AMG: The Outsider of Asset Management

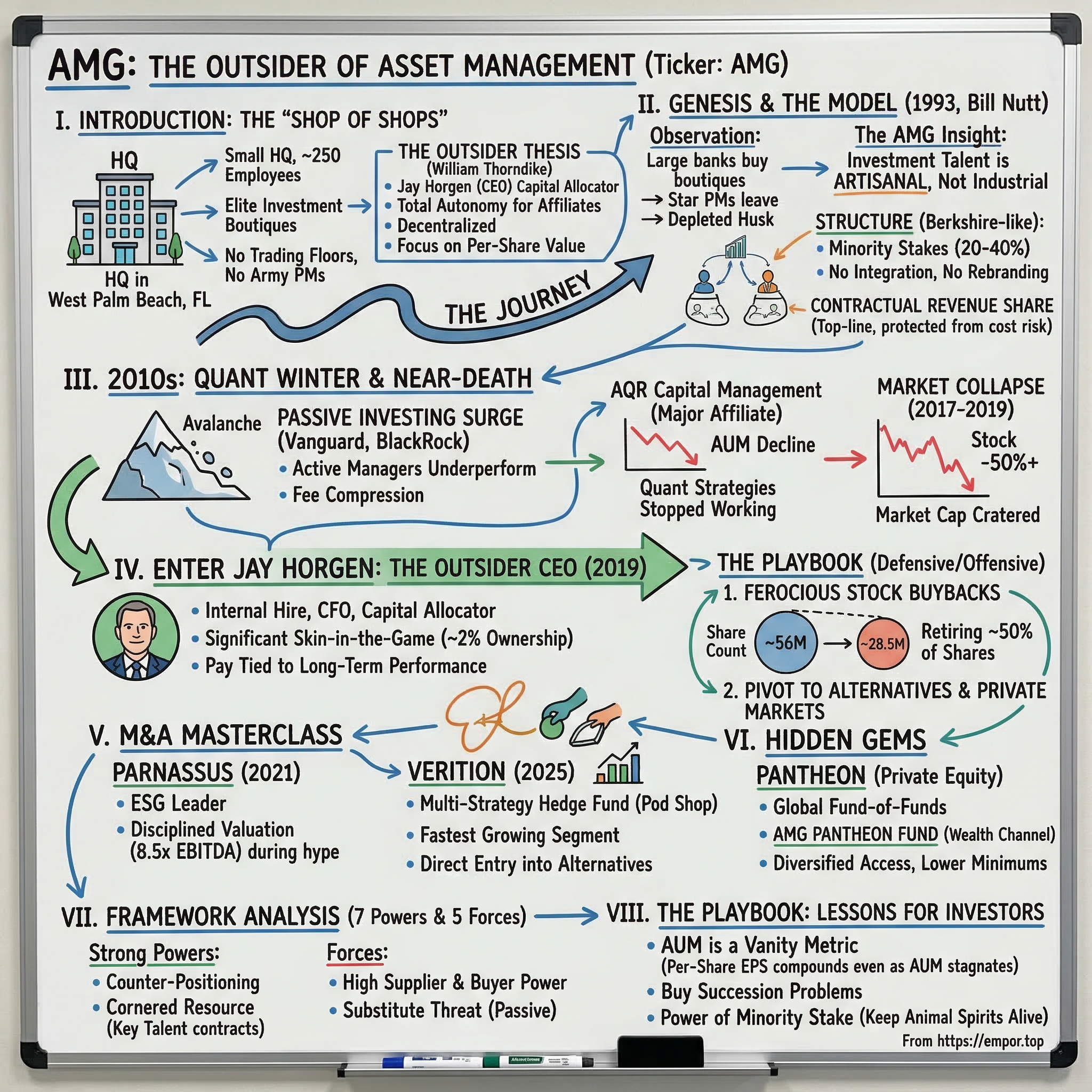

I. Introduction: The "Shop of Shops"

Picture this: a company that oversees more than eight hundred billion dollars in assets under management, yet runs its corporate headquarters with roughly two hundred and fifty employees. No trading floors. No armies of portfolio managers hunched over Bloomberg terminals. No proprietary mutual funds emblazoned with the parent company's name. Just a small team in West Palm Beach, Florida, quietly collecting revenue-sharing checks from some of the most elite investment boutiques on the planet.

That company is Affiliated Managers Group, ticker symbol AMG, and it is one of the most misunderstood businesses in American finance.

Most investors know BlackRock, the eleven-and-a-half-trillion-dollar colossus that owns a piece of seemingly everything. They know Vanguard, the nonprofit juggernaut that made index funds a religion. They might even know Blackstone or Apollo, the private equity titans currently racing to "democratize" alternative investments for everyday savers. But almost nobody outside of institutional finance circles knows AMG, the company that owns the special forces of the investment world: the boutique firms that institutions turn to when they need returns that cannot be replicated by buying an S&P 500 index fund.

Here is the thesis, stated plainly: AMG is the ultimate "Outsider" company. William Thorndike wrote a celebrated book called The Outsiders, profiling eight CEOs who massively outperformed the market not by being operational wizards, but by being brilliant capital allocators. They bought back stock when it was cheap. They made disciplined acquisitions. They ran decentralized organizations and pushed decision-making to the edges. They cared about per-share value, not empire size. AMG, under its current CEO Jay Horgen, reads like a case study ripped from that playbook. They do not pick stocks. They pick the people who pick stocks, and then they give those people the one thing that Wall Street almost always destroys: total autonomy.

But to understand why that model is so powerful today, you have to understand how close it came to dying. Because AMG's story is not a smooth arc of compounding returns. It is a story of a brilliant founding insight, a near-death experience during the "Quant Winter" of the late 2010s, a leadership transition that changed everything, and a strategic pivot into private markets and alternative investments that the market is only now beginning to appreciate.

The journey spans three decades. From a scrappy startup in the early 1990s with a contrarian idea about how to buy investment firms, to a peak market capitalization of nearly eleven and a half billion dollars in 2017, to a gut-wrenching collapse that saw the stock lose more than half its value, to a resurrection led by a former CFO who decided that the best thing he could do was stop trying to grow the company's assets and start shrinking its share count instead.

This is the story of AMG.

II. The Genesis and The Model

In 1993, a man named Bill Nutt had an insight that would become the foundation of a multi-billion-dollar enterprise. Nutt, a veteran of the financial services industry, had watched a pattern repeat itself for decades: a large bank or insurance company would acquire a successful boutique investment firm, integrate it into the parent organization, slap a new brand on the door, and within a few years, the star portfolio managers who had made the boutique successful in the first place would walk out the door, start a new shop, and take their clients with them. The acquiring company was left with a depleted husk, some goodwill on the balance sheet, and a painful lesson in the economics of human capital.

Nutt's insight was deceptively simple: investment talent is artisanal, not industrial. You cannot put a great portfolio manager on an assembly line. You cannot "scale" investment genius the way you scale a factory or a software platform. The moment you strip away a manager's independence, their sense of ownership, their ability to run the business as they see fit, you destroy the very thing you paid for.

So Nutt designed a structure that was the opposite of what every major acquirer in the industry was doing. AMG would buy a minority equity stake in a boutique investment firm, typically somewhere between twenty and forty percent. The founders would keep the majority of the economics. AMG's name would not appear on any fund or product. There would be no integration, no centralized compliance overhaul, no "synergies" in the corporate-speak sense. The boutique's name stayed on the door. The founders kept running the investment process exactly as they had before. And AMG would receive a contractual share of the firm's revenues in perpetuity.

Think of it as the Berkshire Hathaway model applied to investment management. Warren Buffett famously buys businesses and lets the managers run them. AMG does the same thing, except its "businesses" are investment boutiques, and the "managers" are some of the most talented investors in the world.

The revenue-sharing structure deserves particular attention because it is the economic engine of the entire enterprise. When AMG acquires an affiliate, it negotiates a "revenue share" arrangement rather than taking a cut of profits. This is a crucial distinction. If an affiliate's costs spiral upward, perhaps because they need to hire expensive quantitative researchers or build out a new technology platform, AMG's revenue share is still calculated on the top line. The affiliate bears the cost risk. AMG's economics are protected. It is an elegant structure that aligns incentives while insulating the parent company from operational volatility at the affiliate level.

AMG went public in November 1997, listing on the New York Stock Exchange. The IPO gave the company access to capital markets, which it used to fund a steady cadence of affiliate acquisitions throughout the late 1990s and 2000s. The model worked beautifully during this era. AMG would identify a high-quality boutique, typically one with a differentiated investment process, strong performance track record, and a founder approaching retirement age. AMG would offer liquidity for the founder's equity stake, a solution to the thorny succession problem that plagues every small firm, and the promise that nothing about the day-to-day operations would change.

This was counter-positioning in its purest form. Every other acquirer in the asset management industry, from Franklin Templeton to Invesco to the big banks, operated under the assumption that integration creates value. They would buy a firm, fold it into their distribution network, cross-sell products, and rationalize costs. AMG did the exact opposite. It promised not to help. And that promise, paradoxically, became its greatest competitive advantage. If you were a founder who had spent twenty years building a firm and could not stomach the thought of some corporate parent rebranding your life's work as "Invesco Sub-Advised Small Cap Value Fund," you called AMG. They were the only game in town for founders who wanted liquidity without losing their soul.

By the mid-2010s, AMG had assembled a remarkable portfolio of affiliates. The crown jewels included AQR Capital Management, the quantitative powerhouse founded by Cliff Asness; Tweedy, Browne, the legendary value investing firm with roots tracing back to Benjamin Graham; Harding Loevner, a respected international equity manager; and Pantheon, a global private equity fund-of-funds platform. Revenue climbed past two billion dollars annually. The stock traded above two hundred dollars per share. The market capitalization approached eleven and a half billion. Everything was working.

But beneath the surface, a tectonic shift was underway that would threaten to destroy the entire model. And it had a name that sounded almost quaint: passive investing.

III. The 2010s: The Quant Winter and The Near-Death Experience

To understand what nearly killed AMG, you need to understand a single, devastating statistic: over any ten-year period ending in December 2024, only seven percent of U.S. large-cap active fund managers survived and beat their passive benchmark. Seven percent. That means ninety-three out of every hundred managers who promised they could beat the index failed to deliver. And investors noticed.

The shift from active to passive management was not a gentle transition. It was an avalanche. Assets in passively managed U.S. funds surged past actively managed funds for the first time in 2024, a milestone that had been approaching with the inevitability of a glacier. BlackRock's iShares ETF platform alone grew from roughly one and a half trillion dollars to over four trillion in the span of a decade. Vanguard, the temple of indexing founded by the late Jack Bogle, accumulated over nine trillion dollars. Average fees for U.S. equity mutual funds were sliced roughly in half, from around one percent in 2000 to about forty-two basis points by 2024. The message from the market was clear: most active managers are not worth what they charge.

For a company like AMG, whose entire business model depended on the proposition that active management was valuable, this was an existential threat. And it manifested most painfully in the firm's single largest affiliate: AQR Capital Management.

AQR, founded by Cliff Asness in 1998, was the intellectual godfather of quantitative investing. Asness, a former student of Eugene Fama at the University of Chicago and a protege at Goldman Sachs's quantitative research group, had built AQR into one of the largest and most influential hedge funds in the world. At its peak, AQR managed approximately two hundred and twenty-six billion dollars. The firm's strategies, which relied on systematic, factor-based approaches to harvesting returns from value, momentum, and other well-documented market anomalies, had generated strong performance for years. For AMG, AQR was the golden goose.

Then came what the industry now calls the "Quant Winter." Beginning around 2018, the quantitative value strategies that had been AQR's bread and butter stopped working. Growth stocks, led by the mega-cap technology firms, relentlessly outperformed value. Momentum strategies whipsawed. Factor crowding, where too many quantitative managers chased the same signals, compressed returns. AQR's AUM began a sickening decline, falling from that peak of over two hundred billion dollars to roughly one hundred and ten billion. The firm's flagship Absolute Return fund posted disappointing numbers. Institutional investors, already nervous about the active-versus-passive debate, began pulling money.

For AMG, the impact was devastating. AQR had been contributing an outsized share of the parent company's revenue. As AQR shrank, so did AMG's earnings. But the problem was bigger than any single affiliate. The entire traditional active equity franchise, which had been AMG's core business for two decades, was under siege. Firms like Tweedy, Browne, Harding Loevner, and other long-only equity managers in the AMG stable were all swimming against the same tide of passive flows.

The stock told the story. From a peak of roughly two hundred and five dollars per share at the end of 2017, AMG's stock price collapsed. By the end of 2019, it traded around eighty-five dollars. The market capitalization, which had stood at nearly eleven and a half billion, cratered to just four and a quarter billion. Analyst ratings, which had been overwhelmingly positive during the boom years, shifted to a wall of "Hold" and "Neutral" calls. Deutsche Bank, Citigroup, Credit Suisse, and others all downgraded or maintained cautious stances. In early 2019, both Jefferies and Deutsche Bank downgraded AMG, signaling that even the firm's long-time supporters had lost confidence.

The narrative on Wall Street was brutal and simple: the multi-boutique model was dead. Active management was a sunset industry. AMG was a holding company full of melting ice cubes, and no amount of clever structuring could save it. BrightSphere, another multi-boutique firm that had been spun out of Old Mutual, seemed to confirm the thesis. Over the next several years, BrightSphere would divest six of its seven affiliates, eventually renaming itself Acadian Asset Management in 2025, a tacit admission that the multi-affiliate model had failed. Legg Mason, once the other major multi-affiliate platform, was absorbed by Franklin Templeton in 2020 for four and a half billion dollars, effectively ending its independent existence.

AMG was the last pure-play multi-boutique standing. And in early 2019, it looked like it might not be standing for much longer. Net income for fiscal year 2019 collapsed to just fifteen point seven million dollars, down from nearly seven hundred million two years earlier. The company reported earnings per share of thirty-one cents, a number that would have been laughable at the firm's peak.

It was at this precise moment of maximum pessimism that the company made a leadership change that would alter its trajectory entirely.

IV. Enter Jay Horgen: The Outsider CEO

In March 2019, Jay Horgen became the Chief Executive Officer of Affiliated Managers Group. The transition was quiet, almost unremarkable in the moment. There was no splashy external hire, no celebrity CEO poached from a rival firm, no dramatic boardroom coup. Horgen had been AMG's Chief Financial Officer. He was an insider, a numbers guy, a capital allocator by training and temperament. Born in 1971, he had spent his entire career in the financial architecture of the business rather than on the sales floor or in front of institutional investors pitching products.

This turned out to be exactly what AMG needed.

Horgen's profile as a leader is worth examining in detail, because it explains nearly everything about what happened next. He is not a charismatic salesman. He does not give rousing keynote speeches at industry conferences. What he does, relentlessly and with unusual discipline, is allocate capital. And in a business where the primary strategic decisions are "which affiliate to buy," "how much stock to repurchase," and "how to structure the balance sheet," a capital allocator is precisely the right person to have in the corner office.

The skin-in-the-game numbers are striking. According to company filings, Horgen owns approximately two percent of AMG's outstanding shares, a stake worth well over a hundred and fifty million dollars at recent prices. For a company with a market capitalization of roughly seven and a half billion, that level of insider ownership is unusual among financial services CEOs. More importantly, roughly ninety-four percent of his total compensation is "at risk," meaning it is tied to long-term stock price performance with vesting schedules stretching out to 2027 through 2030. His base salary and guaranteed cash represent a tiny fraction of his total pay. This is a CEO whose personal wealth rises and falls with the stock. There is no "heads I win, tails you lose" dynamic here.

Horgen's first major strategic decision was one of restraint. He stopped doing deals for the sake of doing deals. The prior regime had been focused on growth, on adding affiliates, on expanding AUM. Horgen looked at the landscape and concluded that the best use of capital was not to buy more of the same. Instead, he did two things simultaneously.

First, he pivoted the acquisition strategy decisively toward alternatives and private markets. No more traditional long-only equity managers. The future would be hedge funds, private equity platforms, quantitative strategies, and wealth management. Every new affiliate would need to be in a category where passive investing could not easily replicate the returns.

Second, and perhaps more importantly, he began buying back AMG's own stock with ferocious intensity. The numbers are staggering. In 2017, AMG had fifty-six million shares outstanding. By the end of fiscal year 2025, that number had fallen to twenty-eight and a half million. Horgen and his team retired nearly half of all outstanding shares. The treasury stock balance swelled from three hundred and eighty-six million dollars in 2016 to four point nine billion by the end of 2025. That is not a rounding error. That is a systematic, multi-year campaign to cannibalize the share count while the stock traded at what Horgen clearly believed were deeply discounted levels.

The logic of the buyback program is straight out of the Outsiders playbook. When a stock trades at eight or nine times earnings and the underlying business generates strong free cash flow, buying back shares is the highest-return use of capital available. Every share retired at a discount to intrinsic value creates immediate per-share value for the remaining shareholders. Horgen did not need AMG's AUM to grow to make shareholders wealthier. He just needed to keep shrinking the denominator.

The results speak for themselves. Diluted earnings per share climbed from that dismal thirty-one cents in 2019 to over fifteen dollars by 2024, and then surged to twenty-two dollars and seventy-four cents in fiscal 2025. Revenue in 2025 reached two point four five billion dollars, the highest level in the company's history, surpassing even the pre-crisis peak. Net income hit seven hundred and seventeen million. And all of this happened with a share count that was half what it had been eight years earlier.

Horgen also assembled a notably young and lean leadership team. Thomas Wojcik, born in 1981, serves as President and Chief Operating Officer. Dava Ritchea, born in 1985, holds the CFO role. Kavita Padiyar, born in 1983, is General Counsel. This is a management team that will be running the company for decades, not winding down their careers. Their total compensation, while competitive, is modest by Wall Street standards: Wojcik earned roughly four million, Ritchea about two million, Padiyar approximately one point three million. The entire C-suite appears to be incentivized for long-term value creation rather than short-term asset gathering.

The market noticed, eventually. After years of Hold and Neutral ratings, the analyst community began upgrading AMG in mid-to-late 2025. Goldman Sachs upgraded to Buy in June 2025. Bank of America followed with an upgrade in September. TD Cowen moved to Buy in August. The stock, which had languished below one hundred and sixty dollars through most of 2023, surged past two hundred and eighty by year-end 2025. But even after the rally, AMG still traded at just eleven and a half times earnings and six point nine times EV/EBITDA, a fraction of the multiples commanded by alternative asset managers like Blackstone, KKR, or Apollo.

The question hanging over the stock, and the question that makes AMG such a fascinating case study, is whether the market is still pricing in the old narrative of a traditional active manager in secular decline, while missing the new reality of a company that has quietly transformed itself into something far more valuable.

V. M&A Masterclass: Parnassus and Verition

If the buyback program was the defensive play, the acquisition strategy was the offense. And two deals in particular illustrate how AMG deploys capital under Horgen's leadership.

The first was Parnassus Investments, announced in 2021. Parnassus was one of the largest dedicated ESG, or environmental, social, and governance, investment managers in the United States. Founded in 1984 by Jerome Dodson in San Francisco, the firm had built a loyal following among institutional and retail investors who wanted their portfolios to reflect their values. By the time AMG came knocking, Parnassus managed roughly thirty billion dollars in assets, primarily in U.S. equity strategies that integrated ESG criteria into fundamental stock analysis.

The timing was revealing. In 2021, ESG investing was at the peak of its hype cycle. Every major asset manager was launching ESG products. BlackRock's Larry Fink was writing annual letters about stakeholder capitalism. Institutional allocators were demanding ESG integration across their portfolios. In that environment, ESG-focused firms were commanding premium valuations. Peers were paying fifteen to twenty times EBITDA for "growth" acquisitions in the ESG space.

AMG paid approximately six hundred million dollars for its stake in Parnassus, which worked out to roughly eight and a half times EBITDA. That is a remarkable number. In a market where everyone was bidding up ESG assets, AMG acquired one of the most established, authentically ESG-focused firms in the country at a valuation that was less than half what the frothiest buyers were paying. This was not a momentum trade. It was a disciplined, surgical strike by a team that understood the difference between paying a fair price for a great business and overpaying for a narrative.

The strategic logic was sound as well. Parnassus gave AMG exposure to a secular growth trend in responsible investing without requiring AMG to build the capability from scratch. And because AMG's model preserves affiliate independence, Parnassus continued to operate exactly as it had before, with its name, its team, its investment process, and its client relationships all intact. Jerome Dodson's legacy was preserved. The firm's culture was untouched. AMG simply became a capital partner and succession solution.

The second deal was even more strategically significant, though it received less attention in the financial press. In April 2025, AMG announced a minority equity investment in Verition Fund Management, a multi-strategy hedge fund that had grown to roughly twelve and a half billion dollars in assets under management.

To understand why Verition matters, you need to understand the hottest corner of the hedge fund industry: the so-called "pod shop" wars. A pod shop is a multi-strategy hedge fund that deploys dozens or even hundreds of semi-autonomous portfolio management teams, called "pods," each running a distinct strategy. The platform provides centralized risk management, technology infrastructure, prime brokerage relationships, and capital allocation. Portfolio managers who underperform get cut. Top performers receive more capital. Think of it as a venture capital model applied to trading: fund many small bets, kill the losers fast, and double down on the winners.

The biggest names in this space are Citadel, run by Ken Griffin, which manages roughly sixty-five billion dollars; Millennium, run by Izzy Englander, at approximately seventy-nine billion; and Point72, Steve Cohen's platform with about forty-six billion across nearly two hundred pods. These firms have become the dominant force in hedge fund asset gathering, with the multi-strategy category reaching four hundred and twenty-eight billion dollars in 2025, growing a hundred and seventy-five percent from 2017 to 2023 while the broader hedge fund industry grew only thirteen percent.

Verition, founded in 2008 by Nicholas Maounis and Josh Goldstein, runs approximately one hundred and fifty portfolio management teams across credit, fixed income, convertible arbitrage, event-driven, equity long-short, and quantitative strategies. The firm has generated average annualized returns of roughly thirteen percent since inception. It is not Citadel or Millennium, but it plays in the same league, offering institutional investors the kind of consistent, uncorrelated returns that justify the premium fees these platforms charge.

For AMG, the Verition investment represents a direct entry into the fastest-growing segment of the hedge fund industry. It complements existing alternatives affiliates like AQR, Capula, Garda Capital, Systematica, and Winton, giving AMG a presence across quantitative, systematic, discretionary, and now multi-strategy hedge fund approaches. The deal terms were not fully disclosed, but the strategic rationale was unmistakable: AMG was planting its flag in the one area of active management where passive investing has no answer and where asset growth shows no signs of slowing.

What both deals reveal is a consistent capital deployment philosophy. AMG does not chase the hottest deal or pay the highest price. It waits for the right opportunity, structures a partnership that preserves the affiliate's autonomy, and pays a disciplined multiple. The Parnassus deal at eight and a half times EBITDA during the ESG frenzy. The Verition deal to enter the pod shop wars at what appears to be a fair valuation for a growing platform. These are not the moves of a company desperate for growth. They are the moves of a capital allocator who understands that the best returns come from discipline, not enthusiasm.

VI. The Hidden Gems: Pantheon and The Wealth Channel

If the Verition deal is AMG's hedge fund play, then Pantheon is its private equity play, and it may be the single most underappreciated asset in the entire portfolio.

Pantheon is a global private equity fund-of-funds manager with a track record stretching back more than four decades. The firm invests across private equity, infrastructure, real assets, and private credit, providing institutional investors with diversified access to private markets through primary fund investments, secondaries, and co-investments. Pantheon manages tens of billions of dollars for some of the world's largest pension funds, sovereign wealth funds, and endowments. It is, by any measure, one of the most established and respected names in private markets.

But the really interesting development is not Pantheon's institutional business. It is the AMG Pantheon Fund, a vehicle designed to bring private equity access to high-net-worth individuals and the broader wealth management channel.

Here is why this matters. For decades, private equity was the exclusive province of large institutions. If you were a pension fund with a billion-dollar allocation, you could invest directly with KKR or Blackstone. If you were a dentist in Ohio with a few million dollars, you were locked out. The minimum investment sizes, the long lock-up periods, the complex partnership structures, and the limited partner agreements all conspired to keep private equity as a walled garden for the ultra-wealthy and the institutional.

That wall has been crumbling. Over the past several years, the major alternative asset managers have been racing to build "semi-liquid" vehicles that package private market investments in a format accessible to retail and high-net-worth investors. Blackstone launched BREIT for real estate and BCRED for private credit. Apollo, KKR, Ares, and Blue Owl all developed their own versions. The logic was irresistible: institutions were largely fully allocated to alternatives, so the next trillions of capital had to come from the roughly eighty-trillion-dollar U.S. retail wealth market.

But this democratization trend ran into serious trouble starting in late 2025. An historic selloff hammered the publicly traded alternative asset managers. Blue Owl restricted withdrawals in November 2025 and conducted a fire sale in early 2026. Blackstone's BCRED faced billions in redemption requests. Senator Elizabeth Warren called for federal stress tests on what she termed the "shadow banking system." The fundamental problem was structural: illiquid long-term loans had been packaged in semi-liquid wrappers that promised quarterly redemptions to retail investors. When those investors wanted their money back simultaneously, the liquidity mismatch became painfully apparent.

This is where AMG's Pantheon Fund stands apart. The fund, which had grown to approximately six point four billion dollars in assets by the end of 2025, is structured differently from the private credit vehicles that ran into trouble. Rather than making direct loans that can become illiquid in a crisis, the Pantheon Fund invests across a diversified portfolio of private equity fund interests, spanning multiple managers, strategies, geographies, and vintage years. It offers quarterly repurchases of up to five percent of net asset value, but its underlying portfolio is inherently more diversified and less concentrated than a direct lending vehicle.

The fund has a relatively low minimum investment of twenty-five thousand dollars and provides 1099 tax reporting, making it far more accessible and tax-friendly for individual investors than a traditional limited partnership structure. It has grown from roughly one billion dollars to over six billion in a remarkably short period, suggesting that the wealth management channel's appetite for this type of product is substantial.

What makes this strategically important for AMG is the earnings mix shift it represents. According to company presentations, alternatives and private markets now drive approximately fifty-five percent of AMG's earnings, despite representing less than half of total assets under management. This is because alternative strategies charge higher fees, generate performance-related income, and have stickier capital bases than traditional long-only equity mandates. The AMG of 2026 is not the same company that the market was writing obituaries for in 2019. It is a company where the majority of earnings come from alternatives, private markets, and strategies where passive investing simply cannot compete.

For investors tracking AMG's evolution, the growth rate of alternatives AUM and the trajectory of the Pantheon Fund are critical signposts. If Pantheon continues to scale its wealth channel distribution and the broader alternatives franchise keeps growing as a percentage of earnings, the market will eventually need to re-rate AMG from a "traditional active manager" multiple to something closer to an "alternatives platform" multiple. The gap between those two valuations is enormous.

VII. Framework Analysis: 7 Powers and 5 Forces

It is worth stepping back from the narrative to ask a structural question: does AMG have a durable competitive advantage, or is it simply a well-managed company in a declining industry? Two frameworks help answer this question.

Hamilton Helmer's 7 Powers identifies the sources of durable strategic advantage that allow a company to sustain excess returns over time. Applied to AMG, two powers stand out as genuinely strong.

The first is Cornered Resource. AMG's contractual relationships with its affiliate founders and key investment talent are, in a very real sense, its most valuable asset. These are not short-term management contracts that can be renegotiated at will. They are long-term equity partnership structures that give founders significant economic interests while locking AMG into a permanent revenue-sharing arrangement. You cannot "replicate" Cliff Asness and the AQR team, or the Pantheon partnership, or the Verition platform. The talent is the product, and AMG has a contractual lock on the economics of that talent. This is analogous to a mining company owning rights to a unique ore deposit. Others can try to find similar deposits, but they cannot take yours.

The second is Counter-Positioning. AMG occupies a strategic position that its competitors literally cannot copy without undermining their own business models. If BlackRock tried to replicate AMG's model of acquiring boutiques and leaving them independent, it would cannibalize its own centralized distribution and brand architecture. If Franklin Templeton, having spent years integrating the Legg Mason affiliates, suddenly decided to give those affiliates true independence, it would unwind billions of dollars in integration cost savings. AMG's promise of non-interference is credible precisely because it has no centralized investment platform to protect. It is the anti-corporate acquirer, and that positioning is self-reinforcing: the more boutiques it acquires without interfering, the stronger its reputation becomes as the partner of choice for the next founder looking for liquidity.

The remaining powers are present to varying degrees. Switching costs are moderate. Once an affiliate has structured its equity partnership with AMG, the relationship is deeply embedded and expensive to unwind. But individual clients of affiliates can and do switch. Process power exists in AMG's three-decade institutional knowledge of structuring affiliate deals, navigating complex equity arrangements, and managing succession transitions, a capability that would take a competitor years to build. Scale economies are modest: AMG's lean corporate structure benefits from spreading overhead across a large affiliate base, but this is not a scale-driven business. Network effects are limited, and branding matters primarily in the "affiliate acquisition" market rather than with end clients.

Porter's Five Forces paints a more sobering picture of the industry AMG operates in, though AMG's strategic positioning mitigates the worst of it.

Supplier power is high. The key "suppliers" in asset management are the investment professionals themselves, and in the alternatives space, the competition for top talent has become ferocious. Multi-strategy hedge funds like Citadel and Millennium routinely offer guaranteed compensation packages of ten to fifty million dollars or more for proven portfolio managers. This talent war creates persistent wage inflation that compresses margins across the industry. AMG's mitigation is its equity partnership structure, which gives affiliate founders and senior investment professionals a direct ownership stake in their business. This is a fundamentally different retention mechanism than simply paying a higher salary, and it has proven remarkably effective over three decades.

Buyer power is also high. Institutional allocators like pension funds, endowments, and sovereign wealth funds are sophisticated, fee-sensitive, and wield enormous purchasing power. The rise of investment consultants like Mercer, Aon, and Cambridge Associates as gatekeepers has further increased the bargaining power of buyers. Fee compression has been relentless across the industry. AMG's response has been to shift toward alternatives and private markets, where fee sensitivity is lower, strategies are harder to commoditize, and investors are more willing to pay for genuinely differentiated returns.

The threat of substitutes is the most dangerous force in the industry. Passive index funds and ETFs represent the most powerful substitute in investment history. When ninety-three percent of active large-cap managers fail to beat their benchmark over a decade, the case for substitution is overwhelming. Factor-based "smart beta" ETFs further commoditize what was once considered active management. AMG's survival depends on being in categories where passive replication is difficult or impossible, which explains the pivot to alternatives, private markets, and quantitative strategies.

Competitive rivalry is intense. The asset management industry is highly fragmented, with thousands of competitors globally. Performance is publicly measurable, and there is little customer loyalty when results lag. The industry is in structural decline in traditional active equity but growing rapidly in alternatives, where AMG is concentrating its resources.

The threat of new entrants is moderate. Starting a fund is easy; scaling one is extraordinarily difficult. The regulatory requirements, operational infrastructure, institutional due diligence processes, and distribution relationships necessary to compete at scale create significant barriers. AMG's three-decade track record and established affiliate network provide meaningful advantages in this regard.

The net assessment is that AMG operates in a structurally challenging industry but has positioned itself in the most defensible and fastest-growing segments. Its two strongest powers, Cornered Resource and Counter-Positioning, are durable and genuinely difficult for competitors to replicate.

VIII. The Playbook: Lessons for Investors

There are three concepts embedded in AMG's story that have implications far beyond this single company.

The first is that AUM is a vanity metric. The asset management industry is obsessed with assets under management as the primary measure of success. Grow AUM, grow revenue, grow market share. Jay Horgen proved that this logic is deeply flawed. Between 2017 and 2023, AMG's total AUM declined or stagnated. By conventional industry metrics, the company was shrinking. But diluted earnings per share went from twelve dollars in 2017 to over twenty-two dollars in 2025, because Horgen was simultaneously improving the quality of the earnings mix by pivoting toward higher-fee alternatives while aggressively reducing the share count. The investors who fixated on AUM missed the real story: per-share value was compounding even as the top-line footprint contracted.

This is a profoundly counterintuitive concept for most market participants. We are trained to equate growth with value creation. But in a capital-light business like asset management, where the marginal cost of managing an additional dollar is near zero, the relationship between AUM growth and shareholder value is not straightforward. A company that manages five hundred billion dollars in low-fee index products may generate far less economic value per share than a company managing two hundred billion in high-fee alternatives. AMG's transformation is a case study in this distinction.

The second lesson is that AMG does not really buy companies. It buys succession problems. The typical AMG affiliate acquisition begins with a founder who has spent decades building a firm and now faces an uncomfortable reality: they are getting older, they want to monetize their life's work, but they cannot sell to a strategic acquirer without destroying the culture and independence that made the firm valuable in the first place. Going public is expensive, complicated, and subjects the firm to the short-term pressures of quarterly earnings. Selling to a private equity fund means a leveraged buyout, cost-cutting, and an exit timeline that may not align with the founder's wishes.

AMG offers a fourth option: sell a minority stake, get immediate liquidity, solve the succession problem, and continue running the business exactly as before. It is "succession as a service," and it addresses a genuine pain point that has no other elegant solution in the marketplace. As the baby boomer generation of investment firm founders continues to age, the pipeline of potential AMG affiliates is naturally replenishing itself. Every year, another cohort of successful money managers approaches retirement and confronts the same dilemma. AMG has been solving that dilemma for thirty years, and its reputation as a trustworthy, non-interfering partner is its primary calling card.

The third lesson is the power of the minority stake itself. By not owning one hundred percent of its affiliates, AMG keeps the "animal spirits" of the founders alive. A founder who retains the majority of the economics in their business is still motivated to grow, to perform, to build. They are not a hired manager collecting a salary; they are an owner-operator with real skin in the game. This structural choice sacrifices some degree of control for AMG, but it preserves the entrepreneurial energy that made the affiliate valuable in the first place. It is a trade-off that most corporate acquirers are unwilling to make, which is precisely why it works.

For investors monitoring AMG's ongoing performance, two KPIs matter more than any others. The first is the percentage of earnings derived from alternatives and private markets. This number, which stood at approximately fifty-five percent in 2025, is the clearest measure of AMG's strategic transformation. If it continues to climb toward sixty or seventy percent, the market will increasingly view AMG as an alternatives platform rather than a traditional active manager, with significant implications for the valuation multiple. The second KPI is the trajectory of economic earnings per share, which adjusts for the complexities of affiliate equity-method accounting. This metric captures the combined effect of the earnings mix shift and the buyback program, and it is the single best measure of whether Horgen's capital allocation strategy is creating per-share value over time.

IX. Conclusion: The Bear and Bull Case

The bear case for AMG is straightforward and must be taken seriously. Traditional active management remains in structural decline. The passive juggernaut has not slowed down. Even within alternatives, there is a reasonable argument that as more capital floods into hedge funds, private equity, and private credit, returns will compress, fees will come under pressure, and the current golden age of alternatives will eventually look as unsustainable as the golden age of active equity management that preceded it. The multi-strategy pod shops are already showing signs of diminishing returns as the space becomes more crowded. And AMG's holding company structure introduces a "conglomerate discount" that may never fully close: the market has historically struggled to value a company that is essentially a portfolio of minority stakes in independent businesses, each with its own growth trajectory, risk profile, and competitive dynamics.

There are also legitimate accounting complexities that make AMG harder to analyze than a typical company. The equity method of accounting for affiliate investments means that AMG's reported earnings do not always intuitively reflect the underlying cash generation of the business. Revenue recognition across the affiliate base involves judgments about revenue-sharing arrangements that require careful scrutiny. These are not red flags, but they are sources of analytical friction that may keep some investors away.

The regulatory environment also bears watching. If regulators impose new restrictions on private fund marketing to retail investors, or if the semi-liquid vehicle structure faces tighter oversight in the wake of the recent private credit stress, AMG's Pantheon Fund and other wealth channel products could face headwinds.

The bull case is equally compelling. At roughly eleven and a half times earnings and less than seven times EV/EBITDA, AMG trades at a steep discount to virtually every comparable company in the asset management industry. BlackRock commands thirty times earnings. Blackstone trades at forty times. KKR at nearly fifty. Even the troubled Invesco trades at a higher EV/EBITDA multiple. AMG's free cash flow yield exceeds twelve percent, among the highest in the sector. The bull argument is that investors are buying a diversified portfolio of some of the world's best hedge funds, private equity platforms, and quantitative investment firms at a single-digit earnings multiple, run by a CEO with over a hundred and fifty million dollars of personal wealth tied to the stock and a demonstrated track record of disciplined capital allocation.

The buyback program provides a structural floor. As long as AMG continues to generate strong free cash flow and the stock remains at a discount to intrinsic value, Horgen has shown that he will aggressively repurchase shares, compounding per-share value regardless of what happens to AUM. The share count has already been cut in half. There is nothing preventing it from being cut further.

The strategic transformation from traditional active equity to alternatives is real and measurable. The Verition investment positions AMG in the fastest-growing segment of hedge funds. The Pantheon Fund provides a differentiated, less risky approach to private markets democratization than the semi-liquid credit vehicles that are currently under stress. And the core Counter-Positioning advantage, the promise of non-interference that makes AMG the preferred acquirer for boutique founders, remains as durable as ever.

Perhaps the most apt comparison is the one AMG would never make publicly but that thoughtful investors have drawn: is this the Berkshire Hathaway of asset management? A decentralized holding company run by a capital allocator who buys great businesses, leaves them alone, and compounds per-share value through disciplined buybacks and acquisitions. The comparison is imperfect, as all analogies are. Berkshire owns its subsidiaries outright and generates insurance float that AMG does not have. But the philosophical DNA, the belief that the best corporate strategy is to find excellent operators, give them autonomy, and allocate capital wisely, is strikingly similar.

Whether the market ultimately embraces this comparison or continues to value AMG as a traditional active manager in decline is the central question for investors. The answer will depend on whether AMG's transformation proves as durable as its leadership believes, and whether the market eventually looks past the AUM headline and sees the earnings engine underneath.

X. References and Further Reading

The Outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success by William Thorndike.

AMG Investor Day presentations, particularly the materials detailing the strategic shift toward alternatives and private markets.

AMG Annual Reports and SEC filings (10-K, Proxy Statement), which provide detailed disclosure on affiliate economics, revenue-sharing structures, and executive compensation.

Morningstar Active/Passive Barometer, for data on active manager survival rates and performance relative to passive benchmarks.

Cliff Asness's published research and white papers on factor investing, the "value winter," and the challenges facing quantitative strategies.

Hamilton Helmer, 7 Powers: The Foundations of Business Strategy, for the framework on durable competitive advantage.

Michael Porter, Competitive Strategy, for the Five Forces framework applied to the asset management industry.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube