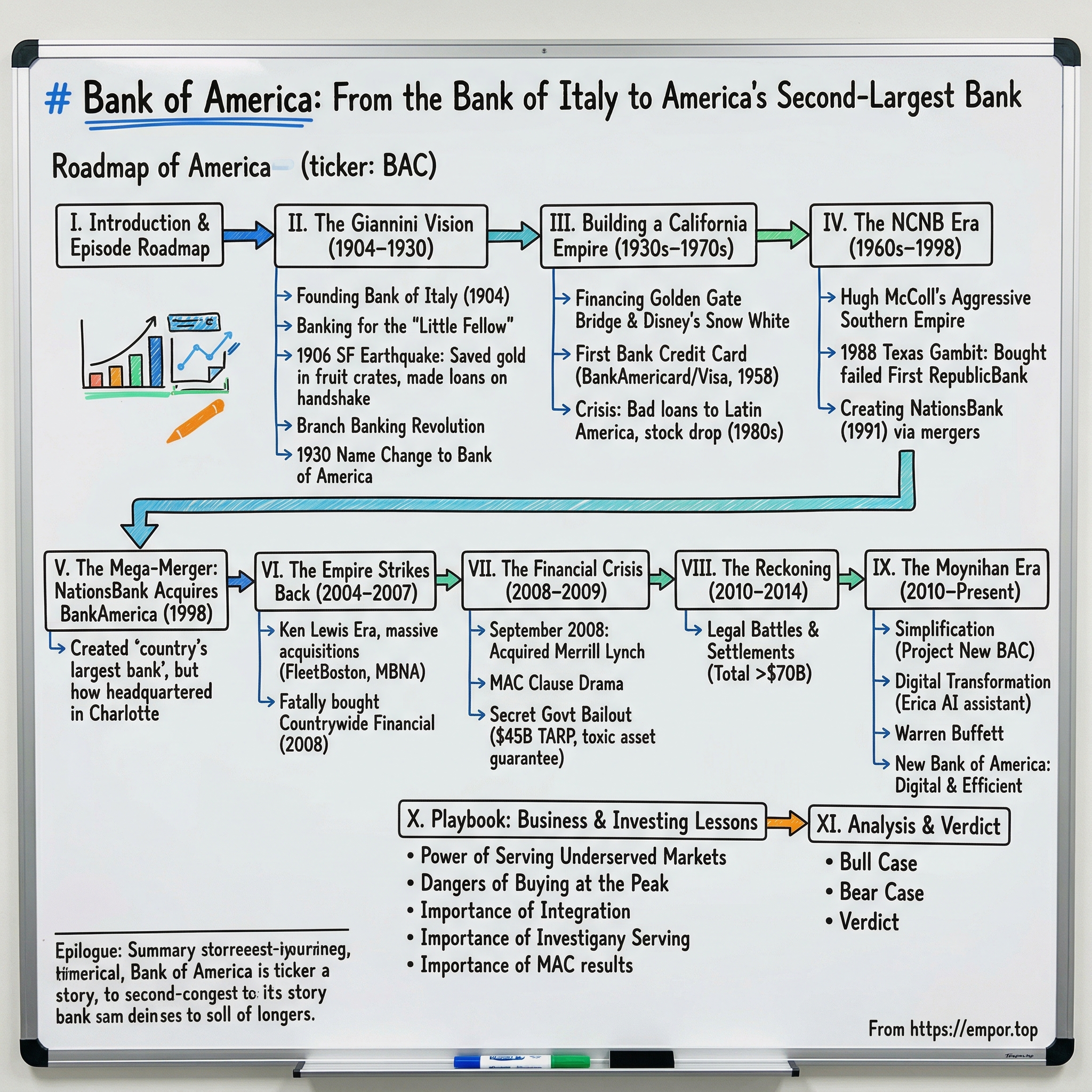

Bank of America: From the Bank of Italy to America's Second-Largest Bank

I. Introduction & Episode Roadmap

The year is 1904. In a cramped storefront in San Francisco's North Beach, an Italian immigrant's son is about to launch a bank with a radical idea: that working-class people deserve credit just as much as the wealthy. That man, Amadeo Peter Giannini, couldn't have imagined that his Bank of Italy would one day become Bank of America—a $3 trillion colossus that touches one in three American households.

Today, Bank of America stands as the second-largest banking institution in the United States, a member of the Big Four that dominates American finance. But here's the question that should fascinate any student of business history: How did a community bank serving Italian immigrants transform into a coast-to-coast financial empire? And perhaps more intriguingly—was this transformation worth the price paid along the way?

This is a story of audacious vision meeting brutal reality. It's about builders like Giannini who saw banking as a democratizing force, and empire-builders like Hugh McColl who turned acquisition into an art form. It's about surviving the 1906 San Francisco earthquake with gold hidden in fruit crates, and nearly dying in 2008 with Merrill Lynch bleeding billions. It's about issuing the first bank credit card that would become Visa, and later buying Countrywide Financial at exactly the wrong moment.

The themes we'll explore cut to the heart of American capitalism: the tension between serving communities and serving shareholders, the seductive danger of growth-by-acquisition, and what happens when institutions become "too big to fail." We'll see how three distinct banking cultures—Giannini's populist California bank, McColl's aggressive Southern empire, and Wall Street's investment banking elite—collided to create today's Bank of America.

What makes this story particularly relevant now? As fintech disrupts traditional banking and regional banks face new pressures, Bank of America's journey offers crucial lessons about adaptation, scale, and survival. This isn't just banking history—it's a blueprint for understanding how American finance really works, and why the biggest players got that way.

II. The Giannini Vision: Founding the Bank of Italy (1904–1930)

The Produce Merchant's Son

Amadeo Peter Giannini arrived in this world in 1870 in San Jose, California, the son of Italian immigrants who ran a small hotel. His father died when he was seven, crushed by a falling chimney. His mother remarried, and young Amadeo went to work for his stepfather in the produce business. By age 31, he'd made enough money to retire. But retirement didn't suit a man with his restless energy and outsized faith in the American dream.

The defining moment came in 1904. Giannini had joined the board of Columbus Savings & Loan, a small North Beach institution serving the Italian community. When the board rejected his proposals to lend to working-class immigrants, he did what any reasonable person would do—he quit and started his own bank. On October 17, 1904, the Bank of Italy opened its doors with $150,000 in capital, a rented saloon for an office, and a revolutionary idea.

Banking for the "Little Fellow"

Most banks in 1904 viewed the working class with suspicion, but Giannini knew better from his experience in the produce business watching immigrant farmers pay their debts religiously. His innovative bank welcomed small borrowers who might otherwise use loan sharks, recognizing that working class people were just as likely to repay loans as wealthy clients.

The Bank of Italy wasn't just different in whom it served—it was different in how it operated. Giannini was the first to offer banking services to the blue collar worker and welcomed small borrowers. Not only did he loan money to them, but also encouraged them to deposit their money in his bank; at that time, they only had the choice to stow away their savings under their mattresses. The bank made loans as small as $25, stayed open late to accommodate workers' schedules, and—revolutionary for the time—had employees who spoke Italian, helping immigrants navigate the financial system in their own language.

Giannini himself embodied this hands-on approach. He used the same tactics he had employed so successfully buying fruits and vegetables. He walked the streets of North Beach, schmoozed with recent immigrants in his fluent Italian, and persuaded them to move their small savings from the mattress to his bank. No private office, no secretary—just Giannini on the bank floor, answering his own phone, seeing up to a hundred people in an afternoon.

The results were staggering: In December 1904, loans amounted to $178,400 and deposits to $134,413. One year later, the figures were $883,522 and $703,024. Within a year of opening, deposits had quintupled.

The San Francisco Earthquake That Made A Legend

At 5:12 AM on April 18, 1906, San Francisco shook violently. Giannini, asleep in his San Mateo home seventeen miles away, was thrown from his bed. As fires began consuming the city—fueled by broken gas mains and unstoppable due to ruptured water lines—most bankers watched helplessly as their steel vaults turned into ovens. Those vaults couldn't be opened for weeks without oxygen rushing in and incinerating everything inside.

But Giannini wasn't most bankers. Racing to San Francisco, he found chaos: buildings collapsing, looters roaming, fires advancing on his bank. He loaded $2 million onto a produce wagon, covered the money with vegetables and headed home. Some accounts say he used garbage carts; others say fruit crates from his stepfather's business. What matters is this: while every other bank in San Francisco sat paralyzed, Giannini had rescued his deposits.

Three days later, as refugees camped in Golden Gate Park and the city still smoldered, Giannini did something extraordinary. Within days after the earthquake Giannini was in the North Beach neighborhood with a plank of wood sitting across two barrels taking deposits and giving out rebuilding loans signed for with a handshake. His makeshift sign read: "Bank of Italy—Open for Business."

Giannini gained fame by setting up a makeshift bank on a North Beach wharf and making loans to local residents "on a handshake." No collateral. No lengthy applications. Just a signature and a promise. While other banks waited weeks for their vaults to cool, Giannini was already financing San Francisco's resurrection. Every loan he made was purportedly repaid in full.

This wasn't charity—it was shrewd business wrapped in genuine empathy. Giannini understood that the people rebuilding San Francisco weren't risks; they were opportunities. The earthquake made him a folk hero, but more importantly, it proved his philosophy: trust the common man, and he'll build uncommon things.

California Dreaming: The Branch Banking Revolution

After 1906, Giannini saw California's future with startling clarity. This wasn't going to remain a frontier state—it would become America's growth engine. But to finance that growth, banking had to change. In 1909, California passed legislation allowing branch banking, and Giannini pounced.

Seeking more customers, the former produce salesman returned to his old haunts—the fertile valleys of California. He "walked in rows beside farmers engaged in plowing" to explain how bank branches make credit cheaper and more reliable. Picture this: a banker in a three-piece suit, trudging through muddy fields, explaining compound interest to skeptical farmers in broken English and fluent Italian.

Town by town, he built what no American bank had attempted: a statewide branch network. In 1909 Giannini began buying banks elsewhere throughout the state of California and converting them into branches of the Bank of Italy. By 1918 the Bank of Italy had become the first statewide branch-banking system in the United States. By 1915, seven branches. By 1918, twenty-four branches with $93 million in resources.

The Eastern banking establishment was horrified. Branch banking, they argued, concentrated too much power, threatened local control. But Giannini saw it differently: branches spread risk, brought capital to underserved areas, and let a farmer in Fresno benefit from deposits in San Francisco. It was financial democracy in action.

The Transformation: From Bank of Italy to Bank of America

By the late 1920s, Giannini faced a naming problem. The "Bank of Italy" worked in California's immigrant communities, but as he expanded nationally, the name limited his reach. Bank of America, Los Angeles had been established in 1923 by Orra E. Monnette. Giannini began investing in the Bank of America, Los Angeles because conservative business leaders in Los Angeles were less receptive to the Bank of Italy than San Franciscans had been. Bank of America, L.A. represented a growth path: the name idealized the broader mission of the new bank.

In 1928, the Bank of Italy merged with the smaller Bank of America, Los Angeles. In 1930, Giannini changed the name from "Bank of Italy" to "Bank of America". The immigrant's bank had become America's bank—literally. This wasn't just rebranding; it was a declaration of ambition. Giannini wasn't content serving California's working class. He wanted to democratize banking for all of America.

By this transformation, Giannini had built something unprecedented. From that converted saloon in North Beach, he'd created California's banking infrastructure, financing everything from small farms to the emerging motion picture industry. His philosophy—"safety before profit," serving the "little fellow"—had proven that doing good and doing well weren't mutually exclusive. As we'd soon see, this California empire would become the foundation for something even larger: America's first truly national bank.

III. Building a California Empire: Innovation and Expansion (1930s–1970s)

The Depression Test

In 1930, just as the Bank of Italy became Bank of America, the world economy collapsed. For most banks, the Great Depression was an existential crisis. For Giannini, it was validation. His conservative lending practices—mocked by Wall Street as unsophisticated—suddenly looked prescient. While New York banks failed by the hundreds, Bank of America kept its doors open, honoring every withdrawal.

But Giannini went further. After the stock market crash of 1929 and the Great Depression that followed, Giannini kept financing with an interest rate close to zero. Not only did his bank survive the Great Depression, by 1945 it was recognized as the strongest bank in the world. When others hoarded capital, he lent aggressively. His slogan during the Depression: "Back to Good Times" and "California Can Lead the Nation." It wasn't empty optimism—it was strategic countercyclical investing, decades before economists had a name for it.

The numbers tell the story: By 1945, it had grown by a branch banking strategy to become the world's largest commercial bank with 493 branches in California and assets totaling $5 billion. Think about that—during the worst economic crisis in modern history, Giannini built the world's largest bank. How? By betting on recovery when everyone else was betting on collapse.

Financing the California Dream

The 1930s marked Bank of America's transformation from a large regional bank to California's economic engine. Consider what Giannini financed during this period—it reads like a greatest hits of American culture and infrastructure.

In 1932, Golden Gate Bridge chief engineer Joseph Strauss called upon Giannini for help. No other bank would touch the project—a suspension bridge during the Depression seemed like madness. Giannini listened to Strauss explain his 14-year struggle, then said simply: "We'll take the bonds. We need the bridge." Bank of America bought $6 million worth of bonds, allowing Strauss' enterprise to get underway. Without Giannini's assistance, it is doubtful that the Golden Gate Bridge would ever have been built.

Hollywood was equally transformed by Giannini's vision. He bankrolled the new California wine industry and loaned money to Hollywood ventures, including Mary Pickford's and Charlie Chaplin's United Artists in 1923. When Walt Disney went $2 million over budget making Snow White, Giannini helped him out with a loan. This wasn't charity—Giannini understood that California's future lay not just in agriculture but in entertainment and tourism.

The bank also pioneered entirely new financial products that would reshape American commerce. The numbers by mid-century were staggering: 493 branches, $5 billion in assets, the world's largest commercial bank. But size wasn't the point—transformation was. Giannini had proven that a bank could be both massive and personal, both profitable and civic-minded.

The Credit Card Revolution

The year 1958 marked another revolutionary moment. On September 18, 1958, Bank of America officially launched its BankAmericard credit card program in Fresno, California. It issued the first bank credit card, BankAmericard, in 1958. This wasn't just a new product—it was the invention of modern consumer credit.

The launch was both brilliant and disastrous. In what became known as the "Fresno Drop," Bank of America mailed 65,000 unsolicited credit cards to residents. No application, no credit check—just a card with a $300-$500 limit showing up in your mailbox. The results were predictable: 22% delinquency rates, rampant fraud, losses of $20 million in the first 15 months.

But Bank of America persevered, cleaning up the program and by 1961, BankAmericard became profitable. The genius wasn't just the card—it was the network. By 1966, Bank of America began licensing its BankAmericard to banks nationwide. This became the first nationally licensed credit card program. The new network adopted the name Visa in 1976 and eventually spun off from Bank of America. BankAmericard becomes Visa - creating a global payment network that would process trillions in transactions annually.

Think about the audacity here: Bank of America didn't just create a product, it created an entire payment ecosystem that would fundamentally change how the world transacts. From Giannini's fruit crates full of gold to magnetic strips processing billions of transactions—the evolution was complete.

The Crisis Years

Giannini's death in 1949 marked the end of an era, and by the 1980s, Bank of America faced its darkest hour since the Great Depression. The bank that had survived 1906 and 1933 nearly died from bad loans to Latin America and poor management.

BankAmerica experienced huge losses in 1986 and 1987 due to the placement of a series of bad loans in the Third World. The company fired its CEO, Sam Armacost, in 1986. Though Armacost blamed the problems on his predecessor, A. W. (Tom) Clausen, Clausen was appointed to replace Armacost. The losses resulted in a huge decline of BankAmerica stock, making it vulnerable to a hostile takeover.

The numbers were catastrophic: In 1985, it posted its first quarterly loss since the Great Depression. By the second quarter of 1986, its trailing 12 months' loss exceeded $1 billion. For context, Only one other bank in history, Continental Illinois, had ever lost as much -- and it ended up as a ward of the FDIC.

Then came the vultures. First Interstate Bancorp of Los Angeles (which had originated from banks once owned by BankAmerica), launched such a bid in the fall of 1986, although BankAmerica rebuffed it, mostly by selling operations. The irony was bitter—First Interstate had been created from Bank of America's own interstate operations, forcibly divested decades earlier. Now the child was trying to devour the parent.

It sold its FinanceAmerica subsidiary to Chrysler and the brokerage firm Charles Schwab and Co. back to Mr. Schwab. It also sold Bank of America and Italy to Deutsche Bank. By the time of the 1987 stock-market crash, BankAmerica's share price had fallen to $8, but by 1992 it had rebounded mightily to become one of the biggest gainers of that half-decade.

Eight dollars. The bank that had financed the Golden Gate Bridge, that had created Visa, that had been the world's largest—trading at eight dollars per share. This wasn't just a crisis; it was an existential moment. Bank of America survived, barely, but the California empire Giannini built would never again dominate American banking. That role would pass to an unlikely successor: a aggressive bank from North Carolina that most Californians had never heard of. The stage was set for Hugh McColl and the transformation of American banking.

IV. The NCNB Era: Hugh McColl's Southern Banking Empire (1960s–1998)

The Marine from North Carolina

While Bank of America was conquering California, a very different banking story was unfolding in Charlotte, North Carolina. This wasn't a story of serving immigrants or financing dreams—it was about raw ambition, military precision, and the relentless pursuit of scale. At its center stood Hugh McColl Jr., a former Marine who approached banking like warfare. McColl joined American Commercial Bank in 1959, fresh out of the Marines with a first lieutenant's commission and a taste for military discipline. In 1960, a year after McColl joined American Commercial Bank, the bank merged with Greensboro's Security National Bank, becoming North Carolina National Bank. Vigorously competitive, McColl deployed a methodical, military approach to transforming the small regional bank, via incremental acquisitions and mergers, into NationsBank and ultimately Bank of America.

The man kept crystal hand grenades on his desk—not replicas, but real ones, deactivated but symbolic. One of NationsBank's coveted internal awards was a crystal hand grenade, an allusion to the real one McColl, an ex-Marine, kept on his desk for years. When he called an acquisition "Operation Overlord" after the Normandy invasion, he wasn't being cute. He meant it.

McColl's approach was the antithesis of Giannini's populist vision. Where Giannini walked through fields talking to farmers, McColl flew in corporate jets plotting takeovers. Where Giannini built branches to serve communities, McColl bought banks to eliminate competitors. His philosophy was brutally simple: get big or get eaten.

The Texas Gambit: First RepublicBank's 1988 Crisis

Texas banking was in ruins—oil prices had collapsed, real estate had crashed, and the state's biggest banks were failing. First RepublicBank Corporation, with $35 billion in assets, was hemorrhaging money. The FDIC needed a buyer, and fast.

McColl saw opportunity where others saw disaster. NCNB made national headlines with its purchase of the failed First RepublicBank Corporation of Dallas, Texas from the Federal Deposit Insurance Corporation (1988). In 1988, NCNB's assets grew to $60 billion after it bought the failed First RepublicBank Corporation of Dallas, Texas from the FDIC.

The deal was brilliant and controversial. The FDIC contributed $4 billion and owned 80 percent of the new NCNB Texas National Bank. NCNB contributed just $210 million for 20 percent, with an exclusive option to buy the rest. Plus, NCNB got tax breaks worth billions—they could use First Republic's losses to offset future profits.

Critics howled about government subsidies. A congressional report later concluded that NCNB won not because it was the best buyer, but because its bid cost the FDIC the least—thanks to nearly $1 billion in projected tax savings. Texans grumbled that NCNB stood for "No Cash for No Body."

But McColl didn't care about popularity. Over the next few years, it acquired more than 200 thrifts and community banks, many through the Resolution Trust Corporation program. What had been a $7 billion North Carolina bank in 1983 was suddenly a $60 billion powerhouse. The Marine had taken the hill.

Creating NationsBank

The Texas deal gave McColl the ammunition for his next assault. In 1991, NCNB targeted C&S/Sovran, itself the product of a merger between Citizens & Southern of Atlanta and Sovran of Virginia. C&S/Sovran was nearly brought down by problem loans in the Washington, D.C./Northern Virginia market, and was all but forced to merge with NCNB to form NationsBank.

This created the largest bank in the Southeast, with assets of $118 billion. The name change was significant—no longer North Carolina National Bank, but NationsBank. McColl's ambition was right there in the name: to create America's first truly national bank.

The acquisition machine kept rolling: Maryland National Corporation (1992), Chicago Research and Trading Group (1993), BankSouth (1995), St. Louis-based Boatmen's Bancshares (1996), Jacksonville, Florida based Barnett Bank (1997). Each deal was bigger than the last. McColl had a ritual—he'd call the target CEO and give them hours to respond before, as he told one target, "I launch my missiles."

A survey of 1,500 bank CEOs ranked NationsBank as the No. 1 acquirer to avoid. But McColl's strategy wasn't about making friends. It was about survival through scale. As he said repeatedly: "Every time I say that people don't believe that I really mean it. But I do. Survive."

By 1997, NationsBank was ready for its ultimate conquest. But this time, the target wouldn't be some troubled regional bank. This time, McColl set his sights on American banking royalty: Bank of America itself. The hunter from Charlotte was about to swallow the wounded giant of San Francisco.

V. The Mega-Merger: NationsBank Acquires BankAmerica (1998)

The Phone Call That Changed Banking

The deal was closed much faster than anyone expected. In March 1998, McColl called David Coulter, CEO of BankAmerica. The timing was perfect—or perfectly terrible, depending on your perspective. BankAmerica, as it was then known, was acquired by the Charlotte-based NationsBank for $62 billion. after suffering significant loss during the 1998 Russian financial crisis.

The Russian crisis had been brutal. BankAmerica Corp. said Friday its trading losses have reached $220 million so far this quarter, due largely to the volatility in global financial markets But this was just the visible wound. Behind the scenes, BankAmerica was bleeding from a disastrous investment in D.E. Shaw & Co., the hedge fund that had imploded in the Russian meltdown.

The Art of the Deal

The negotiations moved at breakneck speed. An Agreement and Plan of Reorganization, dated as of April 10, 1998 was signed just weeks after that first phone call. The terms were telling: BankAmerica shareholders will receive 1.1316 shares of the combined company for each BankAmerica share they own just before the merger.

This wasn't a merger of equals, despite the public positioning. Although NationsBank was the nominal survivor, the merged bank took the better-known Bank of America name It was a brilliant PR move—keep the prestigious name while maintaining control. However, to this day it is headquartered in Charlotte at what is now Bank of America Corporate Center, and retains NCNB/NationsBank's pre-1998 stock price history.

The numbers were staggering: NationsBank Corp. and BankAmerica Corp. completed their merger Wednesday to create the country's largest bank: a coast-to-coast, $572-billion-asset institution that holds $1 of every $12 of the country's banking deposits.

Power Politics

Behind the scenes, the merger was pure McColl. McColl became chairman and CEO of the merged company with Bank of America's David Coulter as president, but Coulter was quickly forced out in favor of NationsBank executive Ken Lewis. This wasn't partnership—it was conquest.

The board composition revealed the true power dynamics: the board consists of 11 directors of NationsBank and 9 directors of BankAmerica. McColl had control from day one. Florida's importance diminished further—The board includes 11 directors from NationsBank, nine from BankAmerica, but none from the former Barnett. Of the four Barnett directors who joined NationsBank's board last year... none were invited to remain.

The integration was ruthless efficiency. NationsBank's culture—aggressive, sales-driven, focused on cross-selling—overwhelmed BankAmerica's more traditional banking approach. Branch managers who had spent decades building relationships were suddenly measured on product quotas. The California establishment watched in horror as their genteel bank was transformed into McColl's war machine.

This union created a bank with assets of $ 570 billion and extensive network of 4800 branches. From sea to shining sea, Bank of America now touched 30 million, or one of three, American households and more than 85 percent of the Fortune 500 businesses.

VI. The Empire Strikes Back: Countrywide and the Lead-Up to Crisis (2004–2007)

The Changing of the Guard

In 2001, McColl handed his remaining posts to Lewis, who began his career at NCNB in 1969. Ken Lewis inherited an empire, but empires demand constant expansion. The early 2000s brought new challenges: the tech bubble burst, interest rates plummeted, and traditional banking margins compressed. Lewis needed growth, and mortgages were booming.

During the period 2004–2007, the Bank of America bought FleetBoston Financial for $47 billion, credit card giant MBNA for $35 billion, US Trust for $3.3 billion, and LaSalle Bank for $21 billion. Each deal made Bank of America bigger, but size alone wasn't enough. The real action was in mortgages, where exotic products and soaring home prices created seemingly endless profits.

The Countrywide Courtship

Angelo Mozilo had built Countrywide Financial into America's mortgage machine. In 2006, Countrywide financed 20% of all mortgages in the United States, at a value of about 3.5% of the United States GDP, a proportion greater than any other single mortgage lender. Mozilo was everything Lewis wasn't—brash, bronzed, unapologetically aggressive. But he had what Lewis wanted: market share.

The warning signs were everywhere. Countrywide's business model depended on originating mortgages and immediately selling them to investors. When the music stopped, they'd be left holding the bag. From 2005 to 2007, Angelo R. Mozilo sold much of his CFC stock realizing $291.5 million in profits. If the CEO was cashing out, what did he know that Lewis didn't?

The August 2007 Lifeline

By summer 2007, the subprime crisis was spreading like wildfire. On November 26, 2007, Countrywide stock was hammered on the NYSE, dropping over 10% to a level of $8.64/share; less than half the share's value in August when the firm faced bankruptcy rumors and a fraction of its value in 2006.

Bank of America threw Countrywide a lifeline in August 2007, investing $2 billion for a 16% stake. Lewis saw opportunity where others saw disaster. This was classic Bank of America strategy—buy distressed assets, integrate them into the machine, extract synergies. It had worked with First Republic in Texas, with troubled banks throughout the Southeast. Why not with Countrywide?

The Fatal Attraction

On January 11, 2008 Countrywide Financial Corporation and Bank of America Corporation announced a business combination in which Countrywide would merge with a subsidiary of Bank of America. The deal terms seemed like a bargain: Bank of America said Friday it will buy Countrywide Financial for $4.1 billion in stock

The rationalization was seductive. The purchase will make Bank of America the nation's largest mortgage lender and loan servicer. In one stroke, Lewis would dominate American home lending. Bank of America expects $670 million in after-tax cost savings in the transaction, or 11 percent of the expense base of the two companies' mortgage operations.

But the critics were howling. "At that point, Bank of America should have stepped back and either renegotiated the deal or cancelled the deal." States were already suing Countrywide for predatory lending. The portfolio was toxic, filled with no-documentation loans, negative amortization mortgages, and borrowers who never had a prayer of repaying.

What They Didn't Know Could Kill Them

On July 1, 2008, Bank of America Corporation completed its purchase of Countrywide Financial Corporation. Almost immediately, the horror became clear. Once the acquisition went through, Bank of America began pouring over Countrywide's books, and it was in for a rude shock. It turned out that the problems were much worse than anyone had suspected. Many of Countrywide's loans had gone to people who couldn't afford them, and with the housing market in turmoil, a flood of foreclosures was coming its way.

The timing couldn't have been worse. Lehman Brothers was wobbling, credit markets were freezing, and Bank of America had just swallowed a company that epitomized everything wrong with American mortgages. "That's when Bank of America recognized that they had purchased a mess."

VII. The Financial Crisis: Merrill Lynch and Near-Death Experience (2008–2009)

September 2008: 48 Hours That Changed Everything

On Friday, September 12, 2008, Ken Lewis was preparing for what he thought would be a quiet weekend. Lehman Brothers was clearly failing, but that was Dick Fuld's problem, not his. Then his phone rang. It was the Federal Reserve. Lehman was going down, and Merrill Lynch was next.

What followed was one of the most dramatic weekends in financial history. While Lehman's executives desperately searched for a buyer in their gleaming Times Square tower, Ken Lewis was secretly negotiating to buy Merrill Lynch. The thundering herd was about to be corralled by a bank from Charlotte.

The negotiations were surreal. John Thain, Merrill's CEO, knew he had hours, not days. If markets opened Monday without a deal, Merrill would face a run that would make Bear Stearns look orderly. Lewis knew it too. This wasn't a negotiation—it was a hostage situation where both parties held guns.

The Sunday Night Special

By Sunday evening, September 14, they had a deal. Bank of America would acquire Merrill Lynch for $50 billion, or $29 per share—a 70% premium to Friday's close. It was either insanely generous or desperately necessary, depending on your perspective. The agreement was announced just hours before Lehman filed for bankruptcy, the largest in American history.

The initial reaction was relief, even admiration. Lewis had saved Merrill Lynch, prevented systemic collapse, and acquired the world's largest brokerage force in one bold stroke. Bank of America would now dominate retail banking, commercial lending, and wealth management. It was the universal bank model taken to its logical extreme.

The December Disaster

But as Bank of America's executives dug into Merrill's books in late November and December, they discovered a nightmare. Merrill's trading positions were hemorrhaging money at an unprecedented rate. The losses weren't just bad—they were catastrophic, potentially fatal to Bank of America itself.

The numbers were staggering and getting worse by the day. Losses that were projected at $5.3 billion in November had ballooned to over $12 billion by mid-December. Lewis faced an impossible choice: complete the merger and potentially destroy Bank of America, or walk away and trigger a systemic crisis.

The MAC Clause Drama

Lewis decided to play the one card he had: the Material Adverse Change clause. In mid-December, he called Treasury Secretary Hank Paulson and Fed Chairman Ben Bernanke. His message was blunt: Merrill's losses were so severe that they triggered the MAC clause. Bank of America would walk away unless the government provided support.

What happened next depends on whom you believe. Lewis claimed that Paulson and Bernanke threatened to fire him and his entire board if he invoked the MAC clause. The regulators said they merely expressed "strong views" about systemic risk. Either way, the message was clear: you will complete this merger.

The Secret Bailout

The solution was unprecedented. On January 16, 2009—two weeks after the merger closed—the government announced a massive rescue package. Bank of America would receive $20 billion in additional TARP funds on top of the $25 billion it had already received. More importantly, the government would guarantee $118 billion of toxic assets, absorbing 90% of losses beyond the first $10 billion.

Think about that: the government essentially provided catastrophic insurance on a portfolio twice the size of Bank of America's entire tangible equity. Without this backdoor bailout, Bank of America might have collapsed, taking the entire financial system with it.

The Price of Salvation

By the end of 2009, Bank of America had repaid the $45 billion in TARP funds, desperate to escape government control and compensation restrictions. But the true cost went far beyond the explicit bailouts. The bank's stock price had collapsed from $45 in 2007 to under $3 in early 2009. Shareholders who had owned the stock before the crisis had lost 93% of their investment.

Lewis himself became a casualty. Under intense pressure from shareholders and regulators, he announced his retirement in September 2009. The man who had dreamed of building America's greatest bank had instead presided over its near-destruction. The Countrywide debacle was one of the big reasons why Ken Lewis was forced out of office - that and the controversial acquisition of Merrell Lynch.

VIII. The Reckoning: Legal Battles and Settlements (2010–2014)

The Bill Comes Due

If 2008-2009 was about survival, 2010-2014 was about accountability. Every regulator, every state attorney general, every class-action lawyer in America wanted their pound of flesh from Bank of America. The charges were serious: predatory lending, securities fraud, foreclosure abuses, money laundering. The bank that had been too big to fail was now too big to jail, but not too big to fine.

The numbers were astronomical. Settlement after settlement, billion after billion. Each one came with Bank of America neither admitting nor denying wrongdoing, the corporate equivalent of a no-contest plea. But the dollars told the real story.

The Record-Breaking Settlement

The crescendo came in August 2014: a $16.65 billion settlement with the Department of Justice, the largest civil settlement with a single entity in American history. The breakdown was telling: $5 billion in penalties, $7 billion in consumer relief, $4.6 billion to other agencies. Most of the conduct being punished wasn't even Bank of America's—it was Countrywide's and Merrill Lynch's.

This was the cruel irony of acquisition. Bank of America was paying billions for the sins of companies it had tried to save. Every toxic mortgage Countrywide had originated, every misleading security Merrill had sold—now they all belonged to Bank of America.

The Total Tally

By 2014, the total settlements exceeded $70 billion. To put that in perspective, that's more than Bank of America's entire market capitalization at the depths of the crisis. The bank had essentially paid for Countrywide and Merrill Lynch twice—once to acquire them, and again in legal settlements.

The human cost was equally staggering. Tens of thousands of employees lost their jobs. Millions of shareholders saw their investments evaporate. Communities across America dealt with foreclosed homes and abandoned properties. The damage rippled through the entire economy.

IX. The Moynihan Era: Simplification and Digital Transformation (2010–Present)

The Cleanup Man

Brian Moynihan became CEO on January 1, 2010, inheriting a bank that was less a coherent institution than a collection of barely integrated acquisitions held together by federal life support. A Boston native who had joined Fleet before its acquisition by Bank of America, Moynihan was the anti-McColl: understated, analytical, focused on operations over acquisitions.

His strategy was radical in its simplicity: no more acquisitions, no more complexity, no more betting the bank. "During 2003 to 2008, our company acquired six major acquisitions — 200,000 employees to add to the 133,000 we started with," Moynihan explained. "That added a lot of complexity."

Project New BAC

Moynihan launched "Project New BAC"—a massive simplification initiative. The bank would exit 40 countries, shut down half its data centers, eliminate overlapping systems, and reduce headcount by 30,000. This wasn't growth through acquisition; it was profitability through subtraction.

The mortgage business—once Ken Lewis's crown jewel—was essentially put in runoff. Proprietary trading was eliminated. The bank sold its international credit card businesses, its private equity portfolios, even its stake in China Construction Bank. Everything that wasn't core retail, commercial, or wealth management had to go.

The Digital Revolution

While shrinking physically, Bank of America was expanding digitally at an unprecedented pace. By 2015, more customers were depositing checks through their phones than in branches. Digital sales exceeded branch sales for the first time in 2017. The bank that Giannini built on personal relationships was becoming an app on your phone.

The crown jewel was Erica, an AI-powered virtual assistant launched in 2018. Within five years, Erica had over 32 million users and had handled over 1.5 billion client interactions. This wasn't your father's Bank of America—it was barely even a bank in the traditional sense.

Warren Buffett's Vote of Confidence

The transformation gained credibility in August 2011 when Warren Buffett invested $5 billion in Bank of America preferred stock. The Oracle of Omaha's investment was more than money—it was validation. If Buffett believed in Moynihan's strategy, maybe the market should too.

The investment proved brilliantly timed. Bank of America's stock rose from $7 to over $40 by 2018. Buffett's $5 billion investment grew to be worth over $30 billion. More importantly, it marked the moment Bank of America transformed from crisis survivor to market leader.

The New Bank of America

Today's Bank of America would be unrecognizable to Giannini, McColl, or even Lewis. It's the second-largest bank in America with $3.2 trillion in assets, but it rarely makes acquisitions. It has 66 million consumer and small business clients, but they increasingly never set foot in a branch. It employs 213,000 people, down from over 280,000 at its peak.

The numbers tell the story of transformation: 37 million digital banking users, 29 million mobile users, over $300 billion in mobile check deposits annually. Physical branches have declined from 6,100 in 2009 to under 4,000 today. Yet customer satisfaction is at record highs. The bank is doing more with less—the opposite of the acquisition-driven growth model that built it.

X. Playbook: Business & Investing Lessons

The Power of Serving Underserved Markets

Giannini's original insight remains profound: serving customers that others ignore can build an empire. He didn't compete with existing banks for wealthy clients; he created an entirely new market. Every immigrant with $25 to deposit was a future homeowner, business owner, wealth creator. The lesson: the biggest opportunities often lie where established players refuse to look.

Serial Acquirer Strategy: The Double-Edged Sword

McColl proved you could build a national champion through relentless acquisition. But Lewis proved the strategy's limits. Acquisitions work when you're buying weakness during distress (First Republic, C&S/Sovran) but fail when you're buying strength at peaks (Countrywide, Merrill Lynch). The price you pay matters more than the asset you're buying.

The Dangers of Buying at the Peak

Countrywide and Merrill Lynch weren't bad businesses—they were great businesses bought at the worst possible moment. Lewis paid $4.1 billion for Countrywide in 2008; the legal settlements alone exceeded $40 billion. He paid $50 billion for Merrill Lynch; it nearly destroyed Bank of America. Timing isn't everything, but in M&A, it's close.

Crisis Management and Government Relations

When crisis hits, government relations matter more than customer relations. Bank of America survived 2008 not because it was well-run but because it was too big to fail. The lesson is uncomfortable but undeniable: in modern finance, political capital is as important as financial capital.

The Importance of Integration

Culture eats strategy for breakfast, and nowhere is this truer than in bank mergers. NationsBank's aggressive sales culture overwhelmed BankAmerica's relationship approach. Countrywide's origination culture poisoned Bank of America's credit discipline. You're not just buying assets and liabilities—you're buying behaviors, incentives, and assumptions.

Building vs. Buying in Financial Services

Moynihan's success came from building digital capabilities, not buying them. While competitors acquired fintech startups, Bank of America built Erica internally. The result: better integration, lower cost, complete control. Sometimes the best acquisition is the one you don't make.

The "Too Big to Fail" Moral Hazard

Bank of America's story embodies the central problem of modern banking: heads the bank wins, tails the taxpayers lose. The ability to privatize gains while socializing losses creates incentives for excessive risk-taking. Until this asymmetry is resolved, financial crises will remain inevitable.

XI. Analysis & Bear vs. Bull Case

The Bull Case

Bank of America trades at a significant discount to JPMorgan Chase despite similar returns on equity. The digital transformation is paying off with industry-leading efficiency ratios. Rising interest rates benefit Bank of America more than peers due to its massive deposit base. The wealth management franchise, bolstered by Merrill Lynch, generates stable, high-margin revenues.

The bank's sensitivity to economic growth makes it a leveraged play on American prosperity. Every 100 basis point increase in rates adds billions to net interest income. The consumer franchise is unmatched in breadth and depth. Credit quality remains strong with charge-offs below historical averages.

The Bear Case

Bank of America remains dangerously exposed to economic cycles. A recession would hit every business line simultaneously: loan losses in commercial, defaults in consumer, market losses in trading, asset declines in wealth management. The bank's size makes it impossible to pivot quickly.

Regulatory requirements keep getting tighter. Capital requirements, stress tests, living wills—all constrain returns. The branch network, while shrinking, remains a massive fixed cost. Fintech competitors cherry-pick profitable products without the regulatory burden. The brand, tainted by the crisis, lacks the prestige of JPMorgan or Goldman Sachs.

The Verdict

Bank of America is a paradox: a growth story built on shrinkage, a technology company trapped in a bank's body, a national champion that might be worth more in pieces. It's simultaneously too big to fail and too big to succeed spectacularly. The transformation under Moynihan has been remarkable, but the question remains whether any bank this size can generate superior returns in a world of increasing regulation and technological disruption.

XII. Epilogue & "If We Were CEOs"

The Unfinished Transformation

If we were running Bank of America, the first recognition would be that the universal banking model is under assault from every direction. Fintechs attack specific products with better user experience. Investment banks poach the best talent. Regulators impose costs that niche players avoid. The response can't be incremental—it must be revolutionary.

The branch network needs more radical surgery. Why maintain 4,000 branches when 500 would suffice? Convert branches into advisory centers for complex products, not transaction processing centers. The savings could fund massive technology investments or be returned to shareholders.

The investment banking operation needs a decision: commit or quit. Bank of America will never out-Goldman Goldman Sachs with half-measures. Either pay up for top talent and accept lower returns, or exit and focus on commercial banking where scale matters.

The ESG Opportunity

Climate finance represents the next frontier. Bank of America has committed $1.5 trillion to sustainable finance by 2030, but this could be even bolder. Become the definitive bank for the energy transition. Finance every solar farm, wind project, and electric vehicle factory. Own the future, not the past.

The Acquisition Question

Despite Moynihan's success with organic growth, one acquisition might make sense: a pure-play digital bank. Not to integrate, but to run separately as a laboratory for innovation. Let it cannibalize the parent. Better to disrupt yourself than be disrupted.

Final Reflections

Bank of America's 120-year journey from Giannini's Bank of Italy to Moynihan's digital colossus is American capitalism in microcosm. It shows how serving ordinary people can build extraordinary institutions. How ambition can create empires and hubris can destroy them. How innovation and tradition, growth and discipline, must be balanced.

The bank that exists today contains DNA from Giannini's populist vision, McColl's imperial ambition, and Lewis's tragic overreach. It's been saved by taxpayers, sued by regulators, and transformed by technology. It's both a triumph and a cautionary tale.

Looking forward, Bank of America faces the same existential question as all incumbent giants: can you disrupt yourself before others disrupt you? Can you maintain the advantages of scale while achieving the agility of startups? Can you serve shareholders, customers, employees, and society simultaneously?

The answer will determine not just Bank of America's future, but the future of banking itself. Because if a bank with $3 trillion in assets, 66 million customers, and 200,000 employees can't adapt and thrive, what hope is there for the rest? The next chapter of this story hasn't been written, but one thing is certain: it will be as dramatic as everything that came before.

In the end, Bank of America's story is America's story—ambitious, flawed, resilient, and always reinventing itself. From Giannini's fruit crates full of gold to Erica's billions of digital interactions, from the rubble of San Francisco to the towers of Charlotte, from serving immigrants to serving everyone, this is what American finance looks like: messy, magnificent, and perpetually unfinished.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube