enormous amount of eggs in one very large basket. What looks like fragility on a hurricane map looks like ruthless efficiency on a spreadsheet. They are the same decision viewed from two directions.

That paradox — a lifesaving oligopolist that is simultaneously indispensable and financially brittle — is what this story is about. And the fragility runs deeper than any one plant. This is a ninety-year-old medical giant that pioneered sterile IV therapy, built one of the great razor-and-blade lock-ins in American healthcare, and then, in the span of a single disastrous decade, nearly broke itself with a debt-fueled acquisition made at precisely the wrong moment in the interest-rate cycle.

Here is the roadmap. We start in the Great Depression, with two Midwestern doctors who decided that hospitals should not be brewing their own IV fluids in back rooms. We move to the postwar decades, when a collapsible plastic bag became one of the quiet miracles of modern medicine — and the foundation of an economic moat built on the sheer weight of water. We watch Baxter turn the rise of hospital purchasing cartels, the Group Purchasing Organizations, from an existential threat into the ultimate customer lock-in. Then comes the modern tragedy: a chief executive who squeezed a commodity utility to its margin ceiling, ran out of organic growth, and reached for a $10.5 billion acquisition of a hospital-bed maker just as the Federal Reserve began the fastest tightening cycle in forty years.3 We trace the "great dissection" that followed — the activist-pressured fire-sale of Baxter's best businesses simply to survive the debt. We stand in the Marion floodwaters. And we end in the present: a leaner, humbled, three-segment medtech company under a brand-new CEO, trying to convince the market that the worst is behind it.

Throughout, we will keep an independent posture. Baxter's management, like all management, tells a story of discipline restored and a turnaround underway. Our job is to ask what evidence supports that story, and what could falsify it.

II. The Depressional Pioneers & The Invention of the Bag

Picture a hospital ward in the 1920s. A patient is dehydrated, or in shock, or bleeding out, and the physician orders intravenous fluids. What happens next would horrify a modern clinician. There is no bag to hang. Somewhere in the building, a pharmacist or a nurse is mixing salt and water by hand, boiling it, and pouring it into a reused glass bottle, hoping the sterilization held. Frequently it did not. The great killer was not the wrong chemical balance, though that happened too; it was pyrogens — fever-inducing bacterial byproducts that survived sloppy sterilization and sent patients into raging, sometimes fatal, chills within minutes of the drip starting. Intravenous therapy in that era was a genuine gamble, and everyone in the room knew it.

Into this problem walked two Iowa physicians. Dr. Donald Baxter and Dr. Ralph Falk shared a conviction that was almost heretical for the time: that sterile IV solutions should be manufactured under controlled industrial conditions and shipped to hospitals ready to use, rather than improvised bedside. In 1931 — the depths of the Depression, hardly an obvious moment to launch a capital-intensive medical venture — they founded the Don Baxter Intravenous Products Company to distribute commercially prepared intravenous solutions to hospitals across the Midwest.4 Two years later, in 1933, they opened a manufacturing plant in Glenview, Illinois, with six employees producing five different solutions, each packed in evacuated glass containers under vacuum.4 Falk bought out Baxter's interest in 1935 and set about turning a distribution idea into an industrial company.5

The intellectual leap here is worth sitting with, because it recurs throughout Baxter's history. The founders' insight was not chemical; the recipes for saline and dextrose were well understood. The insight was industrial: that consistency, sterility, and scale were themselves the product. A hospital could not reliably make safe IV fluid, but a purpose-built factory obsessed with a single process could. Baxter was, from birth, less a pharmaceutical company than a manufacturing-quality company that happened to make medicine.

The Second World War turned that quiet insight into a proven capability. Baxter had already, in 1939, introduced the Transfuso-Vac, a sterile vacuum-type collection and storage unit that made it possible to store blood for up to 21 days — effectively the birth of the modern blood bank.4 A companion product, the Plasma-Vac, followed in 1941 and allowed plasma to be separated and stored from whole blood.4 When the United States entered the war, these were not laboratory curiosities; they were battlefield necessities. Baxter supplied blood-collection products and intravenous solutions to the U.S. armed forces, and the war became a massive operational crucible — a forced march up the learning curve of sterile manufacturing at a scale no peacetime market would have demanded.5 Companies that survive their industry's formative war often emerge with capabilities competitors can never quite replicate, and Baxter came out of the 1940s with exactly that kind of hard-won process knowledge.

But the innovation that defines Baxter to this day arrived in 1970, and it is worth explaining carefully because its economics reverberate straight into the Marion floodwaters. That year, Baxter introduced Viaflex — the first flexible, collapsible plastic IV container.6 For decades, IV fluid had traveled in rigid glass bottles. To drain, a glass bottle needs air to enter as fluid leaves, which means it must be vented — and every vent is an open door for airborne contamination and, in the worst case, a route for a fatal air embolism into the patient's bloodstream. Viaflex solved this with elegant simplicity: a soft plastic bag that collapses on itself as it empties, like a juice pouch, so no air ever needs to enter the system. It was a closed loop, dramatically reducing contamination and embolism risk.6

The clinical benefits were obvious. The economic consequences were subtler and far more important to the story of Baxter as a business. Consider what an IV bag actually is: it is mostly water, sold at a very low unit price, and water is heavy. A pallet of saline is a pallet of salt and purified water in thin plastic — enormous weight and volume relative to its dollar value. This is the defining economic fact of the sterile-fluids business, and it dictates everything. You cannot ship saline economically across an ocean the way you ship a vial of a specialty drug worth thousands of dollars per gram. The freight cost would swamp the product's value. To win in IV fluids, therefore, you must build massive regional manufacturing scale, locate your sterilization infrastructure close to demand, and run a high-volume, tightly optimized distribution network. Viaflex, by making the container lighter and unbreakable, only sharpened this logic — it made scale cheaper to ship and thus made big plants even more advantageous relative to small ones.6

Viaflex was not the only postwar breakthrough that would echo into Baxter's modern portfolio. The same institutional obsession with sterile fluids and closed-loop delivery led Baxter into dialysis — first the artificial-kidney machines that filter the blood of patients whose own kidneys have failed, and later peritoneal dialysis, a technique that uses the patient's own abdominal lining as a filter and depends on large volumes of sterile dialysis solution. That solution is, once again, mostly water in a bag: heavy, low-value-per-unit, and governed by exactly the same manufacturing-and-freight economics as saline. Dialysis therefore grew up inside Baxter as a natural extension of the fluids franchise, sharing plants, sterile-manufacturing know-how, and distribution muscle. It is worth flagging this now because it explains something that will matter enormously later: when Baxter eventually sold its Kidney Care business under duress, it was not shedding a bolt-on acquisition but severing a limb that had grown from the same root as the company itself. The renal business and the IV business were, in a deep sense, two branches of one sterile-fluids tree.

This is the origin of the moat, and also the origin of the fragility. The same physics that makes it nearly impossible for a new entrant to undercut Baxter on saline — because they too would need to sink hundreds of millions into FDA-compliant sterile plants near their customers — is the physics that pushed Baxter toward a handful of gigantic facilities rather than many small ones. Over the decades, that logic concentrated an outsized share of American IV production at the North Cove plant in Marion, North Carolina, which grew into one of the largest sterile-solutions manufacturing sites in the country, employing more than 2,500 people.7 A spreadsheet optimizing purely for cost per bag will always tell you to build one enormous plant rather than three medium ones. Baxter listened to the spreadsheet. Fifty years later, a hurricane sent the bill. But before the bill came due, Baxter would spend decades turning this manufacturing moat into something even more durable: a lock on the hospital itself.

III. The GPO Era: Building the Ultimate Hospital Lock-In

In the 1970s, American hospital administrators looked at their supply costs and had a collective realization: they were being picked off one at a time. A single community hospital negotiating with a national supplier had essentially no leverage. So they did what buyers throughout economic history have done when facing concentrated sellers — they combined. They formed Group Purchasing Organizations, or GPOs, pooling the purchasing volume of dozens or hundreds of hospitals to squeeze suppliers on price. The pivotal moment came in 1977, when Voluntary Hospitals of America launched the national "super group" model, and the trend accelerated through the 1980s as Medicare's shift to fixed, diagnosis-based payments put brutal cost pressure on hospitals and drove them to consolidate their buying.8

On its face, this should have been a catastrophe for a supplier like Baxter. When your customers organize into a cartel to hammer down your prices, the textbook outcome is margin destruction. And for a commodity like saline, where one bag of salt water is chemically identical to the next, the pressure should have been merciless. Yet something counterintuitive happened. The GPO system, which looked like Baxter's greatest threat, became the architecture of its deepest competitive advantage. Understanding how is essential to understanding the entire modern history of the company.

The mechanism was the sole-source contract. Rather than fight the GPOs, Baxter learned to use their structure. It would negotiate multi-year exclusive agreements in which a hospital network, in exchange for favorable pricing on the full portfolio, committed to buy its high-volume products — above all, its saline and dextrose bags — exclusively from Baxter. The volume commitment was the price of the discount. This turned the GPO's purchasing muscle from a weapon against Baxter into a fence around Baxter's installed base. A rival who wanted to sell a hospital a better infusion pump now had to dislodge an entire bundled contract, not just win a single product comparison.8

And the bundle was the genius of it. This is a razor-and-blade model, but a closed-loop version far stickier than a printer and its cartridges. You cannot hang a competitor's IV bag on a Baxter infusion set. You cannot run a rival's tubing through a Baxter pump, because the pump is calibrated and often mechanically keyed to Baxter's own consumables. To secure the cheap, heavy saline bags at the negotiated discount, a hospital progressively integrated Baxter's whole ecosystem: the infusion pumps, the administration tubing sets, the parenteral nutrition, the surgical hemostats and sealants. Each product reinforced the others. The saline was the razor that got Baxter in the door at scale; the pumps, sets, and specialty fluids were the high-margin blades that followed.

The lock-in was never flawless, and one episode is worth pausing on because it exposes the fragility hiding inside the pump franchise. Baxter's Colleague infusion pump — a core "blade" in the razor-and-blade system — was plagued for years by defects: battery failures, unexpected power shutdowns, and software errors. The problems festered through a 2005 product seizure and a 2006 consent decree until, on May 3, 2010, the FDA took the extraordinary step of ordering Baxter to recall and remove from service essentially every Colleague pump in the United States — roughly 200,000 devices — and to refund or replace them.[^12] It was one of the largest infusion-pump recalls in FDA history. The lesson embedded in that episode would echo for the rest of Baxter's story: when a company's competitive advantage rests on being embedded in life-critical workflows, the quality of the embedded product is not a detail — it is the whole franchise. A pump that hospitals cannot trust is a pump that invites exactly the kind of switching the lock-in is supposed to prevent. Baxter survived the Colleague debacle because switching pumps is genuinely hard, but it was a warning that entrenchment is not the same as invulnerability.

It is worth naming the competitive powers at work here, because they explain why this position proved so durable. In the language of Hamilton Helmer's 7 Powers, Baxter enjoyed two of the strongest simultaneously. The first was switching costs. Ripping out a hospital's standardized IV sets and retraining hundreds of nurses on a competitor's pump — with different software, different alarms, different failure modes, in an environment where a dosing error can kill someone — is an operational nightmare that hospital administrators are deeply reluctant to undertake. Inertia, in medicine, is a feature, not a bug; consistency reduces error. The second power was scale economies, layered on top of the water-weight physics from the previous era: the capital and regulatory cost of building FDA-compliant sterile injectable plants, combined with the thin margins the GPOs themselves negotiated, made the business almost impossible for a new entrant to crack profitably. The GPOs had, ironically, helped build the very barrier that protected the incumbent they were trying to squeeze.

None of this made Baxter a pricing-power juggernaut, and that caveat matters for everything that follows. The lock-in protected market share and volume; it did not confer the ability to raise prices at will. The GPO contracts that fenced out competitors also capped Baxter's own pricing — that was the whole point of the hospitals organizing. So Baxter emerged from these decades as something specific and double-edged: a utility. Indispensable, deeply entrenched, extraordinarily hard to displace — and structurally low-margin, low-growth, and unable to charge more just because it was essential. It was a toll road where the tolls were set by a committee of the drivers.

The market noticed the difference between "essential" and "lucrative," and this tension set up the most consequential strategic decision of Baxter's modern era. By the 2010s, Baxter contained two very different businesses under one roof: the stable, slow, cash-generative hospital-products utility, and a fast-growing, high-margin biopharmaceutical operation built around hemophilia treatments and plasma-based therapies. The latter was where the growth and the fat margins lived; the former was where the cash and the entrenchment lived. In 2015, under pressure to unlock the value the market was clearly assigning to the growth engine, Baxter spun off the biopharmaceutical business as a separate public company called Baxalta, effective July 1, 2015.9 Baxalta was itself acquired the following year by Shire for roughly $32 billion, and Shire in turn was swallowed by Japan's 武田薬品 Takeda in 2019.9

The spin-off was celebrated at the time as value creation, and for Baxalta shareholders it was. But look at what it did to the company left behind. Baxter had just handed its highest-growth, highest-margin engine to its own shareholders as a separate stock, keeping for itself the stable-but-slow utility. What remained was a cash cow with a structural problem: nowhere obvious to grow. That problem would define the next chapter, and it would eventually drive a desperate reach for growth that nearly destroyed the company.

IV. Joe Almeida & The Organic Growth Trap

By late 2015, Baxter had a target on its back. The stripped-down, post-Baxalta company was exactly the kind of underperforming, operationally flabby enterprise that activist investors love: a business with real assets, real market position, and mediocre margins that a disciplined operator could obviously improve. Right on cue, Daniel Loeb's Third Point built a stake of roughly 10% and started pushing for change.10 The message from activists in these situations is always some version of the same thing: this company is worth more than the market says, and the people running it are leaving money on the table. The board listened.

The man they brought in to find that money was José "Joe" Almeida, and he was, by reputation, exactly the right operator for the job. On October 28, 2015, Baxter named Almeida chairman and CEO, effective January 1, 2016, succeeding Robert Parkinson, who had led the company since 2004.11 Almeida arrived with a formidable pedigree. He had been chairman, president, and CEO of Covidien, the medical-device giant, which he had steered to a landmark sale to Medtronic — a deal announced in 2014 at roughly $43 billion and completed in early 2015 at a value that had swelled to nearly $50 billion as Medtronic's own shares appreciated.11 Almeida was, in the industry's shorthand, a proven value-creator: a Brazilian-born engineer by training with a reputation for operational rigor and an unsentimental eye for cost.

The Almeida playbook was textbook operational turnaround, and for a while it worked beautifully. He attacked the company's bloated cost structure with discipline: consolidating manufacturing, streamlining procurement, and squeezing selling, general, and administrative expenses that had grown lazy inside a sheltered utility. He redirected the resulting cash flow toward aggressive share buybacks, shrinking the share count and mechanically boosting earnings per share. The financial results were striking. Operating margins, which had languished in the single digits, climbed into the high teens over the second half of the 2010s. Wall Street, which loves nothing more than a self-help margin story that requires no bet on end-market growth, fell in love. Baxter's stock, which had traded in the low $40s when Almeida arrived, roughly doubled, reaching nearly $90 in the fall of 2019.30

Here it is worth pausing to state the analytical conclusion plainly, because it is the hinge of the entire story. Cost-cutting is a real and legitimate source of value, but it has a mathematical ceiling. You can only take out so much cost before you are cutting into the muscle of the business. Once the low-hanging fruit is gone, the margin expansion stops, and the market's attention swings back to the question a cost story can never answer: where does the growth come from? For Baxter, the honest answer was uncomfortable. Its core business was a commodity utility whose organic revenue crept along at 2% to 3% a year. The GPO contracts that protected its share also capped its pricing, so it could not simply raise prices to manufacture growth. And the one genuinely high-growth engine it had once owned — the biopharma business — had been spun off as Baxalta before Almeida even arrived.

There is a deeper pattern worth drawing out here, because it recurs across the medical-device industry and it shaped how Almeida approached his mandate. Almeida had made his name at Covidien by treating a portfolio of businesses as a set of assets to be optimized, pruned, and ultimately sold — the classic playbook of the modern industrial operator, in which value is created less by inventing new products than by relentlessly improving the economics of existing ones and then finding the right buyer at the right multiple. That playbook rewards discipline and punishes sentimentality, and it had made him wealthy and admired. But it is a playbook built for businesses where operational slack genuinely exists. Applied to a franchise like Baxter's core fluids business — already thin-margined by design, already disciplined by GPO negotiation, already lacking a growth engine after the Baxalta separation — the playbook delivers a fast early win and then hits a wall. The very efficiency that made Almeida's early tenure look brilliant meant there was less and less left to cut, and nothing in the operator's toolkit generates organic demand where the market itself is flat.

So Almeida found himself in a classic trap, one that has ensnared many a talented operator brought in to fix a mature business. He had done the thing he was hired to do — extract efficiency — and he had done it well. But efficiency alone does not create a growth narrative, and by the end of the 2010s the efficiency story was running out of road. The stock's ascent stalled. The market began to price Baxter for what it structurally was: a low-growth utility with limited pricing power and no obvious next act. An operator of Almeida's ambition and reputation was not going to accept being remembered as the man who managed a slow decline in earnings-per-share terms. He needed a move — something large enough to change the story from "cost-cutting utility" to "growth platform."

That impulse — the need to buy growth when you cannot generate it organically — is one of the most dangerous in all of corporate finance. It has destroyed more shareholder value than any recession. Because a management team that feels it must do a deal is a management team that will rationalize paying too much, at the wrong time, for the wrong asset. And in September 2021, with credit cheap and hospital-technology valuations at a cyclical peak, Baxter did exactly that.

V. The $10.5 Billion Hillrom Disaster: Overpaying at the Top

On September 2, 2021, Baxter announced that it would acquire Hillrom, the maker of hospital beds and patient-monitoring equipment, for $156.00 per share in cash — a total equity value of approximately $10.5 billion and an enterprise value of roughly $12.4 billion including assumed debt.12 It was the largest acquisition in Baxter's history, and management sold it with a vision that, on the surface, was genuinely compelling.

The pitch was "connected care." Think about the physical geography of a hospital room, the argument went. The bed is the hub — the one piece of furniture the patient never leaves. Hillrom made not just beds but smart beds, wired with sensors, along with patient monitors and clinical communication systems. Baxter made the smart infusion pumps that hang beside those beds. Marry the two, and you could build an integrated digital nervous system for the hospital room: a bed that knows when a patient tries to get up and is a fall risk, a pump that talks to the monitor, an ecosystem that reduces medical errors and eases the crushing workload on nurses. Baxter framed the deal as creating a roughly $15 billion global medtech leader, promising about $250 million in annual pre-tax cost synergies by the end of the third year.13 On a slide, it was the perfect answer to the growth trap: a way to bolt a higher-growth, more differentiated "digital health" story onto the stable IV utility.

The problem was never the vision. The problem was the price, the financing, and above all the timing — and on all three, this deal is close to a case study in how to do it wrong.

Start with the financing, because it is where the real damage was engineered. To fund the acquisition, Baxter raised approximately $11.8 billion in acquisition-related debt.14 Critically, a large slug of that was floating-rate: a $4.0 billion senior unsecured term-loan facility, split into a $2.0 billion three-year tranche and a $2.0 billion five-year tranche, both of which carried interest rates that would reset with prevailing market rates.14 Baxter itself acknowledged at closing that the deal would leave it with net leverage of approximately 4.2x net debt to combined adjusted EBITDA — a heavy load — while promising to deleverage to 2.75x within two years.12 The deal closed on December 13, 2021.13

Now consider what happened in the world during the exact months Baxter was signing those floating-rate loans. Inflation, which had been dismissed as "transitory" through much of 2021, was in fact accelerating toward a four-decade high. Within roughly three months of the Hillrom deal closing, the Federal Reserve embarked on the most aggressive interest-rate-hiking campaign in forty years, lifting its benchmark rate from near zero toward the mid-single digits over the following eighteen months. For a company holding $4.0 billion in floating-rate debt, this was a slow-motion catastrophe. The interest expense on those loans climbed with every Fed meeting. Baxter had, in effect, made a massive leveraged bet at the precise top of the cheap-money era and then watched the cost of that leverage spike almost immediately.14

It is worth being precise about why floating-rate debt was such a dangerous choice, because the mechanism is not intuitive to everyone. When a company borrows at a fixed rate, it knows its interest bill for the life of the loan; a rate spike hurts the lenders, not the borrower. Floating-rate debt inverts that: the interest resets periodically to track a market benchmark, so the borrower — not the lender — carries the risk that rates rise. In a low-rate world, floating debt is cheaper, which is exactly why it is tempting. But it is cheaper because the borrower is being paid a small discount to accept a large risk. Baxter accepted that risk on $4.0 billion at the worst possible moment in the cycle. As the Fed's benchmark climbed, the cost of servicing those loans rose in lockstep, converting a manageable financing plan into a widening drain on cash flow — cash flow the company needed to invest in the very connected-care integration the deal was supposed to deliver.

The macro timing would have been painful on its own. What made it a genuine crisis was that Hillrom's underlying business broke down at the same moment. The connected-care vision depended on selling expensive, semiconductor-laden smart beds — and 2022 was the year of the global chip shortage. Components that went into Hillrom's beds and monitors became scarce and expensive, disrupting production. Simultaneously, hospitals, hammered by their own labor shortages and cost inflation, did precisely what customers do when their budgets are squeezed: they froze capital expenditure. A $15,000 smart bed is a discretionary capital purchase, and discretionary capital purchases are the first thing a cash-strapped hospital defers. The revenue synergies underpinning the deal's valuation simply did not materialize on schedule.

The reckoning came quickly and it was brutal. In the third quarter of 2022 — less than a year after closing — Baxter took $3.1 billion in pre-tax charges for goodwill and indefinite-lived intangible-asset impairments, most of it tied directly to the Hillrom acquisition.15 The breakdown told the story of exactly what had been overpaid for: roughly $2.8 billion in goodwill impairments, including $1.4 billion written off the Patient Support Systems unit and $1.0 billion off the Front Line Care unit — the very hospital-bed and monitoring businesses that had been the strategic heart of the deal — plus a further $332 million in intangible-asset impairments.15 In accounting terms, a goodwill write-down of this kind is management's formal admission that it paid billions more than the acquired business was worth. Less than twelve months after buying Hillrom, Baxter was conceding it had overpaid by a sum approaching a third of the equity value.

The analytical lesson here is not that Baxter bought a bad company; Hillrom was a real business with real products. The lesson is about the fatal interaction of three decisions made together: paying a peak multiple for a cyclical, capital-intensive asset, funding it with floating-rate debt, and doing so at the very moment the monetary cycle turned. Any one of these might have been survivable. Together, they created a debt load that now threatened Baxter's investment-grade credit rating and left management with no good options — only painful ones. To save the balance sheet, Baxter would have to do something almost unthinkable for a company that had spent a decade acquiring and integrating: it would have to start selling off its best parts.

VI. The Great Dissection: Activism & The Fire-Sale of Crown Jewels

By the start of 2023, Baxter was cornered. The debt from Hillrom sat on the balance sheet like a stone, the interest cost on the floating portion kept climbing, and the credit-rating agencies were watching. Something had to give, and what gave was the company's own structure. On January 6, 2023, Baxter announced a sweeping set of strategic actions: a plan to spin off its Renal Care and Acute Therapies businesses into a new, independent public company within 12 to 18 months; a new, simplified operating model; and a formal review of strategic alternatives for its BioPharma Solutions contract-manufacturing arm.16 The verticalized four-segment reporting structure that Baxter would eventually adopt — Medical Products & Therapies, Healthcare Systems & Technologies, Pharmaceuticals, and Kidney Care — was finalized later that year, taking effect with third-quarter 2023 reporting.17 The corporate architecture that Almeida had spent years building was, in effect, being taken apart to pay for a single acquisition.

But a spin-off, however clean, does not raise cash to pay down debt — it merely hands shareholders a new stock. And cash was what Baxter urgently needed. So the plan tilted, under the unrelenting pressure of the balance sheet, from tax-efficient separation toward outright sale. The most valuable, most cash-generative assets went first, and they went at prices that reflected a seller under duress rather than one negotiating from strength.

The first crown jewel to go was BioPharma Solutions, Baxter's sterile contract-manufacturing business — a genuinely attractive, high-margin operation that made injectable drugs on behalf of pharmaceutical companies. This was exactly the kind of asset a healthy company keeps and nurtures; it rode the booming outsourced-manufacturing wave and threw off cash. On May 8, 2023, Baxter agreed to sell it to the private-equity firms Advent International and Warburg Pincus for $4.25 billion in cash, with net after-tax proceeds estimated at approximately $3.4 billion — proceeds explicitly earmarked for debt repayment.18 The sale closed on October 2, 2023, and the business was rechristened Simtra BioPharma Solutions.19 Read the logic carefully: Baxter sold a fast-growing, high-margin business — the sort of asset that generates the growth a mature utility desperately lacks — not because it wanted to, but because it needed the cash to undo the Hillrom mistake. Private equity, as it so often does, was on the other side of a motivated seller's trade.

The second sale cut even deeper into the company's identity. Kidney Care — the dialysis and renal-therapy business — was not just another segment; it was, in a real sense, the lineal descendant of Baxter's founding purpose, tracing back to the sterile-solutions and peritoneal-dialysis heritage that had defined the company for generations. The original January 2023 plan had been to spin it off as an independent public company in a tax-free transaction, preserving value for shareholders. But by 2024, the calculus had changed. Immediate, certain cash was worth more to a deleveraging company than the deferred and uncertain value of a spin-off. In March 2024, Baxter disclosed it was exploring a sale instead, and on August 13, 2024, it announced a definitive agreement to sell the Kidney Care business — branded Vantive — to the Carlyle Group for $3.8 billion.20 The deal closed on January 31, 2025, delivering approximately $3.71 billion in pre-tax cash proceeds at closing.21

Step back and look at what the great dissection actually accomplished, because the picture is genuinely double-edged. On the one hand, it worked as intended: the combined divestiture proceeds materially reduced Baxter's leverage and pulled the company back from the edge of a credit downgrade. On the other hand, look at the price. To repair the damage from one overpriced acquisition, Baxter sold its best growth engine (the BioPharma contract-manufacturing business) and its historic foundation (renal care) — both to private-equity buyers who recognized undervalued, motivated-seller assets when they saw them. The company emerged smaller, more focused, and less levered, but also stripped of the very businesses that might have provided future growth and diversification. This is the true cost of a bad large acquisition: not merely the write-down, which is a one-time accounting event, but the forced dismemberment that follows, which permanently alters what the company can become.

The architect of both the acquisition and the dissection did not stay to see the ending. In February 2025, José Almeida stepped down, and Brent Shafer — a seasoned healthcare executive best known as the former chairman and CEO of the health-records company Cerner — stepped in as chairman and interim CEO to stabilize the company while the board searched for a permanent leader.22 Almeida's tenure had traced a complete arc: the disciplined operator who doubled the stock with cost cuts, then reached for a transformational deal that forced the company to sell the very assets that made it whole. Whether that legacy reads as bad luck with the macro cycle or a failure of capital-allocation judgment is a question we will return to. But before the new era could begin, the physical fragility that Baxter had spent ninety years building would announce itself in the most dramatic way possible.

VII. The Fragility Crisis: Hurricane Helene as a Systemic Warning

We began this story in the Marion floodwaters, and now we can see how the company arrived there — how decades of rational, spreadsheet-driven optimization delivered a single point of catastrophic failure. The North Cove plant was not an accident of concentration; it was the endpoint of the water-weight logic taken to its extreme. Build big, build central, minimize cost per bag. By 2024, that logic had made one facility in one Appalachian valley responsible for roughly 60% of the intravenous solutions used in American hospitals.1

When Helene's rains came in late September 2024, the vulnerability that had lived quietly on the balance sheet as "efficiency" revealed itself as national-security risk. A levee breach sent floodwater through the plant; the bridges that carried raw materials in and finished product out were damaged or destroyed; production stopped.1 And because there was no meaningful domestic redundancy — no second plant of comparable scale sitting idle as insurance — the stoppage did not degrade supply gradually. It cut it off. Hospitals across the country, thousands of miles from any hurricane, suddenly could not get saline.

The scramble that followed exposed just how brittle the system was. There was no domestic switch to flip, so the response had to be improvised across borders and oceans. Baxter activated a global network of facilities to backfill the lost North Cove volume, drawing on plants in Canada, Mexico, Spain, Ireland, the United Kingdom, and China.1 The FDA, treating the shortage as the public-health emergency it was, coordinated temporary importation of IV fluids from Baxter's overseas facilities to bridge the gap. This is the part worth dwelling on: the safety net for 60% of America's IV supply turned out to be foreign factories and emergency regulatory waivers. The redundancy that a resilient supply chain would have built in advance had been optimized away, and it had to be reconstructed, frantically, in the middle of the crisis. The shortage was severe enough and prolonged enough that the FDA did not formally declare the sodium chloride shortage resolved until August 8, 2025 — roughly ten and a half months after the storm.2

The financial hit, while real, actually understates the true cost — and the distinction is worth drawing precisely, because Baxter reported it in two different ways. On the Q4 2024 earnings call in February 2025, management said Hurricane Helene had reduced sales by approximately $110 million in the quarter, about 400 basis points of growth, and cut earnings by roughly $0.10 per share.23 Separately, the company recorded pre-tax charges of about $85 million in continuing operations — $64 million after tax, or $0.13 per diluted share — for the physical damage and remediation.24 These are not enormous numbers against a company with roughly $10.6 billion in annual revenue.25 But the reported dollars capture only the visible, near-term damage. They do not capture the reconstruction capital, the premium air-freight costs of flying saline across the Atlantic, or — most importantly — the strategic damage: the loud, public demonstration to every hospital, every GPO, and every regulator in America that depending on Baxter meant depending on a single point of failure.

That last cost is the one that should concern a long-term investor most, because it strikes directly at the moat. For decades, Baxter's dominance in IV fluids rested partly on the near-impossibility of new entry and partly on the reliability of its scale. Helene converted "reliable scale" into "dangerous concentration" in the minds of the exact decision-makers who write the sole-source contracts. In the aftermath, GPOs and health systems began actively talking about diversifying their supply — dual-sourcing critical fluids specifically so that no single flood could ever again halt elective surgery nationwide. The very efficiency that built the moat had created a strategic opening for competitors like B. Braun and ICU Medical to argue that redundancy is worth paying for. We will weigh how serious that threat is later. For now, the lesson stands as one of the cleanest illustrations in modern business of a hard truth: a system optimized purely for cost eliminates the slack that resilience requires, and in a business supplying something a nation cannot live without, that slack is not waste — it is insurance. Baxter had cancelled the policy years before the storm.

It fell to a new chief executive, arriving in the wake of both the debt crisis and the flood, to decide what kind of company Baxter should become on the other side.

VIII. The New Baxter: Segment Economics & The Andrew Hider Era

On July 7, 2025, Baxter named its new leader. Andrew Hider would become president and CEO, joining the board and taking the helm no later than September 3, 2025, with interim chief Brent Shafer moving to the role of independent chairman.26 The choice was a statement about what the board thought Baxter now needed. Hider was not a healthcare lifer or a dealmaker in the Almeida mold. He was, above all, an operator steeped in the gospel of continuous improvement.

His résumé read like a curriculum in industrial excellence. Since 2017, Hider had been CEO of ATS Corporation, a factory-automation company, where he built a track record of disciplined operational improvement and portfolio management. Before that, he had spent roughly a decade at Danaher — the conglomerate widely regarded as the platonic ideal of the continuous-improvement operating model, whose "Danaher Business System" has been studied and imitated across industry — including a stint running its Veeder-Root unit, after six earlier years at General Electric.26 The signal in this hire was unmistakable. After a decade defined by financial engineering — the buybacks, the transformational acquisition, the leverage, the fire-sale — Baxter's board was reaching for someone whose entire professional identity was about grinding out efficiency and quality on the factory floor, not doing deals. The company that had nearly broken itself on the balance sheet wanted an operator, not a financier.

Hider's early messaging, delivered on his first earnings call in October 2025, was notably disciplined and, refreshingly, short on grand visions. Rather than promise a bold new strategy, he laid out three priorities. First, stabilize the parts of the business that were underperforming — most visibly a shipping-and-installation hold on the Novum IQ large-volume infusion pump, and the ongoing recovery of IV-fluid supply after Helene. Second, strengthen the balance sheet and finish the deleveraging job. Third, build a durable continuous-improvement culture, which he branded the "Baxter GPS" — for Growth and Performance System — explicitly modeled on the kind of operating system he had run at his prior companies.27 He talked about a "say-do ratio," promised a 2026 investor day, and framed any future M&A as a distant, post-deleveraging consideration.27 It is worth flagging one thing for investors watching the narrative: the framing here is deliberately modest, operational, and incremental — the language of a manager who wants to be judged on execution rather than promises. Whether that discipline holds when the pressure to show growth returns is the open question.

To judge that execution, an investor needs to understand what the new, slimmed-down Baxter actually is. After the Kidney Care sale closed, the company reports three continuing segments, and the FY2025 figures tell a clear story about where the profit and the pressure sit.28 The largest and most profitable is Medical Products & Therapies — the historic core of sterile IV fluids, infusion systems, and advanced surgery products. It generated roughly $5.3 billion in FY2025 sales and, on Baxter's adjusted basis in the third quarter, ran at a segment operating margin of about 20.5% — the highest of the three and, tellingly, expanding even amid the post-Helene disruption.2829 This is the cash engine, and its resilience is the single most important thing keeping the recovery on track. But it is also the segment that must now be redesigned for redundancy, which means capital spending on new capacity precisely when the company is trying to conserve cash.

The second segment, Healthcare Systems & Technologies, is what remains of the Hillrom dream — the smart beds, patient monitors, and clinical-communication systems. It generated roughly $3.1 billion in FY2025 sales, but at a markedly lower adjusted margin of about 13.5% in the third quarter, and that margin was down meaningfully year over year, pressured by tariffs, higher research spending, and corporate costs reallocated onto it after the Kidney Care exit.2829 Here is where the analytical skepticism should concentrate. The entire strategic rationale for the $10.5 billion Hillrom acquisition was that "connected care" would be a genuine, high-margin growth driver — software and services layered onto hardware. Several years on, the evidence remains thin. A 13.5% and declining segment margin looks less like a differentiated digital-health platform and more like a capital-intensive hospital-equipment business competing against entrenched players. Proving that this segment is more than an expensive bed company is arguably Hider's single hardest task.

The third segment, Pharmaceuticals — generic sterile injectables, inhaled anesthetics, and drug compounding — generated roughly $2.5 billion in FY2025 sales at the thinnest margin of all, about 8.9% on an adjusted basis in the third quarter, and also declining, squeezed by intense generic-pricing competition and the compliance costs of sterile manufacturing.2829 It is a reminder that even in its "pharmaceutical" arm, Baxter is largely a low-margin manufacturer, not a patent-protected innovator.

One quirk of the current financials deserves a note, because it flatters the near-term numbers. Following the Vantive sale, Baxter continues to manufacture products for its former Kidney Care business under a manufacturing supply agreement, recording roughly $320 million of such "other" revenue across FY2025, plus separate transition-services income.29 These are real cash flows, but they are transitional by design — a temporary bridge that will fade as Vantive stands fully on its own, and a reminder of how entangled Baxter remains with the businesses it sold under duress.

The clearest sign of just how serious the balance-sheet repair has become came in the capital-allocation decisions announced with the third-quarter 2025 results. Management conceded that the 3.0x net-leverage target, once expected sooner, would now not be reached until the end of 2026, and — most strikingly for a company that had paid a dividend for decades — the board slashed the quarterly dividend to a token $0.01 per share beginning in January 2026, freeing more than $300 million of annual cash flow to accelerate debt repayment.27 For income-oriented shareholders who had held Baxter as a stable dividend payer, this was a jarring signal. For a clear-eyed analyst, it was the most honest thing management had done in years: an admission that the balance sheet still comes first, and that the Hillrom hangover is not yet cured. By mid-2026, the market's verdict on the whole saga was visible in the stock, which traded near $22 a share for a market capitalization of roughly $11 billion — a fraction of the near-$90 peak of 2019, and a standing reminder of how much value the past decade destroyed.30

IX. Playbook: Business & Investing Lessons

Every company's history is also a set of transferable lessons, and Baxter's recent decade offers three that are unusually clean — each expensive enough to be worth internalizing.

The first is the floating-rate trap. The Hillrom deal is destined to become a business-school case study not because acquisitions are inherently unwise, but because of the specific, compounding recklessness of how it was financed. Funding a large, cyclical, peak-multiple acquisition with billions in floating-rate, short-tenor debt is a bet that interest rates will stay low — a bet made, in this case, with inflation already stirring and a rate-hiking cycle visibly on the horizon. The lesson is not "avoid debt." It is that the structure of financing embeds a macro view whether management intends it or not, and matching floating-rate liabilities against a long-lived, cyclical asset is a mismatch that turns a manageable deal into a crisis the moment the cycle turns. Baxter locked in the downside precisely when the downside was most likely to arrive.

The second is the redundancy paradox, and it generalizes far beyond healthcare. Scale economies are a legitimate and powerful moat; concentrating production to drive down unit cost is often exactly the right call. But there is a point past which optimization stops buying efficiency and starts buying fragility, and that point is invisible on any spreadsheet because the cost of a low-probability catastrophe does not appear in a normal-year P&L. A business that supplies 60% of a critical national resource from a single facility looks like a triumph of operational discipline right up until the flood, at which point the missing redundancy reveals itself as the most expensive line item that was never budgeted. For investors, the takeaway is a diligence question worth asking of any efficient-looking industrial: where is the single point of failure, and what would it cost if it failed?

The third is the cost of M&A remediation, which is the subtlest and perhaps the most important. The naive view of a bad acquisition is that its cost equals the write-down — the goodwill impairment, booked once, and then the company moves on. Baxter shows why that view is dangerously incomplete. A large, debt-funded mistake does not merely dent the income statement; it can force the company to dismember itself to survive. Baxter had to sell its best growth business and its historic foundation — not at prices it chose, but at prices a motivated seller accepts — to repair damage from a single deal. The true cost of the Hillrom acquisition was never the $3.1 billion write-down. It was the permanent loss of BioPharma Solutions and Vantive, and with them, a meaningful share of whatever Baxter's future growth might have been. Bad acquisitions do not just cost money. They cost optionality, and optionality, once sold to private equity under duress, does not come back. The buyers of Simtra and Vantive did not overpay; they bought good businesses from a seller who had no choice but to sell, which is the single most favorable position a private-equity acquirer can occupy. Baxter's misfortune was their opportunity, and the value transfer ran in one direction only.

These lessons frame the central question for anyone weighing Baxter today: is this a broken company still paying for its sins, or a chastened, refocused one whose worst chapter is finally closing?

X. Analysis & Bear vs. Bull Case

Start with the moat, because everything depends on whether it still holds. Run Baxter through Hamilton Helmer's 7 Powers and the picture is one of a franchise that is durable but visibly under strain. The switching costs remain genuinely intact: hospitals are still deeply integrated with Baxter's infusion hardware, consumables, and software, and the operational pain of ripping that out and retraining clinical staff has not diminished. This is the strongest remaining pillar of the franchise, and it is why even a decade of self-inflicted wounds has not cost Baxter its entrenched position in the pump-and-set ecosystem. Through a Porter's Five Forces lens, the threat of new entrants in high-volume sterile fluids stays low — the capital and regulatory barriers that the water-weight economics and FDA plant requirements erect are as real as ever.

But the scale-economies power, once impregnable, has been partially compromised — not by a competitor out-scaling Baxter, but by Baxter itself demonstrating the downside of its own concentration. Helene handed Baxter's rivals, principally B. Braun and ICU Medical, an argument they could never have manufactured on their own: that Baxter's efficiency is a liability, and that resilience is worth paying a premium for. The buyer power in Porter's framework — always high in this industry because of the GPOs — now points in a new and dangerous direction. Where GPOs once used their leverage purely to extract lower prices, they may now use it to demand dual-sourcing, deliberately seeding a second supplier to protect against another single-point failure. That would erode both Baxter's volume share and the sole-source contract architecture that has anchored its lock-in for forty years. The rivalry, in other words, is intensifying precisely at the moment Baxter is least able to invest aggressively in response.

That tension defines the bear and bull cases, and both are coherent.

The bear case is structural and unforgiving. It holds that Baxter is a low-growth utility whose modest pricing power is now actively eroding as GPOs push dual-sourcing, that the Hillrom-derived Healthcare Systems & Technologies segment is a permanent capital drag that will never deliver the connected-care growth it promised — competing, as it does, against far stronger players in hospital equipment and monitoring — and that the company faces years of low-single-digit organic growth and compressed margins while it grinds down a debt load that forced it to cut its dividend to a penny. In this view, the divestitures fixed the immediate solvency problem but left behind a smaller, lower-quality collection of businesses with no obvious engine of value creation, and the stock's collapse from near $90 to the low $20s is not an overreaction but a repricing to reality.30 The activist-style critique writes itself: a management team that promised deleveraging discipline, then made an aggressively leveraged acquisition, then had to dismantle the company to clean it up, has not earned the benefit of the doubt on capital allocation.

The bull case rests almost entirely on execution and on the man now running the company. It holds that Baxter is a genuinely essential, deeply entrenched business that got its balance sheet — not its franchise — badly wrong, and that the franchise is fixable. In this view, Andrew Hider's Danaher-honed continuous-improvement discipline is exactly what a sprawling, under-managed manufacturing base needs; that there are years of margin gains to be harvested by simply running the factories better; that deleveraging, however painful, is nearly done and will restore capital flexibility; and that the post-Helene push for supply resilience could, counterintuitively, let Baxter charge for reliability — negotiating the redundancy premium into its GPO contracts rather than eating the cost. The dividend cut, on this reading, is not a distress signal but a rational, unsentimental prioritization of the balance sheet by a management team finally telling the truth. The Medical Products & Therapies segment's expanding 20.5% margin, achieved during the Helene disruption, is the single best piece of evidence that the core engine is healthier than the share price implies.29

It is worth war-gaming the competitive threat concretely, because the bear and bull cases hinge on how much share Baxter actually loses. The two most credible challengers in U.S. sterile fluids are B. Braun, the family-owned German medical giant with its own substantial IV-solutions manufacturing, and ICU Medical, which had already built scale in infusion systems partly by absorbing Pfizer's Hospira infusion business years earlier. Neither can replicate Baxter's footprint overnight — the water-weight economics and multi-year FDA plant qualification that protect Baxter also protect the incumbency from a fast assault. Building a new sterile-fluids plant is a multi-year, multi-hundred-million-dollar undertaking, and hospitals cannot switch their standardized fluids and sets casually. That is Baxter's breathing room. But the threat is not a sudden displacement; it is a slow reallocation. Every new GPO contract that specifies a second qualified source, every health system that decides it wants 20% of its saline coming from a non-Baxter plant as insurance, chips a little off the volume base and a little off the pricing architecture. Over five to ten years, a determined dual-sourcing push by buyers who now have a vivid memory of empty supply portals could meaningfully erode the franchise even if no competitor ever "wins." Death by a thousand qualified second sources is a real, if slow, risk — and it is the specific mechanism through which Helene could prove more costly than its $110 million headline.

Weighing these honestly, the case is genuinely unresolved, and that is the intellectually honest conclusion. Baxter is neither obviously a value trap nor obviously a turnaround. It is a real, essential business with a durable core moat, saddled with a self-inflicted balance-sheet problem it is methodically working off, run by a new CEO whose operating philosophy is well suited to the task but who has not yet proven it in this context. The switching-cost moat gives it time; the eroding pricing power and the unproven connected-care segment limit the upside; the execution is unproven but the leadership fit is plausible.

For investors who want to cut through the noise, three key performance indicators will reveal which case is winning, and they are worth tracking above all others. The first is net debt-to-adjusted-EBITDA leverage: the whole recovery hinges on reaching and holding the roughly 3.0x target, now slated for the end of 2026, because only a repaired balance sheet restores the capital flexibility Baxter needs.27 The second is Healthcare Systems & Technologies organic growth and margin: this is the direct, unforgiving scoreboard on whether the Hillrom thesis was ever real, or whether $10.5 billion bought a permanent drag. The third is the trajectory of operating margin and free cash flow as the post-Helene reconstruction costs roll off and Hider's efficiency program — if it works — begins to show up in the numbers. Watch those three, and the abstract debate between bull and bear resolves itself into something concrete and measurable.

Ninety years after two Iowa doctors decided hospitals should not brew their own saline, Baxter remains what it has always been at its core: an indispensable maker of the most basic and essential products in medicine. The tragedy of the past decade is that being indispensable was never enough to protect shareholders — not from a cost ceiling, not from a leveraged deal at the top of the cycle, and not from a flood in a mountain town. Whether being indispensable is finally enough, from here, is the question the next few years will answer.

References

-

Hurricane Helene triggers dialysis and IV fluid shortage — TechTarget, 2024-10-18 ↩↩↩↩↩↩

-

FDA declares IV saline shortage over — Medical Device Network, 2025-08-11 ↩↩

-

Baxter to Acquire Hillrom, Expanding Connected Care and Medical Innovation Globally — Baxter International (SEC 8-K Exhibit 99.1), 2021-09-02 ↩

-

Baxter International — Encyclopedia.com company history ↩↩↩↩

-

Baxter restarts second IV manufacturing line at North Cove — Healthcare Dive, 2024 ↩

-

GPO Evolution and Progress 1977–1987 — Healthcare Purchasing News ↩↩

-

Shire buys Baxalta for $32 billion, ending months-long pursuit — BioPharma Dive, 2016-01-11 ↩↩

-

Meet Baxter's new CEO: Covidien vet Jose Almeida — BioPharma Dive, 2015 ↩

-

Baxter Names José Almeida Chairman and CEO — Baxter International, 2015-10-28 ↩↩

-

Baxter to Acquire Hillrom (net leverage ~4.2x at closing) — Baxter International (SEC 8-K Exhibit 99.1), 2021-09-02 ↩↩

-

Baxter Completes Acquisition of Hillrom, Creating ~$15 Billion Global Medtech Leader — Baxter International (SEC 8-K Exhibit 99.1), 2021-12-13 ↩↩

-

Baxter International FY2021 Form 10-K (acquisition-related debt financing; $4.0 billion term-loan facility) — SEC, 2022-02 ↩↩↩

-

Baxter International Q3 2022 Form 10-Q (goodwill and intangible impairments of $3.1 billion) — SEC, 2022-11 ↩↩

-

Baxter Announces Strategic Actions to Enhance Operational Effectiveness — Baxter International (SEC 8-K Exhibit 99.1), 2023-01-06 ↩

-

Baxter International Q3 2025 Form 10-Q (segment reporting structure) — SEC, 2025-11-04 ↩

-

Baxter Announces Agreement to Divest Its BioPharma Solutions Business to Advent and Warburg Pincus for $4.25 Billion — Baxter International (SEC 8-K Exhibit 99.1), 2023-05-08 ↩

-

Advent International and Warburg Pincus Complete Acquisition of Baxter's BioPharma Solutions Business — Advent International, 2023-10-02 ↩

-

Baxter Announces Definitive Agreement to Divest Its Vantive Kidney Care Segment to Carlyle for $3.8 Billion — Baxter International (SEC 8-K Exhibit 99.1), 2024-08-13 ↩

-

Baxter International FY2024 Form 10-K (completion of Kidney Care sale, January 31, 2025) — SEC, 2025-02 ↩

-

Baxter Appoints Andrew Hider Chief Executive Officer (Brent Shafer interim CEO since February 2025) — Baxter International, 2025-07-07 ↩

-

Baxter Q4 2024 Earnings Call Transcript (Hurricane Helene ~$110M sales / ~$0.10 EPS impact) — Investing.com, 2025-02-20 ↩

-

Baxter Reports Fourth Quarter and Full Year 2024 Results — Baxter International, 2025-02-20 ↩

-

Baxter International FY2024 Form 10-K (continuing-operations revenue) — SEC, 2025-02 ↩

-

Baxter Appoints Andrew Hider Chief Executive Officer (ATS Corporation and Danaher background) — Baxter International, 2025-07-07 ↩↩

-

Baxter International Q3 2025 Earnings Release (guidance, leverage target, dividend action) — SEC 8-K Exhibit 99.1, 2025-10-30 ↩↩↩↩

-

Baxter International Q3 2025 Form 10-Q (segment net sales) — SEC, 2025-11-04 ↩↩↩↩

-

Baxter International Q3 2025 Earnings Release (segment adjusted operating margins; Vantive MSA revenue) — SEC 8-K Exhibit 99.1, 2025-10-30 ↩↩↩↩↩

-

Baxter International Inc. (BAX) stock quote and market data — Reuters ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube