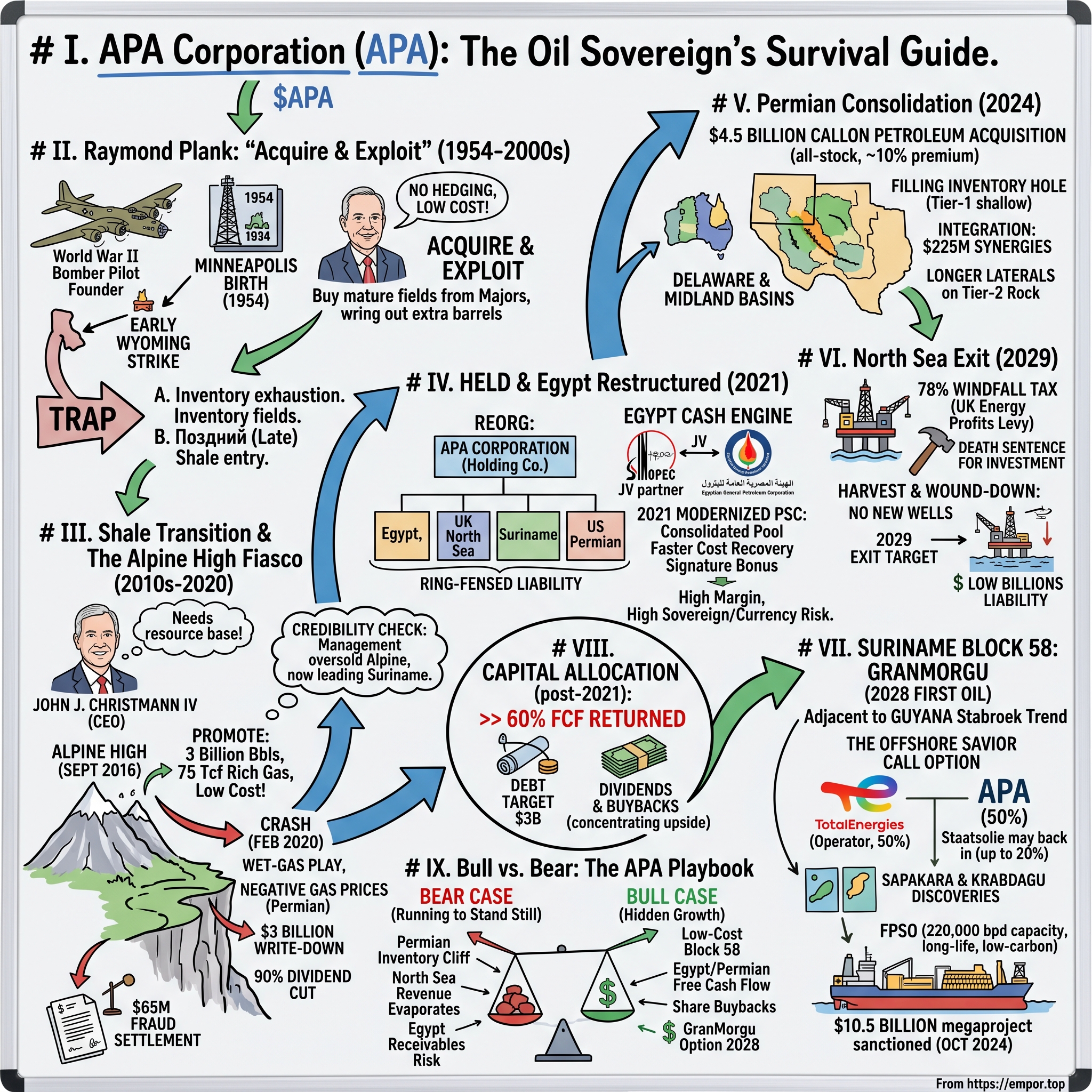

APA Corporation: The Oil Sovereign's Survival Guide

I. Introduction & Episode Roadmap

In the early months of 2020, the ticker "APA" looked less like an investment and more like an obituary in progress. The company then still legally called Apache Corporation had, only three years earlier, told the world it had stumbled onto a "world-class" oil and gas province in a forgotten corner of West Texas. By February 2020, that province — christened Alpine High — was wiped off the balance sheet in a roughly $3 billion write-down, two years of profit erased in a single accounting stroke.1 The board slashed the quarterly dividend by 90%, from $0.25 a share to a token $0.025. The stock, which had cleared $100 a few years earlier, collapsed toward single digits. Over the full arc of the debacle, Apache shed roughly $24 billion of market value.1 Shareholders were not merely disappointed; they were litigious, and lawyers were already assembling the securities-fraud case that would eventually cost the company $65 million to settle.2

Now fast-forward. By late 2024 the same company — reorganized, renamed, and re-underwritten — had done three things that few would have predicted in the depths of the Alpine High wreckage. It closed a $4.5 billion all-stock acquisition of Callon Petroleum, doubling down on the Permian Basin it had once flirted with abandoning.3 It joined France's TotalEnergies in sanctioning a $10.5 billion deepwater megaproject offshore Suriname, one of the largest greenfield oil developments in the Western Hemisphere.4 And it had rebuilt itself around one of the most explicit shareholder-return formulas in the entire exploration-and-production (E&P) business.

That whipsaw — from near-death to global sovereign partner in under five years — is the story of this episode. The thesis worth testing is not that APA is a great company or a bad one. It is that APA is the ultimate survivor of the independent E&P space, a firm that has cycled through three distinct identities: the mid-century wildcatter that bought other people's tired oilfields and squeezed them dry; the swaggering shale operator that nearly destroyed itself chasing a narrative; and the modern, disciplined capital allocator that now describes itself less as an explorer than as a returns machine attached to a small number of very large assets.

To understand whether that third identity is durable, you have to understand the four engines that drive the company today. The US Permian Basin is the volume workhorse, the bulk of production, prized for short-cycle barrels you can turn on and off like a tap. Egypt's Western Desert is the high-margin cash cow, run through a restructured production-sharing contract alongside China's 中国石化 Sinopec. The UK North Sea is the dying-but-generous mature asset, now formally slated for a tax-driven exit by the end of 2029. And Suriname's Block 58 is the zero-revenue-today future — a set of deepwater discoveries that produce nothing yet but underpin the entire long-term bull case.

A word on posture, because it matters for how to read everything that follows. It would be easy to tell this as a redemption arc — the fallen company that found its discipline and its deepwater prize — and management would be happy for you to hear it that way. But a fallen company that gets rescued by a rising oil price, a well-timed supermajor partnership, and an accounting reset is not obviously the same thing as a company that fixed its culture. The interesting question is which of those two APA is, and the only way to answer it is to test the claims against behavior over time: what management promised, what it delivered, how it explained its misses, and whether the incentives actually point where the rhetoric does. That test runs through every section below.

Here is the roadmap. We start with the maverick founder Raymond Plank and the "Acquire and Exploit" DNA he stamped on the company. We move through the shale pivot and the Alpine High disaster that nearly ended everything. We examine the 2021 holding-company reorganization and the renegotiation of the Egyptian crown jewel. We benchmark the Callon consolidation play against the wave of Permian mega-mergers. We walk the North Sea tax cliff. We cross the Atlantic to the deepwater savior in Suriname. And we close with the frameworks — Porter's Five Forces, Hamilton Helmer's 7 Powers, and a hard-nosed bull-versus-bear stress test — that let a sophisticated investor decide what, if anything, the market is getting wrong.

II. The Maverick Heritage: Raymond Plank and "Acquire & Exploit"

On December 6, 1954, three men in Minneapolis pooled $250,000 and started an oil company with six employees.5 The founders were Truman Anderson, Raymond Plank, and Charles Arnao, and the company's name was a small act of wordplay on their initials — A, P, A — with "che" tacked on the end at the suggestion of an early employee named Helen Johnson, who collected a $25 savings bond for the idea.5 The first well Apache drilled, in the Cushing field of Oklahoma, produced a comical seven barrels a day. The company's entire first year generated net income of $12,535 on revenue of $190,000.5 From that almost absurdly modest start would eventually grow a global independent worth tens of billions.

The company's early identity was not oil at all. Apache spent its first decade as a diversified investment vehicle — a manager of income partnerships that at various points touched agriculture, minerals, and manufacturing — before it fully committed to the drill bit. Its reputation as an explorer was forged in Wyoming's Powder River Basin, where the Fagerness No. 1 well came in flowing 1,200 barrels a day and was followed by more than twenty additional producers.5 That early experience taught a durable lesson: Apache did its best work in places the industry's giants considered too marginal to bother with. The habit of hunting where others had lost interest became the company's temperament long before it became a strategy.

The man who defined the culture was Raymond Plank, a blunt, combative World War II bomber pilot who would run Apache for more than half a century. Plank was, by every account, allergic to the pieties of Wall Street and openly contemptuous of the oil majors. He built a company in his own image: lean on overhead, skeptical of fashion, obsessed with the unglamorous arithmetic of getting more barrels out of the ground for fewer dollars. His signature refusal to hedge commodity prices — a stance that would look either brilliant or reckless depending on the year — reflected a conviction that Apache's job was to be the low-cost operator, not to play the futures market. Plank believed that hedging was a tacit admission that you did not trust your own cost structure; if you were genuinely the cheapest producer in the field, you would survive the low prices that killed everyone else, and you would keep the full upside when prices recovered. It was a philosophy that worked beautifully in a rising market and left the company fully exposed when the market fell — a trade-off Plank made with his eyes open, and one that instilled in Apache a permanent bias toward controlling the one variable it actually could control: cost per barrel.

Plank himself was a character out of an earlier age of American capitalism. He wrote sharp-tongued letters to shareholders, feuded openly with the majors he bought assets from, and cultivated an image of the scrappy outsider needling a clubby industry. He poured a portion of his fortune into philanthropy and Native American education initiatives, and he ran the company with a founder's proprietary intensity well past the age at which most executives retire. When he finally stepped back, he left behind not just a balance sheet but a worldview — that an independent's survival depended on being leaner, hungrier, and more disciplined about unit economics than the lumbering giants it fed on.

Out of Plank's worldview came the strategy that carried Apache for decades: "Acquisition and Exploit." The idea was almost contrarian in its simplicity. The majors — Exxon, BP, Shell — were forever high-grading their portfolios, selling off fields they deemed too small, too old, or too far into decline to matter to a company their size. Apache made a business of being the buyer. It would purchase those mature, unloved assets at prices that reflected their supposed exhaustion, then apply superior engineering, tighter cost control, and relentless well-level attention to wring out years of additional cash flow the sellers had left on the table. Where a major saw a depleted nuisance, Apache saw an annuity.

Two deals crystallize the model. In 1994, Apache pushed into Egypt's Western Desert, buying concession acreage that laid the foundation for what became a decades-long relationship with the Egyptian state — an asset that, thirty years later, still throws off some of the company's highest-margin barrels. The second is the stuff of North Sea legend. In 2003, Apache bought roughly 97% of the Forties field from BP for about $630 million.6 Forties had been the first big British North Sea oilfield, discovered in 1970, and by the time BP sold it, output had sagged to around 40,000 barrels a day with the field widely written off as a spent force.6 Wall Street snickered. Apache promptly launched an aggressive drilling and workover campaign, drove down operating costs, and produced hundreds of millions of additional barrels over the following years — a textbook demonstration that the value in a mature field is often a function of the operator's attention, not the geology's generosity.

For a long stretch, this was a very good business. The "acquire and exploit" playbook is really a discipline: buy assets whose decline is already priced in, so that competent operations produce upside almost by default. But it carries a structural vulnerability that would matter enormously later. A company built on buying other people's mature fields is, by definition, a company that does not generate much of its own new inventory. As long as the majors kept selling and prices behaved, the machine ran. The trouble arrives when the mature fields you own finally exhaust for real, and the only way to replace them is to become the very thing Plank distrusted — a big-ticket explorer betting shareholder capital on rock nobody has proven yet. That is precisely the trap the next generation of leadership walked into.

III. The Shale Transition & The Alpine High Fiasco

By the early 2010s, the ground had shifted under every US independent. The marriage of horizontal drilling and hydraulic fracturing — cracking open shale rock with high-pressure fluid to release oil and gas that conventional wells could never reach — had turned the United States from a declining producer into the fastest-growing source of new barrels on earth. For a company like Apache, whose international mature fields were entering genuine, irreversible decline, the message was unambiguous: pivot to American shale or slowly fade. The problem was that Apache came late and came scattered, with a patchwork of second-tier US acreage rather than a concentrated, "Tier-1" core in the best rock.

Into this arrived a leadership change with a jarring abruptness. In early 2015, longtime chief executive G. Steven Farris departed, and the top job passed to John J. Christmann IV, a company insider who had run the Permian region.7 Christmann took over an oil price in free-fall — crude had collapsed from over $100 to under $50 — and moved fast, slashing Apache's North American rig count from 93 to around 20 within his first year.7 Christmann was not a Wall Street import but a company man who had come up through the Permian and understood the basin's operational grind. That background cut both ways in the years that followed. It made him credible on the nuts and bolts of drilling and completions — the man knew a well from a spreadsheet — but it may also have made him susceptible to the promoter's temptation that afflicts operators who become convinced they have seen something in the rock that the market has not. Farris's abrupt exit handed him a company under acute pressure to prove it still had a future in the shale age, and a leader under pressure to prove something is a leader inclined to believe the most exciting version of his own data.

But cost-cutting alone does not solve an inventory problem. What Christmann needed, and knew he needed, was a marquee resource base that could anchor the company's US future. What he found — or thought he found — became the defining catastrophe of his tenure.

In September 2016, Apache went public with a stunning claim. In a quiet stretch of Reeves County in the southern Delaware Basin — acreage other operators had studied and dismissed — the company said it had identified a massive new play holding, on its own estimates, something like 3 billion barrels of oil and 75 trillion cubic feet of rich gas in place.8 Christmann branded it "Alpine High" and told an oil conference that it held some of the cheapest hydrocarbons to produce not just in America but in the world, economic at oil prices as low as $40.8 The market swooned. Here, seemingly, was Apache's ticket back to relevance: a company-maker discovered on the cheap in rock everyone else had ignored.

It is worth pausing on why a claim like this could move a stock so violently, because the mechanics of shale explain a great deal about the boom-and-bust psychology of the era. A conventional oilfield is a discovery: you find a trapped pool of hydrocarbons and produce it. Shale is closer to manufacturing. The oil and gas are locked inside dense source rock, and you liberate them by drilling horizontally through the layer and fracturing it with high-pressure fluid to create a network of cracks. Because the resource is spread across a whole formation rather than concentrated in a pool, the key questions are not "did we find it?" but "how many locations can we drill, and how much will each one produce for what cost?" That reframes an oil company as an inventory of repeatable manufacturing sites — which is exactly why a claim of "3 billion barrels in place" across a huge, cheap acreage position sounded like a factory nobody else had noticed.

The reasons everyone else had ignored it turned out to be excellent reasons. Alpine High was not, at its core, an oil play. It was overwhelmingly a wet-gas and natural-gas-liquids play, and its value therefore hinged on the price of gas and NGLs rather than crude — a crucial distinction the early promotion tended to blur. Worse, the acreage sat far from existing pipelines, which meant Apache had to sink billions of its own capital into midstream plants, gathering lines, and processing infrastructure before it could sell much of anything. And then the timing turned malicious: as Permian gas production overwhelmed the region's takeaway capacity in 2018 and 2019, spot gas prices in West Texas periodically went negative, meaning producers were effectively paying customers to haul the gas away. A field whose economics depended on gas was being built out precisely as gas became a liability.

The unraveling had a name inside the company. Late in 2019, an internal geological review reportedly dubbed "Project Neptune" concluded that the wells were underperforming and the play was not economic at scale, and the geologist most associated with the discovery departed. Then, in February 2020, Apache stopped pretending. It effectively wrote Alpine High off, took the roughly $3 billion charge, gutted capital spending, and cut the dividend by 90%.1 The timing could hardly have been crueler. The write-down landed in late February 2020, just weeks before the COVID-19 pandemic froze global travel and vaporized oil demand. In April 2020, the front-month US crude futures contract did something it had never done in history — it settled below zero, at roughly negative $37 a barrel, as traders with nowhere to store physical oil paid to offload it. For a company that had just confessed to a $3 billion mistake, cut its dividend to a token, and watched its shares collapse, a once-in-a-century demand shock arriving on top was the definition of a stress test. The stock, already weak, cratered as the COVID-19 demand collapse arrived on top of the self-inflicted wound. Shareholders sued, alleging management had knowingly oversold a play it had reason to doubt; the class action covered buyers from September 2016 through March 2020, and the company ultimately agreed to a $65 million settlement that received court approval in late 2024.2

For investors, Alpine High is not just a historical embarrassment; it is the permanent reference point against which every subsequent management claim must be measured. It showed a leadership team capable of turning a geological hypothesis into a public narrative faster than the geology could be verified — and a capital-allocation culture willing to build billions of dollars of infrastructure around that narrative. The relevant question for the rest of this story is whether the company that emerged genuinely internalized the lesson, or merely got lucky with its next big bet. That test begins with a corporate restructuring that, on the surface, looked like paperwork.

IV. The Holding Company Pivot & the Egypt Cash Engine

On March 1, 2021, Apache Corporation did something that generated few headlines and mattered a great deal: it reorganized itself under a new publicly traded parent called APA Corporation, with the old Apache Corporation surviving as a subsidiary.9 To a casual observer this was a name change and a new ticker relationship. To anyone reading the structure, it was a deliberate act of legal and financial engineering. A holding-company umbrella let APA sit above its various operating units and, crucially, ring-fence its large international businesses — Egypt, the North Sea, and the nascent Suriname interest — from the liabilities and tax exposures of the US operations. It gave the parent flexibility in how it financed, taxed, and, if it ever wished, separated those pieces. Coming barely a year after Alpine High, it also signaled a company trying to modernize the machinery of the enterprise, not just its drilling program. The structure matters most in scenarios investors do not like to dwell on. Ring-fencing the international subsidiaries means that a catastrophe in one jurisdiction — a US environmental liability, a North Sea decommissioning cost overrun, a dispute in Egypt — is less likely to reach across and infect the others or the parent. It also preserves optionality: a holding company can, if the board ever decides the market is undervaluing a piece, separate or spin an operating unit far more cleanly than a single integrated entity could. Nothing about the 2021 reorganization committed APA to breaking itself up, but it built the plumbing that would make such a move possible — a quiet insurance policy written into the corporate structure.

The jewel that the new structure was partly designed to protect sat in the Egyptian desert. The Western Desert is a geological gift: a deep, "stacked" basin where multiple productive layers sit on top of one another, so a single surface location can access many pay zones. Apache had been drilling it since the 1990s, and in 2013 it had sold a one-third stake in its Egyptian business to 中国石化 Sinopec for about $3.1 billion, creating a joint venture that remains two-thirds APA and one-third Sinopec.10 For years, though, the asset's brilliance was blunted by its contracts. Egyptian production ran under a tangle of older production-sharing agreements whose terms discouraged exactly the kind of higher-cost, deeper drilling the basin rewarded — a classic case of a fiscal regime fighting the geology.

A production-sharing contract, or PSC, is worth pausing on, because it governs how much money actually reaches APA. Under a PSC, the company does not own the oil; the state does. The operator funds the drilling and, in exchange, recovers its costs out of a capped slice of production (the "cost recovery" barrels) and then splits the remaining "profit" barrels with the state on a set formula. Two dials determine everything: how big the cost-recovery slice is, and how the profit barrels are divided. If the cost-recovery cap is too low or the profit split too lean, expensive wells simply do not pay, no matter how much oil the rock holds.

So in 2021, APA and Sinopec renegotiated. Late that year, after Egyptian parliamentary approval, the partners ratified a modernized, consolidated PSC that merged the bulk of their Western Desert concessions into a single agreement with the Ministry of Petroleum and the الهيئة المصرية العامة للبترول Egyptian General Petroleum Corporation (EGPC).11 The new deal created one unified cost-recovery pool and refreshed the split so that the economics of an incremental well improved materially. Most tangibly, it granted the joint venture the right to recover roughly $900 million of previously unrecovered "backlogged" costs over a five-year window, retroactive to April 1, 2021 — an accelerant to near-term cash generation.11 In return, the venture committed to a much heavier drilling program, sharply increasing its Egyptian rig count and paying a signature bonus to the state. In effect, APA traded a promise of activity for a fiscal structure that made the activity worth undertaking.

The strategic logic is sound, and the Western Desert remains among APA's most profitable acreage. But the neutral investor has to hold two facts at once. Egypt is a high-margin cash engine and a concentrated sovereign risk. The country runs chronic shortages of hard currency, and EGPC has a documented history of falling behind on payments to its foreign operators. If Egypt's central bank tightens dollar convertibility, or if EGPC's receivables balloon, the cash that looks so attractive on a margin basis can become trapped or delayed — a live issue that management has had to address on multiple earnings calls. This is not a hypothetical concern. Between 2022 and 2024, the Egyptian pound lost a large fraction of its value against the dollar through a series of sharp devaluations, as the country burned through foreign reserves and negotiated repeated support packages with the International Monetary Fund. For a foreign operator, currency weakness in the host country is a double-edged phenomenon: it can lower local operating costs measured in dollars, but it also strains the government's ability to convert local revenue into the hard currency APA needs to repatriate. Payments to service companies and to the joint venture can stretch out, and receivables from the state can accumulate faster than they are cleared. Management has periodically had to reassure analysts that it is managing the balance actively — adjusting activity levels to the pace at which it is actually being paid, rather than drilling into a growing receivable.

APA has worked to manage this, including through gas-pricing arrangements intended to improve the economics of its Egyptian gas, but the exposure is structural, not something a contract renegotiation makes disappear. The Egyptian barrel is cheap to produce and hard, at times, to get paid for. With the international cash cow restructured, management turned its attention back home, to the inventory hole Alpine High had left behind.

V. Permian Consolidation: The $4.5 Billion Callon Petroleum Acquisition

Strip away the Suriname optionality and the Egyptian margins, and APA's day-to-day existence rests on the Permian Basin of West Texas and New Mexico. After the Alpine High abandonment, the company's US position had a specific, well-understood weakness: it was highly cash-generative but shallow. In shale, the currency that matters is "inventory" — the count of undrilled, high-return locations you can turn into wells. A company rich in current production but poor in Tier-1 inventory is a melting ice cube, funding today's dividends by drilling up its own future. By the early 2020s, skeptics argued APA had perhaps four or five years of premium drilling locations left, a runway short enough to threaten the whole equity story.

There are two ways to fix an inventory problem: find more rock, or buy it. Having been badly burned by the "find it" approach, APA chose to buy. In January 2024 it announced an all-stock agreement to acquire Callon Petroleum, a pure-play Permian operator, in a deal valued at roughly $4.5 billion including Callon's debt; the transaction closed on April 1, 2024, after both shareholder bases approved it in late March.3 The mechanics were straightforward: each Callon share converted into 1.0425 APA shares, an exchange ratio that implied a premium of only about 10% to Callon's undisturbed price.3 That modest premium is itself a data point worth dwelling on.

Because 2023 and 2024 were the years the American shale patch consolidated in earnest, and the price tags were enormous. ExxonMobil agreed to buy Pioneer Natural Resources for around $60 billion; Chevron struck a roughly $53 billion deal for Hess; Occidental bought CrownRock; Diamondback absorbed Endeavor. In that company, APA's Callon deal was a minnow — and, notably, a cheaply priced one, with a premium at the low end of the range rather than the 15–20% that several larger tie-ups fetched. The all-stock structure deserves a moment, because it reveals how APA thought about the deal. Paying in shares rather than cash meant APA did not have to raise debt or drain its balance sheet to close, and it handed Callon's shareholders continued exposure to the combined company's upside — including, implicitly, the Suriname optionality that a cash buyout would have cut them out of. It also aligned the risk: if the acquired acreage disappoints, APA's own shareholders and the former Callon holders sit in the same boat. The flip side is dilution. Issuing stock to buy assets expands the share count, and for a company whose entire capital-return thesis rests on shrinking the share count through buybacks, an acquisition that inflates it is a strategic contradiction the company then has to work back down through repurchases. The deal, in other words, spent some of the very ammunition the return framework was designed to accumulate.

There was also a broader logic to consolidating at all. The Permian by the early 2020s had become a mature, crowded basin where the returns increasingly went to operators with scale — the ability to run continuous drilling programs, negotiate down service costs, and stitch together contiguous acreage so that longer horizontal wells could be drilled from shared infrastructure. Sub-scale operators like Callon, carrying heavy debt and drilling a patchwork of leases, were structurally disadvantaged and made natural targets. The wave of 2023–2024 mergers was, at bottom, the basin rationalizing itself: fewer, larger operators absorbing the smaller ones because scale had become the closest thing to an edge in an otherwise undifferentiated business.

Management framed the discipline as a virtue: it paid up modestly, in its own paper, for acreage adjacent to assets it already ran. The transaction added roughly 120,000 net acres in the Delaware Basin and 25,000 in the Midland Basin, and lifted APA's total reported production to around 500,000 barrels of oil equivalent per day, with roughly two-thirds of it coming from the Permian.3

Here is where the neutral posture earns its keep, because the bear case on Callon is not obscure — it is the consensus. Callon's inventory was widely graded by analysts as "Tier-2": productive, but with a history of elevated costs, a heavy debt load, and inconsistent well spacing that had produced middling productivity. The uncomfortable interpretation is that APA bought second-tier rock because it could no longer organically source first-tier rock — that the deal was less a bold consolidation than a confession about the state of its own drilling cupboard. A skeptical investor should not let the low premium obscure that possibility; a cheap price for mediocre acreage is still a bet that the acquirer can do with it what the seller could not.

Which is exactly the claim APA has spent the time since integration trying to prove. Management initially guided to about $150 million in annual cost synergies and later raised the run-rate target to roughly $225 million as integration progressed, and it has pointed to operational gains from applying its own drilling techniques to the legacy Callon acreage — longer horizontal laterals and lower breakeven costs on the former Callon Delaware wells.12 More broadly, the company has framed the pro-forma combination, after selling non-core pieces, as delivering something like a decade of economic drilling inventory across thousands of remaining locations — the depth that was missing before.12 The honest read is that the direction of these metrics has been favorable, but that "we can uplift Tier-2 rock with better engineering" is a claim that only fully validates over years of well results, not quarters of synergy accounting. This is the single most important thing to watch on the US onshore business: whether the productivity of the acquired acreage genuinely converges toward APA's legacy performance, or whether the inventory "depth" turns out to be depth of the wrong quality. Notably, the buy-versus-harvest tension shows up in an even starker form across the Atlantic, where APA made the opposite decision — not to invest, but to leave.

VI. The North Sea Harvest and 2029 Exit Strategy

Twenty-plus years after Apache turned the written-off Forties field into a cash machine, the same North Sea business became a case study in how a government can tax an asset into abandonment. The trigger was the energy crisis that followed Russia's 2022 invasion of Ukraine, which sent oil and gas prices soaring and handed producers windfall profits. The UK's response, in May 2022, was the Energy Profits Levy — a windfall tax layered on top of the existing regime. It began at 25%, but successive increases pushed it higher, and under the Labour government the levy rose to 38%, lifting the headline marginal tax rate on UK upstream oil and gas profits to a punishing 78%.13 At that rate, the government captures more than three of every four incremental pounds of profit.

For a mature, high-cost basin, a 78% marginal rate is close to a death sentence for new investment, and the reason is worth making concrete. Aging North Sea infrastructure demands continuous reinvestment simply to stay safe and to slow the steep natural decline of old fields. But that reinvestment only makes sense if the operator keeps enough of the resulting profit to earn a return. When the state takes 78 cents on the marginal dollar, the math on a new well or a facility upgrade frequently stops working — the operator bears the full cost and capital risk but keeps a sliver of the upside. Faced with that arithmetic, APA did the rational thing for a returns-focused company: it stopped drilling new wells and shifted the North Sea into pure harvest mode.

The formal endgame arrived in late 2024. In the third quarter, APA recorded a pre-tax impairment of roughly $793 million on its North Sea proved properties, part of a broader $1.1 billion of impairments that quarter, as it reassessed the assets against the tax regime and looming regulatory and infrastructure obligations.14 Then it announced the decision that removed all ambiguity: APA would cease all UK North Sea production and exit the basin entirely by the end of 2029, citing the "uneconomic" combination of the tax hikes and tightening regulation.15 A business that Apache had once made famous by refusing to let it die was now being deliberately wound down — not because the geology was finally exhausted, but because the fiscal terms made further life uneconomic.

APA was hardly alone. The windfall levy triggered a broad retreat from the UK Continental Shelf, with operators large and small cutting investment, deferring projects, and in several cases announcing plans to divest or exit British waters entirely. From an investor's standpoint, the episode is a clean illustration of political and fiscal risk in resource extraction: a government can, with a single tax change, convert a profitable asset into a liability faster than any competitor or commodity move could. It is precisely the kind of risk that does not show up in a reserve report or a well-productivity chart, and it is a reminder that in this industry the tax authority is often a more important variable than the reservoir. For APA, the practical consequence is that the North Sea now offers no growth optionality and no reinvestment case — only a managed decline toward a hard 2029 deadline.

The North Sea's role in the equity story from here is narrow and defensive. Until 2029, APA aims to squeeze maximum free cash flow from the existing wells while spending only what safety and integrity require, all while carrying a substantial decommissioning liability — the legally mandated, expensive obligation to plug wells and dismantle offshore infrastructure at the end of field life. Those abandonment costs, running into the low billions on a present-value basis, are a real cash drag that will persist even as production winds down. The decommissioning obligation deserves a closer look, because it is the part of the North Sea story most likely to spring an unpleasant surprise. When an offshore field reaches the end of its life, the operator is legally required to plug every well, remove or make safe the platforms and subsea equipment, and restore the seabed — a process that can run for years and cost enormous sums, and one whose price tag has a habit of rising as the work actually begins. APA carries a substantial present-value liability for these obligations, a meaningful share of which comes due around the end of the decade as production ceases. Because the UK tax regime allows some relief against decommissioning costs, the interaction between the windfall levy, the exit timing, and the abandonment spending is genuinely complex, and the net cash outcome of the wind-down is harder to pin down than a simple production forecast would suggest. For a company selling itself on capital discipline, an under-provisioned or back-end-loaded cleanup bill would be exactly the kind of tail risk a skeptic should keep an eye on.

For investors, the North Sea is best understood not as a growth or even a stable asset but as a declining annuity with a cleanup bill attached: a source of near-term cash that is contractually and fiscally programmed to disappear. The obvious question is what replaces it — and for that, APA's answer sits under 150 kilometers of Atlantic water off the coast of South America.

VII. The Offshore Savior: Suriname Block 58 & the GranMorgu Project

Geography set the stage for the most important bet APA has ever made. The tiny nation of Suriname sits directly southeast of Guyana, and Suriname's offshore Block 58 lies immediately adjacent to Guyana's Stabroek Block — the same geological trend where ExxonMobil and its partners discovered on the order of 11 billion barrels of light, low-carbon oil and turned Guyana into the most exciting new petro-state on earth. For years, the industry's obvious question was whether the prolific rock stopped politely at the maritime border. Apache had a lease on the Suriname side and a chance to find out.

In 2019, it did. Apache announced its first major offshore discovery in Block 58, and immediately confronted the limits of what a mid-cap independent could do with it. Developing a world-class deepwater field is a different sport from operating onshore shale or mature North Sea platforms; it requires tens of billions in capital, specialized floating production vessels, and deepwater execution capability APA simply did not possess in-house. So it made the defining structural choice of the project: it brought in TotalEnergies as a 50/50 partner and, critically, as the operator. APA would own half the upside and hand the multi-billion-dollar execution risk to a French supermajor with a deep deepwater track record. It was an admission of limitation dressed as a strategy — and, given the Alpine High history of overreaching alone, arguably a mark of hard-won maturity.

Then came the years of doubt. The early appraisal wells revealed a technical gremlin known as the gas-to-oil ratio, or GOR — essentially, how much gas comes up with the oil. Some Block 58 wells showed high and volatile GORs, and too much gas relative to oil can undermine the economics of a development designed to produce and sell crude. TotalEnergies, temperamentally cautious and disciplined about capital, refused to be rushed. It deferred the Final Investment Decision — the formal, binding commitment to build — for years while it ran additional seismic and appraisal work, mapped the oil-rich fairways, and waited out a bout of global supply-chain and cost inflation that had inflated project budgets industry-wide. Critics wondered aloud whether Block 58 would ever be sanctioned, or whether it would join the long list of stranded offshore discoveries.

The doubt ended on October 1, 2024. TotalEnergies and APA jointly announced the Final Investment Decision on the GranMorgu project — named for a prized local fish — with total investment estimated at around $10.5 billion.4 The development targets the Sapakara and Krabdagu discoveries, roughly 150 kilometers offshore, holding estimated recoverable reserves of more than 750 million barrels.4 At its heart will sit a floating production, storage, and offloading vessel — an FPSO, essentially a giant ship-shaped factory moored over the field that processes oil, stores it, and offloads it to tankers — designed for a capacity of 220,000 barrels per day.4 The partners guided to a roughly four-year construction phase and first oil in 2028; by the company's early-2026 reporting, that timeline had been sharpened to mid-2028.416

Two features make GranMorgu the linchpin of the bull case. First, the unit economics: management and its partner describe breakeven costs well under $40 a barrel and a notably low carbon intensity — meaningful in a world where institutional investors increasingly discount high-emission barrels. Low-cost, low-carbon deepwater oil is exactly the kind of resource that can command a premium valuation relative to marginal shale. Second, the ownership carries a wrinkle: Suriname's national oil company, Staatsolie, holds a contractual option to back into the project with up to a 20% participating interest.[^16] If Staatsolie exercises fully, APA's effective working interest in the development would fall from 50% toward roughly 40% — reducing both its share of the eventual barrels and its share of the remaining capital bill. That is a genuine dilution of the headline stake, though it also shifts some funding burden onto the state. The back-in is a common feature of resource nationalism in its constructive form: the host country wants a direct equity seat at the table of its own signature project, both to capture more of the economics and to build the domestic capability of its national champion. For APA, it is a reminder that the ultimate landlord in Suriname is the Surinamese state, and that the split of a windfall this large is never purely a matter of the original contract — governments that watch a neighbor grow rich on adjacent barrels tend to sharpen their pencils.

The Guyana comparison is what makes analysts salivate, and it deserves scrutiny rather than acceptance. Next door, ExxonMobil's Stabroek partners moved from first discovery in 2015 to first oil by the end of 2019 and then to a rapid cadence of FPSOs, each one adding hundreds of thousands of barrels a day of low-cost production and re-rating the whole venture. The bullish syllogism for Suriname runs: same geological trend, same deepwater play type, therefore same trajectory. But the analogy has limits. Suriname's Block 58 took far longer to reach a development decision than Stabroek did, partly because of the gas-to-oil-ratio problem and partly because TotalEnergies is a more capital-cautious operator than the Exxon-led Guyana consortium. GranMorgu is a single FPSO, not the multi-vessel machine Guyana became. The rock may rhyme, but the pace and scale so far do not — and the market's willingness to pay for "the next Guyana" should be weighed against the reality that Suriname is, for now, one project years from producing a barrel.

What ultimately underwrites the excitement is the 2023 appraisal campaign that de-risked the two target discoveries enough to sanction them, and the specific quality of the resource. Deepwater oil of this type is prized for two reasons that matter to modern investors. It is long-life: an FPSO development produces steadily for a decade or more, unlike a shale well that declines 70% in its first two years and must be constantly replaced. And, in this case, it is low-carbon-intensity, meaning fewer emissions per barrel produced — a feature that matters as institutional investors increasingly screen portfolios for carbon exposure and as high-emission barrels risk trading at a discount. A barrel that is cheap to produce, long-lived, and relatively clean is the closest thing the oil business has to a premium product, and that is the re-rating case in a sentence.

For the neutral investor, Suriname is simultaneously the most valuable and the least de-risked thing APA owns. It produces exactly zero revenue today and will produce none until 2028 at the earliest, yet it is where the entire long-term re-rating thesis lives. Everything that can go wrong with a $10.5 billion deepwater project — shipyard delays on the FPSO, installation bottlenecks, cost overruns, a slipped first-oil date — bears directly on the net present value of APA's half. A single year of delay meaningfully erodes that value through the time-value of money alone. The optimistic frame is that a disciplined supermajor operator and a proven FPSO design de-risk the execution; the sober frame is that offshore megaprojects have humbled better-resourced partners than these. Whichever way it breaks, GranMorgu is the reason APA is interesting rather than merely cheap — which brings us to how management is trying to convert that optionality into per-share value in the meantime.

VIII. The APA Playbook: Hamilton Helmer's 7 Powers & Capital Allocation

Strip an E&P company down to its foundations and you find an uncomfortable truth: it sells a commodity it cannot differentiate, at a price it cannot control, into a market that does not know or care which company pumped the barrel. That is the lens Hamilton Helmer's 7 Powers framework — a taxonomy of the durable advantages that let a business earn excess returns — forces on us. Run APA through it honestly and most of the seven powers register as absent. Switching costs? None; a refiner does not care whose crude it buys. Network effects? None. Brand? None that commands a price premium; nobody pays up for "Apache oil." Counter-positioning? Essentially nonexistent — APA is a conventional price-taker, not a disruptor with a business model incumbents cannot copy.

Where APA does register, it registers modestly and specifically. Its strongest claim is to a cornered resource: the 50% interest in Block 58 is a genuinely scarce, hard-to-replicate deepwater position that cannot simply be re-created by a competitor with capital, and in Egypt the unified concession grants privileged access to a vast, prospective slice of the Western Desert. Scale economies are a split verdict — weak in the US Permian, where APA remains a mid-cap dwarfed by the likes of Chevron, ExxonMobil, and Diamondback, but real in Egypt, where APA is the dominant producer with corresponding leverage over local infrastructure and services. And there is a moderate process power, or system advantage: if APA truly can drill longer laterals and lower breakevens on acquired acreage than its sellers could, that operational edge is a repeatable, if unglamorous, source of value — the modern descendant of Plank's "exploit" discipline.

The blunt conclusion is that APA has no fortress. Its "moat," to the extent it has one, is a couple of specific irreplaceable assets plus a culture of operational cost control — advantages that are real but neither wide nor permanent. And when a business cannot out-differentiate its rivals, the game shifts entirely to capital allocation: not what you produce, but what you do with the cash it throws off. This is where APA has tried hardest to reinvent itself, and where the neutral investor should focus the most scrutiny.

The centerpiece is a formula the company adopted in the fourth quarter of 2021 and has repeated ever since: return at least 60% of free cash flow to shareholders through dividends and buybacks.16 The logic is a direct rebuke to the Alpine High era, when narrative-driven spending destroyed capital. By pre-committing a majority of free cash flow to owners, management constrains its own worst instinct — the temptation to plow every spare dollar into the next company-making story. The buyback is the sharpest tool here: with a huge, undeveloped Suriname stake sitting in the background, every share retired at a depressed price concentrates that future upside into fewer hands. The remaining roughly 40% of free cash flow is aimed primarily at debt reduction, toward a stated long-term net-debt target of around $3 billion to defend the investment-grade balance sheet.

The choice to emphasize buybacks over a fat dividend is itself a considered one, and it carries a message. A high, fixed dividend is a promise that becomes painful to break — as APA learned viscerally in 2020, when the 90% cut inflicted its own reputational wound on top of the operational one. A buyback, by contrast, is discretionary: management can lean in when the stock is cheap and pull back when it is not, or when capital is needed elsewhere, without the trauma of formally cutting a payout. For a commodity business with volatile cash flows, that flexibility is valuable, and it also happens to be the more mathematically potent tool when a company believes its own shares are undervalued relative to hidden optionality. The risk is the mirror image: buybacks are only value-creating if the shares are genuinely cheap, and a management team that misjudges its own stock — or that repurchases through a cyclical peak — destroys value just as surely as a bad acquisition. The buyback is a bet on management's read of intrinsic value, and after Alpine High, management's read of intrinsic value is precisely the thing under scrutiny.

There is a deeper tension embedded in the framework that a careful investor should name. APA is simultaneously promising to return the majority of its free cash flow to owners, to pay down debt toward a firm target, and to fund its share of a $10.5 billion offshore megaproject. In years of strong prices and robust cash flow, those three claims coexist comfortably. In a downturn, they compete. Suriname's construction spending is largely non-discretionary once sanctioned — you cannot half-build an FPSO — which means that if oil prices fall hard before first oil, something else has to give, and the most flexible lever is the shareholder return. The 60% commitment is a floor stated in percentage terms, not dollars; 60% of a shrunken free-cash-flow number in a bad year is a much smaller absolute return. The framework is disciplined, but it is not magic, and it has never yet been tested by a sustained price collapse coinciding with peak Suriname spending.

How is the formula holding up in practice? In full-year 2024, APA generated about $841 million of free cash flow and returned $599 million to shareholders — roughly 71% of free cash flow, comfortably above the 60% floor.17 For 2025, the company reported $4.5 billion of operating cash flow, about $1.0 billion of free cash flow, and $5.4 billion of adjusted EBITDAX, while continuing to pay down debt.16 And it has paired the returns with genuine cost discipline: management hit $350 million of run-rate controllable-spend savings by the end of 2025 — two years ahead of its original schedule — and set a new target of $450 million by the end of 2026.16 Crucially, the 2026 capital budget was guided down to about $2.1 billion of upstream capital, a 10% cut from 2025, of which only around $230 million funds GranMorgu and $70 million funds Suriname and Alaska exploration.16 Against the uncontrolled, story-driven spending of the Alpine High years, a shrinking capital budget funding a deliberately narrow set of projects is the single clearest evidence that the capital-allocation culture has, in fact, changed. The open question — the one the next section stress-tests — is whether that discipline survives a downturn, and whether the people running the company have earned the benefit of the doubt.

IX. The Skeptical-Investor Stress Test & Bull vs. Bear Case

Every credibility question about APA eventually circles back to one man. John J. Christmann IV has been chief executive since early 2015, which means the same person presided over both the Alpine High disaster and the Suriname recovery. That continuity cuts two ways. A charitable read is that Christmann learned the lessons of 2016–2020 in the most painful way possible and rebuilt the company around discipline, partnership, and shareholder returns precisely because he lived through the alternative. A skeptical read is that the executive who oversold a play he had reason to doubt is now asking the market to trust him on an even larger, longer-dated bet in Suriname — and that the burden of proof should sit heavily on him. An activist would put it bluntly: has this management team actually earned back the right to be believed, or has a rising commodity tide and a well-timed supermajor partnership flattered a mixed record?

The compensation question is the natural next probe. A skeptical owner does not ask how much the CEO is paid so much as what for. If pay is tethered to absolute production growth, the incentive structure quietly rewards exactly the empire-building that produced Alpine High — get bigger, whatever the return on capital. If instead it is anchored to return on capital employed, free cash flow per share, and relative shareholder return, then the incentives point toward the disciplined model management now espouses. The proxy statement is where that alignment can be verified, and it is the document a serious investor should read before taking the "we've changed" narrative at face value.[^19] The stated framework and the incentive design need to actually match, year after year, for the credibility to compound.

Then there is the balance-sheet critique of the Callon deal, which sharpens the earlier discussion of Tier-2 rock. A hostile analyst would argue that APA took on Callon's debt to acquire second-tier inventory whose main function is to mask the organic decline of its legacy Permian position — buying production to paper over a shrinking base rather than genuinely deepening its high-return runway. If that reading is right, the synergies and lateral-length improvements are real but ultimately cosmetic, delaying rather than solving the inventory problem. The counter is that the deal was struck in stock at a modest premium and has been followed by debt reduction and cost cuts. Both stories are currently consistent with the visible facts; only years of well productivity data will adjudicate between them.

It is worth puncturing one consensus narrative directly, because it cuts against the reflexive skepticism. The myth: APA is a slow, shrinking, second-tier producer coasting on legacy assets. The reality is more mixed. A genuinely coasting company does not voluntarily cut its capital budget while accelerating cost savings two years ahead of schedule, and it does not sit on a half-interest in one of the hemisphere's largest new oil developments. At the same time, the bullish counter-myth — that Suriname makes APA a hidden growth story — is equally lazy, because that growth is years away, unproven at first oil, and subject to a national-oil-company back-in that trims the stake. The honest description is a mature cash business bolted to a single large call option. Both the bears who ignore the option and the bulls who price it as a certainty are telling themselves a simpler story than the facts support.

There is a governance dimension a skeptical owner would probe as well. Portfolio complexity is itself a risk: APA is running short-cycle US shale, a fiscally exotic Egyptian PSC, a wind-down in the North Sea, and a deepwater development off South America, each with a different risk profile, currency, counterparty, and time horizon. That breadth is hard to manage and hard for the market to value cleanly, and it is the kind of sprawl activists sometimes attack as a candidate for simplification. On the ownership side, the stock has long attracted value-oriented and event-driven investors drawn precisely to the gap between a mature-producer valuation and the Suriname optionality; shifts in that concentrated holder base, and any activist accumulation, are worth monitoring as a tell on how sophisticated money is reading the same set of facts. None of this is a scandal, but all of it belongs in the diligence file alongside the reservoir and the tax rate.

Layer on the risk radar, and three exposures dominate. Egypt carries sovereign and currency risk: if EGPC's payment delays worsen or dollar convertibility tightens, the highest-margin cash engine can partially freeze regardless of how many barrels the rock yields. Suriname carries execution risk of the classic offshore variety — shipyard and installation delays, cost overruns, and slippage in the mid-2028 first-oil date, each of which erodes net present value. And the Permian carries the inventory-cliff risk: if the Callon synergies plateau and the acquired acreage underdelivers, the depth problem re-emerges in the early 2030s, right around when Suriname is supposed to be ramping. These risks are not independent; a low oil price would strain all three at once and put the 60% return commitment directly in tension with Suriname's remaining capital calls.

Which frames the bull-versus-bear debate cleanly. The bear case: APA is a company running to stand still. Its Tier-1 Permian inventory is structurally thin, forcing dilutive M&A; the North Sea cash flows are contractually evaporating by 2029; Egypt's geopolitical and currency risks are chronic; and if oil falls below roughly $65 a barrel, the free cash flow that funds the buyback thins out just as Suriname's capital needs peak — turning the shareholder-return story off precisely when investors need it most. The bull case: APA is structurally mispriced. The market values it as a mature, inventory-short Permian operator and assigns little credit to the low-breakeven, low-carbon, long-life deepwater barrels coming from Block 58 in 2028. In the interim, the Permian and the restructured Egyptian assets throw off enough free cash flow to retire shares at a discount and cut debt, so that when GranMorgu's oil finally flows, the upside lands on a shrunken share count. Running Porter's Five Forces underneath both cases only reinforces that APA competes in a brutal industry — no pricing power against a global commodity, high supplier power from oilfield-service providers, the ever-present threat of substitution from renewables, and low barriers that keep the field crowded. In an industry with no structural profit protection, the only durable edge is being a lower-cost, better-allocating operator than the next firm. Whether APA clears that bar is, ultimately, the whole question.

X. Epilogue & Key Takeaways

The deepest lesson of APA's story is one the entire shale era eventually taught its investors the hard way: the independent oil and gas business is not, at bottom, about finding oil. It is about the cold, unsentimental management of capital. Raymond Plank understood a version of this in the 1950s when he built a company around buying other people's tired fields and running them cheaply. His successors forgot it in the 2010s when they let a compelling narrative — Alpine High — outrun the arithmetic, and they nearly destroyed the company doing so. The APA of 2026, with its pre-committed return formula, its shrinking capital budget, its outsourced deepwater execution, and its deliberate North Sea exit, is a company that has been re-engineered around the discipline it once abandoned. Whether that re-engineering is permanent or merely the posture of a favorable cycle is the thing time will reveal.

For an investor tracking this company from here, the noise is enormous but the signal reduces to a short list. First, watch Suriname's project milestones — the fabrication and installation progress of the GranMorgu FPSO and any movement in the mid-2028 first-oil date, because that single asset carries most of the long-term valuation freight and offshore timelines slip in expensive ways. Second, watch former-Callon well productivity — the lateral lengths and breakeven costs on the acquired Delaware acreage — because that is the direct test of whether APA can genuinely uplift Tier-2 rock or is simply drilling down a shallow inventory. Third, watch the share count alongside free cash flow yield, because the entire bull thesis depends on management retiring stock cheaply today so that tomorrow's deepwater barrels accrue to fewer owners. A rising share count paired with a heavy Suriname bill would be the clearest signal that the discipline is fraying under pressure; a steadily falling count through a soft price environment would be the strongest evidence that the culture really has changed. Everything else — reserve replacement, Egyptian receivables, North Sea decommissioning cash, quarter-to-quarter production noise — is context around those three signals rather than a substitute for them. An investor who tracks only those three, and reads each new earnings call for whether management's explanations stay consistent with the last one, will understand this company better than one drowning in the full firehose of E&P metrics.

It is also worth being honest about what an investor is actually underwriting when they engage with this company, because it is not a bet on a moat or a franchise. APA has neither. It is a bet on a specific chain of execution: that the Permian keeps throwing off cash while the acquired acreage proves itself, that Egypt keeps paying, that the North Sea winds down without a nasty decommissioning surprise, that TotalEnergies delivers GranMorgu roughly on time and on budget, and that management keeps the capital-allocation discipline it has recently professed even when prices make indiscipline tempting again. Each link in that chain is plausible; none is guaranteed; and the commodity price sits underneath all of them as a variable no one at APA controls. That is the unromantic truth of owning an independent E&P — you are underwriting operators and geology and governments and a price you cannot forecast, all at once.

There is a certain symmetry in where this leaves the company. Raymond Plank built Apache by refusing to let mature assets die and by treating Wall Street's disdain as a buying signal. Seventy years later, APA is again a company the market largely treats as a mature, second-tier survivor — while it quietly holds a half-interest in one of the largest new oil developments in the hemisphere. The bet embedded in the stock is essentially a bet on that old Plank instinct: that the value overlooked by the majors, and by the consensus, is exactly where the returns hide. The company has stared down corporate death once already and drawn a map to deepwater sovereignty. The market's job now is to decide whether the map is real — and management's job is to prove, this time, that the resource is as good as the story.

References

-

Inside Apache's Alpine High Fiasco: Deception, Fraud, and a $3 Billion Write-Down — Benzinga, 2024-10-28 ↩↩↩

-

Apache Investors Secure Initial Approval of $65 Million Deal — Bloomberg Law, 2024 ↩↩

-

APA Corporation Completes Acquisition of Callon Petroleum Company — APA Corporation, 2024-04-01 ↩↩↩↩

-

Suriname: TotalEnergies announces Final Investment Decision for the GranMorgu development on Block 58 — TotalEnergies, 2024-10-01 ↩↩↩↩↩

-

Apache CEO: Alpine High Discovery Shows How to Survive and Thrive Amid the Oil Bust — Forbes, 2016-09-28 ↩↩

-

Apache Corp. Represents The Thorn That America's Oil Frackers Have Stuck In The Side Of OPEC — Forbes, 2016-09-28 ↩↩

-

Sinopec Buys 33% of Apache's Egypt Business for $3.1 Billion — Bloomberg, 2013-08-30 ↩

-

APA Corporation Announces Ratification of Modernized Production Sharing Contract in Egypt — GlobeNewswire, 2021-12-27 ↩↩

-

APA Corporation Q4 and Full-Year 2025 Financial and Operational Results — APA Corporation, 2026-02-25 ↩↩

-

Changes to the Energy Profits Levy — UK Government, 2024-07-29 ↩

-

APA Corporation Form 10-Q for the Quarter Ended September 30, 2024 — SEC EDGAR ↩

-

APA Corp to exit UK North Sea by 2029 — Reuters, 2024-11-07 ↩

-

APA Corporation Announces Fourth-Quarter and Full-Year 2025 Financial and Operational Results — APA Corporation, 2026-02-25 ↩↩↩↩↩

-

APA Corporation Announces Third-Quarter 2024 Financial and Operational Results — APA Corporation, 2024-11-06 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube