Alimentation Couche-Tard: The Global Convenience Empire

I. Introduction & Episode Roadmap

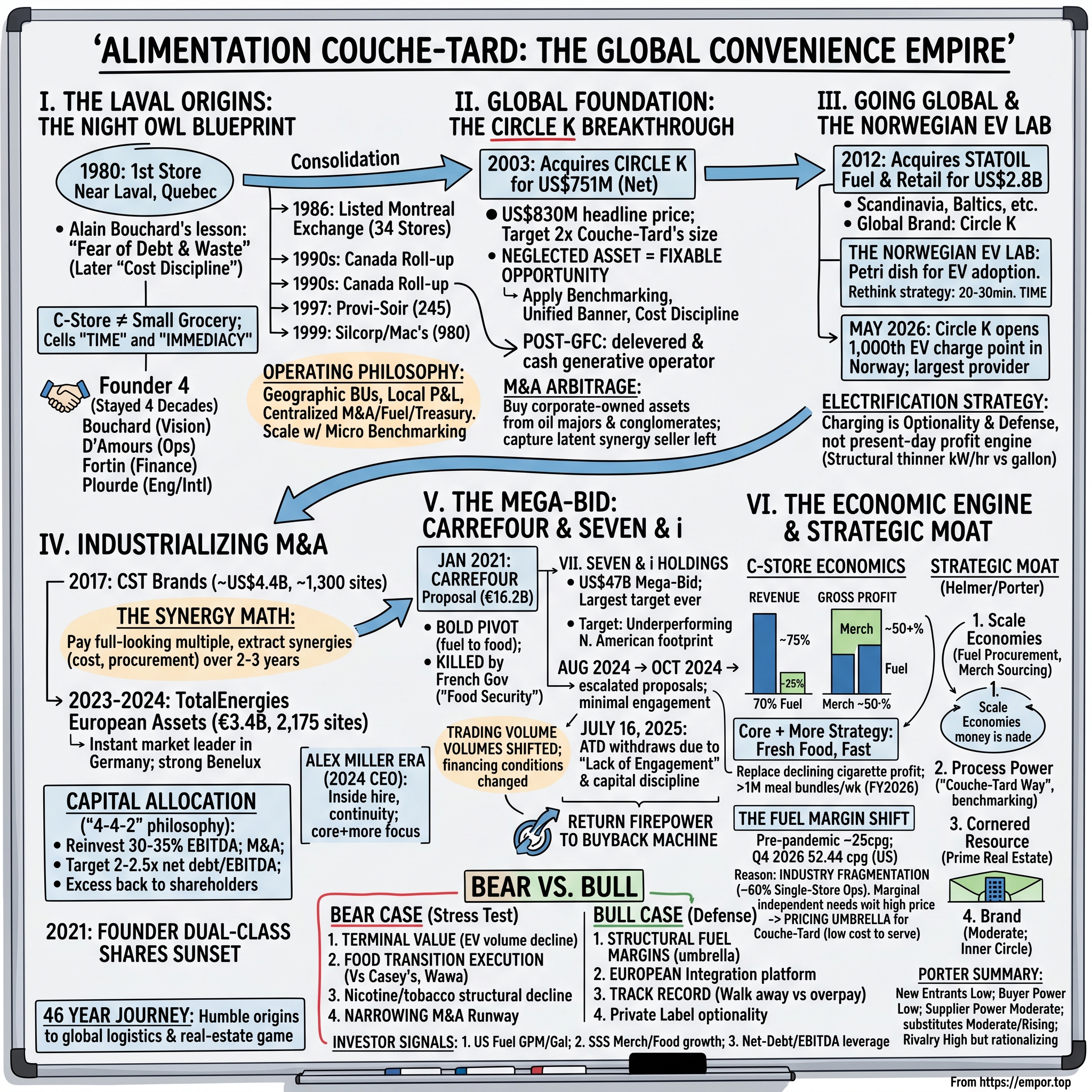

Picture a corner lot at a highway exit somewhere in suburban America. A driver pulls in, swipes a card at the pump, walks inside for a coffee and a bag of chips, and is gone in four minutes. It is the most forgettable transaction in modern commerce — and one of the most repeated. Across the world, this scene plays out roughly eleven million times a day inside stores run by a company most of its own customers could not name.

That company is Alimentation Couche-Tard Inc. — "night owl food," in Quebec French — which trades on the Toronto Stock Exchange under the ticker ATD. It began as a single store opened in 1980 near Laval, Quebec, by a French-Canadian entrepreneur named Alain Bouchard whose father had gone bankrupt when he was a teenager. Forty-six years later, that one store had multiplied into a network of 17,267 sites and, in the fiscal year ended April 26, 2026, generated $76.5 billion in total revenue and $3.14 billion in net earnings attributable to shareholders.1 The convenience business is famously unglamorous. Couche-Tard turned its very dullness into a compounding machine.

Here is the thesis this episode will test rather than assume. Couche-Tard is, on paper, a textbook study in three disciplines that rarely coexist in one firm: programmatic mergers and acquisitions, obsessive operational benchmarking, and hard-nosed capital allocation. Its edge is not a secret product or a patent. It is scale applied to a stubbornly fragmented industry — the ability to buy underperforming assets from oil majors and distracted conglomerates, run them harder than the previous owner could, and pay down the debt before the next deal. The question a serious long-term investor has to answer is whether that edge is durable, or whether it is a machine built for an age of cheap credit and abundant sellers that is quietly running out of both.

Along the way we will trace the arc of the story. The humble Quebec roots, and the founding partnership of four men who stayed together for four decades. The M&A engine that swallowed Circle K, Statoil, CST Brands, and TotalEnergies' European stations, and what each deal taught the company. The economics of the modern convenience store — where fuel supplies most of the revenue but the coffee, cigarettes, and roller-grill hot dogs supply most of the profit. The dramatic, and ultimately failed, $47 billion pursuit of Japan's 7-Eleven parent, abandoned exactly one year ago on the very date this is being written. And finally, the honest bull-and-bear reckoning: what could keep this compounding going, and what could break it.

Let us start where every good origin story does — with a man who had nothing, and a store that stayed open late.

II. Laval Origins & The Night Owl Blueprint

Alain Bouchard did not grow up expecting to build an empire. Born in 1949 in Chicoutimi, deep in Quebec's Saguenay region, he was one of six children of a man who ran an excavation and construction business. When that business collapsed, the family's comfortable life collapsed with it; by Bouchard's own telling, they ended up living in a mobile home in a remote company town called Micoua, where his father found work on a hydro project.2 The lesson a boy absorbs from watching a parent lose everything is not usually entrepreneurial ambition. It is a bone-deep fear of debt and waste. That fear — later rebranded as "cost discipline" — would become the company's founding religion.

At nineteen, Bouchard took a job as a stock boy in a convenience store belonging to the Perrette dairy chain. He turned out to be unusually good at the unglamorous parts: setting up new locations, watching what sold, noticing where the previous manager had left money on the floor. Before long he was opening stores for Perrette by the dozen.2 He had found, almost by accident, the industry he would spend his life inside. When he finally struck out on his own in 1980 with a single store near Laval, he brought with him a conviction that most retailers underestimated: that a convenience store is not a small grocery, but a completely different machine — one that sells time and immediacy rather than selection and price.

The name captured the whole strategy. Couche-tard is the Quebec French term for a night owl, someone who goes to bed late. The stores would stay open long after the grocery chains had locked their doors, catering to shift workers, students, and anyone who needed a carton of milk or a pack of cigarettes at eleven at night. High-velocity items, long hours, tiny footprints, relentless attention to what moved off the shelf and what did not. It was, from day one, a velocity business dressed up as a retail business.

Bouchard did not build it alone, and this matters more than it first appears. Around him formed a founding partnership of four: himself, Jacques D'Amours, Richard Fortin, and Réal Plourde.3 D'Amours ran operations, Fortin handled finance, Plourde managed engineering and later international expansion. What is striking is not that they came together but that they stayed together — for decades, through every acquisition, without the ego wars that fracture most founder groups. That stability let them build a culture rather than merely a company: frugal, decentralized where it counted, ruthlessly centralized where it mattered.

The 1980s and 1990s were an education in consolidation on home turf. The predecessor company listed on the Montreal Exchange in 1986 with a network of thirty-four stores, was taken private again in 1994, and emerged as Alimentation Couche-Tard Inc.4 Then came the roll-up of Quebec and Ontario. In May 1997 the company absorbed 245 Provi-Soir stores in Quebec along with 50 Wink's outlets, and in April 1999 it acquired Silcorp, pulling in roughly 980 stores under the Mac's, Mike's Mart, and Becker's banners across Ontario and Western Canada.4 In the space of two years, a regional Quebec operator had become the largest convenience chain in Canada. Note the pattern already forming: buy a tired incumbent, standardize it, wring out the waste, repeat.

The operating philosophy that emerged in these years is the part worth dwelling on, because it explains everything that follows. Couche-Tard organized itself into geographic business units, each led by a vice president with genuine profit-and-loss accountability over their stores. Local managers were given autonomy over the things that are genuinely local — the product mix, the staffing, the feel of a store in a Texas suburb versus one in Oslo. But the functions where scale creates advantage — fuel sourcing, treasury, and above all M&A — were kept tightly centralized at head office. And every store's numbers were laid bare and compared against its peers, week after week, so that a laggard could not hide.

The key lesson of the origin years is deceptively simple: scale is worthless without micro-level benchmarking. Owning a thousand stores means nothing if you cannot see which of them is bleeding and why. Couche-Tard's founders built a nervous system for their retail body — one that could feel pain in a single limb — before they ever attempted to make it a giant. That nervous system was about to be tested by a target twice the company's size, sitting fresh out of bankruptcy on the far side of a continent.

III. The Foundation: The Circle K Breakthrough

By the early 2000s, Couche-Tard had conquered Canada and run out of room. The Canadian convenience market is a rounding error next to the American one; to keep compounding, the company had to cross the border. The trial run came in June 2001, when it bought 172 stores operating under the Bigfoot banner across Indiana, Illinois, and Kentucky.4 It was a modest bet — a way of proving that the Couche-Tard operating model was not some quirk of Quebec culture but a portable system that worked on American soil. It worked. And it emboldened the founders to attempt something that looked, to most observers, like recklessness.

The opportunity arrived because a big oil company wanted out. ConocoPhillips had inherited Circle K, a sprawling and storied American convenience chain, and had no strategic love for running gas-station snack shops. Circle K was large — around 1,663 corporate stores across sixteen states, plus hundreds more franchised and licensed sites — and it was a mess: recently emerged from bankruptcy, operationally neglected, the kind of asset a major sheds without sentiment.4 It was also roughly twice the size of the company trying to buy it.

On October 6, 2003, Couche-Tard agreed to acquire Circle K for a headline price of about US$830 million.5 The deal closed on December 17, 2003, with the actual net cash outlay coming in nearer US$751 million after adjustments.4 The reaction from the analyst community ranged from skeptical to derisive. A French-Canadian upstart, barely known south of the border, was swallowing an American icon twice its size and levering up to do it. The consensus was that Couche-Tard had bought a problem it did not understand.

What the skeptics missed was that a neglected asset is exactly what the Couche-Tard machine was built to fix. The company did not need Circle K to be well run; it needed it to be fixable. In moved the benchmarking system, store by store, exposing the underperformers. Fuel supply contracts were renegotiated with the leverage of a suddenly larger buyer. Supply chains were rationalized, corporate stores were converted to the unified Circle K banner, and the bloated cost structure of a business that had been managed as an oil-company afterthought was slowly starved of its excess.

The financial result was the proof of concept the whole future would rest on. Couche-Tard's consolidated operating margins, thin to begin with, expanded materially over the following few years as the acquired stores were brought up to standard, and the enlarged company threw off enough free cash flow to pay down its acquisition debt well ahead of schedule. That deleveraging turned out to be exquisitely timed: by the time the Global Financial Crisis arrived in 2008, Couche-Tard was not a fragile, over-levered roll-up but a cash-generative operator with a cleaned-up balance sheet, ready to keep buying while weaker rivals retrenched.

Here is what the Circle K episode really taught the company, and what an investor should take from it. The most reliable form of M&A arbitrage in this industry is not clever financial structuring — it is buying corporate-owned assets from sellers who do not want them, from oil majors and conglomerates for whom retail is a distraction, and then applying operating rigor those sellers were never willing to supply. The seller books a tidy divestiture; the buyer captures years of latent synergy the seller left on the table. Couche-Tard had found its lifelong hunting ground. The only remaining questions were how far it could travel, and whether the model would survive contact with a genuinely foreign market. The answer would come from Scandinavia.

IV. Going Global & The Norwegian EV Lab: Statoil Fuel & Retail

For a company that had just spent a decade proving it could run American gas stations, Europe was a different kind of leap — not merely geographic but linguistic, regulatory, and cultural, across markets where fuel is taxed to the hilt and consumer habits bear little resemblance to a Texas interstate. In April 2012, Couche-Tard reached for it anyway, launching a bid for Statoil Fuel & Retail, the leading fuel-and-convenience operator across Scandinavia.6

The target was substantial: roughly 2,300 stations spread across Norway, Sweden, Denmark, Poland, the Baltics, and beyond, carrying the Statoil name under license from the Norwegian energy group. By June 19, 2012, Couche-Tard had become principal owner, ultimately paying around NOK 51.20 per share and taking control of a business valued at roughly US$2.8 billion.6 Investors again voiced the familiar worry — a big geographic jump, heavy exposure to European retail fuel volumes, a brand the company would eventually have to replace. The Statoil banner was gradually retired in favor of Circle K, giving Couche-Tard, for the first time, a genuinely global consumer brand spanning two continents.

But the most interesting thing Couche-Tard bought in Norway was not stations or a brand. It was a laboratory. Norway has spent the past decade as the world's most advanced petri dish for electric-vehicle adoption, its generous tax incentives pushing EVs to a share of new-car sales that no other country approaches. For a company whose profits still lean heavily on selling gasoline and diesel, owning a large retail network in the one market where liquid-fuel demand is visibly eroding could have been a slow-motion disaster. Couche-Tard chose to treat it as R&D instead.

The strategic reframing is the part worth understanding. An electric vehicle does not pull in and leave in four minutes. It parks for twenty or thirty while it charges — a captive window of dwell time that a well-designed store can monetize far more richly than a quick fuel-and-go visit ever allowed. The Norwegian business became the place where Couche-Tard learned to capture that window: deploying fast chargers, upgrading coffee and fresh-food programs, and testing the digital tools that turn a charging stop into a shopping trip. In May 2026 the company marked a milestone that neatly closed the loop — Circle K opened its 1,000th EV charge point in Norway, at the very Oslo site that hosted the country's first commercial fast charger back in 2011, and it now stands as the largest EV charging provider in that market.7 Across Europe the network had grown past 4,300 charge points by late in fiscal 2026.8

An honest investor should keep the economics in proportion. EV charging today generates a rounding error of profit next to the supernormal fuel margins Couche-Tard earns in North America, and the margins on a kilowatt-hour are structurally thinner and more contested than those on a gallon of gasoline. Management's own framing on recent calls is telling: charging is described as optionality and defense, not as a present-day profit engine. That is the right way to read it. Norway does not make money for Couche-Tard the way Texas does. What it does is buy the company knowledge — a rehearsal, on someone else's timeline, for the fleet transition that will eventually reach every market it operates in.

The lesson of Statoil is therefore twofold. First, that early-adopter markets are worth owning precisely because they show you the future before it becomes your problem. Second — and more soberingly — that Couche-Tard's answer to electrification is still largely a European experiment, not a proven North American profit stream. Whether the dwell-time playbook scales into real earnings, or remains a hedge that quietly dilutes returns, is one of the genuinely open questions in the investment case. With Europe now a permanent part of the portfolio, the machine turned back toward the deals that had always paid the bills.

V. The M&A Machine: CST Brands, European Scale, and Synergy Math

If Circle K proved the model and Statoil globalized it, the second half of the 2010s was about industrializing it — turning acquisition into something closer to a repeatable manufacturing process than a series of one-off bets. Two deals frame the era, one on each side of the Atlantic.

The first was CST Brands, and its provenance tells you why Couche-Tard wanted it. CST was the retail business that the refiner Valero Energy had spun off — another oil-adjacent asset severed from a parent that had no interest in running convenience stores. On August 22, 2016, Couche-Tard agreed to buy it for US$48.53 per share, an enterprise value of roughly US$4.4 billion, closing the following June after clearing U.S. antitrust review.9 The prize was around 1,300-plus stores concentrated in the U.S. Southwest — Texas above all — plus a meaningful eastern Canadian footprint. To satisfy regulators and to prune the parts it did not want, Couche-Tard divested selected sites, including a package of Canadian assets sold to Parkland.9

The CST deal is where the outline's "synergy math" deserves a careful, skeptical look rather than a management-brochure retelling. The pattern Couche-Tard aims to repeat is well established: pay a full-looking multiple on the seller's trailing earnings, then drive the effective multiple down over two or three years by extracting cost and procurement synergies the seller never bothered to capture — cheaper fuel supply, combined purchasing, shared overhead, banner conversion. When it works, a deal that looked expensive on day one looks cheap in hindsight. The important caveat for an investor is that the headline synergy figures companies attach to deals are self-reported targets, not audited outcomes, and they are rarely disclosed cleanly enough afterward to verify. The right posture is to treat Couche-Tard's synergy record as credible because of the Circle K precedent, not proven because management asserted a number.

The second defining deal of the era carried the company deeper into Europe. In March 2023, Couche-Tard agreed to acquire the European retail networks of TotalEnergies, and it closed in two steps — the German business on December 28, 2023, and the Belgian, Dutch, and Luxembourg operations on January 3, 2024.10 The enterprise value was about €3.1 billion, with TotalEnergies ultimately receiving roughly €3.4 billion in cash after adjustments.10 The structure is worth getting right, because it is frequently reported wrong: Couche-Tard took full ownership of the German and Dutch assets, but only a 60 percent controlling interest in Belgium and Luxembourg, leaving TotalEnergies with a 40 percent stake there.11 In total the deal added 2,175 sites — 1,191 in Germany, 562 in Belgium, 378 in the Netherlands, and 44 in Luxembourg.11

The strategic logic was straightforward and, for once, hard to argue with. It made Couche-Tard an instant market leader in Germany, the largest economy in Europe, and gave it dense, profitable positions in the Benelux countries — a coherent northern-European bloc rather than a scattering of flags. By fiscal 2026, management reported the European integration running at roughly €61 million of annual synergies and set out a path toward €120 million by fiscal 2027 and €170 million by fiscal 2029 — targets, again, to be watched rather than taken on faith.1

Underpinning all of this is a capital-allocation philosophy the outline labels a "4-4-2 rule." That specific formulation is not one the company itself uses in its public disclosures, so it is better described in the terms management actually articulates. On the fiscal-2026 calls, CFO Filipe Da Silva laid out the real framework: reinvest roughly 30 to 35 percent of EBITDA back into the business organically, pursue disciplined M&A, hold leverage in a target band of about two-to-two-and-a-half times net debt to EBITDA, and return whatever excess remains to shareholders through buybacks.12 The behavioral pattern is the tell. After a large acquisition, Couche-Tard levers up, then attacks the debt aggressively with its organic cash flow and pulls leverage back down — the balance sheet at fiscal 2026 year-end sat at 1.99 times, comfortably inside the band.1 And when the M&A pipeline goes quiet, the company turns the cash toward its own shares, buying back 30 million of them for $1.6 billion in fiscal 2026 alone.1 It is a system engineered to keep compounding whether or not a deal is available — which is precisely the discipline that would be tested when the two biggest targets of the company's life came into view.

VI. The Pivot, The Block, and The Mega-Bid: Carrefour & Seven & i

Every acquisitive company eventually reaches for something too big, and how it handles the reach reveals more than any successful deal ever could. Couche-Tard reached twice. Both times it came home empty-handed. Both episodes are, paradoxically, among the most instructive in its history.

The first reach was audacious in a different direction — not bigger convenience, but a wholesale change of category. In January 2021, Couche-Tard approached the French grocery giant Carrefour with a friendly merger proposal valuing the company at roughly €16.2 billion.13 The vision was a leap from fuel-and-convenience into global multi-format food retail: Carrefour's enormous private-label supply chain, its urban fresh-food expertise, its European density, married to Couche-Tard's operating discipline. It was the boldest strategic pivot the founders had ever contemplated.

It lasted roughly forty-eight hours. The French government, with Finance Minister Bruno Le Maire out front, killed it on the grounds of national "food security" and sovereignty, treating a grocery chain as a strategic national asset that could not fall into foreign hands.13 There was no antitrust process to litigate, no counter-offer to sweeten — just a political wall, erected almost overnight. Couche-Tard withdrew and pivoted straight back to the convenience competencies it understood. The episode was a hard lesson in a variable no benchmarking system can price: cross-border protectionism, and the reality that in some countries a retailer is a flag, not just a business.

The second reach was the largest of them all, and it targeted the one rival that had always loomed over Couche-Tard: 株式会社セブン&アイ・ホールディングス Seven & i Holdings, the Japanese parent of セブン-イレブン 7-Eleven and Couche-Tard's biggest global competitor. Seven & i owned a dominant position in Japan and a vast but famously underperforming North American footprint — exactly the kind of neglected asset Couche-Tard had spent forty years learning to fix, except this time wrapped inside a proud Japanese conglomerate rather than a distracted oil major.

The courtship, when it became public, was a masterclass in escalating pressure meeting immovable resistance. Couche-Tard's initial approach in August 2024, at around US$14.86 per share, was rejected as grossly undervaluing the company.14 In October 2024 it raised the bid more than 22 percent to about US$18.19 per share, valuing Seven & i at roughly ¥7 trillion, or about US$47 billion — which would have been the largest-ever foreign takeover of a Japanese company.14 By January 2025 the proposal had been recast at the yen equivalent of ¥2,600 per share, and in April 2025 the two sides finally signed a non-disclosure agreement giving Couche-Tard access to Seven & i's books.14 For a moment, it looked like engagement.

It was not. On July 16, 2025 — one year ago to the day — Couche-Tard withdrew, in a blistering letter to Seven & i's board signed by both Alex Miller and Alain Bouchard.15 The language was extraordinary for a company usually so buttoned-up. There had been, the letter said, "no sincere or constructive engagement" from Seven & i; the due diligence permitted, including just two tightly constrained management meetings, had been "negligible"; and the whole process amounted to "a calculated campaign of obfuscation and delay, to the great detriment of 7&i and its shareholders."15 Seven & i fired back that Couche-Tard's account was a "mischaracterization," and pointedly suggested that shifting global economics, exchange rates, and financing conditions might have had as much to do with the walk-away as any lack of engagement.16 The market rendered its own verdict: Seven & i shares slid sharply, closing well below the offer price once the bid vanished.17

There is a genuinely debatable question buried here, and a neutral telling has to acknowledge both sides. Couche-Tard framed the withdrawal as an act of capital discipline — a refusal to launch a destructive, expensive hostile campaign or to overpay to force a deal that a founder-family-influenced Japanese board plainly did not want. That framing is consistent with everything in the company's history, and it is largely persuasive. But Seven & i's counter-suggestion is not baseless: by mid-2025 the yen, financing markets, and Couche-Tard's own currency exposure had all moved, and a deal that pencilled out in late 2024 may simply have become harder to justify. The most honest read is that discipline and changed circumstances pointed in the same direction, and the company took the exit that its history had trained it to take. Either way, the largest bet Couche-Tard ever placed ended not with a signature but with a walk to the door — and a return of firepower to the buyback machine.

VII. Current State: Segment Breakdown, Alex Miller's Era, & Convenience Economics

The Seven & i drama unfolded during a quiet changing of the guard at the top. In June 2024, Couche-Tard announced that Brian Hannasch — the American operator who had run the company since 2014 and overseen a decade of aggressive value creation — would retire, with chief operating officer Alex Miller succeeding him as president and CEO effective September 6, 2024.18 Miller was the definition of an inside hire: he had joined Couche-Tard in 2012 and climbed through its U.S. operations, and his elevation signaled continuity rather than reinvention — the same fuel-procurement expertise, the same benchmarking discipline, the same reluctance to chase growth at any price. The Seven & i letter bearing his signature alongside Bouchard's was, in a sense, his introduction to the world.

Above him sits a governance structure that quietly transformed a few years earlier. From its origins, Couche-Tard had carried a dual-class share structure that concentrated control in its founders through multiple-voting shares carrying ten votes each. But that structure came with a sunset clause written back in the 1990s, tied to the age of the youngest founder. When Jacques D'Amours turned 65, the clause triggered, and on December 8, 2021, the multiple-voting shares converted one-for-one into ordinary single-vote shares.[^19] Alain Bouchard remains executive chairman with an enormous personal equity stake — founder skin in the game aligned with ordinary shareholders — but the era of founder super-voting control is over. For an investor, the sunset is a genuine improvement in governance quality: influence now travels with economic ownership rather than sitting in a special class of votes.

Now to the engine itself, because the economics of a convenience store are far stranger and more interesting than the pump price suggests. Start with the headline split. Roughly three-quarters of Couche-Tard's revenue comes from selling road-transportation fuel, and only about a quarter from the merchandise and services sold inside the store. That makes it look like a gas-station company. But revenue is a liar here, because fuel is a low-margin, pass-through business whose top line balloons and shrinks with the oil price. Follow the gross profit instead, and the picture inverts: merchandise and services now generate more than half of Couche-Tard's total gross profit, while fuel supplies the rest.19 The gasoline gets people onto the lot; the coffee, cigarettes, energy drinks, and hot food are where the money is actually made.

The inside-store margins explain why. In the fourth quarter of fiscal 2026, merchandise gross margins ran at 34.4 percent in the United States, 33.5 percent in Canada, and 39.6 percent in Europe.1 The European premium reflects a different product mix and pricing culture; the North American figures reflect the classic convenience blend of high-margin packaged beverages, tobacco and nicotine, private label, and — increasingly — fresh food. Under the "Core + More" strategy that Miller has made the centerpiece of his tenure, the company has been pushing hard into food service, where gross margins can exceed 50 percent and where a hot, fresh meal does something a pack of cigarettes cannot: it brings the same customer back tomorrow. On the fiscal-2026 calls, management reported U.S. food-service same-store sales growing above 5 percent, its "Fresh Food, Fast" program growing above 10 percent, and more than a million meal-deal bundles moving each week.12 The strategic motive is defensive as much as offensive — fresh food is the designated replacement for the profit that declining cigarette volumes will eventually take away.

Then there is the fuel side, where something genuinely structural has happened, and where the outline's numbers need correcting to what the company actually reported. For much of the 2010s, U.S. retail fuel margins sat in the low-to-mid-twenty-cents-per-gallon range. Post-pandemic, they have reset dramatically higher. In the fourth quarter of fiscal 2026, Couche-Tard earned 52.44 U.S. cents per gallon in the United States, up more than nine cents year over year, and for the full year the U.S. figure was 47.49 cents per gallon.1 Industry-wide, the National Association of Convenience Stores has documented the same shift, with average fuel margins climbing toward 40 cents per gallon in 2025 from the mid-twenties a decade earlier.20

Why is this durable rather than a temporary windfall? The answer lies in the industry's fragmentation. Roughly 60 percent of America's convenience stores are owned by single-store operators — mom-and-pop businesses running one site.21 These independents face brutal cost pressures: wage inflation, credit-card swipe fees that now eat a large slice of every fuel transaction, and slowly declining fuel volumes as vehicles grow more efficient. To survive, they need to price fuel to cover those rising costs, which pushes the entire industry's marginal price higher. That creates a pricing umbrella under which a low-cost scale operator like Couche-Tard can shelter — matching the price the marginal independent needs to charge, while enjoying a structurally lower cost to serve. The result is supernormal fuel profits that persist as long as the independents' costs keep rising.

An investor should hold two thoughts at once here. The structural argument is real and is corroborated by independent NACS data, not just management assertion. But margins this elevated also invite the obvious question analysts pressed on the fiscal-2026 calls — whether they are as sticky as management claims, or whether competition eventually competes some of the excess away. On the Q4 call, several analysts probed exactly this, questioning how Couche-Tard's reported fuel margins could run ahead of broader industry benchmarks, and whether the company should be sacrificing some margin to win back the fuel volume it has been quietly losing.12 Miller declined, prioritizing a consistent customer value proposition over chasing gallons. That is a defensible answer. It is also, unmistakably, a bet — and it sets up the harder question of whether the whole edifice holds together when viewed through a competitive-strategy lens.

VIII. Strategic Moat: Hamilton Helmer's 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the cold question a strategist would ask: what, precisely, stops someone else from doing what Couche-Tard does? Two frameworks help pressure-test the answer — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — and applied honestly, they yield a moat that is real but narrower and more concentrated than the company's fans sometimes suggest.

Begin with Helmer, and with the power that does most of the work. Scale economies are Couche-Tard's primary and most defensible advantage, and they operate in two distinct places. The first is fuel procurement. A company that buys billions of gallons a year, operates its own terminals and trading desk, and can move supply around its network commands a per-gallon cost advantage that a single-store operator buying at the rack simply cannot match. On the fiscal-2026 calls, Miller repeatedly credited "more than a decade building supply-chain optionality, terminals and trading capabilities" for the company's ability to profit when fuel markets turn volatile — a capability that is expensive to build and therefore hard to copy.12 The second is merchandise sourcing: buying directly and at enormous volume from the Cokes, Pepsis, and nicotine manufacturers of the world, Couche-Tard secures rebates and terms that no independent, and few regional chains, can approach.

The second power is process power — Helmer's term for an advantage embedded in a company's accumulated way of operating, which competitors cannot simply buy but must slowly build. This is "the Couche-Tard Way": decades of refinement in labor scheduling, energy use, inventory turns, and shrink reduction, enforced by the weekly store-level benchmarking that has been the company's signature since Laval. It is genuinely hard to replicate because it is not a single practice but a culture and a data system built up over forty years. The honest caveat is that process power is quieter and less measurable than scale, and it erodes if the discipline slips — it is a power that has to be re-earned every week.

The third, cornered resource, applies partially: prime real estate. High-traffic corner lots at highway exits and in mature suburbs cannot be conjured up on demand — zoning, environmental permitting for underground fuel tanks, and land cost all limit new supply, which protects the value of an existing network. But this is an industry-wide advantage shared by every incumbent with good sites, not something unique to Couche-Tard, so it is better read as a barrier to entry than a proprietary edge.

Brand, finally, is the weakest of the four. Circle K is a globally recognized logo, and the Inner Circle loyalty program — around 15 million members by the end of fiscal 2026 — is building genuine stickiness.12 But convenience retail remains, at its core, a location-and-convenience purchase; few customers drive past a closer store to reach a Circle K. Brand equity here is moderate, a supporting player rather than a moat in its own right.

Now turn to Porter, which reframes the same business as a competitive battlefield. The threat of new entrants is very low: the combination of prime-real-estate scarcity, the environmental cleanup liability attached to underground fuel tanks, and the sheer scale needed to compete on fuel procurement makes greenfield entry economically irrational. Buyer power is low: a customer buying a cold drink or emergency gasoline is paying for immediacy and does not shop around for pennies, which is the deep reason convenience pricing holds. Supplier power is moderate: the big tobacco and beverage conglomerates wield real leverage, but a retail footprint the size of Couche-Tard's makes the company an indispensable channel they cannot afford to alienate. The threat of substitutes is moderate and rising: quick-service restaurants compete for the food dollar, dollar stores for the snack dollar, and — over a longer horizon — fleet electrification threatens the liquid-fuel franchise itself.

The force that matters most is competitive rivalry, and here the picture is high but rationalizing. The named field is formidable: Seven & i's 7-Eleven still operates well over 12,000 U.S. stores, Casey's General Stores runs roughly 2,900 sites concentrated in the Midwest, Murphy USA around 1,700, and EG America some 1,400.22 What makes the rivalry tolerable rather than ruinous is consolidation itself — as scale players absorb independents, pricing behavior across the industry grows more rational, particularly in fuel, which is precisely the dynamic that sustains the margin umbrella described earlier. The synthesis, then, is this: Couche-Tard's moat is real, it is anchored in scale and process, and it is defended by high entry barriers — but it is concentrated in fuel procurement and operating discipline, it is weakest exactly where the future is headed (brand loyalty and the shift away from liquid fuel), and it depends on an industry structure that could, in principle, change. Which is the perfect setup for the argument between the bulls and the bears.

IX. Bear vs. Bull Case: The Long-Term Investor's Stress Test

The best way to value a compounding machine is to try, in good faith, to break it. So let us convene the skeptics first, and give them their strongest ammunition before the defense gets to reply.

The bear case begins with terminal value, and it is the argument that keeps thoughtful shareholders awake. Passenger-vehicle electrification will, over time, shrink the volume of liquid fuel sold — slowly at first, then less slowly. Couche-Tard's own U.S. same-store fuel volumes already fell in fiscal 2026, down 1.0 percent for the full year and 2.1 percent in the fourth quarter.1 The bear does not need a collapse; even a persistent 1-to-2 percent annual decline through the 2030s would, over time, compress the multiple the market is willing to pay for a business whose profit pool is still meaningfully tied to gasoline. A single-digit volume erosion sounds survivable until you remember how much of the company's gross profit the fuel line still carries.

The second prong is the food transition, which the bear regards as easier to announce than to execute. Selling fresh, prepared food well is a genuine operational discipline — commissaries, waste management, consistent quality across thousands of sites — and Couche-Tard is charging into it against entrenched specialists. Casey's has quietly become one of the largest pizza chains in the United States; Wawa and Sheetz have built cult followings on food that convenience customers actively seek out. Couche-Tard has historically been a fuel-and-packaged-goods operator, not a kitchen operator, and closing that gap at scale is unproven. Impressive early growth rates off a low base, the bear notes, are not the same as a durable food business.

Third is nicotine, a category in structural decline. Cigarettes have been shrinking for years, and while newer products — nicotine pouches like Zyn, vaping — are growing fast, they carry heavier regulatory scrutiny and less certain margins, and they are subject to the whims of tax and enforcement policy. On the fiscal-2026 calls, management pointed to disciplined pricing keeping U.S. cigarette sales in modest growth and to strong momentum in modern oral nicotine, while flagging genuine regulatory and illicit-trade headwinds in Canada.12 The category is not falling off a cliff, but it is a diminishing pillar under a meaningful share of inside-store profit.

The fourth bear point is about the growth model itself. Couche-Tard's compounding has always been fed by large, accretive acquisitions. With Seven & i off the table, Carrefour long gone, and the North American independent base already heavily consolidated, the runway for needle-moving deals is narrowing. If the M&A engine stalls, the company is left leaning on organic growth and buybacks — good, but arithmetically slower than the decades of transformative dealmaking that built the legend. An activist would press further: is management's insistence that it "does not rely on M&A to deliver the growth algorithm" strategic confidence, or is it pre-emptive expectation management for a future with fewer big deals in it?12

Now the defense, which is more than mere rhetoric. On fuel margins, the structural argument stands on independent evidence: as long as single-store operators face rising costs and need 40-plus cents a gallon to survive, the pricing umbrella protects the scale player, and fuel gross profit can hold even as volume slowly declines — the price per gallon is doing the work the gallons no longer do. On growth, the TotalEnergies-built European platform is now consolidated and offers a real runway to cross-pollinate North American food and private-label programs into markets that never had them. On capital allocation, the track record is the strongest witness: return on equity of 20.2 percent in fiscal 2026, a decade of double-digit adjusted EPS growth, and — the single most persuasive data point — the willingness to walk away from a $47 billion deal rather than overpay.1 A management team that destroys value for the sake of size does not abandon the biggest acquisition of its life at the altar.

And on optionality, the bull points to private label, still underpenetrated relative to grocery peers and carrying margins several points above national brands — a lever the company has barely begun to pull, and one that requires no acquisition to deploy. Weighing it all, the neutral verdict is that both cases are substantially true at once. Couche-Tard is a superbly run, disciplined operator sitting on a structurally advantaged fuel position and a credible food and private-label runway — and it is also a company whose core profit pool faces a slow secular headwind and whose historic growth engine is running short of fuel of a different kind. The investment case is not a slam dunk in either direction; it is a genuine debate about the pace of decline versus the pace of reinvention.

For an investor actually tracking this business quarter to quarter, the noise can be cut down to a very small number of signals. Watch three things above all. First, U.S. fuel gross margin per gallon — the single most important swing factor in near-term earnings and the clearest test of whether the pricing-umbrella thesis is holding. Second, same-store merchandise sales growth, especially in food service — the proof of whether "Core + More" is genuinely replacing tobacco profit or merely talking about it. Third, the net-debt-to-EBITDA leverage ratio — the tell for capital-allocation discipline, which reveals whether management is deleveraging as promised or gearing up for a deal that stretches the balance sheet. Those three numbers, tracked over time, will tell a shareholder more than any press release.

X. Epilogue & Key Takeaways

Return, one last time, to that corner lot and the four-minute transaction. What Couche-Tard built its fortune on is the recognition that a boring, low-margin, endlessly repeated act — fueling a car, grabbing a coffee — becomes extraordinary when you own tens of thousands of the machines that perform it and run each one a little better than anyone else could. There is no magic here. There is a nervous system, built in Laval in 1980, that could feel pain in a single store and act on it, extended across two continents over four decades.

Three lessons endure for founders and investors watching from the outside. The first is that benchmarking is not bureaucracy; it is the difference between owning stores and understanding them, and a scale operator that cannot compare its own units against each other is leaving money on the floor every week. The second is that price discipline in acquisition is a form of courage. Walking away from a historic $47 billion deal was harder, and almost certainly more value-creative, than the empire-building alternative — and it is the clearest evidence the company has ever offered about what it truly optimizes for. The third is the uncomfortable one: a scale leader quietly benefits when its industry's costs rise, because rising costs break the weakest competitors first and raise the price umbrella under which the strong shelter. It is not a sentiment that reads well in a press release, but it is the real economic engine beneath the fuel-margin story.

Whether the machine keeps compounding from here is, honestly, unresolved. The company has a structurally advantaged fuel position, a disciplined culture, and a war chest freed up by the deal it declined to overpay for. It also faces the slow gravity of electrification, an unproven pivot into fresh food, a declining nicotine franchise, and a narrowing runway for the transformative deals that built it. What is not in doubt is the character of the operator. Alimentation Couche-Tard is a quiet compounding machine that has spent forty-six years proving that convenience retail is not a dying legacy business but an elite logistics-and-real-estate game — and the next decade will test whether that machine can reinvent its own profit pool as skillfully as it once consolidated everyone else's.

References

-

Alimentation Couche-Tard Announces Its Results for Its Fourth Quarter and Fiscal Year 2026 — PR Newswire (Couche-Tard), 2026-06-22 ↩↩↩↩↩↩↩↩

-

Alimentation Couche-Tard Inc. Form 40-F, Fiscal Year 2006 — U.S. Securities and Exchange Commission, 2006 ↩↩↩↩↩

-

No. 3: Couche-Tard Acquires Circle K — Biggest C-Store Deals So Far This Century — CSP Daily News ↩

-

Alimentation Couche-Tard Becomes Principal Owner of Statoil Fuel & Retail — PR Newswire (Couche-Tard), 2012-06-19 ↩↩

-

Circle K Celebrates 1,000th EV Charging Point in Norway, Back Where the Journey Began — Alimentation Couche-Tard, 2026 ↩

-

Earnings Call Transcript: Alimentation Couche-Tard Q3 2026 Shows Strong Growth — Investing.com, 2026-03 ↩

-

Alimentation Couche-Tard Inc. Announces Competition Clearance in the United States and Closing Date of the Acquisition of CST Brands, Inc. — Couche-Tard Corporate, 2017-06-26 ↩↩

-

Service Stations in Europe: TotalEnergies Closes Its Deals with Alimentation Couche-Tard — TotalEnergies, 2024-01-03 ↩↩

-

Alimentation Couche-Tard Announces the Closing of the Acquisition of Certain European Retail Assets from TotalEnergies — Couche-Tard Corporate, 2024-01-03 ↩↩

-

Alimentation Couche-Tard Q4 2026 Earnings Call Complete Transcript — Benzinga, 2026-07 ↩↩↩↩↩↩↩

-

Quebec's Couche-Tard Drops Bid for France's Carrefour After Government Opposition — CBC News (Thomson Reuters), 2021-01-15 ↩↩

-

Alimentation Couche-Tard Provides Update on Proposal for a Combination with Seven & i — Couche-Tard Corporate, 2025-03-10 ↩↩↩

-

Alimentation Couche-Tard Announces Withdrawal of Proposal to Acquire Seven & i Holdings Due to Lack of Engagement — Couche-Tard Corporate, 2025-07-16 ↩↩

-

Seven & i Responds to Alimentation Couche-Tard's Withdrawal of Its Acquisition Proposal — CSP Daily News, 2025-07 ↩

-

Shares in Japan's Seven & i Plunge 7% After Couche-Tard Withdraws $47 Billion Takeover Bid — CNBC, 2025-07-17 ↩

-

Alimentation Couche-Tard to Appoint Alex Miller President and Chief Executive Officer Effective September 6, 2024 — PR Newswire (Couche-Tard), 2024-06-26 ↩

-

Couche-Tard Sees Strong Growth in Merchandise and Profit Through 2030 (Business Strategy Update summary) — Meyka, 2026-02 ↩

-

5 Key Metrics Defining the Convenience Industry's Health — NACS Magazine, 2026-06 ↩

-

Single-Store Operators Continuing to Leave the C-Store Industry (citing NACS data) — Convenience Store News, 2025 ↩

-

Top 100 Convenience Retailers of 2025 — NACS Magazine, 2025-03 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube