Axon Enterprise: From Garage Startup to Public Safety Platform

I. Introduction & Episode Roadmap

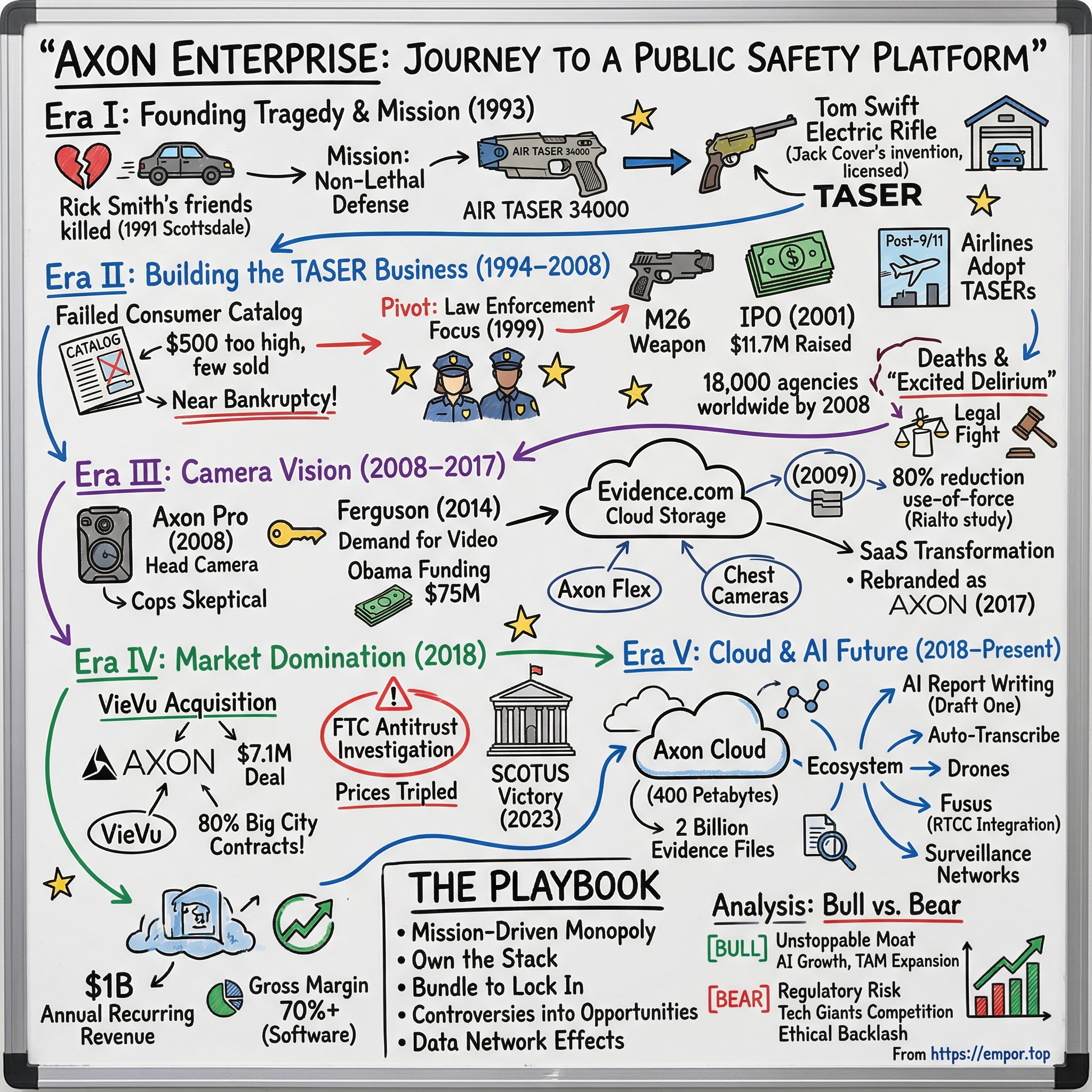

Picture this: A $58 billion company that controls 80% of America's police body camera market, processes 400 petabytes of criminal evidence in the cloud, and is now using AI to write police reports. This is Axon Enterprise in 2024—a monopoly-like platform that touches nearly every aspect of modern policing. But rewind three decades, and you'll find two brothers in an Arizona garage, driven by personal tragedy, tinkering with electroshock weapons that nobody wanted to buy.

How did a company founded to avenge the senseless killing of two friends become the technological backbone of law enforcement across 107 countries? How did a hardware company selling controversial stun guns transform into a SaaS juggernaut with over $1 billion in annual recurring revenue? And perhaps most intriguingly—how did they pull off one of the most audacious pivots in corporate history, from "the TASER company" to a full-stack public safety platform that's increasingly indispensable to modern policing?

This is the story of Axon Enterprise—a tale of mission-driven monopoly building, aggressive market consolidation, and the delicate dance between public safety and civil liberties. It's about Rick Smith, the Chicago Booth-trained finance MBA who became an unlikely law enforcement tech mogul, and his brother Tom, the engineer who helped turn a NASA researcher's failed invention into a global phenomenon.

We'll trace Axon's journey through four distinct eras: the scrappy TASER years when they nearly went bankrupt selling to consumers; the body camera revolution sparked by Ferguson; the platform transformation that saw them become the "Salesforce of policing"; and today's AI-powered future where they're automating everything from evidence management to report writing.

Along the way, we'll examine their playbook: how they used hardware as a trojan horse for software subscriptions, why they paid seemingly modest sums to acquire competitors only to dominate entire markets, and how they've built switching costs so high that even cities uncomfortable with their pricing have nowhere else to turn. We'll also confront the controversies—from TASER-related deaths to antitrust lawsuits to the ethical implications of AI in policing.

This isn't just a business story. It's about the intersection of technology, justice, and monopoly power in one of society's most sensitive domains. Because when one company controls the tools that document police encounters, store criminal evidence, and increasingly make decisions about public safety—well, that's a story worth understanding deeply.

So buckle up. We're about to dive into one of the most fascinating, controversial, and consequential business stories of our time. From that garage in Scottsdale to courtrooms, boardrooms, and patrol cars across the globe—this is Axon Enterprise.

II. The Founding Tragedy & Mission (1993)

The phone call came on a September evening in 1991. Rick Smith, then working in Europe, learned that two of his high school friends had been shot and killed in a road rage incident in Scottsdale, Arizona. The killer had cut them off in traffic, an argument ensued, and within seconds, both young men were dead. The senselessness of it all—how a traffic dispute escalated to double homicide—haunted Smith. He couldn't stop thinking: what if they'd had another option? What if there was a way to defend yourself without lethal force?

This wasn't an abstract philosophical question for Rick. These were his friends from high school—guys he'd grown up with, shared teenage adventures with. The randomness and finality of gun violence had suddenly become visceral and personal. While grieving, he found himself sketching out ideas, researching non-lethal weapons, trying to channel his anger and helplessness into something constructive.

Rick wasn't your typical entrepreneur destined for the defense industry. He'd studied at Harvard, earned his MBA from the University of Chicago's prestigious Booth School of Business, and completed another MBA in International Finance at Belgium's University of Leuven. His resume screamed "investment banking" or "private equity," not "electroshock weapons inventor." But tragedy has a way of redirecting ambition.

He recruited his brother Tom, an engineer with the technical chops Rick lacked. Their dynamic was classic—Rick the charismatic business mind, Tom the methodical builder. Together, on September 7, 1993, they founded AIR TASER, Inc. in a Scottsdale garage, with their mother Moya serving as the company's first CEO. Yes, you read that right—Mom was the CEO, a detail that perfectly captures the scrappy, all-hands-on-deck nature of those early days.

But the Smith brothers weren't starting from scratch. They'd discovered the work of Jack Cover, a NASA researcher who'd invented something called the "TASER" back in the 1970s. Cover, a physicist who'd worked on the Apollo moon landing project, had named his invention after a childhood literary hero—Tom Swift and his Electric Rifle, adding an "A" to make it TASER. Cover's device fired darts connected to wires that delivered electrical pulses, theoretically incapacitating someone without permanent harm.

Cover's invention was brilliant but deeply flawed. His original TASER used gunpowder to fire the darts, which meant the ATF classified it as a firearm—killing its commercial viability. By the time the Smiths found him, Cover was in his seventies, his patents were expiring, and his invention was largely forgotten. The brothers struck a deal with the aging inventor: they'd license his technology and patents, redesign the device to use compressed air instead of gunpowder (hence "AIR TASER"), and finally bring his vision to market.

The early days were quintessentially startup—chaotic, cash-strapped, and filled with technical setbacks. They worked out of that garage, testing prototypes on themselves (Rick would later joke about how many times Tom shocked him "for science"), and burning through their modest seed capital. Rick was constantly on the phone, trying to convince skeptical investors that Americans would buy a $500 electroshock device for self-defense. Tom was perpetually hunched over workbenches, trying to engineer a device that was powerful enough to incapacitate an attacker but safe enough to sell to consumers. Their mission wasn't just about building a business—it was deeply personal. Rick and Tom Smith were on a mission to reduce gun violence after former high school football teammates were killed in a senseless act of road-rage violence in December 1991. Every late night in that garage, every failed prototype, every investor rejection was measured against that original tragedy. Could they have saved their friends' lives if this technology existed?

The technical challenges were immense. Jack Cover, who had worked for NASA (Apollo program), IBM and Hughes Aircraft, had already spent years trying to commercialize his invention. Cover, a NASA researcher, began developing the first Taser in 1969, and got the idea for the Taser after hearing about a man who was briefly immobilized by a fallen power line. He began tinkering in his garage, and in the late 1960s he came up with a device that looked something like a flashlight but fired darts that delivered an electrical charge.

The name itself tells a story. Cover got the name for the weapon from one of his favorite childhood books, "Tom Swift and His Electric Rifle," one in a popular early 20th century series by Victor Appleton. In the book, the young Swift invents a rifle that shoots bolts of electricity. The story apparently continued to animate Dr. Cover's imagination decades later, when he conceived the word "Taser" as an acronym for "Thomas A. Swift Electric Rifle".

But Cover's original design had a fatal flaw for commercialization. Because the Taser used gunpowder to launch the darts, the federal government considered it a firearm, a classification that ruled out a civilian market and also discouraged police and military sales. This is where the Smith brothers' innovation became crucial—they redesigned the propulsion system to use compressed nitrogen instead of gunpowder, removing the firearm classification and opening up vast new markets.

The contrast between the two generations of inventors was stark. Cover was the brilliant scientist—he earned a bachelor's degree and a doctorate in nuclear physics at the University of Chicago, studying under Enrico Fermi—but he lacked the business acumen to commercialize his invention. The Smiths brought youth, business training, and most importantly, a burning mission that transcended profit. They weren't just selling a product; they were evangelizing a philosophy about the value of human life.

As 1993 turned to 1994, the brothers prepared to launch their first product, the AIR TASER 34000. They had no idea that their journey would take them from near bankruptcy to building one of the most powerful monopolies in American business. But first, they had to survive what would become known internally as "the consumer years"—a period so disastrous it nearly killed the company before it could transform policing forever.

III. Building the TASER Business (1994–2008)

The Sharper Image catalog arrived in mailboxes across America in late 1994, filled with its usual array of massage chairs, air purifiers, and executive toys for the affluent. But sandwiched between the ionic breezers and the motorized tie racks was something unprecedented: a $500 electroshock weapon you could order by phone. The AIR TASER 34000 had arrived.

Rick Smith had convinced the upscale retailer that safety-conscious consumers would embrace non-lethal self-defense. The logic seemed sound—if people would pay $400 for a radar detector or $600 for a bread maker, surely they'd invest $500 to protect their families without the moral weight of owning a gun. The brothers ran focus groups where suburban parents nodded enthusiastically. Early sales projections suggested they'd move 50,000 units in the first year.

They sold fewer than 1,000.

The consumer market rejection was swift and brutal. Despite the Rodney King riots fresh in memory, despite rising crime statistics, despite their evangelical pitch about saving lives—Americans simply wouldn't buy electroshock weapons for their nightstands. The product was too aggressive for liberals, not lethal enough for conservatives, and too expensive for everyone. By 1996, AIR TASER was hemorrhaging cash, down to their last $20,000, with Rick maxing out credit cards to make payroll. The pivot came in desperation. After nearly going bankrupt marketing other products such as an electroshock-based anti-theft system for automobiles known as "Auto Taser" in 1997, the company, later renamed TASER International, introduced its TASER M26 weapon in 1999—this time targeting law enforcement exclusively. The non-compete agreement that had precluded sales to the law enforcement and military markets had finally expired in 1998, opening the door to what would become their salvation.

The transformation was immediate and dramatic. Where consumers saw an uncomfortable moral choice, police departments saw a solution to an existential crisis. The late 1990s had brought a series of high-profile police shootings, massive civil settlements, and community outrage. Chiefs of police were desperate for alternatives. Rick Smith, now polished from years of rejection, would walk into police departments with a simple demonstration: he'd shock himself with the TASER, stand back up, and ask, "Would you rather I shot you with a gun?"

Over 400 police departments in the United States had made initial purchases of their products and 15 police departments, including San Diego, Sacramento, and Albuquerque, had purchased their products for every patrol officer by 2001. The contrast with the consumer market failure was stark—police departments didn't just buy TASERs; they evangelized them. Officers would share stories of lives saved, both civilian and their own. Every successful deployment became a case study, every prevented shooting a marketing victory.

The timing of their IPO in May 2001 could hardly have been worse. Taser International went public in May 2001, pricing its shares at $13. The company's Initial Public Offering (IPO) in May 2001, when it went public as TASER International, raised approximately $11.7 million. The price dropped from there, making the deal a modest success, not one of the eye-popping instant-millionaire IPOs of a few years earlier. The dot-com bubble had burst, the NASDAQ was in free fall, and investors were fleeing anything that looked speculative.

Then came September 11th.

Barely two months after the attacks, United Airlines announced that it was buying Tasers for all its 600 plus planes. Other airlines soon followed suit. Suddenly, TASER wasn't just a law enforcement tool—it was part of America's homeland security apparatus. Taser International finished 2001 in the black, making a profit for the first time since its founding. Revenue stood at $6.8 million.

The next phase was about scaling aggressively. Rick Smith understood something fundamental: once a police department adopted TASERs, they rarely went back. The switching costs weren't just financial—they were political and operational. Officers trained on the devices, policies were written around them, and communities expected their use instead of firearms. By 2003, they had grown to more than 4,300 agencies deploying TASER brand weapons.

But success brought scrutiny. Between 2001 and 2008, hundreds of deaths occurred after TASER deployments. The company's response was aggressive and controversial. They funded studies, challenged medical examiners, and promoted the concept of "excited delirium"—a disputed condition they argued was the real cause of deaths, not their weapons. They built a medical advisory board stacked with sympathetic experts and turned every lawsuit into a battle over the science of electrical incapacitation.

The business model was evolving too. Training became a profit center—On January 1, 2001, we implemented a $195 charge for each training attendee. They created a network of certified instructors who became embedded advocates within police departments. The company also took significant action against competitors, acquiring Tasertron and aggressively defending its patents. Patent lawsuits by TASER International led to the shutdown of Stinger Systems and its successor company, Karbon Arms.

By 2008, TASER devices were deployed in over 18,000 law enforcement agencies across 107 countries. They'd survived the consumer market disaster, navigated the post-9/11 transformation of American security, and built what appeared to be an unassailable position in less-lethal weapons. But Rick Smith was already thinking about the next transformation. Because in 2008, hidden in their product catalog next to the latest electroshock weapons, was something that would eventually dwarf the TASER business entirely: a head-mounted camera called the Axon Pro.

IV. The Camera Vision: From Hardware to Platform (2008–2017)

The prototype looked ridiculous—a bulky camera strapped to an officer's head like a coal miner's lamp. When Rick Smith unveiled the Axon Pro in 2008, even his own sales team was skeptical. "We're the TASER company," they said. "Why are we making cameras?" Smith's response was prescient: "Because the real product isn't the camera. It's the truth."

In 2008, the company unveiled its first body-worn camera, the Axon Pro. It was designed to be head-mounted, and upload footage for online storage on a web-based service known as Evidence.com. This wasn't just a hardware pivot—it was a fundamental reimagining of what Axon could be. While competitors saw body cameras as recording devices, Smith saw them as data collection points for a software platform that would transform policing.

Evidence.com, launched in 2009, was the real innovation. Police departments had been drowning in digital evidence—dashcam footage, interrogation videos, crime scene photos—all stored on DVDs and local servers, impossible to search, share, or secure. Evidence.com offered cloud storage with chain-of-custody protection, automated redaction tools, and seamless sharing with prosecutors. It was Dropbox meets LexisNexis, built specifically for law enforcement.

The initial market response was tepid. Police chiefs worried about storing sensitive data in the cloud. Officers complained about wearing cameras. Privacy advocates raised concerns about surveillance. Sales crawled along for three years, with Smith burning cash on server infrastructure for a product few wanted. Board members questioned the strategy. Why not just stick to TASERs?

Then came Rialto. In April 2013, the Rialto Police Department released the results of a 12-month study on the impact of on-officer video using Axon Flex cameras. The study found an 88% drop in complaints filed against officers and nearly a 60% reduction in officer use-of-force incidents. These weren't marginal improvements—they were transformative results that no other police technology had ever achieved. The study went viral in law enforcement circles. Chiefs of police who'd been skeptical suddenly became believers.

But it was Ferguson that changed everything.

On August 9, 2014, 18-year-old Michael Brown was shot and killed by police officer Darren Wilson in Ferguson, Missouri, a suburb of St. Louis. Brown was accompanied by his 22-year-old male friend Dorian Johnson. Wilson, a white male Ferguson police officer, said that an altercation ensued when Brown attacked him in his police vehicle for control of his service pistol. Johnson claimed that Wilson initiated the confrontation by grabbing Brown by the neck through Wilson's patrol car window, threatening him and then shooting at Brown. At this point, both Wilson and Johnson state that Brown and Johnson fled, with Wilson pursuing Brown shortly thereafter. Wilson stated that Brown then stopped, turned around and charged at him after the short pursuit. Johnson contradicted this account, stating that Brown turned around with his hands raised up after Wilson shot him in the back.

The absence of video footage turned Ferguson into a national Rorschach test. Without objective evidence, the incident became whatever people's preconceptions told them it was. In the fevered moments after the grand jury's decision not to charge Ferguson, Mo., police officer Darren Wilson in the fatal shooting of Michael Brown, the family of the slain 18-year-old released a statement pleading for peace — and urging people to join their campaign to get police around the nation to wear cameras.

The lesson wasn't lost on other police departments. In the weeks after Brown's death, numerous law-enforcement agencies around the U.S. began experimenting with body cameras. Anaheim, Calif.; Denver; Miami Beach; Washington, D.C.; and even Ferguson have all begun outfitting officers with cameras or announced plans to start. President Barack Obama announced the federal government would spend $75 million on body cameras for law enforcement officers, as one of the measures taken in response to the shooting.

Suddenly, Axon wasn't selling cameras—they were selling political cover, community trust, and litigation protection. Every police shooting without video became an argument for body cameras. Every cleared officer with video became a testimonial. The narrative shifted from "cameras watching cops" to "cameras protecting everyone."

Smith and his team moved with remarkable speed. They redesigned the cameras to be chest-mounted rather than head-mounted, making them less intrusive. They built automated upload systems so officers wouldn't have to manually manage footage. They created audit trails that made tampering impossible. Most importantly, they priced it as a subscription service, turning a capital expense into an operating expense that could be justified as insurance against lawsuits.

Especially in the wake of the Michael Brown shooting, the company's body-worn camera business saw significant growth. Smith argued that the company was "not just about weapons, but about providing transparency and solving related data problems."

The growth was explosive. Revenue from Axon cameras and services went from essentially zero in 2010 to a quarter of the company's business by 2017. But Smith saw something his competitors missed: the cameras were just the beginning. Once you controlled the video, you controlled the entire evidence chain. Once you controlled the evidence, you controlled the entire information flow of modern policing.

In June 2015, the company announced the formation of a new Seattle-based division known as Axon, which would encompass the company's technology businesses, including body-worn cameras, digital evidence management, and analytics. Rick Smith explained that the branch was inspired by Microsoft's use of the Xbox brand to branch into entertainment businesses, stating that "Axon was the name that we used for selling cameras historically, but we realized that brand had the room to grow and encompass all of our connected technologies." The Taser brand would still be used for the company's weapons products.

This dual-brand strategy was brilliant. TASER had baggage—deaths, lawsuits, controversy. Axon was fresh, tech-forward, solution-oriented. It allowed them to pitch to the same police departments with two different narratives: TASER for officer safety, Axon for community trust.

By 2016, they were ready for the ultimate transformation. The board was skeptical—why mess with the TASER brand that had taken two decades to build? Smith's answer was prescient: "We're not a weapons company that happens to do software. We're a platform company that happens to make weapons."

On April 5, 2017, TASER rebranded as Axon to reflect its expanded business. In 2017, TASER International officially changed its name to Axon Enterprise, Inc. The name change was more than cosmetic—it was a declaration of intent. They weren't the TASER company anymore. They were building something much bigger, much more powerful, and much harder to compete with: the operating system for law enforcement.

V. The VieVu Acquisition & Market Domination (2018)

The call came on a Friday afternoon in February 2018. The Federal Trade Commission wanted to discuss Axon's proposed acquisition of VieVu, their second-largest competitor in body cameras. Rick Smith wasn't worried—the deal was tiny, just $4.6 million in cash and $2.5 million in stock. In the world of tech M&A, this was pocket change. But the FTC understood something Smith was hoping they'd miss: this wasn't about the price tag. It was about monopoly.

VieVu wasn't just any competitor. Axon's purchase of private player Vievu gave Axon contracts with police departments in New York, Miami and Phoenix. These weren't just customers—they were the crown jewels of American law enforcement. The NYPD alone meant 36,000 officers, the largest police force in the nation. Miami-Dade was the gateway to Latin America. Phoenix was the proving ground for extreme weather conditions.

The competitive landscape before the acquisition was already tilted heavily in Axon's favor. Motorola had been trying to break in through acquisitions. Digital Ally was struggling to scale. Panasonic had the technology but not the relationships. VieVu was the only player with real traction, the only one that could credibly claim to be an alternative to Axon's ecosystem.

VieVu's founder, Steve Ward, was a former Seattle police officer who understood cops in a way Silicon Valley never could. He'd built the company on a simple premise: police departments needed an alternative to Axon's increasingly expensive and closed ecosystem. His pitch resonated, especially with large departments worried about vendor lock-in. By 2017, VieVu had won contracts that Axon had assumed were theirs by right.

The acquisition negotiations were swift and brutal. Safariland, VieVu's parent company, was hemorrhaging money. They'd acquired VieVu thinking body cameras would be easy money, only to discover that competing with Axon required massive investments in cloud infrastructure, support staff, and R&D. Every quarter they held on meant millions more in losses. Smith paid $4.6 million in cash and $2.5 million in stock to VIEVU parent company Safariland. The Federal Trade Commission soon began an antitrust investigation into Axon. According to the complaint, Axon's May 2018 acquisition reduced competition in an already concentrated market. The FTC alleged that Axon violated Section 5 of the FTC Act by acquiring VieVu, which the FTC characterized as Axon's "closest competitor."

What the FTC discovered in their investigation was damning. Internal emails showed Axon executives celebrating VieVu's demise. Market analyses revealed that after the acquisition of VIEVU is completed, Axon will own 80% of all big-city police department contracts. Most troubling were the pricing documents showing exactly what monopoly power looked like in practice. Within a year, Axon's body cam prices had risen 50 percent. By 2022, those prices had nearly tripled, reaching $490 per camera. The pattern was brazen—acquire the only real competitor, then jack up prices knowing police departments had nowhere else to go. Switching costs weren't just about the cameras; departments had years of evidence stored in Axon's cloud, officers trained on their systems, prosecutors integrated with their workflows.

The FTC's investigation revealed something even more troubling: Post-transaction, Axon has enacted substantial price increases and stopped developing new generations of VieVu products. They weren't just eliminating competition; they were actively degrading the alternative products to force migrations to Axon's platform.

But Smith had anticipated the regulatory challenge. Just before the FTC filed its administrative action, Axon filed a complaint in federal court seeking a declaratory judgment that the FTC's adjudication process was constitutionally deficient. It was an audacious move—challenging not just the merger review but the entire structure of the FTC itself.

The legal battle that followed was extraordinary. Axon argued that the FTC violates due process by trying cases in administrative hearings, with its own commissioners and judges, instead of in federal court. The case went all the way to the Supreme Court, which in April 2023 issued a unanimous decision in Axon's favor, finding district court jurisdiction over Axon's constitutional challenges to the FTC's structure and existence.

By October 2023, exhausted and facing years more litigation, the FTC threw in the towel. The Federal Trade Commission (FTC) has dismissed its administrative enforcement action against Axon Enterprise Inc., (NASDAQ: AXON), the global public safety technology leader, regarding Axon's 2018 acquisition. Unconditional dismissal follows Supreme Court's historic decision to allow Axon's constitutional challenges to the FTC's structure to proceed in federal court.

The implications were staggering. Not only had Axon successfully defended its monopolistic acquisition, but it had fundamentally weakened the FTC's ability to challenge future mergers through administrative proceedings. It was a masterclass in using constitutional litigation as an antitrust defense.

Meanwhile, the business impact was exactly what the FTC had feared. Major cities found themselves trapped. Mesa's contract, which can jump to $2.5 million annually without further council action, is nearly four times the size of the annual cost Mesa was paying in 2017 for body cameras. Scottsdale City Council is now paying Axon $850,000 annually for body cameras and its signature Taser stun gun — a 41,500% increase over the $20,000 the city was paying a decade ago.

The numbers tell the story of monopoly power in action. Phoenix alone approved a five-year $39.26 million contract for body cameras. Cities that had once played Axon and VieVu against each other for better prices now faced a single supplier with no incentive to negotiate.

But Smith wasn't celebrating the antitrust victory—he was already focused on the next phase. Because while everyone was fixated on the body camera monopoly, Axon was quietly building something far more powerful: an AI-powered platform that would make the cameras seem quaint by comparison. The VieVu acquisition wasn't the endgame; it was just clearing the field for what came next.

VI. Software Eats the World: The Cloud & AI Transformation (2018–Present)

The email arrived at 3 AM, sent from Rick Smith to his entire engineering team. The subject line read simply: "GPT-3 changes everything." It was March 2021, and Smith had just spent the weekend experimenting with OpenAI's latest language model. While the rest of Silicon Valley was using it to write poetry and code, Smith saw something different: the future of police paperwork.

Consider the daily reality of a patrol officer. After every incident—a traffic stop, a domestic dispute, an arrest—they spend hours writing reports. The average officer spends 40% of their shift on paperwork. In major cities, that translates to millions of hours annually that could be spent on actual policing. Smith's revelation was that body camera footage plus AI could eliminate most of this burden.

But first, Axon needed to own the entire evidence chain. Evidence.com had evolved far beyond its origins as a simple cloud storage service. By 2018, it had become Axon Evidence, and by 2020, simply "Axon Cloud"—a name change that signaled its transformation into a comprehensive platform. Axon Evidence is used by more than 20,000 agencies, in every state within the United States and in over 90 countries worldwide. Over 2 billion evidence files have been loaded into Axon Evidence and our cloud stores more than 400 petabytes of data.

The scale is staggering—400 petabytes is roughly equivalent to 80 million DVDs worth of data. But the real power wasn't in storage; it was in what Axon could do with that data. They built Axon Records for report writing, Axon Standards for policy management, Axon Respond for real-time operations, and dozens of other modules that transformed every aspect of police work into a software problem. The numbers told the story of transformation. Annual recurring revenue grew 37% year over year to $1.0 billion in 2024. Surpassed $2 billion in annual revenue and $1 billion in annual recurring revenue. Third consecutive year of 30%+ annual revenue growth demonstrates Axon's strong product-market fit and customer expansion. But these metrics only hinted at the real revolution happening under the hood.

The AI integration began with seemingly mundane problems. Auto-Transcribe could turn body camera audio into searchable text. Redaction software could automatically blur faces and license plates to protect privacy. These weren't headline-grabbing features, but they saved departments thousands of hours of manual work. Each feature that automated drudgery made Axon more indispensable.

Then came Draft One, launched in 2024—the product that would fundamentally change policing documentation. Using generative AI, Draft One could watch body camera footage and automatically write a police report. Not a template or outline, but a complete, detailed, legally compliant report that captured everything from the suspect's clothing to the exact sequence of events. An officer could review and edit in minutes what used to take hours to write from scratch.

The implications were staggering. If officers spent 40% of their time on paperwork, and AI could reduce that by 80%, you'd effectively increased police capacity by 30% without hiring a single new officer. For cash-strapped departments facing staff shortages, this wasn't just convenient—it was transformative.

But Smith understood something deeper: whoever controlled the AI that wrote police reports would essentially control the narrative of law enforcement. Every report would be structured according to Axon's algorithms, using Axon's language patterns, reflecting Axon's understanding of what mattered in a police encounter. It was power that no single company had ever wielded over law enforcement.

The platform strategy was working perfectly. Net revenue retention was 123% in the quarter, reflecting our ability to deliver additional value to our customers over time and de minimis attrition. This meant that existing customers were spending 23% more each year—not because Axon raised prices (though they did that too), but because departments kept adding more products, more users, more capabilities.

Recent acquisitions accelerated the platform buildout. In 2023, Axon acquired Fusus for $106 million, bringing real-time crime center technology that could integrate feeds from private security cameras, gunshot detectors, and license plate readers into a single operational view. Sky-Hero added tactical drones. Foundry 45 brought virtual reality training capabilities. The Fusus acquisition in 2024 revealed Axon's ultimate ambition. Axon, the global leader in connected public safety technologies, announced today it has acquired Fusus, a global leader in real-time crime center (RTCC) technology. Fusus excels in aggregating live video, data and sensor feeds from virtually any source, enhancing situational awareness and investigative capabilities for public safety, education and commercial customers.

This wasn't just about police cameras anymore. Fusus could integrate feeds from private businesses, schools, hospitals—essentially turning entire cities into surveillance networks feeding into Axon's platform. The Atlanta Police Department's Video Integration Center powered by Fusus had demonstrated the power: when a gunman opened fire in Midtown Atlanta in May 2023, they tracked him through multiple camera systems and jurisdictions, leading to his capture in just 8 hours.

The ethical implications were profound and largely undiscussed. Axon was building a surveillance apparatus that would make China's social credit system look primitive. But they wrapped it in the language of public safety, community partnership, and protecting life. Every crime solved, every missing person found, every officer protected became justification for expanding the network.

Future contracted bookings increased to $10.1 billion, up 42% year over year. This wasn't just revenue—it was lock-in. These were 5-to-10-year contracts that would be nearly impossible to unwind. Once a department's entire evidence chain, reporting system, and operational intelligence ran through Axon, switching to another provider would be like trying to change the foundation of a skyscraper while people were still working inside.

The gross margin evolution told the story of the business model's genius. Software gross margins exceeded 70%, while hardware margins hovered around 25%. But the hardware was essential—it created the data that fed the software, which generated the recurring revenue, which funded the R&D, which created better hardware and software, which captured more data. It was a virtuous cycle that competitors couldn't replicate without massive capital and a decade of catch-up.

Smith's vision was becoming reality. Axon wasn't just a supplier to law enforcement; they were becoming law enforcement's operating system. Every interaction between police and public would soon flow through Axon's servers, be interpreted by Axon's algorithms, and be stored in Axon's cloud. It was power that J. Edgar Hoover could only have dreamed of, privatized and publicly traded.

VII. Business Model & Unit Economics

The genius of Axon's business model becomes clear when you follow a single dollar through the system. A police department spends $490 on an Axon Body 4 camera—a one-time hardware purchase with roughly 25% gross margins. But that camera requires Evidence.com storage at $79 per officer per month. Add Axon Respond for real-time streaming. Add Auto-Transcribe. Add Redaction Assistant. Add Records management. Add Standards for policy updates. Soon that $490 camera is generating $2,000+ in annual software revenue at 70%+ margins. Multiply by five-year contract terms, and that single camera purchase has triggered $10,000+ in high-margin recurring revenue.

This is the "hardware as a trojan horse" strategy perfected. The camera isn't the product—it's the gateway drug to an entire ecosystem of software subscriptions. And once you're in, you can't get out. Net revenue retention was 123% in the quarter, reflecting our ability to deliver additional value to our customers over time and de minimis attrition. That "de minimis attrition" tells you everything—customers simply don't leave.

The bundling strategy amplifies the lock-in. Axon doesn't sell products; they sell "Officer Safety Plans" and "Productivity Bundles" that package hardware, software, warranties, and training into single subscription payments. A department doesn't buy cameras and then software—they buy "Axon Officer 4" at $199 per officer per month, which includes the camera, unlimited storage, AI transcription, and automatic hardware upgrades every 2.5 years.

This subscription model transforms capital expenditures into operating expenses, making it easier for departments to justify and budget. It also means Axon controls the upgrade cycle. When they release new cameras or features, departments automatically get them, ensuring the entire customer base stays current and engaged with the latest technology.

The unit economics are staggering. Customer acquisition cost is essentially zero for existing TASER customers—they already have the relationship, the contract vehicles, the procurement approval. The lifetime value of a customer approaches infinity because they never churn. The payback period on new customer acquisition is under 18 months, even with aggressive upfront pricing and free trials.

Capital efficiency has improved dramatically as the business has scaled. R&D spending runs at about 17% of revenue—high for a traditional hardware company but reasonable for a SaaS platform. The beauty is that R&D investments benefit the entire installed base immediately through software updates, creating compound returns on innovation spending.

The working capital dynamics are equally attractive. Customers often pay upfront for multi-year contracts, creating negative working capital. Axon gets paid before they deliver the service, using customer prepayments to fund growth. It's the same model that made Dell and Amazon so capital efficient, applied to law enforcement technology.

Manufacturing has become increasingly automated and outsourced, reducing capital intensity. The real assets are the software, the data, and the customer relationships—all of which appreciate over time rather than depreciate. This asset-light model enables enormous operating leverage as the company scales.

The pricing power is unprecedented. When you control 80% of a market with massive switching costs, you set the prices. Cities that balked at Axon's post-VieVu price increases found they had no alternatives. Even building their own systems would require years and millions of dollars, with no guarantee of achieving Axon's functionality.

Most remarkably, Axon has achieved this while maintaining the perception of being the "good guys." They're not seen as predatory monopolists but as mission-driven partners in public safety. Every price increase is justified by new features, better AI, more comprehensive solutions. Departments complain about budgets, not about Axon.

The network effects keep compounding. More departments using Axon means more shared evidence protocols, more standardized procedures, more interagency compatibility. A department choosing a competitor doesn't just get inferior technology—they get isolated from the ecosystem their peers operate in.

Looking forward, the model only gets stronger. AI capabilities will drive another wave of upselling. International expansion offers virgin markets. Enterprise and federal opportunities multiply the addressable market. And the core law enforcement business keeps growing as departments add more cameras, more storage, more capabilities.

This isn't just a good business model—it's an nearly perfect one. High margins, negative churn, minimal competition, regulatory moats, mission-critical use cases, and infinite expansion opportunities within existing customers. Warren Buffett talks about finding businesses with moats. Axon hasn't just built a moat—they've built the only bridge across it and they charge whatever toll they want.

VIII. Competitive Dynamics & Market Position

The competitive landscape in 2024 looks less like a battlefield and more like Axon's victory parade with a few stubborn holdouts refusing to acknowledge defeat. Axon currently dominates the domestic body camera market with an iron grip that tightens every quarter. But understanding how they achieved this monopoly-like position requires examining both who they've defeated and who's still trying to compete.

Motorola emerged as the most serious threat through sheer financial force. Axon's most formidable rising competitor is Motorola, which in 2019 acquired two companies that make body cameras in the U.S. and in Europe. They bought WatchGuard Video and its body camera business for $250 million, then acquired Avigilon's video business. With Motorola's deep pockets and existing relationships in public safety communications, they seemed positioned to challenge Axon's dominance.

But Motorola made a critical strategic error—they tried to compete on features rather than ecosystem. Their body cameras might match Axon's specifications, their video quality might be comparable, but they couldn't replicate the decade of software development, the AI capabilities, the evidence management ecosystem, the millions of hours of footage used to train machine learning models. Motorola was selling products; Axon was selling an operating system.

Digital Ally became a cautionary tale of what happens when you challenge Axon directly. They accused Axon of patent infringement, claiming Axon stole their auto-activation technology. Axon counter-sued, buried them in legal fees, and systematically targeted their customers with aggressive pricing and migration offers. Digital Ally's stock price collapsed from $30 to under $1. They still exist, technically, but as a zombie company subsisting on legacy contracts.

Panasonic had the technology and manufacturing prowess but lacked the stomach for a protracted fight. They'd been in the in-car video business for decades, had relationships with thousands of departments, and built solid products. But they couldn't match Axon's software capabilities or pricing aggression. By 2023, they'd essentially retreated to niche markets and international opportunities where Axon hadn't yet focused.

Utility Associates tried a different approach—positioning themselves as the open-source alternative, the anti-monopoly choice. Their pitch resonated with some IT-forward departments concerned about vendor lock-in. But open systems require technical expertise that most police departments lack. When officers struggled with compatibility issues or prosecutors couldn't access evidence, chiefs quickly learned that "open" meant "you're on your own."

The international competition revealed different dynamics. In the UK, Reveal Media held significant market share by being first and local. But as Axon entered with aggressive pricing and superior technology, Reveal found itself fighting a retreat. In Europe, various national champions emerged—Zepcam in the Netherlands, Edesix in Scotland—but none could match Axon's R&D spending or ecosystem approach.

China presented an interesting case. Companies like Hikvision had the technology and state backing to compete, but Western governments increasingly viewed Chinese surveillance technology as a security risk. Axon brilliantly positioned themselves as the "trusted" alternative, turning geopolitical tensions into competitive advantage.

The enterprise market opened a new front in the competitive war. Retailers, hospitals, schools, and private security firms needed body cameras but didn't want to be associated with "police technology." Motorola saw opportunity here, as did newer entrants like Reveal Media. But Axon's acquisition of Fusus and push into real-time crime centers gave them an integrated offering none could match.

Network effects created insurmountable barriers for new entrants. A startup might build a better camera or clever software feature, but they couldn't replicate millions of hours of training data, thousands of agency relationships, and years of procedural refinement. Venture capitalists learned this expensive lesson repeatedly—competing with Axon required not just capital but time travel.

The antitrust challenges actually strengthened Axon's position in a perverse way. Competitors hoped government intervention would level the playing field. Instead, Axon's successful constitutional challenge of the FTC created precedent that made future antitrust enforcement harder. Competitors who'd waited for regulatory salvation found themselves more isolated than ever.

Pricing became Axon's ultimate weapon. With enormous gross margins and minimal customer acquisition costs, they could undercut any competitor while remaining profitable. They'd offer free cameras to win a contract, knowing the software subscriptions would generate massive returns. Competitors matching these offers would bleed cash; Axon was investing in future recurring revenue.

The talent war tilted decisively in Axon's favor. The best engineers wanted to work on AI and computer vision problems with real-world impact. Axon could offer that plus competitive compensation funded by their monopoly profits. Competitors struggled to retain talent, creating a vicious cycle of declining innovation and market share.

Looking ahead, the competitive dynamics only favor further consolidation. Standalone body camera companies can't survive against Axon's bundle. Communications companies like Motorola must decide whether to keep subsidizing money-losing divisions. International players face the choice of selling to Axon or slowly bleeding market share.

The most likely competitor isn't another body camera company—it's a tech giant deciding police technology is strategic. Amazon, Microsoft, or Google have the resources and technology to compete. But they also have brand risks, regulatory scrutiny, and activist shareholders to consider. So far, they've chosen to partner with Axon rather than compete, integrating their cloud services and AI capabilities rather than building competing products.

This is how monopolies sustain themselves—not through illegal behavior but through legal advantages compounding over time. Axon's competitive moat isn't any single factor but the combination of technology leadership, ecosystem lock-in, customer relationships, data advantages, and financial resources. Crossing one moat only reveals another, each deeper than the last.

IX. Playbook: Lessons for Founders & Investors

The Axon playbook reads like a masterclass in monopoly building disguised as a mission to protect life. Every strategic decision, every acquisition, every product launch followed principles that founders and investors should study, whether they admire or fear the outcome.

Lesson 1: Mission-Driven Businesses Can Build Monopolies Rick Smith's genuine mission—born from personal tragedy—provided cover for aggressive monopolistic behavior. When you're "protecting life," price increases seem less predatory, competitor acquisition seems less anticompetitive, and market domination seems less problematic. The mission attracted talent, justified premium pricing, and deflected criticism. Founders take note: authentic mission alignment doesn't conflict with monopoly building—it enables it.

Lesson 2: Platform Transitions Require Patience and Capital The shift from TASER weapons to body cameras took five years of losses before breaking even. The transition from cameras to software platform took another five years. Most companies and investors lack this patience. Axon could afford it because the TASER business generated cash throughout. The lesson: use a profitable core business to fund platform transformation, and give it twice as long as you think.

Lesson 3: Own the Entire Stack Axon could have partnered for cloud storage, licensed AI technology, or outsourced hardware manufacturing. Instead, they built or acquired everything critical to their platform. This vertical integration created competitive advantages competitors couldn't replicate. When Motorola tried to compete, they found themselves dependent on the same cloud providers and AI technologies Axon had already optimized for police use cases.

Lesson 4: Data Network Effects Compound Every hour of body camera footage made Axon's AI better. Every police report refined their language models. Every use case expanded their capability set. Competitors starting today would need millions of hours of police interaction data that simply doesn't exist outside Axon's servers. The playbook: design your business so customer usage automatically creates competitive moats.

Lesson 5: Bundle to Lock In, Then Expand the Bundle Start with one critical product (TASERs), add complementary products (cameras), bundle them together (Officer Safety Plan), then keep expanding the bundle (AI, real-time, analytics). Each addition increases switching costs and customer lifetime value. The genius is making each component work better with the others than alone, creating logical lock-in rather than contractual lock-in.

Lesson 6: Acquire Competitors Before They Scale VieVu was bought for $7 million when they had momentum but no scale. Fusus was acquired before they could build an independent ecosystem. These weren't expensive acquisitions—they were monopoly insurance. The lesson: identify and eliminate threats while they're still affordable. The FTC might investigate, but as Axon proved, enforcement is difficult and slow.

Lesson 7: Turn Controversies into Product Opportunities Every police shooting without video became marketing for body cameras. Every criticism of report writing became justification for AI automation. Every privacy concern became a feature request for redaction software. Axon turned societal problems into business opportunities, positioning themselves as the solution to controversies their products partially enabled.

Lesson 8: Build Switching Costs Into Architecture It's not enough to have the best product—make it painful to leave. Store evidence in proprietary formats. Build workflows that depend on your ecosystem. Create interdependencies between products. Train entire departments on your interfaces. Make the cost of switching not just financial but operational, legal, and political.

Lesson 9: Control the Narrative Through Data Axon funds studies showing TASERs save lives and body cameras reduce complaints. They built databases of police shootings that shape public discourse. They provide data to researchers who reach favorable conclusions. The lesson: whoever controls the data controls the narrative, and whoever controls the narrative controls the market.

Lesson 10: Use Capital Markets as a Weapon Going public gave Axon currency for acquisitions, credibility with governments, and capital for R&D. Their high valuation let them invest aggressively, acquire strategically, and price predatorily while remaining profitable. Meanwhile, private competitors struggled for funding. The playbook: use public markets to create insurmountable advantages.

Lesson 11: Regulatory Capture Through Partnership Axon doesn't fight regulations—they help write them. They sit on standards committees, advise on procurement requirements, and shape certification processes. Unsurprisingly, these regulations often require capabilities that only Axon provides. The lesson: don't just comply with regulations, help create ones that favor your business model.

Lesson 12: International Expansion as Monopoly Extension Axon used U.S. dominance to fund international expansion, entering markets with proven products and unlimited capital. Local competitors couldn't match their R&D spending or ecosystem capabilities. The playbook: build monopoly in one geography, then use those profits to achieve monopoly elsewhere.

The Darker Lessons:

The Axon playbook also reveals uncomfortable truths about modern capitalism. They built a surveillance apparatus that would terrify civil libertarians, but wrapped it in public safety rhetoric. They achieved monopoly pricing power over cash-strapped municipalities, extracting enormous profits from taxpayers. They turned tragic police shootings into business development opportunities.

For investors, Axon demonstrates that the best returns come from necessary evils—products society needs but doesn't want to think about. For founders, it shows that mission-driven messaging can justify almost any competitive behavior. For society, it raises questions about whether critical infrastructure should be controlled by profit-maximizing monopolies.

The ultimate lesson might be the most troubling: in winner-take-all markets, the victors write history. Axon is no longer the controversial TASER company that fought wrongful death lawsuits. They're the "public safety technology leader" protecting life through innovation. The playbook worked so well that we've forgotten to question whether one company should wield this much power over policing.

X. Analysis & Bear vs. Bull Case

Bull Case: The Inevitable Infrastructure Play

The bulls see Axon as the Palantir of public safety—a monopolistic platform so embedded in government operations that it becomes sovereign infrastructure. With third consecutive year of 30%+ annual revenue growth, the company has proven it can maintain hypergrowth even at $2+ billion in revenue scale. This isn't a growth story slowing down; it's accelerating.

The TAM expansion opportunity is massive and multi-dimensional. Domestic law enforcement penetration remains under 50% for full platform adoption. International markets represent 10x the U.S. opportunity. Enterprise verticals—retail, healthcare, education, transportation—are just beginning adoption. Federal agencies remain largely untapped. Each vector alone could double the business; combined, they represent decades of growth runway.

The AI revolution is Axon's iPhone moment. Draft One and automated report writing will drive another complete refresh cycle as departments upgrade to AI-capable infrastructure. This isn't incremental improvement—it's fundamental transformation of police work. Departments will have no choice but to adopt or fall catastrophically behind in operational efficiency.

Insurmountable competitive advantages only strengthen over time. The data moat deepens with every hour of footage. The switching costs increase with every integrated workflow. The network effects compound as more agencies standardize on Axon. A competitor starting today would need $10+ billion and a decade to maybe reach parity with where Axon is now.

International expansion is hitting inflection. UK, Australia, and Canada are adopting at accelerating rates. European privacy concerns are being overcome by public safety needs. Even traditionally closed markets like Japan and South Korea are opening. The playbook that worked in the U.S.—land with TASERs, expand with cameras, lock in with software—translates globally.

Operating leverage is finally manifesting. After years of heavy R&D investment, incremental margins are expanding dramatically. The next billion in revenue will drop 40%+ to the bottom line. This is the harvest phase of a decade of platform building.

The acquisition pipeline provides endless growth optionality. Drones, robotics, virtual reality, real-time analytics—each adjacent market is ripe for Axon's playbook. They have the capital, customer relationships, and platform to roll up the entire public safety technology sector.

Valuation remains reasonable for the growth profile. At 15x revenue, Axon trades at a discount to high-growth SaaS peers despite better unit economics, lower churn, and a larger moat. As the market recognizes this is a software company with some hardware, not vice versa, multiple expansion is inevitable.

Bear Case: The Icarus Complex

The bears see a company flying too close to the sun, with multiple existential risks converging. Regulatory and antitrust risks loom large. The FTC loss was tactical, not strategic. Congressional scrutiny is intensifying. State attorneys general are mobilizing. International regulators are awakening. One successful antitrust action could force divestiture, price controls, or competitive remedies that destroy the business model.

Market saturation in core U.S. law enforcement is real. Major cities have cameras. Most departments have TASERs. The easy growth is behind them. Remaining departments are smaller, budget-constrained, and less sophisticated. Growth requires either price increases that trigger backlash or expensive international expansion with uncertain returns.

Privacy and civil liberties backlash is building. The surveillance apparatus Axon enables is becoming unconscionable to growing segments of society. Portland's resistance to body cameras isn't an anomaly—it's a leading indicator. One high-profile misuse of AI or surveillance overreach could trigger a societal rejection of Axon's entire premise.

Competition from tech giants is inevitable. Amazon, Microsoft, or Google entering the market would change everything. They have deeper pockets, better AI, and existing government relationships. Axon's moat might be wide, but it's not wider than Big Tech's resources. The question isn't if but when they decide this market matters.

The business model depends on government spending that may not sustain. Police budgets face pressure from both defunding movements and fiscal constraints. Cities choosing between teachers and cameras might choose teachers. Federal spending is increasingly unpredictable. International customers might build domestic alternatives for sovereignty reasons.

Valuation concerns are significant at current multiples. At $58 billion market cap on $2 billion revenue, Axon is priced for perfection. Any growth deceleration, margin compression, or competitive threat could trigger massive multiple compression. The stock has 50%+ downside if it trades at mature technology multiples.

Technical disruption remains possible. Open-source alternatives, blockchain evidence management, or quantum encryption could obsolete Axon's platform. Their R&D spending is high but not infinite. A technical paradigm shift they don't see coming could strand their entire infrastructure investment.

Management key person risk is extreme. Rick Smith IS Axon. His vision, relationships, and credibility built this business. His departure would be catastrophic. There's no clear successor, no proven second act. This is a founder-dependent company trading at founder-independent valuations.

The Verdict:

The bull case is compelling but requires everything to go right—continued execution, regulatory forbearance, competitor complacency, and societal acceptance of surveillance. The bear case has multiple paths to materialization, any one of which could devastate the stock.

The asymmetry favors the bears at current valuations. The upside might be 2-3x over five years if all goes perfectly. The downside is 70%+ if any major risk materializes. For a company this controversial, this dominant, this exposed to regulatory intervention—that's not an attractive risk/reward.

The truth likely lies between extremes. Axon will probably continue growing, but at decelerating rates. They'll face increased scrutiny but avoid catastrophic intervention. Competition will emerge but not dominate. The stock will generate positive but not spectacular returns.

For society, the bigger question isn't whether Axon is a good investment, but whether we're comfortable with one company having this much control over policing, surveillance, and public safety. That's a question the market won't answer, but democracy must.

XI. Epilogue & "If We Were CEOs"

If we were running Axon today, the strategic choices would be fascinating and morally complex. The company stands at an inflection point where every decision shapes not just shareholder returns but the future of policing, surveillance, and civil society.

First Priority: International Expansion with Localization We'd accelerate international growth but with a crucial twist—local partnerships and data sovereignty. Create Axon Europe, Axon Asia, Axon LatAm as semi-autonomous entities with local data centers, local leadership, and local customization. This addresses sovereignty concerns while maintaining platform advantages. The playbook: think McDonald's franchising, not Uber colonization.

Second Priority: Open Up the Platform (Strategically) The monopoly backlash is building. We'd preempt it by opening APIs, publishing standards, and enabling interoperability—but carefully. Create an "Axon Connect" ecosystem where competitors can integrate but must pay for access. This maintains control while deflecting antitrust criticism. Think Apple's App Store: open enough to avoid regulation, closed enough to maintain dominance.

Third Priority: Acquire the AI Layer We'd make a massive acquisition in AI—not another police tech company but a core AI capability. Acquire Anthropic, Cohere, or a similar foundation model company. This would give Axon proprietary AI that competitors can't access, accelerating the moat. The integration of genuine AI research capabilities would transform every product and create insurmountable technical advantages.

Fourth Priority: Launch Axon Federal The federal opportunity is massive but requires different approaches. Create a dedicated division with security clearances, FedRAMP certification, and D.C. presence. Target DoD, DHS, FBI, and intelligence agencies with customized offerings. The margins are lower but the contracts are massive and sticky. This diversifies customer concentration and reduces local government dependence.

Fifth Priority: Build the Consumer Brand The enterprise expansion into retail, healthcare, and education requires a different brand perception. Launch "Axon Protect"—consumer-friendly security products for businesses and eventually homes. This isn't about revenue initially; it's about normalizing surveillance technology and building societal acceptance. Make Axon synonymous with safety, not just policing.

The Ethical Hedging Strategy: We'd also build in ethical safeguards that actually protect the business long-term. Create an independent privacy board with real power. Implement algorithmic auditing. Publish transparency reports. Fund civil liberties research. This isn't altruism—it's insurance against the techlash that destroyed Facebook's reputation and triggered regulatory intervention.

The Capital Allocation Revolution: With massive free cash flow generation ahead, we'd implement an aggressive capital return program. Large special dividends would reward shareholders while reducing the capital available for potentially value-destructive acquisitions. A meaningful buyback program would offset dilution and support the stock. This financial discipline would force operational efficiency.

The Succession Solution: Rick Smith can't run Axon forever. We'd recruit a world-class COO from enterprise software—someone from Salesforce, Microsoft, or Oracle who understands platform dynamics. Give them P&L responsibility and public visibility. Create a graceful transition plan that maintains founder involvement while ensuring continuity.

The Innovation Imperative: We'd 10x R&D spending but focus it narrowly. Don't try to build everything—build the things that matter. Quantum-resistant encryption for future-proofing. Edge AI for real-time processing. Behavioral prediction algorithms (with careful ethical constraints). Patent everything aggressively. Make the technical moat so deep that even Big Tech would rather partner than compete.

The Regulatory Offense: Instead of playing defense on regulation, we'd go on offense. Propose federal standards for police technology that we already meet but competitors don't. Advocate for mandatory body cameras with specific technical requirements. Push for AI auditing standards we've already implemented. Use regulation as a competitive weapon while appearing civic-minded.

The Ultimate Vision: The end state would be Axon as the "Microsoft of Public Safety"—an essential platform that everyone uses, complains about, but can't leave. Diversified across geographies, customer types, and products. Generating $10+ billion in annual free cash flow. Trading at 30x earnings as a stable, dividend-paying, monopolistic platform.

The Questions We'd Wrestle With:

But running Axon would mean confronting uncomfortable questions daily. Are we making society safer or just more surveilled? Does our technology reduce police violence or just document it better? Are we empowering communities or creating digital panopticons?

The hardest decision would be where to draw lines. Should Axon's AI predict crime? Should it identify suspects? Should it assess threat levels? Each capability is technically feasible and potentially profitable, but the societal implications are staggering.

We'd probably implement a "10-year test"—would we be comfortable with our children living in a world where this technology is ubiquitous? If not, don't build it, regardless of the revenue potential. This long-term thinking might reduce short-term profits but would ensure the business remains socially sustainable.

The ultimate realization: Axon's CEO isn't just running a business but architecting the future of policing and public safety. That's a responsibility that transcends quarterly earnings and stock prices. It requires balancing shareholder returns with societal impact, growth with governance, innovation with introspection.

If we were CEOs, we'd build Axon into an unstoppable business machine while somehow maintaining its social license to operate. Whether that's actually possible—whether any company should have this much power over public safety—remains the question nobody wants to answer but everybody needs to confront.

The final thought: Axon will shape how billions of people interact with law enforcement over the coming decades. That's either the greatest business opportunity of our time or a responsibility too great for any single company to bear. Probably both.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube