Atmos Energy: The 119-Year Pipeline to America's Largest Natural Gas Distributor

I. Introduction & Episode Roadmap

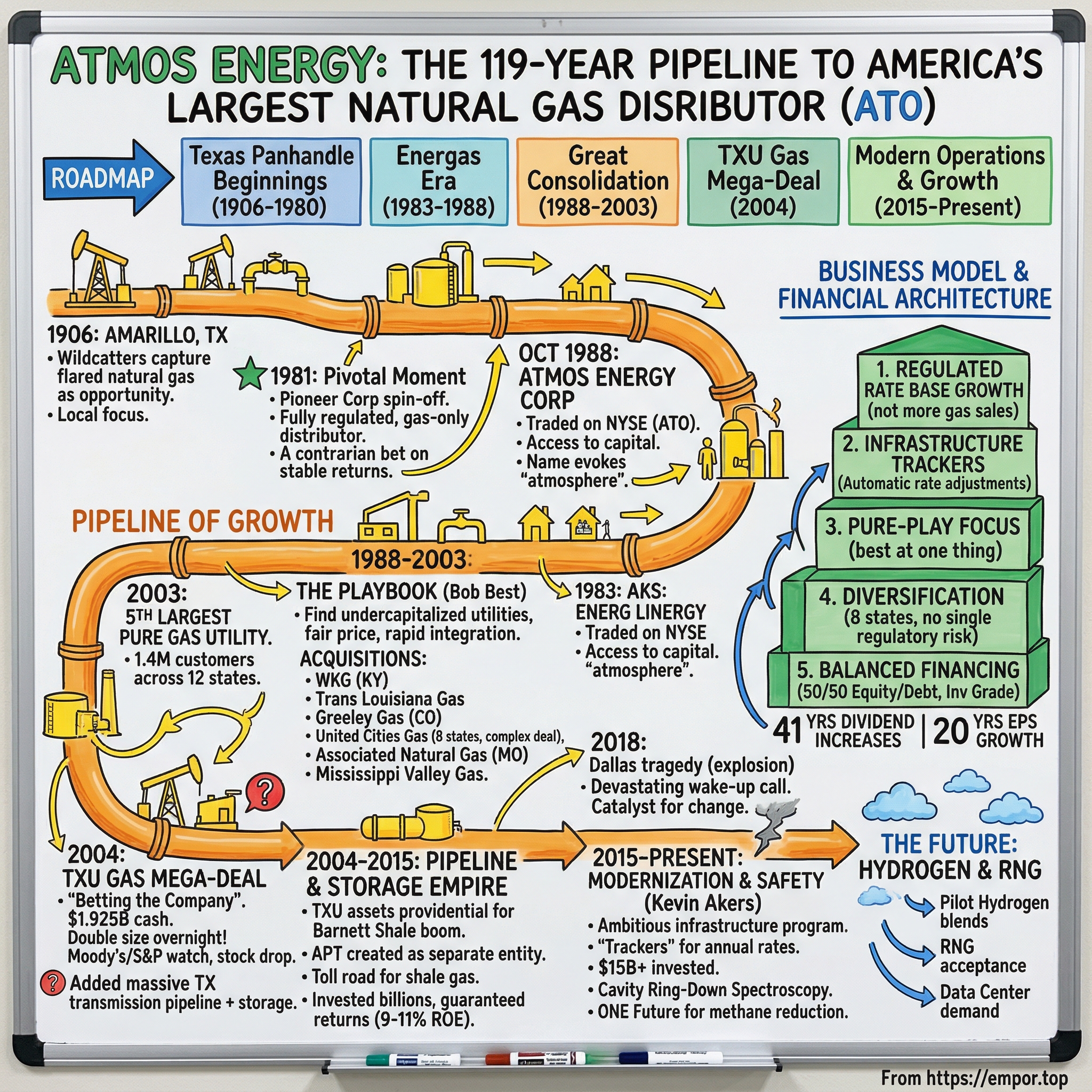

Picture this: It's 1906 in the Texas Panhandle. The land stretches endlessly flat, punctuated only by the occasional windmill and the new derricks sprouting like metallic weeds. A group of wildcatters and local businessmen gather in Amarillo, not to drill for oil, but to capture something even more ephemeral—natural gas, the "waste product" that most drillers simply flared off into the West Texas sky. They couldn't have imagined that their modest gas distribution company would evolve into Atmos Energy Corporation, today serving over 3 million customers across nine states with a market capitalization exceeding $20 billion.

The central question that drives this story isn't just how a regional Texas gas company survived 119 years—plenty of utilities have longevity. It's how Atmos transformed from a frontier operation into America's largest pure-play natural gas distributor through a combination of regulatory mastery, perfectly-timed acquisitions, and an almost religious devotion to the unglamorous work of pipe replacement. This is a story about compound growth in the most literal sense: laying pipe, mile by mile, acquisition by acquisition, rate case by rate case. Today's Fiscal Year 2024 highlights: Earnings per diluted share of $6.83 on net income of $1 billion, marking the culmination of what might be the most remarkable growth story in American utility history. With 41 consecutive years of dividend increases and 20 consecutive years of EPS growth, Atmos has transformed itself from regional player to national powerhouse through a masterclass in regulated utility operations.

What makes this story particularly compelling isn't just the scale—though serving 3.3 million customers across 1,400 communities is impressive—but the strategic clarity with which Atmos has pursued its vision. While competitors diversified into electricity, renewable energy, or unregulated businesses, Atmos doubled down on being the best at one thing: natural gas distribution. This focus, combined with an acquisition strategy that would make any private equity firm envious, created a compounding machine that has delivered returns few utility investors thought possible.

We'll explore how a company in the most boring, regulated corner of the energy sector became a stock market darling, how its management team turned regulatory relationships into competitive moats, and why, in an era of energy transition and electrification threats, Atmos continues to invest nearly $3 billion annually in natural gas infrastructure. This is the story of patient capital, regulatory expertise, and the power of compound growth in America's energy heartland.

II. Origins: The Texas Panhandle Beginning (1906-1980)

The year was 1906, and in the windswept plains of the Texas Panhandle, something remarkable was happening. While the rest of America was racing to find oil—that black gold that powered the industrial revolution—a group of forward-thinking businessmen in Amarillo saw opportunity in what others considered waste. Natural gas, the invisible byproduct that oil drillers routinely flared off in spectacular but wasteful displays, was about to become the foundation of what would eventually become Atmos Energy.

These weren't Wall Street financiers or Eastern industrialists. They were local merchants, ranchers, and yes, a few wildcatters who understood something fundamental about the Texas Panhandle: winters were brutal, distances were vast, and the newfound natural gas seeping from the Permian Basin could heat homes more efficiently than anything else available. The company they formed would go through various incarnations and combinations over the next seven decades, but the DNA was set from the beginning—this would be a utility focused on serving communities, not chasing the latest energy fad. By the 1970s, through decades of mergers and acquisitions that would make today's private equity firms dizzy, these various entities had coalesced into Pioneer Corporation, a large diversified West Texas energy company. But Pioneer was a conglomerate in the classic 1970s sense—oil drilling, gas distribution, real estate, even cattle ranching. It was everything and nothing, a company searching for identity in the post-oil embargo world.

The pivotal moment came in 1981. With deregulation sweeping through the energy sector and Wall Street demanding focus over diversification, the company was incorporated and became a fully regulated natural-gas-only distributor. This wasn't just a corporate restructuring; it was a philosophical revolution. While others chased the boom-bust cycles of oil exploration or the emerging opportunities in electricity generation, the leadership made a contrarian bet: natural gas distribution, the most boring, regulated, predictable part of the energy value chain, would be their future.

Think about the audacity of this decision. In 1981, America was still reeling from the energy crises of the 1970s. Solar panels were being installed on the White House roof. Nuclear power was supposed to be the future. And here was a Texas energy company saying, "No, we're going to distribute natural gas to homes and businesses, collect our regulated return, and compound that for decades."

The infrastructure they inherited was a patchwork quilt of local distribution systems, some dating back to the 1920s when natural gas was first being commercialized. Cast iron pipes ran under dusty West Texas towns, serving customers who had been with the company since their grandparents first switched from coal heating. The customer relationships were multigenerational, the infrastructure was aging but functional, and the regulatory framework was stable if not generous. It was, in short, the perfect platform for what would come next.

III. The Energas Era: Spinning Off & Going Public (1983-1988)

Two years after committing to focus solely on natural gas distribution, Pioneer's board made another transformative decision. In 1983, Energas, the natural gas distribution division of Pioneer, was spun off and became an independent, publicly held natural gas distribution company. The name "Energas" itself was a statement of intent—energy from gas, nothing else. No hedging, no diversification, just pure play natural gas distribution.

The spinoff was orchestrated with the precision of a leveraged buyout, but without the leverage. Management, led by a group of executives who had spent their entire careers in the Texas gas patch, received significant equity stakes. This wasn't just about creating shareholder value through financial engineering; it was about aligning incentives for a long-term consolidation play that would require patience, capital, and most importantly, credibility with regulators across multiple states.

The early days as a public company were not glamorous. Energas traded on regional exchanges, barely covered by analysts, with a market cap that wouldn't have registered on Wall Street's radar. The company's investor presentations—if you can find them in dusty archives—read like engineering reports: miles of pipe replaced, compression ratios improved, customer connections added. There were no promises of revolutionary technology or disruption. Just the steady beat of infrastructure investment and customer growth.

But beneath this mundane exterior, management was laying the groundwork for something extraordinary. They were studying every gas distribution asset in America, building relationships with regulators in neighboring states, and most importantly, developing what would become their secret weapon: the ability to acquire, integrate, and optimize gas distribution assets better than anyone else in the industry.

In October 1988, Energas changed its corporate name to Atmos Energy Corporation and its stock began trading on the New York Stock Exchange under the ticker symbol "ATO". The name change was more than cosmetic. "Atmos" evoked the atmosphere, the air we breathe, positioning natural gas as essential to life itself. The NYSE listing provided access to institutional capital that would fund the acquisition spree about to begin.

The timing was perfect. The late 1980s saw the final waves of energy sector deregulation, creating a fragmented landscape of regional gas utilities, many of them subscale, undercapitalized, and struggling with aging infrastructure. For a company with Atmos's ambitions and capabilities, it was like being a well-capitalized buyer in a distressed market. The stage was set for one of the great consolidation plays in American utility history.

IV. The Great Consolidation Play (1988-2003)

If you want to understand how Atmos Energy became America's largest natural gas distributor, you need to understand Bob Best. When Best became CEO in 1988—the same year Atmos went public on the NYSE—he wasn't a charismatic visionary or a Wall Street darling. He was a utility executive who understood one thing better than anyone else: in the fragmented world of natural gas distribution, scale equals survival, and survival equals returns.

Best's playbook was deceptively simple. Find undercapitalized gas utilities in growing markets. Pay a fair price—not a steal, but fair. Finance with a mix of equity and debt that wouldn't spook the rating agencies. Then execute the integration with military precision. Repeat. It sounds easy, but in practice it required a combination of operational excellence, regulatory finesse, and timing that few could master.

The acquisition spree began in 1989 with Western Kentucky Gas Company, purchased from Texas American Energy. WKG had started in 1934 serving 2,200 customers, but by the time of its acquisition by Energas (Atmos), WKG's customer base had grown to almost 150,000. It was serving Kentucky communities in the higher growth regions of the state and serviced major industrial customers, including aluminum plants, food processors, and the only Corvette plant in the world.

This wasn't just about adding customers. Kentucky represented Atmos's first major expansion outside Texas, and it came with a crucial lesson: every state's regulatory environment was different, but the fundamentals of running a safe, reliable gas distribution system were universal. Master the operations, build trust with regulators, and the rate cases would follow.

The 1990s saw the pace accelerate. Atmos expanded its gas distribution to Louisiana with the acquisition of Trans Louisiana Gas Co. in 1988, and picked up Denver-based Greeley Gas Co. in December 1993. Each acquisition brought new challenges—different pipe materials, varying customer densities, unique regulatory frameworks—but also new capabilities. Greeley, for instance, brought expertise in high-altitude operations and cold-weather resilience that would prove invaluable as Atmos expanded into the Rockies.

In July 1997, the company bought United Cities Gas Co., adding customers in Georgia, Tennessee, Virginia, Illinois, Kansas, Missouri, Iowa and South Carolina. This was the deal that transformed Atmos from a regional player into a truly national utility. United Cities wasn't just large—it was complex, with operations scattered across the South and Midwest. The integration took two years and tested every system Atmos had built.

But here's what separated Atmos from the failed roll-ups of the era: they never tried to centralize everything. Each acquired utility maintained its local identity, its relationships with municipal officials, its understanding of local needs. Atmos provided capital, best practices, and economies of scale in procurement and back-office functions. But the guy who showed up when your furnace wouldn't light? He was still a local, still knew the mayor, still understood that in small-town America, a utility's reputation was built one service call at a time.

In 2000, Atmos purchased the Missouri-based Associated Natural Gas Co., and in 2001 bought Louisiana Gas Service Co. and LGS Natural Gas Co. In December 2002, Atmos acquired Mississippi Valley Gas Co. By 2003, through nine major acquisitions over 15 years, Atmos had assembled a portfolio of gas distribution assets that served over 1.4 million customers across 12 states. The additions made it the fifth largest pure gas utility in the United States.

The financial engineering behind these deals was as impressive as the operational integration. Atmos maintained its investment-grade credit rating throughout, using a carefully calibrated mix of debt and equity that kept leverage ratios within the comfort zone of both rating agencies and regulators. The company's dividend, that sacred cow of utility investing, never missed a beat, growing every single year even as billions were deployed for acquisitions.

But the biggest deal—the one that would define Atmos's future—was yet to come. And it would require not just capital and operational excellence, but the courage to bet the entire company on a single transaction.

V. The TXU Gas Mega-Deal: Betting the Company (2004)

In the spring of 2004, John Wilder, the newly appointed CEO of TXU Corp., surveyed the wreckage of what had once been Texas's energy colossus. TXU, the product of decades of consolidation in the Texas electricity market, had bet big on merchant power generation just as that market collapsed. Debt had ballooned to dangerous levels. Assets needed to be sold, and fast. Among them: TXU Gas, the company founded as Lone Star Gas in 1909, serving 1.4 million customers including the entire Dallas-Fort Worth metroplex.

For Bob Best and his team at Atmos, this was the opportunity of a lifetime. But it was also terrifying. The deal would require $1.925 billion in cash—more than Atmos's entire market capitalization at the time. Permanent funding for the acquisition would consist of approximately $500 million to $600 million of equity, with the remainder of the purchase price funded with long-term debt. This wasn't just leverage; it was a complete recapitalization of the company.

The board meeting where Best presented the deal was, by all accounts, electric. Here was Atmos, which had spent 18 years carefully acquiring small and mid-sized utilities, proposing to double its size overnight. TXU Gas had approximately 26,400 miles of intrastate distribution pipelines, 6,800 miles of transmission pipeline within Texas delivering approximately 400 Bcf annually, and five natural gas storage reservoirs with a working capacity of 38 Bcf.

But Best had done his homework. The presentation to the board wasn't about dreams or synergies—it was about math. The regulated rate base would double. The customer concentration in Texas, a state with favorable regulatory treatment and explosive population growth, would give Atmos unprecedented scale advantages. Most importantly, TXU Gas came with something Atmos had never had: a massive intrastate pipeline system that connected the booming shale gas fields of Texas to its distribution networks.

The negotiation with TXU was swift and decisive. Wilder needed cash, and he needed certainty. Best provided both. The transaction was unanimously approved by the board of directors of Atmos Energy, creating the country's largest pure-play natural gas distribution company with 3.1 million customers in 12 states.

Wall Street's reaction was mixed. Moody's Investors Service placed Atmos' ratings under review for a possible downgrade, and Standard & Poor's placed the company on CreditWatch with negative implications. Both ratings agencies said they were concerned about the business risks and amount of debt Atmos was taking on. The stock dropped 15% on the announcement.

But Best was playing a longer game. He knew something the rating agencies didn't fully appreciate: Texas was about to experience the shale gas revolution, and Atmos would own the pipes connecting that gas to millions of homes and businesses. The 6,800 miles of transmission pipeline weren't just assets; they were toll roads for the coming energy boom.

The integration was a masterclass in execution. Unlike previous acquisitions where Atmos maintained local brands and identities, TXU Gas would be fully rebranded as Atmos Energy. Nearly all of TXU Gas's 1,350 employees would be retained, bringing deep expertise in Texas operations and critical relationships with state regulators.

The TXU Gas operations were expected to be immediately accretive to Atmos earnings in fiscal year 2005 by 5-10 cents/share—a modest projection that would prove laughably conservative. Within five years, the TXU assets would contribute more than half of Atmos's earnings. The deal that had seemed like a dangerous gamble would be remembered as one of the greatest acquisitions in utility history.

VI. Building the Pipeline & Storage Empire (2004-2015)

The acquisition of TXU Gas didn't just make Atmos bigger—it transformed the company into something entirely different. With the stroke of a pen, Atmos had inherited 6,800 miles of transmission pipeline that crisscrossed Texas like veins in a body, and five natural gas storage reservoirs with a working capacity of 38 billion cubic feet. But in 2004, nobody—not even Bob Best—fully understood what was about to happen in the Texas energy market.

George Mitchell, the legendary wildcatter who had spent decades and hundreds of millions of dollars trying to crack the code of the Barnett Shale, had finally succeeded in the late 1990s with a combination of horizontal drilling and hydraulic fracturing. By 2005, just as Atmos was integrating its TXU assets, the Barnett Shale was exploding into one of the largest onshore natural gas fields in the United States, covering 5,000 square miles across 27 counties in north-central Texas.

For Atmos, the timing was almost providential. The Atmos Pipeline - Texas (APT) infrastructure was located at or near existing, new and proposed gas production fields including the Barnett Shale in north Texas and the Bossier Sand in east Texas. The company didn't need to build new pipes to connect to the shale revolution—they already owned them. It was like inheriting a toll road just before a gold rush.

The creation of Atmos Pipeline - Texas as a separate regulatory entity was a stroke of genius. In Texas, intrastate pipelines are regulated by the Railroad Commission of Texas, not FERC, giving Atmos more flexibility in rate-setting and expansion. APT became one of the largest intrastate pipeline operations with approximately 5,700 miles of transmission pipelines within the state, connecting to natural gas production areas in central, north, west and east Texas.

The numbers tell the story of explosive growth. In 2005, new horizontal wells outnumbered new vertical wells in the Barnett for the first time. Gas production from the Barnett area reached peak production in 2009, exceeding 1.7 trillion cubic feet. And Atmos was there to move every molecule, charging regulated rates for transportation and storage that provided steady, predictable returns while the commodity markets gyrated wildly.

But the real innovation wasn't just in owning the pipes—it was in how Atmos managed them. The company pioneered what they called "seamless transportation," working with other pipeline operators like Enbridge to create integrated systems that could move gas from wellhead to burner tip without interruption. The proposed BIG Pipeline (Barnett Intrastate Gas Pipeline) exemplified this approach, connecting Atmos's Line X to Enbridge's systems, creating a 100-mile natural gas transmission pipeline with a capacity of up to 1 billion cubic feet per day.

The storage facilities inherited from TXU became increasingly valuable as the shale boom created new volatility in gas supplies. Atmos Pipeline and Storage operated gas storage with a working capacity of 39 billion cubic feet, the majority of which was contracted by local gas utilities to support winter-season requirements. This wasn't just infrastructure—it was a physical hedge against price volatility that made Atmos indispensable to both producers and consumers.

Between 2005 and 2015, Atmos invested billions in expanding and upgrading its pipeline network. But unlike the wildcatters drilling in the Barnett, Atmos's investments came with guaranteed returns. Every dollar spent on pipeline expansion, every compressor station upgraded, every storage facility enhanced—all of it went into the rate base, earning regulated returns that typically ranged from 9% to 11%.

The company also made a crucial strategic decision: while others were building long-haul interstate pipelines to move Barnett gas to distant markets, Atmos focused on serving Texas. The bet was that Texas's booming population and industrial growth would create insatiable demand for natural gas right where it was being produced. No need for complex interstate regulatory approvals, no exposure to basis differentials between regions—just pure, Texas-regulated returns.

By 2015, Atmos Pipeline - Texas was transporting gas to the largest local distribution company in the state (Atmos's own distribution division), along with other smaller utilities, industrial end-users, independent power plants, and other pipelines. The system had become the circulatory system of Texas's natural gas economy, invisible to most but essential to all.

The Barnett Shale boom would eventually slow, victims of their own success as overproduction crashed prices. Many of the independent producers who had rushed into the play would go bankrupt. But Atmos? They kept collecting their regulated returns, quarter after quarter, year after year. They had built the roads, not the cars, and in the infrastructure business, the roads always get paid.

VII. Modern Operations: Safety, Modernization & Growth (2015-Present)

On January 13, 2018, a house exploded in Dallas. The blast killed 12-year-old Linda Rogers and injured four others. The cause: a leak in an aging cast-iron gas main that Atmos Energy had been scheduled to replace—but hadn't yet. For a company that had built its reputation on operational excellence, it was a devastating wake-up call.

The tragedy could have destroyed Atmos. Instead, under the leadership of CEO Kevin Akers, who had taken the helm in 2017, it catalyzed the most ambitious infrastructure modernization program in American utility history. We replaced 900 miles of distribution and transmission mains and 47,700 service lines. Over the last eleven years, we have invested over $15 billion dollars to modernize and expand our natural gas systems.

But the numbers only tell part of the story. What Akers and his team understood was that the traditional utility playbook—replace pipes when they fail, invest the minimum required by regulators—was no longer sufficient. Climate activists were targeting natural gas infrastructure. Electrification advocates were pushing to ban gas in new construction. The industry that had seemed invulnerable was suddenly under existential threat.

Atmos's response was counterintuitive: lean into the criticism. The company launched the most transparent safety program in the industry, publishing detailed pipeline replacement schedules neighborhood by neighborhood. From 2019 to 2024, we have invested $10.7 billion to enhance safety, reliability, lower methane emissions, and support growth and economic development in Texas. Similar investments were made across the system: $866 million in Louisiana, $849 million in Kentucky, Tennessee, and Virginia, and $780 million in Mississippi.

The technology deployed was cutting-edge. Atmos pioneered the use of Cavity Ring-Down Spectroscopy (CRDS) technology, which is 1,000 times more sensitive than traditional leak detection methods. By fiscal year 2023, the company had sixteen CRDS units operating across every division. They initiated pilot programs using satellite and aerial methane detection, turning their entire 76,000-mile pipeline network into a monitored, intelligent system.

But perhaps the most innovative aspect of Atmos's modernization wasn't technological—it was financial. The company pioneered what they called "infrastructure trackers," regulatory mechanisms that allowed for annual rate adjustments based on safety and reliability investments without the need for contentious rate cases. Over the next five years, we plan to replace between 4,000 and 5,000 miles of distribution and transmission pipe and between 120,000 and 170,000 steel service lines.

This wasn't just maintenance; it was transformation. Old cast-iron and bare steel pipes that had been installed when Eisenhower was president were being replaced with modern polyethylene pipes that could last a century. The company developed sophisticated risk models that considered pipe age, material, location, leak history, and dozens of other factors to prioritize replacements. Every decision was data-driven, every investment optimized for both safety and return.

The Charles K. Vaughan Center in Plano, Texas, epitomized this new approach. Named after the company's first chairman and CEO, the facility featured "Gas City," a simulated community complete with houses, apartments, commercial buildings, and city streets with natural gas infrastructure. Here, technicians didn't just learn procedures—they practiced in conditions that replicated real-world complexity.

The environmental angle became increasingly important. Atmos joined Our Nation's Energy Future Coalition (ONE Future), committing to reduce methane emissions across its operations. The company set aggressive targets: a 50% reduction in methane emissions from distribution system mains and services by 2035 from 2017 levels. For a natural gas company in the age of climate activism, this wasn't just good PR—it was existential.

Earnings per diluted share of $6.40 on net income of $1.0 billion. Capital expenditures were $2.6 billion; approximately 86% focused on safety and reliability. The latest guidance shows the momentum continuing: Fiscal 2025 earnings per diluted share guidance expected to be in the range of $7.35 - $7.45 per diluted share. Fiscal 2025 capital expenditure guidance expected to be approximately $3.7 billion.

The transformation has been rewarded by both regulators and investors. The company maintained strong relationships with state utility commissions, who saw Atmos as a partner in modernizing critical infrastructure rather than an adversary seeking to extract maximum profits. The stock price reflected this success, consistently outperforming utility indices as investors recognized that Atmos had cracked the code: how to be a growth company in a no-growth industry.

VIII. The Business Model & Financial Architecture

To understand Atmos Energy's financial success, you need to understand a fundamental truth about regulated utilities: they're not really in the energy business—they're in the capital deployment business. Every dollar invested in approved infrastructure earns a regulated return, typically 9-11% annually. The game isn't about selling more gas; it's about growing the rate base while maintaining regulatory goodwill.

Atmos operates through two distinct segments that work in beautiful symbiosis. The Distribution segment, which serves approximately 3.3 million customers across eight states, operates under traditional utility regulation. This segment distributes natural gas to approximately 3.3 million residential, commercial, public authority, and industrial customers; and owned 73,689 miles of underground distribution and transmission mains.

The Pipeline and Storage segment, primarily consisting of Atmos Pipeline-Texas, operates under a different but equally attractive regulatory framework. This segment transports natural gas for third parties and manages five underground storage facilities in Texas; provides ancillary services customary to the pipeline industry, including parking arrangements, lending, and inventory sales; and owned 5,645 miles of gas transmission lines.

The genius of this two-segment structure is how it creates multiple avenues for growth. The distribution business benefits from steady customer additions in growing markets like Texas. The pipeline business capitalizes on Texas's unique intrastate market, where Atmos can earn attractive returns moving gas from production areas to consumption centers without federal oversight.

Capital allocation at Atmos follows a disciplined hierarchy. First priority: safety and reliability investments that go directly into the rate base. Capital expenditures were $2.9 billion; approximately 83% focused on safety and reliability. These investments are essentially risk-free—regulators approve them because they improve system safety, and they earn guaranteed returns for decades.

Second priority: the dividend. ATO has increased its dividend for 41 consecutive years. This isn't just about rewarding shareholders; it's about signaling stability to the rating agencies and regulators. A utility that can raise its dividend for four decades straight is a utility that regulators trust with rate increases.

The financing strategy is equally sophisticated. Atmos maintains an investment-grade credit rating, essential for accessing cheap capital in a capital-intensive business. The company targets a capital structure of roughly 50-55% equity, 45-50% debt—conservative enough to weather downturns, leveraged enough to juice returns.

But here's the real magic: infrastructure trackers and annual rate mechanisms. Instead of fighting massive rate cases every few years—expensive, contentious affairs that anger customers and politicians—Atmos has negotiated annual adjustment mechanisms in most of its jurisdictions. Spend a billion on pipe replacement? That goes into rates automatically next year. It's compound interest for infrastructure investment.

The regulatory relationships that enable this are carefully cultivated. Atmos doesn't maximize every rate case; they leave something on the table. They invest ahead of mandates, not in response to them. When regulators need a utility to pilot a new safety program or environmental initiative, Atmos volunteers. This regulatory goodwill is an intangible asset worth billions, though it appears nowhere on the balance sheet.

The numbers validate the strategy. The indicated annual dividend for fiscal 2025 is $3.48, which represents an 8.1% increase over fiscal 2024. The company has delivered 20 consecutive years of EPS growth. The stock trades at a premium to utility peers, which makes equity financing accretive and creates a virtuous cycle of growth.

Risk management is embedded in the model. Geographic diversification across eight states means no single regulatory decision can cripple the company. The focus on distribution and intrastate transmission avoids commodity price exposure. Long-term gas supply contracts match long-term customer commitments. Even weather risk is mitigated through weather normalization adjustments in rates.

The recent financial performance shows the model hitting on all cylinders. Revenue growth comes not from selling more gas—volumes are actually declining slightly due to efficiency—but from rate base growth. Operating margins expand as fixed costs are spread over a larger asset base. Return on equity consistently hits regulatory targets, justifying future rate increases.

This is financial engineering at its most elegant: turning the boring, regulated utility model into a growth machine that compounds capital at equity-like returns with bond-like risk. It's a model that works in boom times and recessions, in high interest rate environments and low ones, because people need heat in winter regardless of what the Fed does.

IX. Playbook: Lessons in Regulated Utility Excellence

If you wanted to build Atmos Energy from scratch today, you couldn't. Not because the opportunity doesn't exist—there are still thousands of subscale gas utilities across America—but because the conditions that allowed Atmos to consolidate the industry have fundamentally changed. The playbook they wrote, however, remains instructive for anyone trying to build enduring value in regulated industries.

Lesson 1: Consolidation in Fragmented Markets Creates Exponential Value

When Atmos began its acquisition spree in 1988, there were hundreds of small gas distribution companies across America, many family-owned, most subscale. Atmos understood that the regulatory model rewards scale: larger utilities can spread fixed costs, negotiate better with suppliers, and most importantly, have the balance sheet to fund massive capital programs that smaller utilities can't afford.

But successful consolidation requires more than just capital. Atmos developed a repeatable integration playbook: retain local management and relationships, centralize back-office functions, immediately begin infrastructure upgrades to build regulatory goodwill. They didn't try to squeeze synergies through layoffs; they created value through capital deployment.

Lesson 2: Regulatory Expertise Is the Ultimate Moat

In regulated industries, the customer isn't really the customer—the regulator is. Atmos understood this earlier and more deeply than competitors. They hired executives from regulatory commissions. They studied each state's unique regulatory philosophy and tailored their approach accordingly. In Texas, where growth and infrastructure investment are prized, they proposed aggressive expansion. In Kentucky, where affordability is paramount, they focused on efficiency.

This expertise compounds. Regulators trust utilities with good track records, creating a virtuous cycle where good relationships lead to favorable rate treatment, which enables more investment, which strengthens relationships further.

Lesson 3: Infrastructure Investment vs. Financial Engineering

While merchant power companies were leveraging up to juice returns in the 2000s, Atmos stuck to a simple formula: invest in pipes, earn regulated returns. No trading desks, no unregulated ventures, no complex derivatives. Just pipes in the ground earning 10% returns for decades.

This discipline seemed boring when competitors were promising 20% returns from merchant power. But when those competitors blew up in the 2008 financial crisis, Atmos kept investing, kept earning, kept compounding. Boring became beautiful.

Lesson 4: Geographic and Regulatory Diversification

Operating in eight states isn't efficient from an operational perspective, but it's brilliant from a risk management perspective. When Louisiana tightens regulations, Texas might loosen them. When Kentucky faces economic headwinds, Colorado booms. This diversification smooths earnings and provides options—if one state becomes inhospitable, capital can be redirected to friendlier jurisdictions.

Lesson 5: Pure-Play Focus

The temptation to diversify is constant in utilities. Why not add electricity distribution? Why not get into renewable energy? Why not upstream into production? Atmos resisted all of these. By staying pure-play natural gas distribution, they became the best at one thing rather than mediocre at many things. When pension funds want exposure to gas distribution, Atmos is the obvious choice.

Lesson 6: Long-Term Thinking in Capital Allocation

Atmos makes investment decisions on 40-year timelines, not quarterly earnings. A pipe replaced today will earn returns until 2065. This long-term orientation allows them to make investments that don't pay off immediately but compound tremendously over time. It also aligns perfectly with the regulatory model, where patient capital is rewarded with steady returns.

Lesson 7: Balance Sheet Management for Utilities

Utilities live and die by their credit ratings. One notch can mean tens of millions in additional interest expense. Atmos maintains deliberate balance sheet slack—they could leverage up and juice near-term returns, but that would limit their flexibility to respond to opportunities or crises. The discipline to stay investment-grade through all cycles is what enables long-term compounding.

Lesson 8: Culture as Competitive Advantage

In an industry where a single safety incident can destroy decades of goodwill, culture matters more than strategy. Atmos built a culture of safety and operational excellence that permeates from the CEO to field technicians. This isn't just about avoiding disasters; it's about thousands of small decisions made correctly every day that compound into superior performance.

The playbook seems simple in retrospect: buy subscale utilities, upgrade their infrastructure, earn regulated returns, repeat. But the execution required patience, discipline, and expertise that few management teams possess. It required saying no to exciting opportunities to say yes to boring but profitable ones. It required thinking in decades when Wall Street thinks in quarters.

Most importantly, it required understanding that in regulated utilities, you don't win by being the smartest or the most innovative. You win by being the most trusted, the most reliable, the most steady. In a world obsessed with disruption, Atmos built a fortune on continuity.

X. Analysis & Investment Case

The Bull Case: Essential Infrastructure in an Energy-Hungry World

The bullish thesis for Atmos Energy rests on a fundamental reality: natural gas isn't going anywhere. Despite the headlines about electrification and renewable energy, natural gas heats half of American homes and powers a third of our electricity. In Texas, Atmos's largest market, population growth and industrial expansion create insatiable energy demand that wind and solar alone cannot meet.

The regulatory framework provides downside protection that's rare in public markets. When Atmos spends $3 billion on infrastructure, they don't hope to earn a return—they're guaranteed one by law. This isn't venture capital; it's more like lending money to a government that can raise taxes to pay you back. The infrastructure tracker mechanisms in states like Texas mean investments flow into rates automatically, removing regulatory lag and political risk.

The company's positioning in the Texas intrastate market is particularly attractive. Texas has its own grid, its own gas market, and its own regulatory framework. As the state continues its remarkable growth trajectory—adding the population equivalent of a new San Francisco every year—Atmos's pipes become more valuable, not less. The transition from coal to gas in power generation, far from complete, provides another decade of demand growth.

Atmos Energy stock is attractive for investors looking for an above-average yield and regular dividend growth. Because of this, it can serve a valuable purpose in an income investor's portfolio. The stock offers a very secure and growing dividend income stream, and its dividend yield is well above the average dividend yield of the S&P 500 Index.

ESG concerns, counterintuitively, might actually benefit Atmos. As the cleanest fossil fuel, natural gas is increasingly seen as the essential transition fuel to a renewable future. Gas plants can ramp up when the wind doesn't blow and the sun doesn't shine. Modern gas infrastructure with minimal methane leakage is dramatically cleaner than the coal plants it replaces.

The Bear Case: Electrification and Stranded Assets

The bearish thesis starts with a simple observation: the world is electrifying, and electricity doesn't need gas pipes. Electric heat pumps are now more efficient than gas furnaces in most climates. Electric stoves are preferred by many chefs. Electric water heaters powered by solar panels are cheaper to operate than gas ones. Every Tesla sold is a car that will never need natural gas.

Cities from Berkeley to Boston are banning natural gas in new construction. The political winds have shifted decisively against fossil fuel infrastructure. Even if these bans are eventually overturned, they signal a broader societal shift away from combustion-based energy. For a company investing $3 billion annually in gas infrastructure with 40-year depreciation schedules, this creates massive stranded asset risk.

Climate change poses both physical and transition risks. Physical risks include extreme weather events that damage infrastructure and disrupt operations. Transition risks include carbon taxes, methane regulations, and the accelerating cost declines in renewable energy and battery storage. The fact that Atmos has performed well during the energy transition so far doesn't mean it will continue to do so as the pace accelerates.

Interest rate sensitivity is another concern. Based on expected earnings of $7.20 this year, the stock trades with a price-to-earnings ratio of 21.3x. This is above our fair value estimate of 19x earnings, and above the 10-year average price-to-earnings ratio for the stock. As a result, Atmos Energy shares appear to be overvalued. If the stock valuation compresses from 21.3 to 19 over the next five years, the corresponding multiple compression would decrease annual returns by 1.6%.

The capital intensity of the business model creates its own risks. Atmos needs constant access to capital markets to fund its growth. Any disruption—a credit crisis, a regulatory shock, a major safety incident—could force the company to cut its capital program, which would immediately impact earnings growth and potentially the dividend.

Valuation and Returns Analysis

At current prices around $150 per share, Atmos trades at approximately 22x forward earnings, a significant premium to both utility peers (typically 16-18x) and its own historical average. The dividend yield of 2.3% is below the utility average of 3-4%, suggesting the market is pricing in significant growth.

The math for forward returns is straightforward but sobering. If Atmos can grow earnings at 7% annually (the high end of guidance) and maintain its current multiple, total returns would be approximately 9.3% (7% growth + 2.3% dividend). However, if multiples compress to historical averages, returns could be closer to 5-6% annually.

The quality factors are undeniable: 41 consecutive years of dividend growth, predictable earnings, essential service, strong regulatory relationships. But quality is already reflected in the price. The question for investors is whether paying a premium for the best-in-class operator makes sense when cheaper alternatives exist.

The most likely scenario is neither explosive growth nor dramatic decline, but rather steady, high-single-digit returns for patient investors. For retirees seeking income and stability, Atmos offers both. For growth investors seeking the next doubling, they should look elsewhere. This is a tortoise stock in a market obsessed with hares—and that might be exactly what some portfolios need.

XI. Epilogue: The Future of Natural Gas Distribution

As we look toward 2030 and beyond, Atmos Energy faces a paradox: never has natural gas infrastructure been more essential to the American economy, and never has its long-term future been more uncertain. The company's response to this paradox will define not just its own trajectory, but potentially the entire natural gas distribution industry.

The hydrogen opportunity represents the most intriguing option. Natural gas pipelines can carry hydrogen blends up to 20% without significant modifications. Atmos has begun pilot programs injecting hydrogen into select distribution systems. If green hydrogen becomes economical—still a big if—Atmos's pipeline network could transport zero-carbon energy using existing infrastructure. It's a trillion-dollar option that costs almost nothing to maintain.

Renewable natural gas (RNG) from landfills, dairy farms, and waste treatment plants offers another avenue. While volumes will never match traditional natural gas, RNG commands premium prices and comes with valuable environmental attributes. Atmos has modified its pipeline specifications to accept RNG and is actively courting producers. Every molecule of RNG flowing through their pipes is a political and environmental win.

The data center boom presents an unexpected tailwind. AI computations require enormous amounts of reliable electricity, and natural gas generators provide the reliability that renewables cannot. Major tech companies are contracting directly for gas-fired power plants to support their data centers. Atmos's pipelines feed these generators, creating a new source of demand just as residential use faces pressure.

Fiscal 2025 earnings per diluted share guidance expected to be in the range of $7.35 - $7.45 per diluted share. Fiscal 2025 capital expenditure guidance expected to be approximately $3.7 billion. This guidance implies management's confidence in the near-term trajectory, but the longer-term questions remain.

If we were CEO, the strategy would be clear: maximize cash generation from existing assets while building optionality for multiple futures. Continue the infrastructure replacement program—safer pipes are valuable in any scenario. Invest in hydrogen and RNG capabilities, but don't bet the company on them. Most importantly, strengthen the balance sheet to ensure survival through any transition.

The greatest risk isn't electrification or regulation—it's complacency. The natural gas distribution industry has operated largely unchanged for a century. The next decade will bring more change than the previous five combined. Companies that adapt will thrive; those that don't will become stranded assets themselves.

Atmos Energy's story, from its humble beginnings in the Texas Panhandle to its position as America's largest pure-play natural gas distributor, is ultimately a story about the power of compound growth in boring industries. It's a reminder that in business, as in life, tortoise strategies can beat hare strategies if executed with patience and discipline.

The company has survived the transition from manufactured gas to natural gas, the deregulation of the 1980s, the shale revolution of the 2000s, and the energy transition of the 2010s. Each challenge was met not with revolutionary change but with steady adaptation, infrastructure investment, and regulatory partnership.

As America grapples with its energy future—balancing reliability, affordability, and environmental concerns—companies like Atmos will play a crucial but often invisible role. The pipes under our streets and the storage caverns beneath our feet represent more than just infrastructure; they represent the physical manifestation of our energy choices as a society.

Whether natural gas is a bridge fuel to a renewable future or a permanent part of our energy mix remains to be seen. What's certain is that for the foreseeable future, millions of Americans will turn on their furnaces on cold winter nights, and natural gas will flow through Atmos Energy's pipes to keep them warm. In that simple transaction, repeated millions of times, lies a business model that has created enormous value for over a century—and may well continue for another.

The question for investors isn't whether Atmos Energy will exist in 20 years—it almost certainly will. The question is whether it will thrive or merely survive, whether it will compound wealth or preserve it, whether it will lead the energy transition or be dragged along by it. These are questions without easy answers, but they're the right questions to ask about a company that has made a fortune by moving invisible molecules through buried pipes, earning a regulated return on every mile.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube