Aptiv PLC: The Ultimate Mutating Machine of Detroit

I. Introduction & Episode Roadmap

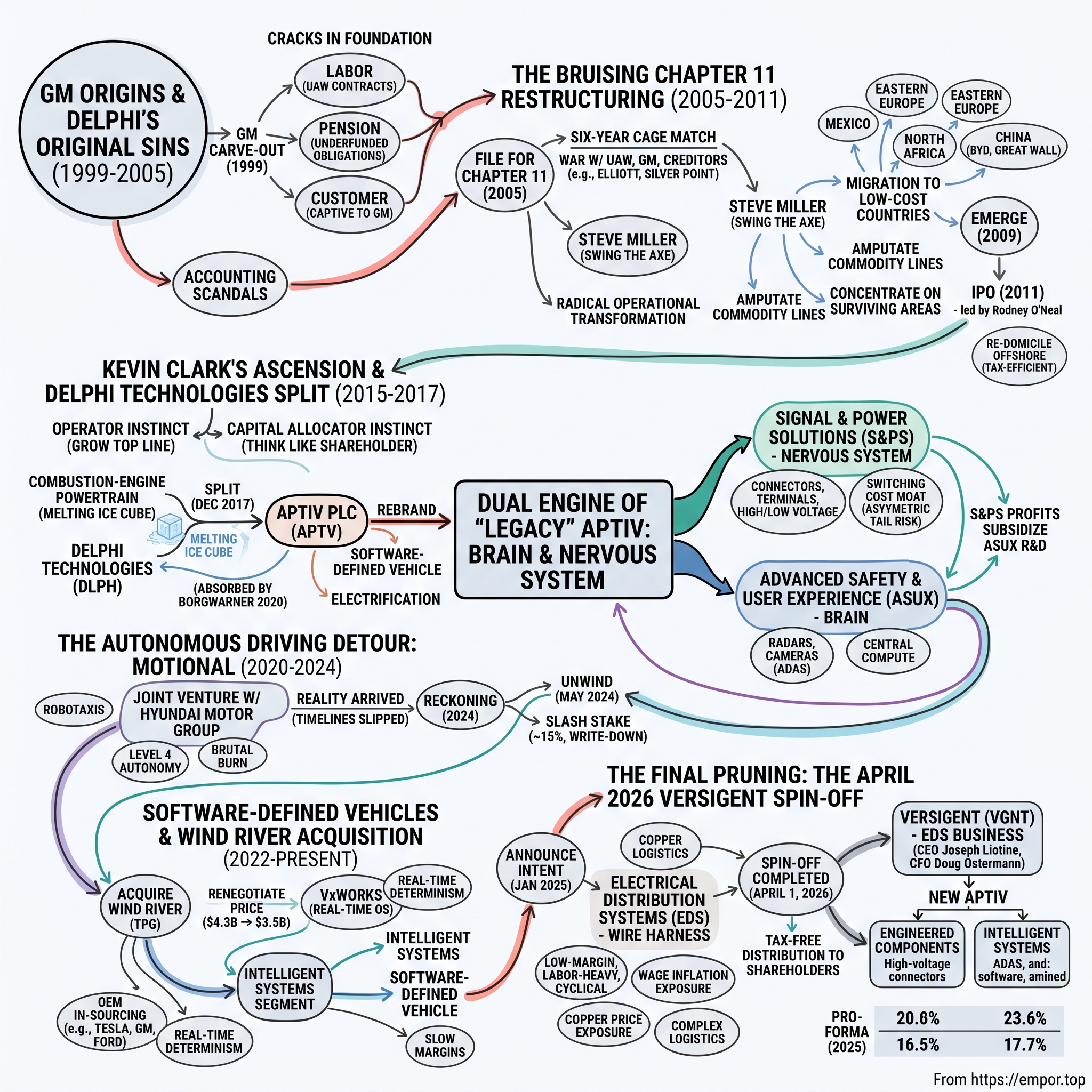

On the morning of April 1, 2026, a company that did not exist the day before began trading on the floor of the New York Stock Exchange under the ticker VGNT. It was called Versigent, and inside it sat one of the oldest, most labor-intensive businesses in the entire automotive supply chain: the manufacture of wire harnesses — the bundled arteries of copper and insulation that thread through every car ever built. For every three shares of Aptiv PLC an investor held at the close on March 17, one share of Versigent landed in the account, delivered as a tax-free distribution.2 With that single stroke, Aptiv shed roughly $8.8 billion of annual revenue and, more to the point, shed the part of itself it had spent thirty years trying to escape.1

Here is the paradox worth sitting with. The corporate DNA of the entity now branded "New Aptiv" — a $12–13 billion revenue technology company pitching Wall Street on software-defined vehicles, central compute, and premium electrical interconnects — traces directly back to the parts division of General Motors.1 This was the division saddled with the most expensive union labor in American manufacturing, the division that filed one of the largest industrial bankruptcies in U.S. history, the division that at its low point was a punchline for everything wrong with legacy Detroit. How does a business go from that to a company whose entire investment thesis rests on earning a "tech multiple"? That is the story of the ultimate mutating machine.

The recent catalyst — the Versigent spin — is the fifth or sixth act in a decades-long serial reinvention, and it deserves scrutiny rather than applause. Management's framing is seductive: cut loose the low-margin, manual assembly business, and the market will finally re-rate the high-margin "brain" and "joints" of the modern vehicle. Post-separation, Aptiv is a power-agnostic supplier organized around two engines: Intelligent Systems (the perception, compute, and software stack) and Engineered Components (high-voltage connectors, interconnects, and cable management).1 The pitch is that these are structurally better businesses than the harness assembly they left behind. The counter-question, which we will press throughout, is whether serial financial engineering is a substitute for durable organic growth — or a distraction from its absence.

To get there, this is the roadmap:

- The original sins baked into the 1999 GM carve-out and the legacy Delphi structure.

- The grueling 2005–2011 Chapter 11 bankruptcy and the great migration to low-cost countries.

- Kevin Clark's ascension and the 2017 split that jettisoned the combustion-engine business and birthed "Aptiv."

- The autonomous-driving detour — the cash-torching Motional joint venture with 현대자동차그룹 Hyundai Motor Group, and its abrupt 2024 unwind.

- The software bet: the renegotiated $3.5 billion acquisition of Wind River.

- The 2026 Versigent spin — strategic rationale, segment economics, and an activist-grade bull/bear stress test.

The through-line is not technology. It is capital allocation. Aptiv's defining competency, for better and worse, has been an almost restless willingness to buy, sell, spin, and restructure its own body. Whether that restlessness has actually created durable value — or merely rearranged it — is the question the market is now, once again, being asked to answer.

One more framing device is worth installing before the story begins, because it will recur at every turn: the tension between narrative and arithmetic. Aptiv has, for a decade, been sold to investors as a story — a story of transformation, of secular megatrends, of a Detroit dinosaur reborn as a Silicon Valley-adjacent platform. Stories move multiples. But underneath every story sits a set of numbers — segment margins, cash conversion, organic growth — that either validates the narrative or quietly contradicts it. The most useful posture toward this company is neither the bull's enthusiasm for the transformation nor the bear's cynicism about the financial engineering, but a stubborn insistence on checking the story against the arithmetic at each step. That is the discipline this piece tries to model.

II. GM Origins & Delphi's Original Sins (1999–2005)

Picture the American auto industry at the tail end of the 1990s. Sport-utility vehicles were minting money, gas was cheap, and General Motors was the largest industrial enterprise on Earth. Buried inside it was a component-making colossus that stamped, wired, and assembled a staggering share of the parts in every GM vehicle. In 1999, GM spun that division out as Delphi Automotive Systems in one of the largest corporate separations of its era. On paper, it was liberation: Delphi could finally chase business from Ford, Toyota, and Volkswagen instead of being a captive vassal. In practice, it was closer to an eviction — and the new tenant inherited a house with a cracked foundation.

The first crack was labor. Delphi walked out the door bound to the same United Auto Workers contracts that governed GM's assembly plants, contracts written for a company that could pass costs on to buyers of full-margin trucks. A senior Delphi production worker's fully loaded cost — wages plus healthcare, pensions, and the notorious "Jobs Bank" that paid idled workers — could reach the mid-$60s per hour, at a time when non-union component peers operated at a fraction of that. For a business selling connectors and modules priced in pennies and dollars, where an automaker's purchasing department fights over tenths of a cent, that cost structure was not a disadvantage; it was a slow-motion death sentence.

The second crack was the pension. Delphi left GM carrying enormous, chronically underfunded retirement and retiree-healthcare obligations for a workforce that had been promised gold-plated benefits in a different economic age. These liabilities behaved like a mortgage taken out against a house whose value was falling: fixed, senior, and indifferent to how the business was actually doing.

The third crack was the customer. In its early years the overwhelming majority of Delphi's revenue flowed from a single account — General Motors — a customer that was itself losing U.S. market share year after year to Japanese rivals.10 This is the worst of both worlds for a supplier. Your largest customer squeezes you hardest on price because it can, and its own decline drags your volumes down with it. Meanwhile, rival automakers are understandably wary of routing their most sensitive component business through a supplier that is, in effect, GM's former organ.

Under that pressure, something predictable happened: the numbers started to bend. In the early 2000s Delphi became ensnared in accounting scandals involving improperly booked transactions and inventory and rebate schemes designed to flatter results, drawing scrutiny from regulators and forcing out senior management. The specifics matter less than the lesson. When a business is structurally unable to earn its cost of capital, the temptation to manufacture the appearance of health becomes overwhelming.

It is worth pausing on why the captive-customer problem was so uniquely toxic for a components company, because it is the sort of structural trap that recurs across the supplier economy. A diversified supplier plays its customers against one another: if Ford squeezes too hard, it wins more business at Toyota, and that credible alternative is what preserves its pricing power. A captive supplier has no such leverage. Its dominant customer knows exactly how dependent it is and prices accordingly, extracting the supplier's margin as a matter of routine. Worse, rival automakers view a former in-house division as a competitor's appendage and are reluctant to hand it their most sensitive programs — so the very captivity that caps the margin also blocks the diversification that would cure it. Delphi was thus locked in a box: too dependent on GM to earn a decent return, and too tainted by that dependence to easily escape it. This is the single most important thing to understand about the company's starting position, and it explains why nearly every strategic move for the next twenty-five years was, at bottom, an attempt to break out of that box.

The deeper analytical point — and the one that echoes through everything that follows — is that a carve-out engineered primarily to offload a parent's legacy labor and pension burdens is unviable from birth. GM did not spin out Delphi because Delphi was a great standalone business poised to flourish. It spun it out, in significant part, to move liabilities off its own books. A company designed as someone else's "bad bank" starts the race already carrying the weight of two. Everything Delphi's successors did over the next quarter-century — the bankruptcy, the offshoring, the serial spin-offs — can be read as an escalating attempt to finally set that weight down. The first, most violent attempt came in a Manhattan bankruptcy court.

III. The Bruising Chapter 11 Restructuring (2005–2011)

On October 8, 2005, Delphi filed for Chapter 11. What followed was not a tidy, prepackaged restructuring but a six-year cage match — one of the longest and most contentious industrial bankruptcies the American courts had ever processed, a war fought simultaneously against the UAW, against GM, and against a rotating cast of some of the most aggressive investors on Wall Street.10

The man brought in to swing the axe was Steve Miller, a restructuring specialist with a résumé built on distressed and dying industrial giants. Miller was blunt to the point of provocation about the arithmetic: a company could not pay first-world union wages to build commodity parts sold into a globalized market and survive. His job was to say the unsayable out loud and then act on it — to break contracts, close plants, and force concessions that decades of collective bargaining had made politically untouchable. He became, depending on which side of the negotiating table you sat on, either the surgeon or the executioner.

Around the wreckage circled the distressed-debt funds, and this is where the drama sharpened. Paul Singer's Elliott Management and Silver Point Capital, among others, accumulated large positions in Delphi's debt and equity, turning the bankruptcy into a proxy battle over one central question: who would pay to fill the pension hole and fund the reorganization — GM, or the new creditors?10 GM had a powerful incentive to keep Delphi alive; a disorderly liquidation of its largest supplier would have halted GM's own assembly lines. That leverage is precisely what the funds sought to exploit. The negotiation dragged on so long partly because the 2008 financial crisis detonated in the middle of it, vaporizing an earlier equity-infusion deal and dragging GM itself toward its own government-backed bankruptcy in 2009.

While the lawyers fought, the operational transformation underneath was radical and permanent. Delphi took a scalpel to its U.S. manufacturing footprint, collapsing dozens of American plants down to a bare handful and relocating the bulk of its labor-intensive work to lower-cost geographies — Mexico, Eastern Europe, North Africa, and China. This was the pivotal, irreversible act: the physical relocation of the wire-harness and assembly base to wherever manual labor was cheapest. In China, the strategy meant building out capacity alongside the rising domestic automakers — the ecosystem that would later include champions like 比亚迪 BYD and 长城汽车 Great Wall Motor — positioning the company inside the fastest-growing car market on the planet rather than defending a shrinking one at home.

There is a human cost buried in that sentence that the financial framing tends to erase, and it is worth naming plainly, because it is also part of why the transformation was so wrenching and so slow. Collapsing the U.S. footprint meant shuttering plants in the industrial Midwest that had employed generations of the same families, communities whose entire economic existence had been organized around a Delphi facility. The bankruptcy court's cold arithmetic — that a wire could be assembled in Ciudad Juárez for a fraction of the loaded cost in Ohio — was, for tens of thousands of workers and retirees, a rupture in the American industrial compact. Investors evaluating the company today are looking at the far side of that rupture: a cost structure rebuilt from the ground up in low-wage geographies. But the political and reputational residue of how it was rebuilt has never entirely dissipated, and it is part of why the wire-harness business, even reorganized and profitable, remained something Aptiv's leadership seemed to want at arm's length.

Just as important as where Delphi made things was what it chose to stop making. Management deliberately amputated whole commodity product lines — brakes, chassis, steering, spark plugs — categories where it had no path to a defensible margin, and concentrated the surviving company around two areas: electrical architecture and vehicle electronics. This was the intellectual seed of everything Aptiv would later become. The insight was that the value in a car was migrating from mechanical hardware toward the electrical and electronic systems that made the vehicle safer, more connected, and more computerized. Delphi decided, in the depths of bankruptcy, to bet the surviving company on that migration.

Delphi emerged from Chapter 11 in 2009 as a leaner, restructured entity, and in November 2011 it returned to the public markets with an initial public offering, now led by CEO Rodney O'Neal.10 Crucially, it re-domiciled offshore, adopting a tax-efficient structure that would eventually settle into a Jersey-incorporated, Switzerland-tax-resident form.6 This was not a footnote; it was a competitive weapon. In a business where operating margins are thin and every point of the tax rate matters, a supplier that pays a materially lower effective tax rate than its Detroit-domiciled peers keeps more of every dollar it earns and can either underprice competitors on bids or out-invest them in R&D from the same revenue. The offshore structure that emerged from bankruptcy quietly widened Delphi's — and later Aptiv's — cash-flow advantage over rivals still anchored to higher-tax jurisdictions, and it remains a structural feature of the company to this day, with the corporate headquarters registered in Schaffhausen, Switzerland.6 It is one of the least-discussed but most durable legacies of the restructuring: the company emerged not just leaner and offshored operationally, but re-engineered at the level of the tax code itself. The company that walked out of bankruptcy court had shed its plants, much of its union labor, and a good chunk of its pension burden — and had quietly acquired something its GM-owned predecessor never had: the freedom to reinvent itself again. It would use that freedom almost immediately.

IV. Kevin Clark's Ascension & The Delphi Technologies Split (2015–2017)

The executive who would define the modern company did not come from Detroit, did not come from engineering, and had spent much of his career nowhere near a factory floor. Kevin Clark was a finance man — a former chief financial officer whose formative years included senior finance roles in the scientific-instruments world before he joined Delphi as CFO in 2010. When he took over as chief executive in 2015, it marked a subtle but decisive shift in the company's center of gravity: from the operators who ran the plants to the capital allocator who ran the portfolio.

Clark's worldview was that of an investor who happened to own an auto-parts company. He looked at the collection of businesses he inherited and asked the question a private-equity partner asks: which of these deserve capital, and which are quietly destroying it? His personal incentives were wired to reinforce that lens — a compensation structure weighted toward performance-based equity measured against relative total shareholder return and cash-flow conversion, aligning his payout with the stock's performance versus peers rather than with revenue for its own sake. He was, in the most literal sense, paid to think like a shareholder.

That distinction — thinking like a shareholder rather than like an operator — turns out to matter enormously in the auto-supply business, and it is worth dwelling on because it defines the entire Clark era. The traditional Tier 1 supplier is run by lifers who came up through engineering and manufacturing, people whose instinct is to grow the top line, win more platforms, and defend market share plant by plant. That instinct builds sprawling, low-margin conglomerates — companies that make a little bit of everything for everyone and trade at the depressed multiples such businesses deserve. A capital allocator's instinct is the opposite: to be indifferent to size, ruthless about return, and willing to shrink the company if shrinking raises its per-share value. Clark brought the second instinct to an industry dominated by the first. Whether one views his tenure as visionary or as serial financial engineering, it flows from that single temperamental fact. He did not love cars the way a Detroit lifer loves cars; he loved returns on capital, and he happened to be pointing them at a car-parts company.

The business Clark fixed on first was the powertrain division — the fuel injectors, valvetrain systems, and engine-management hardware that had descended from Delphi's original combustion-engine heritage. It was a real business: cash-generative, technically respectable, globally scaled. But Clark saw it for what it was becoming — a "melting ice cube." Every serious forecast pointed toward the long, slow decline of the internal combustion engine as electrification advanced. A cash cow tied to a dying propulsion technology does something corrosive to a company's valuation: the market prices the whole enterprise for the terminal business, and the growth businesses trapped inside it never get the multiple they deserve. Clark's instinct was that the powertrain unit was dragging down the entire company's rating.

So in December 2017, Delphi executed the split that would give the modern company its name.9 The combustion-engine powertrain and aftermarket operations were spun off as a separate, independent public company called Delphi Technologies, trading under DLPH. The remaining, higher-technology core — the electrical architecture business and the advanced safety and infotainment electronics — kept the crown jewels and adopted a new identity: Aptiv PLC.9 The epilogue for the discarded half is instructive. Delphi Technologies struggled as a standalone melting ice cube, its valuation compressed by exactly the forces Clark had foreseen, and in 2020 it was absorbed by BorgWarner in an all-stock deal at a modest price. The market had, in effect, ratified the diagnosis: the powertrain business really was worth less on its own, and separating it protected the rest.

The rebrand was more than cosmetics; it was a repositioning aimed squarely at Wall Street. The name "Aptiv" — a coinage meant to evoke aptitude and activity — was chosen precisely because it carried none of the century of Detroit baggage that clung to "Delphi." Management set out to reintroduce the company not as a cyclical, capital-heavy Tier 1 auto supplier trading at single-digit earnings multiples, but as a pure-play enabler of two secular megatrends: the software-defined vehicle and the electrification of the fleet. It was a bid to change the peer group in the market's mind — to be compared not with parts makers but with technology platforms. Whether the underlying business truly deserved that reclassification is the tension that has animated the stock ever since, and it starts with understanding the two very different engines that now sat inside Aptiv.

V. The Dual Engine of "Legacy" Aptiv: Brain & Nervous System

To understand why Aptiv could plausibly claim to be more than an ordinary parts supplier, you have to open the hood and look at the two fundamentally different machines humming underneath — and appreciate that they earned their money in almost opposite ways.

The first engine was the electrical architecture business, historically reported for years as Signal and Power Solutions — think of it as the car's nervous system. This was the empire of connectors, terminals, cable management, and high- and low-voltage distribution: the tens of thousands of small, unglamorous physical parts that carry electrons and data from one end of a vehicle to the other. The moat here is one of the most underappreciated in the entire auto supply chain, and it is worth explaining in plain terms. A single connector may cost a few cents, but if it fails, the airbag doesn't fire or the battery pack doesn't communicate. Automakers therefore qualify these components through years of grueling testing and then design them directly into the vehicle's electrical platform. Once a connector is engineered in, ripping it out to save a fraction of a cent means re-validating an entire safety-critical system — an enormous risk for a trivial reward. The result is exactly the kind of switching cost that compounds into pricing power and long product lifecycles. In this arena Aptiv went head-to-head with the two acknowledged royalty of interconnect — TE Connectivity and Amphenol — companies the market has long rewarded with premium multiples precisely because of these dynamics.13

It helps to make the connector moat concrete, because "switching costs" is the kind of phrase that gets thrown around until it loses meaning. Imagine you are the purchasing manager at a major automaker, and a connector supplier offers you an identical part for a tenth of a cent less than the incumbent. To take that saving, you must re-qualify the new connector: subject it to thousands of hours of thermal cycling, vibration testing, corrosion exposure, and mating-durability trials; re-validate every wiring assembly and electronic module it touches; update the engineering documentation; and accept legal and warranty liability if the substitution ever contributes to a field failure in a safety-critical system like braking or airbag deployment. All of that expense and risk — to save a tenth of a cent on a part you may buy by the million, but which represents a rounding error against the cost of the car. No rational purchasing manager does it. That asymmetry — trivial reward, catastrophic tail risk — is the moat, and it is why a boring little connector business can quietly earn margins that a glamorous software business struggles to match. It is also why the interconnect leaders have compounded shareholder returns for decades while flashier auto-tech names have flamed out.

The second engine was Advanced Safety and User Experience, or ASUX — the car's brain. This was the higher-technology, faster-growing, and considerably more temperamental business: the radars and cameras that feed advanced driver-assistance systems (ADAS), the central compute platforms meant to consolidate a car's dozens of scattered control units into a few powerful ones, the body controllers, and the in-cabin infotainment and cockpit electronics. The proposed moat here is different in kind — it lives in perception algorithms and in the difficult art of integrating hardware with software so that a camera, a chip, and a line of code all agree on what they are seeing. But it is also a far more crowded and contested battlefield. Aptiv here squared off against the full weight of the Tier 1 giants — Bosch, Continental, Magna — and against sharp technology pure-plays, most notably Mobileye, the Israeli perception specialist whose chips and vision software set the pace for much of the industry.

The strategic prize inside ASUX was the idea of central compute, and it is worth explaining in plain language because it is the crux of the whole software-defined-vehicle thesis. A traditional car is a chaotic federation of dozens — sometimes over a hundred — small, dedicated computers called electronic control units, each one bolted to a specific function: one runs the power windows, one the seat memory, one the parking sensors, and so on. It is the automotive equivalent of a house wired with a separate, incompatible fuse box for every appliance. The software-defined vision is to sweep all of that away and replace it with a handful of powerful central computers — the car's equivalent of a smartphone's main processor — running software that can be updated over the air. Do that, and the carmaker can add features, fix bugs, and even sell subscriptions to a vehicle years after it is built. Aptiv's ambition was to be the company that architected and supplied that central brain and the high-speed data network feeding it. It is a genuinely large prize. It is also, as the industry discovered, a prize that the automakers themselves increasingly want to keep — a tension that would define the company's software struggles.

The economic relationship between these two engines is the single most important thing to grasp about the pre-spin company, and it explains a great deal of Aptiv's strategic behavior. The nervous system was the earner: the electrical and connector businesses threw off the lion's share of the profit and cash flow at healthy operating margins, and that cash quietly subsidized the enormous, front-loaded research-and-development spending required to build a credible brain. In other words, Aptiv was using a fortress-like hardware business — durable, cash-generative, low-drama — to fund a moon-shot software-and-perception business whose margins were thinner and whose competitive position was far less settled. That is a defensible strategy when the brain is genuinely on a path to scale. It becomes a value trap when the brain keeps consuming cash without ever earning its keep. Nowhere did that risk become more visible, or more expensive, than in Aptiv's four-year detour into full autonomy.

VI. The Autonomous Driving Detour: Motional (2020–2024)

Rewind to the turn of the decade, when Silicon Valley and Detroit alike were intoxicated by the same shimmering promise: the fully driverless car was just around the corner. Robotaxis would blanket cities, personal car ownership would wither, and whoever owned the autonomy stack would own the future of transportation. Into that euphoria, in 2020, Aptiv poured its own big bet. It combined its autonomous-driving unit with 현대자동차그룹 Hyundai Motor Group in a joint venture valued at roughly $4 billion, split 50/50, and christened it Motional. The mission was audacious: commercialize Level 4 autonomy — cars that could drive themselves with no human backup within a defined operating area — and put robotaxis on public roads at scale.

For a while, the narrative wrote itself. Motional ran driverless pilots, inked a high-profile partnership to put autonomous vehicles on a major ride-hailing network, and gave Aptiv a genuine claim to a seat at the autonomy table alongside the likes of Waymo and Cruise. In the language of the era, Aptiv wasn't just supplying the future; it was building it.

There was a real strategic logic to the venture structure, and it deserves credit before the criticism. By folding its autonomy unit into a 50/50 joint venture rather than keeping it wholly owned, Aptiv did two shrewd things at once. It shared the staggering cost of the moonshot with a deep-pocketed partner in Hyundai, and it moved much of the losses off its own consolidated income statement into equity-method accounting, softening the optical drag on reported earnings. It was, in effect, a way to place a large bet on autonomy while capping the immediate blast radius. The trouble is that a joint venture only limits the damage if the losses actually stay contained — and Motional's did not. The venture's cash needs kept climbing, and a 50% owner cannot simply ignore capital calls without diluting itself into irrelevance. The structure that was meant to cap the burn instead became a recurring obligation to feed it.

Then reality arrived, as it tends to. The timeline for genuinely driverless commercial operations — the point at which the economics actually work without a safety driver and without burning cash on every ride — slipped from the early 2020s to the late 2020s, and then toward the 2030s. Level 4 autonomy turned out to be one of those problems where the last few percent of reliability is exponentially harder and more expensive than the first ninety-five. And the burn was brutal. Motional consumed hundreds of millions of dollars of Aptiv's cash every year, a recurring drain on the parent's free cash flow with no near-term prospect of a return. For a CEO who measured himself on cash-flow conversion, this was an increasingly intolerable line item.

The reckoning came under the glare of the earnings calls. Through 2023 and into 2024, analysts pressed Clark with mounting impatience on the same theme: why was a disciplined, finance-first company pouring capital into a science project with a receding payday? The pressure landed on exactly the metric Clark cared about most. In public appearances around this period Clark returned repeatedly to the language of capital-allocation discipline, framing the company's choices explicitly through the lens of return on invested capital rather than ambition for its own sake.11 And so, in May 2024, he executed the kind of fast, unsentimental pivot that had become his signature. Aptiv announced it would stop funding Motional. Hyundai stepped in with a fresh injection of close to a billion dollars, and Aptiv slashed its ownership stake from 50% down to roughly 15%, taking a substantial write-down in the process.7 The company later trimmed its economic interest further, toward the low teens by late 2025, effectively converting an operational commitment into a small residual option on someone else's balance sheet.6

How should an investor grade this? The honest assessment cuts both ways. On one hand, the initial Level 4 enthusiasm was a case study in overpromising — Aptiv, like nearly everyone in the sector, sold a timeline the technology could not meet, and shareholders funded years of losses chasing it. That is a real mark against management's judgment at the point of entry. On the other hand, the exit was a genuine display of discipline. When the economics deteriorated and the goalposts kept moving, Clark did not double down to protect his ego or the sunk cost; he cut fast, offloaded the burn onto a willing partner, and redeployed attention and capital. In a sector littered with autonomy programs that torched billions before collapsing, a controlled, negotiated retreat is not nothing.

For the investor trying to grade management over time — which is ultimately the most important diligence exercise for a company defined by capital allocation — Motional is a revealing data point precisely because it contains both the vice and the virtue in one episode. The vice is a susceptibility to narrative: Aptiv, like the broader market, allowed the seductive story of imminent robotaxis to override sober underwriting, and shareholders paid for that lapse in years of losses and a chunky write-down. The virtue is that the same management did not let sunk cost or reputational pride trap it; when the numbers turned decisively against the thesis, it acted quickly and structured a graceful exit that transferred the ongoing burden to a partner still willing to carry it. A management team's willingness to publicly reverse a high-profile bet, absorb the write-down, and move on is genuinely rare and genuinely valuable — it is the behavioral signature of a team that answers to arithmetic rather than to ego. It is, in fact, the same finance-first reflex that would soon drive the company's software strategy — and its next large acquisition.

VII. Software-Defined Vehicles & The Wind River Acquisition (2022–Present)

If Motional was Aptiv's bet on the far frontier of autonomy, Wind River was its bet on the more immediate, more grounded prize: the operating system of the car itself. The phrase animating the entire industry was the "software-defined vehicle" — the idea that a modern car is becoming less a mechanical object with some electronics bolted on, and more a computer on wheels whose features, and even whose revenue, can be updated over the air long after it leaves the dealership. To play in that world, Aptiv decided it needed to own foundational software.

In 2022, Aptiv agreed to acquire Wind River from the private-equity firm TPG. Wind River is a piece of computing history that most consumers have never heard of but have relied on for decades: its flagship product, VxWorks, is a real-time operating system — the kind of ultra-reliable, deterministic software that runs systems where a delay of milliseconds is unacceptable, from Mars rovers to industrial controllers to aircraft. Alongside it came Wind River Studio, a cloud-native platform for developing, deploying, and managing software across fleets of connected devices. The strategic logic was to marry this proven software backbone with Aptiv's own Smart Vehicle Architecture — the company's blueprint for rewiring the car around a handful of powerful central computers instead of a hundred scattered black boxes.

It is worth unpacking what a real-time operating system actually is, because the term is opaque and the distinction is the whole point of why Aptiv wanted VxWorks rather than, say, an ordinary version of Linux. Most software you interact with — a phone, a laptop — is built for "good enough on average" timing; if a web page loads a few hundred milliseconds late, nobody dies. A real-time operating system makes a fundamentally different promise: it guarantees that a given task will execute within a hard, bounded, predictable slice of time, every single time, without exception. That determinism is non-negotiable in systems where a late response is a catastrophe — the flight controls of an aircraft, the safety interlocks of an industrial robot, or the braking and steering commands of a car driving itself. VxWorks earned its reputation over decades in exactly those unforgiving environments, including aerospace and defense. Aptiv's thesis was that as cars became computers, they would need this class of ultra-reliable software foundation, and that owning a battle-tested one would be cheaper and safer than building it from scratch. That is a coherent argument. The question, as always, was whether owning the foundation translated into selling it.

The deal's financial history tells you something about the discipline running through the company. Aptiv initially agreed to pay $4.3 billion. But between signing and closing, regulatory review dragged and the operating environment shifted, and rather than plow ahead at the original number, Aptiv renegotiated. When the transaction closed in December 2022, the price had been cut to $3.5 billion — an $800 million reduction extracted before the ink dried.[^8]8 For a management team that talks constantly about capital discipline, walking the price down by nearly a fifth was a tangible demonstration of it, and a useful counterweight to the Motional experience.

Owning the technology, however, is not the same as monetizing it — and here the story gets harder for the bulls, in ways that surfaced most clearly not in the polished prepared remarks on earnings calls but in the analyst Q&A that followed. Two headwinds recurred. The first, and most existential, is the risk of OEM in-sourcing. The uncomfortable template is Tesla, which built its own vertically integrated electronic architecture and software stack from scratch and demonstrated that a carmaker could treat software as a core competency rather than something to be outsourced to a Tier 1 supplier. That example lit a fire under the traditional automakers. When General Motors, Ford, Volkswagen, and others announce that they intend to build their own vehicle operating systems in-house, they are announcing, in effect, that they may not need to license Aptiv's. A supplier's software platform is only as valuable as the customers willing to standardize on it, and the largest customers are precisely the ones most tempted to go it alone.12

The second headwind is more prosaic but just as damaging to the thesis: the margins have been slow to show up. Software was supposed to be the high-margin future that lifted the whole enterprise. Instead, the cost of integrating Wind River, scaling the platform, and funding the R&D to make central compute real has weighed on the profitability of the segment now called Intelligent Systems, which continued to earn margins well below those of the connector business it was meant to eventually rival.1 The bull case says these are the ordinary growing pains of building a platform, and that operating leverage will arrive once the booked business converts to production revenue. The bear case says this is what a structurally lower-margin, more contested business looks like, and no amount of narrative will change its economics.

The evidence, as of now, is genuinely ambiguous — and honesty requires saying so rather than pretending the case is settled. In the software platform's favor: the shift toward centralized, over-the-air-updatable vehicle architectures is real and directionally unstoppable, the addressable content per vehicle is rising, and Aptiv has accumulated a substantial multi-year backlog of awarded business that has not yet flowed through the income statement. Against it: the timeline for that backlog to convert into high-margin revenue keeps stretching, several marquee automakers have publicly committed to building competing software in-house, and the segment's margins have not yet demonstrated the structural upward break that the entire thesis requires.12 A disciplined investor holds both of these truths at once and refuses to let the appealing half crowd out the inconvenient half. That unresolved tension is precisely what set the stage for Aptiv's most consequential act of self-surgery yet.

VIII. The Final Pruning: The April 2026 Versigent Spin-Off

The signal came in January 2025, and for anyone who had followed the company's logic, it was both a shock and the inevitable next move. Aptiv announced its intent to separate its Electrical Distribution Systems business — the wire-harness operation — into a standalone public company. It was a striking decision, because EDS was not some fringe unit. It was the single largest revenue segment in the entire company. Management was proposing to spin off the biggest piece of itself.

To understand why, you have to understand what a wire harness actually is and why it resists everything modern manufacturing prizes. A wire harness is the tailored bundle of wires, connectors, and terminals custom-built for a specific vehicle — often literally hand-assembled by workers threading and taping wires around a board, because the routing is too complex and too variable to fully automate. It is one of the last great manual-labor strongholds in car-making. That makes EDS a business defined by things Aptiv's investors had learned to hate: intense exposure to wage inflation in the low-cost countries where the assembly happens, such as Mexico and Morocco; direct exposure to the price of copper, the raw material coursing through every harness; and heavy, complex logistics to move bulky product across borders on tight automotive schedules. Each of those exposures deserves a beat, because together they explain why no amount of good management could make EDS look like a technology business. Copper is a globally traded commodity whose price swings with macroeconomic cycles far beyond any supplier's control; a harness maker can hedge and pass through some of it, but it is forever partially at the mercy of the London Metal Exchange. Labor is the larger issue: because the work resists automation, the business's cost base rises directly with wages in the developing economies where the assembly is done, and those wages have been climbing as places like Mexico and Morocco develop — the very success of a low-cost country erodes its cost advantage over time. And logistics bind the whole thing together under punishing just-in-time schedules, because a car cannot be built without its harness, so the harness maker carries the cost and risk of moving heavy, custom product across borders exactly when the assembly line demands it. It is a decent business run well, but it is structurally low-margin, labor-heavy, and cyclical — precisely the profile that compresses a valuation multiple. In fiscal 2025, EDS generated roughly $8.8 billion of net sales but an adjusted operating margin of only about 7.6%, less than half the margin of Aptiv's connector business.1 It was, in the cold language of portfolio management, the anchor dragging on the rating of everything around it.

There is a subtler reason a management team spins a business rather than selling it, and it applies squarely here. A sale of EDS would have generated cash but almost certainly triggered a large tax bill, and — given how few buyers can absorb an $8.8 billion, globally distributed, labor-intensive harness operation — likely at a depressed price reflecting the very margin profile Aptiv was fleeing. A tax-free spin sidesteps both problems: it hands the business directly to existing shareholders without a corporate-level tax hit, and it lets the public market, rather than a single strategic acquirer, set the price. The catch is that a spin raises no cash for the parent and imposes strict conditions — the parent generally cannot be seen to be doing it primarily to sell, must maintain the distribution's structural integrity, and must equip the spun entity to survive on its own with its own balance sheet and leadership. That Aptiv chose the spin route rather than shopping EDS for cash is itself a tell: management judged that the separation's value lay less in the proceeds than in the re-rating of what stayed behind.

The separation completed on April 1, 2026, structured as a tax-free distribution to shareholders — a form that lets a company hand a subsidiary to its owners without triggering a corporate-level tax bill, provided it satisfies a demanding set of IRS conditions.5 Aptiv shareholders received one share of the new company, Versigent, for every three Aptiv shares they held as of the March 17 record date.2 The EDS business — around $8.8 billion in revenue — walked out the door under CEO Joseph Liotine and CFO Doug Ostermann, trading on the NYSE as VGNT.34 What remained behind was recast into a cleaner, two-segment company that management branded "New Aptiv."1

The realignment sharpened the story into two businesses with very different characters. Engineered Components — the renamed and refocused hardware franchise built around high-voltage interconnects, connectors, and cable management — was the crown jewel, posting roughly $6.66 billion of net sales in 2025 at an adjusted operating margin near 17%, generating about $1.13 billion of segment profit.1 This is the fortress: the business whose economics genuinely resemble the premium interconnect peers, and one Aptiv had been deliberately reinforcing — its 2022 acquisition of Intercable Automotive Solutions added specialized high-voltage interconnect capability aimed squarely at the electrified vehicles where connector content is richest.[^12] Intelligent Systems — the renamed ASUX, now carrying ADAS, central compute, and the Wind River software stack — contributed about $5.79 billion of net sales at a markedly lower adjusted operating margin of roughly 11%, or about $658 million of profit.1 Put those side by side and the picture is candid: the "boring" hardware business earned meaningfully fatter margins than the "exciting" technology business it was long meant to subsidize.

That candor cuts against a comfortable version of the story management would prefer investors absorb — namely, that Aptiv shed its low-value business and kept its high-value ones. The margins complicate that framing. Yes, EDS at roughly 7.6% was the lowest-margin of the three legacy segments and the clearest drag.1 But the highest-margin survivor is Engineered Components, the hardware business — the atoms, not the bits — while Intelligent Systems, the software-and-perception crown that justifies the entire "tech company" reclassification, earned a margin closer to the middle. An honest reading is therefore that Aptiv did not simply trade down-market assets for up-market ones; it traded a low-margin physical business for a portfolio still anchored, in profit terms, by a high-margin physical business. The technology narrative and the profit reality point in slightly different directions, and that gap is exactly what a discerning investor should keep in view when weighing whether the promised "tech multiple" is warranted.

The narrative meaning management wants investors to take away is that Aptiv has, at long last, decoupled its secular-growth, high-margin technology and components from its cyclical, low-margin assembly footprint — the final, cleanest version of the pruning it began with Delphi Technologies in 2017. The skeptic's version is worth holding alongside it: Aptiv has now spun off, sold, or restructured so many pieces of itself that the more important question is not what it discarded but whether what remains can actually grow. Management guided pro-forma "New Aptiv" toward roughly $12.8–13.2 billion of revenue in 2026 at an adjusted EBITDA margin near 18.6% — a genuinely higher-quality profile than the conglomerate it dismantled.15 The market's job now is to decide whether that quality is the beginning of a re-rating or simply the residue left after the growth was spun away.

IX. Playbook: Business & Investing Lessons

Step back from the chronology and three durable lessons emerge from Aptiv's serial mutation — lessons that generalize well beyond a single auto-parts company. Each is a principle a long-term investor can carry into the analysis of any transforming industrial, and each carries a warning label, because the same behaviors that create value in one context destroy it in another.

Lesson 1: The power — and the limits — of ruthless portfolio pruning. Aptiv's central management skill has been an almost surgical willingness to cut. Twice in a decade it amputated its own largest or most legacy-burdened businesses — the combustion powertrain in 2017, the wire harness in 2026 — on the theory that a high-growth segment strangled inside a conglomerate will never earn the multiple it deserves. The logic is sound and the evidence largely supports it: the discarded powertrain business really did prove worth less on its own, and the connector franchise really is a better business than the assembly work around it. But there is a shadow side worth naming. Pruning improves the quality of what remains; it does not, by itself, create growth. A company can prune its way to a beautiful margin profile and still have nothing left that compounds. The discipline is admirable; it is not a substitute for a growth engine. An investor watching a serial pruner should always ask the harder second question: after the cutting is done, what is left that actually compounds — and is it enough to matter?

Lesson 2: The physical moat can beat the software moat. For years, Wall Street's imagination was captured by the software-defined vehicle — the sexy, high-multiple story of ADAS and central compute. Yet the most durable, highest-margin asset in the entire post-spin company turned out to be the least glamorous one: the premium connector and interconnect business. Its advantage is almost embarrassingly physical — components qualified years in advance, designed into safety-critical systems, protected by switching costs so high that customers rarely bother to challenge them, and sold across platform lifecycles measured in many years. The software business, by contrast, faces well-capitalized customers actively trying to build the same capability in-house. The lesson for investors is to be suspicious of the narrative that assumes atoms are dull and bits are magic. Sometimes the boring physical business has the wider, deeper moat.

Lesson 3: The danger of the tech narrative. Rebranding a Tier 1 auto supplier as a technology platform is a powerful trick in a bull market — it can expand the multiple and re-rate the equity toward a peer group it aspires to join. But that trick carries a hidden cost: it raises expectations to a level the underlying business must then live up to quarter after quarter. When ADAS growth cools, when EV adoption decelerates, when major OEMs announce they are insourcing the very software stack the company was pitching, the gap between the tech promise and the automotive reality becomes a source of acute credibility damage. A company that invites the market to value it as a technology platform has, in effect, posted a bond — and it forfeits that bond the moment the growth fails to arrive. Narrative is leverage in both directions.

Taken together, these lessons frame the central investment debate over the standalone company — a debate best conducted through the discipline of a formal competitive stress test.

X. Analysis, Bull vs. Bear, & The Activist Stress Test

Strip away the story and put New Aptiv on the analyst's dissection table. What follows applies two well-worn frameworks — Hamilton Helmer's 7 Powers and, implicitly, Porter's five forces — to separate durable advantage from wishful thinking, then runs the bull and bear cases and the questions a skeptical activist would actually ask.

Myth versus reality. Before scoring the powers, it is worth puncturing the consensus narrative directly, because the market's story about Aptiv has often diverged from its financial anatomy. The myth, repeated across a decade of bullish coverage, is that Aptiv is fundamentally a technology company whose value derives from software and autonomy — the ADAS, the central compute, the Wind River stack. The reality the segment numbers keep insisting on is that the company's profit engine is, and has long been, its connector and electrical-hardware franchise, a business whose advantage is physical and old-fashioned rather than digital and novel.1 A second myth is that the serial spin-offs are evidence of a brilliant, value-creating strategy. The more neutral reality is that they are evidence of a company that has repeatedly found itself holding businesses the market would not reward, and has responded by cutting them loose — an entirely rational response, but one that describes a company solving a persistent problem, not one enjoying a durable solution. A third myth is that separation "unlocks" value as if by magic. Value is only unlocked if the standalone parts sustainably out-earn the combined whole; a spin can just as easily reveal that the growth everyone assumed was there never was. Holding these corrections in mind, the formal power analysis becomes sharper.

The 7 Powers read. Start with switching costs, which are the company's strongest and clearest power. In Engineered Components, connectors and high-voltage interconnects are qualified years in advance and welded, contractually and technically, into a vehicle's electrical platform. Displacing an incumbent connector supplier mid-program means re-validating safety-critical systems for a rounding-error saving — a trade almost no automaker will make. This is a genuine, high, and durable power, and it is the analytical heart of the bull case. Scale economies rank as a medium power: Aptiv's global manufacturing and distribution let it spread fixed costs across enormous volumes, but its principal interconnect rivals — TE Connectivity and Amphenol — enjoy the same advantage, so scale is table stakes among the leaders rather than a decisive edge for any one of them.13 Cornered resource is the weakest and most contested: Wind River's VxWorks carries real, hard-won intellectual property, but it competes against open-source Linux variants that cost nothing to license and against proprietary operating systems that the largest OEMs are building for themselves.12 Owning valuable IP is not the same as owning a resource no one else can replicate, and in automotive software the "cornering" is far from secure.

Run the same businesses through Porter's lens and the picture is consistent. Buyer power is high — a handful of global automakers account for enormous portions of revenue and are relentless on price, structurally capping supplier margins. The threat of substitutes and new entrants is asymmetric: negligible in connectors, where the qualification barrier is a moat, but severe in software, where the "substitute" is the customer deciding to make the product itself. Rivalry is intense in both segments but civilized in interconnect, where a stable oligopoly of TE, Amphenol, and Aptiv shares a lucrative field, and brutal in ADAS, where Bosch, Continental, Magna, Mobileye, and a rising cohort of low-cost Chinese sensor makers all press on price.

The current risk radar. Two risks stand out as material rather than generic. OEM insourcing is the high-severity one, and it is not hypothetical — it is the single greatest threat to the entire Intelligent Systems thesis, because the customer Aptiv most wants to sell software to is the customer most capable of replacing it.12 The second is EV-adoption deceleration, a medium-severity risk with a specific mechanism: much of the growth case for high-voltage connectors is levered to battery-electric vehicles, so if the BEV transition slows — as it did across several major markets in 2024 and 2025 — the scale-up of the highest-value connector content is delayed with it. A third, quieter risk sits underneath both: commoditization of ADAS hardware as Chinese suppliers drive sensor costs down, squeezing the very margins the technology segment was supposed to eventually expand.

The bull case. Post-spin, New Aptiv is a cleaner, higher-quality company: a low-double-digit consolidated operating margin, anchored by a best-in-class connector franchise that arguably trades at a discount to the pure-play multiples awarded to TE Connectivity and Amphenol despite comparable economics.13 The portfolio is deliberately power-agnostic — management stresses that the large majority of its technology content applies across combustion, hybrid, and electric vehicles alike, insulating it from the timing of any single propulsion transition. And the company enters its standalone life with a multi-year backlog of booked business — the pre-spin group logged three consecutive years of new business awards above $30 billion — and a management team with a demonstrated record of returning capital, including some $4.1 billion of share repurchases in 2024 alone.14 If the market eventually re-rates the connector business toward its peers and the software segment's margins inflect upward, there is real upside embedded in the separation.

The bear case. The skeptic sees a company addicted to financial engineering. Strip away the spin-offs, the stake reductions, and the restructurings, and what is the underlying organic growth rate — and has it ever been as high as the narrative implied? The bear argues that the constant reshuffling is not strategy but distraction, a way to keep generating headlines and "value-unlock" events while the core software business stubbornly refuses to earn its promised margins and the ADAS hardware business faces relentless Chinese price competition. In this reading, each spin-off is less a masterstroke than an admission that the previous configuration didn't work.

The activist stress test. This is where the analysis gets pointed, because Aptiv is, by construction, an activist-ready situation — it has essentially spent a decade doing to itself what an activist would demand. A skeptical long/short investor would press on precisely the seams the company's own history exposes. On capital allocation: the record is genuinely mixed. The Wind River price cut and the Motional exit show discipline; but the multi-hundred-million-dollar Motional write-down and the years of autonomy cash-burn that preceded it show a management team that overpaid for a hype cycle before correcting.7 An activist would ask whether the same pattern lurks inside the Wind River bet. On portfolio complexity: having finally simplified into two segments, does the software business belong inside a components company at all, or is it the next candidate for separation? On margins: the central challenge is that after all the pruning, the company has still not demonstrated structural margin improvement in its technology segment — the very segment whose growth justifies the tech multiple. And on accountability: with a chairman-and-CEO who has presided over serial reinvention, the fair question is whether the reinvention has compounded shareholder value or merely churned it. These are not rhetorical jabs; they are the live debate the separated equities must now settle in public.

The KPIs that actually matter. Cutting through the noise, three metrics will tell the story of standalone Aptiv better than any earnings-call adjective:

- Engineered Components segment margin. This is the fortress. It sits near 17% today; holding — or expanding — that level is the proof that the connector moat is intact and pricing power is real.1 Erosion here would undercut the entire bull case.

- Intelligent Systems organic revenue growth, driven specifically by central-compute bookings converting to production revenue. This is the referendum on whether the software-defined-vehicle bet is materializing or stalling against OEM insourcing.

- Free cash flow conversion. Management has long anchored its credibility on converting a high share of earnings into cash; sustained conversion above roughly 80% is the quantitative test of whether the capital discipline it preaches is real.

Track those three, and the abstract debate over "tech multiple versus auto multiple" resolves into something an investor can actually monitor.

XI. Epilogue & Outro

As of this writing in July 2026, the experiment is finally running in the open. For the first time in the company's long, mutating history, the market can price the two halves of the old Aptiv separately — the technology-and-components company under APTV, and the wire-harness business under VGNT — and the sum of those two public verdicts is the market's real-time judgment on whether thirty years of restructuring created value or merely relocated it. Each stock now carries its own investor base, its own multiple, and its own burden of proof: Aptiv must show that a cleaner, higher-margin body can actually grow, and Versigent must show that a labor-heavy assembly business can stand on its own without a technology story to lean on.

Versigent's independent life poses its own quietly interesting question. Freed from a parent that treated it as a margin-dragging embarrassment, and with revenue guided toward roughly $9 billion for 2026 at an adjusted EBITDA margin near 11%, the wire-harness business will now be valued for exactly what it is rather than discounted for what it was attached to.15 Harness assembly is unglamorous, but it is also indispensable, sticky, and — in the hands of a management team for whom it is the main event rather than the unwanted stepchild — potentially a serviceable cash generator that returns capital to its own shareholders. Whether the market rewards a focused, low-margin industrial with a modest but stable multiple, or punishes it for the very structural exposures that drove Aptiv to shed it, will be its own referendum, run in parallel with the parent's. Two experiments, one lineage, both now public.

The larger arc is what makes this company a genuine business-history case study rather than just another auto-parts ticker. Aptiv is the improbable survivor of a lineage that began inside the largest industrial enterprise of the twentieth century, passed through one of the ugliest bankruptcies in American manufacturing, and re-emerged by treating its own corporate structure as something to be endlessly re-cut. Its defining conviction — the thing that separates it from the dozens of legacy suppliers that quietly faded — has been a near-total refusal to remain static, paired with an obsession over where each dollar of capital earns its return. That obsession has been, at various moments, its greatest strength and the source of its sharpest failures.

Whether the latest mutation is the one that finally lets the market see a technology company rather than the ghost of a GM division is a question no outsider can yet answer with confidence. What the record does establish is the pattern: this is a company that, whenever the shape of the automobile changed, changed its own shape to match — sometimes brilliantly, sometimes expensively, and always restlessly. The next few years of standalone results will reveal which of those adverbs history ultimately assigns to the Versigent spin. For now, the mutating machine of Detroit has reinvented itself one more time, and the market is left to do what it has always done with Aptiv: watch, weigh the evidence, and wait for the numbers to settle the story.

References

-

Aptiv Reports Fourth Quarter 2025 Financial Results — Aptiv PLC Newsroom, 2026-02-04 ↩↩↩↩↩↩↩↩↩↩↩

-

Aptiv Board of Directors Approves Spin-Off of Versigent — Business Wire, 2026-03-05 ↩↩

-

Aptiv Announces Leadership Appointments and Company Name for New Independent EDS Company — Business Wire, 2026-01-27 ↩

-

Aptiv PLC Completed the Spin-Off of Versigent — Investing.com, 2026-04-01 ↩

-

Aptiv PLC Form 8-K (Versigent Form 10 filing; tax-free spin-off timing) — SEC EDGAR, 2026-03-06 ↩

-

Aptiv PLC Form 10-K for fiscal year 2025 — SEC EDGAR, 2026-02-18 ↩↩↩

-

Aptiv Announces Agreement to Restructure Motional Joint Venture — Business Wire, 2024-05-02 ↩↩

-

TPG and Aptiv Amend Wind River Acquisition Price — Reuters, 2022-12-05 ↩

-

Delphi to Spin Off Powertrain Business as Delphi Technologies — CNBC, 2017-12-05 ↩↩

-

Delphi Restructuring and Distressed Debt Battle — Financial Times, 2008-11-12 ↩↩↩↩

-

Aptiv CEO Kevin Clark Discusses Capital Allocation — Bloomberg Technology, 2024-06-15 ↩

-

The Slowdown in Autonomy and OEM Software Stacks — S&P Global Mobility, 2025-08-14 ↩↩↩↩

-

TE Connectivity Competitor Analysis and Interconnect Moats — Seeking Alpha, 2025-11-03 ↩↩↩

-

Aptiv Reports Fourth Quarter and Full Year 2024 Financial Results — SEC EDGAR (Exhibit 99.1), 2025-01-30 ↩

-

Aptiv Reports Fourth Quarter 2025 Financial Results (segment detail and 2026 pro-forma guidance) — StockTitan, 2026-02-04 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube