Atkore: The Hidden Champion of Electrical Infrastructure

The Invisible Conduit That Powers America

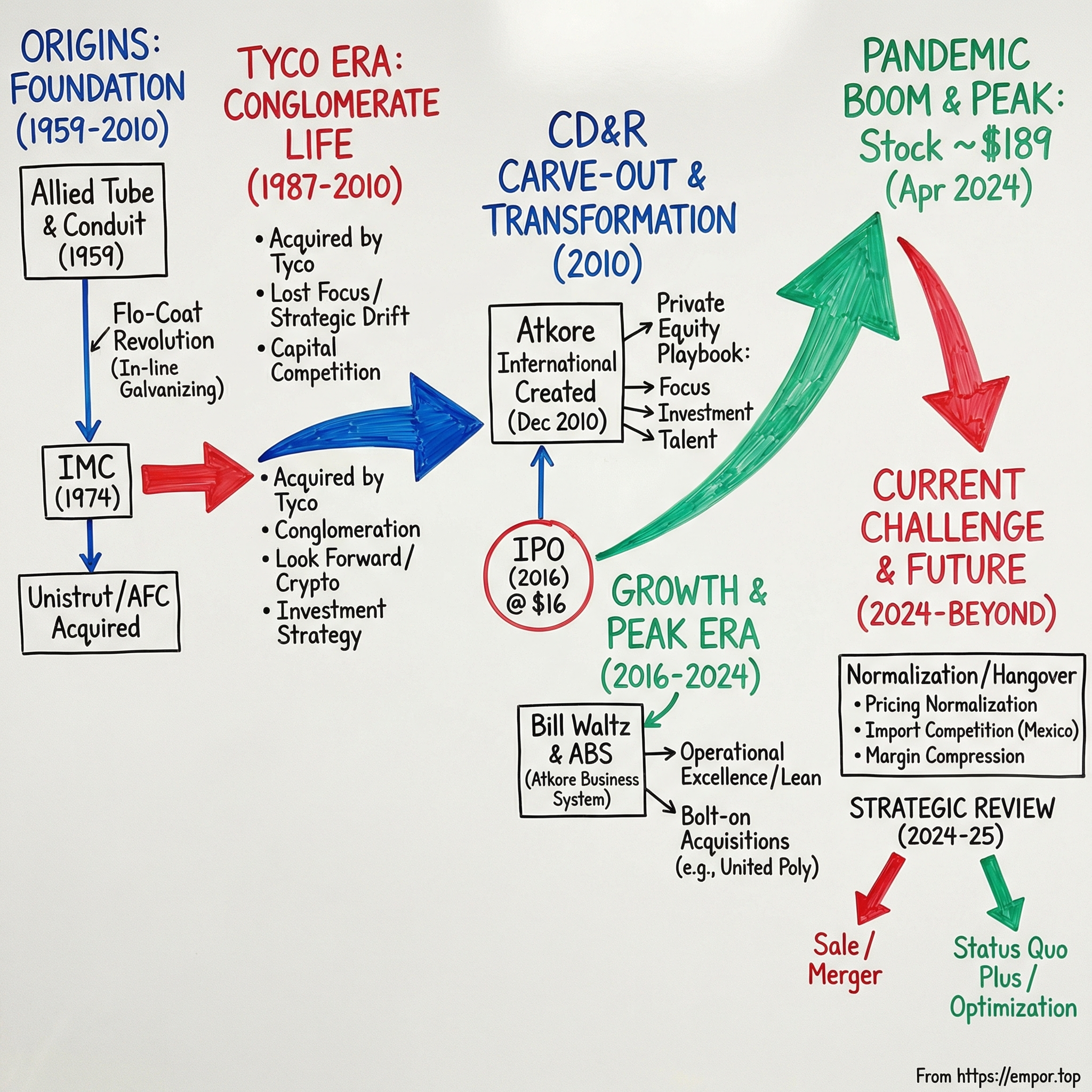

Picture the scene: It's December 2010, and somewhere in the labyrinthine offices of Clayton, Dubilier & Rice in Manhattan, a team of private equity veterans is finalizing the paperwork for an acquisition that few outside the industrial world will ever notice. The target: Tyco International's Electrical & Metal Products division—a collection of factories in Illinois, Indiana, and beyond, churning out steel tubes, armored cables, and metal framing systems. The price tag: roughly $720 million. The plan: carve out a neglected conglomerate division and transform it into a focused, operationally excellent market leader.

That transaction marked the birth of Atkore International.

Fast forward to April 2024, and the all-time high Atkore stock closing price was $189.01—more than ten times the $16 IPO price from June 2016. For investors who spotted this "boring" industrial play early, Atkore became one of the great multi-bagger opportunities of the post-financial crisis era. But as of late 2025, the company finds itself at another inflection point: Atkore's Board of Directors has expanded the scope of its strategic alternatives review to consider a potential sale or merger of the whole company.

How did a manufacturer of steel tubes and electrical conduit—products most people never see and couldn't identify—become a case study in private equity value creation, operational excellence, and infrastructure investing? And what does the current strategic review signal about Atkore's future?

This is the story of the invisible infrastructure that powers every building, factory, and data center in America—and the company that built an empire making it.

I. Origins: Allied Tube & Conduit and the Flo-Coat Revolution (1959–1987)

A Revolution in Rust Prevention

The story of Atkore begins not in a corporate boardroom but on the factory floor in Harvey, Illinois, in 1959. Allied Tube & Conduit was incorporated in Blue Island, IL, introducing Flo-Coat, the first patented "in-line" tube galvanization process. In 1960, the company began operations with 10 employees and one tube mill.

To appreciate what Allied's founders accomplished, you need to understand a fundamental problem in the steel tube industry. Before Flo-Coat, protecting steel pipes from corrosion required either "hot-dipping" them in molten zinc after manufacturing (an expensive, batch process) or using "pre-galvanized" steel (which offered inferior protection at weld points). Allied's innovation was elegantly simple but technically demanding: Flo-Coat is "the original in-line galvanized product." Developed in 1959 when Allied Tube & Conduit first created a technique to run welded tubing through molten zinc on the line. Flo-Coat features advanced levels of corrosion protection, higher strength through cold forming and is capable of being painted or powder coated.

The genius of in-line galvanizing was threefold. First, it was faster—coating happened as part of the manufacturing process, not as a separate step. Second, it was more consistent—the zinc coating applied uniformly across the entire tube surface. Third, and most importantly for competitive positioning, it created a better product: The signature Flo-Coat galvanizing process produces superior corrosion resistance by utilizing a triple-layer of protection. First 99.99% pure zinc is applied, followed by a conversion coating. Finishing the process is a clear organic topcoat that seals in the protection and produces a smooth shiny appearance.

Building the Foundation

The early years followed the classic trajectory of an industrial innovator gaining market acceptance. By 1965, Allied's ranks swelled to 100 employees. They relocated to a 110,000 sq ft facility in Harvey, IL. In 1974, they pioneered IMC, the first light-weight alternative to rigid conduit.

This 1974 innovation—Intermediate Metallic Conduit (IMC)—deserves attention because it illustrates Allied's approach to the market. Rigid conduit, the industry standard for heavy-duty applications, was expensive and labor-intensive to install. Allied's IMC offered comparable protection at roughly 30% less weight, reducing material costs and making installation easier. The product wasn't revolutionary in the way Flo-Coat was, but it showed a company focused on solving customer problems rather than merely manufacturing commodities.

In 1985, Allied's channel framing line grew with the purchase of Power-Strut. The company launched Kwik-Couple®, a time-saving conduit coupling product. These moves expanded Allied beyond electrical conduit into the broader "metal framing and support systems" market—the Unistrut-style products that contractors use to mount electrical and mechanical systems in commercial buildings.

Why Electrical Conduit Matters

Before we proceed further into Atkore's corporate evolution, it's worth pausing to understand what electrical conduit actually does and why it matters.

Electrical Raceway products form the critical infrastructure that enables the deployment, isolation and protection of a structure's electrical circuitry from the original power source to the final outlet.

In practical terms, every commercial building, industrial facility, data center, hospital, and piece of critical infrastructure in America requires electrical conduit. Building codes mandate it. Contractors can't skip it. When you flip a light switch in an office building, the wires carrying that electricity are routed through metal or plastic conduits running behind walls, above ceilings, and under floors. The conduit protects the wires from physical damage, provides a ground path for electrical safety, and enables maintenance and upgrades.

This is the "invisible infrastructure" thesis that makes companies like Atkore interesting to investors. Demand is non-discretionary (you can't build a building without conduit), switching costs are moderate (contractors and distributors develop relationships and familiarity with specific brands), and the products are genuinely essential rather than merely convenient.

The challenge, of course, is that essential and non-discretionary doesn't mean profitable or differentiated. Steel tubes are steel tubes, and the electrical conduit market has always been competitive, cyclical, and subject to commodity pricing pressures. Allied's innovation advantage—the Flo-Coat process—was significant but not impregnable. The company would need scale, distribution relationships, and operational excellence to maintain market leadership.

II. The Tyco Era: Conglomerate Life (1987–2010)

Swallowed by the Roll-Up Machine

In 1987, Tyco Laboratories Inc. acquired Allied Tube & Conduit. It later became Tyco International with U.S. headquarters in Princeton, N.J.

This acquisition placed Allied within one of the most aggressive corporate acquirers of the late 20th century. Following aggressive acquisition periods through the 1970s, Tyco management focused the early 1980s on organizing its newly acquired subsidiaries. Tyco divided the company into three business segments, Fire Protection, Electronics, and Packaging. Once organized, Tyco returned to the strategy of growth by acquisition in the later part of the decade acquiring Grinnell Corporation, Allied Tube and Conduit, and the Mueller Company.

Under Tyco, the electrical and metal products business expanded through additional acquisitions. In 1987, Allied was acquired by Tyco. In 1995, Tyco acquired Unistrut (US Division), expanding the metal framing line. In 1996, they acquired TJ Cope, a manufacturer of cable tray systems. In 1997, the fire protection and construction line grew with the purchase of American Pipe & Tube. In 1999, they acquired AFC Cable Systems and entered the Canadian market with the acquisition of Columbia-MBF.

These acquisitions assembled what would become Atkore's core brand portfolio. Unistrut—acquired in 1995—was and remains the dominant brand in metal framing systems, the steel channels and fittings that contractors use to mount everything from HVAC ducts to electrical panels. AFC Cable Systems—acquired in 1999—brought armored cable and metal-clad cable products, which represent the "pre-wired" alternative to traditional conduit-and-wire installations.

The Dennis Kozlowski Years

To understand why Atkore would eventually need to be carved out of Tyco, you need to understand what happened to Tyco under Dennis Kozlowski. Tyco grew tremendously in the 1990s and early 2000s, with revenues increasing from $3.07 billion in 1992 to $34.04 billion in 2001; an aggressive program of acquisition during this period saw the company spend an estimated $62 billion to purchase more than 1,000 companies. But the engineer of this ascent, L. Dennis Kozlowski, resigned in June 2002 under a cloud, and he and Mark H. Swartz (former Tyco CFO) later faced criminal charges for allegedly stealing $600 million from the company and its shareholders.

The Kozlowski scandal devastated Tyco's reputation and forced a fundamental rethinking of its conglomerate strategy. Under new CEO Ed Breen, Tyco began divesting non-core businesses to focus on fire protection and security—areas where it had genuine market leadership.

The Challenges of Conglomerate Life

For the Electrical & Metal Products division, life inside Tyco presented the classic challenges of being a non-core asset within a sprawling conglomerate:

Capital Allocation Competition: When Tyco was acquiring healthcare companies for billions of dollars, the electrical conduit business—essential and profitable though it was—received limited investment attention.

Management Distraction: Tyco's corporate governance crises consumed leadership bandwidth throughout the early 2000s, leaving operating divisions to manage themselves through a turbulent period.

Strategic Drift: Without focused ownership, the electrical and metal products portfolio accumulated some businesses that made sense strategically and others that had simply been acquired because they were available.

By 2010, the electrical and metal products division was generating approximately $1.4 billion in annual revenue with leading North American market positions in electrical conduit, marketed under the Allied brand, metal clad cable, marketed under the AFC brand, as well as strut and support systems marketed under the Unistrut and Power-Strut brands. In addition to electrical products, the mechanical tube, sprinkler pipe and fence product lines also held strong market positions.

It was a solid business—but one that needed focus, investment, and operational transformation to reach its potential.

III. The CD&R Carve-Out: Private Equity Transformation (2010)

The Deal That Created Atkore

On November 9, 2010, Clayton, Dubilier & Rice, LLC announced a definitive agreement to acquire a 51% ownership stake in Tyco International's Electrical and Metal Products business. The transaction in which a CD&R-managed fund invested $306 million equity was valued at approximately $1 billion.

On December 22, 2010, Tyco International completed the sale of a 51% stake in its Electrical and Metal Products business to the private equity firm Clayton, Dubilier & Rice, LLC. Under terms of the transaction, Tyco received total cash proceeds of approximately $720 million. The Electrical and Metal Products business began operating as a standalone entity under the name Atkore International. The business designs, manufactures and sells galvanized steel tubes and pipes, electrical conduit, armored wire and cable, metal framing systems and building components. The business generated 2010 revenue of $1.4 billion.

The name "Atkore" itself tells a story about the company's positioning. "When the business became public, it was ATCOR, which was traded on the NASDAQ. When we separated from Tyco, we needed a name that represented the global corporation we are today, yet was universal enough to account for future expansion. The name Atkore primarily emphasizes that the products we manufacture are core to our customers. There's a nod back to the fact that Allied represents the largest part of the portfolio. AT can be seen as a nod to Allied Tube and the past history of how the company has grown."

Why CD&R?

Clayton, Dubilier & Rice was not a random private equity buyer. The firm had a specific playbook for industrial carve-outs and a track record of transforming overlooked divisions into standalone market leaders. Clayton, Dubilier & Rice, LLC is an American private equity company. CD&R is the 24th oldest private equity firm in the world. It has $30 billion invested in approximately 90 businesses.

CD&R's most famous carve-out success was Lexmark, which CD&R formed from IBM's printer and keyboard manufacturing business in 1990. The deal was named one of the 30 Most Influential Private Equity Deals by Private Equity International in 2004.

The Atkore transaction fit CD&R's pattern: take a business with good market positions but unfocused operations, provide capital and management attention, implement operational excellence programs, and either sell or IPO once the transformation is complete.

The Private Equity Transformation Playbook

The company's trajectory was fundamentally reshaped by two key events and one core operational philosophy. These moves were less about incremental change and more about strategic re-platforming. The 2010 Spin-Off: Being acquired by CD&R for $720 million was the catalyst.

What made the CD&R ownership transformational?

Focus: For the first time since 1987, the electrical and metal products business had owners whose sole focus was making that business succeed. Every dollar of profit, every capital expenditure decision, every strategic choice was made in service of Atkore's growth—not balanced against the competing priorities of a sprawling conglomerate.

Investment: CD&R brought not just capital but a willingness to invest in the business for long-term value creation. This meant upgrading manufacturing facilities, investing in lean manufacturing capabilities, and building the infrastructure for future acquisitions.

Management Talent: Private equity firms like CD&R bring executive networks and operational expertise. The Atkore transformation would ultimately require bringing in new leadership, including the CEO who would lead the company through its most successful years.

Portfolio Optimization: Almost immediately, Atkore began rationalizing its portfolio. In 2013, Atkore strengthened its position in the PVC market by expanding its offering of electrical conduit, fittings, elbows, irrigation pressure and plumbing & sewer pipe with the acquisitions of Heritage Plastics, Liberty Plastics and Ridgeline Manufacturing. As Atkore continued to build its Electrical Raceway portfolio, it divested a non-core business in Brazil and closed its factory in France.

In 2014, Atkore repurchased Tyco International's remaining stock in the company. Atkore continued its focus on delivering value-added solutions for electrical raceway customers with the acquisition of American Pipe & Plastics, a manufacturer of PVC conduit serving the telecommunications, power, cable TV and fiber optic infrastructure markets.

By 2014, Atkore had bought out Tyco's remaining stake, acquired complementary PVC conduit businesses, divested non-core assets, and established the foundation for the next phase of growth.

IV. The IPO and Public Market Journey (2016–Present)

A Rocky Debut

Atkore's common stock is listed on the New York Stock Exchange (NYSE) under ticker "ATKR." Atkore priced its IPO on Thursday, June 9, 2016 and began trading on the NYSE on Friday, June 10, 2016.

The IPO did not go smoothly. Atkore had originally targeted a price range of $20 to $22 per share, but investor reception was tepid. The market in 2016 was skeptical of industrial companies tied to construction cycles, wary of commodity exposure in steel and PVC, and generally unexcited about "boring" infrastructure plays.

The resulting IPO raised $192 million at $16 per share—well below expectations. For CD&R, which still held a significant stake, this was disappointing. But for long-term investors, the discounted IPO price would prove to be a gift.

The 2016 IPO: Going public was the capital-unlocking moment. It provided the necessary liquidity and currency to execute the bolt-on acquisition strategy that has defined their growth over the last decade.

The Bill Waltz Era

The transformation of Atkore from a competent industrial company into a genuine value-creation story accelerated with the leadership of Bill Waltz. "I have been part of Atkore's leadership team for 12 years, including seven as CEO. Leading Atkore truly has been the honor and privilege of my 40-year business career."

Waltz's background prepared him perfectly for Atkore's challenges. Previously, he spent 15 years in various divisions of Pentair plc, including President-Pentair Flow Technologies. Mr. Waltz began his career at General Electric Company and as a Deloitte Management consultant.

The GE and Pentair pedigree meant Waltz understood both lean manufacturing principles and the operational discipline required to drive consistent improvement in industrial businesses. Under his leadership, Atkore would institutionalize these principles through the Atkore Business System.

The Atkore Business System (ABS)

The Atkore Business System (ABS) is the operational backbone—a lean manufacturing and continuous improvement methodology. It drives efficiency across their approximately 65 manufacturing and distribution facilities.

Through three fundamentals (People, Strategy, Process), ABS focuses on developing our people, advancing a market-driven strategy, and continually improving all that we do. The People fundamental is reflective of who we are and how we drive organizational excellence. With a holistic approach, the Atkore Business System is key to our success, and we consider it a differentiator amongst employers when considering a career.

The ABS framework borrowed from the Danaher Business System—one of the most successful operational excellence frameworks in industrial history. The core of their efficiency is the Atkore Business System (ABS), a continuous improvement framework borrowed from the Danaher playbook.

Key elements of ABS include:

- Lean Daily Management (LDM): Managing day-to-day operations with structured processes, visual management, and problem-solving routines

- Strategy Deployment Process (SDP): Aligning the entire organization around breakthrough objectives and cascading goals

- Kaizen Events: Focused improvement workshops targeting specific processes or problems

- Standard Work: Documenting and continuously improving the best-known methods for every process

The results were dramatic. From the 2016 IPO through fiscal 2023, Atkore's revenue nearly doubled while margins expanded significantly. The company went from a competent industrial manufacturer to one of the best-performing stocks in its sector.

The Acquisition Machine

Waltz and his team deployed capital aggressively through bolt-on acquisitions. The strategy focused on strengthening core product categories, expanding geographic reach, and building capabilities in growing end markets.

In November 2022, Atkore announced the acquisition of the assets of Elite Polymer Solutions, a manufacturer of High Density Polyethylene (HDPE) conduit, primarily serving telecommunications, utility, and transportation markets for a purchase price of $91.6 million. "The acquisition of Elite Polymer Solutions strengthens our HDPE conduit product portfolio, expands our national presence and enables us to better serve increased demand for underground protection in the electrical, utility and telecom industries."

Atkore acquired United Poly Systems, a manufacturer of High Density Polyethylene (HDPE) pressure pipe and conduit, primarily serving telecom, water infrastructure, renewables, and energy markets. "We are pleased to complete the acquisition of United Poly Systems, which strengthens Atkore's product portfolio, expands our manufacturing capacity and further enables us to meet HDPE customers' needs. HDPE pipe and conduit is a growing market that is expected to benefit from U.S. infrastructure legislation." Bill Waltz added, "The acquisition of United Poly Systems advances our objective announced in November 2021 to deploy more than $1 billion in cash toward capital expenditures and other organic investments, M&A and stock repurchases over the next two to three years."

With the latest two deals, Atkore deployed more than $310 million to complete six acquisitions in fiscal year 2022.

The Pandemic Boom

Like many industrial companies, Atkore experienced extraordinary conditions during the COVID-19 pandemic and its aftermath. Supply chain disruptions, combined with massive fiscal stimulus and infrastructure investment, created a perfect storm for pricing power.

The company's revenue exploded from approximately $1.8 billion to a peak of roughly $3.5 billion. More importantly, margins expanded dramatically as Atkore was able to pass through material cost increases and capture additional pricing in a tight supply environment.

The all-time high Atkore stock closing price was $189.01 on April 01, 2024—representing more than an 11x return from the IPO price in less than eight years.

V. Product Portfolio: What Atkore Actually Makes

Understanding the Business Segments

Atkore Inc. engages in the manufacture and sale of electrical, mechanical, safety, and infrastructure products and solutions in the United States and internationally. It operates through two segments, Electrical, and Safety & Infrastructure. The company offers metal electrical conduit and fittings; plastic pipe conduit and fittings; electrical cable and flexible conduit; and international cable management systems; and mechanical tubes and pipes, metal framing and fittings, construction services, perimeter security, and cable management for the protection and reliability of critical infrastructure.

Electrical Segment (~70% of revenue): This is the core business, encompassing everything that protects and routes electrical wiring in buildings:

- Metal Conduit: Steel tubes in various configurations (EMT, IMC, rigid) with the proprietary Flo-Coat galvanizing

- PVC Conduit: Plastic alternatives to metal conduit for specific applications

- Armored Cable: Pre-wired solutions (AC and MC cable) that combine wire and protective sheathing

- Cable Tray and Fittings: Open raceways for routing cables in industrial and commercial applications

Safety & Infrastructure Segment (~30% of revenue): Supporting products and adjacent businesses:

- Metal Framing (Unistrut, Power-Strut): Channel systems for mounting electrical and mechanical equipment

- Mechanical Tubing: Steel tubes for non-electrical applications

- Perimeter Security: Bollards and barriers (Calpipe Security)

- Construction Services: Prefabrication and installation services

Brand Portfolio Strength

Atkore offers its products under the Allied Tube & Conduit, AFC Cable Systems, Kaf-Tech, Heritage Plastics, Unistrut, Power-Strut, Cope, US Tray, FRE Composites, Calbond, and Calpipe brands.

The brand portfolio represents decades of accumulated market position and contractor familiarity. Allied Tube & Conduit remains the flagship brand for metal conduit, while Unistrut dominates the metal framing category. AFC Cable Systems is a leader in armored cable. These aren't consumer brands with advertising-driven awareness, but they carry enormous weight with electrical contractors and distributors who specify and purchase these products.

End Markets Served

Atkore serves a group of end markets, including new construction; maintenance, repair, and remodel, as well as infrastructure, diversified industrials, alternative power generation, healthcare, data centers, and government through electrical, industrial, and specialty distributors, as well as original equipment manufacturers.

The end market exposure is diverse but heavily weighted toward non-residential construction:

- Commercial Construction: Office buildings, retail, hospitality

- Industrial: Manufacturing facilities, warehouses, logistics centers

- Data Centers: A growing and increasingly important end market

- Healthcare: Hospitals and medical facilities

- Infrastructure: Power generation, utilities, transportation

- Government: Federal, state, and local facilities

VI. The Current Challenge: Normalization and Strategic Uncertainty (2024–2025)

The Post-Pandemic Hangover

The extraordinary conditions that drove Atkore's pandemic-era performance have reversed. For the full fiscal year 2025, Atkore reported net sales of $2.85 billion, down 11% from $3.2 billion in FY 2024. Net income swung to a loss of $15 million compared to a profit of $473 million in the previous year, while adjusted EBITDA fell 50% to $386 million.

The decline reflects several factors:

Pricing Normalization: The decrease was primarily due to lower average selling prices of $53.6 million as the result of expected pricing normalization. The extraordinary pricing power of the pandemic era has evaporated as supply chains normalized and competition intensified.

Import Competition: ATKR delivered worse-than-expected Q3 2024 results and lowered 2024 EBITDA guidance by -11% due to higher amounts of imported steel conduit entering the market and a slower summer construction season.

In recent years, Mexican steel producers have built numerous mills equipped to produce conduit, with their eye on the U.S. market. In October 2022, Zekelman Industries announced the closure of its Long Beach, California plant, with the loss of 150 jobs, due mainly to Mexican imports of steel conduit reducing the market for Zekelman's products.

The import pressure from Mexico has become a significant industry issue. According to Zekelman's President of Electrical Products Jim Hays, Mexican producers are persistently pricing their products at 25% below the prevailing prices in the U.S. market. The result has been huge growth in U.S. imports of Mexican conduit. Figures from import reporting services show that after rising steadily in 2021, 2022, and 2023, Mexican conduit imports in the last two months of 2023, if annualized, were running at some 760% above the historic levels of 2015-2017.

Construction Cycle Softness: Non-residential construction has slowed as interest rates rose and economic uncertainty increased.

Margin Compression

Gross profit was $147.8 million in Q4 2025, down roughly $68.2 million from about $216.1 million in the prior-year quarter, a decline of around 31.6%. Gross margin fell to about 19.7% from 27.4% a year earlier, reflecting substantial margin compression driven by the combination of lower average selling price and high material costs.

Strategic Review and Activist Involvement

As part of this expanded review, the Board and management team will consider a broader range of alternatives to maximize shareholder value, including, among other things, a potential sale or merger of the whole company. Atkore also announced it will appoint Franklin Edmonds to its Board of Directors as part of a cooperation agreement with Irenic Capital Management LP.

Most notably, the company has expanded its strategic alternatives review to include the potential sale or merger of the entire business. Atkore is also sharpening its focus on electrical end markets through the divestiture of non-core businesses, having already divested Northwest Polymers in February 2025 and currently exploring the sale of its High-density polyethylene (HDPE) business.

The CEO succession adds another layer of uncertainty. Earlier today, Bill Waltz indicated his decision to retire from Atkore having recently informed the Board. He is focused on a seamless transition and plans to lead Atkore in his current roles until a successor is appointed. However, given the expanded strategic review, Waltz has decided to stay on as CEO through at least the conclusion of the strategic review.

Cost Reduction Initiatives

The company expects to see about $10 to $12 million in annualized cost reductions from the closure of three plants. These actions, along with other initiatives, are expected to contribute to improved financial performance in 2027.

Atkore has undertaken a review of select assets that may not fit the Company's core electrical infrastructure portfolio, including the potential sale of its HDPE pipe and conduit business, which primarily serves the telecommunications market. The Company is also taking steps to reduce costs, including a recent reduction in headcount and the identification of three manufacturing facilities that will be consolidated in calendar year 2026. Earlier this year, Atkore announced the divestiture of its Northwest Polymers business.

VII. Competitive Analysis: Porter's Five Forces

Threat of New Entrants: LOW

Building a competitive electrical conduit business requires substantial capital investment in specialized manufacturing equipment, decades of process optimization, and established relationships with electrical distributors. Flo-Coat tube galvanized steel is manufactured using the advanced processing technique of in-line galvanizing first introduced by Allied in 1959. Over the years the Flo-Coat steel tubing product has benefited from continuous advances in technologies and processes.

The barrier isn't any single factor but the combination of: - Capital intensity of manufacturing facilities - UL certifications and building code compliance requirements - Established distributor relationships (distributors prefer stocking known brands) - Scale advantages in commodity purchasing (steel, zinc, PVC resin) - 60+ years of accumulated manufacturing know-how

Bargaining Power of Suppliers: MODERATE

Raw materials like steel and resin account for roughly 65% of Cost of Goods Sold. Atkore's primary inputs—hot-rolled steel coil, zinc, and PVC resin—are commodity materials with multiple sourcing options. The company's scale provides meaningful purchasing power, but it cannot escape commodity price volatility.

The company has pursued some vertical integration (particularly in plastics recycling through the Northwest Polymers acquisition, though that was later divested) to mitigate supplier power.

Bargaining Power of Buyers: MODERATE-HIGH

Atkore sells primarily through electrical distributors—companies like Graybar, Wesco, and Rexel—who aggregate products from multiple manufacturers and sell to electrical contractors. This creates a concentrated distribution channel with significant pricing visibility and leverage.

The 'one-stop shop' approach—offering a complete system of conduits, fittings, and metal framing—simplifies procurement for distributors and contractors, creating high switching costs once they are designed into a project.

However, stakeholders highlighted declines in PVC and steel conduit pricing due to imports and competition. When alternative sources (particularly imports) are available at competitive prices, buyer power increases.

Threat of Substitutes: LOW

Electrical conduit is mandated by building codes—there is no substitute for protecting and routing electrical wiring in commercial and industrial buildings. The only substitution occurs within the category: metal vs. plastic conduit, rigid vs. flexible conduit, traditional conduit vs. armored cable.

Atkore addresses this by offering products across all categories, so substitution within conduit types benefits the company rather than threatening it.

Competitive Rivalry: HIGH

The top players in the market are Atkore International Inc., Legrand, and ABB, Cantex Inc. The electrical conduit and cable management market includes several well-capitalized competitors, and products are fundamentally commoditized.

The increasing import of steel conduit from Mexico and sector softness are impacting Atkore's market competitiveness and demand for its products.

Competition intensifies during cyclical downturns when capacity exceeds demand, leading to price-based competition that pressures margins across the industry.

VIII. Hamilton's 7 Powers Framework Analysis

Scale Economies: STRONG

Atkore holds a #1 or #2 market position by net sales in the vast majority of its product categories in the United States, giving them an oligopolistic advantage in pricing and scale. Their national presence and large distribution network create economies of scale, significantly reducing the transportation costs for their heavy, low-cost products, which makes competition from smaller or international players less viable.

With 49 manufacturing and distribution facilities across North America, Atkore can serve customers nationally with reasonable freight costs—a significant advantage for heavy, low-value products where transportation is a meaningful portion of delivered cost.

Network Effects: WEAK

Physical products don't create network effects in the traditional sense. However, the breadth of Atkore's product portfolio creates some "ecosystem" value—a distributor who stocks Allied conduit naturally considers AFC Cable and Unistrut framing, reducing the friction of dealing with multiple suppliers.

Counter-Positioning: MODERATE

The Atkore Business System represents operational discipline that larger, more diversified competitors struggle to replicate. Atkore's culture is created from the disciplined use of the Atkore Business System (ABS), which is a critical part of our mission and a foundational system based on excellence in People, Strategy, and Processes, tied together with Lean Daily Management.

The counter-positioning is more evident against conglomerate competitors (like ABB or Schneider Electric) whose electrical products divisions are small parts of much larger enterprises with different strategic priorities.

Switching Costs: MODERATE

Product standardization limits switching costs for commodity conduit—a contractor can use any UL-listed EMT conduit and meet code requirements. However, comprehensive solutions (design assistance, prefabrication services, complete product lines) create meaningful stickiness with distributors and specifying engineers.

Contractor familiarity with specific brands also creates soft switching costs—electricians who've used Allied conduit for years develop intuitive familiarity with product characteristics that reduces installation time.

Branding: MODERATE

Allied Tube & Conduit is reputable within the industry for its premier manufacturing capabilities and long-standing commitment to innovation and quality. By maintaining a robust product portfolio coupled with innovative solutions, Allied Tube & Conduit continues to be a vital contributor to infrastructure and construction projects globally.

These aren't consumer brands, but they carry substantial weight with the contractors and distributors who make purchasing decisions. Decades of reliability and code compliance build trust that influences specification and purchasing.

Cornered Resource: WEAK

Atkore has no proprietary natural resources or exclusive intellectual property. The Flo-Coat galvanizing process, while superior, is no longer truly proprietary—competitors have developed similar in-line galvanizing capabilities over the decades.

Process Power: STRONG

"I'm proud of our company's achievements to date, including expanding our capabilities to capture opportunities from global megatrends and instilling a culture of discipline and excellence by leveraging the Atkore Business System."

The Atkore Business System represents embedded operational excellence that's difficult to replicate. It's not a single process or technique but a comprehensive operating system that drives continuous improvement across every function. This process power shows up in manufacturing efficiency, quality consistency, and the ability to integrate acquisitions quickly.

Overall Assessment

Atkore's competitive moat is best characterized as "moderate"—built primarily on Scale Economies and Process Power, with supporting contributions from Branding and Switching Costs. This is a "low-moat but well-operated" business that benefits from market leadership in essential products but faces genuine competitive pressure from imports and price-based competition during downturns.

IX. Growth Vectors and the Investment Thesis

The Electrification Megatrend

The company is positioned to benefit directly from secular growth trends like data center construction, solar energy adoption, and broader infrastructure spending on electrification, which drives demand for their core products.

The fundamental investment thesis for Atkore centers on the "electrification supercycle"—the multi-decade trend of increasing electricity consumption driven by:

- Data Centers: Artificial intelligence, cloud computing, and digital transformation are driving massive investments in data center capacity

- Grid Modernization: Aging electrical infrastructure requires replacement and upgrading

- Renewable Energy: Solar and wind installations require extensive electrical infrastructure

- EV Charging: The buildout of electric vehicle charging networks creates new demand for conduit and cable management

- Reshoring: Manufacturing returning to the United States drives industrial construction

Strong growth is projected in several construction markets for FY 2026, including data centers, healthcare, power utilities, and education.

Tariff and Trade Policy Tailwinds

Outgoing CEO William Waltz stressed that the 25% tariff on steel imports (post-exemption removal) was a tailwind for regaining market share, improving gross margins over time, and boosting demand for domestic products like Atkore's, though short-term volatility persists.

Tariff policies and onshoring trends are reducing foreign competition and boosting demand for Atkore's domestically-produced conduit and cable management systems.

The trade policy environment has become more favorable for domestic manufacturers. Recent legal victories limiting Mexican conduit imports in certain markets, combined with potential tariff actions, could reduce competitive pressure and support pricing.

Fiscal 2026 Outlook

Full-year 2026 Net sales expected to be in the range of $3.0 - $3.1 billion. Full-year 2026 Adjusted EBITDA outlook of $340 - $360 million; Full-year Adjusted net income per diluted share outlook of $5.05 - $5.55.

Management's guidance suggests stabilization rather than recovery—revenue essentially flat with fiscal 2025 and EBITDA margins remaining compressed relative to pandemic-era peaks.

X. The Strategic Review: What Happens Next?

The Range of Outcomes

"It's early in the process, but we're exploring a full range of strategic alternatives, from selling the entire company to continuing operations as is. The board is focused on pursuing the best outcome for shareholders."

The strategic alternatives under consideration include:

Full Company Sale: A private equity buyer or strategic acquirer could take Atkore private or merge it with another industrial company. Given the current stock price discount to peak levels, this represents a potential arbitrage opportunity for acquirers.

Asset Divestitures: The company is already pursuing sales of non-core assets like the HDPE business and mechanical tubing. A more aggressive portfolio rationalization could enhance focus on core electrical infrastructure.

Status Quo Plus: Continue operating independently with cost reduction initiatives and wait for market conditions to improve.

Potential Acquirers

Private equity firms with industrial expertise—including CD&R itself, which knows the business intimately—could be logical buyers. Strategic acquirers might include larger electrical equipment companies seeking to add conduit and cable management capabilities.

Activist Influence

On November 21, 2025, Atkore Inc. announced it had reached a cooperation agreement with Irenic Capital Management, resulting in board expansion, the appointment of Franklin S. Edmonds as director, and the formation of a Strategic Review Committee exploring alternatives such as a sale or merger. This agreement highlights growing activist investor influence at Atkore and signals the company may pursue transformative actions to unlock shareholder value.

The activist involvement adds urgency to the strategic review process. Irenic Capital has pushed for a comprehensive evaluation of alternatives, and the expanded board presence suggests they will have meaningful input into whatever path the company chooses.

XI. Key Performance Indicators for Investors

For investors monitoring Atkore's ongoing performance, three metrics matter most:

1. Organic Volume Growth

Volume growth is the purest indicator of underlying demand and market share. Pricing can be influenced by commodity costs and competitive dynamics, but volume growth reflects whether Atkore is winning or losing in the market.

The company has achieved organic volume growth for three consecutive years, with particular strength in plastic pipe, conduit, and fittings, which grew at low single-digit rates in FY 2025.

Positive organic volume growth—even in a challenging pricing environment—suggests the company is maintaining or gaining share. Negative volume growth would be a significant red flag.

2. Adjusted EBITDA Margin

Given the company's cyclical exposure and commodity input costs, EBITDA margin is a better indicator of operational performance than gross margin alone. The margin captures pricing power, manufacturing efficiency, and overhead discipline.

During the pandemic peak, Atkore's EBITDA margins reached extraordinary levels. The current normalization has compressed margins significantly. Investors should watch for margin stabilization as a sign that the pricing reset is complete.

3. Price vs. Cost Spread

The relationship between selling prices and input costs (primarily steel and PVC resin) determines profitability. When prices fall faster than input costs, margins compress; when prices rise faster than costs (as during the pandemic), margins expand.

The company anticipates continued price versus cost headwinds in fiscal 2026.

XII. Bull and Bear Cases

The Bull Case

Electrification Tailwinds Are Real: Data center construction, grid modernization, and renewable energy deployment represent genuine multi-year demand drivers that transcend normal construction cycles.

Import Protection Could Improve: Trade policy actions limiting Mexican steel conduit imports would reduce competitive pressure and support pricing.

Strategic Review Creates Optionality: A sale at reasonable multiples could deliver significant value to shareholders; alternatively, cost reduction and portfolio optimization could drive earnings recovery.

Valuation Is Reasonable: At current prices, Atkore trades at modest multiples relative to its history and to normalized earnings power.

Market Leadership Endures: Despite competitive pressure, Atkore remains the market leader in most of its product categories, with strong brands and distribution relationships.

The Bear Case

Cyclical Business in a Downturn: Non-residential construction is cyclical, and economic uncertainty could lead to further project delays and cancellations.

Import Competition Is Structural: Mexican conduit producers have invested in capacity specifically to serve the U.S. market; even with trade policy actions, competitive pressure may persist.

Margin Normalization May Not Be Complete: The extraordinary margins of 2021-2023 may have been an aberration; normalized margins could be lower than current levels.

Management Transition Risk: CEO succession during a strategic review creates execution risk; the next leader inherits significant challenges.

Commodity Exposure: Material input costs remain volatile, and the company has limited ability to hedge this exposure long-term.

XIII. Conclusion: The Invisible Infrastructure Investment

Atkore's story is fundamentally about the gap between perception and reality in industrial investing. The products are unglamorous—steel tubes, PVC pipes, metal framing—but they're essential. The business model is simple to describe but difficult to execute well. The competitive advantages are real but not insurmountable.

The company has demonstrated that operational excellence can create significant value even in commodity-like markets. From a $16 IPO price to a peak above $189, Atkore proved that "boring" industrial companies can deliver exceptional returns when they execute consistently.

The current challenges—pricing normalization, import competition, margin compression—are real but not unprecedented. Cyclical businesses go through cycles. The question is whether the fundamental demand drivers (electrification, infrastructure investment, data center construction) are sufficient to support a recovery, and whether management can navigate the strategic review process to maximize shareholder value.

"Under his leadership, Atkore has built a diverse portfolio of products and solutions to meet increased demands for electrification and digitization, all while delivering value to our employees, customers and shareholders."

Whatever the outcome of the strategic review—continued independence, asset sales, or a full company sale—Atkore's journey from Tyco division to market leader offers lessons for investors: the power of focus, the value of operational excellence, and the opportunity hidden in essential but invisible infrastructure.

The conduits may be invisible, but the value they create doesn't have to be.

Key Metrics Summary

| Metric | FY 2024 | FY 2025 | FY 2026 Guidance |

|---|---|---|---|

| Net Sales | $3.20B | $2.85B | $3.0-3.1B |

| Adjusted EBITDA | $771M | $386M | $340-360M |

| Net Income | $473M | $(15)M | N/A |

| Organic Volume Growth | Positive | +0.7% | Mid-single digit |

| Employees | ~5,600 | ~5,400 | N/A |

Company Timeline

| Year | Event |

|---|---|

| 1959 | Allied Tube & Conduit founded; Flo-Coat process introduced |

| 1974 | IMC (Intermediate Metallic Conduit) pioneered |

| 1987 | Acquired by Tyco International |

| 1995 | Unistrut acquisition |

| 1999 | AFC Cable Systems acquisition |

| 2010 | CD&R acquires 51% stake; Atkore name adopted |

| 2014 | Tyco's remaining stake repurchased |

| 2016 | IPO at $16/share |

| 2018 | Bill Waltz becomes CEO |

| 2022 | $310M+ deployed on six acquisitions |

| 2024 | Stock reaches all-time high of $189 |

| 2025 | Strategic review expanded; potential sale explored |

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube