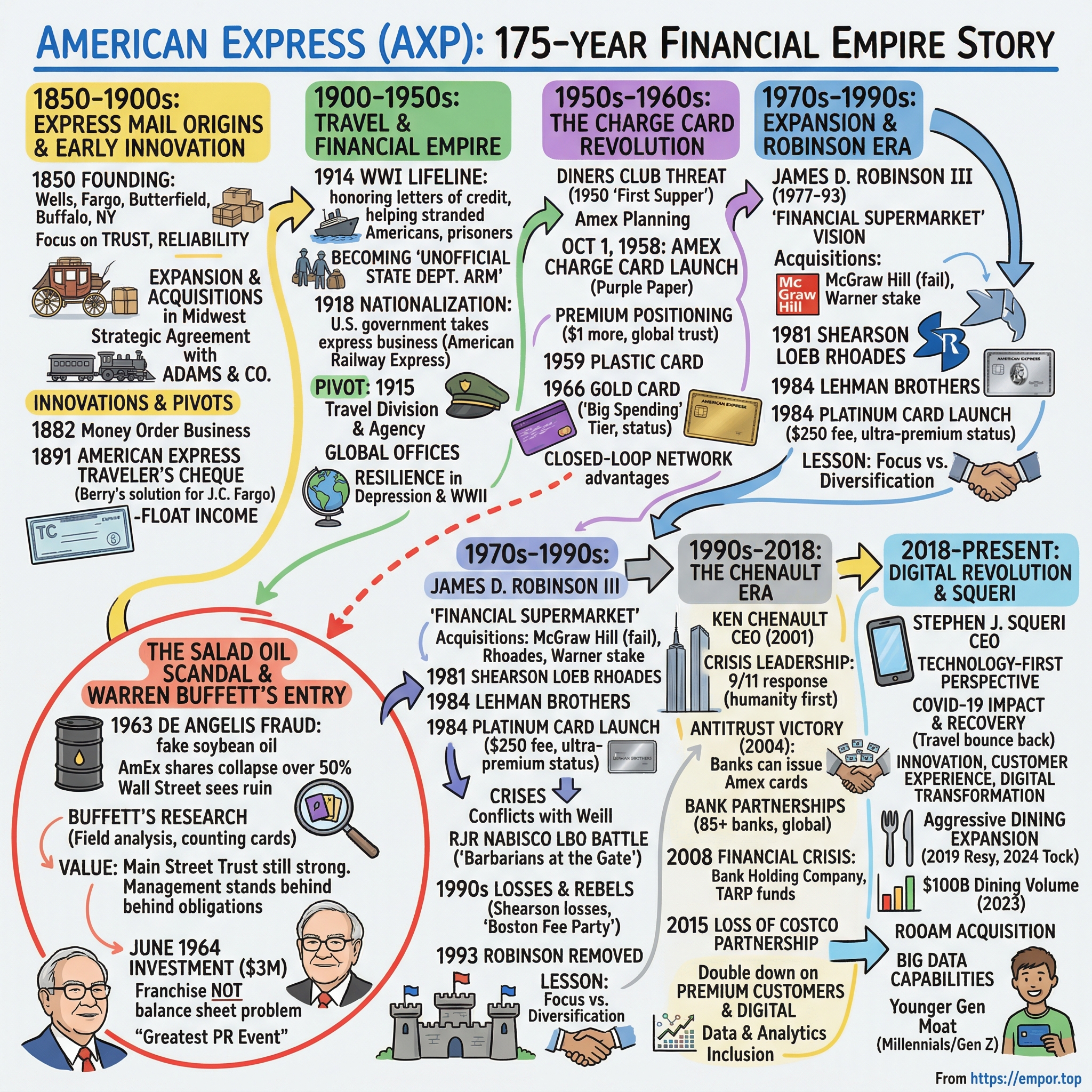

American Express: The Story of a 175-Year Financial Empire

I. Introduction & Episode Roadmap

Picture this: It's 1964, and a young investor from Omaha walks into a steakhouse in midtown Manhattan. He's not there for the porterhouse. Instead, he's watching carefully as diners pull out their wallets to pay. One card appears again and again—a purple piece of plastic that seems to command respect from both cardholders and waitstaff. That investor was Warren Buffett, and he was conducting field research on what would become his longest-held equity position: American Express.

Today, American Express stands as the fourth-largest card network globally by purchase volume, trailing only China UnionPay, Visa, and Mastercard. With 141.2 million cards in force worldwide as of December 31, 2023, and an average annual spend per card member of $24,059, the company processes over $1.7 trillion in purchase volume annually. It's a bank holding company and multinational financial services corporation that has somehow maintained premium positioning in an increasingly commoditized payments world.

But here's the fascinating part: American Express didn't start as a financial services company at all. It began as a freight forwarding business in Buffalo, New York, moving packages across the American frontier. The question that drives our story today is deceptively simple yet profound: How did a company that started by moving mail and packages transform into a financial services powerhouse that Warren Buffett has refused to sell for over six decades?

This is a story about survival, reinvention, and the raw power of brand equity. It's about building network effects before Silicon Valley coined the term, about creating premium positioning in markets that naturally trend toward commoditization, and about navigating existential crises that would have killed lesser companies. From the express mail routes of the 1850s to the travelers cheques that revolutionized global commerce, from the charge card battles of the 1960s to today's digital payments ecosystem—American Express has consistently found ways to extract extraordinary value from what others saw as ordinary transactions.

The themes we'll explore resonate far beyond payments: How do you build a brand so powerful that customers pay more for the privilege of using it? How do you create network effects in a closed-loop system while competing against open networks? And perhaps most intriguingly, what did Warren Buffett see in 1964 that made him bet big on a company facing potential bankruptcy—and why has he never sold a single share?

II. The Express Mail Origins & Early Innovation (1850-1900)

The year was 1850, and America was exploding westward. The California Gold Rush had begun just two years earlier, railroads were stretching across the continent like iron arteries, and fortunes were being made—and lost—at unprecedented speed. In Buffalo, New York, three men saw opportunity in the chaos. Henry Wells, William G. Fargo, and John Warren Butterfield weren't prospectors or railroad barons. They were logistics men who understood a fundamental truth: in a rapidly expanding nation, whoever controlled the flow of goods, money, and information would hold enormous power. On March 18, 1850, three express companies merged in Buffalo to create the American Express Company, a joint-stock company with initial capital of $150,000. The consolidation brought together Livingston, Fargo & Company (formerly Western Express), founded in 1845 by Henry Wells and William G. Fargo; Wells & Co., cofounded by Wells in 1846; and Butterfield & Wasson, founded by John Butterfield and James D. Wasson. Wells was elected the new company's first president; Fargo became vice-president.

The genius of this merger wasn't just in eliminating "wasteful competition," as the founders put it. It was in recognizing that in the express business—moving valuable goods, money, and documents across vast distances—trust and reliability mattered more than speed or price. Under Wells's leadership American Express was immediately and unexpectedly profitable, expanding rapidly and acquiring small competitors in the Midwest, negotiating contracts with the first railroads, and running packet boats on the Illinois Canal.

Within a year, American Express had engineered what would become a recurring pattern in its history: transforming competitive threats into strategic advantages. In 1851, American Express reached an amicable agreement with its major rival, Adams & Company. American Express was to expand north and west of New York while Adams was free to grow south and east. This agreement was kept and renewed over the next 70 years, essentially creating geographic monopolies that allowed both companies to prosper without destructive price wars.

But the real foreshadowing of American Express's future came in 1852, when a disagreement over western expansion would create one of business history's great ironies. When Wells proposed his old dream of a transcontinental express service to the American Express board of directors, they rejected his idea. But in 1852 Wells and Fargo got the board's blessing to launch an independent venture, Wells Fargo & Company, to provide express and banking services in California. The board's conservatism in refusing to expand to California—driven largely by Butterfield's objections—led Wells and Fargo to create what would become American Express's greatest competitor in financial services over a century later. The company's first major pivot into financial services came in 1857, seven years after its founding. American Express started its expansion in the area of financial services by launching a money order business to compete with the United States Post Office's money orders. This wasn't just an incremental business extension—it was a fundamental recognition that moving money could be more profitable than moving packages. The U.S. Postal Service had introduced money orders in 1864, but they had a critical flaw: their face value could be altered without detection. American Express employee Marcellus Berry designed a safer money order that was also more readily available than the postal version. The money order provided a new source of revenue to American Express, with more than 250,000 issued in the first year.

By the end of the Civil War, American Express had flourished to such an extent that it operated some 900 offices in 10 states. But success bred competition. Merchants Union Express Company formed in 1866, and for two years the companies engaged in cutthroat competition. On the verge of financial exhaustion, they finally merged on November 25, 1868, to form the American Merchants Union Express Company, with Fargo succeeding Wells as president. The company was renamed American Express Company in 1873.

The story that would define American Express's transformation from express company to global financial services giant began sometime between 1888 and 1890. J. C. Fargo took a trip to Europe and returned frustrated and infuriated. Despite the fact that he was president of American Express and that he carried with him traditional letters of credit, he found it difficult to obtain cash anywhere except in major cities. Fargo went to Marcellus Flemming Berry and asked him to create a better solution than the letter of credit.

Berry's solution was revolutionary in its simplicity. Berry introduced the American Express Traveler's Cheque which was launched in 1891 in denominations of $10, $20, $50, and $100. The traveler's cheque solved multiple problems at once: it was safer than carrying cash, more convenient than letters of credit, and—crucially—it generated float income for American Express as customers paid for cheques they wouldn't cash for weeks or months. Within ten years, its sales revenue from the instrument exceeded $6 million annually.

This innovation wasn't just about creating a new product. It was about recognizing that American Express's real asset wasn't its stagecoaches or express routes—it was trust. When someone bought a traveler's cheque in New York and cashed it in Paris, they were essentially betting that American Express would honor its obligations across continents and currencies. That trust, painstakingly built over four decades of reliable express service, would become the foundation of everything that followed.

III. Building the Travel & Financial Services Empire (1900-1950)

The dawn of the 20th century found American Express at a crossroads. The company had built a global network through its traveler's cheques, but it was the summer of 1914 that would transform it from a financial services provider into something more profound: a lifeline for Americans abroad.

In 1914, at the onset of World War I, American Express in Europe was among the few companies to honor the letters of credit (issued by various banks) held by Americans in Europe, because other financial institutions refused to assist these stranded travelers. Picture the scene: tens of thousands of American tourists trapped in Europe as war erupted, their money suddenly worthless, banks shuttering, and panic spreading. While other financial institutions turned their backs, American Express offices from London to Rome stayed open, converting letters of credit into cash, arranging emergency passage home, and essentially becoming an unofficial arm of the U.S. State Department.

This moment crystallized what would become American Express's defining characteristic: being there when customers needed them most. The British government appointed American Express its official agent at the beginning of World War I. They were to deliver letters, money, and relief parcels to British prisoners of war. Their employees went into camps to cash drafts for both British and French prisoners and arranged for them to receive money from home. By the end of the war they were delivering 150 tonnes of parcels per day to prisoners in six countries.

The war years also forced a fundamental transformation of the business. During the winter of 1917, the United States suffered a severe coal shortage and on December 26 President Woodrow Wilson commandeered the railroads on behalf of the United States government to move federal troops, their supplies, and coal. Treasury Secretary William Gibbs McAdoo was assigned the task of consolidating the railway lines for the war effort. All contracts between express companies and railroads were nullified and McAdoo proposed that all existing express companies be consolidated into a single company to serve the country's needs. This ended American Express's express business and removed them from the ICC's interest. The result was that a new company called the American Railway Express Agency formed in July 1918. The new entity took custody of all the pooled equipment and property of existing express companies (the largest share of which, 40%, came from American Express, who had owned the rights to the express business over 71,280 miles (114,710 km) of railroad lines, and had 10,000 offices, with over 30,000 employees).

In a single stroke, American Express lost the business it had been founded on. But rather than collapse, the company pivoted with remarkable agility. In 1915, American Express established a travel division and soon established its first travel agency. The timing was prescient—just as the express business was being nationalized, American Express was already building what would become the world's largest travel services company.

Under the leadership of George Chadbourne Taylor, who became president in 1914, American Express embraced its new identity. At the end of the Wells–Fargo reign in 1914, an aggressive new president, George Chadbourne Taylor (1868–1923), who had worked his way up through the company over the previous thirty years, decided to build a new headquarters. The old buildings, dubbed by The New York Times as "among the ancient landmarks" of lower Broadway, were inadequate for such a rapidly expanding concern. After some delays due to the First World War, the 21-story neo-classical American Express Co. Building was constructed in 1916–17 to the design of J. Lawrence Aspinwall, of the firm of Renwick, Aspinwall & Tucker, the successor to the architectural practice of James Renwick Jr. The building consolidated the two lots of the former buildings with a single address: 65 Broadway.

The interwar years saw explosive growth in both travelers cheques and the travel business. By the 1920s, American Express offices dotted the globe—from Shanghai to Buenos Aires, from Cairo to Stockholm. The company wasn't just facilitating travel; it was creating the infrastructure for the first age of mass tourism. American Express travel offices became embassies of American capitalism, places where a traveler could cash a cheque, book a steamship ticket, receive mail from home, and get advice on local customs.

The Great Depression tested this model but didn't break it. While international travel plummeted, American Express's financial services—particularly money orders and travelers cheques—proved remarkably resilient. Americans might not be traveling to Paris, but they were still sending money to relatives, paying bills, and conducting the mundane financial transactions that kept the economy moving.

World War II brought another existential challenge and another transformation. Once again, American Express offices became lifelines—this time not just for stranded tourists but for millions of American servicemen. The company's global network, built to serve travelers, pivoted to serve the greatest mobilization in American history. From processing military money orders to facilitating correspondence between soldiers and their families, American Express became an essential part of the war effort.

By 1950, American Express had completed a remarkable evolution. What began as an express company had become a global financial services and travel conglomerate with assets approaching $100 million. The company's travelers cheques were accepted in over 100 countries, its travel offices spanned the globe, and its brand had become synonymous with reliability and prestige. But the biggest revolution was yet to come. American Express executives discussed the possibility of launching a travel charge card as early as 1946, but it was not until Diners Club launched a card in March 1950, that American Express would be forced to confront its next great transformation.

IV. The Charge Card Revolution & Competing with Diners (1950s-1960s)

February 8, 1950. Frank McNamara returned to Major's Cabin Grill in Manhattan with his partner Ralph Schneider. When the bill arrived, McNamara paid with a small cardboard card. This event, dubbed "The First Supper," would ignite a revolution that forced American Express to confront its most fundamental transformation yet.

In 1949, businessman Frank McNamara forgot his wallet while dining out at a New York City restaurant. It was an embarrassment he resolved never to face again. Luckily, his wife rescued him and paid the tab. February 1950. McNamara returned to Major's Cabin Grill with his partner Ralph Schneider. When the bill arrived, McNamara paid with a small cardboard card, known today as a Diners Club® Card. This event was hailed as the "First Supper," paving the way for the world's first multipurpose charge card.

The genius of Diners Club wasn't just the convenience—it was the business model. At the time, the company was charging participating establishments 7% and billed cardholders $5 a year. This dual revenue stream—merchant fees plus annual cardholder fees—created a powerful economic engine. When the card was first introduced, Diners Club listed 27 participating restaurants, and 200 of the founders' friends and acquaintances used it. Diners Club had 20,000 members by the end of 1950 and 42,000 by the end of 1951.At American Express headquarters, the success of Diners Club created what one executive later called "seven years of watching and worrying." American Express executives discussed the possibility of launching a travel charge card as early as 1946, but it was not until Diners Club launched a card in March 1950, that American Express began serious planning. The company had everything it needed—a global brand, millions of travelers cheque customers, relationships with merchants worldwide—except the conviction to move.

The delay was costly but instructive. By watching Diners Club's mistakes and successes, American Express learned crucial lessons: the importance of rapid merchant acquisition, the value of prestige positioning, and the critical need for operational excellence in processing transactions. When American Express finally moved, it moved decisively.

On October 1, 1958, American Express launched its charge card in the U.S. and Canada. The strategy was brilliant in its simplicity: position above Diners Club from day one. The card was launched with an annual fee of $6, $1 higher than Diners Club, to be seen as a premium product. Made of paper, the original American Express Card was purple to match our Travelers Cheque. By October 1, 1958, the official launch date, we had issued 250,000 cards and had 17,500 establishments signed on to accept them.

The purple paper card might have seemed primitive, but it represented something profound: American Express wasn't just entering the charge card business; it was redefining it. Where Diners Club sold convenience, American Express sold status. Where Diners Club promised acceptance at restaurants, American Express promised global reach through its existing network of travel offices and relationships.

In May 1959, we became the first major issuer to introduce a plastic card. The embossed plastic card was much more durable and also enabled us to take advantage of a new technology: imprinters that mechanically transferred the Card Member's number, name and address from the card to the record of charge. This wasn't just a material upgrade—it was a statement that American Express was here to stay and to lead.

The real masterstroke came in 1966, when American Express introduced the Gold Card for "big-spending members." This wasn't just product segmentation; it was the creation of a status hierarchy within the card itself. Suddenly, having an American Express card wasn't enough—you wanted the Gold Card. This innovation would prove far more valuable than anyone imagined, creating a premium tier that competitors would struggle to match for decades.

The battle between American Express and Diners Club in the 1960s established patterns that persist to this day. American Express's closed-loop network—where it controlled both the merchant relationships and the cardholder accounts—gave it advantages in data, customer service, and economics that the emerging bank card associations (which would become Visa and MasterCard) couldn't match. But it also created vulnerabilities: every merchant who didn't accept American Express was a potential lost customer, every bank that issued a competing card was a threat to the franchise.

By the end of the 1960s, American Express had effectively won the charge card war. Diners Club, which had 1.3 million cardholders by the mid-1960s, began to face intense competition not just from American Express but from banks that issued revolving credit cards through Bank of America's BankAmericard (later Visa) and Interbank Master Charge (later MasterCard). American Express, meanwhile, had built something more valuable than market share: it had built a brand that meant something, a closed-loop network that generated superior economics, and a customer base that valued prestige over price.

The charge card revolution wasn't just about replacing cash with plastic. It was about creating a new form of financial identity, where your card said something about who you were. And in that game, American Express had played its hand perfectly.

V. The Salad Oil Scandal & Warren Buffett's Entry (1963-1965)

November 19, 1963. Anthony "Tino" De Angelis's Allied Crude Vegetable Oil company filed for bankruptcy, and the dominoes began to fall. Within hours, it became clear that American Express was holding guarantees on what appeared to be $150 million worth of soybean oil that didn't exist. The stock market was about to open, and American Express shares were poised to collapse.

In 1963, Anthony De Angelis used Allied Crude Vegetable Oil Company's inventory as collateral for loans from more than 50 companies, including AmEx. De Angelis used these loans to drive up prices in the soybean oil market. The scheme was breathtaking in its audacity: Allied would store what it claimed was soybean oil in massive tanks in Bayonne, New Jersey. American Express's field warehousing subsidiary would inspect the tanks and issue warehouse receipts guaranteeing the oil's existence. Banks and finance companies would then loan money against these receipts.

The fraud was elegantly simple. To deceive inspectors, De Angelis employed various tactics: Filling tanks mostly with water, with only a thin layer of oil floating on top. Connecting tanks with pipes to transfer oil between them during inspections. What puzzled authorities about Amex's Field Warehousing operation was that De Angelis' soybean oil stock exceeded the stock available in the entire United States, according to the Department of Agriculture.

Eventually, a whistleblower came forward claiming that Allied was misleading AmEx by filling up oil tanks with water. When inspectors investigated more thoroughly, they found the water. A massive soybean oil futures crash ensued and wiped out the value of the loan collateral in minutes. On November 19, 1963, De Angelis' company filed for bankruptcy and investors found hundreds of millions of dollars in unaccounted funds. American Express stock dropped more than 50% as a result, which cost the company nearly $58 million. Between November 20 to December 2, its price dropped from $61.81 to $40.00 and would bottom on June 2, 1964, at $35.31, a drop of 43 percent in less than eight months since the scandal broke. Wall Street saw bankruptcy. The market saw ruin. Warren Buffett saw opportunity.

What led Buffett to swoop in and buy it at such a discount? The answer reveals everything about what makes a great investment. Buffett wondered what impact the scandal would have on Amex's reputation. With travelers cheques and credit cards, trust mattered. Buffett needed facts. So he and an acquaintance visited restaurants and other places that accepted Amex cards and cheques. They talked to bank tellers, bank officers, credit-card users, hotels employees, and restaurants workers to get a feel for whether usage had fallen off.

This wasn't desktop research or financial modeling—it was boots-on-the-ground intelligence gathering. Buffett would sit in restaurants and watch people pay their bills, counting how many pulled out American Express cards versus cash or competitors' cards. He'd chat with travel agents about whether customers still wanted American Express travelers cheques. He discovered something remarkable: while Wall Street was panicking about warehouse receipts and legal liabilities, Main Street customers didn't care. They still trusted the American Express brand.

Based on that research, Buffett concluded that while Wall Street had punished Amex by battering the stock price, Amex's reputation hadn't been tarnished on Main Street. The scandal was a balance sheet problem, not a franchise problem. And critically, American Express management was doing the right thing: they were standing behind the obligations of their subsidiary even though they likely had no legal requirement to do so.

Buffett sent a letter to Clark, praising management, and imploring them to settle for the sake of reputation. He understood what the market didn't: American Express's real asset wasn't its balance sheet or its field warehousing operation—it was trust. And by honoring obligations it didn't legally have to honor, management was protecting that trust.

By June 1964, he had invested $3 million in Amex, BPL's largest single holding, at 17 percent. The period when Buffett was buying Amex's stock was mid-April to June 1964. Its average price was $41.22. AMEX was a big position for the Buffett Partnership at once the stock started to appreciate it grew to 40% of the total portfolio. This wasn't just concentrated investing—it was betting the farm on a single insight: that a company's reputation, once earned, is remarkably resilient.

Two-and-a-half years later, Amex's stock was $92.50, a gain of 124 percent. By 1967, Amex negotiated a $60 million settlement with creditors. After-tax, that was $31.6 million. Profits between the time the scandal broke and the settlement exceeded that amount. The company had earned more than enough to pay for the scandal while the market was still pricing in bankruptcy. What makes this story remarkable isn't just the investment itself—it's what happened next. The first American Express trade was made in Q4 1998. The stake costed the investor $8.42 Billion, netting the investor a gain of 453% so far. As of September 29, 2022, Berkshire held 151,610,700 AmEx shares, or 20.29% of the total. Berkshire Hathaway hasn't purchased any American Express stock since the late 1990s, but its stake has continued to increase as a result of stock buybacks.

This is the power of what Buffett discovered in 1964: when you find a truly wonderful business, stick with it. American Express executives later realized the swindle was the greatest public-relations event in its history. Press coverage was favorable, and the public saw that Amex stood behind its obligations. The scandal that nearly destroyed the company actually strengthened its brand.

The Salad Oil Scandal marked a turning point not just for American Express but for Warren Buffett as an investor. Beginning with American Express, Buffett sought to uncover undervalued but fundamentally good businesses with capable managers, then let them do their jobs. This wasn't cigar-butt investing anymore—it was buying wonderful companies at fair prices, a philosophy that would define the next six decades of Buffett's career.

VI. Expansion & Transformation Under Robinson (1977-1993)

In 1977, James D. Robinson III became chairman and CEO of the company. Known to friends as "Jimmy Three Sticks" for the Roman numerals in his name, Robinson was a soft-spoken son of Georgia gentry who had followed a well-worn path to financial success: private school to Harvard MBA to Wall Street. But beneath the Southern gentility was a corporate warrior who believed American Express had grown complacent.

Robinson moved into the chief executive suites at American Express in 1977 after an internal power struggle that left him on top. He was eager to shake up a company with roots stretching back to before the Civil War. To Mr. Robinson, American Express had grown too complacent sticking with its flagship credit cards and traveler's checks and services. His vision was audacious: transform American Express into a comprehensive "financial supermarket" that ranged from boutique services for the wealthiest investors to credit cards and travel reservations.

The acquisition spree began almost immediately. Robinson made an unsuccessful bid in 1978 for the publishing company McGraw Hill, seeking to expand the Amex portfolio into media. He followed up by striking a deal with Warner Communications for a stake in emerging cable television systems. But these were just warm-ups for the main event.

In the 1980s, American Express embarked on an effort to become a financial services holding company and made several acquisitions, creating an investment banking arm. In mid-1981 it purchased Sanford I. Weill's Shearson Loeb Rhoades, the second-largest securities firm in the United States to form Shearson/American Express. With capital totaling $250 million at the time of its acquisition, Shearson Loeb Rhoades was the second-largest brokerage firm, behind Merrill Lynch. After the purchase of Shearson, Weill was given the position of president of American Express in 1983.

The Shearson acquisition was just the beginning. In 1984, American Express acquired the investment banking and trading firm, Lehman Brothers Kuhn Loeb, and added it to the Shearson family, creating Shearson Lehman/American Express. During his tenure, the American Express travel and charge-card empire expanded to include Shearson Lehman Hutton; First Data Corporation, a payments concern; Investors Diversified Services, a mutual fund company; and the Fireman's Fund Insurance Company.

But the crown jewel of Robinson's empire-building came with the 1984 launch of the Platinum Card. This wasn't just another tier of service—it was the creation of ultra-premium as a category. With a $250 annual fee (about $630 in today's dollars), 24-hour concierge service, travel insurance, and access to private clubs around the world, the Platinum Card redefined what a payment card could be. It wasn't about credit; it was about membership in an exclusive club.

The problem with empire-building is that empires require management, and by the late 1980s, cracks were showing. Weill grew increasingly unhappy with responsibilities within American Express and his conflicts with American Express' CEO James D. Robinson III. Weill soon realized that he was not positioned to be named CEO and after the firm's merger with Lehman Brothers Kuhn Loeb, Weill chose to resign from American Express in August 1985.

Robinson's biggest gamble—and ultimate undoing—came with the RJR Nabisco leveraged buyout battle. Mr. Robinson gave the green light to one of Amex's crown jewels, the newly merged investment firm Shearson Lehman Hutton, to back an RJR Nabisco management group seeking to take control. In the end, the company directors accepted a $109-a-share buyout deal with Kohlberg Kravis Roberts, valued at nearly $25 billion. The deal was chronicled in the bestselling book "Barbarians at the Gate," where Robinson was portrayed as out of his depth in the cutthroat world of 1980s takeovers.

By the early 1990s, the wheels were coming off. Shearson Lehman Brothers posted a jarring loss of $166 million for the last quarter of 1992, dragged down by tanking property investments and other ill-fated bets. The "Boston fee party" saw merchants revolting nationwide over the high cost of accepting American Express cards. The rebellion forced the company to cut its so-called discount rate—about 4 percent per transaction—to match that of its credit-card competitors, which were charging one-third as much.

Robinson was removed as chairman of American Express in late January 1993 after a messy battle with several of the company's outside directors, who argued that the company had suffered a string of financial reversals during his 15 years as chairman. He received a retirement package valued at about $10 million, substantial by any measure but far less than he had requested—including lifetime access to the corporate jet and an endowed chair at Harvard Business School in his name.

The Robinson era teaches a fundamental lesson about corporate strategy: diversification and focus are often at odds. Robinson's vision of a financial supermarket wasn't wrong—Citigroup would later prove the model could work—but it was wrong for American Express. The company's strength wasn't in being everything to everyone; it was in being something special to a select few. The charge card business, the travel services, the premium positioning—these weren't just products to be bundled with others. They were the essence of what made American Express unique.

VII. The Chenault Era & Modern Transformation (1993-2018)

Ken Chenault became CEO of American Express in 2001. When he was named AMEX chair, he became the third Black CEO of a Fortune 500 company. The timing could hardly have been worse—or more defining. Just nine months into his tenure, the September 11 attacks struck. American Express had to leave its headquarters temporarily because it was located directly opposite the World Trade Center and was damaged during the fall of the towers. The company lost 11 employees in the tragedy.

Chenault's response to 9/11 became a masterclass in crisis leadership. While other companies focused on financial losses, Chenault personally called the families of every American Express employee who died. He established a fund for the victims' families. He kept the company running smoothly despite the chaos, setting up temporary operations and ensuring no customer transactions were disrupted. Most importantly, he understood that in moments of crisis, leadership isn't about spreadsheets—it's about humanity.

The early 2000s brought another challenge that would define Chenault's tenure. Until 2004, Visa and Mastercard rules prohibited issuers of their cards from issuing American Express cards in the United States. These rules were struck down as a result of antitrust litigation brought by the United States Department of Justice. This was a watershed moment: suddenly, American Express could partner with banks that had previously been locked into exclusive relationships with Visa and MasterCard.

Chenault seized this opportunity with both hands. To further increase American Express's market share and profitability, Chenault led the company's campaign to build links with banks by allowing them to issue credit cards through American Express. Chenault subsequently secured partnerships with more than 85 banks in more than 90 countries by 2005. This wasn't just expansion—it was transformation. American Express was no longer just a closed-loop network; it was becoming a hybrid model that combined the best of both worlds.

Then came 2008. The financial crisis threatened to destroy everything Chenault had built. In 2008, amid a global credit crisis and a worldwide economic slowdown, the U.S. Federal Reserve System approved American Express's application to become a licensed bank holding company. Amex converted to a bank holding company during the 2008 financial crisis, enabling American Express to receive emergency financing from the TARP program. This wasn't just a regulatory change—it was a fundamental transformation of what American Express was.

But the real test of Chenault's leadership came with the loss of exclusive partnerships. American Express shares have struggled since the company ended its partnership with Costco Wholesale in February 2015. That co-branding partnership accounted for one in 10 Amex cards in circulation. The loss was devastating—not just financially, but symbolically. If American Express could lose Costco, what else might it lose?

Chenault's response was to double down on what made American Express unique. Rather than chase volume by lowering standards, he focused on premium customers and experiences. He invested heavily in the dining and travel ecosystem, understanding that American Express's real value wasn't in being everywhere—it was in being essential to the moments that mattered most to affluent customers.

The digital transformation under Chenault was less visible but equally important. While competitors focused on payments, American Express built a data and analytics capability that turned transaction information into customer insights. This wasn't just about fraud prevention—though American Express became industry-leading in that area. It was about understanding customers so well that American Express could anticipate their needs before they articulated them.

Chenault also understood something fundamental about brand value in the 21st century: it couldn't just be about exclusivity. It had to be about inclusion too. Under his leadership, American Express expanded its customer base while maintaining its premium positioning—a trick few brands have managed. He launched products for small businesses, for millennials, for international markets, all while maintaining the core promise of membership having its privileges.

After overseeing various initiatives that helped restore investors' confidence, Chenault announced in 2017 that he was stepping down as CEO. He left the following year and subsequently became chairman and managing director of General Catalyst Partners, a venture capital firm. In March 2020, he joined the board of Berkshire Hathaway, replacing Bill Gates—a fitting capstone to a career that began when Warren Buffett first bet on American Express during another existential crisis.

Chenault's 37-year career at American Express, including 17 years as CEO, transformed the company from a charge card issuer into a global payments and lifestyle brand. He navigated the dot-com bubble, 9/11, the financial crisis, and the digital revolution. He lost Costco but gained millions of new customers. He turned American Express from an American company that operated globally into a truly global company that happened to be headquartered in America.

VIII. The Digital Revolution & Squeri Leadership (2018-Present)

When Stephen J. Squeri took the helm as CEO and Chairman on February 1, 2018, he inherited a company at a crossroads. Squeri became chairman and CEO of American Express on February 1, 2018, having been appointed by the board of directors to succeed Kenneth Chenault. The Costco wound was still fresh, digital disruption was accelerating, and fintech startups were attacking every segment of the payments value chain. Squeri first joined American Express in 1985, becoming chief information officer in 2005 and vice chairman in 2015, along with other upper management roles.

Unlike his predecessors who came from traditional finance backgrounds, Squeri brought a technology-first perspective. Under Mr. Squeri's leadership, American Express has been strategically investing in its colleagues, premium customers, brand, and unique Membership model to drive the long-term success of the company. His 33 years at American Express before becoming CEO gave him an intimate understanding of the company's technology infrastructure and digital capabilities—knowledge that would prove essential in navigating the digital revolution.

The pandemic that struck in early 2020 could have been catastrophic for a company so dependent on travel and entertainment spending. Instead, it became a catalyst for transformation. While travel collapsed in the early months, American Express saw unprecedented resilience in its business model. "We don't see demand in the T & E categories declining significantly anytime soon based on the strength of future bookings coming through our consumer travel agency and the trends our partners in the travel industry like Delta are experiencing, particularly in the premium space."

By Q4 2021, the recovery was remarkable. In Q4 2021, global Card Member bookings made through American Express Travel were up 24% compared to 2019 and have continued to strengthen in 2022. The company's travel and entertainment spending reached 82% of 2019 levels by the end of 2021, with "When we looked at travel bookings in the fourth quarter, it was 24 percent up over 2019," said Steve Squeri during an earnings call on Tuesday. "When we look at the first couple of weeks in January, we're 44 percent up over 2019.

The digital transformation under Squeri accelerated dramatically during the pandemic. During his tenure, Amex has emphasized innovation, customer experience, and digital transformation. He has been responsible for introducing new products and services, deepening strategic partnerships, and propelling growth in global markets. American Express didn't just digitize existing processes—it reimagined what a card company could be in the digital age.

One of Squeri's most strategic moves has been the aggressive expansion into the dining ecosystem. The 2019 acquisition of Resy for an undisclosed amount had already positioned American Express at the center of restaurant reservations. But In June 2024, Amex acquired Tock, a restaurant reservation platform, further expanding its portfolio in dining reservations following its earlier acquisition of Resy. The $400 million all-cash deal for Tock wasn't just about adding 7,000 more restaurants to the network—it was about owning the infrastructure of dining experiences.

The latest acquisition will give Amex influence over a portfolio of 7,000 restaurants and other bookable entertainment experiences listed on Tock. The company already gives cardholders special table access not available to the general public through Resy. This creates a powerful moat: the more exclusive restaurants American Express controls access to, the more valuable its cards become to affluent diners, and the more those diners spend, the more attractive American Express becomes to restaurants.

The strategy extends beyond just reservations. In a dual announcement, the credit card company will also be acquiring Rooam — a mobile payment, ordering, and integrations tech company — for an undisclosed sum. By acquiring payment and ordering technology, American Express is building an end-to-end dining platform that touches every aspect of the restaurant experience.

The numbers validate the strategy. "Restaurants are one of our largest card member spending categories within travel and entertainment, with $100bn in volume in 2023." For perspective, that's more than the GDP of many countries, all flowing through American Express's dining ecosystem.

The digital revolution under Squeri goes far beyond dining. American Express' Risk & Information Management team in partnership with the company's Technology group embarked on a journey to build world-class Big Data capabilities. AmEx is thus, able to analyze trends and information on cardholder spending and build algorithms to provide customized offers to attract and retain customers and leverage this information to maintain relationships with merchants using targeted marketing to match merchants with the right customers, who are likely to spend more and stay loyal.

This closed-loop advantage—where American Express sees both sides of every transaction—has become even more powerful in the digital age. The benefit of the "closed loop" is that AmEx can view all transactions on both customer and merchant side, in real time, whereas Visa and MasterCard have limited access to customer data because the contracting banks are reluctant to share information. This gives AmEx a strong competitive advantage and provides some of the key components for a new digital structure.

The company has also made significant strides in appealing to younger demographics. In recent years, Amex has moved beyond its stuffy reputation as the credit card of the business elite by reaching out to younger generations like millennials and Gen Z. The effort has largely been a success, with these younger customers making up about 75% of new cardholders for Amex's Platinum and Gold cards last year, Grosfield told Fortune last month. This isn't your grandfather's American Express anymore.

But Squeri's tenure hasn't been without challenges. In January 2025, American Express announced a significant settlement with federal authorities. American Express will pay a total of about $230 million to resolve federal wire fraud investigations and to settle civil allegations of deceptive marketing, the company said Thursday. The tally includes more than $138 million as part of a non-prosecution agreement with the U.S. Attorney's Office in Brooklyn, New York, related to allegations that American Express gave customers "inaccurate tax advice" for two wire products.

The separate civil settlement announced Thursday centered on allegations that American Express "deceptively marketed credit cards" through "an affiliated entity that initiated sales calls to small businesses." The practices, which took place from 2014 through 2017, included "misrepresenting the card rewards or fees" and "whether credit checks would be done without a customer's consent," the DOJ said. The practices also allegedly included "submitting falsified financial information for prospective customers, such as overstating a business's income."

While these issues predated Squeri's CEO tenure, they underscore the challenges of managing a vast financial services organization. The company's response—firing 200 employees, discontinuing products, and implementing new compliance measures—demonstrates a commitment to addressing problems head-on.

Looking ahead, American Express under Squeri is positioning itself not as a credit card company but as a lifestyle platform. The partnership with Toast announced in early 2025 exemplifies this vision, creating tools that will allow restaurants to provide more personalized service based on American Express customer data. The integration of AI and machine learning throughout the organization is transforming everything from fraud detection to customer service to marketing personalization.

The recognition speaks to Squeri's impact: In April 2025, TIME named him one of the 100 Most Influential People of 2025. Under his leadership, American Express has proven that a 175-year-old company can still innovate, that premium positioning can coexist with digital transformation, and that owning the customer relationship—not just processing their payments—is the key to surviving in the fintech age.

IX. Playbook: Business & Investing Lessons

After 175 years of reinvention, crisis, and triumph, what can we learn from the American Express story? The lessons extend far beyond payments, offering insights into brand building, network effects, capital allocation, and the art of surviving when everyone thinks you're finished.

Lesson 1: Trust Is the Ultimate Moat

From the Wells Fargo split in 1852 to the Salad Oil Scandal in 1963 to the 2008 financial crisis, American Express has faced existential threats that should have killed it. Each time, the company survived because of one asset that doesn't appear on any balance sheet: trust.

When American Express honored warehouse receipts it wasn't legally obligated to pay after the Salad Oil Scandal, it was protecting something more valuable than the $60 million it cost: the belief that when American Express makes a promise, it keeps it. This is what Warren Buffett understood when he conducted his field research in 1964. The scandal might have damaged the stock price, but it hadn't damaged the franchise.

Trust compounds over time. Every transaction honored, every dispute resolved fairly, every traveler helped in a crisis adds to a reservoir of goodwill that becomes nearly impossible for competitors to replicate. You can copy a product, you can match a price, but you can't copy 175 years of keeping promises.

Lesson 2: Premium Positioning Is About Saying No

American Express has consistently chosen to be expensive. When it launched its charge card in 1958, it deliberately priced it $1 higher than Diners Club. When Visa and MasterCard were racing to sign up every bank and every merchant, American Express chose to be selective. When fintech startups promised free everything, American Express raised its Platinum Card annual fee to $695.

This isn't arrogance—it's strategy. By saying no to customers who only care about price, American Express can say yes to investments that matter to customers who care about value. The concierge service, the airport lounges, the exclusive restaurant reservations—none of these make sense if you're competing on price. All of them make sense if you're competing on experience.

The numbers prove the strategy works. American Express cardholders spend an average of $24,059 annually, compared to roughly $5,000 for the average credit card. That's not because American Express customers are five times richer—it's because American Express has given them reasons to consolidate their spending on a single card.

Lesson 3: Network Effects in Closed Systems Can Beat Open Networks

Conventional wisdom says open networks always beat closed networks. Visa and MasterCard, with their open bank partnership model, process far more transactions than American Express. But American Express proves that a closed-loop network, properly managed, can generate superior economics.

Because American Express sees both sides of every transaction, it knows things Visa and MasterCard can never know. It knows that the customer who just bought a $5,000 business class ticket also dines at Michelin-starred restaurants. It knows that the small business that processes $100,000 monthly also needs working capital loans. This information asymmetry allows American Express to underwrite risk better, target marketing more precisely, and create products that feel personally designed for each customer.

The closed loop also means American Express captures more value from each transaction. While Visa and MasterCard split economics with issuing banks, American Express keeps it all. This allows for more generous rewards, better customer service, and continued investment in the premium experience.

Lesson 4: Capital Allocation Is About Courage and Conviction

Warren Buffett's American Express investment teaches us that the best investments are made when things look worst. But it also teaches us something about holding periods. Berkshire Hathaway hasn't sold a share of American Express since the 1990s, watching its stake grow from 5% to over 20% through buybacks alone.

This isn't laziness—it's brilliance. As Buffett has said, "Our favorite holding period is forever." When you find a business with durable competitive advantages, the best capital allocation decision is often to do nothing. Let the company compound, let management buy back shares, let the moat widen. The hardest thing in investing isn't finding great companies—it's holding them through the inevitable storms.

American Express's own capital allocation has been exemplary. The company has returned over $50 billion to shareholders through dividends and buybacks over the past decade while still investing in growth. This isn't financial engineering—it's the natural result of a business that generates more cash than it can reasonably reinvest.

Lesson 5: Reinvention Requires Abandoning What Made You Successful

American Express's history is littered with abandoned businesses that were once core to its identity. The express business that gave the company its name? Gone in 1918. The travelers cheque that defined it for a century? A tiny fraction of today's revenue. The financial supermarket strategy of the 1980s? Unwound at great cost.

Each abandonment was painful. Each seemed like betrayal of the company's heritage. Each was necessary for survival. The express business was commoditized by railroads. Travelers cheques were killed by ATMs. The financial supermarket was too complex to manage. Holding onto them would have meant slow decline.

The lesson for founders is brutal but essential: the business model that makes you successful will eventually become the business model that kills you. The only way to survive decades, much less centuries, is to repeatedly destroy your own business before someone else does.

Lesson 6: Brand Premium Survives Technology Disruption

Every technology wave was supposed to kill American Express's brand premium. ATMs would make travelers cheques obsolete. The internet would make comparison shopping destroy pricing power. Mobile payments would commoditize all cards into invisible rails. Cryptocurrency would make traditional financial services irrelevant.

Instead, American Express's brand has become more valuable, not less. In a world of infinite choice, brands that signal something become more important, not less. When every restaurant is bookable online, exclusive access becomes more valuable. When every payment is digital, the weight of a metal card matters more. When every startup promises to disrupt financial services, 175 years of history becomes a differentiator, not a liability.

The lesson isn't that technology doesn't matter—American Express has invested billions in digital transformation. It's that technology amplifies brand value rather than destroying it. The companies that win aren't those with the best technology or the best brand, but those who use technology to make their brand more valuable.

Lesson 7: Crises Are Features, Not Bugs

If you plot American Express's stock price over its history, the crises are obvious: deep valleys that look like disasters. The Salad Oil Scandal. The Boston Fee Party. The loss of Costco. The pandemic. Each looked like potential extinction events.

But if you zoom out, something remarkable emerges: each crisis preceded a period of innovation and growth. The Salad Oil Scandal led to Buffett's investment and a focus on brand value. The merchant revolt led to product innovation and international expansion. The Costco loss forced a focus on premium customers and digital transformation. The pandemic accelerated the shift to lifestyle services and younger customers.

This isn't coincidence—it's pattern. Crises force choices. They kill sacred cows. They create urgency. They separate companies that can adapt from those that can't. For a company that survives 175 years, crises aren't interruptions to the business—they're the rhythm of the business.

The Ultimate Lesson: Time Arbitrage

Perhaps the most profound lesson from American Express is about time horizons. In a world obsessed with quarterly earnings, American Express has played a longer game. When it honored the warehouse receipts in 1963, it was thinking in decades. When it invests in airport lounges that won't pay back for years, it's thinking in decades. When it acquires restaurant reservation platforms, it's thinking in decades.

This time arbitrage—doing things that don't make sense in the short term but make perfect sense in the long term—is perhaps the most sustainable competitive advantage in business. It's why Warren Buffett has never sold. It's why the brand keeps getting stronger. It's why a company founded when California was barely a state is still growing in the age of AI.

As Buffett himself put it: "When you find a truly wonderful business, stick with it." After 175 years, American Express has proven that some businesses aren't just built to last—they're built to last forever.

X. Analysis & Bear vs. Bull Case

As we stand in 2025, American Express trades at approximately 20 times earnings, a premium to traditional banks but a discount to pure-play payment networks. The question facing investors isn't whether American Express is a good company—175 years of history settles that—but whether it's a good investment at today's prices.

The Bull Case: A Fortress Built on Affluence

The optimists see American Express as perfectly positioned for the next decade. Start with the macro backdrop: wealth inequality, whether you celebrate or deplore it, continues to widen globally. The top 10% of earners control an ever-larger share of spending power. American Express doesn't need to fight for market share in the bottom 90%—it just needs to entrench itself deeper with the top 10%.

The numbers support this thesis. Despite having only 141 million cards in force compared to Visa's billions, American Express processes $1.7 trillion in annual volume. That's the power of focusing on customers who spend $24,000 annually versus $5,000. As wealth concentrates, American Express's addressable market paradoxically grows even as it serves fewer people.

The brand moat appears unassailable. In an age where every financial product can be copied in weeks, American Express has something that can't be replicated: prestige. The metal card that thuds when you drop it on the table. The Centurion Lounge access. The Resy reservation at the impossible-to-book restaurant. These aren't features—they're status symbols. And status, as luxury brands have proven for centuries, is recession-resistant.

The Warren Buffett factor cannot be ignored. Berkshire Hathaway owns 21.90% of American Express, a stake worth over $35 billion. Buffett doesn't just bring capital—he brings credibility. His six-decade holding period sends a message: this is a business built for generations, not quarters. When the Oracle of Omaha refuses to sell despite a 500%+ gain, it suggests he sees something the market doesn't.

The digital transformation under Squeri has repositioned American Express for the next era. The acquisition of Resy and Tock isn't just about restaurant reservations—it's about owning the infrastructure of experiences. As physical goods become commoditized and experiences become the ultimate luxury, American Express is positioning itself as the gateway to those experiences.

International expansion remains a massive opportunity. While American Express dominates the U.S. premium card market, its international presence is relatively small. As middle classes emerge in India, Southeast Asia, and Africa, American Express has decades of growth simply by exporting its U.S. playbook to new markets. The brand travels better than almost any in financial services.

The ecosystem is finally coming together. For years, American Express talked about being more than a card company. Now, with dining reservations, travel booking, exclusive experiences, and lifestyle services, it's delivering. Each new service makes the core card more valuable, which attracts more spending, which attracts more merchants, which enables more services. It's a virtuous cycle that's just beginning to spin.

The Bear Case: The Barbarians Are Inside the Gates

The skeptics see gathering storms that the bulls are ignoring. Start with the fundamental challenge: merchant acceptance. Despite decades of effort, American Express is still not accepted everywhere Visa and MasterCard are. In an increasingly digital world where checkout happens in milliseconds, any friction is death. Why would a merchant pay 3% to American Express when they can pay 2% to Visa?

The fintech disruption is real and accelerating. Buy Now, Pay Later providers like Klarna and Affirm are attacking the lending business. Digital wallets like Apple Pay and Google Pay are intermediating the customer relationship. Crypto payments promise to eliminate intermediaries entirely. American Express's response—acquiring restaurant reservation platforms—feels like rearranging deck chairs while the hull is breached.

The premium customer base that bulls celebrate is also a vulnerability. Affluent customers are sophisticated. They have multiple cards. They optimize rewards. They're the first to adopt new payment methods. The idea that they'll remain loyal to American Express out of tradition seems quaint. When a crypto payment saves them 2% on a yacht purchase, brand prestige won't matter.

Regulatory pressure is intensifying globally. The European Union has already capped interchange fees. The U.S. Congress regularly threatens similar action. The recent $230 million settlement for deceptive marketing practices suggests American Express's aggressive sales culture might be a liability in an era of increased scrutiny. How much of the company's growth has come from practices that won't be tolerated going forward?

Competition from banks is more serious than ever. JPMorgan's Sapphire Reserve, Citi's Prestige, Capital One's Venture X—every major bank now has a premium card with comparable rewards and lower fees. These banks have existing relationships, broader product sets, and deeper pockets. They're willing to lose money on cards to win the overall relationship. American Express can't match that math.

The China problem looms large. While bulls see international expansion opportunity, the reality is that China—the world's largest payment market—is effectively closed to American Express. UnionPay dominates domestically, and Alipay and WeChat Pay own digital payments. Even if American Express could enter, would Chinese consumers pay premium fees for a foreign brand when domestic options are free?

Economic sensitivity remains a critical weakness. American Express customers might be affluent, but they're also often leveraged. Small business owners, entrepreneurs, consultants—these customers cut spending fast when recession hits. The company's performance during the 2008 crisis, when it needed TARP funds and emergency conversion to a bank holding company, suggests the fortress isn't as strong as bulls believe.

The Valuation Debate

At 20 times earnings, American Express trades at a premium to traditional banks (10-12x) but a discount to payment networks like Visa (30x) and Mastercard (35x). Bulls argue this is appropriate—American Express is neither a bank nor a pure network but something more valuable: a lifestyle brand with financial services attached.

Bears counter that American Express deserves a bank multiple because it takes credit risk, holds deposits, and is regulated like a bank. The payment network comparison is false because Visa and Mastercard have better economics, faster growth, and no credit risk.

The truth, as always, is somewhere in between. American Express is a hybrid that defies easy categorization. Its returns on equity (30%+) are far superior to banks. Its brand value exceeds most consumer companies. Its network effects are real, even if not as powerful as pure platforms.

The Verdict

Investment decisions ultimately come down to time horizon and temperament. For those thinking in quarters or even years, American Express faces real challenges. Fintech disruption, regulatory pressure, and economic uncertainty make near-term performance unpredictable.

But for those thinking in decades—like Warren Buffett—American Express offers something rare: a business model that has survived everything from civil wars to world wars to financial crises to technological revolutions. The company that began moving packages by stagecoach now moves billions digitally. The brand that meant trust in 1850 still means trust in 2025.

The bear case is about what could go wrong. The bull case is about what has gone right for 175 years. In a world where most companies don't survive a decade, betting against American Express's second century seems like fighting history. The barbarians might be at the gates, but this fortress has repelled barbarians before.

XI. Epilogue & Future Outlook

As American Express enters its 176th year, the company stands at another inflection point. The $230 million settlement announced in January 2025 for deceptive marketing practices to small businesses is more than a financial penalty—it's a reminder that even the oldest institutions must constantly earn their social license to operate.

The future of payments is being rewritten in real-time. Central bank digital currencies threaten to nationalize payment rails. Embedded finance means every company can become a financial services provider. Artificial intelligence promises to make human judgment in underwriting obsolete. The metaverse might make physical cards as quaint as travelers cheques.

Yet American Express has survived every supposed extinction event. The company that was supposed to die when railroads nationalized express mail became a financial services giant. The company that was supposed to die when ATMs killed travelers cheques became a charge card leader. The company that was supposed to die when the internet commoditized payments became a lifestyle brand.

What would a new CEO focus on? The challenge for American Express's next leader—whenever they succeed Squeri—will be to balance preservation with revolution. The brand must be protected but not pickled in amber. The premium positioning must be maintained while expanding access. The closed-loop network must be defended while opening to partnerships.

International expansion remains the most obvious opportunity. While American Express dominates the U.S. premium segment, vast markets remain untapped. India's growing affluent class, Southeast Asia's emerging entrepreneurs, Africa's mobile-first generation—each represents decades of potential growth. But expansion must be thoughtful. The American Express brand means something precisely because it's not everywhere.

The small business segment presents both opportunity and challenge. Small businesses are the economy's growth engine, and American Express has strong positions with established businesses. But the next generation of entrepreneurs starts businesses on their phones, expects instant everything, and has no patience for traditional banking. Serving them requires capabilities American Express doesn't currently possess.

Technology investment must accelerate, but not at the expense of human connection. The company's concierge service, travel advisors, and restaurant specialists provide value that algorithms can't match. The winners in financial services won't be those who eliminate humans but those who use technology to make human interactions more valuable.

The dining and travel ecosystem needs to evolve from a collection of acquisitions into an integrated platform. Owning Resy and Tock is just the beginning. The real value comes from creating experiences that can't be replicated—exclusive chef's tables, private wine tastings, access to sold-out events. American Express must become not just a payment method but a curator of life's special moments.

Partnerships will become increasingly critical. The Toast partnership announced in 2025 shows the way forward—combining American Express's customer relationships with best-in-class technology providers. The company can't build everything itself, but it can be the orchestrator that brings together the best solutions for its customers.

The regulatory environment will only become more complex. Privacy laws, data protection requirements, interchange regulations—each presents compliance challenges but also competitive opportunities. Companies that can navigate regulatory complexity while still innovating will have massive advantages over those that can't.

Climate change and sustainability can't be ignored. American Express's commitment to net-zero emissions by 2035 is a start, but younger customers expect more. The company that built its reputation on conspicuous consumption must figure out how to maintain premium positioning in an era of conscious consumption.

The competitive landscape will continue to evolve in unexpected ways. The next threat to American Express might not come from Visa or Mastercard or even fintech startups. It might come from Apple, which already has millions of payment credentials and unmatched customer loyalty. It might come from Amazon, which knows more about purchasing behavior than anyone. It might come from China, where super-apps have redefined what financial services can be.

But perhaps the biggest challenge—and opportunity—is demographic change. American Express has successfully attracted millennials and Gen Z to its premium cards, but keeping them requires constant evolution. These generations value experiences over possessions, purpose over profit, flexibility over tradition. They're willing to pay for value but ruthless about switching when they find better options.

The key lessons for founders and investors remain timeless:

Build trust before you build products. American Express spent decades earning trust as an express company before entering financial services. That trust, not any particular product, is the company's true asset.

Choose your customers before they choose you. American Express's decision to focus on affluent customers wasn't lucky—it was strategic. Knowing who you won't serve is as important as knowing who you will.

Invest in relationships, not just transactions. The closed-loop network creates data advantages, but the real advantage is the relationship. American Express knows its customers' names, their preferences, their special occasions. That's not replicable by technology alone.

Survive long enough to get lucky. American Express has faced existential crises roughly every 20 years. Each time, survival came first, strategy second. Companies that survive long enough eventually find new sources of growth.

Brand value compounds. Every year American Express maintains its premium positioning, the brand becomes more valuable. In a world of infinite choice and instant comparison, brands that mean something become priceless.

As we look to American Express's third century, the question isn't whether the company will survive—history suggests it will. The question is what it will become. Will it remain a premium card issuer with lifestyle services attached? Will it evolve into a full-scale luxury lifestyle company that happens to process payments? Will it become a technology platform that powers experiences for multiple brands?

The answer might be all of the above. The company that started as an express service became a travel company, then a financial services company, then a lifestyle brand. Each transformation built on what came before while abandoning what no longer worked. The next transformation is already underway.

What would Warren Buffett do? He would probably buy more if he could. But SEC regulations limit Berkshire Hathaway from owning more than 25% of a company. So instead, he waits. He watches. He lets American Express buy back shares, slowly increasing Berkshire's ownership percentage without spending a dollar.

It's the ultimate expression of confidence: doing nothing. In a world obsessed with action, sometimes the best strategy is patience. American Express has been patient for 175 years. It can afford to be patient for 175 more.

The story of American Express is far from over. The company that survived the Civil War, two World Wars, the Great Depression, the Salad Oil Scandal, the merchant revolt, the financial crisis, and the pandemic has proven one thing above all: resilience isn't about avoiding crises—it's about emerging from them stronger.

As Ken Chenault once said, "Success is never final." For a company entering its 176th year, that's not a warning—it's a promise. The best chapters of the American Express story might still be unwritten.

XII. Recent News

The drumbeat of news around American Express never stops. Beyond the January 2025 settlement for deceptive marketing practices, the company continues to make moves that will shape its future for decades.

The partnership with Toast announced in early 2025 represents more than just a technology integration—it's a blueprint for how American Express plans to compete in the platform economy. By combining American Express's dining network with Toast's restaurant operating system, the companies are creating something neither could build alone: a complete ecosystem that serves both restaurants and diners.

The competitive landscape continues to shift rapidly. Capital One's pending acquisition of Discover, if approved, would create a payments giant with the scale to challenge American Express's premium positioning. The combination would bring together Capital One's technology capabilities with Discover's network, creating a formidable competitor in the affluent segment.

Regulatory scrutiny is intensifying globally. The Consumer Financial Protection Bureau has proposed new rules on credit card late fees that could impact billions in revenue across the industry. While American Express's affluent customer base makes it less exposed than others, any regulation that caps fees challenges the economics of the rewards arms race.

The macro environment presents both opportunities and challenges. Interest rates remain elevated, benefiting American Express's lending business but potentially cooling the consumer spending that drives transaction volume. The labor market remains tight, supporting spending but also driving up American Express's own costs as it competes for talent.

International expansion continues with mixed results. While growth in Europe and Asia remains strong, American Express pulled back from some emerging markets where the investment required to build acceptance exceeded near-term returns. The company is increasingly selective about where it deploys capital, focusing on markets with existing affluent populations rather than betting on emerging middle classes.

Technology investments are accelerating. American Express's annual technology spend now exceeds $4 billion, rivaling pure technology companies. The focus isn't just on digital channels but on artificial intelligence and machine learning that can personalize every interaction. The company processes billions of transactions annually—each one is a data point that, properly analyzed, can predict future behavior.

The war for talent has become existential. American Express competes not just with banks but with technology companies for engineers, data scientists, and product managers. The company's New York headquarters, once an advantage, is now a challenge as talent increasingly prefers Silicon Valley or remote work. Squeri has responded by opening technology centers in multiple cities and embracing hybrid work, but cultural transformation takes time.

XIII. Links & Resources

For those seeking to go deeper into the American Express story, the following resources provide invaluable perspective:

Essential Books: - "Charging Ahead: The Story of American Express" by Peter Z. Grossman - The definitive corporate history - "The Salad Oil Swindle" by Norman C. Miller - A detailed account of the scandal that brought Buffett - "House of Cards: A Tale of Hubris and Wretched Excess on Wall Street" by William D. Cohan - Chronicles the Robinson era - "The Warren Buffett Way" by Robert Hagstrom - Includes detailed analysis of the American Express investment

Key Buffett Shareholder Letters: - 1964 Buffett Partnership Letter - First discussion of American Express investment - 1991 Berkshire Hathaway Letter - Reflection on American Express's competitive advantages - 2016 Berkshire Hathaway Letter - 50-year retrospective including American Express

Academic Research: - "Network Effects in Two-Sided Markets" (Harvard Business Review) - Framework for understanding American Express's business model - "The Economics of Credit Cards" (Federal Reserve studies) - Multiple papers on industry structure - "Brand Equity in Financial Services" (Journal of Financial Services Marketing) - Analysis of brand value in commoditized markets

Industry Reports: - Nilson Report - The definitive source for payment industry statistics - McKinsey Global Payments Report - Annual analysis of payment trends - Boston Consulting Group's Global Payments Model - Forward-looking industry projections

Documentaries and Media: - "The Card Game" (Frontline PBS) - Investigation of credit card industry practices - "Spent: Looking for Change" - Documentary on financial services access - American Express Investor Day presentations - Direct from management on strategy

Historical Archives: - American Express Company Archives at Princeton University - The Smithsonian National Museum of American History - American Express artifacts - Library of Congress Business Reference Services - Historical reports and documents

Regulatory Filings: - SEC EDGAR database - All American Express filings since 1994 - Federal Reserve statistical releases - Credit card industry data - CFPB complaint database - Customer feedback and trends

These resources offer multiple lenses through which to view American Express: as a business, as an investment, as a cultural institution, and as a case study in corporate resilience. The company that started with stagecoaches continues to write new chapters, and understanding its past remains the best guide to imagining its future.

The story of American Express reminds us that in business, as in life, the only constant is change. Companies that survive centuries don't do so by standing still—they do so by constantly reinventing themselves while maintaining the core values that made them successful in the first place. For American Express, those values—trust, service, and premium quality—have remained constant even as everything else has changed. As the company enters its next chapter, the question isn't whether it will survive but what it will become. If history is any guide, it will be something we can't yet imagine.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube