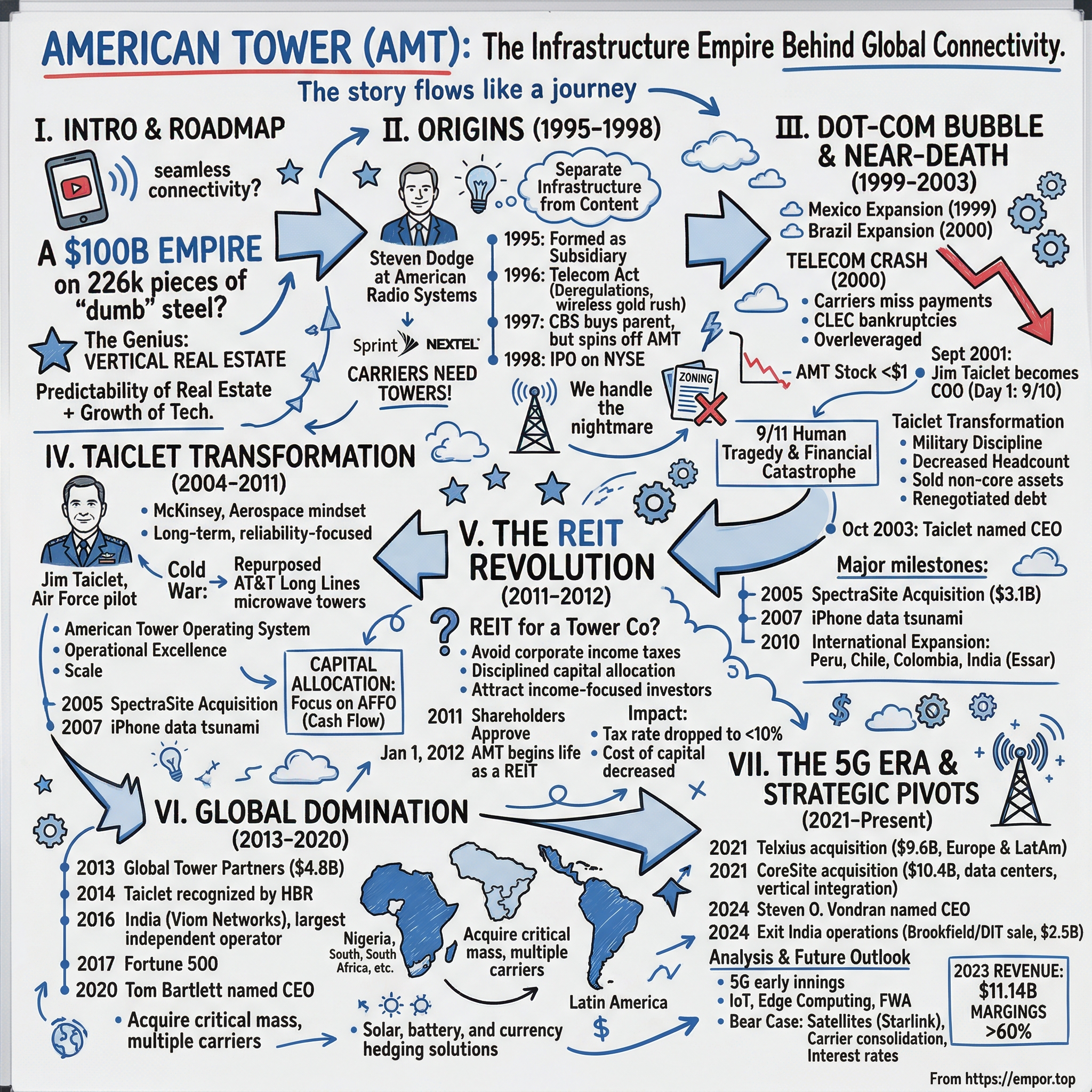

American Tower: The Infrastructure Empire Behind Global Connectivity

I. Introduction & Episode Roadmap

Picture this: You're scrolling through Instagram on your phone, streaming a video that loads instantly despite being in the middle of downtown Manhattan with millions of other users around you. That seamless connectivity? It doesn't happen by magic. Behind every swipe, every call, every byte of data flowing to your device stands a vast network of steel towers—and increasingly, one company owns the tower your signal is bouncing off of: American Tower Corporation.

Here's the counterintuitive truth that makes American Tower one of the most fascinating business stories of the past three decades: In an era where software supposedly eats the world and asset-light business models reign supreme, a company that owns 226,000 pieces of "dumb" steel and concrete infrastructure has built a $100 billion empire. American Tower generated $11.14 billion in revenue in 2023, boasts operating margins that would make most tech companies jealous, and has delivered returns that have crushed the market over the past two decades.

The genius of American Tower isn't in the towers themselves—it's in recognizing that in the digital age, the most valuable real estate isn't in Manhattan or Silicon Valley. It's the vertical real estate that enables our hyperconnected world. Every smartphone user, every IoT device, every autonomous vehicle depends on these towers, yet most people have never heard of the company that dominates this critical infrastructure layer.

What we're about to explore is how a small subsidiary of a Boston radio company, spun off at the worst possible time during the dot-com crash, transformed into one of the most powerful infrastructure monopolies on the planet. It's a story of near-death experiences, brilliant capital allocation, the unexpected benefits of boring businesses, and how sometimes the best technology investment is decidedly low-tech.

This is the story of how American Tower built an empire one tower at a time, why every major wireless carrier is essentially held hostage by their business model, and what happens when you combine the predictability of real estate with the growth of technology. Buckle up—we're climbing the tower.

II. Origins: The Radio Systems Spinoff (1995–1998)

The year was 1995, and Steven B. Dodge was running American Radio Systems, a Boston-based company that had been aggressively rolling up radio stations across the country. But Dodge saw something others missed: while everyone was focused on content and programming, the real bottleneck in the radio business was transmission infrastructure. Radio stations needed towers to broadcast their signals, and most were building their own—an incredibly capital-intensive and inefficient model.

Dodge's insight was elegantly simple: What if you could separate the infrastructure from the content? What if one company owned the towers and leased space to multiple broadcasters? It was the same mental model that had created fortunes in commercial real estate—you don't need to run the businesses in the building to profit from owning the building itself.

In 1995, Dodge formed American Tower as a subsidiary of American Radio Systems. The initial business model was focused on radio and television broadcast towers, but the timing couldn't have been more fortuitous. The Telecommunications Act of 1996 had just deregulated the telecom industry, and a gold rush was beginning. Suddenly, new wireless carriers were sprouting up everywhere, each needing thousands of cell sites to build their networks.

The cellular industry in the mid-1990s was chaos—beautiful, profitable chaos if you knew where to position yourself. Sprint PCS, Nextel, VoiceStream, and dozens of other carriers were racing to build nationwide networks. Each carrier faced the same problem: they needed towers everywhere, but building towers meant dealing with zoning boards, environmental reviews, and angry neighbors who didn't want 200-foot steel structures in their backyards. The permitting process alone could take 12-24 months per tower.

American Tower's pitch was compelling: "We'll handle the nightmare of getting towers built and approved. You just lease space on them." The carriers, desperate to accelerate their network buildouts, eagerly signed long-term leases. The economics were magical from day one—the first tenant might cover 60% of the tower's operating costs, the second tenant was pure profit, and by the third tenant, returns on invested capital were astronomical.

By 1997, American Radio Systems had attracted the attention of CBS, which acquired it for $2.6 billion. But CBS had no interest in the tower business—they wanted the radio stations. So in 1998, American Tower was spun off as an independent public company, listing on the NYSE under the ticker AMT. Steven Dodge would lead the newly independent company as CEO, with a clear mandate: build or buy as many towers as possible, as fast as possible.

The IPO raised $870 million, and American Tower went on an acquisition spree. They weren't just building new towers; they were buying existing ones from carriers who needed cash and wanted to focus on their core business of providing wireless service. The company's tower count grew from a few hundred to several thousand within months.

The market loved the story. Here was a picks-and-shovels play on the wireless revolution—American Tower didn't care whether AT&T or Sprint or Nextel won the wireless wars. They'd lease to everyone. The stock soared, and by late 1999, American Tower had a market cap approaching $20 billion. Dodge and his team were being hailed as visionaries who had discovered a new asset class.

But storm clouds were gathering. The telecom sector was becoming increasingly frothy, with companies taking on massive debt to fund network buildouts. American Tower itself was leveraging up aggressively to fund acquisitions, with debt-to-EBITDA ratios that would make a private equity firm blush. The company was betting everything on continued explosive growth in wireless demand.

As 1999 turned to 2000, that bet was about to be tested in ways no one could have imagined.

III. The Dot-Com Bubble & Near-Death Experience (1999–2003)

In early 1999, American Tower was flying high—literally and figuratively. The company had just closed on a transformative deal that seemed to validate their international ambitions: they launched operations in Mexico and became Mexico's largest independent tower operator with more than 3,000 sites. The Mexican expansion wasn't just about tower count; it represented a bold bet that the infrastructure playbook perfected in the U.S. could work globally.

The Mexico deal showcased American Tower's aggressive dealmaking style. In September 1999, they entered into an agreement with TV Azteca, one of Mexico's two broadcast television companies, loaning up to $120 million in exchange for annual net payments of approximately $13.9 million, plus the rights to all existing and future third-party revenue on approximately 200 broadcast towers. These weren't just any towers—they were strategically located throughout Mexico and covered approximately 95% of the population, including highly populated cities such as Mexico City, Monterrey, Guadalajara, Acapulco and Cancun

. The portfolio made them essentially the largest independent tower operator in Mexico overnight.

But 2000 marked both triumph and the beginning of disaster. American Tower launched operations in Brazil, pursuing their vision of becoming the dominant tower operator across the Americas. The expansion looked brilliant on paper—Latin American wireless penetration was still in single digits in many markets, compared to over 30% in the U.S. The growth potential seemed limitless.

Behind the scenes, however, the telecom industry was beginning to crack. The competitive local exchange carriers (CLECs) that had been building fiber networks with abandon started missing payments. NextWave, which had bid $4.7 billion for wireless spectrum, declared bankruptcy. WorldCom's accounting fraud was about to be exposed. The entire telecom sector was overleveraged, overbuilt, and over.

By mid-2000, American Tower's stock had fallen from its peak of nearly $60 to under $30. But the real pain was just beginning. The company had taken on billions in debt to fund acquisitions and international expansion, assuming that revenue growth would continue at 30-40% annually. When carrier capital expenditures suddenly stopped, American Tower found itself with massive fixed costs, declining revenues, and debt trading at distressed levels.

Then came September 10, 2001. Jim Taiclet was appointed President and Chief Operating Officer of American Tower Corporation in September 2001, taking over operational responsibilities from founder Steven Dodge. Taiclet's first day at the company was Sept. 10, 2001. He had spent months studying the company and industry, building rapport with Dodge, and preparing for the challenge of turning around a company in crisis.

The next day was 9/11, and everything changed. Tragically, American Tower lost 13 employees at the World Trade Center. The company had technicians and engineers working on rooftop antenna installations in the towers. The first job responsibility Taiclet had was to set up funds for their families and make sure that they got all of their benefits.

The human tragedy was compounded by financial catastrophe. The value of American Tower's stock plunged to less than a dollar per share. The company was burning through cash, violating debt covenants, and facing potential bankruptcy. Many of their customers—the CLECs and smaller wireless carriers—were themselves going bankrupt, leaving American Tower with empty towers and no rent.

Taiclet, a former U.S. Air Force pilot who had flown missions in the Gulf War, brought a military discipline to the crisis. American Tower decreased its headcount from 5,000 people in September 2001 to 1,000 people by the end of its recovery process. But in a move that would define the company's culture, when they sold non-core businesses, they took lower proceeds with the requirement that the buyer had to take on all the people and keep their jobs.

The company sold its construction services division, its components manufacturing business, and various other non-core assets. They renegotiated debt covenants with banks, convincing lenders that the tower business model was fundamentally sound even if the timing had been terrible. It was financial triage—stop the bleeding, stabilize the patient, then figure out how to heal.

By October 2003, Dodge stepped aside and American Tower Corporation announced its board of directors named James D. Taiclet Chief Executive Officer, succeeding Steven B. Dodge in the role. The company that Taiclet inherited was a shadow of its former self, but it was alive. The question now was whether it could thrive.

IV. The Taiclet Transformation: From Survival to Strategy (2004–2011)

Jim Taiclet's background seemed almost tailor-made for American Tower's situation. He began his career as a U.S. Air Force officer and pilot and served in the Gulf War. He holds a Masters Degree in Public Affairs from Princeton University and is a Distinguished Graduate of the United States Air Force Academy. After leaving the military, he had worked at McKinsey & Company specializing in telecommunications and aerospace strategy, then held senior positions at Pratt & Whitney and Honeywell Aerospace.

The aerospace experience was particularly relevant. In aerospace, you think in decades-long product cycles. You invest heavily upfront in platforms that generate returns over 20-30 years. You maintain and upgrade assets continuously. Most importantly, you understand that reliability and safety aren't just nice-to-haves—they're existential requirements. Taiclet would bring this long-term, reliability-focused mindset to American Tower.

His first strategic move was counterintuitive but brilliant. Around 2000, the company began purchasing numerous AT&T Long Lines microwave telephone relay towers from AT&T Communications, Inc., and repurposing them as cell towers. These towers, built during the Cold War to create a hardened communications network, were engineering marvels—200-300 feet tall, capable of withstanding hurricane-force winds, with power and access roads already in place. AT&T had decommissioned the microwave network in the 1980s as fiber optics took over long-distance transmission, leaving these towers standing idle.

American Tower acquired hundreds of these towers for a fraction of what it would cost to build new ones. The locations were perfect—on hilltops and ridgelines with clear lines of sight, exactly where wireless carriers needed towers for optimal coverage. It was asset recycling at its finest, transforming obsolete Cold War infrastructure into critical 21st-century wireless assets.

The next phase of the transformation focused on operational excellence. Taiclet instituted what he called the "American Tower Operating System"—a set of standardized processes for everything from lease negotiations to tower maintenance. The company began measuring and optimizing every metric: time to process a collocation application, tower climb time for maintenance, generator run-time during power outages.

This operational discipline paid off in customer satisfaction. While competitors treated tower leasing as a real estate transaction, American Tower positioned itself as a partner in network deployment. They guaranteed response times, created online portals for carriers to manage their leases, and invested in structural analysis software to speed up the collocation process.

The 2005 acquisition of SpectraSite for $3.1 billion was Taiclet's first major deal and a defining moment for the company. SpectraSite owned over 7,800 towers and had similarly survived the telecom meltdown. The merger created a company with over 22,000 towers, achieving the scale necessary to drive operating leverage. More importantly, it eliminated a competitor and gave American Tower increased pricing power with carriers.

But the real innovation was in how Taiclet thought about capital allocation. He introduced the concept of "Adjusted Funds From Operations" (AFFO) as the key metric for measuring performance—essentially the cash flow available after maintenance capital expenditures. This focus on cash generation rather than accounting earnings would later prove prescient when American Tower converted to a REIT.

The international strategy also evolved during this period. Rather than the scattershot expansion of the late 1990s, Taiclet focused on markets with specific characteristics: low wireless penetration, multiple competing carriers, and regulatory frameworks that permitted or encouraged infrastructure sharing. In 2010, American Tower launched operations in Peru, Chile and Colombia, and acquired Essar Telecom Infrastructure in India, adding approximately 4,450 wireless tower sites.

The India expansion deserves special attention. India in 2010 had over 600 million mobile subscribers but was adding 15-20 million new users per month. The country had 8-10 competing carriers in each region, creating massive infrastructure duplication. The government was pushing infrastructure sharing to reduce environmental impact and improve economics. It was the perfect market for American Tower's model.

Meanwhile, the U.S. business was experiencing a renaissance. The iPhone had launched in 2007, and data traffic was exploding. Carriers that had been in harvest mode suddenly needed thousands of new cell sites to handle the data tsunami. American Tower's towers, which had been built for voice coverage, were perfectly positioned to add capacity for data.

By 2011, American Tower had transformed from a near-bankrupt survivor to a highly profitable growth company. Revenue had grown from $684 million in 2003 to $2.0 billion in 2011. More impressively, EBITDA margins had expanded from 45% to over 60% as the company added tenants to existing towers. The stock, which had traded below $1 in 2002, was now over $50.

But Taiclet's masterstroke was yet to come. He had been studying the REIT structure for years, recognizing that American Tower's predictable, contract-based cash flows were more similar to real estate than to traditional telecom companies. The REIT conversion would transform American Tower from a good business into a great one.

V. The REIT Revolution (2011–2012)

The idea of converting American Tower to a Real Estate Investment Trust was either brilliant or crazy, depending on who you asked. No tower company had ever been approved as a REIT. The IRS had stringent requirements about what constituted "real property," and it wasn't clear that towers and the associated equipment would qualify.

But Taiclet saw what others missed. The tower business was fundamentally about real estate—vertical real estate, but real estate nonetheless. The company owned land, structures permanently affixed to that land, and generated income by leasing space. The business model was virtually identical to that of office or apartment REITs, just with steel towers instead of buildings.

In 2011, American Tower announced its intentions to become a REIT. The announcement sent shockwaves through both the telecom and real estate industries. If approved, American Tower would avoid corporate income taxes on earnings distributed to shareholders as dividends, potentially saving hundreds of millions annually.

The technical challenge was immense. American Tower hired teams of tax lawyers and consultants to navigate the IRS requirements. They had to restructure their entire business, separating "good REIT" assets (the towers and land) from "bad REIT" assets (services and equipment). They created a taxable REIT subsidiary (TRS) to house the non-qualifying activities.

The international operations posed another challenge. REITs have restrictions on foreign income, and American Tower was generating significant revenue from its international towers. The solution was elegant: they structured the international operations through subsidiary REITs in each country, creating a kind of REIT inception—REITs within REITs.

In November 2011, shareholders overwhelmingly approved the REIT conversion. Taiclet promised $0.80 to $0.90 per share annual dividends, yielding between 1.36% and 1.53%. For a company that had never paid a dividend, this was a dramatic shift in capital allocation philosophy.

January 1, 2012 marked the official beginning of American Tower's life as a REIT. The impact was immediate and dramatic. The company's effective tax rate dropped from approximately 35% to under 10%. The dividend requirement forced disciplined capital allocation—no more empire building or speculative investments. Every dollar had to generate sufficient returns to support the dividend.

The REIT structure also changed American Tower's investor base. Traditional telecom investors, focused on growth and capital gains, were replaced by income-focused REIT investors who valued predictable, growing dividends. This new investor base better understood the tower business model and valued the company more appropriately.

The financial engineering was sophisticated. American Tower created a dividend policy that balanced growth and income—a relatively low payout ratio (about 50% of AFFO) that allowed for significant retained capital for growth investments. This was unusual in the REIT world, where most REITs distributed 90-100% of taxable income.

The market's reaction was enthusiastic. The stock rose from $61 at the beginning of 2012 to $75 by year-end. More importantly, American Tower's cost of capital decreased dramatically. As a REIT with investment-grade credit ratings, the company could access debt markets at rates previously unimaginable for a "telecom" company.

The REIT conversion also forced operational improvements. The IRS requirements meant that at least 75% of revenue had to come from real property rents. This pushed American Tower to focus relentlessly on its core tower leasing business, divesting or restructuring ancillary services that didn't qualify.

Competitors took notice. Crown Castle would announce its own REIT conversion in 2012, following American Tower's playbook almost exactly. But American Tower had first-mover advantage and had already locked in the best tax structures and international arrangements.

The REIT structure would prove to be a competitive moat. Any new entrant to the tower industry would face a roughly 35% tax disadvantage if they couldn't qualify as a REIT, and the IRS was becoming increasingly strict about new REIT applications. American Tower had pulled up the ladder behind them.

By the end of 2012, American Tower had completed one of the most successful corporate transformations in business history. From near-bankruptcy to REIT conversion, from domestic focus to global expansion, from survival to dominance. The foundation was set for the next phase: global domination.

VI. Global Domination: The International Land Grab (2013–2020)

The REIT conversion had given American Tower a war chest and a cost of capital advantage that Taiclet was determined to deploy aggressively. The thesis was simple: the mobile revolution that had transformed the U.S. was just beginning in emerging markets. Countries with 20% smartphone penetration would eventually reach 80%. Every percentage point of penetration meant thousands of new towers needed.

In 2013, the company acquired Global Tower Partners for $4.8 billion. This acquisition added sites to the U.S. portfolio and added operations in Costa Rica and Panama. The GTP deal was significant not just for its size but for what it represented—consolidation in the mature U.S. market while simultaneously expanding American Tower's foothold in Central America.

The international expansion accelerated dramatically through the decade. American Tower wasn't just buying towers; they were buying entire market positions. In many countries, they would acquire the tower portfolio of a major carrier, instantly becoming the largest independent tower operator in that market.

2014 brought recognition of Taiclet's transformation of the company. CEO Jim Taiclet was recognized by Harvard Business Review as one of the 100 top-performing CEOs in the world. The recognition was well-deserved—American Tower's total shareholder return under Taiclet's leadership had exceeded 1,000%.

The crown jewel of the international expansion came in 2016. American Tower acquired a 51% controlling interest in Viom Networks Limited, which operated over 42,000 communications sites in India. The Viom deal made American Tower the largest independent tower operator in India, a market adding millions of new mobile subscribers monthly.

India represented both the greatest opportunity and the greatest challenge. The market had over a billion potential mobile users, but also intense competition among carriers that drove prices down to among the lowest in the world. Tower rental rates in India were a fraction of those in the U.S., but the volume opportunity was immense.

In 2017, American Tower was named to the Fortune 500 for the first time, a milestone that reflected the company's transformation from a speculative startup to an infrastructure giant. The company now operated over 150,000 towers globally and generated over $6 billion in annual revenue.

The strategy in each new market followed a similar playbook: acquire a critical mass of towers (usually from a cash-strapped carrier), sign long-term master lease agreements with multiple carriers, then gradually increase tenancy ratios and rental rates. The beauty was in the execution—American Tower had refined this playbook over hundreds of transactions.

Africa became a major focus in the late 2010s. American Tower expanded into Nigeria, South Africa, Ghana, Uganda, and other markets. African markets presented unique challenges—political instability, currency volatility, power grid unreliability—but also unique opportunities. Mobile phones were the primary means of internet access for hundreds of millions of Africans, making towers critical infrastructure.

The company developed innovative solutions for emerging market challenges. In markets without reliable power grids, American Tower installed solar panels and battery backup systems. In countries with currency volatility, they negotiated contracts with inflation escalators and dollar-denominated components.

By 2019, American Tower's international operations generated more revenue than its U.S. business. The transformation was complete—what had started as a domestic radio tower company was now a global infrastructure powerhouse operating on six continents.

In 2020, Tom Bartlett was named President and CEO after Taiclet left to become CEO of Lockheed Martin. Taiclet's departure marked the end of an era. He had taken over a company on the brink of bankruptcy and built it into one of the most valuable REITs in the world with a market capitalization exceeding $100 billion.

Bartlett, who had served as CFO for over a decade, represented continuity. He had been instrumental in the REIT conversion and the international expansion strategy. His appointment signaled that American Tower would continue executing the playbook that had worked so well.

The timing of the leadership transition proved fortuitous. The COVID-19 pandemic in 2020 accelerated digital transformation globally. Work-from-home, video conferencing, and streaming entertainment drove unprecedented demand for wireless infrastructure. While many businesses struggled, American Tower thrived—their towers were more essential than ever.

VII. The 5G Era & Strategic Pivots (2021–Present)

Tom Bartlett inherited a company at an inflection point. 5G deployment was beginning in earnest, promising to drive the next wave of tower demand. But 5G also brought new challenges—it required many more cell sites than 4G, but at shorter ranges, potentially changing the economics of traditional macro towers.

Bartlett's first major move was bold. In 2021, the company agreed to acquire the European and Latin American tower divisions of Telxius from Telefonica for $9.6 billion, adding approximately 31,000 communications sites in Spain, Germany, Argentina, Brazil, Chile, and Peru. The Telxius deal was strategic on multiple levels—it strengthened American Tower's position in Latin America and gave them a significant foothold in Europe, a market they had largely avoided.

But the really transformative deal came later in 2021. American Tower acquired CoreSite for $10.4 billion, with its carrier-neutral data center facilities in the U.S., to strengthen its position in 5G. This wasn't just another tower acquisition—it was a fundamental expansion of American Tower's business model.

The CoreSite acquisition recognized a crucial trend: the convergence of wireless and wireline networks. 5G required not just towers but also edge computing facilities to process data closer to users. CoreSite's data centers in major metropolitan areas could serve as aggregation points for wireless traffic and edge computing nodes for latency-sensitive applications.

The strategic logic was compelling. American Tower's towers collected wireless traffic, CoreSite's data centers processed and routed that traffic, and the combination created an end-to-end infrastructure platform for 5G and beyond. It was vertical integration for the digital age.

In 2023, the American Tower Board of Directors named Steven O. Vondran President and Chief Executive Officer, effective February 1, 2024. Previously, Mr. Vondran served as Executive Vice President and President, U.S. Tower Division, and held various leadership positions since joining the Company in 2000. Vondran, a company veteran who had been with American Tower since the dot-com era, represented both continuity and change.

Under Vondran's leadership, American Tower made a surprising strategic pivot. In 2024, American Tower divested 100% of its India operations to Data Infrastructure Trust (DIT), an Infrastructure Investment Trust sponsored by an affiliate of Brookfield Asset Management. The India exit, after 17 years in the market, was a recognition that some international markets might never generate acceptable returns.

The India decision reflected a new focus on portfolio optimization over growth at any cost. The Indian market had become increasingly challenging—carrier consolidation had reduced the number of potential tenants, pricing pressure was intense, and regulatory changes had made operations more difficult. The $2.5 billion from the sale could be redeployed into higher-return opportunities.

In early 2023, the company announced plans to erect 4,000 new towers worldwide, mainly in Africa, India and Latin America—though the India plans would obviously change with the subsequent divestiture. The focus on Africa and Latin America reflected where American Tower saw the best risk-adjusted returns.

The company also began experimenting with new infrastructure types. Small cells for urban 5G densification, in-building systems for enterprise customers, and even fiber networks in select markets. The goal wasn't to become a fiber company but to own strategic fiber routes that connected their towers and data centers.

American Tower's approach to 5G was pragmatic. While competitors made bold predictions about revolutionary new use cases, American Tower focused on the basics: more devices, more data, more infrastructure needed. Whether 5G enabled autonomous vehicles or just faster Instagram scrolling, towers would be essential.

The company also invested heavily in platform innovations. They developed AI-powered tools to optimize tower loading and structural analysis. They created digital marketplaces where carriers could shop for tower space like booking a hotel room. They even experimented with drone-based tower inspections to reduce costs and improve safety.

Environmental, Social, and Governance (ESG) considerations became increasingly important. American Tower committed to carbon neutrality, investing in renewable energy for their international sites. They also focused on digital inclusion, working with governments and NGOs to bring connectivity to underserved communities.

The financial performance remained strong. By 2023, American Tower generated $11.14 billion in revenue with EBITDA margins exceeding 60%. The company's dividend had grown every quarter since the REIT conversion, creating enormous wealth for long-term shareholders.

As of late 2024, the company owns 148,957 communications sites, including 42,222 sites in the U.S. and Canada, 26,642 sites in Asia-Pacific and Africa, 31,786 sites in Europe, and 48,307 sites in Latin America. The global footprint is staggering—American Tower operates in more countries than McDonald's.

VIII. Business Model Deep Dive: The Beautiful Economics

To truly understand American Tower's dominance, you need to understand the beautiful economics of the tower business model. It's a model that combines the best aspects of real estate, utilities, and technology infrastructure.

The foundation is the lease structure. American Tower signs initial lease terms of 5-10 years with wireless carriers, but here's the kicker: these leases come with multiple renewal options that can extend the total relationship to 30-40 years. The carriers have enormous switching costs—moving antennas to a different tower means re-engineering their network, risking service disruptions, and potentially losing coverage. Once a carrier is on a tower, they almost never leave.

The leases include annual price escalators, typically around 3% in the U.S. and often tied to inflation in international markets. This means that even if American Tower never added another tenant, their revenue would grow 3% annually. It's like owning a bond with an inflation adjustment and a 30-year duration.

But the real magic is in co-location. A tower that costs $250,000 to build might generate $2,000 per month from the first tenant. That barely covers the operating costs and generates modest returns. But the second tenant might pay $1,800 per month, and the third $1,600. The incremental cost of adding these tenants is minimal—maybe $10,000-20,000 in additional equipment and structural modifications.

Let's do the math: Tower cost: $250,000. First tenant: $24,000/year (barely profitable). Second tenant: $21,600/year (almost pure profit). Third tenant: $19,200/year (pure profit). Fourth tenant: $18,000/year (pure profit). Total annual revenue: $82,800. Operating costs: ~$15,000. Net operating income: $67,800. Return on investment: 27%.

And that's conservative. In dense urban areas, American Tower can have 5-6 tenants per tower. Some towers generate over $200,000 in annual revenue. The best towers—those in perfect locations with multiple tenants—can generate 50%+ returns on invested capital.

The operating leverage is extraordinary. Once a tower is built, the ongoing costs are minimal: ground rent (if they don't own the land), property taxes, electricity for lighting, periodic maintenance, and insurance. These costs are largely fixed regardless of the number of tenants. Every additional tenant is essentially 90%+ margin revenue.

American Tower has also mastered the art of operational efficiency. They use master lease agreements (MLAs) with carriers that streamline the leasing process. Instead of negotiating each site individually, carriers can quickly add sites under pre-negotiated terms. This reduces transaction costs and speeds deployment.

The capital allocation framework is disciplined. For new tower builds, American Tower typically requires an "anchor tenant" committed before construction begins. This de-risks the investment and ensures immediate cash flow. They target 3-5 year paybacks on new builds and acquisitions, with returns increasing substantially as they add tenants.

The competitive moats are formidable. First, there's the zoning moat. Getting approval to build a new tower can take 12-24 months and cost hundreds of thousands in legal and consulting fees. Communities resist new towers for aesthetic reasons. Once a tower is built and approved, it's extremely difficult for competitors to build nearby.

Second, there's the relationship moat. American Tower has master lease agreements with every major carrier globally. These relationships, built over decades, create switching costs beyond just the physical infrastructure. Carriers have integrated American Tower's systems into their network planning and operations.

Third, there's the scale moat. American Tower's 150,000+ towers give them negotiating leverage that smaller operators can't match. They can offer carriers package deals across multiple markets, one-stop shopping for national deployments, and volume discounts that still maintain healthy margins.

The financial moat might be the strongest. As a REIT with investment-grade credit ratings, American Tower can borrow at rates that would be impossible for new entrants. This cost of capital advantage makes it nearly impossible for competitors to underbid them on acquisitions while still generating acceptable returns.

The network effects are subtle but powerful. The more towers American Tower owns in a market, the more valuable they become to carriers who need comprehensive coverage. A carrier might accept suboptimal terms on some towers to get access to critical sites. This portfolio effect creates value beyond the sum of individual towers.

American Tower has also built switching costs into their operations. They provide carriers with proprietary software for managing their leases, structural analysis tools for planning equipment additions, and integrated billing systems. Switching to another tower company means replacing all these systems.

The business model is also naturally hedge against technological change. Every new wireless generation (2G→3G→4G→5G) requires more infrastructure, not less. Higher frequencies require more towers for the same coverage. More data consumption requires more capacity, which means more equipment on towers.

Even potential disruptions play to American Tower's advantage. Satellite internet services like Starlink? They need ground stations, preferably on tall structures with good sight lines—like towers. Fixed wireless access to compete with cable? That requires even more tower infrastructure. Autonomous vehicles needing ultra-low latency networks? That means edge computing facilities co-located with towers.

IX. Playbook: Strategic & Investment Lessons

American Tower's journey from near-bankruptcy to global dominance offers a masterclass in strategic execution and capital allocation. The playbook they've developed is worth studying for any business leader or investor.

Lesson 1: The Power of Boring in Exciting Markets

American Tower owns boring infrastructure in exciting markets. While everyone focuses on the latest smartphone or killer app, American Tower quietly collects rent from the infrastructure that makes it all possible. This positioning—boring assets in growing markets—provides both stability and growth.

Lesson 2: Capital Allocation is Everything

From Taiclet's early focus on AFFO to the disciplined REIT conversion, American Tower has been fanatical about capital allocation. Every dollar is evaluated on its return potential. They're willing to pay up for strategic assets (CoreSite) but also willing to exit markets that don't meet return thresholds (India).

Lesson 3: Build Once, Lease Many

The tower business model is the physical manifestation of software's "build once, sell many" model. The first tenant pays for the tower; every subsequent tenant is gravy. This model creates enormous operating leverage and returns that improve over time.

Lesson 4: Master the Local, Scale the Global

Tower economics are intensely local—each tower serves a specific coverage area. But American Tower has figured out how to scale local expertise globally. They use the same playbook in Nigeria that worked in Nebraska, adapted for local conditions but fundamentally similar.

Lesson 5: Embrace Financial Engineering

The REIT conversion wasn't just about tax savings—it fundamentally changed American Tower's cost of capital and investor base. They understood that how you finance assets can be as important as which assets you own.

Lesson 6: Time Arbitrage

American Tower plays a different game than their customers. Carriers think in quarters; American Tower thinks in decades. This time arbitrage allows them to make investments that might look expensive short-term but generate enormous long-term value.

Lesson 7: The Platform Power

American Tower isn't just a collection of towers—it's a platform. The value of the platform exceeds the sum of individual assets. This platform power creates competitive advantages that are nearly impossible to replicate.

Lesson 8: Diversification vs. Focus

American Tower maintains laser focus on their core business (infrastructure) while diversifying across geographies and asset types. They don't try to be a carrier or equipment manufacturer. They stick to what they know: owning and leasing infrastructure.

Lesson 9: Manage Through Cycles

American Tower has survived and thrived through multiple technology cycles (2G→3G→4G→5G), economic cycles (dot-com, financial crisis, COVID), and industry cycles (carrier consolidation and expansion). The key is building a business model resilient to cycles, not dependent on timing them.

Lesson 10: Exit When Necessary

The India divestiture showed maturity. After 17 years and significant investment, American Tower recognized the market wasn't delivering acceptable returns. Rather than double down or hope for improvement, they sold to a buyer who might generate better returns. Knowing when to fold is as important as knowing when to raise.

X. Analysis & Future Outlook

The Bull Case

The bull case for American Tower is compelling. 5G deployment is still in early innings globally, with most countries at less than 30% 5G penetration. Each generation of wireless technology has required 1.5-2x more infrastructure than the previous generation. If this pattern holds, 5G could drive a decade of growth.

The Internet of Things (IoT) revolution is just beginning. Billions of devices—from cars to refrigerators to industrial sensors—will need wireless connectivity. While not all IoT connections require towers, the sheer volume of devices and data will drive infrastructure demand.

Emerging markets remain underpenetrated. Smartphone penetration in Africa is still under 50%. India, despite American Tower's exit, will need hundreds of thousands of new towers. Latin America is experiencing rapid digital transformation. The growth runway in these markets is measured in decades, not years.

The edge computing opportunity could be transformative. As applications require lower latency—autonomous vehicles, AR/VR, real-time AI—computing will move from centralized clouds to the network edge. American Tower's towers are perfectly positioned to house edge computing facilities.

Fixed wireless access (FWA) could drive unexpected tower demand. As carriers use 5G to compete with cable companies for home broadband, they'll need dense tower networks. Early FWA deployments are already driving tower leasing demand in suburban and rural markets.

The Bear Case

The bear case centers on several risks. Satellite technology, particularly Low Earth Orbit (LEO) constellations like Starlink, could theoretically reduce tower demand. While satellites can't match terrestrial networks for capacity in dense areas, they could serve rural markets that might otherwise need towers.

Carrier consolidation remains a perpetual risk. Every merger reduces the number of potential tenants. The T-Mobile/Sprint merger in the U.S. eliminated a major customer. Further consolidation could pressure lease rates and reduce co-location opportunities.

Interest rate sensitivity is a real concern. As a REIT, American Tower is valued partially on its dividend yield. Rising interest rates make that yield less attractive relative to bonds, potentially pressuring the stock price. Higher rates also increase borrowing costs for acquisitions.

Technology evolution could change infrastructure needs. What if 6G or some future technology requires completely different infrastructure? What if carriers develop technology to share spectrum more efficiently, reducing the need for towers? These are low-probability but high-impact risks.

Regulatory and political risks are growing. Governments increasingly view telecom infrastructure as strategic national assets. Some countries are restricting foreign ownership or demanding local partners. Tax policies could change, potentially affecting the REIT structure.

Competitive Dynamics

American Tower's main competitors each have different strategies. Crown Castle has focused on the U.S. market and invested heavily in fiber infrastructure. They're betting that the convergence of wireless and wireline makes fiber as valuable as towers. The verdict is still out.

SBA Communications remains subscale compared to American Tower but maintains impressive margins through operational efficiency. They've been more selective in international expansion, focusing on the Americas. Their smaller size makes them more nimble but limits their acquisition firepower.

New entrants face enormous barriers. Digital infrastructure funds have raised billions to invest in towers, but they struggle to compete with American Tower's scale and cost of capital. Carriers periodically threaten to build their own towers, but the economics rarely make sense except in specific situations.

The Verdict

American Tower has built one of the great infrastructure monopolies of the digital age. Their towers are essential infrastructure with no practical substitutes. The business model combines growth with stability, global scale with local market power, and technological agility with infrastructure permanence.

The next decade will bring challenges—new technologies, changing carrier dynamics, evolving regulations. But American Tower's track record suggests they'll adapt and thrive. They've survived the dot-com crash, navigated the financial crisis, and emerged stronger from COVID.

The key insight is that American Tower isn't really in the tower business—they're in the connectivity infrastructure business. Whatever form that infrastructure takes—towers, small cells, edge data centers, or something not yet invented—American Tower will likely own it and lease it to others.

XI. Epilogue & Reflections

What would have happened if CBS had kept American Tower instead of spinning it off in 1998? It's fascinating to consider. CBS, focused on content and broadcasting, would likely have underinvested in the tower business. They might have sold it during the dot-com crash for a fraction of today's value. The spin-off, painful as it was during the crash, was essential to American Tower's success.

The paradox of American Tower is that they've built a technology fortune on decidedly non-technology assets. In an industry obsessed with innovation, disruption, and software, American Tower proves that sometimes the most valuable thing is the boring infrastructure that makes everything else possible.

For founders, the lesson is about finding leverage points in value chains. American Tower identified that towers were a bottleneck in wireless networks and built a business around removing that bottleneck. They didn't try to compete with carriers or equipment manufacturers—they found their niche and dominated it.

For investors, American Tower demonstrates the power of predictable, growing cash flows. While tech investors chase the next unicorn, American Tower has delivered steady, market-beating returns for two decades. Sometimes the best technology investment isn't in technology at all.

American Tower might be the best business nobody knows about. Most people have never heard of them, yet everyone depends on them. Every call, every text, every byte of mobile data likely touches an American Tower asset. They're the invisible infrastructure of our connected world.

The story of American Tower is ultimately about transformation—from radio to wireless, from domestic to global, from startup to infrastructure giant. But it's also about persistence. Through booms and busts, through technology transitions and market crashes, American Tower kept building and buying towers.

Steven Dodge had the vision. Jim Taiclet had the execution. Tom Bartlett and Steven Vondran continue the mission. Thousands of employees worldwide maintain and expand the infrastructure. Millions of investors have funded the growth. Billions of users depend on the result.

As we look to the future—to 6G, to autonomous vehicles, to the metaverse, to whatever comes next—one thing seems certain: it will require infrastructure. And if history is any guide, American Tower will own that infrastructure, lease it to others, and quietly collect rent on the future.

The empire of steel and concrete towers that started as a small subsidiary of a Boston radio company has become the foundation of global digital infrastructure. American Tower didn't just build towers—they built a business model so powerful, so resilient, and so essential that it's hard to imagine the modern world without it.

That's the ultimate measure of American Tower's success: they've become invisible because they're everywhere, forgotten because they're essential, boring because they just work. In the attention economy, American Tower has built a fortune on being ignored. And they wouldn't have it any other way.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube