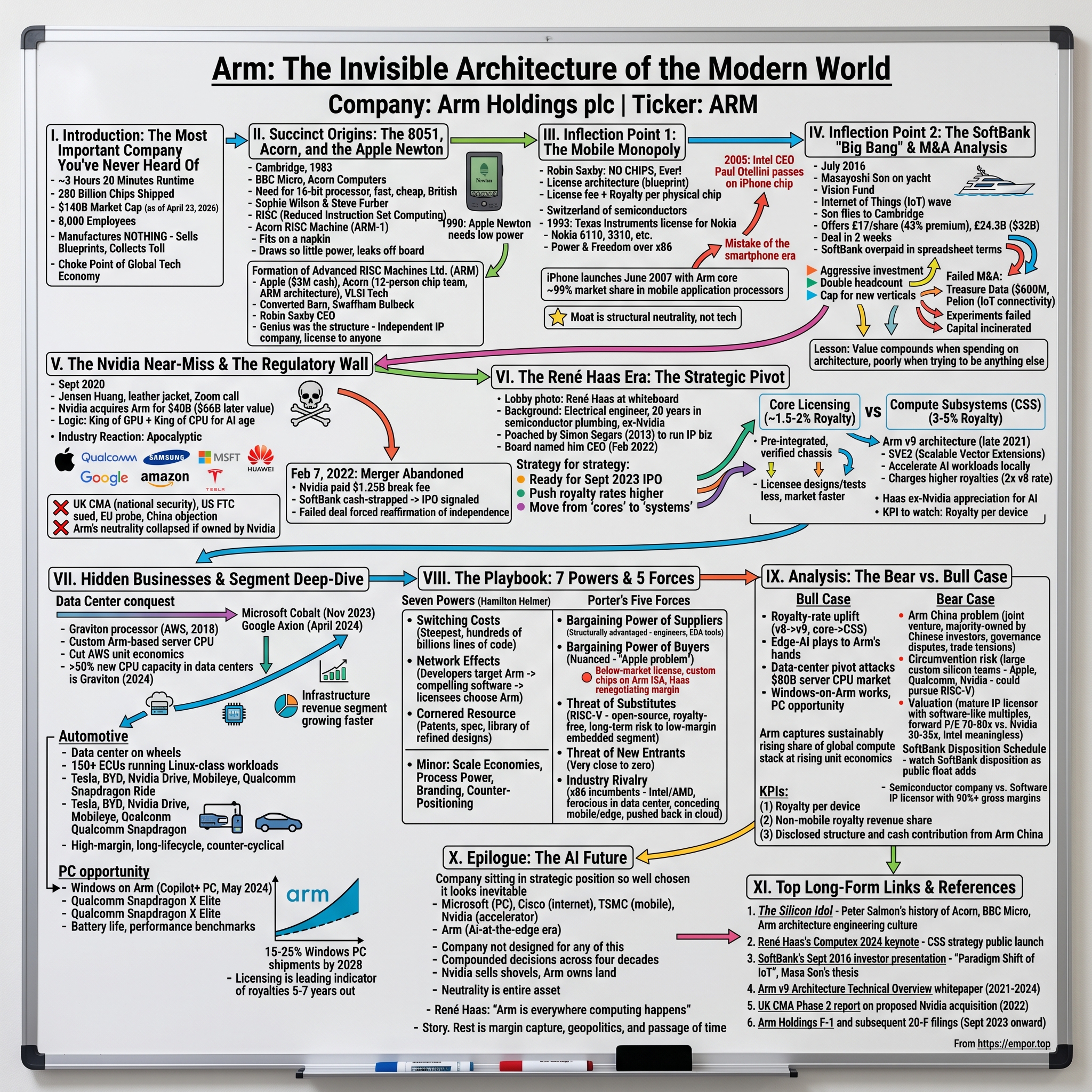

Arm: The Invisible Architecture of the Modern World

I. Introduction: The Most Important Company You've Never Heard Of

Sometime this morning, before the coffee cooled, you picked up your phone. You tapped a screen. You opened an app. You listened to a song, summoned a rideshare, paid a bill, asked a large language model a question that would have looked like witchcraft to a computer scientist a decade ago. Every one of those actions — every single one — was adjudicated, for a fraction of a nanosecond, by a piece of logic designed in a converted turkey barn on the outskirts of Cambridge, England.

That barn is gone now, paved over into a business park. But the logic it birthed lives on in roughly 280 billion chips shipped to date — a number so large it loses meaning unless you anchor it: roughly 35 chips for every human alive. The company behind it, Arm Holdings plc, trades on the Nasdaq under the ticker ARM and sits, as of this recording on April 23, 2026, somewhere in the neighborhood of a $140 billion market capitalization depending on the hour. It employs around 8,000 people. It manufactures, quite literally, nothing.

That last sentence is the whole episode in miniature. Arm is the "Intel of the mobile age" — except Intel spent eighty years and tens of billions of dollars owning its fabrication destiny, and Arm, by contrast, never poured a single wafer of silicon. It sells blueprints. It collects a toll. And for the better part of three decades, it has quietly sat at the exact choke point where the global technology economy does its thinking.

This is a company that was spun out of a failing British computer maker in 1990 as a twelve-engineer joint venture with Apple. It was sold to SoftBank in 2016 for $32 billion, a number Masayoshi Son decided on during what was effectively a weekend holiday. It was almost sold to Nvidia in 2020 for $40 billion — a deal that would have been, for better or worse, one of the most consequential mergers in computing history — before it was strangled in regulatory cribs on three continents. It re-emerged in September 2023 as the year's most anticipated IPO, a listing so oversubscribed that the pricing committee could essentially name its number.

And now, under a CEO named René Haas who most of the financial press still cannot quite place, Arm is attempting something audacious: it is trying, for the first time in its life, to get paid what it is actually worth.

This is the roadmap. We will start in a Cambridge barn. We will pass through a failed Apple tablet, a Nokia flip phone, an iPhone that Intel turned down, a $32 billion buyout that half of SoftBank's board thought was insane, a collapsed Nvidia merger, a 2023 IPO that became the tape-bomb of the year, and a 2026 landscape in which Arm is no longer merely the invisible architecture of your pocket — it is the battleground for who controls the margin structure of artificial intelligence.

Every act of this story is a decision about whether Arm should be a tool, a toll, or a platform. The most interesting part of Arm, in 2026, is that the answer is finally the third.

II. Succinct Origins: The 8051, Acorn, and the Apple Newton

Picture Cambridge in 1983. Margaret Thatcher is in power, synth-pop is on the radio, and every British schoolchild is being introduced to computers for the first time via a strange beige machine called the BBC Micro, made by a small outfit called Acorn Computers. Acorn is, briefly, the Apple of the United Kingdom — a plucky, engineer-led company whose founders, Hermann Hauser and Chris Curry, genuinely believe they can build a British Silicon Valley on the banks of the River Cam.

Their problem is that by the mid-1980s, the BBC Micro is running out of runway. The 16-bit era is coming. Intel's 80286 and Motorola's 68000 are the processors the rest of the world is moving toward. Acorn needs something faster, cheaper, and ideally British. So two young engineers — Sophie Wilson, who had already designed the BBC Micro's BASIC interpreter in her head, and Steve Furber, a motorcyclist-turned-chip architect — are asked to do something that sounds completely deranged. Go design a processor. From scratch. With almost no budget.

What happens next is the kind of story that gets embellished over time, but the embellishments are, mostly, true. Wilson and Furber get their hands on a stack of academic papers out of Berkeley and Stanford about something called Reduced Instruction Set Computing, or RISC — the radical idea that a processor should do a small number of simple things very fast, rather than a huge number of complicated things at uneven speeds. They decide to build one. In the spring of 1985, the first silicon returns from VLSI Technology, and when Furber plugs the chip into a development board, it works. He notices the power supply is reading zero milliamps on the rail. He panics, thinks the chip is dead. Then he realizes — the chip is running. It is just drawing so little power it is leaking off the board through the signal wires.

That chip is the Acorn RISC Machine. ARM-1. Its instruction set fits on a napkin. Its power draw is a tenth of a watt. It does not need a fan. It does not need a heat sink. In an industry where chips were becoming hotter, hungrier, and more expensive every year, Wilson and Furber had accidentally built the opposite.

Fast-forward to 1990. Acorn is drowning; its PC business is being crushed by IBM-compatibles. But a strange telephone rings in Cambridge. It is Apple Computer. John Sculley has a secret project called the Newton — a handheld "personal digital assistant" that needs a chip drawing almost no power because it is supposed to run off a handful of AA batteries for weeks. Apple has looked at every processor on Earth and the only one that fits is the ARM core.

On November 27, 1990, Apple, Acorn, and VLSI Technology announced the formation of a joint venture called Advanced RISC Machines Ltd. — ARM. Apple contributed $3 million in cash. Acorn contributed its 12-person chip team and the ARM architecture itself. The new company was headquartered in a converted barn in the village of Swaffham Bulbeck, outside Cambridge. Its first CEO, Robin Saxby — more on him in a moment — famously said the business plan for ARM's first year was "survive."

The Newton, as everyone now knows, flopped. Apple launched the MessagePad in 1993. It was expensive, its handwriting recognition was so bad it became a Doonesbury punchline, and Steve Jobs killed the product line shortly after returning to Apple in 1998. But the ARM architecture Apple had helped fund did not die with the Newton. It was now in the world, ownership-diversified, engineer-focused, and — critically — not owned by any one chipmaker.

The genius of 1990 was not the chip. The genius of 1990 was the structure — an independent IP company, jointly owned, with a mandate to license its design to anyone who would pay. That structural decision, made almost accidentally, would in seventeen years' time put an ARM core inside the device that reinvented the consumer electronics industry: the iPhone.

III. Inflection Point 1: The Mobile Monopoly

Robin Saxby is worth a moment of your attention, because every company that dominates a market eventually has a founder-CEO whose personality imprints on its strategy, and Saxby is Arm's. Picture a Midlands electronics salesman — not an engineer, not a Cambridge don — who had spent the 1970s and 1980s selling semiconductors for Motorola. Tall, gregarious, allergic to corporate jargon, Saxby walked into ARM in 1991 and did something that the engineers around him found mildly heretical. He decided the company should not build chips at all. Not one. Ever.

The received wisdom in 1991 was that a chip company had three choices. You could be Intel and own your own fabs. You could be AMD and lease fabs. Or you could be a "fabless" designer like the recently founded Qualcomm and have TSMC make your silicon. Saxby rejected all three. He proposed instead that ARM would license its architecture — the blueprint — to other chipmakers, collect a license fee upfront, and then collect a royalty on every physical chip that was ever made using that design. ARM would never touch silicon. ARM would never carry inventory. ARM would never fight a price war.

It sounded insane. It was, in retrospect, one of the most elegant business model innovations in the history of semiconductors. Saxby's pitch to licensees was simple: pay us a few million dollars upfront, then pennies per chip, and in exchange you get the freedom to wrap our core in whatever you want. Add your own radio. Add your own graphics. Add your own accelerators. We do not compete with you. We do not favor your rival. Arm, he told customers, would be the "Switzerland of semiconductors."

The first domino fell in 1993 when Texas Instruments signed a major license deal to use the ARM7 core in a new chip for a Finnish customer. That customer was Nokia. The chip ended up inside the Nokia 6110, which shipped in 1997, and then in the 6210, the 3310, the 8210, and eventually in every cellular handset Nokia made for a decade. Why did Nokia pick ARM over Intel's x86? It was not speed. Intel was faster. It was not price. It was power consumption and, just as importantly, freedom. With Arm, Nokia could design exactly the chip it wanted. With Intel, Nokia would have had to take what Intel gave it.

Between 1998 and 2007, ARM quietly absorbed the mobile phone industry. By the time the iPhone was a glimmer in Steve Jobs's eye, more than 80% of the world's cellphones already had an Arm core inside them. The decisive moment, the one Acquired listeners will recognize, came in 2005. Intel CEO Paul Otellini met with Jobs to discuss making the processor for a secret new Apple device. Apple wanted a custom mobile chip at a specific price point. Otellini, haunted by Intel's famously thin mobile margins, passed. As he later admitted in a Atlantic interview: "The thing you have to remember is that this was before the iPhone was introduced, and nobody knew what the iPhone would do. At the end of the day, their forecast was for a certain price point, and I could not see it."

Intel's pass was the single most expensive strategic mistake of the smartphone era. The iPhone launched in June 2007 with a Samsung-made chip called the APL0098 — which was, under the hood, an Arm11 core. Every subsequent iPhone chip, from the A4 in 2010 through the A19 in the devices on shelves today, is built on the Arm architecture.

By the early 2010s, Arm's market share in mobile application processors had reached something close to 99%. That is not market leadership. That is oxygen. When a technology achieves that kind of coverage, its business ceases to be about winning deals and becomes about collecting a tax on industrial activity.

For investors, the "so what" of the Saxby era is this: Arm's moat is not its technology. Other RISC architectures existed. MIPS existed. PowerPC existed. DEC Alpha existed. The moat was the structural decision that Arm would never compete with its own customers. That single choice is why every major fabless designer on Earth — Apple, Qualcomm, Samsung, MediaTek, NVIDIA, Marvell — felt safe building their entire roadmap on an Arm foundation. Remove that neutrality, and the entire edifice wobbles. Remember that, because it becomes the central issue in the next act of this story.

IV. Inflection Point 2: The SoftBank "Big Bang" & M&A Analysis

It is July 2016. Masayoshi Son is on a yacht off the coast of Turkey, and he is about to write the biggest check of his life.

To understand what happens next, you have to understand Masa Son as he existed in mid-2016. He is 58 years old. He has just convinced the Saudi Public Investment Fund to anchor a $100 billion technology investment pool that will eventually be called the Vision Fund. He has spent the previous five years telling anyone who will listen that the next great technology wave will not be mobile — it will be what he calls the "Internet of Things," a planet in which trillions of sensors, cameras, actuators, and appliances all talk to one another. And he has concluded, correctly, that every single one of those trillion devices will need a chip, and that chip will almost certainly run on Arm.

On July 3, Son flies from Turkey to Cambridge. He sits across a table from Arm's then-CEO Simon Segars and its chairman Stuart Chambers. He does not negotiate. He offers £17 per share in cash — a 43% premium over the previous trading day's close. The total price: £24.3 billion, or about $32 billion at the prevailing exchange rate. He tells Chambers he wants the deal announced within two weeks. In two weeks. For context, comparable transactions of that scale typically take six to twelve months of due diligence.

The deal was announced on July 18, 2016. Arm's board recommended it unanimously. The Brexit referendum, three weeks earlier, had knocked about 12% off the pound, which had the accidental effect of making the deal cheaper for a Japanese buyer. Son later admitted he had been thinking about Arm for a decade and had decided he could not wait any longer.

Was it too expensive? At the time of announcement, the price represented a trailing twelve-month P/E ratio of approximately 71x and an EV/EBITDA multiple north of 40x. That is a growth-software multiple paid for a mature IP licensing business growing low-double-digits. In pure spreadsheet terms, yes — SoftBank overpaid. By how much? Set aside the synergies (SoftBank had none) and compare it to the contemporaneous M&A benchmark set. In the years that followed, Broadcom would pay $61 billion for VMware and AMD would pay $49 billion for Xilinx. Those deals were justified by clear revenue synergies: cross-selling, consolidated R&D, margin capture. SoftBank had nothing like that. It was buying Arm as a financial and strategic holding, not as a combination.

What SoftBank promised in exchange — and this is important for understanding the next seven years — was an aggressive investment program. Son pledged to double Arm's headcount within five years and to pour capital into new verticals that a public Arm, accountable to quarterly earnings, could not have funded. He kept that promise, sort of. Arm's engineering headcount did roughly double between 2016 and 2022. R&D spending nearly tripled.

But SoftBank also did something less wise. It acquired, through Arm, two companies that fit Son's "IoT trillion-sensor" vision but did not fit Arm's architecture-licensing DNA. The first was Treasure Data, a data analytics platform purchased in 2018 for roughly $600 million. The second was Pelion, an IoT connectivity service that Arm itself built out. For four years, Arm's leadership was forced to operate what was essentially a software startup grafted onto a chip IP company, with different gross margins, different sales cycles, and — most corrosively — different cultures.

By 2020, it was clear the experiment had failed. Treasure Data was carved out and sold back to SoftBank as a separate portfolio company in early 2021. Pelion's connectivity business was spun out in 2020. The total amount of capital incinerated on the IoT software side was never cleanly disclosed but is widely estimated in the low hundreds of millions of dollars.

The verdict? Every one of Arm's M&A "swings" during the SoftBank era underperformed. The best capital Arm deployed in those years was not external at all — it was internal. The engineering hires, the v9 architecture project kicked off in 2017, the massive investment in a new data-center-grade CPU called Neoverse. Those returns are the ones that are paying off in 2026.

For investors, the SoftBank chapter carries one durable lesson. Arm's value compounds most reliably when it spends money on its own architecture and most poorly when it tries to become anything else. Keep that in mind when you read the next earnings release.

V. The Nvidia Near-Miss & The Regulatory Wall

In September 2020, Jensen Huang wore his leather jacket to a Zoom call and announced that Nvidia had agreed to acquire Arm from SoftBank for $40 billion — a mix of cash and Nvidia stock that, by the time the deal actually closed (or rather, failed to close), would have been worth closer to $66 billion given where Nvidia's share price ran.

To Huang, the logic was so obvious it barely needed explaining. Nvidia was the undisputed king of the GPU, the most important accelerator for training neural networks. Arm was the undisputed king of the CPU in mobile and edge computing. The combination would produce, in Huang's phrasing, "the premier computing company for the age of AI." Imagine a Grace-Hopper-style superchip, he argued, but years earlier, owned entirely by one company.

The reaction from the rest of the industry was, to put it mildly, apocalyptic. Within weeks, Apple, Qualcomm, Samsung, Microsoft, Google, Tesla, Amazon, and even Huawei — companies that competed with one another on everything else — filed formal objections with regulators in the US, the UK, the EU, and China. They all said, essentially, the same thing: Arm's value to the industry is its neutrality. If Nvidia — which makes processors — owns the IP that competes with Nvidia's own processors, the entire Switzerland proposition collapses. Qualcomm will not trust Arm's roadmap. Apple will worry that Nvidia-friendly instructions get prioritized. MediaTek will fear that licensing terms change. The architecture becomes a weapon.

The regulatory response was correspondingly severe. The UK's Competition and Markets Authority opened a Phase 2 investigation in mid-2021 and, critically, invoked national security concerns. The US FTC sued to block the deal in December 2021. The European Commission opened its own in-depth probe. China's State Administration for Market Regulation was widely expected to block it on competition grounds, but also — more pointedly — because half the world's licensees were Chinese companies that had no intention of taking architectural marching orders from an American-owned entity.

On February 7, 2022, Nvidia and SoftBank officially abandoned the merger. The press release used language about "significant regulatory challenges," which was diplomatic for "there is no version of this deal any government on Earth is going to approve." Nvidia paid SoftBank a $1.25 billion break fee. SoftBank, cash-strapped after the 2021-2022 drawdown in its other Vision Fund bets, immediately signaled that a public listing of Arm would follow.

The Arm Holdings that emerged from the wreckage was a chastened but fundamentally more valuable company. In hindsight, the failed Nvidia deal was arguably the single best thing to happen to Arm in the 21st century. It forced every one of Arm's major licensees to publicly reaffirm why they needed Arm to stay independent. It gave Arm's management a once-in-a-generation negotiating chit with those same licensees. And it cleared the runway for a new CEO — a former Nvidia executive, of all people — to step in and push the company into its next chapter.

For investors, the Nvidia chapter crystallized the core truth of Arm as a business. The moat is not technical. The moat is structural neutrality. Any attempt to re-own that moat through acquisition would have destroyed the very asset being acquired. It is a rare thing in capital markets — a company whose optimal owner is no one. Arm's eventual IPO structure would have to reflect that, and the story of how it did is the next section.

VI. The René Haas Era: The Strategic Pivot

Walk into the main lobby of Arm's Cambridge headquarters today and you will see, mounted in a glass case, a framed photo of a relatively ordinary-looking man in a polo shirt standing in front of a whiteboard covered in acronyms. He is grinning. The acronyms are largely illegible. The man is René Haas, and he is — quietly, methodically — running the most consequential strategic pivot in Arm's history.

Haas's background is worth a minute because it explains almost everything about the post-2022 Arm playbook. He is American, Long-Island-born, with an electrical engineering degree from Clarkson University. He spent twenty years at companies like NEC, Tensilica, and LSI Logic — none of them famous, all of them in the plumbing of the semiconductor industry. Then in 2006, he joined a then-mid-size graphics company called Nvidia, where he eventually became vice president of the "Compute Products" business under none other than Jensen Huang. Haas ran Nvidia's Tegra mobile processor business, which was, uncomfortably for him, an Arm licensee. In 2013, Simon Segars — then Arm's CEO — poached Haas to run Arm's intellectual property business.

Haas spent the next nine years running various businesses inside Arm, building a reputation as the executive who would actually tell the sales force to raise prices. In February 2022, two weeks after the Nvidia deal collapsed, the Arm board named him CEO.

His mandate was simple and brutal. Ready the company for an IPO by September 2023. Push royalty rates higher. Stop apologizing for being expensive. And — this is the deepest shift — move Arm from a company that sells "cores" to a company that sells "systems."

To understand why this matters, you need a brief technology primer. For decades, Arm's product was an instruction-set architecture (the "grammar" of the chip) and sometimes a specific CPU core design (an "engine"). Licensees took the core, wrapped it in their own memory controllers, their own graphics, their own I/O, and shipped a finished chip. Arm collected a royalty of roughly 1.5% to 2% on the final chip's wholesale price.

Under Haas, Arm started doing something new. It started selling what it calls "Compute Subsystems," or CSS. Think of it as the difference between selling someone an engine and selling them a complete, road-ready chassis with engine, transmission, drivetrain, and exhaust all pre-integrated and verified. The licensee now has to design less, test less, and can get to market faster. In exchange, Arm charges far more — royalty rates that industry analysts peg at 3% to 5% of final chip wholesale price on CSS-based designs, more than double the legacy core-only rate.

The other pillar of the Haas pivot is the Arm v9 architecture, which launched in late 2021 and has been the driving force of new designs since 2023. V9 introduced a suite of instructions called SVE2 — Scalable Vector Extensions — designed specifically to accelerate the kind of matrix-heavy math that modern AI workloads rely on. In plain English: v9 chips are much, much better at running AI locally on a device. And because v9 is substantially more complex than v8, Arm charges higher royalties on v9-based chips — roughly 2x the v8 rate on equivalent designs.

Put the two shifts together — v9 displacing v8, and CSS displacing naked core licensing — and you get the core investment thesis of Arm in 2026. The company is not relying on unit volume growth, which is already high. It is relying on royalty rate expansion on a per-unit basis. Arm's management, in its most recent quarterly commentary, characterized this as a mix shift that will play out over five to seven years.

Haas himself is a different sort of CEO than Arm has had before. He is blunt where Saxby was gregarious, metrics-obsessed where Segars was consensus-driven, and — critically — he has an ex-Nvidia appreciation for what the AI era actually requires. He has aggressively shut down several of Arm's older exploratory businesses, cut the IoT software overhang, and reallocated R&D to data center and automotive compute. He has also publicly said, repeatedly, that Arm is "not a CPU company" but a "compute platform" — a linguistic shift that would be easy to dismiss as marketing if you did not understand the CSS strategy underneath it.

For investors, the Haas era has one defining KPI: royalty per device. Unit shipments will grow or shrink based on the global electronics cycle, but the lever under management's direct control is the rate Arm captures on each device. Every quarter, investors should watch whether this number is drifting up, flat, or down. In the quarters since the September 2023 IPO, it has been unambiguously up — and the question for the years ahead is whether Arm can keep bending that curve.

VII. Hidden Businesses & Segment Deep-Dive

Here is a parlor question. Of the last ten thousand server-class CPUs you have interacted with, how many were built on the Arm architecture? If you guessed zero, that was correct five years ago. If you guessed fifty, that was correct two years ago. In 2026, the honest answer is probably closer to one in four, and in some specific workloads it is closer to one in two. Arm's quiet conquest of the hyperscale data center is arguably the most underappreciated compounding story in semiconductors.

Begin with Amazon Web Services. In 2015, AWS acquired a small Israeli chip design firm called Annapurna Labs. It was a modest-looking $350 million deal at the time. In 2018, that team shipped the first generation of what AWS called the Graviton processor — a custom, Arm-based server CPU designed to do one thing: cut AWS's unit economics on commodity compute. Graviton was cheaper to make, drew less power, and ran enough common web workloads well enough that AWS could offer customers a roughly 20% price-performance improvement over x86 instances. By 2024, AWS was publicly stating that more than 50% of all new CPU capacity deployed in its data centers was Graviton-based. Every Graviton core shipped is a royalty for Arm. Every watt of AWS power saved is a dollar Intel and AMD did not earn.

Microsoft followed with Cobalt, its own Arm-based server chip announced in November 2023 and deployed into Azure fleets throughout 2024 and 2025. Google followed with Axion, announced in April 2024 and rolled into Google Cloud during 2025. These are not experiments. These are strategic shifts by three of the four largest computing buyers on the planet — and the fourth, Meta, has its own Arm-based silicon project well underway. Collectively, the hyperscaler shift to custom Arm silicon represents a multi-year, multi-hundred-billion-dollar realignment of the data center CPU market.

For Arm, the financial implication is enormous. Data center chips have a radically higher average selling price than mobile chips — often ten to fifty times higher — and Arm's royalty, though smaller as a percentage, still translates to a much larger absolute dollar per unit. Arm's "Infrastructure" revenue segment, which includes data center and networking, grew meaningfully faster than its mobile segment in fiscal 2025 and is expected to be the largest single driver of incremental royalty dollars through the rest of this decade.

Then there is automotive. A modern car is, not to be glib about it, a data center on wheels. A 2015-era vehicle had maybe 50 electronic control units running largely simple microcontrollers. A 2025-era electric vehicle may have 150-plus ECUs running Linux-class workloads, plus one or two central compute blocks running advanced driver assistance and infotainment stacks. Every one of those nodes is a candidate for an Arm core. Arm's "Automotive Enhanced" product line — v9 cores with functional safety certification for ISO 26262 — has become the default compute stack for next-generation automotive platforms at companies including Tesla, BYD, Nvidia's Drive platform, Mobileye, and Qualcomm's Snapdragon Ride.

The punchline of automotive: it is high-margin, long-lifecycle, and counter-cyclical to the consumer electronics mobile cycle. A design win in 2025 will generate royalty revenue through roughly 2035 as the platform scales and variants proliferate.

And then there is the long-rumored, finally-real PC opportunity. For two decades, people have said "Windows on Arm" was coming. For most of those two decades, it was not. In May 2024, Microsoft launched the Copilot+ PC initiative, anchored around Qualcomm's Snapdragon X Elite chip — which is, of course, Arm-based. For the first time, a mainstream Windows laptop could match or beat an equivalent Apple MacBook Air on battery life, fan noise, and in many benchmarks on performance. Qualcomm shipped meaningful volume through 2024 and 2025. MediaTek and Nvidia each announced their own Arm-based Windows PC chips in 2025, with commercial launches through 2026.

The PC market is roughly 250 million units a year. Arm's share in 2023 was effectively zero outside the Mac. Industry forecasts range wildly but cluster around Arm taking 15% to 25% of Windows PC shipments by 2028. That is, at the high end, 40+ million additional royalty-bearing units at data-center-adjacent ASPs.

Stitch these segments together and the 2024-2026 mix shift in Arm's revenue is striking. Mobile is still the majority of royalty revenue but is now low-growth. Infrastructure, automotive, and PC are the three compounding engines, and all three are sitting at or near the beginning of their adoption curves. Licensing revenue — the upfront fee customers pay for new architectural licenses — has accelerated sharply through the AI buildout as every hyperscaler, every auto OEM, and every second-tier chip startup rushes to get access to v9 and CSS. Licensing is the leading indicator of royalties five to seven years out. When you hear Arm management talk about "record licensing quarters," that is what they are telegraphing.

For investors, the segment KPI to watch is not total revenue. It is the share of quarterly royalty revenue coming from non-mobile end markets. That number has crossed 40% for the first time and its continued expansion is the cleanest evidence of the Haas-era strategy working.

VIII. The Playbook: 7 Powers & 5 Forces

A lot of analysts, when they try to reason about a company, reach first for Porter's Five Forces and then for Hamilton Helmer's Seven Powers. For most companies, one of those frameworks lights up obviously and the other one is fuzzy. For Arm, both frameworks resolve into almost cartoonishly sharp pictures, and they tell you exactly where the business is strong and exactly where it is vulnerable.

Start with the Seven Powers. The primary power Arm enjoys is what Helmer calls Switching Costs, and they are among the steepest in modern technology. Every line of code ever written for an iPhone, an Android phone, an AWS Graviton instance, an automotive ECU, a smart thermostat — every one of those is compiled against the Arm instruction set. Estimates of the total installed base of Arm-compiled software range into the hundreds of billions of lines of code. To move from Arm to, say, RISC-V, a company must either recompile (which is nontrivial but possible for cleanly written high-level code) or rewrite from scratch (which is the case for any assembly, driver, firmware, or performance-tuned kernel). The cost of such a transition is measured not in dollars but in engineer-years, and compounded across an ecosystem of thousands of partners, it is essentially prohibitive.

The second power is Network Effects, and here Arm enjoys a classic two-sided flywheel. More Arm devices in the world mean more developers target Arm natively. More Arm-native developers mean more compelling software stacks on Arm. More compelling stacks mean more licensees choose Arm for their next design. Repeat. This dynamic is why ISA competitions almost always collapse to one dominant standard (x86 in PCs for decades, Arm in mobile). ISA markets behave like QWERTY keyboards.

Third, Cornered Resource. Arm owns the patents underpinning the instruction set, the architectural specification itself, and a library of production-grade CPU and GPU designs refined across thirty-five years of engineering. Even if a competitor wanted to clone the architecture (and was willing to accept the patent risk), recreating the tooling, the verification infrastructure, and the ecosystem of third-party IP that Arm enjoys is a decade-long project with no obvious commercial payoff.

The remaining four powers — Scale Economies, Process Power, Branding, and Counter-Positioning — are minor contributors. Arm is modestly strong on process power (the v9 architecture required institutional knowledge few can replicate) but these are not the load-bearing columns.

Now Porter. On Bargaining Power of Suppliers, Arm is structurally advantaged: its inputs are engineering talent and EDA tools, and while both are in some sense scarce, neither is concentrated in a way that gives any single supplier leverage. On Bargaining Power of Buyers, the picture is more nuanced, and this is where the real interesting investor conversation happens.

The "Apple problem," as it is sometimes called in the industry, is the fact that Apple holds an architectural license — a perpetual, below-market license to design its own Arm-compatible chips without using any of Arm's specific CPU cores. Apple pays Arm a royalty on every chip it ships, but the rate is widely understood to be the lowest in the industry. Apple can, in principle, design entirely custom chips on the Arm architecture and pay Arm essentially a fixed cost per device. This structural discount has been in place since 1990. Every subsequent CEO at Arm has looked at Apple's contribution to total revenue, looked at Apple's share of units, winced, and moved on.

Haas, for the first time, is reportedly renegotiating the economic structure of Apple's relationship at the margin — specifically around access to new v9 instruction blocks and AI extensions. The details are not public, but industry reporting suggests a modestly uplifted royalty on Apple's 2026+ chip generations. If true, even a small rate increase on Apple's volume would be financially material.

The Threat of Substitutes force is where you will hear the acronym RISC-V. RISC-V is an open-source instruction set architecture, meaning its specifications are freely available to anyone, royalty-free. Its cheerleaders argue that RISC-V will eat Arm from below the way Linux ate proprietary Unix. The Acquired take on RISC-V in 2026 is more measured. RISC-V has real traction in embedded microcontrollers — the sub-$1 chip market for things like door sensors, TV remotes, and simple industrial controllers — because at that price point, a zero-royalty architecture is genuinely disruptive to Arm's $0.02-per-chip economics. RISC-V has some early traction in specialized AI accelerators, where startups want total freedom. But in the performance CPU tier — phones, laptops, servers — the ecosystem gap between Arm and RISC-V remains measured in years, not months. The smart investor reads RISC-V as a long-term risk to Arm's low-margin embedded segment, not its high-margin compute core.

Threat of New Entrants in instruction-set architectures is very close to zero. The last successful new ISA (meaning one that achieved meaningful commercial scale) was Arm's v1 in 1985. Industry Rivalry is largely confined to the x86 incumbents — Intel and AMD — who are ferocious at defending the existing data center CPU market but who have effectively conceded mobile and edge to Arm and are now being pushed back in cloud.

Net-net: Arm is one of the most structurally powerful businesses in technology. The primary risk vectors are (a) whether buyer power — especially from Apple and the hyperscalers — ever translates into rate pressure, and (b) whether RISC-V climbs up-market faster than expected. Both are real. Neither is imminent.

IX. Analysis: The Bear vs. Bull Case

Every good business is a coiled argument between its believers and its skeptics. The interesting ones are not the ones where the bulls are obviously right or the bears are obviously right — those are trading opportunities, not investment theses. The interesting ones are where both sides have genuinely defensible claims on the same set of facts. Arm in 2026 is one of those.

The Bull Case rests on four pillars. First, the royalty-rate uplift from v8 to v9 and from core licensing to CSS is real, ongoing, and largely within management's control. Arm is effectively running a price-increase strategy disguised as a technology strategy, and because the underlying technology genuinely is better, the licensees do not have the option of saying no. Second, the edge-AI thesis — the idea that more and more inference will happen on the device rather than in the cloud to preserve privacy and save latency — plays directly into Arm's hands, because every edge device on Earth already runs on Arm. More AI at the edge means more v9 cores, higher royalty rates, and more licensing upfront. Third, the data-center pivot driven by AWS, Microsoft, Google, and Meta is structurally attacking the $80 billion server CPU market that Intel and AMD have split, and every percentage point of share Arm takes is a long-duration annuity of royalties. Fourth, Windows-on-Arm finally works, and the PC opportunity alone could add tens of millions of new royalty-bearing devices per year at attractive ASPs.

The bull case, in one sentence: Arm captures a sustainably rising share of the global compute stack and does so at sustainably rising unit economics. That is the kind of setup where software-like multiples are arguably defensible.

The Bear Case is equally serious and rests on three pillars. First, the Arm China problem. Arm's Chinese operations, through a peculiar joint venture structure negotiated back in 2018, are not wholly controlled by Arm Holdings. Arm Technology (China) Company Limited is majority-owned by a consortium of Chinese investors, with Arm retaining a minority stake and ongoing licensing royalties. The entity has had governance disputes that spilled into public view, and U.S.-China trade tensions continue to cast a shadow over what portion of royalty revenue from Chinese licensees ultimately flows back to Arm Holdings. Arm China is not a rounding error — it represents low-double-digit percent of total reported revenue, and any structural disruption there is material. Management has, since the IPO, been more transparent about the arrangement than in prior years, but the fundamental structural ambiguity remains.

Second, the circumvention risk. Apple, Qualcomm, Nvidia, and the hyperscalers all have large custom silicon teams. In theory, any of them could pursue a mixed strategy in which some workloads migrate to RISC-V-based internal designs, using Arm only where the ecosystem demands. The early signs of this are real: Qualcomm's 2021 acquisition of Nuvia (a CPU-design startup that had already had a substantial license dispute with Arm) and the subsequent ARM lawsuit produced a 2024 trial that was largely inconclusive but that revealed the strain in what had previously been the industry's most sacred relationship. If the largest customers begin to hedge their Arm exposure, even gradually, the long-term royalty base contracts.

Third, valuation. Arm trades on multiples more typical of a high-growth enterprise software company than of a mature semiconductor IP licensor. At the time of this recording, Arm's forward P/E is in the range of 70-80x depending on how one treats stock-based compensation, against an Nvidia forward multiple in the 30-35x range and an Intel multiple that is arguably meaningless given its earnings trough. The bear's question is not whether Arm is a great business — nobody serious argues that. The question is whether the public market is paying too much today for a great business tomorrow. Historically, when semiconductor companies have traded at sustained software-like multiples, reversion to the industry mean has been painful.

A material second-layer item for the file: Arm's stock is still more than 80% owned by SoftBank. Every marginal share that SoftBank elects to sell in the open market (the company has periodically done so since the lockup expired) adds to public float and tests price discovery. Watch the SoftBank disposition schedule as closely as the fundamental KPIs.

One more piece of disciplined analysis. Benchmarking Arm's multiple: if you believe Arm should trade like a semiconductor company, it is expensive. If you believe Arm should trade like a software IP licensor with 90%+ gross margins and a multi-decade royalty annuity — which is what it actually is — the multiple looks more defensible. Where you land on that question should determine where you land on the stock. That is not a recommendation. It is a framework.

The three KPIs to watch going forward: (1) royalty per device, which captures the rate-expansion thesis in a single number; (2) non-mobile royalty revenue share, which captures the end-market diversification thesis; and (3) the disclosed structure and cash contribution from Arm China, which is the clearest single proxy for the geopolitical overhang. Ignore most other metrics management throws at you. Those three matter.

X. Epilogue: The AI Future

Every so often in technology history, a company ends up sitting in a strategic position so well chosen that it looks, in retrospect, almost inevitable — as if the company had been designed from inception for the moment it is currently having. Microsoft in the PC era. Cisco in the internet era. TSMC in the mobile era. Nvidia in the accelerator era. Arm, in the AI-at-the-edge era, fits that template.

What makes Arm's position unusual is that the company was not designed for any of this. A small team of engineers in a Cambridge barn in 1985 wanted to build a chip cool enough not to need a fan. A small spun-out company in 1990 needed to find a customer — any customer — that would keep the lights on. A sales-trained CEO in 1991 decided to license rather than manufacture because it was the only path available to a business with no capital. None of those decisions were aimed at 2026. All of them, compounded across four decades, produced the architecture that now sits underneath roughly every device that does anything interesting with artificial intelligence outside the cloud.

The closing thought is a cliché for a reason. In the 21st-century gold rush of AI, Nvidia sells the most valuable shovels anyone has ever built. Arm, quietly, owns much of the land those shovels are digging in. The royalties are smaller per unit. The volume is larger. The duration is longer. The neutrality — fought for in 1990, tested in 2016, almost surrendered in 2020, and re-won in 2022 — is the entire asset.

René Haas ends nearly every investor conversation with the same line: "Arm is everywhere computing happens." In 2026, that sentence is more literally true than at any point in the company's history. Whether it continues to be true in 2030 depends on whether the company can keep expanding the scope of "everywhere" faster than its largest customers can expand the scope of "not Arm."

That is the story. The rest is margin capture, geopolitics, and the passage of time.

XI. Top Long-Form Links & References

- The Silicon Idol — Peter Salmon's history of Acorn Computers, the BBC Micro, and the engineering culture that produced the original Arm architecture.

- René Haas's keynote at Computex 2024, which laid out the CSS strategy in public for the first time.

- SoftBank's September 2016 investor presentation, "The Paradigm Shift of IoT," which remains the clearest articulation of Masa Son's original thesis for the Arm acquisition.

- The Arm v9 Architecture Technical Overview whitepaper, published by Arm in 2021 and updated through 2024.

- The UK Competition and Markets Authority's Phase 2 report on the proposed Nvidia acquisition, published 2022 — the most substantive public document on why the deal failed.

- Arm Holdings F-1 and subsequent 20-F filings from September 2023 onward, which contain the first rigorous public disclosures of Arm's segment economics and Arm China structure.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube