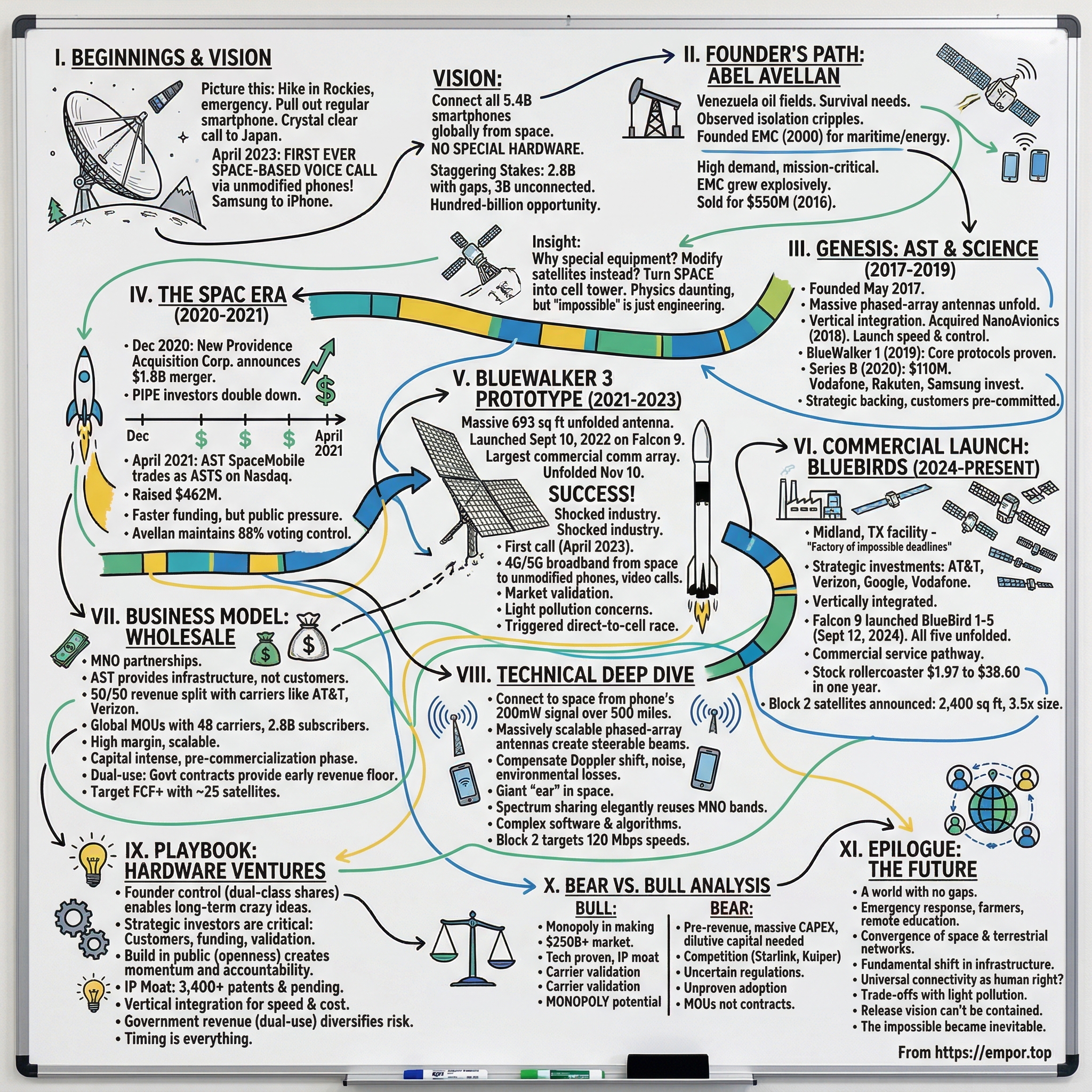

AST SpaceMobile: The Audacious Quest to Connect Every Phone on Earth from Space

I. Introduction & Episode Roadmap

Picture this: You're hiking through the Rockies, miles from the nearest cell tower, when an emergency strikes. You pull out your iPhone—the same one sitting in your pocket right now—and make a crystal-clear call. No special equipment. No satellite phone. No modifications. Just your regular smartphone connecting directly to a massive antenna array orbiting 500 miles above Earth.

This isn't science fiction. On April 25, 2023, a company called AST SpaceMobile made history by completing the world's first space-based voice call using unmodified smartphones. The call connected a Samsung Galaxy S22 in Texas to an iPhone in Japan, routed through a 693-square-foot antenna unfurled in space—the largest commercial communications array ever deployed in low Earth orbit.

The audacity of this vision cannot be overstated. While Elon Musk's Starlink requires a pizza-box-sized terminal and Jeff Bezos's Kuiper needs ground equipment, AST SpaceMobile aims to connect directly to the 5.4 billion smartphones already in people's pockets. No hardware. No apps. No changes whatsoever to how you use your phone today.

The stakes? Colossal. Despite decades of telecom infrastructure buildout, 2.8 billion mobile subscribers still experience coverage gaps. Another 3 billion people remain completely unconnected. The economic opportunity stretches into the hundreds of billions. The technical challenges seem insurmountable. The capital requirements are astronomical.

Yet AST SpaceMobile, led by a Venezuelan-American serial entrepreneur who previously sold a satellite company for $550 million, has assembled an unprecedented coalition: Vodafone, AT&T, Verizon, Google, Rakuten, and dozens of other carriers representing nearly 3 billion subscribers worldwide. They've raised over $1 billion, launched test satellites that shocked the engineering community, and sent their stock on a rollercoaster from $1.97 to $38.60 in a single year.

This is the story of how a company attempts the impossible: turning space itself into a cell tower for planet Earth. It's a tale of technical audacity, financial engineering through SPACs, regulatory innovation, and a founder's relentless pursuit of universal connectivity. Along the way, we'll explore the graveyard of failed satellite phone companies, the physics of connecting to space, and what happens when you try to build hardware in public markets.

The journey ahead takes us from Venezuelan oil fields to Space Coast launch pads, from SPAC boardrooms to FCC hearings, from astronomical observatories worried about light pollution to emergency responders desperate for reliable communications. It's a story that touches on some of the biggest questions in technology: Can space-based infrastructure ever be economically viable? How do you fund moon-shot hardware companies? And ultimately—what happens to humanity when every person on Earth can connect from anywhere?

II. The Founder's Journey: From Venezuela to Space

Abel Avellan's path to revolutionizing global connectivity began in the oil fields of Venezuela, where communication wasn't just convenient—it was survival. Born in Caracas but educated as an engineer, Avellan witnessed firsthand how isolation could cripple operations and endanger lives. Oil rigs, cargo ships, remote facilities—they all needed to stay connected, yet traditional infrastructure couldn't reach them.

In the 1990s, while working for Swedish telecom giant Ericsson, Avellan saw an opportunity others missed. Satellite capacity was expensive and clunky, but demand from maritime and energy sectors was exploding. Ships needed internet. Oil platforms required constant data links. Remote operations demanded reliable communications. The infrastructure didn't exist, but the customers were desperate and willing to pay. In 2000, Avellan made his move. He founded Emerging Markets Communications (EMC), targeting exactly these underserved markets. The timing was perfect—the dot-com bubble had burst, satellite capacity was cheap, and established players were retreating. While others saw disaster, Avellan saw opportunity.

EMC grew explosively. Under Avellan's management, the company was ranked for several years as the fastest growing satellite service provider in the world and became a global leading provider of mission-critical content and connectivity for the main mobility and hard-to-reach markets. The numbers told the story: EMC served more than 200 customers in over 140 countries and delivered connectivity and content services to all key maritime markets, including cruise lines and ferries, yachts, commercial shipping and energy.

What made EMC different wasn't just the technology—it was Avellan's obsession with solving real problems for real customers. Ships didn't just need bandwidth; they needed reliability in storms. Oil platforms didn't just want internet; they required mission-critical communications that could mean life or death. Avellan built EMC to deliver both, creating infrastructure with 20+ patented technologies and establishing 52 global field support centers operating in 140 countries.

The maritime industry became EMC's cash cow. Cruise ships wanted to offer passengers internet. Cargo vessels needed real-time logistics. Offshore drilling platforms required constant headquarters contact. By 2016, EMC was projected to reach $190-200 million in revenue and $55-65 million in Adjusted EBITDA. The company had become indispensable infrastructure for global shipping.

Then came the exit that would fund Avellan's next venture. In July 2016, EMC was sold for $550 million to Global Eagle Entertainment, with ABRY Partners taking a major position. The sale validated Avellan's thesis: connectivity in hard-to-reach places was valuable enough that acquirers would pay premium multiples. But for Avellan, the EMC exit wasn't an ending—it was seed capital for something far more ambitious.

During his EMC years, Avellan had noticed something troubling. Despite all the satellite capacity he managed, despite all the technology advances, one problem remained unsolved: regular people couldn't access satellite communications. You needed special equipment—satellite phones that cost thousands, terminals the size of pizzas, installations that required technicians. The infrastructure existed, but it was inaccessible to billions.

The insight that would become AST SpaceMobile crystallized during Avellan's final years at EMC. What if, instead of bringing special equipment to people, you could modify the satellites themselves? What if you could build an antenna so large, so powerful, that it could connect directly to the phone already in someone's pocket? The physics were daunting. The capital requirements seemed impossible. The regulatory hurdles appeared insurmountable.

But Avellan had spent two decades proving that "impossible" was just another engineering problem. With over 25 years in the space industry and 24 U.S. patents to his name, he understood both the technical challenges and market opportunity better than perhaps anyone alive. The $550 million from EMC's sale would provide the initial capital. The relationships with carriers, built over decades, would open doors. The technical expertise, accumulated through thousands of installations, would guide development.

In 2017, less than a year after the EMC sale, Avellan incorporated a new company: AST & Science. The name was deliberately modest, almost academic. But the vision was anything but: to build a constellation of satellites with massive phased-array antennas that could turn space itself into a cell tower, connecting every smartphone on Earth without modification. The journey from Venezuelan oil fields to space-based cellular networks was about to begin its most audacious chapter.

III. Genesis: AST & Science and the Original Vision (2017–2019)

May 2017. A nondescript office in Miami. Abel Avellan sits across from his first potential investors, explaining something that sounds like pure fantasy: satellites that can connect directly to the phone in their pocket. No special equipment. No modifications. Just space talking to smartphones. The investors look skeptical. Satellite phones already exist—clunky $3,000 bricks that barely work indoors. Why would this be different?

AST SpaceMobile was founded in May 2017 by Abel Avellan as AST & Science LLC. The name was deliberately understated—"AST" standing for "Advanced Science and Technology"—almost academic in its blandness. But the technology Avellan described was anything but bland. He envisioned massive phased-array antennas, hundreds of square feet in size, unfolding in space like origami. These weren't traditional satellites; they were space-based cell towers, powerful enough to reach standard phones 500 miles below.

The technical breakthrough came from a simple insight with complex implications. Traditional satellite phones required powerful transmitters because their satellites were small. But what if you reversed the equation? What if you made the satellite enormous—with an antenna array larger than a basketball court—so the phone could remain small? The physics worked, at least on paper. The engineering would be unprecedented.

Avellan's credibility from the EMC exit opened doors that would have remained shut for most founders. He wasn't asking investors to bet on an unproven entrepreneur; he was offering them a chance to back someone who had already built and sold satellite infrastructure. By leveraging his personal capital from the EMC sale and his industry relationships, Avellan raised approximately $121 million before any major institutional rounds—a war chest that would fund the critical early development.

The company's first strategic move was securing manufacturing capability. AST & Science purchased a controlling interest in NanoAvionics, a Lithuanian satellite manufacturing company, on March 6, 2018. This wasn't just an acquisition; it was vertical integration from day one. NanoAvionics brought proven satellite bus technology, existing relationships with launch providers, and most importantly, a team that had actually built and launched satellites. All the key executives and management team of NanoAvionics will remain unchanged under the leadership of CEO Vytenis Buzas and CCO Linas Sargautis, both founders of the company. Abel Avellan, chairman and CEO of AST & Science, will become chairman of the board of NanoAvionics.

The NanoAvionics deal revealed Avellan's strategy: move fast, control the supply chain, and test in space as quickly as possible. While competitors spent years in terrestrial testing, AST would launch actual satellites to prove the concept. "The flexibility of the proven M6P bus and the close collaboration with our associates at NanoAvionics will enable us to design, build, integrate, launch and test a multitude of experimental payloads in orbit within six months or less," said Avellan. "This is unprecedented in the satellite industry."

By early 2019, the company had launched BlueWalker 1, built by NanoAvionics—a small test satellite that validated basic communication protocols. It wasn't meant to connect to phones; it was meant to prove AST could build, launch, and operate satellites. The real test would come later, but BlueWalker 1 showed the company could execute in space, not just in PowerPoint presentations.

Then came the moment that transformed AST from startup to serious contender. In March 2020, AST & Science LLC announced a Series B investment round, led by Vodafone and Rakuten, that raised $110 million for the company. Samsung Next, American Tower, and Cisneros also participated. This wasn't venture capital betting on a moonshot—these were strategic investors who understood telecommunications infrastructure. Vodafone brought 300 million subscribers across Europe and Africa. Rakuten controlled Japan's mobile market. American Tower owned cell tower infrastructure globally.

The strategic investors weren't just providing capital; they were essentially pre-committing to become customers. Vodafone's investment came with agreements to test the technology on their networks. Rakuten offered spectrum and regulatory expertise in Asia. These partnerships solved the chicken-and-egg problem that kills most infrastructure startups: how do you build a network without customers, and how do you get customers without a network?

The $110 million Series B valued the company at approximately $800 million—impressive for a pre-revenue company with one tiny test satellite. But the investors weren't buying current reality; they were buying future possibility. The physics worked. The partnerships were real. The team had done this before. All that remained was execution.

Behind the scenes, AST's engineers were tackling problems that had never been solved. How do you unfold a 700-square-foot antenna in space without it tearing itself apart? How do you maintain precise positioning when your satellite is essentially a giant solar sail catching every particle of solar wind? How do you cool electronics in the vacuum of space when your antenna array blocks traditional radiators? Each solution spawned new patents—Avellan would eventually be named on 24 U.S. patents, building an intellectual property moat around the technology.

The company also began building out its ground infrastructure, establishing gateway facilities that would route calls from space to terrestrial networks. This wasn't just about the satellites; it was about creating an entire parallel telecommunications infrastructure that could seamlessly integrate with existing carrier networks. Every major decision reflected the wholesale strategy: AST wouldn't compete with carriers; it would enable them to offer truly universal coverage.

By late 2020, AST & Science had momentum, technology, and strategic backing. The company had raised over $230 million, secured partnerships with carriers representing nearly a billion subscribers, and successfully tested core technologies in space. But to achieve the vision of connecting every phone on Earth, they would need something more: massive capital, public market access, and a way to fund the construction of hundreds of satellites. The answer would come from an unlikely source: the SPAC boom that was about to sweep Wall Street.

IV. The SPAC Era: Going Public in the Space Gold Rush (2020–2021)

December 15, 2020. The Nasdaq MarketSite in Times Square. While most of America focused on vaccine rollouts and stimulus packages, a different kind of announcement rippled through financial markets. New Providence Acquisition Corp., a special-purpose acquisition company led by telecom veterans, announced it would take AST & Science public in a deal valuing the company at $1.8 billion. The space SPAC gold rush had found its next candidate.

The timing was perfect—or perfectly crazy, depending on your perspective. SPACs were having their moment, with blank-check companies raising $83 billion in 2020 alone. Virgin Galactic had shown the path, going public via SPAC in 2019 and seeing its stock soar. Every space company with a PowerPoint deck was suddenly talking to SPAC sponsors. But AST was different: it had real technology, major partnerships, and a founder putting his own money on the line.

New Providence had raised $462 million through an initial public offering (IPO) and a private investment in public equity (PIPE) to fully fund the development and first phase of its satellite constellation. The PIPE investors read like a who's who of strategic and financial players: Vodafone doubled down, American Tower increased its stake, and new investors including UBS O'Connor and Avellan himself participated. This wasn't speculative retail money; these were sophisticated investors who had done the diligence.

The SPAC structure offered AST something a traditional IPO couldn't: speed and certainty. A traditional IPO would have taken 12-18 months, required profitable operations or at least revenue, and subjected the company to market volatility during the roadshow. The SPAC merger could close in four months with guaranteed capital. For a capital-intensive hardware company racing to deploy satellites, time was everything.

But the real story was in the deal's structure and what it revealed about Avellan's control. Through a dual-class share structure, Avellan would retain 88% voting control despite owning 51% of the economic interest. He was essentially taking the company public while maintaining founder control—a structure more common in tech than in aerospace. The message was clear: this was Avellan's vision, and public shareholders were along for the ride, not driving the bus.

The investor presentation that accompanied the announcement was audacious in its projections. AST forecasted $16 billion in revenue by 2030, with 90% EBITDA margins once the constellation was operational. The company claimed a total addressable market of $1 trillion. Skeptics noted these projections assumed perfect execution, rapid customer adoption, and no meaningful competition. But believers pointed to the strategic investor commitments: carriers representing 1.8 billion subscribers had already signed preliminary agreements.

The deal's valuation implied enormous faith in future execution. At $1.8 billion, investors were valuing the company at approximately $1,000 per potential connected subscriber, based on the carrier agreements. Traditional telecom companies traded at $200-300 per subscriber. The premium reflected either the transformative nature of the technology or the frothy SPAC market—likely both.

April 2021 brought the closing. AST SpaceMobile began trading on the Nasdaq under the symbol "ASTS." The first day saw volatile trading, with the stock swinging between $8.50 and $12.50 before closing at $10.85. For a company that had existed for less than four years and had yet to generate meaningful revenue, it was now worth nearly $2 billion on paper.

The public listing brought new challenges. Quarterly earnings calls meant explaining complex satellite technology to analysts focused on near-term metrics. Retail investors, drawn by the space story and Reddit hype, created volatility that had nothing to do with business fundamentals. Short sellers began circling, questioning whether the technology could work and if the economics made sense.

But going public also brought advantages beyond capital. The public currency allowed AST to attract talent with stock options. The transparency requirements forced operational discipline. The quarterly reporting created accountability milestones. And perhaps most importantly, being public made AST "real" in a way that helped with regulatory approvals and customer negotiations.

The SPAC proceeds would fund the construction and launch of BlueWalker 3, the prototype that would make or break the company. At 693 square feet, its antenna would be the largest commercial communications array ever deployed in low Earth orbit. If it worked—if it could actually connect to unmodified phones—it would validate the entire business model. If it failed, AST would join the graveyard of space companies that promised more than they could deliver.

Behind the financial engineering, the real work continued. Engineers in Texas were solving problems like how to package a gymnasium-sized antenna into a rocket fairing. Supply chain teams were sourcing specialized components that had never been manufactured at scale. Regulatory lawyers were navigating the maze of international spectrum rights. The SPAC had provided the capital, but capital alone wouldn't put satellites in space.

The public market debut also intensified competitive dynamics. SpaceX and T-Mobile began discussing their own direct-to-cell service. Amazon's Kuiper project lurked in the background with unlimited capital. Apple started investing in satellite technology through Globalstar. The race to connect phones from space had officially begun, and AST's early lead was no longer a secret.

As 2021 progressed, AST's stock became a proxy for investor sentiment about space companies. When Virgin Galactic's stock soared on tourism hype, ASTS followed. When a Chinese rocket's uncontrolled reentry sparked fears about space debris, all space stocks sold off. The company's actual progress—supplier agreements, regulatory filings, engineering milestones—seemed secondary to macro sentiment about SPACs and space.

Yet through the volatility, one thing remained constant: the satellites were being built. In AST's Midland facility, BlueWalker 3 was taking shape—a massive array of components that would soon attempt something never done before. The SPAC era had given AST the capital and platform it needed. Now came the hard part: proving the impossible was actually possible.

V. BlueWalker 3: The Prototype That Shocked the World (2021–2023)

The clean room in Midland, Texas, looked more like an aircraft hangar than a satellite facility. Engineers in white bunny suits moved around a structure that defied every convention of satellite design. BlueWalker 3 wasn't just big—it was absurdly, impossibly big. Folded up, it would barely fit in a SpaceX Falcon 9 fairing. Unfolded, it would span 693 square feet, larger than a racquetball court. The engineers had a running joke: they weren't building a satellite with an antenna; they were building an antenna that happened to be a satellite.

The technical challenges were staggering. Traditional satellites were rigid structures designed to minimize moving parts—every hinge, every deployment mechanism was a potential point of failure. BlueWalker 3 had hundreds of potential failure points. The antenna array had to unfold in a precise sequence, with each panel locked into exact position. A single stuck mechanism would render the entire satellite useless. The deployment would happen 300 miles above Earth, with no possibility of repair.

The physics were equally daunting. The massive array would act like a solar sail, catching pressure from sunlight and particles from Earth's magnetic field. The satellite would need constant attitude adjustment to maintain position. The thermal management was nightmarish—one side would face the sun at 250°F while the other faced the cold of space at -250°F. The electronics had to work across this 500-degree temperature differential.

It successfully launched on September 10, 2022, on a SpaceX Falcon 9 Block 5 rocket from Kennedy Space Center Launch Complex 39A. The launch was flawless, but that was the easy part. SpaceX had mastered putting things in orbit. The question was whether AST had mastered what happened next.

For two months, the world waited. AST's engineers worked through commissioning sequences, checking every system, every sensor, every communication link. The satellite was healthy, but the real test—the unfolding—loomed. The company's stock price gyrated with every update, every rumor, every delayed announcement. Short sellers predicted failure. Believers held their breath.

The 693-square-foot (64 m2) antenna array of BlueWalker 3 was successfully unfolded to full deployment on November 10, 2022. The announcement came via a simple tweet from Avellan: "The bird has spread its wings." But the implications were anything but simple. AST had just deployed the largest commercial communications array ever put in orbit. The engineering had worked. The impossible had become possible.

Then came the unintended consequence that nobody at AST had fully anticipated. Astronomers around the world began reporting a new object in the night sky, sometimes as bright as the brightest stars. BlueWalker 3, with its massive reflective array, had become one of the brightest objects in orbit. The International Astronomical Union issued concerned statements. Reddit threads exploded with amateur astronomers complaining about ruined observations. AST had solved the engineering challenge but created a public relations nightmare.

The brightness issue revealed a fundamental tension in the new space economy. Companies like AST were democratizing access to space-based services, but at what cost to scientific observation and the night sky? The company scrambled to respond, promising to work with astronomers on future designs to minimize reflection. But the damage to AST's reputation in the scientific community was done. They were now the company that had "polluted" the night sky.

But if astronomers were unhappy, the telecommunications world was electrified by what came next. On April 25, 2023, AST SpaceMobile made the world's first space-based two-way telephone call with unmodified smartphones (a Samsung Galaxy S22 and an Apple iPhone) using the BlueWalker 3 satellite. This initial call was made from Midland, Texas to Japan using an AT&T 2G cellular frequency spectrum.

The call quality was crystal clear. Engineers who had worked for years on the project broke into tears. Avellan, typically reserved, allowed himself a smile. They had done it. A regular, unmodified smartphone had connected to a satellite in space and completed a normal phone call. No special equipment. No apps. No modifications. Just physics and engineering converging to achieve the impossible.

The successful call triggered a cascade of tests. The company also made the first 4G and 5G connectivity from a satellite in space directly to unmodified smartphones using the prototype satellite, achieving download rates as high as 21 Mbit/s. These weren't just voice calls anymore; this was real broadband from space. Engineers successfully streamed video, conducted video calls, and ran standard speed tests—all through regular phones connecting to a satellite traveling at 17,000 miles per hour.

The market reaction was swift and dramatic. ASTS stock jumped 40% in after-hours trading following the announcement. Analysts upgraded ratings. Competitors scrambled to explain why their approaches were still superior. But the proof was undeniable: AST had demonstrated the core technology worked. The question was no longer "if" but "when" and "how profitably."

The tests continued through 2023, each one pushing boundaries. Engineers tested handoffs between satellite passes, connectivity in different weather conditions, and performance in urban versus rural environments. They discovered unexpected challenges: urban areas with tall buildings created "canyon" effects that blocked signals, rain attention was higher than modeled, and the Doppler shift from the satellite's movement required constant frequency adjustment.

But they also discovered unexpected advantages. The satellite's height gave it a coverage area of over 300,000 square miles—roughly the size of Texas and Oklahoma combined. A constellation of just 90 satellites could provide continuous coverage to the entire United States. The economics suddenly looked more favorable than anyone had projected.

The BlueWalker 3 success also triggered a regulatory scramble. The FCC had approved experimental testing, but commercial operation would require new frameworks. How would spectrum sharing work? Who had priority—terrestrial or satellite signals? How would emergency services be handled? Every successful test created new regulatory questions that had never been asked because the technology had never existed.

Competitors took notice. Within months of AST's successful test, SpaceX announced an acceleration of its direct-to-cell partnership with T-Mobile. Amazon quietly filed patents for similar technology. Apple increased its investment in Globalstar. The success of BlueWalker 3 hadn't just validated AST's approach; it had fired the starting gun on a new space race.

As 2023 drew to a close, BlueWalker 3 continued to orbit, a 693-square-foot testament to engineering audacity. It had proven the technology worked, validated the business model, and triggered a competitive frenzy. But it was still just a prototype. The real challenge lay ahead: building and launching commercial satellites that could deliver actual service to actual customers. The prototype had shocked the world. Now AST had to deliver on the promise.

VI. Commercial Launch: BlueBird Satellites and the Path to Revenue (2024–Present)

The Midland, Texas manufacturing facility hummed with an energy that bordered on frantic. It was January 2024, and AST SpaceMobile's 185,000-square-foot complex had transformed into what employees called "the factory of impossible deadlines." Five BlueBird satellites—each the size of a small apartment when folded—were being assembled simultaneously. Engineers worked 24-hour shifts. Supply chain managers slept in their offices. The pressure was crushing: after years of promises, AST had to deliver commercial satellites or risk becoming another space industry cautionary tale.

The manufacturing challenges were unlike anything in traditional aerospace. The BlueBird 1-5 satellites — built by AST SpaceMobile in the company's 185,000 square feet of assembly, integration, and testing space in Midland, Texas — will be the largest commercial communications arrays in low Earth orbit. Each satellite required precision assembly of thousands of components, many custom-designed and sole-sourced. A single failed part could delay the entire constellation.

The financial pressure was equally intense. AST's stock had cratered to $1.97 per share on April 2, 2024—a 90% decline from its SPAC heights. Short sellers circled like vultures, betting the company would run out of cash before achieving commercial deployment. The narrative was brutal: another space SPAC heading to zero, another founder's impossible dream meeting reality.

Then came the strategic lifeline that changed everything. During 2024, AST SpaceMobile has secured additional strategic investments from AT&T, Verizon, Google and Vodafone. These weren't just investments; they were votes of confidence from the world's largest technology and telecom companies. Verizon committed $100 million. AT&T increased its stake. Google—which rarely invested in hardware companies—took a position. The message was clear: the incumbents believed AST's technology worked.

The manufacturing process itself was a marvel of vertical integration. AST SpaceMobile has more than 3,400 patents and patent-pending claims for its technology and operates state-of-the-art, vertically integrated manufacturing and testing facilities in Midland, Texas, which collectively span 185,000 square feet. Unlike traditional satellite manufacturers who outsourced components globally, AST controlled nearly every aspect of production. This gave them speed and flexibility but also meant every problem was their problem to solve.

By July 2024, the satellites were complete but the drama was far from over. That milestone, which means the satellites have completed the manufacturing, assembly and environmental testing phase, sets the stage for a seven-day launch window in September for the company's first handful of Bluebirds. Each satellite weighed 3,300 pounds and contained an antenna array that would unfold to 693 square feet—the same size as BlueWalker 3 but with ten times the processing power.

The market began to sense something had shifted. From its April lows, ASTS stock began a relentless climb. By August, speculation about the September launch had driven shares up 500%. Then came the confirmation that sent the stock parabolic: On August 21, 2024, after the company confirmed its first commercial satellite launch in early September, AST SpaceMobile stock price jumped to $38.60 per share, or around 1,800% compared to record lows of $1.97 per share on April 2, 2024.

The mathematics of the move were staggering. In less than five months, AST's market capitalization had grown from $400 million to over $8 billion. Retail investors who had held through the pain were suddenly sitting on life-changing gains. The r/ASTSpaceMobile subreddit exploded with celebration and disbelief. Short sellers covered in panic, further fueling the rally.

September 12, 2024, 4:52 AM EDT. Cape Canaveral, Florida. On September 12th at 4:52 am EDT, the BlueBird 1-5 mission lifted off from Cape Canaveral, Florida, and delivered the five largest-ever commercial communications arrays into low Earth orbit. The groundbreaking launch started at 4:52 a.m. EDT from Cape Canaveral, Florida. The event was witnessed by partners and retail shareholders from around the globe who had gathered to be a part of this historic milestone.

The scene at Cape Canaveral was unlike any commercial satellite launch in history. Hundreds of AST SpaceMobile's retail investors attended the mission's launch from Cape Canaveral, Florida. These weren't institutional investors in suits; they were teachers, engineers, retail workers—people who had bet their savings on Avellan's vision. As the Falcon 9 lifted off, many wept openly. This wasn't just a satellite launch; it was vindication for everyone who had believed when the world said it was impossible.

The deployment sequence began weeks later. On October 4, 2024, Avellan announced the first of the mission's Block 1 satellites had unfolded "ahead of schedule." By October 25, the company stated all five satellites had completely unfolded. Each unfolding was a moment of terror and triumph—693 square feet of antenna array deploying in the silence of space, transforming from a compact package into a massive communications platform.

With five commercial satellites operational, AST could finally begin the transition from technology demonstrator to service provider. These first five satellites are built on the success of our in-orbit BlueWalker 3 satellite and will provide U.S. nationwide non-continuous service with over 5,600 cells in premium low-band spectrum, with a planned 10-fold increase in processing bandwidth. Non-continuous meant gaps in coverage—a satellite would pass overhead, provide service for minutes, then move on. But it was real, commercial service.

The strategic partnerships crystallized into commercial reality. AT&T and Verizon together will share with AST SpaceMobile a portion of their respective bands of 850 MHz low-band spectrum to enable nationwide satellite coverage. This spectrum sharing agreement was unprecedented—competitors collaborating to enable a new form of connectivity. The 850 MHz band was particularly valuable, offering superior building penetration and range compared to higher frequencies.

But even as AST celebrated its BlueBird success, the company was already looking ahead. On November 14, 2024, AST SpaceMobile announced a launch campaign for its next-generation Block 2 BlueBird satellites. These wouldn't just be larger—at 2,400 square feet, they would be 3.5 times the size of the current BlueBirds. Each Block 2 satellite would have the capacity to serve millions of users simultaneously, transforming the economics of space-based cellular.

The capital requirements remained daunting. The cost to build and deploy each Block 2 BlueBird satellite has increased to $19-21 million from $16-18 million due to recent launch costs. With plans for 60 to 90 satellites in the full constellation, AST needed billions more in funding. But now they had something they'd never had before: proven technology, operational satellites, and the world's largest carriers as committed partners.

The transformation from manufacturing hell to market darling revealed a fundamental truth about space companies: success required not just technical achievement but perfect timing, strategic partnerships, and enough capital to survive the valley of death between prototype and profit. AST had navigated that valley, but the hardest climb still lay ahead. The BlueBirds were flying, but could they build a business that could sustain itself? The path to revenue had begun, but the destination remained distant.

VII. The Business Model: Wholesale Revolution or Pipe Dream?

The conference room at AT&T's Dallas headquarters, February 2024. Network executives are running the numbers for the tenth time, and they still can't quite believe what they're seeing. In exchange for a 50/50 revenue split, the MNOs promote the service to their subscribers, manage billing, customer service, and network integration and benefit from incremental revenue and a more reliable network to reduce customer churn. No infrastructure investment. No tower construction. No maintenance. Just pure margin expansion by reselling satellite capacity as premium coverage.

This is the genius—or the delusion—at the heart of AST SpaceMobile's business model. Unlike traditional telecom infrastructure plays that require carriers to invest billions in equipment, AST asks for nothing upfront except spectrum sharing and customer access. The carriers keep doing what they do best: managing subscribers, handling billing, providing customer service. AST does what no carrier wants to do: launch satellites, manage space operations, and handle the complexities of orbital mechanics.

For AST, this wholesale model should simplify its business plan, accelerate user adoption, and facilitate a scalable, high margin business. No consumer marketing. No retail stores. No customer support call centers. Just wholesale capacity sold to carriers who mark it up and sell it to their subscribers. It's the same model that made tower companies like American Tower worth $100 billion—own the infrastructure, let others handle the customers.

The economics, on paper at least, are compelling. Wholesale Model: Revenue relies on securing large-scale, long-term capacity agreements with major MNOs worldwide. A single Block 2 BlueBird satellite, costing $19-21 million to build and launch, could theoretically serve millions of users. At just $1 per month per user—a fraction of what carriers charge for international roaming—a satellite serving 2 million users generates $24 million annually. The payback period: less than a year. The remaining satellite life: 5-7 years of nearly pure profit.

But the "on paper" caveat is doing heavy lifting. High Upfront Capital Expenditure: Significant investment is required for satellite design, manufacturing, launch, and ground infrastructure. AST needs to spend billions before seeing meaningful revenue. Each satellite requires not just construction and launch costs but also ground stations, gateway facilities, and integration with terrestrial networks. The company must build the entire constellation before achieving continuous coverage—imagine building a cellular network where you can't charge customers until every tower is operational.

The carrier partnerships reveal both the promise and the precarity of the model. Currently AST has preliminary agreements and/ or memorandums of understanding with more than 48 mobile network operators with over 2.8 billion unique subscribers. But "preliminary agreements" and "memorandums of understanding" aren't contracts. They're expressions of interest, options for the future, hedges against competitive disadvantage. Until AST demonstrates continuous commercial service, carriers won't commit to firm, long-term contracts.

AST also has strategic commitments and/or investments in the form of convertible debt and prepaid revenue from AT&T, Google, Verizon, and Vodafone. AT&T is the first MNO to complete a definitive commercial agreement with AST and several additional operators are expected to sign on in the coming months. This is more substantial—actual money changing hands, real commercial terms being negotiated. But even here, the commitments are largely contingent on successful deployment and service quality metrics.

The dual-use strategy adds another revenue stream. AST SpaceMobile started generating revenue through a U.S. Government contract in 2024. The same satellites that connect consumer phones can provide secure communications for military operations, emergency response, and intelligence gathering. Government contracts offer higher margins and longer terms than commercial agreements, providing ballast during the risky early deployment phase.

Gateway equipment bookings from MNO partners of $13.6M in Q1 2025, with expected gateway equipment bookings of approximately $10.0 million, on average, per quarter during 2025, as a precursor to the rollout of SpaceMobile Service These gateway sales represent an clever interim monetization strategy—selling carriers the ground equipment they'll need to connect to AST's satellites. It generates cash flow before satellite services launch while deepening carrier commitment to the platform.

The competitive dynamics complicate the wholesale model. SpaceX's Starlink has partnered with T-Mobile for direct-to-cell service, but their approach differs fundamentally. Starlink modifies existing satellites designed for fixed broadband, limiting capability to text and basic data. AST purpose-built satellites for mobile connectivity, enabling full voice and broadband. But Starlink has SpaceX's launch capabilities and Musk's unlimited capital. The race isn't just technological; it's financial.

The spectrum puzzle adds another layer of complexity. These satellites establish communication links directly with standard mobile devices using cellular spectrum licensed by partner MNOs. AST doesn't own spectrum; it borrows it from carrier partners. This creates an elegant solution to a regulatory nightmare—no need for AST to acquire billions of dollars in spectrum licenses. But it also creates dependence. If carriers withdraw spectrum access, AST's satellites become expensive space junk.

The path to profitability requires precise execution of multiple variables. Management reaffirmed on the call that ASTS expects to become FCF+ with ~25 operational satellites, as revenue from government contracts, MNO agreements, and infrastructure sales (gateways) begins to scale. Twenty-five satellites for cash flow breakeven—a number that seems tantalizingly close with five already in orbit and 60 more planned. But each satellite must work perfectly, carriers must market aggressively, and customers must actually subscribe.

The wholesale model's ultimate test isn't technical or financial—it's behavioral. Will carriers actively promote a service that highlights their coverage gaps? Will customers pay extra for coverage they might never use? Will the economics work when actual usage patterns emerge? The mobile industry is littered with technically superior solutions that failed commercially. AST's wholesale model is elegant in theory, but theory and reality often diverge in telecom.

However, the company does not expect to begin generating substantial revenue through mobile network operators like AT&T and Verizon until the company's BlueBird 1-5 satellites are fully operational. The waiting game continues. The satellites are flying, the partnerships are signed, the technology is proven. But until continuous commercial service launches and subscribers start paying, AST's revolutionary wholesale model remains an expensive experiment in space-based economics.

VIII. Technical Deep Dive: How Do You Connect a Phone to Space?

The cleanroom air tastes metallic, sterile. An engineer holds a smartphone—an ordinary iPhone 14, nothing special—and dials a number. The signal leaves the phone at 200 milliwatts, barely enough power to light an LED. It must travel 500 miles straight up, through the troposphere, stratosphere, and into the vacuum of space, to reach a satellite moving at 17,000 miles per hour. The fact that this works at all violates every intuition about how phones communicate.

To understand the audacity of AST's technical achievement, start with the physics problem. A typical cell tower transmits at 20-40 watts and reaches phones 1-2 miles away. AST's satellites transmit similar power but must reach phones 500 miles away. By the inverse square law, signal strength decreases with the square of distance. The path loss from satellite to phone is approximately 170 decibels—that's the signal getting 100 million billion times weaker. It's like trying to hear someone whisper from across the Atlantic Ocean.

The solution begins with size. Our planned satellites are designed to have a large surface area of phased-array antennas, which work together to electronically form, steer, and shape wireless communication beams into cells of coverage – just like the kind that cell towers and other cell sites provide. The 693-square-foot arrays on the BlueBird satellites aren't just big; they're precisely engineered surfaces containing thousands of individual antenna elements, each capable of transmitting and receiving independently.

The phased array technology is what makes the impossible possible. In a phased array, the power from the transmitter is fed to the radiating elements through devices called phase shifters, controlled by a computer system, which can alter the phase or signal delay electronically, thus steering the beam of radio waves to a different direction. Think of it like thousands of people in a stadium doing "the wave"—by controlling the timing of when each person stands, you can make the wave move in any direction. AST's satellites do this with radio waves, creating focused beams that can track individual phones on Earth.

But focusing the beam is only half the battle. The satellites are moving at 17,000 mph, creating massive Doppler shift. You also have to take into account environmental losses such as noise, compensate for signal delay, and adjust for Doppler effect, which is the shift in radio waves as something moves closer or further away – like when a siren passes you in the street. A phone that appears at one frequency when the satellite approaches will shift to a completely different frequency as it passes overhead. AST's systems must continuously adjust for this shift, recalibrating thousands of times per second.

The uplink challenge—getting the weak signal from phone to satellite—is even more daunting. The most daunting challenge lies in achieving indoor-grade cellular uplink at frequencies as low as 600 MHz from devices never intended to communicate with satellites. For satellites at an altitude of 350 km, the free-space path loss alone at 600 MHz is approximately 133 dB. When combined with clutter, penetration, and polarization mismatches, the system must close a link budget approaching 153–160 dB, from a smartphone transmitting just 23 dBm (200 mW) or less.

This is where AST's massive arrays become crucial. With an area of more than 64 square metres, a BlueBird is also sensitive enough to pick up relatively weak mobile signals from hundreds of kilometres away. The array acts like a giant ear in space, collecting every photon of radio energy from the phone's transmission. Advanced signal processing then extracts the phone's signal from the noise—like picking out a single conversation in a crowded stadium.

The ground infrastructure is equally sophisticated. Signals are then relayed between the user's phone, the satellite, and terrestrial gateway facilities owned or leased by AST SpaceMobile. These gateways interconnect with the core networks of partner MNOs, enabling seamless service integration for the end-user. The gateways must handle the complexity of routing calls through space while making it appear to the terrestrial network as if the phone is connected to a regular tower.

Spectrum sharing adds another layer of complexity. These satellites establish communication links directly with standard mobile devices using cellular spectrum licensed by partner MNOs. The satellites must coexist with terrestrial towers using the same frequencies. AST uses sophisticated algorithms to ensure satellite signals don't interfere with ground networks, dynamically adjusting power and beam patterns based on real-time conditions.

The thermal management alone would make most engineers quit. One side of the satellite faces the sun at 250°F while the other faces the cold of space at -250°F. The electronics must operate across this 500-degree differential. The massive arrays act as solar sails, creating torque that must be constantly countered. Every component must survive radiation, micrometeorite impacts, and the violence of launch.

Why did Iridium, Globalstar, and others fail where AST succeeds? They required special phones because their satellites were too small to close the link budget with regular devices. Iridium's satellites had antennas measured in feet, not football fields. They compensated with special handsets with larger antennas and more power, but consumers rejected carrying a second device. AST flipped the equation: make the satellite enormous so the phone can stay small.

The software challenge rivals the hardware. The satellites must simultaneously track potentially thousands of phones, each moving relative to the satellite, each requiring constant beam steering and frequency adjustment. The system must hand off calls between satellites as they pass overhead, maintain quality of service, and integrate seamlessly with terrestrial networks—all while the entire constellation orbits Earth every 90 minutes.

Even successful connections face unique challenges. The round-trip signal delay to Low Earth Orbit is about 10-15 milliseconds—noticeable but manageable. Weather affects signal propagation—rain attention can degrade performance. Urban canyons create multipath interference as signals bounce off buildings. Each problem requires algorithmic solutions running in real-time on the satellites.

The next generation Block 2 satellites push the boundaries further. This initiative aims to deploy up to 60 Block 2 BlueBird satellites, each equipped with a communication array spanning approximately 2,400 square feet (223 square meters). These satellites are designed to achieve data transmission speeds of up to 120 Mbps, enabling voice, data, and video communication capabilities for end users. At 2,400 square feet, they'll be able to support more users with higher data rates, finally delivering true broadband from space.

The achievement cannot be overstated. AST has solved problems that the entire telecommunications industry considered unsolvable. They've built flying cell towers that work with unmodified phones, creating infrastructure that exists entirely above Earth's surface. The physics are unforgiving, the engineering is unprecedented, but the proof is undeniable: a regular phone can now call space, and space can call back.

IX. Playbook: Lessons in Audacious Hardware Ventures

The boardroom at AST SpaceMobile, November 2023. The stock has just crashed 40% after another launch delay. Short sellers are circulating reports calling the company "uninvestable." Yet Abel Avellan sits calmly at the head of the table, reviewing plans for Block 2 satellites that will cost $20 million each. "We're not building for next quarter," he tells his team. "We're building for next decade." This moment encapsulates the AST playbook: founder control, long-term vision, and an almost religious belief in the mission.

The super-voting structure isn't just about control—it's about permission to be crazy. Through the dual-class share arrangement established during the SPAC merger, Avellan maintains 88% voting control despite owning 51% of economic interest. This isn't corporate governance best practice; it's corporate governance heresy. But for audacious hardware ventures, it might be necessary. Hardware requires multi-year development cycles, billions in capital, and the ability to survive multiple near-death experiences. Democratic decision-making would have killed AST five times over.

Consider the traditional venture capital model applied to AST: Year 1, impressive prototype. Year 2, delays and cost overruns, partners get nervous. Year 3, pivot to software or sell to incumbent. That's the pattern that kills most hardware startups. Avellan's control structure prevents this. When investors panicked about BlueWalker 3's delays, Avellan couldn't be forced to pivot. When the stock crashed to $1.97, he couldn't be pushed into a fire sale. The lesson: if you're doing something truly difficult, maintain control or watch your vision get watered down to nothing.

The strategic investor strategy reveals another key insight: get your customers to fund you. AST's investors aren't just providing capital; they're pre-committing to become customers. Vodafone, AT&T, Verizon, Rakuten—they're not betting on technology; they're buying insurance against competitive disadvantage. If space-based cellular works, they need access. If it fails, they've lost a rounding error on their balance sheets. For AST, these investments provide not just capital but validation, market access, and technical expertise.

This alignment goes deeper than money. When Vodafone invests, they also provide spectrum access, regulatory support, and technical integration resources. When AT&T signs on, they bring 100 million potential customers. Each strategic investor multiplies AST's capabilities beyond what pure financial investment could achieve. The playbook lesson: in infrastructure plays, strategic money is worth 10x financial money.

The SPAC as a funding mechanism for capital-intensive hardware deserves scrutiny. Traditional IPOs require profitability or at least a clear path to it. Venture capital wants 10x returns in 5-7 years. Private equity wants cash flow. SPACs offered something different: public market capital for pre-revenue companies with multi-year development horizons. The structure wasn't perfect—the volatility has been brutal—but it enabled AST to raise $462 million when no other path existed.

The SPAC also forced a different kind of discipline. Public companies must report quarterly, providing transparency that private companies avoid. For AST, this transparency became a weapon. Every successful test was publicly announced. Every partnership was press released. Every technical milestone became a stock catalyst. The company built in public, turning their development process into a multi-year marketing campaign.

Managing technical risk while being public creates unique challenges. When BlueWalker 3's deployment was delayed, the stock crashed. When it succeeded, the stock soared. This volatility would destroy most management teams. AST's approach: radical transparency about technical challenges while maintaining unwavering confidence in the ultimate vision. They admit problems but never doubt the mission. It's a delicate balance that few companies manage successfully.

The decision to build in the open versus stealth mode represents a philosophical choice. Stealth protects against competition but limits access to capital and partners. Building in public invites copying but creates momentum and accountability. AST chose radical openness: live-streaming launches, publishing technical papers, even acknowledging light pollution concerns. This openness attracted critics but also created a community of believers—retail investors who became evangelists, engineers who joined the mission, partners who signed on early.

The power of an impossible vision cannot be underestimated. If Avellan had pitched "slightly better satellite phones," nobody would have cared. But "connect every phone on Earth to space without modification"—that's a vision worth dedicating a career to. Impossible visions attract exceptional people willing to work for below-market compensation plus equity. They attract investors looking for transformational returns. They attract media coverage that no marketing budget could buy.

The patent strategy reveals sophisticated thinking about competitive moats. With over 3,400 patents and patent-pending claims, AST hasn't just protected their technology; they've made it legally dangerous to compete. Every approach to direct-to-cell communication potentially infringes AST patents. Competitors must either license AST technology, find completely novel approaches, or risk devastating litigation. In hardware, where copying is easier than innovating, intellectual property becomes existential.

The vertical integration decision—controlling manufacturing, launch integration, and ground systems—violates the modern gospel of focus and outsourcing. But for AST, vertical integration provides speed, quality control, and cost advantages. When suppliers failed to deliver components for BlueBird satellites, AST brought production in-house. When launch providers raised prices, AST multi-sourced across SpaceX, Blue Origin, and ISRO. Control of the full stack enables rapid iteration and problem-solving impossible with outsourced production.

The government revenue strategy provides crucial early cash flow. AST SpaceMobile started generating revenue through a U.S. Government contract in 2024. Military and intelligence agencies need secure satellite communications and will pay premium prices for early access. These contracts provide non-dilutive funding, validate the technology, and create a revenue floor during the risky deployment phase. The dual-use approach—commercial and government—diversifies risk and accelerates development.

Perhaps the most important lesson: timing matters more than technology. AST wasn't first to attempt satellite-to-phone communication. But they arrived when smartphones achieved ubiquity, when launch costs had fallen 90%, when phased array technology matured, when carriers faced coverage mandate pressure. The confluence of these factors created a window that didn't exist five years earlier and might close five years later. The playbook: don't just build breakthrough technology; build it when the world is ready to adopt it.

The AST playbook isn't universally applicable. Most companies shouldn't have super-voting shares. Most shouldn't attempt impossible missions. Most shouldn't build hardware in public markets. But for the rare company attempting something truly audacious—fusion power, quantum computing, space manufacturing—AST provides a template: maintain control, align strategic partners, embrace public accountability, protect intellectual property, vertically integrate critical capabilities, pursue dual-use strategies, and most importantly, make the vision so compelling that exceptional people will dedicate their careers to achieving it.

The playbook's ultimate test isn't whether AST succeeds—that story is still being written. It's whether their approach enables them to attempt something nobody else would dare try. By that measure, they've already succeeded. They've built satellites that shouldn't exist, achieved connections that shouldn't work, and created a company that shouldn't be possible. Whether that translates to commercial success remains uncertain. But they've proven that with the right structure, capital, and conviction, even the impossible becomes merely difficult.

X. Bear vs. Bull: Investment Analysis

The elevator at One Manhattan West accelerates toward the 60th floor, where a hedge fund's investment committee is about to debate AST SpaceMobile. In one corner: the bull analyst who sees a $100 billion opportunity. In the other: the bear who thinks it's worthless. Both have compelling cases. The stock has traded between $1.97 and $38.60 in a single year—the market clearly has no idea what this company is worth. Let's examine both sides of this cosmic wager.

The Bull Case: Monopoly in the Making

Start with the total addressable market: 2.8 billion mobile subscribers experience coverage gaps, another 3 billion remain completely unconnected. At just $5 per month per user—less than a single coffee—that's $250 billion in annual revenue opportunity. AST doesn't need to capture all of it. At 10% penetration among partner carriers' subscribers, we're talking about $15 billion in annual revenue. With satellite infrastructure economics, that could mean $13 billion in EBITDA once the constellation is deployed.

The competitive moat is widening daily. ASTS has over 3,500 patents protecting its technology, which sets a high bar for anyone trying to match their performance and services. SpaceX's Starlink direct-to-cell is limited to text messaging initially. Apple's Globalstar investment only enables emergency SOS. AST offers full broadband—voice, data, video—to unmodified phones. They're not just first; they're years ahead with technology that others may not be able to replicate without infringing patents.

The strategic investor validation is unprecedented. When AT&T, Verizon, Vodafone, Google, and Rakuten all invest in the same company, they're seeing something retail investors might miss. These aren't venture capitalists making scatter-shot bets; these are the companies that would be disrupted if AST fails. Their investment is both offensive and defensive—ensuring they have access to the technology while preventing competitors from exclusive deals.

AST extended its partnership with Vodafone for another ten years and entered into a joint venture (JV) with Vodafone in Europe to create a "jointly-owned European satellite service business to serve MNOs in European markets." This isn't just a commercial agreement; it's a deep strategic partnership that locks in European market access for a decade. Similar deals with AT&T and Verizon secure the North American market.

The unit economics are compelling once deployed. Each Block 2 satellite costs approximately $20 million to build and launch. With 2,400 square feet of antenna area and advanced processing, each satellite could theoretically serve millions of simultaneous users. At full utilization, the payback period could be months, not years. The remaining 5-7 year satellite life becomes nearly pure profit generation.

Government revenue provides a floor. On the government front, AST secured an additional contract with the U.S. Space Development Agency for $43mm of revenue to provide satellite services through a prime contractor. AST also signed a new contract with the Defense Innovation Unit for up to $20mm via a prime contractor. Military and intelligence applications for secure, global communications are enormous. This dual-use model means AST isn't entirely dependent on consumer adoption.

The technology has been definitively proven. This isn't theoretical anymore—real phones have made real calls through real satellites. The first five Block 1 BlueBird satellites, launched in September 2024, are now fully operational. These satellites successfully conducted video calls with AT&T, Verizon, and Vodafone, proving their ability to deliver broadband speeds for voice, text, and data services. The technical risk that terrified investors for years has been largely eliminated.

First-mover advantage in a winner-take-most market could be decisive. Carriers won't sign with multiple satellite providers for the same service. As AST locks in exclusive or semi-exclusive deals with major carriers, competitors lose addressable market. The company that achieves global coverage first might lock out competitors permanently.

The Bear Case: Physics Meets Reality

But let's inject some reality into this fantasy. As of the end of fiscal year 2024, AST SpaceMobile remained in the pre-commercialization phase for its primary space-based cellular broadband service. Reported revenue was minimal and derived mainly from specific engineering services or early government contracts, not the core business model. After seven years and over $1 billion invested, the company has essentially no revenue. This isn't a business; it's a science experiment.

The capital intensity is crushing. High Upfront Capital Expenditure: Significant investment is required for satellite design, manufacturing, launch, and ground infrastructure. AST needs approximately 90 satellites for global coverage. At $20 million each, that's $1.8 billion just for satellites, not including ground infrastructure, operations, or replacement satellites. They'll need to raise billions more in dilutive capital before achieving positive cash flow.

Competition from infinitely funded rivals is intensifying. SpaceX has already launched direct-to-cell satellites and has its own rockets, making their economics fundamentally better. Amazon's Project Kuiper has unlimited capital. Apple is investing billions in satellite capabilities. Chinese companies are developing similar technology without patent constraints. AST's first-mover advantage could evaporate quickly.

The regulatory pathway remains uncertain. As of November 2024, the FCC has not yet decided if AST SpaceMobile can operate in terrestrial cellular frequencies and enable the company to provide commercial satellite-to-cell services. Without full regulatory approval, the entire business model is at risk. International regulations are even more complex, with each country requiring separate approvals.

Customer adoption is completely unproven. Will consumers pay extra for coverage they rarely need? Rural customers who need the service most often have the least ability to pay. Urban customers who can afford it rarely lose coverage. The actual addressable market might be a fraction of the theoretical TAM.

The "agreements and understandings" with carriers aren't binding contracts. Currently AST has preliminary agreements and/ or memorandums of understanding with more than 48 mobile network operators with over 2.8 billion unique subscribers. These MOUs can be terminated, renegotiated, or simply ignored. Until AST has firm, long-term contracts with minimum revenue commitments, these partnerships are just press releases.

Technical challenges remain enormous. The satellites must work perfectly for years in the harsh environment of space. The light pollution issue has made AST enemies in the scientific community. Debris from a single satellite collision could destroy the entire constellation. One major technical failure could end the company.

The valuation assumes perfect execution. At current prices, the market is valuing AST at over $10 billion despite no meaningful revenue. This implies the constellation gets built on schedule, adoption meets projections, competition doesn't materialize, and regulations align favorably. The probability of all these factors aligning is low.

Valuation Framework: Between Zero and Infinity

So how do you value a pre-revenue space company? Traditional DCF models are useless when revenue is theoretical and costs are astronomical. Comparable company analysis fails because there are no true comparables. This requires scenario analysis:

Scenario 1: Complete Success (20% probability) - 90 satellites deployed by 2030 - 50 million paying subscribers at $10/month average - 80% EBITDA margins at scale - $6 billion annual revenue, $4.8 billion EBITDA - 15x EBITDA multiple = $72 billion valuation - Present value at 15% discount rate = $30 billion

Scenario 2: Partial Success (40% probability)

- 45 satellites deployed, regional coverage only

- 10 million subscribers at $8/month

- 60% EBITDA margins

- $960 million revenue, $576 million EBITDA

- 12x EBITDA multiple = $7 billion valuation

- Present value = $3 billion

Scenario 3: Struggle to Scale (30% probability) - 25 satellites deployed, limited service - 2 million subscribers at $5/month - Break-even operations - Acquired for $1 billion by strategic buyer

Scenario 4: Failure (10% probability) - Technical, regulatory, or competitive failure - Patents sold in bankruptcy - Recovery value = $200 million

Probability-weighted value = (0.2 × $30B) + (0.4 × $3B) + (0.3 × $1B) + (0.1 × $0.2B) = $7.5 billion

This suggests the current $10+ billion valuation prices in more success than the probabilities warrant. But these probabilities are highly subjective. Bulls would argue the success probability is higher given proven technology. Bears would argue failure probability is higher given capital requirements.

The Path Forward

Management reaffirmed on the call that ASTS expects to become FCF+ with ~25 operational satellites, as revenue from government contracts, MNO agreements, and infrastructure sales (gateways) begins to scale. This is the key milestone. If AST can achieve cash flow breakeven with 25 satellites, the existential risk disappears. They can fund remaining deployment from operations, eliminating dilution risk.

The next 12-18 months will determine AST's fate. Either they launch Block 2 satellites, sign firm commercial agreements, and begin generating meaningful revenue, or they join the graveyard of ambitious space companies that promised more than they could deliver. For investors, this is a binary bet on humanity's need for ubiquitous connectivity. The bears see expensive infrastructure that nobody will pay for. The bulls see essential infrastructure that everybody will pay for. Both could be right—just at different times.

XI. Epilogue: The Future of Ubiquitous Connectivity

Standing in the Sahara Desert, 200 miles from the nearest city, a Tuareg nomad pulls out his Samsung phone and video calls his daughter studying in Paris. In the Amazon rainforest, an indigenous leader documents illegal logging and uploads the evidence in real-time. On a cargo ship in the middle of the Pacific, a engineer troubleshoots machinery with headquarters via augmented reality. These scenes, impossible just years ago, represent the world AST SpaceMobile is building—where geography no longer determines access to the global conversation.

On November 14, 2024, AST SpaceMobile announced a launch campaign for its next-generation Block 2 BlueBird satellites. The company revealed plans to utilize multiple launch providers, including Blue Origin's forthcoming New Glenn rocket, SpaceX's launch vehicles, and those operated by the Indian Space Research Organization (ISRO). This initiative aims to deploy up to 60 Block 2 BlueBird satellites, each equipped with a communication array spanning approximately 2,400 square feet (223 square meters).

The scale of this ambition defies comprehension. Sixty satellites, each the size of a basketball court, creating an invisible infrastructure layer surrounding Earth. The Block 2 satellites aren't just larger; they're smarter, with advanced processing enabling data transmission speeds of up to 120 Mbps, enabling voice, data, and video communication capabilities for end users. This isn't just connecting phones; it's enabling full broadband experiences anywhere on the planet.

The implications cascade across industries and societies. Emergency responders reaching disasters where infrastructure has been destroyed. Farmers in remote regions accessing market prices and weather data. Students in isolated communities joining virtual classrooms. Refugees maintaining contact with separated families. The smartphone becomes truly universal, a portal to information and opportunity regardless of location.

But this future isn't predetermined. The challenges facing AST remain formidable. Regulatory approval in dozens of countries, each with unique spectrum allocations and sovereignty concerns. Competition from tech giants with unlimited resources. Technical challenges of maintaining hundreds of stadium-sized satellites in precise orbital formation. The fundamental question of whether people will pay for coverage they might rarely use.

The emergency communications use case alone could justify the entire constellation. Climate change is increasing the frequency and severity of natural disasters. Traditional infrastructure—cell towers, fiber cables, power grids—fails precisely when communication is most critical. A phone that works everywhere, always, becomes essential safety equipment. Governments might mandate or subsidize access, transforming the business model from consumer luxury to public utility.

The convergence of terrestrial and space networks represents a fundamental shift in how we think about infrastructure. Today's networks are binary—you have signal or you don't. Tomorrow's networks will be fluid, seamlessly transitioning between terrestrial towers when available and satellites when necessary. The user won't know or care whether their call routes through a tower two miles away or a satellite 500 miles above. Coverage becomes assumed, like electricity or running water.

This convergence enables new applications we're only beginning to imagine. Autonomous vehicles navigating areas without cellular coverage. Drone delivery networks operating beyond urban centers. IoT sensors monitoring everything from wildlife migration to glacier melt, all connected through the same infrastructure serving smartphones. The satellite constellation becomes not just a backup for terrestrial networks but an enabler of entirely new capabilities.

Yet the societal implications raise profound questions. Should universal connectivity be a human right? Who controls the infrastructure that connects humanity—corporations, governments, or some new form of global governance? How do we preserve digital sovereignty when satellites overhead can beam information across borders? What happens to societies that have chosen isolation when connection becomes involuntary?

The light pollution controversy hints at deeper tensions. The SpaceMobile constellation has drawn criticism for its potential contribution to light pollution in the night sky, as well as radio-frequency interference with certain telescopes that operate outside of the visible light spectrum. Observations of BlueWalker 3 were obtained after it unfolded into a large flat-panel shape in November 2022. We're literally changing the night sky to enable connectivity. Is the trade-off worth it? Who decides?

AST SpaceMobile represents something larger than a business or technology. It's an experiment in planetarty-scale infrastructure, an attempt to eliminate one of the last remaining inequalities—access to information. The company might succeed or fail, but the vision will persist. Someone, somehow, will connect every phone on Earth. The question isn't if but when, and whether AST will be the one to do it.

The journey from Avellan's Venezuelan oil fields to a constellation of orbiting cell towers illustrates humanity's relentless drive to connect. We've built cables across oceans, towers across continents, and now we're building networks in space. Each generation expands the definition of "connected" until being disconnected becomes unthinkable.

Looking forward, AST's success or failure might matter less than what they've proven possible. They've shown that phones can talk to satellites, that massive structures can be deployed in space, that the physics of connecting to orbit can be conquered. Whether AST builds the constellation or someone else does, the path has been illuminated. The impossible has become inevitable.

In the end, AST SpaceMobile is betting on a simple proposition: that humans everywhere deserve connection, that geography shouldn't determine opportunity, and that the technical challenges, however daunting, can be solved. It's a bet on human ingenuity and human need. The satellites orbiting overhead aren't just machinery; they're monuments to ambition, testimonies to the belief that every person on Earth should be able to reach out and touch the world.

The story continues to unfold with each launch, each test, each connection. Whether AST SpaceMobile becomes the AT&T of space or a footnote in aerospace history remains unwritten. But they've already achieved something remarkable: they've made us imagine a world where "no signal" is as archaic as "no electricity," where the most remote places on Earth are as connected as Times Square, where the phone in your pocket truly works everywhere. That vision, once released, can never be fully contained. Someone will build this future. The only question is who, and when, and whether the builders will be remembered as visionaries or cautionary tales.

XII. Recent News

The momentum accelerated dramatically as 2024 progressed into 2025. Gateway equipment bookings from MNO partners of $13.6M in Q1 2025, with expected gateway equipment bookings of approximately $10.0 million, on average, per quarter during 2025, as a precursor to the rollout of SpaceMobile Service. "Today, we are at an inflection point for the company. We have ramped up manufacturing capacity and are now able to announce our plans to support five scheduled orbital launches over the next six to nine months. Commercially, we have also expanded our U.S. Government opportunity and are in a position to start generating meaningful revenue during 2025."

The demonstration momentum continued building credibility with each test. Two-way broadband video call completed by Rakuten Mobile in front of a live audience using unmodified smartphones on the SpaceMobile network enabled by a Block 1 BlueBird satellite in orbit today, following successful video calls with AT&T, Vodafone, and Verizon. Each successful demonstration with a major carrier represented not just technical validation but commercial commitment deepening.

Regulatory progress accelerated alongside technical achievements. Received Special Temporary Authority from the FCC for FirstNet evaluation on public safety's Band 14 spectrum, supporting mission-critical capabilities with direct-to-device cellular broadband connectivity. The FirstNet approval was particularly significant—if AST could provide emergency communications for first responders, government contracts worth billions could follow.

The manufacturing scaling became tangible with aggressive launch schedules. Announced multi-provider satellite orbital launch plan with five contracted launches over the next six to nine months · Anticipate orbital launches every one to two months on average during 2025 and 2026 · First Block 2 BlueBird satellite expected to ship in Q2 2025, with orbital launch scheduled during July 2025. This represented a dramatic acceleration from the years-long delays of early satellites to potentially monthly launches.

XIII. Links & Resources

Primary Sources: - AST SpaceMobile Investor Relations: https://investors.ast-science.com/ - SEC Filings (EDGAR): https://www.sec.gov/edgar/browse/?CIK=1835512 - FCC Filings & Proceedings: Search for "AST SpaceMobile" in FCC ECFS

Technical Resources: - AST SpaceMobile Patent Portfolio: USPTO search for assignee "AST & Science" - BlueWalker 3 Technical Specifications: Available through investor presentations - Direct-to-Device Technology Primers: ITU-R recommendations for satellite-to-terrestrial

Industry Analysis: - NSR (Analysys Mason): "Land Mobile via Satellite Markets Report" - Euroconsult: "Prospects for Direct-to-Device Satellite Communications" - Space Capital: Quarterly space investment reports

Partner Resources: - Vodafone Space Initiatives: Technology blog posts on D2D testing - AT&T Network Evolution: Public statements on satellite partnerships - Nokia Network Infrastructure: Technical papers on space-terrestrial integration