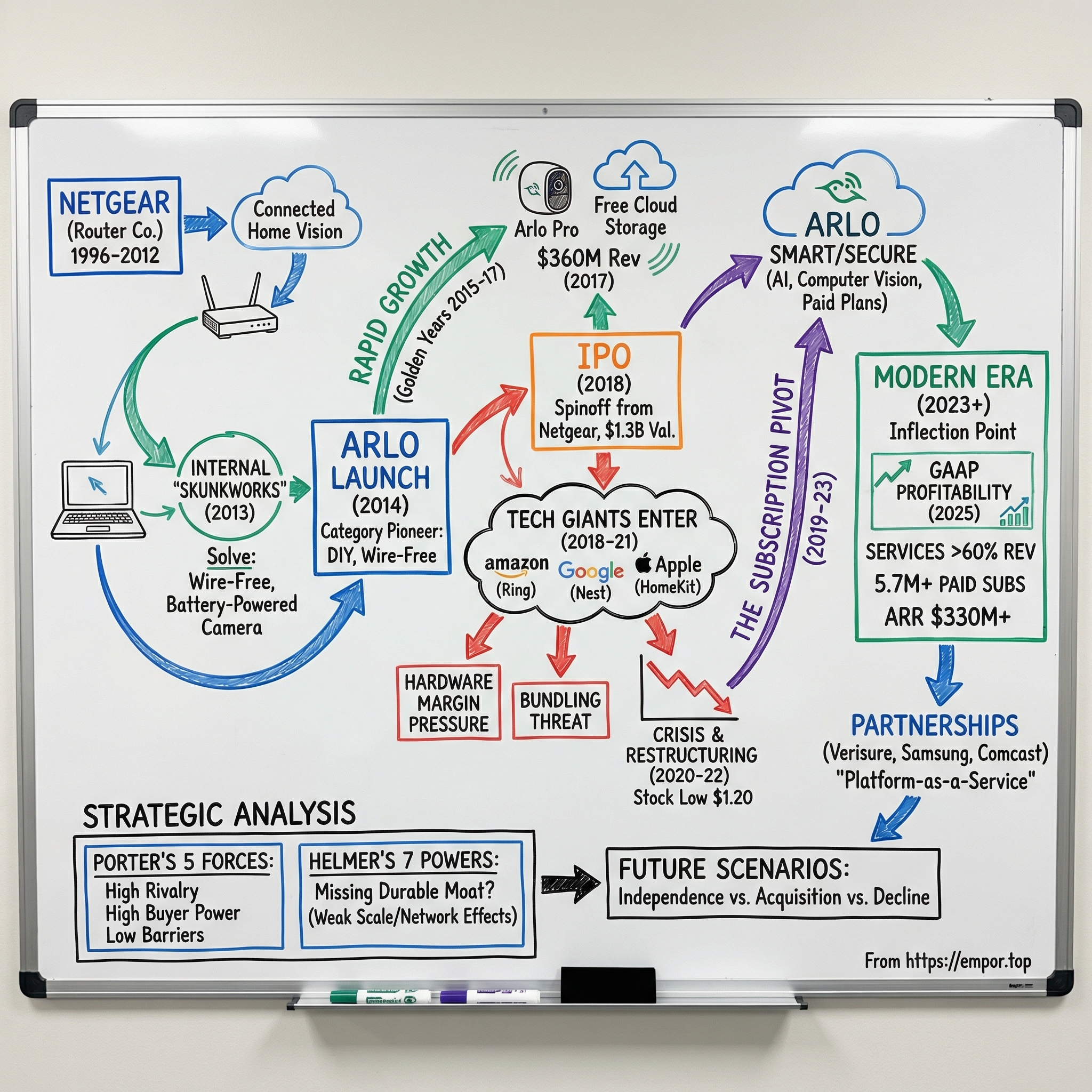

Arlo Technologies: The Story of the Standalone Smart Home Security Pioneer

I. Introduction and Episode Roadmap

Here is a question worth sitting with: How does a router company accidentally create a billion-dollar home security business, and then decide the best thing to do is set it free?

That is the story of Arlo Technologies, the pure-play wireless security camera company that began life as an internal skunkworks project inside Netgear—the company best known for the black box sitting in your living room blinking green lights at two in the morning. Netgear saw something in the early 2010s that most networking companies missed: the router was not just a utility, it was a gateway. And if you controlled the gateway, maybe you could control what flowed through it—including video from security cameras that homeowners were increasingly hungry to install themselves.

What followed was one of Silicon Valley's more unusual corporate births. Arlo grew from a side project into Netgear's fastest-growing division, got spun off in a 2018 IPO that valued it at roughly $1.3 billion, and then promptly found itself in the crosshairs of the largest technology companies on the planet. Amazon bought Ring. Google already owned Nest. Apple started bundling security camera storage into iCloud. And suddenly, the plucky little wire-free camera company that had pioneered a category was fighting for oxygen in a room full of giants who could afford to give away the very product Arlo needed to sell at a profit.

Today, Arlo generates roughly $530 million in annual revenue, has crossed 5.7 million paid subscribers, and just posted its first year of GAAP profitability. The stock, which touched as low as $1.20 during the pandemic panic of March 2020, recently surged past $15 after a blowout fourth quarter. It is a comeback story, a cautionary tale, and an ongoing strategic puzzle all wrapped into one.

The structure of this deep dive runs from Netgear side project to standalone public company navigating the subscription revolution. Along the way, the narrative passes through golden-age growth, a bruising IPO, a near-death experience, a business model transformation, and a set of strategic questions that extend well beyond Arlo to every hardware company fighting platform giants.

The central question running through every section is deceptively simple: Can an independent hardware company survive—and thrive—when tech giants bundle similar products for free as ecosystem bait? The answer illuminates something fundamental about competitive moats, subscription economics, and the brutal realities of building a consumer hardware business in the platform era.

To understand how Arlo got here—and where it might go—requires starting at the very beginning, with a networking company that had no business being in the camera business at all.

The story begins not with cameras, but with routers.

II. Prehistory: Netgear's Journey and the Connected Home Vision (1996–2012)

Patrick Lo founded Netgear in 1996 with a straightforward thesis: networking equipment was about to go mainstream. In the mid-nineties, networking was still an enterprise affair—Cisco sold expensive routers to corporations, and home internet meant a dial-up modem screeching through your phone line. Lo, a Hewlett-Packard veteran born in China and educated in Australia, saw the consumer opportunity before most. Broadband was coming. Homes would need routers. And someone had to make them affordable and simple enough for a non-technical person to set up in their living room.

Netgear carved out a profitable niche doing exactly that. The company went public on the Nasdaq in 2003 and grew steadily through the broadband boom, selling routers, switches, and network-attached storage devices through retail channels like Best Buy and Costco. By the late 2000s, Netgear was doing north of a billion dollars in annual revenue. It was not glamorous work—routers are the textbook definition of a commodity product—but Lo ran a tight ship with healthy margins and disciplined operations.

The problem with commodity hardware, though, is that it commoditizes. Router margins compressed relentlessly as TP-Link, D-Link, and a parade of Asian manufacturers drove prices down. Lo needed a higher-margin growth vector, and he started to see one emerging in the early 2010s: the connected home.

The thesis was intuitive. If Netgear already owned the home network—the pipes through which all smart home data would flow—why not own some of the devices on those pipes too?

The market was sending clear signals. Dropcam, a San Francisco startup, had launched in 2009 with a simple Wi-Fi camera that streamed video to the cloud. It was a revelation—no DVR boxes, no coaxial cables, no professional installer drilling holes in your walls. Just plug it in, connect to Wi-Fi, and watch your living room from your phone. By 2012, Dropcam was one of the best-selling cameras on Amazon.

Tony Fadell's Nest Labs, which had launched with its iconic learning thermostat in 2011, was starting to signal interest in cameras too.

Meanwhile, the traditional home security market—dominated by ADT, Vivint, and a constellation of regional alarm companies—was ripe for disruption. These incumbents operated on a model that had barely changed since the 1980s: a technician came to your house, drilled sensors into your doors and windows, ran wires through your attic, installed a keypad by the front door, and locked you into a three-to-five-year monitoring contract at $30 to $50 a month. For renters, apartment dwellers, or anyone who just wanted to keep an eye on their front porch, the traditional model was overkill.

Three forces were converging to create what turned out to be a massive market opportunity. First, broadband penetration in American households had crossed 70 percent, meaning most homes had the internet speeds necessary to stream video. Second, smartphones were reaching ubiquity—by 2012, more than half of American adults owned one—which meant the "monitor" for your security system was already in your pocket. And third, cloud computing costs were plummeting, making it economically feasible to store and process video in the cloud rather than on expensive local hardware.

Netgear's leadership debated the classic build-versus-buy question. They could acquire a company like Dropcam—which Google would end up buying in 2014 for $555 million—or they could build something from scratch. Lo and his team chose to build internally, and they made a crucial decision that would define Arlo's identity: they would focus on wire-free cameras.

Every competitor at the time—Dropcam, Nest, the cheap Chinese cameras flooding Amazon—required a power outlet. Netgear bet that the killer feature was not better video quality or a slicker app. It was the ability to put a camera anywhere, indoors or outdoors, without running a single wire.

That bet would prove prescient—but the engineering challenge of making it work was far harder than anyone at Netgear initially appreciated. Making a camera run for months on batteries while delivering reliable video over a wireless connection required rethinking nearly every assumption about how security cameras worked.

III. Birth of Arlo: The Netgear Incubation (2013–2014)

Picture a conference room in Netgear's San Jose headquarters in early 2013. The whiteboard is covered in sketches of what looks like an oversized golf ball—a white, rounded camera with a magnetic mount. The engineering team is wrestling with a problem that sounds simple but is fiendishly difficult: How do you build a camera that runs on batteries and lasts for months?

The physics work against you at every turn. Video is data-hungry. Streaming high-definition video continuously over Wi-Fi would drain a set of lithium batteries in hours, not months. The engineers needed the camera to be smart enough to know when to wake up—when there was actually something worth recording—and sleep the rest of the time.

This meant building sophisticated motion detection that could distinguish between a person walking up your driveway and a tree branch swaying in the wind, all while consuming almost no power. Think of it like a guard dog that somehow needs to be simultaneously alert and asleep.

The team solved the problem through a combination of hardware and software innovation. The camera used a passive infrared sensor—the same basic technology used in those automatic hallway lights that turn on when you walk past—to detect motion. Only when the PIR sensor triggered would the camera wake up its processor, connect to the base station, and begin recording.

The base station, which plugged into the home router, acted as a relay—handling the heavy lifting of internet connectivity so the camera itself could stay in a low-power state. It was a clever architectural decision that traded a small amount of latency (the camera took a couple of seconds to wake up) for dramatically extended battery life. The original Arlo cameras ran on four CR123 lithium batteries and lasted four to six months under typical use.

The target customer was specific and deliberate: the do-it-yourself homeowner who wanted basic security monitoring without a professional installation or a long-term contract. This was explicitly not the ADT customer who wanted a full-house alarm system with professional monitoring and a panic button. It was the suburban homeowner who wanted to see who was at the front door, keep an eye on the backyard while on vacation, or check in on their garage.

The "job to be done," in Clayton Christensen's framework, was peace of mind—not fortress-level security.

Arlo launched in late 2014 as a Netgear product, initially sold through the retailer channels where Netgear already had deep relationships. Best Buy gave it prominent shelf space. Costco, which had been a cornerstone of Netgear's distribution strategy for years, featured Arlo in its electronics section. Amazon was a major online channel.

The initial system—a base station and two cameras—retailed for around $350, positioning it above the cheap Chinese cameras on Amazon but well below the cost of a professional installation.

The early reception was encouraging. Tech reviewers praised the wire-free design as genuinely novel. Wirecutter, the influential product review site, named Arlo its top pick for outdoor security cameras. Consumer adoption followed the pattern Netgear had hoped for: customers bought a starter kit, experienced the ease of installation—literally just stick the magnetic mount on a wall and snap the camera onto it—and then came back to buy additional cameras for the back door, the side yard, the baby's room.

The average Arlo household ended up with between two and three cameras, creating a small but meaningful installed base that would later become the foundation for the subscription business.

What made this moment strategically significant was not just the product's success, but what it represented in category terms. Arlo was not competing head-to-head with existing security cameras. It was creating a new category—the wire-free, DIY, app-connected home camera—that sat between the cheap indoor Wi-Fi cameras and the expensive professional systems. Category creation is the holy grail of product strategy because it lets you define the rules rather than play by someone else's.

For a brief, golden window, Arlo owned this category almost entirely by itself.

The strategic importance of category creation cannot be overstated. When a company creates a new category, it gets to define the purchasing criteria, set the initial price anchor, and build the first brand associations in consumers' minds. For Arlo, "wire-free security camera" meant Arlo in the same way that "video doorbell" would soon mean Ring. These mental associations are extraordinarily valuable—and extraordinarily difficult to dislodge once established.

But windows close. And the companies peering through this particular window had very deep pockets.

IV. The Golden Years: Rapid Growth and Market Leadership (2015–2017)

The numbers told a story of almost absurd growth. In 2016, Netgear's "Arlo" segment—which the company had begun breaking out separately in its financial reporting, a signal of its growing importance—generated approximately $287 million in revenue. By 2017, it had grown to roughly $360 million. For context, Netgear's entire company revenue was about $1.4 billion, meaning Arlo had grown from a side project to more than a quarter of the parent company's business in just three years.

Product iteration was relentless during this period. The original Arlo cameras were good, but limited—720p resolution, no audio, no rechargeable batteries. The Arlo Pro, launched in 2016, addressed all three: 1080p video, two-way audio so you could talk through the camera from your phone, and rechargeable battery packs that eliminated the need to buy disposable batteries.

The Arlo Pro 2, which followed in 2017, added an activity zone feature—you could draw a virtual box around your driveway and only get alerts when motion was detected in that zone—and the ability to plug in for continuous power if you had an outlet nearby.

Each product generation expanded the addressable market. The original Arlo appealed to early adopters willing to tinker. The Pro series brought in mainstream consumers who expected polish and convenience.

Around the core camera products, Arlo built an ecosystem of accessories that deepened the customer relationship: solar panels that could power outdoor cameras indefinitely, weather-resistant skins in various colors, and mounts designed for specific use cases like ceiling installation or pole mounting. The base station evolved from a simple relay into a local hub that could connect to smart home platforms like Amazon Alexa, Google Assistant, Apple HomeKit, Samsung SmartThings, and IFTTT.

Distribution expanded in parallel. Arlo moved beyond its North American retail strongholds into European markets, partnering with retailers and distributors across the UK, Germany, France, and Scandinavia. The direct-to-consumer channel, through arlo.com, grew as a complement to retail. Importantly, Arlo was also sold through Amazon.com—a channel that would become increasingly awkward as Amazon prepared to enter the exact same market.

The subscription model was still embryonic during this period, but the seeds were being planted. Arlo offered free cloud storage—seven days of video recordings for up to five cameras—as a core value proposition. This was generous by industry standards and served as a powerful customer acquisition tool.

For customers who wanted more, Arlo offered CVR (Continuous Video Recording) plans that stored 24/7 footage in the cloud for a monthly fee. But the penetration of paid plans was low. Most customers were perfectly happy with the free tier.

This was the paradox at the heart of Arlo's golden years. The company was growing explosively, but it was growing on a hardware-centric business model with thin and compressing margins. Every camera sold was a one-time transaction. The recurring revenue base was tiny.

And the competitive landscape was about to get dramatically more intense.

Ring, founded by Jamie Siminoff in 2013—famously after being rejected on Shark Tank—had found its own explosive product-market fit with the video doorbell. By 2017, Ring was generating hundreds of millions in revenue and had raised over $200 million in venture capital. Nest, acquired by Google for $3.2 billion in 2014, was expanding from thermostats into cameras and doorbells. A wave of ultra-budget Chinese cameras from brands like Yi, Reolink, and the soon-to-be-disruptive Wyze—which would launch a $20 camera in late 2017—threatened to commoditize the hardware from below.

Inside Netgear, a strategic question was crystallizing. Arlo's growth was spectacular, but it was also masking the stagnation of Netgear's core router business. The stock market was valuing Netgear primarily on its mature, slow-growth networking division, effectively giving Arlo little credit.

Meanwhile, Ring—a private company without Arlo's revenue—was attracting a valuation north of a billion dollars. The logic was becoming inescapable: Arlo might be worth more outside Netgear than inside it. Patrick Lo had built Netgear into a disciplined, profitable hardware company. But the next chapter of the Arlo story would require a different kind of thinking—the mindset of a growth-stage technology company willing to burn cash to build a subscription empire while simultaneously defending market share against the largest companies in the world. Whether Arlo could make that transition while going through the wrenching process of becoming an independent public company was about to be tested in the most public way possible.

V. The Carve-Out Decision and IPO (2018)

In August 2017, Netgear formally announced its intention to explore a separation of Arlo from the parent company. The word "explore" is important—it is the corporate equivalent of putting a house on the market to "see what it's worth." But everyone involved knew the direction of travel.

Lo and the Netgear board had concluded that the two businesses were diverging strategically, and keeping them under one roof was creating a classic conglomerate discount.

The bull case for separation was compelling on multiple levels. As an independent company, Arlo would get a pure-play valuation—investors who wanted exposure to the high-growth smart home security market could buy Arlo stock without having to also own a slow-growth router business. Arlo would have its own currency for acquisitions and employee compensation, making it easier to attract and retain talent in the fiercely competitive Bay Area market. Capital could be allocated specifically to Arlo's needs without having to compete with Netgear's own priorities.

The bear case was equally real, if less discussed publicly. Inside Netgear, Arlo had access to shared services—supply chain management, finance, legal, HR—that would need to be replicated or contracted out. Netgear's retail relationships, built over two decades, provided Arlo with distribution reach that a standalone startup could only dream of. And most critically, Arlo as a division did not have to worry about quarterly earnings pressure from Wall Street. As an independent public company, every miss would be magnified.

The IPO arrived on August 3, 2018. Arlo priced at $16 per share, raising approximately $176 million and valuing the company at roughly $1.3 billion.

The timing, in hindsight, was both impeccable and terrible—impeccable because it came just before the broader market wobble of late 2018, and terrible because Amazon had already announced its acquisition of Ring for a reported $1.2 billion earlier that year in February. That acquisition sent a clear signal: the world's most aggressive technology company was now directly in Arlo's lane, with effectively unlimited resources to compete.

Netgear retained approximately 84.5 percent of Arlo's shares post-IPO, planning a gradual divestiture over time. Matthew McRae, a Netgear veteran who had led the Arlo division, became CEO of the newly independent company. McRae was an engineer by training—the kind of leader who understood the guts of the product and could hold his own in conversations about sensor architecture and video compression algorithms.

What remained to be seen was whether he could also navigate the very different challenge of managing a standalone public company through a strategic transformation.

The post-IPO honeymoon was brief. Arlo's stock briefly touched $23 in late August 2018, then began a decline that would continue, with painful intermissions, for years. The market's initial enthusiasm curdled as investors started to grapple with the core question: How does a hardware company with thin margins and a negligible subscription base compete against Amazon, which has every incentive to sell Ring cameras at cost—or even at a loss—to drive Prime subscriptions and Alexa adoption?

The IPO structure itself created an overhang. With Netgear holding 84.5 percent of shares, the float was thin, and every Netgear stock sale created selling pressure.

One detail from the S-1 filing is worth pausing on. Arlo disclosed that the vast majority of its revenue came from hardware sales, with service revenue representing a small fraction. The free cloud storage tier—which had been a brilliant customer acquisition tool during the growth phase—was now a liability on the balance sheet. Every camera sold added another user consuming free cloud storage, increasing costs without a corresponding revenue stream.

The S-1 laid out the strategic intent to shift toward a subscription model, but intent and execution are separated by a chasm that many companies never cross.

There is also a regulatory note worth flagging here. As a publicly traded company handling home security video—streams from inside and outside millions of homes—Arlo entered a regulatory landscape that was becoming increasingly complex. Data privacy laws, from GDPR in Europe to evolving state-level legislation in the United States, created compliance obligations that would only grow over time. The handling of biometric data, such as facial recognition features, carried particular sensitivity. This was not just a legal consideration but a competitive one: privacy-conscious consumers increasingly viewed data handling practices as a purchasing criterion, potentially favoring Apple's privacy-first approach or local-storage solutions from competitors like Eufy.

Arlo entered public life as a hardware company in a market that was rapidly being reshaped by subscription economics, platform bundling, and trillion-dollar competitors.

VI. The Subscription Pivot and Business Model Evolution (2018–2020)

The economics of consumer hardware are punishing, and the Arlo team understood this acutely. A security camera is a physical object that must be designed, manufactured, shipped, stocked on retail shelves, and supported with warranty service. Each unit has a bill of materials—the chips, sensors, plastics, batteries, and packaging—that establishes a hard floor on costs.

Then there are the retailer margins, typically 30 to 40 percent of the retail price, that the manufacturer never sees. After all of that, the hardware company is left with a gross margin in the low-to-mid twenties on a good day.

Compare that to a subscription software business, where gross margins routinely exceed 80 percent, and it becomes obvious why every hardware company in Silicon Valley was desperate to become a "services" company in the late 2010s.

For Arlo specifically, the math was even more daunting. The free cloud storage tier—seven days of recordings for up to five cameras—was costing the company real money. Every new camera sold increased cloud storage and bandwidth costs without generating any recurring revenue. It was like running a restaurant where you gave away free appetizers and hoped customers would eventually order dessert. Some did. Most did not.

The strategic pivot that began in late 2018 and accelerated through 2019 and 2020 was nothing less than a complete reimagining of what Arlo was. The company would still sell cameras—it had to, since hardware was how customers entered the ecosystem—but the cameras would increasingly become the razor, and the subscription would be the blade.

The vehicle for this transformation was Arlo Smart, a subscription service that added AI-powered intelligence on top of the basic camera functionality. Think of the base camera experience as a security guard who can see but cannot think. The camera detects motion and sends you an alert. But it cannot tell you whether that motion was a person, a car, a dog, or a leaf blowing across the frame. You get dozens of false alerts a day, and each one requires you to open the app, watch the clip, and decide whether it matters. It is annoying enough that many users simply turn off notifications—which defeats the entire purpose.

Arlo Smart changed that equation. Using cloud-based computer vision—AI models running in data centers that analyze each video clip as it is uploaded—the service could distinguish between a person, a package, a vehicle, and an animal. Instead of "Motion detected at front door," you would get "Person detected at front door" or "Package delivered at front door," with a thumbnail image.

The system could also define activity zones, send rich notifications with animated previews, and even integrate with emergency services through an e911 feature.

The pricing architecture evolved through several iterations. Arlo Smart launched at $2.99 per month for a single camera or $9.99 per month for unlimited cameras. Higher tiers—Arlo Smart Premier and Arlo Smart Elite—offered extended cloud storage, priority support, and theft replacement warranties. The free tier was gradually restricted: where it once offered seven days of cloud recordings, new customers increasingly found that basic functionality required a paid subscription.

This was a delicate balancing act. Restrict the free tier too aggressively, and you alienate existing customers and generate negative reviews. Keep it too generous, and you eliminate the incentive to subscribe. Arlo's approach was evolutionary rather than revolutionary—tightening the free tier incrementally while making the paid experience conspicuously better.

During this same period, Arlo expanded its product portfolio to create more subscription attachment points. The Arlo Ultra, launched in early 2019, was the company's first 4K camera—targeting the premium end of the market where customers were more likely to subscribe. The Arlo Pro 3 followed, along with Arlo's first video doorbell and a floodlight camera.

Each new product category was designed with the subscription in mind: the doorbell could detect packages, the floodlight could trigger on person detection, and all of these AI features required an Arlo Smart subscription.

The competitive dynamics during this period were fierce. Amazon was bundling Ring Protect plans at nearly identical pricing to Arlo Smart. But Amazon had an advantage Arlo could not match: Ring Protect was increasingly positioned as a complement to Amazon Prime, and Amazon could afford to subsidize hardware aggressively, selling Ring doorbells for as little as $60 during Prime Day. Google's Nest Aware followed a similar trajectory, with pricing designed to pull customers deeper into the Google ecosystem.

Arlo could not afford to subsidize. Every dollar lost on a hardware sale was a dollar that would not come back unless the customer subscribed—and kept subscribing. The customer acquisition cost was effectively the negative margin on the hardware plus the marketing spend, and the payback period depended entirely on subscription conversion and retention.

This was the existential tension at the heart of the business model transition. Move too slowly on the subscription push, and the business would continue burning cash on free-tier users while competitors captured market share. Move too aggressively, restricting free features before the paid experience was compelling enough, and customer satisfaction would crater, generating the kind of negative reviews that are lethal for a consumer electronics brand sold primarily through retail and Amazon.

An analogy helps illustrate the challenge. Imagine running a gym where you have given away free memberships for years. Now you need to start charging. Some members will pay—the ones who truly value the gym. But many will simply leave for the gym down the street that is still offering free memberships (or close enough, because the gym down the street is owned by a billionaire who does not care about gym economics). The tightrope was narrow, and the consequences of falling were severe.

VII. The Competitive Gauntlet: Big Tech Enters (2019–2021)

The home security camera market in 2019 resembled a crowded battlefield where the combatants had wildly asymmetric resources. On one side stood Arlo, a newly independent public company with roughly $400 million in revenue and thin margins. On the other side stood Amazon, a trillion-dollar company for whom Ring was a customer acquisition funnel; Google, which had spent $3.2 billion on Nest and viewed home cameras as data points for its ambient computing vision; and Apple, which was quietly building camera integration into its HomeKit ecosystem as part of a privacy-first smart home strategy.

Amazon's Ring deserves particular attention because its competitive strategy was unlike anything a traditional camera company could match. Ring was not just a camera company—it was a neighborhood surveillance network wrapped in a social media platform.

The Neighbors app, which launched alongside Ring's hardware, let users share video clips and security alerts with nearby Ring owners, creating a community watch effect that strengthened with each additional Ring camera installed on a block. Amazon later extended this further with Sidewalk, a neighborhood mesh network using Ring devices and Echo speakers to create a low-bandwidth wireless network that extended well beyond each customer's Wi-Fi range.

The strategic implication was profound. Ring had network effects—each new Ring camera made the Neighbors app more useful for existing users, creating a flywheel that standalone competitors could not replicate. And because Amazon could cross-subsidize Ring hardware through Prime subscriptions, Echo sales, and the broader Amazon ecosystem, it could price aggressively. During Black Friday and Prime Day events, Ring doorbells regularly sold for $40 to $60—below what most analysts believed was cost.

Arlo, without a trillion-dollar parent to absorb losses, could not match these prices without hemorrhaging cash.

Google's approach was different but equally threatening. After years of neglect, Google revamped the Nest camera lineup in 2021, integrating cameras more deeply with Google Home and Assistant. More significantly, Google struck a partnership with ADT in August 2020, investing $450 million for a 6.6 percent stake in the largest residential security company in North America. The deal signaled Google's intent to bridge the gap between DIY cameras and professional monitoring—exactly the space Arlo occupied.

Apple's entry was more subtle but strategically consequential. HomeKit Secure Video, introduced in 2020, allowed compatible cameras to store encrypted video clips in iCloud without counting against a user's storage quota. For the hundreds of millions of Apple customers already paying for iCloud storage, this effectively meant free, privacy-first cloud storage for security cameras. Apple did not make cameras, but it was making the subscription layer that Arlo depended on increasingly redundant for a large segment of premium customers.

At the budget end, Wyze had detonated a price bomb in late 2017 with a $20 indoor camera that was, by any reasonable standard, surprisingly good. Eufy, a brand from Anker, offered cameras with local storage that required no subscription at all, directly attacking the value proposition of cloud-based services.

Arlo's response to this multi-front assault came through a partnership that would prove transformative. In 2019, the company struck a deal with Verisure, the largest private security company in Europe, with operations spanning Scandinavia, the Iberian Peninsula, France, the Benelux countries, and Latin America.

Under the arrangement, Arlo would supply hardware and cloud services to Verisure, which would sell and service the products through its own channels. Verisure committed to roughly $500 million in aggregate purchases over five years starting in 2020. The deal gave Arlo access to the European market at scale, created a large-volume predictable revenue stream, and shifted Arlo's customer base from pure consumer to a hybrid of consumer and B2B.

The pandemic provided an unexpected tailwind in 2020 and early 2021. With millions working from home, awareness of home security spiked. Package theft surged as e-commerce volumes exploded, making doorbell cameras feel like necessities rather than luxuries.

But the supply chain chaos that accompanied the pandemic—semiconductor shortages, shipping container backlogs, factory shutdowns in Asia—hammered hardware margins and constrained product availability at precisely the moment when demand was highest.

By mid-2021, the competitive landscape was clear. The home security camera market was not winner-take-all, but it was increasingly winner-take-most, with Amazon Ring commanding the largest share. Arlo had survived, but its market position was eroding, and the financial pressure was mounting to a breaking point.

VIII. Crisis and Restructuring (2021–2023)

The stock chart tells the story in stark visual terms. From a post-IPO high near $23 in August 2018, Arlo's shares had cascaded downward through a series of lower highs and lower lows, touching a pandemic-era bottom of $1.20 in March 2020. A brief recovery carried the stock back above $10 in early 2021 on the back of pandemic demand, but by mid-2022, it had cratered again to the $3 to $4 range.

For a company that had IPO'd at $16, this was more than a disappointment—it was a crisis of confidence.

The financial pressures were real and interconnected. Hardware revenue was under relentless margin pressure from competitors willing to sell at or below cost. Service revenue was growing but not fast enough to offset the hardware decline. Operating expenses—R&D, sales and marketing, general and administrative—were running at levels designed for a much larger revenue base.

Several factors converged to create this difficult period. The post-pandemic demand normalization hit hardware sales hard—the pull-forward of demand during COVID lockdowns left a hangover in 2022. The semiconductor shortage, which peaked in 2021 and 2022, drove component costs higher even as retail prices were being pushed down by competitive pressure. And the macroeconomic environment—rising interest rates, inflation fears, a sharp rotation away from growth stocks—punished exactly the kind of unprofitable, hardware-heavy technology company that Arlo was.

The company entered a period of strategic reset. Management acknowledged that the growth-at-all-costs playbook was no longer viable. The emphasis shifted explicitly to profitable growth, a phrase that showed up repeatedly in earnings calls from this period.

In practice, this meant several things.

First, cost cutting. Arlo reduced headcount, consolidated facilities, and renegotiated supplier contracts. The goal was to right-size the operating expense structure for a company generating approximately $500 million in revenue, not the $1 billion that earlier growth projections might have implied.

Second, product portfolio rationalization. Instead of launching a dizzying array of SKUs—different camera models in multiple configurations and price points—the company focused on a smaller number of "hero" products designed to cover the key use cases: outdoor cameras, indoor cameras, doorbells, and floodlights. The Essential line, aimed at the mass market, became the volume play. The Pro and Ultra lines targeted premium customers willing to pay for higher resolution and advanced features.

Third, and most importantly, the subscription strategy accelerated. Arlo began more aggressively gating features behind the paywall. New cameras shipped with a trial of Arlo Smart, designed to hook users on the AI-powered detection features and convert them to paid subscribers when the trial expired. The free tier was further restricted—recording storage, smart notifications, and activity zones all became premium features.

It was a bet that the product was good enough that customers would pay rather than downgrade.

The Verisure relationship deepened during this period, becoming Arlo's single largest customer. By 2022, Verisure accounted for roughly 40 percent of Arlo's total revenue—a concentration that provided stability but also created significant customer dependence risk. The two companies extended their partnership through 2029, with Arlo providing not just hardware but cloud platform services and AI-powered computer vision solutions to support Verisure's operations across more than five million customers in Europe and Latin America.

Technology investment continued despite the austerity measures. Arlo poured R&D dollars into improving its AI detection algorithms, reducing false alerts, and enhancing the user experience. Edge computing—running some AI processing on the camera itself rather than in the cloud—promised to reduce latency and cloud costs simultaneously. Battery efficiency improvements extended run times, addressing one of the most common customer complaints.

The period from 2021 to 2023 was, in many ways, the forge in which the modern Arlo was shaped. The company that emerged was leaner, more focused, and strategically clearer about its identity: a subscription-first business that happened to sell hardware, not a hardware business with a subscription sideline.

The question was whether this transformation had come in time—or whether the competitive damage from the years of crisis was already irreversible. The answer would start to emerge in the financial results of 2023 and 2024, and by 2025, the picture would look dramatically different from the darkest days.

IX. The Modern Era: Finding Sustainable Footing (2023–Present)

The inflection point, when it came, was measurable in a single metric: service revenue as a percentage of total revenue. In 2022, services represented roughly 28 percent of Arlo's business. By 2023, that figure crossed 40 percent—a milestone that fundamentally changed the company's financial profile.

By full-year 2025, service revenue reached $316 million, representing approximately 60 percent of total revenue, with Q4 2025 hitting 63 percent. The transformation was no longer a strategic intent—it was a financial reality.

The subscriber growth curve that powered this shift was steep and accelerating. Arlo crossed two million paid accounts at the end of 2022, hit three million in early 2024, surpassed four million by mid-2024, and ended 2025 with 5.7 million paid subscribers.

Equally important was the ARPU trajectory: average revenue per user climbed from roughly $12.60 to $15.30 over the course of 2025, a 21 percent increase driven by customers selecting higher-tier AI-powered plans. Annual recurring revenue reached $330 million by year-end 2025, growing 28 percent year-over-year.

The financial improvement was dramatic. Full-year 2025 marked Arlo's first year of GAAP profitability, with earnings per share of $0.14—modest in absolute terms but monumental given the company's history of losses. Non-GAAP earnings per share came in at $0.70, more than double the prior year. Adjusted EBITDA reached roughly $75 million, representing a 14 percent margin.

The company reported hitting the "Rule of 40"—the SaaS benchmark where revenue growth rate plus profit margin exceeds 40 percent. For a company that had been burning cash just two years earlier, these were transformative numbers.

Gross margins told the most important story. GAAP gross margins expanded to 44 percent for full-year 2025, up more than 700 basis points from the prior year, with Q4 2025 reaching 46.4 percent. The driver was straightforward: as service revenue—which carries margins above 80 percent—grew as a proportion of total revenue, the blended gross margin rose mechanically.

Product innovation continued to fuel the subscriber flywheel. In September 2023, Arlo launched the Essential 2nd Generation lineup, including cameras priced as low as $39.99—a dramatic reduction from earlier price points that signaled a willingness to sacrifice hardware margin to drive subscriber acquisition. In 2025, the company unveiled a comprehensive product refresh across the Essential, Pro, and Ultra lines, with AI-powered "Arlo Intelligence" as the unifying differentiator. Two new pan-tilt cameras offering 360-degree coverage were added to the lineup.

The partnership strategy evolved in ways that could prove transformative.

Beyond the continued Verisure relationship, Arlo struck two deals in 2025 that significantly expanded its addressable market. First, a partnership with Samsung SmartThings created "SmartThings Safe Premium powered by Arlo"—notably, Arlo's first purely SaaS-based partnership with no hardware component, potentially reaching 425 million SmartThings users globally.

Second, a deal with Comcast Xfinity to provide connected home security to millions of Xfinity Internet households. Management indicated during the Q4 2025 earnings call that the Xfinity partnership, with a nine-to-twelve-month integration timeline, could eventually grow larger than the Verisure relationship, with meaningful revenue expected to ramp in 2027.

The Arlo for Business vertical—targeting small and medium businesses with cloud-managed security cameras—represented an emerging opportunity. CEO Matthew McRae referenced "planting the seeds for the small business market and the age-in-place market" during the latest earnings call, signaling two new verticals beyond residential home security.

The company entered 2026 in a position of considerable momentum. Fourth quarter 2025 revenue of $141 million beat analyst expectations by roughly $6 million. The stock surged more than 10 percent on the earnings release, briefly touching $16—almost exactly its IPO price from nearly eight years earlier.

Full-year 2026 guidance of $550 to $580 million implied roughly 17 percent growth at the midpoint, with continued margin expansion expected. The balance sheet was clean: $166 million in cash with no debt.

The transition from "Will Arlo survive?" to "Can Arlo thrive independently?" is encouraging, but the competitive questions that defined the crisis years have not disappeared. They have merely become more nuanced. And answering them requires the kind of rigorous strategic analysis that separates momentary trading enthusiasm from durable investment conviction.

X. Strategic Analysis: Porter's Five Forces

To understand Arlo's competitive position, it helps to run the company through Michael Porter's Five Forces framework—the classic lens for assessing industry attractiveness and the durability of a company's position within it.

The threat of new entrants remains moderate to high, and the reason is a tale of two barriers. On the hardware side, barriers are low. The components that make a security camera—image sensors from Sony or OmniVision, Wi-Fi chipsets from Qualcomm or Realtek, injection-molded plastic housings, lithium batteries—are available off the shelf. Any reasonably competent hardware team in Shenzhen can design, manufacture, and ship a functional security camera in six to nine months. The hundreds of no-name camera brands on Amazon are proof.

But hardware is only half the story. The software and services layer—the mobile app, the cloud infrastructure, the AI detection algorithms, the subscription billing and customer support systems—is substantially harder to replicate. Building a reliable, scalable, secure cloud video platform requires years of investment and operational expertise. This creates a bifurcated barrier: easy to enter the hardware market, hard to build a competitive end-to-end experience.

Supplier bargaining power is moderate and situationally volatile. Arlo relies on contract manufacturers—primarily in China and Vietnam—for hardware production, and on cloud infrastructure providers for its backend. The semiconductor shortage of 2021-2022 demonstrated how quickly supplier power can spike: when chips are scarce, the manufacturer with the largest purchase commitments gets priority allocation, and smaller players get pushed to the back of the line.

Buyer power is high—arguably the most significant force working against Arlo. The consumer electronics buyer is price-sensitive, well-informed thanks to review sites and YouTube comparisons, and has abundant alternatives. Switching costs are modest: a customer can replace an Arlo system with Ring or Nest cameras in an afternoon, losing only their historical video recordings and the sunk cost of the hardware.

The retail channel further amplifies buyer power. Best Buy, Costco, and Amazon—the three most important channels for Arlo—have enormous leverage over camera manufacturers. And Amazon, uniquely, is both Arlo's largest retail channel and its most dangerous competitor, creating a fundamentally conflicted relationship.

The threat of substitutes is high and evolving. Professional monitoring from ADT and Vivint represents a substitute for the DIY approach. At the other extreme, ultra-budget cameras from Wyze and Eufy offer "good enough" functionality at a fraction of the price. Apple's HomeKit Secure Video turns the iPhone into a security hub, making the subscription layer largely invisible to users already paying for iCloud.

Competitive rivalry is intense—the force that most shapes Arlo's daily reality. Amazon Ring commands the largest market share. Google Nest is the number two player with Alphabet's backing. Budget players compete viciously on price. Traditional security companies have launched DIY product lines. The result is a market where no player has pricing power, innovation is rapidly copied, and customer loyalty is fragile.

The Five Forces analysis paints a picture of an industry that is structurally challenging for any standalone player. High buyer power, high substitution threat, and intense rivalry create persistent margin pressure. Arlo's subscription-first model with AI-powered differentiation is a strategy to mitigate these forces rather than overcome them. It is playing defense in a structurally challenging industry—and the question is whether defense can be enough.

One accounting note worth flagging: Arlo's revenue recognition involves judgment around hardware revenue versus deferred service revenue, particularly in bundled sales where a camera comes with a subscription trial. The allocation of transaction price between hardware and service performance obligations affects reported margins in both segments. Investors should pay attention to changes in these allocation methods across reporting periods.

XI. Strategic Analysis: Hamilton's Seven Powers

If Porter's Five Forces describe the industry landscape, Hamilton Helmer's Seven Powers framework asks a sharper question: Does this company have a durable competitive advantage—a "Power"—that will allow it to capture value over the long term?

For Arlo, the honest answer is sobering.

Scale economies are weak. In a market where Amazon sells more Ring cameras than Arlo sells total units, Arlo cannot achieve the manufacturing scale advantages that drive down per-unit costs. The one area where Arlo has scale is in its cloud video platform—processing billions of video clips and training AI models improves the service for all users. But Amazon and Google have far larger AI teams and far more compute infrastructure.

Network effects are weak to moderate. Home security cameras are fundamentally single-household products—your camera does not become more valuable because your neighbor also has one. Ring's Neighbors app is the exception that proves the rule, and it is a network effect that Arlo has not replicated. The ecosystem lock-in within a single household—where a family with three Arlo cameras is somewhat reluctant to rip them all out—provides a mild form of stickiness, but it is not a true network effect.

Counter-positioning was Arlo's original strategic advantage, and it was genuinely powerful in the early years. When Arlo launched its wire-free cameras, the incumbent home security companies—ADT, Vivint—could not easily replicate the DIY, no-contract, wire-free approach without cannibalizing their own installation-based businesses. This is textbook counter-positioning: the incumbent's existing business model prevents them from responding effectively.

But counter-positioning is a transient advantage. It works until the new model becomes mainstream, at which point incumbents either adapt or new competitors emerge who are native to the new model. By 2020, Ring, Nest, and others had fully adopted the DIY wire-free approach, and Arlo's counter-positioning advantage had largely evaporated.

Switching costs are moderate and represent perhaps Arlo's most tangible source of stickiness today. A household with multiple Arlo cameras, a base station, a subscription plan, and months of recorded video history faces a non-trivial switching cost—not just financial but also in terms of time and hassle. The subscription itself creates inertia: once a customer has set up their activity zones, notification preferences, and emergency contacts, they are less likely to switch on a whim.

But these switching costs are mild compared to true enterprise software, where data migration and workflow disruption can make switching prohibitively expensive.

Branding provides moderate power. Arlo has established meaningful brand recognition in the home security camera category, particularly at the premium end. But brand power in consumer electronics is notoriously fickle—it can be undermined by a single product flop or simply by a competitor's aggressive marketing campaign.

Cornered resources are weak. Arlo does not possess unique patents, exclusive supplier relationships, or irreplaceable talent that competitors cannot access. Process power is weak to moderate—Arlo has operational expertise in wire-free cameras, but larger competitors can replicate these processes.

The overall assessment is that Arlo currently lacks a durable Power in the Helmer sense. This is not a death sentence—plenty of companies operate profitably for years without a Helmer Power. But it does mean that Arlo's long-term profitability is inherently fragile, dependent on continued excellence in execution rather than structural advantages that would protect it during a period of weaker execution.

The difference matters enormously for long-term investors. A company with Power can stumble and recover—the moat protects it. A company without Power must execute well every quarter, because there is no structural buffer. One bad product cycle, one pricing war, one partnership dissolution, and years of progress can evaporate.

The recent partnerships with Samsung SmartThings and Comcast Xfinity represent an intriguing evolution—if Arlo can become the embedded security platform inside other companies' ecosystems, it could develop a form of switching cost power at the B2B level that its consumer business lacks. This is perhaps the most important strategic development to watch.

XII. Bull versus Bear Case and Investment Thesis

The bull case for Arlo begins with the subscription transformation, which is no longer a thesis but a demonstrated reality. Service revenue reaching 60 percent of total revenue in 2025, with gross margins expanding by more than 700 basis points, shows that the business model pivot is working.

The 5.7 million paid subscribers and $330 million in ARR growing at 28 percent year-over-year give the company the financial profile of a SaaS business, not a hardware company. If Arlo can sustain subscriber growth in the mid-teens to twenties percentage range while expanding ARPU through AI-powered premium tiers, the profit trajectory inflects sharply upward because service revenue falls almost entirely to the bottom line once the cloud infrastructure is scaled.

The partnership strategy adds optionality that the market may be underappreciating. The Samsung SmartThings deal—a pure SaaS arrangement reaching 425 million potential users—and the Comcast Xfinity partnership represent a new growth vector: Arlo as an embedded security platform inside other companies' ecosystems. This "platform-as-a-service" model, if it scales, would dramatically reduce customer acquisition costs, improve unit economics, and create B2B switching costs substantially higher than consumer switching costs.

The pure-play focus argument also has merit. Unlike Ring, which is a small piece of Amazon's vast empire and competes for attention with Alexa, Prime Video, and a thousand other priorities, Arlo's entire management team wakes up every morning thinking about one thing: home security cameras and the services that surround them.

The valuation provides a floor of sorts. At roughly 2.3 times enterprise value to trailing revenue, with no debt and $166 million in cash, Arlo trades at a significant discount to comparable SaaS companies. If the market reclassifies Arlo from "hardware company" to "subscription platform," the valuation multiple could expand meaningfully.

The bear case is equally serious and deserves equal weight.

The structural competitive disadvantage against Amazon and Google has not changed. These companies can still subsidize hardware, bundle subscriptions into broader ecosystems, and outspend Arlo on R&D and marketing by a factor of fifty. Amazon Ring remains the market leader, and Google's revamped Nest lineup and ADT partnership give it a compelling proposition.

The lack of a durable competitive moat—the "missing Power" in Helmer's framework—means that Arlo's success depends on continued execution rather than structural protection. Execution is inherently fragile: a product misstep, a pricing war, a key partnership dissolution, or a management departure could erode years of progress.

Customer concentration adds risk. Verisure accounted for approximately 40 percent of revenue in 2022 and remains Arlo's single largest customer. While the relationship has deepened and extended through 2029, dependence on a single customer of this magnitude creates vulnerability.

The hardware business, while increasingly a subscriber acquisition tool rather than a profit center, still creates capital intensity and operational complexity that pure software companies avoid. Manufacturing, warehousing, shipping, returns, and warranty service consume management attention and working capital.

Finally, the competitive dynamics at the budget end continue to erode the category. When Wyze sells a functional camera for $20 and Eufy offers local storage with no subscription, Arlo's premium pricing depends entirely on the perceived superiority of its AI detection and cloud platform. If the budget players close the quality gap—and they are improving rapidly—the willingness to pay for Arlo's premium becomes harder to sustain.

Myth versus reality deserves a moment here. The consensus narrative on Arlo has shifted from "doomed hardware company" in 2022 to "subscription transformation success story" in 2025. Both framings contain truth but neither captures the full picture. The myth of doom ignored the genuine quality of Arlo's products and the real attachment rate improvements. The myth of transformation success risks ignoring the structural competitive disadvantages that have not changed. The reality is somewhere between: Arlo has executed a genuine and impressive business model transformation, but it has done so in a market that remains structurally challenging, without the durable competitive moat that would make the transformation self-sustaining.

For investors tracking this story, two KPIs stand above the rest.

First, paid account growth rate and paid subscriber penetration against the total registered user base. This metric captures both the effectiveness of the subscription conversion engine and the health of new customer acquisition. It is the purest signal of whether the flywheel is working—are new camera buyers converting to subscribers, and are existing subscribers staying?

Second, service revenue as a percentage of total revenue. This ratio is the single best indicator of business model transformation progress and directly drives gross margin expansion, since service revenue carries margins above 80 percent versus low-to-mid twenties for hardware. When service mix is expanding and paid accounts are growing, the flywheel is spinning. When either metric stalls, the fundamental thesis is at risk.

XIII. Playbook: Lessons for Founders and Investors

Arlo's journey offers a rich set of lessons that extend well beyond the home security camera market.

The spin-off timing dilemma is the most immediate takeaway. Netgear spun off Arlo in 2018, at a moment when the division was growing rapidly but had not yet built a sustainable business model. With hindsight, it is fair to ask whether the spin-off came too early—before Arlo had achieved the subscription economics needed to survive independently—or whether the protection of remaining inside Netgear would have simply delayed an inevitable reckoning.

The lesson is that the optimal time to spin off a high-growth division is not at peak revenue growth, when the division looks most attractive to public market investors, but at the point where the division has established independent unit economics, when it can actually survive on its own. These two moments rarely coincide, and the pressure to monetize peak growth often wins over strategic patience.

The hardware-to-subscription transition illuminates the unit economics challenge that every hardware company attempting this pivot must confront. The core tension is temporal: hardware revenue is recognized at the point of sale, but the subscription revenue that justifies the hardware subsidy accrues over months and years.

This creates a cash flow trough during the transition—hardware margins decline as prices are cut to drive adoption, while subscription revenue has not yet scaled enough to compensate. Companies attempting this transition need either a strong balance sheet, patient investors, or a parent company willing to fund the gap. Arlo, as a standalone public company facing quarterly earnings scrutiny, had none of these luxuries in abundance.

The competitive lesson is perhaps the most broadly applicable: when platform companies enter your market, best-of-breed loses to bundling. Amazon did not win the home security camera market by building a better camera than Arlo. It won by making Ring cameras a gateway to the Amazon ecosystem—Alexa integration, Prime delivery alerts, Sidewalk neighborhood networking, Neighbors community sharing.

The individual camera quality differences between Arlo, Ring, and Nest are marginal. The ecosystem differences are enormous. For founders building standalone hardware products, this is the cautionary tale: your product may be objectively superior, but if a platform player can bundle a "good enough" version into an ecosystem that customers already depend on, the platform wins.

The "missing Power" problem is strategic kryptonite. A company can execute brilliantly—great products, smart marketing, disciplined operations—and still lose if it operates in a market without structural competitive advantages. Doing things right is different from having a moat. Doing things right requires perpetual excellence; having a moat means you can survive the occasional stumble.

The distribution paradox deserves its own case study. Arlo sells through Amazon, which is also Ring's parent company. It sells through Best Buy, which gives Ring and Nest prominent shelf space alongside Arlo. It sells directly through arlo.com, where customer acquisition costs are high. Each channel has trade-offs, and the complexity of managing all of them simultaneously consumes management bandwidth that a simpler distribution model would not require.

The profitability-versus-growth trade-off is a lesson Arlo learned the hard way. The early years of independence were marked by growth-at-all-costs spending. This worked while investors were willing to fund losses in exchange for top-line growth. When the market turned in 2022, the lack of a path to profitability became an existential liability. Founders should recognize that the growth-to-profitability transition is much harder to execute than to plan, and the time to build the foundation for profitability is during the growth phase, not after the market forces your hand.

XIV. Epilogue and Future Scenarios

Three scenarios bracket Arlo's future, and the company's trajectory over the next two to three years will determine which one prevails.

In the independence scenario, Arlo continues on its current trajectory: subscriber growth in the high teens to twenties, ARPU expansion through AI-powered premium tiers, and operating leverage driving margins higher. The Samsung SmartThings and Comcast Xfinity partnerships scale successfully, creating a "platform-as-a-service" revenue stream that reduces dependence on consumer hardware sales. Service revenue reaches 70 percent or more of total revenue, the company generates consistent free cash flow, and Arlo establishes itself as a durable, profitable niche player. This scenario requires continued strong execution, no major competitive disruption, and successful partnership scaling.

In the acquisition scenario, Arlo's improving financial profile and strategic partnerships make it an attractive target. The logical buyers are diverse: ADT, which already has a Google partnership but might want to own its camera technology; Resideo Technologies, the Honeywell spin-off focused on home comfort and security; private equity firms attracted by the recurring revenue base; or an international player seeking to vertically integrate.

The clean balance sheet and established subscriber base would make integration straightforward. CEO McRae's decision to join the Snap Inc. board in December 2025, while continuing to lead Arlo, may or may not signal anything about long-term intentions, but boards tend to notice when a CEO diversifies their professional portfolio.

In the decline scenario, the competitive pressures prove insurmountable. Amazon and Google continue to subsidize hardware and bundle services, gradually eroding Arlo's subscriber base. The budget players improve their AI and app quality to the point where Arlo's premium positioning becomes unjustifiable. Key partnerships fail to scale as expected. Revenue stagnates, and Arlo becomes a distressed acquisition target sold at a fraction of its peak value.

Several wild cards could alter any of these scenarios. The AI revolution in home security is accelerating—generative AI and large language models are beginning to transform how cameras interpret scenes, enabling natural language queries like "Did anyone come to the door between 3 and 5 PM yesterday?" and predictive alerts. A company that nails AI-powered security could create meaningful differentiation in a market that has struggled to escape commoditization.

New connectivity standards like Matter and Thread promise to make smart home devices more interoperable, which could either benefit Arlo—by making its cameras work seamlessly in any ecosystem—or hurt it by further reducing switching costs.

Privacy regulation, particularly in Europe where GDPR already creates compliance burdens, could advantage premium players with robust data protection practices while squeezing budget competitors who cut corners on security.

The broader question that Arlo's story raises extends far beyond home security cameras: Can specialized hardware companies survive the platform era? The answer, emerging from Arlo's experience, is conditional. They can survive if they successfully transition to subscription-first economics, if they find partnership models that give them ecosystem reach without ecosystem dependence, and if they maintain product quality that justifies a premium in a market trending toward commodity pricing.

It is possible. But it requires the kind of sustained excellence that is rare in any industry and exceptionally rare in consumer electronics, where product cycles are short, consumer loyalty is shallow, and the giants never sleep.

Was the Netgear spin-off a mistake? The honest answer depends on the time horizon. For shareholders who received Arlo stock near the IPO price and held through the trough, it was painful. For Arlo as a company, independence forced a strategic clarity that might never have emerged inside a diversified parent. The subscription transformation, the partnership strategy, the operational discipline—all of these were born from the urgency of independence. Whether that urgency will prove sufficient to build a durable, standalone business is the question that makes Arlo one of the more fascinating companies to watch in the consumer technology landscape.

XV. Further Reading and Resources

For those looking to go deeper on the Arlo story and the strategic frameworks that shape it, here are ten essential resources.

The Arlo S-1 Filing from 2018 remains the foundational document for understanding the business model, risk factors, and financial structure at the time of independence. The candor in the risk factors section foreshadowed many of the challenges that materialized.

Netgear's quarterly earnings calls from 2015 through 2018 provide the internal narrative of Arlo's growth within the parent company and the strategic rationale for separation.

Arlo's own quarterly earnings calls from 2018 to the present document the strategic evolution in management's own words. The shift in emphasis from hardware revenue growth to service metrics, and eventually to profitability, tracks the company's learning curve in real time.

Brad Stone's "The Everything Store" and its sequel "Amazon Unbound" provide essential context for understanding Amazon's smart home strategy and why Ring's acquisition was about ecosystem building, not camera margins.

Clayton Christensen's "Competing Against Luck" offers the jobs-to-be-done framework that explains why home security cameras succeed or fail based on the functional, emotional, and social jobs they perform for customers.

Ben Thompson's Stratechery articles on bundling and aggregation theory explain with precision why platform companies win when they bundle "good enough" products into ecosystems, and why standalone best-of-breed products often lose despite being objectively superior.

Hamilton Helmer's "7 Powers" provides the framework for evaluating competitive moats—or the absence of them—that is central to understanding Arlo's strategic challenge.

Parks Associates' annual smart home research reports offer the most comprehensive market sizing and consumer survey data on the home security category, including adoption rates, willingness to pay, and brand awareness metrics.

The Ring case study—from Jamie Siminoff's Shark Tank rejection to the billion-dollar Amazon acquisition—is the competitive counterpoint to Arlo's story, illustrating how a company with an inferior initial product but superior distribution and ecosystem strategy can win a market.

Finally, Clayton Christensen's "The Innovator's Dilemma" frames the meta-question: Is Arlo being disrupted from above by tech giants bundling security into ecosystems and from below by budget players offering "good enough" at a fraction of the price simultaneously? The answer may determine whether Arlo's story ends as a tale of resilience or a cautionary example of disruption in action.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube