Avery Dennison: The Materials Science Pioneer Powering the Connected World

I. Introduction & Episode Roadmap

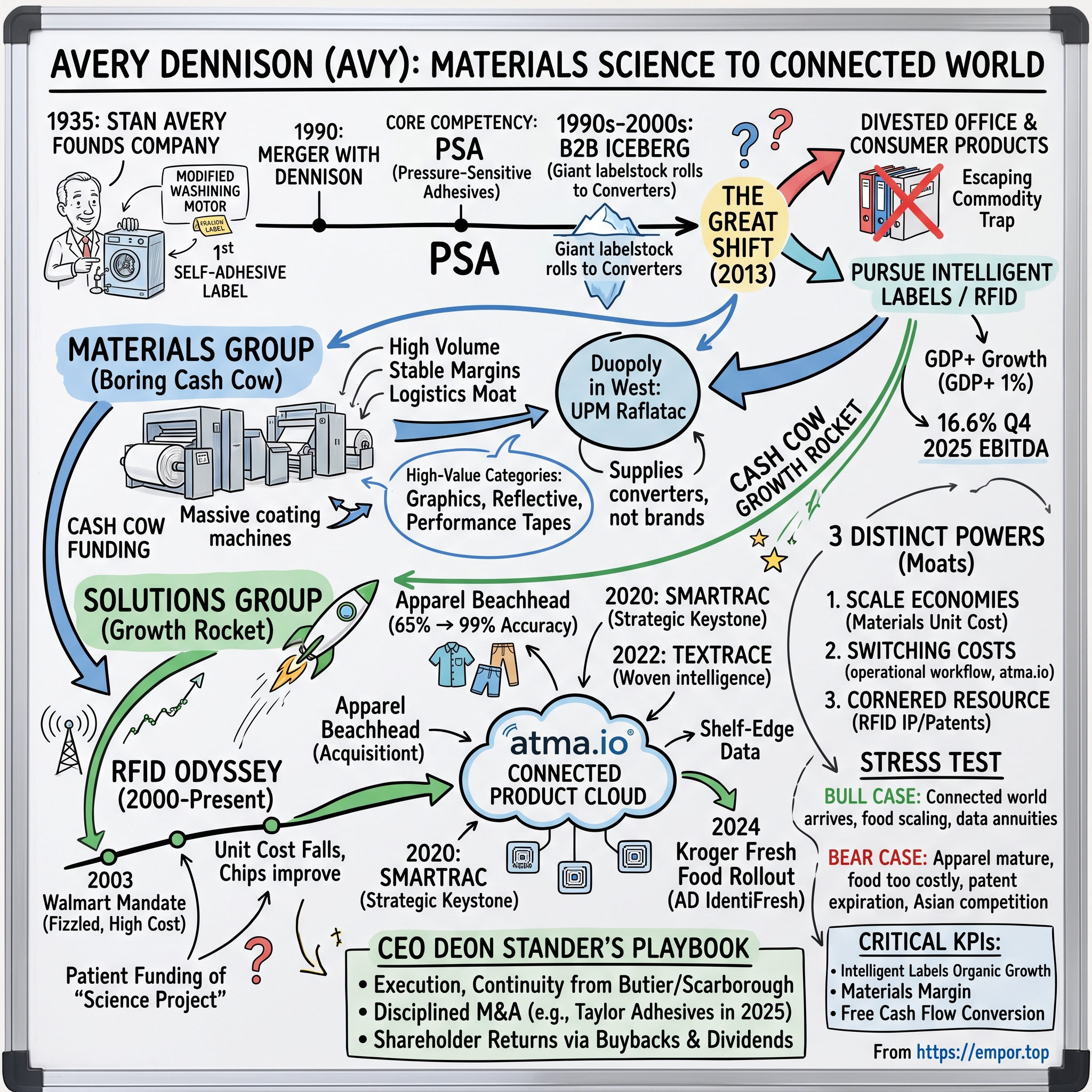

Walk into a Kroger on a Tuesday morning and pick up a loaf of sourdough. Somewhere inside that unglamorous paper band around the bag sits a sliver of aluminum antenna, thinner than a human hair, wired to a grain-of-sand silicon chip. Wave a handheld reader past the shelf and, in a fraction of a second, the store knows exactly how many loaves it has, when they were baked, and which ones need to be pulled before they go stale. The bakery clerk never counts a thing. That invisible little tag is the product of a company most Americans still associate with the binder labels they bought for a school project in 1998.

That is the puzzle at the heart of Avery Dennison Corporation. How did a business founded on paper stickers and office supplies become the world's dominant maker of item-level digital identities — the silent nervous system running underneath the inventory of Walmart, Target, Zara, and Kroger?

The scale is genuine. Avery Dennison, listed on the NYSE under the ticker AVY, generated roughly $8.9 billion in revenue in fiscal 2025, operates in more than 50 countries, and by most industry estimates commands around half of the global market for RFID inlays — the tiny antenna-plus-chip assemblies that make contactless tracking possible.1 It is, improbably, one of the largest buyers of radio-frequency silicon chips on the planet, yet its core competency remains what it has always been: the physics of making one material stick to another.

The thesis of this story is a study in corporate evolution done right. Avery Dennison took a deep, unglamorous mastery of materials science — polymers, adhesives, coatings, siliconized release liners — and used the cash it threw off to build, patiently and expensively, an intellectual-property and data platform on top of it. It is a rare example of an old-economy industrial champion that did not get disrupted so much as it quietly digitized its own franchise before anyone else could.

That framing is the flattering version, and it is important to hold it at arm's length. This is not an investor-relations brochure, and the "materials science pioneer powering the connected world" tagline is the kind of self-description that deserves scrutiny rather than applause. The honest question that runs underneath this entire story is whether Avery Dennison is genuinely becoming a technology-and-data platform or is a very good industrial company narrating itself into a higher valuation multiple. There is real evidence on both sides — a dominant, patiently built RFID position and a real cloud platform on one hand; decelerating growth and a rich-multiple acquisition on the other — and a serious analysis has to weigh the evidence rather than accept the tagline. So we will treat every management claim as a hypothesis to be tested against behavior, numbers, and competitors, and we will be explicit about what would prove the story right and what would prove it wrong.

Here is the road we will travel. We start in a Los Angeles loft in 1935, where a broke inventor with a borrowed $100 built the first self-adhesive label out of scrap parts. We trace the high-volume, low-margin "sticker" business that made the company a household name and a Wall Street afterthought. We examine the pivotal 2013 decision to sell off the very office-products division that gave the company its public identity. We follow the fifteen-year, cash-burning bet on RFID that most observers wrote off as a science project — until it wasn't. We dissect the high-stakes acquisitions of Smartrac and Vestcom, and the software platform, atma.io, that turns hardware into a subscription relationship. And we close with the playbook of current CEO Deon Stander, the competitive war-game, and an honest accounting of what could break the whole story.

Let us begin where every good origin myth begins: with someone who had almost nothing to lose.

II. Founding Context & The Adhesives Revolution (1935–1989)

Los Angeles, 1935. The country was still clawing its way out of the Great Depression, and a former ceramics and printing worker named Ray Stanton Avery — everyone called him "Stan" — had an idea he couldn't afford to build. Labels, at the time, were miserable things. You brushed them with water or wet glue, slapped them on, and hoped they didn't curl, smear, or fall off. Stan believed there was a better way: a label that came pre-glued, protected by a peel-away backing, that a person could apply with nothing more than the pressure of a thumb.

The problem was capital. Stan had none. He borrowed $100 from his fiancée, Dorothy Durfee, and went to work in a rented loft with a genuinely absurd bill of materials: a washing-machine motor, a saber saw, and salvaged parts from a player piano.3 Out of that Frankenstein contraption came the world's first machine for making pressure-sensitive, die-cut, self-adhesive labels — and the founding of what would become Avery Dennison.3

It is worth pausing on what pressure-sensitive adhesive, or PSA, actually is, because it is the physical foundation of everything that follows. A wet glue works by chemically drying or curing — you activate it, it sets, it's permanent, and it's a hassle. A pressure-sensitive adhesive is different. It is a viscoelastic polymer: a material that behaves partly like a solid and partly like a very slow liquid. It stays permanently tacky. Press it against a surface and it flows, at a microscopic level, into every pit and groove, gripping through simple molecular attraction. No water, no heat, no waiting. Think of it as the difference between the glue on an old postage stamp — which you had to lick — and a modern peel-and-stick shipping label. Stan Avery didn't invent the chemistry so much as he industrialized the idea of it, building the coating and converting machinery that could produce these labels reliably and at scale.

That distinction — owning the machinery and the process, not just the recipe — became the company's DNA. Through the 1940s, 50s, and 60s, Avery Adhesive Label Corporation expanded across the United States and abroad, licensing its patents, building custom high-speed coating lines, and standardizing industrial labeling for a booming consumer economy. The company was, in effect, selling the picks and shovels of the packaging age. Every product that needed a label — every can, bottle, box, and drum — was a potential customer, and increasingly the label was self-adhesive.

The commercial genius of the model was that Avery rarely had to sell to the end consumer at all. Under the Fasson brand — a name Avery Dennison still uses for roll label materials across much of the world — the company positioned itself as the arms dealer to an entire industry of printers and converters, supplying the raw coated stock that they turned into finished labels. It was a business of tonnage and consistency rather than marketing flash: win the converter's loyalty with reliable quality, fast delivery, and hands-on technical support, and you captured a recurring customer with high switching costs who would keep buying reels for decades. There is a lesson here that echoes through the entire hundred-year arc of the company. Stan Avery's real innovation was never a single sticker; it was a repeatable, industrial-scale way to make adhesion cheap, consistent, and fast. Everything the modern company does — including embedding radios in bakery labels — is a descendant of that founding instinct to own the process rather than the product.

The defining corporate event of the era came in 1990, when Avery Corporation merged with Dennison Manufacturing Company in a transaction valued at roughly $415 million.3 Dennison was the older house by far, tracing its roots to 1844 and a New England trade in jewelry boxes, shipping tags, crepe paper, and the little reinforced binder-hole stickers that generations of schoolchildren would recognize. The merger fused two complementary strengths: Avery's mastery of adhesive chemistry and coating, and Dennison's franchise in retail tickets, fasteners, and office products. The combined Avery Dennison Corporation was born.

And here is where the company acquired what we might call its legacy trap. To the public and to much of Wall Street, "Avery" meant printable labels, mailing stickers, and binder sheets you fed through your inkjet at home. That consumer-facing recognition was enormous — and deeply misleading. Beneath the retail brand sat a far larger, far less visible business: an industrial coating empire selling giant rolls of adhesive "labelstock" to the printers and converters of the world. The company that everyone thought they knew was the small, shiny tip of a very large B2B iceberg. For decades, that gap between perception and reality would depress how investors valued the whole enterprise — and set up the wrenching strategic decision that would define the next chapter.

III. The Great Shift: Escaping the Commodity Trap (1990–2013)

By the mid-2000s, a quiet crisis was building inside the division Avery Dennison was best known for. The internet had arrived. Email replaced the memo. The "paperless office," long promised and long delayed, was finally starting to bite. And the Office and Consumer Products division — the binder labels, the dividers, the mailing stickers, the highlighters that carried the Avery name into every Staples and Office Depot in America — was slowly becoming a melting ice cube.

The economics were brutal in their simplicity. Office products were a mature, commoditized, retail-shelf business. Margins were thin, private-label competition was relentless, and volumes were structurally declining as offices digitized. Worse, the division was a drag on the entire corporation's return on capital: it consumed management attention, working capital, and shelf-space negotiating energy while generating anemic growth. The most recognizable part of Avery Dennison had become one of the least valuable.

The man who chose to cut the cord was Dean Scarborough, then chief executive. In January 2013, Avery Dennison announced a definitive agreement to sell both its Office and Consumer Products (OCP) business and its Designed and Engineered Solutions unit to a familiar rival, Canada's CCL Industries, for $500 million in cash.[^5] The OCP business alone had booked roughly $730 million in sales in 2012.[^5] Read that again: the company sold a three-quarter-billion-dollar revenue line for a five-hundred-million-dollar check. That price tells you everything about how the market valued declining, low-margin, commoditized revenue. Volume was not the point. Quality of earnings was the point. The transaction closed on July 1, 2013.[^5]

What did management do with the proceeds? It did not chase a splashy acquisition. It planned to funnel the net cash — roughly $400 million after taxes — into share repurchases and a pension contribution, essentially returning capital and cleaning up the balance sheet.[^5] The strategic message was that Avery Dennison was no longer going to apologize for being an industrial materials company pretending to be a consumer brand. It was going to become, unambiguously, a B2B pure-play.

It is worth situating this decision in the company's recent scar tissue. Avery Dennison had, for decades, been the kind of blue-chip dividend payer that widows and pension funds owned without a second thought — a company that raised its payout year after year for more than three decades. Then the 2008–2009 financial crisis hit, demand for industrial labels cratered, and management made the painful choice to slash the dividend, ending that long streak of increases. That episode mattered psychologically. It taught the company's leadership, in the most public way possible, that being big and recognizable was no protection against a low-quality, cyclical earnings base. The 2013 divestiture was, in part, that lesson applied: a deliberate move to improve the durability and quality of what remained, even at the cost of shedding a beloved brand and a big chunk of headline revenue.

That reorientation deserves a moment of explanation, because it is the hidden engine of the modern company. Avery Dennison does not, for the most part, sell finished labels to the brands you know. It sells enormous rolls of pressure-sensitive labelstock — face material, adhesive, and release liner, laminated together and wound onto reels — to an ecosystem of intermediaries called "converters." A converter buys the raw roll, prints the design, die-cuts the shape, and sells the finished labels to a shampoo brand, a pharmaceutical company, or a beverage maker. Avery Dennison is the indispensable upstream supplier: the company that coats the raw material the entire label industry runs on. It is a picks-and-shovels position, one step removed from the consumer, and vastly more defensible for it.

That upstream position is easy to underrate, so it is worth being concrete about why it is durable. A converter that has qualified Avery Dennison's labelstock on its presses, dialed in its adhesives for a particular end-use, and built its delivery schedule around Avery Dennison's local warehouses does not casually switch to a rival to save a fraction of a cent. The materials have to run cleanly at high speed, die-cut without tearing, and adhere predictably to the customer's chosen surface — glass, HDPE, corrugate, film. Requalifying an alternate supplier costs time, press downtime, and risk. The result is a business that grows roughly with global consumption of packaged goods — unspectacular, but remarkably steady, and very hard to dislodge from below.

The final, easily overlooked thread of this chapter is what the cash from that steady roll-goods machine quietly funded. Beginning in the early 2000s, Avery Dennison had started seeding speculative, long-horizon research into wireless identification — radio-frequency tags that could give a physical object a digital voice. For years it looked like a rounding error, a curiosity in the R&D budget. But the cash cow was, without much fanfare, financing the moonshot. And that moonshot is where the real story begins.

IV. Segment-Level Deep Dive: The Cash Cow vs. The Growth Rocket

To understand Avery Dennison as an investment rather than a nostalgia trip, you have to understand where the money actually lives. The company today runs on two engines that could hardly be more different in temperament — one a broad, low-drama river of cash, the other a volatile, high-ceiling growth bet — and the entire corporate strategy is about using the first to feed the second.

The way the company presents itself has itself evolved to make this dichotomy legible. For years, Avery Dennison reported in three segments — Label and Graphic Materials, Retail Branding and Information Solutions, and Industrial and Healthcare Materials. Beginning with fiscal 2023, management collapsed that structure into just two reportable segments: the Materials Group and the Solutions Group. The reorganization was more than cosmetic. It drew a clean line between the scale-driven materials franchise and the higher-value, more digital solutions franchise, making it far easier for investors to see the "cash cow funds the growth rocket" logic that had always been the real strategy. When a management team reshapes its own segment reporting to spotlight a narrative, it is worth asking whether the reporting reflects the business or is being used to flatter it — but in this case the two-engine framing genuinely maps to how the company operates and allocates capital.

graph TD

A[Avery Dennison Total Revenue: ~$8.9B] --> B[Materials Group: ~70% of Sales]

A --> C[Solutions Group: ~30% of Sales]

B --> B1[Pressure-Sensitive Label Materials]

B --> B2[Graphics & Reflective Solutions]

B --> B3[Performance Tapes & Adhesives]

B1 --> B_Economics[High Volume, Stable Margins, Low-Mid Single Digit Growth, Cash Cow]

C --> C1[Retail Branding & Information]

C --> C2[Intelligent Labels / RFID Inlays]

C --> C3[Vestcom Shelf-Edge Solutions]

C2 --> C_Economics[High Growth, High Margin, Digital Ecosystem, Reinvestment Engine]

The Materials Group — roughly 70% of revenue. This is the descendant of Stan Avery's original franchise: the global manufacture of pressure-sensitive label materials, plus industrial tapes, graphics films, and reflective sheeting for road signs and vehicle wraps. In fiscal 2025 the Materials Group grew sales around 5%, though with organic volumes roughly flat to down about 1% — a reminder that this is a slow-growing, GDP-plus business, not a compounder.2 Its adjusted EBITDA margin ran near 16.6% in the fourth quarter of 2025, and management has consistently steered it in a stable mid-teens band.2

Why is this business so hard to attack? It is a textbook case of scale economies. The industry structure in the West is effectively a duopoly: Avery Dennison and Finland's UPM Raflatac together control the lion's share of the market, with specialty players like Italy's Fedrigoni occupying premium paper niches.14 Avery Dennison, holding an estimated 30–35% global share, buys polymers, paper pulp, and silicones in volumes almost no one can match, and it runs a fleet of massive, highly automated coating factories where the fixed-cost-per-roll advantage compounds.

But the deepest part of the moat is not chemistry — it is logistics. Converters operate on brutal timelines; a beverage company needs its labels this week, not next month. That means labelstock has to be available for next-day delivery from a local distribution point. Avery Dennison's dense, distributed network of coating plants and warehouses lets it promise speed that a new entrant, however clever its adhesive, simply cannot replicate without spending a decade and a fortune building the same physical footprint. The moat is poured in concrete and diesel, not just poured in polymer.

The Materials Group is not monolithic, though, and the parts that grow fastest are the ones that carry the highest value. Alongside plain-vanilla label materials sit two more specialized franchises. Graphics and Reflective Solutions supplies the films used for vehicle wraps, building signage, and — importantly — the retroreflective sheeting that makes highway signs and license plates glow in headlights, a niche with real regulatory tailwinds and technical barriers. Performance Tapes and adhesives, meanwhile, sell engineered bonding solutions into automotive, electronics, and construction, where a tape that permanently replaces a screw or a weld is worth far more than a commodity roll. Management groups these under the banner of "high-value categories," which reached roughly 38% of Materials Group sales in 2025 and grew low single digits organically even as the plain label base was flat to down.2 The strategic read is that even inside the cash cow, Avery Dennison is deliberately mixing toward more differentiated, harder-to-copy products — a quiet, continuous upgrading of the least glamorous part of the company.

The Solutions Group — roughly 30% of revenue. This is the growth rocket. It houses apparel branding — the woven labels, printed tickets, heat transfers, and hangtags that clothe the world's garments — alongside the crown jewels: the Intelligent Labels (RFID and NFC) division and the Vestcom shelf-edge business. The economics here are structurally richer. Where the Materials Group lives in the mid-teens, the highest-value pieces of Solutions carry meaningfully fatter margins, and the segment as a whole grows several times faster, propelled by a secular shift toward digitizing physical items. In 2025 the group's high-value categories — Intelligent Labels, Vestcom, and the Embelex branding portfolio — represented roughly 60% of the Solutions mix and grew high single digits, with Vestcom alone expanding more than 10%.2

The investor's takeaway from the two-engine design is subtle but important. Avery Dennison is not a growth company and not a value company; it is a value company deliberately manufacturing a growth company inside itself. The Materials Group's job is to be boringly, reliably cash-generative through every cycle, so the Solutions Group can afford to place expensive, patient bets on a future that may take a decade to arrive.

Myth vs. Reality

It is worth puncturing two consensus narratives before moving on, because both distort how people value this company. The first myth is that Avery Dennison is essentially a "sticker company" riding a retail fad. The reality is that the overwhelming majority of its revenue comes from an industrial materials franchise embedded in the supply chain of nearly every packaged good on earth — a business whose fortunes track global consumption, not a fashion cycle. The second, and increasingly common, myth runs in the opposite direction: that Avery Dennison is now fundamentally an RFID and software company with a legacy materials appendage. That, too, is wrong. Intelligent Labels and the digital adjacencies remain the minority of revenue and the source of the excitement, but the cash that funds everything — the buybacks, the dividends, the R&D, the acquisitions — still comes overwhelmingly from coating adhesive onto liner and shipping it to converters. An investor who buys the stock as a pure RFID play is mispricing what they actually own, and one who dismisses it as a stagnant sticker maker is missing the optionality. The truth is the uncomfortable middle: a mature industrial compounder with a genuine, unproven-at-scale technology call option bolted on. Whether that call option is in the money is the question the next chapter confronts head-on.

V. The RFID Odyssey & The Rise of Intelligent Labels (2000–2023)

For the better part of fifteen years, the RFID program inside Avery Dennison was the corporate equivalent of a garage band that kept insisting it would make it big. The company began developing radio-frequency inlays in the early 2000s, and for roughly a decade and a half the division lost money — a persistent, speculative, high-cost line item that a more impatient management team would have killed a dozen times over.

To see why it eventually mattered, you need to understand the problem it solves, in plain terms. A traditional barcode is a picture. To read it, a scanner needs a clear line of sight, one item at a time, held at the right angle. It is slow, it is manual, and it is error-prone. An RFID inlay is not a picture — it is a tiny radio. It consists of an etched metal antenna and a microchip, and when a reader emits radio waves, the tag harvests just enough energy from those waves to wake up and broadcast its unique identity back. No line of sight required, no one-at-a-time. A worker can wave a reader over a sealed carton and instantly count everything inside it, or walk a sales floor and inventory an entire store in minutes.

There is important history here that explains why the science project stayed a science project for so long. In June 2003, Walmart — never shy about using its scale to bend an industry — mandated that its top 100 suppliers put RFID tags on pallets and cases, with a broader rollout targeted for 2005.17 The industry went into a frenzy of investment, convinced the future had arrived. It hadn't. By the late 2000s the mandate had largely fizzled. The tags cost somewhere between forty cents and a dollar apiece, Walmart declined to subsidize them, and suppliers balked at eating the cost. The technology itself was immature: early ultra-high-frequency tags were confounded by exactly the physics that still challenges the fresh-food rollout today — liquids absorbed the radio signal and metals reflected it, producing dead spots and phantom reads.17 The first great RFID hype cycle collapsed under the weight of cost and physics. What changed over the following decade was mundane but decisive: the price of a tag fell to single-digit cents, chip sensitivity improved, and read reliability climbed. Avery Dennison's willingness to keep funding its inlay program straight through that trough — when the conventional wisdom said RFID had already failed once — is the unglamorous foundation of the position it holds today.

It helps to know, in plain terms, how one of these inlays is actually made, because the manufacturing is the moat. Start with a thin film substrate. Onto it, etch or deposit a metal antenna — a precisely shaped loop or dipole whose geometry is tuned, almost like a musical instrument, to resonate at the right radio frequency for the item and packaging it will live on. Then, at blistering speed, a machine places a microscopic silicon chip and bonds its contacts to the antenna to microscopic tolerances, thousands of times a minute. Get the antenna geometry or the chip placement slightly wrong and the tag reads poorly or not at all. Doing this reliably, at global volume, at a cost of pennies, is a genuinely hard industrial problem — and it is exactly the kind of high-speed, high-precision converting problem that a company descended from Stan Avery's coating machines is unusually well equipped to solve. The whole standard now runs under the industry's RAIN RFID banner, the ultra-high-frequency passive protocol that Avery Dennison and its chip partners have helped push toward ubiquity.

The inflection point came from an unglamorous corner of retail: apparel inventory accuracy. For years, the dirty secret of clothing retail was that stores simply did not know what they had. Industry studies pegged average inventory accuracy at a dismal 65% — meaning roughly a third of what the system thought was on the shelf was wrong, lost, misplaced, or phantom. In an omnichannel world where a store doubles as a fulfillment center for online orders, that inaccuracy is fatal: you cannot ship an item you cannot find. Retailers including Macy's, Target, and Zara discovered that RFID could push inventory accuracy toward 99%, transforming the economics of buy-online-pickup-in-store and ship-from-store. Apparel became the beachhead, and demand finally caught up with the science project.

Why apparel and not, say, groceries or electronics? The economics were almost perfectly suited. A shirt or a pair of jeans is a high-margin item that comes in dozens of size-and-color variants — precisely the kind of SKU sprawl that makes manual counting hopeless and stockouts common. A missed sale on a $60 garment dwarfs the few cents a tag costs, so the return on tagging is overwhelming. The item is also dry, non-metallic, and radio-friendly, which sidesteps the physics problems that killed the Walmart pallet experiment. Zara's parent famously wove RFID into its fast-fashion operating model to keep its rapid-replenishment engine fed; American department stores adopted it to survive the Amazon era by turning their stores into fast, accurate fulfillment nodes. Once a critical mass of major apparel retailers standardized on item-level tagging, it became a de facto requirement flowing down the supply chain to garment manufacturers — and Avery Dennison, already the dominant supplier of the woven labels and printed tickets on those garments, was ideally positioned to add the RFID layer to products it was already making. The beachhead, in other words, was not luck; it was the collision of favorable unit economics, friendly physics, and an existing distribution relationship.

Once the market turned, Avery Dennison moved to consolidate its lead through acquisition rather than wait for organic growth to compound.

The Smartrac acquisition (2020). In November 2019, Avery Dennison agreed to buy the Transponder (RFID inlay) division of Netherlands-based Smartrac for €225 million, a deal that closed on March 2, 2020, just as the pandemic was descending.[^6]4 Smartrac's inlay unit generated roughly €125 million in annual revenue, which pencils out to a purchase price of about 1.8 times sales.[^6] That multiple is the analytical point worth dwelling on. In an era when anything with a whiff of "IoT" or "connected devices" was fetching double-digit revenue multiples, Avery Dennison paid a decidedly industrial price for what was, in fact, a strategic keystone. The deal folded Smartrac's deep patent library, its high-performance antenna designs, and its manufacturing plants in Germany, Malaysia, China, and the United States directly into Avery Dennison's distribution machine.4 Discipline, not exuberance — a pattern worth remembering when we get to the more expensive deals.

The TexTrace acquisition (2022). In February 2022, Avery Dennison acquired TexTrace, a Swiss specialist in woven and knitted RFID labels that can be sewn directly into a garment or built into its seam.5 The strategic logic was elegant: instead of hanging a disposable plastic RFID tag off a shirt, you weave the intelligence permanently into the fabric itself, so the item carries a digital identity for its entire lifetime — through manufacturing, retail, resale, and even recycling. It was a bet that item-level identity would eventually be a permanent feature of a product, not a temporary sticker discarded at checkout.

Which brings us to the competitive landscape and the oft-repeated claim that Avery Dennison holds roughly 50% of the RFID inlay market. That figure is an industry estimate rather than an audited fact, and it deserves a skeptic's asterisk — but the sources of the company's edge are concrete. Avery Dennison designs the inlay (the marriage of antenna geometry and chip packaging), manufactures it at a global scale few can match, and sits in direct partnership with the integrated-circuit designers who make the actual RAIN RFID chips, principally Impinj and NXP Semiconductors. Its rivals are real — the apparel-focused SML Group, the inlay maker Tageos, and Checkpoint Systems, now a division of CCL Industries, the same company that bought Avery Dennison's office-products business a decade earlier.1615 The competitive question, which we will stress-test later, is whether that inlay-design-plus-scale advantage survives once the basic patents age and low-cost Asian manufacturers pile in. For now, the lead is real; its durability is the debate.

War-gaming the competition is instructive here. Avery Dennison's rivals are not weak. SML Group, out of Hong Kong, is a formidable apparel-focused competitor with its own item-level RFID and care-label franchise, sitting close to the same garment customers. Tageos, a French inlay specialist, competes hard on inlay design and price. Checkpoint Systems — now, in a delicious irony, owned by CCL Industries — brings deep roots in retail loss prevention and labeling. And looming over all of them is the chip. The silicon at the heart of every inlay is designed by a handful of firms, above all Impinj, the leader in RAIN RFID reader and tag chips, and NXP Semiconductors. Avery Dennison's partnerships with these designers are an advantage today — privileged access, co-development, volume commitments — but they are also a dependency. If a chipmaker chose to integrate forward into inlays, or if a rival locked up preferential chip supply during a shortage, Avery Dennison's position would feel that squeeze. The company's answer is to compete on the parts it controls: antenna engineering, high-speed manufacturing yield, the breadth of its inlay catalog for hostile environments, and — decisively — its ownership of the customer relationship and the data platform. In a commoditizing hardware market, the winner is often not the cheapest tag but the one wired most deeply into the customer's operations.

The deeper strategic move, though, was not in the hardware at all. It was in wrapping the hardware in software — and in a $1.45 billion bet on grocery shelves.

VI. The Digital Twin: Software, Vestcom, and the Grocery Expansion

If Smartrac showed Avery Dennison's discipline, Vestcom showed its ambition — and its willingness to pay up when it believed the strategic prize justified it. In July 2021, the company agreed to acquire Vestcom for $1.45 billion in cash.[^8] Vestcom is not a maker of stickers in the ordinary sense. It manages the shelf-edge — the price tags, promotional labels, and pricing data that line the aisles of grocery stores and pharmacies — and it does so as a deeply embedded, technology-driven outsourcing partner, printing and delivering store-specific, aisle-accurate pricing media at national scale.

The price tells its own story. At a reported enterprise value near 3.6 times sales on roughly $400 million of revenue, this was, by Avery Dennison's industrial standards, a rich multiple — far above the 1.8x it had paid for Smartrac. Was it an overpay? The defense rests on Vestcom's profile: very high EBITDA margins, minimal capital intensity, and sticky, contractually embedded relationships with the largest retailers in America. You are not buying a label printer; you are buying a recurring, capital-light franchise wired into the pricing operations of grocery chains. The bull interpretation is that this was the right kind of asset at a defensible price. The bear interpretation is that management, flush with confidence, paid a premium multiple for a business whose growth is tethered to the mature U.S. grocery sector. Both readings are legitimate, and how Vestcom compounds from here is a live question rather than a settled win.

The strategic synergy is where it gets interesting. Place Vestcom next to Intelligent Labels and Avery Dennison suddenly controls both ends of the retail data equation: the item-level identity of the product (the RFID tag) and the shelf-level price of the product (the electronic shelf-edge). In principle, that is a uniquely complete picture of what is on a store's floor and what it costs — a position no pure-play inlay maker or pure-play pricing vendor can claim.

Stitching it all together is the company's least understood asset: atma.io, a cloud platform Avery Dennison describes as a "connected product cloud."13 Here is the concept in plain language. Every physical item — a shirt, a steak, a vaccine vial — gets a unique digital identity when it is tagged, and atma.io is the software layer that stores, tracks, and makes sense of that identity from the moment of manufacture, through the supply chain, onto the shelf, and into the consumer's hands. It is, in effect, a "digital twin" for physical objects: a live database record shadowing every tagged item through its life. The strategic weight of this cannot be overstated for the investment case, because it is what transforms Avery Dennison from a company that sells a piece of hardware once into a company that can, in theory, sell a data relationship that renews. Whether atma.io becomes a genuine high-margin software annuity or remains a supporting feature that helps sell more inlays is not yet proven — but the optionality is real, and it is why the company insists it is no longer just a materials maker.

There is a second, slower-burning catalyst behind the software story that deserves a mention, because it is the kind of structural tailwind investors tend to under-appreciate until it arrives: regulation. The European Union is moving toward a Digital Product Passport regime under its broader sustainable-products agenda, beginning with categories like textiles, that would require products to carry machine-readable records of their materials, origin, and recyclability. A unique, scannable item-level identity — precisely what an RFID or QR-linked label plus a cloud database provides — is the natural infrastructure for such a mandate. If that regulatory wave materializes as drafted, it would convert item-level digital identity from a nice-to-have efficiency tool into a compliance requirement, and Avery Dennison sits at the intersection of the physical tag and the data layer needed to satisfy it. This is optionality rather than a booked order, and regulatory timelines slip notoriously, so it belongs in the "watch, don't count on it" column. But it is a real reason the company keeps insisting that item-level identity is a structural trend, not a retail fad. Beyond compliance, the same atma.io plumbing enables use cases the hardware alone never could: verifying a product is authentic rather than counterfeit, executing a precise product recall down to the individual unit, and giving a consumer who scans a tag a direct digital relationship with the brand. Whether those become large revenue lines or remain features is, again, unproven — but they are the reason the platform is strategically more interesting than the inlay.

The most consequential proof point of the whole thesis, though, is happening in the least glamorous place imaginable: the fresh-food aisle. In October 2024, Kroger began rolling out Avery Dennison's RFID technology across fresh departments, starting with the bakery, with a plan to extend it across most of its roughly 2,750 stores.67 This matters far beyond one grocer. Apparel is dry, flat, and forgiving; fresh food is wet, cold, wrapped in metallic film, and physically hostile to radio waves. Getting a tag to reliably read on a package of meat in a refrigerated case is genuinely hard engineering, which is why Avery Dennison developed a dedicated inlay line (branded AD IdentiFresh) for the purpose. The payoff for the grocer is automated inventory counts, better product rotation to sell older stock first, and — the real prize — a meaningful reduction in food spoilage. And in 2025, Avery Dennison confirmed it was working with Walmart to extend item-level RFID into fresh categories including meat, a signal that the largest retailer in the world sees the same opportunity.8 If fresh food adoption compounds the way apparel did, it would validate the entire fifteen-year bet. If it stalls on cost-per-tag and physics, the bears have their case. That tension is the story of the next several years — and it lands squarely in the lap of the man now running the company.

VII. Deon Stander's Playbook: Current Management & Capital Allocation

To understand Deon Stander, you have to understand the two men whose strategy he inherited. Dean Scarborough, chief executive from 2005 until 2016, was the surgeon who made the hard cuts — most notably the 2013 office-products divestiture — and steadied the company after the dividend-slashing trauma of the financial crisis. Mitchell "Mitch" Butier, a finance man who rose through the ranks and became CEO effective May 2016, was the architect who turned that cleaned-up industrial base into a growth story, doubling down on Intelligent Labels and pushing the high-value-category strategy across both segments.[^24] It was Butier who oversaw the Smartrac and Vestcom acquisitions that assembled the modern platform.

In June 2023, the board elected Deon M. Stander — then president and chief operating officer — to succeed Butier, who moved to executive chairman, with the transition taking effect that autumn.12 The continuity is the point. Stander was not an outside change agent brought in to challenge the strategy; he was a long-serving insider who had spent years running exactly the part of the company that now carries its growth narrative — the retail and branding solutions business that grew to encompass Intelligent Labels. The board's message was that the digital pivot had a playbook and a proven author, and it wanted execution, not reinvention. For investors, that continuity cuts both ways: it lowers the risk of a jarring strategic U-turn, but it also means there is no fresh outsider's skepticism being applied to bets — like the Vestcom multiple or the pace of RFID commercialization — that an insider is invested in defending.

Stander's compensation structure is worth reading as a statement of intent. His total pay runs around $9.5 million, and the overwhelming majority of it is not salary but performance-linked equity — long-term incentive awards tied to metrics like return on invested capital and cumulative adjusted earnings per share.11 His direct ownership of AVY stock is modest, on the order of a tenth of a percent, which is worth flagging honestly: this is a professional-manager compensation model, not a founder-owner with a life-defining personal stake. The incentive design pushes toward disciplined capital returns and margin-accretive growth, but an activist would note that the alignment comes from the plan design rather than from a large personal shareholding.

What has Stander actually done? The behavior, so far, matches the words — and behavior is the only honest test of management credibility. The strategy is unchanged and unambiguous: run the Materials Group as a cash generator, and deploy that cash into scaling Intelligent Labels and the higher-margin software and data adjacencies. On the capital-allocation front, the balance sheet has been kept deliberately conservative, with net debt to adjusted EBITDA held around 2.4 times at the end of 2025, comfortably inside the company's stated 2.0x–2.5x comfort zone.2

The shareholder-return record is substantial. In 2025, Avery Dennison returned roughly $861 million to shareholders through a combination of share repurchases and a rising dividend — buying back about 3.2 million shares for some $572 million and paying out close to $289 million in dividends.2 That is a large return relative to the company's size, and it does real work: it steadily shrinks the share count, offsetting the dilution from stock-based compensation and mechanically supporting per-share earnings even when organic growth is soft. A skeptic would ask whether heavy buybacks are the best use of cash for a company that claims to be transforming into a growth platform — but the counterargument is that a mature cash cow throwing off more than it can reinvest at high returns should give the surplus back, and that is defensible discipline.

There is a longer arc to the dividend worth noting, because it speaks to how the company thinks about promises. Having been forced to cut its payout during the financial crisis — a humbling end to a decades-long streak of annual increases — Avery Dennison spent the following years methodically rebuilding it, growing the dividend steadily as earnings quality improved. That history is instructive for reading management's current conservatism. A company that has publicly broken a dividend promise once tends to be careful about the commitments it makes, which helps explain the preference for quarter-by-quarter guidance and a leverage target held deliberately in the low-2x range rather than stretched for a splashy acquisition. Whether one reads that as prudence or timidity, it is at least consistent behavior — and consistency, tested across a full cycle, is the currency of management credibility.

The M&A track record under this regime reinforces the disciplined read. The signature deal of Stander's tenure so far has been decidedly unsexy: in 2025, Avery Dennison agreed to acquire the U.S. flooring-adhesives business of Meridian Adhesives Group — the Taylor Adhesives, Polycom, and Frontier brands — for $390 million, closing the transaction in October 2025.910 The target, with roughly $110 million of expected revenue, slots into the Materials Group and expands the company's performance-adhesives franchise.9 Note what this is not: it is not a high-priced, unproven technology moonshot bought at a frothy multiple. After the Vestcom premium, management appears to have returned to bolting on solid, cash-generative industrial businesses at industrial prices — a signal that the capital-allocation discipline is genuine rather than rhetorical.

But discipline is easiest to admire when the numbers cooperate, and lately they have not entirely cooperated. On the fourth-quarter 2025 earnings call, Stander said plainly, "I am not satisfied with our organic revenue growth" — an unusually direct admission that the growth engine had sputtered.2 To his credit, that candor came with specifics rather than spin. Management attributed the softness to a roughly 7% decline in the base apparel business as customers digested inventory and absorbed post-tariff pricing, pointed to food and logistics growing at a high-teens rate as evidence the diversification is working, and set out a concrete plan: about $50 million of targeted restructuring savings in 2026 and an acceleration of product innovation.2 The 2026 framework itself was telling — roughly 6% adjusted-EPS growth at the midpoint built on just 0–2% organic sales growth, which is to say the near-term earnings story leans heavily on cost control and buybacks rather than volume.2 Notably, management declined to give full-year revenue guidance, citing low long-term visibility and preferring to guide quarter by quarter. A charitable reading is prudence in a genuinely murky demand environment; a skeptical one is that a company confident in its growth story would be more willing to commit to it out loud. Both interpretations are on the table, and the tie-breaker is whether Intelligent Labels actually reaccelerates as promised.

That candor sets up the real analytical work: separating the durable moat from the cyclical wobble.

VIII. Playbook: Moats & Investing Lessons (Hamilton Helmer's 7 Powers)

Strip away the narrative energy and ask the cold question an investor should ask: what, precisely, keeps competitors from taking Avery Dennison's business? Hamilton Helmer's framework of durable competitive "powers" is a useful scalpel here, and Avery Dennison plausibly holds three distinct ones — though each carries a caveat.

Scale economies — the Materials power. This is the sturdiest of the three, and it is where the moat is genuinely visible in the financials. The core labelstock business earns stable mid-teens margins through recessions precisely because Avery Dennison's unit cost of chemical compounding, siliconizing release liners, and running wide-web coaters at high speed is structurally below what a subscale entrant could achieve. Add the physical distribution network that guarantees next-day delivery to converters, and you have an advantage that is not about being cleverer but about being bigger and more densely deployed. Only UPM Raflatac operates at a comparable scale in the West, which is why the segment behaves like an oligopoly rather than a commodity free-for-all. The caveat: scale economies protect margins, but they do not generate growth. This power keeps the cash cow alive; it does not make the stock a compounder.

Switching costs — the Solutions power. This is the more interesting and more contingent power. Once a global retailer embeds Avery Dennison's inlays into its supply-chain systems, trains its stores on the readers, and — crucially — maps its inventory through atma.io across hundreds of distribution centers, the friction of ripping all of that out and re-validating a rival's tags becomes substantial. The integration is operational, not just contractual, and operational integration is what makes switching costs real rather than theoretical. The caveat, and it is a serious one: an inlay from a competitor that meets the same technical spec is, at the physical level, a substitutable commodity. The switching cost lives in the software and workflow layer, which is exactly why atma.io matters so much to the long-term thesis — and exactly why its unproven monetization is the soft spot in the moat.

Cornered resource — the RFID IP. Avery Dennison holds a large patent estate — well over a thousand patents by its own account — covering antenna design, adhesive backings, and the high-speed manufacturing process that assembles inlays at volume, reinforced by privileged access to specialized high-speed insertion machinery. In a young, fast-moving market, that IP position is a genuine head start. The caveat is time: patents expire, and the most basic antenna geometries are aging toward the public domain. A cornered resource with a shelf life is a diminishing asset unless it is continually replenished with new invention.

Two lessons generalize from all of this. The first is the value of what we might call slow cooking. Avery Dennison's RFID division looked, for a decade and a half, like an expensive indulgence — a cash-burning distraction that any activist could have credibly demanded be shut down. The company's willingness to fund a long-horizon bet through the patient cash flows of a boring core business is precisely what built an asset rivals now struggle to duplicate. The counter-lesson, which the company would prefer you not dwell on, is survivorship: for every RFID that eventually pays off, there are countless corporate science projects that simply burn cash and die, and "keep funding it" is terrible general advice without the specific conviction that the underlying market will eventually turn.

The second lesson is adjacency expansion by acquisition — the deliberate purchase of missing links. Avery Dennison did not try to invent its way from label paper to a digital-twin platform. It bought the antenna IP (Smartrac), the woven-label capability (TexTrace), and the shelf-edge data franchise (Vestcom), assembling a system piece by piece. Done well, this is how an industrial company earns the right to call itself a technology platform. Done poorly, it is how a focused business becomes a sprawling conglomerate paying premium multiples to buy growth it cannot generate organically.

An activist investor would press exactly on that seam, and the pressure is worth articulating because it is the sharpest available critique. The complaint would run like this: Avery Dennison has spent the better part of a decade telling shareholders it is transforming into a higher-growth, higher-margin, tech-enabled platform, yet organic growth in the very division that justifies the story decelerated to low single digits, and the company paid a rich 3.6x-sales multiple for Vestcom — a mature U.S. grocery-services business — right at the peak of the "everything is a platform" enthusiasm. Then, after promising a transformation, its most recent flagship deal was a $390 million bolt-on of flooring adhesives, about as far from a digital-twin future as one can get. A skeptic would ask whether the acquisition strategy is a coherent adjacency march or an opportunistic drift, and whether the portfolio is getting more focused or merely more complicated. The company's defense — that it buys cash-generative assets at disciplined prices and lets the software optionality ride on top — is credible, but it is a defense that has to be re-earned every year with organic results rather than asserted. Which of those two stories is true for Avery Dennison is precisely what the bull and bear cases fight over.

IX. Stress Test: Bull vs. Bear Case & Risk Radar

Every good investment thesis should be able to state clearly why it wins from here — and just as clearly, what would prove it wrong. Avery Dennison's is unusually well-suited to that discipline, because the two engines pull in opposite directions and the risks are concrete rather than vague.

The Current Risk Radar

Three material threats deserve to be on the dashboard, and each operates through a specific business mechanism rather than as generic macro noise.

The first is raw-material volatility. The Materials Group is directly exposed to the prices of petrochemical resins, paper pulp, and silicones — the physical inputs of adhesive and liner. Avery Dennison passes these costs through to converters via pricing clauses, but the pass-through lags, often by a quarter or two. In a period of rapid input inflation, that lag mechanically compresses margins until pricing catches up. It is a manageable risk, but it is a recurring one, and it is why the Materials margin line is the first place to look for trouble.

The second is slowing apparel and retail spend, and this one is not hypothetical — it is happening. Apparel remains the dominant driver of Intelligent Labels demand, roughly 70% of the portfolio, and in 2025 that base apparel business declined around 7% in the fourth quarter as customers wrestled with inventory levels and post-tariff pricing uncertainty.2 Management framed the weakness as tariff-driven and temporary, expecting a recovery as uncertainty subsides. That framing may well prove correct — but "it's transitory" is exactly what management always says about a demand air pocket, and the honest analytical posture is to treat the recovery as a claim to be verified quarter by quarter, not a fact.

The third is technology disruption, the existential tail risk. The entire Intelligent Labels franchise rests on passive RAIN RFID being the winning standard for item-level tracking. If an alternative — ubiquitous computer vision and camera-based warehouse tracking, radically cheaper next-generation barcodes, or low-cost active Bluetooth tags — leapfrogs passive RFID for enough use cases, the value of Avery Dennison's inlay patents and manufacturing scale erodes. This is a low-probability, high-consequence risk, and it is the reason the software layer matters: a data platform is far harder to disrupt than a piece of hardware.

The Industry Through Porter's Lens

Before scoring the debate, it helps to run the two businesses through Porter's five competitive forces, because they produce strikingly different pictures. In the Materials Group, the structure is genuinely favorable: the threat of new entrants is low (scale and logistics barriers are enormous), rivalry is disciplined in a Western duopoly with UPM Raflatac, and buyer power is fragmented across thousands of converters who value reliability over squeezing pennies. The two forces that bite are supplier power — the petrochemical and pulp majors that set input costs — and the threat of substitutes, though the substitute for a pressure-sensitive label (glue, sleeve, direct print) is usually inferior for most applications. Net, it is a structurally attractive, oligopolistic industry, which is exactly why its margins are so stable.

The Solutions Group's RFID business is the more contested arena, and the forces are less comforting. Buyer power is high and concentrated: a handful of giant retailers — Walmart, Target, Kroger, the big apparel houses — drive the mandates, and when your demand comes from a few whales, those whales set the price. The threat of substitutes is the live existential question, since computer vision and cheaper barcodes lurk as alternative tracking technologies. Rivalry is intensifying as SML, Tageos, and low-cost Asian converters chase the same volumes, and while new-entrant barriers in high-speed inlay manufacturing are real, they are lower than the concrete-and-diesel barriers protecting the materials business. Supplier power is the interesting twist: the RFID chip is designed by a small set of IC firms, principally Impinj and NXP, giving those chipmakers meaningful leverage over the whole value chain. The upshot is that Avery Dennison's most exciting growth engine sits in a structurally tougher neighborhood than its boring cash cow — which is precisely why the software and switching-cost layer is so central to defending it.

The Bull vs. Bear Debate

The bull case rests on the connected world arriving on schedule. In this telling, the Kroger and Walmart fresh-food deployments are the thin edge of an enormous wedge: as major grocers mandate item-level tagging across meat, produce, and deli, RFID volumes scale several-fold from today's apparel-dominated base, because the addressable universe of food and logistics items dwarfs the world's clothing racks. Simultaneously, atma.io and Vestcom drag the Solutions Group's margin mix upward, lifting corporate return on invested capital, while the Materials Group keeps behaving like the resilient oligopoly cash cow that funds the whole enterprise and buys back stock through the cycle. It is a coherent story, and the fresh-food proof points give it real support.

The bear case attacks each pillar in turn. Apparel RFID, it argues, is already mature — the easy adoption is behind us, which is why growth has decelerated to low single digits. Non-apparel expansion faces genuine physical and economic hurdles: reading tags reliably through metal and liquid is hard, and at low-value fresh items the cost-per-tag math is far less forgiving than on a $60 shirt. Meanwhile, as the foundational antenna patents age, low-cost Asian manufacturers can flood the market with cheap, spec-equivalent inlays and trigger a price war that commoditizes the very product Avery Dennison dominates. And sustaining leadership in both chemical coating plants and high-speed electronic inlay factories demands heavy, continuous capital expenditure, capping free-cash-flow conversion. In this reading, Avery Dennison is a good industrial company whose "tech platform" premium is more aspiration than reality.

The honest synthesis is that both cases are partially true today, and the resolution is empirical. That is why the KPIs matter more than the narrative.

Critical KPIs to Track

Three numbers cut through the noise. The first, and by far the most important, is Intelligent Labels organic sales growth. The company's ambition has been for this to compound in the mid-teens or better over time, and the gap between that aspiration and the low-single-digit reality of 2025 is the single most important tension in the story. The subtlety to watch is the mix beneath the headline: apparel — still roughly 70% of the portfolio — versus the food-and-logistics categories that grew at a high-teens clip. A reacceleration led by non-apparel would be the strongest possible evidence that the fresh-food thesis is real and that the addressable market is genuinely expanding; a rebound driven only by apparel restocking would be a cyclical bounce, not a structural win. Reacceleration of the right kind would validate the bull; continued sputtering would validate the bear.

The second is the Materials Group adjusted EBITDA margin, historically anchored in the mid-teens and running near 16.6% in late 2025.2 This is the health monitor for the cash cow and the early-warning system for input-cost pass-through failure. Because the entire strategy depends on this segment reliably funding the growth bets, a sustained slip here would be more damaging to the investment case than a soft quarter in RFID — it would mean the engine paying for the whole transformation is losing compression. The third is free-cash-flow conversion, which ran above 100% of net income in 2025 on roughly $700 million of adjusted free cash flow.2 This is the ultimate test of whether the dual-engine model actually generates the cash it needs to fund growth and return capital simultaneously — and it directly answers the bear's charge that running two capital-intensive manufacturing footprints, chemical and electronic, will choke cash generation. Watch those three, and you are watching the real business rather than the press release.

X. Epilogue & Outro

Step back far enough and Avery Dennison resolves into something rarer than a growth story or a value story: it is a masterclass in how an old-economy industrial champion modernizes without betraying itself. The company did not abandon its core physical strength when the world went digital. It did the harder thing — it digitized the strength it already had, turning a mastery of making one material stick to another into a claim on the digital identity of physical objects.

The surprises are what make the story land. A company that most people still picture as the maker of binder labels quietly sold that very business, at a discount to its revenue, because declining volume is not the same as valuable earnings. A business built on paper and adhesive became one of the largest purchasers of silicon chips in the world. And a fifteen-year cash-burning science project — the kind of thing shareholders usually demand be killed — became the fastest-growing part of the enterprise and the entire basis of its future narrative.

But the story is unfinished, and the honest ending is a question rather than a verdict. Avery Dennison lives in the tension between two identities: the reliable, oligopolistic, cash-generative adhesive-materials business that pays for everything, and the high-tech, high-margin, digital-twin future that justifies the premium the market sometimes assigns it. The bull says the second identity is inevitable and just getting started in the fresh-food aisle. The bear says the second identity is a decelerating apparel business dressed up in software language, vulnerable to commoditization the moment the patents age. The company's own CEO admitted he is not satisfied with the growth. The next several years — measured in Intelligent Labels organic growth, in whether Kroger's bakery becomes Walmart's meat counter, and in whether atma.io becomes a real annuity or stays a feature — will settle which story was true. For a long-term investor, that unresolved tension is not a reason to look away. It is the entire reason to keep watching.

References

-

Avery Dennison Announces Fourth Quarter and Full Year 2025 Results — Avery Dennison Corporation, 2026-02-04 ↩

-

Avery Dennison (AVY) Q4 2025 Earnings Call Transcript — The Motley Fool, 2026-02-04 ↩↩↩↩↩↩↩↩↩↩↩↩

-

Avery Dennison Completes Acquisition of Smartrac's Transponder Business — Avery Dennison Corporation, 2020-03-02 ↩↩

-

Avery Dennison's TexTrace Acquisition Targets Integrated RFID for Apparel — RFID Journal, 2022-02-01 ↩

-

Kroger rolls out Avery Dennison RFID tech to reduce food waste — Packaging Dive, 2024-10-24 ↩

-

Avery Dennison Expands RFID Adoption in Grocery Retail Industry — Avery Dennison Corporation, 2024 ↩

-

Avery Dennison works with Walmart to add RFID to fresh categories — Packaging Dive, 2025 ↩

-

Avery Dennison buys unit of Meridian Adhesives Group for $390M — Crain's Cleveland Business, 2025-08-26 ↩↩

-

Avery Dennison Completes Acquisition of Meridian's Flooring Business — Avery Dennison Corporation, 2025-10-21 ↩

-

Avery Dennison Corporation Definitive Proxy Statement (DEF 14A) — U.S. Securities and Exchange Commission, 2025 ↩

-

Here's how much Avery Dennison will pay its new CEO — Crain's Cleveland Business, 2023 ↩

-

atma.io Connected Product Cloud — Avery Dennison Corporation ↩

-

UPM Raflatac Global Self-Adhesive Label Materials — UPM Raflatac ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube