Antero Midstream: The Story of America's Appalachian Gas Highway

I. Introduction & Episode Roadmap

Somewhere beneath the rolling green hills of West Virginia and southwestern Pennsylvania, buried thousands of feet below hollows that once echoed with coal miners' pickaxes, sits one of the largest concentrations of natural gas on the planet. And connecting that gas to the furnaces, power plants, and export terminals that consume it is a sprawling network of steel pipes, compressor stations, and water handling facilities worth billions of dollars. That network, in large part, belongs to Antero Midstream.

Antero Midstream is a roughly ten-billion-dollar market cap midstream infrastructure company that today stands as one of the most important pieces of plumbing in America's natural gas system. But its story is not a simple tale of building pipes and collecting tolls. It is a story of financial engineering, family dynamics between a parent company and its captive subsidiary, activist investors demanding better governance, and an entire industry's reckoning with whether the structures Wall Street invented to fund the shale revolution were actually good for anyone besides the bankers who created them.

The central question of this episode is deceptively simple: How did a subsidiary created to serve a single customer—its own parent company—evolve into an independent infrastructure business trying to stand on its own? The answer winds through the rise and fall of the Master Limited Partnership, or MLP, structure, through a commodity crash that nearly destroyed an industry, through a global pandemic, and through a governance drama that forced the company to decide what it actually wanted to be when it grew up.

Along the way, we will meet the two geologists-turned-dealmakers who built the Antero empire from scratch, watch Wall Street's love affair with yield vehicles bloom and then sour, and examine whether "boring" businesses that own real physical assets in the ground can create durable value in a world obsessed with software and artificial intelligence.

The themes are universal even if the industry is specialized: When does financial complexity help a business, and when does it become a trap? What happens when a subsidiary's interests diverge from its parent's? And can infrastructure—literal pipes in the ground—constitute a genuine competitive moat? The Appalachian Basin's transformation from coal country to gas capital is one of the great American industrial stories of the twenty-first century, and Antero Midstream sits right at its center.

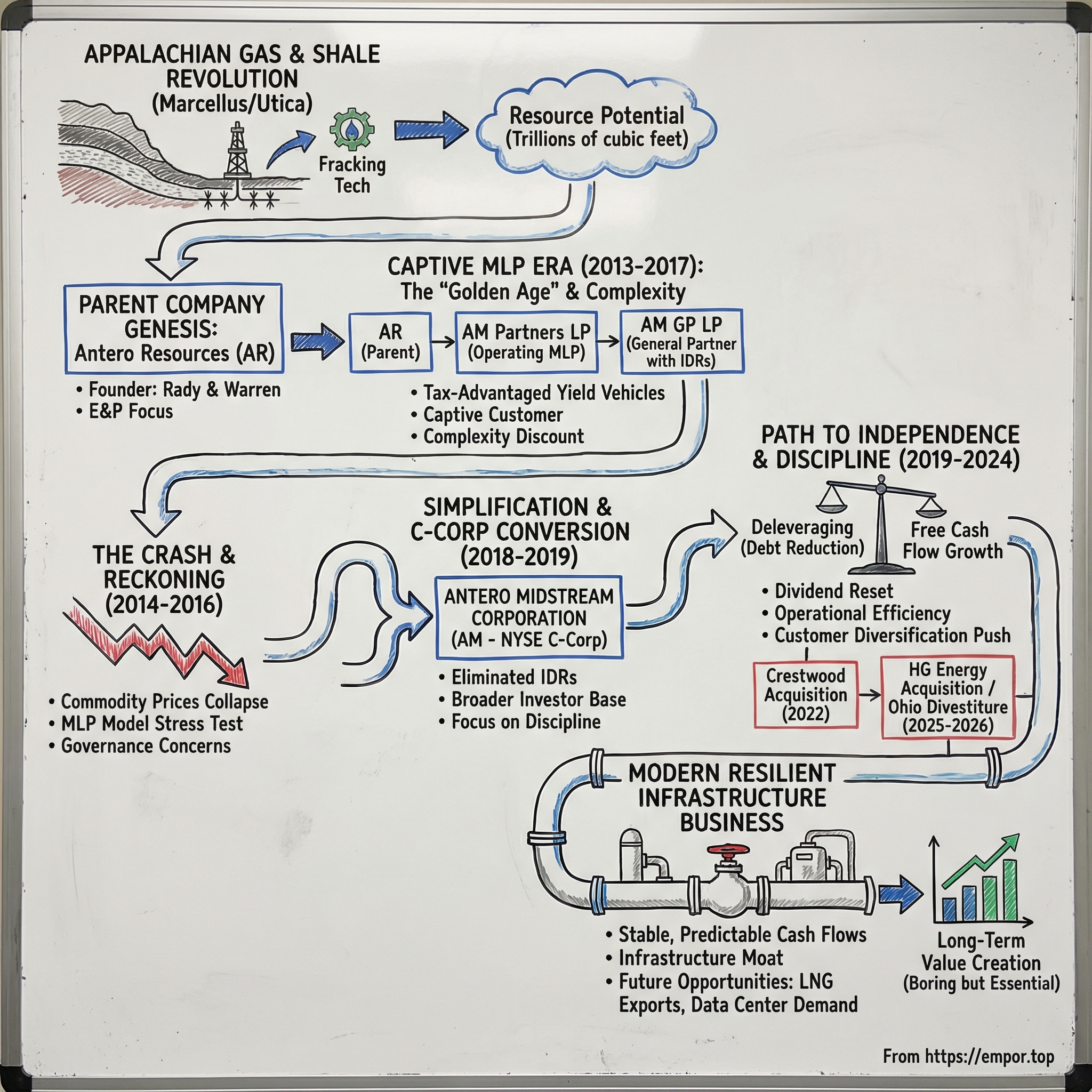

II. Setting the Stage: The Shale Revolution & Appalachian Renaissance

To understand Antero Midstream, you first have to understand what lies beneath Appalachia. The Marcellus Shale is a formation of sedimentary rock stretching from New York through Pennsylvania, West Virginia, and into Ohio. Beneath it sits the Utica Shale, even deeper and in some areas even richer. Together, these formations contain an estimated 214 trillion cubic feet of recoverable natural gas according to the United States Geological Survey—enough to power American homes and industry for decades. The Appalachian Basin has accounted for roughly thirty-two percent of all natural gas produced in the lower forty-eight states every year since 2016. That is a staggering concentration of a critical resource in a region most Americans associate with Rust Belt decline.

But for most of the twentieth century, this gas was economically unreachable. It was locked in tight shale rock formations that conventional vertical drilling could not efficiently tap. The breakthrough came not from Appalachia but from Texas, where a stubborn wildcatter named George Mitchell spent nearly two decades and hundreds of millions of dollars proving that hydraulic fracturing—fracking—combined with horizontal drilling could unlock gas from shale. Mitchell's eureka moment came in the late 1990s when his team at Mitchell Energy cracked the code on slickwater fracking in the Barnett Shale near Fort Worth. When Devon Energy acquired Mitchell Energy in 2002 and married Mitchell's fracking techniques with horizontal drilling, the shale revolution was born.

Think of it this way: conventional gas drilling was like poking a straw vertically into a layer cake, hoping to hit a pocket of gas. Horizontal drilling combined with fracking was like turning that straw sideways within the richest layer and then shattering the rock around it to release gas trapped in millions of tiny pores. The production gains were extraordinary, and operators quickly realized that the technique worked not just in Texas but in shale formations across the country—especially in Appalachia.

Why did Appalachia matter so much? Three reasons stood out. First, geography: the Marcellus and Utica formations sit within a few hundred miles of the densest population corridor in the United States, the Northeast megalopolis stretching from Boston to Washington. Proximity to demand centers meant lower transportation costs and higher realized prices compared to gas produced in remote West Texas or Wyoming. Second, the gas itself was exceptional. Marcellus gas tends to be "dry"—meaning it is almost pure methane with relatively low concentrations of heavier hydrocarbons—which makes it cheaper to process. And some Utica wells produced "wet" gas rich in natural gas liquids like ethane and propane, adding another revenue stream. Third, the wells were prolific. Marcellus wells produced enormous initial volumes, and the formation's geology meant that decline curves, while steep, still left wells producing meaningful gas for years.

But there was a problem—a massive one. You could drill the most productive well in history, but if you had no way to move the gas from the wellhead to a pipeline that connected to customers, it was worthless. This was the midstream bottleneck. Appalachia, unlike the Permian Basin or the Gulf Coast, did not have decades of existing pipeline infrastructure. Coal had been king in West Virginia and southwestern Pennsylvania, and the pipeline networks that existed were designed for a different era. The shale revolution created an urgent, almost desperate need for new gathering lines, compression stations, processing plants, and high-pressure transmission pipelines. Somebody had to build them, and fast.

The standard industry solution was for exploration and production companies—E&Ps, the companies actually drilling the wells—to create their own captive midstream subsidiaries. The logic was straightforward: if you controlled your own gathering and compression infrastructure, you did not have to negotiate with a third-party pipeline company that might charge monopoly rents or, worse, might not build capacity fast enough to keep up with your drilling program. You controlled your own destiny. And there was a financial engineering angle too: by housing midstream assets in a separate entity, an E&P could monetize those assets in the capital markets, raising cheap capital to fund more drilling while retaining operational control. This was the playbook that would give birth to Antero Midstream.

The regulatory landscape added another layer of complexity. Pennsylvania, West Virginia, and Ohio each had different permitting regimes for pipelines, water withdrawal, and well development. Environmental concerns about fracking's impact on groundwater, air quality, and seismicity created political friction, especially in Pennsylvania where the Marcellus underlaid both rural farmland and suburban communities near Pittsburgh. Building midstream infrastructure meant navigating not just engineering challenges but a patchwork of state and local regulations, landowner negotiations, and environmental reviews. The companies that could do this efficiently had a genuine advantage.

This was the world into which Antero Midstream was born—a world of enormous geological promise, urgent infrastructure need, financial innovation, and regulatory complexity. And the men who would build it had already proven they knew how to play this game.

III. Antero Resources: The Parent Company Genesis

Paul Rady is the kind of geologist who thinks in billions of cubic feet the way most people think in gallons. After earning his geology degrees from Western State College of Colorado and Western Washington University, Rady spent a decade at Amoco Production Company in Denver, where he was credited with discovering significant gas fields in Oklahoma's Arkoma Basin. He was not just reading core samples—he was finding gas that other people had missed. From Amoco, he moved to Barrett Resources Corporation, a small NASDAQ-listed company with a twenty-million-dollar market cap. Over eight years, Rady rose from Chief Geologist to CEO and transformed Barrett into a billion-dollar NYSE company with nearly a trillion cubic feet equivalent of reserves across eleven basins. That is a fifty-fold increase in market value driven by one geologist's conviction about where the gas was hiding.

Glen Warren came from a different world but complemented Rady perfectly. Warren started as a landman at Amoco, negotiating mineral rights in the Gulf Coast, before pivoting to Wall Street. He spent a decade as a natural resources investment banker at Lehman Brothers, Dillon Read, and Kidder Peabody, where he focused on equity and debt financings and mergers and acquisitions for energy companies. Warren understood both the rocks and the money—a rare combination. When Rady launched Pennaco Energy in 1998 to develop coal-bed methane in Wyoming's Powder River Basin, he brought Warren in as EVP, CFO, and Director. Together, they grew Pennaco quickly enough that Marathon Oil acquired it in early 2001. The duo had now built and sold two companies together and knew each other's strengths intimately.

In June 2002, with the proceeds from Pennaco and a conviction that unconventional gas was the future, Rady and Warren co-founded Antero Resources Corporation. The name came from Mount Antero, a 14,269-foot peak in the Sawatch Range of Colorado—fitting for two Denver-based entrepreneurs who thought big about what lay beneath the earth's surface. Starting in February 2003, the private equity powerhouse Warburg Pincus began investing in Antero, eventually committing over $1.5 billion. Warburg's backing gave Rady and Warren the financial firepower to move fast and take big positions.

Their first major play was not Appalachia but Texas's Barnett Shale, where George Mitchell had pioneered the fracking revolution. Within three years, Antero became the second-largest producer and second-most active operator in the Barnett—a remarkable achievement for a startup competing against established players. But rather than ride the Barnett to maturity, Rady and Warren made a characteristically bold move: in April 2005, they sold the entire Barnett position to XTO Energy for approximately $685 million in cash, stock, and assumed debt. They cashed out near the top and redeployed capital.

After cycling through positions in the Arkoma, Piceance, and other basins, the pivotal moment came in 2008 when Antero acquired drilling rights on approximately 114,000 net acres in the Marcellus Shale from Dominion Resources for $347 million. This was the bet that would define the company. While other operators were still cautiously testing the Marcellus, Rady's geological instincts told him this formation was extraordinary. He was right. Antero rapidly assembled one of the largest acreage positions in the Marcellus and Utica shales, and by October 2013, when Antero Resources went public on the NYSE, the company raised $1.6 billion by offering 35.7 million shares at $44 per share—above the expected range and the second-largest U.S. IPO of that year.

But Rady and Warren faced a strategic imperative that went beyond drilling. Their Appalachian acreage was remote, infrastructure-poor, and producing volumes that overwhelmed existing third-party pipeline capacity. They needed their own midstream system—gathering lines to collect gas from wellheads, compressor stations to push it through the network, processing facilities to strip out impurities, and water handling infrastructure for the millions of gallons needed to frack each well. Building this infrastructure in-house meant controlling the pace of development, ensuring their wells could flow as soon as they were drilled, and capturing the economics of the midstream value chain rather than paying those margins to someone else.

The logic was compelling: own the highway, not just the cars driving on it. And Wall Street had invented the perfect vehicle to fund this highway construction at an irresistibly low cost of capital.

IV. Birth of Antero Midstream: The Captive Years (2013-2017)

In the fall of 2014, the energy industry was in the grip of MLP fever. Master Limited Partnerships—tax-advantaged entities that passed income through to unitholders without paying corporate taxes—had become Wall Street's favorite way to fund midstream infrastructure. The pitch to investors was seductive: buy units in a pipeline company, receive fat quarterly distributions that often yielded six to eight percent, and watch those distributions grow as the shale revolution demanded ever more infrastructure. For yield-starved investors in a zero-interest-rate world, MLPs were catnip.

Antero Midstream Partners LP was formed in 2013 as a subsidiary of Antero Resources, created specifically to own, operate, and develop the midstream assets serving the parent company's Appalachian drilling program. When the MLP went public on November 10, 2014, the reception was extraordinary. Originally planned at 37.5 million units priced between $19 and $21, investor demand was so intense that the offering was upsized to 46 million units priced at $25—well above the range. The IPO raised approximately $1.1 billion, with Barclays and Citigroup leading the underwriting syndicate. In a single day, Antero had monetized its pipeline network while retaining operational control.

To understand why this structure was so attractive, think of it as a toll road concession. Antero Resources, the parent, was the primary—essentially the only—driver on this toll road. Through long-term dedication agreements covering substantially all of the parent's current and future Appalachian acreage, Antero Midstream was guaranteed the right to gather, compress, and handle water for every molecule of gas Antero Resources produced. Minimum volume commitments provided a floor on revenue regardless of short-term production fluctuations. The fees were fixed per unit of gas gathered or water handled, meaning the midstream entity had no direct commodity price exposure. Whether natural gas traded at two dollars or six dollars per thousand cubic feet, Antero Midstream collected its toll.

The infrastructure buildout was ambitious. The system grew to include hundreds of miles of low-pressure and high-pressure gathering pipelines, multiple compressor stations, and an extensive water handling network. Water is the unsung hero—and environmental flashpoint—of shale development. Each horizontal well requires millions of gallons of fresh water mixed with sand and chemicals for the fracking process, and each well produces millions of gallons of contaminated "produced water" that must be safely disposed of. Antero Midstream built a comprehensive water system that sourced fresh water from the Ohio River and local reservoirs, delivered it to well sites through permanent pipelines (avoiding thousands of truck trips), and then collected and disposed of the produced water. This integrated water handling capability was not glamorous, but it was operationally critical and genuinely difficult for competitors to replicate.

But the MLP structure also created a labyrinthine corporate architecture. By May 2017, the Antero midstream universe consisted of three publicly traded entities: Antero Resources (the E&P parent), Antero Midstream Partners LP (the operating MLP), and Antero Midstream GP LP (the general partner entity that conducted its own IPO in May 2017, raising roughly $875 million at $23.50 per share). The GP entity's sole source of income was its Incentive Distribution Rights, or IDRs—a mechanism that entitled it to escalating percentages of the MLP's cash distributions as those distributions exceeded certain thresholds. At the highest tier, the GP could receive up to fifty percent of every incremental dollar distributed. Think of it as a performance fee on top of a management fee, structured to reward the GP handsomely as the MLP grew.

Wall Street loved this three-entity structure because it created multiple securities to trade and underwrite. Investors in each entity had a slightly different risk-reward profile. But the complexity also created inherent conflicts of interest. The GP's incentive was to maximize distributions from the MLP—even if the MLP would have been better served by retaining cash for investment or debt reduction. The parent company wanted cheap midstream services and maximum capital recycling. And minority unitholders in the MLP wanted steady distributions and fair treatment. These conflicts were manageable when times were good and capital was cheap. But good times in the energy business never last forever.

First-year revenue came in at $266 million. By 2016, it had more than doubled to $590 million as the infrastructure buildout accelerated to keep pace with Antero Resources' aggressive drilling program. The growth was real, the cash flows were tangible, and the distributions kept rising. For a brief, heady moment, it seemed like the MLP machine could run forever.

V. The MLP Bubble & Commodity Crash (2014-2016)

The party ended with shocking speed. In the summer of 2014, crude oil traded above $100 per barrel. By February 2016, it had plunged to $26—a collapse of nearly seventy-five percent driven by Saudi Arabia's decision to flood the market, surging U.S. shale production, and weakening global demand. Natural gas prices, already battered by the very success of the shale revolution that had created oversupply, fell in sympathy. The entire energy sector went into a deep freeze.

For MLPs, the commodity crash exposed a fundamental vulnerability that the yield-chasing boom had obscured. Many MLPs had funded their growth through a combination of debt and continuous equity issuance—a model that worked only as long as capital markets remained open and unit prices stayed high. When energy stocks cratered, MLP unit prices fell too, pushing yields to unsustainable levels and slamming shut the equity issuance window. Without access to cheap equity capital, MLPs that had been living on a treadmill of issuing units to fund distributions suddenly faced a reckoning. Distribution cuts cascaded across the sector. Kinder Morgan, the poster child of the MLP model and once one of the largest energy infrastructure companies in the world, slashed its dividend by seventy-five percent in December 2015. The signal to the market was devastating: if Kinder Morgan could not sustain its payout, nobody was safe.

Antero Midstream, however, occupied a peculiar position. Because its revenue came from fixed-fee contracts with a dedicated producer rather than from commodity prices directly, its cash flows remained remarkably stable even as oil and gas prices collapsed. The parent company, Antero Resources, was hurting—its stock fell from over $60 in mid-2014 to below $15 by early 2016—but it kept drilling, which meant gas kept flowing through Antero Midstream's pipes, which meant the midstream entity kept collecting its tolls. This was the paradox of the captive midstream model: the parent could be hemorrhaging money while the subsidiary remained healthy, as long as the parent kept producing.

But "as long as the parent kept producing" was the critical caveat. Antero Resources was one of the few Appalachian producers that maintained its drilling program through the downturn, partly because its hedging program had locked in attractive gas prices and partly because its Marcellus wells were so productive that they generated acceptable returns even at depressed prices. Other operators were not so fortunate. Across Appalachia and other shale basins, companies slashed capital spending, idled rigs, and in some cases filed for bankruptcy. The midstream entities that served these distressed producers suddenly found that their "guaranteed" minimum volume commitments were only as reliable as their customers' ability to stay solvent.

The downturn also triggered a policy scare that rattled MLP investors. Questions about whether Congress might change the tax treatment of MLPs—eliminating the pass-through structure that was their primary appeal—added to the selling pressure. While no legislation materialized immediately, the uncertainty was enough to keep institutional investors on the sidelines. And in March 2018, the Federal Energy Regulatory Commission issued a ruling that MLPs could no longer recover an income tax allowance in their cost-of-service rates—a technical-sounding change that had profound implications for pipeline companies' cash flows and sent MLP indexes tumbling.

The survivors of the 2014-2016 crash emerged chastened. The era of growth-at-all-costs, funded by continuous capital markets access, was over. The industry began a painful consolidation. Smaller MLPs merged or were acquired. Larger ones began questioning whether the MLP structure itself—with its complexity, conflicts, and dependence on capital markets—was the right corporate form for the future. The answer, increasingly, was no. And Antero Midstream would soon face its own reckoning with this question.

VI. The Great Simplification: Merging Structures (2018-2019)

In January 2018, a relatively unknown activist fund called Chapter IV Investors sent a public letter to the Antero board that articulated what many investors had been thinking. The three-entity structure—parent E&P, operating MLP, and GP holding company—was too complex, riddled with conflicts, and trading at a discount because of it. Chapter IV urged the board to simplify from three entities to two, eliminate the GP-IDR structure that enriched insiders at the expense of MLP unitholders, and adopt what the fund called "best-in-class" corporate governance. The letter was polite but firm, and it landed at exactly the right moment.

Across the midstream industry, a wave of "simplification" transactions was sweeping through. The logic was compelling and, in retrospect, obvious. The IDR structure that had been designed to align GP and MLP interests had become a tax on growth. As MLP distributions climbed into the highest IDR tier, the GP was capturing an ever-larger share of incremental cash flow—up to fifty percent of every additional dollar. This meant that the MLP's cost of equity capital was effectively rising over time, making growth investments increasingly dilutive to MLP unitholders. The only people who benefited from this escalating structure were the GP's shareholders, which in Antero's case meant largely the same insiders who controlled the parent company.

On October 9, 2018, the boards announced the simplification. Antero Midstream GP would acquire all outstanding units of Antero Midstream Partners LP and convert from a limited partnership to a C-corporation, to be renamed Antero Midstream Corporation. Public unitholders of the MLP would receive $3.415 in cash plus 1.635 shares of the new company's stock for each unit they held—aggregate consideration valued at approximately $31.41 per unit based on the prior day's closing price. All outstanding IDR interests were exchanged for approximately 17.35 million shares of the new entity. In one stroke, the three-headed Antero midstream hydra became a single, clean C-corporation.

The transaction closed on March 12, 2019, and the new Antero Midstream Corporation began trading on the NYSE under the ticker AM the following day. The rationale went beyond just eliminating IDRs. Converting to a C-corporation opened the door to a vastly larger investor base. Many institutional investors—mutual funds, pension funds, index funds—were either prohibited from owning MLPs or reluctant to deal with the K-1 tax forms that MLP ownership required. A C-corp structure meant Antero Midstream would show up in standard stock screens, qualify for index inclusion, and attract the kind of long-term institutional capital that could provide a more stable shareholder base.

There were trade-offs, of course. A C-corporation pays corporate income taxes, which meant that on a pretax basis, less cash was available for distribution. But the theory was that a lower cost of equity capital and broader investor access would more than compensate for the tax leakage. The company also hoped that simplification would narrow the "complexity discount"—the gap between what Antero Midstream's assets were worth and what the market was willing to pay given the labyrinthine corporate structure.

The initial quarterly dividend was set at $0.3075 per share, or $1.23 annualized, which represented a meaningful yield. Rady and Warren positioned the simplification as a step toward building a long-term independent midstream company—one that could eventually stand on its own merits rather than being viewed primarily as a financial appendage of Antero Resources.

But simplification addressed only the corporate structure problem. The deeper question—whether Antero Midstream could reduce its near-total dependence on a single customer—remained unanswered. And 2019 brought a new partner to the table: Warburg Pincus, which had backed Antero since 2003, began its final exit. By November 2019, Warburg sold all remaining shares, and its board representatives resigned. The private equity sponsor that had funded the original Antero vision was gone, leaving the company to chart its own course with public market investors who would prove far more demanding.

VII. Breaking Free: The Path to Independence (2019-2021)

The newly simplified Antero Midstream Corporation entered 2019 with a clean corporate structure and an uncomfortable truth: virtually every dollar of its revenue came from a single customer that also happened to be its controlling shareholder. This was not a theoretical risk—it was the defining characteristic of the business. If Antero Resources cut its drilling program, reduced production, or fell into financial distress, Antero Midstream had almost nowhere else to turn.

Diversifying the customer base was the obvious strategic priority, but "obvious" and "easy" are very different words. Midstream infrastructure is, by its nature, geographically fixed. You cannot pick up a gathering pipeline and move it to serve a different producer's wells. Antero Midstream's pipes were connected to Antero Resources' wellheads, on Antero Resources' acreage, under long-term dedication agreements covering Antero Resources' minerals. Acquiring third-party customers meant either building new infrastructure to reach other producers' acreage—expensive and risky—or acquiring existing midstream systems that already served other customers.

The company pursued both paths, with mixed results. Joint ventures became a key tool. In February 2017, Antero Midstream had formed a 50/50 joint venture with MarkWest, a subsidiary of MPLX LP, for gas processing and natural gas liquids fractionation. The JV built on existing Sherwood processing plants in Harrison County, Ohio, with plans for significant incremental capacity. This partnership was strategically important because it gave Antero Midstream exposure to processing economics and a relationship with one of the largest midstream operators in Appalachia, without requiring the company to build and operate processing plants from scratch. The JV also held a separate 15% interest, alongside DT Midstream's 85%, in the Stonewall gathering system—a 68-mile, 1.5 billion cubic feet per day high-pressure pipeline.

The water handling business emerged as a genuine differentiator. While gathering and compression are relatively commoditized services that any well-capitalized midstream operator can provide, integrated water management in Appalachia is genuinely difficult. The terrain is mountainous, the geology is complex, and the volumes are enormous—each modern horizontal well can require five to ten million gallons of fresh water for completion and then produces contaminated water for years afterward. Antero Midstream's permanent water pipeline network, sourcing from the Ohio River and regional reservoirs, avoided the thousands of truck trips that alternative systems required. This was not just a cost advantage—it was an environmental and community relations advantage in a region where truck traffic on narrow mountain roads was a major source of friction.

Then came COVID-19. The pandemic crushed global energy demand in early 2020, and natural gas prices that were already low fell further. Antero Resources, like most E&Ps, curtailed production and slashed its capital budget. For Antero Midstream, this meant a temporary decline in throughput volumes—the absolute worst-case scenario for a company trying to prove it could grow independently of its parent. But the physical infrastructure remained in the ground, the contracts remained in force, and as demand recovered through late 2020 and 2021, volumes rebounded.

The more consequential decision came in early 2021, when management cut the quarterly dividend from $0.3075 to $0.225 per share—a 26.8 percent reduction. In the income-focused midstream world, a dividend cut is tantamount to a confession of failure. But Antero Midstream's management framed it differently: the cut was deliberate, designed to redirect roughly $160 million in annual cash flow from distributions to debt reduction. The company's leverage ratio needed to come down, and management chose to prioritize balance sheet strength over investor income. It was a painful but arguably rational decision that reflected a broader industry shift from growth-at-all-costs to financial discipline.

In April 2021, Glen Warren—co-founder, deal architect, and the financial mind behind both Antero entities—retired as President and CFO of Antero Resources and President of Antero Midstream. His departure marked the end of the founding era, leaving Paul Rady as the sole remaining founder in an active leadership role. Revenue held steady near $900 million in both 2020 and 2021, but the strategic direction had shifted unmistakably toward independence, deleveraging, and operational efficiency over growth.

VIII. Financial Engineering & Governance Drama (2020-2022)

The governance challenges at Antero Midstream were not abstract—they were structural. When a company's controlling shareholder is also its primary customer, its largest supplier of business, and the entity that appoints its management team, the potential for conflicts of interest is not just theoretical. It is embedded in every business decision.

Consider the dynamics. Antero Resources owned approximately thirty-one percent of Antero Midstream's shares following the simplification and had the power to influence board composition and strategic direction. At the same time, Antero Resources was the entity negotiating the terms under which it paid Antero Midstream for gathering, compression, and water handling services. In effect, the buyer and the seller were controlled by the same people. Were the fees that Antero Midstream charged its parent truly arm's-length, market-rate prices? Or were they set at levels that subsidized the parent company's drilling economics at the expense of Antero Midstream's minority shareholders?

These questions attracted scrutiny from analysts, governance watchdogs, and the activist investors who had been circling the Antero complex since Chapter IV's 2018 letter. The concerns extended beyond pricing to capital allocation. When Antero Midstream deployed hundreds of millions of dollars to build infrastructure, was it investing at returns that justified the capital from the midstream entity's perspective? Or was it building infrastructure that primarily benefited the parent's drilling program, regardless of whether it generated adequate returns for midstream shareholders?

Board independence was another flashpoint. Paul Rady served as Chairman of both Antero Resources and Antero Midstream, creating an obvious dual-loyalty issue. Several directors sat on both boards. Critics argued that truly independent oversight was impossible when the same individuals were tasked with protecting the interests of both the parent and the subsidiary—interests that sometimes conflicted directly.

The overhang from Antero Resources' large ownership stake created a persistent market problem as well. A thirty-plus percent concentrated holding by a single entity that might need to sell shares to fund its own operations or reduce its own debt created ongoing uncertainty. Every time Antero Resources disclosed a secondary offering or block trade of AM shares, the midstream stock came under pressure. Investors in Antero Midstream were not just betting on the company's operations—they were betting that the parent would not dump shares at inopportune moments.

On the environmental front, Antero Midstream faced the same pressures confronting the entire midstream industry. Methane emissions from natural gas infrastructure had become a major regulatory and reputational concern. Methane is a greenhouse gas roughly eighty times more potent than carbon dioxide over a twenty-year horizon, and leaks from gathering systems, compressor stations, and processing plants represent both lost product and environmental damage. The company committed to emissions reduction targets and invested in leak detection and repair programs, but the ESG scrutiny added another layer of operational and financial complexity.

The distribution policy debate crystallized the governance tensions. After the 2021 dividend cut, management held the quarterly payout flat at $0.225 per share. Income-focused investors wanted the dividend restored or increased. Growth-oriented investors wanted capital deployed into expansion. Debt-focused investors wanted every spare dollar applied to reducing leverage. Each constituency had a valid argument, but the company could not satisfy all three simultaneously. Management chose deleveraging, and by the end of 2022, the strategy was beginning to show results: revenue reached $920 million, return on invested capital hit seventeen percent, and the balance sheet was strengthening.

The "stranded asset" fear—the nightmare scenario where Antero Resources production declines and Antero Midstream's infrastructure sits partially idle—never fully materialized. But it lingered as a background anxiety, reinforced every time natural gas prices dipped or an analyst questioned the long-term trajectory of Appalachian production.

IX. Modern Era: The Independent Midstream Play (2022-Present)

In September 2022, Antero Midstream made a move that signaled a new chapter. The company announced the acquisition of Marcellus gathering and compression assets from Crestwood Equity Partners for $205 million in cash. The deal added 72 miles of dry gas gathering pipelines, nine compressor stations with roughly 700 million cubic feet per day of capacity, approximately 425 undeveloped drilling locations, and 120,000 dedicated acres in Doddridge and Harrison Counties, West Virginia. Crucially, these assets served producers other than Antero Resources. At an adjusted transaction multiple of 4.5x EBITDA, it was financially disciplined. And it represented the first meaningful step toward the customer diversification that investors had been demanding for years.

The acquisition increased Antero Midstream's compression capacity by twenty percent and gathering pipeline mileage by fifteen percent. But its significance was strategic more than financial. It demonstrated that management was willing to deploy capital outside the captive Antero Resources relationship, and that bolt-on acquisitions of existing infrastructure could be a viable path to diversification without the risk and cost of greenfield construction.

What followed was a period of accelerating financial performance. Revenue crossed the billion-dollar mark for the first time in 2023, reaching $1.04 billion. In 2024, the company set records across virtually every metric: throughput volumes, net income, adjusted EBITDA, and free cash flow all hit new highs. Revenue climbed to $1.11 billion. Leverage declined below 3.0x for the first time, and S&P upgraded the company's credit rating to BB+ while Moody's revised its outlook to positive. Management authorized a $500 million share repurchase program in February 2024—a signal that the company believed its stock was undervalued and that it had sufficient cash flow to return capital to shareholders beyond the dividend.

The competitive landscape was shifting too. In 2024, EQT Corporation completed its transformative acquisition of Equitrans Midstream, creating a vertically integrated natural gas behemoth with an enterprise value exceeding $35 billion. This consolidation removed one of Antero Midstream's primary competitors from the independent midstream universe—but also created a much larger, more formidable vertically integrated rival. Williams Companies continued to expand its Appalachian presence through its Transco pipeline system, the largest natural gas pipeline in the country. The Mountain Valley Pipeline, which began operations in June 2024 after years of regulatory delays, added critical takeaway capacity from the Appalachian Basin and opened new markets for the region's producers.

The LNG export boom provided a powerful tailwind. U.S. liquefied natural gas exports reached approximately 14-15 billion cubic feet per day in 2025, with forecasts projecting 16 billion or more in 2026 as new liquefaction trains came online along the Gulf Coast. This surging export demand was forecast to support natural gas prices rising from $3.52 per million BTU in 2025 to $4.31 in 2026. Higher gas prices incentivized more drilling by Appalachian producers, which meant more throughput for midstream operators like Antero Midstream.

In August 2025, a leadership transition marked the definitive end of the founder era. Michael N. Kennedy, who had joined Antero in 2013 and served as CFO of Antero Resources since 2021, was appointed CEO and President of both Antero entities. Paul Rady transitioned to Chairman Emeritus, with a modest $50,000 annual salary through 2028 and continued vesting of equity awards. Rady's step back represented a generational handoff from the geologist-dealmaker who built the Antero empire to a finance-trained executive who had grown up inside it.

Then, in December 2025, Antero Midstream announced the most consequential pair of transactions in its history as an independent company. First, a $1.1 billion acquisition of HG Energy II Midstream Holdings, adding approximately 900 million cubic feet per day of throughput, 50 miles of gathering pipelines capable of handling dry, lean, and liquids-rich gas, 50 miles of water pipelines, and over 400 undeveloped Marcellus drilling locations. At roughly 7.5x EBITDA—or 7.0x adjusted for synergies—it was a larger and more transformative deal than the Crestwood acquisition. Simultaneously, the company announced a $400 million divestiture of all its Ohio Utica gathering, compression, and water handling assets to Infinity Natural Resources and Northern Oil and Gas. That divestiture closed on February 23, 2026, just days ago.

The combined effect was striking: Antero Midstream was shedding low-growth, non-core Ohio assets generating only about $35 million in annual EBITDA—with only three wells expected on the system over the next several years—and redeploying the proceeds into high-growth West Virginia Marcellus infrastructure. Full-year 2025 results showed adjusted EBITDA of $1.125 billion, representing eleven consecutive years of EBITDA growth since the 2014 IPO. Free cash flow after dividends reached $325 million, up thirty percent year over year. Revenue hit $1.19 billion. The company repurchased 9.4 million shares at a weighted average price of $17.28. Leverage stood at 2.7x—down from 3.3x just two years earlier.

For 2026, management guided for adjusted EBITDA of $1.185 to $1.235 billion, an eight percent increase at the midpoint, and free cash flow after dividends of $330 to $390 million. Leverage is expected to temporarily rise to approximately 3.0x following the HG Energy acquisition before resuming its downward trajectory.

X. The Business Model Deep Dive

Strip away the financial engineering and corporate structure drama, and Antero Midstream's business is fundamentally simple: it gets paid to move gas and water. But the simplicity of that description belies the operational complexity and strategic nuance underneath.

The company generates revenue from three primary service lines. The largest is gathering and compression, which accounted for roughly $241 million of the $297 million in fourth-quarter 2025 revenue. This involves collecting raw natural gas from wellheads through low-pressure gathering pipelines, compressing it to higher pressures at compressor stations, and then moving it through high-pressure gathering lines to interconnection points with larger interstate transmission pipelines. Think of it as the last mile of the natural gas system—except in Appalachia, the "last mile" can stretch across dozens of miles of mountainous terrain.

The second service line is water handling, which generated roughly $56 million in the same quarter. This encompasses both fresh water delivery for well completions and produced water disposal. In a region where each well can consume five to ten million gallons of water for hydraulic fracturing and then generate contaminated water for years, the logistics of sourcing, delivering, and disposing of this water are formidable. Antero Midstream's permanent pipeline network for water handling is a genuine competitive advantage: it reduces truck traffic, lowers costs, minimizes environmental risk, and operates with a reliability that trucking-based alternatives cannot match.

The third component, contributing through joint venture distributions, is the company's interest in processing and fractionation operations through its MPLX partnership and the Stonewall high-pressure gathering system with DT Midstream. These JV distributions, budgeted at $135 to $145 million annually, represent high-margin income that requires minimal additional capital investment from Antero Midstream.

The contract structure is the business's economic foundation. Nearly all of Antero Midstream's revenue comes from fixed-fee contracts with minimum volume commitments. This means the company gets paid a set amount per unit of gas gathered, per unit of gas compressed, or per barrel of water delivered, regardless of whether natural gas prices are at two dollars or six dollars. The minimum volume commitments provide a revenue floor even if the producer temporarily reduces drilling activity. It is a toll-road model, and like a toll road, the economics improve dramatically with scale: once the infrastructure is built, the marginal cost of moving an additional unit of gas or water through existing pipes is minimal.

The capital intensity question is important for investors to understand. Building midstream infrastructure is expensive—Antero Midstream spent $179 million on capital expenditures in 2025 and guides for $190 to $220 million in 2026. But the critical distinction is between growth capital (building new pipes and compressor stations to serve new wells) and maintenance capital (keeping existing infrastructure operational). As the Antero Resources drilling program matures and infrastructure buildout nears completion, the ratio should shift increasingly toward lower maintenance spending, which would further boost free cash flow.

The operating leverage in this business model is significant. Because the fixed costs of operating gathering systems and compressor stations do not increase proportionally with throughput volumes, each additional unit of gas flowing through the system drops a disproportionate share of its revenue to the bottom line. This is why Antero Midstream's adjusted EBITDA margins are consistently in the fifty-plus percent range, and why management can guide for EBITDA growth exceeding revenue growth.

The customer concentration issue, while improving, remains the most important structural feature of the business. Antero Resources still generates the vast majority of throughput volumes. The twenty-year dedication agreement that covers substantially all of the parent's acreage is both the company's greatest asset and its greatest vulnerability. The HG Energy acquisition and Crestwood bolt-on have added meaningful third-party volumes, but full diversification will require years of additional effort.

XI. Strategic Analysis: Porter's Five Forces

Understanding where Antero Midstream sits in its competitive ecosystem requires examining the forces that shape industry profitability, beginning with the barriers that protect—or fail to protect—incumbents.

The threat of new entrants into Appalachian midstream infrastructure is genuinely low. Building gathering pipelines and compressor stations requires hundreds of millions of dollars in upfront capital, years of permitting and construction, and the willingness to accept stranded-asset risk if the producer you built for reduces drilling or goes bankrupt. Right-of-way acquisition across Appalachian terrain—where land ownership is fragmented among thousands of individual landowners, often with complex mineral rights histories dating back to the nineteenth century—is a bureaucratic and legal marathon. A new entrant would need not just capital but also the operational expertise to build and operate infrastructure in difficult mountainous terrain with complex geology. And once an incumbent like Antero Midstream has its pipes in the ground and connected to a producer's wells, the economics of building a parallel competing system to the same wells are nearly impossible to justify.

Supplier power in this industry is moderate and largely unremarkable. The key inputs—steel pipe, compression equipment, construction labor—are available from multiple vendors. Equipment manufacturers like Caterpillar and Ariel Corporation have market power during boom periods when demand for compressors surges, but these are cyclical dynamics rather than structural advantages. Antero Midstream's scale gives it reasonable bargaining power with suppliers.

Buyer power is the critical force and the one that has shaped Antero Midstream's strategic evolution. When a single customer generates the vast majority of your revenue, that customer has enormous leverage. Antero Resources can negotiate aggressively on fees, capital spending obligations, and contract terms because Antero Midstream has limited alternatives. The long-term dedication agreement provides protection against losing the customer entirely, but it does not prevent the customer from pressuring economics within that relationship. The diversification push—the Crestwood and HG Energy acquisitions—is fundamentally an effort to reduce buyer power by adding alternative revenue sources.

The threat of substitutes is low to moderate. The primary "substitute" for a dedicated gathering system is the producer building and operating its own midstream infrastructure—which is exactly what Antero Resources did when it created Antero Midstream in the first place. Vertically integrated producers like the newly combined EQT-Equitrans entity represent this model. For other producers, the option of self-building exists but is unattractive given the capital requirements and operational distraction. Virtual pipelines—trucking gas or using compressed natural gas—are technically feasible for small volumes but economically uncompetitive at scale.

Competitive rivalry in the Appalachian Basin is moderate to high at the strategic level but muted at the local level. The basin is served by a handful of large midstream operators: Williams, MPLX (through MarkWest), the integrated EQT-Equitrans system, and Antero Midstream. At a macro level, there is arguably excess gathering and compression capacity in the basin, which limits pricing power. But at a micro level, gathering systems are natural monopolies: once a specific set of wells is connected to a specific gathering system, switching to a competitor is physically impossible without building entirely new infrastructure. This creates a patchwork of local monopolies within a broader competitive market, which is one of the more interesting structural features of the midstream business.

XII. Strategic Analysis: Hamilton Helmer's Seven Powers

Through the lens of Hamilton Helmer's framework, Antero Midstream's competitive position reveals a company with meaningful but narrowly defined powers, and one important vulnerability.

Scale economies exist at the local level but not at the global level. Within its own gathering systems, Antero Midstream benefits from density—more wells connected to the same network means more throughput over the same fixed-cost infrastructure, driving down per-unit costs. The water handling business has particularly strong scale advantages because the permanent pipeline network becomes more efficient as the number of well pads it serves increases. But these are basin-specific, local scale advantages. Antero Midstream does not have the kind of continental-scale pipeline network that gives Williams or Energy Transfer system-wide cost advantages.

Network effects in midstream infrastructure are weak in the traditional sense. A gathering system does not become more valuable to one producer because another producer uses it—there is no viral growth dynamic. However, there is a localized version of network effects in water handling: as the water pipeline network becomes denser, the cost and time to connect new well pads decreases, making the system incrementally more valuable to producers in the area.

Counter-positioning is largely absent. Antero Midstream is following the established industry playbook—fixed-fee contracts, dedication agreements, bolt-on acquisitions—rather than pursuing a fundamentally different business model that incumbents would struggle to replicate. There is nothing about Antero Midstream's approach that larger competitors could not adopt if they chose to.

Switching costs are arguably the company's strongest power. Once a producer's wells are physically connected to a gathering system, switching to a competitor requires building entirely new pipelines to those well locations—an investment that would cost millions per well pad and take months to construct. The twenty-year dedication agreement with Antero Resources adds contractual switching costs on top of the physical ones. Even for third-party customers acquired through acquisitions, the physical lock-in of connected wells creates meaningful retention.

Branding is essentially irrelevant. This is a business-to-business infrastructure service where operational reliability, pricing, and contractual terms matter infinitely more than brand perception. No producer selects a gathering system based on brand equity.

Cornered resource represents Antero Midstream's second most important power. The company's rights-of-way, permits, and physical infrastructure positions in specific areas of Appalachia are genuinely difficult to replicate. Regulatory approvals for new pipeline construction have become harder to obtain over time, and the finite number of feasible routes through mountainous terrain means that existing right-of-way positions have scarcity value. The HG Energy acquisition was partly motivated by the strategic value of its infrastructure positions in productive areas.

Process power exists in moderate form. Antero Midstream has developed genuine operational expertise in Appalachian geology, water handling, and infrastructure construction. But this knowledge is not insurmountable—other well-capitalized operators with experienced teams could develop similar capabilities.

The primary powers, then, are switching costs and cornered resource—an incumbent's fortress built on physical infrastructure and contractual commitments. The key vulnerability is customer concentration: all the switching costs and resource positions in the world matter less if your dominant customer reduces production or renegotiates terms from a position of strength.

XIII. Bear vs. Bull Case

The bull case for Antero Midstream rests on a straightforward thesis: natural gas demand is growing, Appalachian gas is well-positioned to meet that demand, and Antero Midstream owns irreplaceable infrastructure that captures an economic toll on every molecule that flows through its system.

The LNG export buildout is the most powerful near-term catalyst. With U.S. LNG export capacity expected to reach 16 billion cubic feet per day or more in 2026 and additional projects in development that could add another 7 billion or more, the demand pull for domestic natural gas production is substantial and multi-decade in duration. Appalachian gas, with its proximity to East Coast and Gulf Coast export terminals and its low production costs, is among the most economically competitive supply in the country. The Mountain Valley Pipeline's 2024 startup added critical takeaway capacity, and rising gas prices—forecast at $4.31 per million BTU in 2026 versus $3.52 in 2025—will incentivize more drilling, meaning more throughput for Antero Midstream.

The financial profile is increasingly compelling. Eleven consecutive years of EBITDA growth, free cash flow after dividends of $325 million in 2025 growing to potentially $390 million in 2026, leverage declining toward investment-grade levels, and a $500 million share buyback program all point to a business generating more cash than it needs to maintain operations and service debt. The current dividend yield of roughly four percent provides a base return, with potential for dividend growth as leverage reaches target levels. Management has also demonstrated capital discipline—the HG Energy acquisition at 7.0x adjusted EBITDA and the simultaneous divestiture of lower-quality Ohio assets show a willingness to actively manage the portfolio rather than simply accumulate assets.

The energy security narrative adds a geopolitical dimension. European dependence on Russian gas, Asian demand for LNG diversification, and domestic policy support for natural gas as a "transition fuel" all support the argument that Appalachian gas production will remain robust for decades. Data center power demand, an emerging theme that could drive significant new gas-fired generation in Appalachia, represents an incremental growth opportunity that is not yet reflected in most forecasts.

The bear case, however, is not trivial.

Customer concentration remains the most immediate risk. Despite the acquisitions, Antero Resources still dominates the revenue base. The twenty-year dedication agreement provides contractual protection, but contracts are only as reliable as the counterparty's willingness and ability to honor them. If Antero Resources were to face financial distress, reduce its drilling program dramatically, or pursue a strategic alternative that conflicted with Antero Midstream's interests, the midstream entity has limited recourse. The related-party dynamic means that contract renegotiations could occur under conditions that favor the parent at the subsidiary's expense.

The energy transition poses a longer-term existential question. While natural gas's role as a bridge fuel is widely accepted today, aggressive decarbonization scenarios could see gas demand plateauing by the mid-2030s and declining thereafter. If that happens, some Appalachian gathering infrastructure—built to serve decades of production—could become economically stranded. The industry's standard response is that gas demand will grow through at least 2040 or 2050, but this is a probabilistic bet, not a certainty.

Excess midstream capacity in the Appalachian Basin limits pricing power and creates competitive pressure. The EQT-Equitrans vertical integration removed a competitor from the independent midstream market but also created a massive player with no need for Antero Midstream's services. Williams and MPLX have the scale and financial resources to compete aggressively for third-party volumes. In an oversupplied market, the toll rates that midstream operators can charge face downward pressure over time, even if individual contracts are fixed.

Regulatory and environmental risks should not be underestimated. Methane emission regulations are tightening at both federal and state levels. Water disposal regulations in states like West Virginia and Ohio could become more restrictive, increasing compliance costs. Pipeline permitting, already difficult, could become harder if environmental opposition intensifies—a risk that affects both Antero Midstream's ability to build new infrastructure and potential competitors' ability to enter the market.

The governance overhang, while improved, has not fully resolved. Antero Resources' twenty-nine percent ownership stake creates ongoing uncertainty, and the overlapping leadership between the two entities—even after the CEO transition—raises questions about whether Antero Midstream's management truly prioritizes the midstream entity's shareholders or the parent's interests. As an investor, the key KPIs to monitor are: first, the leverage ratio (currently 2.7x, with a target of moving toward investment-grade below 3.0x even post-acquisition, as this determines financial flexibility and dividend sustainability); second, the percentage of revenue from non-Antero Resources customers (the most direct measure of whether diversification is actually happening); and third, free cash flow after dividends (currently $325 million and guided higher, as this represents the true discretionary cash available for debt reduction, buybacks, or growth investment after all obligations are met).

XIV. Lessons & Playbook for Founders and Investors

The Antero Midstream story offers a rich set of lessons about corporate structure, financial engineering, and the underappreciated power of boring businesses.

The first and most striking lesson is that financial engineering is a tool, not a strategy. The MLP structure served its purpose brilliantly during the early years—it allowed Antero to raise over $2 billion in cheap capital to fund infrastructure construction, attract yield-hungry investors, and monetize midstream assets while retaining operational control. But the same complexity that enabled capital raising eventually became a drag on valuation, created governance conflicts, and made the company uninvestable for large swaths of the institutional market. The simplification transaction of 2019 effectively admitted that the original structure had outlived its usefulness. The lesson is not that MLPs are bad—for a specific period and purpose, they were extraordinarily effective. The lesson is that corporate structures should evolve as businesses mature, and management teams that cling to outdated structures because they benefit insiders will eventually face a reckoning with the market.

The captive relationship between Antero Midstream and Antero Resources illustrates both the benefits and dangers of related-party economics. On the benefit side: guaranteed volumes, long-term contracts, and operational coordination made Antero Midstream's cash flows remarkably predictable and enabled rapid infrastructure buildout. On the danger side: customer concentration created dependency, governance conflicts undermined investor confidence, and the parent's financial struggles directly infected the subsidiary's stock price. For founders considering whether to spin off a subsidiary or create a captive service entity, the Antero example suggests that the initial benefits of a captive structure are real but diminish over time as the need for independence and diversification grows.

Infrastructure as a competitive moat is a concept that deserves nuanced treatment. Antero Midstream's gathering pipelines and water handling systems are genuine barriers to competition—they cannot be replicated easily, they create physical switching costs, and their value increases with utilization. But this moat has limits. It is local, not global. It protects against direct competition for existing customers but does not prevent broader industry forces—overcapacity, price pressure, demand shifts—from eroding returns. The strongest infrastructure moats exist when the asset is both physically irreplaceable and sits at a critical chokepoint in the value chain. Antero Midstream's gathering systems meet the first criterion but only partially the second.

Capital allocation in capital-intensive businesses is perhaps the most important lesson. The trajectory from growth-at-all-costs (2014-2018) to deleveraging (2019-2023) to balanced returns (2024-present) mirrors the broader evolution of the energy industry from shale revolution exuberance to financial discipline. The dividend cut of 2021, while painful for income investors, was the right decision for long-term value creation because it accelerated balance sheet repair. Management teams that can resist the temptation to prioritize short-term distributions over long-term financial health tend to create more durable businesses—even if their stock prices suffer temporarily.

The complexity discount is real and costly. For years, investors avoided the Antero midstream entities not because the underlying assets were unattractive but because the corporate structure—three public entities, IDRs, related-party contracts, overlapping management—was simply too complex and conflict-ridden to underwrite with confidence. Simplification immediately broadened the investor base and reduced the governance risk premium. For any company considering a complex multi-entity structure, the Antero experience suggests that the capital raising benefits must be weighed against the long-term valuation discount that complexity imposes.

Finally, the "boring business" opportunity remains underappreciated. In a market obsessed with artificial intelligence, software-as-a-service, and high-growth technology stocks, infrastructure businesses that generate predictable cash flows from physical assets rarely capture investor imagination. But Antero Midstream's eleven consecutive years of EBITDA growth, its multi-hundred-million-dollar annual free cash flow generation, and its essential role in the domestic energy system demonstrate that boring businesses with real assets can compound value over time. The key is management discipline—the willingness to prioritize returns over growth, balance sheet strength over distribution increases, and long-term positioning over quarterly earnings beats.

XV. Epilogue: The Future of Appalachian Infrastructure

The next decade for Antero Midstream will be shaped by forces largely outside the company's control—but its strategic positioning determines whether it benefits from or is threatened by those forces.

The LNG export buildout is the most significant near-term tailwind. With approximately 7 billion cubic feet per day of additional LNG feed gas demand expected from projects reaching final investment decisions, Appalachian gas producers stand to benefit from both higher prices and increased production incentives. The question is how much of this incremental production will flow through Antero Midstream's system versus competitors' infrastructure. The Mountain Valley Pipeline's startup has already begun to ease the takeaway bottleneck that constrained Appalachian production for years, and further pipeline development could unlock additional growth.

Energy transition scenario planning presents the fundamental long-term question. In scenarios where natural gas serves as a "bridge fuel" for decades—displacing coal in power generation and providing baseload backup for intermittent renewables—Appalachian infrastructure like Antero Midstream's could generate returns for twenty to thirty more years. In more aggressive decarbonization scenarios, gas demand could plateau in the 2030s, and some infrastructure investments could become partially stranded. The honest answer is that nobody knows which scenario will materialize, and companies that build optionality into their asset base—through disciplined capital spending, moderate leverage, and contract structures that protect against volume declines—will be best positioned regardless.

The M&A landscape deserves attention. The HG Energy acquisition and Ohio Utica divestiture demonstrated that Antero Midstream is willing to actively reshape its portfolio. In a consolidating industry where scale matters increasingly, the company could be either an acquirer—picking up additional bolt-on systems from smaller operators—or a target. A larger midstream player seeking to consolidate Appalachian infrastructure might view Antero Midstream's assets, cash flows, and contractual position as attractive building blocks. The Antero Resources ownership stake, while declining, adds complexity to any takeout scenario.

The hydrogen and carbon capture wildcards are speculative but worth monitoring. If Appalachian natural gas becomes a feedstock for blue hydrogen production—natural gas reformed into hydrogen with the carbon dioxide captured and sequestered—the demand for midstream infrastructure could actually increase. Several states in the region are exploring carbon capture, utilization, and storage opportunities that could extend the economic life of natural gas infrastructure. These are long-dated, uncertain possibilities, but they illustrate that the energy transition is not necessarily a zero-sum game for natural gas.

Data center power demand represents another emerging opportunity. The explosion of artificial intelligence computing has driven projections for massive electricity demand growth in the coming decade, much of which will be met by natural gas-fired generation. West Virginia's legislature has explored microgrid frameworks that could enable behind-the-meter gas-fired power for data center campuses—a model that would drive natural gas demand in exactly the areas where Antero Midstream operates.

From financial engineering vehicle to real business—that has been the arc of Antero Midstream's story. Born as a tax-advantaged capital-raising structure to fund its parent's drilling program, the company has spent the better part of a decade shedding complexity, reducing leverage, diversifying its customer base, and building the operational credibility to stand on its own. Whether it succeeds will depend on factors both within management's control—capital discipline, strategic acquisitions, operational efficiency—and beyond it: the trajectory of natural gas demand, the pace of the energy transition, and the regulatory environment. What is clear is that the gas beneath Appalachia is not going anywhere, and the infrastructure that connects it to the world will remain relevant for a very long time. The only question is whether Antero Midstream, after its long journey from captive subsidiary to independent operator, has built the organizational capability to capture that relevance and convert it into durable shareholder value.

XVI. Further Reading

For those who want to go deeper into the Antero Midstream story and the broader midstream industry, the following resources provide essential context.

Antero Midstream's SEC filings from 2014 to the present, particularly the 10-K annual reports, offer the most detailed accounting of related-party transactions, contract terms, and financial performance evolution. Gregory Zuckerman's "The Frackers" provides indispensable context on the shale revolution and the personalities who drove it, including the George Mitchell story that made Appalachian gas production possible. Russell Gold's "The Boom: How Fracking Ignited the American Energy Revolution" offers a complementary perspective with more focus on the environmental and social dimensions of shale development.

The Journal of Petroleum Technology's technical papers on Marcellus and Utica development provide the geological and engineering context for understanding why these formations are so productive and what drives well economics. The Energy Transfer Equity lawsuit documents from the mid-2010s offer a case study in MLP conflict-of-interest dynamics that directly parallels the governance concerns at Antero. The activist investor letters sent to the Antero board between 2018 and 2022, beginning with Chapter IV's January 2018 missive, provide a window into the governance reform movement.

The U.S. Energy Information Administration's natural gas infrastructure reports offer the best publicly available data on basin-level production, pipeline capacity, and demand dynamics. RBN Energy's blog archives are an industry-standard resource for midstream infrastructure analysis, with extensive Appalachian coverage. Antero Resources and Antero Midstream investor presentations from 2013 to the present track the evolution of management's narrative and strategic positioning over time. And Steve Coll's "Private Empire" provides the broadest context for understanding how energy industry power dynamics shape the decisions of companies like Antero.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube