Aon plc: The Sovereign of Risk and Capital Cannibalism

I. Introduction & Episode Roadmap

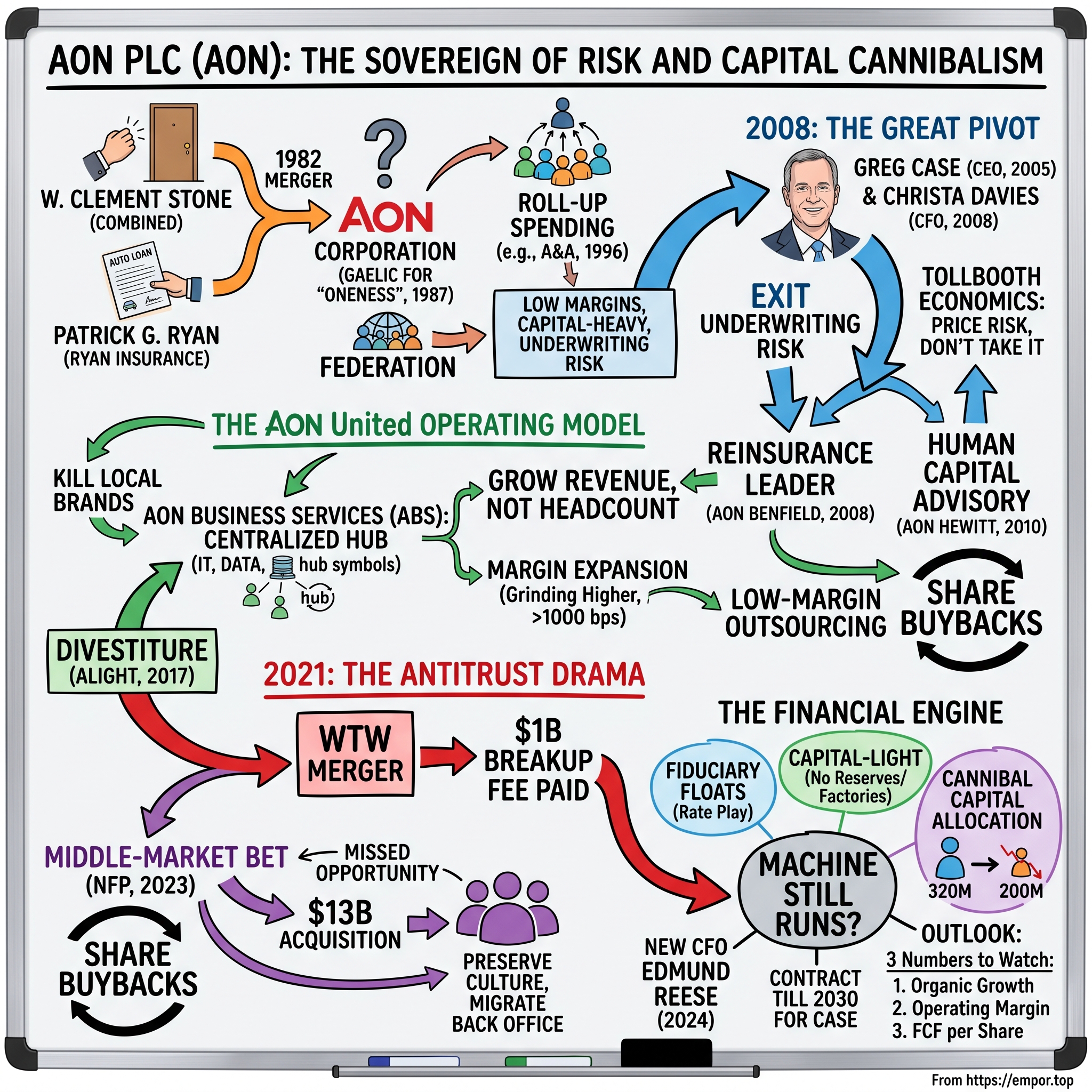

Every year, hundreds of billions of dollars in insurance premiums flow from the world's corporations to the world's insurers. Almost none of it moves directly. It passes through a handful of intermediaries who sit in the middle of that river, dip a cup into the current, and take a fee — without ever assuming a single dollar of the underlying risk. Aon plc is one of the two largest of those intermediaries. It is a business that owns almost no factories, holds almost no reserves against catastrophe, and yet touches the risk transfer of a meaningful slice of global GDP.

Consider the two numbers that frame this entire story. In 2005, Aon was a sprawling, low-margin conglomerate. Two decades later, in its fiscal 2025 results, the company reported total revenue of $17.2 billion, up 9% year over year, with adjusted operating margin of 32.4% and free cash flow of $3.2 billion.1 Over that same span, the share count was ground down relentlessly — from roughly 320 million shares to around 200 million — a reduction of more than a third of the company through steady buybacks. Margins expanded by roughly 1,300 basis points while the ownership pie was cannibalized. That is the puzzle this article unpacks: how a commoditized-looking brokerage became one of the most cash-generative franchises in financial services.

To grasp why this is remarkable, hold the two halves of a brokerage in your mind at once. On one side is a business with almost no capital requirements — no reserves, no factories, minimal fixed assets — which means that nearly every incremental dollar of revenue can fall to the bottom line if costs are held in check. On the other side is a business that has historically been run as a talent shop, a collection of relationship-driven producers who resist standardization and whose loyalty can walk out the door with their clients. The tension between those two natures — capital-light economics begging to be scaled, and a human, artisanal culture resisting scale — is the drama at the center of Aon's modern history. The company that learned to resolve it captured extraordinary economics. The one that failed stayed a federation.

The narrative spine is a partnership. Greg Case, a former McKinsey consultant who took the CEO seat in 2005, and Christa Davies, a former Microsoft finance executive who became CFO in 2008, spent sixteen years running the same playbook with unusual discipline: strip out balance-sheet risk, standardize the plumbing, and recycle every spare dollar of cash into a shrinking share count. They were, in the truest sense, the Great Recyclers. Whether that playbook still has room to run under a new CFO and a heavily levered balance sheet is the open question of the back half of this story.

Here is the road we will travel. First, the dual origins: W. Clement Stone's evangelical door-to-door insurance empire and Patrick Ryan's auto-dealership underwriting innovation, fused into the company that took the Gaelic name for "oneness." Then the Great Pivot of 2008, when Aon sold its underwriting businesses outright and bought its way to the top of reinsurance broking and human-capital advisory. Then the "Aon United" operating model and the shrewd 2017 divestiture of a low-margin outsourcing platform. Then the $30 billion antitrust trainwreck of the blocked Willis Towers Watson merger and its billion-dollar breakup fee. Then the $13.4 billion bet on the middle market via NFP, and the handover of the CFO seat to Edmund Reese. And finally the machine itself — fiduciary floats, the buyback engine, the competitive moat, and the case both for and against Aon from here.

We should be clear about posture from the outset. Aon tells a clean story about itself, and much of it is backed by real numbers. But a broker that has loaded $7 billion of debt onto its balance sheet to chase a fragmented market, at a moment when its legendary CFO has just departed, deserves scrutiny rather than applause. Let us begin where the money did.

II. The Genesis: Patrick Ryan, W. Clement Stone, and the Merger of Oneness (1919–1987)

Picture a young man on the frozen sidewalks of Detroit, knocking on doors he has no invitation to knock on, selling accident policies for pennies of premium to butchers, barbers, and shopkeepers. That was W. Clement Stone, who entered the insurance trade around 1919 and, in 1922, launched his own Chicago agency with a stake of just $100.2 Stone's genius was not actuarial; it was psychological. He built a sales army on the doctrine he would later brand as PMA — the Positive Mental Attitude — and co-authored a bestselling book of that name with Napoleon Hill. His agents chanted maxims, memorized scripts, and were sent out to sell high-volume, low-premium personal accident and health coverage one handshake at a time. Out of that machine grew the Combined Insurance Company of America, a genuine underwriter that manufactured its own policies and carried its own reserves.

Understand what Stone actually built, because it echoes through the culture that Greg Case would later have to reform. Combined Insurance was a manufacturing operation for salesmen. Stone's method was to codify enthusiasm itself — to take the hardest, most demoralizing job in commerce, cold-door selling, and turn it into a repeatable system that an ordinary person could be trained to execute. The maxims his agents repeated each morning — "I feel healthy, I feel happy, I feel terrific" — were not corporate kitsch; they were a technology for keeping a sales force functional in the face of relentless rejection. It worked spectacularly for what it was. But it built a company whose center of gravity was the individual producer's willpower, not systems, data, or scale — the precise inheritance that would later make integration so hard.

By the 1970s, Combined was a cash cow with a problem. It was brilliant at selling small policies to individuals and utterly absent from the lucrative world of corporate risk and commercial broking. It generated float and profit, but it had no seat at the table where large companies bought their coverage. It was, in modern language, a distribution engine pointed at the wrong, lower-value end of the market — rich in cash, poor in strategic direction.

Enter Patrick G. Ryan, a very different kind of insurance man. In 1964, Ryan founded the Ryan Insurance Group on an insight hiding in plain sight: the moment a consumer signs an auto loan is the perfect moment to sell them credit life and accident insurance.2 By embedding coverage directly into the dealership financing process, Ryan captured a captive, high-margin niche and pioneered extended mechanical warranty agreements. He then pushed outward into specialty commercial lines and surplus brokerage, building an entrepreneurial, talent-heavy agency culture — the polar opposite of Stone's scripted door-knockers.

Ryan, a Northwestern-educated Chicagoan who would later become chairman of his alma mater's board and lend his name to the university's football stadium, embodied the opposite of Stone's scripted enthusiasm. His was a business of specialists and dealmakers, of underwriting insight and entrepreneurial hustle at the corporate level. Where Stone manufactured salesmen, Ryan cultivated professionals. Two more different insurance cultures would be hard to design.

The two worlds collided in 1982. Stone, aging and hunting for a successor, agreed to have his holding company acquire Ryan Insurance for $133 million.2 The deal came with a twist that revealed who actually held the strategic upper hand: Ryan, whose firm was the smaller party, walked in as president and CEO of the combined entity. Stone stepped aside. This is worth dwelling on, because it inverted the usual logic of acquisitions — the acquired founder took command of the acquirer. It signaled that the future of the company lay with Ryan's corporate-brokerage vision, not Stone's door-to-door underwriting army. What followed was a slow, deliberate reorientation of the whole enterprise: the direct-sales underwriting business would be milked for cash and eventually shed, while brokerage and advisory would become the growth engine.

In March 1987, shareholders ratified a new name for the holding company: Aon Corporation, from the Gaelic word for "one" or "oneness" — a banner meant to unify a growing patchwork of acquisitions under a single identity.2 The irony, which would echo for the next two decades, is that "oneness" was aspiration, not reality. Ryan chose the name precisely because the company needed a unifying idea it did not yet possess. Naming a thing does not make it so, and the gap between the aspiration of the name and the reality of the operations would define the next twenty years of Aon's story — and eventually give Greg Case his branding slogan, "Aon United," which was simply the 1987 promise finally being kept.

Ryan spent the 1990s on an acquisition spree, rolling up regional and national brokerages across the United States and Europe. The crowning move came in December 1996, when Aon agreed to acquire Alexander & Alexander Services for $1.23 billion, briefly making it the largest insurance brokerage in the world.3 The A&A deal was itself the endgame of a two-year fight to save the struggling brokerage from its debts, and it vaulted Aon to some 40,000 employees across more than 80 countries. But the number-one ranking was fleeting: within months, Marsh & McLennan reclaimed the crown by acquiring Johnson & Higgins, and the pattern of Aon buying scale only to be leapfrogged by a better-integrated rival was set.

But scale purchased through serial acquisition is not the same as integration. By the late 1990s, Aon was a federation, not a company: dozens of unintegrated brokerage brands bolted onto a pair of capital-heavy underwriting subsidiaries, each with its own systems, culture, and P&L. The result was structurally low margins, a balance sheet burdened by insurance reserves, and a persistent valuation discount to its great rival, Marsh & McLennan. Ryan had built a giant. Someone else would have to make it work. That someone arrived from an unlikely place — a consulting firm.

III. The Great Pivot: Greg Case and Christa Davies' Masterclass in Capital Recycling (2005–2010)

In 2005, the Aon board did something that risk-averse boards rarely do: it handed a $10 billion company to a man who had never run one. Greg Case had spent his career at McKinsey & Company, where he led the global financial-services practice — advising insurers and banks rather than operating them. He replaced the founder, Patrick Ryan, and inherited exactly the problem a consultant is trained to diagnose. Aon, in Case's reading, was structurally broken. It bore the volatile, capital-heavy risk of underwriting — holding reserves against claims it had promised to pay — while its far more attractive brokerage business ran as a loose holding company with margins stuck in the low teens, well behind Marsh.

There is a useful way to see what Case brought that a homegrown insurance executive might not have. An industry lifer tends to accept the shape of the business as given — of course a broker also underwrites a little, of course each country runs itself, of course margins are what they are. A consultant who has spent years benchmarking financial-services firms against one another sees the same company as a set of comparisons: this margin is 800 basis points below that peer's, this capital is trapped where it earns nothing, this structure is a historical accident rather than a necessity. Case's outsider eyes let him treat Aon as a problem to be re-engineered rather than a heritage to be preserved. That detachment was the whole point.

The consultant's diagnosis is easy; the operator's cure is hard. Case's answer was to hire the person who would administer it. In 2008 he recruited Christa Davies as CFO. Davies was not an insurance lifer either — she came from Microsoft, where she had served as CFO of the Platform and Services Division, and had earned her stripes in an industry where the marginal cost of the next unit of product is close to zero. What she brought was a software mindset applied to a services business: an obsession with operating leverage, returns on invested capital, and the idea that a company's capital structure is itself a product to be engineered. In a software company, you build the code once and sell it a million times; Davies's insight was that a services firm could approximate that economics if it built its systems and data once and reused them across every client and country. That conviction became the intellectual seed of Aon Business Services. The Case–Davies partnership would last sixteen years and become one of the more studied capital-allocation stories in the sector.

Their opening move was audacious in its timing. On the same day — April 1, 2008 — Aon executed a coordinated exit from underwriting entirely. It agreed to sell Combined Insurance Company of America, W. Clement Stone's original creation, to ACE Limited (the insurer that would later rename itself Chubb) for $2.56 billion in cash.[^4] Simultaneously, it sold Sterling Life Insurance Company to the Munich Re Group for $352 million.[^5] In one stroke, Aon stripped underwriting risk, credit risk, and reserve requirements off its balance sheet and pulled nearly $3 billion of liquidity into the treasury — mere months before the global financial crisis detonated. Selling capital-intensive insurers into cash at the top of a credit cycle was, in retrospect, a spectacularly well-timed act of corporate housekeeping.

What matters is not just that Aon raised cash, but where it put it. The genius of the pivot was the trade it enabled: out of taking risk, into pricing risk. In August 2008 Aon agreed to acquire the Benfield Group, the leading independent reinsurance broker, in a deal with an enterprise value of roughly £935 million — about $1.75 billion — completing the transaction that November.4 The combined Aon Benfield instantly became the undisputed global leader in reinsurance broking.

To appreciate why this trade was so elegant, understand what reinsurance broking actually is. A primary insurer — the company that sells you your homeowner's policy — does not want to keep all the risk of a Florida hurricane season on its own books, so it buys insurance on its insurance: reinsurance, from firms like Munich Re or Swiss Re. Arranging those treaties is fiendishly technical, requiring catastrophe modeling, actuarial analysis, and access to the global pools of capital willing to bear tail risk. Aon Benfield stood in the middle of that market as the essential connector. This is the tollbooth in its purest form: the broker earns a fee for connecting a primary insurer that wants to offload risk with the reinsurance capital willing to absorb it, and it captures the analytical data on both sides of every transaction without ever putting its own capital at stake. Aon had, in the space of a single year, swapped a business that bore hurricane risk directly for one that got paid to price hurricane risk for others — the same storms, an entirely different and far safer relationship to them.

Two years later, Aon anchored the other half of its future. In 2010 it acquired Hewitt Associates, the human-resources consulting and benefits-administration giant, for approximately $4.9 billion — a mix of $2.45 billion in cash and 64 million newly issued shares — and merged it with Aon Consulting to form Aon Hewitt.5 The logic was diversification of the revenue base. Employee benefits, retirement, and HR advisory throw off recurring, contract-based revenue that does not lurch with the property-and-casualty insurance pricing cycle the way commercial broking does. When commercial insurance prices soften and broking commissions dip, companies still need someone to run their pension plans and health benefits. Aon now stood on two legs — risk and human capital — a structure it still organizes itself around today under the labels Risk Capital and Human Capital.

Not everything in the Hewitt deal was clean, and it is worth being honest about the part management tends to skip. Hewitt came with a large, low-margin benefits-administration outsourcing arm — high-volume, transactional, technology-heavy work that sat awkwardly against Aon's ambition to be a high-margin advisory firm. Aon bought the whole thing to get the consulting jewel, then spent the next seven years figuring out how to shed the part it did not want. The 64 million shares issued to fund Hewitt also ran directly against the buyback religion; here, as with NFP much later, the company was willing to dilute when the strategic prize justified it. The scoreboard nonetheless vindicated the broad strategy, if slowly. Freed of underwriting drag and pointed at fee income, the business began the long climb in profitability that would define the Case–Davies era. But margins do not expand on strategy decks alone. They expand when someone rewires how the company actually runs — which is the next chapter.

IV. The "Aon United" Operating Model & The Alight Divestiture (2010–2019)

For most of its history, Aon had behaved like a confederation of local chieftains. The office in Frankfurt ran its own systems, kept its own client relationships, and answered to the Aon name mostly for the letterhead. This decentralization felt entrepreneurial, but it was quietly expensive: every country reinvented the same back office, and no one could see across the whole enterprise to serve a multinational client as a single firm.

The response was a philosophy the company branded "Aon United." Its first principle was almost tribal: kill the local brands. Acquisitions that had traded for decades under their own names — some with a century of goodwill in their nameplates — were folded into a single global identity, so that a CFO in São Paulo and a risk manager in Singapore experienced one Aon, not a franchise. This was not a costless decision. Retiring a respected local brand risks alienating the very producers and clients attached to it, and plenty of acquirers have destroyed value by stamping their name over an acquired firm's. Aon judged that the benefits of a single global face — the ability to serve a multinational client identically in forty countries — outweighed the sentimental cost. It was a bet on scale over heritage, and it repeated the 1987 logic of "oneness" that had never actually been executed.

The second principle was the one that actually moved the numbers — Aon Business Services, or ABS. Rather than letting each office run its own IT, procurement, policy administration, and data processing, Aon migrated those functions into global shared-service hubs, many in lower-cost locations. Think of ABS as the company's centralized factory floor: standardize the software, centralize the data, automate the repetitive claims and placement work, and you can grow revenue without adding headcount in lockstep. In a business where people are the dominant cost, this is everything. If a broker must hire one new administrator for every new account, its margins are capped forever; if it can process ten new accounts on the same platform with the same staff, margins climb with every added client. That decoupling of revenue growth from cost growth is the engine beneath every margin improvement Aon would later report — and the single most important operational idea in the entire company.

The most instructive move of the decade, though, was a sale. Aon Hewitt had brought with it a large benefits-administration outsourcing business — the plumbing that processes health and retirement enrollments for thousands of corporate employees. It was big, but it was also capital-intensive, transactional, and low-margin, running perhaps 12–15% operating margins against a corporate average trending far higher. In February 2017, Aon agreed to sell that platform to private-equity funds managed by The Blackstone Group for $4.3 billion in cash at closing, plus up to $500 million in performance-based earn-outs.[^8] The business was rechristened Alight Solutions and set loose. Aon had deliberately sold its lowest-quality earnings stream.

What Aon did with the proceeds is the tell. A $4.3 billion windfall is enough to fund another empire-building acquisition; a company addicted to growth-by-deal would have spent it that way. Instead, the vast majority of the cash was funneled into share buybacks. This was capital allocation as a statement of identity: Aon would rather shrink its own equity than dilute its returns chasing scale. It was also a quiet admission about the industry — that at Aon's maturity, the highest-returning investment available was often the company's own stock, not another bolt-on brokerage bought at a full price. The effect on reported profitability was immediate and mechanical, as adjusted operating margins that had sat around 19% in 2013 marched toward the high-20s by decade's end. Shedding low-margin revenue mathematically raises the average, and retiring shares concentrates the earnings that remain.

A skeptic should note the two-edged nature of this. Selling Alight flattered the margin percentage without necessarily making the company more valuable in absolute dollars — you can always raise your average grade by dropping your worst class. And a business that leans this heavily on buybacks to manufacture per-share growth is implicitly conceding that its organic engine grows only in the mid-single digits. The bull answer is that mid-single-digit organic growth, compounded on a shrinking share base at high incremental margins, is a genuinely powerful machine. The bear answer is that the machine only looks impressive because the denominator keeps falling. Both are true, and the tension between them is the crux of the Aon investment debate to this day.

There was a jurisdictional subplot running alongside the operational one. In 2012, Aon relocated its corporate headquarters from Chicago to London — closer to Lloyd's of London, the beating heart of global specialty insurance, and to a friendlier corporate tax regime. Then, in 2020, reading the coming turbulence of Brexit, Aon shifted its parent incorporation from the United Kingdom to Ireland, preserving EU market access and a competitive tax rate.1 These were not sentimental decisions about where to hang the sign; they were deliberate optimizations of tax and regulatory footing, of a piece with a management team that treated every line of the income statement as a variable to be tuned. A lower effective tax rate flows straight through to net income and free cash flow, which in turn fuels more buybacks — so even the choice of domicile was, in the end, in service of the same compounding machine. Critics who dislike corporate inversions have a fair moral objection; investors focused on returns simply noted that Aon squeezed value from a lever most companies ignore. Both readings describe the same fact: this is a management team that leaves very little on the table.

By the end of the 2010s, the transformation Ryan's federation had cried out for was largely complete. The brands were unified, the back office was centralized, the worst-margin businesses were gone, and the share count was shrinking. Aon had become the high-margin, capital-light fee machine its leaders had promised. And precisely because it had run out of easy internal improvements to make, management's attention turned to the one move that could reset the entire competitive order in a single stroke.

By 2019, Aon looked less like a roll-up and more like a machine: one brand, one shared-services backbone, a portfolio purged of its worst margins, and a share count in steady decline. Confident in that machine, management decided it was strong enough to attempt the boldest move in the industry's history — swallowing a rival nearly its own size.

V. The Antitrust Drama: The $30 Billion Willis Towers Watson Breakup (2020–2021)

The announcement landed in March 2020, in the same fortnight the world was shutting its doors against a pandemic. Aon declared it would acquire Willis Towers Watson — then the third-largest global broker — in an all-stock transaction valued at roughly $30 billion. The ambition was naked and enormous: leapfrog Marsh & McLennan and become, unambiguously, the largest broker on earth. Management promised $800 million in run-rate cost synergies, largely by dragging Willis's operations onto the ABS platform that had already proven it could squeeze cost out of scale.

The timing deserves a moment of empathy and a moment of skepticism. Announcing a $30 billion all-stock megamerger in the exact week that COVID-19 froze the global economy was either supremely confident or slightly reckless; the two companies were effectively agreeing to spend the next year integrating while the world's risk landscape convulsed. Management's framing was that scale and efficiency mattered more than ever in a crisis. The counter-view is that Aon committed itself to an enormous, distraction-heavy transaction at precisely the moment its clients most needed undivided attention.

There is a certain logic to combining the number two and number three players in a consolidating industry. There is also a name for it, and regulators know that name. The deal walked directly into the buzzsaw of global antitrust review across multiple continents. The European Commission demanded extensive structural divestitures, and Aon, eager to close, agreed to them — proposing to sell major pieces of Willis's reinsurance and other businesses to Arthur J. Gallagher to placate Brussels. That concession package is itself telling: to make the deal legal in Europe, Aon was prepared to hand a meaningful chunk of the combined company's revenue to a direct competitor, strengthening a rival in businesses Aon itself wanted to grow. For a moment, it looked like concessions might carry the day.

The fatal blow came from Washington. In June 2021, the U.S. Department of Justice, under a newly assertive Antitrust Division, filed a civil lawsuit to block the merger outright.6 The government's theory was blunt: combining Aon and Willis would eliminate head-to-head competition across commercial risk broking, reinsurance, and pension and retirement services, leaving America's largest employers to choose between an effective duopoly of Marsh and a supersized Aon. The DOJ argued the divestitures Aon had negotiated were a patch, not a cure — that they would not restore the rivalry the merger destroyed. This was a philosophical shift in enforcement, arriving with the incoming administration's more aggressive competition stance, and a signal that regulators were done accepting behavioral and partial structural remedies for what they viewed as fundamentally anticompetitive combinations. Aon had, in effect, misread the political weather. It negotiated its concessions for the regulatory regime of the past, and the regime of the present rejected them wholesale.

Faced with a multi-year courtroom war that would freeze two organizations in strategic limbo, Case and the Aon board made the unsentimental call. On July 26, 2021, the two companies mutually terminated the combination.7 Aon paid Willis a $1 billion cash termination fee — a staggering sum to walk away with nothing to show for eighteen months of effort.7 Willis promptly turned that windfall into a share-buyback program of its own, which is a quietly humiliating footnote: Aon's failed ambition directly financed its rival's capital return.

The stress test came next. Skeptics wondered aloud whether Case's entire growth strategy had died on the DOJ's desk. The stock fell; analysts questioned whether Aon could generate satisfying growth as a standalone company without the consolidation windfall. Management's answer was not to change the strategy but to intensify it. Rather than acquire scale, Aon would manufacture growth internally — accelerating Aon United, tightening margin discipline, and redirecting attention to an underserved market segment it had long neglected. Within roughly a year, the stock had recovered to new highs. The lesson management drew, and repeated, was that organic execution could outrun the friction of megamergers. The lesson a careful observer should draw is narrower: Aon proved it could survive the failure, not that the failure was costless. A billion dollars and a year of executive attention had been spent to learn that the front door to consolidation was locked. The company would have to find a side door.

VI. The Middle-Market Bet: The $13.4 Billion Acquisition of NFP (2023–2025)

For all its dominance among the Fortune 500, Aon had a persistent blind spot, and it was a lucrative one. The company was superb at serving global multinationals — the accounts where risk programs are custom-built, fiercely negotiated, and priced to the bone by sophisticated corporate buyers who can play brokers against one another. What Aon had never cracked was the middle market: the vast, fragmented universe of companies with roughly 100 to 5,000 employees.

Why does that segment matter so much? Because its economics are, in several respects, better than the mega-account business Aon had spent a century mastering. A global multinational employs its own risk managers, runs competitive tenders, and treats broking as a service to be commoditized and priced down. A 500-person manufacturer does not; it leans on its broker for genuine advice, rarely switches, and pays commissions that are rich relative to the modest work involved. Middle-market clients switch brokers less often, negotiate less aggressively on price, and value continuity over squeezing the last basis point. It is, in short, a stickier and more profitable place to sell — precisely the kind of market that Arthur J. Gallagher and Brown & Brown had been consolidating for years, rolling up hundreds of independent agencies, while Aon watched from the Fortune 500 penthouse. Those two rivals had, in effect, discovered that a thousand small, loyal accounts can be worth more than a handful of giant, mercenary ones. Aon arrived late to that realization and had to buy its way into it.

In December 2023, Aon moved to buy its way in, announcing the acquisition of NFP — a leading middle-market property-and-casualty broker, benefits consultant, and wealth advisor — for an enterprise value of approximately $13.4 billion, purchased from funds affiliated with Madison Dearborn Partners and HPS Investment Partners.[^11] The deal closed on April 25, 2024, faster than originally guided, at an enterprise value of about $13.0 billion, funded with roughly $7 billion in cash and assumed liabilities and about $6 billion in equity — some 19 million Aon shares.8 That equity component is worth pausing on: after two decades of relentlessly retiring shares, Aon issued a slug of new ones to pay for NFP. The cannibal, for once, fed the count it had spent twenty years shrinking.

The price drew fire. NFP was acquired at roughly 15 times its seller-adjusted, estimated EBITDA at closing — an aggressive multiple for what is, at bottom, a roll-up of independent brokers, struck just as interest rates had climbed and made debt-funded acquisitions dearer. Critics asked the obvious question: did Aon overpay for growth it couldn't generate organically? The bull rebuttal has real force, though. Publicly traded middle-market consolidators like Gallagher and Brown & Brown routinely change hands at 18 to 22 times forward EBITDA, so 15 times looked, on a relative basis, like a discount — and Aon layered on a target of roughly $235 million in combined cost and revenue synergies to sweeten the math. If those synergies land, the effective multiple compresses meaningfully.

The integration approach reveals what Aon actually learned from its history of clumsy roll-ups. Rather than absorbing NFP and dissolving it into the mother ship, Aon has kept it as a distinct, "independent and connected" platform under its existing leadership, Doug Hammond, reporting to Aon President Eric Andersen. This is a subtle and important reversal of the "Aon United" playbook. For a decade, the doctrine had been to erase acquired brands and centralize everything; with NFP, Aon deliberately did the opposite, preserving the name, the leadership, and the entrepreneurial autonomy. Why? Because the thing being bought was the culture itself. In the middle market, the producer's local relationships and freedom to move quickly are the product; centralize them into a global bureaucracy and you destroy the very asset you paid fifteen times earnings to acquire. So the plan is surgical: leave the client-facing, producer-driven front office alone, and quietly migrate only the invisible back office — the IT, data, and processing — onto ABS to capture the cost synergies.

Management has guided to around $100 million in cost synergies from the NFP integration in 2026 alone, on the path toward the roughly $235 million total. But the strategy contains an unavoidable tension that no slide can resolve. The synergies come from centralization; the value comes from autonomy. Push too hard on the former and you trigger the producer defections that plague every brokerage acquisition — star brokers who leave, sometimes taking their client books with them, the moment the acquirer's systems and compensation grids start to chafe. Push too little and the synergies never materialize and the price looks foolish. Whether Aon can hold that balance is the single biggest execution question hanging over the company, and it will not be answered for years, because attrition in a book of business reveals itself slowly. The prize is real; so is the risk. And both run through the financial engine we turn to next.

VII. The Financial Engine & Operating Playbook: Aon Business Services, Cannibal Capital Allocation, and Fiduciary Floats

To understand why investors care about a business that sounds, on paper, like a glorified travel agency for insurance, you have to understand the economics of the tollbooth. A broker does not underwrite. It does not hold reserves against hurricanes or lawsuits. It stands between the buyer and the seller of risk, arranges the transaction, and collects a fee or commission. The consequences of that structure are profound. Capital expenditure is minimal — typically well under 2% of revenue, mostly software and IT — because there are no plants to build or claims reserves to fund. And the working-capital cycle is often favorable to the point of being negative, because of a peculiar and beautiful feature of the business called the fiduciary float.

Here is how the float works, in plain terms. When a corporate client buys insurance through Aon, it frequently pays the premium to Aon first. Aon holds that money in fiduciary trust accounts before passing it along to the insurance carriers who actually bear the risk. During the days or weeks that this cash sits in trust, Aon earns interest on it — money it keeps, called fiduciary investment income. It is close to pure profit, because the cash costs Aon nothing; it belongs, temporarily, to the flow of the business itself. This is the same principle that makes banks and insurers valuable, applied to a company that takes none of their risk.

The catch is that the float is a rate play, and rates move. In 2024, with interest rates elevated, Aon generated $315 million of fiduciary investment income. In 2025, as rates eased, that figure fell to $271 million.1 That decline of roughly $44 million is a useful reminder that a chunk of Aon's recent margin story rode a macro tailwind it does not control. When central banks cut, this line shrinks, and management has to find the offset elsewhere. It is exactly the kind of income an activist would flag: high-quality while it lasts, but not evidence of operating skill, and prone to fading just as the reported numbers make management look most heroic. A careful reader mentally separates the margin that ABS earned from the margin that the Federal Reserve donated.

The same tollbooth structure produces one more gift that rarely shows up in headlines: a favorable, often negative, working-capital cycle. Because clients frequently pay premiums before Aon must remit them to carriers, and because the firm carries no inventory and little in the way of receivables tied up in production, the business tends to be funded partly by its own float rather than needing to fund itself. Combine near-zero capital expenditure — mostly software, running under 2% of revenue — with a working-capital dynamic that releases cash rather than consuming it, and you get a company that converts an unusually high share of its accounting profit into actual, spendable free cash flow. That conversion is the quiet foundation of everything the capital-allocation story is built on.

Elsewhere, mostly, means ABS. The reason Aon's adjusted operating margin has climbed to 32.4% in 2025 from 31.5% in 2024 — and expanded by well over a thousand basis points across the Case era — is that the shared-services backbone lets revenue grow faster than cost.19 Standardized software, centralized data, and increasingly AI-assisted automation in claims processing and risk analysis mean Aon can take on more clients without hiring proportionally more people. That is the whole game in a labor-intensive services business: break the link between growth and headcount, and margins expand almost automatically. The evidence that it is working is the margin line itself, which has ground higher with unusual consistency — though the pace has slowed to a more modest 70–90 basis points a year, a sign that the easy gains have largely been harvested.

Then there is the capital-allocation religion. For most of the Case–Davies era, the priority was singular and unwavering: convert profit into free cash flow, and spend the excess buying back stock. In 2025, free cash flow reached $3.2 billion, up 14%, and the company repurchased roughly 2.7 million shares for about $1 billion even while digesting the NFP debt.1 Over two decades the share count fell from around 320 million to roughly 200 million. The strategic beauty of this is arithmetic: if you shrink the denominator, then even mid-single-digit revenue growth converts into double-digit growth in earnings and free cash flow per share. Aon does not need to grow fast to compound value for owners; it needs to grow steadily and keep retiring shares.

It is worth making the arithmetic concrete, because it is the heart of why owners have done well. Imagine a company earning a fixed pool of profit and buying back 3% of its shares every year. Even with zero growth in that profit pool, earnings per share would rise roughly 3% annually, simply because the same pie is sliced into fewer pieces. Now layer on mid-single-digit growth in the profit pool from organic revenue and margin expansion, and the two effects compound: a business growing profits 6–8% can deliver low-double-digit growth in per-share earnings and cash flow, year after year, without ever doing anything heroic. That is the Aon machine in one sentence — modest operating growth, amplified by relentless share retirement, into consistent double-digit compounding for the shareholders who remain. It is not magic; it is discipline applied for twenty years.

But the NFP deal bent this discipline, and honestly so. The $7 billion of debt raised to fund it, plus the 19 million shares issued, temporarily throttled the buyback engine and lifted leverage at a time of higher interest costs. Management frames this as a pause, not a reversal — a deliberate detour to buy a growth platform, after which the cannibalism resumes. The bear reads it differently: a company that promised capital discipline made its largest, most expensive acquisition ever, right as its financial architect headed for the door. Which reading is correct will be settled by the pace at which debt comes down and buybacks come back. That, more than any slogan, is the number to watch.

VIII. The Competitive Landscape: Porter's 5 Forces, Helmer's 7 Powers, and MMC vs. Aon Benchmarking

Step back and survey the battlefield, and you find not a free market but an oligopoly — a "Big Four" that controls the commanding heights of global insurance broking. At the top sits Marsh & McLennan, the scale leader, with revenue of roughly $24 billion in 2024 climbing toward $27 billion in 2025. Aon is the clear number two, and importantly the efficiency leader, with $15.7 billion of revenue in 2024 rising to $17.2 billion in 2025 and the highest operating margins in the group.1 Arthur J. Gallagher is the aggressive middle-market aggregator, growing from around $11.6 billion toward roughly $13.9 billion, largely by acquiring smaller agencies at a relentless pace. And Willis Towers Watson — the bride Aon was forbidden to marry — trails at under $10 billion, still simplifying its portfolio and chronically the slowest grower of the four. The shape of the industry matters: four players large enough to serve any multinational on earth, and a long tail of regional brokers who cannot reach across borders or command the same carrier terms.

The competitive story between Aon and Marsh is a study in two routes to the same fortress. Marsh chose breadth and revenue leadership; Aon chose depth and margin leadership. Aon's operating margins are the envy of the group, which is management's proof point that "Aon United" and ABS are genuine sources of advantage rather than slogans. But the bear will point out that Marsh grows revenue faster and carries less of the integration risk Aon has taken on with NFP, and that a margin lead is a lead only until the follower copies the playbook. Marsh has its own shared-services and offshoring programs; there is no law of nature that keeps Aon's margins permanently ahead. The efficiency edge is real today and must be re-earned every year.

Why is this structure so durable? Run it through Hamilton Helmer's framework of competitive "powers." The first is scale economies. Aon places an enormous volume of premium into the market, and that volume buys it access — exclusive capacity, preferential terms, and pricing arrangements with major carriers that a regional broker simply cannot command. A carrier will build a bespoke product for a broker that can deliver a billion dollars of premium; it will not do so for one that delivers a million.

The second and most powerful is switching costs. A large company's risk program is not a product it buys off a shelf; it is a system woven into its compliance, its operations, and its balance sheet. Global employee-benefits plans, multinational property programs, and treaty reinsurance structures are deeply customized and tightly integrated. Ripping out the broker that built them means risking coverage gaps, losing tailored analytics, and enduring months of administrative friction — for a saving that rarely justifies the danger. This is why Aon's client retention runs consistently above 90%. Customers stay not because they are delighted every year, but because leaving is genuinely frightening.

The third is the cornered resource: proprietary data. Aon sits on decades of global loss histories, claims data, and pricing patterns, accumulated across millions of placements and analyzed through tools like Aon Inpoint. A new entrant cannot buy or replicate this; it can only accumulate it, slowly, over decades it does not have. Increasingly Aon packages this data into predictive models that carriers themselves pay to access — turning the exhaust of the broking business into a product. This is the power an investor should weight most heavily, because unlike scale (which Marsh also has) and switching costs (which protect all incumbents), a genuinely unique data asset can, in principle, separate one broker from the pack. The open question is whether Aon's data is meaningfully richer than its rivals', or whether all four giants sit on comparable troves — in which case data is a shared moat, not a personal one.

The remaining Helmer powers are notable mostly by their absence, which is itself informative. Aon has little in the way of a consumer brand — corporate buyers choose it on capability and relationships, not on a logo that commands a price premium. It has no network effect in the classic sense, no counter-positioning that a rival cannot copy, and no process power so secret it cannot be imitated over time. What it has is a stack of overlapping, largely structural advantages that are individually replicable but collectively very hard to assemble from scratch. That is the honest shape of the moat: wide and deep against a startup, but only modestly differentiated against the three other firms that already sit inside it.

Now overlay Porter's five forces and the picture sharpens. Rivalry among the Big Four is intense but rational: they compete ferociously for talent — poaching star "producers," the relationship-holding brokers who bring books of business with them — but they largely avoid the mutually destructive price wars that wreck less disciplined industries. Barriers to entry are close to prohibitive; building a licensed distribution network across 120-plus countries with deep carrier relationships is not a venture a startup can bootstrap. Supplier power — the carriers — is modest, because underwriters need the brokers to reach customers as much as the reverse. And buyer power sits in the middle: the largest corporate clients are sophisticated and can push on price, but they depend on the global placement networks only a handful of firms possess.

The uncomfortable truth for Aon inside this fortress is that the same forces protect Marsh, Gallagher, and Willis. A moat that shelters everyone shelters no one in particular. Aon's edge over its peers is therefore not the moat itself but what it does inside the walls — its margin leadership and its capital discipline. Which raises the central investment question: is that operational edge real and durable, or is it a lead that rivals are steadily closing? That is the debate we stage next.

IX. The Investment-Story Spine: Bull vs. Bear Case, CFO Transition, and Greg Case's 2030 Horizon

Every compounding story eventually faces a succession test, and Aon's arrived in 2024. Christa Davies — the architect of the buyback machine and the discipline that defined the company for sixteen years — stepped down as CFO. Her successor, Edmund Reese, took the seat on July 29, 2024, arriving from Broadridge Financial Solutions, where he had been CFO, with earlier finance leadership at American Express.[^14] Reese inherits a specific and unforgiving mandate: sustain Davies's capital discipline while working down the NFP debt and proving the acquisition was worth the leverage. Markets do not extend the benefit of the doubt to unproven CFOs at levered companies, and Reese's credibility will be built or dented on the pace at which free cash flow deleverages the balance sheet.

To keep the strategy legible through the transition, the board extended Greg Case's contract through December 31, 2030 — a deliberate signal of continuity for the post-NFP era, and a bet that the man who built the machine should be the one to prove it still runs without its original mechanic. The framework Case has offered is the "3x3 Plan" for 2024–2026, resting on three commitments: integrating Risk Capital with Human Capital, accelerating Aon Business Services, and scaling the firm's client-leadership model down into the middle market. It is backstopped by an "Accelerating Aon United" restructuring program, which delivered net savings of $50 million in the fourth quarter of 2025 alone and continues to feed margin expansion.1 The early operating evidence is supportive: in the first quarter of 2026, Aon reported 5% organic revenue growth, adjusted EPS of $6.48, and free cash flow of $363 million — up sharply as NFP integration costs began to roll off — and reaffirmed full-year guidance for mid-single-digit or greater organic growth, margin expansion, and double-digit free-cash-flow growth.10

On the credibility question, management's record over the Case era earns cautious respect rather than blind faith. The team has generally set targets and hit them, has communicated a consistent strategic story across a decade and a half of filings and calls, and — crucially — reacted to the WTW failure with candor and a concrete pivot rather than denial. That is more than many management teams offer. But the same team is now asking investors to trust it through the two most legitimate points of doubt in its tenure at once: the departure of the CFO who personified its discipline, and the largest, most leveraging acquisition it has ever made. On recent earnings calls, analysts have pressed repeatedly on NFP producer retention and the trajectory of deleveraging, and management's answers have leaned on reaffirmed synergy targets and organic-growth metrics rather than granular disclosure on attrition. Reaffirming a target is not the same as proving it; the honest verdict is that the NFP thesis remains unproven, and management has earned the right to be given time, not the right to be believed in advance.

It is worth puncturing one consensus narrative directly — call it the myth of the pure quality compounder. The popular story holds that Aon's soaring margins and per-share growth are the clean output of operational genius. The reality is more mixed and more interesting. A material slice of the recent margin gain came from the fiduciary-income rate tailwind now reversing; a slice of the multi-year margin story came from selling low-margin businesses rather than improving them; and the celebrated per-share compounding was amplified by a buyback engine that has, for now, been throttled by NFP debt. None of this makes Aon a bad business — the underlying franchise is genuinely excellent — but the tidy "quality compounder" label flatters a story that is really about disciplined portfolio surgery, financial engineering, and one very well-timed macro gift. Seeing that clearly is what separates an investor from a fan.

So why does Aon win from here? The bull case rests on three legs. First, NFP synergy acceleration: if the roughly $235 million synergy target lands on or ahead of schedule, mid-market margins expand and the aggressive purchase multiple looks cheap in hindsight — and Aon gains a durable foothold in the stickiest, highest-retention segment of broking, precisely the fast-growing market it had missed. Second, structural pricing tailwinds: because brokers earn commissions tied to premium volume, a world of rising climate catastrophe, escalating cyber threats, and social-inflation litigation quietly lifts Aon's fee income without any extra effort, since the same policy simply costs more to place. This is a subtle but powerful feature — Aon is partially indexed to the rising price of risk itself, and the world is manifestly becoming riskier, not safer. Third, human-capital convergence: as corporate clients increasingly want risk, health, and wealth advice from a single integrated partner rather than a committee of specialists, Aon's two-legged platform drives cross-selling that pure-play brokers cannot match, deepening switching costs with every additional service woven into the relationship.

And why might the case break? The bear points to the mirror image of each bull argument. Integration friction and attrition is the first and gravest risk: NFP's entrepreneurial producers may chafe against the centralized ABS model, and if key brokers walk — taking their client books with them — the synergy math inverts into value destruction. Second, the leverage-and-buyback pause: the $7 billion of NFP debt constrains the very share-cannibalism engine that powered two decades of per-share compounding, and every quarter the buyback stays muted is a quarter the EPS flywheel spins slower. Third, producer-compensation inflation: the same talent war that makes rivalry "rational" on price makes it brutal on pay, and if Marsh and Gallagher bid up producer compensation, Aon's vaunted margins feel the squeeze.

The activist's stress test cuts deeper still. A skeptical investor would ask whether Aon's margin leadership is genuine operating superiority or partly an artifact of a fiduciary-income tailwind that is now reversing as rates fall. They would question whether serial buybacks have flattered per-share metrics while masking merely adequate organic growth. And they would press hard on the governance optics of a company that preached capital discipline for twenty years and then made its largest, most expensive, most leveraging acquisition in history at the exact moment its disciplinarian CFO departed. None of these are disqualifying. All are legitimate, and management has not yet fully answered them with results.

The current risk radar adds a few genuinely material items worth naming, and dismissing the irrelevant ones. Refinancing and cost-of-capital risk is real: the $7 billion NFP debt was raised in a higher-rate world, and the pace at which Aon can term it out and pay it down directly governs when the buyback engine restarts. Technology disruption cuts both ways — the same AI that Aon is deploying inside ABS to widen its margins could, over a longer horizon, lower the barriers that protect broking, if software begins to automate the analytical and placement work that today justifies the broker's fee. That is not a next-year threat, but it is the kind of slow erosion a patient bear watches for. And talent is the perennial exposure: a broker is a portfolio of relationships that go home every night and can be recruited away, which is why producer-compensation inflation is not a footnote but a structural cost pressure. Conversely, most macro scares that spook generalist investors — recession, supply chains, tariffs — matter far less to a fee-based intermediary with 90%-plus retention than they do to the average industrial. Aon's real risks are specific and internal, not broadly cyclical.

Which is why, for all the strategic narrative, the story reduces to three numbers a patient investor should track. First, organic revenue growth — the truest measure that core demand is intact and that NFP's producers are staying rather than fleeing, targeted at mid-single digits or better. This is the single cleanest read on the health of the franchise, because it strips out the noise of currency, acquisitions, and buybacks to show whether the underlying business is genuinely winning and keeping clients. Second, adjusted operating margin expansion — the scoreboard for whether ABS and NFP integration are actually delivering efficiency, with management guiding to roughly 70–80 basis points a year; watch here for whether the gains persist even as fiduciary income fades, which would prove the efficiency is operational rather than borrowed from interest rates. And third, free cash flow growth — the ultimate fuel, because it simultaneously pays down the NFP debt and refills the buyback tank; the moment repurchases return to their historic pace will be the signal that the balance sheet has healed and the cannibal is hungry again. Everything else is commentary; these three tell you whether the machine still works.

X. Epilogue & Surprises

Here is a wrinkle most investors never associate with an insurance broker: Aon has quietly become a pioneer in lending against ideas.

For as long as banks have existed, they have struggled to lend against intangible assets. A lender can seize a factory or a fleet of trucks if a borrower defaults, but how does it repossess a patent portfolio or a body of proprietary software? Intangibles are hard to value, hard to secure, and hard to sell — so high-growth technology companies, whose entire worth often lives in their intellectual property, have historically been forced to raise capital by selling equity and diluting their founders. Their most valuable assets sat on the balance sheet, financeable by no one.

Aon's insight was to make IP lendable by wrapping it in insurance. The company combined proprietary, increasingly AI-assisted valuation tools with collateral-protection insurance: Aon assesses and effectively underwrites the value of a company's intellectual property, and the insurance policy backstops that value for a lender. Suddenly a bank can extend a loan against patents, because if the borrower fails and the IP proves worth less than appraised, the insurance covers the shortfall. The technology company raises non-dilutive debt against assets that were previously unfinanceable, the lender gets a protected position, and Aon collects fees for valuation and for placing the coverage. It is a small, elegant demonstration of the company's deepest capability: taking a category of risk the financial system finds illegible, making it measurable, and then charging to intermediate it.

The macro backdrop makes this more than a curiosity. The share of corporate value that lives in intangibles — software, patents, brands, data — has grown enormously over the past few decades, yet the machinery of lending still leans heavily on physical collateral. Global bodies studying intangible-asset finance have flagged insurance-backed structures as a promising route to close that gap and unlock lending against intellectual property — precisely the gap Aon set out to fill.[^16] Aon has helped facilitate over $1 billion in IP-backed transactions, a rounding error against a $17 billion revenue base, but that is the point of an option: it costs little today and pays off only if the market it addresses becomes very large. A sober reading is that this is optionality, not yet a business — a reminder that the same risk-intermediation muscle that transformed Aon can be pointed at genuinely new frontiers, with an uncertain but potentially significant payoff.

It is a fitting note to end on, because it captures what Aon actually is beneath the tollbooth metaphor. This is a company whose core competence is not selling insurance but understanding, valuing, and repackaging risk in forms the rest of the financial system cannot. The enduring lesson of the Case–Davies transformation is that intense operational focus, ruthless capital recycling, and a standardized back office can convert a commoditized agency roll-up into one of the highest-quality, most cash-generative franchises in financial services — and that the same discipline, turned outward, can invent entirely new markets. The open question is whether that discipline survives its own founders.

XI. Outro

Greg Case's legacy is, at its heart, a legacy of subtraction. He and Christa Davies made Aon great less by what they added than by what they took away: the underwriting risk sold off in 2008, the low-margin outsourcing platform handed to Blackstone in 2017, the 120 million shares retired over two decades, the complexity stripped out through a single global operating model. The company that emerged is leaner, richer, and more focused than the federation Patrick Ryan bequeathed — but it is also, for the first time in twenty years, meaningfully in debt and betting on a market it has never mastered.

There is a broader lesson in Aon's arc that outlives any single quarter. The company's history is a rebuke to the idea that great businesses are built only by inventing new products. Aon invented almost nothing; it sells the same brokerage service the industry has offered for a century. What it did instead was harder to see and harder to copy: it relentlessly improved the quality of the earnings it already had — shedding the risk, standardizing the cost, and concentrating the ownership — until an ordinary-looking business compounded into an extraordinary one. That is a template as much as a story, and it is why Aon is studied by investors who never buy a single insurance policy.

What to watch, as Edmund Reese guides the capital engine toward the 2030 horizon, is whether the machine's two defining behaviors reassert themselves: the deleveraging that would prove NFP was affordable, and the return of the buyback that would prove the cannibal is still hungry. If organic growth holds in the mid-single digits, margins keep grinding higher, and free cash flow both retires the NFP debt and refills the repurchase tank, then the Case era will be remembered as a clean handoff rather than a peak. If integration falters, producers defect, and leverage lingers, the same story reads as a disciplined company that lost its discipline right as its architect walked out the door. The evidence will arrive one quarter at a time, and it will be written in three numbers — organic growth, operating margin, and free cash flow per share. The tollbooth, for now, keeps collecting.

References

-

Aon Reports Fourth-Quarter and Full-Year 2025 Results — Aon plc, 2026-01-30 ↩↩↩↩↩↩↩

-

A&A agrees to Aon Corp. acquisition — a $1.23 billion deal — The Baltimore Sun, 1996-12-12 ↩

-

Aon to Acquire Broker Benfield for $1.75 Billion — Insurance Journal, 2008-08-22 ↩

-

Hewitt Associates Inc. Form 8-K — U.S. Securities and Exchange Commission, 2010-07 ↩

-

Justice Department Sues to Block Aon's Acquisition of Willis Towers Watson — U.S. Department of Justice, 2021-06-16 ↩

-

Aon and Willis Towers Watson Announce Mutual Agreement to Terminate Combination Agreement — Aon Mediaroom, 2021-07-26 ↩↩

-

Aon completes acquisition of NFP to bring more capability to clients — Aon Mediaroom, 2024-04-25 ↩

-

Aon Reports Fourth Quarter and Full Year 2024 Results — Aon plc, 2025-01-31 ↩

-

Aon Reports First-Quarter 2026 Results — Aon plc, 2026-05-01 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube