Associated Banc-Corp: The Story of Wisconsin's Banking Survivor

I. Introduction & Episode Roadmap

Picture a corner office in Green Bay, Wisconsin, in the spring of 2009. The carpet is worn. The phone rings constantly. On the desk sits a stack of loan files, each one a story of broken promises and sinking collateral values. The man behind the desk has just taken over as CEO of a 148-year-old bank that the market has left for dead. The stock has cratered. The federal government has injected half a billion dollars to keep the institution alive. Employees are whispering about whether to update their resumes. And outside the window, the Fox River flows past as it always has, indifferent to the fact that Wisconsin's largest homegrown bank is teetering on the edge of oblivion.

This is the story of Associated Banc-Corp, ticker symbol ASB on the New York Stock Exchange. Today it sits at roughly $45 billion in assets, making it the largest bank holding company headquartered in Wisconsin. It operates over 220 branches across Wisconsin, Illinois, Minnesota, and now Missouri. It just posted record annual net income of $463 million for 2025, and it recently announced an acquisition that will push it into Omaha and deepen its footprint in the Twin Cities. By most measures, it is a healthy, well-run, mid-sized regional bank.

But here is the central tension of the Associated story, and it is a tension that runs through the entire history of American regional banking: How did a 160-year-old Midwest community bank survive wave after wave of consolidation, nearly die in the financial crisis of 2008, and then claw its way back to respectability? And what does that survival tell us about the brutal economics of being mid-sized in an industry that relentlessly rewards scale?

The arc of this story moves from Civil War origins through a century of quiet compounding, then a fateful detour into Arizona real estate that nearly killed the franchise, followed by a long, humbling rebuild and a modern-day reinvention. Along the way, there are themes that apply far beyond banking: geographic destiny and how where you are shapes what you become, the power of relationship-based business models in an era of algorithms, and the question every mid-sized company in every industry must answer: Are you big enough to matter, or small enough to be special, or are you stuck in the dreaded no-man's-land in between?

Let's start at the beginning.

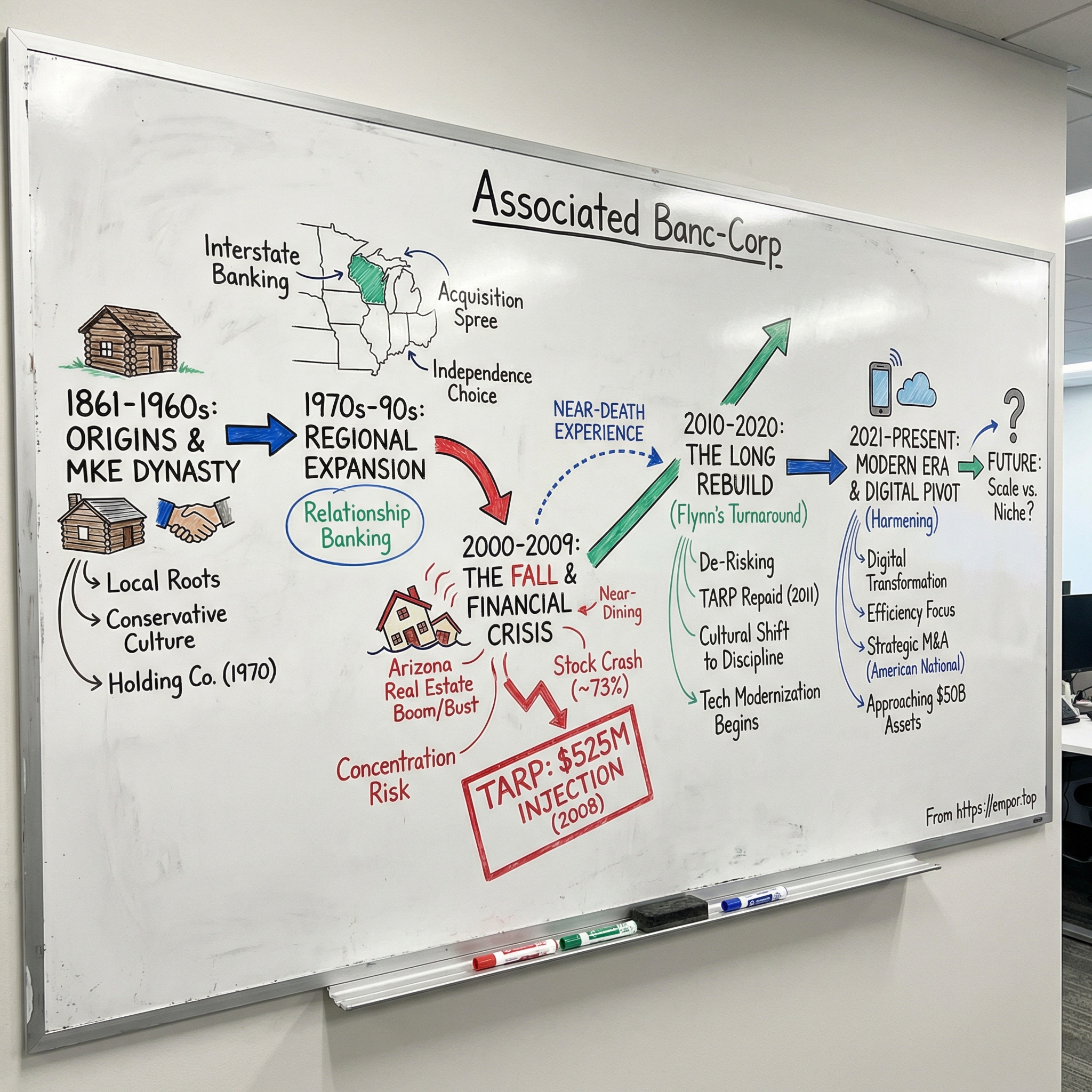

II. Origins & The Milwaukee Banking Dynasty (1861–1960s)

Walk down Water Street in Milwaukee in the 1860s and you would find a city of ambition and sawdust. German immigrants had transformed a lakefront trading post into a manufacturing hub that smelled of hops, fresh-cut timber, and opportunity.

In 1861, as Abraham Lincoln called for troops and the first shots echoed at Fort Sumter, a group of Milwaukee businessmen saw an opportunity that had nothing to do with bullets. The National Banking Act was still two years away, but wartime finance was already creating demand for banking services across the young state of Wisconsin. The founding of what would eventually feed into Associated Banc-Corp's lineage traced back to this era, when small national banks sprang up across Wisconsin's cities and towns to serve the capital needs of a rapidly industrializing frontier economy.

Wisconsin in the mid-nineteenth century was a place of timber and beer. German immigrants had poured into Milwaukee, bringing with them a culture of thrift, savings institutions, and a deep respect for financial prudence. The brewing industry, led by families like Pabst, Schlitz, and Miller, needed banking partners. The lumber barons of the northern forests needed credit lines. And the farmers of the southern tier needed seasonal lending. Banking in Wisconsin was not the rarefied world of Wall Street. It was roll-up-your-sleeves, know-your-borrower, handshake-and-a-ledger-book work.

This culture mattered enormously. While New York and Boston were developing the architecture of investment banking and securities markets, Wisconsin banking remained stubbornly local. Banks were small, numerous, and deeply embedded in their communities.

A bank president in Oshkosh or Appleton or Fond du Lac knew his borrowers personally. He knew whether the hardware store owner was a drinker, whether the farmer's son was responsible enough to take over the operation, whether the new factory would actually find workers. This was relationship banking in its purest form, and it was not sentimental. It was a risk management technology, one that worked remarkably well when the banker and the borrower lived in the same town and went to the same church.

The pivotal moment in Associated's pre-history came in 1964, when a series of Wisconsin banks merged to form a regional network under common ownership. The logic was straightforward: individually, these small-town banks lacked the scale to invest in technology, offer competitive rates, or attract management talent. Together, they could pool resources while maintaining local identities. It was a formula that worked across the Midwest. Think of it as a franchise model: one brand, shared back-office infrastructure, but local faces at every branch.

In 1970, the formal bank holding company structure was established, creating Associated Banc-Corp as the parent entity. This was partly regulatory arbitrage, as the holding company structure allowed for acquisitions and diversification that individual bank charters made cumbersome. But it was also a statement of ambition. The founders of the holding company were not content to remain a scattering of small-town banks. They wanted to build something that could compete across the entire state.

Wisconsin banking stayed fragmented far longer than markets on the coasts. The reasons were cultural as much as regulatory. Unit banking laws, which restricted banks to a single location, persisted in various forms longer in the Midwest. Communities valued having "their" bank. State legislators, many of whom represented rural districts, were suspicious of big-city banking consolidation. The result was that Wisconsin entered the modern era with an unusually large number of small, independent banks, all operating within a few hundred miles of each other, all doing more or less the same thing.

What is striking about this period is the sheer number of banks. In the mid-twentieth century, Wisconsin had hundreds of independently chartered banking institutions. Milwaukee alone had dozens. In an era before electronic banking, each branch had to be physically staffed, each ledger manually maintained. The inefficiency was staggering by modern standards, but it created something valuable: a dense web of local knowledge. Every small-town bank president was a one-person credit bureau, economic development agency, and community pillar rolled into one.

The Associated holding company that emerged from this landscape carried a distinctive cultural imprint. It was not flashy. It did not aspire to be Citibank or Morgan Stanley. Its ambitions were regional, its methods conservative, its pace measured. The executives who ran it came from the communities it served. They wore their conservatism as a badge of honor. In hindsight, this identity would prove to be both the bank's greatest asset and, when it was misapplied in an unfamiliar geography decades later, its near-fatal weakness.

III. The Interstate Banking Revolution & Regional Expansion (1970s–1990s)

For most of the twentieth century, American banking was a patchwork quilt of local and regional institutions, stitched together by regulations that deliberately prevented consolidation. The McFadden Act of 1927 and the Douglas Amendment of 1956 effectively prohibited interstate banking. If you ran a bank in Wisconsin, your world ended at the state line. You could not buy a bank in Illinois, and a bank from New York could not buy you.

This began to change in the 1980s. States started passing reciprocal agreements allowing banks from neighboring states to acquire each other. Wisconsin, characteristically cautious, did not fully embrace interstate banking until 1987, later than many of its neighbors. When the walls finally came down, the Midwest banking landscape transformed with breathtaking speed.

For Associated, the interstate banking revolution presented both an existential threat and a generational opportunity. The threat was simple: larger, better-capitalized banks from Chicago, Minneapolis, and beyond could now enter Wisconsin and compete for Associated's customers. The opportunity was the mirror image: Associated could now expand into Illinois and Minnesota, markets far larger than anything available in its home state.

Management chose the offensive strategy. Through the late 1980s and 1990s, Associated embarked on an acquisition spree, purchasing smaller banks and thrifts across Wisconsin, northern Illinois, and parts of Minnesota. Each deal was relatively modest in isolation, but cumulatively they transformed the company from a collection of small-town banks into a genuine regional franchise. The strategy was to build density, to have enough branches in a metropolitan area that the Associated name became synonymous with banking in the same way that Kwik Trip became synonymous with gas stations across Wisconsin.

The competitive environment during this period was fierce. Norwest Corporation, the Minneapolis-based powerhouse that would eventually merge with Wells Fargo, was expanding aggressively into Wisconsin. Firstar Corporation, another Milwaukee-based holding company, was growing through acquisitions that would ultimately lead to its merger with Star Banc and then with U.S. Bancorp. M&I Bank, headquartered in Milwaukee, was a direct competitor pursuing its own consolidation strategy. And looming over all of them were the New York money center banks, who coveted the stable deposit bases of the Midwest.

At several points during this era, Associated's board faced the fundamental strategic question that every regional bank board must eventually answer: Do we stay independent and keep growing, or do we sell to a larger institution at a premium?

The argument for selling was compelling. Larger banks could invest more in technology, offer customers a wider range of products, and generate better returns on equity through scale efficiencies. The argument for staying independent was equally compelling but harder to articulate. It boiled down to a belief that local banking relationships had intrinsic value, that customers preferred dealing with a Wisconsin-headquartered institution, and that there was a meaningful niche between the community banks below and the mega-banks above.

Associated chose independence. Whether that was the right call depends on your time horizon. In the short term, banks that sold during the 1990s consolidation wave often generated enormous premiums for their shareholders. M&I Bank, for example, eventually sold to BMO Financial Group in 2011 for roughly $4 billion. Firstar merged its way into what is now U.S. Bancorp, one of the most valuable banking franchises in America. Shareholders in those institutions were handsomely rewarded.

But in the longer term, Associated's independence gave it the flexibility to chart its own course, for better and for worse. And there is a counterfactual worth considering: had Associated sold in the late 1990s at a premium, its shareholders would have avoided the catastrophe of 2008 entirely. The decision to stay independent was a bet on management's ability to create value, and for a decade, that bet appeared to be paying off.

The late 1990s brought two additional challenges. First was Y2K, which consumed enormous management attention and technology budgets across the banking industry. The fear that computer systems would fail on January 1, 2000 seems quaint in retrospect, but at the time it was a genuine operational risk that forced banks to audit every system and every vendor. Second was the dawn of internet banking, which threatened to render the branch network, the very infrastructure on which Associated had built its franchise, obsolete.

By 2000, Associated was a successful mid-sized regional bank. It had grown its asset base significantly, built a recognizable brand across its footprint, and maintained strong credit quality. The internet banking challenge, while real, had not yet proven to be the branch-killer that some predicted. Customers still valued the physical presence, particularly for business banking and wealth management.

But Associated was also caught in the middle, too large to enjoy the community bank premium that small institutions commanded, yet too small to achieve the scale economies that the emerging mega-banks were pursuing. This tension, the curse of the mid-sized, would define the next two decades of the Associated story. And the way management chose to resolve it would nearly destroy the company.

IV. The Fateful Diversification: Construction & Commercial Real Estate (2000–2007)

Imagine you are running a mid-sized Midwest bank in the year 2002. Your stock price is respectable. Your loan portfolio is clean. Your customers are loyal. But your margins are shrinking, and your board is asking uncomfortable questions about growth. Where do you find it?

The dot-com crash of 2000-2001 had marked a pivot point for American banking. The Federal Reserve slashed interest rates to stimulate the economy, and suddenly the traditional banking business, taking in deposits and lending them out at higher rates, became brutally difficult. When rates are low, the spread between what a bank pays for deposits and what it earns on loans compresses. This spread, known as net interest margin, is the oxygen of banking. When it thins, banks suffocate unless they find other ways to grow.

Associated's management team looked at the landscape and made a decision that seemed shrewd at the time: lean into commercial real estate and construction lending, where yields were higher and demand was booming. The logic was seductive. Real estate lending was something community and regional banks understood. It was relationship-driven. Borrowers needed local expertise and local decision-making. And the spreads were attractive compared to plain-vanilla commercial lending, where competition from national banks was driving margins toward zero.

But Associated did not just expand its real estate lending in Wisconsin and the Midwest. It reached far beyond its traditional footprint, building a substantial portfolio of construction and development loans in the Phoenix and Scottsdale markets of Arizona. This was the fateful decision, the one that would nearly end the institution's 150-year run.

Why Arizona? The Phoenix metropolitan area in the early and mid-2000s was one of the hottest real estate markets in America. Population was growing. Housing construction was booming. Land values were rising at double-digit annual rates. Developers were building spec homes, condo conversions, and master-planned communities with seemingly insatiable demand. For a bank looking for yield, Arizona was a candy store.

Associated entered the market through relationships. A Wisconsin-based bank did not simply hang up a shingle in Scottsdale and start lending. Rather, it followed borrowers and brokers who connected them to opportunities. The bank built relationships with developers who had track records, who had built successfully before, who presented business plans that penciled out in the context of the market assumptions of the time.

The underwriting was not reckless on its face. It reflected the consensus view that Arizona's growth was structural, not speculative, that people were genuinely moving to the Sun Belt, and that the housing supply was catching up with real demand.

The problem was concentration risk. As the Arizona portfolio grew, it became an outsized share of Associated's total loan book. The bank was making a massive, undiversified bet on one asset class in one geography, thousands of miles from its headquarters, using underwriting standards that had been developed for Wisconsin's much more stable real estate market.

Concentration risk is one of the most dangerous forces in banking. It is the reason regulators track it obsessively. When a bank's loan portfolio is diversified across many industries, geographies, and borrower types, losses in any one category are absorbed by the profits from the others. But when a large percentage of the book is concentrated in a single sector, a downturn in that sector does not just reduce profits. It can threaten solvency.

The warning signs were there. Nationally, housing prices had decoupled from fundamentals. Subprime mortgage originations were reaching absurd levels. But on the ground in Phoenix, optimism was self-reinforcing. Every new project that sold out validated the model. Every competitor that piled in confirmed the opportunity. And at Associated's headquarters in Green Bay, the Arizona lending operation was producing impressive returns that boosted the bank's overall performance metrics.

By 2006 and 2007, Associated's construction and commercial real estate portfolio had swelled to levels that would have alarmed any risk manager looking at the numbers with fresh eyes. But success has a way of muting dissent. The loan officers who were generating volume were the stars. The risk managers who might have raised red flags were under pressure to support growth. And the executive team, judged by quarterly earnings and stock price, had every incentive to keep the machine running.

This dynamic, where short-term success drowns out long-term risk signals, is not unique to Associated or even to banking. It is the central tragedy of every financial crisis. The smartest people in the room all agreed that the fundamentals were sound. The models said the loans would perform. The competitors were doing the same thing. And the market rewarded the behavior with higher stock prices and bigger bonuses. The groupthink was not malicious; it was structural. When everyone's compensation depends on growth, no one has an incentive to be the person who says, "Wait, maybe we should slow down."

In the final months before the crash, Associated's stock reached its all-time high of $35.46 per share, set on February 21, 2007. The market was pricing in continued growth, continued profitability, continued success. No one in Green Bay or on Wall Street had any idea that the bank was sitting on a ticking bomb. Within two years, that $35 stock would be trading in single digits, and the management team that had built the Arizona franchise would be gone. The distance from hubris to humiliation, it turned out, was measured in months, not years.

V. The Financial Crisis: Near-Death Experience (2008–2009)

There is a moment in every financial crisis when the abstract becomes concrete, when the numbers on a spreadsheet become empty houses and abandoned construction sites and human beings whose livelihoods are ruined. For Associated Banc-Corp, that moment arrived in the second half of 2007 and accelerated through 2008 with sickening velocity.

The Arizona real estate market did not decline. It collapsed. Between 2007 and 2009, home prices in the Phoenix metropolitan area fell by roughly 55 percent from their peak. Spec homes sat unsold. Condo conversion projects stalled mid-construction. Land that developers had purchased at the top of the market became worth a fraction of the acquisition price. Borrowers who had seemed creditworthy eighteen months earlier were suddenly underwater, unable to service their debt and unable to sell the underlying collateral at anything close to the loan balance.

For Associated, the cascading defaults were catastrophic. Construction and development loans are inherently riskier than other forms of commercial lending because the collateral is a project in progress, not a finished, income-producing asset. When a half-built condo complex has no buyers and no funding to complete construction, the bank's collateral is essentially a hole in the ground surrounded by a chain-link fence. The recovery value on these assets was pennies on the dollar.

The numbers told the story with brutal clarity. Associated was forced to book massive loan loss provisions as the extent of the damage became clear. The stock price, which had peaked above $35 in early 2007, went into freefall. Cumulatively across 2007, 2008, and 2009, the stock fell approximately 73 percent. Based on annual return data showing declines of 19.5 percent in 2007, 17.2 percent in 2008, and 46.8 percent in 2009, the stock likely bottomed in the $6 to $9 range. Shareholders who had bought at the peak watched their investment lose three-quarters of its value.

The question that hung over every board meeting, every analyst call, and every employee watercooler conversation was simple: Would Associated survive? The answer was genuinely in doubt. Regulators were telling management to raise capital immediately. The credit markets were frozen. And the stigma of being a bank with massive exposure to the worst real estate market in America made it nearly impossible to attract private capital.

On November 21, 2008, the federal government injected $525 million into Associated through the Troubled Asset Relief Program, known as TARP. The money came in the form of preferred stock with warrants, giving the government an ownership stake and a senior claim on the bank's earnings.

TARP was simultaneously a lifeline and a scarlet letter. The capital injection stabilized the bank's balance sheet and reassured depositors and counterparties. But it also signaled to the market that Associated was in serious trouble, that without government intervention, the bank might have been forced into a sale or, worse, into FDIC receivership.

The management shakeup that followed was inevitable. CEO Paul Beideman, who had led the bank during the years when the Arizona exposure was built, announced his retirement in 2009. He remained in the role until a successor could be found, but the writing was on the wall. The board needed fresh leadership, someone who could stabilize the institution, work out the troubled assets, and restore credibility with regulators, investors, and employees.

Inside the bank, the atmosphere was toxic. Employees in the commercial lending groups, many of whom had been responsible for originating the loans that were now blowing up, were demoralized and defensive. Employees in other divisions resented being dragged into a crisis they had not created. Depositors in Wisconsin, who had banked with Associated for decades, began asking questions about the safety of their savings. Although deposits were federally insured up to the applicable limits, the specter of a bank failure was enough to rattle even the most loyal customers.

The workout process, the painstaking effort to manage through the portfolio of troubled loans, was the most grueling chapter in the bank's history. Every borrower in distress presented a difficult decision.

Some borrowers were fundamentally sound operators who had been caught in a market downturn. They deserved forbearance and restructuring. Others were speculators who had overleveraged and had no realistic path to repayment. They needed to be foreclosed on, and the collateral needed to be liquidated, often at devastating losses. Making these calls required judgment, experience, and a willingness to confront unpleasant realities, qualities that are easy to find in good times and scarce in bad ones.

Why did Associated survive when other banks with similar exposures failed? Three factors stand out.

First, despite the Arizona disaster, Associated's core Wisconsin franchise remained fundamentally sound. Deposits were sticky. The consumer and small business loan portfolios in the Midwest performed relatively well. The bank had a healthy base that could absorb losses.

Second, the TARP injection came early enough to prevent a liquidity crisis. Unlike some institutions that waited too long and were eventually seized by regulators, Associated received government capital while there was still time to execute a workout plan.

Third, Wisconsin's regulators, while demanding, were constructive rather than punitive. They pushed for new leadership and better risk management but did not force an immediate sale or liquidation.

The psychological impact of the crisis cannot be overstated. People who lived through it at Associated describe it as a trauma that fundamentally changed the culture of the organization. Consider what it means to work at a bank where the stock has fallen 73 percent, where the government has had to step in with emergency capital, where colleagues are being laid off, and where every day brings news of another borrower defaulting. The fear was not abstract. Employees worried about their jobs, their savings, their mortgages. Many of them held Associated stock in their retirement accounts. The crisis was not just a corporate event; it was a personal one.

The scar tissue from 2008-2009 remains visible today in the bank's risk management practices, its underwriting standards, and its deep institutional aversion to concentration risk. When current management talks about disciplined lending, it is not a platitude. It is a lesson written in blood. And it raises an important question for investors: How long does institutional memory last? Does the caution bred by the 2008 crisis endure as the people who experienced it retire and are replaced by a new generation that knows the crisis only from history books?

VI. The Long Rebuild: De-Risking & Cultural Transformation (2010–2015)

There is a specific kind of person who takes a job that nobody else wants. Philip B. Flynn was that kind of person. He arrived at Associated on December 1, 2009, stepping into one of the most unenviable CEO positions in American banking. He was taking over a company that had just received a half-billion-dollar government bailout, was sitting on more than $2 billion in problem assets, and had a workforce that was shell-shocked and uncertain about the future.

Flynn was an experienced Midwest banker, and his hiring signaled the board's intent to return to basics. He was not a turnaround specialist from Wall Street or a restructuring consultant. He was a commercial banker who understood the rhythms of relationship lending in the upper Midwest. His mandate was clear: stabilize the balance sheet, work out the troubled assets, repay TARP, and rebuild the institution's credibility with every constituency that had been shaken by the crisis.

The workout years were methodical and unglamorous. Month by month, quarter by quarter, Flynn's team ground through the portfolio of nonperforming loans. Some borrowers were restructured with modified terms. Others were foreclosed on, and the properties were sold at whatever the market would bear. The losses were real and they were painful, but the alternative, letting the problems fester, would have been worse. Banks that tried to "extend and pretend," giving troubled borrowers more time in the hope that markets would recover, often found that delays only compounded the losses.

TARP repayment became the symbolic milestone that would mark Associated's return from the brink. In 2010, the company raised $435 million through a common stock offering, diluting existing shareholders but providing the capital needed to repay the government. The first installment of $262.5 million was repaid on April 6, 2011. The remaining $262.5 million followed on September 14, 2011. In total, the government earned approximately $71.5 million in dividends and warrant proceeds from its investment in Associated, a profitable outcome for taxpayers.

For the bank, the repayment was more than a financial transaction. It was a declaration of independence, proof that Associated could stand on its own without government support.

With TARP repaid, Flynn turned to the strategic reset. The bank exited risky asset classes and geographies, pulling back from the kind of out-of-footprint lending that had caused the crisis. The focus returned to bread-and-butter Midwest banking: commercial and industrial loans to middle-market businesses, consumer lending, residential mortgages, and wealth management. The watchword was discipline. Every loan had to meet strengthened underwriting standards. Concentration limits were enforced with religious rigor. The days of chasing yield in Arizona were definitively over.

But the rebuild coincided with an explosion in regulatory burden. The Dodd-Frank Wall Street Reform and Consumer Protection Act, signed into law in July 2010, imposed sweeping new requirements on banks of all sizes. For a mid-sized institution like Associated, the compliance costs were staggering relative to its scale. The largest banks could spread compliance costs across hundreds of billions in assets. Community banks were exempt from many of the most onerous provisions. Associated fell squarely in the uncomfortable middle, large enough to be subject to enhanced regulation but too small to absorb the costs easily. New stress testing requirements, risk management standards, and reporting obligations consumed management time and technology budgets that could otherwise have been invested in growth.

Technology modernization became another priority during this period. Associated had underinvested in digital banking during the years when management attention was focused on growth and then on survival. By the early 2010s, the bank's technology infrastructure was showing its age. Mobile banking, online account opening, and digital payments were becoming table stakes, and Associated was behind the curve. The investments required were substantial, but Flynn understood that falling further behind on technology would erode the franchise value of the branch network that was the bank's core competitive asset.

The branch network itself underwent rationalization. In 2015, the bank consolidated 13 branches across three states, closing underperformers and investing in locations with stronger demographics. This was part of a broader industry trend, as banks recognized that the economics of physical branches were changing. Fewer customers needed to visit a branch for routine transactions, but branches remained important for complex activities like business lending, mortgage origination, and wealth management consultations. The art was figuring out which branches to keep and which to close, a process that required balancing financial optimization against community relationships and employee morale.

Talent retention was a constant challenge during the rebuild years. How do you attract and keep talented bankers at an institution that just nearly failed? The answer involved a combination of cultural messaging, as Flynn repeatedly emphasized that the crisis was behind them and the future was bright, competitive compensation, and the appeal of a turnaround story. For some employees, the opportunity to help rebuild an institution was more compelling than the stability of joining a bank that had never been tested. The people who stayed through the darkest days became the backbone of the new Associated, and their loyalty was not quickly forgotten by management.

Perhaps the most important transformation during this period was cultural. Before the crisis, Associated's culture had rewarded loan growth. Lenders were compensated for origination volume, and there was implicit pressure to stretch on credit quality to win competitive deals.

After the crisis, the culture shifted decisively toward disciplined underwriting and risk-adjusted returns. It was not enough to book a loan; the loan had to meet rigorous standards for credit quality, pricing, and concentration. This cultural shift was Flynn's most important legacy.

Changing a company's culture is the hardest thing a CEO can do, because culture is not a policy manual or a set of metrics. It is the set of unspoken norms that determine how people behave when no one is watching. Flynn made risk management prestigious, not just a compliance function, and he ensured that the lessons of 2008 were embedded in the institution's DNA.

Flynn's tenure lasted roughly twelve years, from December 2009 to April 2021. By the time he announced his retirement in January 2021, the transformation was evident in every financial metric. Problem assets had been resolved. TARP had been repaid. The balance sheet was clean. The culture was disciplined. And the bank had even executed a major acquisition, the Bank Mutual deal, without stumbling. Flynn had done the unglamorous, essential work of turning a broken institution into a functioning one. He had not made Associated exciting, but he had made it trustworthy again, and in banking, trust is the only currency that matters.

The question that remained was whether conservative management would be enough in an industry being disrupted from every direction. The answer required a different kind of leader.

VII. The Andy Harmening Era: Repositioning for Modern Banking (2021–Present)

Andy Harmening did not walk into a crisis when he became CEO on April 28, 2021. He walked into something arguably more challenging: a bank that had been saved but now needed to figure out what it wanted to be when it grew up. The analogy that comes to mind is a patient who has recovered from a heart attack. The immediate danger has passed. The doctors have done their work. But the patient now faces a choice: live cautiously, avoiding all risk, and slowly atrophy. Or find a way to be active again, but this time with the wisdom that comes from having stared at mortality.

Harmening's background was a deliberate contrast to what Associated had been. He had spent 25 years in banking, including nine years at U.S. Bank, a stint as Vice Chairman of consumer banking at Bank of the West, and most recently a senior executive role at Huntington Bank, where he had led the digital and omni-channel strategy for consumer and business banking. He was, in short, a growth-oriented banker with deep experience in digital transformation, exactly the kind of leader a post-crisis institution needs when it is ready to go on offense again.

His first task was articulating a strategic vision. Under Flynn, the imperative had been stabilization. Under Harmening, the question shifted to ambition. What kind of bank would Associated be? The answer emerged through what management described as a multi-phase strategic plan. Phase one focused on laying the foundation: upgrading technology, building out the commercial banking team, and improving operational efficiency. Phase two, which took shape by 2024 and 2025, focused on accelerating growth.

The efficiency agenda was central to the transformation. When Harmening arrived, Associated's efficiency ratio, the percentage of revenue consumed by operating expenses, was running above 60 percent. For context, a regional bank's efficiency ratio is one of the clearest indicators of operational discipline. Every dollar of revenue that goes to overhead is a dollar that does not flow to shareholders. The best-run regional banks target efficiency ratios in the low-to-mid 50s. By 2025, Harmening had driven Associated's adjusted efficiency ratio down to approximately 56 percent, a meaningful improvement that reflected both cost discipline and revenue growth.

The digital transformation was the most visible change. Associated launched a new digital banking platform in September 2022, and over the next three years delivered 11 major customer-facing upgrades. The results were striking: double-digit increases in customer acquisition, double-digit decreases in customer attrition, multi-year highs in digital banking satisfaction scores, and a digital adoption rate of 72 percent. The bank also began integrating artificial intelligence into its operations, not the headline-grabbing generative AI that dominates public discussion, but practical applications in fraud detection, customer service, and operational workflow.

For a bank Associated's size, technology investment is a perpetual challenge. JPMorgan Chase spends roughly $17 billion annually on technology, which is more than Associated's entire market capitalization. Associated's total noninterest expense for all of 2025 was approximately $856 million, covering everything from salaries to real estate to compliance, and only a fraction of that goes to technology. The disparity is staggering. A regional bank cannot out-spend the giants. It has to be smarter about where it invests, choosing platforms and partnerships that deliver the most impact per dollar spent. Think of it as the difference between a Formula One team with an unlimited budget and a scrappy privateer who has to make every dollar count. The privateer cannot win on raw horsepower, but with the right strategy and execution, it can finish in the points.

On the lending side, Harmening executed a significant rebalancing of the loan portfolio. The bank expanded its commercial relationship manager headcount by 28 percent, a bold investment in the human capital that drives commercial banking revenue. By year-end 2025, commercial and business lending reached $13 billion, representing nearly 42 percent of total loans. Commercial real estate, which had been the source of the bank's near-death experience, was managed down to 23 percent of total loans, well within regulatory guidelines and a fraction of its crisis-era concentration.

The Bank Mutual acquisition, which closed on February 1, 2018, during the latter part of Flynn's tenure, provided a template for how Associated could grow through deals. The $482 million all-stock transaction added over 120,000 customer accounts and made Associated the dominant banking presence in the Milwaukee metropolitan area. The integration involved closing 36 redundant branches while retaining the customer relationships, a delicate surgery that tested the bank's operational capabilities. The lessons learned in integrating Bank Mutual informed the playbook for future acquisitions.

The question of the $50 billion asset threshold loomed over strategic planning. Under Dodd-Frank's original provisions, banks crossing $50 billion in assets faced significantly enhanced regulatory scrutiny, including mandatory stress testing and additional capital requirements. Although subsequent legislation raised this threshold to $100 billion for some enhanced standards, banks approaching the $50 billion mark still face incremental regulatory costs.

With total assets now at $45.2 billion and growing, Associated is approaching this line. The American National acquisition will add $5.3 billion in assets, potentially pushing the combined institution above $50 billion. Management's willingness to cross this threshold signals confidence that the revenue benefits of scale outweigh the regulatory costs.

The American National deal itself is strategically significant. Announced on December 1, 2025, the acquisition of American National Corporation brings $5.3 billion in total assets, $3.8 billion in loans, and $4.7 billion in deposits into the Associated franchise. It deepens Associated's presence in the Twin Cities market, where it will become the tenth-largest bank by deposit share, and establishes a number-two position in the Omaha metropolitan area. This is geographic expansion done the right way: into adjacent Midwest markets where the bank's relationship model translates naturally, where the economic and cultural environment is familiar, and where the risk of the kind of distant adventurism that caused the Arizona debacle is minimal.

The deal also signals something important about Harmening's strategic ambition. Associated under Flynn was a conservator. Associated under Harmening is a builder. The Bank Mutual deal added density in Milwaukee. The American National deal adds new metropolitan markets entirely. If both integrations succeed, the combined institution will have a presence across six states and a footprint that stretches from Green Bay to Omaha, a genuinely multi-state Midwest franchise rather than a Wisconsin bank with outposts.

Capital management has been another hallmark of the Harmening era. The bank has maintained 13 consecutive years of dividend increases, with the current annualized dividend at $0.96 per share. Share repurchases have supplemented dividends as a way to return capital to shareholders. The CET1 capital ratio of 10.49 percent provides a comfortable buffer above regulatory minimums while leaving room for growth and acquisitions.

The juxtaposition with the crisis era is stark. Associated went from a bank that needed $525 million in government capital to survive to one that generates nearly half a billion dollars in annual earnings and returns capital to shareholders through dividends and buybacks. That transformation did not happen overnight. It took twelve years under Flynn and now five years under Harmening. The question for investors is whether the current trajectory is sustainable, or whether the structural challenges of mid-sized regional banking will eventually overwhelm even excellent execution.

VIII. COVID, Interest Rates & The Current Chapter (2020–Present)

The years between 2020 and the present have been the most volatile operating environment for American banks since the financial crisis itself, but the nature of the volatility has been entirely different. In 2008, the enemy was credit losses. In the 2020s, the enemy has been interest rate whiplash, pandemic disruption, and an existential scare that briefly threatened to engulf the entire regional banking sector.

When COVID-19 shut down the American economy in March 2020, banks were thrust into the role of economic first responders. Associated moved quickly to participate in the Paycheck Protection Program, originating PPP loans that kept small businesses afloat across Wisconsin, Illinois, and Minnesota. The bank offered forbearance programs for borrowers experiencing pandemic-related hardship and transitioned a large portion of its workforce to remote operations, a logistical challenge for a company that had always prided itself on in-person relationships.

The pandemic also introduced a new kind of financial pain: near-zero interest rates. The Federal Reserve slashed its target rate to essentially zero in March 2020 and kept it there for two years. For a bank that derives over 80 percent of its revenue from net interest income, this was margin compression at its most punishing. Think of it this way: a bank's net interest margin is the difference between the rate it earns on loans and the rate it pays on deposits. When rates are near zero, both sides of the equation compress, but the bank cannot pay depositors less than zero. The floor on funding costs creates a ceiling on profitability.

Associated's NIM fell to the mid-2.7 percent range during the low-rate era, a level that barely covered operating expenses and loan losses. The bank survived, but the experience reinforced a broader truth about the banking business: interest rates are the single most important exogenous variable, and management can only do so much to mitigate their impact.

Then came the fastest interest rate hiking cycle in modern history. Beginning in March 2022, the Federal Reserve raised rates by over 500 basis points in roughly eighteen months, moving from near zero to over 5 percent. For banks, rapid rate increases are a double-edged sword. On one hand, higher rates allow banks to earn more on their loans, boosting net interest income. On the other hand, rising rates put downward pressure on the value of existing bonds and fixed-rate loans in the bank's portfolio, and they create pressure to raise deposit rates to prevent customers from moving their money to higher-yielding alternatives.

Associated's asset-liability management team, the quiet professionals who manage the balance between what the bank earns on its assets and what it pays on its liabilities, earned their keep during this period. The bank actively repositioned its balance sheet, taking significant one-time losses to sell lower-yielding mortgage portfolios and investment securities in the fourth quarters of both 2023 and 2024.

In 2023, this included a $136 million mortgage portfolio sale loss and a $65 million net loss on investment sales. In 2024, the charges were even larger: a $130 million mortgage portfolio sale loss and $148 million in net investment security losses. These repositioning decisions crushed reported earnings in those years, with EPS falling to $1.13 in 2023 and just $0.72 in 2024 on a reported basis.

But here is the crucial nuance: the balance sheet repositioning was strategic, not a sign of distress. Management was deliberately taking short-term pain to improve long-term profitability. By selling low-yielding assets and reinvesting the proceeds at higher rates, they improved the bank's forward-looking net interest margin. The payoff arrived in 2025, when NIM expanded by 25 basis points to 3.03 percent and net interest income surged 15 percent to $1.2 billion, driving record annual earnings.

The regional bank crisis of spring 2023, when Silicon Valley Bank, Signature Bank, and First Republic Bank all failed in rapid succession, provided the most severe stress test of Associated's post-2008 rebuild. The crisis was driven by a toxic combination of uninsured deposit concentration, unrealized losses on bond portfolios, and social media-fueled bank runs. For a brief, terrifying period, the question was whether the contagion would spread to the entire regional banking sector.

Associated weathered the storm. Its deposit base, heavily concentrated in retail and small business accounts in Wisconsin, proved far stickier than the venture capital-fueled deposits that fled SVB. The comparison is instructive. Silicon Valley Bank's deposits were concentrated among technology startups and venture capital firms, customers who were highly networked, highly attentive to risk signals, and capable of moving billions in hours through digital transfers coordinated on Twitter and group chats. Associated's depositors were Wisconsin families, small business owners, and middle-market companies. They were not monitoring social media for bank run signals. They had relationships with their bankers. And their deposits were, for the most part, within FDIC insurance limits.

Associated's bond portfolio losses, while real, were manageable in the context of its capital position. And critically, the bank's reputation for conservative management, forged in the fire of 2008, provided credibility with depositors and regulators. Sometimes the best brand a bank can have is boring. The irony was not lost on observers: the very conservatism that some investors had criticized as a drag on returns turned out to be the bank's most valuable asset when the world was panicking.

As of early 2026, Associated stands in arguably the strongest position of its history. Record earnings, expanding margins, a clean loan portfolio with a net charge-off ratio of just 0.12 percent, and a strategic acquisition in the pipeline.

The bank has grown its total assets to $45.2 billion, generated return on average tangible common equity exceeding 15 percent, and maintained a well-capitalized balance sheet with a CET1 ratio of 10.49 percent. The stock, at roughly $26 per share, remains well below its pre-crisis all-time high of $35.46, a reminder that the scars of 2008 still affect investor perception nearly two decades later.

The succession question appears settled for the near term, with Harmening firmly in control and executing on a clear strategic plan. The bank has also opened its first branch in St. Louis in April 2025, a modest but symbolically important expansion into a new state, signaling that the era of geographic retrenchment is over.

IX. Business Model Deep Dive & Competitive Positioning

Strip away the history, the narrative, the human drama, and ask a cold question: How does this business actually work? What are the mechanics of revenue generation, and what determines whether the machine runs efficiently or sputters?

To understand how Associated actually makes money, start with the raw material: deposits. The bank gathers approximately $35 billion in deposits from individuals, businesses, and institutions across its footprint. About 75 percent of these deposits come from Wisconsin, which is both a strength and a vulnerability. The strength is stability: Wisconsin depositors are loyal, and the state's economy, while not fast-growing, is diversified across manufacturing, healthcare, agriculture, and education. The vulnerability is concentration: a severe downturn in Wisconsin's economy would hit Associated disproportionately hard.

Those deposits are the bank's cheapest source of funding. It lends them out in the form of commercial, consumer, and real estate loans, earning the net interest spread. With a total loan portfolio of $31.2 billion as of year-end 2025, the bank's loan-to-deposit ratio is healthy, meaning it has sufficient funding to support its lending operations without relying heavily on expensive wholesale borrowing.

The revenue mix reveals a bank that is heavily dependent on net interest income: roughly 81 percent of total revenue, or $1.2 billion in 2025, comes from the spread between loan yields and deposit costs. The remaining 19 percent, approximately $286 million, comes from noninterest income sources including wealth management fees, capital markets revenue, mortgage banking, service charges on deposits, and card-based fees.

This revenue mix is typical for a Midwest commercial bank but reveals a strategic challenge. Net interest income is inherently volatile because it depends on interest rates, loan growth, and deposit pricing, variables that management can influence but cannot control.

Fee income, by contrast, is more predictable and less sensitive to rates. The best-performing regional banks tend to have fee income ratios of 30 percent or higher. Associated's 19 percent ratio suggests significant room for growth in fee-based businesses, particularly wealth management.

The relationship banking model is the philosophical core of Associated's business. In practice, it works like this: a commercial relationship manager covers a portfolio of middle-market businesses, companies with revenues typically ranging from $10 million to $500 million.

The RM knows the business owner personally, understands the company's seasonal cash flow patterns, industry dynamics, and growth plans. When the business needs a line of credit, a term loan, treasury management services, or wealth planning for the owner's personal finances, the RM coordinates across the bank's product specialists to deliver a comprehensive solution.

This model creates value through stickiness. A business that uses Associated for its operating account, credit line, treasury management, and owner's personal banking is much harder for a competitor to poach than one that only has a single product relationship. The total cost of switching, not just financial but in terms of disruption and rebuilt relationships, creates meaningful retention advantages.

The customer segmentation reflects this approach. Associated targets middle-market commercial clients, affluent retail customers, and small business owners. These are segments where relationship depth matters and where the bank can compete effectively against both larger institutions (which often treat these customers as too small for dedicated attention) and community banks (which may lack the product breadth to serve complex needs).

Geographically, the bank's competitive position varies by market. In Green Bay, it is a dominant local player with deep roots and high brand recognition. In Milwaukee, the Bank Mutual acquisition established a strong fourth-place position with roughly 10 percent deposit market share. In Chicago, Associated operates primarily as a commercial banking franchise, competing for middle-market relationships against some of the most sophisticated banking competitors in the country. In the Twin Cities, the presence is growing and will expand significantly with the American National acquisition.

The "super-community bank" label captures Associated's structural dilemma, one that is shared by dozens of similar institutions across the country. At $45 billion in assets, it is too large to benefit from the regulatory exemptions and community goodwill that advantage banks under $10 billion. A true community bank does not have to worry about Dodd-Frank stress testing, does not need a Chief Risk Officer with a staff of thirty, and can make lending decisions with a speed and flexibility that larger institutions cannot match. But Associated passed that threshold long ago. At the same time, it is too small to achieve the scale economies in technology, compliance, and brand marketing that banks above $100 billion enjoy. This is the no-man's-land of regional banking, and it is the reason that the industry has been consolidating relentlessly for decades. The number of U.S. banks has declined from roughly 14,000 in 1985 to fewer than 4,500 today, and mid-sized banks have been the most frequent casualties of consolidation.

The Wisconsin economy is the backdrop against which Associated's franchise operates, and understanding that economy is essential for evaluating the bank. Wisconsin's advantages include a diversified economic base anchored by manufacturing (from small-engine maker Briggs & Stratton to heavy equipment), a strong agricultural sector, a robust healthcare system (including major hospital networks and medical device companies), and a cost of living that attracts and retains workers. Unemployment has consistently run below the national average. The state's major universities produce a steady pipeline of educated workers.

Its disadvantages are equally real. Population growth has been slow, averaging well under 1 percent annually for the past two decades. The demographic profile is aging, particularly in rural areas. And Wisconsin lacks the high-growth technology and biotech sectors that drive economic dynamism in places like Austin, San Francisco, or the Research Triangle. For a bank, this translates to a stable but unspectacular growth environment: credit losses are low because the economy does not boom and bust dramatically, but loan growth requires constant effort and competitive market share gains rather than riding a rising tide of demographic and economic expansion.

X. Strategic Frameworks: Porter's Five Forces & Hamilton's Seven Powers

Step back from the specifics of Associated Banc-Corp for a moment and ask a more fundamental question: Is mid-sized regional banking a good business? Not a good service, not a necessary institution, but a good business in the sense that it generates returns above the cost of capital over long periods of time. Two analytical frameworks illuminate the competitive reality and help answer that question: Michael Porter's Five Forces and Hamilton Helmer's Seven Powers.

Starting with Porter's framework, the threat of new entrants into banking is moderate-to-low. Regulatory barriers, including charter requirements, capital adequacy standards, and compliance infrastructure, make it expensive and time-consuming to start a bank from scratch. However, fintech companies have found ways to enter specific product verticals without becoming full-service banks. Companies like SoFi and Ally compete for deposits and consumer loans. Rocket Mortgage dominates digital mortgage origination. But none of these challengers has replicated the full suite of services that a relationship bank provides to a middle-market business customer. For now, the moat around full-service banking remains intact, though it is narrowing.

The bargaining power of suppliers, primarily depositors who provide the raw material of funding, fluctuates with the interest rate environment. In a zero-rate world, depositors have few alternatives and banks enjoy cheap funding. In a high-rate world like the current one, depositors can move money to Treasury bills, money market funds, or higher-yielding online savings accounts with a few clicks. The rate transparency created by the internet has permanently increased depositor bargaining power. Banks can no longer count on customer inertia to maintain below-market deposit pricing.

The bargaining power of buyers, meaning borrowers and banking customers, is high and growing. A middle-market business in Milwaukee can choose from Associated, U.S. Bank, BMO, Huntington, JPMorgan Chase, and numerous community banks and credit unions. Online lenders offer alternatives for simpler credit needs. This abundance of choice means that banks compete aggressively on price, responsiveness, and relationship quality, a dynamic that keeps margins under perpetual pressure.

The threat of substitutes is the force that keeps bank executives awake at night. Non-bank lenders like OnDeck for small business lending and Rocket Mortgage for residential lending have demonstrated that specific banking products can be unbundled and delivered more efficiently outside the traditional banking structure. Payment disintermediation through Venmo, Apple Pay, and Zelle erodes the transaction revenue that banks historically earned. And for larger commercial customers, direct access to capital markets through bond issuances and private credit funds reduces the need for bank intermediation entirely.

Competitive rivalry is intense across the entire industry. Consider Associated's competitive landscape in its home state alone. U.S. Bank holds the number-one deposit share position in Wisconsin, backed by the resources of a $670 billion institution. BMO, backed by a trillion-dollar Canadian parent, holds the third position and leads in markets like Madison. Huntington Bancshares, at roughly $200 billion in assets, entered the Wisconsin market through its acquisition of TCF Financial. JPMorgan Chase has a significant and growing presence. And credit unions, which enjoy a structural tax advantage because they are exempt from federal income tax, compete fiercely for retail deposits and consumer lending. In Wisconsin, institutions like Summit Credit Union and Landmark Credit Union command significant market share and offer rates that for-profit banks struggle to match.

The intensity of rivalry, combined with the other four forces, explains why banking has been a mediocre business for investors over the long term. The KBW Bank Index has underperformed the S&P 500 over most multi-decade periods. Banks generate returns on equity that rarely exceed the cost of equity by a wide margin, and when they do, it is often a sign that they are taking risks that will eventually catch up with them.

Turning to Hamilton Helmer's Seven Powers framework, which identifies the sources of durable competitive advantage, the picture for Associated is sobering. Scale economies, the ability to spread fixed costs over a larger revenue base, are limited. Associated simply cannot match the technology spending, marketing budgets, or global capital markets capabilities of JPMorgan Chase or Bank of America. It does benefit from regional scale, meaning it is large enough within Wisconsin to achieve some efficiencies in branch operations and brand recognition that smaller banks cannot, but this is a thin advantage.

Network effects, one of the most powerful sources of competitive advantage in technology businesses, are largely absent from banking. A customer's choice of bank does not inherently make the bank more valuable to other customers. Treasury management services create modest ecosystem effects: when a business uses Associated for treasury management, its vendors and customers may find it convenient to also bank with Associated. But these effects are weak compared to true platform businesses.

Counter-positioning, the ability to adopt a strategy that incumbents cannot copy without damaging their existing business, presents an interesting opportunity. Associated's relationship banking model, with local decision-making and personalized service, is something that algorithmic lending platforms cannot replicate. But the counter-positioning cuts both ways: fintechs are counter-positioning against all traditional banks, including Associated, by offering faster, cheaper, and more convenient digital-first experiences.

Switching costs represent Associated's strongest competitive power. Business customers who have integrated their treasury management, payroll, and credit facilities with Associated face meaningful disruption if they switch banks. The cost is not just financial; it includes retraining staff, rebuilding reporting integrations, and establishing new relationships.

Wealth management clients are similarly sticky, as the relationship with an advisor creates trust that is difficult for competitors to break. For retail customers, switching costs are lower, limited primarily to the hassle of changing direct deposits and automatic payments, but behavioral inertia keeps many customers in place long after they might find better options elsewhere.

Brand power is regional. Within Wisconsin, Associated Bank is a well-recognized and generally respected brand. Outside the state, brand recognition drops sharply. This limits the bank's ability to attract customers in new markets without significant investment in brand building or acquisition.

Cornered resource and process power round out the analysis. Associated has no proprietary technology, unique intellectual property, or irreplaceable talent that would constitute a cornered resource. Its relationships with customers are the closest analog, but relationships are ultimately portable when bankers move to competitors.

Process power, the ability to execute complex activities with unusual efficiency or quality, is moderate. The post-crisis underwriting culture is genuinely strong, and the bank's risk management processes have been battle-tested. But process advantages are replicable; a competitor can build the same culture with the right leadership and enough time.

The bottom line from both frameworks is sobering but honest: Associated operates in a structurally challenging industry with no truly durable competitive moat. There is no network effect that locks customers in. There is no proprietary technology that competitors cannot replicate. There is no brand power that transcends the upper Midwest. What there is, and what the company must rely on, is execution: doing the basic work of banking, taking deposits, making loans, managing risk, serving customers, a little bit better, a little bit more consistently, than the competition. It is a commodity business that rewards operational excellence and punishes complacency.

That is not a death sentence, and plenty of commodity businesses have created value for shareholders over long periods. Utilities, railroads, and insurance companies are all commodity businesses that, well-managed, generate steady returns. But it does mean that investors in Associated cannot simply buy and forget. The margin for error is thin, and the structural forces of the industry are unforgiving.

XI. Bull vs. Bear Case & Investment Thesis

Every investment thesis is ultimately an argument about the future, and the future for a mid-sized regional bank can be told in two diametrically opposed narratives. Let's lay them both out with intellectual honesty.

The bull case for Associated Banc-Corp begins with management quality. Andy Harmening and his team have demonstrated an ability to drive operational improvement, as evidenced by the efficiency ratio compression, NIM expansion, and record earnings achieved in 2025. Crucially, this is a management team with institutional memory of the 2008 crisis. They know what happens when underwriting discipline slips, and that knowledge is embedded in the culture. In banking, as in medicine, the best practitioners are the ones who have seen what happens when things go wrong.

The valuation argument is straightforward. At roughly 9.5 times normalized 2025 earnings and approximately 1.2 times tangible book value, Associated trades at a meaningful discount to the regional bank peer group average of 11 to 12 times earnings.

The dividend yield of approximately 3.6 percent, supported by 13 consecutive years of increases, provides current income while investors wait for the market to re-rate the stock. A return on average tangible common equity exceeding 15 percent combined with a P/TBV of just 1.2 times suggests either that the market is undervaluing the franchise or that it expects returns to decline.

The interest rate environment, after years of working against regional banks, has swung in their favor. NIM has expanded 25 basis points year over year, and the bank's balance sheet repositioning, which caused painful but deliberate losses in 2023 and 2024, is now paying dividends through higher-yielding assets. If rates stabilize at elevated levels, the bank's earnings power could continue to improve.

The Midwest economy, often dismissed as flyover country by coastal investors, has demonstrated remarkable resilience. Through the pandemic, through the supply chain crisis, through the inflation spike, Wisconsin's diversified manufacturing and agricultural base proved more stable than the technology-dependent economies of Silicon Valley or the financial-services-dependent economy of New York. For a bank whose fortunes are tied to the health of its local economy, Midwest stability is a genuine asset.

There is also the M&A argument. Associated is large enough to be a credible acquirer of smaller institutions, as the American National deal demonstrates, but also small enough to be an attractive acquisition target for larger regional or super-regional banks. Private equity firms have shown increasing interest in banking, and a well-run mid-sized bank with a clean balance sheet and strong Midwest franchise would command a takeout premium. The wealth management business, while still modest in scale, represents an underappreciated growth engine that could become a more significant earnings contributor over time.

The bear case is equally compelling and centers on the structural challenges of mid-sized regional banking. Associated is stuck in a size category that offers few natural advantages. It is too small to compete with the mega-banks on technology spending, product breadth, or brand reach. But it is too large to fly under the regulatory radar or to serve truly local niches with the agility of a community bank.

As the bank approaches the $50 billion asset threshold with the American National acquisition, regulatory costs will increase, potentially offsetting some of the scale benefits.

Long-term margin compression is a legitimate concern. As fintech competition intensifies, as deposit pricing becomes more transparent, and as non-bank lenders continue to cherry-pick the most profitable segments of traditional bank lending, the structural profitability of mid-sized banking may deteriorate. The technology spending arms race is one that Associated cannot win. While the bank has made impressive progress under Harmening, it is competing against institutions that spend more on technology in a single quarter than Associated's total annual operating budget.

Geographic concentration in the slow-growth Midwest is a structural headwind. Wisconsin's population growth lags the national average, and the state lacks the high-growth sectors that drive banking expansion in the Sun Belt and on the coasts. Loan growth requires taking market share from entrenched competitors, which is possible but more difficult than riding demographic tailwinds.

The commercial real estate exposure, while dramatically different from the 2008 debacle, remains a risk factor. At 23 percent of total loans, CRE is a meaningful portion of the book. The post-pandemic shift in commercial real estate usage patterns, particularly in office space, creates uncertainty that will take years to fully resolve. The bank's credit quality metrics are currently pristine, with net charge-offs of just 0.12 percent, but these metrics tend to look best right before they deteriorate.

Finally, the bear case includes the possibility that Associated's long-term destiny is to be acquired, and that the acquisition may come at a less-than-premium valuation. If industry consolidation continues, and if the economics of mid-sized banking become untenable, Associated may eventually find itself in a position where selling is the only rational option. The question is whether the sale price will reflect the franchise value that management has built or whether it will reflect the market's dim view of the mid-sized banking model. History offers mixed precedent: some regional bank sales have generated substantial premiums for shareholders, while others, particularly those forced by deteriorating performance, have been executed at distressed valuations that destroyed wealth for long-term holders.

The KPIs That Matter Most

For investors tracking Associated's ongoing performance, three metrics cut through the noise:

Net Interest Margin (NIM): This is the single most important number for any bank that derives 80 percent of its revenue from the spread business. NIM tells you whether the bank is earning an adequate return on its balance sheet and whether management is effectively navigating the interest rate environment. The trajectory from 2.78 percent in 2024 to 3.03 percent in 2025 is the story of the business right now.

Efficiency Ratio: The percentage of revenue consumed by operating expenses reveals whether management is achieving operating leverage. Associated's improvement from above 60 percent to approximately 56 percent adjusted shows progress, but the best regional banks operate below 55 percent. Continued improvement here is essential for the investment case.

Net Charge-Off Ratio: Credit quality is the third leg of the stool. A low net charge-off ratio confirms that the post-crisis underwriting culture is holding and that loan growth is not coming at the expense of credit discipline. The current 0.12 percent ratio is excellent, but investors should watch for any deterioration, particularly in commercial real estate.

XII. Epilogue & Reflections

Every great survival story has a moment of maximum peril, a point where the outcome could have gone either way. For Associated Banc-Corp, that moment was not a single day but an entire year, stretching from the fall of 2008 through the end of 2009, when the institution's continued existence hung in the balance.

In the winter of 2009, Associated Banc-Corp was worth less than the TARP money the government had just injected into it. The stock traded in single digits. The loan book was riddled with losses. The brand, built over nearly 150 years, was tarnished. Longtime employees wondered whether the bank would exist in six months. Green Bay, Wisconsin, a city synonymous with football and Midwestern grit, faced the possibility of losing its largest homegrown financial institution.

Today, that same bank is worth over $4 billion. It posted record earnings in 2025. It is expanding into new markets. It has repaid every dollar of government assistance, with interest. And it has done so not through financial engineering or aggressive risk-taking but through the oldest strategy in business: doing the simple things well, consistently, for a long time.

The Associated story teaches several lessons about risk management and institutional humility.

The first is that concentration kills. The Arizona real estate exposure was not the result of fraud or incompetence. It was the result of smart people making reasonable decisions that, in aggregate, created an existential risk. Every one of those individual loans might have been sound in isolation. But together, they represented a single, massive, correlated bet. The lesson applies far beyond banking: any business that becomes too dependent on a single customer, a single product, or a single geography is one adverse event away from catastrophe.

The second lesson is about the power of institutional memory. Associated's current risk management culture was forged in the fire of 2008-2009. Employees who lived through the crisis carry that experience into every lending decision, every risk committee meeting, every underwriting review.

This institutional memory is a genuine competitive advantage, but it is also perishable. As the people who experienced the crisis retire and are replaced by a new generation, the challenge is ensuring that the lessons survive. History shows that institutional memory tends to fade over about fifteen years, roughly the span of a career generation. Banks that forgot the lessons of previous crises, from the S&L debacle of the late 1980s to the Asian financial crisis of 1997, were the ones that suffered most in 2008.

The third lesson is about the viability of regional banking in America. The conventional narrative is that consolidation is inevitable, that mid-sized banks are doomed to be acquired by larger ones, and that the industry's future belongs to a handful of mega-banks and a long tail of community institutions.

Associated's story complicates that narrative. It suggests that a well-managed regional bank can survive and even thrive if it maintains discipline, invests in technology, and deepens its relationships with customers who value personal service.

But the honest assessment is that survival is not the same as dominance. Associated has survived for 165 years, and that is remarkable. But it has not built a franchise that generates the kind of excess returns that attract long-term patient capital. It operates in a commodity industry with no durable moat, competing against institutions with vastly greater resources. Its stock trades below its pre-crisis high set nearly two decades ago. Its path forward requires continuous execution without significant margin for error.

The human element is perhaps the most compelling part of the story. Throughout the crisis and recovery, communities across Wisconsin stuck with their bank. Business owners who could have moved their accounts to larger institutions chose to stay. Employees who could have left for more stable employers chose to remain. And customers who had every rational reason to be terrified about the safety of their deposits chose to trust that the institution would survive. That trust was not misplaced, but it was tested in ways that no marketing campaign or annual report can fully convey.

There is a framed photograph in the Green Bay headquarters, the kind of artifact that tells a story if you know what to look for. It shows the bank's employees gathered for a company event in 2012, the year after TARP was repaid. The smiles are not triumphant. They are relieved. These are people who went through something together, something that tested every assumption about the institution they worked for, and came out the other side.

In the end, the most surprising thing about Associated Banc-Corp is the paradox at the heart of its survival story: a 160-year-old institution that had to nearly die in order to learn the most important lesson in banking. That lesson is simple, unglamorous, and endlessly difficult to practice. The lesson is: be boring. Make good loans. Know your customers. Manage your risks. And never, ever forget what happens when you don't.

Whether that lesson, and the execution it demands, is enough to make Associated a compelling long-term investment is a question that each investor must answer for themselves. The company has earned the right to make its case. The numbers are strong. The management is experienced. The franchise is real. But the structural forces arrayed against mid-sized regional banks are formidable, and the history of the industry suggests that most of these institutions will eventually be absorbed into larger ones. Associated's story is not over. It is simply entering its next chapter, and what happens in that chapter will depend, as it always has, on the quality of the decisions made by the people inside that corner office in Green Bay.

XIII. Further Reading

For those who want to go deeper into the Associated Banc-Corp story and the broader context of American regional banking, the following resources provide essential background.

"The Unbanking of America" by Lisa Servon offers a ground-level view of retail banking economics and the forces reshaping how ordinary Americans interact with financial institutions.

Associated Banc-Corp's own 10-K filings from 2007, 2009, and 2023 are primary sources that trace the arc from pre-crisis confidence through the depths of the crisis to the modern rebuild. These documents, available through SEC EDGAR, reveal how management's tone and risk disclosures evolved over time.

Simon Johnson's essay "The Quiet Coup," published in The Atlantic in 2009, places the financial crisis in the broader context of political economy and regulatory capture, essential background for understanding why banks like Associated were allowed to accumulate the risks they did.

The Wisconsin Historical Society Banking Archives provide the deep history of Milwaukee's banking dynasties and the economic forces that shaped the state's financial landscape from the Civil War onward.

Adam Tooze's "Crashed: How a Decade of Financial Crises Changed the World" offers the most comprehensive single-volume account of the 2008 crisis and its global aftermath, providing context for Associated's experience within the broader industry meltdown.

S&P Global Market Intelligence reports on regional banking offer detailed comparative analysis of Associated against its peers, including financial metrics, market share data, and competitive positioning.

FDIC Historical Banking Data provides the raw numbers that track the long consolidation of American banking, from 14,000 institutions in 1985 to fewer than 4,500 today, the secular trend against which Associated's survival must be measured.

Liaquat Ahamed's "Lords of Finance" chronicles the history of central banking and the catastrophic decisions that led to the Great Depression, a reminder that the risks inherent in banking are not new but recur in new forms across generations.

Federal Reserve Bank of Chicago research papers on Midwest banking dynamics provide the academic foundation for understanding the unique competitive and economic forces that shape banking in the upper Midwest.