Allegion: The Unseen Tollbooth of the Physical World

I. Introduction & Episode Roadmap

Start with the discrepancy, because the whole investment case lives inside it.

In fiscal 2025, Allegion generated $4.07 billion in revenue, up 7.8% on a reported basis and 4.1% organically.1 That is a respectable but unremarkable number for an industrial company. What is remarkable is where the profit comes from. The Americas segment — essentially the United States, Canada and Mexico — produced roughly $3.22 billion of that revenue and the overwhelming majority of the company's operating profit, running at a segment operating margin near 28%.12 The International segment, spanning Europe, the Middle East, Asia-Pacific and beyond, delivered about $848 million of revenue but a fraction of the profit, at a reported segment margin of roughly 9%.12

Sit with that for a moment. A company that looks global on a map is, in economic reality, an American business with an international appendage attached. The Americas franchise throws off cash at margins that software companies would envy; the International business, despite years of acquisitions, has struggled to earn its keep. Understanding why that gap exists — and whether it is permanent — is most of the work of analyzing Allegion.

The second thing to understand is the transition. Allegion's crown jewels — Schlage locks, Von Duprin exit devices, LCN door closers — are triumphs of mechanical engineering. They are precisely machined pieces of metal that have barely changed in principle for a century. But the industry is migrating from brass and steel to electronics: card readers, wireless locks, mobile credentials stored on a phone, and cloud software that manages who can open which door at what time. Management calls the destination "Seamless Access." The core tension of the investment case is whether Allegion can ride that migration — which sharply raises the price of every opening — without inviting technology-native competitors to strip away the most valuable layer of the stack.

There is a third thing worth planting early, because it is the reason the business is interesting at all: the cash. In fiscal 2025 Allegion converted its profits into $685.7 million of available cash flow, up 17.6% year over year, on that $4.07 billion of revenue.1 A company that turns roughly seventeen cents of every revenue dollar into deployable free cash, year after year, is not an ordinary industrial. It is a capital-light annuity dressed as a manufacturer. The mechanical brutality of that math — high margins, low reinvestment needs, steady replacement demand — is what makes the tollbooth metaphor apt, and it is also what creates the central management problem: a river of cash that has to be allocated somewhere, wisely or poorly, quarter after quarter. Much of what follows is the story of where that river has been directed.

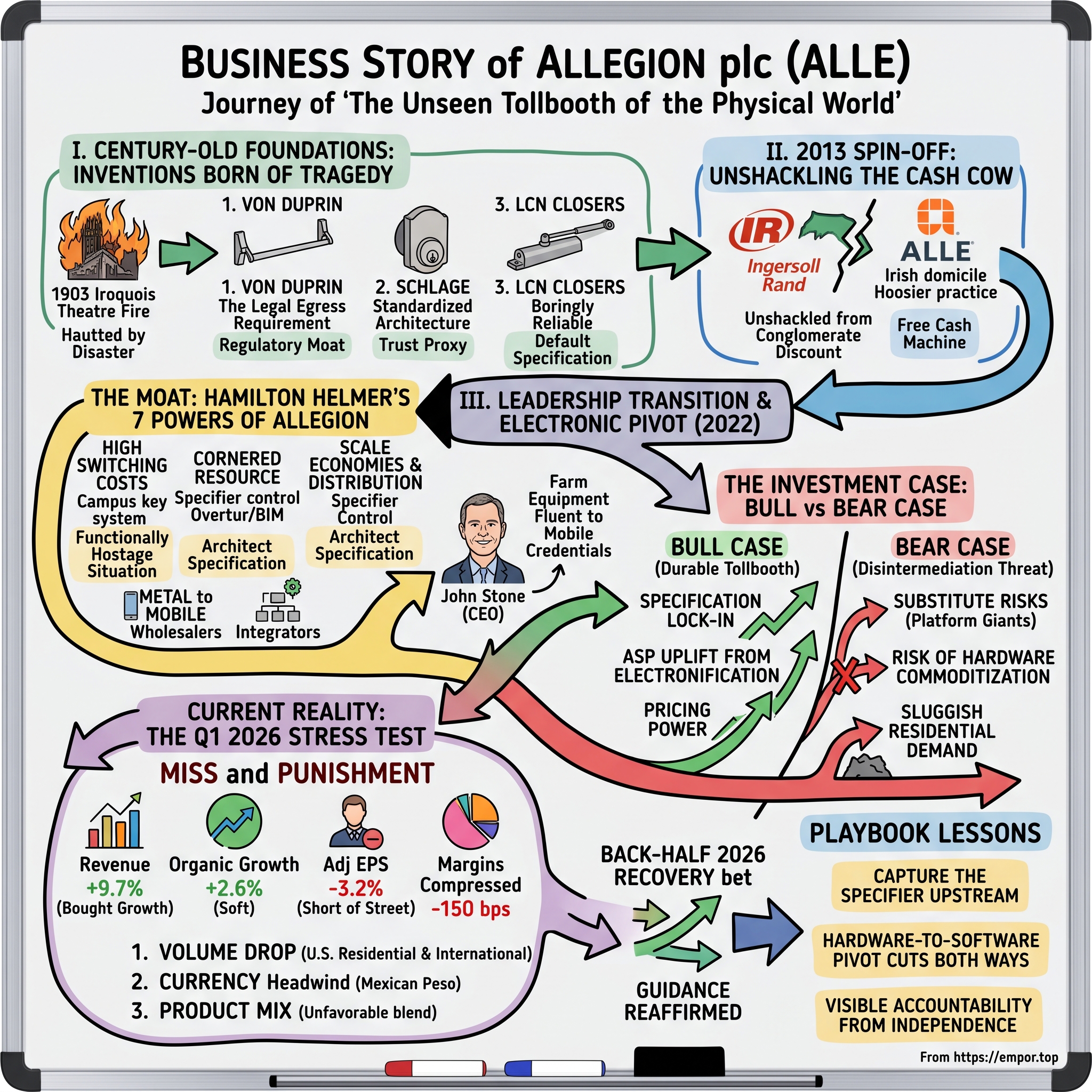

To get there, this story travels from a horrific 1903 theater fire in Chicago that gave birth to the modern exit device; through the 2013 spin-off that freed these brands from an industrial conglomerate; into the mechanics of a moat built on switching costs and architect specifications; across the two-segment divide; through the 2022 arrival of a chief executive plucked from the world of autonomous tractors; into a string of acquisitions that drew fire from analysts; and finally into the stress test of early 2026, when the company missed and the market punished it. Throughout, the question worth holding is the one a skeptical investor would ask on every earnings call: is this a durable tollbooth, or a cyclical hardware supplier wearing a tollbooth's costume?

II. The Century-Old Foundations: Inventions Born of Tragedy and Genius

On the afternoon of December 30, 1903, some 1,700 people packed into Chicago's brand-new Iroquois Theatre for a holiday matinee of Mr. Bluebeard. The theater had been advertised as "absolutely fireproof." It was not. A stage light ignited a curtain, flames raced through the auditorium, and panic did the rest. Many of the exit doors were locked, and some opened inward, so the crush of bodies pressing against them sealed them shut. When it was over, 602 people were dead — a death toll that still ranks among the worst single-building fires in American history.3

Among those who had planned to attend, and did not, was a hardware salesman named Carl Prinzler, who ran the builders' hardware department at the Vonnegut Hardware Company in Indianapolis. Business had called him elsewhere that day. Haunted by the disaster and by the grim engineering lesson inside it — that a locked door is a death trap when a crowd needs to flee — Prinzler set out to solve the problem. Working with an engineer named Henry DuPont, he developed a device that would keep a door secured from the outside while allowing anyone inside to escape simply by pushing against a horizontal bar. In 1908 the first "panic release" exit device reached the market, sold under a name stitched together from its makers: Von Duprin — Vonnegut, DuPont, Prinzler.4

This is the origin of Allegion's deepest and least appreciated moat, and it is worth dwelling on why. The panic bar is not merely a good product; it is a legally mandated one. In the century since the Iroquois fire, North American life-safety and building codes came to require compliant exit devices on the doors of commercial and institutional buildings. A business selling into that requirement does not have to persuade a customer that egress hardware is desirable — the fire marshal has already done the persuading, and the building cannot legally open its doors without it. When demand for your product is written into law, you have a kind of durability that no marketing budget can buy.

The mechanism is subtle enough to be worth spelling out for an investor, because "regulatory moat" gets thrown around loosely. Codes do not name Allegion; they specify performance requirements — a door that latches, a device that releases under a specified force, a closer that shuts a fire door reliably. What that regulatory scaffolding does is convert door hardware from a discretionary purchase into a non-negotiable line item, and then it makes the proof of compliance — the third-party testing, the listings, the fire ratings — a barrier that favors established, deep-catalog manufacturers over newcomers. A startup cannot simply build a cheaper exit device; it must build one that passes the same battery of life-safety tests and then convince a risk-averse specifier to bet a building's occupancy permit on an unknown brand. The code does not hand Allegion the sale, but it dramatically narrows the field of who can credibly compete for it, and it makes the cost of a compliance failure catastrophic. That asymmetry — trivial upside to switching, ruinous downside to getting it wrong — is the quiet engine underneath the whole franchise.

The second pillar came from San Francisco. In 1920, a German immigrant named Walter Schlage set up a small workshop and perfected the cylindrical push-button lock — a design that combined the lock's working parts into a single unit that could be bored into a door and installed quickly, with a button in the knob to lock it.5 It sounds mundane today because it won: the cylindrical lock became the standard architecture for door locks across the continent, and "Schlage" became one of those brand names that quietly stands in for the entire category, the Kleenex of locks.

The third pillar is the least glamorous and the most telling. Decades earlier, a man named Lewis C. Norton had been hired to quiet the banging vestibule doors of Boston's Trinity Church, whose slamming disrupted services with every gust of wind. His answer was a hydraulic door closer — a device using controlled fluid rather than a noisy spring or pneumatic mechanism to ease a heavy door shut smoothly and reliably. In 1926 Norton and a partner formalized the enterprise that would become known as LCN Closers, and the liquid-controlled closer became the standard for the heavy, high-traffic doors of hospitals, schools and offices.6 Notice the pattern across all three: each invention solved a problem of safety or reliability so completely that it became the code, the standard, or the default specification. That is not the same thing as being merely popular.

It is also worth noticing what these three founding stories share, because the pattern is the company's DNA. In every case, the invention was a response to a specific, visceral failure — people dying behind locked doors, locks too crude to install at scale, doors slamming through a church service. In every case, the solution was mechanical, precise, and boringly reliable in a domain where unreliability is intolerable. And in every case, the product did not just sell well; it defined the category and then got absorbed into the standards and habits of an entire industry. Businesses built on "defined the category a hundred years ago and still owns the specification" are extraordinarily rare, and they tend to share a trait Allegion has in abundance: the brand name becomes a proxy for trust in a purchase where trust is the whole point. Nobody wants to be the facilities manager who saved forty dollars a door and then watched an exit device fail.

For most of the twentieth century, these three brands, along with others, were bundled together and run as a security division inside the industrial conglomerate Ingersoll Rand — a sprawling company better known for compressors, pumps and HVAC systems. The locks were a fine business, but inside a conglomerate they were a rounding error, competing for capital and attention against heavier industrial bets. Which raises the obvious question: if these were such wonderful franchises, why were they hiding inside a compressor company at all — and what happened when someone finally decided to let them out?

III. The 2013 Spin-Off: Unshackling the Cash Cow

By 2013, the conglomerate model was out of fashion, and for good reason. Sprawling industrial holding companies tend to trade at a "conglomerate discount" — the market values the whole at less than the sum of its parts, because investors struggle to price a grab-bag of unrelated businesses and management struggles to allocate capital wisely across them. A high-margin, low-capital security business and a heavy, cyclical HVAC business have almost nothing in common except a shared parent, and each was arguably worth more standing on its own.

So Ingersoll Rand cut its security division loose. On December 1, 2013, the spin-off was completed: shareholders received one ordinary share of the new company, Allegion plc, for every three Ingersoll Rand shares they held, and Allegion began trading on the New York Stock Exchange under the ticker ALLE.78 The portfolio that walked out the door included the crown jewels — Schlage, Von Duprin, LCN — alongside international brands such as CISA and the German workforce-management business Interflex.8

Two structural choices from the separation still shape the company today. The first was legal domicile: Allegion was incorporated in Ireland, a decision rooted in the tax and corporate advantages of that jurisdiction, while its operating headquarters and its center of gravity remained in Carmel, Indiana. The company is Irish on paper and Midwestern in practice. The second was independence itself — for the first time, the security brands controlled their own capital, their own research budget, and their own strategic destiny.

Why does a conglomerate discount exist at all? Two reasons, both relevant here. The first is analytical: investors and the analysts who cover a stock specialize, and a fund that wants exposure to security hardware does not want to also underwrite a compressor cycle it cannot model. A pure-play is easier to value, easier to benchmark against peers, and therefore attracts a cleaner, often higher, multiple. The second is behavioral: inside a conglomerate, capital tends to flow toward the businesses that shout loudest or burn cash fastest, not necessarily toward the ones that earn the highest returns. A quietly excellent security division can be starved to feed a struggling industrial one. Spinning it out forces the market to price it on its own merits and forces its managers to earn their own capital. Both effects worked in Allegion's favor.

Wall Street's initial read was nonetheless skeptical and, in hindsight, wrong. The consensus filed Allegion under "building products" — a low-growth, cyclical category tied to construction activity, the kind of business that booms and busts with housing starts and commercial permits. And there is truth in that framing; Allegion is not immune to the construction cycle, as 2026 would remind everyone. But the market underappreciated what sat underneath the cyclicality: a business with extraordinary pricing power, an installed base that generates replacement and upgrade demand for decades, and switching costs so high that customers rarely leave. Over the years following the spin, the durability of those economics became visible in the numbers — steadily expanding margins and reliable cash generation — and the multiple the market was willing to pay expanded with them. The stock became a compounder's darling, the kind of name that quietly triples while the headlines ignore it.

That re-rating is itself a lesson in how markets misprice quality. For most of a decade the doubters were proven wrong not because Allegion grew fast — it did not — but because it grew reliably and returned cash while doing so. The danger, of course, is that a re-rating can run too far, pricing a cyclical business as if it were an annuity; the sharp drawdown from the 2025 highs into 2026 is partly the market re-testing exactly that question. A business can be genuinely excellent and still be temporarily overpriced, and distinguishing the durability of the franchise from the durability of the multiple is one of the harder jobs in analyzing Allegion.

The scoreboard vindicated the separation. Allegion entered independent life as a business of roughly $2 billion in annual revenue; by fiscal 2025 it had grown to $4.07 billion, roughly doubling over the period while steadily lifting margins and compounding its dividend.1 That growth was not explosive — this is a mid-single-digit organic grower supplemented by acquisitions and price — but it was remarkably consistent, and consistency at high margins is what the market eventually pays up for. The re-rating of the multiple did as much for shareholders as the earnings growth itself, which is precisely the value a spin-off is supposed to unlock.

Freed from the conglomerate, management could also do something it could not do inside Ingersoll Rand: reinvest deliberately in the electronic future of the business. The spin gave Allegion the autonomy to begin funding the migration from mechanical to electronic access — the connected locks, the credentials, the software — that would define its next decade and its central strategic gamble. But before we judge that gamble, we need to understand precisely what the moat is that management is trying to carry across the bridge, because a moat you do not understand is a moat you cannot tell is eroding.

IV. The Moat: Hamilton Helmer's 7 Powers of Allegion

Picture the facilities director of a large state university on the morning she inherits the job. Somewhere in a locked office is a document — sometimes literally a bound book, sometimes a database — that describes the campus's master key system: which keys open which doors, how the hierarchy of sub-masters and grand-masters is structured, who is authorized for what. That system was designed, years or decades ago, around a specific manufacturer's cylinders and cores. It governs tens of thousands of openings across dormitories, laboratories, offices and mechanical rooms. And it is, functionally, a hostage situation — with the university as the willing hostage.

This is the first and most powerful of Allegion's advantages, and it maps cleanly onto Hamilton Helmer's framework of competitive "powers."

Power 1: High Switching Costs — the campus lock-in. To rip out an incumbent's hardware and replace it with a competitor's — say, to swap Schlage and Von Duprin for the Swedish giant ASSA ABLOY — a large institution would have to physically replace thousands of lock cores, redesign and re-issue its entire master key hierarchy, retrain staff, and absorb a period of security disorder during the transition. The cost of the hardware itself is trivial next to the operational cost and the risk of getting the security of a hospital or campus wrong during a changeover. So the customer stays, not out of loyalty, but out of arithmetic. The switching cost is the moat, and it compounds every time the institution adds another building keyed to the same system. This is why a locksmith or integrator, once standardized on a brand, tends to stay standardized for a generation.

Power 2: Cornered Resource — the specifier moat. Here is the part outsiders almost never see. In commercial construction, the decision about which door hardware goes into a building is not made by the building's owner or its general contractor. It is made far earlier, by architects and specification consultants who write the technical blueprints — the "specs" — that define exactly which products must be installed. Industry lore holds that the great majority of commercial hardware decisions are effectively locked in at this specification stage, long before a shovel hits the ground. Whoever controls the spec controls the sale.

Allegion has spent years turning that reality into a defensible asset through software. Its cloud tool Overtur integrates directly into the Building Information Modeling (BIM) systems, such as Autodesk Revit, that architects use to design buildings.[^9] By making it dramatically easier for a specifier to design compliant door openings using Allegion's catalog and data, Overtur embeds Allegion into the building's digital DNA before construction begins. Once the hardware is specified and the design is code-compliant, a contractor trying to substitute a cheaper brand faces friction, delay, and liability risk — the "or-equal" substitution has to be proven equivalent, and often it is simply easier to buy what the architect wrote. In Helmer's terms, privileged access to the specification workflow is a cornered resource. It is worth stressing, though, that this is a claimed mechanism as much as a proven one: the company does not publicly disclose spec-conversion rates, so an investor is asked to take the strength of the specifier moat partly on faith and partly on the observable stickiness of the results.

Power 3: Scale Economies and Distribution Power. Finally, there is the un-sexy machinery of getting product to the door. Allegion sits atop decades-old relationships with wholesale distributors, locksmiths and security integrators who are trained and certified on its brands and who carry its inventory. This distribution web is expensive and slow to build, and it reinforces the first two powers: the trained integrator recommends the brand he knows, which deepens the installed base, which raises switching costs. Scale in manufacturing also matters — the company's ability to produce enormous volumes of standardized, code-compliant hardware at low unit cost is hard for a small entrant to match.

There is a fourth power lurking here that Helmer would call branding, and it deserves a mention because it is the most fragile of the four. In a category where the buyer cannot easily verify quality before installation and where the cost of failure is a fire-code violation or a security breach, the brand name does real economic work: it substitutes for verification. A specifier writing "Schlage or equal" is buying insurance against being blamed if something goes wrong. That is why the mid-tier product strategy management has pursued — the Schlage Performance Series locks launched in September 2025, the Von Duprin 70 Series exit devices, mid-price LCN closers — is more clever than it looks.1 It lets Allegion capture price-sensitive aftermarket demand and fend off cheaper competitors without diluting the premium brand's meaning, because the trusted name still sits at the top of the good-better-best ladder. The risk, as management itself acknowledged when pressed on the 2026 mix issues, is that a value-tier push can quietly shift the revenue blend toward lower-margin products; the company insists customers are not "trading down," but the line between broadening the range and cannibalizing the premium is one worth watching.9

It is important to note what is not on this list. Allegion has essentially no network effects in the classic sense — your lock does not get more valuable because your neighbor bought one — and no counter-positioning against incumbents, since it is the incumbent. Its powers are the durable-but-static kind: switching costs, a cornered specification resource, scale, and brand. These are formidable at defending a position but not, on their own, engines of rapid growth. That is the correct frame for the whole business: Allegion is built to hold territory superbly, which is exactly why the electronic transition — an attempt to expand the value of each held position rather than to conquer new ones — is the strategically coherent move, and also the one that most tests whether static powers can survive a dynamic shift.

The honest analytical conclusion is that Allegion's moat is real and, in its Americas mechanical core, genuinely deep — but it is a moat built for a mechanical, code-driven, specification-led world. Every one of these powers was forged in brass and steel. The pressing question, which the rest of this story circles back to again and again, is whether they transfer intact into a world where the "lock" is increasingly a piece of software and a credential on a phone. Before we can weigh that, we have to look squarely at where the moat actually pays off today — and where, conspicuously, it does not.

V. A Tale of Two Segments: Americas Cash Cow vs. International Drag

If you want to understand Allegion, put its two segments side by side and stare at the gap.

In fiscal 2025, the Americas segment delivered roughly $3.22 billion of revenue and about $896.5 million of segment operating profit — a reported segment operating margin near 28%.12 The International segment delivered around $848.5 million of revenue but only about $76.5 million of segment operating profit, a reported margin of roughly 9%.12 On an adjusted basis, which strips out the amortization of intangibles from acquisitions, the International margin looks better — about 16.7% for the year — but the point stands: the Americas business is nearly twice as profitable per dollar of sales, and because it is also far larger, it produces the overwhelming majority of the company's profit.1 One segment is a cash cow; the other, for all the capital poured into it, has behaved more like a project than a franchise.

Why is the Americas so dominant? The answer is that North America is the near-perfect habitat for Allegion's moat. The market runs on highly standardized building and life-safety codes and on ANSI/BHMA hardware standards, which means a compliant, specified product wins predictably across the entire continent. The installed base is vast and decades deep, so replacement and upgrade demand flows steadily regardless of new construction. And brand equity is concentrated: Schlage, Von Duprin and LCN are the names architects and integrators reach for by reflex. All three of the powers described earlier — switching costs, the specifier lock-in, distribution — operate at full strength here, in one language, under one broad regulatory logic.

The Americas is also usefully split between two very different demand personalities, and 2025–2026 pulled them apart in a way that clarifies the business. The nonresidential side — schools, hospitals, offices, institutional buildings — is where the moat is deepest and where growth held up: it grew high-single digits organically in the fourth quarter of 2025 and mid-single digits in the first quarter of 2026, driven by a combination of price and, crucially, real volume, and management repeatedly pointed to strong "spec activity" as evidence that the pipeline of future projects remained healthy.19 The residential side — locks for homes, sold heavily through retail and tied to housing turnover and new construction — is far more cyclical and far more exposed to consumer and interest-rate conditions, and it went the other way, declining high-single digits in the fourth quarter of 2025 as new-build weakness and a soft aftermarket bit hard.1 The lesson for an investor is that "Americas" is not one demand stream but two: a durable, moaty institutional business and a cyclical consumer business, and the reported segment margin blends them. When residential volumes fall, they deleverage the factories and drag the whole segment's margin, which is much of what went wrong in early 2026.

Cross the ocean and every one of those advantages weakens. The International markets are fragmented across dozens of countries, each with its own standards — the continental European DIN conventions differ from North American ANSI, and neither is universal. There is no single dominant specifier culture to corner, no continent-wide master-key lock-in, no one brand that means "lock" the way Schlage does in the United States. Instead there is a patchwork of national brands, national codes, and national distribution, which is exactly the kind of terrain where moats are shallow and margins are thin. Allegion's international footprint was assembled largely through acquisition, and integrating those businesses — harmonizing systems, pruning weak product lines, absorbing the ongoing cost — has repeatedly weighed on profitability.

That said, the International story is not uniformly bleak, and a fair analysis has to hold both halves. Buried inside the segment are genuinely good businesses. Interflex, the German workforce-management and access-software operation, is one management repeatedly singles out: a blue-chip customer base, a seasonal revenue shape that ramps through the year, and — on the February 2026 call — what Stone called "a bang-up year," complete with an effort to weave artificial intelligence into its reporting software.1 The company's European electronics businesses, concentrated in the German-speaking DACH region and expanding pan-Europe, have been the segment's growth engine, and it is exactly this electronics strength that the 2025 ELATEC acquisition was meant to reinforce. So the International segment is really two things stacked together: a promising, higher-quality electronics-and-software layer that is growing, and a soft, low-margin legacy mechanical layer that periodically drags the whole segment down. The bull would say management is deliberately shifting the mix toward the good half through "self-help," selective pruning of non-core assets, and bolt-on acquisitions. The bear would say that after more than a decade of this, the segment still earns single-digit reported margins and remains one ERP project away from wiping out a quarter's progress.

The early-2026 results made the fragility vivid. In the first quarter of 2026, the International segment's organic revenue actually fell 5.3%, and its adjusted operating margin dropped 220 basis points, driven overwhelmingly by a botched enterprise-resource-planning (ERP) software implementation at a single legacy European mechanical business that disrupted production.9 Chief executive John Stone was blunt about it on the April call: this was not a demand problem but an execution problem — "it's our execution that needs to improve," he said, expressing confidence the shortfall would be recovered over the year as production rates normalized.9 One analyst, Goldman Sachs' Joe Ritchie, went straight for the jugular, asking whether it even "makes sense for Allegion to have an international presence" given how well the domestic business runs.9 Stone deflected — "Q1 earnings call is not the time to have such a conversation" — but the fact that the question was asked at all tells you how the market views the segment.9

For an investor, the two-segment split is the central tension of the equity. The Americas is the reason to own the stock: a genuinely advantaged, high-return, cash-generative franchise. The International business is the reason to hesitate: a lower-return, execution-sensitive collection of assets that consumes capital and management attention and periodically produces exactly the kind of self-inflicted stumble that erases a quarter. Whether International is a value-destroying distraction or a necessary beachhead for the electronic future depends heavily on your view of the person now steering the company — which is where the story turns next.

VI. The Leadership Transition: Transitioning from Metal to Mobile Credentials

For its first nine years as an independent company, Allegion was run by Dave Petratis, a steady industrial hand who established the post-spin playbook: disciplined capital allocation, consistent margin expansion, and a clear identity as a focused security company rather than a sprawling conglomerate. Under Petratis, Allegion earned its reputation as a reliable compounder — the kind of chief executive who did not chase headlines but delivered the quiet, repeatable margin and cash-flow gains that re-rated the stock. His tenure answered the question the spin-off posed: yes, these brands could stand on their own and, freed of the conglomerate, could steadily widen their advantage. But a strong operator of a mechanical business is not automatically the right person to lead a mechanical business into an electronic one. By 2022, the board was looking for something the mechanical era had not required — a leader fluent in electronics, connectivity and software. The very consistency that made Petratis valuable in the franchise's steady state was, in a sense, the wrong instinct for a period that would demand a bet on a different future.

They found an unusual one. In July 2022, John H. Stone became president and chief executive of Allegion, arriving not from the security industry but from Deere & Company — the maker of green tractors.9 For roughly two decades at Deere, Stone had worked at the frontier of putting intelligence into heavy iron. He led Deere's Intelligent Solutions Group, the unit responsible for weaving GPS guidance, computer vision, artificial intelligence, IoT sensors and autonomy into farm equipment — the work that turned a tractor from a dumb machine into a connected, data-generating, increasingly self-driving platform.

The logic of the hire is easy to state and harder to execute: if this executive could make a tractor drive itself across a field and phone its data home, perhaps he could make a commercial door part of an intelligent, cloud-connected network — the "Seamless Access" vision in which credentials live on phones, locks talk to software, and every opening becomes a node in a managed system. Stone's mandate was to bring the ag-tech mentality — connectivity, SaaS, data — to an industry still selling most of its value in machined metal.

The analogy is seductive, and it is worth interrogating rather than accepting. Deere's transformation is one of the great industrial-technology stories of the era: a company that sold steel by the ton learned to sell software subscriptions and precision-agriculture data on top of the steel, lifting margins and deepening customer lock-in. If door hardware follows the same arc — dumb metal becomes connected platform, one-time hardware sale becomes recurring credential-and-software relationship — then a leader who has actually done it before is enormously valuable. But there is a crucial disanalogy the bull case tends to skate past. Deere sold to a relatively concentrated base of large, sophisticated farm operators who valued yield gains worth tens of thousands of dollars; Allegion sells fragmented door hardware into buildings owned by thousands of institutions, specified by architects, installed by integrators, and often bought on the basis of code compliance and price. The unit economics, the buyer, and the decision-maker are all different. Whether the ag-tech playbook truly ports to door hardware — or whether the transferable insight is more atmospheric than operational — is precisely the wager the board made, and it will take years of results, not press releases, to settle.

A skeptical investor should treat that thesis as a hypothesis, not a conclusion, and judge Stone the way one judges any manager: by behavior over time. On the credibility ledger, several things are worth watching. His pay is heavily weighted toward equity — total fiscal 2025 compensation of roughly $9.16 million, the bulk of it in stock and performance awards rather than cash — which ties his personal wealth to the long-run share price rather than to a single year's earnings.10 That is the alignment you want, though it is also standard for large-cap CEOs and proves intent rather than results.

More telling is how Stone and his team communicate. Across the 2025 and early-2026 earnings calls, management has been notably consistent in its language: "balanced, disciplined and consistent" capital deployment, a stated top priority of "investing for growth," and a repeated insistence that pricing and productivity must cover inflation and investment.19 Consistency of narrative is a mild positive — it is easier to trust a management team that says the same thing in good quarters and bad. The more searching question, which the next section confronts directly, is whether the actions have matched the words, particularly on the single decision where CEOs most often destroy value: how they spend the cash.

VII. The M&A Engine & Capital Allocation Under Scrutiny

A cash cow generates a problem most companies would love to have: what to do with all the money. Allegion's Americas franchise throws off far more cash than it needs to run itself, and the central strategic question of the Stone era is where that cash should go. Management's answer has leaned heavily toward acquisitions — and that answer has drawn some of the sharpest questioning the company has faced.

The template deal came just before Stone arrived. In 2022, Allegion agreed to acquire Stanley Access Technologies — the automatic-door business — from Stanley Black & Decker for $900 million in cash.[^12] Stanley Access is a storied name; it traces its lineage to the invention of the automatic door itself. But Allegion did not pay up for the privilege of selling metal doors. The strategic logic was about controlling the physical entry point to commercial buildings: automatic sliding and swinging doors are the touchless, high-traffic entrances of hospitals, airports and offices, and owning that platform lets Allegion integrate hardware, automation and access control into a single point of entry. The price — reported at roughly sixteen times that year's expected EBITDA, and lower on a tax- and synergy-adjusted basis — was full but defensible for a strategic asset with recurring service revenue attached.

Then came a burst of activity in 2025. Allegion deployed roughly $630 million on acquisitions during the year, the largest of which was ELATEC, a German-based maker of RFID and mobile-credential reader technology, acquired for €330 million (about $382 million) from the private equity firm Summit Partners and folded into the International segment.1[^13] ELATEC matters because credentials are the connective tissue of Seamless Access: the reader that recognizes your phone or card is the bridge between the mechanical lock and the digital system, and owning that technology is a bet on the migration away from physical keys. Placing it inside the International segment is telling, and slightly awkward for the equity story — the technology that is supposed to power the electronic future was bolted onto the lower-margin, less-loved half of the company, which means the near-term optics of the deal will be muddied by the very segment drag investors already worry about.

In March 2026, Allegion added a smaller, more traditional bolt-on: DCI Hollow Metal on Demand, a West Coast maker of custom hollow-metal doors and frames that lets Allegion serve Western U.S. customers without the freight cost and lead time of shipping from its Cincinnati plant.[^14] Management was candid that DCI carries only a low-double-digit EBITDA margin and would dilute Americas margin rates by roughly 30 basis points for the year, framing it as a strategic cost-position move rather than an immediately accretive one — the logic being that customers buy complete door-and-hardware packages, so being locally competitive on the door itself pulls through the higher-margin hardware around it.9 It is a defensible rationale, but it is also the kind of "strategic, not accretive" deal that a skeptical investor learns to watch carefully, because the phrase can cover a multitude of value-destroying sins if the promised pull-through never materializes.

Step back and the capital-allocation picture takes shape. Alongside the deals, Allegion returned cash the traditional way: it paid $175 million in dividends in 2025 and announced its twelfth consecutive annual dividend increase, a streak that spans essentially its entire life as a public company and signals a genuine commitment to the payout.1 It repurchased $80 million of stock in 2025 — modest, and notably it bought back nothing in the fourth quarter.1 The balance sheet stayed conservative, with net debt at roughly 1.6 times adjusted EBITDA at year-end, leaving ample room for more deployment.1 So the honest characterization is not that management ignored shareholders; it is that within a balanced framework, the marginal dollar was tilting toward acquisitions, and the acquisitions were tilting toward the parts of the portfolio with the least proven returns.

This acquisition-first posture set up the most revealing exchange of the year. On the full-year 2025 earnings call in February 2026, Bank of America's Andrew Obin put the challenge directly to management: the markets have been sluggish, you have delivered consistent EPS growth anyway, and yet you chose to pour capital into M&A — so why isn't your own stock the best value out there? Why not simply buy back Allegion shares rather than acquire other companies?1 It was the classic capital-allocation confrontation: a company with a cheap, cash-generative stock choosing external deals over the highest-certainty return available, its own equity.

Stone's defense was to restate the philosophy: profitable growth is the top priority, the dividend will grow with earnings, and buybacks happen "when the conditions are there," but attractive bolt-on acquisitions that can be integrated for accretive returns will win the capital when they appear.1 It was a coherent answer, but not one that fully satisfied the premise of the question — namely, whether hundreds of millions spent on lower-return international and technology deals clears the bar set by simply retiring cheap shares.

What happened next is the part worth noting, because it speaks to whether management listens. Having repurchased essentially no stock in the fourth quarter of 2025, Allegion moved in the first quarter of 2026 to buy back $40 million of shares and its board authorized a new $500 million repurchase program.9 Management would frame this as continuity rather than course correction — the authorization was "open," they had always said buybacks would happen "as appropriate." A more skeptical reading is that a stock down sharply from its highs, plus persistent analyst pressure, nudged capital allocation toward the shareholder-return end of the spectrum. Either way, the sequence is a useful data point: the words are consistent, and the actions are at least directionally responsive. Whether the acquired businesses — especially the lower-margin international and technology assets — ultimately earn their cost of capital is the open question that no press release can answer, and it can only be judged in the results. Which brings us to the quarter where the results turned uncomfortable.

VIII. Current Reality: The Q1 2026 Stress Test & Margin Compression

For a company that had built a reputation as a metronome, the first quarter of 2026 was a discordant note. Reported on April 28, 2026, revenue crossed $1 billion, up 9.7% — a healthy-looking headline.9 But almost all of that growth was bought: organic growth, which strips out acquisitions and currency, was a soft 2.6%, and the acquisitions doing the heavy lifting were precisely the ones analysts had been questioning.9 Adjusted earnings per share came in at $1.80, actually down 3.2% from the prior year and short of what the Street had been modeling.9 For a business that sells itself on steady compounding, a down-EPS quarter is a jolt.

The margin story was the real concern. Enterprise adjusted operating margin fell 150 basis points, from 22.7% to 21.2%.9 Peel that apart and three distinct forces were at work, each revealing something different about the business.

First, volume. Underneath the price-driven revenue growth, unit volumes declined, with the softness concentrated in two places: the U.S. residential housing market, where new construction remained weak and the aftermarket was, in Stone's phrase, "treading water," and the International segment.9 Residential in the Americas was flat overall as price offset falling volumes — meaning the volume drop itself was worse than the segment total suggested.9 Weak volume matters because Allegion's factories carry fixed costs; when units fall, there is less production to spread those costs over, and margins deleverage. This is the cyclical, building-products side of Allegion showing through the tollbooth costume.

Second, a currency quirk worth explaining because it recurs. Allegion manufactures extensively in Tijuana, Mexico, while selling primarily in U.S. dollars. That creates transactional foreign-exchange exposure: costs in pesos, revenue in dollars. In the first quarter of 2025, a favorable peso had handed the Americas a roughly $3 million benefit — and lapping that easy comparison a year later showed up as a transactional FX headwind in the 2026 quarter.9 It is not that the peso suddenly savaged the business; it is that a prior-year tailwind reversed into a year-over-year drag. Small in dollars, but a clean illustration of how a globally sourced cost base injects volatility into an otherwise steady margin.

Third, mix. The high-margin electronic upgrades that are supposed to lift the business decelerated to mid-single-digit growth in the Americas, down from the low-double-digit pace of prior quarters, and CFO Mike Wagnes attributed the margin pressure to unfavorable product mix — not customers trading down to cheaper products, he was careful to clarify, but an unfavorable blend across the company's various nonresidential lines.9 The distinction matters: a durable shift toward cheaper products would threaten the franchise, whereas quarter-to-quarter mix noise does not. Still, the electronics deceleration is worth flagging, because electronics growth is the single clearest proof point for the entire transition thesis. Management's explanation — that the prior year's double-digit pace was a tough comparison and that electronics remains a long-term growth driver that will "outgrow the mechanical" over time — is reasonable, but two consecutive quarters of slower electronics growth would start to look less like a comparison artifact and more like a stalling adoption curve.9

Layered on top of all this was the macro and policy backdrop, which management addressed candidly. A flurry of shifting U.S. trade actions through late 2025 and into 2026 — various tariff regimes coming and going — plus fuel-cost inflation, added up to an incremental headwind of roughly one point of cost of goods sold, which the company intends to offset on a dollar basis through further pricing and cost actions rather than absorb.9 On the geopolitical front, Stone noted that active conflicts, including in Iran and the broader Middle East, had not produced a notable demand impact and that Allegion's direct exposure to the region was "negligible," though Europe — more directly affected — remained the softer end market.9 This is the texture of running a globally sourced manufacturer in a volatile world: the moat protects pricing power and demand, but it does nothing to shield the cost base from trade policy, currency, and freight, and a chunk of management's job is now simply staying "agile" — a word that appeared repeatedly on the call — in the face of inputs it cannot control.

There is a structural wrinkle worth understanding, because management leaned on it heavily to explain the quarter: the "tyranny of the math." In early 2025, Allegion had not yet absorbed the tariff-driven inflation that later forced list-price increases; pricing arrived in the middle of the year to cover costs that were also rising. That means the first quarter of 2026 laps a period of low inflation and low pricing, so the year-over-year pricing benefit looks small and the margin comparison looks ugly — an artifact of timing more than a deterioration of the business. Wagnes was explicit that the company expects most of the year's margin expansion to land in the back half, once these comparisons ease and volume leverage returns, and pointed analysts toward the "35%-plus" core incremental margins the company had laid out at its 2025 investor day as the underlying earning power once the noise clears.9 This is a plausible account. It is also, conveniently, an account in which almost everything difficult is temporary and self-correcting, which is exactly the kind of explanation a skeptical investor should file and then check against the actual second- and third-quarter results.

The most important thing management did in the face of the miss was hold the line on guidance. Stone and Wagnes reaffirmed full-year 2026 adjusted EPS guidance of $8.70 to $8.90, betting that back-half margin expansion — driven by pricing actions to offset a fresh ~1% of tariff and inflation cost pressure, productivity, and easier volume comparisons — would rescue the year, while raising the reported revenue outlook to 6–8% to fold in the DCI acquisition and affirming organic growth of 2–4%.9 Notably, management chose not to bake incremental tariff-offsetting price into its organic guidance until those price actions were actually in the market — the same cautious approach it used in 2025 — which is a mild point in its favor on the credibility ledger: it is easier to trust guidance that excludes benefits not yet secured. That is a credibility wager nonetheless. If the back half delivers, management looks disciplined and the first quarter looks like noise. If it does not, maintaining guidance into a visible miss will look like optimism, and the reservoir of trust the company has built since the spin will start to drain. For an investor, the quarter is best read not as a verdict but as a live test of two things simultaneously: how cyclical this "defensive" business really is, and whether management's guidance discipline is earned or hopeful.

IX. The Investment Case: Bull vs. Bear Case

Set the bull and bear cases against each other, because the truth about Allegion is that both are substantially correct, and the investment question is which one dominates over the horizon you care about.

The bull case rests on three legs. The first is durability of demand through specification lock-in: a commercial building designed today with Allegion hardware written into its blueprints will run on that hardware, and its replacement parts and upgrades, for decades. That is a long tail of embedded, code-protected, switching-cost-defended revenue that does not evaporate in a recession. The second is the average-selling-price uplift from electronification. A mechanical lock might sell for on the order of $100; a connected electronic lock, with its reader, credential and software, can sell for several times that — and it can carry recurring software revenue for credential management on top. If Allegion converts even a slice of its enormous mechanical installed base to electronic openings, the revenue and gross profit per door rise dramatically without needing more buildings to be built. The third is pricing power, and here the evidence is concrete rather than aspirational: in the first quarter of 2026, with volumes falling, the company still grew revenue organically purely on price, and it has repeatedly shown the ability to push list prices to cover tariffs and inflation.9 The capacity to raise price into weak volume, without triggering customer flight, is the classic signature of a business with a moat.

Run the Porter's Five Forces lens and the bull case firms up in the Americas. The threat of new entrants is low — code compliance, the specifier relationships, distribution certification and brand trust are formidable barriers. Buyer power is diffused and blunted by switching costs. Supplier power is manageable. Rivalry, while real, is a rational oligopoly: Allegion, the Swedish giant ASSA ABLOY, and Fortune Brands' security assets largely respect price. The one force that is intensifying is the threat of substitutes — and that is precisely where the bear case lives.

The bear case is a coherent and serious argument about disintermediation. As the value of an opening migrates from the mechanical lock to the digital credential and the software that manages access, the profit pool may migrate too — and not necessarily to Allegion. If your building credential lives in Apple Wallet or is provisioned through Google's ecosystem, or if a physical-access-control-software (PACS) provider owns the management layer that governs every door, then the high-margin "intelligence" of the system accrues to the software owner, and the lock risks being commoditized into a low-margin dumb actuator that simply opens when told. In that world, the very transition management is championing could hollow out the moat, reducing a premium hardware franchise to a hardware installer competing on price. This is the deepest tension in the whole story: the electronic future that raises ASP could also invite technology-native competition that Allegion's brass-and-steel moat was never designed to repel.

The competitive landscape underscores the stakes. Allegion's principal global rival, the Swedish giant ASSA ABLOY, is larger, more geographically diversified, and has been aggressively consolidating the industry through hundreds of acquisitions over the years. Its willingness to pay up for smart-lock assets is itself a signal: when ASSA ABLOY acquired Spectrum Brands' hardware and home-improvement division (owner of the Kwikset brand) in a roughly $4.3 billion deal, U.S. antitrust regulators forced it to divest the Yale and Emtek residential smart-lock businesses to Fortune Brands to preserve competition in electronic locks specifically.[^15]11 Read that carefully: the Justice Department drew its competitive line not around mechanical locks but around the smart-lock market, an implicit acknowledgment that this is where the industry's future value and pricing power are migrating. The players fighting hardest, and the regulators watching most closely, are all telling you the same thing about where the money is going.

For Allegion, that competitive frame cuts two ways. On one hand, it operates in a rational oligopoly where the major players — Allegion, ASSA ABLOY, dormakaba, and Fortune Brands' security assets — have historically competed on specification, quality and service rather than ruinous price wars, which protects everyone's margins. On the other hand, the electronic frontier lowers the drawbridge to a different class of competitor entirely. The residential smart-lock market already features Amazon-backed and consumer-electronics entrants; the commercial access-control software market features specialists whose credential-and-cloud platforms could, in principle, relegate the physical lock to a component. Allegion's defense is that in commercial buildings — its profit center — the specifier moat, the code compliance, the integrator channel and the switching costs still gate the sale even when the lock goes electronic. That defense is credible today. Whether it holds as the credential increasingly lives on a phone provisioned by a technology platform, rather than on a card issued by the building, is the single most important unresolved question in the entire bear case.

A brief word on second-layer diligence, because it colors how much benefit of the doubt the strategy deserves. The reassuring signals are real: the balance sheet is conservative at roughly 1.6–1.7 times net debt to EBITDA, cash conversion is high, and the dividend streak reflects a board that has consistently returned cash.19 There is no going-concern worry, no obvious accounting aggression, and no sign of the kind of leverage that turns a cyclical downturn into an existential one. The concentration risks are qualitative rather than financial: an extreme dependence on a single geography for profit, a manufacturing base heavily exposed to Mexico and thus to trade-policy and peso volatility, and a portfolio strategy that keeps adding lower-margin and technology assets whose returns will not be visible for years. None of these are red flags in the fraud sense; they are the honest structural tensions of the business, and they are the things that would occupy a thoughtful long-term owner far more than any single quarter's EPS.

The bear case has two further, more prosaic legs. One is commercial real estate: a prolonged structural decline in new office construction — a plausible legacy of hybrid work — shrinks the flow of new openings into which Allegion writes itself, leaving it more dependent on the slower-growing replacement market. The other is capital allocation, the concern from the prior section: if the International segment keeps stumbling and the technology acquisitions fail to clear their cost of capital, then the cash cow is quietly subsidizing value destruction, and shareholders would have been better served by buybacks.

So, why does Allegion win from here, and what breaks the case? It wins if the specification moat and switching costs prove strong enough to let it own the electronic opening rather than merely supply a piece of it — capturing the ASP uplift and attaching recurring software revenue while holding its premium position. It breaks if the digital layer is captured by platform companies or PACS software vendors, if commercial construction stays depressed, or if management keeps spending the Americas' cash on assets that do not earn their keep. The evidence today is genuinely mixed: the pricing power is proven, the mechanical moat is deep, but the electronic-moat thesis is still largely unproven, and the International execution is a live liability.

For an investor trying to cut through all of this, three key performance indicators matter more than the rest, and they are worth tracking each quarter:

- Americas adjusted operating margin — the health of the cash cow. Sustained readings in the high-20s signal the moat is intact; a durable slide would be the first sign the franchise is weakening.

- Organic volume growth — the honest measure of underlying demand, stripped of price and acquisitions. Price can carry revenue for a while, but a business that grows only on price is a business whose end markets are shrinking; the volume line is where cyclicality and true demand show up.

- Electronic and connected-lock revenue as a share of the commercial business — the scoreboard for the entire transition thesis. This is the number that tells you whether Seamless Access is actually happening and whether Allegion is capturing the ASP uplift, or whether the migration is stalling in the residential and commercial base.

X. Epilogue & Playbook Lessons

Strip away the specifics of locks and closers, and Allegion leaves behind three lessons that generalize far beyond door hardware.

Lesson 1: Capture the specifier, not just the customer. The most durable business-to-business moats are not built at the point of sale but upstream, in the workflow of the professional who designs the requirement. By embedding itself in the architect's specification through tools like Overtur, Allegion arranged to win the sale before the building existed — a far stronger position than persuading a buyer at the moment of purchase. Any company that can insert its product into the design tools of the people who write the specs, rather than fighting for shelf space at the end of the process, has found a rare and defensible kind of power. The caution attached to this lesson is that such a moat is only as strong as the workflow it lives in; when the workflow itself digitizes and opens up, the incumbent's privileged position has to be re-won, not assumed.

Lesson 2: The hardware-to-software pivot cuts both ways. Electronification is seductive because it multiplies the price of every unit and dangles recurring revenue. But it is capital-intensive, it demands competencies — software, connectivity, credentials — that a metal-shaping company does not naturally possess, and it lowers the very barriers that protected the mechanical business. The skills that make a lock hard to manufacture do not make software hard to write, and the moat that repels a rival foundry does nothing to repel a platform company or a startup. A company crossing this bridge is trading a moat it understands for economics it covets, and the trade is not obviously in its favor. Allegion's outcome on this pivot is still being written, and an honest observer will hold the question open rather than assume the metal franchise's magic carries over.

Lesson 3: Spin-offs can unlock trapped value — and trapped focus. The most straightforward lesson is the oldest. A high-margin, capital-light business buried inside a heavy industrial conglomerate was worth more standing alone, not because its economics changed on the day of separation, but because independence gave it dedicated capital, dedicated management attention, and a valuation the market could finally see clearly. The security brands did not become better businesses in 2013; they became visible ones. That is often all a great franchise needs — to be let out of the building it was hiding in. The corollary, less often stated, is that visibility runs in both directions: a stand-alone company also has nowhere to hide its mistakes. A botched ERP implementation or a stretch of underperforming international assets that would have vanished inside a conglomerate's consolidated results now shows up starkly in a single segment's margin, quarter after quarter, for everyone to see. Independence is accountability, and accountability is a gift to shareholders precisely because it is uncomfortable for management.

A fourth lesson runs underneath all three, and it is the one most relevant to owning Allegion from here. A great defensive moat and a great growth story are not the same thing, and confusing them is how investors overpay. Allegion's mechanical franchise is one of the more durable competitive positions in the industrial world — but durability defends a position; it does not, by itself, grow one quickly. The company's attempt to turn defense into offense, by riding the electronic transition to a higher price and a recurring-revenue relationship on each opening, is strategically logical and genuinely promising. It is also unproven, capital-hungry, and pursued in a market where the moat's original logic — brass, code, specification — may not fully carry over. The most useful posture toward Allegion is therefore neither the bull's certainty that the tollbooth is eternal nor the bear's conviction that platforms will gut it, but disciplined attention to the three numbers that will actually reveal which future is arriving.

The final verdict on Allegion is deliberately unsettled, because the facts are unsettled. What is proven is a genuinely advantaged mechanical franchise in North America, with pricing power and switching costs that most companies can only envy, run by a management team whose narrative has been consistent and whose capital allocation has been at least responsive to challenge. What is unproven is whether that franchise survives its own transition into electronics with its economics intact, whether the International and technology bets ever earn their cost of capital, and whether a business that still deleverages on falling volumes deserves to be priced as a defensive tollbooth rather than a cyclical building-products supplier. The unseen tollbooth of the physical world is real. Whether it stays a tollbooth as the world goes digital is the question every future quarter will answer.

References

-

Allegion Reports Q4, Full-Year 2025 Financial Results, Introduces 2026 Outlook — Allegion, 2026-02-17 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Allegion plc Q4/FY2025 Earnings Press Release (Form 8-K, Exhibit 99.1) — SEC EDGAR (CIK 0001579241) ↩↩↩↩

-

Iroquois Theatre fire — Encyclopedia of Chicago / Chicagology ↩

-

The inventor that started it all: 100 years of Schlage — Schlage (Allegion) ↩

-

Ingersoll Rand Completes Spinoff of Allegion (Form 8-K press release) — SEC EDGAR ↩

-

Ingersoll Rand Completes Spinoff of Allegion — Allegion, 2013-12-02 ↩↩

-

Allegion Q1 2026 and Q4/FY2025 Earnings Call Transcripts and Analyst Q&A — Seeking Alpha ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Allegion plc SEC Filings, including proxy statement executive compensation disclosure (CIK 0001579241) — SEC EDGAR ↩

-

ASSA ABLOY and Spectrum Brands Reach Settlement with DOJ, Divest Yale and Emtek to Fortune Brands — SDM Magazine, 2023-05-08 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube