Broadcom: The Acquisition Machine That Ate Silicon Valley

I. Introduction & Episode Setup

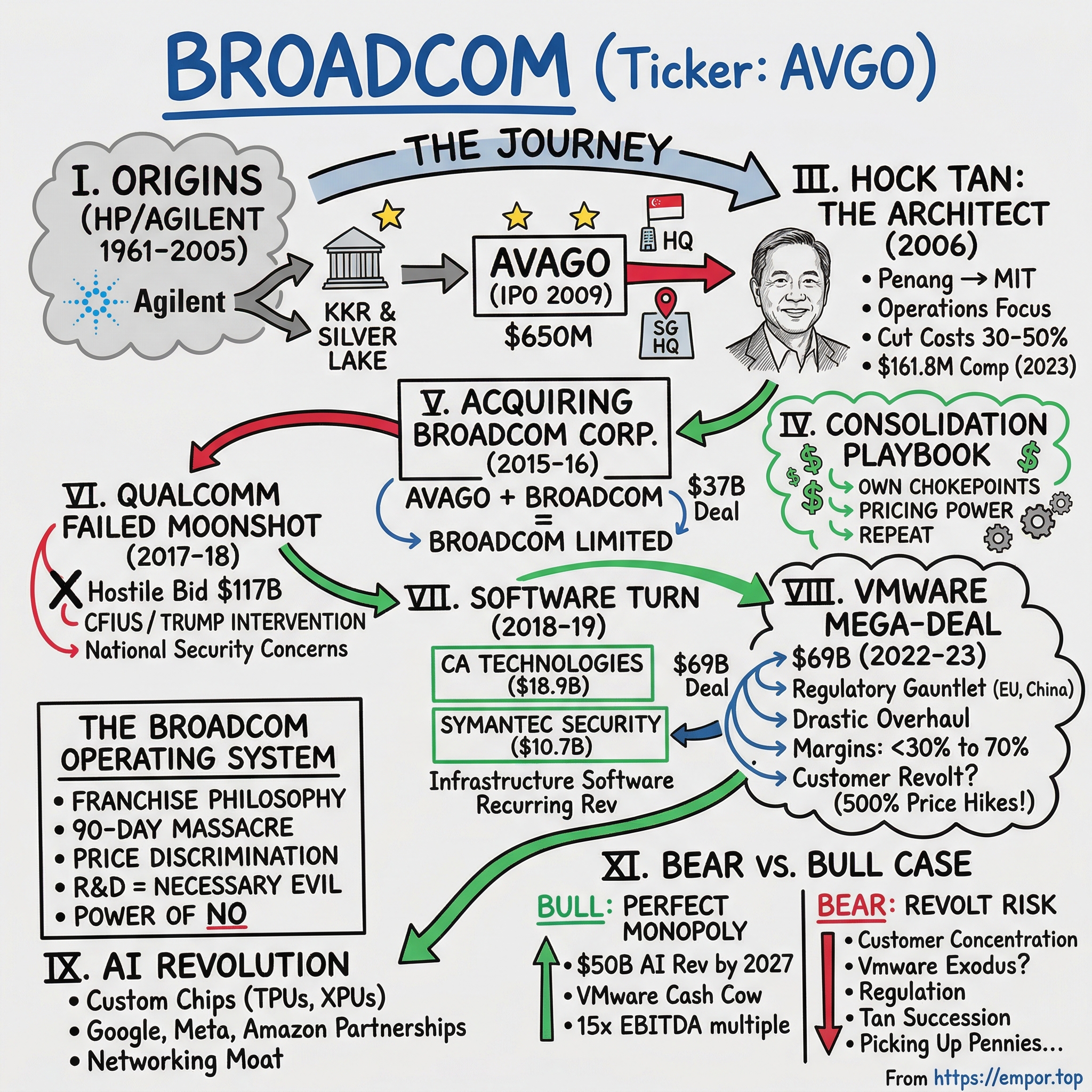

Picture this scene: December 13, 2024. The trading floor at the New York Stock Exchange erupts as Broadcom's market capitalization crosses $1 trillion for the first time. In the company's Palo Alto headquarters, there's no champagne celebration, no bell-ringing ceremony. Just another day at the office for Hock Tan, the Malaysian immigrant who built the most ruthlessly efficient acquisition machine in technology history.

Here's the central paradox that should keep every Silicon Valley founder awake at night: How did a company that spends less on R&D as a percentage of revenue than almost any major tech firm become worth more than Meta, more than Tesla, nearly as much as Amazon? How did a CEO who runs his company like a private equity portfolio, who fires first and asks questions later, who treats innovation labs like expensive hobbies—how did this man become the third-highest-paid executive in America, taking home $161.8 million in 2023?

The answer reveals an uncomfortable truth about modern technology: financial engineering beats product innovation, operational excellence trumps visionary thinking, and the boring business of selling picks and shovels to gold miners remains more profitable than mining for gold yourself.

Broadcom is the anti-Silicon Valley success story. While others chase moonshots and burn cash on the altar of disruption, Tan methodically acquires dominant positions in unglamorous markets—the chips that power your iPhone's WiFi, the software that runs bank mainframes, the virtualization layer beneath every enterprise cloud. Each acquisition follows the same playbook: buy a market leader, slash costs by 30-50%, raise prices, integrate the technology into bundles customers can't refuse, repeat. The stock now trades around $295 as of August 2025, with an all-time high of $312.83 reached just days earlier. The company that employs 37,000 people generates EBITDA margins of nearly 49%—staggering efficiency in an industry where most companies sacrifice profitability for growth.

This is a story about power—how to acquire it, wield it, and compound it relentlessly. It's about a CEO who understood before anyone else that in mature technology markets, consolidation beats innovation. It's about financial engineering so sophisticated it makes Wall Street jealous. And ultimately, it's about how one Malaysian immigrant's vision of operational excellence created more shareholder value than almost any "visionary" founder in Silicon Valley.

Over the next several hours, we'll trace this unlikely journey from a sleepy Hewlett-Packard division to a trillion-dollar colossus. We'll dissect every major acquisition, decode Tan's playbook, and answer the question that haunts every competitor: How do you compete with someone who doesn't play by Silicon Valley's rules?

The uncomfortable truth? You probably can't. And that's precisely why Broadcom keeps winning.

II. The Pre-History: Avago's Origins (1961-2005)

The fluorescent lights hummed in the Hewlett-Packard labs in Palo Alto, 1961. Engineers in white shirts and thin black ties hunched over oscilloscopes, testing the latest semiconductor components. This wasn't the sexy part of HP—no computers here, no calculators that would later define the company. Just diodes, transistors, and the unglamorous building blocks of the electronics revolution. They called it HP Associates, later the Semiconductor Products Division, and for nearly four decades it would remain the forgotten stepchild of the HP empire.

Fast forward to 1999. The dot-com bubble is reaching its frothy peak, and HP makes a decision that would inadvertently create one of the most valuable companies on Earth: spin off the measurement and components businesses into a new entity called Agilent Technologies. The semiconductor division goes along for the ride, still unloved, still generating steady but unspectacular returns from selling optical components and wireless chips.

By 2005, Agilent's semiconductor division is generating about $2.3 billion in annual revenue, decent margins, but zero growth excitement. Management sees it as a distraction from their life sciences and measurement equipment businesses. Enter the private equity wolves: KKR and Silver Lake Partners, who spot what others miss—a solid business with dominant positions in niche markets, ripe for financial engineering.

The $2.66 billion leveraged buyout in December 2005 wasn't just another PE deal. It was the beginning of a transformation that would redefine how technology companies could create value. The newly christened Avago Technologies inherited 6,500 employees across 16 countries, manufacturing facilities in Singapore and Malaysia, and most importantly, entrenched positions in markets too boring for venture capitalists to care about: fiber optic components for data centers, motion control encoders for industrial automation, optocouplers for power management.

The PE playbook began immediately. Costs were slashed—R&D reduced from 15% of revenue to under 10%, sales and marketing trimmed, redundant facilities shuttered. But here's what made Avago different from typical PE slash-and-burn operations: the new owners understood that in semiconductors, you don't need to innovate in every market. You just need to own the critical chokepoints where customers have no alternatives.

They identified what they called "franchise" products—components where Avago had 40%+ market share, where switching costs were prohibitive, where price increases would stick because the component represented less than 1% of the customer's total system cost but failure meant catastrophe. A fiber optic transceiver might cost $50 in a $500,000 data center switch. Raise the price to $75? The customer grumbles but pays—it's not worth redesigning their entire system.

This insight—that pricing power matters more than innovation in mature semiconductor markets—would become the cornerstone of everything that followed. While Silicon Valley chased the next big thing, Avago perfected the art of extracting maximum value from the last big thing.

The Singapore headquarters wasn't chosen by accident. Beyond tax advantages, it positioned Avago at the heart of Asian manufacturing, close to customers like Foxconn and Samsung, with access to lower-cost engineering talent. The company culture reflected this geography—efficient, hierarchical, focused on execution over experimentation. No free lunches or massage chairs here.

By early 2006, the transformation was well underway. Revenue per employee increased 30%. Operating margins expanded from mid-teens to over 25%. The company generated enough cash to begin paying down the acquisition debt faster than anticipated. KKR and Silver Lake knew they had something special—not a technology company in the traditional sense, but a cash-generation machine wrapped in silicon.

But they needed someone to take it to the next level. Someone who understood both semiconductors and financial engineering. Someone willing to be ruthless in pursuit of efficiency. Someone who could spot undervalued assets and integrate them without mercy.

They needed Hock Tan. And in March 2006, that's exactly who they got.

III. Enter Hock Tan: The Architect (2006-2009)

The man who would become Silicon Valley's most feared CEO was eating char kway teow at a hawker center in Penang when he first dreamed of America. Tan Hock Eng—he would later westernize it to Hock Tan—was born in 1951 or 1952 (he's never confirmed which) in British Malaya, just as the country was emerging from colonial rule. His parents ran a small provision shop. His childhood was marked by the peculiar combination of British colonial education, Chinese family expectations, and Malaysian street smarts that would later confound his American competitors.

At 18, Tan won the lottery ticket that would change everything: a Colombo Plan scholarship to MIT. Picture him arriving at Logan Airport in 1971—a teenager from tropical Malaysia experiencing his first Boston winter, carrying everything he owned in two suitcases, speaking accented English that would never quite disappear. While his American classmates debated Vietnam and played Frisbee on the quad, Tan lived on rice and instant noodles, sending money home, studying until his eyes burned.

He blazed through MIT's mechanical engineering program, earning his bachelor's in 1975 and master's the same year—a pace that would define his entire career. But engineering was just the foundation. After MIT, he joined General Motors, then Pepsi, learning the unglamorous art of operations—supply chains, manufacturing efficiency, cost reduction. His colleagues remember him as quiet, methodical, always carrying a notebook where he'd jot down numbers in tiny, precise handwriting.

The entrepreneurial bug bit in the early 1980s. Tan joined a startup called Commodore International, riding the early PC wave. When that ended, he moved to PC components maker Integrated Device Technology. But the formative experience came when he became CFO of a small semiconductor company called ICS in the 1990s. He orchestrated its sale to Integrated Device Technology for $1.9 billion—his first taste of the acquisition game.

By 2005, Tan was running Integrated Device Technology as CEO, but fighting with the board over strategy. He wanted acquisitions; they wanted organic growth. When Silver Lake called in early 2006 about the Avago opportunity, Tan saw his chance to build something without interference from Silicon Valley boards obsessed with consensus.

His first day at Avago: March 1, 2006. No grand speeches. No vision statements. Tan simply gathered the senior staff in a windowless conference room in Singapore and pulled out a spreadsheet. For three hours, he went through every product line, every customer relationship, every manufacturing facility. His questions were surgical: "What's the gross margin?" "Who's the competition?" "What would happen if we raised prices 10%?"

Within weeks, the cuts began. Entire product lines that didn't meet his margin thresholds—gone. R&D projects without clear ROI—terminated. Sales teams selling to small customers—eliminated. One engineer recalled: "He'd walk through the lab, point at a workbench, and say 'What's the return on this?' If you couldn't answer in 30 seconds with a number, you'd find that project canceled by the next morning."

But Tan wasn't just cutting. He was building a machine. He organized Avago into what he called "franchises"—autonomous business units focused on specific market segments. Each franchise president ran their unit like a private equity portfolio company, with strict financial targets and complete operational freedom as long as they hit their numbers. Miss your targets? You're gone. Beat them? You're rich.

The compensation structure was revolutionary for a semiconductor company. Forget stock options vesting over four years. Tan paid cash bonuses that could double or triple base salaries for hitting targets. One franchise president made $3 million in 2007—unheard of for a non-CEO in semiconductors. The message was clear: perform and get paid like a Wall Street trader, fail and find another job.

This wasn't how Silicon Valley worked. The valley celebrated missionaries building cathedrals; Tan hired mercenaries focused on quarterly earnings. The valley valued consensus and collaboration; Tan ran Avago like a benevolent dictatorship. The valley spent lavishly on R&D moonshots; Tan viewed R&D as a necessary evil, useful only when it directly drove revenue.

By 2008, the transformation was stunning. Avago's operating margins had reached 35%, best-in-class for semiconductors. Free cash flow exceeded $500 million annually. The company had paid down most of its acquisition debt. Silver Lake and KKR knew it was time to cash out—but not through a sale. They wanted the big prize: an IPO.

The timing seemed terrible. Lehman Brothers had just collapsed. The global financial system was melting down. Tech IPOs were dead. But Tan saw opportunity in chaos. He flew to New York in early 2009, pitched Avago to skeptical bankers as the "anti-cyclical semiconductor play"—a company that generated cash even in downturns because customers couldn't stop buying their critical components.

On August 6, 2009, Avago went public at $15 per share, raising $650 million. It was the largest tech IPO of 2009, and one of the only ones. The stock opened at $16.50 and never looked back. Silver Lake and KKR would eventually make over $10 billion on their $2.6 billion investment—one of the most successful PE exits in history.

But for Tan, the IPO wasn't an exit. It was ammunition. Public currency meant he could do deals with stock. Access to debt markets meant he could leverage up for larger acquisitions. The real game was just beginning.

In his first earnings call as a public company CEO, an analyst asked about Avago's acquisition strategy. Tan's response was telling: "We don't buy technology. We don't buy R&D. We buy franchises—sustainable, defensible positions in markets where we can generate superior returns."

Translation: We buy monopolies, then squeeze them for cash. Silicon Valley just didn't know it yet.

IV. The Consolidation Playbook: Building Through M&A (2009-2015)

The email landed in LSI Corporation's CEO inbox at 6:47 AM on a September morning in 2013: "We should talk. - Hock." No pleasantries, no explanation. Just two words that would trigger a $6.6 billion acquisition and establish Tan's reputation as semiconductors' most aggressive consolidator.

LSI's CEO knew exactly what this meant. Tan had been circling for months, showing up at the same industry conferences, asking pointed questions about LSI's storage controller business during supposedly casual conversations. The Avago machine had already digested several smaller acquisitions—CyOptics for $400 million, a small optical components company that Tan had stripped down and integrated in less than six months. But LSI would be different. This was Tan's first mega-deal, ten times larger than anything Avago had attempted.LSI was a Silicon Valley institution, founded in 1981 by Wilfred Corrigan, one of the legendary "Fairchildren" who'd left Fairchild Semiconductor to build the modern chip industry. By 2013, LSI had become a sprawling conglomerate—storage controllers, networking processors, custom ASICs, with $2.5 billion in revenue but declining margins and no clear strategy. The deal, announced December 16, 2013, valued LSI at $6.6 billion, a 40% premium to its market cap.

The financing structure revealed Tan's sophistication. Avago would use $1 billion cash from the balance sheet, a $4.6 billion term loan, and crucially, a $1 billion investment from Silver Lake Partners in the form of a seven-year 2% convertible note with a conversion price of $48.04 per share. Silver Lake, Tan's original backer, was doubling down.

But here's where Tan's playbook diverged from typical semiconductor M&A. He didn't want LSI's entire portfolio. Within hours of the deal closing in May 2014, Tan was already carving up the company. Intel bought LSI's Axxia networking processor business for $650 million—a unit that generated $113 million in revenue with 650 employees. Gone. The flash controller business? Sold to Seagate for $450 million. Gone.

What remained were the crown jewels: the storage controller business with 70% market share in enterprise RAID controllers, and the custom ASIC unit that designed chips for companies like Cisco. These were classic Tan "franchises"—dominant positions in markets where customers couldn't easily switch.

The integration was brutal and swift. Avago anticipated achieving annual cost savings at a run rate of $200 million by the end of fiscal 2015. In reality, Tan exceeded that target within six months. Entire buildings in Milpitas were shuttered. The 12,000-person company was reduced to 7,000. R&D projects without clear 18-month revenue visibility were terminated.

One former LSI engineer described the first all-hands meeting: "Tan walked in, no slides, no vision speech. He just said, 'We're not a technology company. We're a business. If you're working on something that doesn't directly generate revenue in the next four quarters, stop now and find something that does.'"

The cultural transformation was even more dramatic. LSI had operated like a traditional Silicon Valley company—consensus-driven, engineering-focused, with elaborate decision-making processes. Tan replaced the entire executive team within 90 days. The new leaders were Tan loyalists who understood the playbook: cut first, ask questions later.

But the genius wasn't just in cost-cutting. Tan understood that LSI's customers—enterprise storage vendors like Dell, HP, and IBM—were locked into multi-year product cycles. They couldn't switch suppliers without redesigning entire product lines. So while he cut costs by 40%, he raised prices by 15-20%. Customers complained but paid. Where else would they go?

The franchise model became clearer with LSI. Each business unit operated independently with its own P&L. The storage controller team in Colorado never spoke to the ASIC team in California. There were no synergies to chase, no grand integration plans. Just autonomous units generating cash, with Tan as the portfolio manager allocating capital to whoever generated the highest returns.

This approach scandalized Silicon Valley traditionalists. "He runs Broadcom like an investment portfolio," one competitor CEO told me, shaking his head. "They are all independent fiefdoms. There's no vision, no innovation culture, no moonshots. Just brutal efficiency."

But the numbers didn't lie. Within 18 months of closing, the LSI acquisition had increased Avago's free cash flow by $800 million annually. The company's stock price doubled. The acquisition was completed on May 6, 2014, and Avago anticipated achieving $200 million in annual cost savings by November 2015—targets that would prove conservative.

The pattern was now established. Buy established franchises in mature markets. Cut costs ruthlessly. Raise prices on locked-in customers. Generate cash. Repeat. It wasn't elegant, it wasn't visionary, but it was devastatingly effective.

As 2014 turned to 2015, Tan was already hunting for his next target. The LSI deal had proven he could digest large acquisitions. The debt markets loved him—Avago's bonds traded at tight spreads despite the leverage. The stock market rewarded him with ever-higher multiples.

The semiconductor industry was ripe for consolidation. Hundreds of companies competed in fragmented markets with duplicative R&D spending. Someone just needed to be ruthless enough to rationalize it all. And Hock Tan had proven he was exactly that person.

Little did anyone know that his next target would shake the entire industry to its core. He was about to go after the crown jewel of communications semiconductors—the original Broadcom itself.

V. The Big Bang: Acquiring Broadcom Corporation (2015-2016)

Henry Samueli was debugging a circuit design in his UCLA lab when his graduate student Henry Nicholas burst through the door. "Professor, we need to start a company. Now." It was 1991, and the two Henrys—teacher and student, methodical engineer and charismatic visionary—were about to create one of Silicon Valley's greatest success stories. They called it Broadcom, a portmanteau of "broad" and "communications," because they believed every device would eventually need to communicate.

Their timing was perfect. The internet was exploding, WiFi was being invented, and smartphones were still a decade away but the infrastructure they'd need was being built. Broadcom rode every wave—cable modems, DSL, Gigabit Ethernet, Bluetooth, WiFi chips. By 2015, the company had $8.4 billion in revenue and its chips were in virtually every connected device on Earth.

But Broadcom had lost its way. The founders had departed—Nicholas in scandal after a wild period involving drugs and prostitutes that led to federal charges (later dropped), Samueli stepping back after SEC issues over backdated stock options. The company drifted through a series of professional CEOs who couldn't recapture the magic. Margins declined. The stock languished. Activist investors circled. On May 27, 2015, word leaked. Broadcom's stock surged 20% in minutes. The next morning, May 28, the announcement came: Avago would acquire Broadcom in a cash and stock transaction that values the combined company at $77 billion in enterprise value. Upon completion of the acquisition, the combined company will have the most diversified communications platform in the semiconductor industry, with combined annual revenues of approximately $15 billion.

The structure was classic Tan financial engineering: Avago would acquire Broadcom for $17 billion in cash consideration and the economic equivalent of approximately 140 million Avago ordinary shares, valued at $20 billion as of May 27, 2015, resulting in Broadcom shareholders owning approximately 32% of the combined company. Based on Avago's closing share price as of May 27, 2015, the implied value of the total transaction consideration for Broadcom is $37 billion.

The most telling moment came at the announcement press conference. Reporters expected the usual merger platitudes about "synergies" and "innovation." Instead, Tan was brutally honest: "Today's announcement marks the combination of the unparalleled engineering prowess of Broadcom with Avago's heritage of technology from HP, AT&T, and LSI Logic, in a landmark transaction for the semiconductor industry. The combination of Avago and Broadcom creates a global diversified leader in wired and wireless communication semiconductors. Avago has established a strong track record of successfully integrating companies onto its platform. Together with Broadcom, we intend to bring the combined company to a level of profitability consistent with Avago's long-term target model."

Translation: We're going to apply the Avago playbook to Broadcom's bloated operations.

The founders' reactions were revealing. Henry Samueli, ever the diplomat, praised the deal publicly: "We have found a culture and a management team that embody the best of the philosophies on which Broadcom was founded." But privately, insiders say he was devastated watching his life's work get dismantled.

Henry Nicholas was more enthusiastic, perhaps seeing in Tan a kindred spirit of ruthless ambition: "The culture on which Broadcom was founded was demanding, execution-oriented, and certainly not guaranteed to mesh with the average technology company. It was, however, a culture that enabled Broadcom to grow exponentially and emerge as the market leader in every major market segment involving broadband communications. In Avago, we have found a culture and a management team that embody the best of the philosophies on which Broadcom was founded, together with a fast-paced, no-nonsense, process-driven business culture that we need to take our combined company to the next level. I am confident that, under the visionary leadership of Hock Tan, the combined company will realize its potential to be the world's greatest semiconductor company."

The integration began before the deal even closed. Tan formed integration teams that mapped every Broadcom product line, customer relationship, and employee. The verdict was swift: connectivity chips (WiFi, Bluetooth) were franchises worth keeping. The digital TV business? Questionable. The cellular baseband unit competing with Qualcomm? Dead on arrival.

At closing, which completed on February 1, 2016, Broadcom shareholders held 32% of the new Singapore-based company to be called Broadcom Limited. But here came Tan's masterstroke: he kept the Broadcom name. Avago Technologies Limited changed its name to Broadcom to acquire Broadcom Corporation in January 2016. Avago's ticker symbol AVGO now represents the merged entity. The Broadcom Corporation ticker symbol BRCM was retired.

This wasn't sentimentality. The Broadcom brand carried weight with customers that "Avago" never could. It was like a private equity firm buying Coca-Cola and keeping the name while replacing the formula with generic syrup. The brand value remained; everything else was negotiable.

The cuts were immediate and deep. Within six months, Broadcom's 11,750 employees were reduced to roughly 7,500. Entire product lines disappeared overnight. The cellular baseband unit, which had burned billions trying to compete with Qualcomm, was shut down, with key assets sold to Cypress Semiconductor for $550 million. The infrastructure software group was reorganized around profitable maintenance contracts rather than new development.

But again, Tan wasn't just cutting. He was consolidating market power. In connectivity, the combined company now had 60%+ share in WiFi chips. In switching and routing, they controlled key patents and products. These weren't competitive markets anymore—they were Broadcom markets, with Broadcom pricing.

The cultural collision was epic. Broadcom engineers, accustomed to pursuing technical excellence, suddenly faced quarterly revenue requirements. One former engineer recalled: "We had this advanced 5G chip in development, two years of work, breakthrough technology. Tan killed it in a five-minute meeting because the revenue wouldn't hit until 2018."

The financial results, however, were undeniable. In the first full year after closing, the combined company generated $17 billion in revenue with operating margins exceeding 40%. Free cash flow nearly doubled to $7 billion. The stock price soared from $150 to over $200.

More importantly, the deal established a new template for semiconductor consolidation. This wasn't about technology synergies or innovation acceleration. It was about market power, pricing leverage, and operational excellence. The rest of the industry watched in horror and admiration as Tan demonstrated that in mature semiconductor markets, the best technology doesn't win—the best operator does.

The new Broadcom also inherited something invaluable: Broadcom Corporation's patent portfolio, ranked among the top ten in semiconductors. These weren't just defensive patents; they were weapons Tan could wield in cross-licensing negotiations, effectively taxing competitors who needed access to Broadcom's intellectual property.

By late 2016, the transformation was complete. The company that started as a $2.6 billion HP spinoff now generated more cash flow than Intel on a fraction of the revenue. Tan had proven his model could scale. The question was: how much bigger could he go?

The answer would shock even his admirers. Tan was about to attempt something that had never been tried in technology: a hostile takeover of one of America's most strategic technology companies. The target: Qualcomm. The price: $117 billion. The outcome would reshape not just the semiconductor industry, but the relationship between technology and national security.

VI. The Failed Moonshot: Qualcomm & Trump's Intervention (2017-2018)

The PowerPoint slide on the wall of Qualcomm's boardroom showed a simple chart: Broadcom's offer of $70 per share versus Qualcomm's closing price of $64.50. It was November 6, 2017, and Hock Tan had just launched the hostile takeover that would define the limits of corporate ambition in the modern semiconductor industry. The initial offer: $105 billion. When rejected, Tan would raise it to $117 billion—what would have been the largest technology acquisition in history.

But this wasn't like buying LSI or even Broadcom Corporation. Qualcomm wasn't just another semiconductor company. It was the crown jewel of American wireless technology, holder of the fundamental patents for 3G, 4G, and the emerging 5G standards. Every smartphone on Earth paid Qualcomm a licensing fee. More importantly, Qualcomm was America's champion in the race against China's Huawei for 5G dominance. Tan's strategy was brilliant in its simplicity. First, move Broadcom's headquarters from Singapore to the United States to avoid regulatory scrutiny. He'd announced this with great fanfare at the White House on November 2, 2017, standing next to President Trump in the Oval Office. Trump beamed as Tan pledged to bring 20,000 jobs to America. "One of the really great, great companies," Trump called Broadcom.

Just four days later, Tan launched his attack. Within days of its redomiciling announcement, Broadcom disclosed its hostile bid for Qualcomm. The initial offer of $70 per share was rejected. Tan raised to $82. Rejected again. Qualcomm resisted Broadcom's bid, which resulted in Broadcom revising its bid on two separate occasions, for a final announced value of $117 billion.

Qualcomm's board was terrified. They knew exactly what Tan would do to their company—the R&D labs shuttered, the moonshot projects canceled, the transformation from technology innovator to cash cow. In desperation, they played the one card that could stop Tan: national security.

On January 29, 2018, Qualcomm submitted a unilateral CFIUS notice requesting review of Broadcom's actions aimed at electing a majority of directors at Qualcomm. This was unprecedented—typically both parties cooperate to seek CFIUS approval. But Qualcomm was using CFIUS as a defensive weapon against a hostile takeover.

The Committee on Foreign Investment in the United States (CFIUS) immediately saw the threat. Sen. Cornyn's letter argued that Broadcom would drastically cut Qualcomm's investment in 5G wireless technology research and development, creating a market opening for China's Huawei to move into a dominant position, potentially threatening U.S. national security.

A CFIUS letter to both companies laid out the concern starkly: The administration did not detail its national security concerns, but CFIUS last week sent a letter to the attorneys of the two companies saying it was concerned research and development at Qualcomm might atrophy under Broadcom's direction, according to a copy that was reviewed by The Washington Post. If that happened, China's Huawei Technologies, a rival to Qualcomm and a major producer of mobile chips, might become much more dominant around the world.

What followed was a chess match of corporate maneuvering. Broadcom tried to accelerate its redomiciling to the United States, hoping to escape CFIUS jurisdiction—deals between American companies fall outside CFIUS's purview. The order was signed just hours after Broadcom sought to avoid the purview of the Committee on Foreign Investment in the United States (CFIUS) by accelerating its relocation of its headquarters from Singapore to the United States. Broadcom said yesterday that it would speed up its relocation plans and have its headquarters in the U.S. by April 3, two days before Qualcomm's rescheduled annual meeting of stockholders where Broadcom hoped to put its directors up to a vote.

But CFIUS moved faster. CFIUS also issued an interim order to the parties directing that Qualcomm's annual stockholder meeting scheduled for March 6, 2018, be adjourned for 30 days to allow for further investigation by CFIUS.

Then came the knockout blow. On March 12, 2018, after CFIUS had met with Broadcom, the president issued the order blocking the transaction. The language was extraordinary in its finality: "[Broadcom] and Qualcomm shall immediately and permanently abandon the proposed takeover." The Order also stipulated that all 15 individuals listed on the proxy card filed by Broadcom were disqualified from standing for election as directors of Qualcomm.

The Order was truly unprecedented, marking the first time in CFIUS' history that a transaction was blocked before an acquisition agreement was even signed. This wasn't just blocking a deal—it was preemptively killing even the possibility of a deal.

Tan's response was measured but revealed his frustration: "Broadcom strongly disagrees that its proposed acquisition of Qualcomm raises any national security concerns." But there was nothing he could do. The President of the United States had personally intervened to stop him.

The irony was thick. The move by Trump to kill the deal comes only months after the U.S. president himself stood next to Broadcom Chief Executive Hock Tan at the White House, announcing the company's decision to move its headquarters to the United States and calling it "one of the really great, great companies."

For Tan, this was more than a failed acquisition—it was a fundamental shift in strategy. If he couldn't consolidate semiconductors through mega-deals, he'd have to find another path to growth. The answer would surprise everyone: software.

In April 2018, just weeks after the Qualcomm deal died, Broadcom announced it would relocate its legal address from Singapore to Delaware, which would avoid the review. The company was now officially American, removing one obstacle to future deals. But Tan had learned his lesson. His next targets wouldn't be strategic semiconductor assets that could trigger national security reviews. They would be something entirely different: boring, essential enterprise software that no regulator would care about but every corporation needed.

The pivot from chips to code was about to begin. And it would prove even more lucrative than anyone imagined.

VII. The Software Turn: CA Technologies & Symantec (2018-2019)

The conference room at CA Technologies' Long Island headquarters felt like a time capsule. Wood paneling from the 1980s, beige carpets, the faint smell of decades-old coffee. It was July 11, 2018, just four months after Trump killed the Qualcomm deal, and Hock Tan was about to announce his most audacious pivot yet: Broadcom was buying a mainframe software company for $18.9 billion. Wall Street was baffled. Broadcom and CA Technologies on Wednesday announced that Broadcom has agreed to acquire the enterprise technology company for $18.9 billion in cash. The deal values CA stock at about $44.50 per share, or a premium of about 20 percent to the closing price of CA common stock on July 11. Why would a semiconductor company buy a mainframe software vendor? CA Technologies, formerly Computer Associates, was everything Silicon Valley wasn't—East Coast, old-school, selling software to run IBM mainframes that most thought would be extinct by now.

But Tan saw what others missed. In fiscal 2018 (ended in March), the company posted revenue of $4.24 billion (up 5%) and free cash flow (FCF) of $1.15 billion. More importantly, Mainframes remain the backbone of the enterprise-computing environment, running mission-critical applications. It is estimated that mainframes process approximately 30 billion transactions per day and $7 trillion of credit card payments annually.

This wasn't about technology synergies. It was about monopoly economics. CA dominated several niches in mainframe software—system management, job scheduling, database tools. Banks, insurance companies, government agencies literally couldn't operate without CA's software. And here's the kicker: switching costs were astronomical. Ripping out CA's software meant rewriting decades of custom code, retesting millions of transactions, risking the systems that processed trillions of dollars.

Historically a semiconductor-based-only company, the failure of the Qualcomm bid led Broadcom and its CEO to look at acquiring infrastructure software as an alternative way of growing in size. Tan's pivot to software wasn't random—it was strategic. Software had even better economics than semiconductors: 90%+ gross margins, subscription revenue models, and switching costs that made even chip design lock-in look weak.

The integration followed the familiar playbook. Within months, CA's workforce was slashed. Entire product lines deemed non-strategic were sold or shuttered. R&D spending dropped from 15% of revenue to under 8%. But prices? They went up. Way up. Some customers reported 30-40% increases on renewal. Just as CA was closing, Tan struck again. On August 8, 2019, Broadcom announced an agreement to acquire the enterprise security business of Symantec Corporation for $10.7 billion in cash. This wasn't the consumer Norton antivirus business—that stayed with Symantec. Tan wanted the enterprise security products: endpoint protection, data loss prevention, web gateways. The boring, essential tools that Fortune 500 companies used to protect their networks.

"M&A has played a central role in Broadcom's growth strategy and this transaction represents the next logical step in our strategy following our acquisitions of Brocade and CA Technologies," said Hock Tan. "Symantec's enterprise security business is recognized as an established leader in the growing enterprise security space and has developed some of the world's most powerful defense solutions that protect against today's evolving threat landscape and secure data from endpoint to cloud."

The pattern was now unmistakable. Tan wasn't building a software company in the traditional sense. He was assembling a portfolio of monopolistic positions in infrastructure software—the unglamorous but essential tools that enterprises couldn't function without. Mainframe management from CA. Storage networking from Brocade (acquired for $5.5 billion in 2016). Enterprise security from Symantec.

Each acquisition followed the same playbook. The Symantec enterprise business produced $2.3 billion in revenue in the 2019 fiscal year. Tan promised $1 billion of run-rate cost synergies within 12 months following close. Translation: half the workforce would be gone within a year.

One industry analyst captured the confusion: "Is it a chip company? Is it a software company? Or is it becoming an investment vehicle, like a tech fund with very little connective tissue between investments? It's hard to say now."

But Tan knew exactly what he was building. Not a technology conglomerate in the traditional sense, but a collection of toll booths on the information superhighway. Every enterprise needed semiconductors for their hardware, mainframe software for their legacy systems, security software for protection, storage software for their data. Broadcom would own critical pieces of each layer.

The financial results validated the strategy. By the end of 2019, Broadcom's infrastructure software division was generating $5 billion in annual revenue with EBITDA margins exceeding 70%. The semiconductor business continued to print cash. Total company EBITDA margins approached 55%—unheard of for a company of Broadcom's scale.

Wall Street was gradually coming around to Tan's vision. The stock price climbed steadily, crossing $300 for the first time. Analysts who'd initially criticized the software pivot now praised Broadcom's "diversified platform" and "recurring revenue streams."

But Tan wasn't done. The CA and Symantec deals were just appetizers. He was hunting for something bigger, something that would cement Broadcom's position as the essential infrastructure provider for every enterprise on Earth.

The target was VMware, the crown jewel of enterprise virtualization. The price tag would be astronomical: $69 billion. The integration would be brutal. The customer backlash would be severe. And it would be Tan's masterpiece.

VIII. The VMware Mega-Deal: Betting the Company (2022-2023)

The Zoom call flickered to life at 6 AM Pacific on May 26, 2022. VMware CEO Raghu Raghuram stared at his screen, knowing what was coming but still unprepared for the reality. On the other end, Hock Tan delivered the news with characteristic brevity: "We're buying you. $142.50 per share. Cash and stock. $69 billion total. Non-negotiable."VMware wasn't just another software company. Founded in 1998, it had invented x86 virtualization—the technology that allowed multiple operating systems to run on a single server, revolutionizing data centers worldwide. By 2022, VMware's software ran in virtually every Fortune 500 data center. Revenue exceeded $12 billion annually. The company employed 38,000 people globally.

In May 2022, Broadcom announced an agreement to acquire VMware in a cash-and-stock transaction valued at $69 billion. The acquisition was closed on November 22, 2023. It would be the fifth-largest technology acquisition in history, behind only Microsoft-Activision, Dell-EMC, and a handful of others.

The structure was complex: Based on the closing price of Broadcom common stock on May 20, 2022, the last trading day prior to media speculation regarding a potential transaction, and a 32% premium to VMware's unaffected 30-day volume weighted average price (VWAP). Upon closing of the transaction, based on the outstanding shares of each company as of the date hereof, current Broadcom shareholders will own approximately 88% and current VMware shareholders would own 12% of the combined company.

But the real story wasn't the price—it was the regulatory gauntlet. Unlike CA or Symantec, VMware was strategically important. Regulators in the US, EU, UK, and China all launched investigations. The European Commission officially decided to start a four-month investigation into the Broadcom-VMware pairing, putting a significant crimp in Tan's plans for closing the deal. The United Kingdom's Competition and Markets Authority (CMA) regulator initiated an advanced review phase on the deal.

The concerns were legitimate. VMware's vSphere hypervisor had 70%+ market share in enterprise virtualization. Broadcom's chips powered many of the servers VMware ran on. Regulators feared Broadcom would use its hardware position to disadvantage VMware competitors or bundle products in anticompetitive ways.

Tan's response was masterful. He made minimal concessions—agreeing to keep VMware products interoperable with competitors' hardware, maintaining certain APIs. But he never wavered on the fundamental strategy. "We are now refocusing VMware on its core business of creating private and hybrid cloud environments among large enterprises globally and divesting non-core assets," Tan told investors.

The 18-month regulatory review gave VMware employees and customers time to panic. And panic they did. Internal documents leaked showing Broadcom viewed VMware's cloud strategy as a failure. It indicated that Broadcom had little faith in VMware's ability to execute on its cloud strategy and said "VMware has failed. "The deal closed on November 22, 2023. Within 30 days, the earthquake began. Less than a month after the deal closed, Broadcom ended perpetual licenses in favor of a subscription-based billing model and announced a drastic overhaul to the VMware portfolio. The company consolidated VMware's 8,000 SKUs down to just four main bundles: VMware Cloud Foundation (VCF) and vSphere Foundation.

The customer revolt was immediate and severe. As a result of some of these changes, many customers are seeing significant cost increases at both purchase and renewal for VMware products, with new more expensive subscription bundles replacing common perpetual software licenses. Customers have reported VMware license cost increases of up to 500%. Some customers faced price hikes of up to 1200%, with some, like AT&T, alleging increases as high as 1050%. For instance, a British university faces a projected increase from £40,000 to £500,000 annually.

The bundling strategy was particularly controversial. As an example, a customer previously purchasing vSphere Enterprise and vCenter Server, at renewal will no longer be able to purchase those licenses individually, instead now having to purchase subscriptions to VMware Cloud Foundation or VMware vSphere Foundation, thus having to purchase the likes of Tanzu and vSAN, regardless of whether that customer requires these products. But here's where Tan's genius—or ruthlessness, depending on your perspective—became apparent. Despite the backlash, the strategy was working financially. By Q1 2025, Broadcom revealed that by the end of Q1, approximately 70% of the company's top 10,000 customers had adopted VCF. The infrastructure software revenue surged 47% YoY to $6.7 billion, largely fueled by increased revenue from VMware.

More impressively, VMware's operating margins transformed from below 30 percent to 70 percent. VMware's quarterly costs have fallen from an average $2.4 billion to $1.2 billion in this quarter. It therefore looks a lot like Broadcom has added around $1 billion to quarterly VMware revenue in a little over a year.

The customer reaction remained severe. The Dutch government even won a court case forcing Broadcom to provide support during migration: Under the court order, VMware and Broadcom must provide exit support for up to two years, including maintenance updates, bug fixes, and technical support. Failure to comply will result in penalties of €250,000 ($290,000) per day, up to €25 million ($29 million).

But Tan was unfazed. As he explained to investors: "We overhauled our software portfolio, our go-to-market approach and the overall organizational structure. We've changed how and through whom we will sell our software. And we've completed the software business-model transition that began to accelerate in 2019, from selling perpetual software to subscription licensing only – the industry standard. Of course, we recognize that this level of change has understandably created some unease among our customers and partners."

Translation: We're extracting maximum value from VMware's installed base, and there's nothing they can do about it. The switching costs are too high, the alternatives too risky, the disruption too severe. Most will complain, negotiate, and ultimately pay.

The VMware acquisition represents the apotheosis of the Broadcom model. Take a company with essential technology, eliminate optionality, bundle products, raise prices, cut costs, and harvest cash flow. It's private equity masquerading as a technology company, and it's working brilliantly from a financial perspective.

By the end of fiscal 2024, Broadcom's infrastructure software division was approaching $25 billion in annual revenue with operating margins exceeding 70%. The semiconductor business continued its steady growth. Total company revenue exceeded $50 billion. The stock price had more than doubled since the VMware announcement.

The transformation was complete. Broadcom had evolved from a $2.6 billion semiconductor spinoff to a diversified infrastructure colossus worth over a trillion dollars. And it had done so not through innovation or vision, but through ruthless operational excellence and financial engineering.

IX. The AI Revolution: Custom Chips & Hyperscaler Partnerships (2023-Present)

The conference room at Google's Mountain View headquarters was silent except for the hum of air conditioning. It was March 2024, and Hock Tan was presenting something unprecedented: Broadcom would design and manufacture Google's next-generation TPU (Tensor Processing Unit) at a scale and complexity never before attempted by an external partner. The price tag wasn't disclosed, but industry insiders estimated it at $15-20 billion over three years.

This wasn't Broadcom chasing the AI hype. While Nvidia was grabbing headlines with its H100 GPUs selling for $40,000 each, Tan was quietly positioning Broadcom as the arms dealer to everyone building their own AI weapons. The strategy was brilliant: let Nvidia own the merchant silicon market while Broadcom owned the custom silicon that hyperscalers really wanted. "Our AI revenue, which came from strength in custom AI accelerators or XPUs and networking, grew 220%" Tan announced in December 2024. For the year, the company said AI revenue jumped 220% to $12.2 billion. But this wasn't about competing with Nvidia on general-purpose GPUs. This was about something far more strategic.

"We currently have three hyperscale customers who have developed their own multi-generational AI XPU roadmap to be deployed at varying rates over the next three years," Tan revealed. Industry insiders knew exactly who these were: Google with its TPUs, Meta with its training clusters, and likely Amazon or another major player. "In 2027, we believe each of them plans to deploy 1 million XPU clusters across a single fabric."

The numbers were staggering. AI revenue serviceable addressable market for XPUs and network in the range of $60 billion to $90 billion in fiscal year 2027 alone. Broadcom was positioning itself to capture the majority of this market.

The strategy was classic Tan: don't compete where you can't win, dominate where others can't compete. Nvidia owned the merchant silicon market for AI training—their CUDA ecosystem was too entrenched. But hyperscalers didn't want to be dependent on Nvidia. They wanted custom silicon optimized for their specific workloads, and only Broadcom had the design expertise, manufacturing relationships, and financial resources to deliver at scale.

Broadcom's 3.5D eXtreme Dimension System in Package (XDSiP) platform technology, enabling consumer AI customers to develop next-generation custom accelerators (XPUs). The 3.5D XDSiP integrates more than 6000 mm2 of silicon and up to 12 high bandwidth memory (HBM) stacks in one packaged device—technology that even Nvidia struggled to match.

But the real moat wasn't just the chips—it was the entire ecosystem. Broadcom's Ethernet networking solutions enhanced the efficiency of high-speed data transfers, crucial for AI operations. The Tomahawk 6 switch, introduced in Q2 2025, is capable of supporting clusters of over 100,000 AI accelerators. Unlike proprietary interconnects such as NVIDIA's NVLink, Broadcom's Ethernet-based solutions offer interoperability and cost efficiency.

The networking component was crucial. AI networking revenue accounted for 76% of Broadcom's total networking revenue, which grew by 158% year-over-year. As demand for AI cluster connectivity grows, networking components could account for 15%-20% of total AI-related silicon content by FY2027, compared to the current 5%-10%.

This wasn't just selling chips—it was becoming the infrastructure backbone of the AI revolution. While the media obsessed over ChatGPT and generative AI applications, Tan focused on the boring but essential plumbing that made it all possible.

The anti-Nvidia positioning was deliberate and brilliant. During one earnings call, an analyst asked about competition with Nvidia. Tan's response was revealing: "We don't compete with Nvidia. They sell merchant silicon to thousands of customers. We partner with three or four hyperscalers to build custom solutions. Different business, different economics, different value proposition."

Translation: Nvidia gets the glory and the headlines. We get the guaranteed revenue from the biggest spenders in tech.

The customer concentration might seem risky—three customers driving the majority of AI revenue. But these weren't ordinary customers. These were Google, Meta, and Amazon, companies spending $50+ billion annually on data center infrastructure. They couldn't afford to have their custom silicon programs fail. Once committed, they were locked in for years.

By mid-2025, the AI transformation was accelerating. Three existing hyperscale customers intend to use Broadcom kit to build million-XPU clusters – an addressable opportunity worth between $60 and $90 billion in 2027. Broadcom's next-generation XPUs, built on a 3nm process, will debut in the second half of 2025—the first products in the field built at 3nm.

The financial impact was profound. AI semiconductor revenue grew 46% YoY to over $4.4 billion in Q2 2025 alone. The company expects growth in AI semiconductor revenue to accelerate to $5.1 billion in Q3, delivering ten consecutive quarters of growth.

But here's what made Broadcom's AI strategy truly brilliant: it wasn't trying to democratize AI like Nvidia. It was creating an oligopoly where only the richest companies could afford to play. Custom silicon development costs hundreds of millions of dollars. Only hyperscalers had the scale to justify it. And only Broadcom had the capability to deliver it.

The rest of the semiconductor industry watched in frustration. They couldn't compete with Nvidia in merchant silicon. They couldn't compete with Broadcom in custom silicon. They were stuck in the middle, fighting for scraps.

As 2025 progressed, Tan's vision was becoming reality. Broadcom wasn't just participating in the AI boom—it was architecting the infrastructure that would define it for the next decade. Every custom chip, every networking component, every piece of software created switching costs that would lock customers in for years.

The AI revolution had made Nvidia famous. But it might make Broadcom even more profitable.

X. Playbook: The Broadcom Operating System

Inside Broadcom's Palo Alto headquarters, there's a conference room called "The Cutting Room." The name isn't accidental. This is where acquisition targets come to die—or more accurately, where they're dissected, their profitable parts preserved, everything else discarded. The walls display a simple chart: every major acquisition since 2005, the purchase price, the cost cuts achieved, the revenue retained. LSI: bought for $6.6 billion, costs cut by 50%, margins expanded from 15% to 45%. CA Technologies: $18.9 billion purchase, 40% headcount reduction, prices raised 30%. VMware: $69 billion acquisition, margins from 30% to 70%.

This is the Broadcom Operating System in its purest form—a repeatable, scalable process for turning bloated technology companies into cash-generating machines. It's private equity dressed up as a technology conglomerate, and it works with ruthless efficiency.

The Franchise Philosophy

"We don't buy companies. We buy franchises." Tan has repeated this mantra hundreds of times, but few truly understand what it means. A franchise, in Broadcom's terminology, isn't just a market-leading product. It's a product that meets four specific criteria:

First, it must have 40%+ market share in its category. Dominance matters more than growth. Second, switching costs must be prohibitive—not just financially, but operationally. Customers should fear the disruption of switching more than the pain of price increases. Third, the product must be mission-critical but represent less than 5% of the customer's total system cost. This allows for significant price increases without triggering procurement revolts. Fourth, the technology must be mature enough that competitors won't disrupt it with innovation.

WiFi chips for smartphones? Perfect franchise—Broadcom has 60% share, switching would require redesigning the entire phone. Storage controllers for enterprise servers? Ideal—70% market share, embedded in millions of systems. Mainframe software? The ultimate franchise—customers literally cannot operate without it.

But here's what Broadcom doesn't buy: moonshots, platforms "with potential," or anything that requires market education. The company has never, not once, created a new product category. It only buys what already dominates.

The 90-Day Massacre

Every acquisition follows the same playbook, executed with military precision. Day 1: Tan's integration team arrives—usually about 50 people who've done this dozens of times. They already know what they're looking for because they've been studying the target for months, sometimes years.

Days 2-30: The mapping phase. Every employee, every product, every customer relationship is categorized. Green means core to a franchise. Yellow means under review. Red means gone. There's no appeal process. The decisions are made by spreadsheet, not sentiment.

Days 31-60: The cutting begins. Red-tagged employees receive termination notices. Entire buildings are shuttered. Product lines are discontinued with immediate effect. Customer support is reduced to the minimum required by contract. One former CA Technologies employee described it: "It was like watching a perfectly efficient plague. Entire floors would empty overnight. Projects we'd worked on for years just... vanished."

Days 61-90: The integration. Remaining employees are moved to Broadcom's systems, Broadcom's processes, Broadcom's culture—which is to say, no culture at all beyond hitting the numbers. The acquired company ceases to exist as an independent entity. Its products are absorbed into Broadcom's franchises.

By day 91, the transformation is complete. Headcount has typically been reduced by 30-50%. R&D spending slashed by 60-70%. Operating margins expanded by 20-30 percentage points. And prices? They're about to go up.

The Pricing Power Play

Broadcom's pricing strategy is perhaps its most controversial—and successful—element. After each acquisition, prices increase, but not uniformly. The company employs what insiders call "price discrimination at scale."

Small customers see the biggest increases—sometimes 200-300%. They can leave if they want; Broadcom doesn't care. The cost to serve them exceeds their value. Medium customers face 50-100% increases, carefully calibrated to be just below their switching pain point. Large enterprises—the Fortune 500—might see only 20-30% increases, but on volumes so large that the absolute dollar impact is enormous.

But the real genius is in the bundling. Broadcom doesn't just raise prices; it forces customers into bundles that include products they don't want but must accept. Need VMware vSphere? You're buying VCF, which includes NSX and vSAN whether you use them or not. Want CA's mainframe tools? You're getting the entire suite.

The bundles serve three purposes. First, they increase average deal size dramatically. Second, they make switching even harder—you're not replacing one product but an entire stack. Third, they allow Broadcom to claim prices haven't increased much per product, even as the total bill soars.

R&D: The Necessary Evil

Traditional tech companies treat R&D as sacred—the more spending, the more innovative you must be. Broadcom treats it as overhead to be minimized. The company spends less than 20% of revenue on R&D, compared to 25-35% for most semiconductor companies.

But here's the counterintuitive part: Broadcom's R&D is incredibly effective precisely because it's so limited. Every dollar must generate measurable return within 18 months. No moonshots. No research for research's sake. Just targeted development to maintain franchise positions.

The company maintains what it calls "innovation theaters"—small teams that create minor feature improvements to justify price increases and prevent customer revolt. Version 2.1 might add 5% better performance, just enough to claim "continuous innovation" without actually disrupting anything.

Real innovation happens through acquisition. Why spend billions developing new technology when you can buy the market leader after someone else took the risk? It's arbitrage masquerading as strategy.

The Power of No

What Broadcom doesn't do is as important as what it does. The company doesn't chase growth markets—it buys mature ones. It doesn't educate customers—it serves those who already understand the value. It doesn't build platforms—it sells products. It doesn't create ecosystems—it extracts value from existing ones.

This discipline is ruthlessly enforced. Executives who propose growth initiatives are often fired. Sales teams who discount to win deals are terminated. Engineers who want to build "cool" products are shown the door.

One former VMware executive recalled proposing a new cloud-native product that could capture share from younger competitors: "Tan listened for about five minutes, then asked one question: 'Will this generate $100 million in revenue next quarter?' When I said it would take two years to build the market, he literally got up and walked out. That product team was gone by the end of the week."

Capital Allocation Mastery

Every dollar at Broadcom has a job, and that job is to generate more dollars. The capital allocation framework is elegant in its simplicity:

First priority: Service debt from acquisitions. Broadcom typically pays down acquisition debt within 24-36 months, faster than almost any comparable company. Second priority: Dividends to shareholders. The dividend has grown every year since the IPO, a sacred commitment. Third priority: Share buybacks, but only when the stock is genuinely undervalued. Fourth priority: Acquisitions, but only those that meet the franchise criteria.

Notice what's missing? Growth investments, market development, strategic initiatives—all the things typical tech companies prioritize. Broadcom doesn't invest in possibilities; it buys certainties.

Why This Only Works With Hock Tan

The Broadcom model seems simple enough: buy mature tech companies, cut costs, raise prices, repeat. So why hasn't everyone copied it?

Because it requires a unique combination of capabilities that exist in exactly one person: Hock Tan. The financial engineering expertise from his PE background. The operational knowledge from decades in semiconductors. The cultural outsider status that lets him ignore Silicon Valley norms. The ruthlessness to fire thousands without blinking. The discipline to say no to growth. The credibility to convince investors this is sustainable.

Multiple companies have tried to copy the Broadcom playbook. They all failed. They couldn't resist the temptation to innovate. They buckled under customer pressure. They let emotions override spreadsheets. They tried to be liked.

Tan doesn't care about being liked. In a valley that celebrates founder-heroes and visionary leaders, he's the anti-hero who wins by not playing their game. He doesn't give TED talks. He doesn't tweet. He doesn't pontificate about the future. He just generates cash.

As one competitor CEO told me, with a mixture of admiration and disgust: "Hock Tan is what happens when you optimize a human being for shareholder value. No vision, no mission, no purpose beyond the efficient extraction of economic rent. It's horrifying. It's also incredibly effective."

The Broadcom Operating System isn't just a business model. It's a philosophy that says in mature technology markets, operational excellence beats innovation, financial engineering beats product development, and discipline beats vision. It's everything Silicon Valley claims to hate.

It's also worth a trillion dollars.

XI. Bear vs. Bull Case & Financial Analysis

The spreadsheet on the screen showed two scenarios, each equally plausible, each reaching opposite conclusions. It was late 2024, and a major pension fund was debating whether to increase its Broadcom position. The bull case showed the stock doubling to $600. The bear case showed it falling to $200. Both analyses used the same facts but reached different conclusions about what those facts meant.

The Bull Case: The Perfect Monopoly Machine

"Broadcom is the Microsoft of infrastructure—impossible to displace, raising prices annually, with switching costs that border on infinite," the bull analyst began. The math was compelling.

Start with AI. The $12.2 billion in AI revenue for 2024 is just the beginning. With three hyperscalers committed to million-XPU clusters by 2027, and Broadcom capturing 70% of custom silicon spending, AI revenue alone could reach $40-50 billion by 2027. At Broadcom's margins, that's $30 billion in operating profit from a business that barely existed three years ago.

VMware's transformation validates the model perfectly. Despite customer fury, 70% of the top 10,000 customers have adopted VCF. Revenue per customer has increased 3-5x. Operating margins expanded from 30% to 70%. The griping is loud but the checks keep clearing. Where else will they go? The alternatives—rebuilding on public cloud, migrating to unproven platforms—are far more expensive and risky than paying Broadcom's ransom.

The infrastructure software portfolio is a collection of monopolies. CA's mainframe software literally cannot be replaced—banks would rather pay 10x than risk their core systems. Symantec's enterprise security is embedded so deeply that extraction would take years. Each acquisition isn't just accretive; it's a permanent tax on enterprise IT.

The semiconductor franchise model continues to compound. Every smartphone needs Broadcom's RF chips. Every data center needs their switches. Every fiber optic network needs their components. These aren't competitive markets anymore—they're Broadcom markets where the company sets prices and terms.

Financially, the company is a fortress. Free cash flow exceeds $20 billion annually and growing. Debt from the VMware acquisition will be paid down within three years. The dividend is sacred, growing every year. Share buybacks are disciplined, only when value is clear.

The multiple expansion story is compelling. Broadcom trades at 15x forward EBITDA, compared to 25-30x for software monopolies like Microsoft or Adobe. As the mix shifts toward higher-margin software, the multiple should re-rate higher. A 20x multiple on $35 billion of 2027 EBITDA implies a $700 billion market cap, or $150 per share upside.

Most importantly, there's no competition. Who else can design custom silicon at scale? Who else can integrate massive software acquisitions? Who else has the balance sheet for $50+ billion deals? Who else has Hock Tan?

"Broadcom isn't a technology company," the bull concluded. "It's a toll booth on the digital economy. And traffic is only increasing."

The Bear Case: The Revolt Risk

"Broadcom is one customer revolt away from catastrophe," the bear analyst countered. "They're extracting value, not creating it, and eventually, customers will find alternatives."

The customer concentration is terrifying. Three hyperscalers drive the majority of AI revenue. If even one decides to develop capabilities in-house or switch to alternative suppliers, billions in revenue evaporate overnight. Google has already shown signs of designing more chips internally. Amazon's Graviton processors prove they can build their own silicon. What happens when they no longer need Broadcom?

VMware's customer exodus is real and accelerating. Despite the claimed 70% VCF adoption, industry surveys show 40-50% of customers actively planning migration. The Dutch government's legal victory forcing support during migration sets a precedent. Once enterprises complete their three-year contracts, many will leave. VMware could lose 30-40% of its revenue base by 2027.

The pricing power is approaching its limits. AT&T's lawsuit over 1,050% price increases is just the beginning. European regulators are investigating. Customer coalitions are forming. Eventually, the backlash becomes unbearable, forcing either regulatory intervention or mass exodus.

The innovation deficit will eventually matter. Broadcom spends the least on R&D of any major tech company. While they milk existing franchises, competitors develop alternatives. Open-source projects like OpenStack threaten VMware. RISC-V could disrupt proprietary architectures. Nvidia's networking products are gaining share. The moats are wide but not eternal.

Hock Tan is 72 years old. The entire model depends on his unique combination of ruthlessness and competence. No successor has been identified. When Tan steps down—and actuarially, that's soon—who runs this machine? The culture is so dependent on one man that succession risk alone could destroy $200 billion in market value.

The regulatory scrutiny is intensifying. The Qualcomm deal was blocked. European authorities are investigating VMware bundling. Chinese regulators could restrict access to their market. The bigger Broadcom gets, the more it attracts regulatory attention. The next major acquisition might be impossible.

Valuation is stretched even in the bull scenario. At $295 per share, Broadcom trades at 35x free cash flow, higher than most growth companies despite being a mature consolidator. The company is priced for perfection. Any stumble—a failed integration, customer defection, regulatory action—could trigger a 40% correction.

The technology sector is cyclical, and we're late cycle. AI spending will eventually slow. Enterprise IT budgets will tighten. When the music stops, Broadcom's leverage to force price increases evaporates. The company has never been tested in a true technology recession with this much leverage and customer antagonism.

"Broadcom is optimized for extraction in a growing market," the bear concluded. "When growth slows and customers have time to switch, the model breaks. They're picking up pennies in front of a steamroller."

The Financial Reality

Strip away the narratives and focus on numbers. Broadcom's fiscal 2024 revenue was $51.6 billion, up 44% year-over-year. But organic growth excluding VMware was just 7%. The company is financially engineering growth through acquisition, not creating it organically.

Operating margins are spectacular—65% company-wide, 76% in software. But these margins come from cutting investment, not operational efficiency. It's harvesting, not building.

Free cash flow is genuinely impressive—$20+ billion annually. But $18 billion goes to dividends and debt service, leaving little for actual investment. The company is a cash machine, but machines eventually wear out.

The balance sheet is leveraged but manageable. Net debt of $60 billion seems high, but at 3x EBITDA, it's sustainable. The problem isn't the current debt but the need for future acquisitions. Without deals, growth stops. With deals, leverage increases.

Return on invested capital exceeds 30%, best-in-class for large-cap tech. But ROIC is high because invested capital is low—they don't invest in the business. It's a liquidation masquerading as a growth story.

The Verdict

Both cases are right. Broadcom is simultaneously a brilliant business model and an unsustainable extraction machine. It's generating enormous value for shareholders while destroying value for customers. It's the most efficient operator in technology and the least innovative. It's worth a trillion dollars and built on sand.

The outcome depends on timing. In the next 2-3 years, the bull case probably wins. AI demand remains robust, VMware customers remain locked in, pricing power persists. The stock could reach $400-500.

But in 5-10 years, the bear case becomes probable. Customers find alternatives, regulators intervene, Tan retires, growth slows. The unraveling could be swift and brutal.

For investors, Broadcom represents a fascinating paradox: a value stock priced like growth, a monopoly that's temporary, a machine that prints money but might be destroying its own future. It's either the best business model in technology or an elaborate private equity scheme that's gone too far.

As one hedge fund manager summarized: "I'm long Broadcom and short humanity. One of those positions will eventually be wrong. I'm betting it's the second one."

XII. Epilogue & Reflections

The sun was setting over San Francisco Bay as Hock Tan stood in his office, looking out at a Silicon Valley he'd conquered without ever truly joining. It was December 2024, days after Broadcom crossed the trillion-dollar threshold. On his desk sat two items: a congratulatory note from Tim Cook, whose Apple depended entirely on Broadcom's chips, and a class-action lawsuit from VMware customers alleging anticompetitive practices. Both made him smile.

What Broadcom Tells Us About Modern Tech

We want to believe technology companies succeed through innovation, that the best product wins, that creating value for customers creates value for shareholders. Broadcom proves the opposite can be true. Sometimes, perhaps often, financial engineering beats product engineering. Sometimes the winner is whoever can extract the most value from existing innovations, not whoever creates new ones.

This is deeply uncomfortable for Silicon Valley's self-image. The valley likes to think of itself as humanity's R&D department, pushing the boundaries of the possible. Broadcom suggests it might actually be humanity's tax collector, extracting rent from innovations that have already happened.

The traditional Silicon Valley playbook—raise venture capital, build innovative products, grow users, monetize later—looks almost quaint compared to Broadcom's approach: buy monopolies, cut costs, raise prices, repeat. One model creates consumer surplus; the other captures it. One requires vision; the other just requires spreadsheets.

Yet Broadcom's success isn't just about financial engineering. It's about understanding a fundamental shift in technology markets. As industries mature, innovation matters less than execution. When every company needs WiFi chips, the winner isn't who makes them 10% better but who can deliver them profitably at scale. When every enterprise runs on virtualization, market share matters more than features.

The Cultural Impact

Broadcom has changed Silicon Valley in ways both subtle and profound. The company has normalized behaviors once considered beyond the pale: mass layoffs immediately after acquisitions, price increases that border on extortion, the complete abandonment of innovation in favor of extraction.

Other companies are learning from Broadcom's playbook. Oracle's infrastructure cloud pricing, Salesforce's acquisition strategy, Adobe's subscription bundling—all show Broadcom's influence. The idea that you can succeed by acquiring and optimizing rather than innovating is spreading.

This creates a troubling dynamic. If the most successful companies are those that extract value rather than create it, why would anyone build anything new? Why take the risk of innovation when you can wait for others to prove the market, then buy and optimize?

We're seeing the early signs of this shift. Venture capital is flowing toward AI and crypto—the last remaining frontiers where innovation still matters. Everything else is consolidating. The middle market of technology is disappearing, replaced by giants like Broadcom that own entire categories.

Lessons for Founders

If you're building a technology company today, Broadcom offers both a cautionary tale and a potential exit strategy. The cautionary tale: build something truly differentiated or you'll eventually be absorbed and optimized out of existence. The exit strategy: build a franchise position in a niche market and Broadcom might pay you billions to go away.

The key is understanding what Broadcom values: market dominance, customer lock-in, predictable revenue, and minimal competition. If you can build that, you're acquisition bait. If you can't, you're irrelevant.

But here's the dark truth: building for acquisition by Broadcom means building something your customers can't escape from. It means creating switching costs so high that price increases don't matter. It means becoming a necessary evil. That's not the founder's journey most entrepreneurs envision.

The Ultimate Question

Is Broadcom the future of technology conglomerates? The answer depends on whether you believe technology markets will continue to mature and consolidate, or whether new waves of innovation will disrupt existing structures.

The bull case for Broadcomification is compelling. Most technology markets do mature. Most innovations do become commoditized. Most customers do value stability over innovation once their basic needs are met. In this world, Broadcom's model—buying mature franchises and optimizing them ruthlessly—is perfectly adapted.

The bear case requires faith in human creativity. It assumes new innovations will continuously disrupt existing markets, that customers will revolt against extraction, that regulators will intervene, that open source and new architectures will break monopolies. It requires believing that Broadcom's model works only in a specific historical moment that's ending.

The Man and the Machine

Perhaps the most fascinating aspect of Broadcom is how completely it reflects one man's worldview. Hock Tan built a company that operates exactly like he does: ruthlessly efficient, financially focused, utterly unsentimental. There's something almost admirable about the purity of it.

Tan never pretended to be a visionary. He never claimed to be changing the world. He simply set out to generate returns for shareholders, and he's done exactly that. In a valley full of founders claiming to make the world a better place while building advertising monopolies, there's something refreshing about Tan's honesty.

But there's also something troubling about a trillion-dollar company with no mission beyond making money. Broadcom doesn't even pretend to have values beyond shareholder value. It doesn't aspire to anything beyond efficiency. It's capitalism reduced to its purest form—the allocation of capital for the generation of more capital, with no higher purpose.

The Final Reflection

Standing in that office, looking out at the valley, Tan might reflect on what he's built. Not technology—he's never invented anything. Not a culture—Broadcom has none. Not a legacy—he'll be remembered as the man who proved you could succeed without innovation.

What he built was a machine. A perfectly efficient machine for turning market dominance into cash flow. A machine that works brilliantly as long as the inputs—mature technology markets with locked-in customers—keep flowing. A machine that might be the logical endpoint of capitalism in the technology age.

Whether that machine is sustainable, whether it's good for technology progress, whether it's the model others should follow—these questions don't interest Tan. The machine works. The cash flows. The stock price rises. By the only metrics that matter to Broadcom, it's a complete success.

But for the rest of us, Broadcom poses uncomfortable questions. If this is what winning looks like in mature technology markets, do we want to win? If operational excellence means abandoning innovation, is it really excellent? If creating shareholder value means extracting customer value, who ultimately benefits?

Broadcom is worth a trillion dollars. It's also a mirror reflecting uncomfortable truths about modern capitalism, technology markets, and what we truly value. It's the company Silicon Valley deserves but doesn't want to acknowledge.

In the end, Broadcom's greatest innovation might be proving that innovation doesn't matter. That's either the ultimate tragedy or the ultimate triumph of financial engineering over human creativity.

The market has rendered its verdict: triumph, by a trillion dollars.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube