Amcor plc: The Consolidation of the Global Packaging Empire

I. Introduction & Episode Roadmap

Pick up almost anything in a supermarket—a pouch of coffee, a blister of pills, a squeeze bottle of ketchup, a sterile film sealing a tray of chicken—and there is a meaningful chance you are holding a product of a company most shoppers have never heard of. That anonymity is the point. Packaging is the ultimate invisible infrastructure of consumer capitalism: nobody buys the wrapper, everybody depends on it, and the best players in the business make their money precisely by being taken for granted. Amcor plc is the largest of them all.

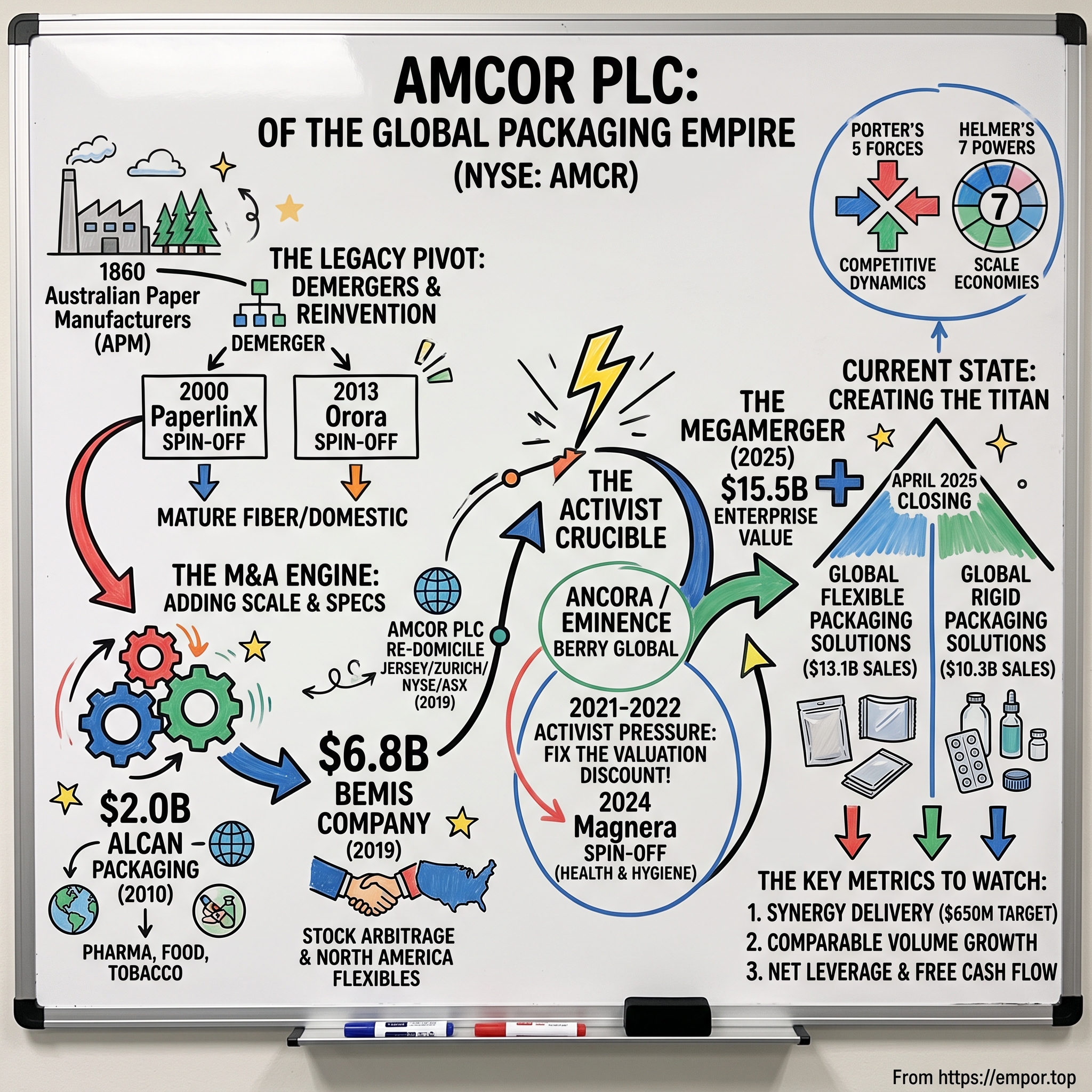

Here is the puzzle worth sitting with. How does a regional Australian paper mill, born in the Victorian gold-rush era of 1860, end up more than a century and a half later as a Zurich-headquartered, Jersey-domiciled, New York-listed packaging colossus with roughly $24 billion in annual sales? The corporate genome contains an Australian founding, a British tax domicile, a Swiss operational home, and an American stock ticker—AMCR on the NYSE—stapled together by four decades of demergers, cross-border acquisitions, and, most recently, the single largest deal in the history of the packaging industry.1

The scale that emerged from that final deal is genuinely difficult to picture. Following the April 2025 combination with America's Berry Global, Amcor operates on the order of 400 production facilities across more than 140 countries and employs roughly 70,000 people.1 It is the king of the grocery aisle and the pharmacy cabinet at once—supplying the flexible films, rigid containers, closures, dispensing pumps, and medical barriers that keep the world's consumer goods fresh, sterile, and sealed. When Nestlé, Unilever, or a global pharmaceutical company needs several billion identical, spec-perfect packages delivered on time across four continents, the list of vendors who can even bid is very short. Amcor engineered itself to sit at the top of that list.

But scale alone is not a story, and it is certainly not an investment case. The interesting question for a long-term owner is not how big Amcor is—it is whether size in packaging is a durable advantage or merely an expensive way to look impressive. This is a low-growth, capital-intensive, commodity-exposed industry where the end customers are some of the most ruthless procurement organizations on earth. So we will spend the next several hours pressure-testing the machine rather than admiring it.

There is a temptation, when a company reaches this size, to assume that bigness itself is the moat—that 400 factories and 140 countries must add up to an unassailable position. Resist that instinct. The graveyard of industrial history is full of enormous companies that mistook scale for safety: steel, textiles, commodity chemicals, and, closer to home, the commodity paper business that Amcor itself deliberately abandoned. Size can be a genuine advantage in packaging—as we'll see, it lowers input costs and spreads research spending—but it can equally be a trap that ties up capital in low-return assets and tempts management into value-destroying empire-building. The whole point of this episode is to separate the parts of Amcor's scale that genuinely compound from the parts that merely accumulate.

It also helps to name, up front, the three numbers that will actually adjudicate this story over the next several years, because everything else is context around them. First, synergy delivery: is the company banking the promised savings from the Berry merger on or ahead of schedule? Second, comparable volume growth: are real units of packaging moving, stripped of commodity-price noise? And third, net leverage and free cash flow: is the debt taken on to build this empire coming down fast enough to restart shareholder returns? Keep those three in your pocket. By the end, you'll understand exactly why they, and not the headline revenue figure, are the dials that matter.

Here is the roadmap for how we get there:

- The Legacy Pivot. How an Australian paper monopoly deliberately shed its own history—spinning off PaperlinX in 2000 and Orora in 2013—to reinvent itself as a focused global plastics-and-flexibles company.

- The M&A Engine. How Amcor learned to grow by buying, acquiring Rio Tinto's Alcan Packaging for roughly $2.0 billion in 2010 and merging with Wisconsin's Bemis Company in an all-stock deal worth about $6.8 billion in 2019.

- The Activist Crucible. How hedge funds Ancora and Eminence Capital cracked open rival Berry Global from the inside in 2021–2022, setting up the marriage that followed.

- The Megamerger. The mechanics, the math, and the debt of the 2025 combination—and the $650 million synergy promise now being audited quarter by quarter.

- The Economic Moat. The unit economics, the index-linked resin "pass-through" plumbing, and an honest tour through Hamilton Helmer's 7 Powers and Porter's 5 Forces—including where the moat is thinner than management would like you to believe.

Let's start where the story starts: not with plastic, but with paper.

II. The Legacy Pivot: From APM to the Great Demergers (1860–2013)

Begin in colonial Victoria, in the decade when the gold rush was minting fortunes and building a settler economy that suddenly needed to wrap, box, and print things. In 1860, the enterprise that would eventually become Amcor was founded as a paper manufacturer, and for the next hundred-plus years it did the most unglamorous thing imaginable extraordinarily well: it made paper and cardboard for a captive continent.1 Under the banner of Australian Paper Manufacturers—APM—it grew into a dominant domestic producer, and geography was its greatest ally. Australia is a long way from everywhere. Shipping heavy, low-value paper across oceans made no economic sense, so a local champion protected by distance and, in the postwar decades, by tariffs, could earn comfortable returns without ever facing a truly hungry foreign competitor.

This is the first thing to understand about Amcor's DNA: it was born into a protected monopoly mindset. That is a wonderful place to make money and a dangerous place to learn habits. Capital-intensive commodity manufacturing behind a tariff wall rewards scale and cost control, not agility or innovation. For a century, the company optimized for the former.

To feel the weight of that history, picture the physical business. Paper and cardboard are heavy, bulky, low-value goods—the economics are dominated by freight and by the enormous fixed cost of the mills themselves. A paper mill is a cathedral of capital: it runs continuously, it cannot be easily switched off, and it demands to be fed with pulp and run near full capacity or it bleeds money. A company built around such assets learns a particular kind of discipline—squeeze the plant, protect the volume, defend the region—but it does not naturally learn how to innovate at the pace of consumer trends or how to serve a demanding multinational brand across a dozen countries at once. The company that would become a global packaging leader had to un-learn as much as it learned.

The world that made APM comfortable began to dissolve in the 1980s, as Australia dismantled tariff protection and its corporates were forced to think globally or shrink. In 1986 the company rebranded as Amcor, a deliberate signal that it no longer saw itself as merely a paper business. The new name accompanied diversification into metals, glass, and—crucially—plastic packaging, along with the first serious steps offshore.1 The rebrand was cosmetic in the way all rebrands are, but the strategic intent underneath it was real: management had begun to sense that the future of packaging value lay not in the heavy fiber businesses of the past but in higher-specification materials sold to multinational consumer-goods companies.

Then came the two decisions that define this chapter—and, arguably, the entire modern company. Amcor did not transform by adding. It transformed by subtracting.

Demerger One arrived in 2000, when Amcor spun off its traditional paper and fine-paper distribution business as a separately listed company, PaperlinX. The logic was cold and correct. Commodity paper manufacturing is brutally cyclical, wildly capital-hungry, and structurally low-return; it consumed cash and depressed the parent's valuation multiple. By cutting it loose, Amcor handed shareholders a pure exposure to a declining business while keeping for itself the parts with better economics. PaperlinX's subsequent long decline—it struggled for years before effectively disappearing—served as a grim vindication of the decision to let go.

Demerger Two, in 2013, was the more consequential and more emotionally difficult amputation. Amcor demerged Orora, the company that held its legacy Australasian fiber, glass, and beverage-can packaging operations—in other words, the businesses closest to Amcor's own historical heart. The rationale, once again, was about focus and returns. Australasia was a mature, slow-growth, capital-intensive market; keeping it inside the company diluted growth and tied up capital that could earn more elsewhere. Spinning off Orora left Amcor as a genuine "pure play" on international flexible and rigid plastic packaging, unencumbered by the low-multiple domestic assets that had anchored it to its past.

There was a cultural dimension here that mattered as much as the financial one. Demerging Orora shifted the company's center of gravity decisively away from Australia and toward the high-volume consumer-packaged-goods hubs of North America, Europe, and the emerging markets, where the real growth in branded consumer products was happening. The company that had spent a century as an Australian institution was choosing, in effect, to stop being primarily Australian. That reorientation is what made everything that followed possible.

It is worth pausing on how unusual this instinct is at the board level. Corporate history overwhelmingly runs the other way: management teams accumulate, they diversify, they cling to legacy divisions out of sentiment and organizational politics, and they justify the sprawl with the language of "synergy" and "balance." The academic literature even has a name for the value destruction that results—the conglomerate discount—and a memorable coinage from investor Peter Lynch for the disease that causes it: "diworsification," the tendency of companies to wander into businesses that dilute rather than strengthen their core. Amcor did the opposite. Twice, in the span of thirteen years, it handed its own shareholders a piece of its history and told them, in effect, "you can own this if you want, but we are going to focus." That is a governance signal—an institutional willingness to shrink in order to improve—and it is the single most attractive thing in the company's long-run track record. Whether the current management has inherited that discipline or merely its rhetoric is a question we will return to when we reach the $2.5 billion non-core review.

The pattern established across these two demergers is the single most important thing to carry forward: Amcor's leadership repeatedly demonstrated a willingness to sell or spin the businesses it had grown up with in order to concentrate on the businesses with better returns. That is rarer than it sounds; most management teams are sentimental about legacy assets and destroy value defending them. Amcor built a muscle for unsentimental portfolio surgery. Hold that thought—because a decade later the company would identify $2.5 billion of its own current revenue as non-core and put it under the same knife.

Having stripped itself down to a focused packaging platform, Amcor faced a new problem. Focus is not the same as scale, and in a business where scale is the moat, the company that had learned to subtract now had to learn to add.

III. The M&A Engine: Alcan (2010) & the Bemis Arbitrage (2019)

If the demergers taught Amcor what it wanted to be, the acquisitions taught it how to become large enough to matter. And the education began even before Orora was spun off, with a purchase that instantly changed the company's weight class.

In 2010, Amcor reached into the wreckage of the global financial crisis and bought Alcan Packaging from Rio Tinto for roughly $2.0 billion. The backstory is one of those deals made possible by someone else's indigestion: Rio Tinto had acquired the Canadian aluminum group Alcan at the top of the commodity cycle in 2007, loaded itself with debt, and then spent the crisis years selling non-core pieces to survive. Alcan's packaging division—prized global assets in pharmaceutical, food-Europe, and tobacco packaging—was exactly the kind of high-specification, high-barrier business Amcor coveted, and it came available at a moment when few buyers had the balance sheet or nerve to act.1

The strategic payoff was immediate and structural. Alcan roughly doubled Amcor's flexible-packaging footprint in Europe and Asia in a single stroke and, more importantly, handed it a genuinely world-class global pharmaceutical and medical packaging division. That last point is the one to underline. Medical and pharma packaging is not a commodity; it is a regulated, validated, deeply sticky business where switching suppliers is slow and expensive. Alcan gave Amcor a durable, high-margin core that would anchor the entire company's quality for the next fifteen years. It was the acquisition that proved Amcor could digest a large, complex, cross-border business and come out stronger—the confidence-builder for everything that followed.

The Alcan deal also seeded a management philosophy that would harden into doctrine: growth by acquisition, funded by disciplined synergy capture, executed by an integration team that treated the first year after a close as a manufacturing process rather than a celebration. In the decade after Alcan, Amcor built an internal capability around exactly this—identifying overlapping plants, standardizing procurement, and consolidating overhead—that became, arguably, its most valuable non-physical asset. A company that has integrated a large acquisition well is far more likely to be handed the next one by nervous sellers, because it can credibly promise to extract value the target could not extract itself. Alcan, in other words, did not just add assets; it added a reputation for being able to swallow assets. That reputation is precisely what made Amcor the natural home for Bemis, and later for Berry.

Which brings us to the deal that solved Amcor's single most glaring weakness: America.

For all its global reach, Amcor had a hole in its map. In North American flexible packaging—the largest, richest consumer-packaging market on earth—it lacked scale. The undisputed leader there was Bemis Company, a quietly excellent, century-old flexible-packaging specialist headquartered in Neenah, Wisconsin, with deep relationships across American food and healthcare brands. Amcor could not out-compete Bemis on its home turf. So in 2019, it did the next best thing: it merged with it.

The Bemis combination was an all-stock transaction valued at an enterprise value of roughly $6.8 billion, and the financial engineering underneath it is worth slowing down for, because it reveals how Amcor thinks about using its own shares as a weapon.1 Here is the core idea in plain terms. A company's stock is a currency, and like any currency, its purchasing power depends on its exchange rate—in equities, that "rate" is the valuation multiple. Amcor's shares historically traded at a premium multiple, in the neighborhood of 11 times EV/EBITDA, reflecting its global scale and quality mix. Bemis traded at a lower multiple. When a higher-multiple company buys a lower-multiple company using its own richly valued stock, the arithmetic of blending the two produces immediate earnings accretion—the acquirer is effectively buying cheaper earnings with expensive paper. Layer on more than $180 million in targeted annual cost synergies from combining overlapping plants and overhead, and the deal was accretive almost by construction.1

Now, a neutral observer should register the obvious caveat: multiple arbitrage is real, but it is not the same thing as creating operating value. Buying lower-multiple earnings with higher-multiple stock flatters per-share numbers on day one, yet it only builds durable value if the acquirer actually harvests the synergies and does not simply import the target's lower-quality economics. Accretion is a promise, not a result. Amcor, to its credit, largely delivered the Bemis synergies—but the pattern of leaning on stock-for-stock arbitrage is one to watch, because the company would run the exact same playbook, at four times the size, six years later.

There is a human coda to the Bemis era worth recording, because it shapes the leadership story later. The CEO who drove the Bemis integration and set Amcor's post-merger tone was Ron Delia, a finance-trained executive who had risen through the company's ranks and become chief executive in 2015. Under Delia, Amcor cultivated the identity it still trades on today: a disciplined, cash-generative, dividend-reliable operator that treats capital allocation as the main event. His retirement for health reasons in April 2024—right on the eve of the largest deal in the company's history—handed the wheel to a new generation at the worst possible moment for continuity, a transition we'll examine when we meet the current management.

The Bemis deal did something else structurally important: it re-domiciled the company. To close the merger and optimize for its now heavily American shareholder base, the group reincorporated as Amcor plc in Jersey, in the Channel Islands, listed primarily on the New York Stock Exchange under AMCR, and maintained a secondary listing on the Australian Securities Exchange through CHESS Depositary Interests under AMC—while running global headquarters out of Zurich, Switzerland.1 Read that sentence again and appreciate the deliberate rootlessness of it: an Australian-heritage company, incorporated in a British tax jurisdiction, operationally headquartered in Switzerland, and trading primarily on Wall Street. This is not an accident of history; it is a tax- and capital-markets-optimized structure, and it is exactly the sort of arrangement a skeptical investor should note when thinking about governance, disclosure regime, and where accountability actually sits.

Why should an investor care about corporate plumbing that looks, at first glance, like a lawyer's diagram? Because domicile shapes taxes, shareholder rights, takeover defenses, and the very rules under which the company reports to its owners. A Jersey-incorporated, NYSE-listed company operates under a particular blend of Channel Islands company law and U.S. securities regulation that differs in subtle but real ways from a plain American incorporation—affecting everything from how easily a hostile bidder could act to what disclosures are mandatory. None of this is sinister; multinationals optimize these choices routinely, and Amcor's structure is a rational response to having a globally dispersed shareholder base after Bemis. But a neutral analyst files it as a fact to monitor rather than a detail to ignore, because rootless structures concentrate accountability loosely, and loose accountability is exactly the soil in which governance problems grow. The activists who reshaped Berry understood this instinctively; governance is never neutral.

By 2019, then, Amcor had assembled a formidable global flexible-and-rigid platform on both sides of the Atlantic. It looked, from the outside, like a completed company. But across the American Midwest, a rival was building a rigid-plastics empire of its own—and it was about to be torn open by outsiders in a way that would deliver Amcor its final, largest prize.

IV. The Activist Crucible: How Ancora & Eminence Forced the Marriage

To understand the 2025 megamerger, you have to understand that it did not originate in Amcor's boardroom at all. It originated in the frustration of hedge-fund managers staring at a chronically undervalued stock in Evansville, Indiana.

That stock was Berry Global Group, and on paper it should have been a winner. Berry had spent two decades rolling up the fragmented world of rigid plastics—cups, bottles, closures, dispensing systems, nonwovens, and specialty films—into a genuine giant of the industry. It was big, it was operationally competent, and it served the same consumer-goods customers Amcor did.

And yet its shares languished. The market looked at Berry and saw two things it disliked: a heavy debt load accumulated through serial acquisitions, and a sprawling, hard-to-love portfolio that mixed attractive consumer-packaging businesses with lower-quality hygiene and nonwovens assets. The result was a persistent valuation discount. By the early 2020s Berry traded around 7.7 times EV/EBITDA against Amcor's ~11 times—a gap that told you the market trusted one management team's capital allocation far more than the other's.

That valuation gap is the entire engine of this chapter, so it's worth understanding what it actually represents. A lower multiple is not an accounting fact; it is the market's verdict on trust. When investors pay 7.7 times a company's earnings while paying 11 times another's, they are saying they believe the second company's cash flows are safer, more durable, or better managed—and they are pricing in a discount for the first company's debt, complexity, and history of aggressive M&A. For an activist, a persistent, unjustified discount is an invitation. If you believe the underlying assets are fine and only the wrapper—the leverage, the portfolio sprawl, the governance—is depressing the price, then closing that gap is a straightforward value-creation thesis: fix the wrapper, and the multiple should re-rate toward the peer. That was precisely the bet Ancora made.

Enter the activists. In November 2021, Ancora Holdings—a Cleveland-based activist fund—went public with a campaign demanding that Berry's board explore strategic alternatives, up to and including an outright sale, and overhaul its approach to capital allocation.6 Ancora's thesis was blunt and, frankly, hard to argue with: Berry was a good collection of assets trapped inside a bad valuation, run by a board that was buying back stock and making acquisitions rather than confronting the discount head-on. The activists wanted the discount closed, and they did not much care whether that happened through a sale, a break-up, or a wholesale change in strategy.

Berry did what cornered companies usually do when a credible activist arrives with a coherent argument: it negotiated. In March 2022, Berry settled with Ancora and a second activist, Eminence Capital, agreeing to add three new independent directors backed by the funds and to establish a dedicated Capital Allocation Committee.[^8] This is the pivotal, under-appreciated moment of the whole saga. Settlements like this are often dismissed as face-saving truces, but this one installed activist-aligned directors directly onto the board and created a formal committee whose entire job was to keep asking the uncomfortable question: is this portfolio worth more together or apart? Once that question is institutionalized at the board level, a company's strategic trajectory changes. The pressure to do something becomes permanent.

What followed was a methodical unwinding. Under the new governance regime, Berry began simplifying its portfolio—shedding complexity rather than adding it. The culmination came in late 2024, when Berry spun off and merged its volatile Health, Hygiene & Specialties nonwovens-and-films business with Glatfelter, creating a separately listed company renamed Magnera. Strip away the corporate jargon and the move was surgical: Berry excised the lowest-quality, most cyclical piece of itself—the exact piece the market had been penalizing—and handed it to shareholders as a standalone entity.

With the hygiene albatross gone, what remained inside Berry was a cleaner set of rigid-packaging, closures, and specialty-film businesses that looked far more like Amcor's world. And now the logic that the activists had forced onto the board reached its natural endpoint. A leaner Berry was not just easier to value; it was easier to sell. An all-stock combination with Amcor offered the ultimate route to closing the valuation gap: legacy Berry holders would exchange their discounted shares for stock in a larger, higher-multiple, more diversified company, while the combined entity could strip out duplicative corporate overhead and wield genuinely world-class purchasing scale against resin suppliers. The activists had, in effect, spent three years renovating Berry into an ideal acquisition target—and then delivered it to the one buyer with the strategic fit and the currency to close.

There is a broader lesson embedded here about how modern corporate control actually works. The popular image of activist investors is of raiders demanding buybacks and quarterly cost cuts—short-term vandals in pinstripes. But the Berry episode shows the more consequential version of the craft: patient activists who reshape a board, install a capital-allocation committee, and then let institutional pressure do its slow work over years until a company that would never have sold itself becomes a company that wants to. Ancora and Eminence never operated Berry's plants or negotiated its resin contracts. They simply changed who sat in the boardroom and what questions got asked there, and that was enough to redirect a multi-billion-dollar enterprise into the arms of a strategic acquirer. For anyone trying to understand where corporate mega-deals come from, that mechanism—governance pressure as the true prime mover—is worth internalizing.

The neutral read here is important. This was not a case of Amcor cleverly spotting a bargain the market had missed. It was a case of outside pressure manufacturing a seller, and Amcor being the obvious counterparty standing in the right place at the right time. That distinction matters for how you weigh management's role in the value creation to come: much of the hard, unglamorous work of making Berry acquirable was done by hedge funds, not by Amcor. What Amcor had to prove was that it could integrate the prize without choking on it—and, crucially, that it would not overpay in the enthusiasm of finally landing the American rigid-plastics scale it had wanted for years. Strategic buyers with a long-held wish list are exactly the buyers most prone to paying too much when the object of desire finally comes up for sale.

V. The Megamerger of 2025: Creating the Packaging Titan

On the morning of November 19, 2024, Amcor and Berry Global announced a definitive agreement to combine in an all-stock deal—the packaging industry's marriage of the decade, and the largest transaction the sector had ever seen.1 Five and a half months later, on April 30, 2025, the merger closed, bringing into existence a combined enterprise valued at roughly $37 billion and instantly reordering the global competitive landscape.2

The choreography between announcement and close is itself instructive about how these deals actually get done. A transaction of this size is not simply agreed and executed; it must clear shareholder votes on both sides and antitrust review in every major jurisdiction where the two companies overlap. In June 2025's rearview, that gauntlet was run successfully—shareholders of both companies approved the combination by wide margins, and regulators, evidently persuaded that a packaging industry with several credible global players remained competitive, cleared it without deal-breaking divestiture demands. The relatively smooth regulatory path tells you something quietly important about the industry structure: even the combination of two giants did not create the kind of dominant single supplier that antitrust authorities block, because the world's largest CPG buyers retain enough alternatives and enough purchasing power to keep the market honest. That same fact, as we'll see, is also the ceiling on Amcor's pricing power.

Let's walk through the actual terms, because the structure tells you what each side thought it was getting. Berry shareholders received a fixed exchange ratio of 7.25 Amcor shares for every Berry share they held.1 "Fixed" is the operative word: the ratio was locked, so Berry holders took on full exposure to Amcor's share-price movements between announcement and close rather than being guaranteed a set dollar value—a structure that signals both sides wanted the deal to be a true merger of ongoing owners, not a cash-out. When the dust settled, legacy Amcor shareholders owned approximately 63% of the combined company and legacy Berry shareholders approximately 37%.1 Amcor was unambiguously the acquirer and the surviving culture; Berry holders became large minority partners in a bigger vehicle. That ownership split also carried the activist DNA forward: the Berry shareholder base, seasoned by three years of governance pressure, now held better than a third of a much larger company, and their expectations for capital discipline traveled with their shares.

Now the valuation, and here is where a neutral analyst should hold two ideas at once. The transaction valued Berry at roughly 9.0 times EV/EBITDA, built from an equity value near $8.4 billion and an enterprise value around $15.5 billion once you add Berry's substantial net debt of roughly $7 billion. On its face, 9 times is a reasonable price—below Amcor's own historical multiple and broadly in line with where packaging deals have cleared, so Amcor was not obviously overpaying. This is the multiple-arbitrage playbook from the Bemis deal, run at scale: use a higher-rated currency to acquire a lower-rated business and let the blend do the work.

But notice what that clean 9-times headline quietly absorbs: the ~$7 billion of Berry debt that came along for the ride. The equity price looks modest precisely because Amcor was also assuming a mountain of borrowings. This is the crux of the bear case on the deal, and we should not let the tidy multiple obscure it. A merger financed with paper does not raise cash to pay down debt; it simply pools two companies' obligations onto one balance sheet. Which is exactly what happened.

The merger pushed Amcor's net leverage to roughly 3.3 to 3.5 times net debt to EBITDA—well above the company's own conservative through-cycle target of 2.5 to 3.0 times. The consequence was concrete and unwelcome to income-oriented shareholders: Amcor suspended its active share-buyback program to prioritize paying the debt back down. For a company that had long marketed itself as a disciplined, shareholder-friendly capital allocator, temporarily parking buybacks to service a leverage spike is precisely the kind of "aggressive capital allocation after promises of discipline" that a skeptical investor is entitled to flag. It is defensible—deleveraging is the right priority—but it is a real cost, and it constrains the company's flexibility for as long as the leverage stays elevated.

Against that cost sits the promise that justifies the whole exercise: synergies. Management committed to $650 million in annual run-rate pre-tax earnings synergies by the end of Year 3—fiscal 2028—drawn from three buckets that are worth distinguishing.1 The first is corporate and general-and-administrative reduction: two headquarters, two boards, two sets of public-company overhead collapse into one. The second is procurement: a combined company buying resin and aluminum at even greater volume squeezes better prices from suppliers. The third, and the hardest, is operational and footprint optimization—rationalizing overlapping plants and supply chains, which takes years and risks disrupting customers if botched. The first two buckets are relatively low-risk and fast; the third is where integrations usually stumble.

So the essential question for any owner of AMCR today is not whether the synergies exist on a slide, but whether management is actually banking them on schedule. And here the early evidence is genuinely encouraging. On the Q3 fiscal 2026 earnings call on May 6, 2026, management reported delivering roughly $170 million in synergies across the first nine months of the fiscal year—including about $77 million in the quarter itself—and raised the full-year target to around $270 million, above the initial $260 million Year-One goal.34 The savings came predominantly from the low-risk buckets first—G&A elimination and procurement—which is exactly the sequencing you would want to see: bank the certain money early, prove the model, and build credibility before tackling the harder footprint work.

Delivering ahead of a Year-One target is the single most important trust signal management has offered since the deal closed. It does not prove the full $650 million will land by fiscal 2028—the hardest synergies are still ahead—but it establishes that the team can set a number and beat it, which is the currency of credibility in an integration this size. The market will be watching each subsequent quarter to see whether that early lead holds as the easy savings are exhausted and the operational surgery begins.

A word of caution belongs here, though, because synergy accounting is one of the most gameable disclosures in corporate finance. "Run-rate synergies" are a management-defined figure, not an audited line item, and the temptation to present gross savings while quietly absorbing the costs of achieving them—the severance, the plant-closure charges, the systems integration—is real across the merger landscape. The right posture for an investor is to treat the synergy scoreboard as a directional signal to be cross-checked against the numbers that cannot be dressed up: reported margins, actual free cash flow, and the trajectory of net debt. If the synergies are as real as management says, they should eventually show up not as a bullet on a slide but as expanding EBIT margins and accelerating debt paydown. If they show up only on the slide, that gap is the story. So far, the early evidence leans genuine—but "so far" is doing a lot of work in a three-year plan that is barely one year old.

Which raises the natural next question: what does this combined titan actually look like on the inside, and who is running it?

VI. Current State: Segments, Portfolio Optimization, & New Leadership

Walk into the combined Amcor of 2026 and the first thing you notice is that the company reorganized itself around a simple, honest distinction: things that bend and things that hold their shape. The old corporate silos of two separate companies collapsed into two global segments defined by material physics.

Global Flexible Packaging Solutions, with combined sales on the order of $13.1 billion, is the larger and higher-margin heart of the business. It fuses Amcor's legacy flexibles—the pouches, films, and laminates that dominate food and healthcare packaging—with Berry's flexible operations. This is the innovation-heavy core, home to the multi-layer barrier films and validated medical packaging that carry the fattest margins and the stickiest customer relationships. Global Rigid Packaging Solutions, at roughly $10.3 billion in combined sales, brings together Amcor's legacy rigid containers with Berry's consumer-packaging franchises in North America and internationally—the bottles, jars, cups, closures, and dispensing systems that were Berry's specialty.3 In one stroke, the merger gave Amcor a commanding position in closures and dispensing—the pumps and caps on everything from shampoo to salad dressing—that it had never possessed at scale before.

But segment charts are the least interesting part of the current story. The more revealing move is what management is doing with the portfolio, because it echoes the demerger discipline of the company's past. Leadership has publicly divided the combined group into a core portfolio of roughly $20 billion in sales—concentrated in the higher-growth, higher-margin end-markets of healthcare, beauty, protein and other foods, pet care, liquids, and foodservice—and a non-core bucket of about $2.5 billion in annual sales earmarked for divestiture, partnership, or restructuring, with the legacy North American beverage business the marquee candidate.3

This is the old "demerge to dominate" muscle flexing again, and it deserves both credit and scrutiny. On the credit side: a management team that, fresh off swallowing a $15 billion acquisition, is already naming 10% of its own revenue as something it would rather not own is behaving like a disciplined portfolio manager rather than an empire-builder. On the scrutiny side: identifying non-core assets is easy; selling them at good prices into a soft market is hard, and low-quality packaging assets like commodity beverage containers do not always fetch attractive multiples. The $2.5 billion review is a promise to watch, not a result to bank. If those disposals stall, the "core $20 billion" narrative starts to look more like a slide than a strategy.

The strategic logic of the core/non-core cut is sound and worth spelling out, because it explains where Amcor wants its future to come from. The "core" end-markets management has ringed—healthcare, beauty, protein and premium foods, pet care, liquids, foodservice—share a common feature: they are categories where the package is functionally critical and often premium-priced, where barrier performance, dispensing convenience, or regulatory validation lets the packaging supplier add real value rather than merely wrap a commodity. A protein tray that extends shelf life, a beauty pump that meters a luxury serum, a healthcare film that keeps a device sterile—these command better margins and stickier relationships than a generic water bottle or a commodity beverage can. Pushing capital toward the former and away from the latter is precisely the mix-shift that could, over time, lift the whole company's margin structure. The bet is coherent. The open question, as always with Amcor, is execution: strategy on a slide is free, and disposals at fair prices are not.

One piece of housekeeping that matters more than it sounds: Amcor is shifting its fiscal year-end from June 30 to December 31 to align with the calendar year, with a transition "stub period" running from July 1 to December 31, 2026. Stub periods are administratively dull but analytically treacherous—they scramble year-over-year comparisons and can be used, at some companies, to obscure trends. It is worth flagging simply so that investors reading the FY2026 and transition-period numbers do not mistake calendar artifacts for real operational change.

Now the humans. Every merger integration is ultimately a test of the people running it, and Amcor's are relatively new to their chairs—which is itself a risk factor worth naming.

Peter Konieczny became permanent chief executive in September 2024, having stepped up as interim CEO in April 2024 when his predecessor, Ron Delia, retired for health reasons.[^5] Konieczny is not a parachuted-in outsider; he is a roughly fifteen-year Amcor veteran who ran the company's commercial organization as Chief Commercial Officer before ascending to the top job. That deep institutional knowledge is an asset in an integration of this complexity—he knows where the company's bodies are buried and how its customers think. It is also, from a governance lens, a continuity appointment rather than a fresh perspective, and his personal ownership stake is modest, on the order of 0.03% of shares outstanding, meaning his alignment with shareholders runs mostly through his incentive compensation rather than through a founder-sized equity position. His pay is heavily weighted toward adjusted EPS growth, free cash flow, return on invested capital, and sustainability metrics—a structure that, on paper, points him at the right targets, though EPS-linked pay during a synergy-driven integration always carries the mild hazard of rewarding financial engineering as much as operating excellence.

Konieczny's background repays a closer look, because a commercial chief and a finance chief run companies very differently. Having spent his Amcor career on the commercial side—closest to the customers, the contracts, and the pricing—he is, by formation, a relationship-and-revenue executive rather than a spreadsheet operator. In an integration whose gravest risk is customer churn during the transition, that commercial fluency is genuinely valuable: the CEO best positioned to reassure a nervous Nestlé or a wavering Procter & Gamble is one who has sat across the table from them for fifteen years. The counterpoint is that the hardest work ahead—footprint rationalization, plant closures, balance-sheet repair—is fundamentally operational and financial, not commercial. Which is almost certainly why the board went looking for a very particular kind of CFO.

His new financial partner arrived more recently and from outside the family. Stephen Scherger became chief financial officer effective November 10, 2025, succeeding Michael Casamento, who stepped down after a decade as CFO to return home to Australia and agreed to stay on as an adviser through mid-2026 to smooth the handoff.5 Scherger's résumé is the tell: he spent roughly a decade, from 2015, as CFO of Graphic Packaging International, a large NYSE-listed fiber-based packaging peer.5 Hiring a sitting CFO away from a direct sector competitor, at the precise moment you are trying to integrate a $15 billion acquisition and deleverage a stretched balance sheet, is a pointed choice. It signals that the board wanted a finance chief who already understands packaging capital allocation, plant footprints, and integration mechanics cold—someone who would not need a year to learn the industry. Whether the Konieczny–Scherger pairing can convert an on-paper synergy plan into sustained returns is the central execution question of the next three years, and it is being asked of a leadership duo that has been working together for only a matter of months.

To judge whether they succeed, though, you need to understand the strange contractual machinery that governs how a packaging company actually makes—and sometimes loses—money. That machinery is the resin pass-through, and it is the least understood, most important thing about this business.

VII. Materiality, Unit Economics, & the Contractual Plumbing

Here is a fear that keeps a certain kind of investor up at night: Amcor's core raw materials are polymers—polyethylene, polypropylene, PET—and aluminum, all of which are derived from oil, gas, and volatile commodity markets. If a packaging company simply bought resin at market prices and sold finished packaging at fixed prices, it would be running an enormous, unhedged bet on the price of crude. A resin spike would vaporize its margins overnight. So how does a company with $24 billion of commodity-linked revenue not get destroyed every time oil moves?

The answer is the single most important mechanical fact about the packaging business, and it is almost invisible from the outside: the contractual pass-through. Amcor does not, for the most part, take outright commodity risk. The great majority of its volume—on the order of 75% or more of its contracts—is written with automatic, index-linked pricing mechanisms.1 In plain English: the contracts contain a formula that says, roughly, "the price we charge you rises and falls automatically with a published index of resin prices." If polyethylene surges, the higher cost flows through, contractually and without renegotiation, to the consumer-goods giant on the other side of the table—the Nestlés and Unilevers and Coca-Colas of the world—and ultimately to the shopper at the shelf.

Think of Amcor less as a bettor on commodity prices and more as a toll booth. It converts resin into engineered packaging and collects a spread for the value it adds—the material science, the barrier performance, the reliability, the global logistics. The underlying resin cost is largely a pass-through, not a risk position. This is the mechanism that lets a commodity-exposed company earn stable, predictable margins across wildly different oil-price environments, and it is the foundation of the "defensive consumer staple" quality that income investors prize in the stock. It is the reason a packaging business can be dull and dependable rather than cyclical and terrifying.

There is a subtler consequence of the toll-booth model that investors frequently misread, and it concerns the shape of revenue. When resin prices spike, Amcor's reported revenue rises—not because it sold more packaging, but because the pass-through mechanically inflates its selling prices. When resin prices collapse, reported revenue falls for the same non-reason. This means the top line is a poor guide to how the business is actually doing; a quarter of "declining sales" can coincide with rising unit volumes and healthy demand, simply because resin got cheaper and dragged the pass-through prices down with it. This is exactly why disciplined analysts of packaging companies fixate on volume rather than revenue, and why Amcor management guides the market to comparable volume growth as the real scoreboard. If you only ever looked at Amcor's headline revenue line, you would routinely draw the wrong conclusion about the health of the business.

But—and this is where the neutral analyst earns their keep—the shield is not perfect, and its imperfection is a recurring source of quarterly noise. The pass-through operates on a lag, typically one to three months. The contractual formulas reset prices periodically, not instantaneously, so when resin costs move fast, there is a window where Amcor's selling prices have not yet caught up to its input costs. During bouts of rapid input-cost inflation—the 2022–2023 period is the textbook case—this timing lag caused temporary but real margin compression: Amcor was buying dear and still selling at yesterday's cheaper contracted prices, and it simultaneously had to fund more expensive inventory, straining working capital. The mechanism runs in reverse, too. In a deflationary resin environment, Amcor's selling prices stay high for a beat while its input costs fall, and the company captures a temporary margin windfall before the formulas ratchet prices back down.

The investor's takeaway is subtle but crucial: do not over-react to margin swings that are really just the pass-through lag breathing in and out. A quarter of compressed margins during a resin spike is not evidence that the business is broken; a quarter of fat margins during a resin collapse is not evidence that it has suddenly gotten better. The lag is noise around a stable structural spread. What actually matters for the long-term owner is volume—how many units of packaging are moving—because volume, not the pass-through, reflects genuine end-demand and competitive share.

Which is exactly why the operating metrics management guided to in mid-2026 are worth reading with a cold eye. In Q3 fiscal 2026, comparable volumes contracted by roughly 1.5%, a sequential softening that management attributed partly to U.S. winter-storm disruptions across January and February 2026, while noting that core categories such as liquids, foodservice, and beauty held up better than the average.34 A volume decline is the metric that should command attention, because it strips out the pass-through noise and speaks to real demand and share. Weather is a legitimate one-off explanation, but it is also the kind of explanation that becomes a yellow flag if it recurs; "it was the weather" is only credible once. The market will want to see comparable volumes return to growth to confirm that the contraction was a storm and not a trend.

This is the right place to name the two or three KPIs that a long-term owner should actually track, because a company this large throws off dozens of metrics and most of them are noise.

The first is comparable volume growth—organic units moved, stripped of acquisitions, currency, and the pass-through's price effects. It is the cleanest read on genuine demand and competitive share, and it is the number that cannot be flattered by resin-price accounting. A packaging company growing volumes is taking share or riding healthy end-markets; one shrinking them is losing ground, weather excuses notwithstanding.

The second is synergy realization against the $650 million plan, cross-checked against reported EBIT margins. This is the metric that will make or break the entire rationale for the Berry deal, and the market will read every quarter's number as a referendum on management credibility.

The third is the net-leverage-and-free-cash-flow pair, which together dictate the capital-return story. Until net debt falls back toward the 2.5-to-3.0-times target, the buyback stays frozen and financial flexibility stays constrained; free cash flow is the engine that gets it there. Watch those three, and you are watching the company. Almost everything else is commentary.

The second number management moved in the spring of 2026 was exactly that cash line. Adjusted free-cash-flow guidance for fiscal 2026 was revised to a range of $1.5 to $1.6 billion, a reduction of roughly $300 million from prior expectations, which the company attributed to deliberate inventory-building to safeguard supply continuity amid input-cost inflation and heightened geopolitical uncertainty.34 This is a genuinely double-edged disclosure. On the charitable read, pre-emptively stockpiling inventory to guarantee you can serve customers during a supply shock is exactly the kind of reliability that makes Amcor indispensable to the world's largest brands—it is defensive spending in service of the moat. On the skeptical read, cutting free-cash-flow guidance by $300 million while carrying 3.3-to-3.5-times leverage and a suspended buyback is not a comfortable combination, because free cash flow is precisely what services the debt and eventually restarts capital returns. Both readings are true at once, and holding them together is the honest way to think about the stock right now. Cash conversion, alongside comparable volume, is one of the handful of numbers that will tell you whether the integration is a triumph or a slog.

With the plumbing understood, we can finally ask the question that determines whether any of this scale is worth owning: does Amcor actually have a durable competitive advantage, or is it just very large?

VIII. Competitive Dynamics: Helmer's 7 Powers & Porter's 5 Forces

Let's war-game the business honestly, using two analytical frameworks investors know well—Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces—and let's resist the temptation to grade every box generously. A moat you can talk yourself into is worse than no moat at all.

Start with Helmer, and with the power Amcor leans on hardest: Scale Economies. This is the real one. At roughly $24 billion in sales, Amcor is one of the largest single buyers of polymer resin and aluminum on the planet—approaching a monopsony-like position with its suppliers—which lets it secure volume discounts that smaller competitors simply cannot match. Scale also lets it spread fixed costs across an enormous unit base. Consider its research budget: Amcor funds roughly $100 million a year in R&D to develop next-generation and more sustainable materials, and because it stamps out billions of units, the cost of that research amortizes down to a rounding error per package.1 A regional competitor spending the same absolute dollars on R&D would be crushed by the per-unit burden. This is a genuine, durable advantage, and it is the primary source of Amcor's moat. The honest caveat: scale economies in packaging are broad but shallow—being the biggest buyer of resin saves you meaningful basis points, but it does not lock customers in the way a network effect or a proprietary platform would. Scale keeps you cost-competitive; it does not make you irreplaceable.

The power that actually makes parts of Amcor irreplaceable is Switching Costs, and they are highest exactly where the money is best: healthcare and pharmaceutical packaging. Here the moat is deep. A medical blister pack, a sterile surgical wrap, or a pharmaceutical film is not simply bought—it is validated, through multi-year FDA and international regulatory processes co-engineered with the drug maker. Once a specific packaging material is registered as part of a drug's approved presentation, switching to a rival supplier means re-running compliance work, risking regulatory delay, and potentially disrupting the supply of a life-critical product. No procurement manager wants to be the person who switched blister-pack vendors to save a few cents and triggered a drug shortage. That is a real, high, durable switching cost—but note carefully that it applies to a subset of Amcor's business, the regulated medical and pharma niches inherited largely from Alcan, not to the coffee pouch or the ketchup bottle, where switching costs are far lower and customers routinely dual-source.

The third Helmer power, Process Power, is genuine but moderate. Amcor possesses decades of accumulated, hard-to-replicate expertise in co-extrusion—the art of simultaneously layering as many as nine different polymers into a single microscopically thin film, each layer tuned to block moisture, oxygen, or UV light. Explaining it simply: it is like baking a nine-layer cake where each layer is thinner than a human hair and every layer does a specific job, all produced at industrial speed with zero defects across billions of units. That accumulated know-how is difficult for a new entrant to copy quickly. But "moderate" is the right label, because the largest competitors—the Sealed Airs, the Sonocos, the Mondi and Huhtamäki-type players—possess broadly similar capabilities. Process Power differentiates Amcor from the small fry, not from its true peers.

Two other Helmer powers are worth mentioning only to dismiss them, because their absence is as telling as the presence of the first three. Network Economies—the dynamic where each additional user makes the product more valuable to every other user—simply does not exist in packaging; a coffee brand does not value Amcor's pouch more because a detergent brand also buys from Amcor. Branding power, in the consumer sense, is likewise near-absent: shoppers do not know or care who made the wrapper, so Amcor cannot charge a premium the way a luxury goods maker can. This matters because it clarifies what kind of moat Amcor actually has. It is a cost-and-integration moat, not a demand-and-desire moat. The company wins by being cheaper to run at scale and harder to switch away from in regulated niches—not by being loved. That is a perfectly good way to make money, but it caps the ceiling: cost moats generate steady returns, not the explosive pricing power of a genuine consumer franchise.

That is the sober verdict on the moat: strong scale economics, genuinely deep switching costs in a valuable minority of the portfolio, and respectable-but-not-unique process expertise, with no network or brand power to speak of. It is a real moat. It is not an impregnable one.

Now Porter, which reframes the same reality through the lens of industry structure.

Bargaining power of buyers is the most uncomfortable force for Amcor, and it is moderate-to-high. Amcor's customers are the largest, most sophisticated procurement organizations in the world—global CPG companies that buy in colossal volumes and relentlessly push for annual price reductions. These are not price-takers; they are ferocious price-negotiators, and they cap Amcor's ability to expand margins. What partially offsets their power is Amcor's ability to be a one-stop, global, supply-secure partner with a credible sustainability roadmap—valuable enough that the biggest brands consolidate spend with it rather than juggle dozens of regional suppliers. But make no mistake: buyer power is the primary structural ceiling on this business's profitability.

Bargaining power of suppliers runs the other way and is only moderate. Yes, the resin sellers are giants—Dow, ExxonMobil, and the other petrochemical majors—but Amcor's own scale as one of their largest customers gives it real negotiating weight, and the pass-through mechanism means much of the supplier-side price risk is contractually exported downstream anyway.

Threat of substitutes is moderate and genuinely worth taking seriously, because it is entangled with politics. The substitution risk is the shift away from plastic toward glass, metal, or paper, driven as much by regulation and consumer sentiment as by economics. Amcor's counter-argument—which happens to be true—is that flexible plastics frequently carry the lowest total lifecycle carbon footprint, because they weigh so little that they slash transport emissions relative to heavy glass or metal. To hedge the sentiment risk, Amcor has invested in recyclable paper-based barrier packaging under its AmFiber platform, giving it a paper option to sell to customers and regulators who demand one.1 The threat is real but two-sided, and Amcor is positioning on both sides of it.

Rivalry among existing competitors deserves its own word, because this is where the day-to-day pressure actually lives. Amcor does not compete against nobody; it competes against a roster of serious global and regional players—the flexible- and protective-packaging specialist Sealed Air, the diversified American packager Sonoco, the Europe-based giants Mondi and Huhtamäki, the plastics group Berry once was, and a long tail of regional converters who compete fiercely on price for the less specialized business. In commodity-adjacent segments—the plain films, the generic containers—this rivalry is intense and margins are thin, which is precisely why Amcor is trying to shift its mix toward the specialized, higher-barrier categories where fewer competitors can play. The competitive intensity varies enormously by segment, and the single most important strategic fact about Amcor is that it is trying to spend more of its life in the calm, high-margin waters and less in the churning commodity shallows.

Threat of new entrants, finally, is extremely low—and this is Porter's most favorable force for the incumbent. The capital intensity is enormous, the required global manufacturing footprint takes decades and billions to build, and the customer relationships are deeply integrated and, in pharma, regulatorily locked. Nobody is going to wake up tomorrow and build a credible global challenger to Amcor from scratch. The competitive war, such as it is, is fought among a handful of existing giants, not against insurgents. The one caveat worth naming is that the real disruptive threat to packaging has rarely come from a new company—it comes from a new material or a new regulation that renders an existing package obsolete, and there the incumbent's scale is as much a liability as an asset, because it has the most invested in the status quo.

Put it all together and the strategic picture is coherent: Amcor operates in a consolidated, high-barrier industry where the real competitive tension is not the threat of being displaced but the grinding, permanent pressure from powerful buyers on its margins. That structure is what makes the whole story ultimately a question of capital allocation and execution rather than survival—which is exactly the terrain of the bull-and-bear debate.

IX. The Investment Story Spine: Bull vs. Bear & Activist Stress Test

Strip away the history and the frameworks, and every investment case reduces to two competing stories about the future. Let's tell both honestly, and then stress-test the whole thing the way a skeptical activist would.

The bull case—why Amcor wins from here—rests on three pillars.

The first is sustainability leadership as a competitive weapon rather than a compliance cost. The largest consumer brands have made public net-zero and recyclable-packaging commitments they cannot meet alone, and Amcor is one of very few suppliers with the scale, R&D, and global footprint to help them get there. By fiscal 2024, the company reported that 95% of its rigid packaging was recyclable and that a recycle-ready alternative was available for 94% of its flexible packaging.7 If sustainability becomes the axis on which the biggest packaging contracts are won, scale in green materials science is a moat that compounds—smaller rivals cannot fund the transition across billions of units the way Amcor can.

The second pillar is the synergy-driven earnings engine. If management harvests the full $650 million by fiscal 2028, the operating leverage on a combined cost base is substantial, and the bull case points to meaningful EPS accretion—management framed the combination as delivering roughly 12% adjusted EPS growth in fiscal 2026, building toward far greater accretion by fiscal 2028 as synergies compound and the balance sheet heals.34 The early over-delivery on the Year-One target, discussed earlier, is the concrete evidence underpinning this pillar.

The third pillar is the defensive income profile. Amcor sells into consumer staples—food, healthcare, everyday products—whose demand barely flinches in a recession, and it has a long history as a reliable dividend payer, with a yield that has generally sat in the 5–6% range. For an income-oriented, risk-averse owner, that combination of staple-backed cash flows and a high, defended dividend is the core of the attraction.

It is worth confronting one popular myth head-on, because it distorts how people value this stock. The myth is that Amcor is a "growth" story unlocked by consolidation—that scale plus synergies plus sustainability equals a re-rating to a higher multiple. The reality is more sober. Amcor is, at its heart, a low-single-digit organic-growth business in a mature industry, whose earnings-per-share growth in the near term comes overwhelmingly from self-help—synergies, cost-out, debt paydown, and share-count management—rather than from booming end-demand. That is not a criticism; self-help-driven EPS growth is real and valuable. But it has a natural shelf life. Synergies are a one-time step-change, not a perpetual-motion machine. Once the $650 million is banked and the balance sheet is repaired, the market will re-focus on the underlying organic growth rate, and that rate is modest. The bull case, told honestly, is a bet on a few years of powerful self-help followed by a return to steady, dividend-anchored, low-growth compounding—not a bet on a secular growth engine.

The bear case—what breaks the story—is equally concrete, and it is mostly about the three things bulls wave away.

Integration indigestion is first. Merging two 30,000-plus-person organizations, with overlapping plants and different cultures, is genuinely hard, and the failure modes are customer churn (a brand that gets frustrated during the transition and dual-sources away), operational disruption, and synergy shortfalls in the hard, back-loaded footprint-rationalization phase that has not yet been attempted at scale. The early synergy wins came from the easy buckets; the bear rightly notes that the hard part is still ahead.

The leverage hangover is second, and it is the bear's strongest card. At 3.3-to-3.5-times net debt to EBITDA against a 2.5-to-3.0-times target, Amcor has less flexibility than it is used to. Buybacks are suspended. Interest expense is elevated in a world where the cost of capital is no longer free. And critically, the deleveraging plan depends on robust free cash flow—which management just cut by $300 million—and on healthy volumes, which just contracted 1.5%. If a destocking cycle drags on or volumes weaken further, the debt paydown slows, the buyback stays frozen longer, and the "disciplined capital allocator" narrative frays.

Regulatory backlash is third and most existential. If political bans on single-use plastics accelerate faster than Amcor can pivot to recyclable and paper-based alternatives, the terminal value of the rigid-plastics business—a large chunk of what it just paid $15 billion to acquire—could permanently shrink. AmFiber is a hedge, not an insurance policy. And the deeper danger is not a sudden ban but a slow, grinding shift in extended-producer-responsibility rules, plastic taxes, and recycled-content mandates across dozens of jurisdictions, each individually survivable but collectively raising the cost and shrinking the addressable market for the plastic-heavy products at the center of Amcor's mix. This is a business whose largest long-term risk is legislative and glacial rather than competitive and sudden—the hardest kind of risk to price, because it never arrives on a single day you can point to.

A fourth bear thread, quieter but real, is the recycled-material paradox. Amcor's customers increasingly demand packaging made with post-consumer recycled resin, but recycled feedstock is often more expensive and less consistent than virgin polymer, and the collection-and-sorting infrastructure to supply it at scale barely exists in much of the world. Amcor is thus being asked to hit sustainability targets whose input economics may not cooperate—a squeeze that could pressure margins in exactly the "green" products that are supposed to be the growth engine. The company's scale helps it invest ahead of this, which is the bull's rejoinder, but the tension between what customers demand and what the recycling supply chain can actually deliver is a genuine, underappreciated risk.

Now the activist stress test, which is not hypothetical for this company—it is genetic. Remember that Berry's board seats were reshaped by Ancora and Eminence, and that activist-influenced governance carried directly into the combined entity. Amcor's management is operating under the kind of oversight that expects results, and the same investors who forced the Berry marriage know exactly how to force the next move if execution slips.

So imagine the short/activist deck being written today. It would target three soft spots. Capital allocation and leverage: if net debt stays above 3.0 times beyond fiscal 2027, expect pressure to accelerate disposals or halt any temptation toward new M&A. The $2.5 billion of non-core assets: an activist would demand these be sold or spun faster, arguing that every quarter they linger is a quarter of trapped value and management complacency—and would point to Amcor's own demerger history as proof it knows how to cut. Portfolio complexity and a possible break-up: the most aggressive case would argue that flexibles and rigids are different businesses with different economics and different natural owners, and that separating them could unlock a higher combined multiple. If Konieczny and Scherger miss the synergy cadence, or if leverage proves sticky, that deck stops being hypothetical.

The neutral synthesis is this: Amcor is neither the obvious compounder its bulls describe nor the value trap its bears fear. It is a well-positioned, high-barrier business carrying a large, mostly self-inflicted debt load into an integration whose early innings have gone better than promised but whose hardest work is still ahead. The bull case and the bear case will be adjudicated by the same two or three numbers, quarter after quarter—and knowing which numbers those are is the whole game.

X. Epilogue & Playbook Lessons

Step back from the quarterly noise, and Amcor's 166-year arc resolves into a handful of durable lessons that outlast any single earnings call.

Playbook Lesson One: The Multiple Arbitrage of Consolidation. Twice, decisively—with Bemis in 2019 and Berry in 2025—Amcor used its own premium-valued stock as an acquisition currency to buy lower-multiple peers, engineering immediate accretion from the valuation gap alone before a single synergy landed. It is a genuinely powerful tool in a consolidating industry. But the honest version of the lesson includes the warning: multiple arbitrage flatters the per-share optics on day one, yet it only creates value if the acquirer actually integrates the target and does not simply inherit its inferior economics and its debt. The arbitrage is the invitation; execution is the meal.

Playbook Lesson Two: Demerge to Dominate. The single most counterintuitive truth of Amcor's history is that it became a global champion by subtracting, not adding. Spinning off PaperlinX in 2000 and Orora in 2013 shed the heavy, low-return, capital-intensive businesses that were anchoring the company to its past and depressing its multiple—and only after that ruthless focus was achieved could the global scaling begin. The same muscle is flexing again in the $2.5 billion non-core review. The lesson for operators and investors alike: the willingness to sell what you grew up on is often the precondition for building what comes next.

Playbook Lesson Three: The Contractual Shield. In an asset-heavy business drenched in commodity-price risk, the thing that separates a stable enterprise from a cyclical casualty is not clever hedging—it is contractual indexing. Amcor's resin pass-throughs convert what could have been a terrifying bet on the price of oil into a comparatively boring, predictable toll on the value it adds. Any investor evaluating a raw-material-exposed manufacturer should ask, before anything else, a single question: who bears the commodity risk in the contract? At Amcor, the answer—mostly, and with a lag—is the customer. That structural feature is why a plastics business can be marketed as a defensive dividend stock at all.

What makes Amcor a genuinely instructive case study is that it refuses to fit a tidy narrative. It is a business built on the least glamorous product imaginable, run through one of the most globally rootless corporate structures in public markets, that arrived at its current size less through singular strategic genius than through a patient sequence of demergers, opportunistic acquisitions, and—in its defining recent chapter—the pressure applied to a rival by outside activists. Packaging, it turns out, is not really about plastic bags and bottles. It is a high-stakes, low-drama game of material science, global logistics, procurement scale, and capital deployment, played by a handful of giants against the relentless downward pressure of the world's biggest buyers.

The next three years will settle the open questions this story leaves hanging: whether the $650 million in synergies fully materializes, whether the leverage comes down on schedule without strangling the dividend, whether the non-core disposals happen at fair prices, and whether comparable volumes turn back to growth. None of those outcomes is guaranteed, and the activists who wrote the last chapter are still in the room. For the sophisticated long-term investor, that is precisely what makes Amcor worth watching: a company with a real moat, a real debt problem, a credible-but-unproven management duo, and a set of KPIs concrete enough that the story will tell on itself, quarter by quarter, in plain numbers.

References

-

Amcor and Berry to combine in an all-stock transaction — Amcor plc, 2024-11-19 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Amcor completes combination with Berry Global — Amcor plc, 2025-04-30 ↩

-

Amcor Reports Solid Third Quarter Results and Updates Fiscal 2026 Guidance — PR Newswire / Amcor plc, 2026-05-06 ↩↩↩↩↩↩

-

Amcor plc (AMCR) Q3 2026 Earnings Call Transcript — Seeking Alpha, 2026-05-06 ↩↩↩↩

-

Amcor Appoints Stephen R. Scherger as Executive Vice President and Chief Financial Officer — PR Newswire / Amcor plc, 2025-10-15 ↩↩

-

Activist Ancora urges board changes and strategic review at Berry Global — Reuters, 2021-11-15 ↩

-

Amcor plc SEC Form 10-K for Fiscal Year Ended June 30, 2024 — SEC EDGAR, 2024-08-21 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube