Aquestive Therapeutics: The "Holy Grail" of Delivery

I. Introduction & The "Postage Stamp" Dream

Picture a parent at a Little League game on a humid August afternoon in suburban New Jersey. The cooler is melting. Sunscreen smears the bench. A seven-year-old runs in from third base, scratches at his lip, then suddenly his eyes go glassy and his throat starts to close. His mom dives into a fanny pack for a cardboard tube the size of a sharpie, twists off the cap, jams it through his shorts into his thigh, and counts to ten. The EpiPen does its job. The boy lives. The pen, used once, is now medical waste.

Now imagine the same scene with one change. Instead of a needle the size of a fountain pen tip, mom peels open a foil pouch no thicker than a postage stamp, slips a translucent strip the size of a fingernail under her son's tongue, and watches it disappear in seconds. No needle. No bulky tube. No anxious teenager refusing to carry it because it doesn't fit in skinny jeans. Same drug. Same lifesaving mechanism. Just delivered the way humans have been swallowing medicine for centuries — through their mouths.

That postage-stamp dream is the entire bull case for Aquestive Therapeutics, the small-cap specialty pharma company trading on the NASDAQ under the ticker AQST. With a market capitalization that has hovered around $500 million in spring 20261, Aquestive is a fraction of the size of the legacy auto-injector incumbents it is trying to disrupt. And yet, sitting inside the company is what management has described as a multi-billion-dollar opportunity built on a deceptively simple polymer: a fast-dissolving oral film.

The "big idea" of this episode is whether a technology company — and that is what Aquestive's predecessor really was, an industrial film manufacturer that happened to stumble into drug delivery — can complete the awkward, expensive, sometimes heartbreaking journey from contract manufacturer to fully integrated specialty pharmaceutical company. The answer is going to be decided not in a boardroom but in a sterile FDA review office in Silver Spring, Maryland, sometime in late 2026.

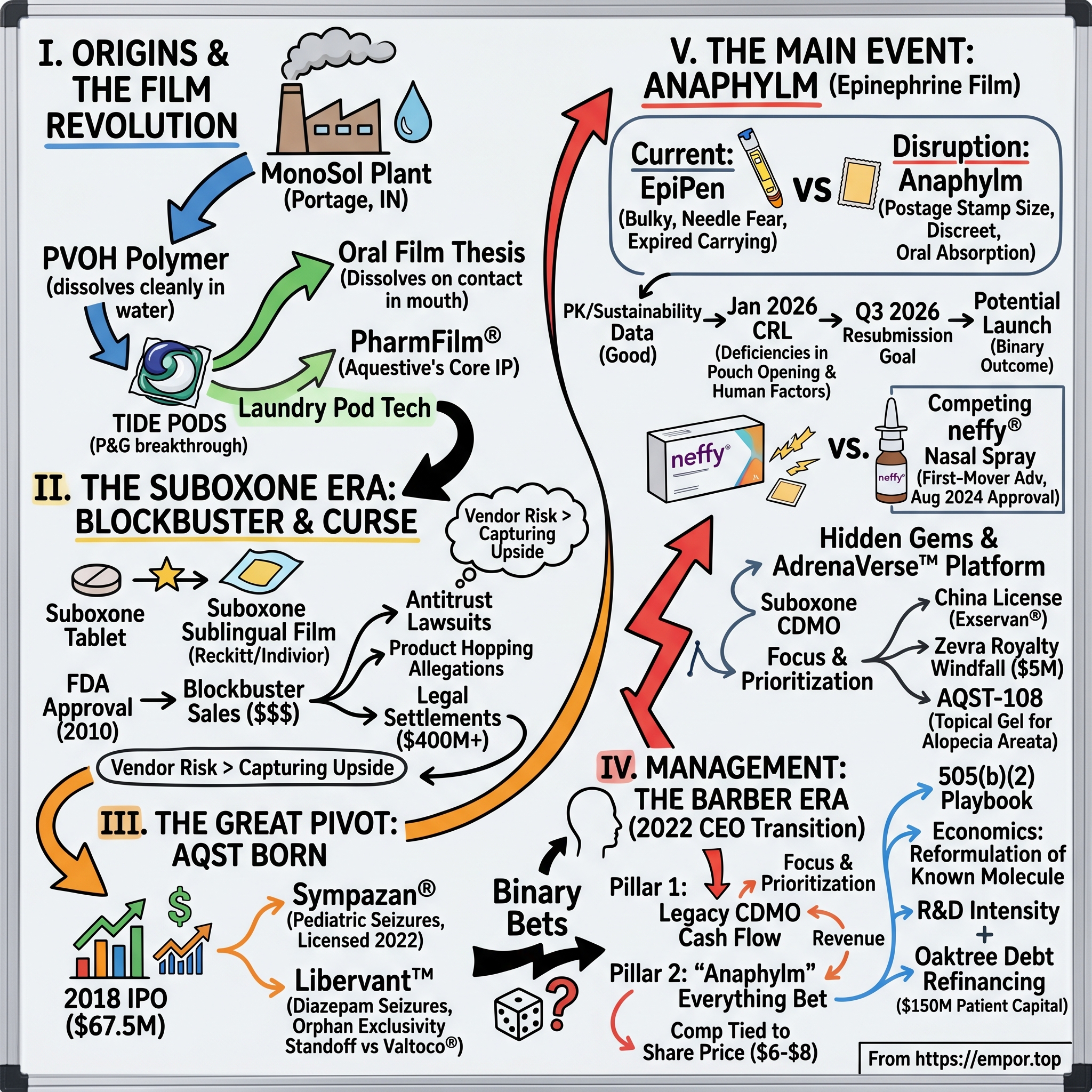

The roadmap for the next two-and-a-half hours runs through some of the strangest corporate genealogy in modern pharma. Aquestive's origin story does not start with a chemist in a lab coat staring at a petri dish. It starts in a polymer plant in northwest Indiana, making the dissolvable plastic that wraps your Tide Pods and your dishwasher tabs. From there, the company learned how to stabilize a complex pharmaceutical molecule inside that same plastic, became the silent manufacturing engine behind the blockbuster opioid-recovery drug Suboxone Sublingual Film, got dragged into one of the ugliest antitrust cases in modern pharma history, spun out as a public company in 2018, lived through a near-death capital crunch, brought in a new CEO with a chemical engineer's pragmatism, and bet the entire company on a single FDA submission for an epinephrine film named Anaphylm.

This is a story about delivery — the unglamorous, deeply technical art of getting a molecule from a foil pouch into a human bloodstream. It is also a story about narrative. The same engineers who taught a Procter & Gamble laundry pod how to fall apart in cold water are now trying to teach the FDA, the allergy community, and the investing public that the most boring word in pharma — formulation — is in fact the most important. Whether the postage stamp wins or whether it ends up as a footnote in the long history of EpiPen alternatives is the question that animates everything that follows.

II. Origins: The MonoSol Split & The Film Revolution

The story begins not in New Jersey, where Aquestive's corporate offices sit today in a low-slung office park in Warren, but on the southern shore of Lake Michigan, in Portage, Indiana. Portage is a steel town. It is where U.S. Steel barges roll in from the Great Lakes and where, in 1953, a company called Chris-Craft Industries spun up a sleepy little chemistry operation to make a strange new polymer: polyvinyl alcohol, or PVOH, a synthetic resin with the rare property of dissolving cleanly in water. For four decades that polymer found a quiet niche packaging agrochemicals — pesticides and fertilizers that farmers wanted pre-portioned so they would not have to handle the raw material. The business was profitable, unsexy, and stagnant.

Then in the late 1990s, somebody at Procter & Gamble had an idea: what if you could put liquid laundry detergent inside one of these dissolvable PVOH packets, throw it into the washing machine, and skip the messy pour-and-measure entirely? The company chosen to make those films was the Portage operation, now consolidated under the name MonoSol. Development of what would become Tide Pods began in earnest in 2004, with MonoSol engineering the dissolvable wrapper.2 By 2012, Tide Pods had become a multi-hundred-million-dollar consumer product, and Japanese specialty chemicals giant 株式会社クラレ Kuraray acquired MonoSol outright2 — confirmation that the humble dissolvable film business was no longer a footnote in industrial chemistry but a global category.

Tucked inside MonoSol, however, was a parallel story that almost nobody noticed at the time. In 2004, the same year P&G greenlit Tide Pods, MonoSol carved out a separate legal entity called MonoSol Rx LLC. The thesis was elegant in hindsight. If you can engineer a film that dissolves on demand in cold water for a washing machine, you can engineer a film that dissolves on demand in saliva for a human mouth. The plumbing is the same; only the customer changes.

It is here that the technological heart of the company — a polymer recipe trademarked as PharmFilm® — was born. To understand why this mattered, you have to appreciate the brutal physics of oral drug delivery. Most pharmaceutical molecules are fragile. Stick them in a pill and they have to survive the stomach, the liver's first-pass metabolism, and the intestines, often losing 80 to 95 percent of their potency before reaching the bloodstream. Stick them in an injection and you bypass all of that, but now you need a needle, a nurse or a panicked patient, sterile manufacturing, and a cold supply chain. Stick them in a sublingual film, however, and the molecule can be absorbed directly through the mucosal tissue under the tongue, bypassing the gut and dumping into the bloodstream within minutes — almost as fast as an injection, but with no needle and no first-pass metabolism.

The problem for the better part of a century was that nobody could figure out how to put a complex drug molecule into a thin water-soluble film without the molecule degrading, crystallizing, or migrating. PharmFilm® cracked that. By layering specific polymers, plasticizers, and stabilizers, MonoSol Rx's chemists figured out how to lock a drug into a film that was paper-thin, shelf-stable for years, and reliably bioequivalent dose to dose. It sounds dull. It was, in fact, the breakthrough that made everything that follows possible.

The early business model was modest and rational: be the picks-and-shovels guy. MonoSol Rx positioned itself as a CDMO — a Contract Development and Manufacturing Organization. Rather than discover drugs, it would license its film platform to big pharma partners who already owned the molecule. Big pharma supplied the drug; MonoSol Rx supplied the delivery. The royalty came back to Indiana. It is the same instinct that built Intel inside personal computers: own the layer everybody else needs and let the rest of the industry pay you rent.

By the late 2000s, the picks-and-shovels strategy was about to get its blockbuster test. And it would come from one of the most controversial, lucrative, and ultimately legally fraught drugs of the modern opioid era.

III. The Suboxone Era: A Blockbuster Blessing and Curse

To understand the Suboxone film, you first have to understand the panic that produced it. By the mid-2000s, the U.K.-based consumer goods giant Reckitt Benckiser — yes, the company that sells Lysol and Durex — had quietly become the dominant player in opioid-addiction treatment, thanks to a tablet product called Suboxone. Suboxone combined buprenorphine, a partial opioid agonist, with naloxone, an overdose blocker, and it was the lifeline keeping hundreds of thousands of Americans off heroin and prescription painkillers. The tablet had received FDA exclusivity in 2002, but that exclusivity was set to expire in late 2009, after which generic manufacturers would be free to crash the party.3

For Reckitt, this was a strategic emergency. Suboxone was generating nearly $1 billion a year. The arithmetic of a generic launch is brutal: within twelve to eighteen months, a brand can lose 80 to 90 percent of its prescription volume to cheaper copies. Reckitt needed a moat — and it needed one fast. So in 2007 the company struck a partnership with the still-obscure MonoSol Rx in Portage, Indiana, to create a sublingual film version of Suboxone. The pitch to physicians and patients would be that the film dissolved faster, was less divertible (harder to snort or smuggle), and was easier to use. The pitch to Reckitt's investors, of course, was simpler: a new patented dosage form would extend the franchise.

In August 2010, the FDA approved Suboxone Sublingual Film.3 Within three years, Reckitt's marketing machine had converted the vast majority of buprenorphine/naloxone prescriptions from tablet to film. For MonoSol Rx, this was nothing short of an industrial transformation. The little Indiana operation went from a curiosity to a manufacturing titan, producing tens of millions of doses per quarter for what became — at its peak — a more than $2 billion global franchise under the Indivior name (Reckitt eventually spun out its pharmaceutical business as Indivior PLC in 2014).

Then came the lawsuits. Beginning in 2013 and accelerating through the late 2010s, generic manufacturers, state attorneys general, and class-action plaintiffs all began alleging the same thing: Reckitt and MonoSol Rx had not switched the market from tablets to film for clinical reasons. They had switched it to block generic competition. The legal term of art is "product hopping" — make a cosmetic change to a drug, ride the new patent, withdraw the old formulation, and force pharmacies to dispense the still-protected version. The civil cases dragged on for a decade. In November 2023, Indivior settled a major antitrust class action for $385 million,4 and shortly thereafter agreed to a separate roughly $102.5 million multi-state settlement that closed the chapter for forty-two state attorneys general.4

It is hard to overstate how formative this episode was for Aquestive's eventual DNA. On one hand, Suboxone Film proved beyond any doubt that the PharmFilm technology could scale to a real blockbuster — clinically, commercially, and at industrial volume. On the other hand, it taught the company, in the most expensive way possible, that being the silent CDMO behind a partner's controversial commercial strategy is not actually a safe haven. When the lawsuits started flying, MonoSol Rx was repeatedly named alongside Indivior. The lesson absorbed by the people who would later run Aquestive was sharp: if you are going to take the regulatory and reputational risk, you might as well capture the upside too.

That epiphany would set the stage for the next, most consequential chapter — the decision to stop being a vendor and start being a brand.

IV. The Great Pivot: From MonoSol Rx to Aquestive

In 2017, the Indiana film maker quietly rebranded itself. The name MonoSol Rx, with its Tide Pods baggage and its CDMO connotation, was retired. In its place came a name engineered to evoke water, fluidity, and scientific inquiry: Aquestive Therapeutics. The new logo was clean. The new website talked about patients, not partners. The new pitch deck talked about pipelines, not capacity. For the first time, the company was not asking what it could manufacture for someone else. It was asking what drugs it could own.

The capital-markets coming-out party arrived on July 25, 2018, when Aquestive priced its initial public offering at $15 a share, sold 4.5 million shares on the NASDAQ Global Market under the ticker AQST, and raised roughly $67.5 million before underwriter overallotments.5 The greenshoe added another 425,727 shares at the same $15 price, layering on about $6.4 million more.5 By specialty-pharma IPO standards, this was a modest debut — but the strategic significance was outsized. For the first time, the company had a public currency, a public mandate, and a roomful of new investors expecting it to behave like a drug owner rather than a drug carrier.

The first proof-point of the pivot was Sympazan® (clobazam), an oral film treatment for seizures associated with Lennox-Gastaut Syndrome, a rare and severe pediatric epilepsy. Sympazan launched in 2018 and represented a meaningful milestone: it was the first commercial drug Aquestive sold under its own brand, with its own sales reps, on its own label. The clinical pitch was straightforward — children with LGS often struggle to swallow tablets, and a film that dissolves on contact with the tongue eliminates a serious adherence problem. Commercially, Sympazan was never going to be a billion-dollar product, but it taught the company that it could in fact build a small specialty sales force and detail to neurologists. In 2022, with capital tighter and focus narrower, Aquestive licensed Sympazan to Otter Pharmaceuticals, a subsidiary of Assertio Holdings, freeing internal resources for higher-conviction bets.[^6]

The harder lesson — and one that would shape Aquestive's strategy for the next five years — came from Libervant™, a buccal film delivery of diazepam designed to treat seizure clusters in patients with epilepsy. Libervant should have been the next clean win. It cleared the FDA's chemistry, manufacturing, and controls reviews. The clinical data held up. Then the company ran into one of the strangest tripwires in U.S. pharmaceutical law: orphan drug exclusivity. A competing product called Valtoco®, a diazepam nasal spray from Neurelis, had received seven years of orphan drug market exclusivity beginning January 10, 2020, for essentially the same indication.[^7] Under FDA rules, even if Aquestive's film was safer, equally effective, and more convenient, it could not be approved for the U.S. market while Valtoco's orphan exclusivity remained in force — unless Aquestive could prove "clinical superiority."

The result was a tentative approval in 2022 that effectively put Libervant in a holding pattern. The legal back-and-forth around pediatric exclusivity and clinical-superiority arguments would absorb significant management time for years. For investors, the Libervant saga became a master class in why specialty pharma is not pure science — it is also a game of regulatory chess, played in seven-year increments, against opponents you may never have heard of.

By the early 2020s, Aquestive had its IPO money, its first commercial drug, a frustrating regulatory standoff, and a complicated relationship with the Suboxone franchise that still paid much of the manufacturing bills. What it did not yet have was a clear, focused, bet-the-company opportunity. That was about to change.

V. Management & The Barber Era

On May 17, 2022, Aquestive's board announced a leadership transition. Keith Kendall, the longtime executive who had taken the company public, stepped aside. In his place came Daniel Barber, then serving as Aquestive's Chief Operating Officer, who was promoted to President and Chief Executive Officer and joined the Board of Directors.6 If Kendall represented the public-company architect — the man who built the brand, ran the IPO, defended the legacy CDMO business — Barber represented something the company desperately needed at that point in its life cycle: a focusing instrument.

Barber's reputation inside Aquestive was that of an operator, not a scientist. He had moved up through the company's commercial and operational ranks. Where Kendall had taken a "let many flowers bloom" approach — running parallel programs in neurology, oncology adjuncts, and consumer health — Barber's first 100 days were defined by aggressive prioritization. The pipeline was pruned. Non-core projects were either licensed out, like Sympazan,[^6] or quietly de-emphasized. Headcount in lower-conviction programs was redirected. The phrase that circulated inside investor calls in late 2022 and early 2023 was something close to "operational excellence over academic curiosity" — a not-very-subtle critique of a culture that, like many small-cap biotechs, had developed a habit of falling in love with too many of its own molecules.

Barber's strategic frame collapsed Aquestive's identity into two pillars. Pillar one was the legacy manufacturing engine: a steady-state CDMO and licensing business with predictable cash flows from partners like Indivior and a roster of international licensees, throwing off enough gross profit to keep the lights on and partially fund development. Pillar two was the "binary bets" — programs with the potential to redefine the company if approved and that, by their nature, would either work spectacularly or not at all. Of those, Anaphylm — sublingual epinephrine — became the everything bet.

The incentive structure put in place under Barber tells you most of what you need to know about management's risk appetite. Executive performance stock units have been tied not to revenue or to milestone announcements but to share-price thresholds in the range of roughly $6.00 to $8.00 per share — multiples above where the stock has traded for much of the past three years.7 In other words, management's biggest paydays only land if the stock works in a big way. That is the kind of comp structure investors love to see in a binary-outcome small cap, because it forces the C-suite into the same lifeboat as common shareholders.

Insider ownership has been consistent with the alignment thesis. Barber and a tight inner circle of insiders have held meaningful positions, and the company's proxy filings have repeatedly emphasized that PSUs make up the bulk of senior executive comp.7 In a sector famous for fat cash salaries paid out regardless of clinical outcome, that profile reads as relatively shareholder-friendly. The flip side — and bears will tell you this loudly — is that compensation tied to a stock price target can encourage promotional behavior, particularly around pivotal regulatory readouts. Whether the comp structure produces discipline or pressure is a question only the next twelve months can answer.

The reorganization, the focus, and the alignment all pointed in one direction: the FDA filing for Anaphylm. By late 2024, every meaningful decision inside Aquestive had been reduced, in some way, to a single question — when does the agency say yes, and what happens to the stock when it does.

VI. The Main Event: Anaphylm & The EpiPen Disruption

To appreciate why Anaphylm matters, take a moment with the EpiPen as it exists today. The device, sold by Viatris (the post-merger successor to Mylan), is essentially a spring-loaded syringe encased in plastic. It costs the U.S. healthcare system on the order of hundreds of dollars per twin-pack at the pharmacy counter. It is bulky, often left at home or in a locker, sensitive to heat and cold (epinephrine degrades when stored above roughly 86 degrees Fahrenheit or frozen), and ten to fifteen percent of patients reportedly carry an expired device at any given time. Surveys of adolescent allergy patients have consistently shown that needle fear and social embarrassment lead to chronic under-carry. In an anaphylactic emergency, the gap between the drug being present and the drug being administered is measured in minutes — and minutes are the difference between recovery and tragedy.

Anaphylm™ is Aquestive's answer. A sublingual film, roughly the size of a postage stamp, containing a proprietary epinephrine prodrug — internally referred to as dibutepinephrine — that is rapidly converted to epinephrine after absorption through the mucosal tissue under the tongue. The pharmacokinetic studies submitted to the FDA showed that Anaphylm delivers epinephrine on a timeline comparable to auto-injectors, including the legacy EpiPen and Auvi-Q, with what the company has described as bracketing, repeat-dose, and sustainability data that the agency did not subsequently question.8

Then came the moment that defined the company's 2026. On January 30, 2026, Aquestive received a Complete Response Letter from the FDA for the Anaphylm New Drug Application in patients weighing 30 kilograms or more.8 A CRL is the regulatory equivalent of "not yet" — not "no," but "go back and fix something." The specific deficiencies cited were not about the molecule. They were about human factors validation: potential challenges associated with pouch opening and film placement, and a request for a single additional pharmacokinetic study to assess the impact of modified packaging and labeling.8 Notably, the CRL did not identify any chemistry, manufacturing, or controls (CMC) issues, and the agency did not question the comparability data versus EpiPen and Auvi-Q.8

For investors, this distinction matters enormously. A CRL based on the molecule failing in pharmacokinetic studies would be existential. A CRL based on whether a panicked teenager can open a foil pouch quickly enough is solvable — by changing the pouch, the instructions, and re-running a relatively contained human factors and PK study. Aquestive's stated path was to request a Type A meeting with the FDA, agree on the most efficient resubmission package, and resubmit in the third quarter of 2026, with the launch dependent on FDA acceptance and a six-month review clock thereafter.8

Standing between Anaphylm and the brass ring is a meaningful competitor: neffy®, the epinephrine nasal spray from ARS Pharmaceuticals. The FDA approved neffy on August 9, 2024, making it the first non-injectable epinephrine product cleared for type I allergic reactions including anaphylaxis in adults and children weighing at least 30 kilograms.9 A pediatric 1 mg dose was approved subsequently for children weighing 15 to under 30 kilograms.9 neffy enjoys the first-mover advantage that Anaphylm now no longer has, and it is in pharmacies, in physician detail bags, and in the cultural conversation. The bull case for Anaphylm versus neffy rests on a clinical wager: that a sublingual film, absorbed through the mouth, will be perceived by patients and prescribers as faster, more discreet, and less affected by edge cases like nasal congestion or runny noses during an active allergic reaction. The bear case is that needle-free is needle-free, and the first product to market often defines the category.

If Anaphylm clears the FDA in 2026 or early 2027, the prize is participation in what management has framed as a multi-billion-dollar U.S. epinephrine market that has historically been almost entirely owned by EpiPen. If it does not, the binary outcome flips against the company in the most uncomfortable way possible.

VII. Hidden Gems & The "AdrenaVerse"

The story Aquestive tells the market is dominated by Anaphylm, but underneath that narrative lies a quieter and arguably more durable business: the legacy CDMO and licensing engine inherited from MonoSol Rx. This part of the company does not generate dramatic headlines, but it pays many of the bills and provides the partial insulation that lets Barber take the binary bet without going bust.

The flagship CDMO relationship remains Suboxone Sublingual Film, where Aquestive continues to manufacture the product as the contract producer behind Indivior — a relationship now more than fifteen years old and one that has generated the bulk of the company's manufacturing and supply revenue for over a decade. Outside Suboxone, Aquestive has built a globally diversified roster of international film licensees. In Brazil, the company has supplied Ondif® (ondansetron oral film) for partner Hypera Pharma, addressing nausea and vomiting in patients who struggle to swallow conventional tablets. In China, on March 3, 2022, Aquestive signed a License, Development and Supply Agreement with 海思科医药集团 Haisco Pharmaceutical Group to develop and exclusively commercialize Exservan® (riluzole oral film) for amyotrophic lateral sclerosis, with Aquestive receiving a $7 million upfront cash payment plus eligibility for milestone payments and royalties on net sales — and crucially, remaining the exclusive global manufacturer of the product.10 Additional international supply relationships extend the geographic footprint.

The most interesting hidden gem in the 2026 income statement, however, has been the windfall from Zevra Therapeutics. In the first quarter of 2026, Aquestive's total revenue rose 66 percent year-over-year to $14.4 million, with license and royalty revenue alone contributing $5.4 million — a category that had been a sleepy contributor in prior years.11 The jump was driven by a roughly $5 million royalty triggered when Zevra Therapeutics sold its SDX portfolio to Commave Therapeutics for $50 million in March 2026; under prior contractual arrangements, Aquestive collected approximately 10 percent of the gross proceeds.11 This is the kind of asset that almost never shows up in a forward DCF model: a dormant royalty stream that suddenly produces a one-time cash event when a partner monetizes a downstream asset.

The other genuinely fresh leg of Aquestive's growth story is the AdrenaVerse™ platform — a portfolio of more than twenty proprietary epinephrine prodrug formulations engineered to release the active drug selectively across different tissues and routes. Anaphylm is the lead asset in this library, but the asset attracting growing attention is AQST-108, a topical epinephrine gel being developed initially for alopecia areata, a relatively common autoimmune-driven form of hair loss that affects an estimated 6.7 million people in the United States.12 Today the standard of care for alopecia areata is dominated by oral JAK inhibitors, which are expensive, systemic, and carry black-box warnings. AQST-108's pitch is the opposite: a topical, non-systemic delivery that, in theory, restricts the epinephrine effect to the skin and follicle, avoiding the side-effect profile that has limited JAK inhibitor uptake.12

Aquestive has guided that AQST-108 had an IND filing on track for late 2025, with a clinical study beginning in the first half of 2026, and management has repeatedly emphasized that the AdrenaVerse library could be extended to atopic dermatitis, rosacea, and psoriasis if early clinical signals look favorable.12 Whether any of this turns into a real commercial franchise is years away from being known. But for an Aquestive valued primarily on Anaphylm, the AdrenaVerse adds a long-dated optionality layer that does not require new platform science — only new indications and new formulations of the same underlying epinephrine prodrug chemistry.

Put together, the manufacturing engine, the international licensing portfolio, the Zevra-style royalty optionality, and the AdrenaVerse pipeline represent a business that, even in a worst-case Anaphylm outcome, would still be doing real work. That is the foundation on which the binary bet sits.

VIII. Playbook: Business & Investing Lessons

Step back from the Anaphylm drama for a moment and look at Aquestive as a case study in modern specialty pharma strategy. The company is, in many ways, a textbook example of how to play the 505(b)(2) game — the FDA pathway for drugs that rely on existing safety and efficacy data for a known active ingredient combined with a new formulation or route of administration. This is the regulatory back door through which the smartest specialty pharma companies have walked for the past two decades, and it is the highest-ROI corner of the industry that most generalist investors do not understand.

The economics of 505(b)(2) are elegant. You take a molecule that has been on the market for decades and has therefore accumulated mountains of safety data — epinephrine, diazepam, clobazam, riluzole — and you reformulate it. The new dosage form might be sublingual instead of injected, or buccal instead of nasal, or topical instead of oral. You do not have to re-prove that the active ingredient works. You only have to prove that your new delivery is comparable and useful. That collapses development costs from the billions associated with a true new chemical entity to something in the tens of millions. If you can solve a real patient problem with the new form — say, "I cannot swallow tablets" or "I refuse to carry a needle" — you can claim a premium price, protect the franchise with formulation patents, and harvest the spread between development cost and reimbursement. Aquestive's entire portfolio, from Suboxone Film through Anaphylm, has been built on this exact bet.

The trade-off is that 505(b)(2) products do not enjoy the same long composition-of-matter patent lives as new molecules. So management has to fight a different war — building patent thickets around the formulation, the delivery, the packaging, even the manufacturing process. This is precisely why Aquestive obsesses over its PharmFilm® patent portfolio and the manufacturing know-how locked inside the Portage, Indiana plant. Without that wall, the moat collapses.

R&D intensity at Aquestive runs in the neighborhood of 30 to 35 percent of revenue, well above the 10 to 15 percent average for established pharma. That ratio is not the sign of an inefficient company; it is the sign of a company front-loading clinical investment ahead of a near-term inflection. Management has consistently framed this as the cost of pursuing the Anaphylm/AdrenaVerse opportunity at the maximum possible speed. The bear interpretation is that high R&D intensity in a small-cap with limited revenue is also high cash-burn intensity, and cash burn in a binary-outcome company is what kills it before the binary outcome can pay off.

Which brings us to capital allocation — and to what is arguably Barber's most important non-clinical decision of his tenure. Rather than fund Anaphylm via dilutive equity raises that would punish existing shareholders, Aquestive returned to private credit. On May 12, 2026, the company closed a $150 million debt refinancing with funds managed by 橡树资本管理 Oaktree Capital Management. The structure was deliberately patient: $55 million funded at close (used primarily to repay an existing $45 million note plus fees), an additional $20 million tranche available upon FDA approval of Anaphylm, and further tranches of $25 million and up to $50 million tied to commercial milestones.13 The five-year term loan pushes principal repayment out to 2031, with interest-only payments in the interim.13

This is what specialty pharma analysts call "synthetic M&A" or, more bluntly, royalty- and debt-backed bridge financing. The point is to monetize the optionality of the pipeline without surrendering equity ownership or selling the company outright. Combined with the existing CDMO cash flows, the Oaktree facility gives Aquestive a runway through the expected Q3 2026 resubmission and into a potential commercial launch.13 If Anaphylm clears, the additional tranches unlock and the company funds its own launch. If it does not, that debt sits on the balance sheet and becomes the next constraint.

Above all, the playbook lesson here is what Hamilton Helmer would call a Cornered Resource. Aquestive's real moat is not a single molecule. It is the combination of the PharmFilm® IP portfolio, the specialized commercial-scale film manufacturing equipment in Portage, the regulatory know-how accumulated across Suboxone and Sympazan and Libervant, and the operational scar tissue from a decade of running large-scale film production for a controversial blockbuster. Competitors can copy a molecule. Replicating the entire stack is harder than it looks.

IX. Analysis: Frameworks & The Bear/Bull Case

Now run Aquestive through the standard analytical machinery — 哈密尔顿·赫尔默 Hamilton Helmer's 7 Powers and 迈克尔·波特 Michael Porter's Five Forces — and the picture sharpens considerably.

On the 7 Powers side, the Cornered Resource argument is the strongest. The PharmFilm® patent estate, layered with decades of process know-how at a single FDA-registered manufacturing site in Portage, Indiana — operating across roughly 34,400 square feet of FDA-approved manufacturing, packaging and distribution space[^16] — constitutes a barrier that has so far prevented serious competition in commercial-scale, drug-loaded sublingual film. Scale Economies are real but bounded; Aquestive is essentially the world's only volume manufacturer of pharmaceutical-grade oral films at this scale, which gives it cost advantages and supplier-of-choice status for global licensees. Switching Costs build slowly: once an allergy treatment protocol embeds Anaphylm into clinical practice — pediatric allergists, schools, anaphylaxis action plans — the inertia of clinical guidelines becomes its own competitive advantage. Branding and Network Effects are weak in this market, and Counter-Positioning is partial; competitors like ARS Pharmaceuticals and Viatris have the resources to compete, but they cannot easily replicate the film manufacturing stack without years of investment.

Porter's Five Forces tells a more nuanced story. Threat of substitutes is the dominant force in the epinephrine market — needle (EpiPen, Auvi-Q), nasal (neffy), and sublingual (Anaphylm) are now three meaningfully different delivery technologies competing for the same anaphylaxis prescription, and patient preference, insurance formularies, and pediatric labeling will sort the winners over time. Rivalry is intensifying; ARS Pharmaceuticals' first-mover position with neffy raises the stakes considerably,9 and Viatris will defend its EpiPen franchise aggressively. Bargaining power of buyers — primarily pharmacy benefit managers and large payers — is significant in U.S. pharma generally, and any newer epinephrine product will need to negotiate formulary placement against existing entrenched coverage. Bargaining power of suppliers is low; the active ingredient (epinephrine) has been a commodity for decades. Threat of new entrants is moderate; the 505(b)(2) pathway is open to anyone, but Aquestive's manufacturing and IP barrier slows the next wave of imitators by years.

The bull case writes itself, but with discipline. If Anaphylm wins approval following a Q3 2026 resubmission, Aquestive will hold the first sublingual epinephrine product on the U.S. market. The clinical pitch — needle-free, pocket-sized, stable across temperature ranges where auto-injectors degrade — is intuitive to allergists and to teenagers, the two constituencies that determine prescription velocity. Even modest market share, in a U.S. anaphylaxis market estimated by various analysts at well over $2 billion in annual branded revenue, translates into transformative economics for a company today valued at roughly half a billion dollars.1 Layer on AdrenaVerse optionality and the international CDMO engine, and the upside scenarios get interesting quickly.

The bear case is just as cleanly drawn. The CRL has already pushed approval out at least nine to twelve months from the original timeline, which means neffy enjoys an extended period of unopposed needle-free competition.89 If the Q3 2026 resubmission produces a second CRL — particularly one citing pharmacokinetics rather than human factors — Anaphylm's path to market could narrow dramatically, and the Oaktree debt would become an active constraint rather than a quiet enabler. Even an approval is not a victory if the commercial launch is bungled: specialty pharma is littered with technically successful drugs that failed because field-force economics, formulary access, and pediatric labeling did not align. And the bear case has a quieter dimension too — the Libervant orphan-exclusivity standoff demonstrated how thoroughly a small competitor with the right regulatory wedge can stall a superior product.[^7]

A few myth-versus-reality calls worth flagging. The first myth is that Anaphylm is a "new drug." It is not; epinephrine has been the standard of care in anaphylaxis since the 1960s. What is new is the delivery. The second myth is that the January 2026 CRL was a "failure." It was a delay; the agency explicitly did not challenge the molecule's clinical comparability to auto-injectors.8 The third myth, often heard in retail investor circles, is that Aquestive is a "needle-free play" interchangeable with ARS Pharmaceuticals. Mechanistically the two products differ — nasal versus sublingual absorption — and the data on rapid uptake during active anaphylaxis (when noses may be running and mucosal absorption variable) will likely become a meaningful clinical battleground.

The KPIs investors should anchor on are not difficult to identify. There are essentially three. The first is the resubmission and ultimate approval outcome for Anaphylm. The second is the quarterly trajectory of manufacturing and supply revenue from the legacy CDMO base — this is the proxy for whether the existing business holds together while the new launch is built. The third is the cash runway in light of the Oaktree facility, particularly the unlocking of additional tranches contingent on FDA approval and commercial milestones.13 Anything else is noise around those three.

X. Epilogue

Aquestive Therapeutics, at this moment in May 2026, is something more interesting than it appears on its market cap line. It is a forty-plus-year-old industrial chemistry company in northwest Indiana that learned how to make Tide Pods, then learned how to make blockbuster pharmaceutical films, then learned how to be a public company, then learned how to be a sales organization, and is now learning whether it can be the company that finally retires the EpiPen.

The question of whether it is "the next great specialty pharma" or a "niche tech company that flew too close to the sun" is genuinely undecided. The answer turns less on the molecule than on three boring, unsexy variables: how cleanly the human factors fix is engineered into the new Anaphylm packaging, how disciplined Daniel Barber and his team are with the Oaktree capital, and how aggressively the U.S. allergy community is willing to swap a familiar needle for an unfamiliar film. The first variable will be resolved in the FDA review queue. The second is being demonstrated quarter by quarter. The third will be settled in the marketplace.

The two events that listeners should circle on their 2026 and 2027 calendars are straightforward. First, the Q3 2026 NDA resubmission for Anaphylm and the FDA's response to it — that single decision rewrites the company's narrative. Second, the eventual full U.S. launch of Libervant in 2027, assuming the orphan drug exclusivity overhang is cleared by then,[^7] which would convert a long-running source of strategic frustration into a genuine commercial product and add a second epilepsy-adjacent revenue stream to the model.

The postage-stamp dream is still just that — a dream. But for the first time in the long arc that runs from a 1953 polymer plant in Indiana through Tide Pods and Suboxone Film and Sympazan and Libervant and the AdrenaVerse, Aquestive has compressed the entire question of its future into something an FDA reviewer, a parent at a Little League game, and an allergist in private practice can each answer in their own way. That clarity, regardless of how the verdict lands, is itself a kind of progress.

References

-

Aquestive Therapeutics (AQST) Market Cap & Net Worth — Stock Analysis, 2026 ↩↩

-

MonoSol's claim to fame: maker of Tide Pod detergent gel-packs — Crain's Chicago Business, 2013-12-07 ↩↩

-

AG Schwalb Secures Over $2.3 Million from Suboxone Maker Accused of Monopolizing Opioid Treatment Drug — Office of the Attorney General for the District of Columbia ↩↩

-

Maker of Opioid Addiction Treatment Drug Suboxone Accused of Conspiring to Keep Monopoly Profits — Office of the Attorney General for the District of Columbia ↩↩

-

Aquestive Therapeutics IPO Prospectus (Form 424B4) — SEC EDGAR, 2018-07-25 ↩↩

-

Aquestive Therapeutics Announces CEO Transition — GlobeNewswire, 2022-05-17 ↩

-

Aquestive Therapeutics Annual Report (Form 10-K) — SEC EDGAR, 2025-03-05 ↩↩

-

Aquestive Therapeutics Announces FDA Issuance of Complete Response Letter for Anaphylm — GlobeNewswire, 2026-02-02 ↩↩↩↩↩↩↩

-

ARS Pharmaceuticals Receives FDA Approval of neffy® (epinephrine nasal spray) — GlobeNewswire, 2024-08-09 ↩↩↩↩

-

Aquestive Therapeutics and Haisco Pharmaceutical Group Enter Licensing and Supply Agreement for Riluzole Oral Film for ALS Treatment in China — GlobeNewswire, 2022-03-03 ↩

-

Aquestive Therapeutics Reports First Quarter 2026 Financial Results and Provides Business Update — GlobeNewswire, 2026-05-13 ↩↩

-

Aquestive Therapeutics Spotlights its Innovative Epinephrine Delivery Pipeline at Virtual Investor Day — GlobeNewswire, 2024-09-27 ↩↩↩

-

Aquestive Therapeutics Completes $150 Million Debt Refinancing with Oaktree — GlobeNewswire, 2026-05-12 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube