Allison Transmission: The Unsung Giant That Keeps the World Moving

I. Introduction & Episode Roadmap

Picture this: you are standing on a busy city street corner. A municipal bus groans to a stop in front of you, exhaling its hydraulic brakes. Behind it, a garbage truck heaves its way through its morning route, stopping every thirty seconds, lurching forward, stopping again. Down at the construction site across the road, a cement mixer rotates patiently while a dump truck climbs a muddy grade with forty tons of gravel. And somewhere far from here, an M1 Abrams tank—seventy tons of American steel—pivots on its tracks with a precision that defies its mass.

What do all of these machines have in common? They all depend on transmissions built by a company most people have never heard of: Allison Transmission, headquartered in Indianapolis, Indiana. Allison is the world's largest manufacturer of fully automatic transmissions for medium- and heavy-duty commercial vehicles, and it holds roughly 77% of the North American market in its core segment. That is not a typo. In a world obsessed with disruption and competition, a single company controls more than three-quarters of a critical infrastructure market—and has for decades.

Here is the question worth sitting with: How does a 111-year-old company dominate a market that most people do not even know exists? And perhaps more importantly, how does it navigate the single biggest technological disruption in the history of ground transportation—the shift from internal combustion to electric propulsion—without losing its footing?

Before diving into the history, it is worth understanding why commercial vehicle transmissions are a fundamentally different animal from the automatic in your sedan. A passenger car transmission handles perhaps 200 to 300 horsepower and shifts a handful of times on a typical commute. A commercial vehicle transmission must manage 1,200 to 2,050 pound-feet of sustained torque—imagine the force needed to start moving an 80,000-pound vehicle from a dead stop on a steep hill—while enduring hundreds of shift cycles per day. A refuse truck collecting garbage on its morning route can shift over 300 times before lunch. That level of mechanical punishment would obliterate a passenger car transmission within hours. The physical size, the material science, the thermal management, and the electronic control systems all operate in a different engineering universe. This is not a commodity product. It is a precision instrument built for extreme conditions, and that distinction explains almost everything about Allison's competitive position.

The Allison story is really four stories layered on top of each other: an origin myth rooted in racing and aviation, a half-century as a hidden gem buried inside General Motors, a private equity transformation that unlocked its potential, and an ongoing strategic pivot that may determine whether the company thrives for another century or fades into obsolescence.

Each chapter reveals something different about how great industrial businesses are built, maintained, and reinvented. And taken together, they form one of the most compelling case studies in American industrial history—a company that has been essential but invisible for so long that most investors have never bothered to look beneath the surface. Those who have looked have generally liked what they found.

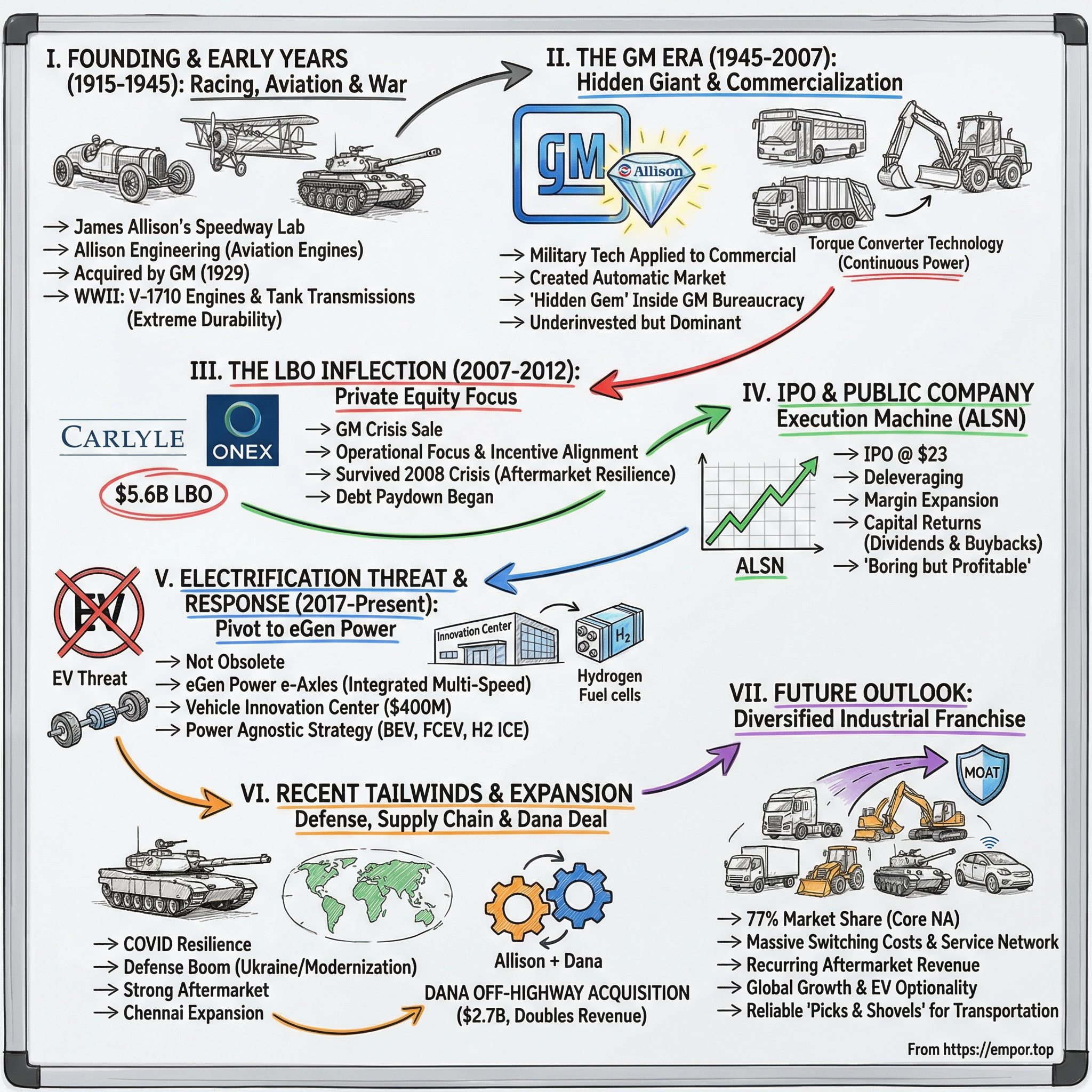

II. The Founding & Early Years: From Racing to Military (1915–1945)

Indianapolis, 1915. The city had already established itself as the beating heart of American motorsport—the Indianapolis 500 had been running for four years, drawing engineers, mechanics, and dreamers from across the country. Among the race's co-founders was James Allison, a man whose name would echo through the next century of American industrial history, though not in the way he initially imagined.

James Allison was not a gearhead in the conventional sense. He was an entrepreneur and a precision-engineering obsessive who had made his early fortune manufacturing automobile headlights and speedometers through the Indianapolis-based Prest-O-Lite company. When he co-founded the Indianapolis Motor Speedway in 1909 alongside Carl Fisher, Arthur Newby, and Frank Wheeler, it was not merely a passion project—it was a laboratory. The Speedway was designed as a proving ground where automotive technology could be pushed to its absolute limits, and Allison understood that the knowledge generated on that oval track would have applications far beyond racing.

In 1915, Allison founded the Allison Engineering Company with a focus that might surprise anyone who knows the company only as a transmission maker: aviation engines. The early years were spent developing and servicing aircraft engines, positioning the company at the intersection of automotive precision and the nascent aviation industry. Allison's engineering shop became known for its obsessive standards of quality—a reputation that caught the attention of the United States military.

Then came the deal that changed everything. In 1929, General Motors acquired Allison Engineering, folding it into the vast GM empire. James Allison himself had passed away in 1928, but his company's trajectory was already set. Under GM's ownership and with access to GM's capital, Allison's aviation division produced the V-1710 liquid-cooled aircraft engine that powered the P-38 Lightning, the P-40 Warhawk, and other iconic fighters during World War II. More than 70,000 of these engines rolled off the Indianapolis production lines, establishing the facility's reputation for high-volume precision manufacturing under extreme wartime pressure.

But the more consequential development—at least for the story being told here—was happening on the ground, not in the sky. The U.S. military needed transmissions capable of handling the extraordinary torque and weight of tanks and armored vehicles. Manual transmissions, the standard for trucks and military vehicles at the time, required skilled drivers who could "double clutch" through gear changes—a technique demanding precise coordination of clutch, throttle, and gear lever. In a tank, under fire, with a crew focused on fighting rather than driving, manual shifting was a dangerous liability. The military wanted automatic transmissions that could handle combat conditions without requiring a trained driver to nurse them through every gear change.

Allison's engineers, steeped in the precision culture of aviation manufacturing and backed by GM's resources, rose to the challenge. The transmissions they developed for military tracked vehicles during the 1940s laid the engineering foundation for everything that followed. The military demanded reliability under the most extreme conditions imaginable—heat, cold, mud, sand, steep grades, shock loads from rough terrain and weapons fire. Meeting those requirements forced Allison to develop the torque converter technology, materials science, and electronic controls that would become the company's core competitive advantage for the next eight decades.

There is a detail worth lingering on here, because it illuminates a pattern that repeats throughout Allison's history. The military did not merely want automatic transmissions—it wanted automatic transmissions that could operate in the Sahara at 130 degrees Fahrenheit, in the Ardennes in freezing mud, at altitude, under vibration, with minimal maintenance by soldiers whose primary job was fighting, not mechanical repair. Every one of those requirements pushed Allison's engineers to design beyond what any commercial customer would ever demand. The resulting products were not just adequate for civilian use—they were massively overengineered, which in the transmission business translates directly to longevity and reliability.

The key insight from this period is straightforward but profound: military requirements drove innovation that commercial markets alone would never have demanded. The specifications were so extreme that meeting them produced technology with an enormous performance margin when applied to civilian applications. A transmission engineered to survive tank combat was dramatically overbuilt for a city bus—which meant it was also dramatically more reliable. That reliability gap between Allison and everything else on the market would prove to be the foundation of the entire business. And the relationship with the military—forged in the desperate urgency of global war—would endure for eight decades and counting, eventually becoming one of Allison's most valuable business segments.

III. The GM Era: Innovation Under the Giant (1945–2000s)

When the guns fell silent in 1945, Allison faced a question common to every wartime manufacturer: what now? The aviation engine business, which had been running at full wartime capacity, was about to collapse as military orders evaporated. But the transmission technology developed for tanks and armored vehicles offered a different path forward.

In 1946, GM's Allison division began applying its military transmission expertise to commercial vehicles. The logic was elegant: if you could build a transmission that survived tank combat, you could certainly build one that handled the daily grind of a city bus or a delivery truck. By the late 1940s, Allison introduced its first fully automatic transmission designed specifically for commercial vehicles—a product category that, remarkably, did not really exist before Allison created it.

To understand why this mattered, consider the state of commercial vehicle transmissions at mid-century. Long-haul trucks and buses used manual transmissions with as many as 10 to 18 forward gears, arranged in complex compound configurations. Drivers had to master the art of "double-clutching"—a technique where, for each gear change, the driver pushes the clutch, shifts to neutral, releases the clutch, blips the throttle to match the engine speed to the new gear ratio, then pushes the clutch again and completes the shift. It is as difficult as it sounds, and it requires years of practice to do smoothly in a fully loaded truck climbing a mountain grade. In vocational applications—garbage trucks that stop every thirty seconds, transit buses in dense urban traffic—this constant manual shifting was not just difficult but exhausting and dangerous.

Allison's fully automatic transmission eliminated all of that. The heart of the technology was the torque converter—a fluid coupling device that sits between the engine and the transmission.

Think of it like two fans facing each other in a sealed chamber filled with oil. The engine spins one fan (the pump), which flings the oil against the other fan (the turbine), which transfers power to the wheels. Between them sits a third element—the stator—which redirects the oil flow to multiply torque, acting like a funnel that concentrates the fluid's energy. At low speeds, the fluid coupling allows the engine to keep spinning while the wheels stay still—this is why you can sit at a red light in "drive" without the engine stalling. At higher speeds, a lock-up clutch mechanically connects the two halves so they spin together with zero power loss.

The elegance of this design is that it provides a smooth, continuous connection between engine and wheels with no physical friction surfaces that wear out during normal operation. A manual transmission's clutch is a friction surface that gradually wears down with each engagement—and in a refuse truck that shifts 300 times per route, clutch wear becomes a serious maintenance issue. The torque converter, using fluid rather than friction, sidesteps this problem entirely.

What made Allison's implementation special—what the company calls "Continuous Power Technology"—was that the torque converter maintained uninterrupted power delivery during every shift. Unlike a manual or automated manual transmission, which must briefly disconnect the engine from the wheels during each gear change (creating a momentary loss of momentum), Allison's automatic never broke the power flow. In a passenger car, that momentary power interruption is barely noticeable. In a 40-ton refuse truck climbing a hill, it means rolling backward. In a transit bus carrying sixty passengers in stop-and-go traffic, it means jerky, uncomfortable rides. Allison's continuous power delivery translated directly into measurable productivity gains—up to 20% higher in vocational applications, according to company data—because the vehicle never lost momentum.

Throughout the second half of the twentieth century, Allison methodically built its installed base across virtually every commercial vehicle segment that required frequent stopping and starting. School buses adopted Allison automatics because manual-transmission bus drivers were increasingly hard to find and train. Municipal transit systems standardized on Allison because the transmissions lasted longer and required less maintenance than alternatives. Fire departments, refuse haulers, construction companies—one by one, the segments fell into Allison's orbit.

Why did no one else successfully compete? Several factors conspired to create what would become one of the most durable moats in American industry.

First, the development cost: Allison has publicly cited $300 to $400 million as the investment required to develop a competitive fully automatic commercial transmission from scratch. That is an enormous bet for an uncertain return in what appears from the outside to be a niche market.

Second, the timeline: from concept to volume production, a new commercial transmission design takes five to eight years, encompassing engineering development, validation testing, OEM qualification with each truck manufacturer, and fleet acceptance trials. That is five to eight years of spending hundreds of millions of dollars before a single unit generates a dollar of revenue.

Third, the certification and qualification burden: each truck manufacturer—Freightliner, Peterbilt, Kenworth, Volvo, Navistar—has its own validation requirements, and a new transmission must be tested, calibrated, and qualified for each specific vehicle platform and engine combination. A transmission that works in a Freightliner does not automatically work in a Kenworth; each integration must be individually validated.

Finally, even after all that investment and effort, a new entrant would face Allison's installed base: thousands of fleets with technicians trained on Allison products, parts inventories stocked with Allison components, and institutional knowledge accumulated over decades. Switching means retraining mechanics, restocking parts rooms, and replacing diagnostic tools and software. The total barrier—combining development cost, time, OEM qualification, and switching costs—is so formidable that rational economic actors consistently conclude the investment is not worth the risk.

There is a useful analogy here. Imagine you are a world-class chef, but you work in the kitchen of a massive hotel chain that is primarily known for its conference rooms. You are excellent at what you do, you generate consistent profits for the hotel, but nobody in the executive suite is thinking about your kitchen when they plan the company's future. That was Allison inside GM for half a century.

Inside GM, this quietly dominant business received relatively little attention. GM was focused on its consumer automobile operations—the bread and butter that drove headlines and stock price. Allison was profitable, but it was small relative to GM's overall revenue, and it served a market that Wall Street and the general public found invisible.

The consequences of this obscurity were tangible. Capital allocation decisions were made at the GM corporate level, where Allison competed for investment dollars against Chevrolet, Cadillac, Buick, and GMC—brands that drove far more revenue and public attention. Allison's engineering team might identify a promising next-generation product opportunity but find the funding delayed or redirected to a higher-profile automobile program. The management talent pipeline was oriented toward GM's auto business; running the Allison division was not the path to the CEO suite at GM. The result was a business that was well-maintained but not fully optimized—a hidden gem that sparkled quietly inside a conglomerate that was too distracted by its own existential challenges to polish it.

This paradox—being enormously valuable within a narrow domain while being completely overlooked by the broader world—would persist until private equity came knocking.

IV. The First Inflection Point: The Carlyle/Onex LBO (2007)

By the mid-2000s, General Motors was a company in crisis—though the full extent of that crisis would not become apparent until 2008. GM's core automobile business was hemorrhaging market share to Japanese competitors, its pension and healthcare obligations were crushing its balance sheet, and its stock price had been in secular decline for years. Rick Wagoner, GM's CEO, was selling off non-core assets to raise cash and focus the company's dwindling resources on its passenger vehicle operations.

Allison Transmission was, by any objective measure, one of GM's healthiest business units. It dominated its market, generated strong cash flows, and possessed technology that competitors could not easily replicate. But it was also completely unrelated to GM's core mission of selling cars and light trucks to consumers. From a strategic standpoint, selling Allison made sense—the proceeds could be redirected to GM's automotive turnaround, and the business would probably thrive with an owner more focused on its specific needs.

Enter The Carlyle Group and Onex Corporation. In August 2007, the two private equity firms completed their acquisition of Allison Transmission for approximately $5.6 billion in a classic leveraged buyout structure. The deal was one of the largest industrial LBOs of its era, and the sponsor consortium included management participation—a detail that would prove important for alignment during the turbulent years ahead.

The PE thesis was straightforward: Allison was a hidden champion with dominant market share, sticky customer relationships, and a predictable cash flow profile that could comfortably service significant debt. Under GM's sprawling bureaucracy, the business had been underinvested and under-managed—not badly run, exactly, but managed as one small division among dozens, without the focused attention that a standalone company of its quality deserved. The private equity sponsors saw what GM's management, distracted by the slow-motion crisis in their automobile business, had overlooked: that Allison's market position was one of the most defensible in all of American industry, and that with focused management and proper capital allocation, the business could generate substantially higher returns.

The timing, of course, was spectacularly challenging. The deal closed in August 2007—literally weeks before the credit markets began seizing up. Within eighteen months, the United States would be deep in the worst financial crisis since the Great Depression. Bear Stearns collapsed, Lehman Brothers vanished, and GM itself—the company that had just sold Allison—filed for bankruptcy in June 2009. Commercial vehicle orders collapsed as construction froze, freight volumes plummeted, and municipal budgets were slashed.

For a company that had just been loaded with billions of dollars in leveraged buyout debt, this was an existential stress test. If there was ever a moment when the Carlyle/Onex investment thesis was going to break, this was it.

What happened next tells you something important about the nature of Allison's business. New truck sales cratered—Class 8 truck orders in North America fell by roughly 50% from peak to trough. But Allison's revenue declined less severely than new vehicle production for a critical reason: the aftermarket. Even when fleets stopped buying new trucks, existing trucks still needed maintenance. Transmissions still required fluid changes, filter replacements, and eventual overhauls. The installed base—hundreds of thousands of vehicles running Allison transmissions with 15- to 30-year lifecycles—continued generating service revenue regardless of the economic cycle. This counter-cyclical buffer in the aftermarket business was precisely the kind of hidden value that the PE sponsors had identified.

Under Carlyle and Onex's ownership, the operational transformation was meaningful but not dramatic—the business was already good, it just needed focus. Management incentives were realigned to reward cash generation and margin expansion rather than the bureaucratic metrics of a GM division. The company gained the freedom to make capital allocation decisions on its own, investing in next-generation products without competing for resources against GM's automobile programs. Research and development spending was directed more efficiently toward products the market actually needed. Overhead was trimmed, and the organizational structure was simplified.

The recession also exposed an important myth-versus-reality about private equity's impact on Allison. The popular narrative around leveraged buyouts is that PE firms strip assets, cut investment, and load companies with unsustainable debt. At Allison, the reality was more nuanced. Yes, the debt load was significant—roughly $4.5 billion at the time of the deal. But Carlyle and Onex did not slash R&D spending. They did not close manufacturing facilities or offshore production. What they did was eliminate the bureaucratic overhead of being a GM division, align management compensation with cash generation, and create an organizational focus that had never existed when Allison was one small unit inside a sprawling automotive conglomerate. The PE owners essentially gave Allison permission to be the company it already was—just without the corporate parent taking a cut and distracting management with unrelated priorities.

By the time the economy recovered, Allison emerged leaner and more focused. The debt load was substantial but manageable, the margins had expanded, and the business had proven it could survive the worst economic downturn in living memory. The private equity sponsors had their proof of concept: Allison was not just a good business—it was a great one, and it was ready for the next chapter.

V. The Second Inflection Point: The 2012 IPO & Becoming Public

On March 12, 2012, Allison Transmission Holdings debuted on the New York Stock Exchange under the ticker ALSN, pricing its initial public offering at $23 per share. The offering raised approximately $690 million, with Carlyle and Onex selling a portion of their stakes while retaining significant ownership. The IPO valued the company at roughly $5 billion—a respectable outcome for the PE sponsors but one that reflected the market's lukewarm reception.

Wall Street's initial reaction was predictable: Allison was seen as "just another boring industrials company"—a leveraged post-LBO play with a significant debt overhang, operating in a niche market that most generalist investors did not understand. The company carried approximately $3.4 billion in net debt at the time of its IPO, a legacy of the leveraged buyout, and skeptics questioned whether cash flows could support both debt service and the investment needed to sustain the business. The stock traded sideways for much of its first year as a public company.

But management, led by CEO Lawrence Dewey, had a playbook that would prove devastatingly effective over the following decade: underpromise, overdeliver, and return cash to shareholders. The strategy was not flashy. It did not involve bold acquisitions, dramatic pivots, or visionary pronouncements about the future. Instead, it was a relentless execution machine built on three pillars.

First, debt reduction. Management treated the LBO-era debt as an urgent priority, directing substantial free cash flow toward paying it down. The debt-to-EBITDA ratio steadily declined year after year, reducing financial risk and increasing strategic flexibility. Second, operational discipline. Allison consistently hit or exceeded its margin targets, benefiting from the pricing power that comes with market dominance and from the operating leverage inherent in its capital-light manufacturing model. Third, shareholder returns. Once the debt was brought to manageable levels, Allison initiated a dividend—and steadily increased it—while simultaneously repurchasing shares. The company became a favorite of income-oriented investors who appreciated the combination of a growing dividend, consistent buybacks, and a business model with obvious durability.

What public markets forced upon Allison was actually beneficial: quarterly earnings calls, transparent financial reporting, and the need to articulate a clear strategic narrative. For a business that had spent decades buried inside GM and then five years in private equity's embrace, this level of public scrutiny turned out to be clarifying. Management had to explain, in plain language, why the company's market position was durable, how the aftermarket business provided recurring revenue, and what the long-term growth drivers looked like. The act of explaining the story forced the team to sharpen the story—and investors who took the time to understand it were richly rewarded.

The financial trajectory tells the story in stark terms. In its first full year as a public company, Allison generated approximately $2.2 billion in revenue. Gross margins hovered around 47%—extraordinary for an industrial manufacturer and indicative of the pricing power that market dominance confers. Free cash flow conversion was strong, allowing the company to simultaneously service its debt, invest in product development, and begin returning capital to shareholders. The debt-to-EBITDA ratio, which had stood above 4x at the time of the IPO, steadily declined as management directed cash flow toward deleveraging.

By 2017—five years after the IPO—Allison's stock had more than tripled from its offering price. The debt had been dramatically reduced, margins had expanded, the dividend had grown substantially, and the company had repurchased a meaningful percentage of its outstanding shares. Carlyle and Onex fully exited their positions, having generated strong returns on a deal that closed just months before the worst financial crisis in generations. The boring industrials company had quietly become one of the best-performing mid-cap stocks on the New York Stock Exchange—a fact that attracted a new kind of attention, not all of it welcome.

The Allison IPO story carries a broader lesson about market psychology. Wall Street tends to assign premium valuations to companies with exciting narratives—technology disruptors, platform businesses, companies with "network effects" and "flywheel dynamics." Companies that make transmissions for garbage trucks do not get that premium, regardless of how dominant their market position or how durable their competitive advantages. This persistent valuation discount is both a risk (the market may never fully appreciate the business) and an opportunity (patient investors can buy an extraordinary franchise at an ordinary price). For the five years following the IPO, those who recognized the gap between Allison's business quality and its market valuation were generously rewarded.

VI. The Third Inflection Point: The Electrification Threat & Response (2017–Present)

If the private equity era was about unlocking Allison's existing value, and the IPO was about proving it to public markets, then what came next was about something far more fundamental: whether the company had a future at all.

Around 2017, a tremor ran through the commercial vehicle industry—and through Allison's stock price. The accelerating momentum of electric vehicles, driven by Tesla's success in passenger cars and increasingly ambitious climate commitments from governments worldwide, raised what appeared to be an existential question for transmission manufacturers: if electric motors can drive wheels directly, are transmissions even needed?

The logic seemed airtight. An electric motor produces maximum torque from zero RPM—no gears needed to multiply torque at low speeds, no transmission required to match engine speed to wheel speed across a range of driving conditions. For passenger EVs, this was largely true: a simple single-speed reduction gear between motor and wheels worked just fine. Investors extrapolated this logic to commercial vehicles and concluded that Allison's core product was on a path to obsolescence. The stock gave back some of its gains as analysts published notes questioning the company's long-term relevance.

The market, however, was making a mistake born of oversimplification. Heavy-duty commercial vehicles are not large cars. A Class 8 truck or a transit bus must deliver enormous torque for climbing grades at low speed with heavy payloads, and it must also cruise efficiently at highway speeds. A single-speed system forces a painful compromise: either the motor and gear ratio are optimized for pulling away from a stop on a steep hill (great at low speed, inefficient at cruise), or they are optimized for highway efficiency (good at cruise, inadequate for hill starts). The physics of commercial vehicles—extreme weight variation, severe duty cycles, demanding grade performance—means that a multi-speed drivetrain actually extends the range of a battery-electric truck by 5 to 15% compared to a single-speed setup. When batteries cost tens of thousands of dollars per kilowatt-hour of capacity, that range extension has enormous economic value.

Allison's engineers understood this long before Wall Street did. In 2018, the company unveiled the eGen Power product line: a family of fully integrated electric axles designed specifically for medium- and heavy-duty commercial vehicles. These units package the electric motor, power electronics (the inverter that converts battery DC to motor AC), a two-speed gearbox, and the differential into a single compact unit that bolts between the rear wheels. The architecture was elegant: by integrating a two-speed transmission into the electric axle, Allison could optimize the motor's operating point across both low-speed torque and high-speed cruise, extending range while reducing the size and cost of the electric motor needed.

The eGen Power lineup expanded to cover multiple configurations: single-motor and dual-motor variants, axle ratings from 8.5 to 13 tonnes, and compatibility with both North American and European/Asian vehicle platforms. Critically, the system was designed to be "power agnostic"—it works with battery-electric, hydrogen fuel cell, and hybrid powertrains. This flexibility meant Allison was not betting on a single winner in the zero-emission powertrain race.

Customer adoption began building, and the early wins came from precisely the segments where Allison was already strongest. Transit authorities—historically Allison's most loyal customer segment—were among the first to commit to battery-electric buses, and many specified eGen Power axles for their zero-emission fleets. The logic for transit operators was compelling: they already knew and trusted Allison, their maintenance teams were already familiar with Allison products, and the eGen Power e-axle offered superior range and gradeability compared to single-speed alternatives.

New Flyer, North America's largest transit bus manufacturer, integrated Allison's electric drivetrain into its battery-electric models. This partnership was strategically significant because New Flyer's dominant position in the transit bus market meant that Allison could reach the majority of North American transit authorities through a single OEM relationship—replicating in the electric world the same OEM channel strategy that had built its ICE business.

Allison also opened a $400 million Vehicle Innovation Center in Indianapolis in March 2022, housing 300 engineers and designers focused on electrified powertrain development, along with a 60,000-square-foot testing center capable of validating every propulsion type from diesel to hydrogen fuel cell. The Innovation Center was not merely a facility investment—it was a statement of strategic intent. By concentrating its electric drivetrain engineering in a purpose-built center adjacent to its traditional manufacturing operations, Allison signaled that electrification was not a skunkworks project but a core business priority.

The hydrogen opportunity added another dimension to the strategy. For long-haul heavy trucks, where battery weight and charging time create significant practical challenges, hydrogen represents a potential alternative path to zero emissions. Allison positioned itself on both sides of that bet: hydrogen internal combustion engines (which burn hydrogen in a modified diesel engine and still require a traditional multi-speed transmission) would keep Allison's conventional product line relevant, while hydrogen fuel cell vehicles (which are electrically driven) would use eGen Power axles. The company demonstrated both applications, equipping the UK's first hydrogen fuel cell refuse collection vehicle and showcasing hydrogen ICE trucks at industry events.

There is a subtlety to the eGen Power strategy that deserves emphasis. Allison did not simply bolt an electric motor onto a traditional axle and call it innovation. The engineering team rethought the entire drivetrain architecture for electric propulsion in commercial vehicles. The parallel-axis gear scheme—where the motors sit parallel to the axle shaft rather than perpendicular—maximizes power transfer efficiency. The integrated thermal management system, with oil cooler and oil pump built directly into the unit, eliminates the external plumbing that plagues competitor designs and reduces installation time for OEMs. The regenerative braking system captures 100% of available regeneration torque, feeding energy back to the battery during every stop—a feature that is particularly valuable in refuse trucks and transit buses that stop hundreds of times per shift. And the entire unit was designed for zero maintenance over the life of the vehicle, eliminating what had been a significant total-cost-of-ownership advantage for simpler direct-drive systems.

What initially looked like an existential threat had been reframed as a growth opportunity. Allison was no longer just a transmission company—it was a commercial vehicle drivetrain company, positioned to serve customers regardless of which powertrain technology prevailed. The stock recovered, and a new investment narrative emerged: Allison as a "picks and shovels" play on the commercial EV transition, leveraging a century of heavy-duty vehicle expertise to solve problems that Silicon Valley EV startups did not even know existed.

VII. The Fourth Inflection Point: COVID, Supply Chains & Defense Resurgence (2020–2024)

In early March 2020, the world changed in a matter of days. Factories shut down. Supply chains seized. And commercial vehicle manufacturers—whose customers make purchasing decisions based on economic confidence—found themselves staring into an abyss.

Fleet operators froze purchasing decisions overnight. Construction sites went dark. Transit ridership collapsed to near zero in major cities as commuters sheltered at home. School buses sat idle in parking lots by the thousands. For Allison, the pandemic represented the second severe cyclical downturn in just over a decade—another stress test of the business model's resilience.

The pattern from 2008-2009 repeated, but faster. New vehicle orders fell sharply, but the aftermarket held up better, cushioning the revenue decline. What distinguished Allison's pandemic response from many industrial peers was supply chain management. While competitors struggled with semiconductor shortages and logistics disruptions that persisted well into 2022 and 2023, Allison's relatively concentrated manufacturing footprint—centered on its massive Indianapolis campus—and its long-standing relationships with suppliers provided an advantage. The company was not immune to supply chain disruptions, but it navigated them more effectively than many competitors, maintaining delivery schedules and capturing share from rivals who could not.

The truly unexpected tailwind, however, came from defense. Russia's invasion of Ukraine in February 2022 sent shockwaves through Western defense establishments, triggering the most significant increase in military spending since the end of the Cold War. For Allison, which had been supplying transmissions for military tracked vehicles since World War II, this was a transformative moment.

Allison's defense products are deeply embedded in the U.S. military's most important ground combat platforms. The X1100 series transmission powers the M1 Abrams main battle tank. The HMPT500 series drives the Bradley Fighting Vehicle. These are not commodity components—they are mission-critical systems that take years to qualify and cannot be sourced from alternative suppliers. When the U.S. and allied nations accelerated military modernization programs and increased orders for tracked combat vehicles, Allison's defense revenue surged. Defense segment revenue reached $267 million in 2025, representing a 26% year-over-year increase—and the growth came at margins that exceeded Allison's already-healthy corporate average.

The defense business also possessed a structural characteristic that investors found increasingly attractive: visibility. Military contracts are long-cycle, often spanning multiple years with firm order quantities. Unlike the commercial truck market, which can swing violently with the economic cycle, defense revenue provided a stable, predictable revenue base that improved the quality of Allison's overall earnings stream. There is an elegant symmetry here: the business that launched Allison into the transmission market during World War II was now, eight decades later, providing a strategic anchor during a period of commercial market volatility.

The defense opportunity extends beyond the United States. NATO member nations, many of which had allowed their military capabilities to atrophy during the post-Cold War peace dividend, began urgent rearmament programs. Countries that operate American-designed vehicles—or vehicles requiring similar drivetrain specifications—represent a growing international defense market for Allison. The combination of U.S. military modernization and allied rearmament created a multi-year demand runway with unusual visibility for a company more accustomed to the boom-and-bust cycles of commercial trucking.

Meanwhile, two domestic policy developments provided additional tailwinds. The Infrastructure Investment and Jobs Act, signed in November 2021, directed hundreds of billions of dollars toward road construction, bridge repair, and transit system modernization—all activities that drive demand for the vocational vehicles that are Allison's bread and butter. And the broader reshoring trend, as American manufacturers brought supply chains back from overseas, benefited a company whose primary manufacturing base had never left Indianapolis.

Management's capital allocation during this period demonstrated the discipline that had characterized the post-IPO era. Rather than chasing acquisitions or dramatically increasing spending during the boom, the team continued its balanced approach: maintain the dividend, repurchase shares opportunistically, invest in eGen Power development, and keep the balance sheet healthy.

The 2020-2024 period also saw meaningful progress on international expansion. The Chennai, India facility—initially a modest manufacturing operation—became the focus of a major expansion initiative as Allison sought to position itself closer to one of the world's fastest-growing commercial vehicle markets. India's combination of rapid urbanization, infrastructure investment, and an increasingly affluent middle class demanding better public transit created a demand profile that mapped perfectly to Allison's vocational transmission strengths. The investment signaled that Allison's future was not exclusively American, even if its heritage and primary manufacturing base remained firmly rooted in Indianapolis.

This discipline and international ambition would prove prescient as the company prepared for its most ambitious acquisition in years.

VIII. The Business Model Deep Dive

To truly understand Allison Transmission, you have to look past the headline product—the transmission itself—and see the business as what it really is: a recurring revenue machine disguised as an industrial manufacturer.

Start with the product portfolio. Allison organizes its business into several segments: On-Highway (the core commercial vehicle transmission business, serving everything from medium-duty delivery trucks to Class 8 highway tractors), Off-Highway (construction equipment, mining trucks, energy sector vehicles), Defense (military tracked and wheeled vehicles), and the emerging electric propulsion business. Within On-Highway alone, the product range spans the 1000/2000 Series for medium-duty applications, the 3000 Series for medium-heavy, the 4000 Series for heavy-duty, and the TC10 for highway applications. Each series is purpose-built for its specific duty cycle, and each requires distinct engineering, calibration, and manufacturing.

But the real economic engine is the aftermarket. When Allison sells a transmission, it is not a one-time transaction—it is the beginning of a multi-decade revenue relationship. Commercial vehicle transmissions operate for 15 to 30 or more years, and during that lifecycle, they require periodic fluid and filter changes, component replacement, and eventually a full rebuild or remanufacture. Every unit sold creates what amounts to an annuity stream of parts and service revenue that persists long after the original sale.

The Service Parts, Support Equipment and Other segment generated record revenue of $696 million in fiscal 2024—a staggering figure for what many investors think of as a simple replacement parts business. This revenue includes Allison-branded service parts, proprietary transmission fluids, extended coverage programs, and the Allison Genuine Reman program, which remanufactures transmissions to original factory specifications with full warranties. The aftermarket business is supported by a global network of approximately 1,600 authorized distributors and dealers, with over 3,600 certified technicians holding more than 17,000 individual accreditations.

The beauty of this model is its counter-cyclicality. When new truck sales boom, Allison benefits from strong original equipment revenue. When new truck sales decline, the existing installed base—which grows larger every year—continues generating aftermarket revenue. This dynamic creates a floor under Allison's earnings that pure-play equipment manufacturers lack.

Customer switching costs reinforce this model at every level. Consider a large municipal transit authority that has standardized its fleet on Allison transmissions. Its maintenance technicians are trained and certified on Allison products through extensive coursework. Its parts rooms are stocked with Allison components. Its diagnostic computers run Allison-specific software. Its procurement specifications literally require "Allison Automatic" transmissions—and all 250-plus vehicle manufacturers that work with Allison know how to integrate them. Switching to a competitor means retraining the entire maintenance organization, writing off existing parts inventory, replacing diagnostic tools, rewriting procurement specifications, and qualifying a new product through years of fleet trials. The total cost of switching is so high that it almost never happens.

Allison's manufacturing footprint reflects both its strength and its concentration risk. The vast majority of production occurs at the 4.6-million-square-foot Indianapolis campus, which houses corporate headquarters, the primary manufacturing plants, engineering centers, the Innovation Center, and the parts distribution center. Additional manufacturing facilities operate in Szentgotthard, Hungary (serving European and international markets) and Chennai, India (currently undergoing a major expansion announced in October 2024 that will double the existing footprint). The Indianapolis concentration has efficiency benefits—everything under one roof reduces logistics complexity and enables tight quality control—but it also means a single catastrophic event at that facility would be devastating.

On pricing, Allison occupies an unusual position for an industrial manufacturer: it has genuine pricing power. When a fleet operator evaluates the total cost of ownership—including productivity gains from continuous power technology, lower maintenance costs from superior durability, reduced driver training requirements, and the availability of a global service network—Allison's premium price is justified. The company has consistently been able to pass through cost increases and maintain or expand its margins, a capability that is far rarer in industrial manufacturing than most people assume.

To illustrate the business model's power: consider a single Allison 3000 Series transmission installed in a transit bus in 2000. Over the following 25 years, that single unit generated revenue from the initial OEM sale, then from multiple fluid and filter service intervals, then from component replacements as wear items aged, then potentially from a full remanufacture through the Allison Genuine Reman program, and finally from the parts and service needed to keep the remanufactured unit running for another decade. One transmission, one customer, generating revenue for a quarter century. Now multiply that by millions of units in the installed base worldwide, and you begin to see why Allison's aftermarket business is not just a nice supplement to new equipment sales—it is the economic backbone of the entire enterprise.

IX. The Competitive Landscape & Why Allison Dominates

The competitive landscape in commercial vehicle transmissions is one of the most unusual in all of industrial manufacturing. On paper, Allison has competitors—ZF Friedrichshafen, Eaton, Voith, and the truck OEMs' own proprietary systems. In practice, the competition is far more nuanced, and Allison's dominance in its core market is nearly absolute.

To understand the competitive dynamics, start with the segmentation. The commercial transmission market divides roughly into three categories.

First, fully automatic transmissions—torque converter-based systems that shift gears without any driver input and without interrupting power delivery. This is Allison's domain.

Second, automated manual transmissions, or AMTs—which are essentially traditional manual gearboxes with computer-controlled shifting mechanisms bolted on. An AMT uses the same gear-and-clutch architecture as a manual, but a computer and actuators handle the shifting instead of the driver. The result is easier driving, but with a brief power interruption during each shift as the clutch disengages and re-engages.

Third, traditional manual transmissions—increasingly rare in developed markets but still common in parts of Asia and Africa where cost is the primary purchasing criterion.

Allison dominates the first category. ZF and Eaton compete primarily in the second. The distinction matters enormously, because the two products serve fundamentally different use cases and customer needs.

In long-haul trucking—Class 8 tractors cruising the interstate at steady speeds with infrequent stops—AMTs from Eaton, ZF, and the OEMs' proprietary systems (Volvo's I-Shift, Mack's mDRIVE, Detroit's DT12) have captured significant market share because fuel efficiency at highway cruise dominates the purchasing decision, and AMTs are lighter and slightly more efficient at constant speed than torque converter automatics. This is the one segment where Allison has historically been less dominant, and the company addressed it with the TC10 transmission specifically designed for highway applications.

But in vocational applications—the bread and butter of refuse collection, transit, construction, fire and emergency, school buses, and delivery—Allison is unassailable. These are stop-start duty cycles where the torque converter's continuous power delivery, smooth shifting, and ability to handle hundreds of shifts per day without wear provide decisive advantages over AMTs. An AMT, which must briefly disengage the engine from the drivetrain during each shift, simply cannot match an Allison automatic in a refuse truck that shifts 300 times on its morning route. The momentary power interruption of an AMT means lost momentum on hills, jerky passenger rides on buses, and accelerated wear on clutch components.

Why has no one successfully entered Allison's core fully automatic commercial market? The barrier is not any single factor but the compounding effect of several factors simultaneously. The $300 to $400 million development cost. The five-to-eight-year timeline from concept to volume production. The need to qualify with each OEM individually. The requirement to build a global service network capable of supporting the product over its 15-to-30-year lifecycle. And the reality that any new entrant would be competing against Allison's 75-plus years of iterative refinement on the torque converter technology—decades of accumulated data on failure modes, duty cycle optimization, and application engineering that cannot be replicated simply by spending money.

Allison's OEM relationships span virtually every major truck manufacturer in North America and many globally. Daimler Truck's Freightliner, PACCAR's Peterbilt and Kenworth, Navistar's International, Blue Bird school buses, REV Group emergency vehicles, and Oshkosh defense platforms all offer or require Allison transmissions. Over 250 vehicle manufacturers worldwide specify Allison products. These relationships have been built over decades and are deeply embedded in each OEM's product development, manufacturing, and service processes.

Globally, the picture is more complex—and more contested.

In China, Allison faces formidable local competition from Shaanxi Fast Auto Drive Group (Fast Gear), a Weichai Power subsidiary that claims 85% market share in Chinese heavy truck transmissions with annual production capacity of 1.2 million units. Those numbers are staggering—Fast Gear has ranked first in China's gear industry for 20 consecutive years. However, the competitive overlap with Allison is more limited than the headline numbers suggest. Fast Gear primarily produces manual and AMT products, not true torque converter automatics. The two companies are competing in different technological categories within the same broad market.

Allison's China strategy has accordingly focused on segments where fully automatic transmissions provide clear value that manual and AMT products cannot match—transit buses operating in dense urban traffic, municipal refuse vehicles with extreme stop-start duty cycles, and mining trucks where the torque converter's ability to handle heavy loads on steep grades is essential. Strategic partnerships with CNHTC (Sinotruk's parent) and SANY, along with a $42 million equity investment in electric motor manufacturer Jing-Jin Electric during its 2021 Shanghai STAR Board IPO, position Allison in the Chinese market without trying to compete head-on in segments where local cost advantages are overwhelming.

In Europe, different market dynamics present both challenges and opportunities. European trucks have traditionally used manual and AMT transmissions, with fully automatic penetration historically lower than in North America. The OEM landscape is also more vertically integrated—Volvo, Daimler, and Scania all produce their own proprietary transmission solutions. But as European cities adopt aggressive zero-emission mandates for urban delivery and transit vehicles, the shift to electric drivetrains—where Allison's eGen Power axles compete on equal footing regardless of the region's ICE transmission preferences—could reshape the competitive landscape entirely. The eGen Power 130-series product line, with its 13-tonne axle rating designed specifically for European and Asian vehicle platforms, represents Allison's bid to establish a foothold in markets where it has historically been a minor player.

The EV transition introduces genuine new competitive dynamics. Electric axle and drivetrain competitors include BorgWarner, Dana (prior to Allison's acquisition of Dana's off-highway business), Meritor (now part of Cummins), and various Chinese manufacturers. This is a more crowded and less defined competitive field than Allison's traditional market.

However, Allison possesses several advantages that are easy to underestimate. First, its deep understanding of commercial vehicle duty cycles—knowledge accumulated over decades of application engineering across thousands of fleet configurations—enables Allison to optimize its eGen Power products for real-world conditions that competitors with less commercial vehicle experience may overlook. Second, its existing OEM relationships provide distribution channels and co-development partnerships that new entrants must build from scratch. Third, the ability to test and validate products in its own dedicated Vehicle Electrification and Environmental Test Center provides a development speed advantage. And fourth, the brand trust that Allison has earned over generations with fleet operators—the people who actually specify and purchase drivetrains—creates a credibility advantage that no amount of marketing spend can replicate overnight.

Where Allison is most vulnerable is in markets where it has never had a strong presence. In China, where domestic EV drivetrain manufacturers operate with significant cost advantages and government support, Allison's brand carries less weight than it does in North America. In passenger and light commercial vehicles, where simpler single-speed drivetrains suffice, Allison has no competitive position and no reason to build one. And in the long-haul highway segment, where AMTs already dominate and where the eventual shift to electric may favor different architectures, Allison faces the same competitive pressures it has always faced—just with different technology.

X. Strategy & Playbook: What Makes Allison Different

There is a telling detail about Allison's headquarters in Indianapolis. The campus does not look like a typical corporate office park—it looks like a factory, because it is one. The executive offices sit adjacent to the manufacturing floor, and engineers outnumber MBAs by a wide margin. Walk the halls and the culture becomes immediately apparent: this is an engineering company that happens to be publicly traded, not a financial company that happens to make transmissions. That distinction matters more than it might seem.

Allison's strategic playbook rests on a principle that sounds simple but is brutally difficult to execute in practice: focus. For over a century, the company has resisted the temptation to diversify into adjacent markets. It does not make engines. It does not make axles—or rather, it did not, until the recent strategic expansion into electric axles where the drivetrain integration opportunity was too compelling to ignore. It does not make brakes, suspensions, or any of the other components that constitute a commercial vehicle's powertrain. It makes transmissions and, increasingly, integrated electric drivetrains. That is it.

This discipline of focus shows up most clearly in R&D spending, which Allison has maintained through cyclical downturns when most industrial companies cut research budgets to protect short-term margins. The logic is counterintuitive but correct: in a business where product development cycles span five to eight years, cutting R&D during a downturn means having no new products when the upturn arrives. Allison has consistently invested through the cycle, ensuring that its technology lead is maintained and that new products are ready when markets recover.

The customer intimacy strategy is another differentiator that does not show up on a balance sheet. Allison does not merely sell to OEMs—it maintains direct relationships with fleet operators, the end users who actually specify and operate its transmissions. Understanding how a refuse fleet in Phoenix operates differently from one in Minneapolis, or how a transit authority's duty cycle in mountainous Denver differs from flat Miami, enables Allison to optimize its products for real-world conditions rather than theoretical specifications. This application engineering expertise—accumulated over decades of working with thousands of fleets across every conceivable duty cycle—is a form of institutional knowledge that new entrants simply do not possess.

David Graziosi, who became CEO in 2018 after serving as CFO, embodies the company's engineering-meets-financial-discipline culture. A career Allison executive, Graziosi spent more than a decade in the CFO role before taking the top job, giving him an unusually deep understanding of the business's financial mechanics—the cash conversion cycle, the aftermarket economics, the capital intensity of product development. His background is important because it shaped his approach to the electrification transition.

Unlike tech-world leaders who might declare a wholesale pivot to electric and "burn the boats" on the legacy business, Graziosi took a pragmatic approach: acknowledge the reality of the technology shift, invest aggressively in electric drivetrain capability, but do not abandon the internal combustion engine business that generates the cash to fund that investment. It is a dual-track strategy that requires managing two very different technology platforms simultaneously—challenging operationally but essential strategically. The alternative—pouring resources into EV while starving the ICE business—would risk destroying the profitable core before the new business could replace it. Graziosi's financial background made him instinctively allergic to that kind of value destruction.

The capital allocation framework under Graziosi has followed a clear hierarchy: first, maintain the balance sheet with manageable debt levels; second, invest in organic growth, particularly eGen Power development and manufacturing expansion; third, pay and grow the dividend; fourth, repurchase shares opportunistically. This framework has been communicated clearly and executed consistently, building credibility with investors who appreciate predictability.

Then came the Dana Off-Highway acquisition. On January 2, 2026, Allison completed its acquisition of Dana Incorporated's Off-Highway Drive and Motion Systems business for approximately $2.7 billion—roughly 7.5 times expected 2025 adjusted EBITDA. This was the largest acquisition in Allison's history as a public company, adding operations in over 25 countries with approximately 11,000 employees serving the construction, forestry, agriculture, mining, and industrial segments. The combined company issued 2026 revenue guidance of $5.575 to $5.925 billion, roughly doubling its pre-acquisition revenue base.

The Dana deal represented a carefully considered departure from Allison's traditional organic-growth-only strategy—but one consistent with its underlying logic. Off-highway markets share the same fundamental characteristics that make Allison's on-highway business attractive: extreme duty cycles, specialized engineering requirements, long product lifecycles, and substantial aftermarket revenue. The acquisition expanded Allison's addressable market without diluting its core competency in commercial vehicle drivetrain technology.

There is a lesson here for any industrial company facing technological disruption: incumbents win when they recognize that their core competency is not the specific product they make but the problem they solve. Allison's core competency is not "making transmissions"—it is "transferring power from propulsion source to wheels in heavy-duty commercial vehicles with maximum efficiency and reliability." Framed that way, the shift from internal combustion to electric propulsion does not obsolete the competency; it merely changes one variable in the equation.

The deeper lesson from Allison's playbook is that "boring and reliable" is not a default strategy adopted by companies that lack vision—it is a deliberate competitive choice that, in the right market, produces extraordinary results. In a segment where customers value uptime, durability, and total cost of ownership above all else, being the company whose products simply work, year after year, decade after decade, is the ultimate competitive advantage.

Compare this to the approach taken by Kodak, the canonical example of an incumbent destroyed by technological disruption. Kodak defined its competency as "film photography" rather than "capturing images," and when digital imaging emerged, the company could not bridge the gap. Allison has explicitly avoided this trap by defining itself as a drivetrain technology company, not a transmission company—a distinction that sounds semantic but is strategically profound.

XI. Porter's Five Forces & Hamilton's Seven Powers Analysis

Having examined the business model, competitive landscape, and strategic playbook, it is time to pressure-test Allison's competitive position with analytical rigor. The two most widely used frameworks for evaluating business quality and durability offer complementary perspectives on Allison's moat.

Starting with Michael Porter's Five Forces. Competitive rivalry in Allison's core fully automatic commercial transmission market is remarkably low. With approximately 77% market share in North American medium-duty fully automatic transmissions and around 60% globally in the on-highway commercial automatic segment, Allison operates in what is effectively a quasi-monopoly. The limited competition that exists comes from different product categories (AMTs competing in highway applications) rather than direct substitutes for Allison's torque converter automatics in vocational duty cycles. This low competitive intensity allows Allison to maintain premium pricing and attractive margins.

The threat of new entrants is extremely low—among the lowest of any industrial market. The barriers are multi-layered: $300 to $400 million in required development investment, five-to-eight-year timelines to reach volume production, the need to individually qualify with each major OEM, the requirement to build a global service network, and the challenge of competing against Allison's decades of accumulated application data and torque converter refinement. In over 75 years since Allison commercialized fully automatic transmissions for commercial vehicles, no new entrant has successfully established a competing product in the company's core vocational market.

Supplier power is moderate. Allison uses a diversified supply base for most components, and its scale as the dominant buyer in its niche gives it reasonable leverage. Some specialized components—particularly certain alloy castings and electronic control modules—create limited supplier concentration, but nothing that fundamentally threatens the business model.

Buyer power is similarly moderate, though the dynamics are nuanced. Large OEMs like Daimler and PACCAR have purchasing leverage by virtue of their scale, and they have increasingly developed their own proprietary AMT solutions for the highway segment, which represents a form of backward integration. However, in vocational applications, these same OEMs have limited alternatives to Allison. Their customers—the fleet operators who actually specify the transmission—demand Allison by name. This creates a three-way dynamic where the OEM sits between Allison and the end customer, with both Allison and the customer exerting influence on the OEM's purchasing decision. The result is a mutual dependency rather than a one-sided power dynamic.

The threat of substitutes was, for a period around 2017-2019, perceived as potentially existential. Direct-drive electric powertrains appeared poised to eliminate the need for transmissions entirely. As discussed earlier, this threat turned out to be overblown for heavy-duty commercial applications, where multi-speed electric drivetrains provide meaningful range and performance advantages. Allison's pivot to eGen Power electric axles effectively internalized the substitute threat, positioning the company to be the provider of the "substitute" product rather than its victim.

Turning to Hamilton Helmer's Seven Powers framework, which focuses on the structural sources of persistent differential returns. Scale economies are strong. Allison's engineering costs—which are substantial, given the complexity of designing, testing, and certifying commercial transmission systems—are spread across a production volume that no competitor approaches in the fully automatic commercial segment. Consider: the fixed cost of developing a new transmission series is roughly the same whether you sell 10,000 units or 100,000 units, but the per-unit cost of that development investment is dramatically different. With 77% market share, Allison amortizes its R&D across a volume base that makes any competitor's per-unit engineering cost structurally higher.

Network effects are limited in the traditional sense—transmissions do not become more valuable as more people use them. But the service network creates a powerful analog. With 1,600 authorized distributors and dealers worldwide and over 3,600 certified technicians, the density of Allison-capable service facilities makes owning an Allison transmission more convenient than owning any alternative. A fleet operating Allison products can find qualified service virtually anywhere in North America. A fleet that standardized on a hypothetical competitor would face a sparse, patchy service network. As the installed base grows, the service network becomes denser, which makes the product more attractive, which grows the installed base further—a virtuous cycle that stops short of a true network effect but produces a similar compounding dynamic.

Counter-positioning does not apply in the traditional Helmer sense, as Allison is the incumbent rather than the disruptor. However, one could argue that Allison's eGen Power strategy contains an element of counter-positioning against pure-play EV drivetrain startups: Allison can afford to invest in electric technology using cash flows from its dominant ICE business, while EV-only startups must fund their development through external capital with no established revenue base.

Switching costs are arguably Allison's single most powerful competitive advantage. The compounding effect of technician training, parts inventory, diagnostic tool investment, procurement specification lock-in, and institutional operational knowledge creates switching costs so high that they approach the theoretical maximum for an industrial product. These are not just contractual switching costs (which can be overcome with sufficiently attractive economic incentives) but operational switching costs embedded in the daily routines of thousands of maintenance shops across the country.

Branding operates at a moderate-to-strong level. "Allison Automatic" is essentially synonymous with fully automatic commercial transmissions in the North American market. When fleet managers specify their vehicle purchases, "Allison" is both a brand name and a product category—the kind of brand power that companies spend billions trying to achieve but that Allison earned through decades of reliable performance.

Cornered resource is strong. Allison's proprietary torque converter intellectual property, refined over 75-plus years of iterative development, constitutes a cornered resource in the Helmer sense: it is a valuable, non-replicable asset that competitors cannot access. The decades of accumulated application data—millions of data points on how transmissions perform across every conceivable duty cycle, climate, terrain, and payload combination—adds another layer of cornered resource that exists nowhere else.

Process power is strong. The manufacturing know-how, quality control processes, and testing protocols developed over a century of commercial transmission production are embedded in organizational routines that cannot be easily documented or transferred. This process power shows up in Allison's defect rates, warranty costs, and product lifecycles, all of which are superior to alternatives.

The dominant powers for Allison are Switching Costs, Cornered Resource, and Process Power—a combination that creates what Warren Buffett would describe as a wide economic moat. The critical question is duration: how long will these advantages persist as the powertrain technology landscape shifts? In traditional ICE applications, the moat appears nearly impregnable. In the emerging EV drivetrain space, Allison is building competitive advantages but has not yet established the same dominance. The next decade will determine whether Allison's moat extends fully into the electric era.

It is worth comparing Allison's competitive position to analogous industrial franchises. Consider HEICO in aerospace, which dominates niche FAA-approved replacement parts through engineering expertise and regulatory barriers. Or consider IDEX Corporation, which holds leading positions in specialized industrial pumps and valves through application engineering and customer lock-in. These companies share Allison's fundamental playbook: dominate a narrow market through technical excellence, build switching costs through training and parts ecosystems, and generate recurring revenue from long-lived installed bases. What distinguishes Allison is the scale of its dominance—77% market share in its core segment is exceptional even among industrial niche leaders—and the sheer longevity of its competitive position, which stretches back to the late 1940s without meaningful challenge.

XII. Bull vs. Bear Case

Every investment case has two sides, and Allison's is no exception.

Before laying out the competing investment narratives, it is worth noting that Allison sits at a genuinely unusual intersection: it is both a value stock (dominant market position, strong cash generation, growing dividend) and a transition story (navigating the ICE-to-EV shift with its eGen Power platform). That duality makes it analytically interesting but also makes it easy for investors to misjudge—either dismissing it as a declining legacy business or overpaying for an EV narrative that has not yet been proven at scale.

The bull case begins with market position—a 77% share in North American medium-duty fully automatic transmissions represents a degree of dominance that is vanishingly rare in industrial manufacturing. This is not a market share that was purchased through aggressive pricing or unsustainable discounting; it was earned through superior technology, multi-decade customer relationships, and switching costs that approach the theoretical maximum. Maintaining this share requires continued execution, but displacing Allison from its core market would require a competitor to spend hundreds of millions of dollars over nearly a decade—with no guarantee of success.

The aftermarket business transforms the cyclical industrial profile into something closer to a recurring revenue model. With a growing installed base of vehicles carrying Allison transmissions—each requiring parts and service for 15 to 30 years—the aftermarket provides a revenue floor that persists through economic downturns. Record aftermarket revenue of $696 million in 2024 demonstrated the scale and profitability of this often-overlooked revenue stream.

The electrification pivot from existential threat to growth opportunity is perhaps the most compelling element of the bull case. By recognizing early that heavy-duty EVs need specialized multi-speed drivetrains, and by leveraging a century of commercial vehicle expertise to develop the eGen Power platform, Allison positioned itself to participate in the EV transition rather than be displaced by it. The company's ability to serve both ICE and EV customers simultaneously—funding electric investment with ICE cash flows—provides a structural advantage over pure-play EV drivetrain companies.

Defense spending adds a high-margin, long-cycle revenue stream with exceptional visibility. Military modernization programs in the U.S. and allied nations, accelerated by geopolitical developments since 2022, provide multi-year contract backlogs with margin profiles that exceed Allison's corporate average. Infrastructure spending tailwinds from the 2021 Infrastructure Investment and Jobs Act further support demand in transit, construction, and refuse segments.

The Dana Off-Highway acquisition, completed in early 2026, roughly doubled Allison's revenue base while maintaining the company's focus on specialized drivetrain technology for demanding duty cycles. The combined entity's 2026 revenue guidance of $5.575 to $5.925 billion represents a step change in scale, potentially unlocking new growth vectors in construction, mining, agriculture, and forestry. If Allison can achieve even modest synergies from the acquisition—through shared engineering resources, combined purchasing leverage, and cross-selling opportunities—the deal could prove to be a value-creating catalyst that repositions the company from a mid-cap niche player to a more broadly diversified industrial franchise.

The bull case also rests on a valuation argument. Allison has historically traded at a discount to its industrial peers on a free cash flow yield basis, reflecting the market's concern about long-term ICE decline. If the eGen Power business demonstrates commercial traction and the Dana integration proceeds smoothly, there is potential for multiple expansion as the market re-rates the business from "legacy industrial" to "industrial compounder with EV optionality."

The bear case centers on the structural reality of the energy transition. Internal combustion engine decline, while gradual in commercial vehicles, is directionally irreversible. As battery technology improves and charging infrastructure expands, the proportion of new commercial vehicles equipped with traditional transmissions will decline. The central risk is not that this happens—Allison's management acknowledges it—but that it happens faster than expected, eroding the core ICE business before eGen Power revenue scales sufficiently to compensate.

Chinese EV drivetrain manufacturers represent a meaningful competitive threat, particularly in global markets outside North America. Chinese companies have demonstrated the ability to manufacture electric motors, inverters, and integrated e-axles at cost points that Western competitors struggle to match. If Chinese EV drivetrains achieve quality parity with Allison's eGen Power products—an outcome that is possible though not certain—they could undercut Allison on price in markets where brand loyalty and switching costs are less established.

Geographic and cyclical concentration remain legitimate concerns. Heavy exposure to the North American Class 8 truck cycle means that Allison's results are significantly influenced by a single market's economic conditions. While the aftermarket provides a buffer, a severe and prolonged trucking recession would still pressure results meaningfully.

The Dana acquisition, while strategically sound, approximately doubled Allison's revenue base and introduced integration complexity along with additional debt. Execution risk associated with integrating operations across 25-plus countries and 11,000 new employees is non-trivial.

Finally, the autonomous vehicle question looms as a longer-term uncertainty. If autonomous driving technology fundamentally changes how commercial vehicles are designed and operated—potentially enabling new drivetrain architectures optimized for autonomous duty cycles—it could alter the competitive landscape in ways that are difficult to predict. Counter-argument: autonomous vehicles still need to move, and moving heavy loads over varied terrain still requires sophisticated drivetrain engineering regardless of who—or what—is driving. Allison's technology solves a physics problem, not a human-factors problem, which means autonomy may change the driver but not the drivetrain.

There is also a myth-versus-reality worth addressing directly. The consensus narrative positions Allison as a "legacy industrial" company living on borrowed time as the energy transition unfolds. The reality is more nuanced. Commercial vehicle electrification is progressing significantly slower than passenger vehicle electrification, for fundamental physics and economic reasons. Battery weight and cost, charging infrastructure limitations for long-haul applications, and the 15-to-20-year replacement cycles of commercial fleets mean that internal combustion engine transmissions will remain the majority of Allison's addressable market well into the 2030s and potentially the 2040s. The company is not racing against imminent obsolescence—it is managing a gradual, multi-decade transition with the advantage of cash flows from the existing business to fund development of the next one.

For investors tracking Allison's performance, the two KPIs that matter most are: first, aftermarket revenue as a percentage of total revenue, which indicates the health and growth of the recurring revenue base that provides earnings stability; and second, eGen Power order backlog and revenue contribution, which will reveal whether the electrification pivot is translating from strategic positioning into actual commercial traction.

XIII. Recent Developments & The Road Ahead (2024–2025)

The years 2024 and 2025 brought a combination of record results, cyclical headwinds, and transformative strategic action that together defined a new chapter in Allison's evolution.

Fiscal year 2024 set records across multiple dimensions: the company reported record full-year revenue and record adjusted net income, driven by strong demand in the North American on-highway market and continued growth in defense. The defense segment's performance was particularly notable, with accelerating revenue growth reflecting the broader increase in military spending. Management executed confidently on its capital allocation priorities, returning substantial cash to shareholders while maintaining investment in both the traditional and electric product lines.