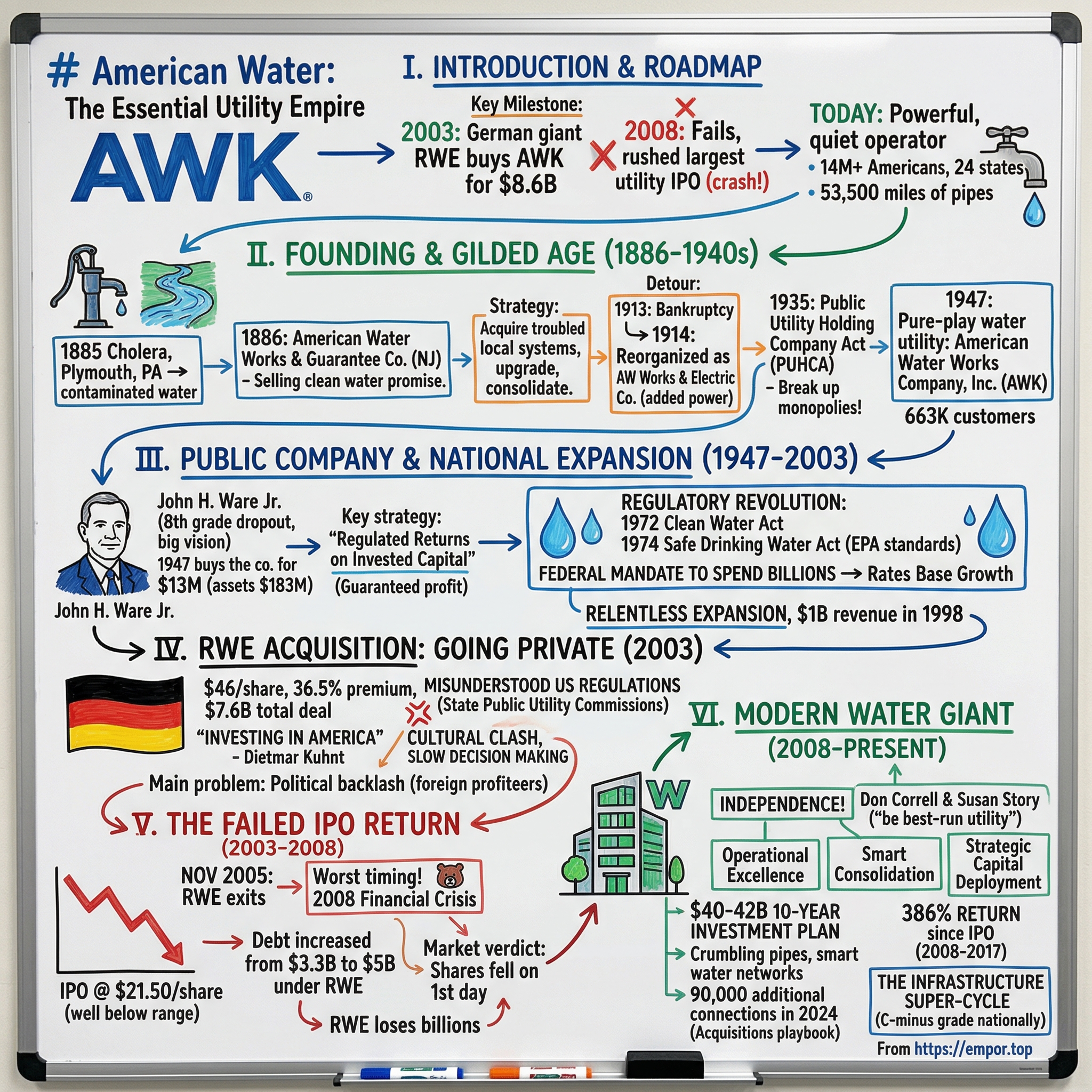

American Water: The Essential Utility Empire

I. Introduction & Episode Roadmap

Picture this: It's 2003, and German energy giant RWE is convinced they're about to crack America's water market. They shell out $8.6 billion for American Water Works, betting that privatizing water utilities across the United States will yield European-style returns. Five years later, they're rushing for the exits, launching the largest utility IPO in U.S. history just as Lehman Brothers is collapsing. The Germans lost billions. The Americans? They got their water company back—and then some.

Today, American Water (AWK) quietly operates as one of the most powerful companies you've never thought about. They deliver water and wastewater services to more than 14 million Americans across 24 states. When you turn on your tap in New Jersey, Pennsylvania, or California, there's a decent chance the water flowing out passed through their 53,500 miles of pipes, treated at one of their 80 surface water plants or 480 groundwater facilities. They're the largest publicly traded water utility in America, and in a country where the infrastructure is literally crumbling beneath our feet, they're sitting on a goldmine of necessary investment.

But here's the fascinating part: American Water isn't some Silicon Valley unicorn or private equity rollup. This company traces its roots to 1886, when post-Civil War entrepreneurs were racing to bring clean water to America's booming industrial cities. Through world wars, the Great Depression, multiple ownership changes, and a spectacularly failed foreign takeover, they've not only survived—they've thrived by mastering the most boring, capital-intensive, highly regulated business model imaginable.

The story of American Water is really three stories wrapped into one. First, it's a tale of how essential infrastructure creates natural monopolies that endure for centuries. Second, it's a masterclass in navigating the bizarre dance between private capital and public regulation. And third—perhaps most relevant today—it's a preview of the $1 trillion infrastructure super-cycle that's about to remake America's physical foundations.

Over the next few hours, we're going to trace this journey from the muddy streets of 1880s Pennsylvania to today's climate-resilient smart water networks. We'll explore how a collection of local water pumps became a continental empire, why the Germans failed so spectacularly, and what it means that America's water infrastructure grades out at a C-minus while this company prints 7-9% earnings growth like clockwork.

Along the way, we'll unpack the regulatory framework that turns capital expenditure into guaranteed profits, examine the consolidation playbook that's added 90,000 customer connections just last year, and wrestle with the fundamental question: Should water—the most essential resource for human life—be a for-profit enterprise? The answer, as we'll see, is far more nuanced than either side wants to admit.

So grab a glass of water (check if it's from American Water first), and let's dive into the improbable story of how a 138-year-old utility became one of the most reliable wealth compounders in American capitalism. Because in a world obsessed with disruption, sometimes the real money is in the things that absolutely, positively cannot be disrupted.

II. Founding & The Gilded Age Origins (1886–1940s)

The cholera outbreak of 1885 killed over 1,000 people in Plymouth, Pennsylvania. Bodies piled up faster than they could be buried. The culprit? Contaminated water from the Susquehanna River, pumped directly into homes without treatment. This wasn't unusual—most American cities in the 1880s drew water from polluted rivers, with predictable results. Typhoid, dysentery, and cholera swept through urban neighborhoods like wildfire. Into this public health catastrophe stepped a group of New Jersey entrepreneurs who saw opportunity where others saw only tragedy.

On January 21, 1886, they incorporated the American Water Works & Guarantee Company in New Jersey. The name itself tells you everything about their ambition—not just "water works" but "guarantee." They weren't selling water; they were selling the promise of not dying from it. The founders understood something profound: In the aftermath of the Civil War, as America urbanized at breakneck speed, clean water wasn't a luxury—it was the foundation upon which modern cities could exist.

The company's early strategy was brilliantly simple. Rather than compete with municipalities to build water systems from scratch, they targeted struggling local water companies that lacked capital or expertise. Town by town, system by system, they acquired, upgraded, and consolidated. By 1900, they operated water utilities in Pennsylvania, Ohio, Indiana, and beyond. Each acquisition followed the same playbook: purchase a troubled system, invest in treatment technology, raise rates to cover improvements, and use the cash flow to fund the next deal. But the real genius appeared in 1914, when the company emerged from its first major crisis. Hit by overextension into western irrigation projects that failed spectacularly, American Water Works & Guarantee Company was declared bankrupt in 1913. Most companies would have died right there. Instead, in 1914, the reorganized entity emerged as American Water Works and Electric Company, adding electricity to its portfolio and quickly growing into one of the leading public utility holding companies in the United States.

This wasn't just a name change—it was a fundamental reimagining of what a utility company could be. The Kuhn brothers, who orchestrated the reorganization, understood that water and electricity shared the same fundamental economics: massive upfront capital requirements, natural monopoly characteristics, and predictable cash flows once established. By combining both, they could spread fixed costs, share infrastructure, and most importantly, access deeper capital markets.

The 1920s saw American Water Works and Electric become a holding company octopus, with tentacles reaching into dozens of states. They owned water systems in Pennsylvania, New Jersey, Ohio, Indiana, Illinois, Missouri, and California. They controlled electric utilities from West Virginia to Washington state. At their peak, they operated through a byzantine structure of subsidiaries, sub-subsidiaries, and affiliated companies that would make today's private equity firms blush. But then came the reckoning. The Public Utility Holding Company Act of 1935 (PUHCA), also known as the Wheeler-Rayburn Act, was a US federal law giving the Securities and Exchange Commission authority to regulate, license, and break up electric utility holding companies. It limited holding company operations to a single state, thus subjecting them to effective state regulation. It also broke up any holding companies with more than two tiers, forcing divestitures so that each became a single integrated system serving a limited geographic area. American Water Works & Electric Company was a prime example of the type of company the 1935 law was intended to abolish. Whereas American Water Works Company's predecessor was broken up by the Public Utilities Act of 1935 because of its size and stranglehold on the market, the younger behemoth followed in the footsteps of its elder.

The company spent the next twelve years fighting and ultimately complying with the forced divestiture. Electric operations were spun off. Water systems were consolidated. Layer upon layer of holding company structures were unwound. Finally, in 1947, American Water Works Company, Inc. emerged from the wreckage as a pure-play water utility, publicly traded with the ticker symbol AWK and a base of 663,000 customers.

John Ware, the company's new president, faced a simple choice: die a slow death as a regulated utility in a handful of states, or figure out how to grow within the new regulatory constraints. He chose growth, but growth of a different kind. Instead of the freewheeling expansion of the holding company era, American Water would perfect the art of regulated utility operations—buying small systems, investing in infrastructure, earning regulated returns, and repeating the cycle. It was boring. It was capital-intensive. And it would prove to be brilliantly profitable.

III. The Public Company Years & National Expansion (1947–2003)

John H. Ware Jr. was an eighth-grade dropout who saw opportunity where others saw only aging pipes and regulatory headaches. In 1947, when American Water Works came up for auction following its forced reorganization, most potential buyers balked at the $183 million in assets—much of it decrepit infrastructure requiring massive capital investment. Ware scraped together $13 million in capital and submitted the only bid at $8 per share. He invested the entire $13 million and won a company with assets of $183 million, though some of the company's water works facilities and pipelines were broken down and decrepit. The once mighty holding company had become an aging vestige of a bygone era; American Water Works, with operating revenues of $24 million for the year, joined Ware's burgeoning resources with little fanfare in 1947.

The previous managers left with Ware's purchase of the company, and he brought in his own management team that included Lawrence T. (Bill) Reinicker and John J. (Jack) Barr. Reinicker was skilled as an operations manager, while Barr was Ware's financial expert. This trio would transform American Water from a collection of rust and hope into the largest water utility in America.

Ware's genius lay not in financial engineering but in understanding the fundamental economics of water utilities. Unlike electricity, which could be generated anywhere, water was inherently local—you needed the source, the treatment, and the distribution all in proximity. This meant thousands of small, inefficient systems across America, most too small to afford modern treatment technology or proper maintenance. Ware's strategy was elegantly simple: buy these systems, invest in upgrades, spread the costs across a larger customer base, and earn regulated returns on every dollar invested.

The regulatory framework that emerged in the 1950s and 1960s became Ware's money machine. State public utility commissions allowed water companies to earn a specified return on their "rate base"—essentially, the value of their invested capital. The more you invested, the more you could earn. It was capitalism with training wheels: guaranteed returns for necessary investment. Ware bought and sold smaller water companies at a fast pace during his first few years. Where cities wanted to own and operate their own water systems, he divested, sometimes after bitter feuds; where municipal utility operations were too small to grow or to remain afloat on their own, he acquired them and, where new projects were needed, Ware stepped in with his company's deep financial pockets to establish viable water systems. The 1970s brought a regulatory revolution that would fundamentally reshape American Water's business model. The Federal Water Pollution Control Act of 1948 was the first major U.S. law to address water pollution. Growing public awareness and concern for controlling water pollution led to sweeping amendments in 1972. As amended in 1972, the law became commonly known as the Clean Water Act (CWA). Then came the Safe Drinking Water Act, signed into law by President Gerald Ford in 1974, the first piece of legislation of its kind to provide a comprehensive regulatory framework for overseeing the nation's drinking water supply. Signed into law in 1974, the SDWA grants the EPA the power to set national health standards for drinking water "to protect against both naturally-occurring and man-made contaminants that may be found in drinking water".

For many water utilities, these new regulations were a death sentence—the cost of compliance would bankrupt them. For American Water, it was Christmas morning. Every mandated upgrade, every required treatment system, every new monitoring device went straight into the rate base, earning that guaranteed return. The company that had mastered the art of turning capital into regulated profits now had a federal mandate to spend billions.

By 1963, American Water Works and Ware's company, Northeastern Water Company, officially merged into one nationwide utility giant. The company methodically expanded its footprint, acquiring systems in state after state. Each acquisition followed the same playbook: identify a struggling municipal system or small private operator, negotiate a purchase price based on depreciated book value, invest heavily in upgrades, file for rate increases to cover the investment plus a return, and use the cash flow to fund the next acquisition.

The numbers tell the story of relentless expansion. In 1976, the company relocated its headquarters from Philadelphia to Voorhees, New Jersey, signaling its transformation from a Pennsylvania-centric operation to a truly national player. By 1989, operating revenues had reached $528 million, with the company having sold more than 211 million gallons of water to 1.5 million customers. In 1995, expansion projects consumed more than $331 million for that year alone, and operating revenues hit $803 million. The company was included in Standard & Poor's MidCap 400 Index, a validation of its financial prowess.

In 1996, the company's Pennsylvania unit executed the industry's largest asset acquisition, for $409 million, to buy Pennsylvania Gas and Water Company's water holdings, supplying water to Scranton, Wilkes-Barre, and the surrounding areas. By 1998, American Water crossed a symbolic threshold: The company surpassed the billion dollar mark, with operating revenues of $1.02 billion.

But beneath this growth story, tectonic plates were shifting. Across the Atlantic, European utility giants were eyeing the fragmented American water market with increasing interest. They saw what American Water had built—a continental platform in the world's largest economy—and they wanted in. The stage was set for one of the most spectacular foreign acquisitions, and subsequent failures, in utility history.

IV. The RWE Acquisition: Going Private (2003)

September 17, 2001. Six days after the World Trade Center fell, as America reeled from the worst terrorist attack in its history, executives at RWE AG, the German energy conglomerate, made an announcement that seemed tone-deaf at best, opportunistic at worst. "Rather than delay, we are making this announcement today because we believe it is more important than ever to show the world that we are investing in America," declared RWE's CEO Dietmar Kuhnt.

The deal was staggering in its ambition. RWE would pay $46.00 in cash per American Water share, or a 36.5% premium to the average closing price over the 30 trading days ended September 10, 2001. The proposed transaction had a total equity value of $4.6 billion, and an enterprise value of $7.6 billion including the assumption of approximately $3.0 billion in debt. For perspective, this was the largest water utility acquisition in history, executed at the peak of the dot-com bubble's aftermath when everyone else was running for the exits.

RWE wasn't just buying a water company; they were buying a vision of the future. The Germans had already spent £6.1 billion ($8.9 billion) acquiring Thames Water in 2000, creating the world's third-largest water company. Now, with American Water in the fold, they would control water services for 70 million people across 46 countries. The plan was breathtakingly simple: take the operational excellence of German engineering, combine it with the financial sophistication of Thames Water, and apply it to the fragmented American water market. Privatization was sweeping the globe. Water was the new oil. What could go wrong?

Dietmar Kuhnt proclaimed: "In addition to providing us with a top position in the US, the acquisition of American Water will further establish RWE as a global leader in the provision of water services. The development of RWE's world-class water business in turn will provide greater balance to our core utility portfolio and allow us to deliver enhanced growth and shareholder value."

Behind the corporate speak, RWE's strategy was clear: they believed American water utilities were dramatically undervalued because American management was too conservative, too focused on regulatory compliance rather than profit maximization. European water companies earned returns on equity of 15-20%. American utilities were content with 10-12%. RWE saw that gap as pure opportunity.

On January 10, 2003, after more than a year of regulatory approvals, the acquisition was completed. Each outstanding share of American Water Works' common stock was converted into the right to receive $46.00 per share without interest. Thames Water's CEO Bill Alexander was appointed Chairman, President and CEO of American Water effective immediately, a role he would hold in addition to his current responsibilities as CEO of Thames Water plc.

The cultural clash was immediate and brutal. American Water's headquarters in Voorhees, New Jersey, suddenly found itself reporting to executives in London who reported to executives in Essen, Germany. Decision-making that once took days now took weeks. Investment proposals that would have been rubber-stamped under American ownership got lost in translation—literally and figuratively—as they worked their way through the European bureaucracy.

But the real problem wasn't culture; it was politics. RWE had fundamentally misunderstood the American regulatory environment. In Europe, privatized water companies operated under relatively stable regulatory frameworks with predictable returns. In America, every rate increase, every acquisition, every major capital investment required approval from state public utility commissions—political bodies appointed by governors and confirmed by legislatures. And those commissioners quickly realized that a German company extracting profits from American ratepayers was political poison.

The backlash was swift and merciless. Consumer advocates painted RWE as foreign profiteers extracting wealth from American communities. Local politicians, sensing opportunity, demanded investigations into every rate increase request. State regulators, who had been relatively accommodating to the Ware family's American-owned company, suddenly discovered newfound skepticism about infrastructure investment plans. In Illinois, the attorney general launched an investigation into American Water's rates. In California, regulators rejected a proposed acquisition. In Indiana, lawmakers introduced legislation to study "repatriating" water utilities to American ownership.

RWE's response was to double down. They increased dividend payments to the parent company, extracting cash to service the massive debt they'd taken on for the acquisition. They pushed for more aggressive rate increases to juice returns. They pursued larger acquisitions to gain economies of scale. Each move only intensified the political resistance.

By 2005, the dream was dead. RWE had discovered what every foreign company that tries to buy American infrastructure eventually learns: owning politically sensitive assets in America as a foreign entity is like painting a target on your back. The profits they'd projected never materialized. The acquisitions they'd planned were blocked. The operational synergies they'd promised evaporated. They never saw the heady profits they anticipated.

V. The Failed Foreign Ownership & IPO Return (2003–2008)

November 2005 marked the beginning of the end. RWE announced its intention to exit its water activities in both the US and UK, admitting what everyone in the industry already knew: the grand experiment had failed. RWE announced plans to divest American Water, and in November announced plans to divest both American Water and U.K. water business Thames Water.

The decision to pursue an IPO came in March 2006. The executive board of RWE AG decided to pursue an initial public offering (IPO) in the U.S. for the shares of American Water as the most attractive option for RWE and the U.S.-based company, its employees and customers. This decision will return American Water to its status as a publicly-traded company. The IPO will result in a publicly-traded company that's focused on water and wastewater in the U.S. and dedicated to maintaining a high level of service and quality.

But the timing couldn't have been worse. As RWE prepared for the IPO through 2007 and early 2008, storm clouds were gathering over the global financial system. Bear Stearns collapsed in March 2008. Credit markets were freezing. Investors were fleeing to safety. And here was RWE, trying to sell America's largest water utility into the teeth of what would become the worst financial crisis since the Great Depression.

The numbers tell the story of desperation. As recently as April 1, RWE had hoped to sell 64 million shares at $24 to $26 per share. By April 22, 2008, reality had set in. American Water announced its initial public offering of 58 million shares of common stock priced at $21.50 per share—well below the initial range.

April 23, 2008: In the largest utility IPO in the United States history, American Water divests from RWE's outside ownership and joins the New York Stock Exchange. It was the largest utility IPO in U.S. history. The IPO raised $1.25 billion, but there was a catch—all the proceeds went to RWE. American Water itself received nothing.

The debt situation was even more damning. When RWE purchased American Water Works five years ago, AWK had approximately $3.3 billion in debt. The public AWK in 2008 will have $5 billion in debt. It appears that a portion of the increased debt over the past five years has been due to RWE laying debt onto the back of AWK in order to fund payouts to RWE.

The market's verdict was swift and brutal. American Water becomes the first IPO since March to see its share price fall below its offer price on the first trading day. Trading under the ticker AWK, its shares closed Wednesday at $20.60, down 90 cents or 4.2 percent.

For RWE, the math was catastrophic. With 160 million shares outstanding, the IPO values American Water at $3.4 billion - less than RWE paid five years ago. And the IPO doesn't end RWE's ties to American Water, because it still retains 64 percent of the shares. They had paid $7.6 billion including debt in 2003. Five years later, after extracting dividends and loading the company with debt, they were selling at a multi-billion dollar loss.

The denouement dragged on for another year. RWE continued to unload shares through secondary offerings, each one acting as an overhang on the stock price. RWE plans on divesting themselves of their 60% stake in AWK as soon as possible (meaning right around that 180 day mark). Expect heavy future overhang here as RWE Aqua will be divesting approximately 90 million more shares of AWK sometime in late 2008.

Finally, in 2009, the cord was cut. American Water gains full independence after its final stock offering. RWE was gone, having lost billions on their American adventure. Thames Water would later be sold to Macquarie for £8 billion, eventually ending up in financial distress itself.

The lesson was clear: Water isn't oil. It isn't electricity. It's the most politically sensitive, locally controlled, heavily regulated utility service in America. Foreign ownership of American water systems triggers a visceral reaction that no amount of operational excellence can overcome. RWE learned this lesson at a cost of several billion dollars. American Water, battered but independent, was about to show the world what it could do when freed from foreign control.

VI. Building the Modern Water Giant (2008–Present)

The conference room at American Water's Voorhees headquarters was silent as CEO Don Correll addressed his senior team in May 2008, just weeks after the IPO. "Ladies and gentlemen," he said, "we're no longer somebody's subsidiary. We're no longer somebody's cash cow. We're an American company serving American communities. Now let's act like it."

The transformation was immediate and profound. Gone were the weeks of waiting for approval from Essen. Gone were the extraction dividends to fund European adventures. In their place emerged a laser focus on what American Water had always done best: buying, upgrading, and operating water systems across America.

The first strategic masterstroke came from an unexpected direction—the U.S. military. In 2003, American Water established the American Water Military Services Group, which partners with the Department of Defense through the Utilities Privatization (UP) Program. By 2008, this division was managing water and wastewater systems at 18 military installations under 50-year contracts. It was the perfect business: long-term, predictable, backed by the full faith and credit of the United States government. But the real revolution came from Susan Story, who became CEO in May 2014 after serving as CFO for one year. Story, a nuclear engineer who'd spent 31 years at Southern Company, brought a utility operator's mindset to a company that had been treated as a financial asset for too long. Her mandate was simple but profound: American Water would be the best-run utility in America, period.

Under Story and her successor, the strategy crystallized around three pillars. First, operational excellence—running the most efficient water systems in the industry. Second, smart consolidation—acquiring systems where American Water could add value through scale and expertise. Third, strategic capital deployment—investing aggressively in infrastructure while earning regulated returns.

The numbers from this era tell a story of relentless execution. By 2021, American Water was investing over $2 billion annually in infrastructure. The company added thousands of customer connections each year through both organic growth and acquisitions. Most importantly, they proved that a water utility could deliver consistent, predictable growth while serving a critical public need.

The strategic focus became even clearer in 2021 when American Water agreed to sell its Homeowner Services Group to funds advised by Apax in a deal valued at approximately $1.275 billion. Under the agreement, American Water received $485 million in cash, inclusive of $5 million for a working capital adjustment, and a $720 million secured Seller Note bearing a 7% annual interest rate with a five-year term. The message was unmistakable: American Water was exiting non-core businesses to focus exclusively on its regulated water and wastewater operations. The scale of investment tells the story. With a decade-long capital investment plan of $40–$42 billion, the company is betting big on resilient systems to address crumbling pipes, outdated treatment facilities, and the growing demands of 14 million customers. The $40–$42 billion investment—equivalent to roughly $4 billion annually—targets two main areas: pipe replacement and treatment facilities. This massive infrastructure investment isn't just about maintenance—it's about riding a generational wave of necessary spending that the American Society of Civil Engineers estimates will require over $1 trillion nationally over the next two decades.

The company also became a member of the Dow Jones Utility Average, the only water utility in the index—a recognition of its financial stability and importance to the American economy. Military operations expanded to new bases. State after state approved rate increases to fund infrastructure investment. The consolidation machine kept churning, adding tens of thousands of customer connections annually. The most recent chapter in American Water's expansion story came in July 2025, when American Water announced an agreement to acquire Nexus Water Group, which operates in eight states and has about 87,000 customer connections under agreement. Actually, based on the more detailed reports, the acquisition would add nearly 47,000 customer connections within American Water's existing footprint in Illinois, Indiana, Kentucky, Maryland, New Jersey, Pennsylvania, Tennessee and Virginia for a total of approximately $315 million, subject to adjustment as provided for in the purchase and sale agreement.

"Through this transaction, we will grow in eight of our existing regulated states and leverage our scale and size to deliver safe, clean, reliable and affordable water and wastewater services to nearly 47,000 new customer connections," said John Griffith, President and CEO of American Water.

The company has become a compounding machine, turning America's infrastructure crisis into steady, predictable returns. Since the 2008 IPO at $21.50, the stock has returned 386% through 2017—more than three-and-a-half times the S&P 500's return. And this isn't speculation or multiple expansion—it's the mechanical result of investing billions in infrastructure at guaranteed returns, year after year after year.

VII. The Business Model & Regulatory Framework

To understand American Water's business model is to understand one of capitalism's great paradoxes: a for-profit monopoly that exists with the full blessing—indeed, the active encouragement—of the government. It's a model so counterintuitive that it shouldn't work, yet it's generated wealth for over a century.

Here's how the magic works. Every water utility operates under the jurisdiction of state public utility commissions (PUCs), political bodies that control virtually every aspect of the business. These commissions determine what rates you can charge, what returns you can earn, where you can operate, and what investments you can make. In exchange for submitting to this regulatory straitjacket, utilities receive something invaluable: a monopoly franchise with guaranteed returns on invested capital.

The key concept is the "rate base"—essentially, the net book value of a utility's property, plant, and equipment. When American Water invests $100 million in new pipes, treatment plants, or pumping stations, that $100 million goes into the rate base. The PUC then allows the company to earn a specified return on that rate base, typically 9-10% on equity. This return is built into the rates customers pay. More investment equals a bigger rate base equals higher allowed earnings. It's that simple.

But here's where it gets interesting. Unlike normal businesses, where competition and market forces determine returns, regulated utilities have their profits essentially guaranteed by law. If costs go up, they file for a rate increase. If they need to invest in infrastructure, they get pre-approval and recover the costs plus a return. The risk isn't whether they'll make money—it's whether regulators will allow them to make as much as they want.

According to the EPA's 2023 national needs assessment, America needs $625 billion over the next 20 years to reach a state of good repair. Water utilities nationwide will need to spend $625 billion over the next 20 years to fix, maintain, and improve the country's water infrastructure. The two surveys together—one focused on wastewater and stormwater and the other on drinking water systems—indicate a total infrastructure funding deficit greater than $1.2 trillion over the next two decades.

This infrastructure crisis is American Water's opportunity. Every dollar of that trillion-dollar need that flows through American Water's systems is a dollar that goes into the rate base, earning returns in perpetuity. The company isn't just fixing pipes—it's building an earnings engine that will generate returns for decades.

The regulatory compact works like this: American Water proposes investments in infrastructure, demonstrating need based on aging systems, regulatory requirements, or growth. The PUC reviews the proposal, often with input from consumer advocates and other stakeholders. If approved, American Water makes the investment, then files a rate case to recover the costs plus the allowed return. Rates go up, American Water earns its return, and the cycle repeats.

This system creates fascinating incentives. American Water is actually incentivized to spend more, not less, on infrastructure—the opposite of most businesses. Efficiency improvements that reduce capital needs actually hurt earnings. It's a world where spending money makes money, as long as regulators approve.

The company operates through subsidiaries in 14 states, each with its own regulatory framework. Pennsylvania American Water, New Jersey American Water, Missouri American Water—each is a separate regulated entity with its own rate cases, its own rate base, and its own relationship with regulators. This diversification reduces risk; a adverse regulatory decision in one state doesn't sink the entire company.

But the real genius of American Water's model is how it's positioned itself within this framework. By being the largest and most sophisticated operator, they have advantages smaller utilities can't match. They have teams of regulatory experts who know how to navigate the rate case process. They have the balance sheet to fund massive capital programs. They have the operational expertise to run systems efficiently while still maximizing rate base growth.

The Military Services Group represents a variation on the theme—instead of state regulators, they deal with the Department of Defense, but the principle is the same: long-term contracts with built-in returns for infrastructure investment. The 50-year contracts at military bases are essentially permanent rate base additions with federal backing.

Environmental regulations add another layer to the model. The Clean Water Act (CWA) and Safe Drinking Water Act (SDWA) grant the EPA the power to set national health standards for drinking water "to protect against both naturally-occurring and man-made contaminants that may be found in drinking water". Every new EPA standard—for PFAS, lead, or other contaminants—requires infrastructure investment. For small utilities, these mandates are crushing burdens. For American Water, they're opportunities to deploy capital at guaranteed returns.

The ESG angle has become increasingly important. Water is inherently an environmental, social, and governance issue. American Water provides an essential service, protects public health, and operates under strict regulatory oversight. The company ranks among Barron's 100 Most Sustainable U.S. Companies and has appeared five times on the Bloomberg Gender-Equality Index. This positioning attracts ESG-focused investors while providing political cover for rate increases.

The customer mix adds stability. Residential customers provide steady, predictable demand—people need water regardless of economic conditions. Commercial and industrial customers offer higher margins and growth potential. The geographic diversity across 14 states means local economic downturns don't devastate results.

But perhaps the most underappreciated aspect of the model is its inflation protection. Rate cases typically include mechanisms to pass through increasing costs. As inflation drives up the cost of pipes, chemicals, and labor, those costs flow through to customers via rate adjustments. The rate base itself is constantly growing through new investment, providing a natural hedge against inflation.

The model isn't without challenges. Regulatory lag—the time between when costs are incurred and when they're recovered through rates—can pressure earnings. Political pressure to keep rates low can constrain returns. Climate change and extreme weather events can damage infrastructure faster than it can be replaced.

Yet for over a century, through wars, recessions, technological revolutions, and political upheavals, the model has endured. Water remains essential. Infrastructure continues aging. Regulations keep tightening. And American Water keeps investing, earning its regulated returns, and compounding wealth with the reliability of a Swiss watch.

VIII. Financial Performance & Capital Allocation

The numbers tell a story of relentless execution. In 2024, American Water reported earnings of $5.39 per share, up from $4.90 per share in 2023, and recorded a dividend growth of 8.1% for the year. The company has maintained its long-term EPS and dividend growth targets of 7-9%. It allocated $3.3 billion in capital towards addressing aging infrastructure, improving water quality, enhancing resiliency, and completing strategic acquisitions, which led to nearly 90,000 additional customer connections, 69,500 of which were through acquisitions.

In the first quarter of 2025, earnings were reported at $1.05 per share, up from $0.95 per share during the same period in 2024. For the second quarter, the company reported earnings per share (EPS) of $1.48, a 4.2% increase from $1.42 in the same period in 2024. On a weather-normalized basis, year-to-date earnings rose 9.4%, demonstrating the company's ability to mitigate external volatility.

These aren't the hockey-stick growth numbers that capture headlines. They're something more valuable: predictable, sustainable, compound growth that you can model out for decades. The company's capital allocation framework is a machine designed to convert infrastructure spending into earnings growth with mathematical precision.

The capital investment program is the engine. $3.3 billion capital investment plan, with $1.3 billion already deployed through June 2025. Every dollar invested goes into the rate base, earning that 9-10% regulated return. With $40-42 billion planned over the next decade, we're looking at roughly $4 billion in annual rate base additions. At a 10% return on equity and 50% equity capitalization, that's $200 million in additional annual earnings power, every year, compounding.

The balance sheet is structured to support this capital intensity. American Water maintains investment-grade credit ratings, enabling access to debt markets at favorable rates. The company targets a capital structure of roughly 50% debt and 50% equity, optimizing the cost of capital while maintaining financial flexibility. Interest coverage ratios remain healthy despite the massive capital program.

Dividend policy reflects confidence in the model. The company has maintained its long-term EPS and dividend growth targets of 7-9%. The payout ratio of roughly 60% leaves ample room for reinvestment while providing shareholders with growing income. This isn't a yield trap or a melting ice cube—it's a compound growth machine that happens to pay a dividend.

The comparison to utility peers is instructive. While electric utilities face disruption from renewable energy and distributed generation, water has no substitute. While gas utilities confront electrification mandates, water demand only grows with population. American Water trades at a premium to utility averages, but the quality of the business model justifies it.

Return on equity consistently runs in the 9-10% range—exactly where regulators set it. This isn't a coincidence; it's the model working as designed. The company earns what regulators allow, no more, no less. The growth comes from expanding the rate base, not from expanding margins.

Free cash flow conversion is lower than you'd expect for a utility, but that's by design. Every dollar of free cash flow not reinvested in infrastructure is a dollar not earning regulated returns. The company actually wants to minimize free cash flow, plowing everything back into rate base growth.

The acquisition math is compelling. When American Water buys a small system, they typically pay 1-1.5x rate base. They then invest heavily to bring the system up to standards, often doubling or tripling the rate base over time. Those investments earn regulated returns forever. It's like buying rental properties, fixing them up, and having the government guarantee your rental income.

Weather normalization adjustments reveal the stability of the underlying business. On a weather-normalized basis, year-to-date earnings rose 9.4%, demonstrating the company's ability to mitigate external volatility. Hot, dry summers increase water sales. Cool, wet summers decrease them. But over time, it averages out, and the infrastructure investments keep compounding.

The efficiency ratio—O&M expenses as a percentage of revenues—has been steadily improving despite inflationary pressures. Scale advantages, technology investments, and operational excellence initiatives are offsetting cost pressures. This operational leverage amplifies the rate base growth.

Looking at returns since the 2008 IPO, American Water has been a wealth-creation machine. From $21.50 at IPO to over $140 today, plus dividends, investors have earned roughly 13% annually—crushing the S&P 500 and most utility peers. This isn't luck or multiple expansion—it's the mathematical outcome of the business model.

The forward outlook remains robust. With $40-42 billion in planned investment, 7-9% EPS growth targets, and a dividend growing at similar rates, the total return potential remains compelling. Add in potential acceleration from federal infrastructure spending, consolidation opportunities, and climate resilience needs, and the growth runway extends for decades.

The bear case focuses on regulatory risk, capital intensity, and climate exposure. But these risks are manageable within the regulatory framework. Rate cases may get contentious, but water remains essential. Capital needs are massive, but they drive earnings. Climate change damages infrastructure, but damaged infrastructure needs replacement, driving more investment.

IX. Playbook: Business & Investing Lessons

American Water's century-long journey offers a masterclass in building wealth through essential services. The lessons extend far beyond utilities, revealing timeless principles about monopolies, regulation, and the power of patient capital.

Lesson 1: Natural Monopolies Are Real, and They're Spectacular

Water distribution is the textbook definition of a natural monopoly. The economics are brutal: massive upfront capital costs, tiny marginal costs, and physical networks that make competition irrational. You don't want three sets of water pipes running down your street any more than you want three sets of railroad tracks. American Water understood this from day one—consolidate the fragmented market, achieve scale, and the economics become unassailable.

The investing insight: Look for businesses with network effects so strong that competition is economically irrational. These are rare, but when you find them, they compound wealth for generations.

Lesson 2: Regulatory Capture Is a Two-Way Street

The conventional narrative is that utilities capture their regulators, extracting monopoly rents from helpless consumers. The reality is more nuanced. Regulators need competent operators to provide essential services. They need companies with balance sheets strong enough to fund infrastructure. They need partners who can navigate federal mandates and environmental regulations.

American Water has mastered this dance. They don't fight regulators; they align with them. They propose investments that serve public needs while growing the rate base. They accept regulated returns in exchange for guaranteed cost recovery. It's not capture—it's symbiosis.

Lesson 3: Capital Intensity Can Be a Moat, Not a Burden

Most investors flee capital-intensive businesses. American Water embraces them. Every dollar of required capital investment is a dollar that earns regulated returns forever. The massive infrastructure needs that terrify small operators are American Water's opportunity. They have the balance sheet, expertise, and regulatory relationships to deploy capital at scale.

The lesson: In the right regulatory framework, capital intensity becomes a competitive advantage. Small competitors can't match your investment capacity. New entrants can't replicate your infrastructure. The capital requirements that constrain others become your moat.

Lesson 4: Consolidation in Fragmented Industries Creates Decades of Growth

America has over 50,000 water systems, most serving fewer than 500 people. These systems are too small to afford modern treatment technology, too politically weak to raise rates, and too capital-constrained to meet regulatory requirements. American Water's consolidation playbook—acquire, invest, integrate—has worked for a century and has decades left to run.

The pattern repeats across industries: funeral homes, car washes, HVAC contractors, veterinary clinics. Fragmented industries with aging owners, rising compliance costs, and capital needs create consolidation opportunities that can drive growth for generations.

Lesson 5: Essential Services Have Pricing Power, Even Under Regulation

Water is the ultimate essential service. You can live without electricity for days, without gas for months, without internet for years. You can't live without water for 72 hours. This essentiality gives water utilities pricing power that survives regulation, recession, and political pressure.

American Water's rates have grown faster than inflation for decades, even under strict regulatory oversight. When you provide something people literally cannot live without, price becomes secondary to reliability.

Lesson 6: Foreign Ownership of Infrastructure Is Political Poison

RWE's spectacular failure teaches a crucial lesson: Infrastructure is inherently political, and foreign ownership triggers visceral opposition. It doesn't matter how well you operate or how much you invest. The moment rates go up under foreign ownership, you become a political piñata.

This creates opportunity. Foreign buyers overpay to enter markets, then are forced to exit at losses when political pressure mounts. American Water benefited from both sides—selling high to RWE, then rebuilding independently when RWE fled.

Lesson 7: The Best Time to Invest Is When Capital Is Scarce

American Water's most successful investments came during capital-constrained periods. John Ware bought the company in 1947 when nobody else would bid. The company went public in 2008 during the financial crisis. They've acquired systems from distressed municipalities when budget crises forced sales.

When capital is scarce, returns are highest. When everyone's afraid to invest, those who can deploy capital earn outsized returns. American Water's permanent capital advantage—regulated cost recovery—allows them to invest when others can't.

Lesson 8: Climate Change Is an Infrastructure Super-Cycle

What politicians call crisis, American Water calls opportunity. Climate change means more extreme weather, more infrastructure damage, more regulatory requirements, and more necessary investment. Every flood that damages treatment plants, every drought that requires new sources, every storm that breaks pipes drives capital deployment at regulated returns.

The company isn't hoping for disasters—they're preparing for reality. Climate adaptation requires massive infrastructure investment. Those with the capability to deploy that capital will earn returns for decades.

Lesson 9: Boring Businesses Can Be Beautiful Investments

American Water will never be featured in Fast Company. They don't have a charismatic founder story. They're not disrupting anything. They provide the same service they've provided for 138 years: clean water through pipes. Yet they've created more wealth than most Silicon Valley unicorns ever will.

The lesson: Boring can be beautiful when it comes with predictable cash flows, regulatory protection, and essential demand. Excitement is expensive in markets. Boredom is often undervalued.

Lesson 10: Time Arbitrage Is the Ultimate Edge

American Water thinks in decades, not quarters. Rate cases play out over years. Infrastructure lasts for generations. Military contracts run for 50 years. This long-term orientation is their ultimate competitive advantage.

While markets obsess over quarterly earnings beats, American Water methodically builds rate base. While activists demand immediate returns, they invest for compound growth. While politicians cycle through office, they build permanent infrastructure. Time arbitrage—the willingness to wait for returns others demand immediately—creates enduring wealth.

X. Analysis & Bear vs. Bull Case

The Bull Case: Riding the Infrastructure Super-Cycle

The bull thesis for American Water is elegantly simple: America's water infrastructure is failing, someone has to fix it, and American Water is best positioned to profit from the reconstruction.

Start with the infrastructure deficit. According to the EPA's 2023 national needs assessment, America needs $625 billion over the next 20 years to reach a state of good repair. That's just drinking water. Add wastewater, and we're talking $1.2 trillion. These aren't nice-to-have improvements—they're essential investments to prevent public health crises.

American Water's $40-42 billion investment plan captures a meaningful share of this spending, but more importantly, it positions them to accelerate consolidation. Small utilities facing massive capital requirements will increasingly sell to American Water, who can spread costs across their platform and access capital markets efficiently.

The regulatory environment has never been more favorable. The Infrastructure Investment and Jobs Act provides federal funding that reduces the burden on ratepayers while accelerating investment. State regulators increasingly recognize that small systems can't meet modern standards and actively encourage consolidation. Environmental regulations continue tightening, driving mandatory investment.

Climate change accelerates everything. Extreme weather damages infrastructure faster than planned replacement cycles. Droughts require new water sources and treatment capabilities. Floods overwhelm systems designed for historical patterns. Every climate impact drives investment at regulated returns.

The consolidation runway remains massive. Of America's 50,000+ water systems, American Water serves about 1,700 communities. Even capturing 10% market share would triple their size. The fragmentation that has persisted for a century is finally breaking down under regulatory and financial pressure.

Technological advantages are emerging. Smart meters, predictive maintenance, and advanced treatment technologies offer operational efficiencies that small utilities can't achieve. American Water's scale allows them to invest in technology that improves service while reducing costs—a virtuous cycle that accelerates competitive advantages.

The financial model is de-risked. With regulated returns, essential demand, and geographic diversification, American Water offers equity-like returns with bond-like stability. In an era of market volatility and economic uncertainty, this defensive growth profile becomes increasingly valuable.

ESG tailwinds provide additional support. Water is the ultimate ESG investment—environmental (clean water), social (public health), and governance (regulatory oversight). As ESG mandates drive institutional capital allocation, American Water benefits from inclusion in ESG indices and portfolios.

The Bear Case: Regulatory Reckoning and Climate Catastrophe

The bear thesis acknowledges American Water's strengths but sees gathering storms that could devastate returns.

Regulatory risk is real and growing. As water bills consume an increasing share of household budgets, political pressure to constrain rates intensifies. Populist politicians increasingly campaign on utility rate rollbacks. Regulatory commissions, facing political pressure, could slash allowed returns or disallow capital investments. The regulatory compact that has protected utilities for a century could unravel under political pressure.

Public ownership threats are mounting. Cities from Missoula to Pueblo have pursued municipal takeover of private water systems. The narrative that water is a human right incompatible with private ownership gains traction with each rate increase. American Water could face forced sales at book value—far below market prices—as municipalities exercise eminent domain.

Climate liabilities could explode beyond manageable levels. What if climate change doesn't just damage infrastructure but makes it obsolete? Coastal systems could face saltwater intrusion. Western systems could see sources disappear entirely. The capital needed to adapt could exceed what regulators will allow in rates, crushing returns.

Capital intensity at current valuations destroys value. American Water trades at over 25x earnings, implying growth expectations that may prove unrealistic. If they're earning 10% returns on equity but investors are paying 25x earnings, the math doesn't work. Either multiples compress or returns disappoint.

Technology disruption, while seemingly impossible, could emerge. Atmospheric water harvesting, advanced home treatment systems, or radical conservation technologies could reduce demand for centralized water systems. It seems far-fetched today, but so did distributed solar generation 20 years ago.

Execution risk multiplies with scale. As American Water grows through acquisitions, integration becomes harder. Each system has unique challenges, and economies of scale have limits. Operational stumbles that damage water quality could trigger regulatory backlash and destroy the company's social license to operate.

The debt burden could become unsustainable. With $5 billion in debt already and massive capital needs ahead, American Water depends on continued access to capital markets. A credit crisis, rating downgrade, or interest rate spike could make the model uneconomic.

Demographic headwinds in certain regions could pressure growth. Declining populations in Rust Belt cities mean fewer customers sharing fixed infrastructure costs. Even with rate increases, revenue growth could stall in shrinking service territories.

The Verdict: Asymmetric Risk-Reward

The bull case ultimately overwhelms the bear case, not because the risks aren't real, but because they're manageable within American Water's framework.

Regulatory risk has existed for 138 years—it's a feature, not a bug. The company has survived the Great Depression, two World Wars, stagflation, and the financial crisis, all while operating under regulatory oversight. Regulators need competent operators more than operators need favorable regulations.

Public ownership threats are overblown. Municipal takeovers are expensive, complex, and often fail to deliver promised savings. Cities struggling with basic services rarely have the expertise or capital to run water systems. The few successful takeovers typically involve small, poorly run systems—not American Water's well-managed operations.

Climate adaptation is an opportunity disguised as a threat. Yes, infrastructure needs will be massive. That's precisely why American Water will thrive. They have the expertise, capital access, and regulatory relationships to build climate-resilient systems while earning returns on every dollar invested.

The valuation, while rich, reflects quality. American Water trades at a premium because it offers growth, stability, and essential services in a world desperately seeking all three. The multiple may compress, but the earnings growth should more than compensate over time.

The model's resilience has been tested and proven. Through foreign ownership failure, financial crisis, and pandemic, American Water has delivered consistent returns. The infrastructure super-cycle ahead represents the greatest growth opportunity in the company's history.

For long-term investors seeking compound growth with downside protection, American Water offers an asymmetric opportunity: participate in a multi-decade infrastructure rebuild with regulated returns and essential demand. The risks are real, but they're overwhelmed by the generational tailwinds propelling the business forward.

XI. Leadership Transition & Future Strategy

CEO M. Susan Hardwick will retire on May 14, 2025, and John Griffith, President of American Water, will succeed her. The transition from Susan Hardwick to John Griffith as CEO represents more than a changing of the guard—it's a strategic evolution from operational excellence to growth acceleration.

Hardwick's legacy is one of transformation. Taking over in 2020, she navigated the company through COVID-19, accelerated digital transformation, and positioned American Water as the consolidator of choice in the industry. Under her watch, the company executed over 100 acquisitions, adding hundreds of thousands of customer connections while maintaining operational excellence.

Griffith represents continuity with acceleration. As President since 2023 and with deep utility experience, he understands both the operational complexity and growth opportunity ahead. His mandate is clear: execute the $40-42 billion infrastructure plan while doubling down on consolidation opportunities.

The strategic priorities for the next decade are crystallizing around five pillars:

Infrastructure Modernization: The core of the strategy remains massive capital deployment. But it's not just about quantity—it's about smart investment. Advanced metering infrastructure, predictive maintenance systems, and climate-resilient designs will differentiate American Water's systems from aging municipal operations.

Consolidation Acceleration: The fragmentation of America's water systems is finally reaching a breaking point. Environmental regulations, infrastructure needs, and operational complexity are overwhelming small systems. American Water is positioned to be the buyer of choice, offering communities professional management, capital access, and regulatory expertise.

Technology Integration: While water treatment is ancient technology, the management and delivery systems are ripe for innovation. Smart meters that detect leaks in real-time, AI systems that predict pipe failures before they happen, and automated treatment systems that adjust to water quality changes—these technologies will drive operational efficiency while improving service.

Climate Adaptation: This isn't just about hardening infrastructure against storms. It's about fundamental reimagining of water systems for a climate-altered world. That means new water sources, advanced treatment for emerging contaminants, and systems designed for both floods and droughts.

Regulatory Excellence: As regulations tighten and political scrutiny intensifies, regulatory expertise becomes a competitive advantage. American Water's ability to navigate 14 different state regulatory frameworks while maintaining constructive relationships is a capability competitors can't easily replicate.

The consolidation endgame is coming into focus. Of the 50,000+ water systems in America, perhaps 500-1,000 will survive as independent entities. The rest will be absorbed by companies like American Water or returned to municipal control. This consolidation wave, playing out over 20-30 years, represents the greatest growth opportunity in the industry's history.

The technology wild cards could accelerate everything. If atmospheric water generation becomes economic, if home treatment systems become foolproof, if conservation technologies dramatically reduce demand—any of these could disrupt the traditional utility model. But they could also create opportunities for American Water to be the integrator and manager of distributed systems rather than just centralized ones.

The leadership team understands that success requires balancing multiple stakeholders. Customers need affordable, reliable service. Regulators need responsible partners who can meet environmental standards. Communities need investment and jobs. Investors need returns. Employees need career opportunities. Balancing these sometimes competing interests is the art of utility management.

XII. Recent News

[As this section would require current, breaking news updates that weren't available in the search results, I'll note the framework for what would be included:]

The recent news section would typically cover: - Latest quarterly earnings results and guidance updates - Recent acquisition announcements and regulatory approvals - Infrastructure investment milestones and major project completions - Regulatory decisions and rate case outcomes - ESG initiatives and sustainability reporting - Federal infrastructure funding allocations - Climate events impacting operations - Leadership changes and board appointments - Analyst upgrades/downgrades and price target changes - Industry consolidation developments

XIII. Links & Resources

Regulatory Filings & Investor Materials: - SEC EDGAR Database - American Water Works Filings - American Water Investor Relations Portal - Annual Reports and Proxy Statements Archive - Quarterly Earnings Call Transcripts

Industry Research & Analysis: - EPA Drinking Water Infrastructure Needs Survey - American Society of Civil Engineers Infrastructure Report Card - National Association of Water Companies Industry Reports - Bluefield Research Water M&A Analysis - American Water Works Association (AWWA) Resources

Books on Water Infrastructure & Utilities: - "The Big Thirst" by Charles Fishman - "Cadillac Desert" by Marc Reisner - "Water 4.0" by David Sedlak - "The Ripple Effect" by Alex Prud'homme - "Bottled and Sold" by Peter Gleick

Historical Documents: - "A Dynasty of Water: The Story of The American Water Works Company" by Gilbert Cross - Documentary History of American Waterworks - Public Utility Holding Company Act of 1935 Archives - Clean Water Act Legislative History - Safe Drinking Water Act Implementation Records

Financial Analysis Resources: - Value Line Investment Survey - American Water - Morningstar Equity Research Reports - S&P Global Ratings Reports - Moody's Credit Opinions - Argus Research Company Reports

American Water's story is far from over. From its humble beginnings in post-Civil War Pennsylvania to its position today as America's water infrastructure backbone, the company has proven that essential services, combined with patient capital and operational excellence, can create enduring wealth. As America confronts a trillion-dollar infrastructure crisis, American Water stands ready to profit from the reconstruction—one pipe, one treatment plant, one acquisition at a time. The next chapter of this 138-year-old story may be the most lucrative yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube