Arista Networks: The Story of Cloud Networking's Disruptor

I. Introduction & Episode Roadmap

Picture this: It's 2014, and Cisco Systems, the $150 billion networking giant that had dominated enterprise infrastructure for three decades, watches as a six-year-old startup they'd dismissed as irrelevant rings the opening bell at the New York Stock Exchange. That startup, Arista Networks, would go on to capture over 20% of the data center switching market, power the AI revolution's infrastructure, and become the nightmare scenario that keeps Cisco executives awake at night.

Today, Arista Networks stands as a $7 billion revenue powerhouse, serving over 10,000 customers globally. But the real story isn't just about market share or financial metrics—it's about how a company founded by ex-Cisco employees decoded the industry playbook, rewrote it, and then had the audacity to beat the masters at their own game.

The provocative question at the heart of this story: How did three engineers in stealth mode create technology so threatening that Cisco would wage a five-year legal war trying to stop them? And more importantly, how did they position themselves perfectly for not one but two technology revolutions—first cloud computing, then artificial intelligence?

We'll trace Arista's journey from its secretive founding in 2004 through its emergence as the backbone of AI infrastructure in 2025. Along the way, we'll explore the David versus Goliath litigation that validated their disruption, the brilliant recruitment of a CEO who knew Cisco's every weakness, and the technical breakthrough that made one operating system more powerful than decades of legacy code.

This isn't just a story about switches and routers. It's about timing technology waves perfectly, the power of simplicity in complex systems, and why sometimes the best founders aren't young dropouts but industry veterans who've seen exactly what's broken and know how to fix it.

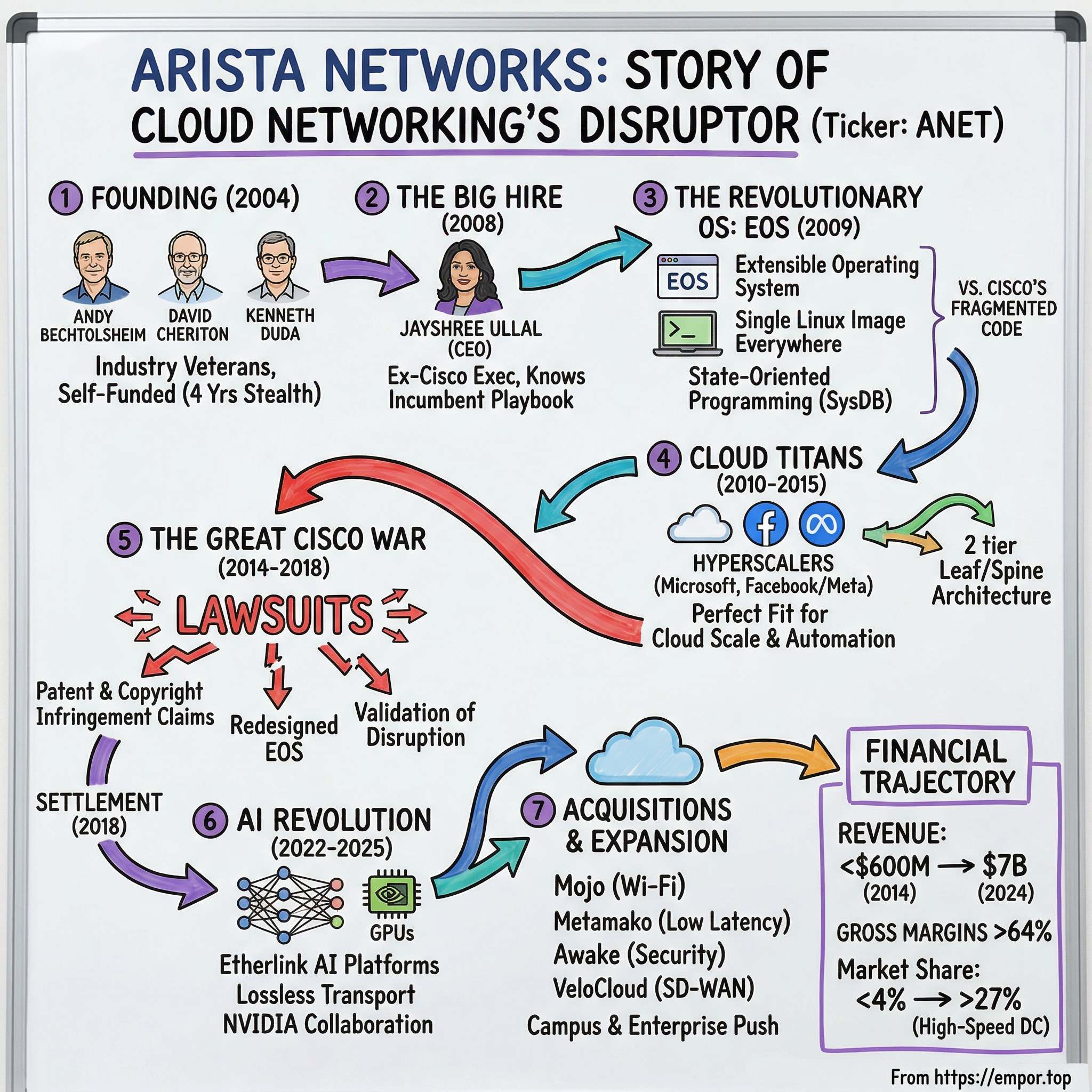

II. The Founding Story & Key Players

In 2004, while Mark Zuckerberg was launching Facebook from his Harvard dorm room, three technology veterans were quietly plotting a revolution in an unglamorous corner of Silicon Valley. They didn't call it Arista Networks yet—the company was originally registered as Arastra, a name they'd later change when they discovered it meant "weapons" in Sanskrit, not exactly the brand image they were seeking.

The founding trio reads like a who's who of Silicon Valley royalty. Andy Bechtolsheim, the technical visionary who had co-founded Sun Microsystems and famously wrote Google's first investment check for $100,000 before the company even existed, brought both engineering brilliance and an uncanny ability to spot transformative technologies. David Cheriton, a Stanford computer science professor who had sold his previous company, Granite Systems, to Cisco for $220 million in 1996, understood the networking industry's architecture—and its limitations—at a fundamental level. Kenneth Duda, the youngest of the three, was the technical architect who would translate their vision into code.

What made this founding team remarkable wasn't just their credentials but their financial independence. Bechtolsheim and Cheriton had accumulated enough wealth from previous ventures that they could fund Arista entirely themselves for the first four years. No venture capital politics, no quarterly board meetings demanding quick wins, no pressure to flip the company for a fast exit. This patient capital would prove crucial—they spent four years in complete stealth mode, telling almost no one what they were building.

"We wanted to build something fundamental," Bechtolsheim would later recall. "Not just another networking company, but a complete rethinking of how data center networks should work." They operated out of a nondescript office in Menlo Park, with no sign on the door, no website, no press releases. Engineers who joined during these stealth years had to sign NDAs before even learning the company's actual mission.

The stealth years from 2004 to 2008 were spent on a singular obsession: building a network operating system from scratch. While Cisco and other incumbents were patching decades-old code bases, adding feature upon feature to legacy systems, Arista's founders started with a blank slate. They asked fundamental questions: What if you designed a network operating system knowing what we know now about Linux, about cloud computing, about state management? What if you prioritized programmability and simplicity over feature bloat?

But brilliant technology alone doesn't disrupt entrenched incumbents. The founders knew they needed someone who understood not just technology but go-to-market strategy, enterprise sales, and most importantly, someone who knew exactly how the incumbent thought. In May 2008, that person became available.

Jayshree Ullal had spent fifteen years at Cisco, rising to become one of their most senior executives, responsible for $10 billion in revenue. She knew every Cisco playbook, every sales strategy, every product weakness. When she left Cisco in May 2008, ostensibly to "take a break," the networking industry was abuzz with speculation about where she'd land.

By October 2008, the speculation ended. Ullal was named CEO of the still-secretive Arista Networks. The hire was a masterstroke—not only did she bring instant credibility to an unknown startup, but she also brought intelligence about the incumbent that money couldn't buy. She knew which Cisco customers were frustrated, which products were vulnerable, and perhaps most importantly, she knew Cisco's institutional blind spots.

"When I first met Andy and David," Ullal would later say, "they showed me what they'd built in stealth. I immediately understood this wasn't just another networking company. They had fundamentally rethought the architecture for the cloud era, while everyone else was still building for the client-server world."

The timing was perfect. Cloud computing was just beginning its explosive growth phase. Amazon Web Services was only two years old. Facebook was scaling rapidly. Google was building data centers at an unprecedented pace. These companies needed networking infrastructure that traditional vendors, stuck in their enterprise mindsets, couldn't provide. And now Arista had both the technology and the leader to capitalize on this shift.

III. The Technology Revolution: EOS & Early Products

The year 2009 marked Arista's emergence from the shadows, and what they unveiled challenged everything the networking industry thought it knew about building switches. At the heart of their revelation was EOS—the Extensible Operating System—a single, Linux-based operating system that would run across every piece of hardware they would ever build.

To understand why EOS was revolutionary, you need to understand the mess it was designed to replace. Cisco's IOS (Internetwork Operating System) wasn't really one operating system—it was dozens of different code bases, each developed for specific hardware platforms, some dating back to the 1980s. A Cisco customer might have five different operating systems running across their network, each with different commands, different bugs, different update cycles. Network engineers spent years mastering the quirks of each variant, and enterprises spent millions on training and certification.

Arista's EOS took a radically different approach. Built on an unmodified Linux kernel, it provided a single binary image that could run on any Arista switch—from the smallest edge device to the largest spine switch in a hyperscale data center. But the real innovation wasn't just consistency; it was the architecture itself. EOS pioneered what Arista called "state-oriented programming," where every piece of configuration and operational data was stored in a central database called SysDB.

"Think of it like this," one early Arista engineer explained. "In traditional networking operating systems, if a process crashes, you might lose state, lose configuration, maybe even crash the entire switch. In EOS, if a process crashes, it just restarts and reads its state from SysDB. The switch keeps forwarding packets. Your network doesn't go down."

This architecture enabled something that seemed like magic to network engineers accustomed to planning maintenance windows weeks in advance: in-service software upgrades. You could upgrade EOS on a production switch without dropping a single packet. For companies running 24/7 operations—which by 2009 was essentially everyone—this was transformative.

The first product to showcase EOS was the 7100 Series, announced in September 2009. On paper, it looked like just another 10 Gigabit Ethernet switch. But the details revealed Arista's philosophy: wire-speed performance on every port, ultra-low latency (under 600 nanoseconds), and deep packet buffers that could handle the bursty traffic patterns common in cloud environments. These weren't switches designed for the predictable traffic patterns of enterprise email and file servers; they were built for the chaotic, massive scale of cloud computing.

Early customers were a who's who of web-scale companies—though Arista couldn't name them publicly due to NDAs. These companies were building data centers unlike anything the enterprise world had seen: thousands of servers running distributed applications, massive east-west traffic patterns, and a need for automation at scale. Traditional networking vendors would send armies of consultants to design custom solutions. Arista sent a few engineers with Python scripts.

The programmability of EOS became Arista's secret weapon. While Cisco's command-line interface required manual configuration of each switch, EOS exposed every function through APIs. Cloud companies could write scripts to automatically provision thousands of switches, implement custom routing protocols, or even modify the switch's behavior in real-time based on application demands. For companies like Facebook and Google, who thought of infrastructure as code, Arista was speaking their language.

The product philosophy that emerged in these early years would define Arista for the next decade: build the best hardware, run one operating system everywhere, make everything programmable, and keep it simple. While competitors added features to check boxes in RFPs, Arista focused on doing fewer things better. They didn't try to build switches for every use case—they built switches for the future of computing.

By 2010, just two years after emerging from stealth, Arista had captured 5% of the 10 Gigabit Ethernet switch market. For a company no one had heard of three years earlier, competing against entrenched players with decades of customer relationships, this was remarkable. But it was just the beginning. The cloud revolution was accelerating, and Arista had positioned itself perfectly to ride the wave.

What happened next would trigger one of the most brutal legal battles in technology history. Cisco had finally noticed that their former executive and her team of ex-Cisco engineers weren't just building another networking company—they were building an existential threat.

IV. The Great Cisco War (2014-2018)

June 5, 2014, should have been a day of pure celebration for Arista Networks. The company's initial public offering on the New York Stock Exchange, under the ticker symbol ANET, valued the company at $2.5 billion. Shares soared 28% on the first day of trading. Jayshree Ullal rang the opening bell, surrounded by employees who had spent a decade building toward this moment. But in San Jose, just thirty miles south, Cisco's legal team was preparing to rain on the parade.

Six months later, in December 2014, Cisco filed two separate lawsuits that would consume both companies for the next four years. The accusations were explosive: patent infringement, copyright infringement, and most dramatically, the allegation that Arista had systematically stolen Cisco's intellectual property. Cisco claimed that Arista's success wasn't due to innovation but to wholesale copying of features, commands, and even error messages from Cisco's IOS.

"They didn't just compete with us," one Cisco executive told the press. "They photocopied our homework and claimed it was their own."

The legal documents revealed the deeply personal nature of the conflict. Cisco didn't just sue Arista as a company—they named eleven former Cisco employees who had joined Arista, claiming these individuals had violated their employment agreements and taken proprietary knowledge with them. The lawsuit painted a picture of corporate espionage: engineers downloading source code before leaving, sales executives taking customer lists, product managers carrying away roadmaps.

But the most incendiary allegation was about EOS itself. Cisco's lawyers had done something clever—they'd run Arista's command-line interface and compared it, keystroke by keystroke, to Cisco's IOS. They found hundreds of identical commands, similar syntax, even matching error messages. To Cisco, this was proof of blatant copying. To Arista, it was something entirely different.

Arista's legal response was swift and fierce. Yes, they acknowledged, EOS used some similar commands to IOS—because those commands had become industry standards over decades. It would be like suing a car manufacturer for putting the gas pedal on the right and brake on the left. Network engineers had trained for years on Cisco's syntax; creating an entirely different command structure would be user-hostile and commercially suicidal.

Moreover, Arista counter-sued, alleging that Cisco was abusing its monopoly position to stifle competition. They pointed to Cisco's 70% market share in switching, their history of acquiring potential competitors, and now their attempt to use the legal system to destroy the one company that had successfully challenged their dominance. The counter-suit sought damages and an injunction preventing Cisco from using litigation as an anti-competitive weapon.

The legal battle played out across multiple venues—federal court in California, the International Trade Commission in Washington, and the Patent Trial and Appeal Board. Each venue became a theater for corporate warfare. In one memorable deposition, Cisco's lawyers grilled Andy Bechtolsheim for eight hours about the origins of specific EOS features. In another, they presented side-by-side code comparisons that filled hundreds of pages.

The turning points came in rapid succession through 2016. First, the U.S. International Trade Commission ruled that Arista had indeed infringed on three Cisco patents, potentially blocking Arista from importing its switches (which were manufactured in Asia) into the United States. Arista's stock plummeted 24% in after-hours trading. But weeks later, a federal jury delivered a shocking verdict: despite finding that Arista had used some Cisco commands, they awarded Cisco zero dollars in damages, determining that the copying wasn't substantial enough to warrant compensation.

Behind the scenes, both companies were hemorrhaging money on legal fees—industry insiders estimated each side was spending over $100 million on lawyers. More importantly, the uncertainty was affecting business. Some customers delayed purchases, worried about injunctions. Engineers on both sides were spending more time with lawyers than writing code. The lawsuit had become a distraction from the real battle in the marketplace.

In August 2018, both sides finally agreed to settle. The terms were revealing: Arista would pay Cisco $400 million—a substantial sum, but far less than the billions Cisco had initially sought. More importantly, both companies agreed to drop all litigation against each other for at least five years. No admission of guilt, no licensing agreements, just a cessation of hostilities.

The settlement's timing was significant. By 2018, the market had rendered its own verdict. Arista's revenue had grown to $2.2 billion, up from $361 million when Cisco first sued. Their market share in 100 Gigabit Ethernet switching had reached 25%. Major customers like Microsoft and Facebook had publicly endorsed Arista's technology. The lawsuit, rather than destroying Arista, had legitimized them. As one industry analyst noted, "You don't spend four years and hundreds of millions of dollars suing a company that isn't a threat."

The war with Cisco had taught Arista valuable lessons. They redesigned portions of EOS to remove any shadow of Cisco's influence. They invested heavily in their own patent portfolio. Most importantly, they'd proven they could survive an existential threat from one of technology's most powerful companies. Now, with the legal cloud lifted, they could focus on what they did best: building products for the future of computing.

V. Cloud Titans & The Hyperscale Opportunity

While Arista and Cisco were battling in courtrooms, a fundamental shift was reshaping the entire technology landscape. The world's compute infrastructure was migrating from corporate data centers to massive cloud facilities run by a handful of hyperscale operators. By 2015, companies like Amazon, Microsoft, Google, and Facebook were each spending billions annually on data center infrastructure, and their requirements were unlike anything the networking industry had seen before.

Consider Facebook's challenge in 2015: they were adding 500 million new users while simultaneously transitioning from text and photos to video streaming. Their data centers needed to handle not just more traffic but fundamentally different traffic patterns. Traditional enterprise networks were designed for "north-south" traffic—users accessing servers. But Facebook's architecture required massive "east-west" traffic—servers talking to servers, databases replicating across regions, machine learning jobs spreading across thousands of GPUs.

"We needed switches that could handle 100 Gigabit Ethernet at scale, with consistent latency and massive buffers," explained one Facebook network architect. "Cisco would show up with their enterprise-focused boxes and complex licensing schemes. Arista understood that we needed simplicity at scale. "The relationship between Arista and the hyperscale giants wasn't just vendor-customer; it was a true partnership. Facebook engineering teams collaborated with Arista for over a year on system-level requirements, with parallel development efforts ensuring full manageability via FBOSS (Facebook Open Switching Software) controlling the system. This collaboration model was revolutionary—instead of vendors dictating product roadmaps, cloud providers were co-designing the hardware they needed.

The numbers told the story of this shift. Between 2014 and 2018, Arista's revenue from cloud titans grew from 25% to over 40% of total sales. Microsoft Azure had deployed Arista switches throughout their global infrastructure. Arista initiated similar developments with Microsoft and SONIC (Software for Open Networking in the Cloud) in building the Azure cloud network since 2016.

What made Arista perfect for hyperscalers wasn't just raw performance—it was philosophy alignment. These companies thought about infrastructure as software. They wanted to automate everything, customize anything, and operate at a scale where human intervention was impossible. Arista's EOS, with its Linux foundation and comprehensive APIs, spoke their language in a way that Cisco's enterprise-focused systems never could.

The virtuous cycle that emerged was powerful: cloud growth drove demand for higher-speed networking, which drove Arista's R&D investment, which produced better products, which enabled cloud providers to scale further. When the industry moved from 10 Gigabit to 40 Gigabit Ethernet, Arista was ready. When 100 Gigabit became the standard, Arista led the transition. By 2018, they were already shipping 400 Gigabit switches while competitors were still talking about roadmaps.

The hyperscale opportunity also transformed Arista's business model. Unlike enterprise customers who bought switches in small quantities with complex configurations, cloud titans bought thousands of identical switches with standardized configurations. This meant lower sales costs, simplified support, and the ability to focus engineering resources on performance rather than features. Gross margins actually improved as volume increased—a rare feat in hardware businesses.

But perhaps the most important aspect of the hyperscale pivot was timing. Arista had positioned themselves perfectly for the next wave of computing infrastructure: artificial intelligence. The same customers who had built massive cloud infrastructure were now building even larger AI training clusters, and they needed networking that could keep up with thousands of GPUs exchanging parameters at unprecedented speeds.

VI. The AI Revolution & Networking for the Future

In 2022, ChatGPT exploded into public consciousness, but inside the data centers of Meta, Google, and Microsoft, the AI revolution had been building for years. Training large language models required connecting thousands of GPUs in configurations that made traditional networking architectures obsolete. A single training run for GPT-4 reportedly cost over $100 million, with much of that expense going toward the infrastructure required to keep thousands of chips synchronized. For Arista, this wasn't just another market opportunity—it was validation of every architectural decision they'd made since 2004.

The challenge of AI networking is fundamentally different from traditional cloud computing. When you're serving web pages or streaming video, latency measured in milliseconds is acceptable. But when you're training a neural network across thousands of GPUs, every microsecond of delay compounds into hours of additional training time and millions in extra costs. The network needs to be not just fast but deterministically fast—consistent latency matters more than average latency. Arista's approach to AI networking centered on their Etherlink platforms, which were specifically designed for the unique demands of AI workloads. Meta deployed the Arista 7700R4 Distributed Etherlink Switch (DES) for its latest Ethernet-based AI cluster, a validation of Arista's technical approach from one of the world's most sophisticated AI operators.

The 7700R4 DES represented a fundamental rethinking of network architecture for AI. While it may physically look and be cabled like a two-tier leaf/spine network, DES provides single-hop forwarding with a highly efficient fabric spine layer that is a standalone, autonomous system with local forwarding lookups and independent path selection decisions. The 7700R4 behaves like a single system, with dedicated deep buffers to ensure system-wide lossless transport across the entire Ethernet-based AI network.

This architecture mattered because AI training workloads are fundamentally different from traditional computing. When thousands of GPUs are working on a single model, they need to synchronize constantly—exchanging gradients, updating parameters, checkpointing progress. Any packet loss means retransmission, which in a synchronized system means every GPU waits for the slowest one. Arista's lossless transport and deep buffers ensured that even under maximum load, packets wouldn't be dropped.

The financial impact of the AI revolution on Arista has been dramatic. The company reported revenue of $2.205 billion for Q2 2025, representing a 30.4% year-over-year increase. More importantly, Cloud titans—what are called the hyperscalers and cloud builders—represented 48 percent of Arista's sales in 2024, up 33.4 percent, significantly faster than the overall growth of the company.

But Arista wasn't just riding the AI wave—they were helping to shape it. In collaboration with NVIDIA, Arista showcased its Arista EOS AI Agent, designed to align compute and network domains as a single-managed AI entity and thus help lower job completion times. This wasn't just about faster switches; it was about intelligent networking that could adapt to AI workload patterns in real-time.

The scale of AI clusters continued to expand beyond what anyone had imagined. Arista's Etherlink AI platforms support AI cluster sizes ranging from thousands to hundreds of thousands of XPUs with highly efficient one- and two-tier network topologies. For context, the largest supercomputers of the previous decade had thousands of processors; AI clusters were now scaling to hundreds of thousands.

The competition with InfiniBand, the traditional high-performance computing interconnect, became a critical battleground. InfiniBand, primarily championed by NVIDIA through their Mellanox acquisition, had advantages in latency and was purpose-built for HPC workloads. But Ethernet had ecosystem advantages—it was an open standard, had multiple vendors, and perhaps most importantly, it was what cloud providers already knew how to operate at scale.

Arista's bet was that Ethernet, enhanced with the right features for AI workloads, would win due to its flexibility and economics. The Ultra Ethernet Consortium, which Arista helped found, was working to standardize these enhancements across the industry. Early customer decisions suggested this bet was paying off—major AI deployments at Meta, Microsoft, and others were choosing Ethernet over InfiniBand.

Looking forward, the AI opportunity for Arista appears to be just beginning. Arista is targeting significant growth in AI networking, with plans to generate over $1.5 billion from AI-related solutions in 2025, including $750 million from AI backend solutions specifically. With AI clusters continuing to scale and new use cases emerging in inference and edge AI, the demand for high-performance, programmable networking shows no signs of slowing.

VII. Acquisitions & Expansion Strategy

While Cisco had built its empire through serial acquisitions—over 200 companies acquired in its history—Arista had taken a remarkably different path. For the first decade of its existence, the company grew entirely organically, preferring to build rather than buy. But by 2018, with the core data center switching business established and generating substantial cash flow, Arista began selective acquisitions to expand into adjacent markets. The first two acquisitions came in quick succession during the summer of 2018. In August, Arista acquired Mojo Networks for its Cognitive Wi-Fi technology, marking Arista's entry into the wireless networking market. Just weeks later, in September, they acquired Metamako, an Australian company specializing in ultra-low latency, FPGA-enabled network solutions for financial services. The combined purchase price for the acquisition of Mojo Networks, Inc. and Metamako Holding PTY LTD for approximately $117.4 million, which consisted of $101.8 million in cash and $15.6 million for the fair value of 58,072 shares of our common stock issued.

These acquisitions revealed Arista's strategic thinking. Mojo Networks brought them into the campus networking market—a massive opportunity where Cisco had long dominated. Earlier this year, Arista announced cognitive cloud networking, designed to address transitional changes as enterprises move to IoT (Internet of things) ready campuses. Designed to bring operational consistency and modern cloud principles to the enterprise campus, Arista extends this architecture with the addition of Mojo Networks by providing secure, high performance cognitive Wi-Fi at cloud scale.

Metamako, on the other hand, served a completely different purpose. The financial services industry, particularly high-frequency trading firms, needed networking with latencies measured in nanoseconds, not microseconds. Layer 1 switching enables mirroring and software-defined port routing with port-to-port latency starting from 4ns, depending on physical distance. The E and L variants allow running custom FPGA applications directly on the switch with a port-to-FPGA latency as low as 3ns. This wasn't about scale; it was about speed at the absolute physical limits of what's possible. The pace of acquisitions accelerated in 2020, revealing Arista's expanding ambitions. In February, they acquired Big Switch Networks, a network monitoring and SDN (Software Defined Networking) pioneer. Big Switch Networks was recognized as a Visionary in Gartner's Magic Quadrant for Data Center Networking for the third time. Additionally, Big Switch won the best of VMworld for Networking in 2019. This wasn't about entering a new market—it was about deepening capabilities in network observability, crucial for managing increasingly complex cloud environments.

Eight months later, in October 2020, came the Awake Security acquisition. Arista Networks, Inc. completed the acquisition of Awake Security, Inc. for approximately $180 million. Awake brought AI-driven network detection and response capabilities, addressing the growing security challenges in distributed networks. The Awake platform is recognized for bringing great value with outstanding ROI between features and cost within the NDR market and ranked #1 by Enterprise Management Associates (EMA). Awake is also widely acknowledged for NDR technical leadership by many, including Emerging Technology Research, IT Central Station and Frost & Sullivan. In 2019, Awake received Frost & Sullivan's Visionary Innovation Leadership Award for its innovation, high customer satisfaction and overall performance. In 2022, the acquisition pace continued with two strategic deals. First came Untangle, a security asset for edge threat management that would be integrated into Arista's Cognitive Unified Edge (CUE) commercial and branch offering. Then in August, Arista acquired Pluribus Networks, a pioneer in unified cloud fabric networking, for integration into Arista's Unified Cloud Fabric (UCF). Together with Untangle, Arista paid $150 million for both companies, adding approximately 150 employees to the team.

Pluribus was particularly strategic as it brought relationships with telecommunications providers, especially through its partnership with Ericsson. "Ericsson has been partnering with Pluribus Networks for the unified cloud network fabric of the Ericsson NFVI solution since 2016. Together we have built a telco-grade networking fabric solution used in NFVI deployments. The acquisition of Pluribus by Arista Networks will further the Ericsson partnership with Arista Networks and benefit our joint customers deploying Ericsson's NFVI solutions through Arista and Ericsson's combined networking expertise," said Lars Martensson, Head of Solutions Area Cloud and NFVi at Ericsson AB.The most recent acquisition, announced in July 2025, represents Arista's boldest expansion move yet. In conjunction, Arista acquired the VeloCloud SD-WAN portfolio from Broadcom. VeloCloud had been a pioneering SD-WAN company founded in 2012, acquired by VMware in 2017, and then became part of Broadcom when it bought VMware for $61 billion in 2023. The deal is an asset-plus-talent carve-out: Arista receives the intellectual property and roughly half of VeloCloud's ≈1,000 employees—primarily core engineering and technical staff—while most sales- and marketing-oriented roles were left behind.

Although neither party disclosed financial terms, multiple press accounts still place the consideration "well under" $1 billion, in line with the May 2025 reporting from The Information that first surfaced the transaction. The acquisition fills a critical gap in Arista's portfolio—SD-WAN capabilities that connect branch offices and remote sites to data centers and cloud resources. VeloCloud offers leading cloud-delivered SD-WAN solutions with integrated security, complementing Arista's wired and wireless switching portfolio. VeloCloud solutions comprise a range of edge hardware platforms featuring integrated secure firewalling and application-optimized SD-WAN, available with a choice of integrated Wi-Fi and/or 5G mobile connectivity. This portfolio of solutions provides expanded choice and performance for Arista customers, enabling global WAN services to interconnect data centers and distributed campus offices, while complementing Arista's existing CloudEOS routing stack and high-end 7000-series WAN routers.

What's remarkable about Arista's acquisition strategy is its discipline and focus. Unlike Cisco's scattershot approach of buying companies across dozens of different markets, every Arista acquisition has been carefully chosen to extend their networking platform into adjacent areas while maintaining architectural consistency. They're not trying to become everything to everyone—they're methodically building a complete networking solution for the cloud and AI era.

The campus and enterprise push, enabled by these acquisitions, represents a significant strategic shift. Arista is no longer content to dominate just the data center; they're going after Cisco's core enterprise business. With wireless from Mojo, security from Awake and Untangle, SD-WAN from VeloCloud, and their core switching expertise, they now have a complete enterprise networking portfolio. The cognitive networking vision—using AI and automation to manage increasingly complex networks—ties it all together.

VIII. Financial Performance & Business Model

The numbers tell a story of remarkable consistency in an industry known for volatility. Revenue of $7.003 billion, an increase of 19.5% compared to fiscal year 2023. But the headline revenue figure only hints at the underlying business model that has made Arista one of the most profitable companies in technology.

Start with gross margins—the most fundamental measure of a hardware company's pricing power and operational efficiency. GAAP gross margin of 64.1%, compared to GAAP gross margin of 61.9% in fiscal year 2023. Non-GAAP gross margin of 64.6%, compared to non-GAAP gross margin of 62.6% in fiscal year 2023. These aren't software margins, but for a company selling physical switches and routers, they're extraordinary. Cisco, by comparison, typically operates with gross margins in the low 60s. The difference? Arista's products command premium prices because customers perceive genuine differentiation.

The revenue trajectory from startup to powerhouse is even more impressive when viewed over the decade since IPO. In 2014, Arista's first year as a public company, revenue was $584 million. By 2024, that had grown to $7 billion—a twelve-fold increase. But unlike many high-growth companies that sacrifice profitability for growth, Arista has been profitable every single year as a public company.

Arista reported robust financial results for the first quarter of 2025, with revenue reaching $2.005 billion, representing a 27.6% increase compared to Q1 2024. The company achieved a non-GAAP gross margin of 64.1% and an operating margin of 47.8%, demonstrating strong profitability despite ongoing investments in growth initiatives. The company's earnings per share reached $0.65, a 30% increase year-over-year, exceeding analyst expectations of $0.59. This performance reflects Arista's ability to maintain operational efficiency while expanding its market presence.

The concentration risk that bears constantly cite is real but evolving. Ullal thinks Microsoft and Meta Platforms will each comprise more than 10 percent of the company's revenues in 2025 (which means the precise percentage has to be provided per rules of the US Securities and Exchange Commission). Having two customers represent such a significant portion of revenue would terrify most companies. But these aren't ordinary customers—they're building the infrastructure for the AI revolution, and their capital expenditure budgets are measured in tens of billions annually.

The financial model's real genius lies in its operating leverage. R&D spending has remained remarkably consistent at around 20% of revenue—high enough to drive innovation but disciplined enough to ensure profitability. Sales and marketing expenses are unusually low for an enterprise technology company, typically around 10-12% of revenue. Compare that to enterprise software companies that routinely spend 40-50% of revenue on sales and marketing.

Why can Arista spend so much less on sales? Product differentiation. When your switches are demonstrably better—lower latency, higher reliability, easier to manage—customers come to you. The company doesn't need an army of salespeople because the products largely sell themselves to sophisticated buyers who understand the technical advantages.

Capital allocation has been similarly disciplined. In Q1 2025, we also completed the highest level of stock repurchases in Arista's history, quarterly or annually, at $787M, reflecting our strong conviction in the long-term value of the business. The company generates enormous cash flow—operating cash flow grew 95% year-over-year in Q4 2024—and returns much of it to shareholders through buybacks rather than dividends, a tax-efficient approach that also signals management's confidence in the business.

Stock performance has reflected this operational excellence. Shares have increased more than four-fold since the 2014 IPO, significantly outperforming both the broader market and most technology peers. The stock trades at a premium valuation—often 30-40 times earnings—but investors have been willing to pay up for the combination of growth, profitability, and strategic positioning in secular growth markets.

The business model's sustainability depends on continued innovation and market expansion. Looking ahead, Arista provided guidance for Q2 2025, projecting revenue of approximately $2.1 billion with a non-GAAP gross margin of around 63% and operating margin of approximately 46%. For the full fiscal year 2025, the company targets revenue growth of approximately 17%, with gross margins in the 60-62% range and operating margins between 43-44%. These projections reflect a continued focus on balancing growth with profitability.

What's perhaps most impressive is that Arista has achieved all this while remaining capital-light. They don't own factories—their products are manufactured by contract manufacturers in Asia. They don't carry massive inventory—their supply chain is optimized for just-in-time delivery. They don't have enormous real estate footprints—their headquarters is modest by Silicon Valley standards. Every dollar of capital is deployed efficiently, resulting in returns on invested capital that consistently exceed 30%.

IX. Playbook: Business & Investing Lessons

Lesson 1: Sometimes the best founders are industry veterans who see what's broken

The conventional Silicon Valley wisdom says revolutionary companies are started by twenty-something dropouts who don't know what's impossible. Arista's founders averaged over fifty years old when they started the company. They had collectively spent decades building networking companies, understanding every architectural decision, every customer pain point, every vendor lock-in strategy. They didn't stumble upon a problem to solve—they had been watching it develop for twenty years.

Andy Bechtolsheim had co-founded Sun Microsystems and designed the workstations that powered the early internet. He knew that data center architectures were fundamentally changing. David Cheriton had sold Granite Systems to Cisco and watched from the inside as Cisco's innovation slowed under the weight of its own success. They didn't need to "discover" product-market fit through iteration—they knew exactly what to build before writing a single line of code.

Lesson 2: One great product can be a platform for everything

EOS wasn't just an operating system—it was a philosophy encoded in software. By building one OS that could run on any hardware, scale from the smallest to largest switches, and be programmed through standard APIs, Arista created a platform that could evolve with customer needs without fundamental rewrites.

Cisco, by contrast, had dozens of operating systems, each with its own quirks, bugs, and command structures. This wasn't just a technical burden—it was a business model constraint. Every new product line meant new training, new certifications, new support structures. Arista's "one OS to rule them all" approach meant that every improvement benefited every customer, every feature worked everywhere, and every engineer only needed to learn one system.

Lesson 3: Litigation as validation of disruption

When Cisco sued Arista in 2014, it seemed like an existential threat. A $150 billion giant with unlimited legal resources versus a six-year-old startup. But the lawsuit actually validated Arista's strategy in the most powerful way possible. You don't spend four years and hundreds of millions of dollars in legal fees trying to stop a company that isn't a threat.

The litigation also forced Arista to innovate further. They rewrote portions of EOS to remove any hint of Cisco influence. They built their own patent portfolio. They created clear documentation of their development process. By the time the lawsuit settled, Arista had emerged stronger, with cleaner IP and a reputation as the company that Cisco feared.

Lesson 4: Focus on the future not the past

While Cisco was protecting its enterprise installed base, Arista was building for cloud scale. While Juniper was optimizing for telecommunications carriers, Arista was designing for hyperscale data centers. While everyone else was fighting over the present, Arista was building for the future.

This forward focus influenced every decision. They didn't build products for traditional three-tier enterprise architectures because they believed leaf-spine would dominate. They didn't optimize for north-south traffic because they saw that east-west would explode. They didn't chase every RFP because they knew that a handful of cloud titans would drive the majority of future demand.

Lesson 5: High gross margins come from genuine differentiation

Arista's 64% gross margins in a hardware business aren't the result of financial engineering or accounting tricks. They're the result of building products that customers value significantly above their cost to produce. When Meta needs switches that won't drop packets during a trillion-dollar AI training run, they don't negotiate on price—they negotiate on delivery time.

This differentiation compounds over time. Higher margins mean more R&D investment, which creates better products, which command higher margins. It's a virtuous cycle that's extremely difficult for competitors to break once established.

Capital efficiency: Self-funded early, profitable growth

Bechtolsheim and Cheriton funding Arista themselves wasn't just about maintaining control—it was about patient capital. Venture capital would have pushed for quick growth, fast exits, or pivots when things got difficult. By funding it themselves, the founders could spend four years in stealth, perfecting the product without market pressure.

Even after going public, Arista has remained remarkably capital-efficient. They've made strategic acquisitions but never bet-the-company deals. They've returned cash to shareholders but maintained a fortress balance sheet. They've invested in R&D but always within the constraint of profitability.

The power of riding technology waves

Arista didn't create the cloud computing wave or the AI revolution—they positioned themselves perfectly to benefit from both. When they started in 2004, cloud computing barely existed. By the time they emerged from stealth in 2008, AWS was taking off. When they went public in 2014, every enterprise was talking about cloud migration. When AI exploded in 2022, they had already spent years building relationships with every company training large models.

This wasn't luck—it was strategic positioning based on deep understanding of technology trends. The founders had seen multiple technology waves in their careers and understood that the companies that win aren't always the ones that create the wave but often the ones that ride it best.

X. Bear vs. Bull Case & Competitive Analysis

Bull Case: The AI Infrastructure Kingmaker

The bulls see Arista as perfectly positioned for the next decade of infrastructure build-out. Start with the AI opportunity: training and running large language models requires networking infrastructure unlike anything built before. We're talking about clusters with hundreds of thousands of GPUs, each needing to communicate with minimal latency and zero packet loss. Arista's longer-term goals include achieving $8.2 billion in revenue for 2025, with specific targets of approximately $750 million each for campus networking and AI back-end solutions.

The technical moat is real and widening. Building networking equipment for AI isn't just about fast speeds—it's about consistency, programmability, and scale. Arista's single-OS architecture means they can optimize across their entire stack in ways that competitors with fragmented systems cannot. When milliseconds of latency translate to millions in additional training costs, Arista's technical advantages become insurmountable.

Market share gains continue to accelerate. In the high-speed data center switching market, Arista has steadily increased its share from just 3.5% in 2012 to 27.5% in 2024 in terms of revenue, while Cisco's share has declined from 78.1% to 29.9% during the same period. This isn't just taking share in a growing market—it's fundamentally displacing an entrenched incumbent.

The customer relationships are perhaps the strongest moat. When you're the primary networking vendor for Meta, Microsoft, and other cloud titans, you're not just a vendor—you're a partner in building infrastructure that doesn't exist anywhere else. These relationships compound over time, creating switching costs that go beyond technology to include trust, expertise, and co-development.

Bear Case: Concentration Risk and Commoditization Threats

The bears point to uncomfortable realities. Customer concentration remains extreme, with two customers representing over 20% of revenue. If Microsoft or Meta decided to build their own switches—as Amazon has done with Nitro—Arista's revenue could crater overnight. The company argues that their technology is too complex to replicate, but history is littered with technology companies that thought they were irreplaceable.

The white box threat looms larger as merchant silicon improves. Broadcom's Tomahawk and Trident chips—which Arista themselves use—are available to anyone. If the hardware becomes commoditized and the value shifts entirely to software, Arista's margins could compress dramatically. Open-source network operating systems like SONiC (ironically started by Microsoft) could theoretically provide "good enough" functionality for basic use cases.

Cisco's renewed competitiveness under Chuck Robbins can't be ignored. They've modernized their product line, embraced software-defined networking, and still have relationships with virtually every enterprise IT department on the planet. Cisco's Silicon One chips, designed in-house, could potentially break Arista's performance advantages. With 10 times Arista's R&D budget, Cisco has the resources to catch up if they execute properly.

Geopolitical and supply chain risks are material. Arista manufactures primarily in Asia, making them vulnerable to trade wars, tariffs, and supply disruptions. The advanced chips they depend on come from a handful of suppliers, any of which could face constraints. In a world where semiconductor supply chains have become national security issues, Arista's asset-light model could become a liability.

Competitive Landscape Deep Dive

versus Cisco: The incumbent's dilemma personified. Cisco still has 45% overall market share in Ethernet switching, but they're losing the high-growth, high-margin segments to Arista. Their attempt to defend everywhere—enterprise, data center, campus, carrier—means they can't focus anywhere. The IOS-XR versus NX-OS versus IOS-XE fragmentation remains a fundamental disadvantage. However, Cisco's annual R&D budget of $7 billion dwarfs Arista's $1.4 billion, and they're investing heavily in Silicon One, their custom chip architecture.

versus Juniper: Now part of HPE after a $14 billion acquisition, Juniper represents a different threat. They've always been strong in service provider routing, and their QFX switches compete directly with Arista in data centers. The HPE acquisition could provide the scale and enterprise relationships Juniper lacked. However, integration challenges and cultural differences could also distract them for years.

versus White Box/ODMs: Companies like Accton and Quanta manufacture switches that run open-source network operating systems. For hyperscalers with massive engineering teams, building their own network stack on white box hardware could theoretically save money. But the hidden costs—development, support, integration—often exceed the savings. Still, this threat caps how much Arista can charge their largest customers.

versus InfiniBand (NVIDIA): The most interesting competitive dynamic. For AI training clusters, NVIDIA's InfiniBand has technical advantages—lower latency, better congestion control, purpose-built for HPC workloads. NVIDIA bundles InfiniBand with their GPUs, creating a powerful ecosystem lock-in. But Ethernet has the ecosystem advantage—more vendors, more options, better understood by network engineers. The Ultra Ethernet Consortium, which Arista helped found, is working to close the technical gaps. This battle will determine tens of billions in infrastructure spending over the next decade.

The competitive analysis reveals an interesting paradox: Arista's greatest threats come not from traditional competitors but from their own customers (who might build their own solutions) and their suppliers (who enable competitors). It's a delicate balance that requires constant innovation, relationship management, and strategic positioning.

XI. Recent News

The momentum heading into late 2025 shows no signs of slowing. "As we enter 2025, AI, cloud, and enterprise customers continue to drive network transformation. We surpassed $2B in revenue for the first time in Q1 2025 despite the unknowns around tariffs," stated Jayshree Ullal, Chairperson and CEO of Arista Networks. "Arista's trifecta of innovation, growth, and profitability is reflected in our results."

The latest product announcements reinforce Arista's AI focus. Arista Unveils Etherlink AI Networking Platforms – Arista announced the Etherlink AI platforms, which support AI cluster sizes ranging from thousands to hundreds of thousands of XPUs with highly efficient one- and two-tier network topologies, offering superior application performance compared to multi-tier networks. Arista Delivers Holistic AI Solutions in Collaboration with NVIDIA – Arista, in collaboration with NVIDIA, showcased its Arista EOS AI Agent, designed to align compute and network domains as a single-managed AI entity and thus help lower job completion times.

Customer wins continue to validate the strategy. Oracle, which is a hardware partner in OpenAI's Project Stargate AI cluster buildout, is now among its cloud titan customers, as is Apple now, too. They are not yet 10 percenters, however. The addition of Oracle and Apple to the customer roster shows that Arista's reach extends beyond the traditional hyperscalers to any company serious about AI infrastructure.

Arista's growth strategy focuses on expanding its total addressable market (TAM) from $41 billion in 2024 to $70 billion by 2028. This expansion is driven by the company's push beyond its core data center business into adjacent markets including campus networking, routing, and software services. The company has made strategic moves to strengthen its portfolio, including the acquisition of Broadcom's VeloCloud SD-WAN portfolio, which enhances Arista's enterprise networking capabilities. Additionally, Arista has expanded its AI-driven campus and branch networking offerings with new switching products and Wi-Fi 7 access points.

Market dynamics continue to favor Arista's positioning. The shift from traditional networking to AI-optimized infrastructure is accelerating. Enterprise customers are increasingly looking for vendors who can provide both campus and data center solutions. The consolidation in the networking industry—HPE acquiring Juniper, Broadcom acquiring VMware—creates opportunities for Arista to position itself as the independent alternative.

Analyst coverage remains broadly positive, with most maintaining buy ratings despite the stock's premium valuation. The consistent theme is that Arista's positioning in AI infrastructure justifies multiple expansion beyond traditional networking comparables. Some analysts have raised concerns about the sustainability of cloud titan spending, but Q1 2025 results suggest demand remains robust.

XII. Links & Resources

For those wanting to dive deeper into the Arista story, the company's investor relations materials provide comprehensive financial and strategic information. The quarterly earnings calls, transcribed and available on the investor site, offer unfiltered insights from leadership about strategy, competition, and market dynamics.

Technical deep dives on EOS are available through Arista's extensive documentation portal. The EOS Central community provides real-world implementation examples, best practices, and peer support. For those interested in the architectural philosophy, the original white papers on state-oriented programming and single-image architecture remain relevant.

The court documents from the Cisco litigation, available through PACER and various legal databases, provide a fascinating window into the competitive dynamics and technical differentiation between the companies. The patent filings and responses detail specific technical innovations and their importance.

Industry reports from Dell'Oro Group, IDC, and Gartner track market share shifts and technology adoption trends. The Ultra Ethernet Consortium's technical specifications show where the industry is heading for AI networking. The Open Compute Project, where Arista has been active, documents the co-development with hyperscale customers.

For broader context, "The Innovator's Dilemma" by Clayton Christensen perfectly describes Cisco's challenge in responding to Arista. "High Output Management" by Andy Grove explains the operational excellence that Arista embodies. The computer history museum's oral histories with Andy Bechtolsheim provide background on one of Silicon Valley's most successful technical entrepreneurs.

The story of Arista Networks is far from over. As AI transforms from experiment to infrastructure, as enterprises modernize their networks, and as new use cases emerge that we can't yet imagine, Arista's combination of technical excellence, operational discipline, and strategic positioning suggests the next decade could be even more transformative than the last. For students of business strategy, technology history, or investment analysis, Arista provides a masterclass in building a sustainable advantage in a market dominated by giants.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube