Alupar Investimento: The Tollbooth King of South American Energy

I. Introduction & The Magic of Regulatory Tollbooths

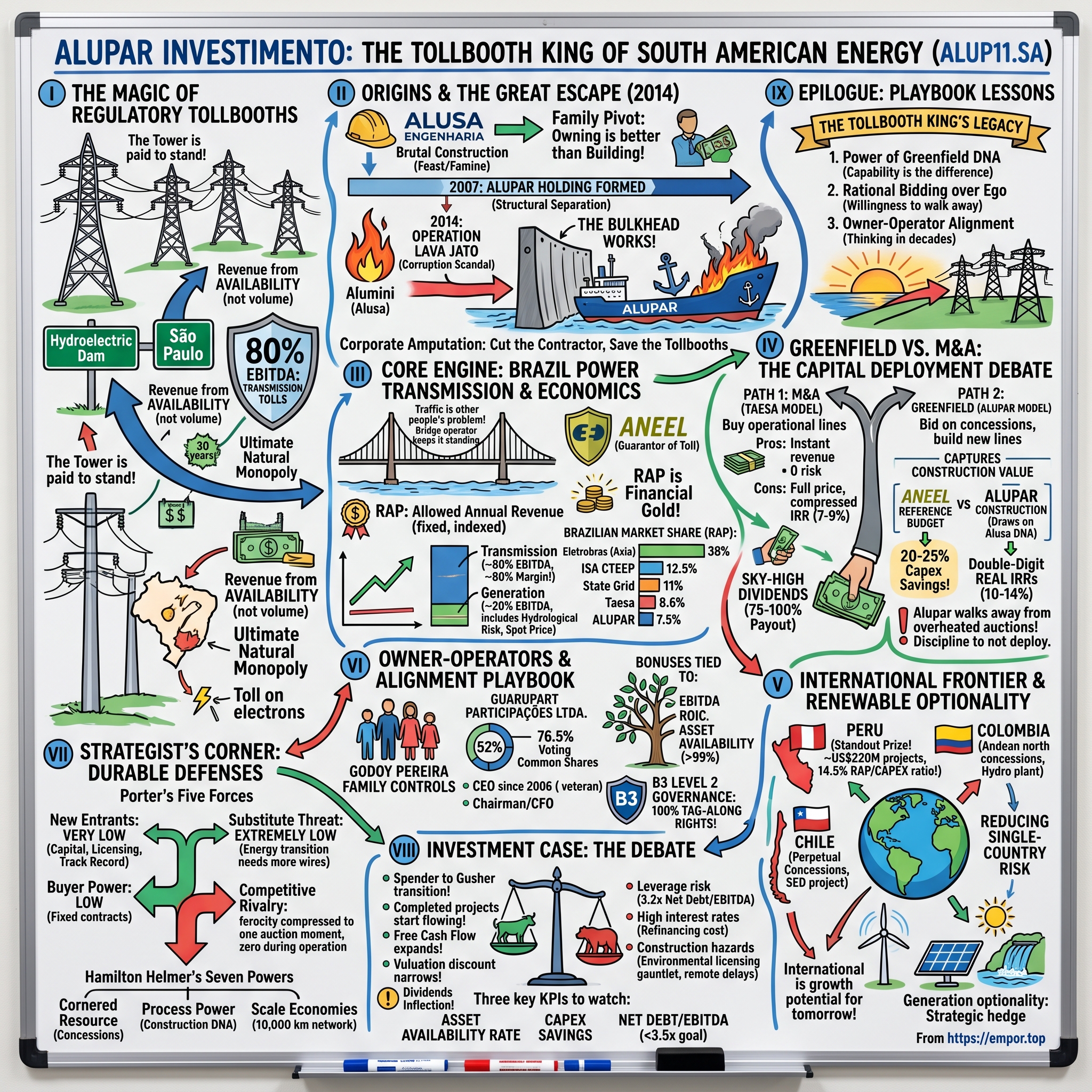

Picture a single steel lattice tower standing alone in the Brazilian Cerrado, that vast tropical savanna that rolls across the country's interior like an ocean of dry grass. There is no city for hundreds of kilometers. There is no factory, no shopping mall, no obvious sign of commerce. There is just this tower, and the next one a few hundred meters away, and the next, marching in a perfectly straight line toward a horizon that shimmers in the heat. Strung between them are high-voltage conductors humming at hundreds of thousands of volts, carrying electricity born from a hydroelectric dam in the Amazon basin toward the air-conditioned apartments and steel mills of São Paulo a thousand kilometers to the south.

Here is the strange and beautiful thing about that tower: from the moment it was energized, somebody has been paid to keep it standing. Not paid based on how much electricity flows through it. Not paid based on whether the economy booms or busts. Not paid based on the weather, the commodity cycle, or who occupies the presidential palace in Brasília. Paid, simply, to keep the line available—up, intact, and ready to carry power—for thirty years, with the payment rising every single year to match inflation. Rain or shine, recession or boom, the cash flows pour in.

This is the magic of the regulatory tollbooth, and it is the closest thing the infrastructure world has to a perpetual motion machine. A power transmission line is the ultimate natural monopoly. Nobody is going to build a second set of towers running parallel to yours—the land rights, the environmental licenses, the capital, and the sheer absurdity of duplicating a wire that already works make it impossible. Once you own the line, you own the toll on a road that electrons have no choice but to travel.

The company at the center of today's story has built an empire on exactly this insight. Alupar Investimento S.A., trading on Brazil's B3 exchange under the ticker ALUP11, is the largest 100% privately controlled electricity transmission player in Brazil.[^1] Roughly 80% of its earnings before interest, taxes, depreciation, and amortization—its EBITDA, the cleanest measure of an infrastructure asset's cash-generating power—comes from these rock-solid, contractually guaranteed transmission tolls.[^2] These are about as close to a government bond as an equity can get, except the coupon grows with inflation and the principal is a physical wall of steel and aluminum stretching across a continent.

And yet—here is the paradox that makes Alupar an interesting business to dissect rather than a sleepy bond proxy to ignore—the company has historically traded at a discount to its "pure yield" peers, the transmission companies that exist mostly to harvest dividends. Why would the market pay less for arguably the most resilient cash flows in Latin American utilities?

The answer is the whole episode. Alupar is not a tollbooth that simply collects coins. It is a builder of tollbooths—a greenfield growth compounder wearing the costume of a sleepy utility. That growth ambition means capital expenditure, leverage, and execution risk, and the market has long debated whether Alupar is a yield stock that's about to start gushing dividends or a perpetual construction project that keeps plowing cash back into the ground.

Over the next two hours, we'll map the full journey. We'll start with the company's roots in the brutal, boom-and-bust world of heavy construction, and the family that realized owning the assets was infinitely better than building them for someone else. We'll watch that same family execute one of the great acts of corporate self-preservation in modern Brazilian history—severing themselves from a construction firm just as it was swallowed whole by the country's largest-ever corruption scandal. We'll dig into the regulatory machinery that makes these tollbooths so reliable, size up the titans Alupar competes against, and unpack the central strategic debate of the business: when growth gets expensive at home, do you buy, build, or board a plane to Peru? Let's get into how the tollbooth king was made.

II. The Origins & The Great Escape of 2014

Every great infrastructure fortune begins with someone holding a shovel for somebody else. In Alupar's case, that shovel belonged to Alusa Engenharia, a Brazilian heavy-construction and engineering contractor that the Godoy Pereira family had spent decades building into one of the country's significant infrastructure builders.1 Alusa did the unglamorous, backbreaking work of the Brazilian economic miracle: pouring concrete, erecting steel, and—crucially for our story—stringing the very transmission lines that crisscross the nation. They were the people in the hard hats and the mud, building the bones of a continent.

To understand the family's pivot, you have to understand how genuinely awful the contracting business is as a way to build durable wealth. Construction contracting is a business of feast and famine. You bid on enormous projects against razor-thin margins, you carry massive working capital, you live and die by the political cycle that funds public infrastructure, and a single delayed payment from a government client or a single cost overrun on a remote project can wipe out a year of profit. You are perpetually exposed—to weather, to labor, to commodity prices, to the whims of whoever controls the public purse. It is a business that demands enormous skill and rewards you with volatility and heartburn.

But the Godoy Pereira family—led by brothers Paulo Roberto and José Luiz—noticed something profound while building all those transmission lines for other people. The companies that owned the finished lines, the concession holders who simply collected the regulated toll for thirty years, had it infinitely better. Same physical asset, completely different economics. The builder eats the risk and earns a one-time, hard-fought margin. The owner sits back and collects an inflation-indexed annuity for three decades. As the old infrastructure adage goes, you don't want to be the one selling shovels in the gold rush if you can quietly own the mine.

So in 2007, the family made the foundational structural decision of this entire saga. They incorporated Alupar as a holding company, designed specifically to hold the stable, regulated concession assets—the tollbooths—and to sit structurally separate from Alusa's volatile engineering and services arm.[^1] On paper in 2007 this looked like ordinary corporate housekeeping, the kind of reorganization that fills a hundred boring legal documents. In hindsight, it was the equivalent of building a watertight bulkhead in a ship years before anyone knew an iceberg was coming. That single act of separation—putting the precious, durable assets in one box and the risky operating business in another—would later save the family's fortune.

The iceberg, when it came, was named Lava Jato.

Beginning in 2014, Brazil was convulsed by Operation Car Wash—Operação Lava Jato—the sprawling corruption investigation that started as a probe into money laundering at a car wash in Curitiba and metastasized into the largest graft scandal in the nation's history.2 At its heart was Petrobras, the state oil giant, and the web of construction contractors who had allegedly paid bribes and rigged bids to win its mega-projects. One by one, Brazil's proudest engineering champions—the Odebrechts, the OAS's, the Camargo Corrêas—were dragged into the maelstrom. Executives went to prison. Companies that had stood for generations were bankrupted, their access to credit cut off overnight, their reputations turned radioactive.

Alusa—by then operating under the name Alumini Engenharia—was swept into this firestorm. The construction arm faced the same existential threat as its peers: financial distress, legal jeopardy, and the slow strangulation that comes when banks, clients, and counterparties all decide at once that they want nothing to do with you.2 Had Alupar still been welded to that engineering business, the contagion would have been catastrophic. Lenders to the contractor could have reached into the whole group. The Alupar name, the concessions, the carefully cultivated relationships with regulators—all of it could have been dragged down into the wreckage by sheer association.

This is the moment the 2007 bulkhead paid off, and the moment the family executed what we'll call the Great Escape. The Godoy Pereiras made the decisive, unsentimental choice to completely detach themselves from the construction business that had made their name. They exited their stake in the contracting firm, walking away from the very company that had been the family's identity for decades, and concentrated 100% of their capital, attention, and—most valuable of all—their reputation on the clean, regulated tollbooths of Alupar.1 It was a corporate amputation performed to save the patient, and it worked. The concession empire was severed from the construction firestorm and sailed on, while the engineering business burned.

There is a lesson here that we'll return to in the epilogue, because it is genuinely one of the more elegant pieces of strategic risk management in Latin American corporate history. But the immediate consequence is what matters for the rest of our story: from roughly 2014 onward, Alupar was no longer a construction family that happened to own some power lines. It was a pure-play infrastructure owner that happened to possess, in its DNA and its institutional memory, the rare ability to build those power lines better than almost anyone. And that inherited engineering knowledge, freed from the toxic balance sheet that had constrained it, was about to become Alupar's single greatest competitive weapon. To see why, we need to understand exactly how the Brazilian transmission machine actually works.

III. The Core Engine: Brazilian Power Transmission & Its Economics

Let's clear up the single most common confusion about the electricity business, because it's the key that unlocks everything about Alupar's quality. When most people think about a power company, they picture either a generator—a dam, a wind farm, a gas plant making the electrons—or a distributor, the utility that sends a bill to your house based on how many kilowatt-hours you burned last month. Both of those businesses care intensely about volume. The generator wants to sell more power; the distributor's revenue rises and falls with how much electricity its customers consume.

Transmission is neither of those things, and that's the whole point. A transmission company owns the high-voltage highway in between—the long-distance superhighway of steel towers and conductors that moves bulk power from where it's made to where it's used. And here is the magic: a transmission company does not have volume risk. It does not care, even slightly, how much electricity Brazilians turn on or off in a given month. It is paid for one thing and one thing only—availability. Keep the physical line up, energized, and ready to carry power, and you get paid your full toll. Whether a thousand megawatts or zero megawatts flow through it on a Tuesday afternoon is completely irrelevant to the check that arrives.

Think of it like a bridge operator who gets paid a fixed, inflation-adjusted annual fee by the government simply for keeping the bridge open and safe to cross—regardless of whether ten cars or ten thousand cars actually drive over it that day. The traffic is somebody else's problem. Your job is to keep the bridge standing. This is why transmission is the most defensive, most predictable corner of the entire energy complex.

The institution that makes this all work—the referee, the rule-maker, the guarantor of the toll—is ANEEL, the Agência Nacional de Energia Elétrica, Brazil's national electricity regulator.3 Over the past quarter-century, ANEEL has built something genuinely rare in an emerging market: a globally respected, deeply stable regulatory framework that international investors trust enough to pour billions into thirty-year commitments. The structure is elegant. The government auctions a concession—the right and obligation to build, own, and operate a specific transmission line—for a term of typically 30 years. In exchange, the winner receives an RAP: the Receita Anual Permitida, or Allowed Annual Revenue.

The RAP is the heartbeat of this entire industry, so let's be precise about what it is. It is a fixed annual revenue, set at the auction, that the concession holder is entitled to collect every year for the life of the contract simply for keeping the line available. And critically—this is the feature that turns a good business into a great one—the RAP is indexed annually to Brazilian inflation, adjusted by indices like the IPCA or IGP-M.3 So as prices rise across the economy, the toll rises automatically to match. The concession holder is structurally protected against the one risk that destroys most long-duration fixed-income-like assets: inflation eating the real value of the cash flow. In a country like Brazil, where inflation has historically been a recurring nightmare, an asset that automatically re-prices with inflation for thirty years is something close to financial gold.

Now, where does Alupar's money actually come from? Two segments, wildly different in character.

The crown jewel is transmission, and it is overwhelmingly the story. Transmission drives roughly 80% of Alupar's regulatory EBITDA—about R$2.82 billion out of a consolidated R$3.30 billion.[^2] And it does so at EBITDA margins of roughly 80%, a figure that sounds almost like a misprint until you remember what the business is.[^2] Once a line is built and energized, the ongoing cost of keeping it available is tiny relative to the toll it collects—a maintenance crew, some monitoring equipment, periodic inspections. There's no raw material to buy, no inventory, no marketing, no volume to chase. You built the asset once; now you mostly just collect. An 80% margin is what it looks like when a business has almost no variable cost and a contractually guaranteed top line.

The second segment is generation, and it plays a supporting role. Alupar owns a portfolio of renewable energy assets—hydroelectric, wind, and solar—totaling 798 megawatts of installed capacity.[^1] Generation contributes the remaining roughly 20% of regulatory EBITDA and gives the company a secondary cash-flow stream plus a foothold in the power-trading side of the market.[^2] But—and this is the honest caveat—generation is a genuinely different animal from transmission. It carries real risks that transmission does not: hydrological risk (in a dry year, the rivers run low and the dams produce less), and merchant price risk (the spot price of electricity swings with supply and demand). Generation is a fine business; it is simply not the serene, weatherproof tollbooth that transmission is. Investors who fall in love with Alupar are falling in love with the 80%, not the 20%.

So how big is Alupar in the grand scheme? The Brazilian transmission sector measured by total RAP is a roughly R$47.4 billion arena, and it is dominated by a handful of titans.4 At the top sits Eletrobras—the recently privatized legacy giant, operating its transmission assets under the Axia Energia banner—commanding something like R$18.0 billion of RAP, a roughly 38% share of the entire market. This is the old state monopoly, vast and sprawling. Next comes ISA Energia Brasil, better known by its historic name ISA CTEEP, which owns the transmission backbone of São Paulo state and holds around R$5.94 billion of RAP, roughly 12.5% of the market. Then there's State Grid Brazil—the local arm of the colossal Chinese state-owned 国家电网 State Grid Corporation—with about R$5.2 billion of RAP, near 11%. And there's Taesa, ticker TAEE11, the celebrated pure-play dividend machine, with R$4.10 billion of RAP, about 8.6%.4

Where does Alupar sit? With roughly R$3.55 billion of RAP, about a 7.5% share of the Brazilian market.4 On paper, that makes Alupar the smaller sibling among giants—the agile private champion competing against privatized state monopolies, a São Paulo state utility, a Chinese sovereign behemoth, and a beloved dividend cow. And that raises the obvious question that defines the next chapter: when you're the nimble private player going up against entities with effectively unlimited balance sheets, how on earth do you grow without getting trampled or, worse, destroying your own capital chasing deals? The answer is a strategic philosophy that sets Alupar apart from nearly every peer it faces.

IV. Greenfield vs. M&A: The Capital Deployment Debate

Here is the fork in the road that every transmission company eventually faces, and the way a management team answers it tells you almost everything about its character. You want to grow your portfolio of tollbooths. There are exactly two ways to do it.

Path one: M&A. You buy lines that already exist, already energized, already throwing off a known RAP. The advantage is obvious—instant, predictable revenue with zero construction risk. The disadvantage is equally obvious: everybody can see exactly what they're worth, so you pay full price, often a premium. You're buying a finished house in a hot market.

Path two: greenfield. You bid at an ANEEL auction for the right to build a line that doesn't yet exist—an empty corridor on a map. You win the concession, then you spend three or four years and a mountain of capital actually constructing it: surveying the route, securing environmental licenses, pouring foundations, erecting towers, stringing conductors. The advantage is that you capture all the value created in the building. The disadvantage is that you carry every ounce of execution risk, and you wait years before the first toll arrives. You're buying an empty lot and building the house yourself.

The cleanest way to see this divergence is to put Alupar's philosophy side by side with that of Taesa, its most famous pure-play peer—because the two companies have made almost opposite bets, and each is internally coherent.

Taesa has historically been the great consolidator, the buyer. Its model is built around acquiring operational, cash-generating lines and funneling that immediate, reliable revenue straight out to shareholders as dividends. A representative move: Taesa acquired five transmission assets from Energisa for R$1.54 billion, picking up roughly R$291 million of incremental RAP in the process.5 That's a clean, fast way to bolt on revenue, and it's precisely what you want if your entire identity is built around a sky-high dividend payout ratio in the range of 75% to 100% of earnings.5 Shareholders buy Taesa for the yield, and M&A keeps the yield fed. But there's a price for that convenience, and it shows up in the returns. Because you're buying finished, de-risked assets in a competitive market, you pay a premium, and that premium compresses your real internal rate of return—the IRR—down into the 7% to 9% range.5 You get certainty and immediacy; you give up upside.

Alupar plays the other game entirely, and it can play it because of who its family used to be. Remember that inherited construction DNA from the Alusa days? This is where it becomes a money machine. Alupar bids on early-stage, greenfield concessions at ANEEL auctions, and then it does something most of its financial-investor competitors cannot: it does its own design, its own engineering, and its own construction management. When ANEEL prepares a transmission auction, it publishes an official reference budget—the regulator's estimate of what the line should cost to build. Most bidders treat that budget as roughly the real cost. Alupar, drawing on decades of hands-on building experience, treats it as a number to beat. And beat it they do, routinely capturing capex savings of 20% to 25% versus ANEEL's official estimate.[^8]

That spread—the difference between what the regulator assumed the line would cost and what Alupar actually spends to build it—is pure value creation, and it flows directly into returns. By building for meaningfully less than the budgeted cost while still collecting the full budgeted RAP, Alupar unlocks double-digit real IRRs in the range of 10% to 14% once the assets are energized.[^8] Compare that to the 7% to 9% a pure acquirer earns paying premiums for finished assets, and you see the entire thesis in one number. Alupar isn't just collecting tolls; it's manufacturing them below cost and pocketing the construction spread. It is, in effect, both the contractor and the owner—capturing the builder's margin and the owner's annuity in a single transaction with itself.

But the greenfield strategy only works if you have the discipline to use it selectively, and this is where Alupar's character is most clearly revealed. Brazilian transmission auctions became fiercely, almost irrationally competitive over the years. To win a concession, bidders compete by offering discounts on the RAP—essentially agreeing to accept a lower annual toll in exchange for the right to build. In the most overheated auctions, competitors have offered RAP discounts of 50% or more, slashing the future revenue to the point where the economics barely make sense even for a low-cost builder.[^8] At those levels, the only way to make the numbers work is to assume heroic construction savings and flawless execution—a recipe for destroying capital while feeling like you're growing.

Alupar's response to these overheated auctions is its single most underrated competitive advantage: it walks away. Management has shown a consistent willingness to sit on its hands when the bidding gets stupid, to let a competitor "win" a concession that's been bid down to a value-destroying RAP, and to wait patiently for a more rational auction or a more attractive opportunity abroad.[^8] In a world where most management teams are addicted to growth for its own sake—where "we deployed capital this quarter" is treated as an achievement regardless of the return—the discipline to not deploy is genuinely rare and genuinely valuable. Walking away from a bad deal isn't a failure to grow; it's the active protection of the only thing that matters, which is the return on every real you invest.

That discipline, however, creates its own challenge. If you refuse to overpay at home, and home is getting more crowded and competitive every year, where do you put the capital? For Alupar, the answer increasingly lies beyond Brazil's borders, in the mountains of the Andes and the high deserts of Peru and Chile—markets where the greenfield-engineering advantage still commands a premium and the auctions haven't yet been bid into oblivion.

V. The International Frontier & Renewable Optionality

There's a moment in the life of every successful, disciplined capital allocator when the home market stops being big enough—or rather, stops being cheap enough—for its ambitions. For Alupar, the relentless compression of returns in Brazilian auctions, where rivals would bid RAP discounts past the point of economic sense, created exactly that moment. If the greenfield-engineering edge couldn't earn a fair return at home because everyone was giving the value away to win, the rational move was to take that edge somewhere the competition was thinner and the math still worked. So Alupar packed up its core competence—the ability to design and build transmission lines cheaper and faster than financial-only bidders—and went looking across South America.

The standout prize came in late 2025, in Peru. Alupar won a substantial package worth approximately US$220 million covering four distinct transmission projects—Palca, Planicie-Industriales, Abancay Nueva, and San Rafael-Ananea—with commercial operation targeted for 2029.6 What made this win so attractive wasn't merely the headline size; it was the ratio buried in the economics. The projects carried a RAP-to-CAPEX ratio of around 14.5%, meaning that for every dollar of capital invested in building the lines, Alupar would collect roughly 14.5 cents of annual regulated revenue.6 In a Brazilian auction bid down 50%, that ratio would be a fraction of this. Peru, with its less crowded field and genuine need for new transmission infrastructure to connect its mining heartland and growing cities, offered Alupar precisely the kind of return its home market had stopped providing. This is the greenfield playbook exported wholesale: same engineering discipline, same construction spread, applied where competition hasn't yet competed away the profit.

Peru is the marquee example, but it's part of a broader regional mosaic. In Chile, Alupar has captured transmission concessions including the SED project—and Chilean transmission concessions carry a particularly appealing feature: many are effectively perpetual or very long-dated, a structural sweetener compared to Brazil's 30-year clock.[^1] In Colombia, the company has pursued long-term concessions and assets including the Morro Azul small hydroelectric plant (PCH), extending both its transmission and generation footprint into the Andean north.[^1] Each of these is a beachhead—individually modest, but collectively transforming Alupar from a purely Brazilian story into a genuine pan–South American infrastructure operator.

Now, it's important to size this honestly rather than oversell it, because the international story is more optionality than core today. Brazil remains overwhelmingly the value driver, contributing on the order of 90% of EBITDA at present.[^2] The international portfolio is not yet large enough to move the consolidated numbers dramatically. What it provides instead is two things that matter enormously to a long-term investor: real geographical diversification—reducing the company's total exposure to any single country's regulatory, currency, or political risk—and a pipeline of high-return optionality that could drive the future investment thesis as those projects energize through the late 2020s. The international frontier is where tomorrow's growth gets seeded while Brazil pays today's bills.

And then there's the generation fleet, which deserves a brief word as the supporting cast. We met it earlier—the 798 megawatts of hydro, wind, and solar contributing roughly a fifth of regulatory EBITDA.[^1] Beyond its direct cash flow, generation plays a strategic role that's easy to miss: it acts as a natural hedge and a source of scale and power-trading capability that complements the core transmission business. A company that both moves power and makes power has more levers, more market intelligence, and more ways to optimize across the energy system than a pure-play transmission operator. It's not the reason to own Alupar, but it's a sensible diversifier that fits the broader infrastructure-owner identity.

What ties all of this together—the disciplined bidding, the construction spread, the patient international expansion, the renewable hedge—is not a strategy document or a consultant's deck. It's a family. Every one of these decisions traces back to a set of owners whose own fortune rises and falls with the same shares ordinary investors hold, and who think in decades because they intend to be holding the same stock in a decade. To understand why Alupar behaves the way it does, you have to understand who owns it.

VI. Owner-Operators & The Alignment Playbook

Walk into the boardroom of a typical large utility and you'll find professional managers—skilled, credentialed, well-compensated—whose personal net worth is largely disconnected from the stock price. They earn salaries and bonuses; if the shares fall 30%, their lifestyle is unaffected. This is the principal-agent problem that haunts public markets, and it's why so much shareholder value gets quietly eroded by empire-building, quarter-chasing, and capital deployed for the sake of looking busy. Alupar is the antidote to that problem, and the reason is structural: this is a classic owner-operator story, where the people running the company are the people who own the company.

The Godoy Pereira family controls Alupar through their private holding company, Guarupart Participações Ltda., which holds approximately 52% of the company's total capital and—more importantly for control—about 76.5% of the voting common shares.[^1] That distinction matters. Total capital tells you their economic stake; the 76.5% of voting shares tells you they have ironclad, unambiguous control over the company's direction. There is no activist who can force a fire sale, no hostile acquirer who can sweep in, no proxy fight that can redirect strategy. The family decides. And because more than half their wealth is bound up in the same equity public shareholders buy, what's good for the family is, by construction, good for minority investors. Their incentive is to compound value over decades, not to juice a quarter.

The two figures at the top embody this. Paulo Roberto de Godoy Pereira has served as CEO since 2006—roughly two decades at the helm, a tenure that itself signals the long-term orientation of the place.[^1] He is a genuine veteran of Brazilian infrastructure, a man who has spent his career in the world of concessions, construction, and energy policy, and who served as President of ABDIB, the Brazilian Association of Infrastructure and Base Industries—the country's premier infrastructure trade body.7 That's not a ceremonial line on a résumé; it means Paulo Roberto sat at the center of Brazil's infrastructure policy conversation, with the relationships and regulatory fluency that come from helping shape the rules of the game he plays. Alongside him, his brother José Luiz de Godoy Pereira serves as Chairman of the Board and CFO, holding the dual reins of governance and finance.[^1] It is, in the most literal sense, a family running its own money.

But here's where Alupar goes beyond the typical family-controlled company, and where the governance story gets genuinely interesting. Family control is a double-edged sword—it aligns the controllers beautifully but can leave minority shareholders vulnerable to a dominant clan that runs the company for itself. Alupar addresses this with two deliberate mechanisms.

First, incentive design that extends past the family to the broader management team. Short-term incentives—the annual bonuses—are tied directly to the operational metrics that actually matter for a tollbooth business: regulatory EBITDA, return on invested capital (ROIC), and, crucially, asset availability rates.[^1] That last one is the heartbeat of the whole model. Remember, transmission companies get paid to keep lines available; if availability slips, ANEEL imposes penalties that deduct from revenue. By tying bonuses to availability, management's pay is welded to the single operational variable that protects the toll. It's a near-perfect alignment of compensation with the economics of the asset. On the long-term side, Alupar runs a structured incentive plan (the PILP) featuring stock options and restricted stock units that expose executives directly to the long-run price action of ALUP11 units.[^1] Managers don't just collect cash for hitting this year's numbers; they hold equity whose value depends on the company still being excellent in five and ten years.

Second, and perhaps most reassuring for any outside investor weighing a family-controlled stock, is Alupar's governance tier. The company is listed on the B3's Level 2 corporate governance segment, one of the elevated standards above the basic listing requirements.8 The single most valuable feature of that tier, in Alupar's case, is 100% tag-along rights extended to both common and preferred shareholders.8 Let's unpack what that means in plain terms, because it's the kind of protection that sounds like legal boilerplate but can be worth a fortune. Tag-along rights mean that if the controlling family ever sells its stake in a change-of-control transaction, minority shareholders have the right to "tag along" and sell their shares at the same price the family receives. The controllers cannot negotiate a fat premium for themselves and leave minority investors holding shares at a depressed market price. With 100% tag-along, the family and the smallest retail shareholder ride out any sale on equal terms. It's a structural guarantee that the family can't enrich itself at minorities' expense in the one moment—a sale of the company—where that abuse most often happens.

Put it all together and you have an unusually clean alignment: a controlling family with the majority of its wealth in the stock, run by veterans with deep policy relationships, with management compensation tied to the right operational metrics, all wrapped in governance protections that put minority investors on equal footing. This is the human foundation beneath the financial machine. But alignment and competence, however admirable, don't by themselves create a moat. To judge whether Alupar's advantages are durable—whether they'll still be standing in twenty years—we need to run the business through the cold, analytical frameworks that strip away the storytelling and ask: what, structurally, protects these cash flows?

VII. The Strategist's Corner: Porter's Five Forces & Hamilton's Seven Powers

Let's put Alupar on the dissection table and apply two of the most respected frameworks in competitive strategy. The point isn't academic box-checking; it's to test whether the tollbooth's defenses are real and lasting or merely comfortable for now. We'll start with Michael Porter's Five Forces, the classic lens for assessing industry structure, and then layer on Hamilton Helmer's Seven Powers, the more modern framework for identifying durable competitive advantage.

Begin with the threat of new entrants, and the verdict is very low—about as low as it gets in any industry on earth. To enter transmission, a newcomer would need three things that are extraordinarily hard to assemble simultaneously. First, staggering capital: building a transmission line costs hundreds of millions of dollars before a single toll is collected, and the payback stretches over decades. Second, the ability to clear Brazil's environmental and land-licensing gauntlet—a process so slow and complex that it defeats even experienced players. Third, a credible engineering track record, because ANEEL auctions favor bidders who can actually deliver. A financial newcomer with a checkbook but no construction history is at a structural disadvantage. These three barriers, stacked together, mean the field of credible competitors is small and essentially fixed.

Next, the bargaining power of buyers, which is low in a fascinating and specific way. Who is Alupar's "buyer"? Not a fragmented base of customers who could shop around—the buyer is effectively the national grid system itself, with revenues pooled and paid through the regulated framework. Now, there's a nuance here that prevents this from being a pure monopoly fantasy: the state, through ANEEL, sets the maximum RAP during the auction, and competitive bidding can drive that revenue down. So there is real pricing pressure—but, and this is the crucial point, it exists only before the contract is signed. Once Alupar has won the concession and signed the 30-year agreement, the cash flows are legally protected, contractually fixed, and adjusted upward for inflation every year. The buyer's power is concentrated entirely in a single moment at auction and then evaporates for three decades. It's the inverse of most businesses, where customers can squeeze you every single year.

The threat of substitutes is extremely low, bordering on nonexistent. What could substitute for a physical high-voltage long-distance wire? There is simply no technology that moves bulk electricity across a thousand kilometers without one. Even the rise of distributed, localized solar generation—rooftops, small solar farms—doesn't threaten the core business; if anything, it complements it. Brazil's renewable bounty, its enormous hydro and wind and solar resources, is concentrated in specific regions, often far from where the power is consumed. Moving that bulk green energy from the windy northeast or the river-rich north to the industrial southeast requires massive transmission systems. The energy transition, far from making transmission obsolete, makes it more essential. The substitute risk runs in Alupar's favor.

Then there's competitive rivalry, and here's the elegant twist that defines the entire industry: rivalry is high at auction and zero in operation. Before a concession is awarded, the competition is ferocious—we've seen bidders slash RAP by 50% or more to win. But the instant a line is built and energized, it becomes a local natural monopoly. There is no rival line running alongside it, no competitor offering the same route at a lower toll, no daily battle for market share. The fierce competition is compressed into a single bidding event, and then it vanishes entirely for the 30-year life of the asset. This is why bidding discipline—Alupar's willingness to walk away—matters so much: the auction is the only moment competition can hurt you, so the entire game is won or lost there.

Now layer on Helmer's Seven Powers, which asks not just whether the industry is attractive but what specific, durable advantages a given company possesses. Three of the seven apply with real force to Alupar.

The first and most obvious is Cornered Resource. Alupar's exclusive 30-year concession contracts, granted by the government, are the textbook definition—a coveted asset that competitors simply cannot access. No rival can build a parallel line on the same route; the concession is the right to be the monopoly. Each contract is a cornered resource with a multi-decade clock, and the inflation indexation means it's a cornered resource that grows in nominal value every year.

The second, and the one that genuinely distinguishes Alupar from its peers, is Process Power—the company's inherited construction DNA. This is the through-line of our entire story. Because Alupar can design and build transmission lines cheaper and faster than financial-only bidders, it captures that 20% to 25% construction spread we discussed, translating into superior IRRs.[^8] Process Power is, by Helmer's definition, an advantage embedded in a company's organization and activities that competitors can't easily replicate even if they know exactly what you're doing—and that fits Alupar perfectly. A financial buyer can't simply hire its way to decades of accumulated engineering know-how overnight. The construction capability is the moat that lets Alupar earn building returns on top of owning returns.

The third is Scale Economies. Alupar operates and maintains a network of roughly 10,000 kilometers of transmission lines, and the operations-and-maintenance cost of that network gets spread across the whole footprint.[^1] The marginal cost to Alupar of maintaining one additional kilometer of wire—dispatching crews, monitoring systems, managing the asset—is lower than it would be for a small, sub-scale regional operator carrying the same fixed overhead across far fewer kilometers. As the network grows, the per-kilometer cost advantage compounds, making each new concession more profitable to operate than it would be in isolation.

The picture these frameworks paint is of a business with extraordinarily durable defenses: nearly impregnable to new entrants, immune to substitution, monopolistic in operation, fortified by cornered concessions, sharpened by process power, and made more efficient by scale. But a great business and a great investment are not the same thing—the question for any investor is whether those durable advantages are fairly priced, and what could still go wrong. That's the debate we turn to now.

VIII. The Investment Case: Bull vs. Bear

Every infrastructure stock eventually arrives at a defining inflection, and for Alupar that inflection is the transition from spender to gusher—from a company plowing capital into the ground to one harvesting the cash those investments throw off. Whether you're a bull or a bear on Alupar largely comes down to how you weigh that transition against the risks of getting there. Let's argue both sides honestly.

The bull case rests on a dividend inflection point. For years, Alupar has been in the heavy-construction phase of its growth cycle—winning greenfield concessions and then pouring billions into building them, which suppresses free cash flow because the money goes out long before the tolls come in. That cycle has been culminating in a wave of major projects reaching completion. The flagship example is the massive TECP project in São Paulo, whose Phase I was energized in late 2025—and energized 11 months ahead of schedule.9 That early completion is doubly meaningful: it brings forward revenue, and it's a vivid demonstration of the Process Power thesis in action, because building faster than planned is exactly what a company with superior engineering capability does.

The mechanics of the bull case flow directly from that. As the big capex projects finish and start generating their inflation-indexed tolls, two things happen at once: the cash going out (construction spending) falls, and the cash coming in (RAP from newly energized lines) rises. Free cash flow expands, potentially dramatically. And Alupar's stated policy is to pay out at least 50% of regulatory net income as dividends.[^1] So as the capital cycle winds down and net income converts more cleanly into distributable cash, the bull argues Alupar transforms from a "growth-utility"—forever reinvesting—into a high-yielding cash cow. If that happens, the historical valuation discount to pure-yield peers like Taesa should narrow, because the very thing that justified the discount (the heavy reinvestment) would be ending. The bull is buying the moment the construction project becomes a tollbooth that finally pays its owner.

The bear case is equally grounded, and it centers on two risks: leverage and construction hazard. Start with leverage. Building all those greenfield lines requires debt, and Alupar's net debt to EBITDA currently sits at roughly 3.2x.[^2] That's a level the company considers secure and consistent with its investment-grade profile, but it's not trivial—and here's where Brazil's macro environment bites. Brazilian interest rates, governed by the central bank's SELIC policy rate, have a history of climbing to punishing levels to fight inflation. Alupar finances itself substantially through inflation-linked debentures, and in a high-rate environment, the cost of refinancing that debt rises. A company carrying 3.2x leverage through a period of expensive money faces real pressure on its interest burden—the kind of pressure that can eat into the very free-cash-flow expansion the bulls are counting on. Leverage is fine until the cost of money spikes; then it's a headwind.

The second bear concern is execution and licensing risk—the flip side of the greenfield strategy. Building transmission lines in remote Brazilian terrain is genuinely, notoriously hard. Consider the TNE project, which involves connecting Roraima—Brazil's only state not linked to the national grid—through dense, ecologically sensitive Amazonian territory.[^1] Projects like this face a gauntlet of environmental licensing bottlenecks, indigenous land considerations, and sheer geographic difficulty that can produce costly delays. And in the greenfield model, delays are expensive in a specific way: you've committed the capital and you're carrying the cost, but the RAP doesn't start flowing until the line is energized. The same construction capability that creates Alupar's edge also exposes it to execution risk that a pure acquirer of finished assets simply doesn't face. The bear isn't saying Alupar can't execute—the TECP early completion argues otherwise—but rather that one badly delayed mega-project in a hostile environment can meaningfully dent returns and stress the balance sheet simultaneously.

How should an investor adjudicate this? Rather than a verdict, the disciplined approach is to watch the handful of metrics that will actually reveal which scenario is unfolding. Three KPIs matter most for tracking Alupar over time.

The first is the asset availability rate. This is the operational heartbeat of the tollbooth model: availability must stay above roughly 99% to avoid ANEEL's penalty mechanism—the Parcela Variável, or Variable Parcel, which deducts revenue when lines underperform on availability.3 A persistent slip in availability would signal operational trouble striking at the core of the cash flow. Watch it.

The second is capex savings—the spread between ANEEL's estimated cost for a project and Alupar's actual construction cost. This single number captures the entire Process Power thesis. As long as Alupar keeps building meaningfully below the regulator's budget, the greenfield engine is working and IRRs stay in the double digits. If that spread compresses, the central competitive advantage is eroding.

The third is net debt to EBITDA, which is the balance-sheet pressure gauge. Alupar aims to keep leverage below roughly 3.5x to preserve its prized AAA(bra) national-scale credit rating—the top domestic rating, which keeps its cost of borrowing low and its access to capital open.10 Leverage drifting above that threshold would be the early warning that the construction cycle is straining the balance sheet faster than the new tolls can repair it. These three numbers—availability, capex savings, and leverage—together tell you whether the bull's gusher or the bear's squeeze is winning.

IX. Epilogue & Playbook Lessons

Step back from the spreadsheets and the strategy frameworks, and what lingers is the human drama at the heart of this story—the surprise that makes Alupar worth remembering. A family that had spent decades as builders, with their name and fortune tied to one of Brazil's significant engineering contractors, watched that entire world come under existential threat as the Lava Jato scandal consumed the country's construction industry. And because they'd had the foresight, years earlier, to wall off their precious concession assets in a separate structure, they were able to perform a clean amputation—cutting loose the contracting business and saving an extraordinarily lucrative, decades-long stream of regulated energy cash flows from being dragged into the legal collapse. It's a vivid illustration of a principle that most companies learn far too late, if at all: isolate your structural risks early, before you know which iceberg is coming, because by the time you see it, it's too late to build the bulkhead.

From that drama and the business that emerged from it, three playbook lessons stand out for any long-term investor.

The first is the power of greenfield DNA. The conventional path to growth in infrastructure is to buy finished cash flows—but you pay a premium for the privilege, and that premium compresses your returns to single digits. Alupar's lesson is the opposite: if you possess genuine operational process power—the inherited ability to design and build the asset yourself at a discount to what the regulator assumed—then don't buy at a premium. Build at a discount and capture the spread. The construction capability that came from the family's contracting roots is precisely what lets Alupar earn double-digit real returns where pure acquirers earn far less. Capability is the difference between paying retail and manufacturing at cost.

The second is rational bidding over ego. In an industry where growth is celebrated and capital deployment is mistaken for achievement, Alupar's willingness to walk away from overheated auctions—to let competitors "win" concessions bid down to value-destroying levels—is its quietest and most important discipline. True competitive advantage often isn't doing more; it's having the temperament to do nothing when the math doesn't work, even when the market is clamoring for growth. Capital not destroyed is capital available for the next great opportunity, whether that's a rational Brazilian auction or a 14.5% RAP-to-CAPEX project in the Peruvian highlands.

The third is owner-operator alignment. When the family controlling a company holds the majority of its wealth in the same common shares and long-term units that public investors own, and when management's compensation is welded to the operational metrics that actually drive the asset's value, you can extend a kind of trust that's impossible with hired managers chasing quarterly optics. The Godoy Pereiras are running Alupar for the next decade because they fully intend to still own it in the next decade. For an investor whose own time horizon stretches across the 30-year life of a transmission concession, that alignment—between the people building the towers and the people who own them—may be the most valuable asset of all.

References

-

Alupar Corporate Profile & Infrastructure Project Tracking — BNamericas ↩↩

-

Alupar Investimento S.A. Financial News & Sector Analysis — Valor Econômico ↩↩

-

Energy Sector Analysis & Concession Auctions Coverage — CanalEnergia ↩↩↩

-

In-depth Corporate Strategy and Utility Sector Insights — Brazil Journal ↩↩↩

-

Alupar Corporate Profile & Infrastructure Project Tracking — BNamericas ↩↩

-

Alupar Investment Coverage & Valuation Reports — BTG Pactual Research ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube