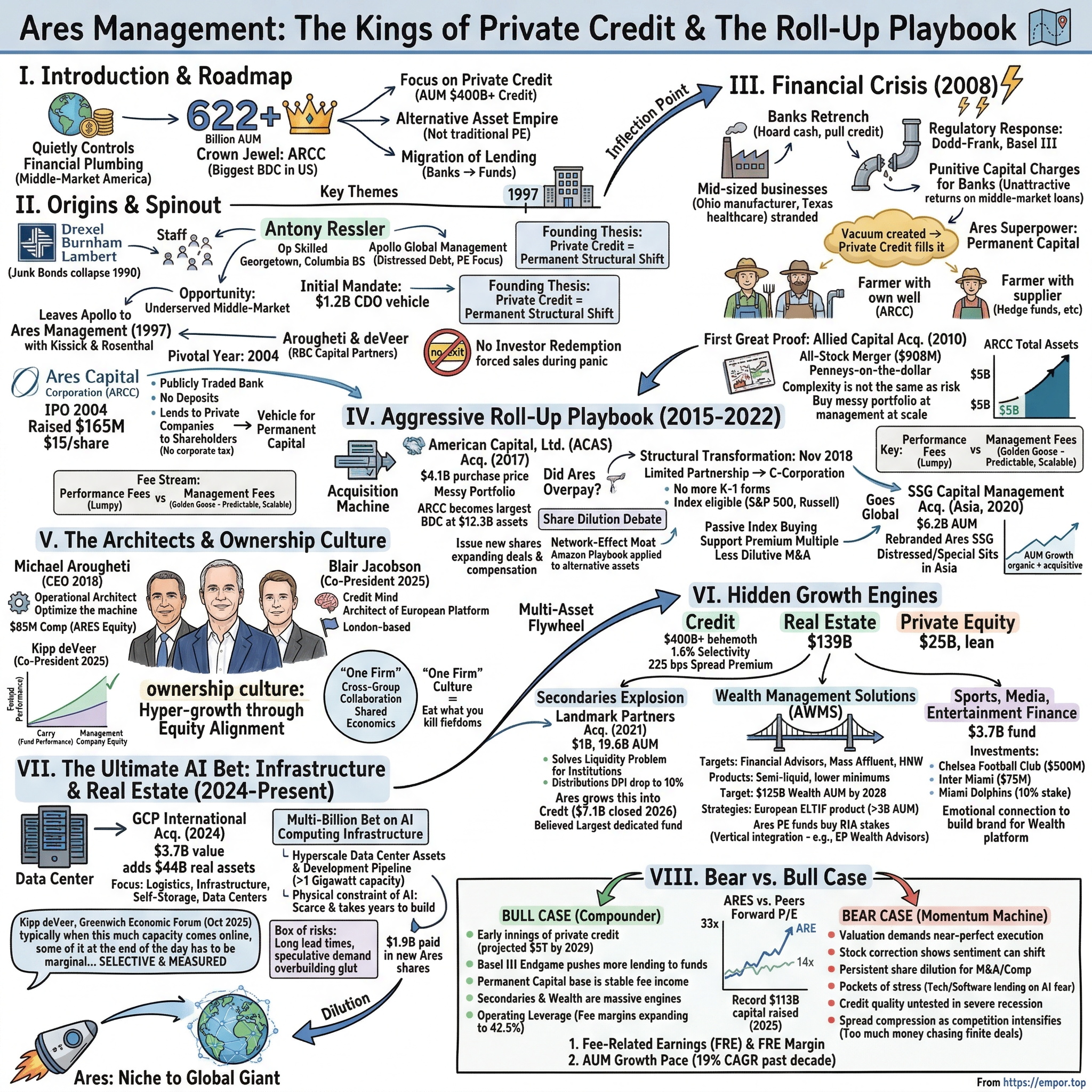

Ares Management: The Kings of Private Credit and The Aggressive Roll-Up Playbook

I. Introduction and Episode Roadmap

There is a company that quietly controls the financial plumbing of middle-market America, and most people outside of Wall Street have never heard its name.

It did not build the flashiest skyscrapers. It did not produce a celebrity CEO who tweets through market panics. It did not make headlines by buying iconic brands or taking companies private in leveraged spectacles. Instead, Ares Management built a more than four-hundred-billion-dollar alternative asset empire by doing something far less glamorous and far more lucrative: lending money to businesses that traditional banks abandoned.

As of late 2025, Ares Management oversees roughly six hundred and twenty-two billion dollars in assets under management, making it one of the largest alternative asset managers on the planet. Its crown jewel, Ares Capital Corporation, is the biggest publicly traded business development company in the United States. Its credit group alone manages over four hundred billion dollars.

And yet, when people rattle off the titans of private equity and alternative assets, the names that come to mind are Blackstone, Apollo, KKR, and Carlyle. Ares, somehow, still operates in a register just below cultural awareness, which is precisely how its founders prefer it.

This is the ultimate story of scaling through acquisition. It is a tale of using highly valued public stock as currency, of betting aggressively on messy portfolios that terrify competitors, and of the most consequential structural shift in global finance over the past two decades: the migration of corporate lending from regulated banks to private credit funds.

The narrative arc here is not one of a scrappy startup disrupting an industry from a garage. It is the story of a group of deeply experienced credit investors who recognized, earlier than almost anyone, that the post-2008 regulatory environment would permanently reroute the flow of capital through the financial system, and who positioned themselves to collect tolls at every new junction.

The roadmap for this exploration begins with the founding in 1997 and the early thesis that private credit was not a niche product but a structural inevitability. But the real story accelerates when the global banking system fractured in 2008, creating the vacuum Ares was perfectly engineered to fill.

From there, we trace the aggressive M&A playbook that turned a credit-focused boutique into a diversified global giant, examine the management team whose personal fortunes are deeply intertwined with the stock price, unpack the hidden growth engines most investors overlook, and wrestle with the central tension of the Ares story: Is this a brilliantly positioned compounder riding a multi-decade secular trend, or a momentum machine priced for absolute perfection on the eve of a credit cycle that could test its entire portfolio?

II. Origins: The Spinout and the Early Thesis (1997-2004)

To understand Ares Management, you first have to understand Drexel Burnham Lambert.

The infamous investment bank essentially invented the modern high-yield bond market before collapsing in 1990 amid fraud charges and the junk bond implosion. When Drexel disintegrated, it scattered a generation of aggressive, credit-obsessed financiers across Wall Street like seeds from a blown dandelion. Some of those seeds landed at Apollo Global Management, co-founded in 1990 by Leon Black, Marc Rowan, Josh Harris, and a handful of other Drexel alumni.

Among those Apollo co-founders was Antony Ressler.

Ressler was not the most famous name at Apollo. That distinction belonged to Leon Black, the firm's legendary and controversial senior partner. But Ressler was among the most operationally skilled.

He had risen to Senior Vice President at Drexel, running the new issue and syndicate desk in the high-yield department. He was a Georgetown and Columbia Business School graduate with a natural instinct for credit markets, a man who understood the mathematics of lending and the psychology of borrowers with equal fluency.

At Apollo, he spent seven years building his reputation as a sharp-elbowed dealmaker. But by the mid-1990s, Ressler saw an opportunity that Apollo, focused primarily on distressed debt and private equity, was not pursuing aggressively enough: the vast, underserved middle-market lending space where companies too large for community banks but too small for Wall Street's syndicated loan desks had few options for growth capital.

In 1997, Ressler stepped away from Apollo and co-founded Ares Management alongside John Kissick, another Apollo partner, and Bennett Rosenthal, who arrived from Merrill Lynch's global leveraged finance group. The firm's initial mandate was modest by today's standards: managing a 1.2-billion-dollar collateralized debt obligation vehicle.

But the founding thesis was anything but modest.

Ressler and his partners believed that private credit was not merely a cyclical trade on distressed assets. They believed it represented a permanent, structural shift in how mid-sized American businesses would finance their operations.

The middle market, that vast expanse of companies with revenues between roughly fifty million and a billion dollars, was fundamentally underserved. These businesses were too large for relationship-driven community bank lending, too small to access the public bond markets, and too complex for the cookie-cutter underwriting models of the big banks.

Consider the predicament of a typical middle-market company. Say you run a specialty chemicals manufacturer with two hundred million dollars in revenue, steady cash flows, and an opportunity to acquire a competitor. You need a hundred and fifty million dollar loan. Your local bank does not have the balance sheet capacity. The syndicated loan market on Wall Street does not want to bother with anything under five hundred million. And the public bond market requires the kind of disclosure, rating agency process, and legal fees that would take six months and cost millions. You are stuck in a financing dead zone.

Someone needed to build an institutional platform to lend to these companies professionally, at scale, with rigorous credit analysis and the ability to move quickly. That was the Ares thesis from day one.

For the first several years, the firm operated in an unusual limbo. Though technically an independent entity, Ares maintained a close relationship with Apollo and functioned as what industry insiders called the "West Coast affiliate" of the larger firm. This cozy arrangement persisted until 2002, when Ares raised its first Corporate Opportunities Fund and formally severed ties with Apollo.

The timing was notable. Apollo was embroiled in legal difficulties with the State of California over its 1991 purchase of Executive Life Insurance Company, and Ares' founders saw an opportunity to establish their own identity, free from the baggage of their former partners.

The pivotal year was 2004. That was when Michael Arougheti arrived at Ares, and with him came the person who would become his closest collaborator: Kipp deVeer.

Both came from RBC Capital Partners, where Arougheti had served as Managing Partner of the Principal Finance Group, overseeing a diversified portfolio of middle-market leveraged loans, subordinated debt, preferred equity, and warrants. Before RBC, Arougheti had cut his teeth at Kidder, Peabody's mergers and acquisitions group and then at Indosuez Capital, where he served as a principal and investment committee member. He was a Yale graduate with an operational intensity and a vision for institutionalizing the credit origination process that would become Ares' defining competitive advantage.

DeVeer, who held degrees from Yale and Stanford's Graduate School of Business, was the analytical complement. A meticulous credit underwriter with a talent for assessing risk across complex, multi-layered portfolios, he brought the intellectual rigor that would underpin Ares' credit culture for the next two decades.

Also in 2004, Ares launched what would become its most important vehicle: Ares Capital Corporation, or ARCC.

This Business Development Company completed its initial public offering in October 2004, raising approximately one hundred sixty-five million dollars by selling eleven million shares at fifteen dollars apiece. For the uninitiated, a BDC is essentially a closed-end fund structure created by Congress in 1980 that lends money to private, mid-sized American companies. Think of it as a publicly traded bank that does not take deposits, does not face the same regulatory constraints as traditional banks, and passes most of its income directly to shareholders. Like a REIT, a BDC that distributes ninety percent or more of its income avoids corporate-level taxation.

By electing BDC status, Ares gained something profoundly valuable: a vehicle for permanent capital. Unlike a traditional private equity fund with a fixed life of ten or twelve years, ARCC's capital was perpetual. Investors could sell their shares on the stock exchange if they needed liquidity, but the fund itself never had to return capital or liquidate positions at inopportune times. No investor could call up Ares during a market panic and demand their money back, forcing fire sales. The capital was locked in, available for deployment precisely when others were fleeing.

This was the seed from which a colossus would grow. But the Ares team knew they needed a catalyst to accelerate the thesis. They would not have to wait long.

III. The Inflection Point: The Financial Crisis and BDC Dominance (2008-2015)

Picture the autumn of 2008. Lehman Brothers has just filed for bankruptcy. Credit markets have seized up entirely. Banks are hoarding cash, refusing to roll over even routine credit facilities. And in corner offices across Wall Street, risk committees are drawing red lines through their middle-market lending books.

The phone is ringing at every regional business that depended on its banking relationship for credit lines, and the voice on the other end is saying the same thing: "We cannot renew your facility. We are pulling back."

Consider what this meant on the ground. A mid-sized manufacturer in Ohio that had relied on the same bank for twenty years to finance inventory purchases suddenly had no credit line. A healthcare services company in Texas that needed to refinance a maturing loan found every bank door slammed shut. A software company in Virginia with steady cash flows and a solid business model discovered that its bank had been told by regulators to reduce its commercial loan book by thirty percent. These were not failing businesses. They were collateral damage in a banking crisis that had nothing to do with their operations.

For most of the financial industry, the crisis was an existential threat. For Ares, it was the moment of validation. Everything the founding team had believed about the structural fragility of bank-dependent lending was playing out in real time, and the regulatory response would ensure it was not a temporary dislocation but a permanent rewiring of the financial system.

The Dodd-Frank Wall Street Reform and Consumer Protection Act, signed into law in 2010, and the concurrent implementation of Basel III capital standards, did something profound to the banking industry. They made it economically irrational for traditional banks to lend to mid-sized companies.

Here is the mechanism, explained simply. Under the new rules, banks had to hold significantly more capital, essentially equity cushion, against their loan portfolios. The regulatory capital charges on middle-market loans became punitive. A bank might need to hold eight or ten cents of equity capital for every dollar it lent to a middle-market company. That equity had to earn a return for the bank's shareholders. When you did the math, the return on equity from middle-market lending was terrible compared to other uses of a bank's capital, like mortgage lending or wealth management or trading. Bank executives, facing relentless pressure from shareholders to improve returns on equity, began systematically retreating from the very lending relationships that mid-sized companies depended upon.

In effect, the government broke the old financial plumbing and created an enormous vacuum. Someone had to fill it.

Ares was standing there with a bucket while it rained gold.

The firm's BDC, ARCC, became the primary vehicle through which this vacuum was filled. Because ARCC's capital was permanent, it could lend during a crisis when traditional banks were pulling back and when competitors with redemption-prone fund structures were forced to sell assets into distressed markets.

This was the superpower of the BDC structure, and it cannot be overstated. Here is an analogy. Imagine two farmers in a drought. One farmer owns his water supply outright, a deep well on his property. The other farmer buys water from a supplier who can cut him off at any time. When the drought hits, the farmer with the well can keep irrigating his fields and even buy his neighbor's parched land at a steep discount. The farmer dependent on the supplier is forced to let his crops wither. ARCC was the deep well. Redemption-prone hedge funds and open-ended credit funds were the farmers dependent on unreliable suppliers. When crisis hit, ARCC could lean in while competitors were forced to retrench.

The first great proof of this structural advantage came on April 1, 2010, when ARCC consummated the acquisition of Allied Capital in an all-stock merger.

Allied Capital had been one of the largest BDCs in the market, but the financial crisis had devastated it. Its portfolio was riddled with problems: overlevered companies, complicated structures, assets that were difficult to value, management teams that had lost their way. Most potential acquirers took one look at the mess and walked away. The complexity was too daunting, the workout risk too high, the potential for hidden losses too frightening.

Ares looked at the same mess and saw opportunity.

The deal valued Allied at approximately nine hundred eight million dollars, with each Allied share converting into 0.325 shares of ARCC stock. It was a pennies-on-the-dollar acquisition of a distressed competitor, and it taught Ares a playbook that would define the next fifteen years of the firm's strategy.

The playbook was deceptively simple: identify a large, complex portfolio that scares other buyers due to its messiness. Use Ares' massive underwriting and credit analysis platform, with hundreds of analysts poring over individual loan files, to accurately assess the true value hidden beneath the chaos. Buy the portfolio at a discount to that true value. Then systematically "clean it up" by working out bad loans, restructuring positions, replacing management teams at troubled portfolio companies, and converting the mess into a performing, fee-generating machine.

This was not financial engineering in the pejorative sense. It was operational credit management at scale. And it required something that almost no competitor possessed at the time: the institutional infrastructure to underwrite thousands of individual middle-market loans simultaneously. Ares had spent the prior decade building exactly that infrastructure, analyst by analyst, process by process, and the Allied deal proved that the investment was paying off spectacularly.

The numbers told the story. Prior to the Allied acquisition, ARCC had total assets of roughly five billion dollars. Afterward, the combined portfolio swelled dramatically, and with that growth came proportionally larger management fees flowing to Ares. The integration, which skeptics had warned would take years and produce painful write-downs, was executed with surgical precision. Ares systematically worked through Allied's troubled loans, renegotiating terms with some borrowers, restructuring others, and exiting positions that were beyond salvage. Within a few years, the vast majority of the acquired portfolio had been converted into performing, fee-generating loans.

The lesson was profound and would echo through every subsequent acquisition. Complexity is not the same thing as risk. To a buyer without the analytical infrastructure to see through the chaos, a messy portfolio looks terrifying. To a buyer with hundreds of trained credit analysts and established workout processes, that same portfolio looks like a bargain. The discount at which these portfolios trade reflects the market's inability to assess them accurately, and that information asymmetry is Ares' primary competitive edge.

By the middle of the 2010s, ARCC had established itself as the undisputed dominant force in the BDC market. It was the largest publicly traded vehicle of its kind by both market capitalization and total portfolio value. Its portfolio generated a dividend yield that attracted income-hungry investors in a zero-interest-rate environment, and its permanent capital structure meant it could continue deploying capital while competitors were stuck in fundraising mode.

The firm's total assets under management grew steadily through this period, but the real prize was not the assets themselves. It was the fee stream.

In the alternative asset management business, there are two types of revenue. Performance fees, sometimes called carried interest, are earned when investments generate returns above a certain threshold. These fees are lucrative but lumpy and unpredictable: they depend on exits, market timing, and individual deal outcomes. Management fees, by contrast, are the golden goose. They are charged as a percentage of assets under management, typically between one and two percent annually, regardless of whether the underlying investments go up or down. They are earned every quarter like clockwork. They are highly predictable. And they scale linearly with AUM.

The more capital Ares managed, the more management fees it earned. And the Allied acquisition had demonstrated something powerful: AUM could grow not just through the slow, steady process of organic fundraising, one institutional investor at a time, but through the rapid acquisition of entire portfolios and platforms. Buy a competitor's asset base, and the management fees start flowing immediately.

The inflection point of the financial crisis did more than just grow Ares' balance sheet. It validated the founding thesis in the most dramatic way possible. The old banking system was never coming back, at least not for middle-market lending. Private credit was the permanent replacement. Every dollar that flowed out of bank lending books flowed toward managers like Ares.

The question was no longer whether private credit would grow. The question was how aggressively Ares could position itself to capture the largest share of a market that would ultimately grow to trillions of dollars. And the answer, as the next chapter would demonstrate, was very aggressively indeed.

IV. M&A as a Feature: The "Overpay" Debate and Capital Deployment (2015-2022)

While most alternative asset managers in the mid-2010s were focused on organic growth, patiently raising fund after fund and growing assets one vintage at a time, Ares was building something different.

The firm was constructing an acquisition machine, using M&A not as an occasional supplement to organic growth but as the primary battering ram for entering new geographies, new asset classes, and new investor channels. To understand Ares, you must understand that its leadership views acquisitions the way a technology company views product launches: not as one-off events, but as a repeatable, scalable process with a known playbook and predictable integration timelines.

The signature deal of this era closed on January 3, 2017: the acquisition of American Capital, Ltd., known by its ticker ACAS. ACAS shareholders had approved the sale on December 15, 2016, after months of negotiation and activist pressure. The total purchase price was approximately four point one billion dollars, making it one of the largest BDC acquisitions ever consummated.

American Capital was another large BDC, but it had stumbled badly during the years after the financial crisis. Its portfolio was a sprawl of direct loans, private equity investments, and externally managed vehicles that had become increasingly difficult to manage. Its stock traded at a persistent discount to net asset value, a sign that the market had lost confidence in management's ability to realize the true value of the underlying assets. Activist investors had circled the company for years.

The immediate reaction from Wall Street analysts was a familiar chorus: Did Ares overpay?

The ACAS portfolio was messy. It contained assets that were difficult to value, management teams that needed to be replaced, and structures that required painstaking unwinding. But this was precisely the type of complexity that Ares had learned to exploit with the Allied Capital playbook. The firm's credit team believed they could underwrite the portfolio better than the market was pricing it, and they set about the familiar process of cleaning, restructuring, and integrating.

The deal cemented ARCC's position as the largest BDC in the United States, with pro forma total assets of twelve point three billion dollars. More importantly, it demonstrated that Ares could execute large, complex acquisitions at a pace and scale that competitors simply could not match.

This was not just about financial firepower. It was institutional capability: the ability to mobilize hundreds of credit analysts and portfolio managers to simultaneously assess thousands of individual loans, assign accurate risk ratings, and execute integration plans. In private credit, where every loan is a bespoke, bilateral relationship between lender and borrower, this kind of operational infrastructure is the product itself.

But the ACAS deal also crystallized what would become the central financial tension of the Ares story: share dilution.

Ares funded its acquisitions, in significant part, by issuing new shares of its own stock. Every acquisition meant more shares outstanding. Every compensation package meant more shares. The firm had gone public in May 2014, pricing its IPO at nineteen dollars per common unit and raising approximately two hundred seventeen million dollars. At the time of the IPO, Ares managed about seventy-four billion dollars and had roughly two hundred twelve million total units outstanding.

A pivotal structural transformation came in November 2018, when the firm converted from a limited partnership to a C-Corporation structure. This may sound like a dry accounting maneuver, but it was a masterstroke of financial engineering. As a limited partnership, Ares distributed complex K-1 tax forms to its unitholders, making the stock unattractive to many institutional investors and entirely ineligible for inclusion in major stock indexes like the S&P 500 or the Russell indices. By converting to a C-Corp, Ares made its shares fungible with any other corporate stock, which brought in waves of passive index-fund buying and opened the shareholder base to the massive pool of institutional capital that cannot hold partnership units.

The conversion was one of several similar moves across the alternative asset management industry during this period. Apollo, KKR, and Blackstone all made similar transitions. But the timing mattered. The influx of passive buying helped support Ares' stock price at premium multiples, which in turn made stock-funded acquisitions less dilutive and more accretive to the firm's growth strategy.

The conversion also made the dilution dynamics more transparent. From 2015 through 2026, the share count expanded meaningfully, driven by acquisition-related share issuance, equity compensation grants, and convertible securities.

For existing shareholders, this created a mathematical headwind. Even as assets under management soared and management fees grew, the per-share economics were being diluted by a steadily increasing denominator.

This dynamic spawned a persistent debate among sell-side analysts and institutional investors. The bears argued that Ares was effectively taxing its existing shareholders to fund empire-building, issuing expensive equity to buy assets that generated lower marginal returns than the market was pricing into the stock. If AUM growth ever slowed, the dilution would become punitive.

The bulls countered with a powerful structural argument. In the alternative asset management business, scale is the product. A firm that can write a two-billion-dollar check unilaterally will always get the first look at the most attractive deals, shutting out smaller competitors who cannot match the size. The dilution, in this view, was an investment in a network-effect moat that would compound for decades. Each acquisition made Ares bigger, which made its origination advantage stronger, which made its next fundraise easier, which made its next acquisition possible.

The market sided with the bulls. Despite continuous share issuance, Ares' stock traded at premium multiples throughout this period, consistently commanding a price-to-earnings ratio above thirty times. Investors were willing to absorb dilution because they believed the underlying growth in fee-earning assets would more than compensate. It was, in essence, the Amazon playbook applied to alternative assets: sacrifice near-term profitability per share to build an unassailable competitive position in a massive, growing market.

The firm also turned its sights global during this period, recognizing that private credit was not merely an American phenomenon. The same forces driving the shift from bank lending to private credit in the United States, tightening bank regulation, growing demand for flexible capital, and the increasing complexity of corporate finance, were playing out across Europe and Asia.

In January 2020, Ares announced the acquisition of a controlling stake in SSG Capital Management, a Hong Kong-based special situations and private credit firm managing approximately six point two billion dollars. SSG had been founded in 2009 by Edwin Wong and was one of the most respected distressed credit platforms in Asia, with particular expertise in the complex legal and regulatory environments of Southeast Asian and Indian credit markets. The deal closed in July 2020, and the firm was rebranded as Ares SSG.

The acquisition gave Ares an instant pan-Asian platform for distressed and special situations investing, with teams on the ground in Hong Kong, Singapore, Mumbai, Shanghai, and other key markets. Rather than spending years building a team, establishing relationships, and compiling a track record in Asia from scratch, Ares simply bought one. This was the same playbook applied to a different geography: acquire an established platform, integrate it into the broader Ares infrastructure, and then scale it using the parent firm's capital-raising capabilities and institutional relationships.

The pattern was now unmistakable. While competitors debated the merits of organic versus acquisitive growth, Ares was executing a roll-up strategy at the holding company level.

This is worth dwelling on because it represents a fundamentally different philosophy from how most alternative asset managers operate. The conventional approach in the industry is to grow organically: hire talented investors, raise a fund, generate strong returns, and then raise a bigger fund. It is slow, methodical, and low-risk. Ares layered acquisitive growth on top of this organic engine, treating the alternative asset management industry the way a private equity firm might treat a fragmented industrial sector: identify attractive platforms in adjacent markets, acquire them using the currency of a premium-valued stock, integrate them into the broader operating infrastructure, cross-sell the combined capabilities to an expanded client base, and repeat.

The question hanging over this strategy was whether Ares could sustain the pace of acquisition without eventually overpaying, over-diluting, or hitting integration problems that would disrupt the fee engine. Each successful deal raised the bar for the next one and made the firm's stock more expensive, which paradoxically made share-funded acquisitions more dilutive. But so far, the execution had been flawless enough to keep the market's faith.

V. The Architects: Current Management and The Ownership Culture

Walk into Ares Management's offices in Century City, Los Angeles, and the atmosphere feels different from what you might expect at a firm managing more than six hundred billion dollars.

There is no trading floor energy, no ticker screens on every wall, no young analysts in fleece vests shouting into Bloomberg terminals. The culture is more corporate law firm than hedge fund: deliberate, process-driven, and intensely collaborative. This is by design, and it reflects the personalities of the three men who have shaped the firm more than anyone else.

Michael Arougheti, who became CEO in 2018, is the operational architect of modern Ares. His management style is methodical and data-driven, more McKinsey than Wall Street in temperament. He is a frequent presence at industry conferences like the Milken Institute Global Conference and on financial television, but his public commentary tends toward the analytical rather than the promotional. When Arougheti discusses Ares' strategy, he speaks in terms of "addressable markets" and "origination throughput" rather than bold predictions about market direction.

This is telling. Ares' competitive advantage is not about making big macro bets on interest rates or economic cycles. It is about building the best underwriting machine in the industry and then feeding it an ever-larger volume of deals to analyze. Arougheti is the engineer who optimizes the machine.

Before arriving at Ares in 2004, Arougheti had built his career in the trenches of leveraged finance. He started at Kidder, Peabody's mergers and acquisitions group, moved to Indosuez Capital where he served as a principal responsible for originating and structuring leveraged transactions, and then to RBC Capital Partners where he ran the Principal Finance Group. Each stop gave him deeper expertise in the mechanics of credit origination: how to evaluate a borrower, structure protections for the lender, price risk accurately, and build relationships that generate repeat business.

His compensation reflects the firm's philosophy of deep equity alignment. In fiscal year 2024, Arougheti's total compensation was approximately eighty-five million dollars, a figure that placed his pay at three hundred fifty-six times the median Ares employee. But the composition of that compensation is what matters for understanding incentives. A large portion comes in the form of Ares equity, meaning Arougheti's personal wealth fluctuates directly with the stock price. He does not merely manage Ares. His net worth is, in practical terms, an Ares position.

Kipp deVeer, promoted to Co-President in February 2025 alongside Blair Jacobson, is the credit mind behind the curtain. If Arougheti is the strategist who decides what Ares should become, deVeer is the tactician who ensures the credit portfolio does not blow up along the way.

His Stanford MBA and years underwriting complex credit structures gave him an almost intuitive feel for credit risk at the portfolio level, the ability to look at thousands of individual loans and understand how they behave collectively in different economic scenarios. DeVeer co-architected the credit group that now manages over four hundred billion dollars, and he chairs the investment committees that approve the firm's most consequential lending decisions.

He is also, notably, one of the few senior executives at any major alternative asset manager who has publicly and voluntarily flagged risks in his own firm's biggest growth bet. More on that later.

Blair Jacobson, the other Co-President, is based in London and is the architect of Ares' European direct lending platform, which has become one of the largest in the continent. His promotion to Co-President signaled Ares' commitment to its international expansion, making it clear that the firm's future is not solely an American story.

Then there is the founder himself. Antony Ressler, now Executive Chairman, has stepped back from day-to-day operations but retains enormous influence over the firm's strategic direction. Ressler is a designated ten-percent-plus owner of Ares Management and holds, directly and indirectly, shares valued at several hundred million dollars.

He is also the owner of the Atlanta Hawks NBA franchise and is married to actress Jami Gertz. In the landscape of private equity moguls who crave media attention and public profiles, Ressler cuts an unusual figure: wealthy enough to own a professional sports team, connected enough to Hollywood to be on a first-name basis with entertainment royalty, but sufficiently camera-shy that most Americans could not pick him out of a lineup.

What unites this leadership team is their aggressive lean into equity-based compensation, and it is worth pausing to explain why this matters so much for understanding Ares.

In the alternative asset management industry, there are two primary ways executives make money. The first is carried interest, the performance fee that fund managers earn when their investments generate returns above a certain hurdle. Carried interest is enormously lucrative, but it is tied to individual fund performance and can create misaligned incentives: a manager might take excessive risk in a single fund to maximize their carry, even if it is not in the best interest of the firm as a whole.

The second way is equity ownership in the management company itself. When executives own significant stakes in the publicly traded parent company, their wealth rises and falls with the stock price, which reflects the market's assessment of the entire platform, not just one fund.

Ares' compensation structure is designed to maximize the second mechanism. Compared to peers at firms like Apollo or KKR, where carried interest from individual fund performance represents a larger share of total compensation, Ares' leaders derive a disproportionate amount of their wealth from the appreciation of ARES stock itself.

This creates a culture of hyper-growth. The fastest way for the management team to increase their personal fortunes is to grow the firm's AUM and fee-related earnings, which drives the stock price. But it also fuels the very share dilution that analysts debate. When you compensate executives primarily in stock, you are creating new shares that dilute existing holders. And when you use stock as acquisition currency, you are doing the same thing at a larger scale. The management team's incentive structure and the dilution debate are two sides of the same coin.

The firm's internal culture deserves attention because it contrasts sharply with some of its competitors. Ares has deliberately cultivated what it calls a "One Firm" culture, emphasizing cross-group collaboration and shared economics.

At many alternative asset managers, individual fund teams operate as quasi-independent fiefdoms, jealously guarding deal flow, client relationships, and carried interest pools. This "eat what you kill" culture creates sharp elbows and limits cross-selling. Ares has built the opposite: a culture where a credit originator who discovers a real estate opportunity is incentivized to pass it to the real estate team, and where the secondaries group collaborates with the wealth management group to create new products.

Whether this cultural aspiration fully matches reality is always debatable at large organizations. But the structural intent is clear, and the firm's ability to rapidly launch new products that span multiple asset classes suggests the collaboration is more than just talk.

VI. Hidden Engines and The Multi-Asset Flywheel

By the early 2020s, Ares had established itself as the undisputed leader in private credit. But the firm's leadership understood that dominance in a single asset class, no matter how large, created concentration risk.

If private credit spreads compressed, or if a severe default cycle hit, a firm that derived two-thirds of its revenue from a single strategy would be devastatingly exposed. The answer was diversification, but not the tepid, incremental kind. Ares pursued diversification the same way it pursued everything: through aggressive acquisition and rapid scaling.

To map the current empire: Credit remains the behemoth, the gravitational center around which everything else orbits. With over four hundred billion dollars under management, it is the single largest private credit platform in the world by most measures. The credit group encompasses direct lending to middle-market companies, liquid credit strategies that trade in public markets, alternative credit including asset-backed lending, and the massive ARCC platform that started it all.

But what makes Ares' credit business distinctive is not merely its size. It is the origination infrastructure. In 2025, ARCC alone reviewed roughly one trillion dollars in potential deals and closed on just one point six percent of them. That staggering selectivity ratio, enabled by the sheer volume of deal flow that flows to the largest lender in the market, produces a portfolio that is, at least in theory, significantly higher quality than what smaller competitors can assemble. The firm estimates that its proprietary origination generates spread premiums of approximately two hundred twenty-five basis points over publicly traded credit markets. In lending, size is not just an advantage. Size is the product.

Real estate and real assets represent the second largest pillar, managing roughly one hundred thirty-nine billion dollars after the transformative GCP International acquisition. Private equity, at approximately twenty-five billion dollars, is the smallest of the major pillars and is deliberately kept lean, focused primarily on corporate private equity and special situations rather than attempting to compete head-to-head with the mega-buyout shops.

But two segments deserve particular attention because they represent the true hidden growth engines of the Ares platform: secondaries and wealth management.

The secondaries explosion is perhaps the most underappreciated story within Ares.

In March 2021, the firm announced the acquisition of Landmark Partners, a Connecticut-based secondaries firm that had been operating since 1989 with a stellar reputation among institutional investors. The price was approximately one point zero eight billion dollars, funded through a mix of roughly seven hundred eighty-seven million in cash and two hundred ninety-three million in Ares operating group units. At the time, Landmark managed roughly nineteen point six billion dollars across more than thirty funds. The deal added an entirely new investment vertical to Ares' platform: secondaries.

To understand why secondaries matter, you need to understand the liquidity problem plaguing institutional investors. When a pension fund commits capital to a private equity fund, that capital is typically locked up for ten to twelve years. There is no stock exchange where you can sell your interest. If the pension fund needs cash before the fund matures, whether to meet pension obligations, rebalance its portfolio, or simply because its board changed strategy, its only option is to sell its fund interest on the secondary market, usually at a discount to the stated net asset value. The secondary buyer, in turn, gets to acquire a portfolio of seasoned, partially mature investments at a discount and then collect the remaining distributions as the underlying assets are sold.

This market has exploded in recent years because distributions from private equity and private credit funds have slowed dramatically. The ratio of distributions to paid-in capital, known as DPI, across the private equity industry hit its lowest recorded level in mid-2025. On a five-year rolling basis, DPI fell to roughly ten percent, compared to a 2015-2019 average of sixteen percent.

In plain language: institutional investors put money into private funds, but they are not getting money back at anywhere near historical rates. This liquidity drought has driven secondary transaction volumes to record levels, reaching an estimated two hundred twenty-six to two hundred forty billion dollars in 2025, up forty-eight percent from the prior year.

Ares took the Landmark platform and scaled it aggressively. In January 2026, the firm closed its inaugural Ares Credit Secondaries Fund at seven point one billion dollars, including approximately four billion in limited partner equity commitments. That figure roughly doubled the original fundraising target. This fund, focused specifically on buying secondary interests in private credit portfolios, is believed to be the largest dedicated institutional credit secondaries fund globally.

Think about the mathematics of that acquisition. Ares paid approximately one billion dollars for Landmark in 2021. Less than five years later, the secondaries platform has grown to approximately forty-two billion dollars in AUM and is producing some of the fastest-growing fee revenue in the entire firm. By any measure, this was one of the most accretive acquisitions in the history of alternative asset management.

The other hidden engine is Ares Wealth Management Solutions, or AWMS.

For the first several decades of the alternative asset management industry, the client base was almost exclusively institutional: pension funds, sovereign wealth funds, endowments, and insurance companies. These are sophisticated investors with long time horizons and high minimum commitment sizes, typically ten million dollars or more. The vast pool of individual investor wealth, the mass affluent and high-net-worth segment that collectively controls hundreds of trillions of dollars globally, was essentially untouched by private markets.

Ares launched AWMS around 2021 to change that.

The platform targets financial advisors and registered investment advisors, offering them semi-liquid private credit and private markets products that their clients can access with much lower minimums than traditional institutional funds. Products like the Ares Strategic Income Fund and the Ares Private Markets Fund are designed as perpetual or semi-liquid vehicles, meaning investors can typically request redemptions on a periodic basis rather than locking up capital for a decade. In Europe, the firm has launched similar products under the European Long-Term Investment Fund, or ELTIF, structure, with its European semi-liquid direct lending product surpassing three billion dollars in AUM by the first quarter of 2025.

The ambition here is breathtaking, and the numbers explain why.

Ares has raised its target to managing one hundred twenty-five billion dollars from individual and wealth investors globally by 2028, up from an earlier target of one hundred billion. To put that in context, global household wealth exceeds four hundred fifty trillion dollars, and the share allocated to private markets is still tiny. If Ares can capture even a fraction of the retail wealth shift into private markets, the fee revenue implications are enormous. Management estimates that the original one hundred billion dollar wealth AUM target alone could generate approximately six hundred million dollars in annual management fees.

To accelerate the wealth strategy, Ares has also begun taking minority stakes in registered investment advisory firms. In 2025, Ares' private equity funds acquired a significant minority stake in EP Wealth Advisors, a fee-only RIA managing approximately forty billion dollars across fifty-four offices in nineteen states. The logic is vertical integration: rather than simply selling products to independent advisors, Ares is investing in the advisors themselves, creating captive distribution channels for its semi-liquid fund products.

Then there is the most headline-grabbing growth engine: sports, media, and entertainment.

In 2022, Ares raised three point seven billion dollars for its inaugural Sports, Media and Entertainment Finance fund, including approximately two point two billion in equity commitments plus anticipated leverage. The fund makes both debt and equity investments in sports leagues, teams, and media properties.

The most visible deployment came in September 2023, when Ares invested five hundred million dollars in preferred equity and holding company notes for the entity that owns Chelsea Football Club, with funds earmarked for stadium expansion and multi-club portfolio acquisitions. The firm also injected seventy-five million dollars into Inter Miami, the MLS franchise co-owned by David Beckham, and acquired a ten percent stake in the Miami Dolphins.

These sports investments serve a dual purpose that reveals the sophistication of Ares' strategic thinking.

First, they generate attractive risk-adjusted returns. Professional sports franchises are among the most unusual assets in global finance. There are only thirty NBA teams, thirty-two NFL teams, and twenty MLS clubs. Supply is artificially constrained by league structures that limit expansion. Meanwhile, demand for ownership stakes is driven by a global class of billionaires for whom sports teams are both status symbols and increasingly attractive financial assets. Media rights valuations continue to escalate as streaming platforms compete with traditional broadcasters for premium live content. The scarcity value of major professional sports franchises has driven consistent price appreciation that exceeds most traditional asset classes over the past two decades.

Second, and perhaps more importantly for Ares' long-term strategy, these sports investments serve as a powerful marketing and brand-building vehicle for the wealth management platform. Nothing attracts high-net-worth client attention quite like offering exposure to Chelsea or the Dolphins. When an Ares wealth management representative sits down with a financial advisor and can offer clients a stake in a fund that owns pieces of iconic sports franchises, it creates an emotional connection that a traditional fixed-income fund simply cannot match. It is a strategy that turns investment returns into distribution leverage, using the glamour of sports to open doors that lead to far larger allocations across Ares' broader product suite.

The flywheel effect across all these segments is what makes Ares' model so difficult to replicate. Credit origination generates deal flow that feeds the secondaries platform. The secondaries platform generates relationships with institutional LPs that can be cross-sold into new credit funds. The wealth management platform provides sticky, permanent capital that supports management fees across all strategies. And the sports and media investments provide headline-grabbing brand recognition that attracts both institutional and retail capital.

Each gear turns the others.

VII. The Ultimate Bet: Infrastructure and Real Estate (2024-Present)

In the alternative asset management industry, there are acquisitions that add to a firm's capabilities, and then there are acquisitions that redefine what a firm is. The GCP International deal was the latter.

On October 8, 2024, Ares announced the acquisition of GCP International, the international business of GLP Capital Partners outside of Greater China. GLP, originally known as Global Logistic Properties, was one of the world's largest logistics and infrastructure platforms, with roots in Singapore and operations spanning dozens of countries. The international business that Ares was acquiring included a vast portfolio of warehouses, logistics facilities, self-storage assets, and critically, a rapidly growing data center platform.

The transaction was valued at approximately three point seven billion dollars, funded through a combination of one point eight billion in cash and one point nine billion in newly issued Ares Class A shares, with a total enterprise value potentially reaching five point two billion dollars. When the deal closed on March 1, 2025, it nearly doubled Ares' real assets under management overnight, adding forty-four billion dollars in logistics, digital infrastructure, and self-storage assets across Asia, the Americas, and Europe.

The centerpiece of the GCP acquisition was not warehouses or storage units. It was data centers.

At the heart of the deal was a significant portfolio of hyperscale data center assets and a development pipeline representing over one gigawatt of IT capacity, including roughly five hundred megawatts under active construction. To put that in perspective, one gigawatt of IT capacity can power the equivalent of several million households. These are not small server rooms in office parks. These are massive industrial facilities consuming as much electricity as small cities, purpose-built to house the computing infrastructure that trains and runs artificial intelligence models.

Ares had effectively made a multi-billion-dollar bet on the proposition that artificial intelligence would drive an unprecedented wave of demand for computing infrastructure, and that the firms controlling the physical facilities where AI models are trained and deployed would earn outsized returns for decades.

To understand why data centers are so valuable, consider the physical reality of AI. Every time someone uses a large language model, every time a company runs an AI-powered analytics tool, every time a self-driving car processes sensor data, the computation happens in a data center. Training a frontier AI model can require thousands of specialized chips running simultaneously for months, consuming enormous quantities of electricity. The demand for this computing infrastructure is not abstract. It is expressed in concrete, steel, copper wiring, and power substations. And unlike software, which can be copied at zero marginal cost, data center capacity is physical, scarce, and takes years to build.

The strategic logic of the GCP deal was compelling on its face. The explosion of generative AI since late 2022 had created a frenzy of demand for data center capacity from hyperscale cloud providers and major technology companies. AI-related private credit loans had nearly doubled in the twelve months leading up to the deal announcement. Major technology firms were announcing capital expenditure plans measured in tens of billions of dollars annually, and the physical infrastructure to house that spending simply did not exist yet.

Someone had to build it. And whoever controlled the land, the power connections, the permitting relationships, and the construction pipelines stood to profit enormously from the buildout.

Ares was not alone in this bet. Blackstone, Brookfield, and Apollo had all poured capital into data center projects. But Ares believed it had structural advantages through the GCP platform: established relationships with hyperscale tenants who had already signed long-term leases, pre-leased developments with fifteen-year-plus terms and built-in rent escalators, and a geographic footprint spanning the markets where data center demand was projected to be highest. The firm also closed an inaugural two point four billion dollar data center development fund in Japan, making it one of the largest data center investors in the country.

But here is where the story gets interesting, and where Ares' leadership distinguishes itself from the typical promotional posture of alternative asset managers.

Speaking at the Greenwich Economic Forum in October 2025, Kipp deVeer, the firm's Co-President and the person who oversees the credit portfolio that would be most affected by a broader economic downturn, voluntarily flagged the risk that Ares' own data center bet could face headwinds.

"If you look historically in areas like this over the past twenty or thirty years," deVeer said, "typically when this much capacity comes online, some of it at the end of the day has to be marginal." He added that "these trends tend to lead to overbuilds in certain places, so us being selective and measured in what we build is important."

This was a remarkable public statement. Here was a senior executive at a firm that had just committed billions to data centers, openly acknowledging the risk of overbuilding and overinvestment. In an industry where promotional optimism is the default setting, where fund managers talk their own book with religious fervor, deVeer's candor stood out. It suggested either genuine intellectual honesty about the risks, strategic signaling to reassure institutional investors that Ares was not blindly chasing the AI hype, or both.

The risk is real and well-documented in the history of infrastructure buildouts. Data center construction lead times are long, often two to three years from breaking ground to delivering capacity. Demand projections for AI computing are inherently speculative, based on assumptions about model sizes, training costs, and enterprise adoption rates that could shift dramatically. If the AI investment cycle slows, or if cloud providers build more capacity than they ultimately need, the market could face a glut of data center space. And a firm that invested billions at the peak of the cycle would face the unpleasant mathematics of assets generating returns below their cost of capital.

Ares' defense against this risk is its pre-leasing strategy. By securing long-term commitments from creditworthy hyperscale tenants before beginning construction, the firm argues it is insulated from speculative vacancy risk. But pre-leased does not mean risk-free. Tenants can encounter their own financial difficulties, renegotiate terms, or slow their expansion plans. And the broader real estate market dynamics, including interest rates, construction costs, and competing supply from every other alternative asset manager rushing into the same space, all influence the ultimate returns.

The GCP deal was also the latest and largest example of the share dilution dynamic. One point nine billion dollars of the purchase price was paid in newly issued Ares shares, directly diluting existing holders. The firm also issued thirty million shares of Series B mandatory convertible preferred stock in connection with the deal, which will automatically convert into between eight and ten million additional Class A shares by October 2027.

The ultimate verdict on the GCP International acquisition will not be known for years. But it represents the clearest expression of Ares' strategic ambition: the firm is betting that alternative asset managers who control both the capital and the physical infrastructure of the modern economy will be the dominant financial institutions of the next several decades.

VIII. Playbook: Business and Investing Lessons

Every great business story contains lessons that extend beyond the specific company, and Ares Management is no exception. The firm's trajectory offers a masterclass in several dimensions of business strategy, and it is worth examining through the formal frameworks that sophisticated investors and strategists use to evaluate competitive moats and industry dynamics.

These frameworks are not academic exercises. They are practical tools for understanding why some companies in the same industry generate spectacular returns while others struggle, and for predicting which advantages are likely to endure and which are likely to erode.

Start with Hamilton Helmer's concept of Scale Economies. In most industries, scale advantages are gradual and incremental, expressed as slightly lower unit costs or modestly better purchasing terms. In private credit, they are decisive.

When a mid-sized company needs to borrow five hundred million dollars to fund an acquisition, it needs a lender that can write that entire check. If the lender can only commit two hundred million and needs to syndicate the rest, bringing in other lenders to share the loan, the process becomes slower, more complex, and less certain. The borrower has to negotiate with multiple parties, share sensitive financial information more broadly, and accept the risk that one of the syndicate members might pull out at the last minute.

Ares can write checks of up to two billion dollars unilaterally. This ability gives the firm first look at virtually every premium middle-market deal in the United States and increasingly in Europe and Asia. Smaller competitors are structurally excluded from the most attractive transactions, not because they lack skill or judgment, but because they lack size. In private credit, being the biggest is not a vanity metric. It is the primary determinant of deal quality and pricing power.

The second Helmer power that applies is Counter-Positioning. Traditional banks and Ares are in the same business: lending to companies. But their structural constraints are fundamentally different and essentially irreconcilable.

Banks fund themselves with deposits that can be withdrawn overnight. They are subject to Basel capital requirements that penalize middle-market lending. They face regulatory examinations that create uncertainty about their ability to maintain lending relationships through cycles. They answer to regulators who can force them to curtail lending at exactly the moments when borrowers need capital most.

Ares funds itself through permanent capital vehicles like ARCC, through long-dated institutional funds with ten-year lockups, and increasingly through semi-liquid wealth products. This capital cannot flee during a panic. When a crisis hits, banks are forced to retrench. Ares can lean in and lend at premium spreads when borrowers are most desperate and competition is weakest.

This is not merely an operational advantage. It is a structural impossibility for banks to replicate without fundamentally changing their business model, which regulation prevents them from doing. The counter-positioning is permanent, locked in by the very regulatory architecture that governments built to make the financial system "safer."

Porter's Five Forces analysis adds further texture. Consider the bargaining power of borrowers. Middle-market companies have steadily fewer alternatives for growth financing. Traditional banks have retreated. Public bond markets are inaccessible for most mid-sized firms. And while the private credit market is growing, borrowers often value speed, certainty, and relationship continuity over getting the absolute lowest interest rate. This gives lenders like Ares significant pricing power, the ability to set terms, covenants, and spreads that favor the lender, because what borrowers are really paying for is the certainty that the capital will actually show up.

On the other side, the threat of new entrants and substitutes is real and growing. The extraordinary returns available in private credit have attracted enormous capital inflows, and every major alternative asset manager is now building or acquiring a private credit capability. Blackstone, Apollo, KKR, and pure-play entrants like Blue Owl Capital are all competing aggressively for the same deals. As more capital chases a finite pool of lending opportunities, spreads compress and terms become more borrower-friendly. This is the natural lifecycle of any attractive market: early entrants earn outsized returns, which attracts capital, which competes away the excess returns.

The lessons for founders and operators are equally instructive. Ares demonstrated that in certain industries, using a highly valued stock as acquisition currency can be a legitimate and powerful strategic weapon. When your stock trades at a premium multiple, every share you issue to acquire assets is, in effect, buying those assets at a discount to your own implied valuation. This only works if the market continues to believe that the acquired assets will grow at a rate that justifies the premium, and Ares managed to maintain that belief through consistent execution over more than a decade.

The deeper lesson is perhaps the most counterintuitive: the most durable competitive advantages are often built on the regulatory constraints of your competitors.

Ares did not lobby for Dodd-Frank or Basel III. The firm had no hand in designing the regulatory architecture that would make traditional bank lending to the middle market economically unattractive. But Ares was extraordinarily well-positioned to benefit from those regulations, and it spent fifteen years building a business model that would be nearly impossible to replicate within the constraints of the regulated banking system.

This is a principle that applies far beyond financial services. In any industry where regulation creates structural constraints on incumbents, the firms that can operate outside those constraints while serving the same customers have a built-in advantage that is self-reinforcing. The regulation is not going away; if anything, it tends to get tighter over time. And the customers are not going away either. They simply migrate to whoever can serve them.

The best moats are not always the ones you build yourself. Sometimes they are the ones that governments build for you.

IX. Analysis: Bear vs. Bull Case

The bull case for Ares Management rests on a single, powerful premise: the secular shift from public to private markets, and from bank lending to private credit, is still in the early innings of a multi-decade transformation.

Consider the scale of what has already happened and what remains ahead. The global private credit market has reached approximately three point five trillion dollars in assets under management, according to industry data compiled in late 2025. Morgan Stanley projects it will reach five trillion by 2029. Capital deployment in private credit surged to nearly six hundred billion dollars in 2024, up seventy-eight percent year-over-year. And the regulatory forces driving this shift, Basel III and its successor frameworks, are not being relaxed. If anything, the so-called Basel III endgame, which introduces even stricter rules for how banks calculate risk-weighted assets, will push more lending activity out of the banking system and into the arms of private credit managers.

To use a real estate analogy: banks are not just closing branches in the lending neighborhood. They are being zoned out of it by the regulators. And the tenants, those mid-sized companies that need capital, are not going away. They are simply signing leases with new landlords.

Ares is arguably the best-positioned firm to capture this growth. Its AUM base provides origination advantages that smaller competitors cannot match. Its permanent capital structures give it a stable and predictable fee base that is less vulnerable to the fundraising cycles that affect traditional fund managers. Its secondaries platform has become a multi-billion-dollar growth engine feeding off the liquidity drought affecting institutional investors. And the wealth management channel represents an entirely untapped revenue stream that could transform the firm's economics over the next several years.

The operational execution supports the bull case. In 2025, Ares raised a record one hundred thirteen billion dollars in new capital. Fee-related earnings grew thirty-three percent year-over-year in the fourth quarter, reaching five hundred twenty-eight million dollars with a margin of forty-two point five percent. Management fees hit a record nine hundred ninety-four million dollars in the same quarter, up twenty-seven percent. The firm is demonstrating the operating leverage that bulls have long predicted: as AUM grows, the incremental cost of managing each additional dollar declines, and fee margins expand.

The bear case, however, is not about the secular trend being wrong. It is about the price of admission.

Ares trades at a forward price-to-earnings multiple of approximately thirty-three times, a staggering premium over the alternative asset manager peer average of roughly fourteen times. The trailing price-to-earnings ratio has been even higher. This valuation assumes near-perfect execution: continued twenty-plus-percent AUM growth, expanding fee margins, successful integration of the GCP acquisition, and no meaningful deterioration in credit quality.

Any stumble, a disappointing fundraising quarter, a rise in non-accrual rates, a slowdown in the wealth management rollout, could trigger a sharp multiple compression. When a stock is priced for perfection, even meeting expectations can disappoint if the market expected perfection-plus.

The stock's recent performance underscores this vulnerability. After roughly tripling between 2020 and 2024 as the private credit narrative gained momentum, ARES experienced a decline of approximately twenty-two percent over the trailing twelve months heading into early 2026, driven by broader concerns about tariffs, private credit crowding, and the technology lending scare. The correction demonstrated how quickly sentiment can shift even when fundamental operating metrics remain strong.

The share dilution concern remains front and center. The issuance of shares for the GCP deal, combined with the convertible preferred stock that will add millions of additional shares by late 2027, means that existing shareholders are seeing their ownership stake steadily reduced. The math only works if the acquired assets grow fee revenue faster than the dilution erodes per-share economics. So far, this has been the case. But in a scenario where AUM growth stalls, the dilution becomes a wealth-destroying headwind rather than a neutral factor.

Then there is the elephant in the room: credit quality in a downturn.

Private credit has scaled massively during a period of historically low default rates. ARCC's non-accrual rates have remained stable and low, and the portfolio's track record through the brief pandemic downturn of 2020 was reassuring. But there is a meaningful difference between a sharp but short recession buffered by trillions of dollars in government stimulus and a severe, protracted downturn with sustained unemployment and widespread business failures. The private credit industry's modern incarnation has simply never been tested against the latter scenario.

This is not a theoretical concern. The sector faces emerging pockets of stress, particularly in technology and software lending, where AI-driven disruption is challenging the business models of borrowers whose revenues once seemed stable and predictable. In early 2026, Blue Owl Capital's anxiety over potential software-sector defaults sent ripples through the broader direct lending market. The concern was specific: private credit lenders had extended billions of dollars in loans to software companies based on the assumption that their recurring revenue streams were nearly as reliable as utility bills. But if AI tools can replicate what those software companies sell, their "recurring" revenue may prove far less durable than underwriters assumed.

The implications extend well beyond software. Private credit portfolios are, by design, concentrated in middle-market companies that are too small to access public debt markets. These companies tend to be more leveraged, more cyclically sensitive, and less diversified than their larger counterparts. In a severe recession, default rates among middle-market borrowers could spike far more sharply than in the investment-grade corporate bond market. And because private credit loans are not publicly traded, the losses would not be immediately visible in daily price movements. They would emerge gradually through rising non-accrual rates and write-downs, potentially creating a slow-motion crisis of confidence that could impair fundraising for years.

Spread compression adds another layer of concern. The extraordinary returns available in early-vintage private credit attracted enormous capital inflows, and the industry now faces a dynamic where too much money is chasing a finite pool of lending opportunities.

Here is how this works in practice. Five years ago, a private credit lender might have charged a middle-market borrower a spread of six hundred basis points over a benchmark rate, with robust covenants that gave the lender early warning if the borrower's financial health deteriorated. Today, as competition intensifies from Blackstone, Apollo, KKR, Blue Owl, and dozens of smaller entrants, that same borrower might attract bids from multiple lenders offering spreads of four hundred basis points with lighter covenants. The lender is earning less per dollar lent and has fewer contractual protections if things go wrong.

This is the natural lifecycle of any attractive market: early entrants earn outsized returns, which attract capital, which competes away the excess returns. If Ares is originating loans at tighter spreads with less protective covenants than it did five years ago, the portfolio's risk-adjusted return deteriorates even before defaults arrive. The question is whether Ares' scale advantages, its ability to see more deals and cherry-pick the best ones, can offset the industry-wide compression in returns.

For those tracking Ares Management's ongoing performance, two metrics matter above all others.

The first is fee-related earnings and FRE margin.

Fee-related earnings strip out the lumpy and unpredictable performance fees that come from carried interest, isolating only the recurring management fees minus operating expenses. This is the truest measure of whether Ares' platform is generating sustainable, compounding revenue. It is the equivalent of looking at a subscription software company's recurring revenue rather than its total revenue, which might include one-time professional services fees.

The FRE margin, which measures fee-related earnings as a percentage of management fees, reveals whether the firm is achieving genuine operating leverage: whether each additional dollar of AUM is being managed more efficiently than the last. In the fourth quarter of 2025, this margin reached forty-two point five percent. A sustained decline in FRE or margin compression would signal that the growth story is maturing or that competitive pressures are eroding the firm's pricing power.

The second is the pace of AUM growth itself, which is the top-line driver of the entire fee engine.

AUM growth is to Ares what same-store sales growth is to a retailer: the single number that tells you whether the core business is gaining or losing momentum. Ares has compounded AUM at approximately nineteen percent annually over the past decade, a rate that justifies a significant valuation premium. Any sustained deceleration below mid-teens growth would challenge that premium. Conversely, continued acceleration, particularly from the wealth management channel and the secondaries platform, would validate the market's willingness to pay a significant premium for what it views as one of the highest-quality compounders in financial services.

X. Epilogue

Step back far enough from the individual deals, the financial metrics, and the competitive dynamics, and the arc of Ares Management's journey becomes almost implausibly clean: from a niche credit shop managing a single CDO vehicle in 1997 to a diversified global alternative asset manager overseeing more than six hundred billion dollars, spanning credit, real estate, infrastructure, secondaries, private equity, wealth management, and sports finance across four continents.

The founders did not invent private credit. They did not pioneer the BDC structure. They did not even set out to build a diversified alternative asset giant. What they did was recognize, earlier and more clearly than almost anyone, that the post-crisis regulatory environment would permanently reroute the flow of corporate lending from regulated banks to private capital markets. And then they built, acquisition by acquisition, the largest and most comprehensive platform to capture that flow.

The story of Ares is, at its core, a story about using constraints as advantages. When banks were constrained by Basel III, Ares stepped into the void with permanent capital. When competitors were constrained by traditional fund structures that forced them to return capital during downturns, Ares deployed capital from vehicles that never had to liquidate. When the market constrained access to private investments to institutions only, Ares built a wealth platform to reach individual investors. When geographic boundaries constrained growth, Ares bought platforms in Asia and Europe. At every juncture, the firm identified someone else's constraint and built a business that profited from it.

The risks are real and should not be minimized.

The valuation demands perfection. The dilution is persistent. The credit portfolio has not been tested through a severe, multi-year downturn. The data center bet is enormous and potentially cyclically timed. The competitive landscape is more crowded than ever.

These are not abstract concerns. They are the specific fault lines along which the Ares thesis could crack.

But the structural advantages are equally real. The permanent capital base, the origination infrastructure, the scale that provides first-look access to premium deals, the cross-platform flywheel, and the regulatory moat that prevents banks from re-entering the territory Ares now occupies: these are not easily replicated. They represent decades of compounding institutional capability.

Whether the market's current premium valuation proves justified depends on factors that are unknowable today: the depth and duration of the next credit cycle, the sustainability of the private credit boom, the success of the data center bet, and the pace of retail adoption of private market products.

What is knowable is that Ares Management has positioned itself at the intersection of the most powerful structural trends in global finance. And the management team's deep personal ownership ensures they will be intensely motivated to navigate whatever comes next.

The firm that Antony Ressler founded as an Apollo spinout nearly three decades ago now stands as one of the most consequential financial institutions in the world, a distinction that most people will never notice, which is exactly how the kings of private credit want it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube