Ball Corporation: The Pure-Play Monarch of the Global Beverage Can Oligopoly

I. Introduction & Episode Roadmap

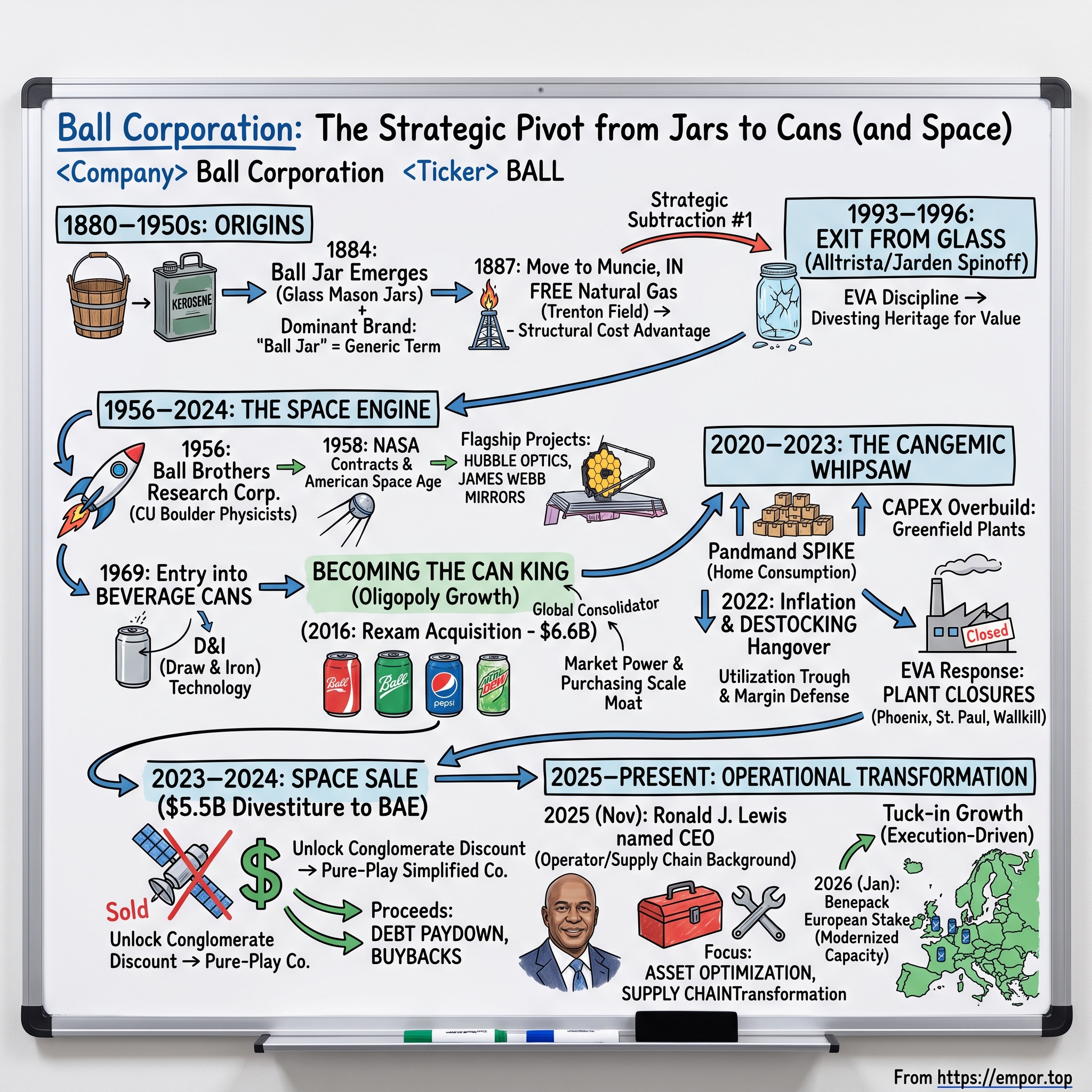

Pick up an aluminum beverage can. Feel how little metal is actually there — a wall thinner than a strand of human hair, drawn and stretched so aggressively that a thimble of aluminum becomes a vessel holding twelve ounces of liquid under pressure. Now consider that a machine somewhere in North America stamped that can, and roughly a thousand of its identical siblings, in the time it took you to read this sentence. There is a decent chance the company that made it began its life in 1880 selling wood-jacketed tin buckets of kerosene, later became a household name synonymous with glass canning jars in American pantries, and — for good measure — spent seven decades building the optical instruments that let the Hubble and James Webb telescopes see to the edge of the observable universe.

That company is Ball Corporation, and the arc of its story is almost too improbable to be a business case study. In 2024 it generated roughly $11.8 billion in revenue, virtually all of it from making metal cans.1 But the more interesting number is the one that isn't there anymore: the aerospace division, the crown-jewel defense and space business, which Ball sold to Britain's BAE Systems for $5.5 billion in cash in February 2024 to become something the market rarely rewards a 145-year-old industrial for becoming — radically, deliberately simple.34

The secular trend underneath the story. For four decades, the world's beverage packaging has been quietly migrating. Away from glass, which is heavy and breaks. Away from PET plastic, which is cheap but carries a mounting environmental and regulatory liability. Toward aluminum, which is light, stacks efficiently on a pallet and a truck, chills fast, and — the crucial part — can be recycled essentially forever without losing quality. A can becomes a new can in as little as sixty days. That tailwind is the current Ball has learned to sail. Whether it is still blowing as hard as it did a decade ago is one of the central questions we will stress-test by the end.

A word on why this business is interesting at all. Beverage cans look, to the untrained eye, like the definition of a boring commodity — a metal cylinder, undifferentiated, sold by the billion. And in one sense that's right: no consumer chooses a soda because Ball rather than Crown made the can. But boring commodities can be wonderful businesses when three conditions hold, and in beverage cans they do. The industry is a tight oligopoly, so pricing behavior is disciplined rather than suicidal. The product is physically integrated into the customer's factory, so relationships are sticky and long. And the dominant input cost — aluminum — is passed straight through to the customer, so the manufacturer earns a spread on conversion rather than gambling on commodity prices. Put those together and you get something closer to a toll road than a smelter: high volumes, modest but defensible margins, and cash flow you can practically set your watch by. The entire investment debate about Ball is really a debate about how durable those three conditions are.

The roadmap. This is a story told in acts of subtraction as much as addition. We start in the Gilded Age with five brothers, a $200 loan, and a lucky natural-gas field in Indiana. We walk into aerospace almost by accident in 1956. We watch Ball, in the 1990s, do something genuinely rare — divest the very glass business that made its name famous — under the cold discipline of a framework called Economic Value Added. We follow the 2016 acquisition of British rival Rexam that made Ball the largest beverage can maker on earth. We sit through the brutal "cangemic" hangover of 2020–2023, when a pandemic demand spike curdled into overcapacity. We examine the 2024 aerospace sale that redefined the company. We watch management cut loose even its beloved aluminum cup in 2025. And we arrive at the present: a November 2025 leadership handoff to a supply-chain operator named Ronald J. Lewis, and a January 2026 European tuck-in acquisition that signals what the next chapter is meant to be about — execution, not expansion. Throughout, we will keep asking the only question that matters for a long-term owner: from here, why does Ball win, and what could break the case?

II. The Origins: From Wooden Buckets to the Glass Mason Jar (1880–1950s)

Buffalo, New York, 1880. Two brothers, Frank and Edmund Ball, borrow $200 from their uncle George Harvey Ball, a Baptist minister, to buy a small operation making wooden jackets that wrapped around tin cans of paint and kerosene. It is an unglamorous, almost comically modest beginning — the wood kept the metal from denting and the volatile contents from leaking. Three more brothers — Lucius, William, and George — would join, and the five-man partnership that formed is the entity from which everything that follows descends.2

The first pivot came fast and it came from paying attention. The Ball brothers noticed that the real money wasn't in kerosene cans; it was in the explosive, distinctly American demand for home food preservation. Before refrigeration, a family's survival through winter depended on canning the summer harvest, and the glass jar with a reliable seal was the enabling technology of the era. In 1884 the brothers began making glass home-canning jars.2 They were entering a market already defined by John Landis Mason's patented screw-thread design — but crucially, the core Mason patents had expired, opening the category to competitors. The "Ball" name, embossed in that famous looping script on the side of the jar, would eventually become so dominant that "Ball jar" entered the language as a generic term, the way "Kleenex" or "Xerox" later would. That is a brand moat most consumer companies would kill for, and Ball acquired it in glass.

Then came the move that a Hamilton Helmer disciple would recognize instantly as a Cornered Resource play. In 1887 the brothers relocated the whole operation to Muncie, Indiana.2 Why abandon Buffalo? Because Muncie sat atop the Trenton Gas Field, at the time one of the largest natural gas reserves in North America, and the town was offering free natural gas and land to lure manufacturers. For a business whose single largest cost was the energy to melt sand into molten glass around the clock, free fuel was not a perk — it was a structural cost advantage that competitors in the Northeast simply could not match. The Indiana gas boom eventually faded, as resource booms do, but by then Ball had built scale, distribution, and that genericized brand. The moat had migrated from the cheap gas to the name on the jar.

One detail from this era is easy to skip but worth pausing on, because it foreshadows the whole company: even at the outset, Ball won not by inventing the category but by executing a known product more cheaply and at greater scale than rivals. The Mason jar design was not Ball's; the demand was not Ball's creation; the innovation was operational and locational — cheaper fuel, tighter manufacturing, a name customers came to trust. That is precisely the shape of the moat Ball would rely on a century later in cans, where again it makes no proprietary product but wins on cost, scale, and physical proximity to the customer. The DNA was set early: Ball is, and has almost always been, a manufacturing-excellence company wearing whatever product happens to reward manufacturing excellence at the time.

Here is the analytical point worth sitting with, because it recurs for the next century-plus: Ball's founders were never romantics about their products. They made kerosene jackets until glass jars were better business. They chased free energy across state lines. They were, from day one, cold-eyed capital allocators wearing the costume of a folksy heritage brand. The Ball Mason jar would survive two world wars and the Great Depression, cementing a cultural presence that persists on pantry shelves and, ironically, in the hipster cocktail bars of the 2010s. But the family that built it was already, in temperament, the kind of organization that would one day sell the jar business without sentiment — and, decades after that, sell a fleet of spacecraft instruments the same way. To understand how a glass-jar company ended up building satellites, we have to walk into a University of Colorado physics lab in the mid-1950s.

III. The Twin Engines: The Serendipitous Walk into High-Tech Aerospace (1956–1990s)

The origin of Ball's aerospace business is the kind of story that sounds invented. In 1956, the company established the Ball Brothers Research Corporation and hired a small group of physicists and graduate students from the University of Colorado in Boulder who had been building rocket-borne pointing controls — devices that could hold a scientific instrument steady on the sun while a sounding rocket tumbled through the upper atmosphere.2 The nominal justification was almost quaint: Ball had deep expertise in vacuum coating and precision glass and metal work from its jar-making machinery, and management reasoned there might be industrial applications for that know-how. What they had actually done was buy a lottery ticket on the American space age one year before Sputnik.

The ticket paid off spectacularly. When NASA formed in 1958 and the space race ignited, Ball's little Boulder outfit was one of a handful of organizations on earth that could build precision pointing systems and satellite platforms. It won early government contracts, then progressively more ambitious ones. Over the following decades Ball Aerospace became a genuine crown jewel of American space science — building instruments and optical components associated with the Hubble Space Telescope, the Kepler planet-hunting mission, and ultimately mirror and instrument work for the James Webb Space Telescope, alongside a large and lucrative business in defense satellites and tactical antenna systems.2 For a company headquartered in a Colorado city better known for canning jars, this was an extraordinary second identity: quiet, technically elite, and — as we will see — eventually impossible to value correctly inside a packaging company.

It is worth dwelling on how genuinely strange this pairing was, because it explains a valuation problem that would take Ball nearly seventy years to solve. When astronauts installed the corrective optics package that fixed Hubble's famously flawed mirror in 1993, Ball hardware was central to the repair — the company had built the instrument that restored the telescope's vision. When Webb unfolded its gold-coated hexagonal mirror a million miles from Earth and began imaging galaxies from the dawn of the universe, Ball engineering was in the optical chain. This is aerospace at the absolute frontier of human capability. And it lived inside the same corporate parent that stamped out cans for cola. The two businesses shared almost nothing — not customers, not sales cycles, not risk profiles, not the kind of investor who understood them. Aerospace ran on multi-year government programs, security clearances, and cost-plus contracts; packaging ran on high-volume conversion economics and quarterly can shipments. That mismatch was tolerable, even charming, for decades. It became intolerable the moment the market started demanding that Ball be one thing or the other.

While the physicists reached for the stars, the core business was undergoing its own metamorphosis. In 1969 Ball entered the commercial metal beverage can market by acquiring Jeffco Manufacturing Company.2 This was the real hinge of the modern company. The technology that mattered was "draw and iron" — D&I — forming, in which a flat disc of aluminum is punched into a cup and then forced through a series of tungsten-carbide rings that iron the walls thinner and thinner, like a rolling pin stretching dough, until you have a seamless can body of astonishing thinness and uniformity. It is high-speed, high-precision, capital-intensive metalworking, and it rewards exactly the kind of manufacturing discipline Ball had spent ninety years developing. Aluminum was on its way to displacing steel in cans, and the two-piece D&I can was on its way to displacing everything else.

Why did aluminum win so decisively? Because the two-piece D&I can is a marvel of material efficiency. A steel three-piece can needed a body, a top, a bottom, and a welded side seam — more metal, more steps, more failure points. The aluminum can uses one continuous piece for body and base, drawn seamless, with only the lid seamed on after filling. It is lighter, cheaper to ship, cools faster in a cooler, takes vivid high-resolution printing directly on the metal, and — the property that would matter more and more — can be melted and reborn as a new can indefinitely, because aluminum does not degrade in recycling the way plastic does. Every one of those attributes would become a selling point to beverage brands over the following half-century. Ball, by buying into D&I aluminum in 1969, had positioned itself on the right side of a material transition that was still decades from fully playing out.

Which set up the hardest, most instructive decision in the company's history: the exit from glass. By the early 1990s, Ball had become one of the earliest and most committed corporate adopters of Economic Value Added, or EVA — the framework popularized by consultants Stern Stewart & Co. that charged every business unit for the capital it tied up, and asked a brutally simple question: after paying for the capital, is this business actually creating value or destroying it?2 The insight EVA forces on a management team is uncomfortable: accounting profit is a liar, because it never charges you for the shareholders' capital sitting in your factories. A business can report "earnings" every year and still be quietly destroying value if those earnings don't clear the cost of the capital tied up to produce them. Run through that lens, the verdict on the iconic glass home-canning business was damning. It was capital-intensive, low-margin, seasonal, and structurally squeezed by a modern food supply chain in which fewer families canned at home and commercial food packaging had consolidated. The jar was a cultural treasure and an economic laggard.

So Ball did the thing companies almost never do to their own heritage. In 1993 it spun off the consumer glass packaging business — the Mason jars, the very product that made the name a household word — into a separate public company called Alltrista Corporation, and completed its exit from glass by 1996.2 Alltrista would later rename itself Jarden, grow into a sprawling consumer-products roll-up, and eventually be acquired by Newell Brands. The Ball jar lived on; it just lived on under someone else's roof.

The lesson here is the thesis of the entire company, stated once, in full, so we need not restate it later: Ball's durable advantage has never been any single product. It has been a willingness to reallocate capital away from what is beloved and toward what earns its cost of capital, even when the beloved thing is the source of the brand itself. Hold that idea. It will explain the aerospace sale, the aluminum cup divestiture, and very likely whatever Ball does next. First, though, the company had to become not just a can maker but the can maker — and that required the biggest check it had ever written.

IV. Becoming the King of Cans: The Rexam Acquisition & Oligopoly Consolidation (2000s–2016)

To understand why Ball spent the 2000s and 2010s buying scale with almost single-minded focus, you have to understand the customer. Ball does not sell to you. It sells to Coca-Cola, PepsiCo, and Anheuser-Busch InBev — a handful of enormous consumer packaged-goods companies whose own strategies were, over these years, turning decisively in aluminum's favor. Sustainability mandates made the infinitely recyclable can attractive against single-use plastic. Freight math made it irresistible: cans nest and stack, ship lighter, and waste less cube on a truck than bottles. And a wave of new beverage categories — craft beer, hard seltzer, energy drinks, canned water, ready-to-drink cocktails — was born in cans and marketed on cans. The can stopped being a commodity container and became, for a premium sparkling water or a $18 four-pack of IPA, part of the product's identity.

Serving those giants profitably, though, is a scale game with almost no room for subscale players. Which is why the defining transaction of modern Ball came in 2016: the acquisition of its largest rival, the British packaging company Rexam PLC, for approximately $6.6 billion, or £4.3 billion.5 In one stroke Ball combined the number one and number two global beverage can makers. Management underwrote the deal on roughly $300 million of targeted annual run-rate cost synergies — the savings that come from buying aluminum in even greater volume, optimizing which plant serves which customer, and eliminating duplicate corporate overhead. On a purchase price that valued Rexam at roughly ten to eleven times EBITDA, a steep multiple for heavy manufacturing, those synergies were not a nice-to-have; they were the entire economic justification. A deal like this only works if the acquirer actually extracts the promised savings, and the market was right to be skeptical until Ball proved it.

Why pay up for Rexam at all, rather than simply grow? Because in this industry, share is not won by building a better can — every top player's can is excellent — it is won by owning the plant nearest the customer's filling line and by buying metal cheaper than the next guy. Both of those advantages compound with size, and both are effectively impossible to buy organically at speed. Rexam brought Ball a European and emerging-markets footprint that would have taken a decade and enormous risk to build greenfield, plus overlapping procurement that could be consolidated into a single, larger aluminum-buying machine. In an oligopoly, the fastest route to durable advantage is often to remove a competitor from the board entirely, and Rexam was the biggest piece left to remove.

The regulators made Ball pay a toll first. Combining the top two players in an already concentrated industry triggered antitrust scrutiny on both sides of the Atlantic, and to win clearance Ball was forced to divest 22 beverage can plants to the Ardagh Group for roughly $3.0 billion.5 Read that carefully: to buy its biggest competitor, Ball had to hand a large package of factories to another competitor, effectively promoting Ardagh into a stronger number-three. Ardagh, buying forced sellers under a regulatory deadline, got those assets at an estimated seven-times-EBITDA neighborhood including synergies — a materially cheaper multiple than Ball paid for Rexam. That is the recurring irony of antitrust-driven divestitures: the seller is a motivated seller, and the buyer knows it. There is a subtler cost, too. By strengthening Ardagh, the remedy the regulators demanded partly recreated the competitive intensity the merger was supposed to reduce — Ball got scale, but it also helped fund a hungrier third player. Whether that trade was worth it depends entirely on how disciplined that reinforced rival chose to be, a question the "cangemic" years would answer uncomfortably.

Then there was the balance sheet. To fund Rexam, pro forma net debt spiked to roughly 4.5 times EBITDA — an uncomfortable, credit-straining level for an industrial company.5 This is where the story could have gone wrong, and where Ball's actual advantage showed itself. The beverage can business, for all its low margins, throws off remarkably predictable free cash flow: contractual volumes, pass-through pricing on metal, and customers who order in steady rhythm. Ball pointed that cash flow at the debt with discipline and pulled leverage back toward its target range within roughly three years. By the end of the decade the integration was, on the numbers, a success — synergies broadly delivered, debt paid down, and Ball established as the undisputed global leader in aluminum beverage packaging.

The analytical takeaway is not "big deals work." Most don't. It is that Ball bought scale in a business where scale is the moat — purchasing leverage on aluminum, network density that lets you assign the nearest plant to each customer, and the fixed-cost absorption that lets you underbid a subscale rival on a contract renewal — and then had the free cash flow and the discipline to survive the leverage it took on to get there. Scale, purchased responsibly, compounded. But scale also creates a specific vulnerability: when you have built the world's largest fleet of high-fixed-cost plants, the one thing you cannot survive is those plants sitting empty. Which is precisely the trap that a global pandemic was about to spring.

V. The "Cangemic" Hangover: Overcapacity, Destocking, and the Hard Pivot (2020–2023)

In the spring of 2020 the world's bars, stadiums, and restaurants went dark, and something strange happened to the humble can. With on-premise draft beer and fountain soda suddenly unavailable, consumption did not vanish — it moved home, into the retail channel, where beverages come in cans and bottles rather than kegs and syrup bags. Demand for aluminum cans spiked so violently that the industry coined a nickname for it: the "cangemic." Can makers, Ball among them, could not physically make enough. Customers were on allocation. For a brief, intoxicating moment, a commodity manufacturer had pricing power and a demand curve that looked like a technology company's.

Ball responded the way a company convinced a shortage is structural responds: it opened the capital-spending taps. It launched a multi-billion-dollar program to build massive new greenfield can plants across North America, each with high-speed lines capable of producing billions of cans a year. The logic was straightforward and, in real time, defensible — if demand had permanently stepped up, the manufacturer with the most modern low-cost capacity would win the next decade of contracts. The risk, equally, was obvious in hindsight: greenfield can lines are enormous fixed-cost commitments, and fixed costs are wonderful when volume is high and catastrophic when it isn't.

The whipsaw arrived in 2022. Input costs — aluminum, energy, freight, labor — surged with broad inflation. The beverage giants, protecting their own margins, pushed through some of the steepest retail price increases in a generation. A case of soda or beer that cost noticeably more at the shelf did what economics predicts: it dented volume. Consumers traded down, bought less, or bought larger formats. And then came the second blow — destocking. Retailers who had bulked up inventory during the shortage years now had too much, and as bars and restaurants reopened and the at-home surge reversed, they aggressively drew those inventories down. Ball's beverage customers, facing softening sell-through and bloated warehouses, abruptly slashed their can orders.

This is where the operating leverage that felt so good on the way up turned vicious. Operating leverage is a simple, unforgiving idea: when most of your costs are fixed, profit swings far more violently than revenue in both directions. A plant designed to run flat-out is enormously profitable at 95% utilization because each incremental can carries almost no added cost — the building, the presses, the crew are already paid for. Run that same plant at 60% and the math inverts: the fixed costs are still fully there, spread over far fewer cans, so unit costs balloon and the margin on the whole line can go negative. Those brand-new greenfield lines, built for a demand curve that had evaporated, now sat underutilized, and Ball had, briefly, the worst version of its own scale: a large fleet of expensive plants and not enough cans to fill them. The very asset base that made Ball the low-cost king when demand was strong became a millstone the instant demand cracked.

For an investor, the cangemic is the single most instructive episode in Ball's recent history, because it is a clean natural experiment in how management behaves when its own optimism proves wrong. The company had, in real time, mistaken a temporary pull-forward of demand for a permanent step-change — an error that looked reasonable in 2021 and reckless by 2023. The tell of a capital-allocation culture is not whether it ever makes that mistake; nearly everyone did. The tell is what it does next.

To management's genuine credit, this is the moment the EVA discipline earned its keep, and it is a fair test of whether the framework is real or just rhetoric. Ball did not chase volume to keep its shiny new lines busy. It did the opposite. Through 2022 and 2023 it permanently closed older, less-efficient plants — Phoenix, Arizona in the fourth quarter of 2022; St. Paul, Minnesota in early 2023; Wallkill, New York in the third quarter of 2023 — and it cancelled a planned mega-plant in North Las Vegas, Nevada.13 The strategic choice embedded in those closures is the whole point: Ball traded market share and top-line growth for capacity utilization and margin defense. It chose to run a smaller, tighter, more fully loaded network rather than a larger, half-empty one. For a company whose entire moat rests on being the low-cost producer, protecting the cost curve mattered more than protecting the volume line.

The scars were real, and investors spent 2022–2023 marking the stock down for them. But the response revealed something durable about how this management team thinks under stress: when the growth story broke, there was a specific plan — shut the marginal capacity, defend utilization, preserve returns on capital — rather than a hope that demand would come back. That instinct to prune ruthlessly was about to be applied to the most valuable asset Ball owned.

VI. Divesting the Space Engine: The $5.5B Sale of Ball Aerospace (2023–2024)

For decades, Ball Aerospace was the division that made engineers swoon and equity analysts squirm. Here was a business building instruments for flagship NASA telescopes and classified defense satellites, riding a rising tide of defense spending and commercial space demand, carrying a backlog north of $5.6 billion in contracted future work.6 By any standard it was an excellent company. The problem was where it lived.

Consider the bind. A packaging investor who buys Ball wants a stable, cash-generative industrial that returns capital — that person has no framework for valuing a lumpy, program-driven defense-aerospace business and no desire to underwrite cost-plus government contracts. A defense investor who could value the aerospace unit properly would never buy a stock that is 80% aluminum cans. So the aerospace business sat inside Ball structurally undervalued, its worth suppressed by what practitioners call the conglomerate discount: the market pays for the mismatched pieces at a blended, lowest-common-denominator multiple rather than for what each piece is worth on its own. Ball was, in effect, hiding a jewel in a toolbox and being priced on the toolbox.

There was also a timing logic that made 2023 the right moment to sell rather than hold. Defense budgets were rising in the wake of renewed great-power tension, commercial space was booming, and defense valuations were rich — buyers were paying up for exactly the kind of resilient, backlog-heavy franchise Ball Aerospace was. A seller wants to sell scarce assets when buyers are most eager to pay, and a defense prime hunting for space capabilities in 2023 was a very eager buyer. Meanwhile, Ball's own need was acute: the balance sheet still carried the strain of the cangemic overbuild, and a large slug of cash to pay down debt and repurchase a depressed stock was worth more to the packaging company than the aerospace division's earnings ever would be inside it.

The resolution came in the second half of 2023, when Ball agreed to sell the aerospace business to BAE Systems, and the deal closed on February 16, 2024, for a headline $5.5 billion in cash — $5.6 billion gross of certain adjustments.345 The strategic elegance of who bought it is worth noting: BAE, a British defense prime, could fold Ball Aerospace directly into a portfolio where those capabilities are core, pay for them at a defense multiple, and extract value a can company never could. It was the right home for the asset. There is a bittersweet coda here for anyone with a sense of history: the company that helped give Hubble its sight and Webb its mirror chose, quite rationally, that it should no longer be in the business of building starlight machines at all. Sentiment lost to arithmetic, as it always has at Ball.

Now the arbitrage, which is the part every capital-allocation nerd should savor. By management's framing, the aerospace unit was sold at roughly 19.6 times its trailing comparable EBITDA — an underlying economic consideration in the neighborhood of $4.8 billion after accounting for a present-value tax benefit of around $750 million on the structure. Set that against the fact that Ball's own core packaging business was, at the time, trading at roughly half that EBITDA multiple. In plain English: Ball sold a piece of itself for about twice the valuation multiple the market was assigning to the rest of it. That is a textbook demonstration of the conglomerate discount working in reverse — crystallizing, in a single transaction, value that the public market had refused to recognize while the two businesses were bolted together. The pre-tax gain on the sale was roughly $4.67 billion, and it single-handedly swung Ball's reported full-year 2024 net earnings to about $4.0 billion, versus $707 million the year before — an accounting artifact of the divestiture, not a leap in operating profit, and one an attentive reader should not mistake for organic performance.4

The more important question was what management would do with roughly $4.5 billion of after-tax cash, net of the roughly $950 million in taxes the transaction triggered.4 The answer was a three-way split that tells you how this team prioritizes. First, deleveraging — paying down debt to drive net leverage toward a conservative long-term target in the range of 2.5 to 3.0 times EBITDA, repairing the balance sheet the cangemic capex had strained. Second, shareholder returns — a large, opportunistic share-repurchase program aimed at shrinking the share count while the stock was, in management's view, cheap. Third, reinvestment in the core — modernizing the global aluminum packaging footprint the company had just spent 2022–2023 rationalizing.

A skeptic should press on one point in that capital-allocation story, though, because it is where good intentions most often go wrong. Buying back stock is only value-creating if the shares are actually cheap relative to intrinsic value; done indiscriminately, it is just a way to shrink the share count while transferring value from patient owners to sellers. Ball's management framed its repurchases as opportunistic — buying when the stock was depressed by the cangemic hangover — which is the right instinct if executed honestly. The test an owner should apply over time is simple: did the buybacks cluster when the stock was demonstrably cheap, or did they run mechanically regardless of price? A company that returns capital because it has capital, rather than because its own shares are the best available investment, is practicing a discipline in name only. On the evidence so far, Ball has bought heavily into weakness, which is the defensible version — but it is a behavior to keep watching, not a virtue to assume.

Strip away the narrative and the aerospace sale is the purest expression of the company's founding instinct: it sold its most technically impressive, most emotionally resonant asset — the spacecraft business, the thing that made Ball special at cocktail parties — because a focused pure-play packaging company was worth more, and more legible to investors, than a two-headed conglomerate. Whether "pure-play" turns out to be a strength or simply a more concentrated bet is a question for the bear case. But before we get there, management had one more piece of pruning to do, and this one cut a product the company had paraded as its ESG showpiece just five years earlier.

VII. Portfolio Optimization: Cutting the speculative novelties (2024–2025)

Around 2020, amid the cangemic's optimism, Ball rolled out a product designed to be seen: the Ball Aluminum Cup, an infinitely recyclable metal replacement for the red plastic party cup, launched with real fanfare and a compelling sustainability pitch. The vision was seductive. Picture a sold-out stadium, tens of thousands of fans, and every beer served in a recyclable aluminum cup instead of a landfill-bound plastic one — then extend that to grocery aisles, where households would buy sleeves of aluminum cups for backyard barbecues. It was ESG marketing you could hold in your hand, and it generated enormous positive press.

The cup is a useful parable about the difference between a good story and a good business, and about the specific temptation that stalks a company with a strong sustainability narrative. Everything about the aluminum cup was easy to love from a marketing deck: it photographed beautifully, it aligned with the corporate mission, it earned goodwill with stadiums and retailers, and it let executives tell a crowd-pleasing story about killing single-use plastic. What it did not do was clear its cost of capital — and a company that lets narrative appeal override return discipline is exactly the company EVA was designed to protect against. The danger for Ball was never that the cup would lose a lot of money; it was small. The danger was cultural: that a business justified by press rather than profit would be allowed to linger because killing it felt like abandoning the mission. That management ultimately applied the same cold arithmetic to its ESG showpiece that it had applied to Mason jars and telescopes is, in its way, more revealing than either larger divestiture.

The economics never caught up to the imagery. Manufacturing an aluminum cup — a wide, thin-walled, structurally awkward vessel — is materially more expensive than stamping a standardized beverage can, and that cost forced a retail price that shoppers, staring at a cheap bag of plastic cups right beside it, largely declined to pay. Stadium and event adoption had a genuine niche; mass retail grocery adoption stalled. The business sat inside Ball's catch-all "Other" reporting segment and did what capital-dilutive novelties do: it consumed investment and dragged on returns while generating a rounding error of profit. It was, in the cold arithmetic of the company's operating framework, value-destructive.

So in March 2025, Ball applied the same discipline it had applied to glass in 1993 and aerospace in 2024 — just at a smaller scale. Rather than pour more capital into a business that could not clear its cost of capital, it formed a joint venture called Oasis Venture Holdings, LLC, contributing the aluminum cup business — the commercial and manufacturing teams and the plant in Rome, Georgia that served as headquarters — and selling a 51% majority stake to Ayna.AI, an industrial-technology advisory and operating firm, while retaining a 49% minority interest.11 The structure is telling. Ball offloaded the capital burden and day-to-day operational headache of a business it had decided not to fund, handed control to an operator whose whole thesis is turning around industrial assets, and kept a minority stake so that if Ayna.AI actually cracks the cost problem and scales the category, Ball still participates in the upside. It is a graceful way to admit a bet did not work without writing it entirely to zero.

With the novelties cleared away, what remained was a clean, three-legged core, and the 2024 segment picture is the right baseline to anchor on. Beverage Packaging, North & Central America — the mature, stable, cash-generative engine — produced $5,619 million in net sales and $747 million of comparable operating earnings.1 Beverage Packaging, EMEA generated $3,466 million in net sales and $416 million of earnings, a lower-margin region wrestling with high European energy costs but real volume growth.1 Beverage Packaging, South America delivered $1,951 million in sales and $296 million of earnings — the highest-margin of the three, reflecting Ball's dominant position in a market (Brazil especially) where cans are culturally entrenched, though also the most exposed to currency swings and macro volatility.1 And the residual "Other," including aerosol packaging, contributed roughly $759 million.1

Here is the update that matters for a reader sitting in mid-2026: this focused portfolio then had a genuinely strong 2025. Full-year 2025 net sales in North & Central America rose to $6.29 billion with volumes up 4.8%; EMEA reached $3.98 billion on 5.5% volume growth; South America hit $2.16 billion on 4.2% growth.12 Comparable diluted earnings per share climbed to $3.57 from $3.17, and adjusted free cash flow set a record at $956 million.12 After the destocking trough, in other words, the underlying can business reaccelerated to mid-single-digit organic volume growth across all three regions simultaneously — evidence that the pruning defended margins without permanently sacrificing the demand base, and that the secular shift to aluminum still had momentum. The question was who would steer the newly simplified company through the next phase. In November 2025, Ball answered it.

VIII. The Next Act: Ronald J. Lewis & Operational Transformation (Late 2025–Present)

On November 10, 2025, Ball Corporation announced that Daniel W. Fisher would step down as chief executive and that the board had appointed Ronald J. Lewis as CEO and a director, effective immediately — the company's thirteenth chief executive.78 In the same breath, the board elected lead independent director Stuart A. Taylor II as chairman and named Daniel Rabbitt chief financial officer.7 A clean-sheet leadership team for the clean-sheet company.

The choice of Lewis is a strategy statement disguised as a personnel announcement, and it repays a close look. Lewis, 59, is not a founder or a financier; he is an operator, and specifically a supply-chain operator forged inside Ball's single most important customer relationship. Before joining Ball in 2019, he spent roughly 19 years across the Coca-Cola system — The Coca-Cola Company, Coca-Cola Enterprises, and Coca-Cola European Partners — in a series of supply-chain and procurement roles.7 At Ball, he ran the EMEA beverage business from 2019 to 2021, became chief operating officer of global beverage packaging from 2021 to 2024, and then served as chief supply chain and operations officer from January 2024 — meaning he was the executive most directly responsible for wringing efficiency out of the plant network through the very destocking and rationalization crunch described earlier.7

Think about what it means to install, atop a company whose largest buyers are beverage giants, a leader who spent two decades inside a beverage giant's supply chain. Lewis has sat on the other side of the table. He understands, from lived experience, how a bottler thinks about inventory buffers, contract structures, service-level penalties, and the operational choreography of a wall-to-wall plant feeding a filling line next door. This is the kind of tacit knowledge that does not show up on a résumé line but shapes every negotiation: knowing where a customer's real pain points sit, which contract clauses they will fight over and which they will concede, how they actually plan production versus how they say they do. In a business where the entire customer base is a dozen giant relationships governed by multi-year contracts, an executive who has lived inside those relationships from the buyer's seat is a genuinely differentiated hire. His mandate reads accordingly: not the wild greenfield expansion of the cangemic years, but execution — asset optimization, supply-chain transformation, and squeezing the returns out of the footprint Ball already owns. After a decade defined by a mega-merger, a pandemic overbuild, and a transformational divestiture, the board chose a plumber over a dealmaker. That is a defensible read of what a mature, focused oligopolist actually needs, but it is also a bet that the value left to create here is operational rather than strategic — and skeptics will note that operators rarely re-rate a stock the way a bold strategic move can. The counter-risk is subtler: an operator promoted from within, who owned the supply chain during the overbuild, may be less inclined than an outsider to question the assumptions that produced it. Continuity is a virtue when the strategy is right and a liability when it needs challenging.

The incentive structure around Lewis is worth putting on the table, because compensation design reveals what a board is actually asking for. Lewis's arrangement carried a base salary of $1,000,000, an annual cash incentive target of 150% of base, and, beginning in 2026, eligibility for performance-based equity awards with a target value of $7,000,000 — so the overwhelming majority of the package is variable and tied to performance rather than salary.8 Ball's governance also requires the CEO to hold stock worth six times base salary, and prohibits hedging or pledging that stock, which forces genuine, unhedged exposure to the share price rather than the paper alignment that pledging can quietly undo.8 None of this guarantees good behavior, but the shape of it — heavy equity weighting, meaningful ownership requirement, anti-hedging rules — is the shape of a company that wants its CEO thinking like a long-term owner.

Lewis's first significant strategic move set the template for the new era, and it is deliberately unglamorous. In December 2025 Ball agreed, and in January 2026 it moved to complete, the acquisition of an 80% stake in the European beverage can business of Benepack from China's 奥瑞金科技 ORG Technology, for total consideration of roughly $218 million (about €184 million); ORG retained a 20% minority interest.910 Read the structure and the discipline jumps out: of that total, Ball paid only about $95 million (€80 million) in cash for its equity stake, with the remainder primarily assumed debt.10 What Ball got were two operational, modern aluminum can plants — in Genk, Belgium and Makó, Hungary — folded straight into the EMEA segment.910 German antitrust authorities cleared the deal in December 2025.[^15]

Contrast this with 2020's playbook. Instead of spending years and a fortune building greenfield capacity into an uncertain demand curve, Ball bought two finished, running plants at a modest price, instantly extending its footprint into Central and Eastern Europe where can demand is growing. It is capital-efficient, low-drama, and squarely aligned with the "optimize, don't overbuild" thesis Lewis was hired to execute — buying existing assets from a foreign owner retreating from the region rather than adding net new capacity to an industry that spent 2022–2023 learning the cost of too much of it.

Which brings us to the numbers Lewis has put his own name against. For 2026, Ball guided to more than 10% comparable diluted EPS growth and adjusted free cash flow greater than $900 million, framed around continued buybacks and further deleveraging toward a conservative net-leverage target in the high-2s.12 These are the promises against which his credibility will be measured. And they are, notably, growth targets built not on a booming can market but on volume in the mid-single digits amplified by buybacks, cost, and mix — which is either prudent underwriting or a quiet admission that the underlying market alone no longer delivers double digits. We will return to that tension in the stress test. First, the machine itself: what, mechanically, keeps competitors out?

IX. Playbook: Competitive Moats (7 Powers & Porter's 5 Forces)

Walk up to a modern Ball plant and the first thing you might notice is that it appears bolted to another factory. That physical detail is, more than any patent or brand, the heart of the company's defensibility. Let's war-game the moat properly, using Hamilton Helmer's 7 Powers and Michael Porter's Five Forces, and — because this is an independent read, not a sales deck — let's note where each supposed power is softer than it looks.

Scale Economies (the primary power). A modern, high-speed, two-line aluminum can plant is a hundreds-of-millions-of-dollars proposition. More importantly, Ball buys aluminum sheet by the billions of pounds a year, and that purchasing volume translates into raw-material pricing a regional player simply cannot match. Since the metal is the dominant cost in a can, even a small per-pound advantage, multiplied across tens of billions of cans, is a structural edge in a business won and lost on pennies. The honest caveat: Ball's scale advantage is real against a small regional maker, but far thinner against Crown Holdings, which operates at comparable global scale. Scale is a moat against minnows, not against the other whales.

Switching Costs (physical integration). This is the most underappreciated and most durable piece of the moat: the "wall-to-wall," or co-located, manufacturing model. Many Ball plants are built physically adjacent to a customer's bottling and filling facility, sometimes connected by overhead conveyors that carry empty cans straight from Ball's line into the customer's filler with no truck, no warehouse, no freight in between. For a bottler, switching suppliers doesn't just mean signing a new contract — it means severing a physical umbilical cord, tearing out conveyor infrastructure, finding warehouse space, and adding freight cost and logistical risk that co-location was specifically designed to eliminate. That is a switching cost measured not in inconvenience but in capital and operational disruption, and it is why these relationships, once won, persist for many years. The caveat: this power only exists where Ball is actually co-located; on standalone plants serving multiple customers, switching costs revert to ordinary contractual stickiness.

Process Power. Running a bank of draw-and-iron presses that each stamp, stretch, coat, and inspect on the order of a couple thousand cans per minute — while holding defect rates down to parts-per-million on a vessel that must survive internal pressure without leaking — is genuinely hard operational craft accumulated over decades. It is not easily bought or copied. But it is broadly shared among the top few players; process excellence is table stakes at the top of this industry rather than a unique Ball secret.

Now Porter's Five Forces, which frames the competitive weather:

Threat of new entrants: very low. Between the capital cost, the specialized operational know-how, and the fact that the available volume is locked up under multi-year contracts with co-located incumbents, there is essentially no room for a new entrant to appear at scale. This is the strongest of the five forces in Ball's favor.

Bargaining power of buyers: moderate, and arguably the swing factor. Ball's customers are among the most powerful companies in consumer goods, and they are concentrated — Anheuser-Busch InBev represents roughly 16% of sales and Coca-Cola roughly 13%. That is real leverage on price at contract renewal. But it cuts both ways: those same giants need volumes so vast that only a top-tier oligopolist can supply them, and they are locked into multi-year contracts (commonly three to ten years) reinforced by co-location. The relationship is a mutual hostage situation more than a one-sided squeeze — but with two customers accounting for nearly 30% of sales, the concentration is a genuine vulnerability, not a talking point.

Bargaining power of suppliers: low, and cleverly neutered. Aluminum sheet comes from a consolidated set of suppliers such as Novelis and Alcoa. Ordinarily that would be a threat. But Ball's contracts feature a pass-through mechanism: movements in the underlying London Metal Exchange aluminum price flow directly through to the beverage customer, so Ball is largely insulated from the commodity price itself. This is a crucial and often-misunderstood feature — Ball is not really betting on the price of aluminum; it converts metal into cans for a spread. The residual risk is not the metal price but the premiums and energy around it, and the working-capital swings when metal prices move sharply.

Threat of substitutes: moderate. Glass and PET plastic remain functional alternatives, and in price-sensitive categories like bottled water, plastic still dominates. The sustainability tailwind — aluminum's high global recycling rate against plastic's far lower one — and regulatory pressure on single-use plastics protect the can in beer, soda, energy, and premium categories. But "moderate" is the right word, not "low": if the relative economics shift, substitution can flow backward, a risk the bear case takes seriously.

Competitive rivalry: moderate and, critically, rational. In North America, Ball and Crown Holdings together control something like 60–65% of the market, with Ardagh holding much of the rest. An oligopoly this concentrated tends toward disciplined behavior — competing on regional capacity utilization and contract bids rather than launching mutually destructive price wars. That rationality is itself a kind of collective moat, but it is a behavioral equilibrium, not a law of nature; a desperate competitor or a wave of overcapacity can break it, as the industry's own recent history shows. The net picture: Ball's defenses are strongest against new and small players and weakest precisely where the money is — across the negotiating table from a handful of giant customers and a couple of equally large rivals.

It is worth briefly locating Ball against those rivals, because the competitive set shapes what "winning" can even mean here. Crown Holdings is the closest peer — comparably global, comparably capable, and Ball's true mirror-image competitor in North America and beyond. The two are less like Coke and Pepsi locked in brand warfare and more like two disciplined utilities that have tacitly agreed the smart move is to protect returns rather than fight for the last point of share. Ardagh, the reinforced number three born partly of the Rexam remedy, has historically carried more leverage and been the more financially stretched of the majors, which makes it the wild card: a distressed competitor is the one most tempted to break pricing discipline to keep its plants full. And around the edges sit regional and emerging-market players, plus the strategic curiosity of Chinese packaging groups like 奥瑞金科技 ORG Technology — the very seller from which Ball bought Benepack — whose periodic advances into and retreats from Western markets reshuffle capacity at the margin. The honest read of this landscape is that Ball's edge over Crown is narrow, its edge over everyone else is wide, and the industry's collective prosperity depends less on Ball's brilliance than on all the majors continuing to behave rationally at once.

A myth worth puncturing. The consensus story sold to retail investors is that Ball is a clean "ESG sustainability play" riding an unstoppable green wave — buy the can maker, ride the war on plastic. The reality is more grounded and, for a serious investor, more useful: Ball is a cyclical, capital-intensive industrial with a genuine but maturing secular tailwind, whose returns depend far more on prosaic factors — plant utilization, contract renewals, oligopoly discipline, and capital allocation — than on any sustainability narrative. The green tailwind is real and it helps; it is not a substitute for the blocking and tackling of running a low-cost manufacturing network. Investors who buy the sustainability story and ignore the operating leverage learned a painful lesson in 2022–2023.

X. The Investment Case: Bear vs. Bull Stress Test

Let's put the company in the interrogation room. If a sharp long/short investor or an activist sat across from Ball's management, what would the fight actually be about?

The skeptic's core question. Is the plastic-to-aluminum transition — the secular engine under the whole thesis — plateauing? For years the bull story rested on cans stealing share from glass and plastic. But if global beer and carbonated soft drink volumes stay flat, and if the substitution gains slow as the easy conversions are exhausted, then Ball's promised double-digit earnings growth has to come from somewhere else: buybacks, cost cutting, and mix. Those are real levers, but they are finite and lower-quality than genuine volume growth. A skeptic would press management hard on European margins in particular, where high energy costs and the risk of regional overcapacity threaten the profitability of the fastest-growing segment. On recent calls, management's answer has leaned on integrating Benepack and driving supply-chain efficiency rather than on a bullish volume forecast — a tell that even the company is underwriting a world where the market grows only modestly and the earnings algorithm must be manufactured through capital allocation and operations.

The bull case, stated fairly. Freed from the aerospace conglomerate discount, Ball is now a legible, high-return packaging utility — a business that converts metal into cans for a contractual spread, protected from commodity swings by pass-through pricing, and throwing off close to a billion dollars of free cash flow a year that it returns aggressively to shareholders. The 2025 record free cash flow of $956 million and mid-single-digit volume growth across all three regions are concrete evidence the model works when it isn't being whipsawed by a pandemic.12 Layer on disciplined, capital-efficient tuck-ins like Benepack that extend the footprint without overpaying, and the algorithm — low-single-digit volume, plus margin, plus a shrinking share count — plausibly compounds earnings at a rate well above the underlying market's growth. The bull does not need the aluminum transition to reaccelerate; the bull needs it merely not to reverse.

The bear case, stated just as fairly. Start with customer concentration: with AB InBev at roughly 16% and Coca-Cola at roughly 13% of sales, the loss — or even an aggressive renegotiation — of either relationship would leave a hole no amount of buyback can fill. Second, volume elasticity: if the beverage brands keep pushing retail prices up to defend their own margins, end-consumer volumes can keep sagging, and Ball's high-fixed-cost network turns that volume softness into amplified margin pain, exactly as it did in 2022–2023. Third, the substitution risk running in reverse: if an oil surplus collapses PET resin prices, the economics could pull price-sensitive categories like bottled water back toward plastic, blunting the sustainability tailwind at the margin. And an activist would add a governance-flavored jab: after a decade of a mega-merger, a pandemic overbuild, a $5.5 billion divestiture, and a string of portfolio reversals — glass, then aerospace, then the aluminum cup — is this a masterclass in disciplined evolution, or a management team that keeps having to undo its own prior enthusiasm? The generous read is capital discipline; the cynical read is serial course-correction. Both readings fit the same facts, and an honest investor holds them in tension.

Which brings us to management credibility, the thread that runs through the whole case. The evidence over time is genuinely mixed in a useful way. On the positive side, Ball did what it said on the hard things: it exited glass when EVA demanded it, it delevered after Rexam as promised, it shut plants and cancelled the Las Vegas project rather than chase vanity volume, and it monetized aerospace at a spectacular multiple and pointed the proceeds at debt and buybacks as advertised. On the cautionary side, the cangemic overbuild was a real capital-allocation error — the company added expensive capacity into a demand spike it treated as structural, then had to write off and close plants a few years later. The most useful conclusion for an owner is not a grade but a behavioral pattern: this is a team that makes aggressive bets and then corrects them with unusual honesty and speed. That is better than a team that overbuilds and denies it, but it is not the same as a team that gets the bet right the first time.

The three KPIs that actually matter. Cut through everything and watch three things. First, global organic beverage can shipment growth — the truest read on real end-consumer demand and the operating leverage that flows from it; if this stays positive in the mid-single digits, the algorithm holds, and if it rolls over, the buyback-and-cost story gets exposed. Second, comparable diluted EPS growth, the metric management is explicitly compensated against and the cleanest scoreboard for whether the capital-return engine is delivering. Third, return on invested capital, or the EVA discipline itself — the ultimate test of whether Ball is deploying its free cash flow into value-creating uses or, as in the cangemic, destroying capital in pursuit of growth. Track those three and you will know how the story is really going, long before the narrative catches up.

One second-layer watch item deserves a place on the radar even though it sits outside those three headline KPIs: the working-capital and premium exposure hidden beneath the "aluminum pass-through" comfort blanket. The pass-through neutralizes the LME base price, but it does not fully neutralize regional metal premiums, energy inputs, or the cash-flow timing effects when metal prices swing sharply — a fast run-up in aluminum can temporarily balloon the receivables and inventory Ball carries, pressuring free cash flow even when the income statement looks fine. In Europe especially, where energy is both expensive and volatile, the gap between "protected from the metal price" and "protected from all input costs" is where margin surprises tend to live. It is not a thesis-breaker, but it is the sort of detail that separates investors who understand the business from those who have merely read the summary.

XI. Outro & Epilogue

Stand back from 145 years and the shape of Ball Corporation is almost startlingly consistent. Five brothers who made kerosene buckets until glass jars were better business. A jar company that walked into the space age because its vacuum-coating knowledge happened to transfer. A can maker that abandoned the very glass jar that made its name the moment the numbers said to. A global consolidator that bought its largest rival, survived the leverage, and then sold its most brilliant division — the spacecraft instruments, the telescope optics — because a focused company was worth more than a fascinating one.

The through-line is not a product; Ball has cheerfully outlived most of its products. The through-line is a temperament — a willingness to be defined as much by what it sells as by what it builds. Glass in the 1990s, aerospace in 2024, the majority of the aluminum cup in 2025: each divestiture was a small act of self-redefinition in service of return on capital. That is a rarer corporate trait than it sounds, and it is the single most important thing to understand about this company. Most organizations cling to their heritage until it kills them. Ball keeps selling its heritage and buying its future.

Under Ronald J. Lewis, the newly simplified company enters an era whose ambition is deliberately modest in the best sense: not to conquer a new frontier, but to run the one it dominates with relentless operational precision — optimizing plants, integrating tuck-ins like Benepack, and returning the bulk of a billion-dollar cash flow stream to shareholders while the world keeps drinking from infinitely recyclable metal. The bet is that in a mature, rational oligopoly, boring execution compounds. The risk is that a pure-play with two customers near 30% of sales and a secular tailwind that may be maturing has traded the conglomerate's complexity for a more concentrated set of ways to be wrong.

For the long-term investor, the assignment is clear even if the verdict is not: watch the shipment growth, watch the earnings algorithm, and watch whether the capital discipline that defined the last three decades survives the next three years — because at Ball, the story has always been written less in what the company keeps than in what it has the nerve to let go.

References

-

Ball Reports Fourth Quarter 2024 Results — Ball Corporation, 2025-02-01 ↩↩↩↩↩

-

Ball Corporation — Investor Relations and Company History ↩↩↩↩↩↩↩↩

-

BAE Systems Completes Acquisition of Ball Aerospace — BAE Systems, 2024-02-16 ↩↩

-

Ball Completes Sale of Aerospace Business — Ball Corporation, 2024-02-16 ↩↩↩↩

-

BAE Systems to Acquire Ball Aerospace for $5.5 Billion — Reuters, 2023-08-17 ↩↩↩↩

-

Ball closes $5.6B sale of aerospace business and now is focused exclusively on packaging — Packaging Dive, 2024-02-16 ↩

-

Ball Corporation Announces Board and Leadership Transitions — Ball Corporation, 2025-11-10 ↩↩↩↩

-

Ball Corporation Form 8-K (CEO Appointment of Ronald J. Lewis) — SEC EDGAR, 2025-11-10 ↩↩↩

-

Ball to Acquire Majority Stake in European Beverage Can Manufacturer Benepack — Ball Corporation, 2025-12-10 ↩↩

-

Ball Corporation to Acquire 80% Stake in Benepack's European Beverage Can Plants — Sahm Capital, 2025-12-11 ↩↩↩

-

Ball Corporation to Sell Ball Aluminum Cup Assets, Forming Joint Venture — PR Newswire, 2025-03-05 ↩

-

Ball Reports Strong Fourth Quarter and Full-Year 2025 Results — Ball Corporation, 2026-02-02 ↩↩↩↩

-

Packaging Giant Ball Corp Closes US Plants Amid Slower Demand — Packaging Dive, 2023-08-04 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube